q2 2019 market report - croft & bender

TRANSCRIPT

Q2 2019 Market Report

Mergers & Acquisitions • Private Equity • Financial Advisory

4401 Northside Parkway Suite 395 Atlanta, Georgia 30327 (404) 841-3131 www.croft-bender.com Member SIPC and FINRA

DEAL CRITERIA

MERGERS & ACQUISITIONS

• Buy side/sell side• Enterprise Values up to $300 million• Exceptions to typical EBITDA criteria:– High growth companies– Technology companies– Special situations

EQUITY & DEBT CAPITAL RAISES

• Middle-market companies• Emerging growth businesses• Large market opportunity• Experienced management team• Differentiated product or service• Greater than $10 million capital need

BROAD INDUSTRY EXPERTISE

BUSINESS SERVICES

Information ServicesMarketing Services Financial Services

Outsourced Services A/R Management

StaffingConsulting

TECHNOLOGY

Software/SaaSFinancial Technology

Human Capital ManagementInternet Marketing

E-CommerceSecurity/ComplianceBusiness IntelligenceTelecommunications

INDUSTRIAL

General ManufacturingBuilding Products

LogisticsSpecialty Contracting

DistributionIndustrial Services

ChemicalsDurable Goods

HEALTHCARE

Healthcare ITClinical Services

Outsourced ServicesAlternate Site Care

Medical Products/Distribution

CONSUMER

Products/ServicesFranchisingRestaurants

RetailEntertainment/Leisure

OVERVIEW

Since 1996, Croft & Bender has provided superior M&A, private capital raising, andfinancial advisory services to middle-market and emerging growth companies. Thesenior professionals have completed more than 1,000 corporate financeengagements, resulting in deep experience across a broad set of industries and typesof transactions. In addition, the firm manages C&B Capital, three growth equity fundswith over $82 million under management.

CONTACT US

Frank H. “Bo” Briggs, IIIManaging [email protected](404) 841-0639

Edward S. Croft, IIIManaging [email protected](404) 841-0055

R. Neale FisherManaging [email protected](404) 574-2906

Ronald B. GoldmanManaging [email protected](404) 841-0735

Steve B. TyeManaging [email protected](404) 841-9351

Erik M. ZalenskiManaging [email protected](404) 841-9826

Kyle C. [email protected](404) 574-2897

Matthew A. VealVice [email protected](404) 841-0056

Christian GivenDirector of Business [email protected](404) 328-4837

4401 Northside Parkway Suite 395 Atlanta, Georgia 30327 (404) 841-3131 www.croft-bender.com Member SIPC and FINRA 2

REPRESENTATIVE TRANSACTIONS

BUSINESS SERVICES TECHNOLOGY INDUSTRIAL HEALTHCARE CONSUMER

has been acquired by

VNS is a leading supplier and manufacturer of building products.

HRI is a leading franchisor of in-home consumer services.

has soldHarris Research, Inc.

Franchisor of

to

has been recapitalized by

has been acquired by

Coverall is a leading franchisor of commercial cleaning services.

Secretariat is a leading provider of dispute resolution advisory services to

public and private sector clients across the world.

has been recapitalized by

has been recapitalized by

ML Healthcare provides financing and access to care for patients unable to

afford medical services.

3

HCSC is a leading provider of hospice and palliative care services

in the Southeast.

has been recapitalized by

Carousel Designs is a leading online provider of original and custom-

designed baby bedding, fabric and nursery décor.

has been acquired by

Mudlick Mail provides data-driven, direct mail and related marketing

solutions to small and medium-sized businesses.

has been recapitalized by

The Erosion Company provides erosion control and related site services

to the construction industry.

Dominion Youth Services a leading provider of behavioral and mental

health support services to the youth and adolescent market.

has been acquired by

Service Brands is a leading multi-concept residential services franchisor.

has been acquired by

Nuesoft Technologies is a leading provider of SaaS solutions and RCM services for the healthcare industry.

has been acquired by

Lexington Manufacturing is a leading provider of engineered components to window and door OEMs in the United

States and internationally.

has been acquired by

has merged with

a portfolio company of

ControlScan is a leading provider of security and compliance solutions.

ASP is the leading swimming pool cleaning franchisor in the U.S.

has been acquired by

a portfolio company of

Merit is the leading distributor of paint sundries and flooring products and

installation supplies.

has been acquired by

a portfolio company of

4th Source is a leading provider of nearshore software development and IT

services to sophisticated clients with complex technology requirements.

has been acquired by

AN GLOBAL

Gro Solutions provides a digital sales platform for financial institutions.

has been acquired by

SIP.US is a leading provider of on-demand, enterprise-class IP

communications software solutions.

has been acquired by

a portfolio company of

IDology is a leading provider of identity verification and fraud prevention

services.

has acquired

FEATURED TRANSACTIONS

4

DEAL OVERVIEW

COMPANY OVERVIEW Headquartered in Chester, UK, GB Group is a $1.4 billion, publicly-traded

company that is a leading data intelligence specialist

The Company can quickly validate and verify the identity and location of4.4 billion people globally and accesses a breadth of data from over 200global partners to establish trust between businesses and theircustomers

Headquartered in Atlanta, Georgia, IDology is a fast-growing provider ofidentity verification services that helps remove friction both inonboarding customers and in the detection of fraud

GB Group had been impressed with Croft & Bender’s approach on theother side of another process

GB Group engaged Croft & Bender to advise the Company on its strategyand approach in acquiring IDology

Croft & Bender worked with the Company to analyze the market andadvise on bidding strategy, which resulted in successfully securing aLetter of Intent

Croft & Bender supported the Company throughout confirmatorydiligence, including negotiating the final definitive documentation

Croft & Bender successfully advised on the $300 million acquisition ofIDology by GB Group

DEAL OVERVIEW

COMPANY OVERVIEW Hospice Care of South Carolina is a leading provider of hospice and

palliative care services

Hospice Care of South Carolina provides all four levels of hospice care, asdefined by Medicare, as well as pediatric and adult palliative care

The Company employs highly trained, certified and dedicatedprofessionals providing evidence-based care through home-, facility-,clinic- and hospital-based settings

Croft & Bender was engaged to help the Company evaluate strategicalternatives, including a majority recapitalization or strategic sale of thebusiness

Croft & Bender worked with the Company to build a financial model,develop marketing materials, conduct management presentations,manage the diligence process and negotiate with buyers

Croft & Bender ran a competitive process that included a broad group ofpotential strategic and financial buyers

Croft & Bender successfully negotiated a recapitalization with The VistriaGroup, LP

HCSC is a leading provider of hospice and palliative care services

in the Southeast.

has been recapitalized by

IDology is a leading provider of identity verification and fraud prevention services.

has acquired

Note: Middle-market transactions are defined as those with a disclosed transaction value of less than $1 billion.

Public Equity Markets Middle Market Deal Volume

($ in billions)

Cash on Corporate Balance Sheets

($ in trillions)

Private Equity Dry Powder

($ in billions)

KEY CAPITAL MARKETS DATA

5

US PE EBITDA Multiples US PE Leverage Multiples

$672 $683$745

$829

$1,029

$1,194

$1,540

'13 '14 '15 '16 '17 '18 Q2 '19

$5.9 $6.0$5.7 $5.9

$6.3 $6.1 $6.2

'13 '14 '15 '16 '17 '18 Q2 '19

$327

$396 $385 $385 $380 $387

$193 $173

'13 '14 '15 '16 '17 '18 YTDQ2 '18

YTDQ2 '19

10.1x

12.8x

9.8x10.5x

12.1x11.5x

12.4x

'13 '14 '15 '16 '17 '18 LTMQ2 '19

6.1x

7.2x

5.4x 5.2x

6.2x5.8x 5.8x

'13 '14 '15 '16 '17 '18 LTMQ2 '19

(20.0%)

0.0%

20.0%

40.0%

60.0%

80.0%

6/16 12/16 6/17 12/17 6/18 12/18 6/19

S&P 500 NASDAQ Dow Jones

40.2%48.4%

65.3%

(1) Indexed relative to 2012.(2) Indexed relative to 1985.

Unemployment RateConsumer Confidence(2)

Real GDP Growth Industrial Production(1)

Retail Sales

($ in billions)

Consumer Spending

($ in trillions)

KEY ECONOMIC DATA

6

0.0%

1.0%

2.0%

3.0%

4.0%

Q1 Q2 Q3 Q4 Q1 Q2 Q3 Q4 Q1 Q2 Q3 Q4 Q1 Q2 Q3 Q4 Q1 Q2

'15 '16 '17 '18 '19

100

102

104

106

108

110

112

Q1 Q2 Q3 Q4 Q1 Q2 Q3 Q4 Q1 Q2 Q3 Q4 Q1 Q2 Q3 Q4 Q1 Q2

'15 '16 '17 '18 '19

70

80

90

100

110

120

130

140

Q1 Q2 Q3 Q4 Q1 Q2 Q3 Q4 Q1 Q2 Q3 Q4 Q1 Q2 Q3 Q4 Q1 Q2

'15 '16 '17 '18 '19

3.0%

3.5%

4.0%

4.5%

5.0%

5.5%

6.0%

Q1 Q2 Q3 Q4 Q1 Q2 Q3 Q4 Q1 Q2 Q3 Q4 Q1 Q2 Q3 Q4 Q1 Q2

'15 '16 '17 '18 '19

$1,000

$1,100

$1,200

$1,300

$1,400

Q1 Q2 Q3 Q4 Q1 Q2 Q3 Q4 Q1 Q2 Q3 Q4 Q1 Q2 Q3 Q4 Q1 Q2

'15 '16 '17 '18 '19

$10

$11

$12

$13

$14

$15

Q1 Q2 Q3 Q4 Q1 Q2 Q3 Q4 Q1 Q2 Q3 Q4 Q1 Q2 Q3 Q4 Q1 Q2

'15 '16 '17 '18 '19

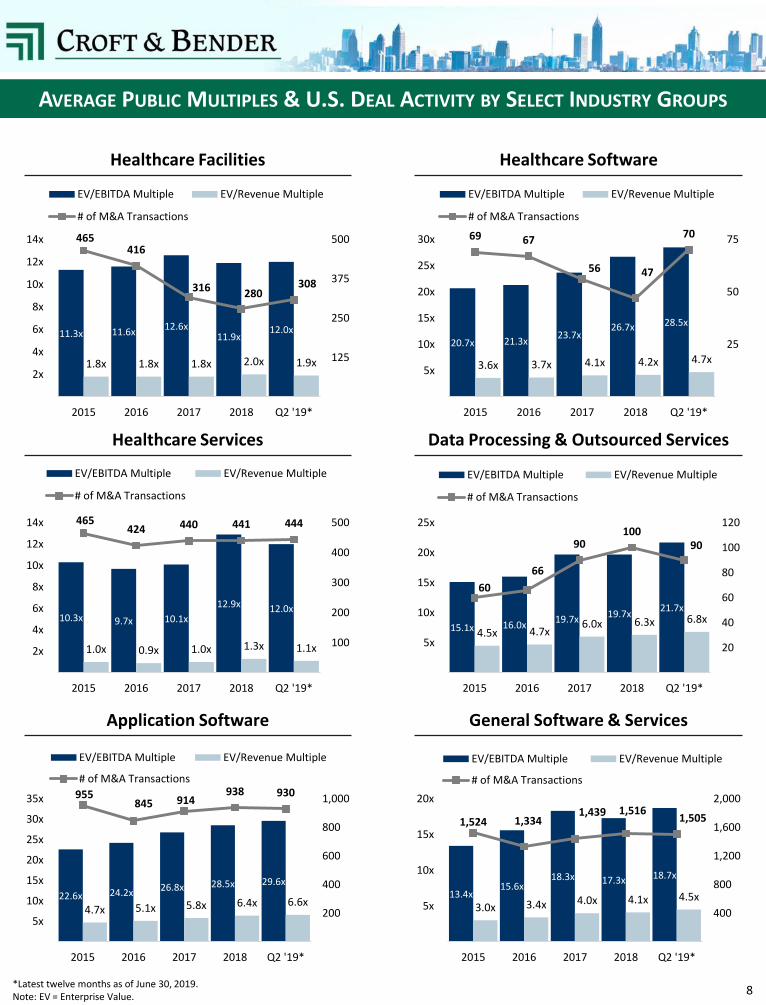

AVERAGE PUBLIC MULTIPLES & U.S. DEAL ACTIVITY BY SELECT INDUSTRY GROUPS

*Latest twelve months as of June 30, 2019.Note: EV = Enterprise Value.

General Industrial IT Consulting & Other Services

Building Products Trading Companies & Distributors

Consumer ServicesRetailing

7

9.9x 11.3x 11.2x

10.3x 10.5x

1.3x 1.4x 1.4x 1.3x 1.3x

2,433

2,167 2,220

2,4192,594

500

1,000

1,500

2,000

2,500

3,000

2x

4x

6x

8x

10x

12x

2015 2016 2017 2018 Q2 '19*

EV/EBITDA Multiple EV/Revenue Multiple

# of M&A Transactions

10.5x 11.5x

12.7x 11.2x 11.9x

1.6x 1.7x 1.8x 1.7x 1.8x

339

269 284

314 314

50

100

150

200

250

300

350

400

2x

4x

6x

8x

10x

12x

14x

2015 2016 2017 2018 Q2 '19*

EV/EBITDA Multiple EV/Revenue Multiple

# of M&A Transactions

9.7x

11.1x 10.8x 9.4x 10.0x

1.2x 1.4x 1.4x 1.2x 1.3x

55

62 63

8982

20

40

60

80

100

2x

4x

6x

8x

10x

12x

2015 2016 2017 2018 Q2 '19*

EV/EBITDA Multiple EV/Revenue Multiple

# of M&A Transactions

11.8x 13.8x

11.3x 9.9x 9.7x

0.8x 0.8x 0.8x 0.7x 0.7x

320

285 256

319

366

50

100

150

200

250

300

350

400

2x

4x

6x

8x

10x

12x

14x

16x

2015 2016 2017 2018 Q2 '19*

EV/EBITDA Multiple EV/Revenue Multiple

# of M&A Transactions

13.3x 14.1x 16.2x

15.0x

15.5x

1.3x 1.3x 1.5x 1.4x 1.5x

602498

374409

453

100

200

300

400

500

600

700

5x

10x

15x

20x

2015 2016 2017 2018 Q2 '19*

EV/EBITDA Multiple EV/Revenue Multiple

# of M&A Transactions

12.4x 12.9x 13.9x 13.0x 13.5x

2.4x 2.6x 2.8x 2.6x 2.7x

1,059

923

829

916 919

200

400

600

800

1,000

1,200

2x

4x

6x

8x

10x

12x

14x

16x

2015 2016 2017 2018 Q2 '19*

EV/EBITDA Multiple EV/Revenue Multiple

# of M&A Transactions

AVERAGE PUBLIC MULTIPLES & U.S. DEAL ACTIVITY BY SELECT INDUSTRY GROUPS

Healthcare Facilities Healthcare Software

Healthcare Services Data Processing & Outsourced Services

General Software & ServicesApplication Software

*Latest twelve months as of June 30, 2019.Note: EV = Enterprise Value.

8

11.3x 11.6x 12.6x

11.9x 12.0x

1.8x 1.8x 1.8x 2.0x 1.9x

465416

316 280308

125

250

375

500

2x

4x

6x

8x

10x

12x

14x

2015 2016 2017 2018 Q2 '19*

EV/EBITDA Multiple EV/Revenue Multiple

# of M&A Transactions

20.7x 21.3x 23.7x

26.7x 28.5x

3.6x 3.7x 4.1x 4.2x 4.7x

69 67

56 47

70

25

50

75

5x

10x

15x

20x

25x

30x

2015 2016 2017 2018 Q2 '19*

EV/EBITDA Multiple EV/Revenue Multiple

# of M&A Transactions

10.3x 9.7x 10.1x

12.9x 12.0x

1.0x 0.9x 1.0x 1.3x 1.1x

465424 440 441 444

100

200

300

400

500

2x

4x

6x

8x

10x

12x

14x

2015 2016 2017 2018 Q2 '19*

EV/EBITDA Multiple EV/Revenue Multiple

# of M&A Transactions

15.1x 16.0x 19.7x 19.7x

21.7x

4.5x 4.7x 6.0x 6.3x 6.8x

60

66

90100

90

20

40

60

80

100

120

5x

10x

15x

20x

25x

2015 2016 2017 2018 Q2 '19*

EV/EBITDA Multiple EV/Revenue Multiple

# of M&A Transactions

22.6x 24.2x 26.8x 28.5x 29.6x

4.7x 5.1x 5.8x 6.4x 6.6x

955845 914

938 930

200

400

600

800

1,000

5x

10x

15x

20x

25x

30x

35x

2015 2016 2017 2018 Q2 '19*

EV/EBITDA Multiple EV/Revenue Multiple

# of M&A Transactions

13.4x 15.6x

18.3x 17.3x 18.7x

3.0x 3.4x 4.0x 4.1x 4.5x

1,524 1,3341,439 1,516

1,505

400

800

1,200

1,600

2,000

5x

10x

15x

20x

2015 2016 2017 2018 Q2 '19*

EV/EBITDA Multiple EV/Revenue Multiple

# of M&A Transactions

Median VC Round Size by Stage

($ in millions)

U.S. VC Activity by Year

U.S. Growth Equity Activity by Year U.S. Growth Equity Deal Size Metrics

($ in millions)

U.S. Private Equity Deals by Deal Size

(# of deals)

U.S. Private Equity Activity by Year

PRIVATE CAPITAL DATA

9

$3

37

$3

79

$4

39

$5

31

$5

62

$6

05

$6

18

$7

27

$2

61

3,1793,559

3,440

4,280 4,446 4,452 4,725

5,181

1,911

0

500

1,000

1,500

2,000

2,500

3,000

3,500

4,000

4,500

5,000

5,500

$0

$100

$200

$300

$400

$500

$600

$700

$800

'11 '12 '13 '14 '15 '16 '17 '18 YTDQ2 '19

Deal value ($B)

# of deals closed 2,183

1,209

1,295

0

500

1,000

1,500

2,000

2,500

'11 '12 '13 '14 '15 '16 '17 '18 YTDQ2 '19

Under $25M

$25M-$100M

$100M-$500M

$47.0 $50.0

$190.0

$203.0

$0

$50

$100

$150

$200

$250

'11 '12 '13 '14 '15 '16 '17 '18 YTDQ2 '19

Median deal size

Median pre-money valuation

$2

4

$2

3

$2

3

$4

1

$4

6

$3

9

$4

2

$6

9

$3

2

641 663 680

882978

852973

1,157

531

0

200

400

600

800

1,000

1,200

1,400

$0

$10

$20

$30

$40

$50

$60

$70

$80

'11 '12 '13 '14 '15 '16 '17 '18 YTDQ2 '19

Deal value ($B)

# of deals closed

$1.1 $1.1

$6.0 $6.5

$11.5

$10.3

$0

$2

$4

$6

$8

$10

$12

$14

'11 '12 '13 '14 '15 '16 '17 '18 YTDQ2 '19

Angel/Seed

Early VC

Later VC

$4

5

$4

1

$4

8

$7

2

$8

4

$7

7

$8

3

$1

37

$6

6

6,7747,881

9,343

10,596 10,839

9,364 9,8899,845

4,868

0

2,000

4,000

6,000

8,000

10,000

12,000

$0

$20

$40

$60

$80

$100

$120

$140

$160

'11 '12 '13 '14 '15 '16 '17 '18 YTDQ2 '19

Deal value ($B)

Deal count

692530457

Croft & Bender LP (www.croft-bender.com) is a leading middle market investment bank focused on the advisory needs of clients nationwide. The firmhas extensive industry knowledge, transaction expertise, and a commitment to its clients’ success. Croft & Bender LP provides sell-side and buy-sideadvisory, capital raising, and financial advisory.

Investment banking services are provided by Croft & Bender, a registered broker-dealer and member of FINRA and SIPC.

THIS REPORT MAY CONTAIN REFERENCES TO REGISTERED TRADEMARKS, SERVICE MARKS AND COPYRIGHTS OWNED BY THIRD-PARTY INFORMATIONPROVIDERS. NONE OF THE THIRD-PARTY INFORMATION PROVIDERS IS ENDORSING THE OFFERING OF, AND SHALL NOT IN ANY WAY BE DEEMED ANISSUER OR UNDERWRITER OF, THE SECURITIES, FINANCIAL INSTRUMENTS OR OTHER INVESTMENTS DISCUSSED IN THIS REPORT, AND SHALL NOT HAVEANY LIABILITY OR RESPONSIBILITY FOR ANY STATEMENTS MADE IN THE REPORT OR FOR ANY FINANCIAL STATEMENTS, FINANCIAL PROJECTIONS OROTHER FINANCIAL INFORMATION CONTAINED OR ATTACHED AS AN EXHIBIT TO THE REPORT. FOR MORE INFORMATION ABOUT THE MATERIALSPROVIDED BY SUCH THIRD PARTIES, PLEASE CONTACT US AT THE ADDRESSES OR NUMBERS AT THE BEGINNING OF THE REPORT.

The information and views contained in this report were prepared by Croft & Bender LP. It is not a research report, as such term is defined by applicablelaw and regulations, and is provided for informational purposes only. It is not to be construed as an offer to buy or sell or a solicitation of an offer to buyor sell any financial instruments or to participate in any particular trading strategy. The information contained herein is believed by Croft & Bender to bereliable, but Croft & Bender makes no representation as to the accuracy or completeness of such information. Transaction numbers include thosetransactions that closed during the year they appear under and the industry classification assigned to the target by S&P Capital IQ. Croft & Bender and/orits affiliates act as advisers or lenders to, have positions in and effect transactions in securities of companies mentioned herein and also may provide,may have provided, or may seek to provide investment banking services for those companies. In addition, Croft & Bender and/or its affiliates or theirrespective officers, directors and employees may hold long or short positions in the securities, options thereon or other related financial products ofcompanies discussed herein. Opinions, estimates and projections in this report constitute Croft & Bender’s judgment and are subject to change withoutnotice. The financial instruments discussed in this report may not be suitable for all investors, and investors must make their own investment decisionsusing their own independent advisors as they believe necessary and based upon their specific financial situations and investment objectives. Also, pastperformance is not necessarily indicative of future results. No part of this material may be copied or duplicated in any form or by any means, orredistributed, without Croft & Bender’s prior written consent. Sources of information include Dealogic, Pitchbook, Preqin, S&P Capital IQ, and the U.S.Department of Labor.

DISCLOSURES

10