q2 2016 dashboard - lmd – sri lanka business magazine · nielsen, sri lanka q2 2016 dashboard . 2...

TRANSCRIPT

Nielsen, Sri Lanka

Q2 2016 DASHBOARD

Co

pyr

igh

t ©

2012

Th

e N

iels

en C

om

pan

y. C

on

fid

enti

al a

nd

pro

pri

etar

y.

2

IMPRESSIONS!

It feels great to be in Sri Lanka! I have been here for little over a month now and feel that’s time enough for me to pen down my impressions about Sri Lanka and the opportunities and challenges ahead of us. Continuation of this quarterly document will aim to bring to you Nielsen’s perspective on latest happenings on the macro-economic front and its impact on business sentiments, consumer confidence and growth for the FMCG market. I hope you find this useful. Do write to me or talk to me for any questions or feedback you may have. Thanks

S h a r a n g P a n t Managing Director, Nielsen Sri Lanka [email protected] +94 779 521 600

Co

pyr

igh

t ©

2013

Th

e N

iels

en C

om

pan

y. C

on

fid

enti

al a

nd

pro

pri

etar

y.

3

GDP GROWTH SHOWED AN UPTICK IN Q1 Services continued to be the key driver of growth. Increase in contribution from Construction

Source: Dept. of Census and Statistics

56.7% 56.4%

30.2% 31.0%

8.3% 8.0% 4.8% 4.6%

Services IndustrialAgriculture Taxes less subsidies

GDP at Constant Prices

QUARTERLY GDP & CONTRIBIUTION BY SECTOR

LKR 1,979 Bn LKR 2,088 Bn

Q1-2015 Q1-2016

Co

ntr

ibu

tio

n t

o G

DP

by

Sect

or

Serv

ice

s In

du

stri

al

Agr

icu

ltu

re

SUB SECTOR WISE GROWTH % (+ SELECTED SUB SECTORS)

Co

pyr

igh

t ©

2013

Th

e N

iels

en C

om

pan

y. C

on

fid

enti

al a

nd

pro

pri

etar

y.

4

BUT ALARM BELLS CAME RINGING IN Q2… News that made headlines in Q2 2016

Source: www.ft.lk

Co

pyr

igh

t ©

2013

Th

e N

iels

en C

om

pan

y. C

on

fid

enti

al a

nd

pro

pri

etar

y.

5

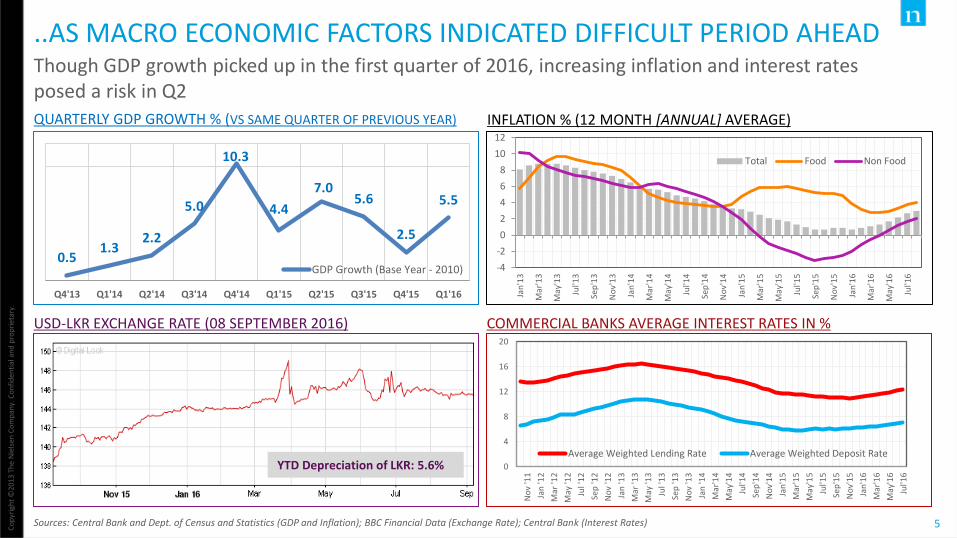

..AS MACRO ECONOMIC FACTORS INDICATED DIFFICULT PERIOD AHEAD Though GDP growth picked up in the first quarter of 2016, increasing inflation and interest rates posed a risk in Q2

Sources: Central Bank and Dept. of Census and Statistics (GDP and Inflation); BBC Financial Data (Exchange Rate); Central Bank (Interest Rates)

0

4

8

12

16

20

Jul'1

6

May

'16

Mar

'16

Jan

'16

No

v'15

Sep

'15

Jul'1

5

May

'15

Mar

'15

Jan

'15

No

v'14

Sep

'14

Jul'1

4

May

'14

Mar

'14

Jan

'14

No

v '1

3

Sep

'13

Jul '

13

May

'13

Mar

'13

Jan

'13

No

v '1

2

Sep

'12

Jul '

12

May

'12

Mar

'12

Jan

'12

No

v '1

1

Average Weighted Lending Rate Average Weighted Deposit Rate

-4

-2

0

2

4

6

8

10

12

Jan

'13

Mar

'13

May

'13

Jul'1

3

Sep

'13

No

v'13

Jan

'14

Mar

'14

May

'14

Jul'1

4

Sep

'14

No

v'14

Jan

'15

Mar

'15

May

'15

Jul'1

5

Sep

'15

No

v'15

Jan

'16

Mar

'16

May

'16

Jul'1

6

Total Food Non Food

0.5 1.3

2.2

5.0

10.3

4.4

7.0 5.6

2.5

5.5

Q4'13 Q1'14 Q2'14 Q3'14 Q4'14 Q1'15 Q2'15 Q3'15 Q4'15 Q1'16

GDP Growth (Base Year - 2010)

QUARTERLY GDP GROWTH % (VS SAME QUARTER OF PREVIOUS YEAR) INFLATION % (12 MONTH [ANNUAL] AVERAGE)

COMMERCIAL BANKS AVERAGE INTEREST RATES IN % USD-LKR EXCHANGE RATE (08 SEPTEMBER 2016)

YTD Depreciation of LKR: 5.6%

Co

pyr

igh

t ©

2013

Th

e N

iels

en C

om

pan

y. C

on

fid

enti

al a

nd

pro

pri

etar

y.

6

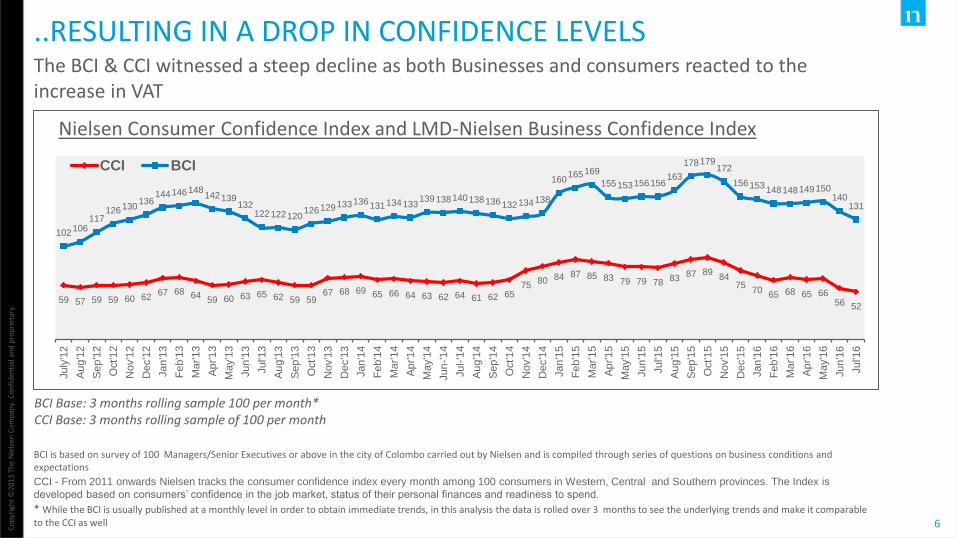

..RESULTING IN A DROP IN CONFIDENCE LEVELS The BCI & CCI witnessed a steep decline as both Businesses and consumers reacted to the increase in VAT

BCI is based on survey of 100 Managers/Senior Executives or above in the city of Colombo carried out by Nielsen and is compiled through series of questions on business conditions and expectations

CCI - From 2011 onwards Nielsen tracks the consumer confidence index every month among 100 consumers in Western, Central and Southern provinces. The Index is

developed based on consumers’ confidence in the job market, status of their personal finances and readiness to spend.

* While the BCI is usually published at a monthly level in order to obtain immediate trends, in this analysis the data is rolled over 3 months to see the underlying trends and make it comparable to the CCI as well

59 57 59 59 60 62 67 68 64

59 60 63 65 62 59 59 67 68 69 65 66 64 63 62 64 61 62 65

75 80 84 87 85 83 79 79 78 83 87 89

84 75

70 65 68 65 66

56 52

102 106 117

126 130 136

144 146 148 142 139

132 122 122 120

126 129 133 136 131 134 133 139 138 140 138 136 132 134 138

160 165 169

155 153 156 156 163

178 179 172

156 153 148 148 149 150

140 131

July

'12

Au

g'1

2

Se

p'1

2

Oct'1

2

Nov'1

2

Dec'1

2

Jan

'13

Fe

b'1

3

Ma

r'13

Ap

r'1

3

Ma

y'1

3

Jun

'13

Jul'1

3

Au

g'1

3

Se

p'1

3

Oct'1

3

Nov'1

3

Dec'1

3

Jan

'14

Fe

b'1

4

Ma

r'14

Ap

r'1

4

Ma

y'1

4

Jun

-'1

4

Jul-'1

4

Au

g'1

4

Se

p'1

4

Oct'1

4

Nov'1

4

Dec'1

4

Jan

'15

Fe

b'1

5

Ma

r'15

Ap

r'1

5

Ma

y'1

5

Jun

'15

Jul'1

5

Au

g'1

5

Se

p'1

5

Oct'1

5

Nov'1

5

Dec'1

5

Jan

'16

Fe

b'1

6

Ma

r'16

Ap

r'1

6

Ma

y'1

6

Jun

'16

Jul'1

6

CCI BCI

Nielsen Consumer Confidence Index and LMD-Nielsen Business Confidence Index

BCI Base: 3 months rolling sample 100 per month* CCI Base: 3 months rolling sample of 100 per month

Co

pyr

igh

t ©

2013

Th

e N

iels

en C

om

pan

y. C

on

fid

enti

al a

nd

pro

pri

etar

y.

7

HIGHER TAXES LED TO CONCERNS ON REGULAR SPENDS Spends on Children’s education, Health, Utilities worried consumers

Source: The Nielsen Company Consumer Confidence Report, Frequency: Quarterly; Base : All respondents n=300 per quarter

52

40

7

3

16

8

10

14

39

37

12

11

25

13

17

13

37

51

9

13

21

11

13

9

The economy

Children's education and / or welfare

Increasing food prices

Increasing utility bills

Health

Work / Life balance

Job Security

Political Stability

Q2 2015

Q1 2016

Q2 2016

Co

pyr

igh

t ©

2013

Th

e N

iels

en C

om

pan

y. C

on

fid

enti

al a

nd

pro

pri

etar

y.

8

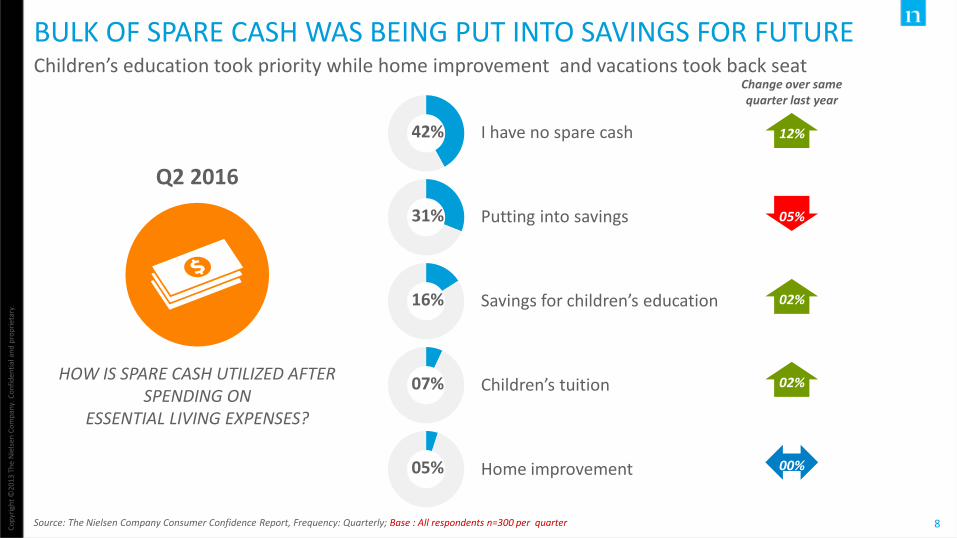

BULK OF SPARE CASH WAS BEING PUT INTO SAVINGS FOR FUTURE Children’s education took priority while home improvement and vacations took back seat

Source: The Nielsen Company Consumer Confidence Report, Frequency: Quarterly; Base : All respondents n=300 per quarter

42%

31%

16%

07%

05%

HOW IS SPARE CASH UTILIZED AFTER SPENDING ON

ESSENTIAL LIVING EXPENSES?

I have no spare cash

Putting into savings

Savings for children’s education

Children’s tuition

Home improvement

Q2 2016

Change over same quarter last year

12%

05%

02%

02%

00%

Co

pyr

igh

t ©

2013

Th

e N

iels

en C

om

pan

y. C

on

fid

enti

al a

nd

pro

pri

etar

y.

9

FMCG CONSUMPTION GROWTH DROPPED AS INFLATION MOVED UP Consistent low inflation helped consumption grow almost in double digits, but dropped in latest quarter. Marginal revival for Household Care products was seen

Source: Nielsen Sri Lanka, RMS Data, for All FMCG (Tracked Categories + Soft Drinks), from General Trade excluding NP, June 2016

6%

4% 1% -1% -1% 0% 1% 2%

8%

8%

9% 9% 7% 8%

11% 5%

14% 12%

10% 8%

6% 8%

13%

7%

Q3 14 Q4 14 Q1 15 Q2 15 Q3 15 Q4 15 Q1 16 Q2 16

Volume change component Price change component Overall growth

Value Growth for Super Categories

Food & Beverages 14% 14% 11% 7% 6% 8% 12% 7% Household Care 5% 3% 1% 2% 2% 4% 7% 5% Personal Care 14% 7% 8% 11% 8% 10% 15% 7% OTC Products 12% 12% 13% 11% 8% 8% 6% 3%

Total FMCG, Value Growth Trend

Co

pyr

igh

t ©

2013

Th

e N

iels

en C

om

pan

y. C

on

fid

enti

al a

nd

pro

pri

etar

y.

10

FMCG GROWTH HALVED IN BOTH URBAN AND RURAL Growth in Rural Sri Lanka, that was faster earlier, has come down over period

Source: Nielsen Sri Lanka, RMS Data, for All FMCG (Tracked Categories + Soft Drinks), from General Trade excluding NP, June 2016

Urban and Rural Value growth % over same quarter last year

12

7

4

6 6

9

16

8

14 14

13 8

6

8

10

6

Q3 14 Q4 14 Q1 15 Q2 15 Q3 15 Q4 15 Q1 16 Q2 16

Urban Rural

Co

pyr

igh

t ©

2013

Th

e N

iels

en C

om

pan

y. C

on

fid

enti

al a

nd

pro

pri

etar

y.

11

THOUGH IN LONG TERM, RETAIL ATTRACTIVENESS HAS IMPROVED The rank in AT Kearney GRDI has improved over the last three years

Source: Global Retail Development Index, AT Kearney analysis 2016

18

14

12

2015

2016

2014

Sri Lanka Ranking

Co

pyr

igh

t ©

2013

Th

e N

iels

en C

om

pan

y. C

on

fid

enti

al a

nd

pro

pri

etar

y.

12

KEY HIGHLIGHTS

Economic growth picked up in Q1 2016, backed by a strong performance of the Construction sector. However, floods, inconsistent taxes, on set of inflation and increasing bank rates could pull back growth again in Q2 2016.

Immediate impact was seen in Business Confidence as well Consumer Confidence levels that dropped to a new low. Businesses have become vary on investments in the short term as consumers focus on savings rather than discretionary spends.

While in the longer run Sri Lanka improved its attractiveness for the Retail Sector, FMCG growth saw a pull back mainly on account of drop in both supply and consumer demand. Consumers may be watchful in their spending given the increasing inflationary pressure and the price hikes resulting from tax adjustments.