qfa pensions - lia pensions...ann, aged 51, is self-employed and will have net relevant earnings of...

TRANSCRIPT

QFA Pensions Exam Buddy

Jo Ryan QFA, RPA

FIN1028B: QFA Pensions

End of Chapter Questions - Chapter 1

1 Which of the following is/are unearned income?

(i) Dividends.

(ii) Deposit interest.

(iii) Salary.

A (iii) only.

B (i) and (ii) only.

C (ii) and (iii) only. D (i), (ii) and (iii).

******

2 A property investment held outside of a pension arrangement is an example of which pillar of provision for retirement?

A First.

B Second.

C Third. D Fourth.

******

3 Continuing to work part time after retirement from an individual’s main occupation is an

example of which pillar of provision for retirement?

A First.

B Second.

C Third. D Fourth.

QFA Pensions – Chapter 1 Solutions Q. Answer Reference 1 B 1.1 Main types of personal financial needs 2 C 1.2.3 Third Pillar - personal savings & investments 3 D 1.2.4 Fourth pillar – continued earnings in retirement

FIN1028B: QFA Pensions

End of Chapter Questions - Chapter 2

1 Aoife is a proprietary director of her own company and is aged 56. Aoife pays PRSI at which class?

A A1

B B1

C D1 D S1

******

2 Ivan joined the civil service in 1992. He pays PRSI at which class?

A A1

B B1

C K1 D S1

******

3 Andrea’s husband has just died. She can qualify for the State Widow's (Contributory)

Pension only if she:

A can pass a means test.

B meets the necessary PRSI conditions based on her or her late husband’s PRSI record.

C is then under age 55. D has children from her marriage.

******

4 Which one of the following factors does NOT impact on Alistair's ability to claim the

State Widower's (Contributory) Pension following the recent death of his wife?

A His level of income from other sources.

B Whether he has remarried since his wife’s death.

C His PRSI contribution record. D His late wife's PRSI contribution record.

5

******

A State Invalidity Pension is potentially payable to qualifying individuals who have been incapable of work for at LEAST how many months?

3

6

12 24

A B

C D

FIN1028B: QFA Pensions

End of Chapter Questions - Chapter 2 Continued

6 The age at which an individual born in 1961 or later can potentially qualify for the State Pension (Non-Contributory) is:

A 65

B 66

C 67 D 68

******

7 Owen, who is single, is receiving the State (Non-Contributory) Pension. This pension will

stop automatically if Owen:

A marries.

B moves abroad to live in Spain permanently.

C starts to cohabit with someone else. D becomes liable to income tax.

QFA Pensions – Chapter 2 Solutions Q. Answer Reference 1 D 2.2.1 The PRSI System 2 B 2.2.1 The PRSI System

3 B 2.2.4 The State Widow's, Widower's or Surviving Civil Partner's (Contributory) Pension

4 A 2.2.4 The State Widow's, Widower's or Surviving Civil Partner's (Contributory) Pension

5 C 2.2.5 Invalidity Pension 6 D 2.3.1 State Pension (Non-Contributory) 7 B 2.3.1 State Pension (Non-Contributory)

FIN1028B: QFA Pensions

End of Chapter Questions - Chapter 3

1 An employer operates a pension scheme for its employees. Employees join the scheme for retirement benefits after two years of service. This employer must provide a facility for employees who have not joined the pension scheme, to contribute by deduction from pay, to at least one:

A non Standard PRSA.

B RAC.

C Standard PRSA. D life assurance savings plan.

******

2 Ann, aged 51, is self-employed and will have net relevant earnings of €100,000 in 2018. If she has already contributed €7,500 to a PRSA in 2018, what is the MAXIMUM additional RAC or PRSA contributions Ann can pay and claim tax relief on in 2018?

A €17,500

B €22,500

C €27,500 D €32,500

******

3 Colin is a self-employed dentist aged 38 and will have net relevant earnings of €215,000 in 2018. The MAXIMUM total Retirement Annuity Contract and PRSA contributions Colin can pay and claim tax relief on in 2018 is:

A €23,000

B €28,750

C €32,750 D €43,000

******

4 Rory is a professional golfer aged 32. What is the MAXIMUM percentage of his golfing earnings he can claim tax relief on in respect of contributions paid to a Retirement Annuity Contract or PRSA?

A 20% B 25% C 30% D 35%

FIN1028B: QFA Pensions

End of Chapter Questions - Chapter 3 Continued

5 Mona, aged 42, is an employee whose 2018 earnings are €75,000. If she personally contributes €10,000 to her PRSA in 2018, what is the MAXIMUM additional amount her employer can contribute to her PRSA in 2018, without causing an income tax charge for Mona in 2018?

A €5,750

B €8,750

C €10,000 D €18,750

******

6 A Retirement Annuity Contract contribution paid in which month CANNOT in any

circumstance be backdated for tax relief purposes to the previous year?

A August.

B September.

C October. D December.

******

7 A charge taken as a percentage of a contribution paid into a Retirement Annuity Contract is called which type of charge?

A Entry.

B Ongoing.

C Contingent. D Exit.

******

8 What are the MAXIMUM permitted charges which can be levied on a Standard PRSA?

A 1% of each contribution, and 1% of the fund value per annum.

B 1% of each contribution, and 5% of the fund value per annum.

C 5% of each contribution, and 1% of the fund value per annum. D 5% of each contribution, and 5% of the fund value per annum.

FIN1028B: QFA Pensions

End of Chapter Questions - Chapter 3 Continued

9 James is a self-employed doctor. What is the LATEST age by which he must draw on his Retirement Annuity Contract?

A 66

B 68

C 70 D 75

******

10 Amelia, aged 62, is maturing her RAC. She previously invested €30,000 of other

retirement funds in the purchase of an annuity, and is currently in receipt of annuity income of €2,500 per annum. What amount will Amelia be required to transfer to an AMRF or use to purchase an annuity from the maturity of her RAC?

A €33,500

B €50,000

C €63,500 D €119,800

******

11 Evelyn is maturing her Retirement Annuity Contract (RAC). She matured a PRSA last year and invested €63,500 from it in an AMRF; she is not currently in receipt of any pension or annuity income. What amount, if any, will Evelyn be required to transfer now to an AMRF or use to purchase an annuity from the maturity of her RAC?

A Nil.

B €30,000

C €43,500 D €63,500

******

12 Kate has matured her Retirement Annuity Contract and after taking her lump sum

and transferring funds to an AMRF, she has €110,000 left. She can use these funds to:

(i) buy an annuity.

(ii) transfer to an ARF.

(iii) take as a taxable lump sum.

A (i) only.

B (ii) only.

C (i) and (iii) only. D (i), (ii) and (iii).

FIN1028B: QFA Pensions

End of Chapter Questions - Chapter 3 Continued

13 A ring fenced amount in a vested PRSA AUTOMATICALLY becomes non-ring fenced:

A when the PRSA holder reaches age 70.

B when the PRSA holder starts to receive pension/annuity income payable for his or her lifetime of at least €12,700 per annum.

C five years after the PRSA vested. D when the ring fenced balance first exceeds €63,500.

******

14 The FIRST Disclosure Notice provided to a client taking out a Retirement Annuity

Contract is usually referred to as which type of notice?

A Specific.

B Modified.

C Precise. D Generic.

******

15 A PRSA holder will receive an Investment Report on his/her PRSA from the PRSA provider every:

A quarter.

B half-year.

C year. D 3 years.

******

16 Which one of the following statements regarding a Preliminary Disclosure Certificate

(PDC) is CORRECT?

A A PDC does not vary according to whether the PRSA is a standard PRSA or a non- standard PRSA.

B A PDC is a document which a PRSA provider may give to a client if it feels the client is a vulnerable customer.

C A PDC is provided to standard PRSA holders to inform them of the sales remuneration payable from the PRSA.

D A PDC shows a projection of retirement benefits the PRSA might provide to the PRSA holder at retirement in return for certain contribution levels.

17

A B C D

18

A PRSA provider must give a PRSA holder a Statement of Reasonable Projection:

on reaching his or her 50th birthday.

on encashment of the PRSA and transfer to another PRSA provider.

on termination of employment.

within seven days of increasing the charges on the PRSA.

******

A Pension Term Assurance policy: (i) can provide life and serious illness cover.

(ii) can run up to the life assured's 70th birthday.

(iii)

A (i) only.

(ii) only.B C (ii) and (iii) only.

(i), (ii) and (iii).

******

Aoife has a Pension Term Assurance policy. If she dies today, the proceeds of her Pension Term Assurance policy must be paid to her:

surviving husband or civil partner.

estate.

nominated beneficiaries.

dependants in equal shares.

******

Emer has a Retirement Annuity Contract (RAC) with associated Pension Term Assurance policy for cover of €100,000 arranged on an ‘inclusive of fund’ basis. If the RAC is currently valued at €60,000, what TOTAL amount would be paid out between the two policies if Emer died today?

€40,000

€60,000

€100,000 €160,000

D

19

A

B C D

20

A B C D

FIN1028B: QFA Pensions

End of Chapter Questions - Chapter 3 Continued

cannot be assigned.

QFA Pensions – Chapter 3 Solutions Q. Answer Reference

1 C 3.2.2 PRSA

2 B 3.3.1 Income tax relief – personal contributions to RACs and PRSAs

3 A 3.3.1 Income tax relief – personal contributions to RACs and PRSAs

4 C 3.3.1 Income tax relief – personal contributions to RACs and PRSAs

5 B 3.3.2 Income tax relief - employer contributions to an employee’s PRSA

6 D 3.3.5 Backdating contributions

7 A 3.4.1 Entry charges

8 C 3.4.5 Restrictions on PRSA charges

9 D 3.5.1 When can retirement benefits be taken?

10 A 3.6.2 €63,500 AMRF or annuity requirement

11 A 3.6.2 €63,500 AMRF or annuity requirement

12 D 3.6.3 Taxable lump sum/ARF/Annuity

13 B 3.6.4 Vested PRSA

14 D 3.7.1 Provision of information – retirement annuities

15 B 3.7.2 Provision of information - PRSAs

16 D 3.7.2 Provision of information - PRSAs

17 D 3.7.2 Provision of information - PRSAs

18 C 3.9.1 Pension Term Assurance l - restrictions

19 B 3.9.1 Pension Term Assurance - restrictions

20 C 3.9.3 Different types of Pension Term Assurance

FIN1028B: QFA Pensions

End of Chapter Questions - Chapter 3 Continued

FIN1028B: QFA Pensions

End of Chapter Questions - Chapter 4

1 An employer pension scheme for a large number of employees is established by the employer completing which one of the following documents?

A Letter of Exchange.

B Declaration of Trust.

C Appointment of Beneficiaries. D Form of Indemnity.

******

2 If a DB employer pension scheme is said to be 'integrated', this means the:

A scheme is approved by the Revenue Commissioners.

B scheme benefits are partly DB and partly DC.

C members' anticipated entitlement to the State Pension is offset against the retirement benefits to be provided by the scheme.

D scheme is frozen and provides no new retirement benefits to members.

******

3 Remuneration for the purposes of an employer pension scheme CANNOT include an employee’s:

A overtime.

B bonuses.

C benefits in kind. D expenses refunded tax free by the employer.

******

4 Sharon is a member of her employer’s pension scheme. She is aged 46 in 2018.

What is the MAXIMUM contribution to the scheme she can claim tax relief on in 2018 if her remuneration from that employment in 2018 is €100,000?

A €25,000

B €28,750

C €29,250 D €30,000

FIN1028B: QFA Pensions

End of Chapter Questions - Chapter 4 Continued

5 Leah is a member of her employer's pension scheme. If she pays €25,000 to the scheme as a personal contribution in December 2018 but can only claim tax relief on €20,000 of this contribution in 2018, what happens to the balance of €5,000?

A She can carry it forward and claim tax relief on it in 2019 against her income from this employment.

B She can backdate it for tax relief purposes to 2017.

C It is refunded to her by the scheme administrator at the end of the year. D She cannot get tax relief on it.

******

6 ABC Ltd is currently paying an ordinary annual contribution of €170,000 to their

employer pension scheme. ABC now proposes to make a special additional once off contribution of €100,000 to the scheme. How much of this special contribution, if any, will qualify for Corporation Tax relief in the company's accounting period in which the special contribution is paid?

A Nil.

B €6,350

C €93,650 D €100,000

******

7 The EARLIEST NRA which an employer pension scheme can use is:

A 50

B 55

C 60 D 65

******

8 Christina is a 20% director of her company and is retiring. She is a member of her

company's pension scheme. Which one of the following ways of calculating her final remuneration must be used for the purposes of calculating the maximum approvable retirement benefits which the scheme can be provide for her on retirement?

A Average of total emoluments over three or more consecutive years, ending no earlier than 10 years before retirement.

B Basic remuneration over the last 12 months prior to retirement, plus the average of fluctuating emoluments over the last five years.

C The annual rate of remuneration payable at the date of her retirement. D Average of total emoluments over the last five consecutive years prior to retirement.

FIN1028B: QFA Pensions

End of Chapter Questions - Chapter 4 Continued

9 In relation to a DC employer pension scheme, the term ‘dynamisation’ refers to:

A the indexing in line with inflation of past remuneration, in order to calculate final remuneration.

B a guaranteed minimum investment return to NRA.

C opting to transfer part of a member's fund at retirement to an ARF. D the provision of actively managed funds as a default investment strategy.

******

10 An individual can contribute AVCs to a:

A PRSA.

B Buy Out Bond.

C Retirement Annuity Contract. D Section 785 policy.

******

11 Lucy is retiring from her employer’s DB pension scheme, on a pension of €24,000 per

annum. She has a separate AVC fund of €150,000. If she uses €100,000 of her AVC fund to provide the maximum tax free lump sum, what happens to the €50,000 balance?

A She must use the €50,000 to buy an annuity.

B She must take the €50,000 as a taxable lump sum, subject to PAYE.

C She can take €12,500 as an additional lump sum and transfer €37,500 to an AMRF. D She can transfer the €50,000 to an ARF or take as a taxable lump sum.

******

12 Sorcha has reached her NRA in her employer's DC pension scheme. Her accumulated

fund is €80,000. Her best final remuneration is €60,000 per annum, she has no retained benefits, and she has 28 completed years' service. Assuming she opts for the traditional benefit option, what is the MAXIMUM lump sum she can take from the scheme at NRA?

A €20,000

B €60,000

C €62,000 D €80,000

FIN1028B: QFA Pensions

End of Chapter Questions - Chapter 4 Continued

13 The Annual Benefit Statement provided to members of employer pension schemes cannot contain information that is out of date by more than which period of months?

A 3

B 6

C 9 D 12

******

14 What MINIMUM number of years' service must an employee member of an employer

pension scheme have to qualify for a preserved retirement benefit on leaving service?

A 2

B 3

C 4 D 5

******

15 John has been a member of his employer's DC employer pension scheme for a number

of years. He has now left service. He can take a transfer value from the scheme to a PRSA if he was a scheme member for which period?

A 12 years.

B 18 years.

C 20 years. D 21 years.

******

16 What is the EARLIEST age at which a buy-out bond holder can take retirement benefits

from their bond?

A 50

B 52

C 55 D The NRA in the scheme from which the transfer value was paid into the bond.

FIN1028B: QFA Pensions

End of Chapter Questions - Chapter 4 Continued

17 Brad is taking a voluntary redundancy package from his employer. His average annual remuneration over the three years prior to the date of termination of employment is €90,000, and he has completed 17 years and 9 months service with his employer. He has no employer pension scheme benefits. What is Brad’s Standard Capital Superannuation Benefit in respect of an ex gratia termination payment his employer is going to pay to him?

A €23,165

B €33,165

C €102,000 D €153,000

******

18 Joe is taking a voluntary severance package from his employer. He has not previously

taken an ex gratia termination payment and was not a member of his employer’s pension scheme. What MINIMUM amount of his ex gratia termination payment will be tax free?

A €10,000

B €10,160 plus €765 for each complete year of service.

C €15,000 D €20,000

QFA Pensions – Chapter 4 Solutions Q. Answer Reference

1 B 4.1 Declaration of Trust

2 C 4.1.4 Integrated or non integrated

3 D 4.3 Who can be included?

4 A 4.5.1 Tax relief on employee contributions

5 A 4.5.1 Tax relief on employee contributions

6 D 4.5.2 Employer Contributions

7 C 4.7 When can retirement benefits be taken?

8 A 4.9.1 Best final remuneration calculation

9 A 4.9.1 Best final remuneration calculation

10 A 4.10.5 Different ways to pay AVCs

11 D 4.10.7 Taking AVC benefits at retirement

12 D 4.10.7 Taking AVC benefits at retirement

13 B 4.11.1 Annual Benefit Statement

14 A 4.12 Termination of employment

15 A 4.12.4 Termination of employment – transfer options

16 A 4.12.5 Buy Out Bonds

17 C 4.12.6 Ex gratia termination payments

18 B 4.12.6 Ex gratia termination payments

1 A transfer value CANNOT be paid from a Buy Out Bond to a(n):

PRSA.

Irish employer pension scheme.

a new buy-out bond to be taken out by the individual.

another buy-out bond held by the same individual.

A B C D

QFA Pensions – Chapter 5 Solutions Q. Answer Reference 1 A 5.3 Transfers not allowed

FIN1028B: QFA Pensions

End of Chapter Questions - Chapter 5

FIN1028B: QFA Pensions

End of Chapter Questions - Chapter 6

1 A corporate bond secured over some of the assets of the company is called a:

A gilt.

B debenture.

C treasury. D coupon.

******

2 The regular income payable by a bond, expressed as a percentage of the nominal value

of the bond, is called the:

A link.

B discount.

C coupon. D debenture.

******

3 Which one of the following CANNOT invest in an exempt unit trust?

A A private investor.

B An employer pension scheme

C A PRSA. D A Retirement Annuity Contract.

******

4 If a collective investment fund aims to outperform a particular Stock Market index, it is

said to be adopting which investment management style?

A Active.

B Lifestyle.

C Passive. D Average.

******

5 A collective investment fund which invests only in technology company shares is called

which type of fund?

A Specialist.

B Smoothed.

C Multi-Asset. D Mixed.

FIN1028B: QFA Pensions

End of Chapter Questions - Chapter 6 Continued

6 The trustees of which one of the following schemes can borrow for long-term investment?

A A Small Self-Administered Pension Scheme (SSAPS) established for one member.

B A SSAPS established for two members.

C A DC employer pension scheme for 2 to 99 members. D A DC employer pension scheme for 100 or more members.

******

7 Which one of the following is a 'regulated market' investment by an employer pension

scheme, for the purposes of the Investment Regulations?

A An office building.

B A share in a private unlisted company.

C A share listed on a recognised Stock Exchange. D Units in an exempt unit trust investing in property.

******

8 A Pensioneer Trustee of a Small Self-Administered Pension Scheme (SSAPS) is a(n):

A independent professional trustee.

B trustee who is also a member of the scheme.

C trustee appointed by the Revenue Commissioners. D 20% director member of the scheme.

******

9 A Pensioneer Trustee of a Small Self-Administered Pension Scheme (SSAPS) must

be:

A a company.

B a co-signatory on all financial transactions of the scheme.

C authorised by the Central Bank. D the only trustee of the scheme.

QFA Pensions – Chapter 6 Solutions Q. Answer Reference 1 B 6.2.1 Traditional asset classes 2 C 6.2.1 Traditional asset classes 3 A 6.3.1 Different types of collective funds 4 A 6.3.5 Fund choice 5 A 6.3.5 Fund choice 6 A 6.8.1 Employer pension schemes – borrowing to invest 7 C 6.8.2 Investment Regulations 8 A 6.8.3 SSAPS 9 B 6.8.3 SSAPS

FIN1028B: QFA Pensions

End of Chapter Questions - Chapter 7

1 Which one of the following issues a Pension Adjustment Order?

A The Courts.

B The Pensions Ombudsman.

C The Pensions Authority. D The Revenue Commissioners.

******

2 Jamie has a PRSA with ABC Life Co. His ex-wife, Bridget, has obtained a Pension Adjustment Order (PAO) over his PRSA. The PAO is served on:

A Jamie.

B Bridget.

C ABC Life Co. D Jamie and ABC Life Co, jointly.

******

3 Luke and Jennifer have divorced. Jennifer obtained a Pension Adjustment Order (PAO) over Luke's PRSA. Jennifer has not yet taken a transfer value. If Jennifer dies before Luke takes his PRSA benefits, what happens to Jennifer's PAO entitlement?

A The Courts can order a payment to be made from the PRSA to Jennifer’s dependants.

B The PAO lapses without benefit.

C A transfer value is paid from the PRSA to Jennifer’s estate, within 3 months of her death.

D 25% of the PRSA is paid to Jennifer’s next of kin.

******

4 A Pension Adjustment Order over a contingent benefit must be sought within what MAXIMUM period after a decree of divorce?

A 9 months.

B 1 year.

C 3 years. D 5 years.

QFA Pensions – Chapter 7 Solutions Q. Answer Reference 1 A 7.1 What is a PAO? 2 C 7.1 What is a PAO? 3 C 7.7 Death of PAO beneficiary before getting benefits 4 B 7.8 Death in service benefits

FIN1028B: QFA Pensions

End of Chapter Questions - Chapter 8

1 Which one of the following is NOT a benefit in kind for income tax purposes for the employee concerned?

A An employer contribution to the employer’s pension scheme for the employee.

B An employer contribution to the employee’s PRSA.

C The provision of a company car. D Payment by the employer of the employee’s medical insurance premium.

******

2 Deposit interest subject to DIRT is assessed to income tax under:

A Schedule D Case I.

B Schedule D Case II.

C Schedule D Case III. D Schedule D Case IV.

******

3 Dividends from an Irish resident company are assessed for income tax under:

A Schedule D Case III.

B Schedule D Case IV.

C Schedule E. D Schedule F.

******

4 For 2018 part of Ralph's earnings were assessed to USC at a rate of 11%. This is

because he:

A earns PAYE income of €60,000 per annum.

B receives benefits in kind from his employment in excess of €20,000 per annum.

C earns investment income in excess of €5,000 per annum. D is self-employed and earns non-PAYE income of €120,000 per annum.

******

5 John is single. What is the EARLIEST age at which he can qualify for the Income

Exemption Limit for income tax purposes?

A 55

B 60

C 65 D 70

FIN1028B: QFA Pensions

End of Chapter Questions - Chapter 8 Continued

What is the Standard Fund Threshold limit in 2018?

€2 million.

€2.2 million.

€2.3 million.

€2.5 million.

******

Jack took retirement benefits from a PRSA in 2009 valued at €2.4 million and at 7th December 2010 had other undrawn Retirement Annuity Contracts and Buy Out Bonds valued at €2.7 million. What Personal Fund Threshold was Jack entitled to apply for at 7th December 2010?

€2.3 million.

€2.4 million.

€2.7 million.

€5.1 million.

******

Rory has a Personal Fund Threshold certificate for €5.5 million. In 2012 he took retirement benefits valued at €3.5 million from a Small Self-Administered Pension Scheme (SSAPS). In 2018 he matured a PRSA at €3 million. He has NOT taken any benefits from any other retirement arrangement. What chargeable excess, if any, will arise for Rory in 2018 when taking benefits from the PRSA?

Nil.

€700,000

€1,000,000

€1,300,000

******

9 Jackie is retiring in 2018 at age 62, on a DB pension of €100,000 per annum (all accrued before 1st January 2014) plus a separate retirement lump sum of €300,000. What total value will be placed on these retirement benefits for the purposes of the Threshold limits?

A €2 million.

B €2.3 million.

C €2.5 million.

D €2.8 million.

6

A B C D

7

A B C D

8

A B C D

FIN1028B: QFA Pensions

End of Chapter Questions - Chapter 8 Continued

10 Daniel took retirement benefits in 2018 from a PRSA valued in total at €2,500,000. He took a lump sum of €500,000, of which €300,000 was taxed at standard rate, and the balance was transferred to an AMRF and ARF. Assuming he took no other retirement benefits previously and is only entitled to the Standard Fund Threshold in 2018, what chargeable excess tax was deducted from his PRSA on maturity in 2018?

A €82,000

B €140,000

C €200,000 D €205,000

******

11 Frank retired from the civil service in 2018. He had a chargeable excess tax liability

on his public service superannuation benefits of €100,000. What is the MINIMUM reduction in his pension Frank can agree to, to discharge his chargeable excess tax liability?

A €5,000 per annum.

B €10,000 per annum.

C €15,000 per annum. D €20,000 per annum.

QFA Pensions – Chapter 8 Solutions Q. Answer Reference 1 A 8.1 Income Tax 2 D 8.1 Income tax 3 D 8.1 Income tax 4 D 8.2 Universal Social Charge (USC) 5 C 8.4 Income Exemption Limit 6 A 8.5.1 The Threshold amount 7 D 8.5.1 The Threshold amount 8 C 8.5.2 Calculation of ‘chargeable excess’ 9 B 8.5.3 Value of Defined Benefit pensions 10 B 8.5.4 Calculation of chargeable excess tax liability 11 A 8.5.5 Recovery of chargeable excess tax

FIN1028B: QFA Pensions

End of Chapter Questions - Chapter 9

1 Longevity insurance is insurance against:

A dying too soon.

B a reduced expectation of life.

C living too long. D developing a serious illness.

******

2 If an annuity is said to have a 'reversion' this means:

A the annuity rate is higher than normal because the investor is in bad health.

B part of the annuity will continue to be paid to a nominated survivor, following the death of the investor.

C the annuity rate is lower than normal because the investor is in excellent health. D the annuity will increase annually in line with the rise in the rate of inflation.

******

3 Alan is retiring and wishes to buy an annuity with part of his fund maturing under a DC

employer pension scheme. The annuity rate offered to Alan by a life company will vary by which of the following factors?

(i) His gender.

(ii) His civil status.

(iii) The level of Government bond yields.

A (i) only.

B (iii) only.

C (ii) and (iii) only. D (i), (ii) and (iii).

******

4 The benefit to a consumer of an open market option in a Retirement Annuity Contract

(RAC) is that he or she:

A will not be taxed on annuity payments in retirement, received from the RAC.

B will be able to take a lump sum of 25% of the RAC value at retirement.

C can secure the highest annuity rate in the marketplace at retirement, if he or she then wants to buy an annuity.

D will be able to exercise the ARF option at retirement.

5 If a life company quotes an annuity rate of 5% for Mary and the annuity will have a contract charge of €5 per annum, what annual annuity will Mary get for a lump sum of €200,000?

A €9,990 per annum.

B €9,995 per annum.

C €10,000 per annum. D €10,005 per annum.

QFA Pensions – Chapter 9 Solutions Q. Answer Reference 1 C 9.1 What is an annuity? 2 B 9.1 What is an annuity? 3 B 9.2 Annuity rates 4 C 9.4 Open market annuity option 5 B 9.3.3 Contract charge

FIN1028B: QFA Pensions

End of Chapter Questions - Chapter 9 Continued

FIN1028B: QFA Pensions

End of Chapter Questions - Chapter 10

1 Jamie is aged 62. What limit, if any, applies to the withdrawal as a percentage of his ARF value, can Jamie make from his ARF?

A No limit.

B 4%

C 5% D 6%

******

2 Martin is aged 68 and has an ARF valued at €500,000 at 30th November 2018. He has

no other ARFs or vested PRSAs. He took a withdrawal of €5,000, before taxes, from his ARF in March 2018. What additional withdrawal, before taxes, must Martin take from his ARF before the end of 2018, to avoid an imputed distribution applying to his ARF for 2018?

A €5,000

B €10,000

C €15,000 D €20,000

******

3 Anne is aged 72 and has an ARF valued at €1,500,000 at 30th November 2018.

Assuming she takes no withdrawal from his ARF in 2018, what notional distribution for income tax purposes will Anne be deemed to take from her ARF for 2018?

A €50,000

B €60,000

C €75,000 D €90,000

******

4 Karl, aged 65, has an ARF and an AMRF with ABC Life Co. He has no other ARFs or

vested PRSAs. In March 2018 he withdrew €1,400 before taxes from his AMRF. If his ARF is valued at €100,000 at 30th November 2018, what level of withdrawal, before taxes, must Karl take from his ARF before the end of 2018 to avoid an imputed distribution applying to his ARF for 2018?

A €2,600

B €3,600

C €4,000 D €6,000

FIN1028B: QFA Pensions

End of Chapter Questions - Chapter 10 Continued

5 Cian, aged 68, has an AMRF valued at €63,500 as of 30th November 2018. He has not taken a withdrawal from the AMRF in 2018, and has no ARFs or vested PRSAs. What imputed distribution amount, if any, will apply to Cian's AMRF for 2018 if he takes no withdrawal from it in 2018?

A Nil.

B €2,540

C €3,175 D €3,810

******

6 An AMRF automatically converts to an ARF at which age?

A 65

B 70

C 75 D 80

******

7 An AMRF automatically converts to an ARF:

A on death.

B when the AMRF value first exceeds €40,000.

C when the AMRF value first falls below €20,000.

D when the AMRF holder starts to receive guaranteed pension income of €10,000 per annum.

******

8 Andrew died in 2012 and the balance of his ARF was transferred to an ARF owned

by his surviving spouse, Sarah. If Sarah dies now in 2018 and leaves the balance of her ARF to her son, Tom, aged 32, how will this benefit be taxed?

A Subject to Capital Gains Tax at 33% at source.

B Exempt from inheritance tax but subject to a 30% income tax charge.

C Exempt from income tax but a taxable inheritance for Inheritance Tax purposes for Tom.

D Under PAYE at Sarah's marginal rate of income tax in the year of death.

9 Jack died in 2018 and in his Will left the balance of his ARF to his friend, Lucy, to whom he was not married or related. How was this payment from Jack’s ARF taxed, if at all, by the QFM?

It was subject to capital gains tax at 33%, deducted by the QFM.

No tax was deducted. It was paid tax free to Lucy.

It was subject to income tax at 30%, deducted by the QFM. The QFM operated PAYE on the payment.

A B C D

QFA Pensions – Chapter 10 Solutions Q. Answer Reference 1 A 10.3 Lifetime withdrawals from ARF 2 C 10.4 Imputed distributions 3 C 10.4 Imputed distributions 4 A 10.5 AMRFs 5 A 10.5 AMRFs 6 C 10.5 AMRF 7 A 10.5 AMRF 8 B 10.8 Death 9 D 10.8 Death

FIN1028B: QFA Pensions

End of Chapter Questions - Chapter 10 Continued

FIN1028B: QFA Pensions

End of Chapter Questions - Chapter 11

1 A PRSA product is jointly approved by the:

A Central Bank and the Pensions Authority.

B Central Bank and the Revenue Commissioners.

C Pensions Authority and the Minister for Finance. D Pensions Authority and Revenue Commissioners.

******

2 The Financial Services & Pensions Ombudsman can investigate and adjudicate on

certain complaints about pension providers in relation to:

(i) Retirement Annuity Contracts.

(ii) employer pension schemes.

(iii) PRSAs.

A (ii) only.

B (iii) only.

C (ii) and (iii) only. D (i), (ii) and (iii).

QFA Pensions – Chapter 11 Solutions Q. Answer Reference 1 D 11.2 Revenue Commissioners 2 C 11.5.1 Complaints about pension providers

FIN1028B: QFA Pensions

End of Chapter Questions - Chapter 12

1 If the Consumer Price Index was 135.3 12 months ago, and today it is 140, what has been the rate of inflation over the last 12 months?

3.2%

3.5%

3.8% 4.7%

A B C D

******

2 If inflation runs at 1.5% per annum over the next four years, which sum would an investment of €25,000 have to grow to, to keep pace with inflation over that period?

A €26,525

B €27,050

C €28,150 D €28,982

******

3 Sinéad invests €1,000 now and another €1,000 in a year’s time. If she earns an investment return of 5% per annum compound on these investments, what total amount will her investments have grown to seven years from now?

A €2,153

B €2,747

C €2,814 D €2,894

QFA Pensions – Chapter 12 Solutions Q. Answer Reference 1 B 12.1.1 CPI – All Items 2 A 12.2.2 Accumulation 3 B 12.2.2 Accumulation

FIN1028B: QFA Pensions

End of Chapter Questions - Chapter 13

Sadie, aged 48, is in non-pensionable employment. A Standard PRSA is likely to be more suitable for her than an Retirement Annuity Contract because with a Standard PRSA she can:

get more tax relief.

take early retirement benefits from age 50 onwards.

take more of her retirement fund as a tax-free lump sum.

add life cover to the contract.

******

Linda, aged 48, has a preserved benefit in her former employer’s DC pension scheme. She has now joined a new employer. If Linda definitely wants to be able to draw on this preserved benefit at 50, even if she continues working with her new employer, she should:

take a transfer value to a PRSA now.

take a transfer value to her new employer’s pension scheme.

keep the preserved benefit in her former employer’s pension scheme.

take a transfer value to a PRSA just before her 50th birthday.

******

3 Buying a fixed annuity exposes a retiree to which of the following risks?

(i) Bomb Out.

(ii) Investment.

(iii) Inflation.

A (i) only.

B (i) and (iii) only. C (iii) only. D (i), (ii) and (iii).

QFA Pensions – Chapter 13 Solutions

Q. Answer Reference 1 B 13.1 RACs v PRSAs 2 C 13.2 Retain a scheme preserved benefit or transfer out 3 C 13.6 ARF v Annuity

1

A B C D

2

A B C

D

FIN1028B: QFA Pensions

End of Chapter Questions - Chapter 14

1 The FIRST step in the financial advisory process is:

A prioritising of needs.

B knowing the consumer.

C determining suitability. D devising a financial planning strategy for the consumer.

******

2 When providing advice to consumers on PRSAs, the requirement to gather and record

relevant information about the consumer, referred to as Knowing the Consumer, arises from:

A the Pensions Act, 1990.

B the Consumer Protection Code.

C Section 785 of the Taxes Consolidation Act, 1997. D the Minimum Competency Code.

******

3 Which one of the following consumers would NOT be classified as a vulnerable

consumer under the Consumer Protection Code?

A Jean, who has a poor credit history.

B Paulo, who is an immigrant with poor English.

C Dermot, who has just inherited a large sum from his father. D Mark, who recently had a brain haemorrhage which has left him unable to write.

******

4 Brian's earnings today are €60,000 per annum. He plans to retire in 10 years' time on a

pension of 2/3rds of his earnings at that time. What will be his annual pension in 10 years’ time assuming his earnings will grow at 2.5% per annum in the meantime?

A €46,440

B €51,200

C €57,920 D €65,160

******

5 The 'Reason Why' statement provided to a consumer is also known as the Statement of:

A Objectivity.

B Suitability.

C Financial Needs. D Financial Objectives.

QFA Pensions – Chapter 14 Solutions Q. Answer Reference 1 B 14.4 The financial planning advisory process 2 B 14.5 Knowing the consumer 3 C 14.5.4 Identifying vulnerable customers 4 B 14.6 Quantifying the retirement funding need 5 B 14.9.3 ‘Reason Why' statement

FIN1028B: QFA Pensions

End of Chapter Questions - Chapter 14 Continued

Seat Number:

Sample Paper 1, 2018-19

FIN1028B: QFA Pensions

Time Allowed: 2 hours

Instructions for candidates

THE EXAMINATION PAPER MUST BE HANDED UP AT THE END OF THE EXAMINATION WITH THE MCQ ANSWER SHEET

1. To be awarded a pass grade in this examination, you must achieve a mark of 40% or above. 2. 120 minutes are allowed for this paper which consists of 100 Multiple Choice Questions (MCQ). 3. Write your membership number in the box provided on the MCQ answer sheet and complete the number grid

indicated according to the instructions listed. 4. There is only one correct answer to each question. 5. Read the instructions on the MCQ answer sheet carefully.

• Use the MCQ answer sheet provided to record your answers. Answers recorded on this examination paper will not be marked.

• Use the pencil provided to complete the MCQ answer sheet. • Insert your name, membership number and examination ID at the top of the MCQ answer sheet and

shade in the grids as indicated. • Each question carries 3 marks for a correct answer, -1 (minus one) for an incorrect answer and 0 for no

answer. 6. Handle the MCQ answer sheet with care and do not write notes or any marks on it, except for recording your

answers to the questions. 7. Mobile phones, electronic devices, books, papers or other aids must NOT be in your possession at any time

during the examination. Calculators may be used provided they are silent, non-programmable and incapable of storing text.

8. Hand this examination question paper, the MCQ answer sheet, and any additional sheets to the invigilator at the end of the examination. Failure to hand in the examination paper and the MCQ answer sheet may preclude the

correction of your examination.

Membership Number:

First Name:

Surname:

Exam Centre:

Signature: Date:

FIN1028B: QFA Pensions

Sample Paper 1, 2018-19

Instructions for entering your answers on the Multiple Choice Question (MCQ) Answer Sheet

The MCQ Answer Sheet will be read by a machine and so these instructions must be read and followed

carefully.

• Please do NOT mark any part of the answer sheet with ticks or lines.

• Fill in the boxes fully, as shown in the diagram below (Assume A is the answer in this case).

• Fill in ONE box only per question as there is only ONE right answer.

If you do not know the answer to a question, and do not want to select A, B, C, or D, you must shade in circle E. Do NOT leave any row blank.

• If you select the correct option, you will score 3.

• If you select an incorrect option, you will score -1 (minus 1).

• If you select option E, you will score 0 (zero).

INCORRECT CORRECT

A B C D E A B C D E

NOTE: Use the separate MCQ Answer Sheet to record your answers. Do NOT record your answers on this

Examination Paper.

.

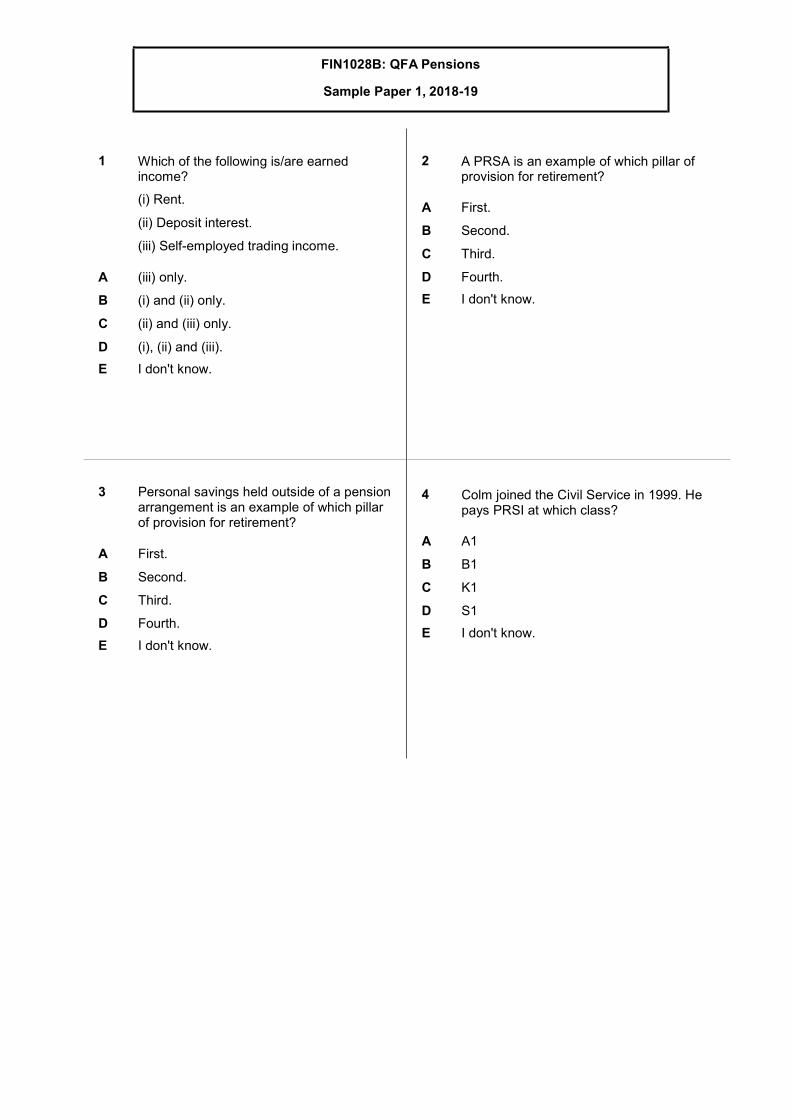

FIN1028B: QFA Pensions

Sample Paper 1, 2018-19

3

Personal savings held outside of a pension arrangement is an example of which pillar of provision for retirement?

A First.

B Second.

C Third.

D Fourth. E I don't know.

4 Colm joined the Civil Service in 1999. He pays PRSI at which class?

A A1

B B1

C K1

D S1 E I don't know.

2 A PRSA is an example of which pillar of provision for retirement?

A First.

B Second.

C Third.

D Fourth. E I don't know.

1 Which of the following is/are earned income?

(i) Rent.

(ii) Deposit interest.

(iii) Self-employed trading income.

A (iii) only.

B (i) and (ii) only.

C (ii) and (iii) only.

D (i), (ii) and (iii). E I don't know.

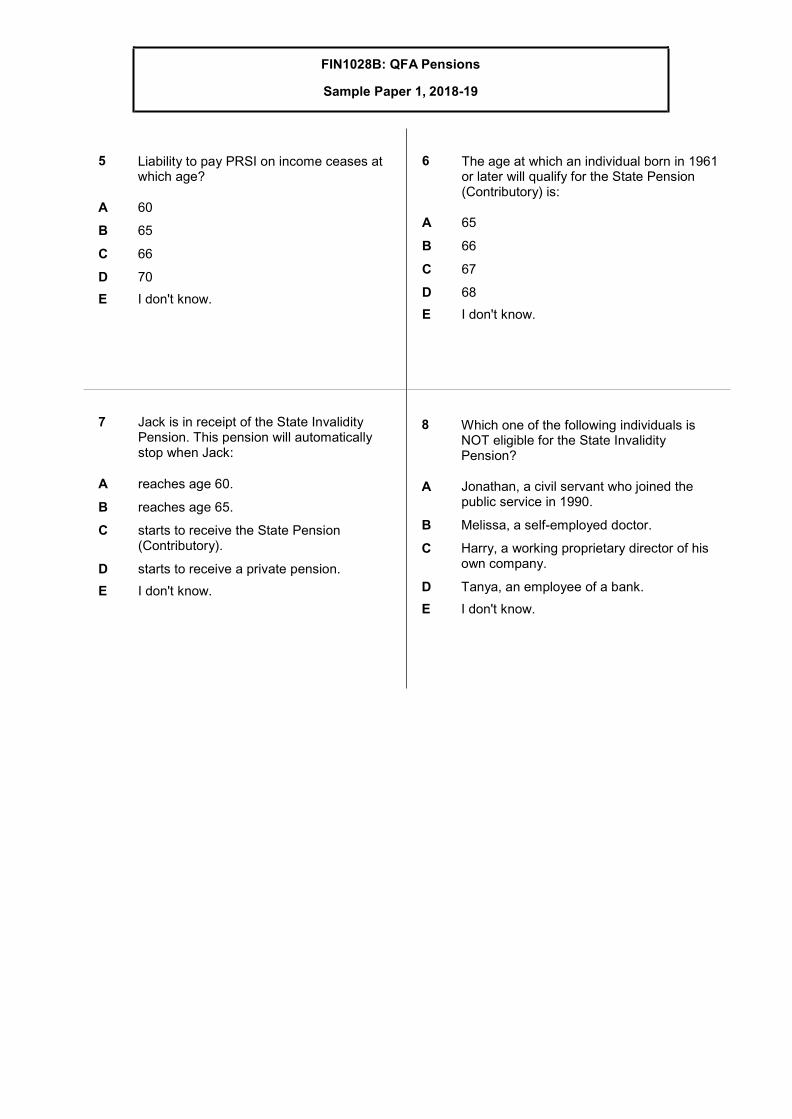

FIN1028B: QFA Pensions

Sample Paper 1, 2018-19

7

Jack is in receipt of the State Invalidity Pension. This pension will automatically stop when Jack:

A reaches age 60.

B reaches age 65.

C starts to receive the State Pension (Contributory).

D starts to receive a private pension. E I don't know.

8 Which one of the following individuals is NOT eligible for the State Invalidity Pension?

A Jonathan, a civil servant who joined the public service in 1990.

B Melissa, a self-employed doctor.

C Harry, a working proprietary director of his own company.

D Tanya, an employee of a bank. E I don't know.

6 The age at which an individual born in 1961 or later will qualify for the State Pension (Contributory) is:

A 65

B 66

C 67

D 68 E I don't know.

5 Liability to pay PRSI on income ceases at which age?

A 60

B 65

C 66

D 70 E I don't know.

FIN1028B: QFA Pensions

Sample Paper 1, 2018-19

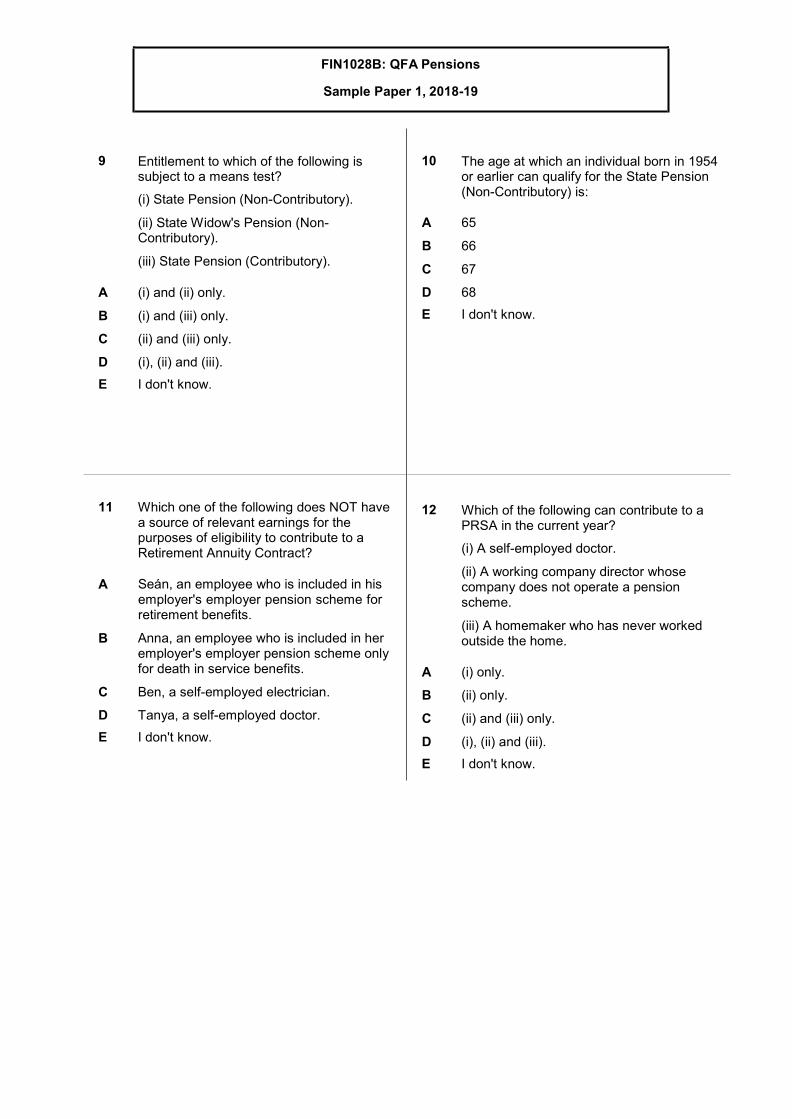

11

Which one of the following does NOT have a source of relevant earnings for the purposes of eligibility to contribute to a Retirement Annuity Contract?

A Seán, an employee who is included in his employer's employer pension scheme for retirement benefits.

B Anna, an employee who is included in her employer's employer pension scheme only for death in service benefits.

C Ben, a self-employed electrician.

D Tanya, a self-employed doctor. E I don't know.

12 Which of the following can contribute to a PRSA in the current year?

(i) A self-employed doctor.

(ii) A working company director whose company does not operate a pension scheme.

(iii) A homemaker who has never worked outside the home.

A (i) only.

B (ii) only.

C (ii) and (iii) only.

D (i), (ii) and (iii). E I don't know.

10 The age at which an individual born in 1954 or earlier can qualify for the State Pension (Non-Contributory) is:

A 65

B 66

C 67

D 68 E I don't know.

9 Entitlement to which of the following is subject to a means test?

(i) State Pension (Non-Contributory).

(ii) State Widow's Pension (Non- Contributory).

(iii) State Pension (Contributory).

A (i) and (ii) only.

B (i) and (iii) only.

C (ii) and (iii) only.

D (i), (ii) and (iii). E I don't know.

FIN1028B: QFA Pensions

Sample Paper 1, 2018-19

15

Employee PRSA contributions are deductible, within limits, for:

(i) income tax.

(ii) USC.

(iii) PRSI.

A (i) only.

B (i) and (iii) only.

C (ii) and (iii) only.

D (i), (ii) and (iii). E I don't know.

16 Grainne is self-employed. If she pays €25,000 to a Retirement Annuity Contract in December 2018 but because of limits on tax relief she can only claim tax relief on €20,000 of this contribution in 2018, what happens to the balance of €5,000?

A She can carry it forward and claim tax relief on it in 2019 against any relevant earnings she may have in 2019.

B She can backdate it for tax relief purposes to 2017.

C It is refunded to her by the life company.

D She cannot claim tax relief on it.

E I don't know.

14 Retirement Annuity Contract contributions are deductible, within limits, for:

(i) income tax.

(ii) USC.

(iii) PRSI.

A (i) only.

B (i) and (iii) only.

C (ii) and (iii) only.

D (i), (ii) and (iii). E I don't know.

13 Sorcha, aged 42, is self-employed and has net relevant earnings in 2018 of €130,000. If she has already contributed €5,000 to a PRSA in 2018, what is the MAXIMUM additional Retirement Annuity Contract or PRSA contributions Sorcha could pay and claim tax relief on in 2018?

A €18,000

B €23,750

C €27,500

D €32,500 E I don't know.

FIN1028B: QFA Pensions

Sample Paper 1, 2018-19

19

Graham is a self-employed doctor. What is the LATEST age by which he must draw on his PRSA?

A 60

B 65

C 70

D 75 E I don't know.

20 Amy, aged 48, has a Retirement Annuity Contract. She can draw on her plan now if she is:

A unemployed for more than 12 months.

B moving overseas permanently.

C adjudged insolvent.

D permanently incapacitated. E I don't know.

18 A commission paid annually by a life company based on the value of a PRSA is called which type of commission?

A Initial.

B Advance.

C Trail.

D Close. E I don't know.

17 Ross terminated his Retirement Annuity Contract (RAC) and opted to take a transfer value to another RAC with a different life assurance company. The transfer value payable was subject to an early encashment charge. This indicates that:

A Ross terminated the first plan within five years of starting it.

B the first plan was invested in a Property Fund.

C Ross was under age 60 at the time of transfer.

D Ross paid regular contributions to the first plan.

E I don't know.

FIN1028B: QFA Pensions

Sample Paper 1, 2018-19

23

Sam is maturing a Retirement Annuity Contract (RAC). He has not previously taken benefits from any other pension arrangement. He wants to transfer the part of the RAC not taken as a lump sum to an ARF.

Sam must then be in receipt of which level of pension/annuity income payable for his lifetime, in order NOT to have to invest part of the RAC proceeds in an AMRF or annuity purchase?

A €7,200 per annum.

B €10,000 per annum.

C €12,700 per annum.

D €18,000 per annum.

E I don't know.

24 Susan has just matured a PRSA. She had not previously taken retirement benefits from any other arrangement and is not in receipt of pension or annuity income from any source. After taking her lump sum she had a balance of €100,000 left in her PRSA, which she opted to retain as a vested PRSA.

What, if any, is the ring fenced part of her vested PRSA?

A Nil.

B €36,500

C €63,500

D €100,000 E I don't know.

22 Aishling has a Retirement Annuity Contract (RAC). If she dies today, the proceeds of her RAC would be payable to her:

A surviving husband or civil partner.

B estate.

C nominated beneficiaries.

D dependants in equal shares. E I don't know.

21 Emma is an employee and contributes to her own PRSA. What is the EARLIEST age Emma could draw on her PRSA on early retirement from her current employment?

A 50

B 55

C 58

D 60 E I don't know.

FIN1028B: QFA Pensions

Sample Paper 1, 2018-19

27

A Preliminary Disclosure Certificate must be given to a consumer taking out a PRSA before the:

A consumer signs the PRSA application form.

B PRSA contract is issued.

C PRSA’s cooling-off period expires.

D PRSA has been in force for more than 30 business days.

E I don't know.

28 Wendy has just taken out a PRSA. The PRSA provider must give her a Statement of Reasonable Projection within which number of days after commencement of the PRSA contract?

A 5

B 7

C 10

D 14 E I don't know.

26 The Disclosure Notice provided to a client taking out a Retirement Annuity Contract (RAC) on issue of the RAC is usually referred to as:

A specific.

B modified.

C precise.

D generic. E I don't know.

25 Jade has a vested PRSA. At age 75, which one of the following will NOT be an option for her with regard to the balance in her PRSA at that time?

A Retain the balance in the PRSA.

B Take the balance as a taxable lump sum.

C Transfer the balance into an AMRF.

D Buy an annuity. E I don't know.

FIN1028B: QFA Pensions

Sample Paper 1, 2018-19

31

An employer pension scheme established with a life assurance company for one employee only is set up by the employer completing which of the following documents?

A Letter of Exchange.

B Declaration of Trust.

C Appointment of Beneficiaries.

D Form of Indemnity. E I don't know.

32 DC employer pension schemes are also known as which type of scheme?

A Integrated.

B Money purchase.

C Career average.

D Dynamised. E I don't know.

30 Anne-Marie has a Retirement Annuity Contract (RAC) with an associated Pension Term Assurance policy for cover of €100,000, arranged on an 'exclusive of fund' basis. If the RAC is currently valued at €60,000, what TOTAL amount would be paid out between the two policies if Anne- Marie died today?

A €40,000

B €60,000

C €100,000

D €160,000 E I don't know.

29 Patricia has invested €50,000 in a single premium Retirement Annuity Contract (RAC), investing in an international equity fund. Within the cooling-off period allowed, Patricia exercised her cooling off right to cancel the RAC. Between issue of the RAC and when she exercised her cooling-off right, the international equity fund price had fallen by 10%.

What is the MAXIMUM amount she is legally entitled to get as a refund on cancellation of the RAC?

A €40,000

B €45,000

C €50,000

D €55,000 E I don't know.

FIN1028B: QFA Pensions

Sample Paper 1, 2018-19

35

An employer must pay which MINIMUM proportion of the total ordinary annual contributions paid to its employer pension scheme?

A 10%

B 20%

C 33%

D 50% E I don't know.

36 ABC Ltd is currently paying an ordinary annual contribution of €100,000 to their employer pension scheme. ABC now proposes to make a special additional once off contribution of €180,000 to the scheme.

How much of this special contribution, if any, will qualify for Corporation Tax relief in the company's accounting period in which the special contribution is paid?

A Nil.

B €90,000 C €100,000 D €180,000 E I don't know.

34 Nora is a member of her employer's pension scheme. If she pays €25,000 to the scheme as a personal contribution in July 2018 but can only claim tax relief on €20,000 of this contribution in 2018, what happens to the balance of €5,000?

A She can elect to transfer it to a PRSA.

B She can backdate it for tax relief purposes to 2017.

C It is refunded to her by the scheme administrator at the end of the year.

D She cannot get income tax relief on it. E I don't know.

33 Molly is a member of her employer's DC pension scheme. Her total accumulated retirement fund in the scheme is €230,000, of which €40,000 was funded by her own contributions.

She has no retained benefits. If her current best final remuneration is €35,000 per annum what is the MAXIMUM lump sum death in service benefit which the scheme could pay out if she died in service today?

A €140,000

B €180,000

C €190,000

D €230,000 E I don't know.

FIN1028B: QFA Pensions

Sample Paper 1, 2018-19

39

Luke is retiring under his employer's DB pension scheme at Normal Retirement Age (NRA) 65, after 25 years' service. His best final remuneration is €60,000 per annum. He has a retained lump sum of €25,000 under a previous employer's pension scheme.

What is the MAXIMUM approvable lump sum his employer's scheme can provide for him now on retirement at NRA?

A €56,250

B €65,000

C €78,750

D €90,000

E I don't know.

40 Service, for the purposes of calculating the Revenue maximum retirement benefits which can be provided by an employer pension scheme, means:

A any period while a member of the scheme.

B any year during which the member received taxable remuneration from the employer.

C any year during which the member received taxable remuneration from any employer.

D any period of time designated by the employer.

E I don't know.

38 The LATEST Normal Retirement Age which an employer pension scheme can use is:

A 65

B 68

C 70

D 75 E I don't know.

37 An employer contribution to its pension scheme to provide retirement benefits for a member is:

A a benefit in kind for income tax purposes for the member.

B subject to deduction of PAYE at source.

C a benefit in kind for income tax purposes for the member, which he or she can then claim tax relief on as if they had paid it themselves.

D not a benefit in kind for income tax purposes for the member.

E I don't know.

FIN1028B: QFA Pensions

Sample Paper 1, 2018-19

43

AVCs can be used to fund an additional:

(i) pension.

(ii) death in service benefit.

(iii) retirement lump sum.

A (i) only.

B (ii) only.

C (i) and (ii) only.

D (i), (ii) and (iii). E I don't know.

44 Saoirse has reached her Normal Retirement Age (NRA) in her employer's DC pension scheme. Her accumulated fund at NRA is €123,000, comprised of €99,000 related to her own and her employer's normal contributions, and an additional €24,000 in AVC funds. Her best calculation of final remuneration is €60,000 per annum, she has no retained benefits, and she has 28 completed years' service.

Assuming she opts for the ARF option, what is the MAXIMUM lump sum she can take in total at NRA?

A €30,750

B €66,000

C €90,000

D €114,000

E I don't know.

42 To be eligible to contribute currently to AVCs, an individual must:

(i) be an employee.

(ii) be a member of their employer’s approved employer pension scheme.

(iii) have remuneration from their employment of less than €115,000 per annum.

A (i) only.

B (ii) only.

C (i) and (ii) only.

D (i), (ii) and (iii). E I don't know.

41 Which part of a retiring employee’s remuneration can NOT be dynamised for the purposes of calculating the best final remuneration in an employer pension scheme?

A Benefits in kind.

B Bonuses.

C Remuneration received in the last 12 months.

D Remuneration received in the last three consecutive years.

E I don't know.

FIN1028B: QFA Pensions

Sample Paper 1, 2018-19

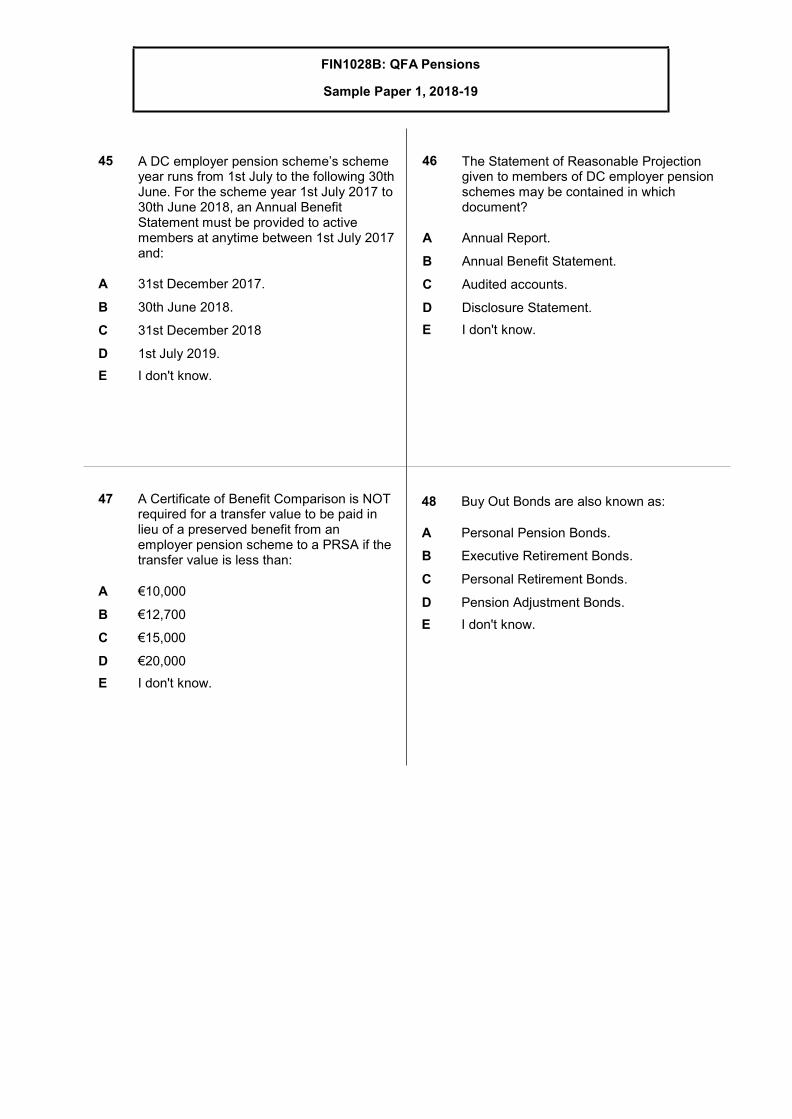

47

A Certificate of Benefit Comparison is NOT required for a transfer value to be paid in lieu of a preserved benefit from an employer pension scheme to a PRSA if the transfer value is less than:

A €10,000

B €12,700

C €15,000

D €20,000 E I don't know.

48 Buy Out Bonds are also known as:

A Personal Pension Bonds.

B Executive Retirement Bonds.

C Personal Retirement Bonds.

D Pension Adjustment Bonds. E I don't know.

46 The Statement of Reasonable Projection given to members of DC employer pension schemes may be contained in which document?

A Annual Report.

B Annual Benefit Statement.

C Audited accounts.

D Disclosure Statement. E I don't know.

45 A DC employer pension scheme’s scheme year runs from 1st July to the following 30th June. For the scheme year 1st July 2017 to 30th June 2018, an Annual Benefit Statement must be provided to active members at anytime between 1st July 2017 and:

A 31st December 2017.

B 30th June 2018.

C 31st December 2018

D 1st July 2019. E I don't know.

FIN1028B: QFA Pensions

Sample Paper 1, 2018-19

51

The basic amount of an employee's ex gratia termination payment which is always tax free is:

A €10,000

B €10,160 plus €765 for each complete year of service.

C 1/15th of final remuneration, for each complete year of service.

D €20,000 E I don't know.

52 A transfer value can be paid into a Buy Out Bond from a(n):

A ARF.

B employer pension scheme.

C PRSA.

D An RAC. E I don't know.

50 Paula is 38 and a deferred member of her

A

employer's DC pension scheme.

What is the EARLIEST age at which she can take retirement benefits form the scheme?

45

50

55

60

I don't know.

B

C

D E

49 What is the limit on the total amount of all tax free ex gratia termination payments an individual can take over their lifetime?

A €200,000

B €300,000

C €500,000

D €575,000 E I don't know.

FIN1028B: QFA Pensions

Sample Paper 1, 2018-19

55

A penalty or charge CANNOT be levied on the payment of a transfer value from which one of the following:

A Buy Out Bond.

B Retirement Annuity Contract.

C Standard PRSA.

D Employer pension scheme E I don't know.

56 A collective investment fund in which investors can only invest by buying shares in the fund on a Stock Exchange is called which type of fund?

A Debenture.

B Exchange Traded Fund (ETF).

C Unit Linked Fund.

D A Closed End Fund. E I don't know.

54 A transfer value CANNOT be paid from a Standard PRSA into which one of the following?

A Non Standard PRSA.

B DB employer pension scheme.

C Retirement Annuity Contract.

D DC employer pension scheme. E I don't know.

53 A Retirement Annuity Contract (RAC) can be transferred to a(n):

(i) PRSA.

(ii) Buy Out Bond.

(iii) employer pension scheme.

A (i) only.

B (i) and (ii) only.

C (ii) and (iii) only.

D (i), (ii) and (iii). E I don't know.

FIN1028B: QFA Pensions

Sample Paper 1, 2018-19

59

The main benefit of a unitised with profit fund to a Retirement Annuity Contract holder is:

A The right to choose which individual assets the fund should invest in.

B A smoothed investment return over time.

C The right to take retirement benefits at any time.

D The right to encash the units at guaranteed terms at any time.

E I don't know.

60 A Lifestyle Fund is an investment fund:

A which changes its asset allocation to more secure assets as the investor approaches retirement age.

B open only to wealthy investors, with a minimum investment of €100,000.

C which invests only in shares of companies making exclusive clothing and accessories.

D which changes its asset allocation to higher risk/return assets as the investor approaches retirement age.

E I don't know.

58 If a collective investment fund aims to track the movement of a particular Stock Market index, it is said to be adopting which investment management style?

A Active.

B Dynamic.

C Passive.

D Aggressive. E I don't know.

57 A UCITS fund is NOT allowed to invest in which of the following?

(i) Shares listed on the Stock Exchange.

(ii) An office building.

(iii) Gold.

A (i) only

B (ii) only.

C (i) and (ii) only.

D (ii) and (iii) only. E I don't know.

FIN1028B: QFA Pensions

Sample Paper 1, 2018-19

63

A Pension Adjustment Order can be made following:

(i) a decree of judicial separation.

(ii) the ending of a period of cohabitation by a couple who are neither married to nor registered civil partners to each other.

(iii) a decree of dissolution of a registered civil partnership.

A (ii) only.

B (i) and (ii) only.

C (ii) and (iii) only.

D (i), (ii) and (iii).

E I don't know.

64 Ciara is a member of her employer's employer pension scheme. Her marriage has been dissolved by a decree of divorce and her ex-husband has obtained a Pension Adjustment Order (PAO) against her scheme benefits. This PAO is served on:

A Ciara.

B Ciara's employer.

C the scheme trustees.

D the registered administrator of the scheme. E I don't know.

62 Which one of the following types of employer pension schemes is NOT required to be predominantly invested on regulated markets?

A One member DC scheme.

B DC scheme with more than 50 active members.

C All schemes, other than one member schemes.

D A DC scheme for 100 or more members. E I don't know.

61 Which one of the following investment transactions by an employer pension scheme would cause an immediate taxable withdrawal from the scheme of the funds and assets involved in the transaction?

A The scheme buys quoted shares direct from an unconnected third party.

B The scheme buys shares in a close company in which a member’s spouse is already a shareholder.

C The scheme invests in a life company geared property unit fund.

D The scheme invests in bonds denominated in US currency.

E I don't know.

FIN1028B: QFA Pensions

Sample Paper 1, 2018-19

67

In relation to a Pension Adjustment Order, contingent benefits include:

A death in service benefits only.

B retirement benefits only.

C death in service and retirement benefits only.

D death in service, ill health and retirement benefits.

E I don't know.

68 USC does NOT apply to:

A PAYE income.

B deposit interest.

C self-employed income.

D earned income in excess of €12,012. E I don't know.

66 Michael and Majella have divorced. Majella obtained a Pension Adjustment Order (PAO) over Michael's PRSA. She has not yet taken a transfer value. If Michael dies before drawing on his PRSA, what happens to Majella's PAO entitlement?

A It becomes a debt on Michael's estate.

B The PAO lapses without benefit.

C A transfer value is paid from the PRSA to Majella, within 3 months of Michael’s death.

D The PRSA continues in her name. E I don't know.

65 A Pension Adjustment Order (PAO) in relation to retirement benefits will direct the trustees or financial institution to pay part or all of the member's retirement benefit to the beneficiary of the PAO. This is called:

A forfeiture.

B salary sacrifice.

C earmarking.

D contingency. E I don't know.

FIN1028B: QFA Pensions

Sample Paper 1, 2018-19

71

What is the MAXIMUM Personal Fund Threshold which an individual could have obtained at 1st January 2014?

A €1.3 million.

B €2.3 million.

C €3.75 million.

D €5.4 million. E I don't know.

72 Jimmy has a Personal Fund Threshold certificate for €5.5 million. In 2018 he took retirement benefits valued at €3.5 million from a Small Self-Administered Pension Scheme (SSAPS). He had NOT previously taken any benefits from any other retirement arrangement.

What chargeable excess, if any, will arise for Jimmy in 2018 when taking benefits from the SSAPS?

A Nil.

B €687,107

C €1,000,000

D €1,500,000 E I don't know.

70 Retirement benefits taken from a pension arrangement before which date do not count against an individual’s available Threshold amount?

A 7th December 2005.

B 15th November 2009.

C 7th December 2010.

D 1st January 2014. E I don't know.

69 For income tax purposes, a Retirement Annuity Contract contribution is treated as a:

A tax credit.

B charge.

C relief.

D personal allowance. E I don't know.

FIN1028B: QFA Pensions

Sample Paper 1, 2018-19

75

Rob retired from the civil service in 2018. He had a chargeable excess tax liability on his public service superannuation benefits of €100,000. Rob can opt to pay this tax by a reduction in his gross pension over what MAXIMUM period?

A 5 years.

B 10 years.

C 15 years.

D 20 years. E I don't know.

76 Which one of the following counts against an individual’s remaining Standard Fund Threshold amount?

A Retaining a PRSA beyond age 75, without taking any benefits from it.

B Transfer of funds from one ARF to another ARF.

C Growth in the value of an ARF since its establishment from €1 million to €1.4 million.

D Payment of a transfer value from a retirement annuity contract to a PRSA.

E I don't know.

74 Cara has just taken retirement benefits which have given rise to a chargeable excess tax liability of €78,000. Which one of the following can she offset against this tax liability?

A Any income tax deducted from pension lump sums she has taken before 1st January 2014.

B Any amount transferred to an AMRF from her retirement benefits.

C Any standard rate income tax deducted from pension lump sums she has taken after 1st January 2011.

D Any amount from her retirement benefits which was used to purchase a taxable annuity.

E I don't know.

73 Chloe does not have a Personal Fund Threshold. If Chloe matures a PRSA in 2018 at a value of €2.4 million, what chargeable excess, if any, will arise for Chloe in 2018 when taking benefits from the PRSA?

A Nil.

B €100,000

C €200,000

D €400,000 E I don't know.

FIN1028B: QFA Pensions

Sample Paper 1, 2018-19

79

Louis is retiring and has a €200,000 retirement fund which must be used to buy an annuity. Which of the following types of annuity will provide Louis with the LOWEST initial level of annuity income?

A An escalating joint life.

B A level joint life.

C An escalating single life.

D A level single life. E I don't know.

80 Thomas has a Retirement Annuity Contract which is about to mature at €450,000. He is taking the ARF option but is required to purchase an annuity of €2,250 per annum to avoid having to invest part of the plan value in an AMRF.

Assuming an annuity rate for the type of pension Thomas wants is 4%, what amount will he have to use to purchase the annuity of €2,250 per annum?

A €23,625

B €42,850

C €56,250

D €63,500 E I don't know.

78 Annuity rates are currently at historically low levels because:

A AAA rated Government Bond yields are so low.

B deposit rates are so low.

C equity markets are so high.

D very few people are buying annuities. E I don't know.

77 An annuity provides which type of insurance for the investor?

A Longevity.

B Mortality.

C Life.

D Serious illness. E I don't know.

FIN1028B: QFA Pensions

Sample Paper 1, 2018-19

83

Nancy is aged 69 and has an ARF. Any withdrawal she takes from her ARF will be liable in her hands to:

(i) income tax.

(ii) USC.

(iii) PRSI.

A (i) only.

B (i) and (ii) only.

C (ii) and (iii) only.

D (i), (ii) and (iii). E I don't know.

84 Alan is aged 64 and has a vested PRSA, with a ring fenced part of €63,500 and a non-ring fenced part of €100,000, as at 30th November 2018. He has no other ARFs or vested PRSAs.

What minimum withdrawal, before taxes, must he take from his PRSA before the end of 2018 to avoid an imputed distribution applying to it for 2018?

A €2,540

B €4,000

C €6,540

D €8,175 E I don't know.

82 Jack is aged 58 and has an ARF. What limit, if any, applies to the withdrawal, as a percentage of his ARF value, Jack can make from his ARF?

A No limit.

B 4%

C 5%

D 6% E I don't know.

81 The right to buy an annuity with any life company offering the best annuity rate from the maturing proceeds of a RAC is referred to as which type of option?

A Open market.

B Continuation.

C Conversion.

D Reversionary. E I don't know.

FIN1028B: QFA Pensions

Sample Paper 1, 2018-19

87

How many withdrawals can an AMRF holder make from their AMRF in a year?

A 1

B 2

C 5

D Unlimited. E I don't know.

88 A benefit paid from a vested PRSA following the death of the PRSA holder is taxed as if it were a payment made from a(n):

A ARF.

B Section 785 policy death benefit.

C employer pension scheme.

D annuity contract. E I don't know.

86 Joyce’s AMRF is valued at €70,000 at 1st July 2018. What is the MAXIMUM withdrawal Joyce could take from her AMRF at that date, assuming she has not taken any previous withdrawal from her AMRF in 2018?

A €2,100

B €2,800

C €3,500

D €7,000 E I don't know.

85 Damien is aged 62 and at 30th November 2018 has an AMRF valued at €50,000 with ABC Life Co and an ARF valued at €100,000 with a different QFM. He has no other ARFs or vested PRSAs. He took a withdrawal, before taxes, of €1,000 from his AMRF in July 2018.

What minimum withdrawal, before taxes, must he take from his ARF before the end of 2018 to avoid an imputed distribution applying to his ARF for 2018?

A €3,000

B €4,000

C €5,000

D €6,000 E I don't know.

FIN1028B: QFA Pensions

Sample Paper 1, 2018-19

91

Which one of the following types of pension arrangement does NOT require prior approval from the Revenue Commissioners or Pensions Authority before being marketed or sold to the public?

A ARFs.

B Retirement Annuity Contracts.

C Buy Out Bonds.

D PRSAs. E I don't know.

92 If the Consumer Price Index 12 months ago was 142.5 and today it is 148.4, what has been the rate of inflation over the last 12 months?

A 3.5%

B 3.9%

C 4.1%

D 5.9% E I don't know.

90 Who has legal responsibility to issue guidelines on the operation of Pension Adjustment Orders?

A The Pensions Authority.

B The Revenue Commissioners.

C The Central Bank.

D The High Court. E I don't know.

89 Andrew died in 2018 and left the balance of his ARF to his son, Paul, who was aged 27 at that time. This benefit was:

A subject to capital gains tax at 33% at source.

subject to income tax at standard rate at source.

subject to income tax at 30% at source.

taxed under PAYE at Paul's marginal rate of income tax. I don't know.

B

C D

E

FIN1028B: QFA Pensions

Sample Paper 1, 2018-19

95

A Standard PRSA differs from a Non Standard PRSA in relation to which of the following?

(i) Maximum contribution.

(ii) Investment funds it can offer.

(iii) Limit on charges.

A (i) only.

B (i) and (iii) only.

C (ii) and (iii) only.

D (i), (ii) and (iii). E I don't know.

96 Which of the following offers an employee the option of taking voluntary early retirement benefits at age 55?

(i) Retirement Annuity Contract.

(ii) Standard PRSA.

(iii) Non Standard PRSA.

A (i) only.

B (i) and (iii) only.

C (ii) and (iii) only.

D (i), (ii) and (iii). E I don't know.

94 If Harriet invests €20,000 now for seven years and earns an investment return of 5% per annum compound over that period, what amount will her investment have grown to after seven years?

A €27,000

B €27,600

C €28,140

D €33,180 E I don't know.

93 If Katie achieved an investment return for the year of 5% per annum and inflation over the same year was 2% per annum, what real rate of investment return did she achieve in that year?

A 2%

B 3%

C 5%

D 7% E I don't know.

FIN1028B: QFA Pensions

Sample Paper 1, 2018-19

99

Eve requires a pension of €10,000 per annum starting in 10 years' time.

If the annuity rate applying in 10 years' time for the type of pension she wants will be 4%, what lump sum does she need to invest now to make up that pension in 10 years’ time, assuming her investment can earn a return of 5% per annum compound over that period?

A €153,500

B €186,000

C €195,250

D €201,250 E I don't know.

100 You have completed a Factfind with a client. The Consumer Protection Code requires you to:

A ask the client to certify the accuracy of the information provided by him or her by signing the form.

B read back to the client all the information collected and ask the client to confirm verbally the accuracy or otherwise of the information recorded.

C photocopy the Factfind and provide a copy to the client, before you proceed any further.

D stop the meeting and arrange another meeting, at least seven days later, at which you will provide advice to the client based on their needs.

E I don't know.

98 What is the SECOND step in the financial planning advisory process?

A Identify, quantify and prioritise financial needs.

B Fact finding.

C Devising a strategy.

D Making a recommendation. E I don't know.

97 Taylor is aged 48 and has a preserved benefit in her former employer’s DC pension scheme. She has now joined a new employer who operates a DC pension scheme.

Which one of the following options in relation to her preserved benefit will NOT provide her with the traditional benefit option when she comes to draw on her benefits?

A Take a transfer value to a PRSA.

B Take a transfer value to her new employer’s pension scheme.

C Keep the preserved benefit in her former employer’s pension scheme.

D Take a transfer value to a Buy Out Bond. E I don't know.

QFA Pensions

REVENUE UPLIFTED SCALES

Pension

Years of service completed with employer by NRA

Maximum approvable pension @ NRA as a fraction of final remuneration

1 1/10th x 2/3rds

2 2/10th x 2/3rds

3 3/10th x 2/3rds

4 4/10th x 2/3rds

5 5/10th x 2/3rds

6 6/10th x 2/3rds

7 7/10th x 2/3rds

8 8/10th x 2/3rds

9 9/10th x 2/3rds Lump Sum

Years of service completed with employer by NRA

Maximum approvable lump sum @ NRA as a fraction of final remuneration

1-8 3/80th for each year of service

9 30/80ths

10 36/80ths

11 42/80ths

12 48/80ths

13 54/80ths

14 63/80ths

15 72/80ths

16 81/80ths

17 90/80ths

18 99/80ths

19 108/80ths

ANNUAL TAX RELIEF LIMIT ON PERSONAL CONTRIBUTIONS TO ALL PENSION ARRANGEMENTS

Age attained during year

Tax relief limit (as % of net relevant earnings)

Under 30 15% 30 to 39 20% 40 to 49 25% 50 to 54 30%* 55 to 59 35% 60 and over 40%

* the 30% limit also applies to certain professional sportspeople under age 50, in relation to their income from their professional sports occupation.

INHERITANCE TAX THRESHOLDS 2018

Class Threshold

1 €310,000 2 €32,500 3 €16,250

REVENUE BENEFIT CAPITALISATION FACTORS

NRA

Female

no dependant

Female

with dependant

Male

no dependant

Male

with dependant

60 27.5 30.0 24.4 32.4 65 23.8 25.9 20.4 28.4 70 20.2 21.8 16.7 24.4

DEFINED BENEFIT PENSION ACCRUED BEFORE 1ST JANUARY 2014

DB Pension accrued before 1st January 2014

DB Pensions accrued after 1st

January 2014

20:1 for all ages Varies by the age attained in the year in which the pension starts

Up to and incl. 50 37:1 51, 52 36:1 53 35:1 54 34:1 55, 56 33:1 57 32:1 58 31:1 59, 60 30:1 61 29:1 62 28:1 63, 64 27:1 65 26:1 66 25:1 67, 68 24:1 69 23:1 70 and over 22:1

QFA Pensions

After

(Years)

1.5% pa

(€)

2.5% pa

(€)

5% pa

(€)

1 1,015 1,025 1,050

2 1,030 1,051 1,103

3 1,046 1,077 1,158

4 1,061 1,104 1,216

5 1,077 1,131 1,276

6 1,093 1,160 1,340

7 1,110 1,189 1,407

8 1,126 1,218 1,477

9 1,143 1,249 1,551

10 1,161 1,280 1,629

11 1,178 1,312 1,710

12 1,196 1,345 1,796

13 1,214 1,379 1,886

14 1,232 1,413 1,980

15 1,250 1,448 2,079

16 1,269 1,485 2,183

17 1,288 1,522 2,292

18 1,307 1,560 2,407

19 1,327 1,599 2,527

20 1,347 1,639 2,653

21 1,367 1,680 2,786

22 1,388 1,722 2,925

23 1,408 1,765 3,072

24 1,430 1,809 3,225

25 1,451 1,854 3,386

Payable in

(Years)

1.5% pa

(€)

2.5% pa

(€)

5% pa

(€)

1 985 976 952

2 971 952 907

3 956 929 864

4 942 906 823

5 928 884 784

6 915 862 746

7 901 841 711

8 888 821 677

9 875 801 645

10 862 781 614

11 849 762 585

12 836 744 557

13 824 725 530

14 812 708 505

15 800 690 481

16 788 674 458

17 776 657 436

18 765 641 416

19 754 626 396

20 742 610 377

21 731 595 359

22 721 581 342

23 710 567 326

24 700 553 310

25 689 539 295

FUTURE VALUE OF €1,000 INVESTED NOW AT THE END OF YEAR X, AT THE RATES SHOWN

PRESENT VALUE OF €1,000 PAYABLE NOW AT THE END OF YEAR X, AT THE RATES SHOWN

QFA Pensions - Solutions to 2018-19 Sample Paper 1 Q. Answer Reference