q4 & fy10 financial results - iis windows...

TRANSCRIPT

Q4 & FY10 Financial Results

January 25, 2011

Business Overview

Alain DutheilChief Operating OfficerChief Operating Officer

2

STMicroelectronicsA Global Semiconductor Company

FY10 revenue: $10.35BBy location of order shipment

13%America

25%EMEA

44%Greater China &

South Asia

18%Japan & Korea

15 main manufacturing sites Advanced R&D centers in 10 countries

South Asia

Advanced R&D centers in 10 countries Over 53,000 employees, including

ST-Ericsson Listed on NYSE Euronext (New York &

Paris) and Milan stock exchanges

3

Business Segment Overview

50/50 JV with Ericsson

Automotive, Consumer, Computer &

Communication Infrastructure (“ACCI”)

Industrial and Multisegment Sector

(“IMS”)Wireless

Home Entertainment

& Displays

Computer & Communication Infrastructure

Automotive Products

Group

Analog, Power and

MEMS

Microcontrollers, Memories and

SmartcardsMajor Product Lines

Products

Major Customers

4

Semiconductor Market Growth

300350$B

Total Available Market

150200250300

050

100

1 2 3 4 5 6 7 8 9 e e

2001

2002

2003

2004

2005

2006

2007

2008

2009

2010

e

2011

e

Serviceable Available Market (SAM):

Estimated SAM Growth in 2010: ~26%

E t d 5% t 8% th f SAM i 2011

Serviceable Available Market (SAM):

Source: WSTS, Nov. 2010

Expected 5% to 8% growth of SAM in 2011

5

ST Total Revenues

FY10 Reported Revenues = $10.35B+21.6% vs. FY09

12,000US$M

Record revenues driven by ACCI and IMS

8,000

10,000

Flash Memory

4,000

6,000ST ex Flash

0

2,000

FY05 FY06 FY07 FY08 FY09 FY10

* See appendix

6

Market Share Gains for ACCI & IMS

Total Available Market9 Months 20109 Months 2010

In the first 9 months of 2010:

49% ACCI & IMS SAM*STE SAM

ACCI & IMS SAM up 36%

Combined ACCI & IMS revenue up 46%Non SAM**

10 points ahead of the market

* SAM = Serviceable Available Market** Non SAM = Microprocessor, Optoelectronics, DRAM and Flash memoriesSource: WSTS, Company

7

Top Customers

Top 10 OEM Customers FY 2010 (listed alphabetically)

Apple

Bosch

Cisco/Scientific Atlanta

Continental

HPHP

Nokia

Research in Motion

Samsung

Seagate

8

Sony Ericsson

Revenues by Market Segment / Channel*

FY10 Sales: $10.35B FY10 vs. FY09

• Automotive +39%14%21%

• Automotive +39%• Industrial & Other +30%• Consumer +28%• Computer +23%

13%

12%32% p• Telecom -3%

8%32%

• Distribution +61%Automotive Computer

Consumer Industrial & Other

Telecom Distribution

* See appendix

9

Revenues by Region

FY10 Revenue up 21.6%By location of order shipment

Greater China & South Asia

AmericasFY10 +31%

Q410 +14% y-o-y

EMEAFY10 +7%

Q410 -2% y-o-y

& South AsiaFY10 +32%

Q410 +15% y-o-y

Japan & KoreaFY10 +15%

Q410 +12% y-o-yQ y y

10

Revenues by Product Segment

ACCI Segment

Computer and Communication f (CC )

FY10 Sales: $10.35B

27%

38%

35%Infrastructure (CCI)

Home Entertainment & Displays (HED)**

Automotive (APG)

40%22%

IMS Segment

38%

70%

30%Analog, Power and MEMS (APM)

Micro, non-Flash Memory and

ACCI IMS Wireless*

ST’s exposure to the Wireless segment

Smartcard (MMS)

ST’s exposure to the Wireless segment at the earnings level is ~12% * See appendix

** Includes Imaging business

11

ACCI in 2010

ACCI RevenueRevenue up 32% with contribution from all key product families particularly for Automotive, Set-Top-

4000

4500

particularly for Automotive, Set TopBoxes, Printers and Communication Infrastructure Applications

US$M

2000

2500

3000

3500

Key Achievements:

Led STB in Europe & Asia

500

1000

1500

2000Significant design wins gained especially in

automotive, printers and communication infrastructure applicationsLaunch of Freeman, new single-chip TV SoC

L h f th fi t 32 b lk t h l0

FY08 FY09 FY10

Launch of the first 32nm bulk technology platform for networking applications

12

ACCI – Q410 Products Highlights

Automotive Key design win in China for a full engine-control kit from a tier-one playerCooperation between ST, a major Chinese car maker and a major European p , j j p

tier-one OEM to generate a next-generation direct-injection engine platform Key design win for car infotainment chips for an OEM radio-navigation

application

Digital Consumer Significant new deployments of second-generation STB decoders in Europe,

China, India, Middle East and South America with more than 50 customers in production 10 major designs for third-generation STBsWorld’s first demonstration to key customer of the Freeman Premier single-chip

TV SoC Key design wins for DisplayPort and monitor chipsets

Computer and Communications Infrastructure ZT Systems announced the first ARM-based computing server, embedding

ST’s SPEAr1310 microprocessorDesign win for a 32nm ASIC for a very high capacity networking switchDesign win for a 32nm ASIC for a very high capacity networking switch

application

13

IMS in 2010

Record sales with revenue up 45% driven by MEMS, advanced analog and microcontroller f ili

IMS Revenuefamilies

Key achievements:

ST MEMS everywhere: games smartphones 3500

4000

4500

US$M

ST MEMS everywhere: games, smartphones, tablets “Year of the gyroscope”Tremendous growth in 32-bit microcontrollersSeveral breakthroughs in Advanced Analog and 2000

2500

3000

3500

Several breakthroughs in Advanced Analog and SmartPowerQualification of Advanced Analog completed in

Crolles 300mm0

500

1000

1500

0FY08 FY09 FY10

14

IMS - Q410 Product HighlightsMEMS 3-axis digital MEMS gyroscope in production for a leading tablet maker based in

KoreaMEMS e-compass now in volume production at smartphone maker in China Launch of new family of high-g acceleration sensors for advanced airbag systems

Sensors & Analog Increased market penetration for micro-power op amps in glucose meters, LED

lights bulb and hard-disk drive applicationslights bulb and hard disk drive applications Launch of extremely small silicon pressure sensor for various applications

including smartphones, sports watches and other portable equipment

Smartcard & MicrocontrollersF th t i f th 32 bit MCU f il t i l d ARM C t M0 d M4 Further extension of the 32-bit MCUs family to include ARM Cortex-M0 and -M4 coresDesign wins for the new 1-Mbyte-Flash Access/Performance Line of 32-bit MCUs

at leading OEMs in consumer, healthcare and smart-metering applicationsNew NFC-enabled SIM card from Oberthur Technologies based on ST33 MCU

Energy Metering and PowerDesign win as the sole source for STarGRIDTM SoCs for smart metering

equipment in SpainMultiple design wins for power transistors including for a leading European maker p g p g g p

of solar panels and an important games platform power supply.

15

ST-Ericsson in 2010

Pivotal year for ST-Ericsson

As expected, on going legacy portfolio decrease not yet compensated by new products ST-Ericsson Revenue

(FY09 f )

4000

not yet compensated by new productsST Wireless Product Segment revenue down 14%

Key achievements:

(FY09 proforma)

US$M

2000

3000

Key achievements:

Restructuring efforts completed Strong performance of new 2G/EDGE platformsLaunch of HSPA+ M570 thin modem

1000

Launch of HSPA+ M570 thin modemPrepared product portfolio expansion in the

smartphone and tablet markets……including U8500 smartphone platform expected

to ramp in the second half of 2011 with several0

FY09 FY10

to ramp in the second half of 2011 with several Tier 1 customers

16

ST-Ericsson – Q410 Product Highlights

Collaboration with Quanta Computer on LTE modules and USB dongles

Joined forces with Nokia in TD-LTE in China, demonstrating multimedia services on a TD-LTE Nokia booklet containing ST-Ericsson’s M700 TD-LTE thin modem.

Smart mobility & multimedia

Samsung selected single-chip G4906 GSM/GPRS platform

Acer, Ericsson and Telstra launched the first netbook with a built-in 21Mbps HSPA+ mobile broadband module, based on p ,ST-Ericsson’s M570 thin modem

17

ST Products / Priorities for 2011Innovative products in highly successful applications continue to grow

MEMS gyroscopes & accelerometersgy pGeneral and secure 32-bit microcontrollers families ICs for Automotive

B kth h i d tBreakthrough in new products

SoCs for 3-D and connected TVsMEMS microphones and pressure sensors Advanced analog products for medical and smart grid applications Advanced analog products for medical and smart grid applications 32-bit Power PC microcontrollers for Automotive

ST-Ericsson’s key new products to ship in volume including HSPA+ thin modems and U8500 platform

We are ready for the next wave…

E M t & S i / H lth & W ll / T t d D t S it / Energy Management & Saving / Healthcare & Wellness / Trust and Data Security / Smart Consumer Devices

18

ST Manufacturing Evolution

ST STRATEGY PATH:

IDM Flexible IDM Lighter Asset

17 14 9 8

NUMBER OF FRONT END FABS:

17 14 9 8

WAFER PROBING (EWS):

From Europe to a major WW center in Singapore

ASSEMBLY NUMBER OF PLANTSASSEMBLY – NUMBER OF PLANTS:In Mediterranean :In Asia:

3 3 (1 China)

24 (2 China) Expand Asia

2005 end Q111end 2009

19

Manufacturing LocationsFrance

(Crolles I & II, Rousset, Tours)

Italy(Agrate, Catania 6”& 8”)

China Morocco

Malaysia

Phoenix(final stages of closure) Philippines

(Shenzhen, Longgang)Malta

Malaysia

Front-end fabs

Back-end fabs

20

Key Initiatives to Increase Capacity - 2010

Crolles 300mm Ramp to 3,200 w/week 32nm R&D capability

Agrate 200mm Increase capacity in BCD technologies & MEMS

Singapore 150mm Ramp to 18,000 w/day Partial conversion to 200mm

Q409 to Q410:Increase in total capacity including foundry ~20%

Foundry

Electrical Wafer Sort Increase capacity in wafer probing Increase capacity in wafer probing

Longgang / Shenzhen / Calamba Increase capacity in back-end fabs

21

Capacity Strategy for 2011

Objectives:

Support key product ramps:

AutomotiveMEMSWireless (U8500 smartphone platform)

30%

35%

40%

45%

Fuel revenue growth faster than SAM:

Anticipated CapEx between $1.1B and $1.5B as a transitional effort to support revenue growth and new products 10%

15%

20%

25% 2005 – 2010 ~11%ST 1995 – 2005 ~26%

growth and new products

Model:

Committed to asset lighter model

0%

5%

10%

Committed to asset lighter model 2009-10 capex/sales 7.9% 80% internal / 20% externalAdvanced CMOS targeting 2/3 external

CapEx as % of Revenues

22

Financial Results

Carlo FerroChief Financial Officer

Q4 & FY10 Highlights

2010: A year of improvement of financial results

Q410: Exiting the year with strong results and a solid capital structurea solid capital structure

Met our financial model

2011 opportunities

24

Financial Performance

In US$M, except EPS Q110 Q210 Q310 Q410 FY10 FY09

Net Revenues 2,325 2,531 2,657 2,833 10,346 8,510

Gross Margin 37.7% 38.3% 39.2% 39.9% 38.8% 30.9%

Adjusted Operating Profit*Adjusted Operating Margin*

120 5%

1034 1%

2208 3%

2458 6%

5805 6%

(732)8 6%Adjusted Operating Margin

Attributable to ST*0.5%4.0%

4.1%7.7%

8.3%11.6%

8.6%12.4%

5.6%9.2%

-8.6%-6.8%

Net Income – Reported 57 356 198 219 830 (1,131)

EPS Diluted 0 06 0 39 0 22 0 24 0 92 (1 29)EPS DilutedAdjusted EPS Diluted*

0.060.07

0.390.18

0.220.23

0.240.27

0.920.75

(1.29)(0.72)

Net Operating Cash Flow**Net Financial Position*

176565

212702

224878

3491 152

9611 152

1363420Net Financial Position 565 702 878 1,152 1,152 420

Effective Exchange Rate €/$ 1.39 1.35 1.34 1.34 1.36 1.37

* See appendix

** Including M&A, main amount being $1,145M in Q109

25

ST Total Revenues12 000

8 000

10,000

12,000

Flash Memory*US$M

4 000

6,000

8,000 yST ex FlashOthersWPSACCI

0

2,000

4,000 ACCIIMS

ACCI: +32%• Driven by all key families

IMS: +45%• MEMS – “year of gyros”

WPS: -14%• Ongoing transition

0FY01 FY02 FY03 FY04 FY05 FY06 FY07 FY08 FY09 FY10

Driven by all key families• Automotive• Printers• Set-top Box• Comm. Infrastructure

MEMS year of gyros• Microcontrollers• Advanced analog• Power & Industrial

Ongoing transition• New products ramping:

• 2G/EDGE• HSPA+ modem

• Preparing for U8500

* See appendix

26

Comm. Infrastructure Preparing for U8500

Operating Profitability

580

Operating Income(in US$M; excluding restructuring)

-7322009 Unused

CapacityVolume Price

EffectEfficiency

of Operations

Other Inc Exp

ProductMix

Opex $ Effect Operating Income

Wireless

2010

Leverage$1.31B operating income

Ongoing investment in ST-Ericsson

Analysis excluding ST-Ericsson

27

$ p g$1.84B revenue growth

Completed Exit from FlashM h 2008 F b 2010 M 2010 D b 2010March 2008

Numonyxformation

February 2010

Sale Agreementwith Micron signed

May 2010

Transaction Closing

December 2010

Monetized 70% of share

66.88M shares of Micron common stock At Micron’s share price of $8.75 on May 6, 2010 (transaction close) the value of the shares

were $585.2M A payable of $77 8M was due by ST to Francisco Partners

Considerationfor ST

proceeds

A payable of $77.8M was due by ST to Francisco Partners

Full ownership of the Numonyx M6 facility in Catania, Italy Contributed for 60M € by ST to the new photovoltaic joint initiative owned 33% by ST

46 8M h ld i d f $397M

for ST

St t f 46.8M shares sold against net proceeds of $397M 20.1M shares outstanding are fully hedged

At hedged price, total net consideration similar to value at closingE ti i h t f th $225M ST’ t t N lFinancial

Status as of Dec 31, 2010

Extinguishment of the $225M ST’s guarantee to a Numonyx loan Recovered $250M of restricted cash

Financial impact to ST

Over $1B improvement to ST’s capital structure

28

Over $1B improvement to ST s capital structure$265M gain recorded in ST’s 2010 P&L

ST Q410 Revenues

Q410 Revenues: +6.6% sequentially to $2,833M IMS, ACCI and Wireless increased 12%, 4% & 3%, respectively Growth in all regions; led by Japan-Korea, GC-South Asia, & America at 10%, 8%, & 7%, respectively

M k t t d i b A t ti I d t i l d C t t 16% 13% & 10% ti l

3,000US$M

Market segments driven by Automotive, Industrial and Computer at 16%, 13% & 10%, respectively

2,000

2,500

1,000

1,500

500

1,000

0Q308 Q408 Q109 Q209 Q309 Q409 Q110 Q210 Q310 Q410

29

ST Q410 Gross Margin

40%39.9%

35%

37.0%

30%

25%Q409 GM FX Price Volume & Product Mix* Group Mix* Q410 GM

Efficiency

30

* Product mix indicates the impact on the gross margin within each of the product groups. Group mix indicates the impact on the gross margin of business mix changes among product groups.

Operating Margin by SegmentWi l

25%1200

ACCI IMS Wireless

25%1200

50

100

150800

0%

13%

400

800

0%

13%

400

800

-150

-100

-50

0

0

400

Q308 Q409 Q410 Q308 Q409 Q410 Q409 Q410

Operating MarginRevenue Operating Income (US$M)

• 2010 Sales: $4.2B• FY10/09 Sales: +32%• Q410 Op Margin: 11.9%

• 2010 Sales: $3.9B• FY10/09 Sales: +45%• Q410 Op Margin: 22.5%

• 2010 Sales: $2.2B• FY10/09 Sales: -14%,

ongoing transition• Q410 Op Result: -$136M• 50% minority interesty

Targets*:

Q410: High single digitsMid t T

Targets*:

Q410: High teensMid t > 20%

Target:

Sustainable profitability

31

Mid-term: Teens Mid-term: > 20%

* Targets set on June 3, 2010; assumed revenues based on a substantial continuity in market demand trends and an effective exchange rate between 1.25 €/$ to 1.30 €/$

IMS BusinessesAnalog, MEMS & Microcontrollers (AMM) Advanced analog

Op Amps / Comparators MEMS

Gyroscopes / AccelerometersAMM Q410:

Gyroscopes / Accelerometers Microphones Pressure sensors

Microcontrollers 32-bit General purpose / secure

Revenues: $786MOperating Margin: 24.4%

p p Memories

E-EPROM / EPROMIMSQ410 Sales:

$1 13BPower Discrete Products (PDP) Discrete

Thyristors / Triacs / RectifiersPDP Q410:

$1.13B

y IPAD Protection

Power Transistors MOSFET IGBT

P RF

Revenues: $366MOperating Margin: 17.2%

Power RF

32

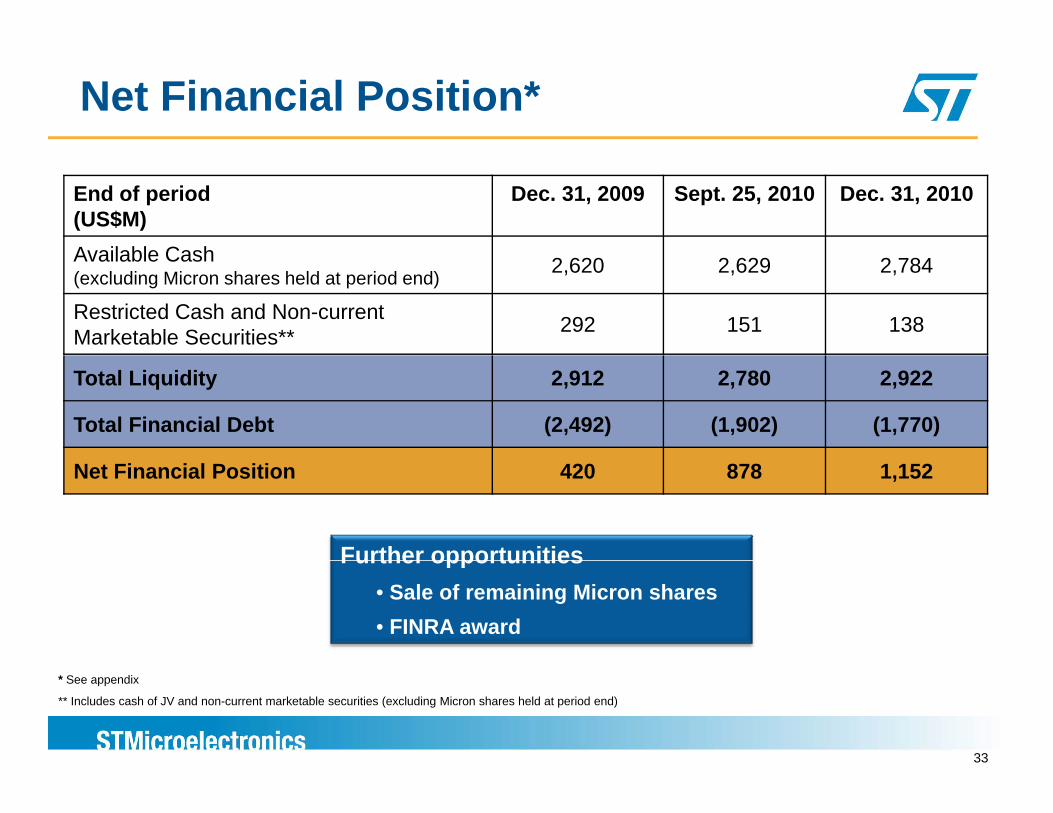

Net Financial Position*

End of period(US$M)

Dec. 31, 2009 Sept. 25, 2010 Dec. 31, 2010

Available CashAvailable Cash(excluding Micron shares held at period end) 2,620 2,629 2,784

Restricted Cash and Non-current Marketable Securities** 292 151 138

Total Liquidity 2,912 2,780 2,922

Total Financial Debt (2,492) (1,902) (1,770)

Net Financial Position 420 878 1,152

Further opportunitiesFurther opportunities• Sale of remaining Micron shares• FINRA award

* See appendix

** Includes cash of JV and non-current marketable securities (excluding Micron shares held at period end)

33

2 Years of Improving ST Capital Structure

1,152

-545

(US$M)

Dec. 312008

Operating Cash Flow before M&A

M&A Others Dividends Dec. 312010

-545

$1.7B swing in 8 quarters through 2009 recession + 2010 recovery

Capex/sales 7.9%

34

Dividend yield ~3% (on average share price in the period)

Return on Invested Capital

Return on Net Assets* (%)

19.020.7

20

30 RONA RONA attributable to ST*

10.5

4.60 7

6.0

13.0 13.9

7.65.1

11.9

10

-0.8

-7.1

0.7

-16 1-13.8

-5.3

-10

0

-16.2 -16.6

-16.1

-20Q3 08 (**) Q4 08 Q1 09 Q2 09 Q3 09 Q4 09 Q1 10 Q2 10 Q3 10 Q4 10

* See appendix

** w/o NXP acquisition-related one-time IP/inventory

35

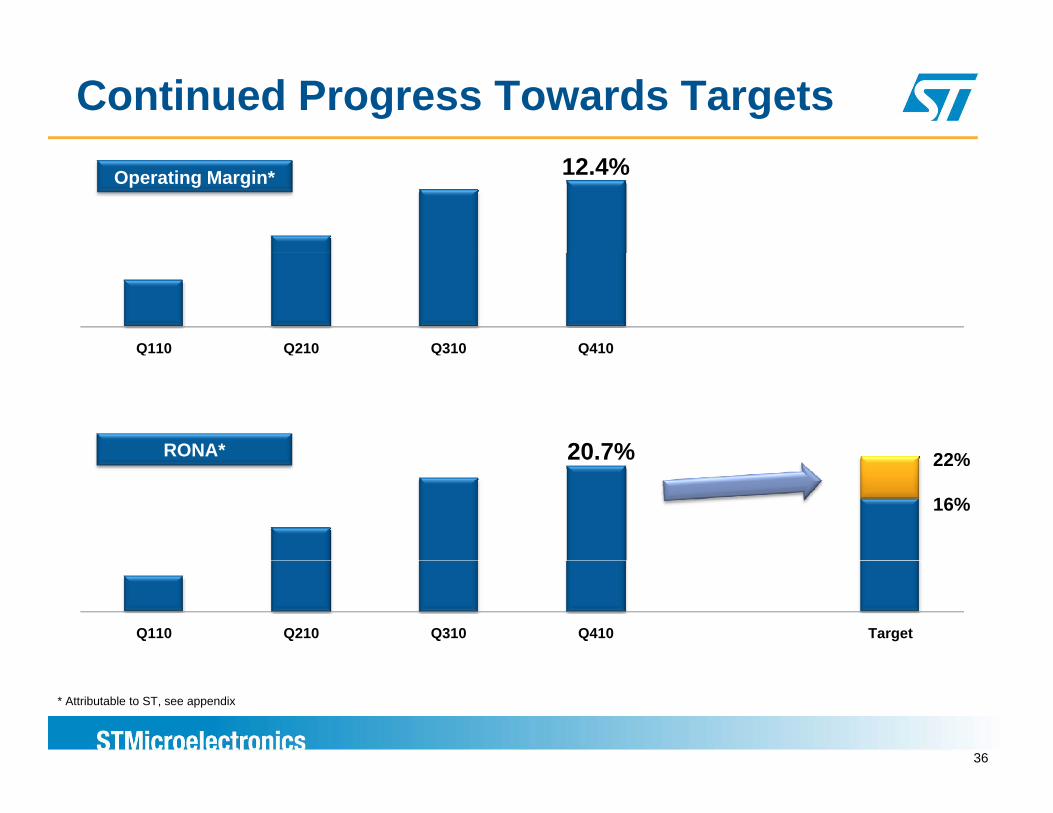

Continued Progress Towards Targets12.4%Operating Margin*

Q110 Q210 Q310 Q410

20.7% 22%RONA* 20.7% 22%

16%

Q110 Q210 Q310 Q410 Target

36

* Attributable to ST, see appendix

Q4 & FY10 – Summary

2010: A year of improvement of financial results Revenues up 21.6% to a record $10.35B Y-o-Y growth of 38% in ACCI+IMS higher than expected SAM growthg % g p g Operating income of $476M Completed exit from Flash Memory business Transition in Wireless progressing

Q410: Exiting the year with strong results and solid capital structure Revenues up 6.6% sequentially Gross margin increased again to 39.9%, up 70 basis points sequentially ACCI and IMS operating margins reached 11.9% and 22.5%, respectively, while

ti l f Wi l $136Moperating loss for Wireless was $136M Net financial position of $1.15B

Met our financial modelRONA and Operating Margin attributable to ST progressed throughout 2010 to reach RONA and Operating Margin attributable to ST progressed throughout 2010 to reach 20.7% and 12.4%, respectively in Q410*

Targets set in June 2010 for Q410 achieved one quarter in advance

* See appendix

37

Looking Forward to 2011

SAM expected to grow 5% to 8%:

ST to gain market shareST to gain market share

Leverage product portfolio:All segments targeting

operating margin

Deliver results:Y-o-Y improvements in operating margin

improvement from current levels

o p o e e tsquarterly operating

profitability

Anticipated CapEx of between $1.1B to $1.5B as a transitional effort to support

revenue growth and new productsproducts

Q1 2011 Outlook:Revenues sequentially about -7% to -12% (assuming midpoint, up 10% y-o-y)

38

q y % % ( g p , p % y y)Gross Margin about 39% ± 1%

Shareholders Value Proposition

World-wide semiconductor

leader

ST value driven by strategic

transformations

Sustainable profitability & strong

capital structure

Wireless as a value opportunity

Expanded customer base y

Innovative products serving high-growth

d k t

39

end markets

Appendix Net operating cash flow is defined as net cash from operating activities minus net cash used in investing activities, excluding payment for purchases of and

proceeds from the sale of marketable securities (both current and non-current), short-term deposits and restricted cash. We believe net operating cash flow provides useful information for investors and management because it measures our capacity to generate cash from our operating and investing activities to sustain our operating activities. Net operating cash flow is not a U.S. GAAP measure and does not represent total cash flow since it does not include the cash flows generated by or used in financing activities. In addition, our definition of net operating cash flow may differ from definitions used by other companies

Net financial position: resources (debt), represents the balance between our total financial resources and our total financial debt. Our total financial resources include cash and cash equivalents net of bank overdrafts if any current and non current marketable securities excluding Micron shares received in connection withinclude cash and cash equivalents, net of bank overdrafts, if any, current and non-current marketable securities excluding Micron shares received in connection with the sales of Numonyx, short-term deposits and non-current restricted cash, and our total financial debt includes the current portion of long-term debt and long-term debt, all as reported in our consolidated balance sheet. We believe our net financial position provides useful information for investors because it gives evidence of our global position either in terms of net indebtedness or net cash by measuring our capital resources based on cash, cash equivalents and marketable securities and the total level of our financial indebtedness. Net financial position is not a U.S. GAAP measure.

Return on Net Assets (RONA) is the ratio of operating income before impairment and restructuring charges divided by average net assets used during the period. ST defines average net assets as average total assets net of total liabilities as reported in our consolidated balance sheet excluding all items related to our financial position such as cash and cash equivalents marketable securities short term deposits bank overdrafts current portion of long term debt and long term debtposition such as cash and cash equivalents, marketable securities, short term deposits, bank overdrafts, current portion of long term debt and long term debt.

Adjusted operating income (loss) excludes impairment, restructuring charges and other related closure costs.

Adjusted operating income attributable to ST is calculated as adjusted operating income (loss) excluding 50% of ST-Ericsson operating income (loss) before restructuring as consolidated by ST. Adjusted operating margin attributable to ST is calculated as adjusted operating income attributable to ST divided by reported revenues excluding 50% of ST-Ericsson revenues as consolidated by ST. Return on Net Assets (RONA) attributable to ST is calculated as annualized adjusted operating income attributable to ST divided by reported net assets excluding 50% of ST-Ericsson net assets as consolidated by ST.

Adjusted net earnings and earnings per share (EPS) are used by our management to help enhance an understanding of ongoing operations and to communicate the impact of the excluded items. Adjusted earnings exclude impairment, restructuring charges and other related closure costs attributable to ST, the impact of equity investment divestiture, other-than-temporary impairment (OTTI) charges on financial assets, net of the relevant tax impact.

Key Information on Consolidation / Deconsolidation: ST completed the deconsolidation of its Flash Memory Group (FMG) segment and took an equity interest in Numonyx on March 30, 2008. Numonyx was

sold to Micron on May 7, 2010. ST-NXP Wireless, a joint venture initially owned 80% by ST, began operations on August 2, 2008 and was fully consolidated into ST’s operating results. On

February 1, 2009 and prior to the closing of the merger of ST-NXP Wireless and Ericsson Mobile Platforms to create ST-Ericsson, ST exercised its option to buy out NXP’s 20% ownership stake of ST-NXP Wireless.

ST-Ericsson, a joint venture owned 50% by ST, began operations on February 3, 2009 and is consolidated into ST’s operating results as of that date. ST-Ericsson is led by a development and marketing company and is consolidated by ST. A separate platform design company providing platform designs mostly to the development and marketing company is accounted for by ST using the equity method.

Wi l S t A f F b 3 2009 “Wi l ” i l d th ti f l d ti lt f th 50/50 ST E i j i t t lid t d i Wireless Segment: As of February 3, 2009, “Wireless” includes the portion of sales and operating results of the 50/50 ST-Ericsson joint venture as consolidated in the Company’s revenues and operating results, as well as other items affecting operating results related to the wireless business.

Sales recorded by ST-Ericsson and consolidated by ST are included in Telecom and Distribution

40

Pre-Tax Items to Adjusted Earnings*

In US$M Q110 Q210 Q310 Q410 FY10 FY09

ULT

U.S. GAAP Net Earnings 57 356 198 219 830 (1,131)

I i t & R t t i ChRAT

ING

RES

UG

S

Impairment & Restructuring Charges(attributable to Parent Company’s shareholders)**

20 8 18 20 66 240

Other-than-Temporary Impairment 140

OPE

RET

EA

RN

ING

Other-than-Temporary ImpairmentNumonyx ImpairmentEquity Investment DivestitureLoss on sale of Micron sharesEstimated Income Tax effect of Adj. (15)

(265)

60 (5)13(9)

(265)1331

140200

(76)

N

Adjusted Net Earnings* 62 159 211 243 675 (627)

* See appendix

** Total Impairment & Restructuring Charges were $33M in Q110, $12M in Q210, $27M in Q310, $33M in Q410, $104M in FY10 and $291M in FY09

41

Forward Looking StatementsS f th t t t t i d i thi l th t t hi t i l f t t t t f f t t ti d th f d l ki t t t ( ithi Some of the statements contained in this release that are not historical facts are statements of future expectations and other forward‐looking statements (within the meaning of Section 27A of the Securities Act of 1933 or Section 21E of the Securities Exchange Act of 1934, each as amended) that are based on management’s current views and assumptions, and are conditioned upon and also involve known and unknown risks and uncertainties that could cause actual results, performance or events to differ materially from those in such statements due to, among other factors:

Changes in demand in the key application markets and from key customers served by our products, which make it extremely difficult to accurately forecast and plan our future business activities. In particular, following a period of significant order cancellations in 2009, we have over the last quarters experienced a strong surge in customer demand, which has led to capacity constraints in certain applications; however we may again in the future, inexperienced a strong surge in customer demand, which has led to capacity constraints in certain applications; however we may again in the future, in case of excessive inventory at customers or distribution channels, experience order cancellations;

our ability to utilize and operate our manufacturing facilities at sufficient levels to cover fixed operating costs during periods of reduced customer demand, as well as our ability to ramp up production efficiently and rapidly to respond to increased customer demand, in an intensely cyclical and competitive industry, and the financial impact of obsolete or excess inventories if actual demand differs from our expectations;

the operations of the ST‐Ericsson Wireless joint venture, which represents a significant investment and risk for our business and which may lead to significant additional impairment and restructuring charges, in the event ST‐Ericsson is unable to successfully compete in a rapidly changing and increasingly competitive market;

our ability to compete in the semiconductor industry since a high percentage of our costs are fixed and are incurred in Euros and currencies other than U.S. dollars, especially in light of the increasing volatility in the foreign exchange markets and, more particularly, in the U.S. dollar exchange rate as compared to the Euro and the other major currencies we use for our operations;

the outcome of ongoing litigation as well as any new litigation to which we may become a defendant; changes in our overall tax position as a result of changes in tax laws or the outcome of tax audits, and our ability to accurately estimate tax credits,

benefits, deductions and provisions and to realize deferred tax assets; the impact of intellectual property (“IP”) claims by our competitors or other third parties, and our ability to obtain required licenses on reasonable terms

and conditions;and conditions; product warranty or liability claims based on epidemic failures or recalls by our customers for a product containing one of our parts; our ability in an intensively competitive environment to secure customer acceptance and to achieve our pricing expectations for high‐volume supplies of

new products in whose development we have been, or are currently, investing; availability and costs of raw materials, utilities, third‐party manufacturing services, or other supplies required by our operations; and changes in the political, social or economic environment, including as a result of military conflict, social unrest and/or terrorist activities, economic

turmoil, as well as natural events such as severe weather, health risks, epidemics, earthquakes, volcano eruptions or other acts of nature in, or affecting, the countries in which we our key customers or our suppliers operatethe countries in which we, our key customers or our suppliers, operate.

Such forward‐looking statements are subject to various risks and uncertainties, which may cause actual results and performance of our business to differ materially and adversely from the forward‐looking statements. Certain forward‐looking statements can be identified by the use of forward‐looking terminology, such as “believes,” “expects,” “may,” “are expected to,” ”, “should,” “would be,” “seeks” or “anticipates” or similar expressions or the negative thereof or other variations thereof or comparable terminology, or by discussions of strategy, plans or intentions.

Some of these risk factors are set forth and are discussed in more detail in “Item 3. Key Information— Risk Factors” included in our Annual Report on Form 20‐F for the year ended December 31, 2009, as filed with the SEC on March 10, 2010. Should one or more of these risks or uncertainties materialize, or should underlying

42

the year ended December 31, 2009, as filed with the SEC on March 10, 2010. Should one or more of these risks or uncertainties materialize, or should underlying assumptions prove incorrect, actual results may vary materially from those described in this release as anticipated, believed or expected. We do not intend, and do not assume any obligation, to update any industry information or forward‐looking statements set forth in this release to reflect subsequent events or circumstances.