qualified plans part 2 - mazursky constantine · qualified plans part 2 . nondiscrimination ....

TRANSCRIPT

The MC Academy

The Employee Benefits and Executive Compensation Series

June 4, 2013

Qualified Plans

Part 2

Nondiscrimination

Nondiscrimination in General

Qualified Retirement Plans may not Impermissibly

Discriminate in Favor of Highly Compensated Employees

(“HCEs”)

3

Who is an HCE?

An HCE is an employee who either:

Received more than $115,000 in compensation from the

employer in the prior year; or

Was a 5% owner in either the current year or the prior

year

The $115,000 threshold is indexed annually

4

HCE Example

2012 Compensation = $105,000

2013 Compensation = $120,000

Not an HCE for 2013

5

Note: Unless an individual is a 5% owner, he will never be an

HCE in his first year of hire (because no compensation

from the employer in the prior year)

Top-Paid Group Election

Can limit HCEs under the first prong (i.e., by

compensation instead of ownership) to top 20% of all

employees by compensation

Cannot expand the group of HCEs (i.e., will not pick up

an individual with less than $115,000 in compensation

in the prior year)

6

How Does a Plan Show That It is

Nondiscriminatory?

Various Numerical Tests

Safe Harbors

7

Plan Features Subject to

Nondiscrimination Requirements

Contributions to a Defined Contribution Plan

Benefits under a Defined Benefit Plan

Coverage

Benefits, Rights and Features

8

Examples of Benefits, Rights and

Features

Optional Forms of Payment

Death Benefits

Investment Options

Deferral Limits

Rates of Match

Vesting Schedules

9

Coverage

Minimum Coverage in General

The number of an employer’s HCEs who benefit under

a plan cannot be too disproportionate to the employer’s

other employees who benefit under that plan

11

Minimum Coverage in General

Five basic questions:

Who is an HCE?

Who is the employer?

Which employees are counted?

What is the plan?

What is “too disproportionate”?

12

Who is the Employer?

To prevent employers from avoiding the coverage rules

by moving all non-HCEs to a related company, certain

related companies are treated as a single company for

coverage purposes

13

Which Employees Are Counted?

Subject to 4 specific exceptions, all employees of the

employer are taken into account for coverage purposes

14

Employees Not Taken Into

Account in the Coverage Test

Employees who do not satisfy the plan’s age and

service requirements

Union employees (but subject to separate testing)

Nonresident aliens with no U.S. source income

15

Employees Not Taken Into

Account in the Coverage Test

For a plan with a last-day or minimum service accrual

requirement, employees who:

Are eligible but do not benefit under the plan

Are not employed on the last day of the plan year and

Complete less than 500 hours of service during the plan

year

16

What is the Plan?

Multiple plans may be combined for coverage testing

purposes (“aggregation”)

A single plan may be treated as separate plans for

coverage testing purposes (“disaggregation”)

17

Plan Aggregation

Always permissive (never required to aggregate plans

for coverage testing purposes)

If plans are aggregated for coverage testing purposes,

the plans must also satisfy the nondiscrimination

requirements on a combined basis

18

Plan Disaggregation

Permissive disaggregation – if two (or more) portions of a single plan separately satisfy coverage, these portions may be treated as separate plans for nondiscrimination testing purposes

Mandatory disaggregation – certain plan components and/or groups of employees must be treated as separate plans for coverage testing purposes

19

What is “Too Disproportionate”?

A plan may satisfy coverage by satisfying one of two

tests:

Ratio Percentage Test

Average Benefits Test

20

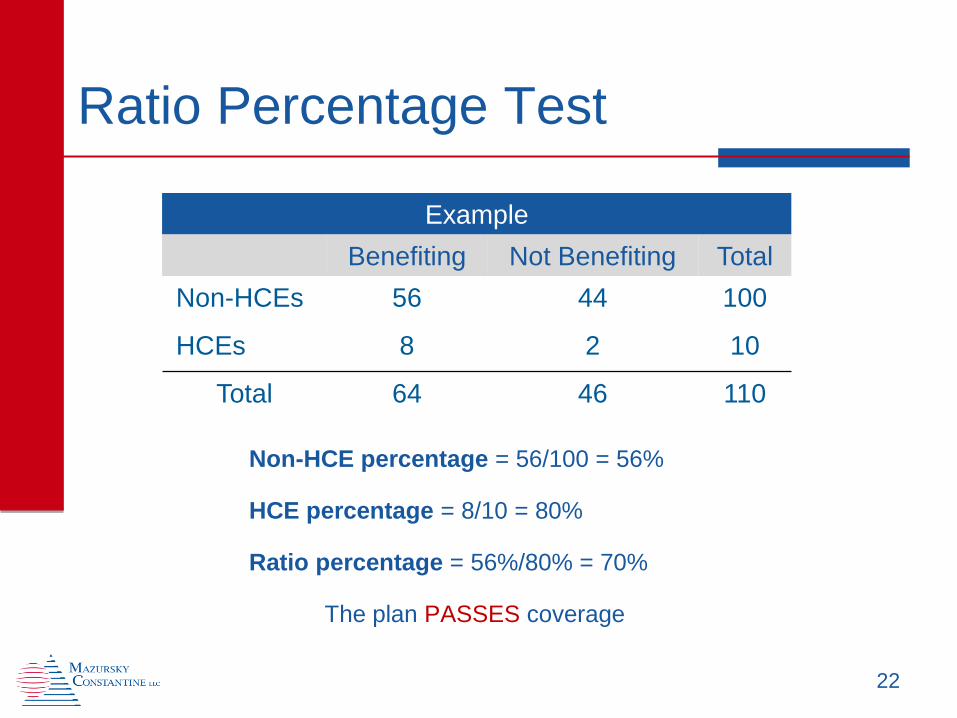

Ratio Percentage Test

The percentage of non-HCEs participating in the plan

must be at least 70% of the percentage of HCEs

participating in the plan

21

Ratio Percentage Test

Example

Benefiting Not Benefiting Total

Non-HCEs 56 44 100

HCEs 8 2 10

Total 64 46 110

22

Non-HCE percentage = 56/100 = 56%

HCE percentage = 8/10 = 80%

Ratio percentage = 56%/80% = 70%

The plan PASSES coverage

Average Benefits Test

More complicated than the Ratio Percentage Test

Takes into account the level of contributions and/or

benefits under the plan, not just whether an employee

is participating

23

ADP & ACP Testing

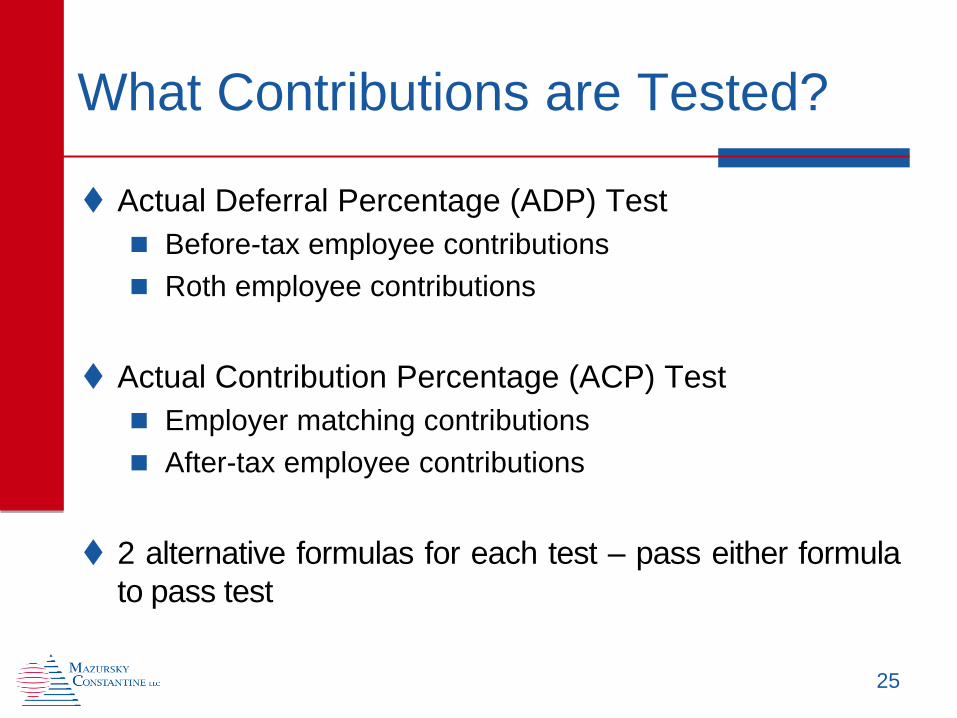

What Contributions are Tested?

Actual Deferral Percentage (ADP) Test

Before-tax employee contributions

Roth employee contributions

Actual Contribution Percentage (ACP) Test

Employer matching contributions

After-tax employee contributions

2 alternative formulas for each test – pass either formula

to pass test

25

What is ADP?

Each eligible employee’s actual deferral ratio (ADR) is

An eligible participant who made no deferral contributions

has a 0% ADR

ADP = Average of individual ADRs

26

Before-Tax and Roth Deferrals (no catch-ups)

Compensation

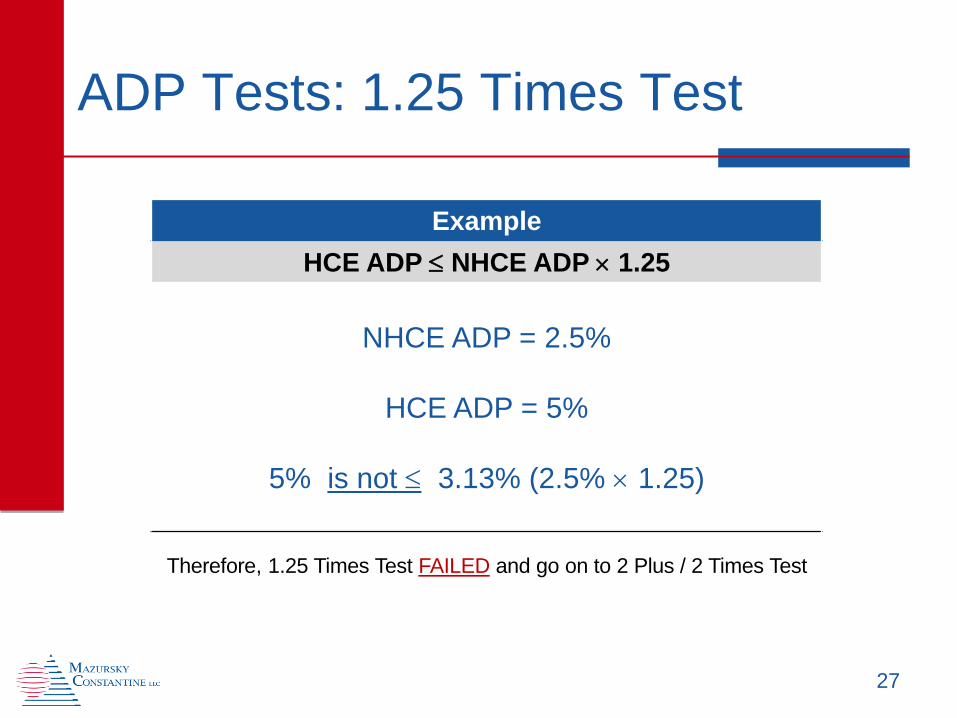

ADP Tests: 1.25 Times Test

27

Example

HCE ADP NHCE ADP 1.25

NHCE ADP = 2.5%

HCE ADP = 5%

5% is not 3.13% (2.5% 1.25)

Therefore, 1.25 Times Test FAILED and go on to 2 Plus / 2 Times Test

ADP Tests: 2 Plus / 2 Times Test

HCE ADP NHCE ADP + 2%

and

HCE ADP NHCE ADP 2

28

ADP Tests: 2 Plus / 2 Times Test

Example

2 Plus Portion 2 Times Portion

NHCE ADP = 2.5% HCE ADP = 5% 5% is not 4.5% (2.5% + 2%) Therefore, 2 Plus portion FAILED

NHCE ADP = 2.5% HCE ADP = 5% 5% is 5% (2.5% 2) Therefore, 2 Times portion PASSED

Since 2 Plus portion failed, entire 2 Plus / 2 Times Test FAILED

Since both 1.25 Times Test and 2 Plus / 2 Times Test failed, ADP Test FAILED

29

How Can Failing Test Be Corrected?

Return Deferrals to HCEs

Make Additional Contributions for NHCEs

Rerun test with different parameters

Disaggregate test group

Alternative test compensation definition

30

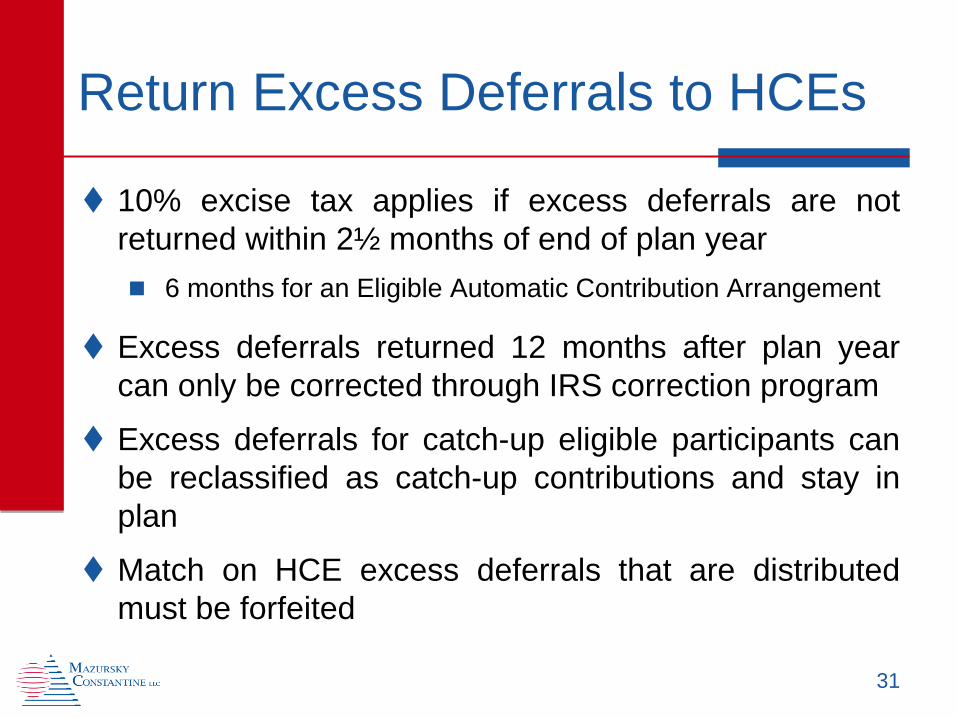

Return Excess Deferrals to HCEs

10% excise tax applies if excess deferrals are not

returned within 2½ months of end of plan year

6 months for an Eligible Automatic Contribution Arrangement

Excess deferrals returned 12 months after plan year

can only be corrected through IRS correction program

Excess deferrals for catch-up eligible participants can

be reclassified as catch-up contributions and stay in

plan

Match on HCE excess deferrals that are distributed

must be forfeited

31

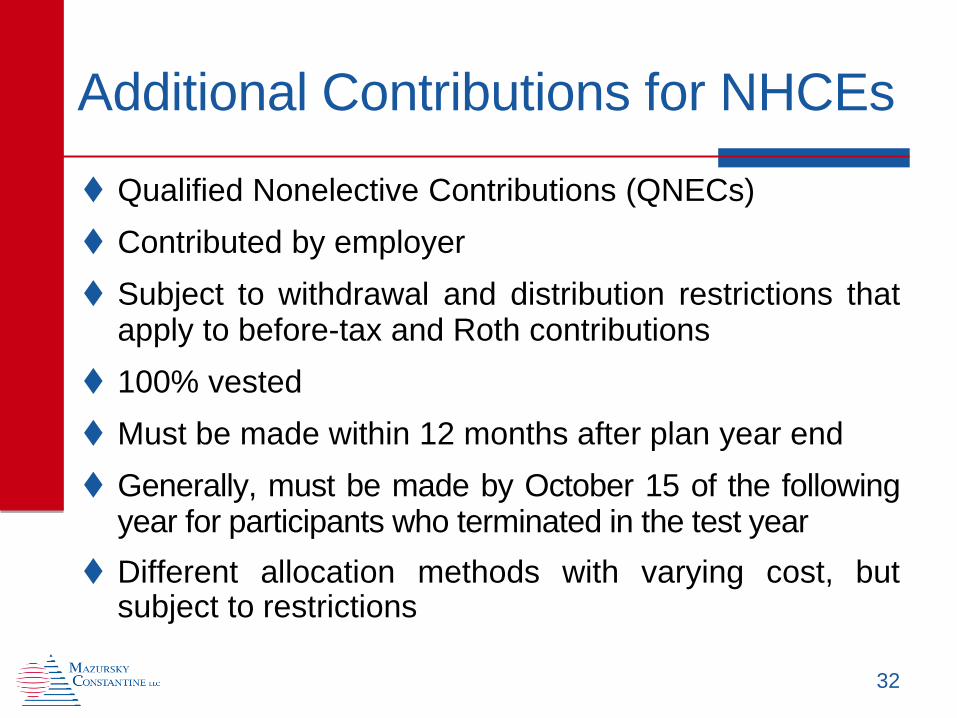

Additional Contributions for NHCEs

Qualified Nonelective Contributions (QNECs)

Contributed by employer

Subject to withdrawal and distribution restrictions that apply to before-tax and Roth contributions

100% vested

Must be made within 12 months after plan year end

Generally, must be made by October 15 of the following year for participants who terminated in the test year

Different allocation methods with varying cost, but subject to restrictions

32

ACP Test

Calculation is largely identical to ADP Test

Employer matching contributions and employee after-tax

contributions are used in place of deferrals

Must pass either 1.25 Times Test or 2 Plus / 2 Times

Test

Failed test corrected by either

Making QNECs to NHCEs

Distributing (if vested) or forfeiting (if not vested) HCEs’

contributions

33

How To Improve Testing Results

Limit amount that HCEs can contribute

Encourage participation by NHCEs

Auto-enrollment of employees

Auto-increase of employee deferral rates

Employee Education

Matching contributions

Safe Harbor plan design

34

Prior-Year Testing

Tests can be run on a prior-year basis

Same tests apply (1.25 Times and 2 Plus / 2 Times)

However current year’s HCE contribution rate is

compared to prior-year’s NHCE contribution rate

Allows employer to anticipate how much HCEs can

contribute

Limits availability of QNECs as correction method

Plan document must provide for current or prior-year

test method

35

Safe Harbor 401(k) Plans

37

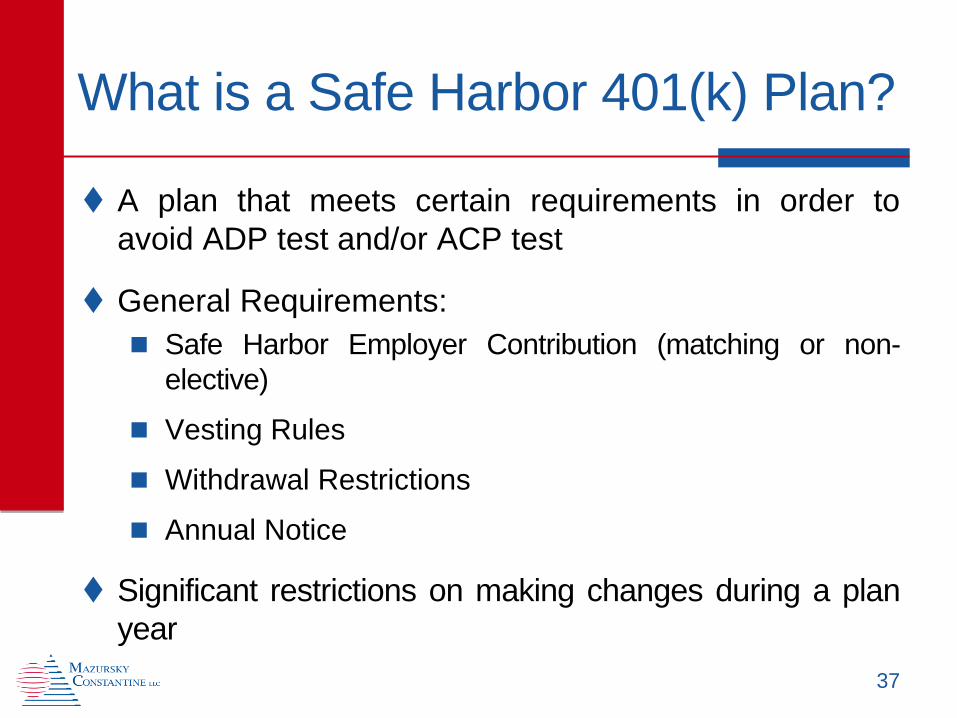

What is a Safe Harbor 401(k) Plan?

A plan that meets certain requirements in order to

avoid ADP test and/or ACP test

General Requirements:

Safe Harbor Employer Contribution (matching or non-

elective)

Vesting Rules

Withdrawal Restrictions

Annual Notice

Significant restrictions on making changes during a plan

year

38

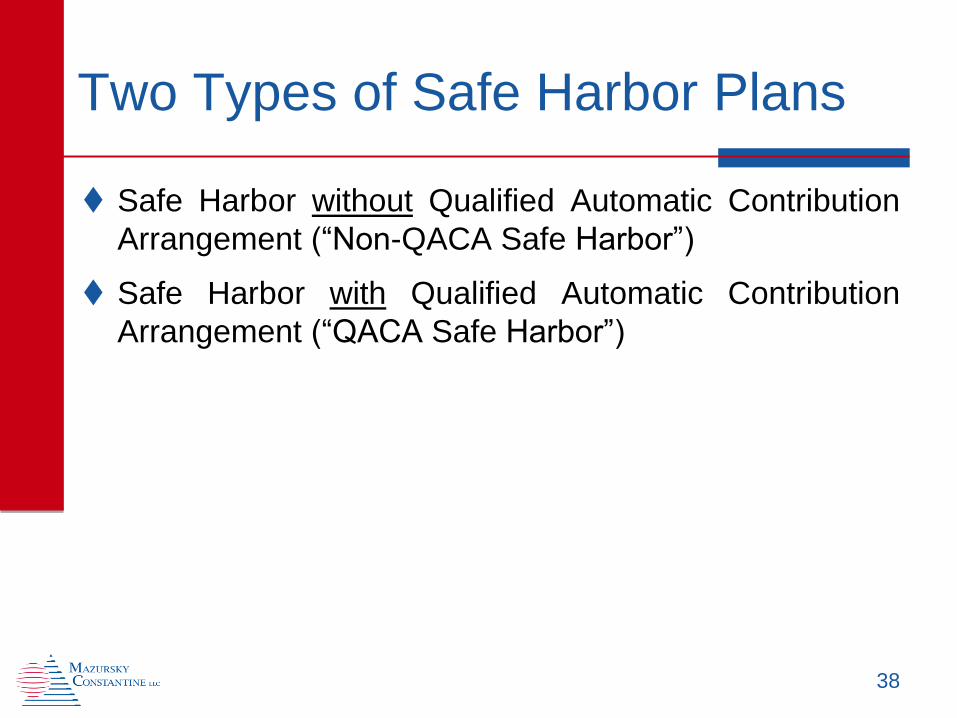

Two Types of Safe Harbor Plans

Safe Harbor without Qualified Automatic Contribution

Arrangement (“Non-QACA Safe Harbor”)

Safe Harbor with Qualified Automatic Contribution

Arrangement (“QACA Safe Harbor”)

39

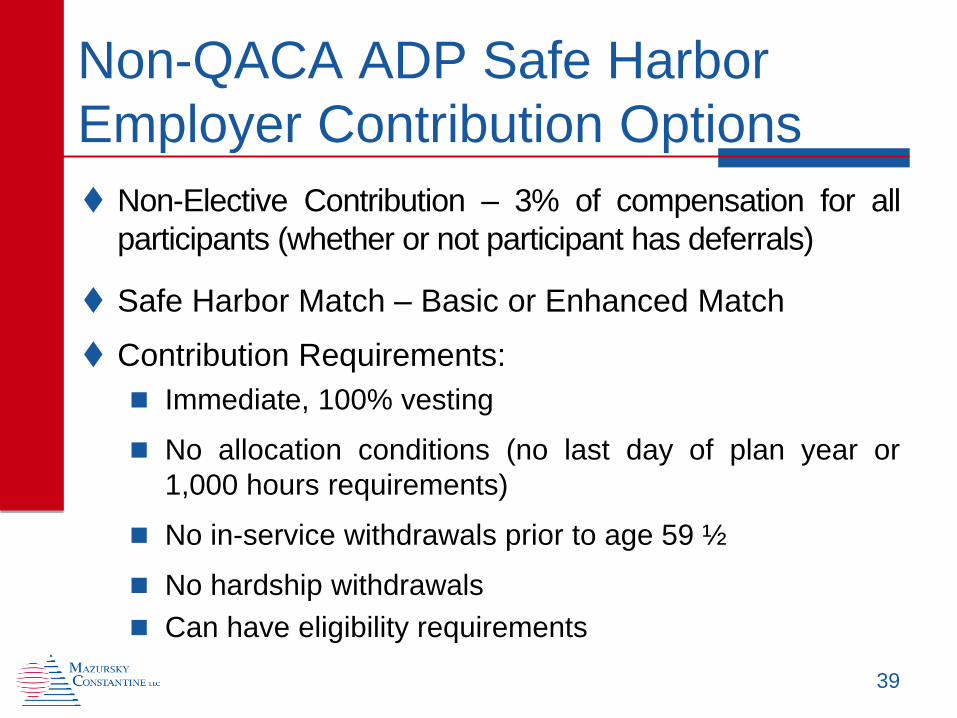

Non-QACA ADP Safe Harbor

Employer Contribution Options

Non-Elective Contribution – 3% of compensation for all

participants (whether or not participant has deferrals)

Safe Harbor Match – Basic or Enhanced Match

Contribution Requirements:

Immediate, 100% vesting

No allocation conditions (no last day of plan year or

1,000 hours requirements)

No in-service withdrawals prior to age 59 ½

No hardship withdrawals

Can have eligibility requirements

40

Basic Safe Harbor Match

100% of first 3% of compensation

plus

50% of next 2% of compensation

(4% total match)

41

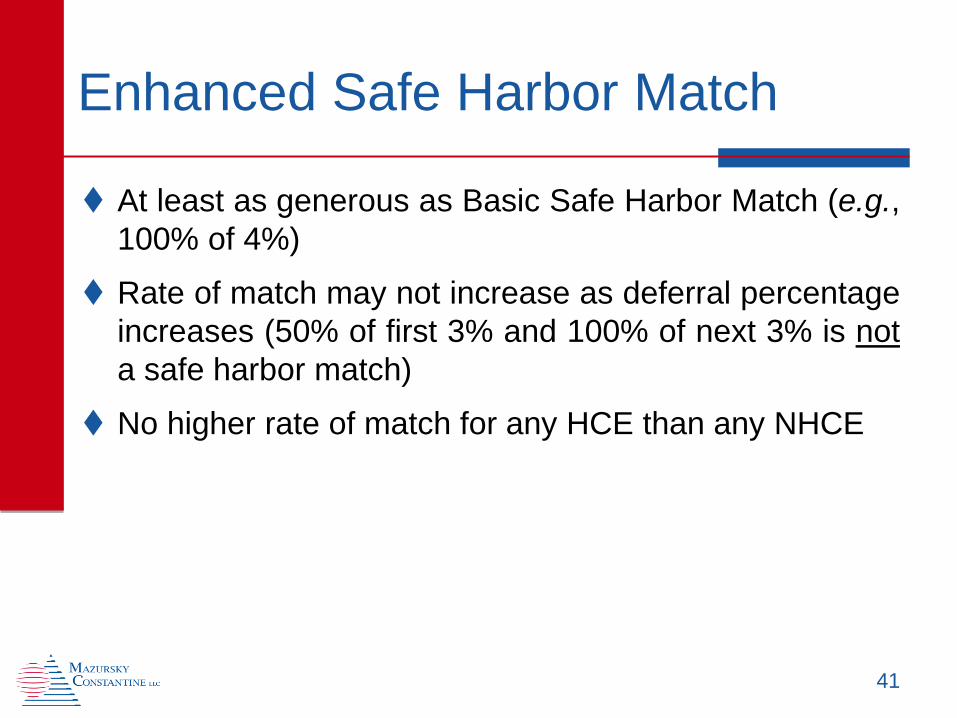

Enhanced Safe Harbor Match

At least as generous as Basic Safe Harbor Match (e.g.,

100% of 4%)

Rate of match may not increase as deferral percentage

increases (50% of first 3% and 100% of next 3% is not

a safe harbor match)

No higher rate of match for any HCE than any NHCE

42

Other Considerations for ADP

Safe Harbor

Must match catch-up contributions

Can make other employer contributions in addition to

safe harbor contribution

Match may be made on a payroll by payroll or on a

plan year basis

ACP Safe Harbor

Nonelective safe harbor contribution (3% of compensation)

will satisfy ACP test

Safe harbor match will satisfy ACP test as long as:

Do not match deferrals in excess of 6% of compensation

Discretionary matching contributions do not exceed 4%

of compensation

43

Notice Delivery Requirements

Deliver annual notice between 30 and 90 days before

beginning of every plan year

Deliver notice to newly eligible employees

No more than 90 days before employee becomes

eligible, or

If it is not administratively practicable to do so (e.g.,

plans with immediate eligibility), as soon as possible

after eligibility

44

Notice Content Requirement

Description of safe harbor contribution

Description of any other contributions*

How to make elective deferrals

Description of plan compensation*

Withdrawal and vesting provisions

How to obtain additional information

45

* Can be incorporated from SPD

Conditional Safe Harbor –

“Wait and See” Approach

Applies only to 3% non-elective (not match)

Plan document must provide for current year non-

discrimination testing

Safe harbor notice before plan year says employer

may make safe harbor contribution

Must adopt safe harbor amendment and provide follow-

up notice no later than 30 days before end of plan year

If the employer does not adopt the amendment, must

satisfy ADP and ACP tests for year

46

47

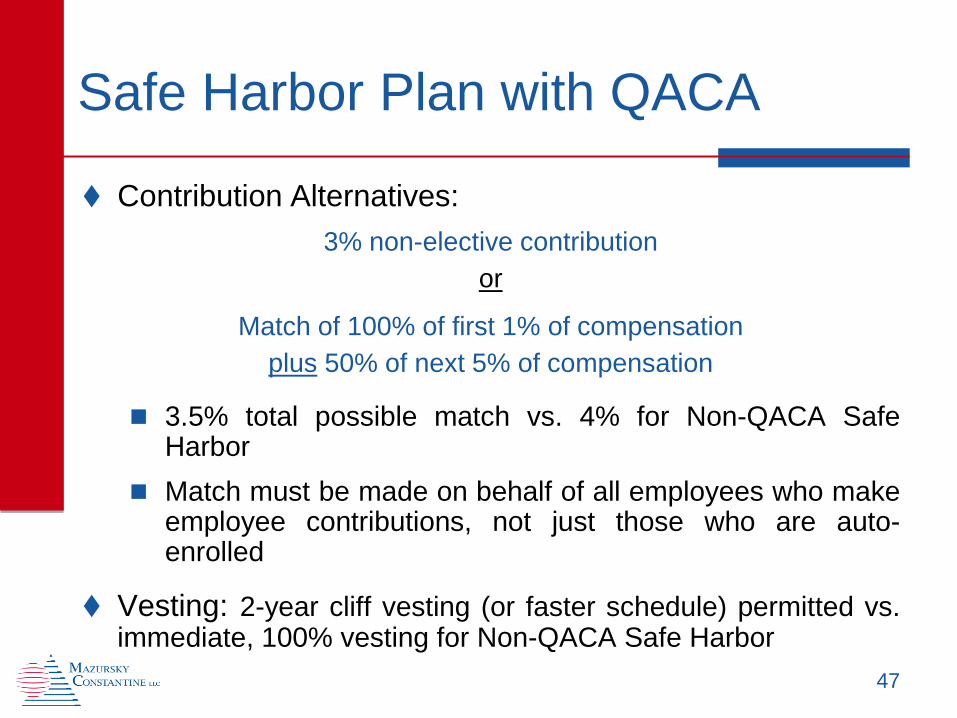

Safe Harbor Plan with QACA

Contribution Alternatives:

3% non-elective contribution

or

Match of 100% of first 1% of compensation

plus 50% of next 5% of compensation

3.5% total possible match vs. 4% for Non-QACA Safe Harbor

Match must be made on behalf of all employees who make employee contributions, not just those who are auto-enrolled

Vesting: 2-year cliff vesting (or faster schedule) permitted vs. immediate, 100% vesting for Non-QACA Safe Harbor

QACA Requirements

Must auto-enroll any participant who has not made an affirmative election as of QACA effective date

Participant must be automatically enrolled at 3% (or more)

from initial eligibility through end of following plan year

Automatic deferrals must automatically increase to 4% in

third year of participation, 5% in fourth year and 6% for

every year thereafter

Participant can always opt out of initial automatic enrollment or from automatic increases

Automatic enrollment percentage cannot exceed 10%

48

Compensation

Importance of Compensation

Calculation of Benefits

Satisfying Legal Requirements

Contribution and Benefit Limits

Nondiscrimination Testing

Identifying HCEs

50

Statutory Compensation Definition

Uses:

Identify highly compensated employees for testing

Calculate statutory limits on contributions and benefits

Can be used for ADP and ACP testing

Must use an IRS-approved 415 definition

51

IRS-Approved 415 Definitions

All amounts received for personal services and

includable in income (i.e., gross income), before pre-

tax deductions, but excluding nonqualified deferred

compensation, stock options, restricted stock, group term

life insurance premiums and similar items

Wages subject to withholding, before pre-tax deductions

W-2 wages, before pre-tax deductions

52

Benefits Compensation

Used to calculate amount of contributions and/or benefits

May also be used for ADP and ACP testing

Described in plan document

Must not discriminate in favor of highly compensated

employees

53

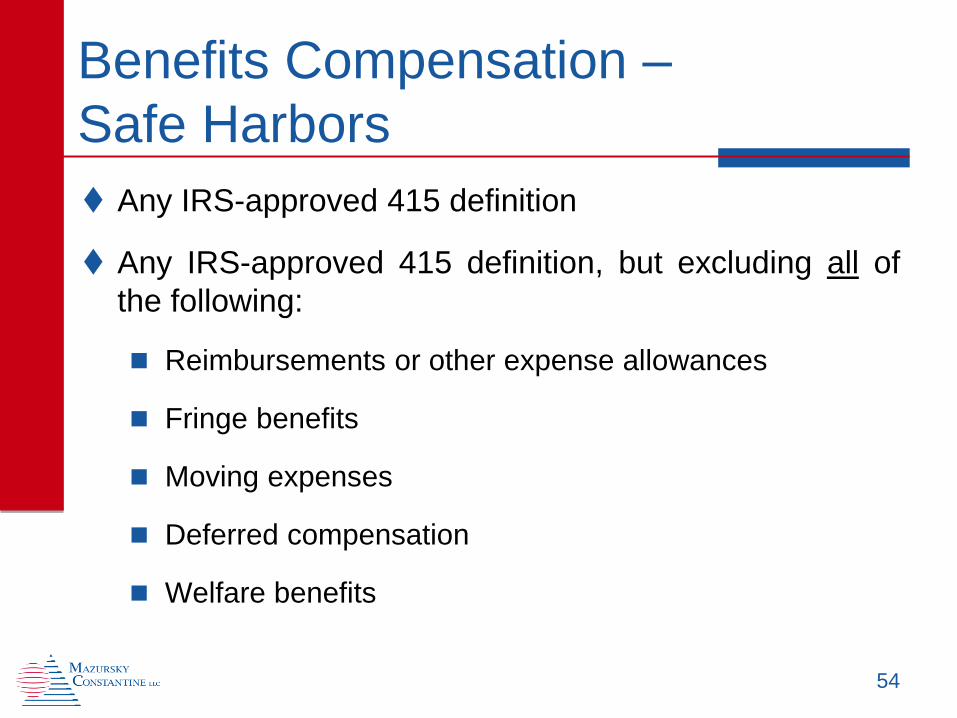

Benefits Compensation –

Safe Harbors

Any IRS-approved 415 definition

Any IRS-approved 415 definition, but excluding all of

the following:

Reimbursements or other expense allowances

Fringe benefits

Moving expenses

Deferred compensation

Welfare benefits

54

Compensation Limit

Compensation taken into account under the plan in a

year may not exceed IRS dollar limit ($255,000 for 2013)

Does not apply when determining HCEs

Does not require participant deferrals to be cut off when

the participant reaches the dollar limit

Limit may be applied by prorating limit for each pay

period, or based on YTD compensation

55

Post-Termination Pay

Compensation for contributions made after termination

of employment is restricted in a 401(k) plan

Post-termination severance may not be deferred

Post-termination trailing pay may be deferred (e.g., salary,

bonus, commissions, shift premiums and similar pay)

Post-termination leave payouts may be deferred

Plan is not required to allow deferral post-termination

The default restrictions also apply to IRS 415 definitions

56

Compensation and Payroll

Payroll must coordinate with plan terms to ensure that

correct compensation items are being used for each

purpose

Area of frequent errors in IRS audits

Post-termination items may be different than included

before termination

Must be updated when payroll codes are added

57

Internal Revenue Service

Correction Programs

Employee Plans Compliance

Resolution System (“EPCRS”)

IRS-approved corrections

3 Components:

Self-Correction Program (“SCP”)

Voluntary Correction Program (“VCP”)

Audit Closing Agreement Program (“Audit CAP”)

59

General EPCRS Principles

Encourages voluntary correction of errors

Corrections should:

Restore plan to the position it would have been in had

the failure not occurred

Be adjusted for earnings

Not favor highly compensated employees

May be more than one reasonable method of correction

Must update administrative procedures to avoid

recurrence of the failures

60

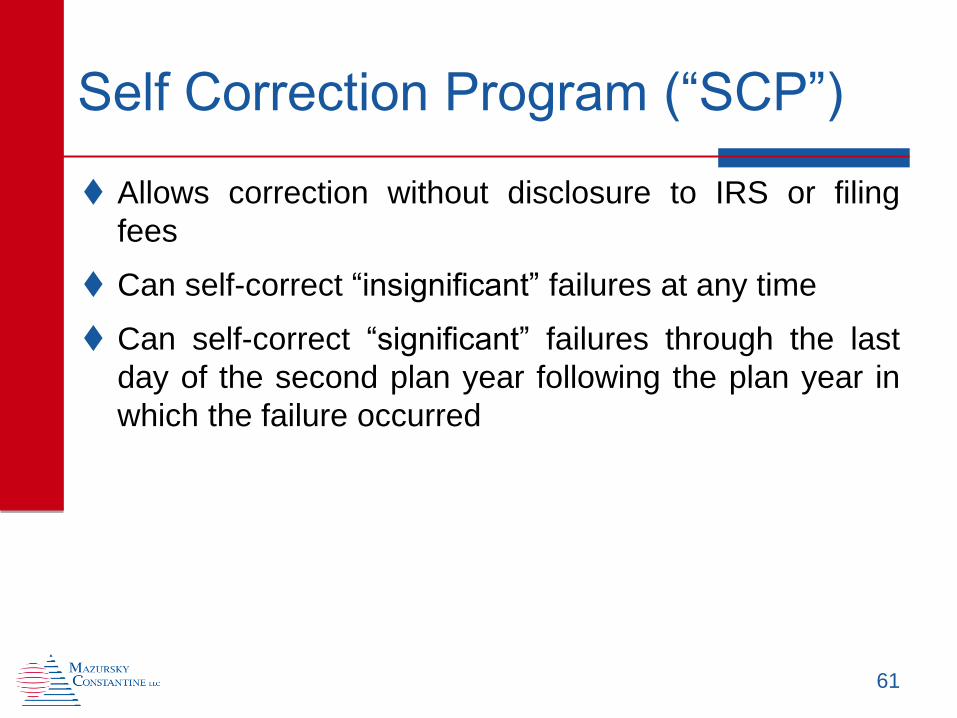

Self Correction Program (“SCP”)

Allows correction without disclosure to IRS or filing

fees

Can self-correct “insignificant” failures at any time

Can self-correct “significant” failures through the last

day of the second plan year following the plan year in

which the failure occurred

61

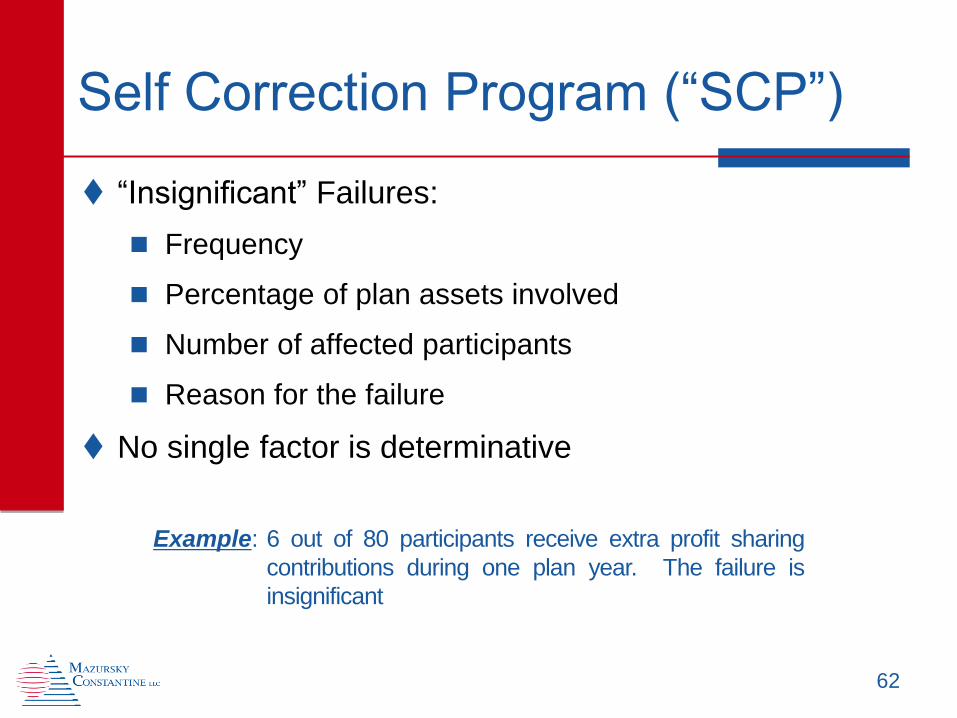

Self Correction Program (“SCP”)

“Insignificant” Failures:

Frequency

Percentage of plan assets involved

Number of affected participants

Reason for the failure

No single factor is determinative

62

Example: 6 out of 80 participants receive extra profit sharing

contributions during one plan year. The failure is

insignificant

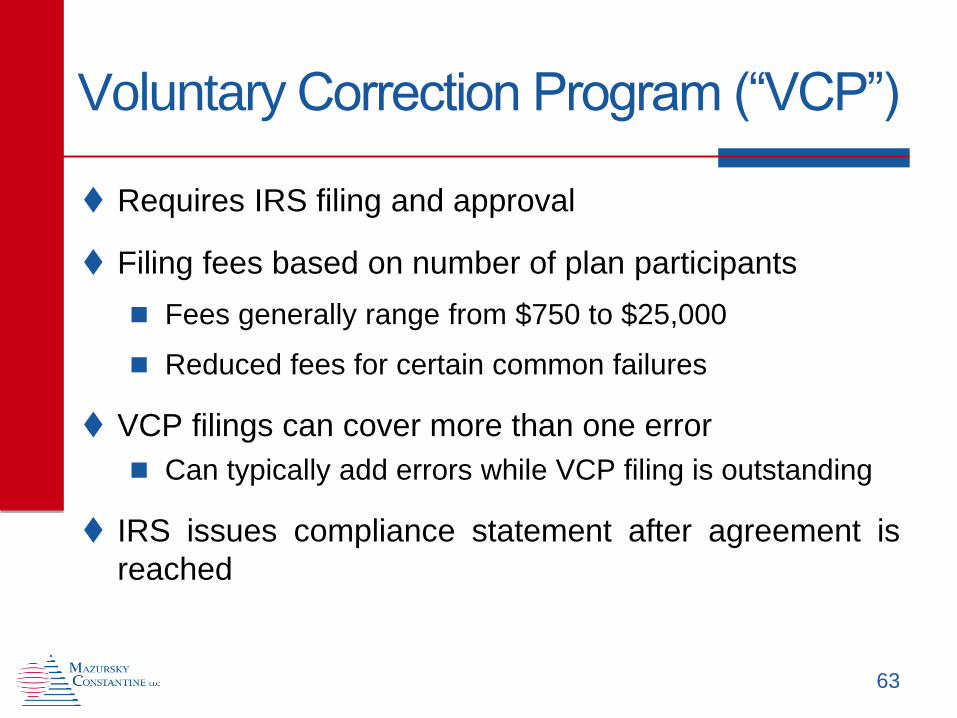

Voluntary Correction Program (“VCP”)

Requires IRS filing and approval

Filing fees based on number of plan participants

Fees generally range from $750 to $25,000

Reduced fees for certain common failures

VCP filings can cover more than one error

Can typically add errors while VCP filing is outstanding

IRS issues compliance statement after agreement is

reached

63

Why would you use VCP?

Error not eligible for correction under SCP

Retroactive plan amendments

Significant failure that is beyond 2-year correction period

No standard correction under EPCRS

Different method of correction than as described by IRS

IRS can waive excise/penalty taxes that apply to certain

errors

64

Voluntary Correction Program (“VCP”)

Streamlined submissions for common errors follow pre-

approved methods of correction:

Nonamender Failures

Correction: Execute missed amendments

Missed Loan Repayments

Correction: Reamortize impacted loans or allow participants to

repay missed payments in one lump sum

Tax relief available

Failure to pay required minimum distributions

Correction: Distribute missed required minimum distributions

Excise tax relief available

65

Voluntary Correction Program (“VCP”)

Audit CAP

Errors the IRS identifies

IRS-required correction plus penalty

Audit CAP penalties extremely unpredictable

Failure to reach resolution with the IRS will result in

plan disqualification

66

Common Errors and Corrections

Improperly Excluded Employees

Corrective contribution equal to 50% of “missed deferral

opportunity”

Based on average deferral percentage (ADP) for the year

Special rules apply to safe harbor and 403(b) plans

Corrective contribution equal to 100% of matching

contributions participant would have received on

“missed deferral opportunity”

Can be treated as a matching contribution subject to the

plan’s vesting schedule

67

Common Errors and Corrections

Overpayments

Participant must return overpayment

Under a defined benefit plan, if participant is receiving

periodic payments, overpayment may be recovered from

future payments

Plan sponsor may be required to make the plan whole if

participant does not return overpayment

Notify participant that overpayment is not eligible for

rollover

68

Common Errors and Corrections

Plan Eligibility Errors

If letting participants in early, amend the plan to conform

to operations (does not require VCP submission)

If letting participants in late, follow correction for

improperly excluded employees

Plan Compensation Errors

If more favorable to participants, amend the plan to conform to operations (VCP submission may be required)

If less favorable to participants, make corrective contribution based on plan definition of compensation

69

Example: The plan document requires 1 year of service. The employer has been allowing employees to participate after 6 months

Department of Labor

Correction Programs

Department of Labor Corrections

Voluntary Fiduciary Correction Program (“VFCP”)

Delinquent Filer Voluntary Compliance Program (“DFVCP”)

71

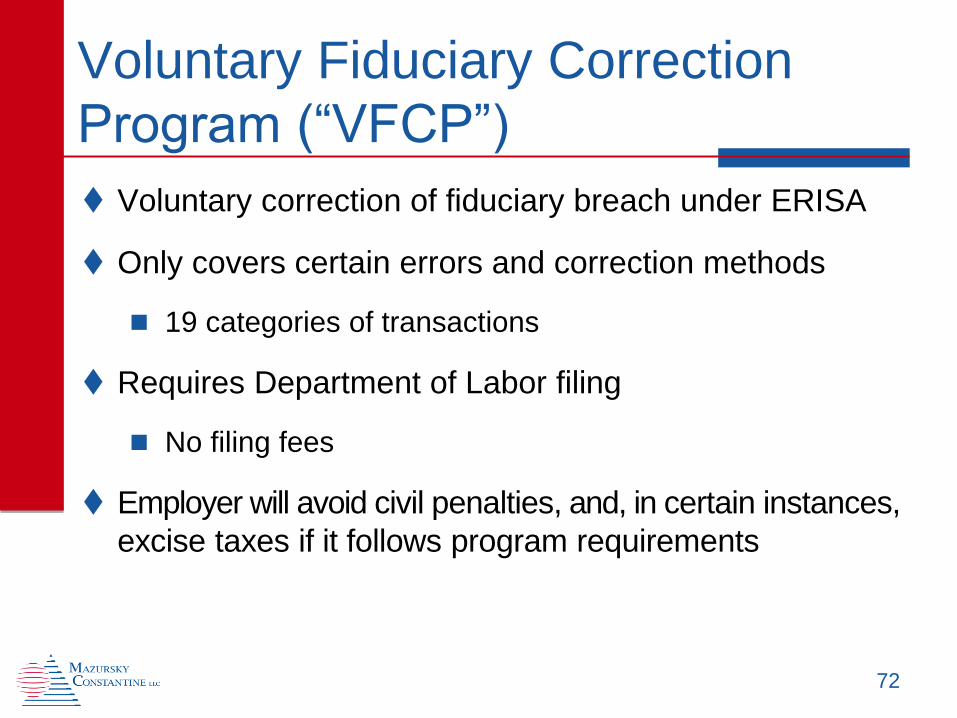

Voluntary Fiduciary Correction

Program (“VFCP”)

Voluntary correction of fiduciary breach under ERISA

Only covers certain errors and correction methods

19 categories of transactions

Requires Department of Labor filing

No filing fees

Employer will avoid civil penalties, and, in certain instances,

excise taxes if it follows program requirements

72

Voluntary Fiduciary Correction

Program (“VFCP”)

Most common error – late participant contributions

Pay contributions to plan

Adjust contributions for earnings (or, if greater, profits

earned by employer from use of contributions)

Use DOL online calculator to determine earnings

Correction will typically eliminate excise taxes

73

Delinquent Filer Voluntary

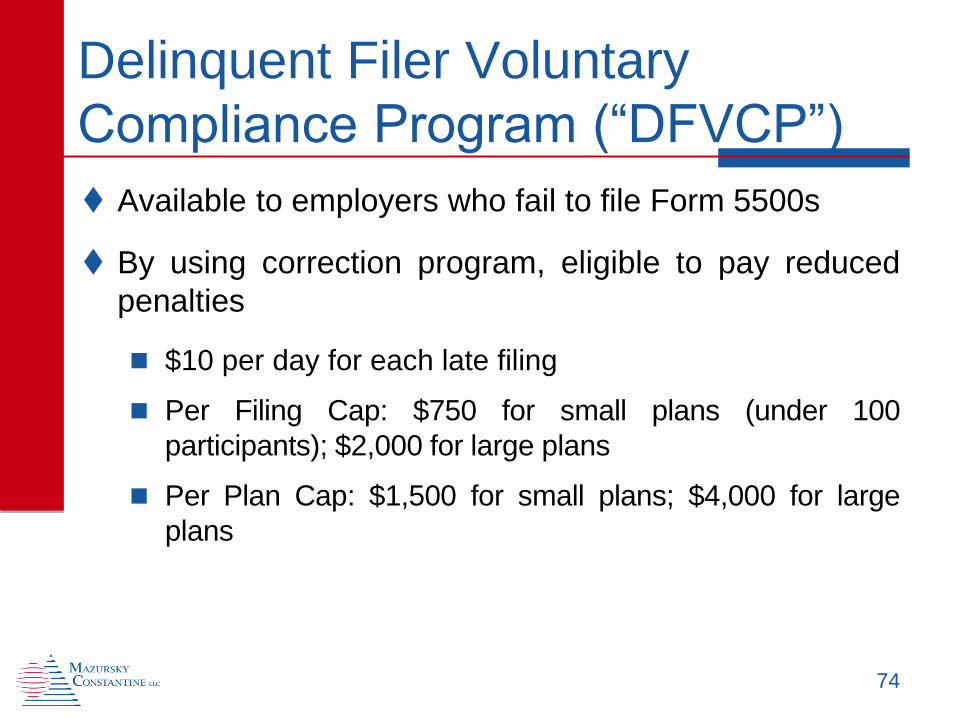

Compliance Program (“DFVCP”)

Available to employers who fail to file Form 5500s

By using correction program, eligible to pay reduced

penalties

$10 per day for each late filing

Per Filing Cap: $750 for small plans (under 100

participants); $2,000 for large plans

Per Plan Cap: $1,500 for small plans; $4,000 for large

plans

74

Plan Audits and Common Errors

IRS Audits

IRS Audits – Common Problems

Missing Amendments

Amendments required by law changes must be adopted by

date specified by law or regulation

Discretionary plan amendments – design changes generally

must be adopted by last day of plan year, but some

amendments (e.g., those that cut back eligibility or benefits)

must be adopted before they become effective

77

IRS Audits – Common Problems

Eligibility Errors

Participants not timely enrolled after meeting age/service

requirements

Rehires improperly required to re-complete service

requirements

78

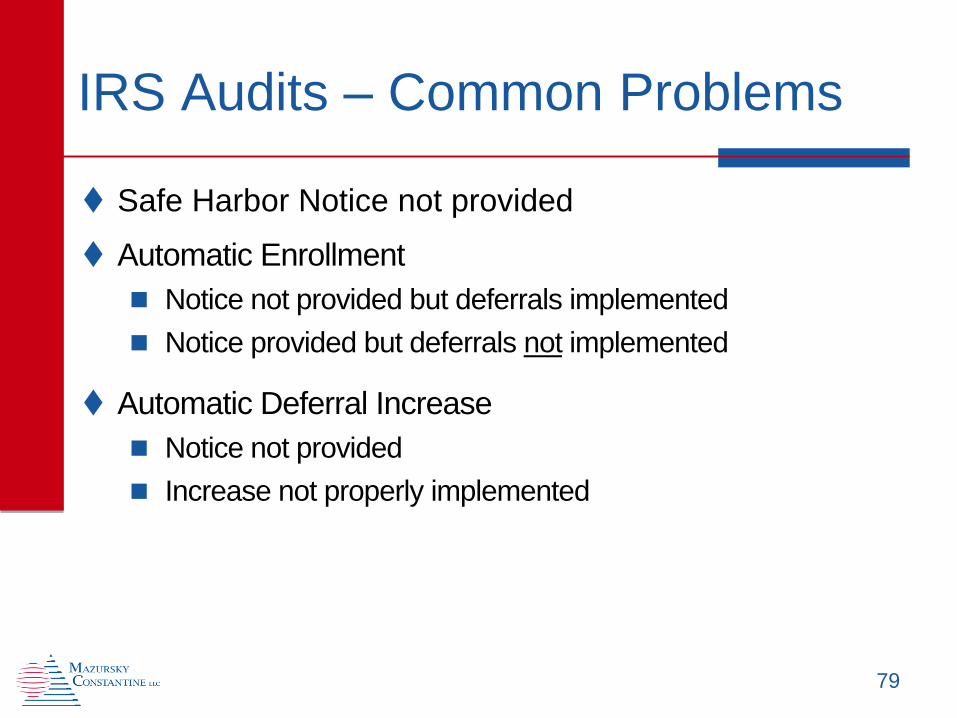

IRS Audits – Common Problems

Safe Harbor Notice not provided

Automatic Enrollment

Notice not provided but deferrals implemented

Notice provided but deferrals not implemented

Automatic Deferral Increase

Notice not provided

Increase not properly implemented

79

IRS Audits – Common Problems

Matching Contributions

Plan formula not followed

Plan match eligibility rules not followed

80

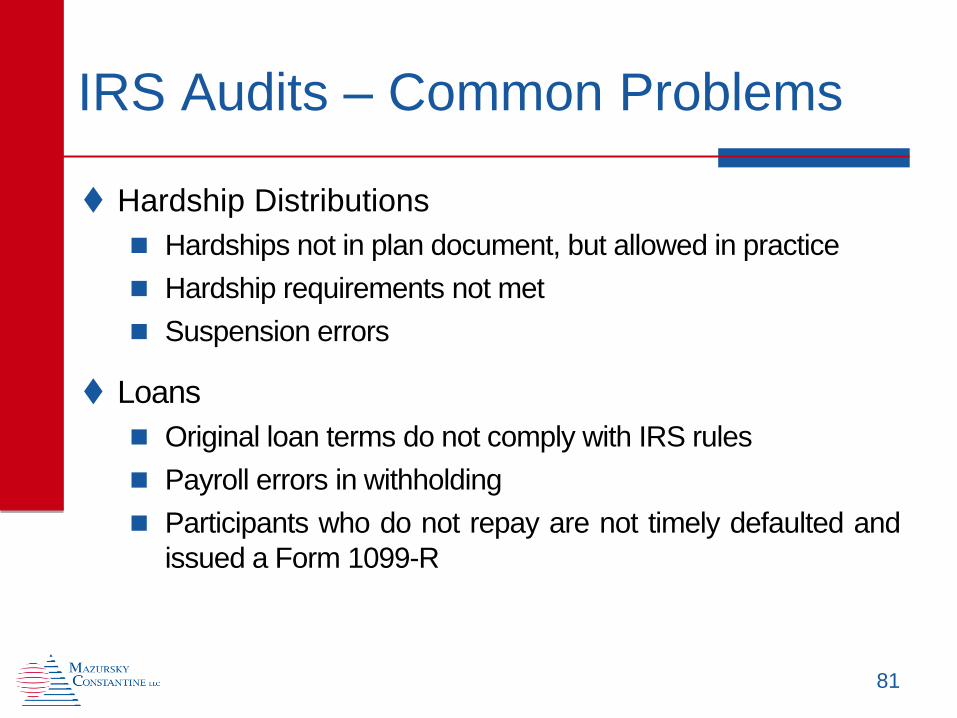

IRS Audits – Common Problems

Hardship Distributions

Hardships not in plan document, but allowed in practice

Hardship requirements not met

Suspension errors

Loans

Original loan terms do not comply with IRS rules

Payroll errors in withholding

Participants who do not repay are not timely defaulted and

issued a Form 1099-R

81

IRS Audits – Common Problems

Failure to follow written plan document

“Compensation” definition not followed in determining

participant deferrals and/or employer contributions

Plan document does not cover all entities whose

employees participate

Participation by subsidiaries may require written action of

both plan sponsor and subsidiary

Defined benefit plan formula not followed

82

IRS Audits – Common Problems

Vesting

Vesting service not properly calculated

Partial termination (20% active participant reduction) not

identified

Minimum Required Distributions (Age 70½) are not

timely made

83

IRS Audits – Common Problems

Forfeitures Not Timely Used

Forfeitures must be used to pay plan expenses, reduce

employer contributions or (rarely) allocated to participants

Plan document may require that forfeitures be used in

the year they arise or the next following year

Some documents are more flexible than others

Failure to use forfeitures may be both a qualification

defect and excise tax on nondeductible contributions

84

IRS Audits – Common Problems

ADP/ACP Testing Issues

Incorrect compensation used to identify “highly

compensated employees” or in performing test

Other data errors affecting tests

Failure to perform test for safe-harbor plan with delayed

eligibility for matching contributions

85

IRS Audits –

Corrections and Penalties

“Insignificant” errors identified in IRS audit may be

corrected without penalty

Significant errors may be corrected through a closing

agreement (“Audit CAP”) and payment of a

negotiated sanction

86

IRS Audits – Audit CAP Sanction

Amount of sanction will depend on size of plan and

nature of error(s)

Sponsor has no real leverage in negotiating the

sanction

Alternative is likely plan disqualification with far

greater consequences

87

DOL Audits

DOL Audits – Common Problems

Late Deposit of Participant Contributions

Deadline – earliest date on which contributions can be

reasonably segregated from sponsor’s general assets

15th business day of the following month will never be

considered timely

7 business day safe harbor for plans with under 100

participants

DOL will look to sponsor’s shortest period as setting

standard for reasonableness

89

DOL Audits – Common Problems

Improper Plan Expenses

Employer (“settlor”) expenses cannot be paid from the

Trust

Expenses paid from wrong plan (e.g., 401(k) plan

expenses paid from defined benefit plan)

Nonqualified plan expenses paid for by related qualified

plan

For multi-purpose communications, may need to allocate

between different plans and plan-employer

90

Examples: Cost of optional amendment; accounting expenses

relating to preparation of the employer’s financial

statements

DOL Audits – Common Problems

Fiduciary Oversight Issues

Fiduciaries are unaware of their fiduciary roles

Lack of fiduciary processes (e.g., including 401(k)

investment fund review)

Failure to monitor vendor expenses (e.g., annuity

contract costs)

91

Reliance on Form 5500 Auditor

Financial accounting audits are limited in scope and

consistency

Do not rely on Form 5500 auditors to identify errors

Late contributions and other errors sometimes, but not

always, identified in Form 5500 audit

92