qualitative and quantitative management tools used …

TRANSCRIPT

QUALITATIVE AND QUANTITATIVE MANAGEMENT TOOLS USED BY

FINANCIAL OFFICERS IN PUBLIC RESEARCH UNIVERSITIES

A Dissertation

by

GRANT LEWIS TREXLER

Submitted to the Office of Graduate Studies of

Texas A&M University in partial fulfillment of the requirements for the degree of

DOCTOR OF PHILOSOPHY

Approved by: Chair of Committee, Bryan R. Cole Committee Members, Eddie J. Davis

Kerry Litzenberg David Parrott

Head of Department, Fred M. Nafukho

December 2012

Major Subject: Educational Administration

Copyright 2012 Grant Lewis Trexler

ii

ABSTRACT

This dissertation set out to identify effective qualitative and quantitative

management tools used by financial officers (CFOs) in carrying out their management

functions of planning, decision making, organizing, staffing, communicating,

motivating, leading and controlling at a public research university. In addition,

impediments to the use of these tools were identified which may assist in breaking down

barriers to the implementation of these tools within higher education. The research

endeavor also provided additional significance through the CFOs identifying benefits

from the use of quantitative and qualitative management tools. Finally, the study

undertook the task of identifying quantitative and qualitative management tools that are

important to public research university CFOs in carrying out their management functions

in the future.

In this study, the Delphi method was used to gain consensus from a panel of

fifteen public research university CFOs who were experts on qualitative and quantitative

management tools. The experts were self-identified through their response to a

questionnaire on their use of the management tools and represented 12 different states.

Due to the nature of the research, a computer-based Delphi method was used to facilitate

a four round, electronically based Delphi study. The questionnaires were based upon a

review of the literature and tested by a pilot group of higher education CFOs.

Through a series of four electronic questionnaires, the Delphi panel identified

twenty-three qualitative and quantitative management tools which they believe are

moderately effective for use by public research university CFOs in carrying out their

iii

functions of planning, decision making, organizing, staffing, communicating,

motivating, leading and controlling. Additionally, the panel of experts identified sixteen

barriers/impediments to the use of qualitative and quantitative tools in carrying out the

above functions. The panel also identified eighteen benefits that the tools provide to

public research university CFOs in carrying out their management functions. Finally, the

Delphi panel identified three qualitative and quantitative management tools that will be

highly important, and twenty qualitative and quantitative management tools that the

panel of experts considered to be important, for public research university CFOs in

carrying out their management functions in the future.

This dissertation study is significant because the results are expected to provide

public research university CFOs qualitative and quantitative management tools that they

may use to assist them in carrying out their management functions. The

barriers/impediments and benefits noted also provide CFOs with knowledge to assess

whether the tools can be used at their institutions, knowing the specific climate and

culture which exists. The qualitative and quantitative management tools which were

identified as being important in the future can serve as a guide to develop training

programs to enhance the knowledge of public research university CFOs.

iv

ACKNOWLEDGEMENTS

There are many faculty and friends who provided me with the encouragement

and support throughout the dissertation process. First and foremost, I would like to

express my sincere gratitude to Dr. Bryan R. Cole, chair of my dissertation committee,

for his encouragement, wisdom, direction, expertise and guidance throughout the

completion of my dissertation. He always provided helpful advice, words of wisdom and

encouragement.

I am most grateful to my dissertation committee members for their knowledge,

time, expertise and insight: Dr. Kerry Litzenberg, during my first semester at Texas

A&M I learned so much from you through your interaction with students, motivating

them to do their best while providing practical knowledge which they could use in their

careers. That first class of Ag Econ 440 was exceptional. I did not realize how much I

grew that semester until several years later. I want to also thank you for your ideas,

review, advice (personal and professional), and continued support, not only through my

dissertation but also in life. To Dr. Eddie Joe Davis, I took your class on higher

education finance and that set me on my way to determine what analytical tools were

actually being used by higher education CFOs. Thank you for your support of my

thoughts, your wisdom, and your patience over the course of my dissertation. Dr. Toby

Egan, after I took your Epistemology class I knew I wanted you to be on my committee.

Your fresh perspectives and your ability to bring in real world experience to higher

education is something that I want to achieve if I teach in a college or university setting.

I’m only sorry that you could not finish as a committee member. Dr. Dave Parrott, thank

v

you for your encouragement, always asking me how my writing was going and telling

me to press on. Thank you for stepping in and joining my committee. Stefanie Baker,

Stef you kept me going when I could have easily put my dissertation aside. I am so

happy that your life is moving in the direction that you always desired. Don’t let your

hard work on your dissertation slip to the wayside. I know it’s tough balancing a family,

work and moving your dissertation forward but you can do it.

I would like to extend my sincere appreciation to the members of the Delphi

panel. A list of some of their names, with their permission, is included in Appendix 8.

They participated in all rounds of the Delphi process and helped to shape the final

outcome of this research. I would like to thank them for their commitment and support. I

would also like to thank the members of my pilot group for helping me refine my study

and providing me hard questions as to why CFOs would want to provide me their

valuable time to complete this study.

My family has allowed me to be the person I am at this point in my life. Mom

and Dad, you gave me the foundation to believe that anything was possible and showed

me at an early age what responsibility was and how it helps you mature. Although I have

made mistakes many times, you have always been there to support me and help me learn

from those mistakes. I love you both very much. Who would have thought that when you

had Cary and me when you were in your late teens you would end up with two children

with Doctorate’s?

To my children, Amanda, Sarah and Ethan, I love you more than you will ever

know. I am thankful to see the young adults you have become. Each of you makes me so

vi

proud of you in so many different ways. When your mom and I made the decision to

move from Orange County to College Station, you probably thought we were crazy and

did not look forward to the changes in your lives. I hope that the change was for the best

and you are glad we made the move. You all have so much potential. I only hope that

someday each of you achieve your goals and dreams. The three of you are the inspiration

of my life and you make me a better man. To Toni, thank you for your support and

encouragement during our life together. To Dana, twenty-nine more like the last one.

vii

TABLE OF CONTENTS

Page

ABSTRACT...................................................................................................................... ii

ACKNOWLEDGEMENTS ............................................................................................. iv

TABLE OF CONTENTS................................................................................................ vii

LIST OF FIGURES .......................................................................................................... x

LIST OF TABLES ........................................................................................................ xiii

CHAPTER I INTRODUCTION .................................................................................................. 1

Statement of the Problem ............................................................................. 5 Purpose of the Dissertation .......................................................................... 7 Research Questions ...................................................................................... 8 Operational Definitions ............................................................................... 8 Assumptions .............................................................................................. 11 Limitations ................................................................................................. 11 Significance ............................................................................................... 12 Organization of the Dissertation ................................................................ 13

II LITERATURE REVIEW .................................................................................... 14

Section 1: The Current State of Higher Education .................................... 14 Section 2: Decision Making in Higher Education ..................................... 37 Section 3: Tools Used in Higher Education .............................................. 51

III METHODOLOGY .............................................................................................. 105

Introduction .............................................................................................. 105 Purpose………………………………………………………………….105 Delphi Method ......................................................................................... 106 Sample Size and Population .................................................................... 110 Selection of Delphi Experts ..................................................................... 111 Use of Electronic Communications in Delphi Studies ............................ 114 Importance of the Rating Scale ................................................................ 115 Description of Delphi Study Questionnaires ........................................... 115

viii

CHAPTER Page

Consensus in a Delphi Study ................................................................... 118 Statistical Analysis ................................................................................... 120 Summary .................................................................................................. 121

IV RESULTS ......................................................................................................... 123

Introduction .............................................................................................. 123 Results of Data Analysis .......................................................................... 123 Dealing with Missing Data ...................................................................... 125 Delphi Panel Description ......................................................................... 126 Non-representative Outlier ...................................................................... 126 Research Question One ............................................................................ 127 Research Question Two ........................................................................... 159 Research Question Three ......................................................................... 185 Non-representative Outlier Effects on the Study Results ........................ 203 Research Question Four ........................................................................... 205 Summary .................................................................................................. 235

V SUMMARY OF FINDINGS, CONCLUSIONS, AND RECOMMENDATIONS.. 236

Introduction .............................................................................................. 236 Summary of Study Methodology and Procedures ................................... 237 Summary of Findings .............................................................................. 241 Summary of Dissertation Study Conclusions .......................................... 246 Recommendations for the Field ............................................................... 251 Recommendations for Further Studies .................................................... 253 Summary: Dissertation Study Significance ............................................. 257

REFERENCES……………………………………………………….………………. 259

APPENDIX 1 ................................................................................................................. 284

APPENDIX 2 ................................................................................................................. 286

APPENDIX 3 ................................................................................................................. 289

APPENDIX 4 ................................................................................................................. 290

APPENDIX 5 ................................................................................................................. 291

APPENDIX 6 ................................................................................................................. 295

ix

Page

APPENDIX 7 ................................................................................................................. 299

APPENDIX 8 ................................................................................................................. 301

x

LIST OF FIGURES FIGURE Page 1 Consensus Example for a Four Point Likert Scale…………………………….119 2 Initial Means and Standard Deviations for the Effectiveness of Qualitative and Quantitative Management Tools in Currently Carrying Out Public Research University CFO Management Functions..…………..……..………..137 3 Initial and Consensus Means for Qualitative and Quantitative Management

Tools in Currently Carrying Out Public Research University CFO Management Functions……………………………….……..……………..…..147 4 Initial and Consensus Standard Deviations for Qualitative and Quantitative

Management Tools in Currently Carrying Out Public Research University CFO Management Functions………………..…………..…………….…….....148

5 Initial Means and Standard Deviations for Barriers/Impediments to the Use of Qualitative and Quantitative Management Tools by Public Research University CFOs in Currently Carrying Out Their Management Functions…..162

6 Initial and Consensus Means for Barriers/Impediments to the Use of

Qualitative and Quantitative Management Tools by Public Research University CFOs in Currently Carrying Out Their Management Functions..…169

7 Initial and Consensus Standard Deviations for Barriers/Impediments to the Use of Qualitative and Quantitative Management Tools by Public Research University CFOs in Currently Carrying Out Their Management Functions…..169

8 Initial Means and Standard Deviations for Barriers/Impediments Added by Delphi Panelists to the Use of Qualitative and Quantitative Management Tools by Public Research University CFOs in Currently Carrying Out

Their Management Functions……………..….……………………………..…177 9 Initial and Consensus Means for Barriers/Impediments Added by Delphi Panelists to the Use of Qualitative and Quantitative Management Tools by Public Research University CFOs in Currently Carrying Out Their

Management Functions…………………………….…………………………..181

xi

FIGURE Page 10 Initial and Consensus Standard Deviations for Barriers/Impediments Added by Delphi Panelists to the Use of Qualitative and Quantitative Management

Tools by Public Research University CFOs in Currently Carrying Out Their Management Functions…………………..………………………..……...……182

11 Initial Means and Standard Deviations for Benefits from the Use of Tools to Public Research University CFOs in Carrying Out Their Management

Functions……………………………………………………………………….187 12 Initial and Consensus Means for Benefits from the Use of Qualitative and Quantitative Management Tools to Public Research University CFOs in Carrying Out Their Management Functions…………………………………...192 13 Initial and Consensus Standard Deviations for Benefits from the Use of

Qualitative and Quantitative Management Tools to Public Research University CFOs in Carrying Out Their Management Functions……….....….192

14 Initial Means and Standard Deviations for Benefits Added by Delphi Panel from the Use of Qualitative and Quantitative Management Tools to Public

Research University CFOs in Carrying Out Their Management Functions.......198 15 Initial and Consensus Means for Benefits Added by Delphi Panel from the Use of Qualitative and Quantitative Management Tools to Public Research

University CFOs in Carrying Out Their Management Functions….……….....200 16 Initial and Consensus Standard Deviations for Benefits Added by Delphi Panel from the Use of Qualitative and Quantitative Management Tools to

Public Research University CFOs in Carrying Out Their Management Functions……………………………………………………………………….201

17 Initial Means and Standard Deviations for Qualitative and Quantitative Management Tools in Carrying Out Public Research University CFO

Management Functions in the Future………………………………………….209 18 Initial and Consensus Means for Qualitative and Quantitative Management Tools in Carrying Out Public Research University CFO Management

Functions in the Future……………………….…………….………………….218 19 Initial and Consensus Standard Deviations for Qualitative and Quantitative Management Tools in Carrying Out Public Research University CFO

Management Functions in the Future……………………….…………..……..219

xii

FIGURE Page 20 Comparison of Consensus Means for the Current Effectiveness and Future Importance of Qualitative and Quantitative Tools in Carrying Out the Public Research University CFO Management Functions………………………..…..233

xiii

LIST OF TABLES TABLE Page 1 Demographics of Expert Panel……………………………..………………….126 2 CFO Experience in Using Qualitative and Quantitative Management Tools

In Carrying Out Their Management Functions – Sorted by Initial Mean…..…128

3 Initial Means and Standard Deviations for the Effectiveness of Qualitative And Quantitative Management Tools in Currently Carrying Out Public Research University CFO Management Functions – Sorted by Initial Mean....136

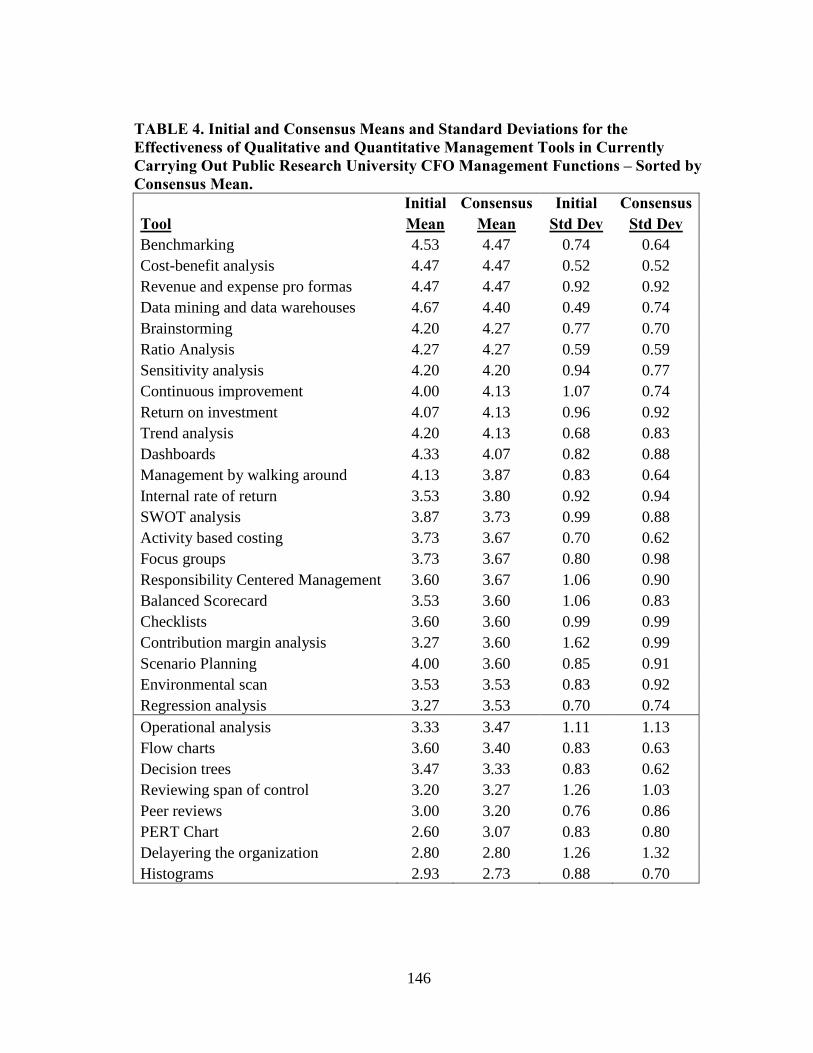

4 Initial and Consensus Means and Standard Deviations for the Effectiveness Of Qualitative and Quantitative Management Tools in Currently Carrying Out Public Research University CFO Management Functions – Sorted by Consensus Mean……………………………………………………………….146

5 Initial Mean and Standard Deviations for Barriers/Impediments to the Use Of Qualitative and Quantitative Management Tools by Public Research University CFOs in Currently Carrying Out Their Management Functions – Sorted by Initial Mean.……………………………….………………………..161

6 Initial and Consensus Means and Standard Deviations for Barriers/ Impediments to the Use of Qualitative and Quantitative Management Tools by Public Research University CFOs in Currently Carrying Out Their Management Functions – Sorted by Consensus Mean……………………..….168

7 Initial Means and Standard Deviations for Barriers/Impediments Added by Delphi Panelists to the Use of Qualitative and Quantitative Management

Tools by Public Research University CFOs in Currently Carrying Out Their Management Functions – Sorted by Initial Mean...............................................177

8 Initial and Consensus Means and Standard Deviations for Barriers/ Impediments Added by Delphi Panelists to the Use of Qualitative and Quantitative Management Tools by Public Research University CFOs in Currently Carrying Out Their Management Functions – Sorted by Consensus Mean …………………………………………………………………..………181

9 Initial Means and Standard Deviations for Benefits from the Use of Tools to Public Research University CFOs in Carrying Out Their Management

Functions – Sorted by Initial Mean ……………………...................................187

xiv

TABLE Page 10 Initial and Consensus Means and Standard Deviations for Benefits from the

Use of Qualitative and Quantitative Management Tools to Public Research University CFOs in Carrying Out Their Management Functions – Sorted by Consensus Mean……………………………………………………………….191

11 Initial Means and Standard Deviations for Benefits Added by Delphi Panel From the Use of Tools to Public Research University CFOs in Carrying Out Their Management Functions – Sorted by Initial Mean …................................197

12 Initial and Consensus Means and Standard Deviations for Benefits Added by Delphi Panel from the Use of Tools to Public Research University CFOs in

Carrying Out Their Management Functions – Sorted by Consensus Mean…...200

13 Comparison Between Consensus Means and Standard Deviations With and Without the Rankings of the Outlier Participant – Sorted by Consensus Mean with Outlier Included.………… …………………...……………………….....204

14 Initial Means and Standard Deviations for Qualitative and Quantitative Management Tools in Carrying Out Public Research University CFO Management Functions in the Future – Sorted by Initial Mean...………..……208

15 Initial and Consensus Means and Standard Deviations for Qualitative and Quantitative Management Tools in Carrying Out Public Research University CFO Management Functions in the Future – Sorted by Consensus Mean..…...217

16 Comparison of Consensus Means for the Current Effectiveness and Future Importance of Qualitative and Quantitative Tools in Carrying Out the Public Research University CFO Management Functions– Sorted by Current

Effectiveness ……………………………...…..…………………………….…232

1

CHAPTER I

INTRODUCTION

The more things change the more things stay the same. Hutchins (1933) wrote:

Hard times are producing nothing less than a complete change in character of our institutions of higher learning. Every aspect of their work is being affected. Their faculty, their students, their organization, their methods, their teaching, and their research are experiencing such alteration that we who knew them in the good old days shall shortly be unable to recognize them. Many of these changes are for the better. Others may wreck the whole system. (p.714)

While Garcia (1991) stated:

There are rarely any new problems, according to some; only variations on old ones – “old wine in new bottles.” Perusal of any recent issues of the Chronicle of Higher Education might seem to confirm this. “Current issues” may give long-time readers a sense of déjà-vu, but those new to higher education will find them fresh and different. In point of fact, there are some of each-old and new. Whatever one’s perspective, issues and problems will never disappear, though immediacy of their need for solution may lessen with progress. There are increased calls for assessment and accountability, the redefinition of scholarship, the inclusion of other voices within curricula and the tension between new and old voices, the new paradigms that are being introduced within the research community, the national fiscal crisis and concomitant cost containment that will bind our colleges and universities. (p.675) Today, legislators, students, and families are demanding that higher education do

more with less while at the same time improving access and requesting greater

accountability. Productivity gains and improved cost-effectiveness are crucial in

meeting higher education’s goals of teaching, research, and service. As higher education

continues to struggle with these issues, the role of the Chief Financial Officer (“CFO,”

as used herein, describes the highest ranking financial officer in an institution of higher

education, other titles can be vice president of finance or vice president of finance and

administration) within these institutions has become more important. Anderson (1986)

2

stated that because of the multiplicity of the problems in higher education, especially the

financial ones, the business officer has to develop new ways and new technologies to

achieve a situation where the academic world uses new techniques in decision making.

Anderson (1986) noted that decisions need to be based upon a sound analysis of facts

while studying and weighing all of the possible alternatives. Alas, even though these

statements were made more than 25 years ago it seems in the end, CFOs end up doing

the same thing about the same way.

A number of characteristics differentiate higher education from other enterprises.

The most important are the lack of profit motive, a variety of goals within the institution

(often times competing), and distributed decision making. These characteristics preclude

the use of the relatively clear guiding principles of profit maximization and cost

minimization, and closely circumscribe the decision making of senior administrators.

Birnbaum (1988) stated that “there is no metric in higher education comparable to

money in business, and no goal comparable to profits,” p.11. Most colleges and

universities see themselves as unique and an institution’s culture is so intertwined with

the existing order that new ideas which may come up are not put forward. Decision

making occurs in an environment where the goals, and constraints, the effects of

potential outcomes are not always known (Bellman & Zadeh, 1970). Financial

management in higher education is becoming more complex and hence more difficult to

manage. As a result, there is a need for leaders to generate good ideas and to translate

them into strategies for effective actions.

3

Higher education CFOs have varied backgrounds and skill sets. Hacking (2004)

in a survey of higher education CFOs found that the typical CFO had fifteen years of

experience with less than nine years in their current position (more than 35% were in

their current position for fewer than four years), 44% had some experience outside of

higher education, 90% had an advanced degree (typically an MBA), and most had a

degree in accounting. These CFOs also stated that their analytical skills were one of their

strengths while their soft skills (communication and written) could be improved. The

analytical skills of CFOs will continue to be tested as researchers (Bender, 2002;

Gumport, 2000; Wellman, 2008) acknowledged that the current environment facing

higher education is not expected to change in the near future as increasing financial

demands for health care, prisons, and public education must be confronted by both state

and the federal government. Wellman (2008) stated that “realistically, most of the

funding needed to support future program innovation and change is going to come from

reallocation of internal resources, not from new dollars from the state or tuition

revenues” (p.6). As a result, students and their families are paying a higher percentage of

their education costs; on November 20, 2009 the University of California Board of

Regents approved a 32 percent increase in undergraduate tuition, amid the protests of

hundreds of students (Lewin & Cathcart, 2009).

The influence of higher education CFOs on their campuses has increased over

the past several decades. Institutions’ have faced declining public and private support,

increased dependence on tuition revenues to offset the loss of this support, expensive

technology upgrades, a growing backlog of long neglected deferred maintenance on

4

campuses, an emphasis on revisiting decades old budgeting techniques and fiscal

policies, and increased scrutiny from stakeholders and governing bodies. Academic

leaders are challenged by an expanding universe of information technology and its uses

and by a changed focus from a provider-centered culture to a learner-centered culture.

Facing storms of change within and outside the academy, higher education officials have

realized that major realignments are underway creating demographic, economic,

political, and cultural imperatives. Quality, accountability, efficiency, and institutional

effectiveness have become part of the culture for stakeholders in higher education

(Gumport, 2000; Nedwek, 1996; Wellman, 2008).

The decentralized structure of the university as a complex adaptive system has

evolved over the centuries to solve extremely complex problems. However, this structure

is not conducive to risk taking and one size does not fit all due to the diversity of

missions within institutions of higher education. Accordingly, the current culture of

accountability and transparency can be enhanced, facilitated by new systems of data

measurement. To meet this improved culture of accountability and transparency requires

the leadership of financial officers that can effectively implement and utilize qualitative

and quantitative management tools to make complex decisions in a difficult

environment, an environment that seems to be becoming more difficult each day. While

increased data, its analysis, and expertise in interpreting the data are needed, Trussell

and Bitner (1996) found that many institutions have accounting systems that are

inadequate for decision making; higher education is relying on antiquated hardware and

software as it faces difficult, complex decisions. Higher education has not invested in

5

their information systems to the extent seen in private industry and as a result, decision

making is more complex due to a lack of information. Purves and Glenny’s study (as

cited by Floyd, 1991), stated that a minimal level of logic and analysis should be

factored in public sector decision making. Attention needs to be given to providing

higher education CFOs quality information to assist them in making decisions but not so

much that both universities that produce the information and the stakeholders that

receive it are swamped by its detail.

Statement of the Problem

In all enterprises, managers face the same dilemma of how, given the constraints

imposed on them, to achieve an optimal or at least satisfactory allocation of scarce

resources across an array of competing activities. Higher education CFOs are looked

upon as organization experts on finance and accounting by internal and external

stakeholders and are often asked to provide guidance and analysis on areas outside of

their direct span of control or authority, maybe more so than in for-profit entities. Higher

education CFOs are expected to monitor the interface within the institution as well as the

impact from external forces, establish appropriate strategies, and develop useful linking

and cushioning methods. As a result, their role in institutions of higher education has

become increasingly important and technical, with a greater reach across the institution

(Iwanowsky, 1996; Lai, 1996, Lambert, 2002).

The world has moved from the industrial age to the knowledge age to the

information economy. Information and knowledge are replacing physical resources as

the most important currency in the world (W.K. Kellogg Foundation, 1999). In the

6

current economic and political environment surrounding higher education, the

management of resources – their purchase, safeguarding and allocation – and the

management of relationships between the institution and its internal and external

environments – become a key institutional practice. However, the application of

qualitative and quantitative approaches to higher education, in which the underlying

processes are not fully understood and in which adequate measures of the conceptual

constructs have not been developed, has not occurred (Lindsay, 1982).

Critical to the decision making process is the quality and quantity of information

that higher education leaders have readily available (Dodd, 2004; Ehrenberg, 2005;

Ferren & Aylesworth, 2001). There is minimal research on effective qualitative and

quantitative management tools used by higher education CFOs and the extent of their

use in performing the CFO management functions. Past studies on CFOs have mainly

addressed the identification of CFOs routine assignments and educational and career

backgrounds, or an exploration of organizational relationships within higher education

administration and CFO leadership orientations (Hacking, 2004).

Research as to the management tools that higher education CFOs use to assist

them managing in these difficult times has been limited. Redenbaugh (2005) researched

accounting tools that CFOs use in managing their work and also discussed barriers to the

use of management accounting tools. Valero (1999) researched qualitative and

quantitative management techniques used by non-academic and academic administrators

in Virginia institutions of higher education. Since 1993, Bain & Company has been

conducting surveys (every year or two) of tools used by managers (Rigsby, 2011).

7

Higher education CFOs have to manage multifaceted systems with many interrelated,

yet unpredictable, components.

Purpose of the Dissertation

The purpose of this study was to identify effective qualitative and quantitative

management tools used by CFOs in carrying out their management functions of

planning, decision making, organizing, staffing, communicating, motivating, leading and

controlling at a public research university. In addition, impediments to the use of these

tools were identified which may assist in breaking down barriers to their

implementation. The research endeavor provides additional significance through the

CFOs identifying the benefits from the use of quantitative and qualitative management

tools. Finally, the study also identifies quantitative and qualitative management tools that

the CFOs believe will be important in carrying out their management functions in the

future. CFOs at public research universities were chosen as the population due to the

complexity of the organizations and a review of research that noted CFOs from these

institutions typically had advanced degrees and therefore were more likely to have been

trained in the use of these tools.

“The quality of a decision depends on the quality of the knowledge used to make

it” (Evangelou & Karacapilidis, 2007, p. 2069). One major benefit of the study is

providing knowledge on qualitative and quantitative management tools to higher

education CFOs which they can then use to make better decisions in these times of

limited resources.

8

Research Questions

The study addresses the following questions:

1. What qualitative and quantitative management tools are currently effective for public

research university CFOs in carrying out their management functions of planning,

decision making, organizing, staffing, communicating, motivating, leading and

controlling (Kreitner, 2004)

2. What are the barriers/impediments to the use of qualitative and quantitative

management tools in carrying out the public research university CFO management

functions?

3. What benefits do public research university CFOs perceive from using qualitative and

quantitative management tools in carrying out their management functions?

4. What qualitative and quantitative management tools will be important to public

research university CFOs in carrying out their management functions in the future?

Operational Definitions

To the end that this research effort establishes the current situation of the use of

qualitative and quantitative management tools at public research universities, it is

imperative to develop a list of tools that are used in an academic environment. For this

study, the following operational definitions will be used:

Qualitative management tools. Techniques in which data are typically obtained from a

relatively small group of respondents and not analyzed with statistical techniques. The

user’s judgment, experience, and the complexity of the decision to be made may affect

9

whether a qualitative tool is used in decision making. Qualitative tools may include:

focus groups, factor analysis, flow charts, peer reviews, benchmarking, brainstorming,

checklists, and decision trees.

Quantitative management tools. The orderly scientific investigation of quantitative

phenomena and their associations, the objective of which is to develop and utilize

mathematical models, theories and/or hypotheses (Hanacek, 2010). Quantitative tools

may include activity based costing, cost-benefit analysis, trend analysis, responsibility

centered management, ratio analysis, strengths-weaknesses-opportunities and threats

(SWOT) analysis, data mining and data warehouses, and continuous improvement (CI).

Planning. Planning is the formal process of deciding in advance what is to be done and

how and when to do it. It involves selecting goals and objectives and developing

policies, programs, and procedures for achieving them. Planning prescribes desired

behaviors and results (Hellriegel & Slocum, 1992).

Decision making. Decision making is a process of identifying and choosing alternative

courses of action. (Kreitner, 2008). Evangelou & Karacapilidis (2007) describe decision

making as an organizational activity that includes a series of knowledge representation

and processing tasks to resolve an issue, reach a goal or objective, or take hold of an

opportunity.

Organizing. Organizing is viewed as determining how resources (physical and human

resources) are to be allocated and arranged (prepared) for accomplishing an

organization’s goals and objectives (Boone & Kurtz, 1981; Higgins, 1991).

10

Staffing. Staffing may also be considered more broadly as the management of the

organization’s human resources. Staffing by itself can be described as the process of

recruiting and training qualified individuals for positions within an organization. Bartol

and Martin (1991) define staffing as activities that are developed to improve the

effectiveness of an entity’s workforce in attaining the organization’s goals and

objectives.

Communicating. Communication is often one of the most difficult tasks that a manager

performs on a daily basis. How much communication is enough and at what level and

when should communication occur? Communication is the exchange of information

between two or more people. Communication can occur through both verbal and non-

verbal means. Communication is the most dominant activity performed at all levels of an

organization (Daft, 1988).

Motivating. Kreitner (2008) stated that motivating is a psychological process giving

behavior purpose and direction. Motivating involves developing an understanding of

internal and external factors and traits that stimulate a specific employee to perform or

behave in a particular manner.

Leading. Bartol and Martin (1991) described leading as working with others while

developing an outline of what is expected to be achieved, providing direction and

motivating members of the organization. Kreitner (2008) described leading as inspiring

and guiding others in a common effort to reach a goal or objective.

Controlling. Controlling involves methods used to make sure that certain behaviors

conform to an organization’s objectives, plans, and standards. Controls help maintain or

11

redirect actual behaviors and results. Thus, planning and controlling complement and

support each other (Hellriegel & Slocum, 1992).

Process. A process is the interaction of organizational members where the objective is to

change, manage, or develop an organizational pattern or outcome (Childers, 1991).

The above list does not include definitions for all of the tools which will be

studied; these definitions are included in Chapter II, Literature Review.

Assumptions

1. The methodology proposed for this study is an appropriate design for this particular

research project.

2. Participant CFOs have the requisite expertise and experience to participate in the

Delphi group.

3. Participant CFOs comprehend the study; they will be knowledgeable in their answers

and will respond purposely and truthfully during the Delphi process.

4. Participant CFOs will be able and willing to devote time to the Delphi process.

Limitations

1. The study is limited to “Public Research Universities” as defined in Carnegie

Classification of Universities and may not be applicable to other institutions of

higher education or private universities.

2. The study is limited to the information developed during the literature review and

results of the Delphi method based on the responding CFOs answers to the research

questions.

3. Participant CFOs may feel influenced to respond in a particular way.

12

4. The study is limited in time dimension to an assessment of changes during the period

of observation. Longer term changes, improvements and other considerations should

be accessed through multiple cycles of improvement over time.

5. The economic environment during the period of the study was conducted may have

influenced the CFOs perspective of the importance of the use of the quantitative and

qualitative tools.

Significance

Higher education lags behind other industries in the use of management tools

(Patterson, 2004). At the same time, events in the last decade have produced a number of

factors that have led to the increased significance of the CFO in higher education.

Increased demands are being placed on CFOs due to institutional and societal demands

for: increased access, greater accountability and transparency, a focus on student

retention and success, quality and educational excellence (however defined), all while

operating in a climate of lower state and federal funding of higher education and

increased demands to lower tuition growth. CFOs must stretch their budget dollars

further, doing more with less, or even less with less. The use of qualitative and

quantitative management tools can enhance the CFOs role in higher education by

improving their decision making processes. The importance of implementing managerial

tools for improving CFO management functions in for-profit organizations has been

stressed in the literature; however, only limited research has been performed specifically

to review the extent of the use of management tools in colleges and universities. As a

result, there is a need to determine what qualitative and quantitative tools are used by

13

CFOs in order to enhance knowledge, training, and thereby the effectiveness of these

CFOs.

This study will also benefit higher education CFOs and academicians. CFOs will

obtain a practical understanding of the qualitative and quantitative management tools

that are used by their colleagues in higher education which could help them evaluate

alternative management techniques that may be effective for their unique campus culture

and environment. Higher education institutions may be able to use the knowledge

obtained in this study related to qualitative and quantitative management tools used by

CFOs and the important tools for use in the future to tailor their teaching and research

towards the needs of higher education administrators.

Organization of the Dissertation

This study consists of five chapters. Chapter I is an introduction of the topic of

qualitative and quantitative management tools used by higher education CFOs. Chapter

II reviews existing literature providing background as to the current context surrounding

higher education, discussing management functions in higher education, reviewing the

qualitative and quantitative management tools used in the for-profit sector and in higher

education, and the use of the Delphi technique. Chapter III describes the research

methodology used in the study. Chapter IV explains and analyzes the results of the

study. A summary of findings, conclusions and recommendations for further research are

presented in Chapter V.

14

CHAPTER II

LITERATURE REVIEW

Section 1: The Current State of Higher Education

One component of a study of the use of qualitative and quantitative management

tools in higher education is importance of understanding the current state of higher

education. For the last three decades, higher education has faced rising costs, declining

resources on the state and federal level, calls from stakeholders inside the institution and

those that regulate higher education for accountability, demands for more efficient

allocation of resources, and improved outcome evaluation. These features along with

others influence higher education CFOs; a review of internal and external attributes that

influence higher education CFOs follows.

Rising Costs

The cost of higher education has risen more than four times the rate of the cost of

living, increasing 498 percent from 1985 to 2011 (Wood, 2012). One factor that

influences the costs of higher education is the increasing cost of sophisticated scientific

research and the high percentage of costs associated with salaries and benefits that are

difficult to cut (Clotfelter, 1996; Hayden, 2010). Faculty salaries have also increased as a

result of institutions competing for the services of expert faculty who bring in significant

research grants and the associated research funding. As a result, universities bid up

salaries for high quality candidates (Duderstadt & Womack, 2003; Ehrenberg, 2003;

Rowley, Lujan & Dolence, 1997).

15

Institutions of higher education use the following strategies to offset the rising

costs of higher education: expanding undergraduate enrollments; increasing the number

of out of state and foreign students admitted; using graduate assistants or adjunct faculty

to teach large undergraduate classes; using lecturers rather than tenure track faculty to

instruct classes; and increasing class sizes. According to Gerdes (2011), over half of

faculty members are part-time and more than 40 percent of full-time professors are

temporary or off the tenure track. However, as tuition rates at universities continue to

rapidly increase, state and federal officials, students, and parents, have started

questioning these practices and these studies have become concerned with the quality of

instruction within higher education. The demands of these key stakeholders on higher

education to manage tuition rates has led administrators to look at new methods to

reduce costs and/or find other sources of funding (Gumport, 2000; Suskie, 2006;

Wellman, 2008). With state budget deficits hitting $130 billion in 2011, legislators and

boards of trustees have had no choice but to increase tuition (KPMG, 2011). The

significant increase in tuition places a greater financial burden on students and their

families.

Declining Resources

Universities face increasing indecision, volatility, deregulation, and a scarcity of

financial and human capital (Perkin, 2007). Competing social issues, for example crime,

gender and race inequality, public welfare, and healthcare and retirement costs create a

difficult situation wherein colleges and universities cannot claim a major portion of

available public funding. Higher education competes for funding with other societal

16

needs and as a result higher education has seen funding decreases over the past two

decades as state and federal governments allocate their budgets to other societal

concerns (Duderstadt & Womack, 2003). Mortenson (2011) stated that from 1980 to

2011 there was a forty percent decrease in average state support for higher education,

with 2011 levels approximating 1967 funding after accounting for inflation. As a result,

institutions of higher education have had to find alternative funding sources to make up

for declining federal and state financial support (Kerr, 2001).

Over the past several decades, at the same time as costs of higher education have

increased, federal and state funding has decreased. For example, in California, the

budget projection for the fiscal year beginning July 1, 2011, cut $500 million from

California State University System (CSU) and $500 million from University of

California (UC) campuses. The CSU could potentially face a $1 billion reduction in state

funding if certain revenue measures aren’t extended by voters or the state

legislature. That potential level of reduction – to $1.79 billion in state general fund

allocation - would drop the CSU's state support below 1996-97 levels when the CSU

served 100,000 fewer students (CSU Reviews Initial Strategies to Address $500 Million

Cut in State Funding, 2011). In April 2011, Jerry Brown, California’s governor, warned

that if a special election to extend temporary increases in sales, personal income, and

vehicle taxes is not called and the measures passed, then UC undergraduate tuition could

reach $20,000 to $25,000 a year, making the UC system the most expensive public

system in the world (Williams, 2011). In July 2012, CSU Trustees discussed two

possible approaches to close an additional $250 million budget gap if the special election

17

fails; both necessarily include salary and benefit reductions because salaries and benefits

account for nearly 85 percent of the CSU’s annual costs:

• The first approach protects student access—and avoids further reductions in student enrollment—with a $150 tuition fee increase and a 2.5 percent system wide average pay and benefit reduction for faculty, staff and administrators.

• The second preserves tuition “price” by reducing enrollment and by implementing a 5.25 percent system wide average pay and benefit cut for faculty, staff and administrators (personal communication, Gail Brooks - Vice Chancellor Human Resources, July 19, 2012). In the United States, the amount of student loan debt surpassed the amount of

credit card debt in the third quarter of 2011. Americans had a total of about $870 billion

in student loan debt surpassing the nation's $693 billion credit card balance based upon

an analysis from the Federal Reserve Bank of New York (Kurtzleben, 2012). Calls for

lowering the costs of higher education can be heard in most every state as well as at the

national policy level.

President Barack Obama, in his 2010 State of the Union address said, "It's time

for colleges and universities to get serious about cutting their own costs, because they

too have responsibility to help solve this problem" while in a speech at the University of

Michigan on January 27, 2012 he stated that state governments need to spend more on

higher education, describing cuts by Michigan and 39 other states as "the largest factor

in tuition increases at public colleges over the past decade." And he urged students to

pressure Congress to keep the interest rate on federal student loans from doubling in

July. The President also warned that colleges themselves needed to do more to cut costs,

instead of assuming they can "just jack up tuition every single year." Government "can't

18

just keep on subsidizing skyrocketing tuition," (Blumenstyk, Stratford, & Supiano,

2012).

Accountability and Efficiency in Higher Education

Bowen’s (1980) revenue theory of costs describes the dominant goals of higher

education institutions. Bowen’s revenue theory of costs are:

1) The dominant goals of institutions are educational excellence, prestige, and influence; 2) In the quest of excellence, prestige, and influence, there is virtually no limit to the amount of money an institution could spend for seemingly fruitful educational ends; 3) Each institution raises all the money it can; 4) Each institution spends all that the money it raises which leads toward ever increasing expenditure (Mills, 2008).

While the statements within Bowen’s theory of costs are generalizations, they

depict the prevailing objectives and the related actions of public and private universities.

In Bowen’s view, public self-control is a mechanism that keeps institutions of higher

education from over spending. However, historically, institutions spent all the money

they could raise, their only limit were costs. As costs rose, institutions responded by

requesting and seeking more revenue from government and students. However, state and

the federal government has not been able to provide additional funding those institutions

requested, resulting in the amount of support provided to higher education declining to a

level not seen in decades. State and local support per full‐time‐equivalent student was

$6,454 in 2010, a 7 percent decrease from 2009, and the lowest in the last 25 years (State

Higher Education Executive Officers “SHEEHO,” 2011).

Bowen’s revenue theory of costs has been well studied in the literature and has

caught the attention of higher education stakeholders who have been increasingly

demanding on institutions of higher education and required a call for greater

19

accountability and institutional efficiency and effectiveness. This is not a new

phenomenon as demands for evaluation and accountability, and a concern with

effectiveness were discussed more than twenty years ago by Carter (1972), Hoos (1975),

and Romney, Bogen & Micek (1979). However, many in higher education still regard

the notion of efficiency as being wholly inappropriate in the context of the educational

process.

Today, higher education administrators must be responsible for cultivating

improved performance while overseeing efficiency gains in their operations, in addition

to acquiring additional resources. Higher education has become an industry under a

microscope as federal and state governments question the return on their investment in

higher education (Massy, 2003). It seems that higher education’s stakeholders:

prospective and currently enrolled students and their families; businesses; federal and

state governments; accrediting agencies; faculty and staff within the university; and the

media; are all asking for evidence that higher education is providing effective programs

and services (Padro, 2007). In addition, concerns about the success rates of for profit

universities, student loan debt, student persistence and retention rates, along with the fact

that higher education costs are outpacing most other sectors of the U.S. economy,

increases the focus on the finances of universities. Members of the public and their

representatives in government want evidence about value for money – what are they

getting for the massive sums being plowed into higher education (Massy, 2003).

Facing storms of change within and outside the academy, higher education

officials have realized that major realignments are underway creating demographic,

20

economic, political, and cultural imperatives. Improving productivity and reducing the

higher education costs are core issues in the demands for accountability while the most

important financial challenge is not how colleges and universities can obtain new

revenue sources but how to increase returns from existing investments (Burke, 2004).

Quality, accountability, and institutional effectiveness have become part of the culture

for stakeholders in higher education. The academy has been asked to improve

effectiveness, efficiency and economy in what it does; more importantly, higher

education must change while living in a fishbowl (Nedwek, 1996).

Questions related to higher education include: the value of institutional activities

after four to six years of attendance (often times without graduation); its caginess for

documenting and the distributing results of the outcomes of higher education; and its

reluctance to accept its limitations and attempt to improve (SHEEHO, 2005). These

factors have placed increasing demands for higher education to be more efficient,

effective, and accountable. Higher education has become a “prime target for

accountability in terms of how faculty spend their time, what the products of higher

education are, and what costs are associated with those products” (Wellman, 2008, p. 3).

Boards of trustees, along with state legislatures, have called for increased

accountability as they believe that their best possible option to improve accountability is

to legislate change (Lucas, 2000). Due to the budget deficits currently faced by most

states and the federal government, appropriations to higher education have decreased

while private donors and private sector contributions have become an increasingly

critical part of institutional budgets. At the same time, private donors are requiring

21

greater accountability as to the use of their funds with some companies tying their

donations to controlling an aspect of the university’s research agenda.

The call for higher education to be more transparent and accountable for student

learning, efficiency, and effectiveness is not going away. Therefore, colleges and

universities should embrace the call and begin to deliver more effective communications

to internal and external stakeholders (Welsh & Metcalf, 2003). Institutions of higher

education must hear the cry from their stakeholders for further accountability, efficiency

and effectiveness, and improved outcomes. However, efficiency and effectiveness are

generally not highly ranked within academia (Kerr, 2001). Taking action to address the

calls for greater accountability, institutional efficiency, and effectiveness has been

difficult for many institutions of higher education due to their preference, as well as that

of their faculty and staff, for autonomy in running the institution. Massey (2003)

described the challenge for higher education administrators to balance stakeholder

requirements for accountability against faculty who view these efforts as additional

bureaucracy.

Faculty view additional restrictions as a precursor to additional regulation and

controls that the faculty believe will decrease autonomy and academic freedom (Perkin,

2007). On the other hand, higher education’s stakeholders argue that their interest may

not be served if institutions of higher education have liberal autonomy with little to no

oversight over their affairs. In order for public universities to be provided autonomy in

their operations, they need to put forth evidence that the institutions are meeting

demands for efficiency and effectiveness while meeting learning and other institutional

22

objectives. To achieve better results, accountability, efficiency, and effectiveness must

be a thorough process in which shared goals and objectives are explicitly stated,

advancement towards the goals and objectives is measured, and progress towards

improved performance is encouraged and guided (SHEEHO, 2005). However, one of the

most significant challenges of shared governance is its inability to address the deeper

and most comprehensive challenges that confront an institution (Morrill, 2007).

The problem in higher education is a failure to create and put into practice

accountability advances that improve performance in a complex, decentralized system

(SHEEHO, 2005). Public expectations of higher education have increased while public

confidence has declined. It would appear – at least superficially – that many colleges and

universities have permitted an erosion of the culture of professional accountability that

have traditionally assured the quality and standards of their academic programs and

degrees (Dill, 1999). As colleges and universities attempt to respond to the demand for

increased accountability, they are confronted with the paradox that as accountability

activities within the academy become institutionalized, campus support for these

activities becomes weaker and more shallow (Welsh & Metcalf, 2003). Accountability,

efficiency, and effectiveness are often a battleground between faculty, administration,

and higher education policymakers. Often faculty see external accountability standards

as a reason to place blame or avoid responsibility for a lack of financial support while

external stakeholders, frustrated because existing investments in higher education are not

achieving the results they believe should be produced, believe stronger external

accountability is the only way to see improvement within academia (SHEEHO, 2005).

23

The call for higher education to be accountable for the investments that

governments, parents, and students are making will continue to impact colleges and

universities; the call for accountability, increased efficiency and effectiveness will be a

rallying call in the future. The calls for institutional effectiveness, efficiency, and

accountability grew louder with the Spellings Commission report - “Charting the Future

of U.S. higher Education” as well as the 2004 National Commission on Accountability

in Higher Education report. These reports called for further productivity, efficiency,

accountability, and transparency in regard to the costs of higher education (Keating &

Riley, 2005; Padro, 2007).

Ruben, Lewis and Sandmeyer (2008) stated that a robust culture of

accountability, efficiency, effectiveness, and transparency must be developed within

higher education, aided by new systems of data measurement. Burke (2004) stated that

accountability programs that use large amounts of data limit their usefulness. Better

accountability requires clearer goals and better information about outcomes. However,

more data is not more accountability. Policymakers need information systems that are

able to provide information regarding the experiences and accomplishments of faculty

and students. Such systems require a considerable investment in technology, gathering

data (typically in a central repository), and the development of strategies for managing

the data (Davenport, 2006). Institutions of higher education, along with federal and state

governments, must better define how they measure outcomes and how these

organizations react to the results of these measurements. What has been missing in

higher education are systems that hold faculty accountable for performance (Massy &

24

Zemsky, 1994). A new era of accountability will hold greater promise for informing

effective education practice if it incorporates respect for the professionalism and

professional development needs of administrators (Dowd, 2005).

Outcomes of Higher Education

In higher education, quality is often looked at as the intrinsic form of value

created in the discovery and transmission of knowledge. There is a prevailing belief that

quality plays an increasingly essential role in higher education (Owlia & Aspinwall,

1997). However, the products of higher education - teaching, research, and service - are

difficult, at best, to measure. As Haworth and Conrad (1997) pointed out, one of the

reasons why “quality” is such an elusive concept in higher education is the diversity of

views about what the criteria should be used to judge quality. They note that views of

program quality all share similar problems: a heavy reliance on program “inputs,” such

as library resources; few empirical connections to student learning outcomes; an

overreliance on quantitative indicators; and the general lack of attention to the views of

such important stakeholders as students, alumni, and employers. Current perspectives

about quality suffer from a lack of clarity and agreement about that the standards should

be, often times institutions may have information that could lead to judgments regarding

quality but they often lack a shared understanding about how the information is to be

interpreted (Wergin & Seingen, 2000).

Teaching is a good that is evaluated after it is consumed, be it a class, a semester,

or a degree. As a result, proxies are often used as signs of quality, the number of Nobel

Prize faculty on staff, the difficulty in being accepted to a program, or the cost of an

25

education, all of which can influence the decisions of students and their parents. Despite

multiple instruments and surveys to measure the inputs and outcomes of higher

education, higher education does not do a good job on measuring quality (SHEEHO,

2005). Despite this weakness, there are assessments that can be used to evaluate the

performance of institutions of higher education. Two common proxies as to the

effectiveness of an institution of higher education are faculty research productivity

(typically measured in research dollars from external grants) and institutional graduation

rates (six year graduation rates are the most common measure); Dugan (2006) noted that

six year graduation rates are frequently used as a measure of student learning. External

stakeholders (trustees, federal and state governments, accreditation boards) are keenly

interested in student graduation rates as a means to determine the “success” of the

investment the institution has made into its academic programs.

The quality of an institution’s faculty is often judged by faculty research

productivity while an institution’s research expenditures are a common proxy for

measuring research productivity (Mills, 2008). Research productivity is of importance to

federal and state governments, faculty, and other higher education stakeholders, because

of the continued economic growth within the community surrounding the institution, the

prestige of the university, and its role as a funding source for many institutions. Research

funding is now viewed as an essential revenue stream to institutions of higher education,

becoming ever more important with the loss of state funding to higher education.

Duderstadt & Womack (2003) stated that the amount of sponsored research

conducted at a university is a determinant of institutional reputation as faculty research

26

and scholarship activity increases an institution’s attractiveness to prospective students.

A 2003 DFES white paper on higher education funding noted that institutions are driven

towards greater involvement in research by the incentives in funding mechanisms as

well as the status criteria awarded to a university with increased research funding. As a

result, the more attractive the institution, the greater the demand (number of applications

for enrollment), the higher the grade point average and standardized entry test scores of

applicants, which can lead to increased financial resources (Volkwein & Sweitzer,

2006).

The call for improved measures of higher education’s performance has been a

constant throughout this century with only minor variations in the fundamental message

(Stupak & Leitner, 2001). Issues of performance measurement remain controversial.

Behn (1995) called performance measurement one of “the questions” in public

management. Based on the continued calls for additional accountability in higher

education since the release of the Spellings Commission report, the calls for

accountability and measures of the outcomes higher education by external and internal

stakeholders will not go away.

Competition for Resources

Colleges and universities have varying missions, institutional cultures,

governance structures, enrollments, stakeholder influences, and endowments, Each of

these factors influence how an institution of higher education positions its resources to

acquire top notch students and increased funding dollars. Colleges and universities need

to focus their missions and sharpen their priorities. In education, as in private industry,

27

the stated mission and the true mission of the organization may not coincide; goals that

comprise the mission of an institution of higher education can be hard to identify. Higher

education institutions compete to acquire intellectual and financial capital, distinguishing

themselves by offering superior quality products (a “better education”) or services (new

and more attractive amenities) to lure high quality faculty and students (Rowley &

Sherman, 2001). SHEEHO (2005) stated that institutions of higher education competing

to obtain resources and prestige, pursuing rankings based on measures such as student

selectivity and faculty prestige, have pushed cost-effectiveness to the side while

detracting attention from institutional goals.

As competition to attract top faculty and students intensifies, institutions of

higher education such as Harvard or Yale that once seemed to be resistant to the need for

additional financing are finding that they must focus on efficiency and effectiveness due

to shrinking endowments (Kirwan, 2007). To meet the needs of today’s students,

institutions of higher education pour money into state of the art recreation centers and

housing facilities, remodel food courts, increase their student services offerings, and

provide other amenities to attract the very best faculty and students. This viscous cycle

of competition for faculty and students requires more resources than those that are

available to higher education in the pursuit of high-quality faculty and students

(Slaughter & Rhoades, 2004).

However, the current budget crisis in some states has left colleges unclear about

how to plan financially for the forthcoming academic year. Amid the fiscal uncertainty,

college leaders in the Northeast, like those in other parts of the country, sought new

28

ways to save money while maintaining or improving quality (Sewall, 2010). The “new

normal” assumes that state aid remains limited, and in hope of avoiding severe

institutional cuts in the future the call at many institutions of higher education is not

“doing more with less” but “doing less with less.”

Sewall (2010) noted: The University of Maine system has cut 300 positions and an estimated $30 million in operating costs while also expanding its online branch to provide double the programs now offered. In June 2010, the Pennsylvania State System of Higher Education discontinued or suspended nearly 80 programs with low enrollment, but as it did so, it encouraged more online enrollment.

Prestige, Institutional Attractiveness, and Reputation

Newman & Couturier (2001) stated that competition was a strength within the

system of higher education as it requires that universities seek out their competitive

advantages. Colleges and universities attempt will look to position themselves in such a

manner that they can maximize their prestige, institutional attractiveness, and reputation

(Mills, 2008). Prestige is not synonymous with the quality of an education and the two

concepts are relatively independent of each other (Duderstadt & Womack, 2003). The

focus on the prestige of an institution of higher education has required colleges and

universities to focus resources and administrative efforts on factors that affect inputs

included in rankings, such as student enrollments, the size of the library, the number of

Nobel laureates, instead of on other critical factors that impact a student’s learning

experience (Hossler, 2004). Prestige brings more revenue, which can then be spent to

produce more prestige, which generates more market power – not to mention additional

research funding and gift support (Massy, 2003). The impact of competition for

29

resources and quality faculty and students, along with other market forces has led

institutions of higher education to market themselves through elaborate “branding”

initiatives to differentiate themselves from the competition (Kirp, 2003). Universities

can cite their prestige when trying to persuade prospects to come to their university but

in the end willingness and ability to pay determine whether potential students accept a

university’s offer of admittance and whether potential sponsors accept or reject its

research proposals.

The selectivity of an institution of higher education by prospective students is

directly correlated with the institution’s academic rankings and reputation (Duderstadt &

Womack, 2003). Many institutions of higher education pursue prestige through factors

such as the relative “quality” of incoming students, as measured by SAT scores; the

quality of their faculty, as evidenced by federal research funding, and the success of their

athletic programs (Gayle, Tewarie, & White, 2003). Institutions of higher education

understand that the recruitment of high quality students strengthens the reputation of the

institution and eventually adds to its financial well-being (Brint, 2002). As a result, most

universities spend right up to their budget limits after allowing for reserves as spending

increases the realization of the institution’s values.

As Bowen’s (1980) revenue theory of costs states, institutions of higher

education will continue to increase revenues and expenditures in the pursuit of power,

influence, and prestige. Higher tuition allows more spending, and more spending

improves value fulfillment, which is what the university is trying to maximize. Bowen

30

(1986) also noted that the goals of excellence, prestige, and influence are not

counteracted by motivations of frugality or efficiency.

Universities as Economic Enterprises

University performance depends on its production processes and market forces.

Production refers to the methods institutions of higher education use to accomplish their

goals of education, research and public service. At the same time, performance also

depends on resource availability, that is, on the institution’s financial condition.

However, more money has given many universities the opportunity to avoid doing one

thing critics of higher education see as their core competency, actually teaching large

numbers of students; after a certain point, the more money you have, the fewer

distinguished professors you will have in the classroom (Bennett, 1986).

Trustees and other higher education stakeholders believe institutions of higher

education should be more business-like while there is some evidence that cost

containment remains somewhat of a budgetary afterthought (Wellman, 2008). At the

same time, professors and others within higher education argue that the academy is not a

business and should not behave like one, fearing that the incorporation of a more

business-like culture will emphasize improving efficiency by looking at results in

comparison to resources provided (Levin, 2001; Massy, 2003). Traditional colleges and

universities are not-for profit-enterprises which in a simplistic sense exist to “do good”

while for profit universities exist to make money. Unfortunately, the university’s non-

profit status does not ensure that quality will exist; the quality of education is difficult to

31

evaluate, and the public relies on academic traditions and values to safeguard quality

(Massy, 2003).

Higher Education’s Resistance to Change

Many scholars have written about the difficulty of change in higher education

(Birnbaum, 1988; Bowen, 1986: Kerr, 2001; Kirwan, 2007; Massy, 2003; and Morrill,

2007) due to its loose coupling, shared governance, and fragmented decision making.

The general human tendency is to resist change, the threat of the unfamiliar, which is

especially evident in academic communities. Change is difficult and complex in all

organizations, but especially so in institutions of higher learning. Institutions of higher

education stick to their long valued traditions rather than adopt new innovations (Massy,