qis5 august 2010 seminar - eiopa · guidance ifrs-sii adjustments (assets) •goodwill •other...

TRANSCRIPT

26 August 2010 Page 1

CEIOPS

Disclaimer

Please note that those slides are not part of the formal QIS5 documentation as issued by the European Commission. They are not intended to, and do not, replace the QIS5 Technical Specifications or any other part of the QIS5 documentation. They do not supersede the European Commission documentation.

The seminar relied to a large extent on the QIS5 technical specifications, QIS5 spreadsheet, qualitative questionnaires as well as simplifications and helper tabs.

Answers to questions raised of European relevance will be integrated in the Q and A document.http://www.ceiops.eu/index.php?option=content&task=view&id=752

26 August 2010 Page 2

QIS5 planning

26 August 2010 Page 3

CEIOPS

QIS5 - objectives

•Will require a high level of participation of solo undertakings and groups

• The main issues are

– The calibration of the standard formula

– Groups calculations

– Internal model

– Complexity

• But also to foster preparedness of industry and supervisors

CEIOPS is committed to ensuring the success of QIS5

26 August 2010 Page 4

CEIOPS

QIS5 versus QIS4

26 August 2010 Page 5

CEIOPS

Page 5

Aligning technical specification with level 2 implementing measures

•Design: ensure the inherent consistency of the proposals

•Quality: ensure that the proposals provide the appropriate level of financial soundness

–For example, what is the use of discussing the level of the capital requirements if these requirements are not supported by sufficient quality of capital?

•Calibration: regular review – transparency and credibility of the process

26 August 2010 Page 6

CEIOPS

Preparing and running QIS5

26 August 2010 Page 7

CEIOPS

QIS 5 - timeline

2010

2011

March 2010 - CEIOPS provides draft technical specifications to EC

July 2010 – EC/EIOPC provide final technical specifications to CEIOPS

August–Nov – QIS 5 exercise• End of October for solo entities

• Mid November for Groups (analysis to be performed in a centralised database)

April 2011 – QIS 5 Report

26 August 2010 Page 8

CEIOPS

Pre-test and spreadsheets

6 Jul 12 Jul 19 Jul 26 Jul 2 Aug 9 Aug 16 Aug 23 Aug 30 Aug

Publication of final technical

specifications by EC

Solo+group spreadsheets available

Pre-test solo spreadsheets

•Aim of the pre-test is to debug the spreadsheets (highly involved but limited number of participants ideally) •Pre-test spreadsheets can not be used to submit final results

26 August 2010 Page 9

CEIOPS

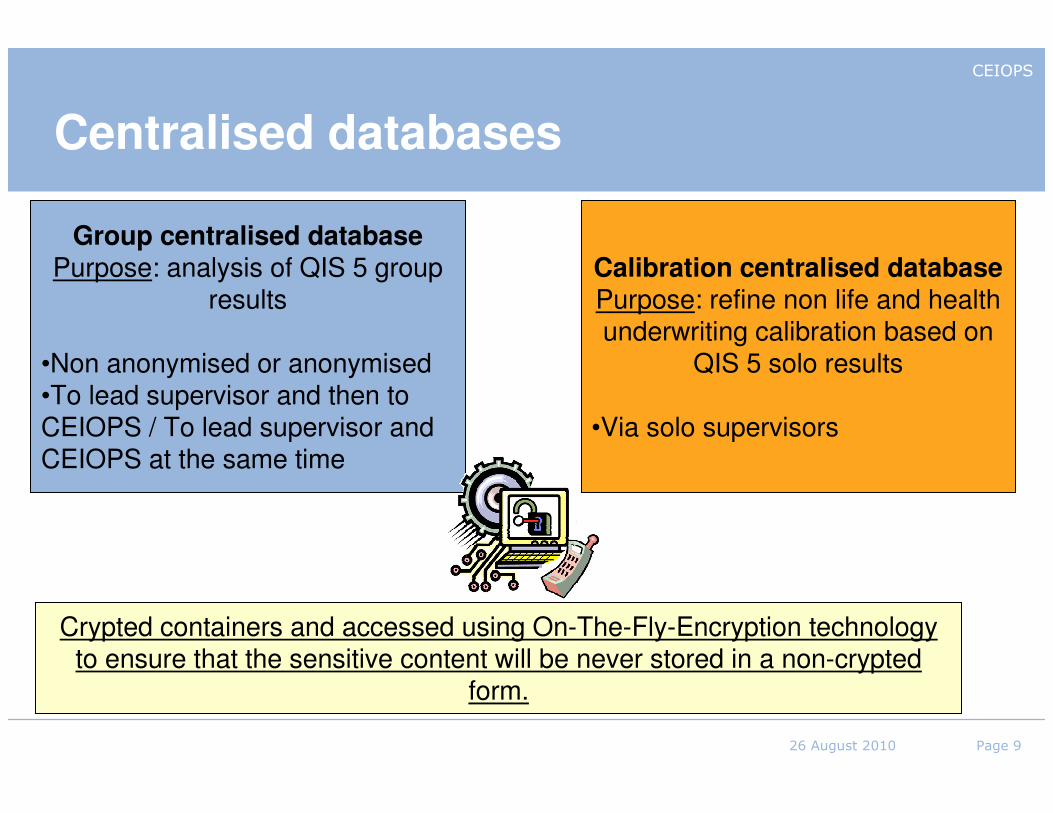

Centralised databases

Group centralised databasePurpose: analysis of QIS 5 group

results

•Non anonymised or anonymised•To lead supervisor and then to CEIOPS / To lead supervisor and CEIOPS at the same time

Calibration centralised databasePurpose: refine non life and health underwriting calibration based on

QIS 5 solo results

•Via solo supervisors

Crypted containers and accessed using On-The-Fly-Encryption technology to ensure that the sensitive content will be never stored in a non-crypted

form.

26 August 2010 Page 10

CEIOPS

Spreadsheets and technical specifications but also …

•Simplification

•Helper tabs

•QIS5 for beginner guide

•National guidance

•Centralised databases

•Q and A

•Training

•Qualitative questionnaires

26 August 2010 Page 11

CEIOPS

Simplifications and helper tabs

26 August 2010 Page 12

CEIOPS

Page 12

National guidance

26 August 2010 Page 13

CEIOPS

Q and A

•Escalation process at EEA level: if national supervisors can not answer the question

•Content of the specifications: started on 6 July– EC included in the red flag procedure before the publication

•Spreadsheets: started on 23 August

26 August 2010 Page 14

CEIOPS

Trainings

•CEIOPS seminars

•European workshops

•Sharing experience

•National initiatives from supervisors and trade associations

26 August 2010 Page 15

CEIOPS

Qualitative questionnaires

•All undertakings

•Internal model users

•Group users

26 August 2010 Page 16

CEIOPS

After QIS5

•Further impact assessment based on data collected for “fine tuning”L2 and developing L3 – process to be agreed in the November MM

•If needed, short and restricted QIS6

•Implementation of Solvency 2!!!

26 August 2010 Page 17

CEIOPS

Page 17

To conclude

•QIS5 is crucial to test the system

–Therefore important not to make approximations (feasibility)

–To assess the impact

•QIS5 results will be use also to assess the needs and contents of L3 guidance linked to pillar 1

•QIS5 is a major step in the preparedness to Solvency 2

26 August 2010 Page 18

Valuation of assets and Valuation of assets and ‘‘other liabilitiesother liabilities’’

26 August 2010 Page 19

CEIOPS

The balance sheet

• Starting position for QIS5!

• Economic valuation

26 August 2010 Page 20

CEIOPS

Valuation approach

• Economic, market consistent approach

– No subsequent adjustment for own credit risk

• IFRS as a proxy

– Only if reflects economic value!

• Materiality applies

• Valuation hierarchy

– Requirements for the valuation process

26 August 2010 Page 21

CEIOPS

Guidance IFRS-SII adjustments (assets)

CEIOPS

• Goodwill

• Other intangible assets

• Property, plant and equipment

• Inventories

• Finance leases

• Investment property

• Participations in subsidiaries, associates and joint ventures

• Financial assets

• Non-current assets held for sale or discontinued operation

• Deferred tax assets

• Current tax assets

• Cash and cash equivalents

26 August 2010 Page 22

CEIOPS

Guidance IFRS-SII adjustments (liabilities)

CEIOPS

• Provisions

• Financial liabilities

• Contingent liabilities

• Deferred tax liabilities

• Current tax liabilities

• Employee benefits and termination benefits

26 August 2010 Page 23

Market risk for non with Market risk for non with

profit business profit business

26 August 2010 Page 24

CEIOPS

26 August 2010 Page 24

Agenda

• Market risk in QIS 5

• Look-through approach

• Market risk sub-modules

• Focus on spread risk

26 August 2010 Page 25

CEIOPS

26 August 2010 Page 25

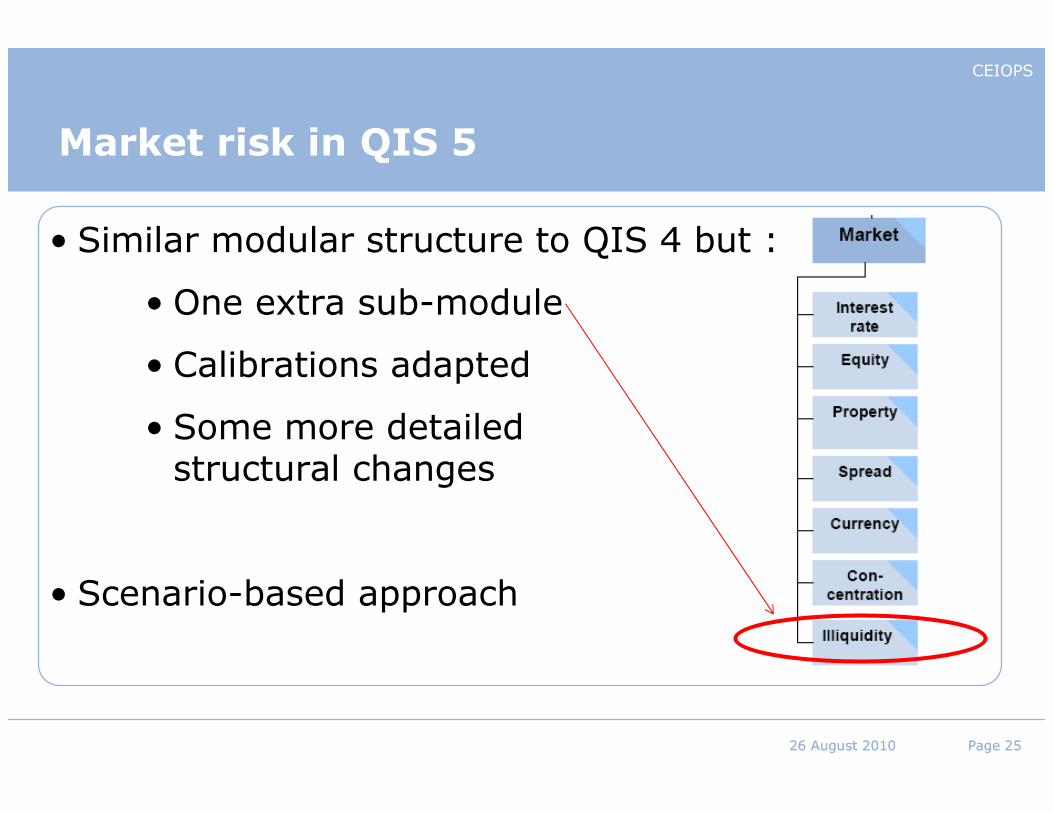

Market risk in QIS 5

• Similar modular structure to QIS 4 but :

• One extra sub-module

• Calibrations adapted

• Some more detailed structural changes

• Scenario-based approach

26 August 2010 Page 26

CEIOPS

26 August 2010 Page 26

Market risk in QIS 5 – Correlation matrix

• New correlation parameters

• Up/Down correlation matrix

26 August 2010 Page 27

CEIOPS

26 August 2010 Page 27

Look-through approach

• “Substance over form” principle

=> Economic substance rather than legal form of the investment determines its treatment

• Assets underlying collective investment vehicles/funds must be examined and would be subjected to the relevant sub-modules.

• Look-through approach required while risks are material

26 August 2010 Page 28

CEIOPS

26 August 2010 Page 28

Equity

• 39% “Global” and 49% “Other”

• Symmetric ajustment : -9% in QIS 5

• 0,75 correlation between “Global” and “Other”

• Participations

• Strategic

• Financial and credit institutions

• Excluded from the scope of the group

• Duration dampener (article 304 of the Directive)

26 August 2010 Page 29

CEIOPS

26 August 2010 Page 29

Interest rate

• Scenario-based approach

• Shocks applied to the risk free term structures (not to the illiquidity premium)

• Upward stress and downward stress for each maturity (SCR.5.21)

• Two sets of correlation

26 August 2010 Page 30

CEIOPS

26 August 2010 Page 30

Property

• Scenario-based approach

• 25% charge

• Look-through approach for collective real estate vehicles

• Taking in account of gearing

26 August 2010 Page 31

CEIOPS

26 August 2010 Page 31

Currency

• Worst of -/+25% charge for all foreign currency holdings

• Erratum of the EC for this submodule

• Lower for several currencies pegged to the euro :

26 August 2010 Page 32

CEIOPS

26 August 2010 Page 32

Concentration

• Calculation per exposure:

• Exposures of the same group are not independent

• Charge depends on the rating

• Aggregation with zero correlation

• Special treatments:

• Sovereign bonds

• Covered bonds

• Property

• Participations

● Helper tab for this sub-module

26 August 2010 Page 33

CEIOPS

26 August 2010 Page 33

Liquidity premium

• New sub-module

• Capture the illiquidity premium risk (increase of the value of TP due to a decrease of in the illiquidity premium)

• 65% fall in the value of the illiquidity premium

• Negatively correlated with spread risk

26 August 2010 Page 34

CEIOPS

26 August 2010 Page 34

Focus on spread risk

• Scenario-based approach

• Separate treatment for:

• Bonds

• Structured products

• Credit derivatives

• Helper tab for this submodule

• Link with counterparty default risk

26 August 2010 Page 35

CEIOPS

26 August 2010 Page 35

Focus on spread risk - Bonds

• Simplification: factor-based approach

• Special treatment for:

• Covered bonds

• Sovereign and supranational debts

26 August 2010 Page 36

CEIOPS

26 August 2010 Page 36

Focus on spread risk – Structured products

• Two scenarios:

• direct spread shock (level of the shock depends on the rating class and the duration of the credit exposure)

• shock on underlying assets

• Scenario-based approach => 0 < Shock < 100% of MV

26 August 2010 Page 37

CEIOPS

26 August 2010 Page 37

Focus on spread risk – Credit derivatives

• Scenario-based approach

• Only credit derivatives which are not part of undertaking’s risk mitigation policy

• Upward shock (in absolute terms) and downward shock (in relative terms)

26 August 2010 Page 38

SCRSCR-- nnon life underwriting riskon life underwriting risk

26 August 2010 Page 39

CEIOPS

Index

• Non life underwriting risk module

� General principles

� Catastrophe risk

- natural cat scenarios (regional)

- man made scenarios

- factor based method

�Undertaking specific parameters

• Counterparty default risk

• Technical specification, the spreadsheet, the qualitative questionnaires, helper tabs

• New in QIS 5, from QIS 4

26 August 2010 Page 40

CEIOPS

Non life underwriting risk –general principles

• Premium and reserve risk- factor based approach: volume of the business * volatility

• News about premium & reserve risks

– Geographical diversification

– Adjustment for non-proportional reinsurance (premium risk)

– New factor in premium volume measure for existing contracts expected to be earned after the following year

• New lapse submodule

• New structure of cat risk

26 August 2010 Page 41

CEIOPS

Non life underwriting risk –cat risk – new structure

• Method 1 (default one)

� regional scenarios for nat cat & man made,

� scenarios for perils/event (not LoB), brutto calculation

� nat cat & man made capital requirements aggregated (independency)

• Method 2 – factor based approach if method 1 can not be applied and PIM is not appropriate

� outside EEA

� for miscellaneous LoB

� for non-proportional reinsurance

• Own reinsurances programme

• Aggregation of methods 1 & 2 (independency)

26 August 2010 Page 42

CEIOPS

Non life underwriting risk –cat risk – method 1 – nat cat

• Perils:

�windstorm

� flood

� earthquake

� hail

� subsidence

• Capital requirement is calculated for each peril and country separately, aggregation at first by countries then by perils

• For each zone (cresta, post-code) undertaking’s exposure are required (total insured value) for each LoB affected by the peril (LoBs given in TS, for flood: Fire & other damages, MAT & MPD)

26 August 2010 Page 43

CEIOPS

Non life underwriting risk –cat risk – method 1 – nat cat

• Flood:

where CATflood_ctry – capital requirement for flood and the country

Qctry – factor for the country

FZONE – factors for the zones

AGGr,c – aggregation matrix for the country between the zones

TIVZONE – exposure (total insured value) for each zone

• Multiple events: subsequent losses for windstorm, flood and hail – capital requirement calculated as maximum from A and B type events

�A – one large event and additionally one smaller event (for flood 1 i 0,1)

�B – two moderate events (for flood 0,65 i 0,45)

ZONEZONEZONE TIVFWTIV *=

∑=rxc

cZONErZONEcrCTRYctryFlood WTIVWTIVAGGQCAT ,,,_ **

26 August 2010 Page 44

CEIOPS

Non life underwriting risk –cat risk – method 1 – man made cat

• The same events for all undertakings – no differentiation between countries or zones

• Events:

� fire

�motor

�marine, aviation

� liability

� credit & suretyship

� terrorism

• Aggregation capital requirements from above events with the independence assumption

26 August 2010 Page 45

CEIOPS

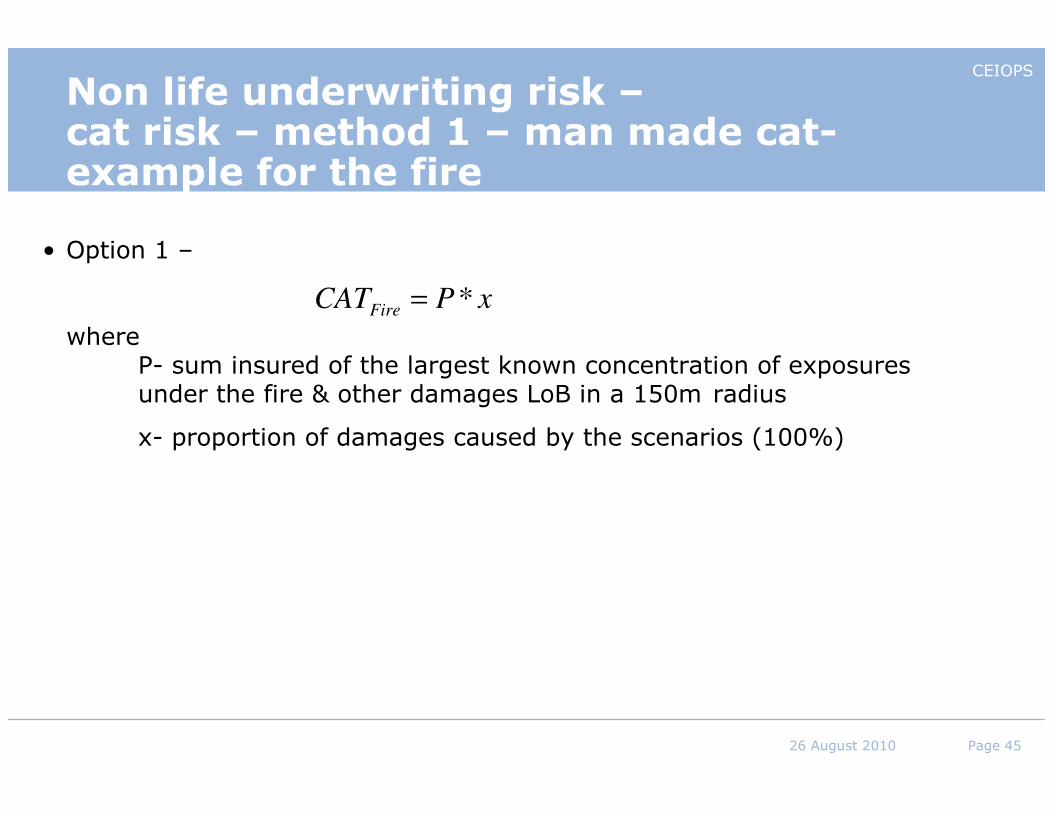

Non life underwriting risk –cat risk – method 1 – man made cat-example for the fire

• Option 1 –

where P- sum insured of the largest known concentration of exposures under the fire & other damages LoB in a 150m radius

x- proportion of damages caused by the scenarios (100%)

xPCATFire *=

26 August 2010 Page 46

CEIOPS

Non life underwriting risk –cat risk – method 1 – man made cat-example for the fire

• Option 2 (simplification)

where SI – sum insured by sub-line of business

(residential, commercial and industrial)

LSR – single largest risk across all sub-lines

Fx – market wide factors for each sub line

= ∑

−linessub

xxFire FSILSRMaxCAT *,

26 August 2010 Page 47

CEIOPS

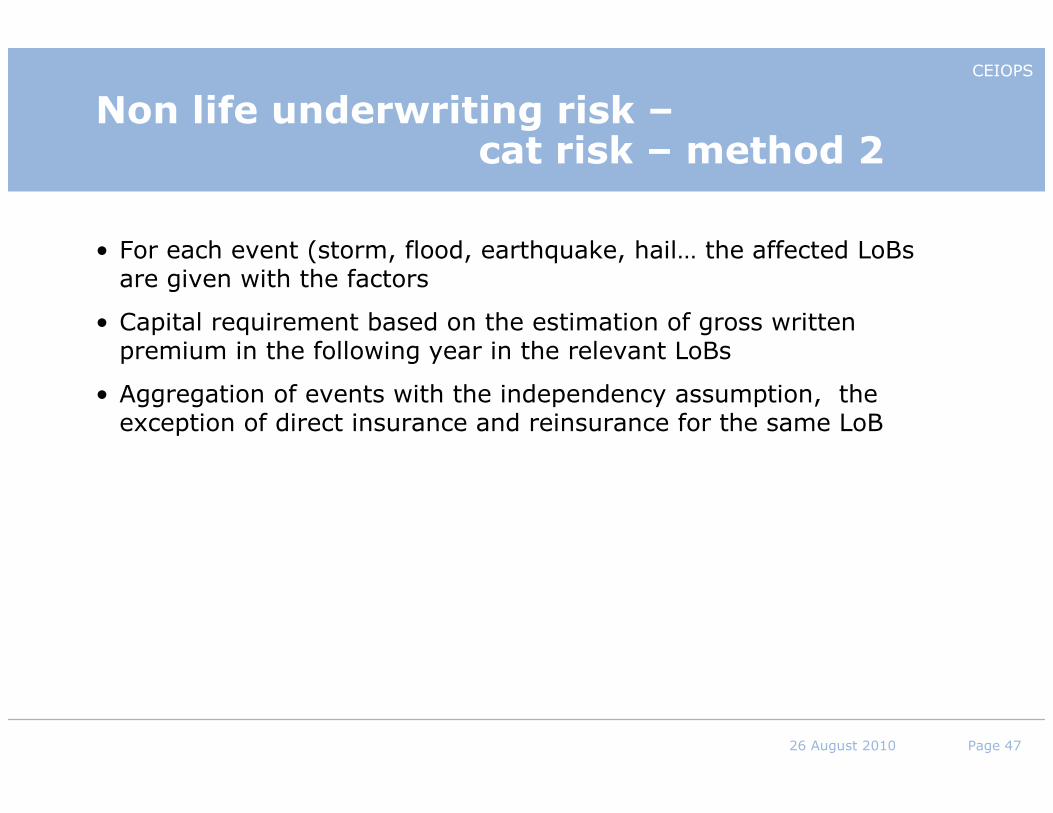

Non life underwriting risk –cat risk – method 2

• For each event (storm, flood, earthquake, hail… the affected LoBsare given with the factors

• Capital requirement based on the estimation of gross written premium in the following year in the relevant LoBs

• Aggregation of events with the independency assumption, the exception of direct insurance and reinsurance for the same LoB

26 August 2010 Page 48

CEIOPS

Undertaking specific parameters

• Hierarchy:simplifications

=> standard formula => standard formula with USPs=> standard formula with PIM=> full internal model

• The approach based on the credibility factor –

�mix with the market factors

� longer history => higher weight

� 100% for 10/15 years

26 August 2010 Page 49

CEIOPS

Undertaking specific parameters

• Parameters to replace: σprem,lob , σres,lob, - in non life risk module and NSLT health

• For σprem,lob and σres,lob , there are 3 methods method can be chosen but the choice must be justified in the future (anty - cherry picking)

• Assumption of the methods should be checked, quality of data in the future is subject to the supervisory approval

26 August 2010 Page 50

SCR SCR -- counterparty default riskcounterparty default risk

26 August 2010 Page 51

CEIOPS

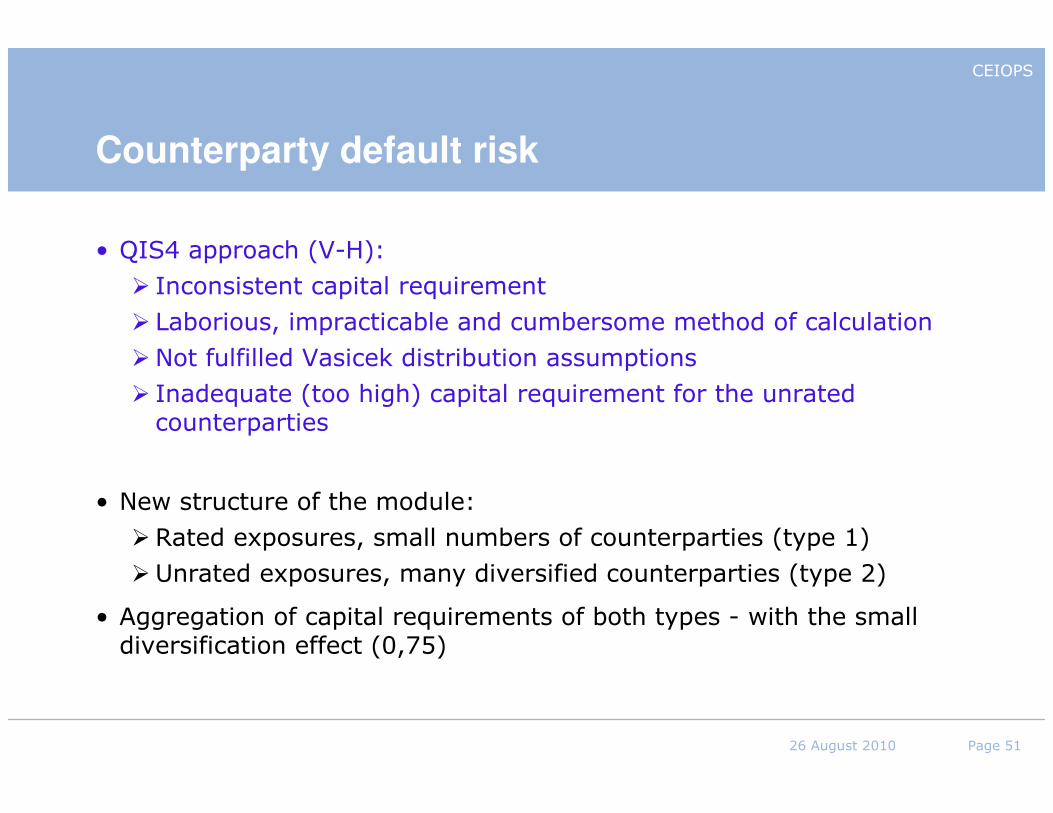

Counterparty default risk

• QIS4 approach (V-H):

� Inconsistent capital requirement

� Laborious, impracticable and cumbersome method of calculation

�Not fulfilled Vasicek distribution assumptions

� Inadequate (too high) capital requirement for the unrated counterparties

• New structure of the module:

�Rated exposures, small numbers of counterparties (type 1)

�Unrated exposures, many diversified counterparties (type 2)

• Aggregation of capital requirements of both types - with the small diversification effect (0,75)

26 August 2010 Page 52

CEIOPS

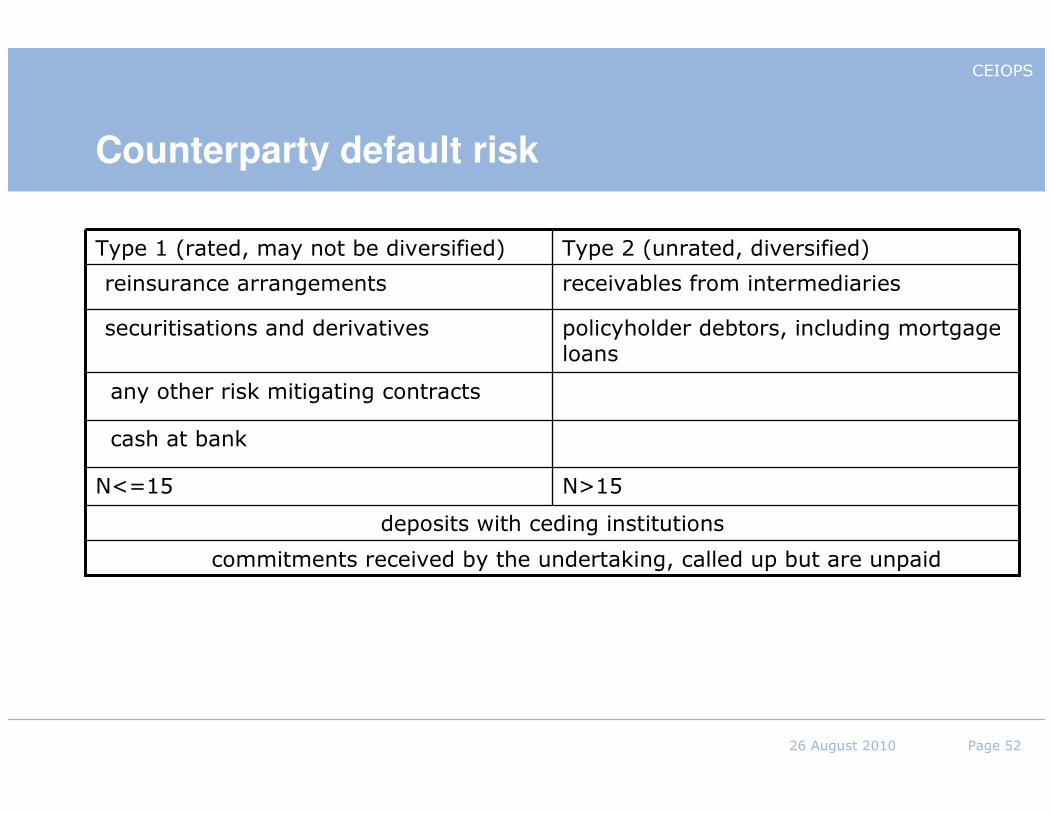

Counterparty default risk

commitments received by the undertaking, called up but are unpaid

deposits with ceding institutions

N>15N<=15

cash at bank

any other risk mitigating contracts

policyholder debtors, including mortgage loans

securitisations and derivatives

receivables from intermediariesreinsurance arrangements

Type 2 (unrated, diversified)Type 1 (rated, may not be diversified)

26 August 2010 Page 53

CEIOPS

Counterparty default risk –type 1 –SCRdef,1- theory

Probablility of default of the counterparty i:

where b – basic probability of default of the counterparty i

S – the amount of the shock, common for all counterparties with the probability distribution

α, τ -parameters

,)1()( ib

iiii SbbSPDPDτ

−+==

,10,)Pr( <<=≤ sssSα

26 August 2010 Page 54

CEIOPS

Counterparty default risk –type 1 –SCRdef,1- method of calculation

where

Input: LGDi

rating or solvency ratio

Given in the TS: PDj - depending on rating or solvency ratio,

coefficients ωjk

∑∑

⋅≤

⋅

⋅

= i

i

i

idef

LGDV

else

if

VLGD

V

SCR%5

, 5;min

3

1,

),,,(,1 1

ατωωω kjjkkj

N

j

N

k

jk PDPDLGDLGDV ==∑∑= =

26 August 2010 Page 55

CEIOPS

Counterparty default risk –type 1 –SCRdef,1- LGD method of calculation

• Cash at bank

• Deposits with ceding institutions

• Unpaid but called up capital

• Guaranties letters of credit, etc.

=> LGD = Value according to Valuation section of the TS

26 August 2010 Page 56

CEIOPS

Counterparty default risk –type 1 –SCRdef,1- LGD method of calculation

• Reinsurance, securitization, derivative

=>

RM = hypothetical SCR (without taking into account RM contracts) –real SCR for underwriting and market risk – real SCR for those risk

* Different percent values

( ) ( )( ),0;covRe%50max*

iiii CollateralRMerablesLGD −+⋅=

( ) ( )CollateralCollateral MktRiskMktValueCollateral −⋅=*

%100

26 August 2010 Page 57

CEIOPS

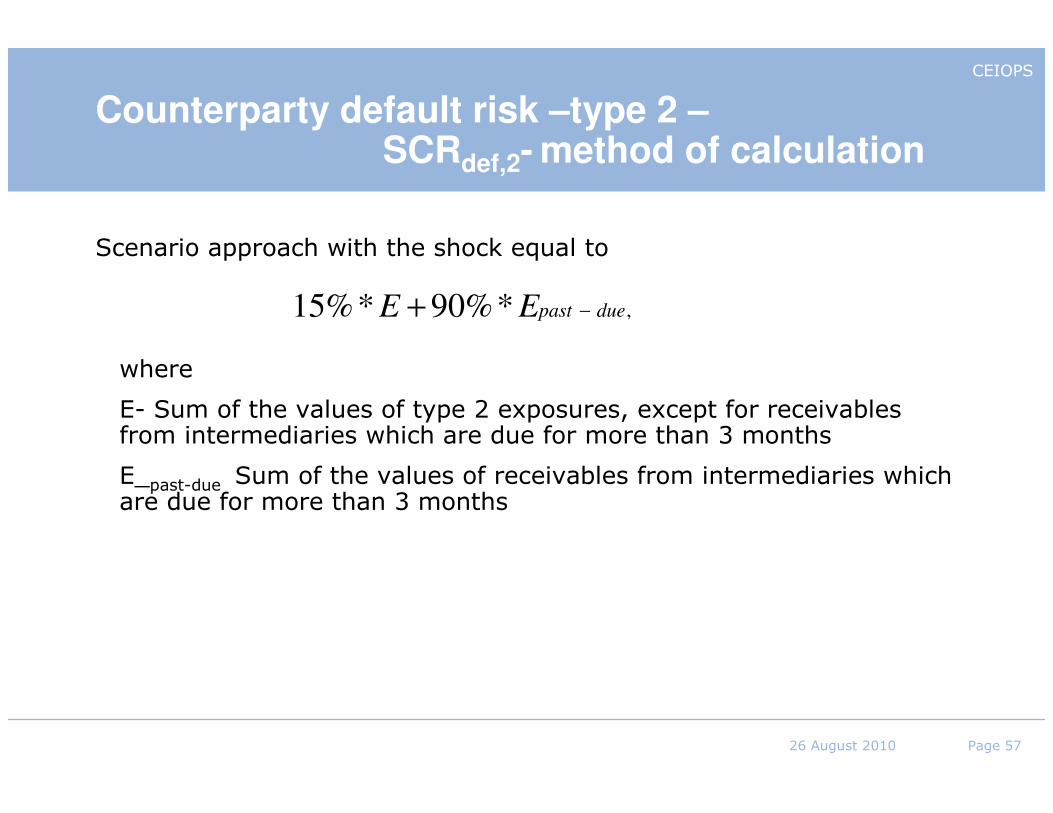

Counterparty default risk –type 2 –SCRdef,2- method of calculation

Scenario approach with the shock equal to

where

E- Sum of the values of type 2 exposures, except for receivables from intermediaries which are due for more than 3 months

E_past-due Sum of the values of receivables from intermediaries which are due for more than 3 months

,*%90*%15 duepastEE −+

26 August 2010 Page 58

CEIOPS

Counterparty default risk

• Simplifications of RM calculation (conditions!)

�Derivatives, which affect in RM one submodule of market risk – only market risk

� For reinsurance: calculate the difference in non-life risk for all reinsurance counterparties and allocate them as follows

SCRhypnl − SCR withoutnl≈ SCRhyp

nl − SCR withoutnl *Reci/Rectotal

where Reci are the reinsurance recoverables towards counterparty (i) and Rectotal the overall reinsurance recoverables

�Calculation by subsets not every single counterparty

�Collateral =85*% Market Value of collateral

• Qualitative questionnaire

26 August 2010 Page 59

QIS5 for Life InsurersQIS5 for Life Insurers

26 August 2010 Page 60

CEIOPS

Areas Covered

This Morning

– Technical Provisions• Best Estimate• Discounting and Liquidity Premium• Contract Boundaries

This Afternoon

– SCR and MCR• Life modules• Loss absorbing capacity of technical provisions• Op Risk• MCR

26 August 2010 Page 61

CEIOPS

Structure

•Theory (briefly)

•Spreadsheet

•Helper tabs

•Questionnaire

•Questions and discussion

26 August 2010 Page 62

CEIOPS

Best Estimate

• Probably the fundamental part of the Solvency II calculation

• Best Estimate: corresponds to the probability-weighted average of future cash-flows, taking into account the time value of money (Article 77(2))

• No margins

• Market consistent

26 August 2010 Page 63

CEIOPS

Discounting and Liquidity Premium

• Risk free rate

• Swaps – 10 bps

• Provided by CEIOPS

• Liquidity Premium for all products

• Three buckets

• Liquidity premium transitional

26 August 2010 Page 64

CEIOPS

Contract Boundaries

• Very important for EPIFP

• TP 2.15

• Only include cash flows within contract boundary:

– Where insurer has unilateral right to:•terminate contract

•reject premiums

– Where insurer has unlimited ability to:•amend premiums or benefits in future

– “Unlimited ability” - economic perspective

– Includes future policies exercised under options / guarantees

26 August 2010 Page 65

RiskRisk marginmargin

26 August 2010 Page 66

CEIOPS

Principles from the technical specifications

• Section V.2.5:

� TP.5.3: COC of providing eligible own funds at the level of the futursSCR over the lifetime of the (re)insurance obligations

� TP.5.4: futurs SCR with minimal market risk. Includes:� Underwriting risk� Unavoidable market risk� Credit risk (reinsurance and SPV)� Operational risk

� Loss absorbing capacity of TP, no loss absorbing capacity of deferred taxes

�Same future management actions

26 August 2010 Page 67

CEIOPS

General formula (TP.5.9)

26 August 2010 Page 68

CEIOPS

Calculation

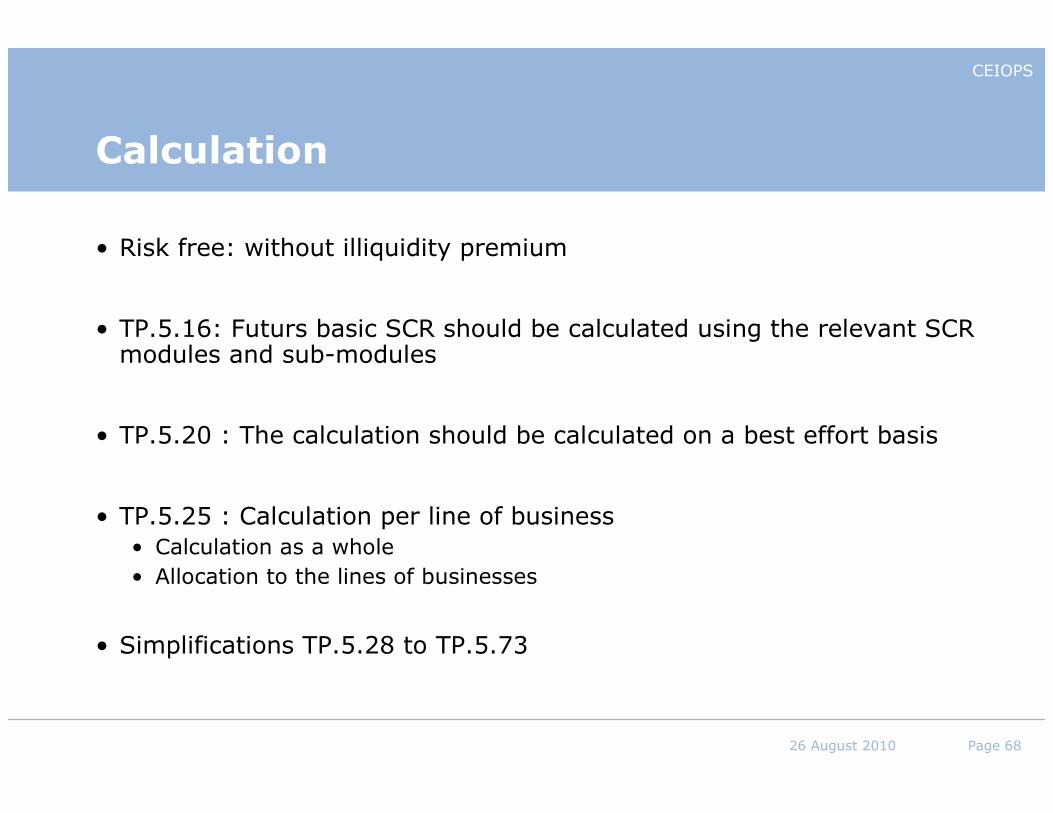

• Risk free: without illiquidity premium

• TP.5.16: Futurs basic SCR should be calculated using the relevant SCR modules and sub-modules

• TP.5.20 : The calculation should be calculated on a best effort basis

• TP.5.25 : Calculation per line of business

• Calculation as a whole

• Allocation to the lines of businesses

• Simplifications TP.5.28 to TP.5.73

26 August 2010 Page 69

CEIOPS

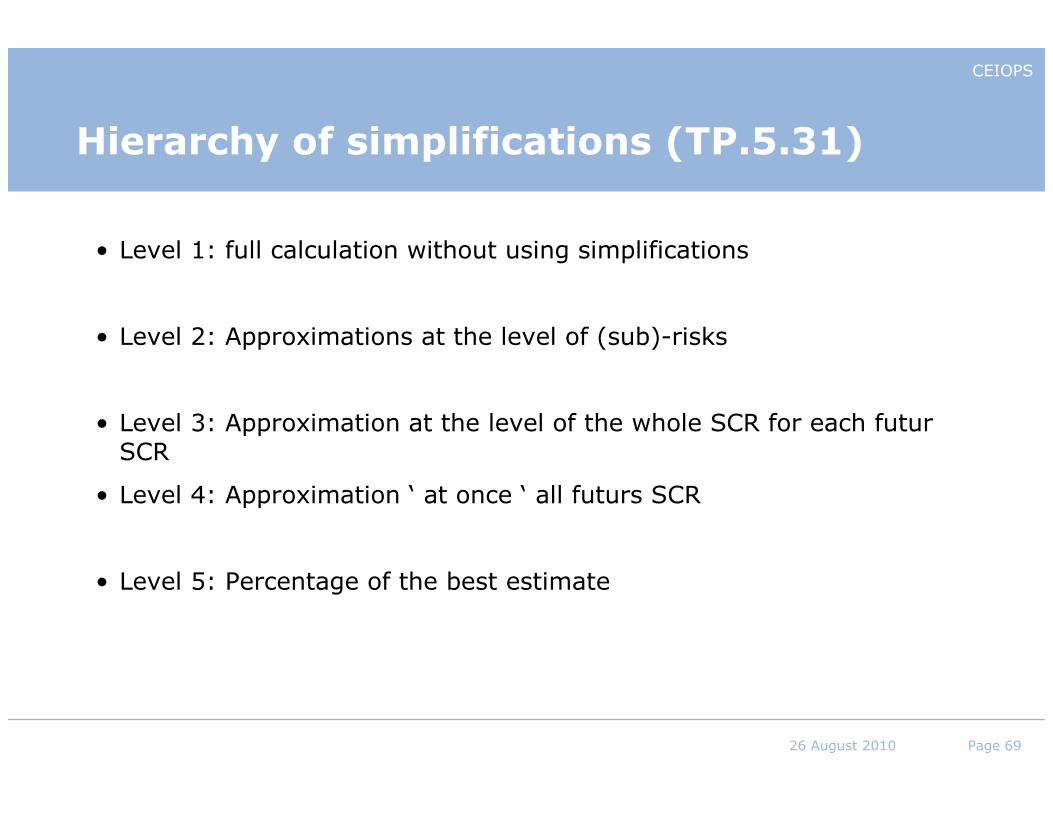

Hierarchy of simplifications (TP.5.31)

• Level 1: full calculation without using simplifications

• Level 2: Approximations at the level of (sub)-risks

• Level 3: Approximation at the level of the whole SCR for each futurSCR

• Level 4: Approximation ‘ at once ‘ all futurs SCR

• Level 5: Percentage of the best estimate

26 August 2010 Page 70

CEIOPS

Life modules

• 99.5% VaR over one year

• Seven modules:

– Mortality

– Longevity

– Morbidity

– Revision

– Lapse

– Catastrophe

– Expense

• Simplifications and USP available

26 August 2010 Page 71

CEIOPS

Loss absorbing capacity of technical provisions

• SCR can be reduced to take account of the loss absorbency of technical provisions

Assets

Before stress

Liabs

Own

Funds

Post-stress,

no actions taken

AssetsLiabs

Own

Funds

Post-stress, with impact of

management actions

and deferred taxes

Assets

Liabs

Own

Funds

26 August 2010 Page 72

CEIOPS

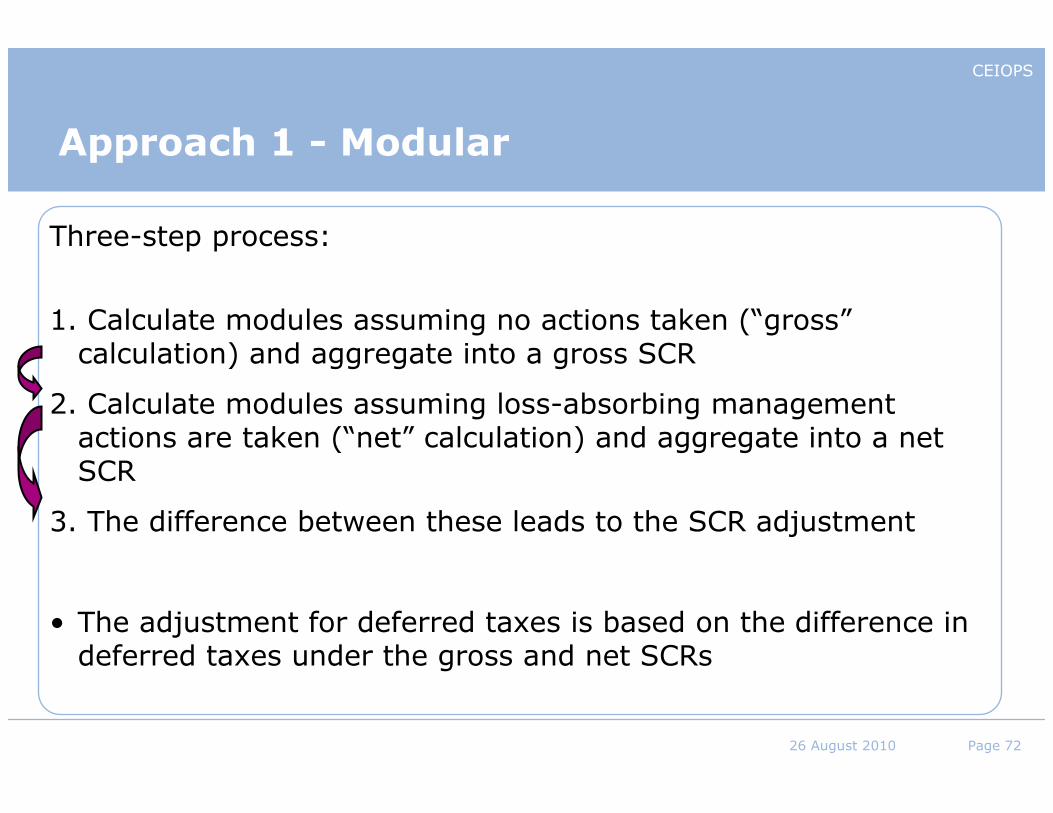

Approach 1 - Modular

Three-step process:

1. Calculate modules assuming no actions taken (“gross”calculation) and aggregate into a gross SCR

2. Calculate modules assuming loss-absorbing management actions are taken (“net” calculation) and aggregate into a net SCR

3. The difference between these leads to the SCR adjustment

• The adjustment for deferred taxes is based on the difference in deferred taxes under the gross and net SCRs

26 August 2010 Page 73

CEIOPS

Approach 2 – Equivalent Scenario

3-step process:

1. Calculate undiversified capital charges for each risk (either gross or net)

2. Find the diversified capital requirement

3. Allocate the diversification benefit back to each risk to find the single equivalent scenario

– This is done by using the relative weights of risks and correlations

– Adjusted SCR is then calculated by running the single equivalent scenario stresses

• Adjustment for deferred taxes is calculated by looking at the value of deferred taxes under the single equivalent scenario

26 August 2010 Page 74

CEIOPS

Loss absorbing capacity of technical provisions

Modular approach

• Simpler to understand

• More extensively tested in QIS4

But

• Requires two calculations for each relevant risk module

• May not fully capture the effects of possible double counting of loss absorbency

Single equivalent scenario

• Avoids double counting of loss absorbency

• Fewer calculations required

• More realistic treatment of management actions

• Easier to incorporate deferred taxes

But

• More complex to understand the methodology

26 August 2010 Page 75

Financial Financial HedgingHedging

26 August 2010 Page 76

CEIOPS

26 August 2010 Page 76

Agenda

• Scope

• Conditions for using of risk mitigation techniques

• Financial Risk Mitigation

– Basis Risk

– Rolling hedging

– Credit derivatives

26 August 2010 Page 77

CEIOPS

26 August 2010 Page 77

Scope

• Purchasing or issuing of financial instruments which transfer risk to the financial markets

• Examples:

• Put options to cover the risks of falls in assets

• Credit derivatives to cover the risk of failure (or downgrade) of a counterparty

• Currency swaps to cover currency risk

26 August 2010 Page 78

CEIOPS

26 August 2010 Page 78

Conditions for using in QIS 5

• Legal certainty, effectiveness and enforceability

• Liquidity and certainty of the value

• Direct, explicit, irrevocable and unconditional features

• No double counting of mitigation effects

• Credit quality of the counterparty : at least BBB

26 August 2010 Page 79

CEIOPS

26 August 2010 Page 79

Financial risk mitigation – Basis risk

• Matching between underlying assets or references of the financial mitigation instrument and undertaking exposures is required

• When matching is not perfect, financial risk mitigation technique should be accepted in QIS 5 if:

• Correlation between hedged assets and assets underlying the derivatives is nearby 1

• Correlation between hegded name and names referring to CDS is nearby 1

26 August 2010 Page 80

CEIOPS

26 August 2010 Page 80

Financial risk mitigation – Rolling hedging

• Pro rata temporis used for risk mitigation techniques which cover only a part of the next year

• Dynamic hedging : not a risk mitigation technique in QIS 5

• Rolling hedge programme can be accepted under conditions

=> Taking into account of all the risks that can arise from the rolling over of the hedge

26 August 2010 Page 81

CEIOPS

26 August 2010 Page 81

Financial risk mitigation – Credit derivatives

• Applied procedures for the using of credit derivatives required

• Following credit events must be covered:

• Failure to pay the amounts due

• Bankruptcy or insolvency of the obligor

• Restructuring of the underlying obligation

• Mismatch between the underlying obligation and the reference obligation allowed if:

• Reference obligation is junior to the underlying obligation

• And same obligor shared

26 August 2010 Page 82

CEIOPS

Operational Risk

• Straight forward factor based approach

• No diversification benefits

26 August 2010 Page 83

CEIOPS

MCR

• Approximately 85% VaR over 1 year

• Straight forward factor based approach

• Subject to a window

• And to an absolute minimum

26 August 2010 Page 84

Main points to check when finalisingsolo undertakings submission

26 August 2010 Page 85

CEIOPS

Elements• Core spreadsheets .xls

– Participants tab!!!!!! (currency, internal model, …)

– Check all tabs are complete and right

– Use the overview tab and checks (true/false) that are in the spreadsheets)• E.g. Balanced BS!

• Qualitative questionnaire– Solo or group! - .doc

– Excel file (solo or group, information on transitional for own funds, internal models if relevant) .xls

– Internal model if relevant .doc

• Additional request for refining calibration of non life and Health non SLT underwriting risks .xls

• Simplification and helper tabs .xls– if asked by national supervisors or considered useful for the understanding of the results

26 August 2010 Page 86

CEIOPS

Key points for solo undertakings

•Liquidity premium

•Transitional on discount rate

•Risk margin

•Equivalent scenario versus modular approach

•Internal model results

•Expected profits in future premiums

•Transitional on own funds

26 August 2010 Page 87

CEIOPS

Post submission

•Be ready to answer questions from your supervisors!

•It will help improve quality of results and avoid misunderstandings