pwc’s insurance insightsunit-linked insurance plans history of unit-linked insurance plans (ulip)...

TRANSCRIPT

PwC’s Insurance InsightsAnalysis of regulatory changes and impact assessment for May 2018

2 PwC PwC’s Insurance Insights

PrefaceLatest technology

disruption and its influence on insurance sector

Current trends in unit-linked insurance plans

Key guidelines issued by the Authority in May 2018 Contacts

During FY2017-18, there has been an increase in the amount of premiums that have been collected, particularly from private life insurance companies. Presented below are few key points regarding general and life insurance sectors:

• During April 2018, LIC’s market share remains unchanged at 69% of the life insurance market in India.

• Over FY 2017-18, there has been a significant shift in favour of private life insurance companies. In April 2017 private life insurance companies collected 2,562 crores INR as premium and has increased to 2,924 crores INR for April 2018.

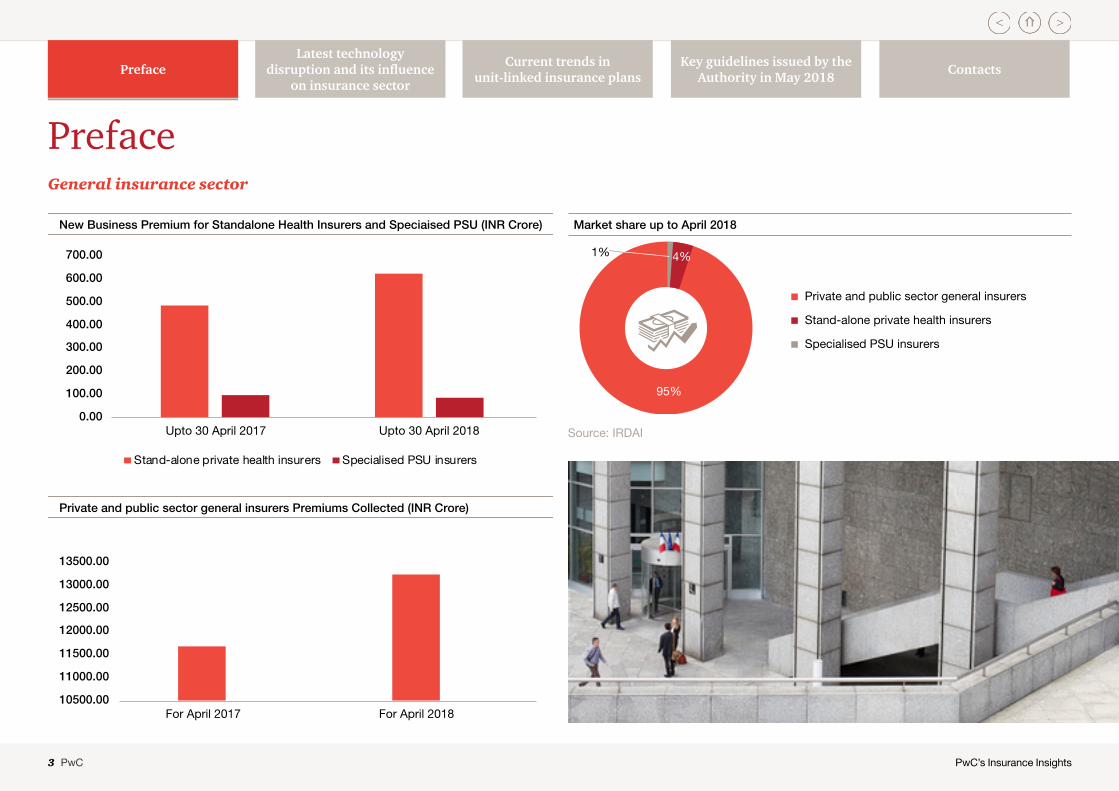

• In the general insurance category, although the market is dominated by public and private sector insurers, standalone private health insurers have had a 29% increase in the amount of premiums collected for FY2018. In April 2017, the premium collected was 474 crores INR, which increased to 612 crores INR in April 2018. However specialised PSU insurers have had a 15% decline in premium collected—from 88 crores INR in April 2017 to 74 crores INR in April 2018.

Source: IRDAI

Preface

Premium in crore (INR)

0

20000

40000

60000

80000

100000

120000

140000

Upto April 2017 Upto April 2018

Private life insurers LIC

160000

180000

Market share up to March 2018

Private life insurers

LIC

31%

69%

Life insurance sector

Preface

3 PwC PwC’s Insurance Insights

PrefaceLatest technology

disruption and its influence on insurance sector

Current trends in unit-linked insurance plans

Key guidelines issued by the Authority in May 2018 Contacts

General insurance sector

Preface

New Business Premium for Standalone Health Insurers and Speciaised PSU (INR Crore)

0.00

100.00

200.00

300.00

400.00

500.00

600.00

700.00

Upto 30 April 2017 Upto 30 April 2018

Stand-alone private health insurers Specialised PSU insurers

Private and public sector general insurers Premiums Collected (INR Crore)

10500.00

11000.00

11500.00

12000.00

12500.00

13000.00

13500.00

For April 2017 For April 2018

Market share up to April 2018

Private and public sector general insurers

Stand-alone private health insurers

Specialised PSU insurers

4%1%

95%

Source: IRDAI

Preface

4 PwC PwC’s Insurance Insights

PrefaceLatest technology

disruption and its influence on insurance sector

Current trends in unit-linked insurance plans

Key guidelines issued by the Authority in May 2018 Contacts

Latest technology disruption and its influence on insurance sector

Latest technology disruption and its influence

on insurance sector

Blockchain

In today’s digital era, technology and digitalisation are playing a major role in shaping people’s lives and their decision making. Improvement in technology has played a paramount role in solving societal issues. Simple examples such as the usage of batteries and microchips being used in medical research are all cases of the positive impact of technology. One such application is Blockchain, which was dubbed as a potential ‘beating heart’ of the global financial system in a report released by the World Economic Forum in 2016. According to the report, it is predicted that Blockchain will account for 10% of GDP at a global level by 2027.

A Blockchain is a peer-to-peer distributed ledger that is cryptographically secure, append-only, immutable, and updatable only via consensus or agreement among peers.

There is a significant opportunity that has arisen for insurance companies to implement Blockchain to solve major problems that are affecting the entire industry. Blockchain can be applied in different areas. For example in the case of mandatory Third Party Insurance in motor insurance. According to the Motor Vehicles Act, 1988 third party insurance is mandatory. Road transport authorities, insurers and car manufacturers, can create a chain wherein motor vehicles can be monitored whether every vehicle is insured through third party insurers. This will ensure that no vehicles on road are operating without insurance and will also reduce cases of fake insurance policies held by vehicle owners/drivers to effectively operate vehicles on road.

5 PwC PwC’s Insurance Insights

PrefaceLatest technology

disruption and its influence on insurance sector

Current trends in unit-linked insurance plans

Key guidelines issued by the Authority in May 2018 Contacts

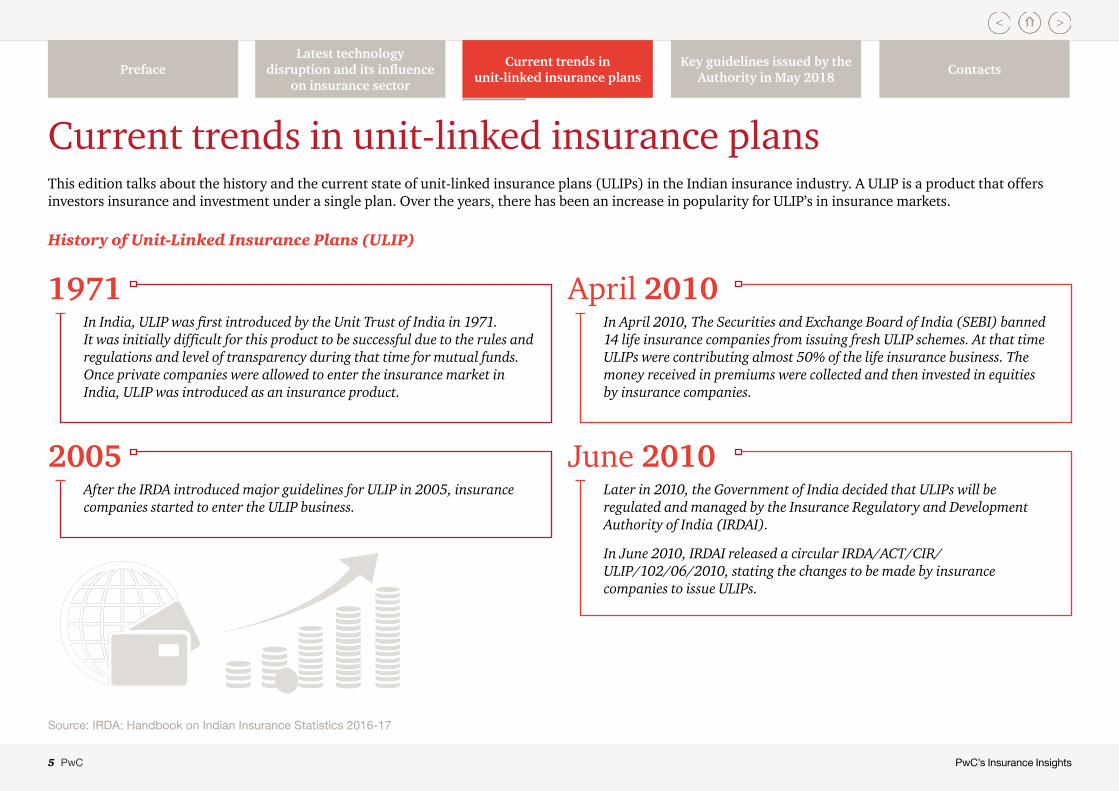

Current trends in unit-linked insurance plansThis edition talks about the history and the current state of unit-linked insurance plans (ULIPs) in the Indian insurance industry. A ULIP is a product that offers investors insurance and investment under a single plan. Over the years, there has been an increase in popularity for ULIP’s in insurance markets.

Source: IRDA: Handbook on Indian Insurance Statistics 2016-17

Current trends in unit-linked insurance plans

History of Unit-Linked Insurance Plans (ULIP)

In India, ULIP was first introduced by the Unit Trust of India in 1971. It was initially difficult for this product to be successful due to the rules and regulations and level of transparency during that time for mutual funds. Once private companies were allowed to enter the insurance market in India, ULIP was introduced as an insurance product.

1971

After the IRDA introduced major guidelines for ULIP in 2005, insurance companies started to enter the ULIP business.

2005

In April 2010, The Securities and Exchange Board of India (SEBI) banned 14 life insurance companies from issuing fresh ULIP schemes. At that time ULIPs were contributing almost 50% of the life insurance business. The money received in premiums were collected and then invested in equities by insurance companies.

April 2010

Later in 2010, the Government of India decided that ULIPs will be regulated and managed by the Insurance Regulatory and Development Authority of India (IRDAI).

In June 2010, IRDAI released a circular IRDA/ACT/CIR/ULIP/102/06/2010, stating the changes to be made by insurance companies to issue ULIPs.

June 2010

6 PwC PwC’s Insurance Insights

PrefaceLatest technology

disruption and its influence on insurance sector

Current trends in unit-linked insurance plans

Key guidelines issued by the Authority in May 2018 Contacts

Current trends in unit-linked insurance plansBelow are given some of the changes suggested by IRDAI to issue ULIPs:

The lock-in period for all ULIPs will be increased to five years as against three years previously. During these five years there will be uniform premium payment; if there are to be any additional premiums these will have to be considered as single premiums and any charges will be distributed across the tenure. Another important change is that no partial withdrawals are allowed during the initial accumulation phase of premiums. In terms of returns, all ULIP pension or annuity products will offer a guaranteed minimum return of at least 4.5% or the rate as specified by the IRDA.

Importance of ULIPs

ULIPs have gained popularity over the last decade, among insurance companies and customers. There are many reasons for the following:

• Investors find ULIP an attractive option due to its lock-in feature. The lock-in period creates a habit of disciplined investment in customers.

• ULIPs have two important aspects: investors can avail life cover and an avenue for long-term investment. Investors will also be able to avail tax benefit every year till the end of the term for paying the premium.

• With customers required to pay a consolidated premium for investment option and life insurance cover, the premium includes a mortality charge, which customers do not need to separately pay for.

Current trends in unit-linked insurance plans

7 PwC PwC’s Insurance Insights

PrefaceLatest technology

disruption and its influence on insurance sector

Current trends in unit-linked insurance plans

Key guidelines issued by the Authority in May 2018 Contacts

Current trends in unit-linked insurance plansWay forward

For a unit-linked product to continue to be successful, insurers must ensure that they make it easy for the policyholder/prospect to access the information relevant to their investment decisions and which enables them to make comparisons with other providers. The sales literature must disclose all key elements, which are essential to enable the policyholder/prospect to make effective and informed choices.

It is also important to note that the level of information/disclosure should match customer needs. At the same time, an overload of information may prevent consumers from making an appropriate assessment of a product and therefore, just adding additional disclosures may not be the solution. Thus, under a unit-linked policy, the disclosures should give the customers’ confidence that their funds are managed fairly in line with their expectations so that they can take effective and informed decisions.

In India, over the last decade, there has been a significant increase in the total investments of life insurer’s funds comprising traditional and ULIP products. Particularly, in the case of ULIP funds, the investment amount has doubled since 2009.

ULIP Fund Investment (Rs. Crore)

0

50000

100000

150000

200000

250000

300000

ULIP Fund Investment (Rs Crore)

350000

400000

450000

2009 2010 2011 2012 2013 2014 2015 2016 2017

Source: IRDAI Annual Reports

Current trends in unit-linked insurance plans

8 PwC PwC’s Insurance Insights

PrefaceLatest technology

disruption and its influence on insurance sector

Current trends in unit-linked insurance plans

Key guidelines issued by the Authority in May 2018 Contacts

Ref. no.: IRDA/ACT/MISC/MISC/066/05/20181 Date of issue: 1 May 2018

This circular is in reference to the requests that IRDAI has received from insurers to avail services of empanelled actuaries. This is primarily required to value actuarial liabilities of insurers on a quarterly basis. In order to enhance the availability of actuaries from the panel and ease the process of utilising the services of such actuaries, the following changes have been made:

• In the case of general insurance, a panel actuary can be involved during any quarter of a financial year in the valuation of, maximum of:

a. One stand-alone health insurer b. One general insurer c. General insurance business of one reinsurer (including general insurance

business of a foreign reinsurer’s branch office)

• In the case of life insurance, a panel actuary can be involved during any quarter of a financial year in the valuation of, at the most, one life insurer and life insurance business of one reinsurer (including life insurance business of a foreign reinsurer’s branch office.

• All these conditions are also applicable to annual statutory actuarial valuation as at 31 March of any financial year being the last quarter of a financial year.

Key guidelines issued by the Authority in May 2018

Key guidelines issued by the Authority in May 2018

Panel of actuaries

Implication

In India, there is a shortage in number of actuaries as well as in the expertise of actuaries. Hence, in order for strong growth within the industry, the IRDAI has facilitated this arrangement of asking all insurance companies to be a part of this panel. By forming a panel of actuaries, this will lead to strong growth and enhanced skills within the insurance industry.

1 https://www.irdai.gov.in/ADMINCMS/cms/whatsNew_Layout.aspx?page=PageNo3464&flag=1

9 PwC PwC’s Insurance Insights

PrefaceLatest technology

disruption and its influence on insurance sector

Current trends in unit-linked insurance plans

Key guidelines issued by the Authority in May 2018 Contacts

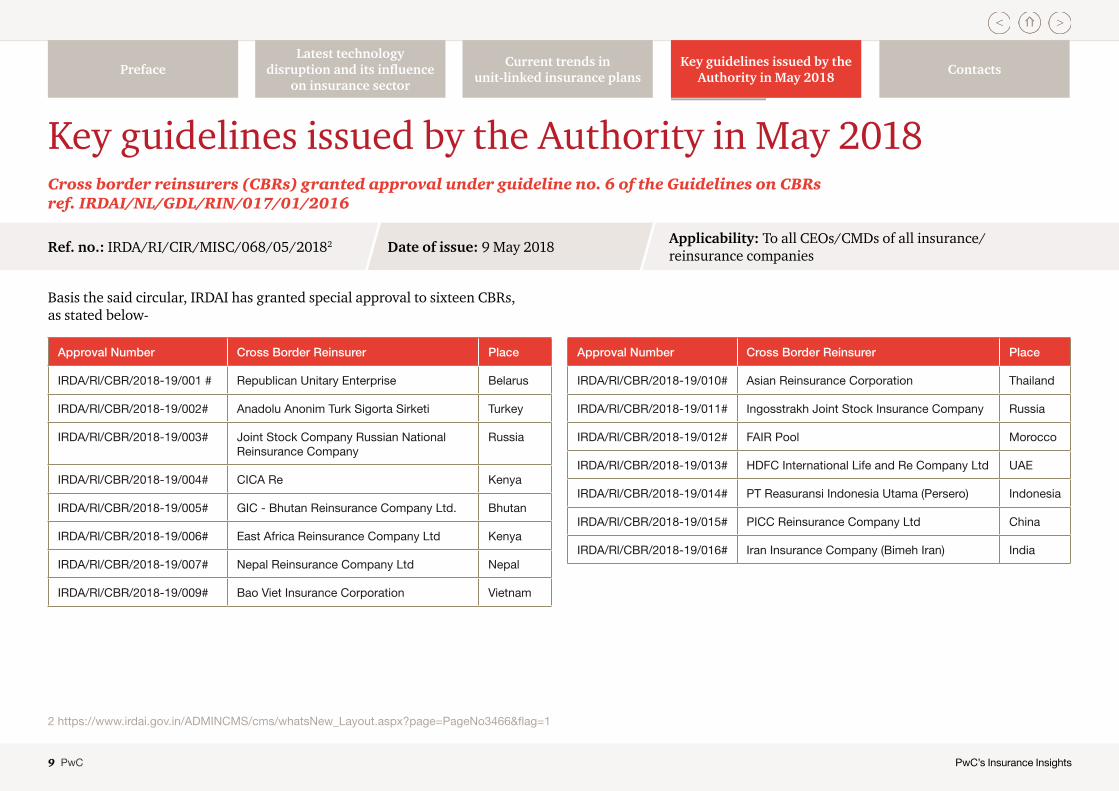

Ref. no.: IRDA/RI/CIR/MISC/068/05/20182 Date of issue: 9 May 2018 Applicability: To all CEOs/CMDs of all insurance/reinsurance companies

Basis the said circular, IRDAI has granted special approval to sixteen CBRs, as stated below-

Cross border reinsurers (CBRs) granted approval under guideline no. 6 of the Guidelines on CBRs ref. IRDAI/NL/GDL/RIN/017/01/2016

Approval Number Cross Border Reinsurer Place

IRDA/Rl/CBR/2018-19/001 # Republican Unitary Enterprise Belarus

IRDA/Rl/CBR/2018-19/002# Anadolu Anonim Turk Sigorta Sirketi Turkey

IRDA/Rl/CBR/2018-19/003# Joint Stock Company Russian National Reinsurance Company

Russia

IRDA/Rl/CBR/2018-19/004# CICA Re Kenya

IRDA/Rl/CBR/2018-19/005# GIC - Bhutan Reinsurance Company Ltd. Bhutan

IRDA/Rl/CBR/2018-19/006# East Africa Reinsurance Company Ltd Kenya

IRDA/Rl/CBR/2018-19/007# Nepal Reinsurance Company Ltd Nepal

IRDA/Rl/CBR/2018-19/009# Bao Viet Insurance Corporation Vietnam

Approval Number Cross Border Reinsurer Place

IRDA/Rl/CBR/2018-19/010# Asian Reinsurance Corporation Thailand

IRDA/Rl/CBR/2018-19/011# Ingosstrakh Joint Stock Insurance Company Russia

IRDA/Rl/CBR/2018-19/012# FAIR Pool Morocco

IRDA/Rl/CBR/2018-19/013# HDFC International Life and Re Company Ltd UAE

IRDA/Rl/CBR/2018-19/014# PT Reasuransi Indonesia Utama (Persero) Indonesia

IRDA/Rl/CBR/2018-19/015# PICC Reinsurance Company Ltd China

IRDA/Rl/CBR/2018-19/016# Iran Insurance Company (Bimeh Iran) India

2 https://www.irdai.gov.in/ADMINCMS/cms/whatsNew_Layout.aspx?page=PageNo3466&flag=1

Key guidelines issued by the Authority in May 2018

Key guidelines issued by the Authority in May 2018

10 PwC PwC’s Insurance Insights

PrefaceLatest technology

disruption and its influence on insurance sector

Current trends in unit-linked insurance plans

Key guidelines issued by the Authority in May 2018 Contacts

Ref. no.: IRDA/INT/CIR/CDB/082/05/2018 Date of issue: 30 May 2018 Applicability: To all Insurers and all Insurance Marketing Firms

With reference to circular IRDAI/INT/CIR/CDB/19708/2017 dated on 24 August 2017, all insurance intermediaries have been advised to upload details of qualified persons, specified persons and authorised verifiers on the database of Insurance Information Bureau of India.

Mandatory compliance

The following are the requirements:• Insurers are required to upload details of their individual agents.• Insurance marketing firms are required to upload details of their insurance

sales persons in the prescribed format.

Implication

This database is required for the purpose of better tracking and monitoring by the IRDAI. If, in case, there are circumstances whereby customers may complain in the future or have any issues with the sales persons, the regulator will be able to maintain better control and be able to undertake an analytical approach towards handling of these cases.

Constitution of central database of licensed insurance sales persons in India (ENVOY) at IIB- Phase II3

3 https://www.irdai.gov.in/ADMINCMS/cms/whatsNew_Layout.aspx?page=PageNo3475&flag=1

Key guidelines issued by the Authority in May 2018

Key guidelines issued by the Authority in May 2018

11 PwC PwC’s Insurance Insights

PrefaceLatest technology

disruption and its influence on insurance sector

Current trends in unit-linked insurance plans

Key guidelines issued by the Authority in May 2018 Contacts

4 https://www.irdai.gov.in/ADMINCMS/cms/whatsNew_Layout.aspx?page=PageNo3479&flag=1

Ref. no.: IRDA/ACT/CIR/SLM/090/05/20184 Date of issue: 31 May 2018 Applicability: CEOs/CMDs of all non-life insurance companies and registered Indian reinsurers including foreign reinsurance branch offices

• The circular is issued under the powers of subsection 2(e) of Section 14 of the IRDA Act.

• Reference is drawn to the provisions of Para 6 and Para 8 of the Circular No. IRDA/ACT/CIR/SLM/066/03/2017 dated 28 March 2017.

• The provisions of Para 6.3.1 will remain effective for one more year, that is, for the period up to 31 March 2019 and the situation will be reviewed accordingly.

• Other provisions of the aforesaid Circular will remain unaltered.• This circular will be effective from 1 April, 2018.

Paragraph 6 of the IRDA/ACT/CIR/SLM/066/03/2017 circular talks about concessions regarding the determination of solvency margin. Any premiums that were relating to any state or Central Government schemes should be placed with a value of zero. Crop insurance will now appear as a line item number 10 under line of business in Table 1 as under Schedule III of the regulations.

Solvency margin for crop insurance business

Key guidelines issued by the Authority in May 2018

Key guidelines issued by the Authority in May 2018

12 PwC PwC’s Insurance Insights

PrefaceLatest technology

disruption and its influence on insurance sector

Current trends in unit-linked insurance plans

Key guidelines issued by the Authority in May 2018 Contacts

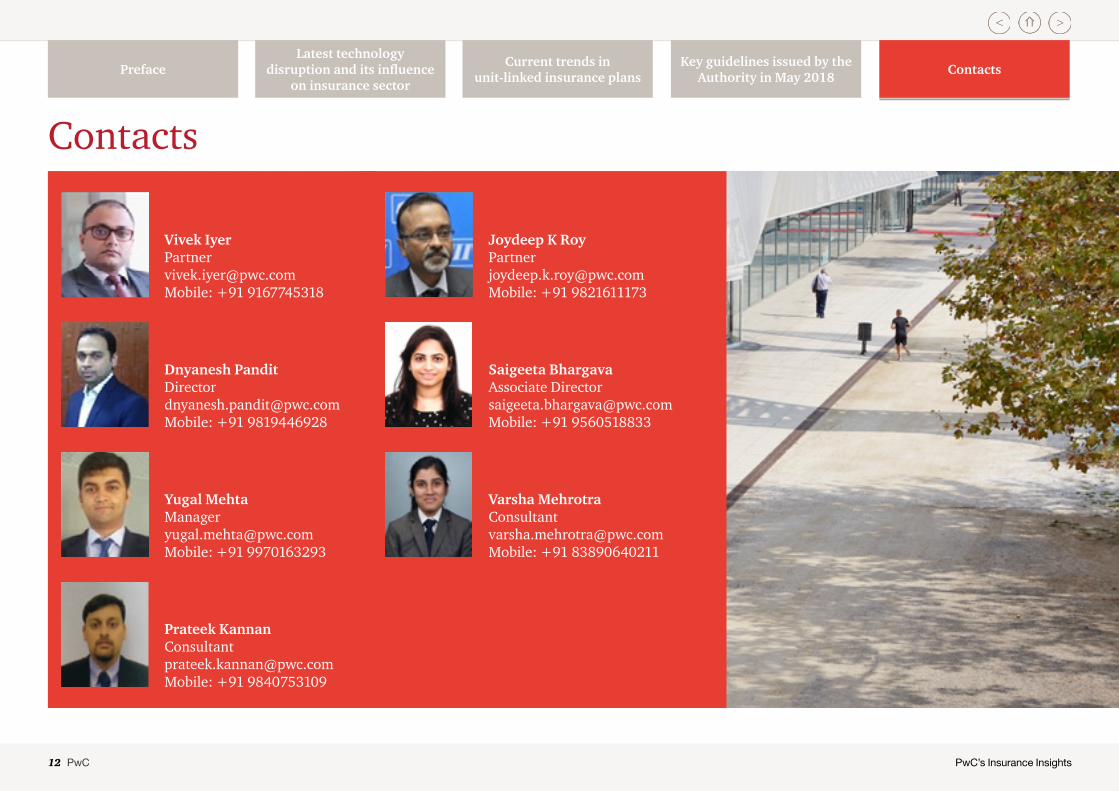

Vivek [email protected] Mobile: +91 9167745318

Joydeep K Roy Partner [email protected] Mobile: +91 9821611173

Dnyanesh Pandit Director [email protected] Mobile: +91 9819446928

Saigeeta Bhargava Associate Director [email protected] Mobile: +91 9560518833

Yugal Mehta Manager [email protected] Mobile: +91 9970163293

Varsha Mehrotra Consultant [email protected] Mobile: +91 83890640211

Prateek Kannan Consultant [email protected] Mobile: +91 9840753109

Contacts

Contacts

About PwCAt PwC, our purpose is to build trust in society and solve important problems. We’re a network of firms in 158 countries with more than 2,36,000 people who are committed to delivering quality in assurance, advisory and tax services. Find out more and tell us what matters to you by visiting us at www.pwc.com

In India, PwC has offices in these cities: Ahmedabad, Bengaluru, Chennai, Delhi NCR, Hyderabad, Kolkata, Mumbai and Pune. For more information about PwC India’s service offerings, visit www.pwc.com/in

PwC refers to the PwC International network and/or one or more of its member firms, each of which is a separate, independent and distinct legal entity. Please see www.pwc.com/structure for further details.

© 2018 PwC. All rights reserved

pwc.inData Classification: DC0

This publication contains certain examples extracted from third party documentation and so being out of context from the original third party documents; readers should bear this in mind when reading the publication. The copyright in such third party material remains owned by the third parties concerned, and PwC expresses its appreciation to these companies for having allowed it to include their information in this publication. For a more comprehensive view on each company’s communication, please read the entire document from which the extracts have been taken. Please note that the inclusion of a company in this publication does not imply any endorsement of that company by PwC nor any verification of the accuracy of the information contained in any of the examples.

© 2018 PricewaterhouseCoopers Private Limited. All rights reserved. In this document, “PwC” refers to PricewaterhouseCoopers Private Limited (a limited liability company in India having Corporate Identity Number or CIN : U74140WB1983PTC036093), which is a member firm of PricewaterhouseCoopers International Limited (PwCIL), each member firm of which is a separate legal entity.

MJ/June 2018-13297