pwc / cb insights moneytree™ reportandhealth.com.au/wp-content/uploads/2019/04/cb-insights...pwc |...

TRANSCRIPT

PwC / CB Insights

MoneyTree™ ReportQ1 2019

PwC | CB Insights MoneyTree™ Report Q1 2019 2

Executive summaryUS VC funding and deal activity fell in Q1’19 from near-record levels in 2018

US VC funding and deal activity fell in Q1’19: US VC funding fell 36% in Q1’19 to $25B, with 4% fewer deals compared to Q4’18. Q4’18’s $39B and 2018’s $115B were the second largest quarter and year, respectively.

US mega-rounds were down from a record Q4’18, but well above historic levels: US private companies raised 46 $100M+ rounds in Q1’19, down from a record Q4’18 but well above historic levels.

Seed-stage deals continued to fall in Q1’19: Seed-stage deals as a percentage of total US deal activity continued to fall in Q1’19. Seed-stage deals began to decline starting in Q3’17, at 36% of all deals, falling to 24% in Q1’19.

Artificial Intelligence-related funding fell for the second-straight quarter: AI-related companies raised $2B in Q1’19, falling 22% compared to Q4’18, the second straight quarterly decline.

FinTech funding fell slightly after a record Q4’18: FinTech-related funding remained elevated at $3B in Q1’19, falling only 3% after a record Q4’18. Deal activity rose 13% in Q1’19, to 170 transactions.

Global funding fell 22% in Q1’19 after 2018 surge to near record levels

Global funding and deal activity fell in Q1’19: Funding fell by 22% to $52B, raised over 3,327 transactions. Deal activity fell by 5%.

Asian funding dropped off: Asia-based private companies raised $18B in Q1’19, a 12% decrease compared to Q4’18. Deal activity fell 7% to 1,128 transactions, the second-straight quarterly decrease.

North America minted 10 new unicorns: North America beat out Asia for the third-straight quarter in private companies newly valued at $1B+. NA saw 10 new $1B+ private company valuations, compared to 5 in Asia.

Silicon Valley funding fell amid declining deal activity: Silicon Valley fell by 19% to $4B, raised over 118 deals. Deal activity fell for the third straight quarter.

NY metro area funding jumped: NY metro-based VC backed companies raised $4.5B in Q1’19, a 110% increase compared to Q4’18. New York VC funding rounds included 6 mega-rounds, including one $1B round.

Note: Report includes all rounds to VC-backed companies. For a detailed brief on methodology, please reference page 94 of this report.

PwC | CB Insights MoneyTree™ Report Q1 2019

Table of contents

3

4 US Overall Trends

74 Global Trends

59 US Movers and Shakers

45 US Places

12 US Sector Activity

US Overall Trends01

4

5PwC | CB Insights MoneyTree™ Report Q3 2017

In Q1 2019

UNITED STATES

VC-backed companies raised

$24.6B

PwC | CB Insights MoneyTree™ Report Q1 2019 6

8-quarter US financing trendUS funding and deal activity decreased in Q1’19

• Funding was down 36% in Q1’19 as $24.6B was invested across 1,279 deals. Deal activity declined for the third consecutive quarter.

• US-based unicorns brought in noteworthy deals. Flexport, Nuro, and WeWork all raised $900M+ rounds in Q1’19.

$19.6 $20.8 $20.0 $22.8 $24.5 $28.9 $38.7 $24.6

1,4731,561

1,434 1,5241,639

1,4271,328 1,279

0

200

400

600

800

1,000

1,200

1,400

1,600

1,800

Q2'17 Q3'17 Q4'17 Q1'18 Q2'18 Q3'18 Q4'18 Q1'19

Title

Investments ($B) Deals

PwC | CB Insights MoneyTree™ Report Q1 2019 7

US financing trends

”

Over the past three quarters, we’ve seen the number of deals moderate down, while the total amount invested stays relatively consistent.

“

— Tom Ciccolella, Partner, US Ventures Leader at PwC

PwC | CB Insights MoneyTree™ Report Q1 2019 8

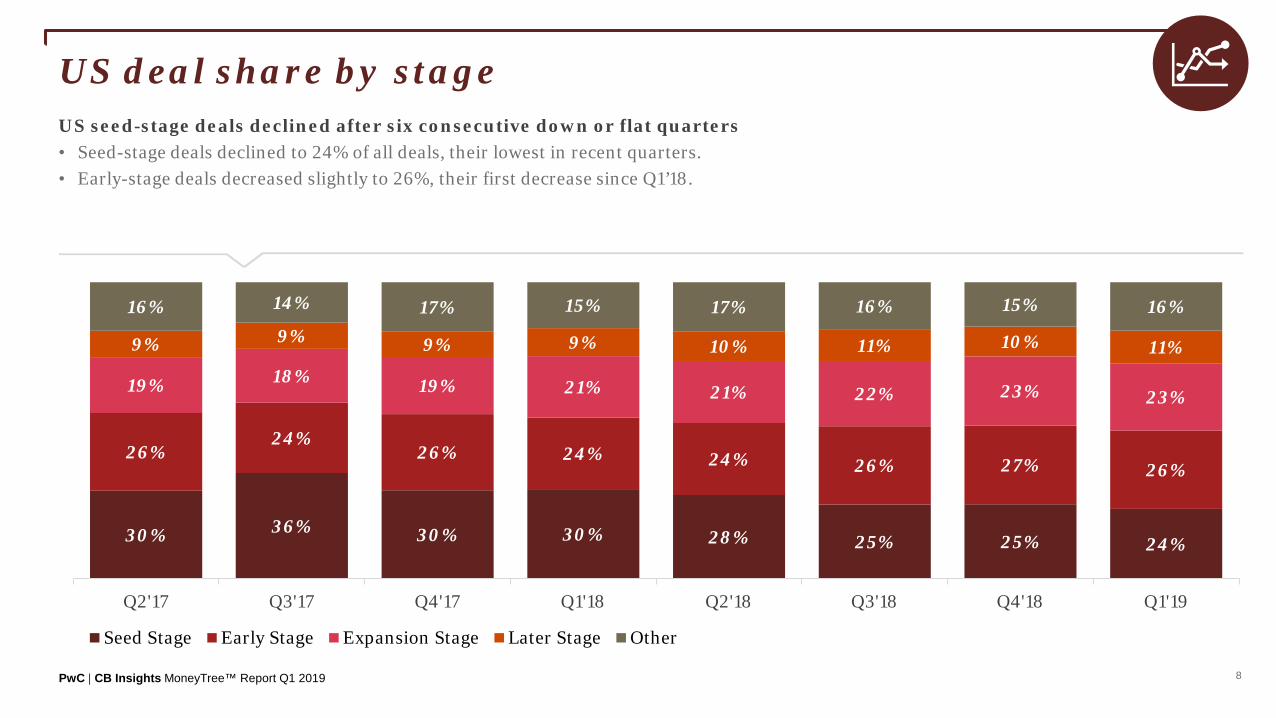

US deal share by stageUS seed-stage deals declined after six consecutive down or flat quarters• Seed-stage deals declined to 24% of all deals, their lowest in recent quarters.• Early-stage deals decreased slightly to 26%, their first decrease since Q1’18.

30% 36% 30% 30% 28% 25% 25% 24%

26%24%

26% 24% 24% 26% 27% 26%

19% 18% 19% 21% 21% 22% 23% 23%

9% 9% 9% 9% 10% 11% 10% 11%

16% 14% 17% 15% 17% 16% 15% 16%

Q2'17 Q3'17 Q4'17 Q1'18 Q2'18 Q3'18 Q4'18 Q1'19

Seed Stage Early Stage Expansion Stage Later Stage Other

PwC | CB Insights MoneyTree™ Report Q1 2019 9

Median US deal sizes by stageLater-stage median deal size increased for second consecutive quarter in Q1’19

• Median later-stage deal size increased to $40M in Q1’19, an $8M increase from Q3’18, while median deal size shrank to $32M.

• Expansion-stage median deal size was flat at $20M.

$1.7 $1.1 $2.0 $1.6 $2.0 $1.5 $2.1 $2.0$6.0 $6.0 $7.0 $7.0 $7.0 $6.5 $7.4 $7.0

$15.8 $15.5$18.0 $16.0 $15.5 $16.0

$20.0 $20.0

$36.2

$30.9

$25.0

$31.0

$44.0

$32.0

$37.5$40.0

Q2'17 Q3'17 Q4'17 Q1'18 Q2'18 Q3'18 Q4'18 Q1'19

Seed Stage Deal Size ($M) Early Stage Deal Size ($M) Expansion Stage Deal Size ($M) Later Stage Deal Size ($M)

PwC | CB Insights MoneyTree™ Report Q1 2019 10

US corporate deal participationCorporate participation in US deals increased to 30%, its highest level in recent quarters

• Corporate participation in US deals increased in Q1’19 to 30%, its highest level in recent quarters.

76% 77% 77% 76% 75% 73% 73% 70%

24% 23% 23% 24% 25% 27% 27% 30%

Q2'17 Q3'17 Q4'17 Q1'18 Q2'18 Q3'18 Q4'18 Q1'19Other Investors Corp / CVC Deal Participation

PwC | CB Insights MoneyTree™ Report Q1 2019 11

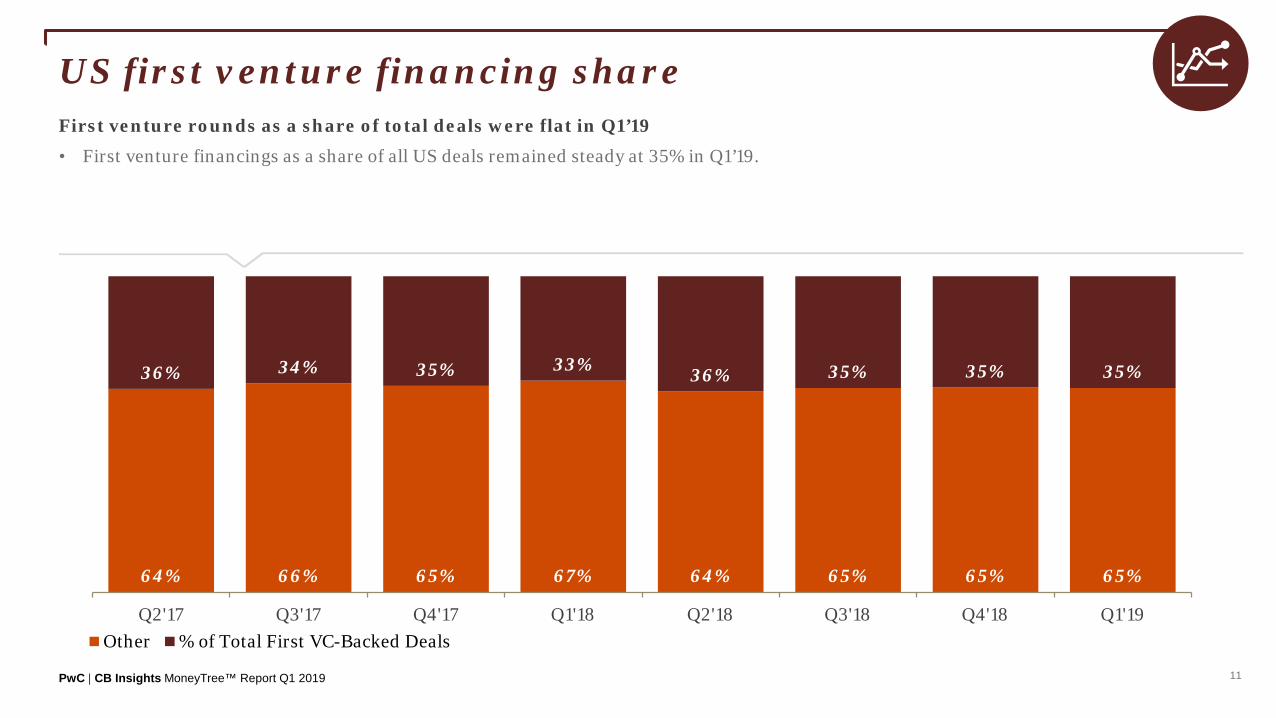

US first venture financing shareFirst venture rounds as a share of total deals were flat in Q1’19

• First venture financings as a share of all US deals remained steady at 35% in Q1’19.

64% 66% 65% 67% 64% 65% 65% 65%

36% 34% 35% 33% 36% 35% 35% 35%

Q2'17 Q3'17 Q4'17 Q1'18 Q2'18 Q3'18 Q4'18 Q1'19Other % of Total First VC-Backed Deals

US Sectors02

PwC | CB Insights MoneyTree™ Report Q1 2019

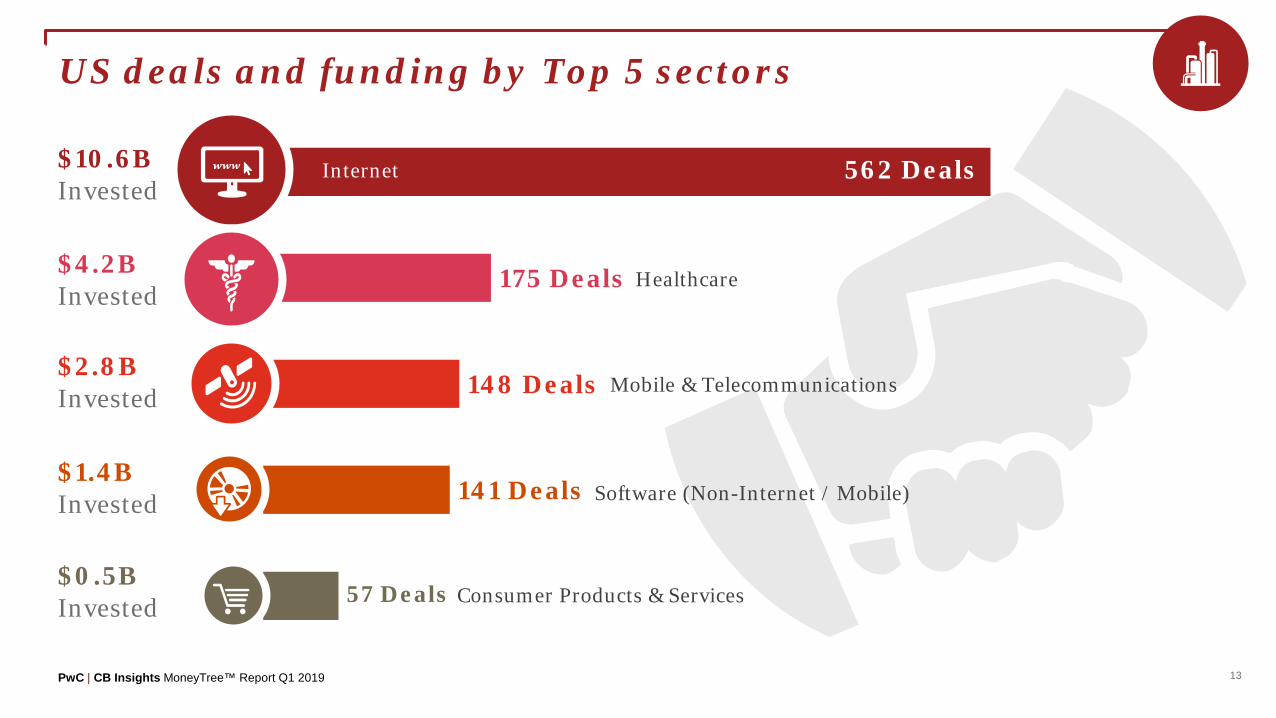

57 Deals

141 Deals

148 Deals

175 Deals

562 Deals

13

US deals and funding by Top 5 sectors

$10.6BInvested

$4.2BInvested

$2.8BInvested

$1.4BInvested

$0.5BInvested

Internet

Mobile & Telecommunications

Software (Non-Internet / Mobile)

Consumer Products & Services

Healthcare

PwC | CB Insights MoneyTree™ Report Q1 2019 14

US deal share by sectorDeal share for several sectors declined, with software (non-internet/mobile) deals increasing share

• The software (non-internet/mobile) sector increased slightly to 11% of US deals in Q1’19.

44% 46% 42% 46% 44% 44% 45% 44%

15% 13%11%

12% 12% 12% 12% 12%

13% 15%15%

13% 15% 15% 14% 14%

7% 8%8% 8% 9% 8% 10% 11%

5% 4%6% 4% 5% 3% 5% 4%

15% 14% 18% 17% 15% 18% 16% 15%

Q2'17 Q3'17 Q4'17 Q1'18 Q2'18 Q3'18 Q4'18 Q1'19

Internet Mobile & Telecommunications Healthcare Software (non-internet/mobile) Consumer Products & Services Other

PwC | CB Insights MoneyTree™ Report Q1 2019 15

Artificial Intelligence

PwC | CB Insights MoneyTree™ Report Q1 2019 16

Artificial Intelligence: US funding over timeArtificial intelligence deal activity increased after three consecutive quarterly declines

• Artificial intelligence deals increased in Q1’19 to 116 deals, up from 104 deals in Q4’18.

• While deals increased, funding dropped to $2B in Q1’19. Close to half of all artificial intelligence funding for Q1’19 was driven by a $940M investment in Nuro by SoftBank Group.

$1,334 $1,475 $1,487 $2,012 $2,384 $2,740 $2,568 $2,000

121

151

120

148 145 112104

116

0

20

40

60

80

100

120

140

160

Q2'17 Q3'17 Q4'17 Q1'18 Q2'18 Q3'18 Q4'18 Q1'19

Title

Investments ($M) Deals

PwC | CB Insights MoneyTree™ Report Q1 2019 17

Artificial Intelligence: US deal share over timeArtificial intelligence seed-stage deals increased for first time in five quarters

• Seed-stage deals rose to 32% in Q1’19, up from 27% in Q4’18, and the first increase since Q3’17.

• Seed-stage deals included investments in artificial intelligence for retail, such as cashier-less store startup AiFi and smart shopping cart startup Caper.

31%45% 39% 36% 33% 29% 27% 32%

33%

28%25% 32%

31%30% 29%

26%

19%18%

22% 18% 21%21% 31% 27%

7%3% 7% 7% 8% 13% 9%

5%9% 7% 8% 7% 8% 6% 5% 10%

Q2'17 Q3'17 Q4'17 Q1'18 Q2'18 Q3'18 Q4'18 Q1'19

Seed Stage Early Stage Expansion Stage Later Stage Other

PwC | CB Insights MoneyTree™ Report Q1 2019 18

Artificial Intelligence: Top states by deals

61 deals$1,473M Invested

1. CA

18 deals$248M Invested

8 deals$85M Invested

2. NY

3. MA

3. TX 8 deals$58M Invested

PwC | CB Insights MoneyTree™ Report Q1 2019 19

Artificial Intelligence: Largest US deals of Q1’19Company Location Sector Industry Stage of

Funding$ Valueof Deal Select Investors

Nuro Mountain View, CA Automotive & Transportation

Automobile Manufacturing $940M SoftBank Group

Figure Technologies San Francisco, CA Internet Internet Software & Services $65M DCM Ventures, DST Global, Morgan Creek

Capital Management, Nimble Ventures

Ojo Labs Austin, TX Mobile & Telecommunications

Mobile Software & Services $45M LiveOak Venture Partners, Royal Bank of

Canada

PerimeterX San Mateo, CA Internet Internet Software & Services $43M Adams Street Partners, Canaan Partners,

Data Collective

Saama Technologies Campbell, CA Software (non-internet/mobile)

Business Intelligence $40M Perceptive Advisors

Gong San Francisco, CA Internet Internet Software & Services $40M Battery Ventures, Norwest Venture

Partners, Cisco Investments

Expansion Stage

Early Stage

Later Stage

Seed Stage

PwC | CB Insights MoneyTree™ Report Q1 2019 20

Cybersecurity

PwC | CB Insights MoneyTree™ Report Q1 2019 21

Cybersecurity: US funding over timeCybersecurity funding was flat in Q1’19 at $1B

• Cybersecurity funding was flat, while deal activity declined slightly to 48 transactions

• The quarter was led by large funding rounds to content delivery network services provider Cloudflare ($150M Series E+) and identity and access management software OneLogin ($100M Series D).

$1,353 $1,083 $847 $599 $1,702 $1,086 $1,050 $1,082

6771

59

6970

53 51 48

0

10

20

30

40

50

60

70

80

Q2'17 Q3'17 Q4'17 Q1'18 Q2'18 Q3'18 Q4'18 Q1'19

Title

Investments ($M) Deals

PwC | CB Insights MoneyTree™ Report Q1 2019 22

Cybersecurity: US deal share over timeCybersecurity later-stage deals increased significantly as a percentage of deals

• Later-stage deals increased in Q1’19 to 25% as a share of cybersecurity deals.

• Seed-stage deals declined significantly as a percentage of deals in Q1’19.

21%30% 27%

38%

17% 17% 22%8%

27%

31%20%

23%

19%30% 27%

29%

30%18%

34%22%

36%26% 24%

27%

16% 14% 10% 12%

16%21%

16% 25%

6% 7% 8% 6%13%

6% 12% 10%

Q2'17 Q3'17 Q4'17 Q1'18 Q2'18 Q3'18 Q4'18 Q1'19

Seed Stage Early Stage Expansion Stage Later Stage Other

PwC | CB Insights MoneyTree™ Report Q1 2019 23

Cybersecurity: Top states by deals

25 deals$733M Invested

1. CA

4 deals$111M Invested

3 deals$44M Invested

3. MA

3 deals$5M Invested

2. NY

3 deals$2M Invested

3. CO

3. FL

PwC | CB Insights MoneyTree™ Report Q1 2019 24

Cybersecurity: Largest US deals of Q1’19

Company Location Sector Industry Stage of Funding

$ Valueof Deal Select Investors

Cloudflare San Francisco, CA Internet Internet Software & Services

$150M Franklin Templeton Investments

OneLogin San Francisco, CA Internet Internet Software & Services

$100M CRV, Greenspring Associates, Silver Lake Partners, Scale Venture Partners

Keyfactor Independence, OH Computer Hardware & Services IT Services $77M Insight Venture Partners

Contrast Security Los Altos, CA Internet Internet Software & Services

$65M Battery Ventures, General Catalyst, Warburg Pincus

Illumio Sunnyvale, CA Internet Internet Software & Services $65M N/A

Expansion Stage

Early Stage

Later Stage

Seed Stage

PwC | CB Insights MoneyTree™ Report Q1 2019 25

FinTech

PwC | CB Insights MoneyTree™ Report Q1 2019 26

FinTech: US funding over timeFinTech funding decreased slightly in Q1’19, amid a jump in deal activity

• FinTech decreased slightly to $3.3B in Q1’19, down from $3.4B in Q4’18.

• The quarter was led by a large funding round for Clover Health, a data-driven health insurance startup. The company raised a $500M Series E+ from Greenoaks Capital Management.

$2,114 $2,117 $2,438 $2,482 $3,339 $2,989 $3,401 $3,292

152 156 155

212 178168

150170

0

50

100

150

200

250

Q2'17 Q3'17 Q4'17 Q1'18 Q2'18 Q3'18 Q4'18 Q1'19

Title

Investments ($M) Deals

PwC | CB Insights MoneyTree™ Report Q1 2019 27

FinTech: US deal share over timeFinTech deal share was largely flat in Q1’19

• Despite no significant fluctuations, early-stage and “other” deal shares decreased slightly.

• While later-stage deal share was only 8% of FinTech deals in Q1’19, the category accounted for close to $1.4B in funding during the quarter, around 42% of total FinTech funding.

38% 38% 35% 37%26% 26% 27% 27%

28% 20% 26% 25%29% 32% 29% 28%

17%21% 20% 18%

21% 23% 25% 25%

8% 12% 8% 9% 11% 10% 8% 8%

9% 9% 10% 10% 13% 10% 12% 11%

Q2'17 Q3'17 Q4'17 Q1'18 Q2'18 Q3'18 Q4'18 Q1'19

Seed Stage Early Stage Expansion Stage Later Stage Other

PwC | CB Insights MoneyTree™ Report Q1 2019 28

FinTech: Top states by deals

51 deals$1,253M Invested

1. CA

43 deals$575M Invested

14 deals$399M Invested

2. NY

3. MA

PwC | CB Insights MoneyTree™ Report Q1 2019 29

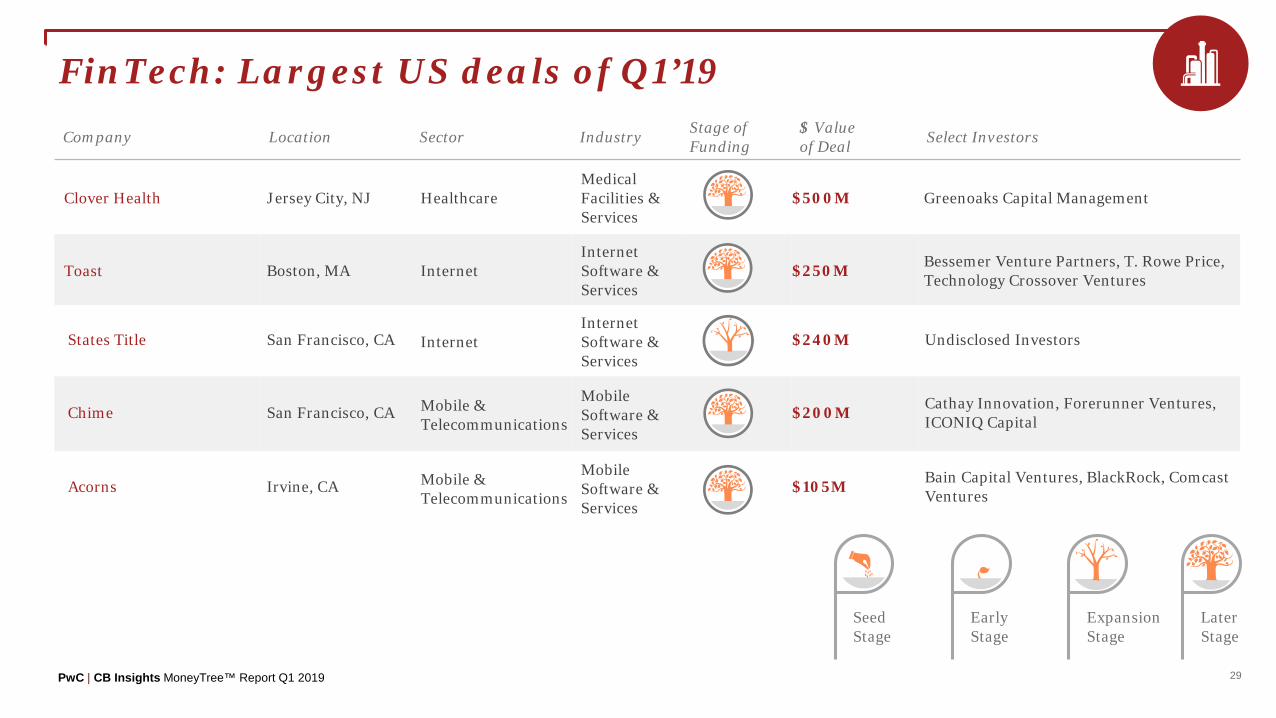

FinTech: Largest US deals of Q1’19Company Location Sector Industry Stage of

Funding$ Valueof Deal Select Investors

Clover Health Jersey City, NJ HealthcareMedical Facilities & Services

$500M Greenoaks Capital Management

Toast Boston, MA InternetInternet Software & Services

$250M Bessemer Venture Partners, T. Rowe Price, Technology Crossover Ventures

States Title San Francisco, CA InternetInternet Software & Services

$240M Undisclosed Investors

Chime San Francisco, CA Mobile & Telecommunications

Mobile Software & Services

$200M Cathay Innovation, Forerunner Ventures, ICONIQ Capital

Acorns Irvine, CA Mobile & Telecommunications

Mobile Software & Services

$105M Bain Capital Ventures, BlackRock, Comcast Ventures

Expansion Stage

Early Stage

Later Stage

Seed Stage

US Places03

PwC | CB Insights MoneyTree™ Report Q1 2019

$7,105M

31

US top five regions of Q1’19 by deals

98

118

131

205

236San Francisco (N. Bay Area)

New York Metro

New England

Silicon Valley (S. Bay Area)

Midwest

$4,455M

$2,758M

$4,333M

$664M

PwC | CB Insights MoneyTree™ Report Q1 2019 32

US: Q1’19 funding by region

Total US:$24.6B

SF (N. Bay Area)$7,105M

Northwest$608M

AK/HI/PR$1M

North Central$75M

Southeast$412M

CO$313M

Texas$1,164M

New England$2,758M

Midwest$664M

New York Metro$4,455M

Upstate NY$52M

DC/Metroplex$320MLA/Orange County

$1,464M

Philadelphia Metro$321M

Silicon Valley (S. Bay Area)$4,333M

San Diego$204M

Sacramento/N. Cal$52M

Southwest$210M

South Central$23M

PwC | CB Insights MoneyTree™ Report Q1 2019 33

US: Q1’19 deals by region

SF (N. Bay Area)236 Deals

Northwest63 Deals

AK/HI/PR3 Deals

North Central

24 Deals

Southeast65 Deals

CO40 Deals

Texas66 Deals

New England131 Deals

Midwest98 Deals

New York Metro205 Deals

Upstate NY7 Deals

DC/Metroplex48 DealsLA/Orange County

72 Deals

Philadelphia Metro31 Deals

Silicon Valley (S. Bay Area)118 Deals

San Diego20 Deals

Sacramento/N. Cal9 Deals

Southwest18 Deals

South Central5 Deals

Total US:1,279 Deals

PwC | CB Insights MoneyTree™ Report Q1 2019 34

8-quarter financing trend: San Francisco (North Bay Area)San Francisco funding fell compared to Q4’18, but stayed within its historical range

• San Francisco startups raised $7B over 236 deals in Q1’19.

• Q4’18 funding was pushed up by a $13B corporate minority investment in vape maker JUUL Labs.

$4,243 $3,855 $5,768 $6,716 $6,034 $8,890 $19,702 $7,105

277 290263

318 311278 256

236

Q2'17 Q3'17 Q4'17 Q1'18 Q2'18 Q3'18 Q4'18 Q1'19

Title

Investments ($M) Deals

PwC | CB Insights MoneyTree™ Report Q1 2019 35

8-quarter financing trend: New York MetroNew York Metro funding increased sharply, deals increased

• Funding jumped to $4.5B in the New York Metro area, an increase of 110% over Q4’18.

• Late-stage NYC-based companies raised six $100M+ funding rounds, including a $1B Series H raised by coworking space provider WeWork.

$2,930 $4,605 $3,001 $2,700 $2,898 $5,888 $2,122 $4,455

207232 224 220 219

184169

205

Q2'17 Q3'17 Q4'17 Q1'18 Q2'18 Q3'18 Q4'18 Q1'19

Title

Investments ($M) Deals

PwC | CB Insights MoneyTree™ Report Q1 2019 36

8-quarter financing trend: Silicon Valley (South Bay Area)Silicon Valley funding and deal activity declined

• Silicon Valley funding fell 19% to $4B amid declining deal activity.

• Deals fell for the third-consecutive quarter to 118 transactions.

$4,230 $2,653 $2,958 $4,019 $3,952 $4,955 $5,382 $4,333

161179 177

187 189

152146

118

Q2'17 Q3'17 Q4'17 Q1'18 Q2'18 Q3'18 Q4'18 Q1'19

Title

Investments ($M) Deals

PwC | CB Insights MoneyTree™ Report Q1 2019 37

8-quarter financing trend: New EnglandNew England funding increased for the second-consecutive quarter

• New England-based companies raised $2.7B in Q1’19, an 8% jump compared to Q4’18.

• Deal activity fell for the third-straight quarter, falling to 131 transactions.

$1,559 $1,978 $2,227 $2,748 $3,123 $2,475 $2,550 $2,758

130

134126

137

148

142135

131

Q2'17 Q3'17 Q4'17 Q1'18 Q2'18 Q3'18 Q4'18 Q1'19

Title

Investments ($M) Deals

PwC | CB Insights MoneyTree™ Report Q1 2019 38

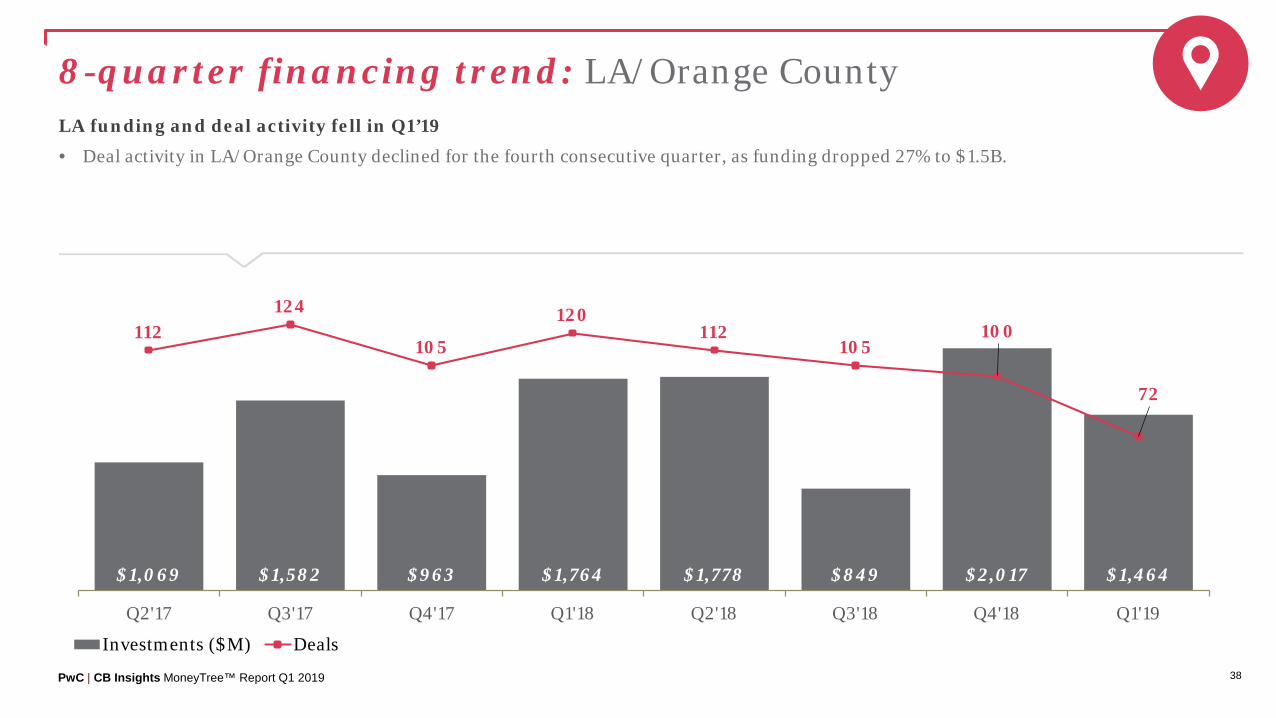

8-quarter financing trend: LA/Orange CountyLA funding and deal activity fell in Q1’19

• Deal activity in LA/Orange County declined for the fourth consecutive quarter, as funding dropped 27% to $1.5B.

$1,069 $1,582 $963 $1,764 $1,778 $849 $2,017 $1,464

112124

105

120112

105100

72

Q2'17 Q3'17 Q4'17 Q1'18 Q2'18 Q3'18 Q4'18 Q1'19

Title

Investments ($M) Deals

PwC | CB Insights MoneyTree™ Report Q1 2019 39

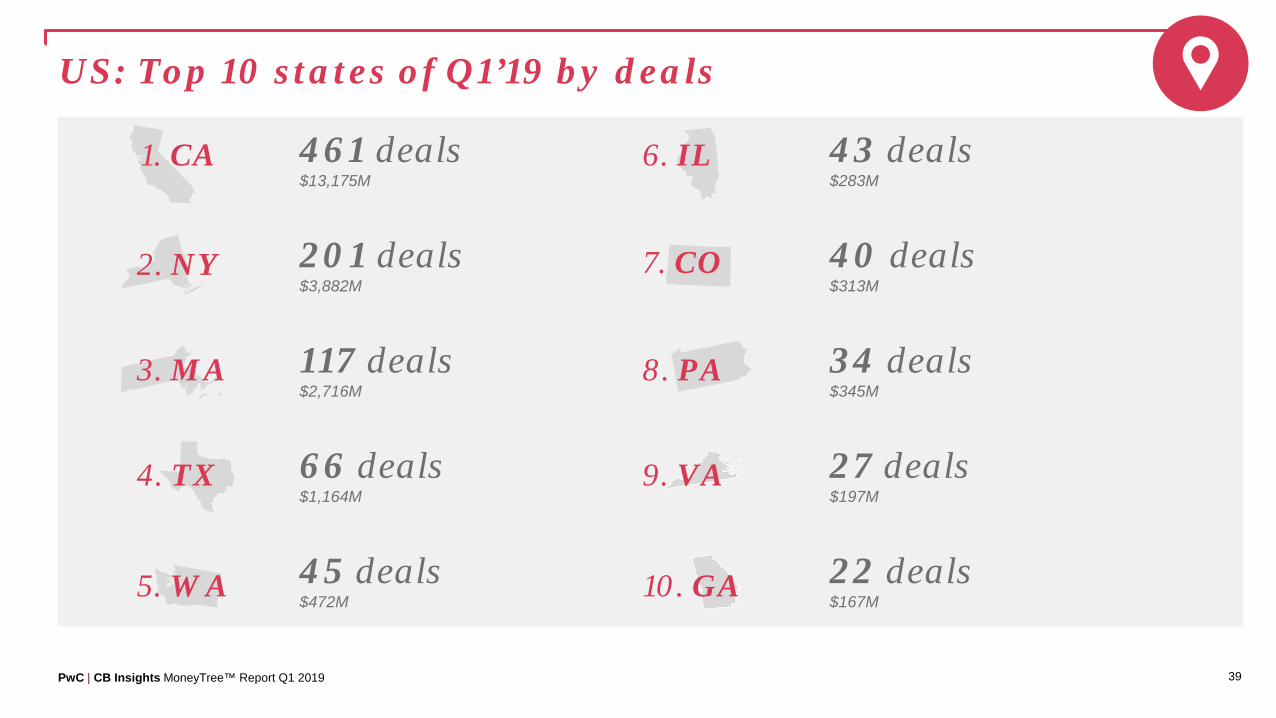

US: Top 10 states of Q1’19 by deals

461 deals$13,175M

201 deals$3,882M

117 deals$2,716M

66 deals$1,164M

45 deals$472M

1. CA

2. NY

3. MA

4. TX

5. WA

6. IL 43 deals$283M

40 deals$313M

34 deals$345M

27 deals$197M

22 deals$167M

7. CO

8. PA

9. VA

10. GA

PwC | CB Insights MoneyTree™ Report Q1 2019 40

Q1’19 Regional comparison: Deals CA vs. NY vs. MADeals declined in California and Massachusetts, jumped in New York

• New York deal activity rose to 201 in Q1’19, from 164 in Q4’18.

591634

585656 670

571541

461

195 220 214 218 217177 164

201

114 117 114 121 126 123 123 117

Q2'17 Q3'17 Q4'17 Q1'18 Q2'18 Q3'18 Q4'18 Q1'19

California New York Massachusetts

PwC | CB Insights MoneyTree™ Report Q1 2019 41

Q1’19 Regional comparison: Financing CA vs. NY vs. MACalifornia funding declined sharply in Q1’19

• California-based companies saw funding fall from $28B to $13B in Q1’19, a 53% decrease compared to Q4’18.

• New York funding increased from $2B in Q4’18 to $4B in Q1’19.

$10.0$8.7

$10.0

$12.9 $12.6

$15.7

$27.9

$13.2

$2.6$4.4

$2.9 $2.5 $2.9

$5.8

$2.0$3.9

$1.5 $1.5 $2.2 $2.7 $3.0 $2.4 $2.5 $2.7

Q2'17 Q3'17 Q4'17 Q1'18 Q2'18 Q3'18 Q4'18 Q1'19

California New York Massachusetts

US Movers & Shakers04

PwC | CB Insights MoneyTree™ Report Q1 2019 43

Mega-rounds

”

The prevalence of mega deals - characterized as rounds greater than $100 million - continues to shape the VC landscape.

“

— Tom Ciccolella, Partner, US Ventures Leader at PwC

PwC | CB Insights MoneyTree™ Report Q1 2019 44

Largest US deals of Q1’19

Company Location Sector Industry Stage of Funding

$ Valueof Deal Select Investors

WeWork New York, NY Business Products & Services Facilities $1,000M SoftBank Group

Flexport San Francisco, CA Internet Internet Software & Services $1,000M SoftBank Group, Founders Fund, Cherubic

Ventures

Nuro Mountain View, CA Automotive & Transportation

Automobile Manufacturing $940M SoftBank Group

Aurora Palo Alto, CA Automotive & Transportation

Automobile Manufacturing $530M Amazon, Greylock Partners, Lightspeed

Venture Partners, Sequoia Capital

Clover Health Jersey City, NJ Healthcare Medical Facilities & Services $500M Greenoaks Capital Management

DoorDash San Francisco, CA Internet eCommerce $400M Sequoia Capital, SoftBank Group, Y Combinator

Expansion Stage

Early Stage

Later Stage

Seed Stage

PwC | CB Insights MoneyTree™ Report Q1 2019 45

US mega-round activityUS $100M+ rounds fell, but remained at elevated levels

• US-based companies saw another big quarter for mega-rounds, raising 46 $100M+ rounds, down from the Q3’18 record but still elevated.

• Later-stage companies raised several massive funding rounds in Q1’19, including two $1B rounds by coworking provider WeWork and freight forwarding startup Flexport.

34 32 35 33 48 56 51 460.0

10.0

20.0

30.0

40.0

50.0

60.0

Q2'17 Q3'17 Q4'17 Q1'18 Q2'18 Q3'18 Q4'18 Q1'19

Mega-rounds Into US VC-Backed Companies

PwC | CB Insights MoneyTree™ Report Q1 2019 46

8-quarter US mega-round trendMega-rounds fell from record percentage of total US funding

• Mega-rounds accounted for 45% of all US VC funding, down from a record 64% in Q4’18.

• Mega-rounds were largely raised by late-stage companies, though there were three early stage $100M+ rounds in Q1’19.

$7.0 $8.5 $7.6 $7.9 $8.2 $14.8 $24.7 $11.1

$12.6 $12.3 $12.4 $14.9 $16.3

$14.2

$13.9

$13.5

36%41% 38% 35%

34%

51%

64%

45%

Q2'17 Q3'17 Q4'17 Q1'18 Q2'18 Q3'18 Q4'18 Q1'19

Mega-round funding ($B) Non Mega-round funding ($B) % Mega-rounds funding

PwC | CB Insights MoneyTree™ Report Q1 2019 47

US new unicorn births10 new unicorns were created in Q1’19

• 10 US companies saw their valuations rise to $1B+ in Q1’19.

• New $1B+ valuations included mattress startup Casper and direct-to-consumer beauty company Glossier.

108 7 7 8

17

21

10

Q2'17 Q3'17 Q4'17 Q1'18 Q2'18 Q3'18 Q4'18 Q1'19

US New VC-backed Unicorns

PwC | CB Insights MoneyTree™ Report Q1 2019 48

Unicorn population countsA record number of US companies were valued at $1B+ in Q1'19

• At 147, the number of US private companies with $1B+ valuations has never been higher.

102 106 109 112 112123

139147

Q2'17 Q3'17 Q4'17 Q1'18 Q2'18 Q3'18 Q4'18 Q1'19

US VC backed unicorn population

PwC | CB Insights MoneyTree™ Report Q1 2019 49

Aggregate unicorn valuation by periodQ1’19 set a new record for aggregate unicorn valuation

• Private companies worth $1B+ reached a combined value of $582B in Q1’19, the highest aggregate valuation on record.

$353.6 $374.7 $376.6 $400.6 $410.0 $469.0 $566.4 $582.4

Q2'17 Q3'17 Q4'17 Q1'18 Q2'18 Q3'18 Q4'18 Q1'19

Unicorn Valuation ($B)

PwC | CB Insights MoneyTree™ Report Q1 2019 50

M&A and median years to exitM&A activity declined in Q1’19 but stayed within the historical range

• M&A activity declined to 154 deals in Q1’19, compared to 183 in Q4’18.

• Median years to exit from first financing declined to 5 years, from 6.5 in Q4’18.

135 148 156 165 175 159 183 154

4.9

6.1 5.8 5.65.1

5.6

6.5

5.1

0

1

2

3

4

5

6

7

Q2'17 Q3'17 Q4'17 Q1'18 Q2'18 Q3'18 Q4'18 Q1'19

Title

M&A Median Years

PwC | CB Insights MoneyTree™ Report Q1 2019 51

Top 5 valued US unicorn companies as of Q1’19

Company Location Industry Valuation (as of 3/31/2019)

Select Investors

1. Uber San Francisco, CA On-Demand $72BLowercase Capital, Benchmark Capital, Google Ventures

2. WeWork New York, NY Facilities $47B SoftBank Group, Benchmark Capital, T. Rowe Price

3. JUUL Labs San Francisco, CA Consumer Electronics $38B Altria Group, M13, Tiger Global Management

4. Airbnb San Francisco, CA eCommerce/Marketplace $29BGeneral Catalyst Partners, Andreessen Horowitz, ENIAC Ventures

5. Stripe San Francisco, CA Fintech $23B Khosla Ventures, Lowercase Capital, capitalG

PwC | CB Insights MoneyTree™ Report Q1 2019 52

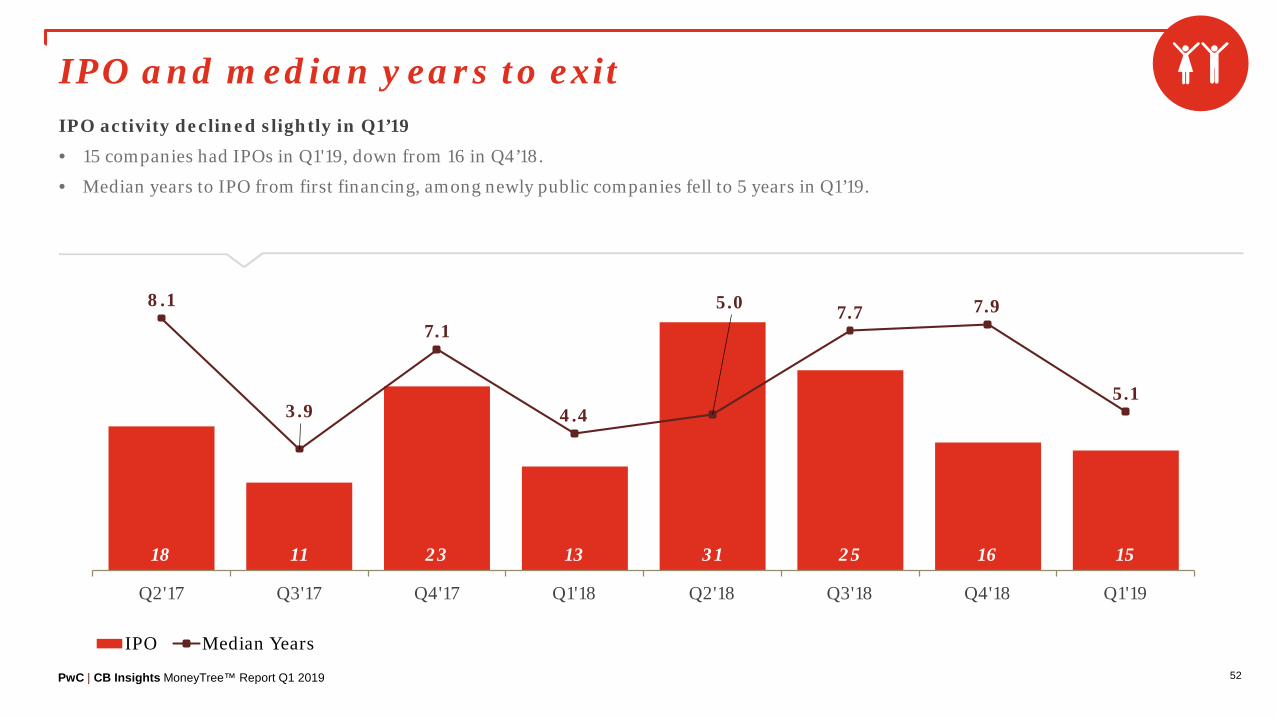

IPO and median years to exitIPO activity declined slightly in Q1’19

• 15 companies had IPOs in Q1'19, down from 16 in Q4’18.

• Median years to IPO from first financing, among newly public companies fell to 5 years in Q1’19.

18 11 23 13 31 25 16 15

8.1

3.9

7.1

4.4

5.0 7.7 7.9

5.1

0

1

2

3

4

5

6

7

8

9

Q2'17 Q3'17 Q4'17 Q1'18 Q2'18 Q3'18 Q4'18 Q1'19

Title

IPO Median Years

PwC | CB Insights MoneyTree™ Report Q1 2019 53

Largest US IPOs of Q1’19

Company Location Sector Industry $ Valuation at IPO

Lyft San Francisco, CA Mobile & Telecommunications Mobile Commerce $24.3B

Alector South San Francisco, CA Healthcare Biotechnology $1.2B

Gossamer Bio San Diego, CA Healthcare Drug Discovery $966M

Precision BioSciences Durham, NC Healthcare Biotechnology $784M

Kaleido Biosciences Bedford, MA Healthcare Biotechnology $441M

PwC | CB Insights MoneyTree™ Report Q1 2019 54

Most active VC firms of Q1’19 in the US

Investor Location No. of US Companies Select Q1’19 Investments

1. New Enterprise Associates Chevy Chase, MD 27 OpenDoor Labs, Databricks, Desktop Metal

2. Google Ventures Mountain View, CA 24 Lime, OpenDoor Labs, Clutter

Palo Alto, CA 24 OpenDoor Labs, Casper, Influx Data

Menlo Park, CA 20 Aurora, DoorDash, reddit

2. Norwest Venture Partners

3. Sequoia Capital

4. Bessemer Venture Partners Menlo Park, CA 18 Toast, Vlocity, CS Disco

PwC | CB Insights MoneyTree™ Report Q1 2019

Stage of funding

Location of investors

Seed Total number of seed stage deals: 221

Early Total number of early stage deals: 324

Expansion Total number of expansion stage deals: 385

Later Total number of later stage deals: 177

55

Q1’19 investor locationsCalifornia investor presence most prominent across all stages

• California and New York investors dominated the later-stage deals that have driven US funding to record levels.

• Funding was more geographically diverse at earlier stages, with other US states and international investors accounting for more deals.

26%

32%

36%

38%

13%

11%

12%

13%

3%

3%

3%

1%

26%

28%

25%

27%

33%

25%

25%

22%

California New York Illinois Other US International

PwC | CB Insights MoneyTree™ Report Q1 2019 56

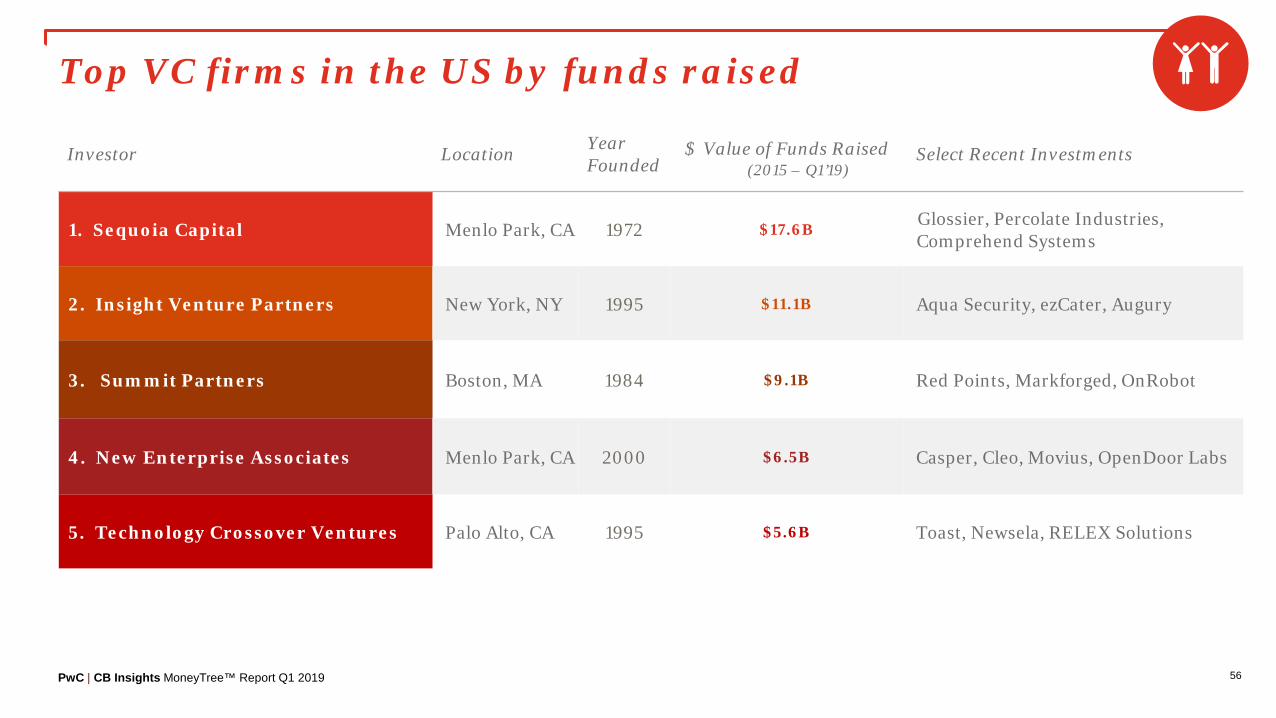

Top VC firms in the US by funds raised

Investor Location Year Founded

$ Value of Funds Raised(2015 – Q1’19)

Select Recent Investments

1. Sequoia Capital Menlo Park, CA 1972 $17.6B Glossier, Percolate Industries, Comprehend Systems

2. Insight Venture Partners New York, NY 1995 $11.1B Aqua Security, ezCater, Augury

3. Summit Partners Boston, MA 1984 $9.1B Red Points, Markforged, OnRobot

4. New Enterprise Associates Menlo Park, CA 2000 $6.5B Casper, Cleo, Movius, OpenDoor Labs

5. Technology Crossover Ventures Palo Alto, CA 1995 $5.6B Toast, Newsela, RELEX Solutions

Global Trends05

PwC | CB Insights MoneyTree™ Report Q1 2019 58

Q1’19 Global regional comparison

Deals

Deals

1,375$25.6B

1,128$18.4B724

$7.7B

3,327 Deals$52.2B Invested

Globally

PwC | CB Insights MoneyTree™ Report Q1 2019 59

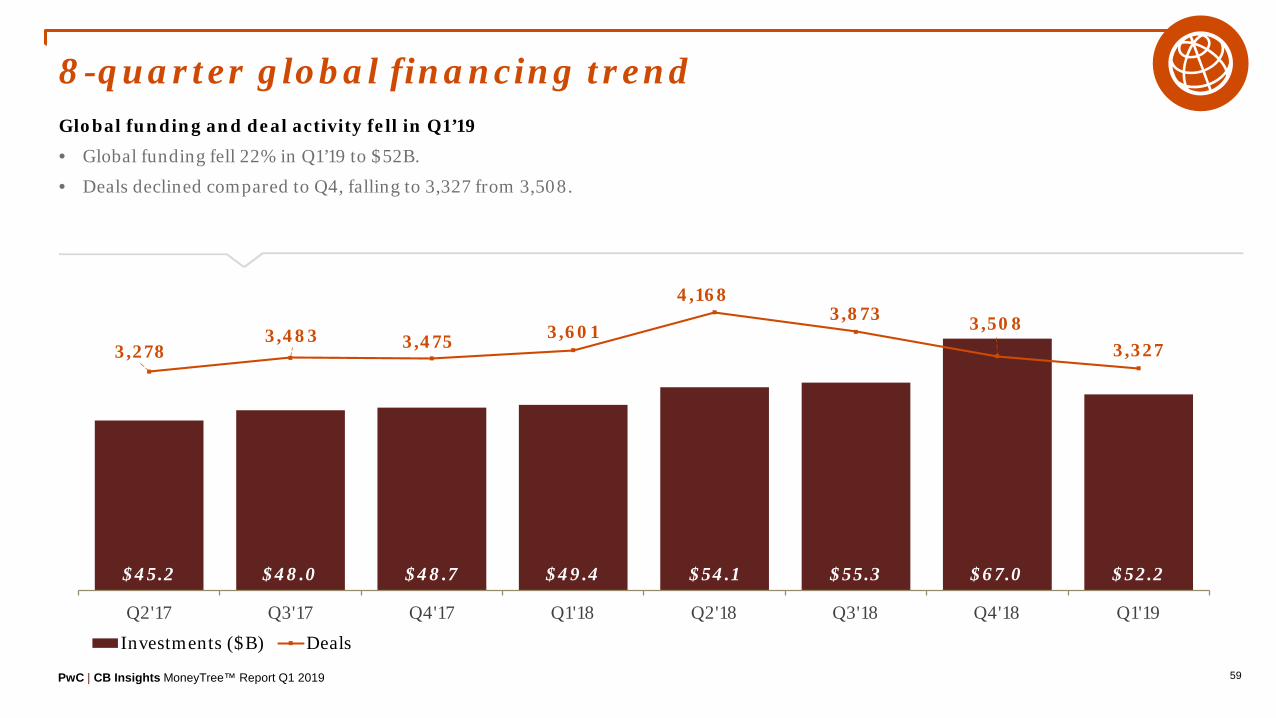

8-quarter global financing trendGlobal funding and deal activity fell in Q1’19

• Global funding fell 22% in Q1’19 to $52B.

• Deals declined compared to Q4, falling to 3,327 from 3,508.

$45.2 $48.0 $48.7 $49.4 $54.1 $55.3 $67.0 $52.2

3,2783,483 3,475 3,601

4,1683,873 3,508

3,327

Q2'17 Q3'17 Q4'17 Q1'18 Q2'18 Q3'18 Q4'18 Q1'19

Investments ($B) Deals

PwC | CB Insights MoneyTree™ Report Q1 2019 60

Global corporate deal participationCorporate participation increased slightly

• Corporations (and/or their venture arms) participated in 32% of all deals to VC-backed companies in Q1’19, up from 30% in Q4.

74% 75% 73% 74% 71% 70% 70% 68%

26% 25% 27% 26% 29% 30% 30% 32%

Q2'17 Q3'17 Q4'17 Q1'18 Q2'18 Q3'18 Q4'18 Q1'19

Other Investors Corp / CVC Deal Participation

PwC | CB Insights MoneyTree™ Report Q1 2019 61

8-quarter financing trend: North AmericaNorth American funding and deal activity fell in Q1’19

• VC-backed companies in North America raised $26B in Q1’19, down 36% compared to Q4’18.

• Deal activity declined slightly compared to Q4’18, falling to 1,375.

$20.1 $21.7 $20.6 $23.6 $25.5 $29.4 $39.7 $25.6

1,5611,663

1,5171,646

1,760

1,5361,424 1,375

Q2'17 Q3'17 Q4'17 Q1'18 Q2'18 Q3'18 Q4'18 Q1'19

Investments ($B) Deals

PwC | CB Insights MoneyTree™ Report Q1 2019 62

North American corporate deal participationCorporate participation increases in North America

• Corporations (and/or their venture arms) participated in 30% of Q1’19 deals in North America.

76% 77% 77% 76% 76% 73% 73% 70%

24% 23% 23% 24% 24% 27% 27% 30%

Q2'17 Q3'17 Q4'17 Q1'18 Q2'18 Q3'18 Q4'18 Q1'19

Other Investors Corp / CVC Deal Participation

PwC | CB Insights MoneyTree™ Report Q1 2019 63

8-quarter financing trend: EuropeEuropean funding jumped amid a drop in deal activity

• Europe-based startups raised $8B in Q1’19, a 48% jump compared to Q4’18.

• Deal activity fell 4% to 724 transactions.

$4.8 $5.6 $5.1 $5.2 $5.9 $5.1 $5.2 $7.7

704

728 729 725

766

699

751

724

Q2'17 Q3'17 Q4'17 Q1'18 Q2'18 Q3'18 Q4'18 Q1'19

Investments ($B) Deals

PwC | CB Insights MoneyTree™ Report Q1 2019 64

European corporate deal participationCorporate participation increased slightly

• Corporations (and/or their venture arms) participated in 27% of Q1’19 deals in Europe, up slightly compared to Q4’18.

76% 79% 78% 77% 75% 72% 74% 73%

24% 21% 22% 23% 25% 28% 26% 27%

Q2'17 Q3'17 Q4'17 Q1'18 Q2'18 Q3'18 Q4'18 Q1'19Other Investors Corp / CVC Deal Participation

PwC | CB Insights MoneyTree™ Report Q1 2019 65

8-quarter financing trend: AsiaFunding and deal activity fell in Asia

• Asia funding dropped 13% in Q1’19, falling to $18B.

• Deal activity fell to 1,128, down from 1,212 in Q4’18.

$19.8 $20.4 $22.5 $19.8 $22.4 $20.1 $21.1 $18.4

8841,002

1,110 1,124

1,495 1,497

1,2121,128

Q2'17 Q3'17 Q4'17 Q1'18 Q2'18 Q3'18 Q4'18 Q1'19

Investments ($B) Deals

PwC | CB Insights MoneyTree™ Report Q1 2019 66

Asia corporate deal participationCorporate participation increased slightly

• Corporations (and/or their venture arms) participated in 40% of Asia VC deals, up from 38% in Q4’18.

68% 69% 65% 67% 65% 66% 62% 60%

32% 31% 35% 33% 35% 34% 38% 40%

Q2'17 Q3'17 Q4'17 Q1'18 Q2'18 Q3'18 Q4'18 Q1'19

Other Investors Corp / CVC Deal Participation

PwC | CB Insights MoneyTree™ Report Q1 2019 67

Largest global deals of Q1’19Company Location Sector Industry Stage of

Funding$ Valueof Deal Select Investors

Chehaoduo Beijing, China Internet eCommerce $1,500M SoftBank Group

Grab Singapore Mobile & Telecommunications Mobile Commerce $1,460M SoftBank Group

OneWeb London, UK Mobile & Telecommunications Telecom Services $1,250M Airbus Ventures, Qualcomm Ventures,

SoftBank Group, Virgin Group

Flexport San Francisco, US Internet Software & Services

Supply Chain & Logistics $1000M SoftBank Group, Founders Fund, Cherubic

Ventures

WeWork New York, US Business Products & Services Facilities $1000M SoftBank Group

Expansion Stage

Early Stage

Later Stage

Seed Stage

PwC | CB Insights MoneyTree™ Report Q1 2019 68

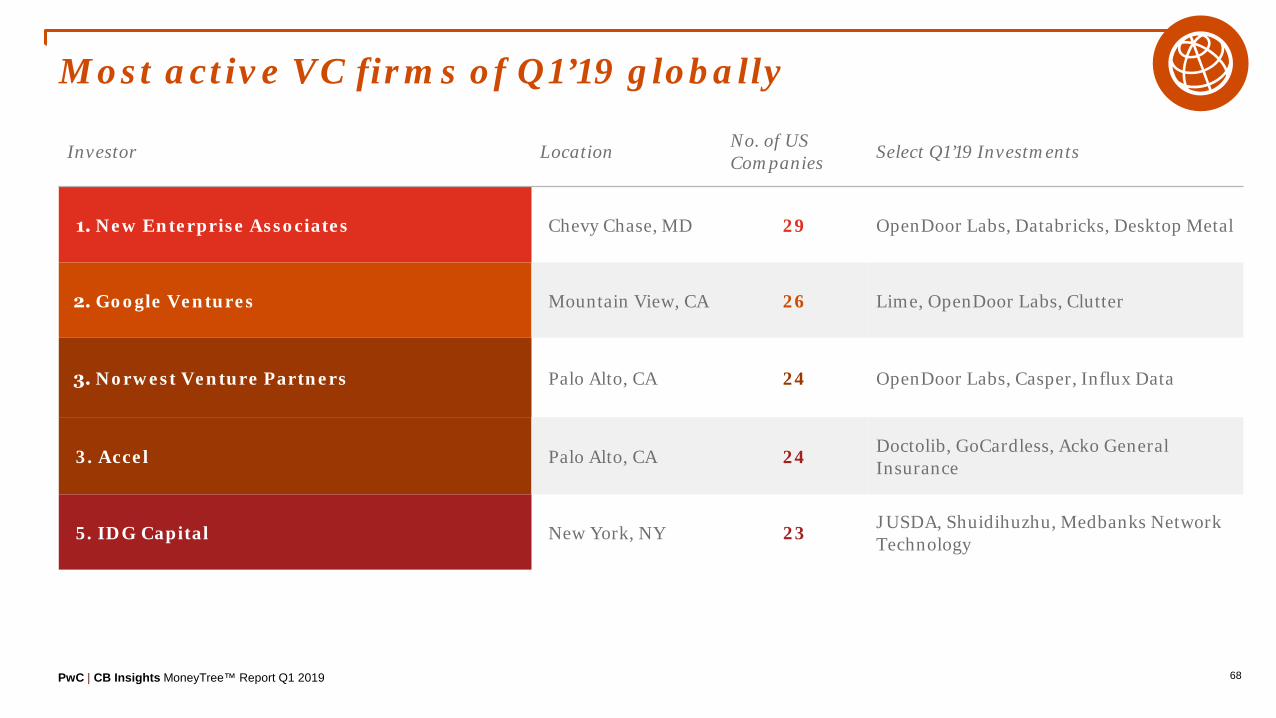

Most active VC firms of Q1’19 globally

Investor Location No. of US Companies Select Q1’19 Investments

Chevy Chase, MD 29 OpenDoor Labs, Databricks, Desktop Metal

Mountain View, CA 26 Lime, OpenDoor Labs, Clutter

1. New Enterprise Associates

2. Google Ventures

3. Norwest Venture Partners Palo Alto, CA 24 OpenDoor Labs, Casper, Influx Data

3. Accel Palo Alto, CA 24 Doctolib, GoCardless, Acko General Insurance

5. IDG Capital New York, NY 23 JUSDA, Shuidihuzhu, Medbanks Network Technology

PwC | CB Insights MoneyTree™ Report Q1 2019 69

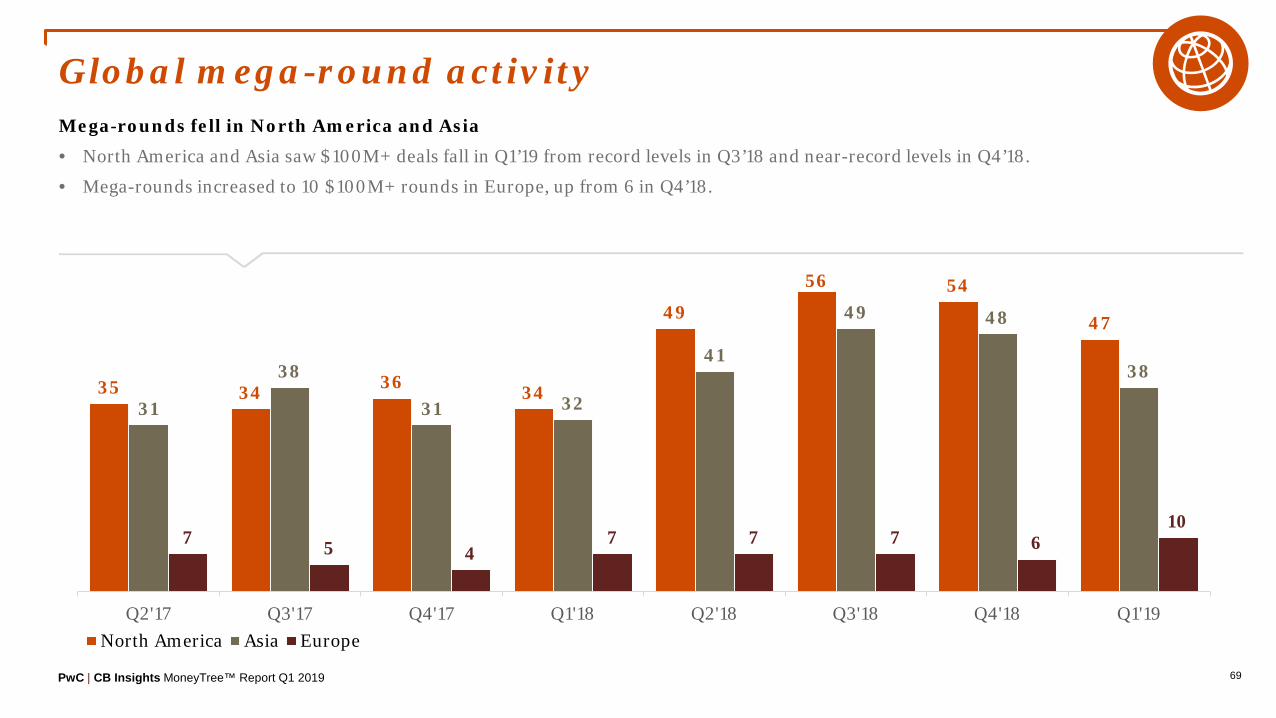

Global mega-round activityMega-rounds fell in North America and Asia

• North America and Asia saw $100M+ deals fall in Q1’19 from record levels in Q3’18 and near-record levels in Q4’18.

• Mega-rounds increased to 10 $100M+ rounds in Europe, up from 6 in Q4’18.

35 34 36 34

49

56 54

47

31

38

31 32

41

49 48

38

7 5 47 7 7 6

10

0.0

10.0

20.0

30.0

40.0

50.0

60.0

Q2'17 Q3'17 Q4'17 Q1'18 Q2'18 Q3'18 Q4'18 Q1'19North America Asia Europe

PwC | CB Insights MoneyTree™ Report Q1 2019 70

Global new unicorn birthsNorth America minted more unicorns than Asia for the third-straight quarter

• North America saw 10 private companies hit $1B+ valuations in Q1’19, compared to 5 in Asia

• New unicorns in Q1’19 were down compared to Q4’18 in North America, Europe, and Asia.

67

8 7

1116

8

5

108

7

7 8

17

21

10

1 20

35

24 3

Q2'17 Q3'17 Q4'17 Q1'18 Q2'18 Q3'18 Q4'18 Q1'19

Asia North America Europe

PwC | CB Insights MoneyTree™ Report Q1 2019 71

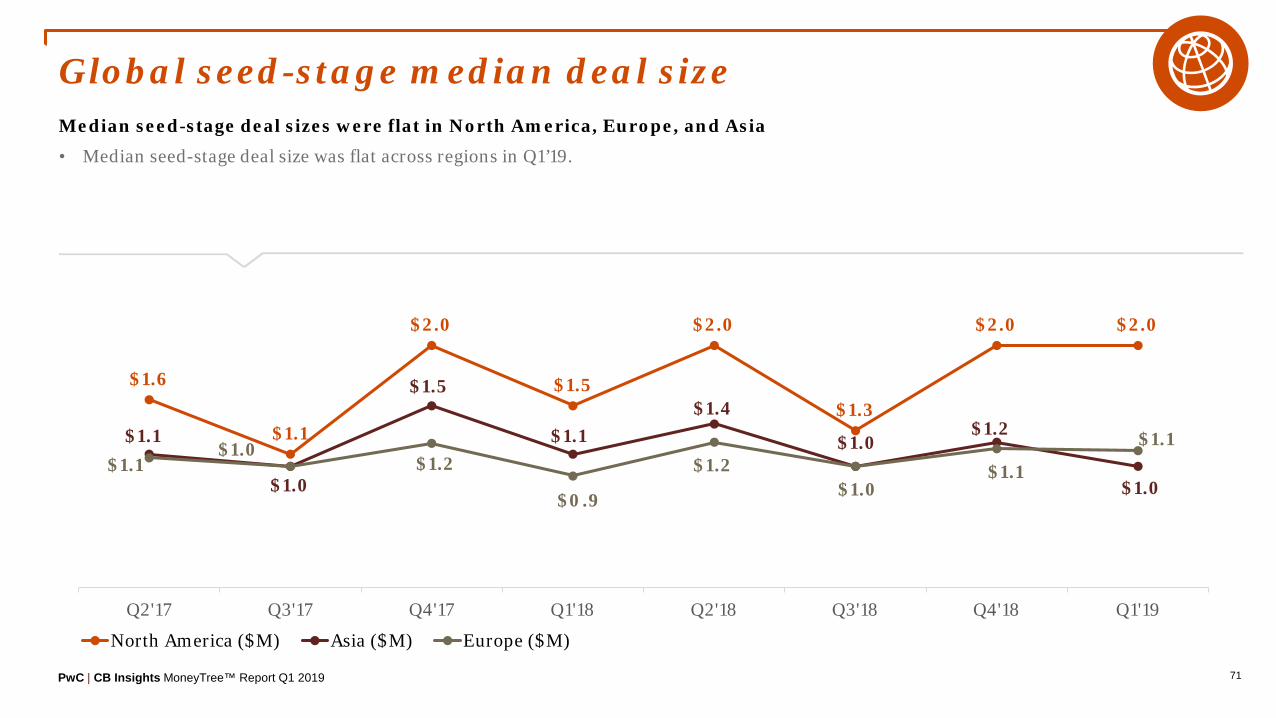

Global seed-stage median deal sizeMedian seed-stage deal sizes were flat in North America, Europe, and Asia

• Median seed-stage deal size was flat across regions in Q1’19.

$1.6

$1.1

$2.0

$1.5

$2.0

$1.3

$2.0 $2.0

$1.1

$1.0

$1.5

$1.1$1.4

$1.0$1.2

$1.0$1.1

$1.0$1.2

$0.9

$1.2$1.0

$1.1

$1.1

Q2'17 Q3'17 Q4'17 Q1'18 Q2'18 Q3'18 Q4'18 Q1'19

North America ($M) Asia ($M) Europe ($M)

PwC | CB Insights MoneyTree™ Report Q1 2019 72

Global early-stage median deal sizeMedian early-stage deal size jumped in Europe

• Early-stage median deal size increased to $5.2M in Europe, up from $4.6M in Q4’18.

$6.0

$6.0

$6.8 $7.0$7.3

$6.5$7.2 $7.2

$5.8$6.0

$5.7 $6.4

$6.3

$5.9 $5.0

$4.4$5.0

$4.7$5.2

$4.2

$5.3$4.6 $4.6

$5.2

Q2'17 Q3'17 Q4'17 Q1'18 Q2'18 Q3'18 Q4'18 Q1'19

North America ($M) Asia ($M) Europe ($M)

PwC | CB Insights MoneyTree™ Report Q1 2019 73

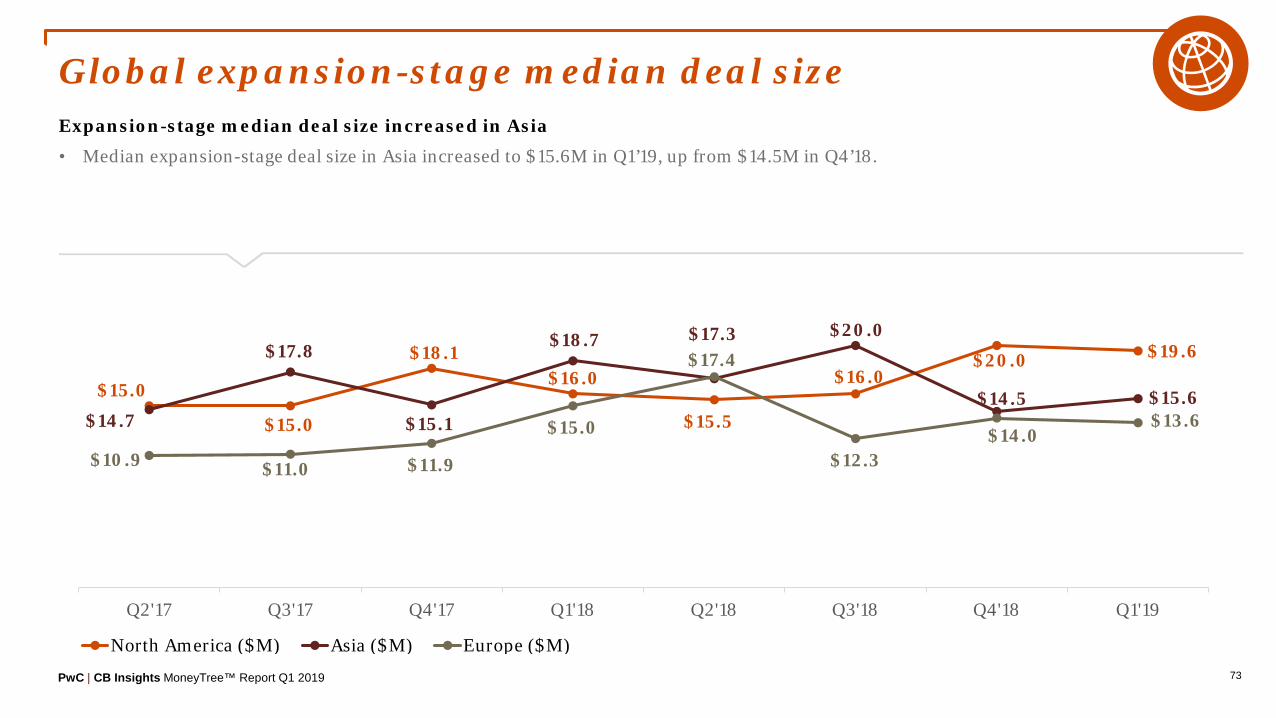

Global expansion-stage median deal sizeExpansion-stage median deal size increased in Asia

• Median expansion-stage deal size in Asia increased to $15.6M in Q1’19, up from $14.5M in Q4’18.

$15.0

$15.0

$18.1$16.0

$15.5

$16.0$20.0 $19.6

$14.7

$17.8

$15.1

$18.7 $17.3 $20.0

$14.5 $15.6

$10.9 $11.0 $11.9

$15.0

$17.4

$12.3$14.0

$13.6

Q2'17 Q3'17 Q4'17 Q1'18 Q2'18 Q3'18 Q4'18 Q1'19

North America ($M) Asia ($M) Europe ($M)

PwC | CB Insights MoneyTree™ Report Q1 2019 74

Global later-stage median deal sizeMedian later-stage deal size rose across the board

• Median later-stage deal size increased in North America, Europe, and Asia.

• Asia saw median later-stage deal size increase to $56M, up from $50M in Q4’18.

$34.2 $30.9 $26.6 $30.0

$44.5

$32.0 $35.0$40.0

$70.0

$90.0

$73.1$68.0

$88.0

$100.0

$50.0$56.1

$13.8 $12.0

$24.9$13.9 $11.2 $13.0

$18.5$27.9

Q2'17 Q3'17 Q4'17 Q1'18 Q2'18 Q3'18 Q4'18 Q1'19

North America ($M) Asia ($M) Europe ($M)

AppendixAppendix

PwC | CB Insights MoneyTree™ Report Q1 2019 76

US States: Full listingState $M No. of

Deals

Alabama - 1

Arizona $55.5 4

Arkansas $13.2 1

California $13,175.3 461

Colorado $313.2 40

Connecticut $87.2 14

DC $46.1 3

Delaware $14.7 5

Florida $107.1 20

Georgia $167.0 22

Hawaii $0.7 2

No disclosed quarterly activity: AK, MS, NM, ND, OK, VT, WV, WY

State $M No. of Deals

Idaho $26.2 3

Illinois $283.0 43

Indiana $35.0 7

Iowa $3.7 5

Kansas $8.5 3

Kentucky $1.8 1

Louisiana $1.1 1

Maine $3.1 3

Maryland $77.0 18

Massachusetts $2,716.4 117

Michigan $55.4 14

State $M No. of Deals

Minnesota $41.1 10

Missouri $109.6 9

Montana $13.2 4

Nebraska $4.5 3

Nevada $26.0 2

New Hampshire $4.1 2

New Jersey $623.5 14

New York $3,881.7 201

North Carolina $73.9 12

Ohio $141.2 16

Oregon $96.3 11

State $M No. of Deals

Pennsylvania $344.8 34

Rhode Island $7.2 1

South Carolina $8.9 2

South Dakota $3.0 1

Tennessee $54.9 8

Texas $1,163.9 66

Utah $128.1 12

Virginia $197.1 27

Washington $472.0 45

Wisconsin $22.6 5

PwC | CB Insights MoneyTree™ Report Q1 2019 77

Notes on methodologyPwC (pwcmoneytree.com) and CB Insights (cbinsights.com) encourage you to review the methodology and definitions employed to better understand the numbers presented in this report. If you have any questions about the definitions or methodological principles used, we encourage you to reach out to CB Insights directly. Additionally, if you feel your firm has been underrepresented, please send an email to [email protected] and we can work together to ensure your firm’s investment data is up-to-date.

Rankings, e.g., top states and top sectors, are done by quarterly deal activity (that is, deal count for the given quarter).

What is included:

- Equity financings into emerging companies. Fundings must be to VC-backed companies, which are defined as companies that have received funding at any point from either: venture capital firms, corporate venture arms, or super angel investors.

- Fundings of private companies only. Funding rounds raised by public companies of any kind on any exchange (including Pink Sheets) are excluded from our numbers, even if they received investment by a venture firm(s).

- Only includes the investment made in the quarter for tranched investments. If a company does a second closing of its Series B round for $5M and previously had closed $2M in a prior quarter, only the $5M is reflected in our results.

- Round numbers reflect what has closed – not what is intended. If a company indicates the closing of $5M out of a desired raise of $15M, our numbers reflect only the amount which has closed.

- Only verifiable fundings are included. Fundings are verified via (1) various federal and state regulatory filings; (2) direct confirmation with firm or investor; (3) press release; or (4) credible media sources.

- Equity fundings to joint ventures and spinoffs/spinouts are included, given that they meet the VC-backed criteria.

- Geography note: Israel funding figures are classified in Asia.

What is excluded:

- No contingent funding. If a company receives a commitment for $20M subject to hitting certain milestones but first gets $8M, only the $8M is included in our data.

- No business development / R&D arrangements whether transferable into equity now, later or never. If a company signs a $300M R&D partnership with a larger corporation, this is not equity financing nor is it from venture capital firms. As a result, it is not included.

- No buyouts, consolidations or recapitalizations. All three of these transaction types are commonly employed by private equity firms and are tracked by CB Insights. However, they are excluded for the purposes of this report.

- No private placements. These investments, also known as PIPEs (Private Investment in Public Equities), are not included even if made by a venture capital firm(s).

- No debt/loans of any kind (except convertible notes). Venture debt or any kind of debt/loan issued to emerging, startup companies, even if included as an additional part of an equity financing, is not included. If a company receives $3M with $2M from venture investors and $1M in debt, only the $2M is included in these statistics.

- No non-equity government funding. Grants or loans by the federal government, state agencies, or public-private partnerships to emerging, startup companies are not included.

- No fundings to subsidiaries of a larger parent corporation.

This content is for general information purposes only, and should not be used as a substitute for consultation with professional advisors. Data is current as of April 1, 2019. PricewaterhouseCoopers and CB Insights have taken responsible steps to ensure that the information contained in the MoneyTree™ Report has been obtained from reliable sources. However, neither PwC nor CB Insights can warrant the ultimate validity of the data obtained in this manner. Results are updated periodically. Therefore, all data is subject to change at any time.

© 2019 PwC. All rights reserved. PwC refers to the US member firm or one of its subsidiaries or affiliates, and may sometimes refer to the PwC network. Each member firm is a separate legal entity. Please see www.pwc.com/structure for further details.