pw ra - sÉ{:ïï hÿe þ ¹&¹p j¹ Ï *4Én¸ È ô [ú ¼g¾ `Õ ï w ³ ...€¦ · global...

TRANSCRIPT

Investor presentation

Phil WagstaffGlobal Head of Distribution

Global Distribution Strategy

This document is solely for the use of professionals and is not for general public distribution.The value of an investment and the income from it can fall as well as rise and you may not get backthe amount originally invested.

May 2014

1

Today

• 5 year plan

• Changes made and changes ongoing

• People

• Our global business

• The importance of product

• Brand

• The next 3 years

2

My background

• Over 25 years in asset management distribution

• NM Schroder, Henderson, M&G Investments, New Star, Gartmore

• ‘Done the job’

• Build the people and they will build your business

• Joined via Gartmore acquisition

• Why I came back!

3

A combination of art and science

Right people

Right relationships

Right time

Right products

Right performance

Right brand

Right client service

Competitive advantage

Distribution is a combination of art and science; application of science to the art of relationships

4

Distribution strategy

• Performance, and the perception of performance, is critical to long term success

• Global Product Development is a key driver

• We need a brand that conveys the sense of performance

• A distribution structure based around client types gives a better understanding of investment objectives, product and service needs

• Quality of people will determine the quality of success

• Team work and collaboration critical in a global market

• Need to build our core franchises

• We have to back our winners

The 5 year plan

2 years in, 3 to go

5

(747)

(423)

(833)(708)

(1,457)

(581)

(107)

197113

1Q12 2Q12 3Q12 4Q12 1Q13 2Q13 3Q13 4Q13 1Q14

Global Institutional net flowsInstitutional flows continue to stabilise

£m

6

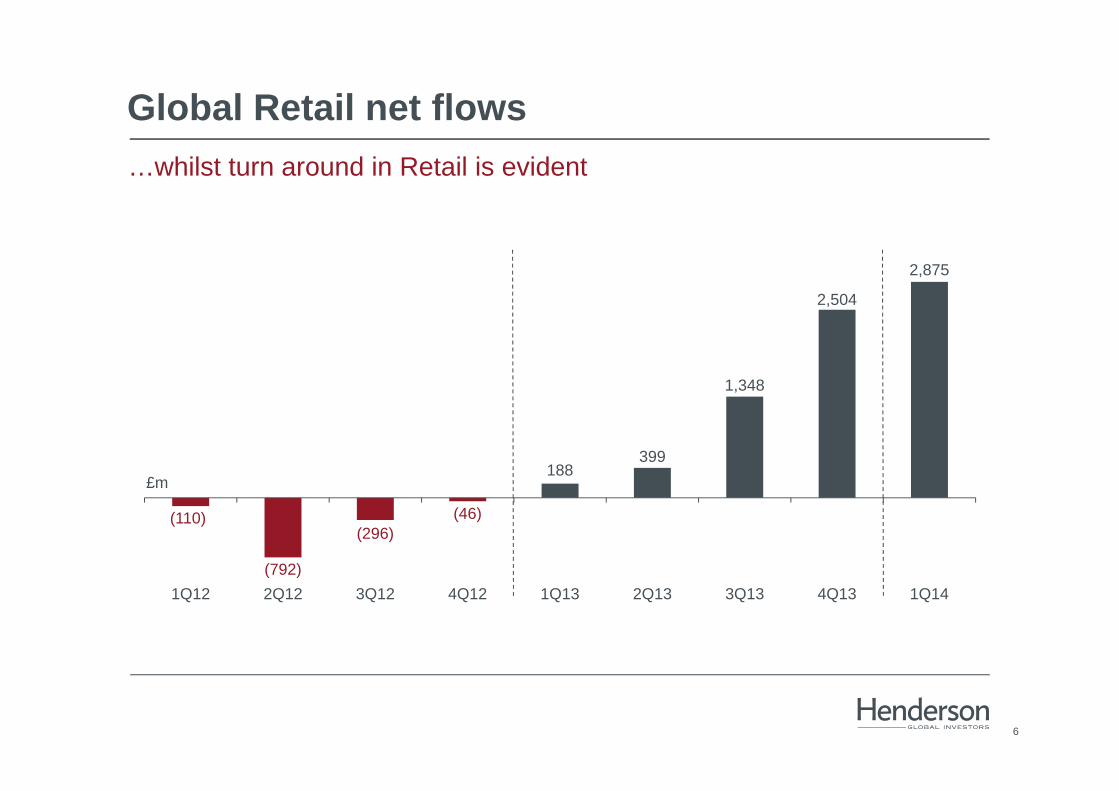

(110)

(792)

(296)(46)

188399

1,348

2,504

2,875

1Q12 2Q12 3Q12 4Q12 1Q13 2Q13 3Q13 4Q13 1Q14

Global Retail net flows…whilst turn around in Retail is evident

£m

7

(376) (367) (399)(337)

(159)

154

473

690 646

1Q12 2Q12 3Q12 4Q12 1Q13 2Q13 3Q13 4Q13 1Q14

Onshore OEIC / Unit Trust Retail net flowsRe-establishing our market position

£m

8

246

(252)

108

307

480

(36)

470

1,114

1,554

1Q12 2Q12 3Q12 4Q12 1Q13 2Q13 3Q13 4Q13 1Q14

Offshore SICAV Retail net flowsRecord Q1 2014 built off strong performance

£m

9

(25)

(164)

(16)

5

187

97

398

608 609

1Q12 2Q12 3Q12 4Q12 1Q13 2Q13 3Q13 4Q13 1Q14

US Mutuals Retail net flowsRobust Retail flows continuing in 2014

£m

10

(110)

(792)

(296)(46)

188399

1,348

2,504

2,875

1Q12 2Q12 3Q12 4Q12 1Q13 2Q13 3Q13 4Q13 1Q14

Global Retail net flows

£m

11

198 96

600

1,064419

251

356

410

173

18

68

135

27

190

67

73

100302

400

712

1Q13 2Q13 3Q13 4Q13

European Equities

Global Equities

Global Fixed Income

Multi-Asset

Alternatives

Diversity of flows by fund, strategy and geography20 Retail funds in FY13 with net flows of £100m+

£917m £857m

£1,491m

£2,394m

1Q14 continued this momentum: 10 Retail funds with net inflows of £100m+

12

What is Distribution?

• Sales

• Marketing communications

• Investment communications

• Client service

• Product strategy / development

• Brand

25% of Henderson’s staff work in Distribution which sits at the centre of the business

Clients

PortfolioManagers

Pre-financial crisis model

PortfolioSpecialists Sales Relationship

ManagersOperations

Loose coordination

Clients

PortfolioManagers

Emerging model

Sales OperationsRelationship Managers

PortfolioSpecialists

Tight coordination

Source: KPMG – Evolving Distribution Models in Asset Management.

13

What have we been doing?

Changed…• Our model• Our behaviour• Compensation• Building a global infrastructure

Focus…• Increasing and up skilling resources

in core markets• Rebranding the business• Globalising the product suite• Increasing marketing spend• Identifying key franchises and ‘run our winners’• Centres of excellence

Working as a team to help us better serve our clients

Old model

New model

Institutional

Retail LiquidAlternatives

Institutional

Retail LiquidAlternatives

14

Developing a truly global distribution model

Note: All data as at 31 Dec 2013.1 Based on total AUM.2 Includes Middle East and Africa.

Distribution31 FTEs

Distribution39 FTEs

Distribution23 FTEs

Distribution151 FTEsUK

66%AUM¹

North America11%AUM¹ Europe and

Latin America19%AUM¹,²

Asia / Australia4%AUM¹

15

New people

Head of EMEA Retail & LatAm

Greg Jones

Head of EMEA Institutional

Nick Adams

Head of Global MarketingRob Page

Head of Advisory SalesSam Mettrick

CEO of Japan Business

Shiro Tsubota

Head of Asia Wholesale

Mabel Chan

Head of Germany

Daniela Brogt

Head of Content

Darrel Billingham

Head of Distribution Australia

Matt Gaden

Head of Corporate Communications

Angela Warburton

…and more to come

16

Europe & Latin AmericaDepth and breadth in distribution supported by a strong brand presence

Note: Clients from the EMEA region are serviced either directly from London or through one of our European offices.1 Teams: UK Discretionary team, UK Advisory team, JV team (Telesales team 2Q14).2 Teams: UK Client & Consultant Relationships, Nordics & Netherlands Sales teams.

13

Private investors, financial advisers, platforms, discretionary wealth managers

UK Property, Cautious Managed, Strategic Bond, European Special Sits, Global Equity Income

8

Local authority pension funds, corporate pension funds, institutions, SWFs

Sterling Credit, Total Return Bond, Multi Asset Credit

3

Private investors, financial advisers, platforms, discretionary wealth managers

The City of London Investment Trust, Bankers Investment Trust

2

National pension funds (AFPs), banks, discretionary wealth managers

Absolute Return, European Equities, European long/short

17

Platforms, banks, insurance companies, discretionary wealth managers

European Equities,European Credit,Equities long/short,Global Equity Income

UK Retail¹ EMEA Institutional²

Investment Trusts Latin America Continental

Europe Retail

London, Paris, Milan, Amsterdam, Frankfurt, Zurich, Madrid base

Sales Professionals

Clients

Key Products

17

North America

18

Wire houses, wholesale platforms, RIA’s

Global Equity Income, European Focus, International Opportunities

3

State pension funds, corporate pension funds institutions

Global Equity, Global Fixed Income

Strong Retail Distribution network

US Retail US Institutional

Boston and Chicago base

Sales Professionals

Clients

Key Products

Note: Background reflects current Henderson US distribution territories.

18

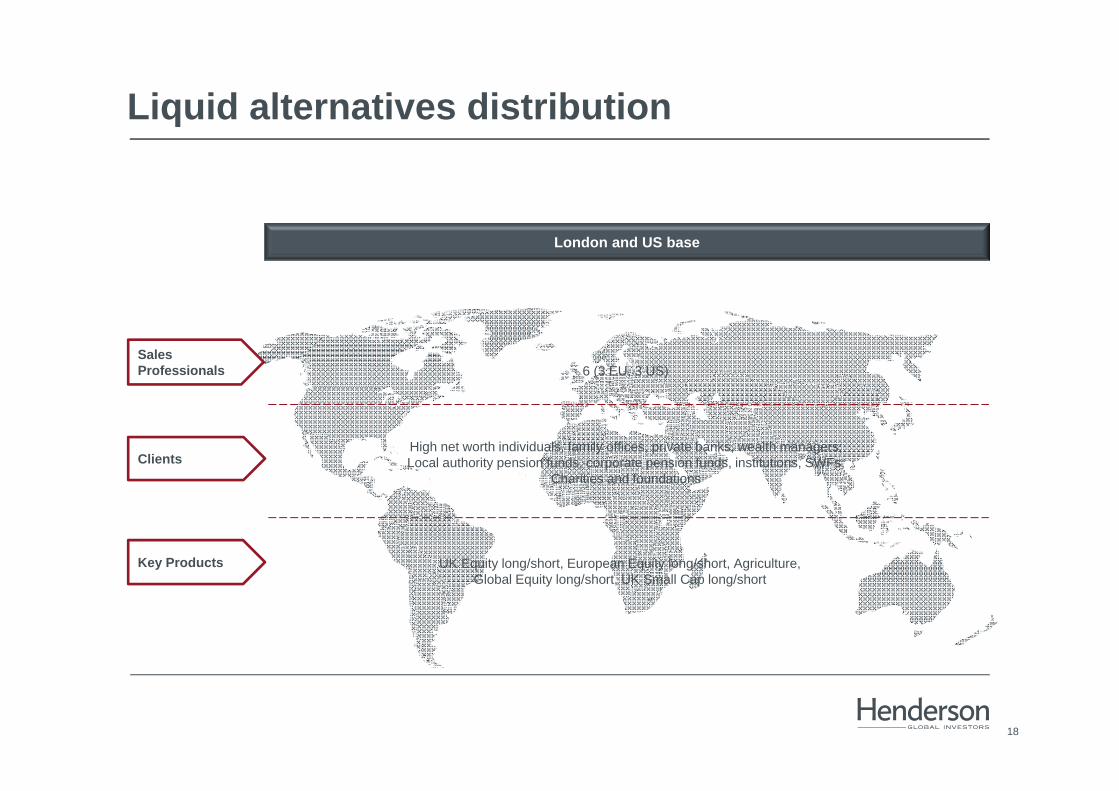

Liquid alternatives distribution

6 (3 EU, 3 US)

High net worth individuals, family offices, private banks, wealth managers;Local authority pension funds, corporate pension funds, institutions, SWFs;

Charities and foundations

UK Equity long/short, European Equity long/short, Agriculture, Global Equity long/short, UK Small Cap long/short

Sales Professionals

Clients

Key Products

London and US base

19

Global product governance framework

• Strategic – high-level / long-term • Product innovation• Life cycle review

• Execute new product ideas• Coordinate and prioritise initiatives

• Product specification• Stress testing• Pipeline reporting

Global Strategic Product Group

Product Implementation

Committee

Product and projects

stakeholder meetings

20

Global product development

1. Global Equity• EAFE & ACWI

2. Global Equity Income

3. Global Fixed Income• High Yield• Investment Grade• Emerging Market Debt

4. Unconstrained Bond Funds

5. Global Equity Long Short

1. Asian Equity

2. Natural Resources

3. Agriculture

4. Liquidity

5. Commodities

Strategic / Global Tactical / Regional

21

The winner takes it all

1,317

(564)-1,000

-500

0

500

1,000

1,500

Top 1% Remaining 99%

US mutual flows – Europe stock²Global flows 2013¹$bn

¹ Source: Morningstar Direct, Worldwide OE & MM ex FoF ex Feeder Database, as at Dec 2013.² Source: Morningstar Direct, US OE ex MM ex FoF Database, as at Dec 2013.³ Source: Morningstar Direct, Europe OE & MM ex FoF ex Feeder Database, as at Dec 2013.4 Source: IMA EchoWeb, as at Dec 2013.

2,739

738 738 707

0500

1,0001,5002,0002,5003,000

Top 5 Remaining 22funds

JP MorganIntrepid European

Fd

HendersonEuropean Focus

Fund

$m

European flows – European ex-UK large-cap equity³

2,947

5641,279

615 396 334 3220

1,0002,0003,0004,000

Top

5 fu

nds

Rem

aini

ng 1

49fu

nds

BG

FC

ontin

enta

l Eur

Flex

ible

Sta

ndar

d Li

feE

ur E

q In

c Fd

Thre

adne

edle

Eur

Sel

ect

Hen

ders

onG

artm

ore

Fund

Con

t Eur

ope

Fund

Bla

ckR

ock

Eur

opea

nD

ynam

ic

€mUK Retail flows – IMA Property4

Top 5 funds

569

2,511

0

500

1,000

1,500

2,000

2,500

3,000

Henderson UK Property Total sector

£m

Top selling fund in sector 2013

Top 2 funds

22

Henderson Horizon Euro Corporate Bond Fund

Source: Morningstar Direct, comparison with the Morningstar Fixed Income Euro-Corporate Universe, Lux domiciled funds only.

0

5

10

15

20

25

30

35

40

0.0 €

0.2 €

0.4 €

0.6 €

0.8 €

1.0 €

1.2 €

1.4 €

1.6 €

1.8 €

2.0 €

Dec

-09

Mar

-10

Jun-

10

Sep

-10

Dec

-10

Mar

-11

Jun-

11

Sep

-11

Dec

-11

Mar

-12

Jun-

12

Sep

-12

Dec

-12

Mar

-13

Jun-

13

Sep

-13

Dec

-13

Henderson Hz Euro Corp Bd FdHenderson Hz Euro Corp Bd Fd Performance

Henderson Horizon Euro Corporate Bond Fund since inception

• Second best performing fund in the sector since inception

• Second best net selling fund in the sector in the past 2 years

• 1.68% market share in the Morningstar EUR Corporate Bond sector

December 2010The first anniversary of the fund marks the beginning of marketing activities supporting sales efforts to establish Henderson’s reputation as a FI fund manager.

With client interest in Credit remaining high, marketing activity focused heavily on:• Sponsored events: 12 events across Europe, including high

profile pan-European events • Major PR focus principally in France, Germany and Italy• Webcasts (on average every trimester), supported by transcripts• Frequent webinars on topical issues• Frequent collateral, such as ‘Fund updates’ and

‘View from the Credit desk’• Exact target from September 2011Higher level of marketing activity coincides with rising flows into the fund.

2011 – 2013

Marketing activities on this fund scaled back to make use of limited fund managers’ time on promotion of EHY and GHY fund.

2014

23

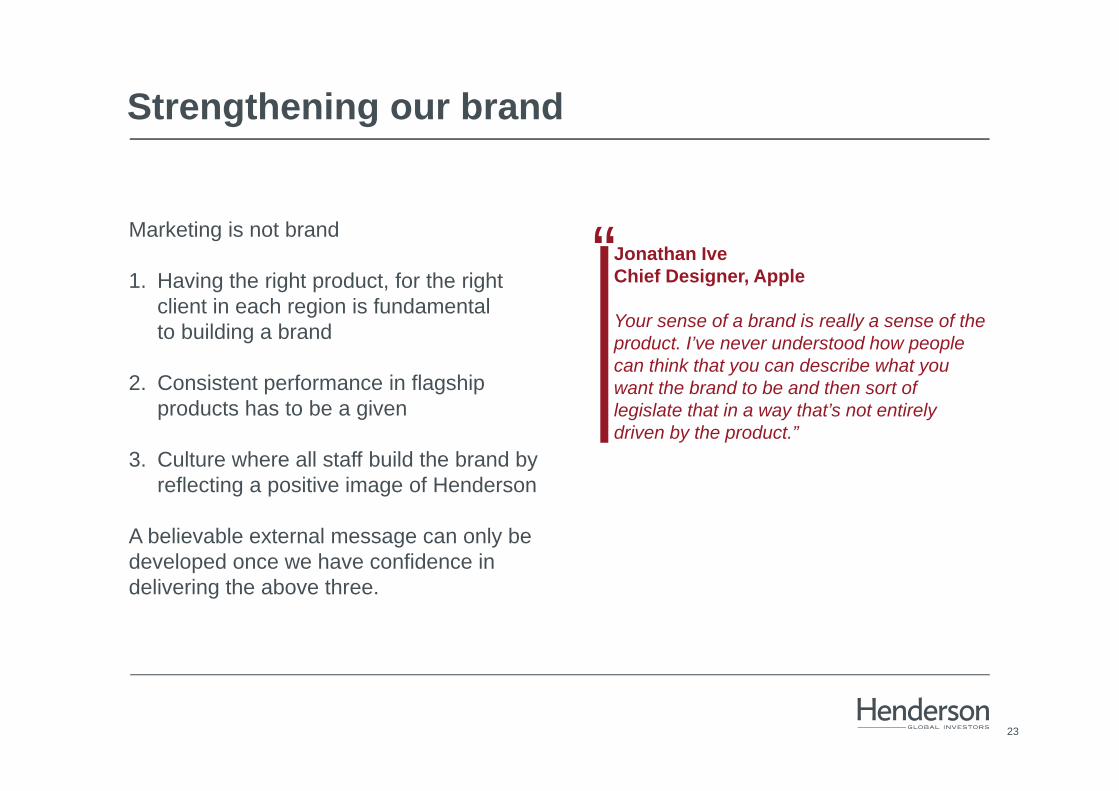

Strengthening our brand

Marketing is not brand

1. Having the right product, for the right client in each region is fundamental to building a brand

2. Consistent performance in flagship products has to be a given

3. Culture where all staff build the brand by reflecting a positive image of Henderson

A believable external message can only be developed once we have confidence in delivering the above three.

Jonathan IveChief Designer, Apple

Your sense of a brand is really a sense of the product. I’ve never understood how people can think that you can describe what you want the brand to be and then sort of legislate that in a way that’s not entirely driven by the product.”

“

24

Rebrand

• Sophisticated, upmarket

• Non retail leverage

• Non UK leverage

• More coherent and consistent

• New websites

Why?

• A fresh start for Henderson

• A line in the sand post M&A

• Establish our credentials around our core competencies

• Position Henderson as an intelligent, sophisticated and aspirational brand

• Positioned for todays clients –the buying process is institutionalised

• Allow us to engage with our audience through the various routes to market and establish

Objectives

25

Our competitive advantage

• RDR means that existing brands are more desirable

• High barriers to entry for guided architecture• Strong fit of product to market demand

UK Retail

• Well established sub-brand AlphaGen• Operational expertise• Cultural advantage over traditional asset

managers

Liquid Alternatives

• Existing relationships with wirehouses and platforms

• High barriers to entry

US Retail

• Established network of local offices, local languages and support to build on

• Strong fit of product to market demand

Continental Europe

Rob AdamsExecutive Chairman, Asia Pacific

Global Distribution Strategy – Focus on Asia

27

Why Asia?

• Asian Century is upon us – by 2030 Asian GDP will be greater than 35% of global GDP¹

• Asia will comprise 22% of global investment management revenues over the next 5 years (US$385 billion)2

• Sovereign funds, large Japanese pensions and Australian superannuation shape the Asian institutional opportunity

• Henderson has a good foot-print in key markets, but needs to build strong “franchise” capabilities

• Focus will be critical…• Asia’s top 50 asset owners represent 90% of the institutional revenue opportunity • Australia will drive the DC market• Japan will drive the retail sub-advisory market (local partnership opportunity)• China could become a major growth engine (local partnership opportunity)

Pan Asia should become a growth engine for Henderson

¹ Source: ANZ – “The Caged Tiger – the Transformation of the Asian Financial System” , March 2014

2 Source: Casey Quirk.

28

Asia’s heterogeneous marketplaces force firms to make concentrated bets

Market dynamics Competitive dynamics Success factors Henderson focus

• Deteriorating corporate pension funding• Lack of domestic income‐generating

instruments

• Most local players abandoning global product

• Local distributors seek foreign brand names for thematic offers

• High‐yielding, credit‐oriented products• Sub-advisory relationships with key

providers and local distributors

• Substantial fee pressure from regulators• Growing need to diversify domestic‐heavy

portfolios overseas

• Oversupply in Australian equities• Greater need to move toward passive and

alternative mandates in superannuation

• Differentiated global equity and alternatives

• Access to higher‐fee market segments such as SMSF, HNW

• MPF fee pressure reduces growth• Local HNW marketplace increasingly

RMB‐denominated

• Chinese players linking HK, mainland vendors

• More unified “Greater China” market will create more intense local competition

• Local products and structures• Strong mainland‐oriented partners• Range of global strategies

• Regulators opening new pools of assets• Global product demand slowly rising as

government eases curbs

• Highly concentrated distribution• Regulatory arbitrage favours “national

champions”

• Strong JV partner…• …offset with individual firm ties to

insurers, distributors, trusts

• Pension reform poor growth catalyst• Local HNW marketplace sophisticated• Local structures increasingly favoured

• Master trust rule changes could impede offshore fund sales

• Local competitors to tie up with mainland

• Local SITE/SICE infrastructure• Connections with strongest local FHC

distributors

• Strong sovereigns, weak retail demand• HNW booking centre for Asian wealth

• Sovereigns insourcing significantly• Retail favours brand names that play well in

CPFIS

• Local presence• Alternatives, global products for HNW

investors

• Demand focused on local, regional product• Sovereign and pension market growing

• Aggressively globalising local players• Waning interest in cross‐border funds

• Local product development• Bank distributor connections

Secondary Focus

• Fund flows roiled by regulatory changes• No institutional market on horizon

• Local players have best distribution links• Slim demand for non‐Indian product

• Ownership in solid local manager• Long‐term strategy for asset accretion

Greater China

Source: Casey Quirk.

29

Pan AsiaExpanding distribution presence

2

SWFs, platforms, banks, institutions, distribution partnerships

Global Equities,Global Fixed Income,Hedge funds

4

National pension funds, institutions, banks, distribution partnerships

Global Equities, Global Fixed Income,Managed Futures, Hedge funds

3

Super funds, institutions, charities, platforms, banks, financial advisors, SMSFs

Global Equity, Global Fixed Income,Enhanced Index, Global Commodities, Global Resources

6

Banks, discretionary wealth managers, institutions, private banks

Global Equities, Global Fixed Income, Hedge funds, Global Property, European Equities

Greater China Japan Australia Rest of Asia

Singapore, Hong Kong, Sydney, Tokyo base

Sales Professionals

Clients

Key Products

30

Blueprint for Pan Asia

• Gain better leverage from existing business operations in Singapore, Tokyo, Hong Kong & Beijing

• Likely requirement for local product structures• Investigate partnership opportunities to accelerate growth

• Strong focus on promoting our global capabilities• Re-shape Asian equities under new leadership• Focus on key institutional relationships

• Develop a strong institutional brand• Build a diversified book of AUM – global + local capabilities• Become a solid contributor to Group

Leverage local business

infrastructure

Introduce key capabilities to

market

Build brand presence and

grow AUM

31

Spotlight on Australia

• Local team, full RE license, local transactions• Approach shows long-term commitment • Build on positive brand perception

• ‘Import’ rated and relevant capabilities - global• Local deals with local and global appeal (‘export’)• Demonstrate commitment to the market

• Develop a strong institutional brand• Build a diversified book of AUM – dominated by global capabilities• Become a solid contributor to Group

Create local business

infrastructure

Introduce key capabilities to

market

Build brand presence and

grow AUM

32

Competing in Australia’s crowded market

• Pure play active manager, with diversification of offers

• Focus on contemporary global capabilities

• Best quality local team, combining with world-class PMs

• No legacy – a clean sheet and an open mind

• Historical connection with Australia

Early signs support our aspirations

33

For Pan Asia…

Build core product franchises across Asia

Institutionally recognised

Active partnerships delivering

Become a material contributor to the Group

Build foundation for Australia

Re-assess Asia strategy

Produce a plan that sees Asia as a key growth contributor

Investigate strategic partnerships in key markets

Create focus

Last 2 years Next 3 years

…back to the global plan…

34

Back to the 5 year plan

Globalise the product suite

Institutional development• US• Europe• Asia

European and LatAm Retail expansion

Japan on stream

Australia on stream

People upgrades/ culture

Process

Product development

Brand

Home market strength

Retail

Last 2 years Next 3 years

…only the start of the journey

35

Henderson Global Investors201 Bishopsgate, London EC2M 3AETel: 020 7818 1818 Fax: 020 7818 1819

G:\CreativeServices\UK\2014\!Presentations\Gen14\Sydney Investor Presentation 20140422.pptx

Important informationThis document is intended solely for the use of professionals, defined as Eligible Counterparties or Professional Clients, and is not for general public distribution.

Past performance is not a guide to future performance. The value of an investment and the income from it can fall as well as rise and you may not get back theamount originally invested. Tax assumptions and reliefs depend upon an investor’s particular circumstances and may change if those circumstances or the lawchange.

If you invest through a third party provider you are advised to consult them directly as charges, performance and terms and conditions may differ materially.

Nothing in this document is intended to or should be construed as advice. This document is not a recommendation to sell or purchase any investment. It doesnot form part of any contract for the sale or purchase of any investment.

Any investment application will be made solely on the basis of the information contained in the Prospectus (including all relevant covering documents), which willcontain investment restrictions. This document is intended as a summary only and potential investors must read the prospectus, and where relevant, the keyinvestor information document before investing.

Issued in the UK by Henderson Global Investors. Henderson Global Investors is the name under which Henderson Global Investors Limited (reg. no. 906355),Henderson Fund Management Limited (reg. no. 2607112), Henderson Investment Funds Limited (reg. no. 2678531), Henderson Investment ManagementLimited (reg. no. 1795354), Henderson Alternative Investment Advisor Limited (reg. no. 962757), Henderson Equity Partners Limited (reg. no.2606646),Gartmore Investment Limited (reg. no. 1508030), (each incorporated and registered in England and Wales with registered office at 201 Bishopsgate, LondonEC2M 3AE) are authorised and regulated by the Financial Conduct Authority to provide investment products and services. Telephone calls may be recorded andmonitored. Ref: 34S