pw kitt co pty ltd (in liquidation) acn 635 767 047 (pwk

TRANSCRIPT

1

PW Kitt Co Pty Ltd (In Liquidation) ACN 635 767 047

(PWK)

Statutory Report to Creditors

We refer to the initial information for creditors dated 3 December 2020 in which you were advised of the appointment of Michael Hill, Anthony Connelly and Kathy Sozou as Liquidators of PWK on 5 November 2020 and your rights as a creditor in the liquidation.

The purpose of this report is to:

provide you with an update on the progress of the liquidation; and

advise you of the likelihood of a dividend being paid in the liquidation.

Update on the progress of the liquidation

Background and events leading up to the liquidation

The Liquidators’ understanding of PWK’s history is as follows:

On 7 August 2020, the Federal Court of Australia (FCA) ordered that Michael Hill, Anthony Connelly and Katherine Sozou of McGrathNicol be appointed as Receivers and Managers (Receivers) to the property and assets of:

− Larry John Dawson (Mr Dawson); and

− PWK (ACN 635 767 047)

− (collectively, the Defendants).

The Receivers were to conduct certain investigations into the pre-appointment affairs of the Defendants and to provide a Report to the Court within 42 days which addressed:

− the identification of the assets and liabilities of the Defendants;

− an opinion as to the solvency of the Defendants;

− an opinion as to the value of the assets of the Defendants;

− the likely return to creditors if PWK is wound up;

− an opinion as to whether PWK holds proper financial records;

− any other information necessary to enable the financial position of the Defendants to be assessed;

− any suspected contraventions of the Act by PWK; and

− any suspected contraventions of the Act by Mr Dawson in his personal capacity and in his capacity as a director of PWK.

The Receivers’ provided the Report to the FCA on 26 August 2020. The Australian Securities and Investments Commission (ASIC) brought this matter before the FCA on the basis of suspected fraudulent activity in relation to PWK. The Receivers’ investigations supported ASIC’s concerns and, on that basis, ASIC sought to have PWK wound up.

On 5 November 2020, the FCA ordered PWK be wound up and that Michael Hill, Anthony Connelly and Katherine Sozou of McGrathNicol be appointed as Liquidators, at which time the receivership of PWK ceased. The Receivers continue to be appointed over Mr Dawson’s assets.

In late 2020, Mr Dawson was arrested by the New South Wales police force and charged with 48 fraud offences. Any specific queries in this regard should be directed to the New South Wales police force.

2

Offices and personnel

The Liquidators have been unable to identify a physical location from which PWK operated. On 10 August 2020, the Receivers’ staff members physically attended the PWK registered office located at Level 36, Governor Phillip Tower, 1 Farrer Place, Sydney, NSW 2000. This was a virtual office whereby there was an agreement for PWK to use the receptionist services and to list the office address on their websites, pwkittco.com and smsfadvisory.com (Websites). There was no physical PWK presence at this location.

The Websites also listed the following offices of PWK:

Level 33, Australia Square, 264 George Street, Sydney, NSW 2000; and

Level 24, Three International Towers, 300 Barangaroo Avenue, Sydney, NSW.

The Receivers’ staff members also attended the above addresses. Similarly, these addresses were virtual offices with no physical PWK presence.

The Liquidators understand investors liaised with various individuals purporting to be associated with PWK; however, the Liquidators have been unable to make contact with anyone associated with PWK other than Mr Dawson. The Liquidators’ investigations to date indicate the various individuals purporting to be associated with PWK may not exist and may in fact be aliases.

Estimated assets

The Liquidators have not received any books and records of PWK and have had to rely on searches of available public information and information provided by third parties to understand the assets of PWK as at the date of the appointment of the Receivers, which are detailed below.

Estimated assets

Description Note At appointment of Receivers ($) Liquidators' estimate ($) ROCAP ($)

Cash at bank 1.3.1 60,247.15 60,247.15 Unknown

Pre-appointment debtor 1.3.2 10,500.00 10,500.00 Unknown

Cryptocurrency 1.3.3 54,770.25 54,770.25 Unknown

Total assets 125,517.40 125,517.40

1.3.1 Cash at bank

On appointment of the Receivers, the following banks responded advising of accounts held in the name of PWK:

Australia and New Zealand Banking Group;

Bendigo and Adelaide Bank;

Bank of Queensland;

Commonwealth Bank of Australia;

St George Bank; and

Westpac Banking Corporation.

The majority of these accounts have been closed and the remaining funds were transferred to the PWK receivership or liquidation bank accounts. The Liquidators are continuing to liaise with the remaining banks to transfer the closing balances into the PWK liquidation bank account. The Liquidators do not anticipate any further recoveries in relation to cash at bank in addition to what is listed in the table above.

Certain investors transferred funds into the PWK bank accounts following the Receivers’ appointment on 7 August 2020. The Liquidators are in the process of returning these post-appointment advances of funds to the relevant investors. The Liquidators are unable to return funds to investors who transferred funds to PWK prior to the Receivers' appointment.

3

1.3.2 Pre-appointment debtor

On 2 October 2020, the Receivers wrote to two pre-appointment debtors that were disclosed on the Report on Company Activities and Property (ROCAP) submitted by Mr Dawson for undisclosed amounts owing in relation to loans. Following this, the Receivers recovered $10,500 from one of the pre-appointment debtors. The remaining disclosed pre-appointment debtor, who is located overseas, has not responded to the Receivers or Liquidators’ requests or correspondence. The Liquidators do not anticipate any further debtor recoveries.

1.3.3 Cryptocurrency

The Liquidators are aware that approximately $8.4 million was received into bank accounts held in the name of PWK during the period 3 September 2019 to 23 July 2020. Most of the funds raised from investors appear to have been paid into PWK bank accounts and subsequently disbursed to other accounts that appear to be inconsistent with the purpose for which they were invested; for example, a significant amount of money was transferred to bitcoin exchanges.

It appears that a significant portion of the money was transferred overseas, particularly to what may be entities in Indonesia. The Liquidators’ review of a sample of the bitcoin transactions conducted through the CoinSpot bitcoin exchange in Australia, suggests the majority of the bitcoins acquired by PWK were sent to a wallet that appears to be associated with an Indonesian bitcoin exchange.

Given the bitcoins held in the PWK CoinSpot account have all been transferred to other bitcoin addresses and then subsequently transferred to a series of other addresses, it is almost impossible to identify the ultimate recipient of the bitcoins purchased by PWK.

The Receivers notified both CoinSpot and Independent Reserve, two bitcoin exchanges, of the appointment and froze the PWK accounts held with each exchange. The Receivers requested the exchanges sell any non-AUD holdings for AUD and transfer the total available funds to the PWK receivership bank account. Following the conversation of bitcoin to AUD, the funds received from CoinSpot and Independent Reserve were $25,749.34 and $29,020.91 respectively.

1.3.4 Other assets

The Liquidators are unable to identify the extent of any other assets that PWK may own, which may include recoveries from the entity or entities to which the creditor funds were transferred, directly or indirectly. Given the nature of the way in which the funds were disbursed, it appears that that there will be difficulties in obtaining significant recoveries of assets belonging to PWK. At this stage and without further information becoming available, the Liquidators do not anticipate any further asset recoveries for the benefit of creditors in the liquidation of PWK.

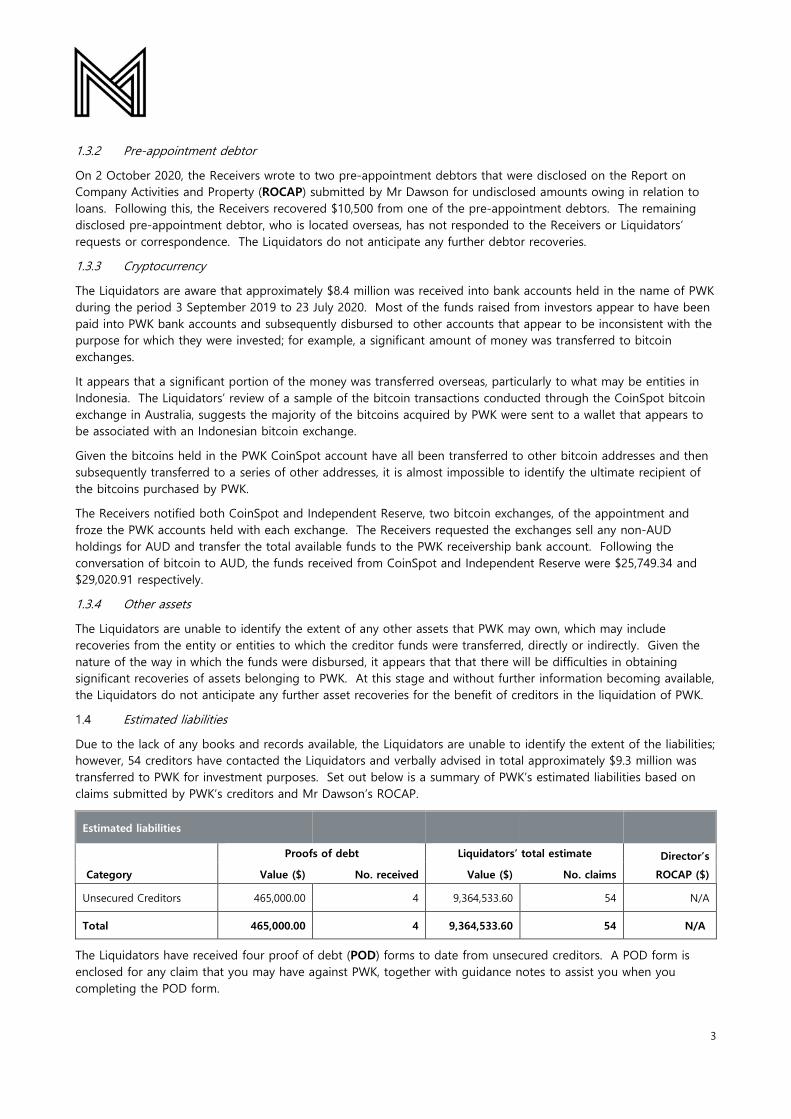

Estimated liabilities

Due to the lack of any books and records available, the Liquidators are unable to identify the extent of the liabilities; however, 54 creditors have contacted the Liquidators and verbally advised in total approximately $9.3 million was transferred to PWK for investment purposes. Set out below is a summary of PWK’s estimated liabilities based on claims submitted by PWK’s creditors and Mr Dawson’s ROCAP.

Estimated liabilities

Category

Proofs of debt Liquidators’ total estimate Director’s

ROCAP ($) Value ($) No. received Value ($) No. claims

Unsecured Creditors 465,000.00 4 9,364,533.60 54 N/A

Total 465,000.00 4 9,364,533.60 54 N/A

The Liquidators have received four proof of debt (POD) forms to date from unsecured creditors. A POD form is enclosed for any claim that you may have against PWK, together with guidance notes to assist you when you completing the POD form.

4

The Liquidators have insufficient evidence to indicate any secured creditors and the Personal Properties and Securities Register search results indicate no party has registered a security interest against PWK.

Investigations

The Liquidators have lodged a section 533 report with ASIC and commenced their statutory investigations into PWK’s affairs using information made available by third parties. Our investigations to date indicate the following:

it appears Mr Dawson breached the director duties, obligations and responsibilities imposed on him pursuant to sections 180 to 184 of the Corporations Act 2001 (the Act);

it appears Mr Dawson engaged in fraudulent conduct pursuant to section 590 of the Act;

it appears Mr Dawson breached sections 286 and 364 of the Act in respect of maintaining books and records to correctly record and explain PWK’s transactions and financial position and performance; and

the books and records were insufficient to establish insolvent trading and whether there are any voidable transactions (including unfair preference payments).

At this stage, we are unable to comment on whether there will be potential recoveries available for the benefit of creditors.

The Liquidators intend to submit an Assetless Administration Fund (AAF) funding request with ASIC shortly. If successful, ASIC would provide funding to the Liquidators to enable further investigations to be conducted into PWK’s pre-appointment affairs. The Liquidators will provide creditors with an update regarding the outcome of their AAF funding request in due course.

Receipts and payment to date

Enclosed are details of all receipts and payments for the following appointments and periods:

receivership from 7 August 2020 to 5 November 2020; and

liquidation from 5 November 2020 to 1 February 2021.

Likelihood of a dividend

A number of factors will affect the likelihood of a dividend being paid to creditors, including:

the size and complexity of the liquidation;

the amount of assets realisable and the costs of realising those assets;

the statutory priority of certain claims and costs;

the value of various classes of claims including secured, priority and unsecured creditor claims, and

the volume of enquiries by creditors and other stakeholders.

Based on information available to us at this time, and absent any unforeseen issues, we consider it unlikely that a dividend may be payable to creditors with admitted claims in the liquidation.

If a dividend is going to be paid, you will be contacted before that happens and, if you have not already done so, you will be asked to lodge a POD form. This formalises the record of your claim in the liquidation and is used to determine all claims against PWK.

Cost of the liquidation

As previously advised in the initial information to creditors, the Liquidators estimated that the total remuneration for the liquidation of PWK would be approximately $100,000 (GST exclusive). However, remuneration can only be paid from available funds in the liquidation. We do not get paid if there are insufficient asset realisations and/or recoveries.

5

What happens next?

We will proceed with the liquidation, which will include:

recovering any further available property;

submitting an AAF funding request with ASIC;

completing further investigations into PWK’s affairs (if the AAF funding request is successful);

if identified, pursuing any viable claims for statutory recovery actions; and

completing the necessary reports to the corporate insolvency regulator, ASIC.

We will write to you again with further information on the progress of the liquidation within three months from the date of this report. The Liquidators estimate it may take more than one year to finalise the liquidation due to the complex nature of the investigations and ASIC’s requirements.

Where can you get more information?

You can access information which may assist you on the following websites:

ARITA at www.arita.com.au/creditors.

ASIC at www.asic.gov.au (search for “insolvency information sheets”).

If you have any queries, please contact Georgia Wilson on (07) 3333 9818. For further information about this engagement, please refer to the website from https://www.mcgrathnicol.com/creditors/pw-kitt-co-pty-ltd/.

Dated: 5 February 2021

Michael Hill Liquidator

Enclosures:

Proof of Debt (Form 535)

Proof of Debt Guidance Notes

Receipts and payments for the period of the receivership from 7 August 2020 to 5 November 2020

Receipts and payments for the period of the liquidation from 5 November 2020 to 1 February 2021

ARITA Information Sheet – Offences, Recoverable Transactions & Insolvent Trading

Subregulation 5.6.49(2)

FORM 535

FORMAL PROOF OF DEBT OR CLAIM (GENERAL FORM)

ACN

“the Company”

To the Liquidator/Administrator of the Company

1. This is to state that the Company was on , and still is, justly and truly indebted to:

___________________________________________________________________________________________________ (name of creditor)

of _____________________________________________________________________________________________ (address of creditor)

for $_________________________and____________cents (GST inclusive) GST amount _______________________________

Date Consideration (state how the

Debt arose)

Amount

$ c

Remarks (include details of

voucher substantiating payment)

2. To my knowledge or belief the creditor has not, nor has any person by the creditor's order, had or received any

satisfaction or security for the sum or any part of it except for the following: (insert particulars of all securities

held. If the securities are on the property of the company, assess the value of those securities. If any bills or

other negotiable securities are held, show them in a schedule in the following form).

Date Drawer Acceptor Amount $c Due Date

3. Select which of the below applies (choose one):

The creditor is a company and I am signing as

a director of the company The creditor is a partnership and I am signing as

a partner of the partnership

The creditor is a company and I am signing as

an authorised representative/duly constituted

attorney of the company

I am signing in my personal capacity as a

member or contributory of the Company

I am an individual and I am signing in my

personal capacity (which includes employees) Other: ____________________________________________

The creditor is a sole trader and I am signing

as the proprietor

Page 1 of 2

4. If you are a related party, state your relationship ________________________________________________________________

This debt was inncurred for the consideration stated and the debt, to the best of my knowledge and belief,

remains unpaid and unsatisfied.

Signature ............................................................................................ Dated ………………………………………………………..

Name: ___________________________________________________________

Address: ____________________________________________________________________________________________________________

Page 2 of 2

5. Is this debt claimed on the basis of an assignment? Yes☐ No☐If so, what consideration was paid for the debt? _________________________

☐ I nominate to receive electronic notifications of documents in accordance with Section 600G of the

Corporations Act at the following email address

Email: __________________________________________________

1

Proof of Debt

Guidance Notes

(Please read carefully before filling in Form 535 or Form 536)

It is a creditor’s responsibility to prove their claim to our satisfaction.

When lodging claims, creditors must ensure:

the proof of debt form is properly completed in every particular; and

evidence, as set out under “Information to support your claim”, is attached to the Form 535 or Form 536.

Directions for completion of a Proof of Debt

1. Insert the full name and address of the creditor.

2. Under “Consideration” state how the debt arose, for example “goods sold to the company on

______________________”.

3. Under “Remarks” include details of any documents that substantiate the debt (refer to the section “Information

to support your claim” below for further information).

4. Where the space provided for a particular purpose is insufficient to contain all the information required for a

particular item, please attach additional information.

Information to support your claim

Please note that unless you provide evidence to support the existence of the debt, your debt is not likely to be

accepted. Detailed below are some examples of debts creditors may claim and a suggested list of documents that

should accompany a proof of debt to substantiate the debt.

Trade Creditors

Invoice(s) and statement(s) showing the amount of the debt; and

Advice(s) to pay outstanding invoice(s) (optional).

Guarantees/Indemnities

Executed guarantee/indemnity;

Notice of Demand served on the guarantor; and

Calculation of the amount outstanding under the guarantee.

Judgment Debt

Copy of the judgment; and

Documents/details to support the underlying debt as per other categories.

Deficiencies on Secured Debt

Security Documents (eg. mortgage);

Independent valuation of the secured portion of the debt (if not yet realised) or the basis of the creditor’s

estimated value of the security;

Calculation of the deficiency on the security; and

Details of income earned and expenses incurred by the secured creditor in respect of the secured asset since the

date of appointment.

Loans (Bank and Personal)

Executed loan agreement; and

2

Loan statements showing payments made, interest accruing and the amount outstanding as at the date of

appointment.

Tax Debts

Documentation that shows the assessment of debts, whether it is an actual debt or an estimate, and separate

amounts for the primary debt and any penalties.

Employee Debts

Basis of calculation of the debt;

Type of Claim (eg. wages, holiday pay, etc);

Correspondence relating to the debt being claimed; and

Contract of Employment (if any).

Leases

Copy of the lease; and

Statement showing amounts outstanding under the lease, differentiating between amounts outstanding at the

date of the appointment and any future monies.

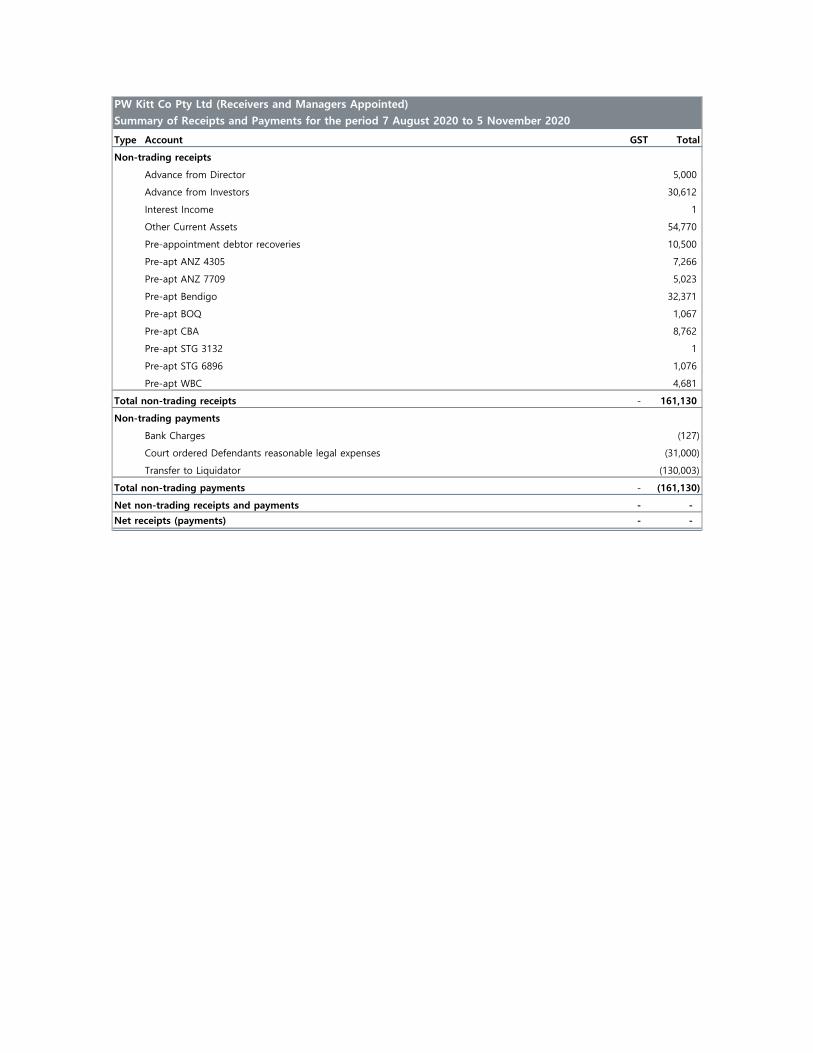

Type Account GST Total

Non-trading receipts

Advance from Director 5,000

Advance from Investors 30,612

Interest Income 1

Other Current Assets 54,770

Pre-appointment debtor recoveries 10,500

Pre-apt ANZ 4305 7,266

Pre-apt ANZ 7709 5,023

Pre-apt Bendigo 32,371

Pre-apt BOQ 1,067

Pre-apt CBA 8,762

Pre-apt STG 3132 1

Pre-apt STG 6896 1,076

Pre-apt WBC 4,681

Total non-trading receipts - 161,130

Non-trading payments

Bank Charges (127)

Court ordered Defendants reasonable legal expenses (31,000)

Transfer to Liquidator (130,003)

Total non-trading payments - (161,130)

Net non-trading receipts and payments - -

Net receipts (payments) - -

PW Kitt Co Pty Ltd (Receivers and Managers Appointed)

Summary of Receipts and Payments for the period 7 August 2020 to 5 November 2020

Type Account GST Total

Non-trading receipts

Advance from Investors 22,020

Pre-apt STG 3132 2,100

Pre-apt WBC 24,750

Returned payments 2,365

Transfer from Receiver and Manager 130,003

Total non-trading receipts - 181,238

Non-trading payments

Advance from Investors (30,612)

Bank Charges (95)

Returned payments (2,365)

Total non-trading payments - (33,072)

Net non-trading receipts and payments - 148,166

Net receipts (payments) - 148,166

PW Kitt Co Pty Ltd (In Liquidation)

Summary of Receipts and Payments for the period 5 November 2020 to 1 February 2021

Note: The Liquidators have not received statements from ANZ since 5 November 2020 after various requests. The receipts and payments in respect of ANZ has been prepared based on the monies received into the PWK liquidation bank account noting there are immaterial bank charges and interest that are yet to be confirmed once ANZ provides the Liquidators with the final statements.

Creditor Information Sheet Offences, Recoverable Transactions and Insolvent Trading

AUSTRALIAN RESTRUCTURING INSOLVENCY & TURNAROUND ASSOCIATION

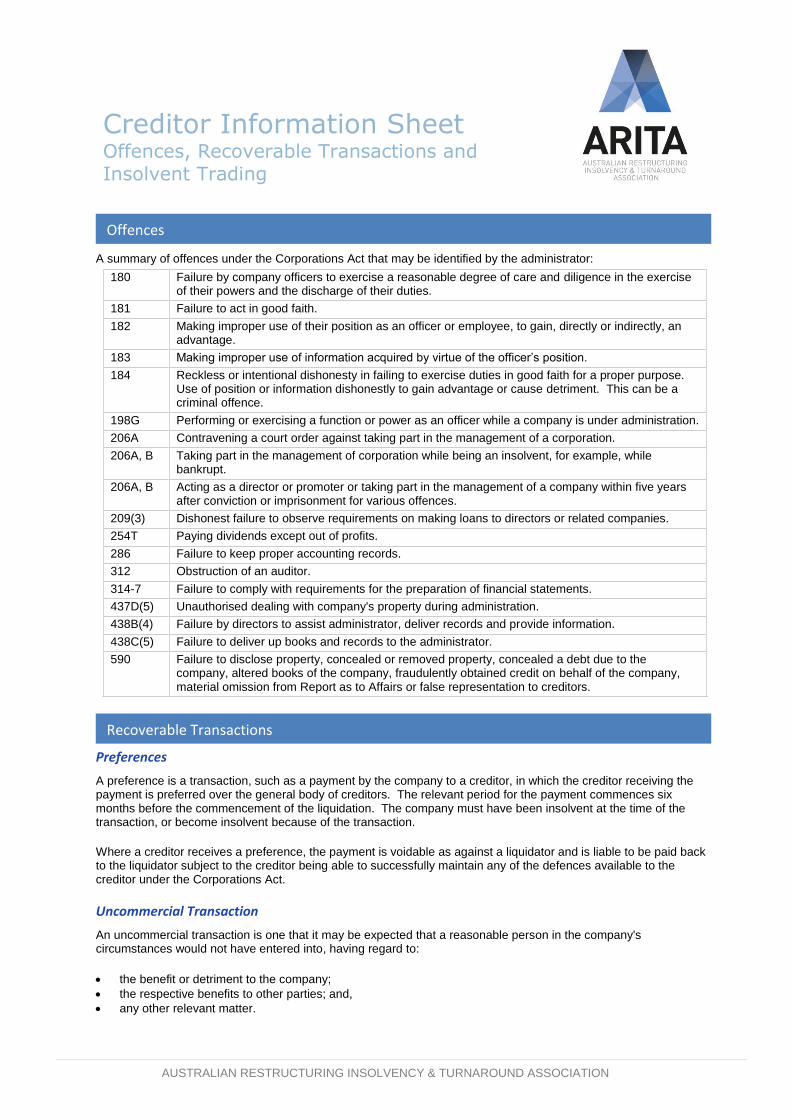

A summary of offences under the Corporations Act that may be identified by the administrator: 180 Failure by company officers to exercise a reasonable degree of care and diligence in the exercise

of their powers and the discharge of their duties. 181 Failure to act in good faith. 182 Making improper use of their position as an officer or employee, to gain, directly or indirectly, an

advantage. 183 Making improper use of information acquired by virtue of the officer’s position. 184 Reckless or intentional dishonesty in failing to exercise duties in good faith for a proper purpose.

Use of position or information dishonestly to gain advantage or cause detriment. This can be a criminal offence.

198G Performing or exercising a function or power as an officer while a company is under administration. 206A Contravening a court order against taking part in the management of a corporation. 206A, B Taking part in the management of corporation while being an insolvent, for example, while

bankrupt. 206A, B Acting as a director or promoter or taking part in the management of a company within five years

after conviction or imprisonment for various offences. 209(3) Dishonest failure to observe requirements on making loans to directors or related companies. 254T Paying dividends except out of profits. 286 Failure to keep proper accounting records. 312 Obstruction of an auditor. 314-7 Failure to comply with requirements for the preparation of financial statements. 437D(5) Unauthorised dealing with company's property during administration. 438B(4) Failure by directors to assist administrator, deliver records and provide information. 438C(5) Failure to deliver up books and records to the administrator. 590 Failure to disclose property, concealed or removed property, concealed a debt due to the

company, altered books of the company, fraudulently obtained credit on behalf of the company, material omission from Report as to Affairs or false representation to creditors.

Preferences

A preference is a transaction, such as a payment by the company to a creditor, in which the creditor receiving the payment is preferred over the general body of creditors. The relevant period for the payment commences six months before the commencement of the liquidation. The company must have been insolvent at the time of the transaction, or become insolvent because of the transaction.

Where a creditor receives a preference, the payment is voidable as against a liquidator and is liable to be paid back to the liquidator subject to the creditor being able to successfully maintain any of the defences available to the creditor under the Corporations Act.

Uncommercial Transaction

An uncommercial transaction is one that it may be expected that a reasonable person in the company's circumstances would not have entered into, having regard to:

• the benefit or detriment to the company; • the respective benefits to other parties; and, • any other relevant matter.

Offences

Recoverable Transactions

AUSTRALIAN RESTRUCTURING INSOLVENCY & TURNAROUND ASSOCIATION PAGE 2

Version: August 2017 22143 (VA) - INFO - Offences recoverable transactions and insolvent trading v1_1.docx1

To be voidable, an uncommercial transaction must have occurred during the two years before the liquidation. However, if a related entity is a party to the transaction, the period is four years and if the intention of the transaction is to defeat creditors, the period is ten years.

The company must have been insolvent at the time of the transaction, or become insolvent because of the transaction.

Unfair Loan

A loan is unfair if and only if the interest was extortionate when the loan was made or has since become extortionate. There is no time limit on unfair loans – they only must be entered into before the winding up began.

Arrangements to avoid employee entitlements

If an employee suffers loss because a person (including a director) enters into an arrangement or transaction to avoid the payment of employee entitlements, the liquidator or the employee may seek to recover compensation from that person. It will only be necessary to satisfy the court that there was a breach on the balance of probabilities. There is no time limit on when the transaction occurred.

Unreasonable payments to directors

Liquidators have the power to reclaim ‘unreasonable payments’ made to directors by companies prior to liquidation. The provision relates to payments made to or on behalf of a director or close associate of a director. The transaction must have been unreasonable, and have been entered into during the 4 years leading up to a company's liquidation, regardless of its solvency at the time the transaction occurred.

Voidable charges

Certain charges over company property are voidable by a liquidator:

• circulating security interest created within six months of the liquidation, unless it secures a subsequent advance;

• unregistered security interests; • security interests in favour of related parties who attempt to enforce the security within six months of its

creation.

In the following circumstances, directors may be personally liable for insolvent trading by the company:

• a person is a director at the time a company incurs a debt; • the company is insolvent at the time of incurring the debt or becomes insolvent because of incurring the debt; • at the time the debt was incurred, there were reasonable grounds to suspect that the company was insolvent; • the director was aware such grounds for suspicion existed; and • a reasonable person in a like position would have been so aware.

The law provides that the liquidator, and in certain circumstances the creditor who suffered the loss, may recover from the director, an amount equal to the loss or damage suffered. Similar provisions exist to pursue holding companies for debts incurred by their subsidiaries.

A defence is available under the law where the director can establish:

• there were reasonable grounds to expect that the company was solvent and they did so expect; • they did not take part in management for illness or some other good reason; or • they took all reasonable steps to prevent the company incurring the debt.

The proceeds of any recovery for insolvent trading by a liquidator are available for distribution to the unsecured creditors before the secured creditors.

Important note: This information sheet contains a summary of basic information on the topic. It is not a substitute for legal advice. Some provisions of the law referred to may have important exceptions or qualifications. This document may not contain all of the information about the law or the exceptions and qualifications that are relevant to your circumstances.

Insolvent trading