publication - rsm india budget 2016 key aspects

TRANSCRIPT

THE POWER OF BEING UNDERSTOOD

INDIA BUDGET 2016- Key Aspects

Let’s understand the IndiaBudget

RSM in India

nConsistently ranked amongst India’s top six accounting and consulting groups (International Accounting Bulletin, September 2015)

nNationwide presence through offices in 12 key cities across India

nMulti-disciplinary personnel strength of over 1,200

rsmindia.in

RSM around the globenSixth largest global audit, tax and consulting network (with total fee income

of US$ 4.64 bn)

nFirms in 120 countries and in each of the top 40 major business centresthroughout the world

nCombined staff of over 38,000 in over 760 offices across the Americas, Europe, MENA, Africa and Asia Pacific

rsm.global

INDIA BUDGET 2016 - Key Aspects

RSM INDIA BUDGET 2016 - Key Aspects

Table of Contents

Executive Summary 1

Chapter 1 : Introduction 8

Chapter 2 : Indian Economy - An Overview 12

Chapter 3 : Tax Rates 15

Chapter 4 : G-20 Countries - Comparative Corporate And Personal Tax Rates 22

Chapter 5 : Tax Incentives For Businesses 23

Chapter 6 : Direct Taxes - Significant Changes 39

6.1 Business Entities

6.2 Personal 46

6.3 Non Residents 49

6.4 Transfer Pricing 51

6.5 General 54

Chapter 7 : Indirect Taxes - Significant Changes 59

7.1 Service Tax 60

7.2 Customs Duty 65

7.3 Central Excise 67

7.4 Central Sales Tax Act 71

Chapter 8 : Other Significant Proposals 72

Chapter 9 : Impact On Select Industries 76

Chapter 10 : DTAA Rates 87

Chapter 11 : TDS Rates 96

Chapter 12 : Direct Tax And Service Tax Compliance Calendar 99

Abbreviations 102

39

RSM 1INDIA BUDGET 2016 - Key Aspects

Executive Summary

1.0 DIRECT TAXES1.1 Effective Tax Rates1.1.1 Personal taxation

nThe Bill proposes no change in personal tax rates and basic exemption limit continues at Rs.2,50,000. However, there is an increase in surcharge from 12% to 15% for Individuals / HUFs having income above Rs. 1,00,00,000. This will result in maximum marginal rate of 35.535% {(30%+15% surcharge thereon)+3% cess} for FY 2016-17 as against 34.608% {(30%+12% surcharge thereon)+3% cess} at present.

1.1.2 Corporate taxation nNew manufacturing domestic companies incorporated on or after 1

March 2016 may opt for corporate tax rate of 25% plus applicable surcharge and cess provided profit linked incentives / investment linked deductions / investment allowance / accelerated depreciation are not claimed.

nCorporate tax rate for relatively smaller domestic companies with turnover not exceeding Rs. 5,00,00,000 (For FYE 31 March 2015) to be 29% plus applicable surcharge and cess.

nCorporate tax rate for other domestic companies remains unchanged @30% plus applicable surcharge and cess.

nSurcharge on corporate tax / MAT of domestic company remain unchanged @7% where income exceeds Rs. 1,00,00,000 not exceeding Rs. 10,00,00,000 and @12% where income exceeds Rs. 10,00,00,000.

nCorporate tax rate for foreign companies remains unchanged @40% plus applicable surcharge and cess.

1.1.3 Partnership firms / LLPnFor total income exceeding Rs. 1,00,00,000, tax is chargeable @34.608%

[(tax rate 30% plus surcharge 12% thereon) plus education cess 3% thereon]. In other cases, effective tax rate remains unchanged @ 30.90%.

nAMT remains unchanged @21.346% [(tax rate 18.50% plus surcharge 12% thereon) plus education cess 3% thereon] in case the adjusted total income exceeds Rs. 1,00,00,000. In other cases, the effective tax rate remains unchanged @ 19.055%.

nDeduction up to 100% of the profits allowed for 3 out of 5 years for start-ups setup during April 2016 to March 2019. However, MAT will apply in such cases.

1.2 Tax Incentives and Proposals for Businesses

Back to Content

Executive Summary

RSM 2INDIA BUDGET 2016 - Key Aspects

nDeduction up to 100% of profits allowed to an undertaking in housing project for flats upto 30 sq. meters in 4 metro cities and 60 sq. meters in other cities, approved between June 2016 and March 2019 and completed within 3 years. However, MAT / AMT will apply in such cases.

nIn respect of foreign company engaged in the business of mining of diamonds, it is proposed that no income shall be taxed from the activities confined to display of uncut and unassorted diamonds in a Special Notified Zone.

nThe new tax regime provides pass through treatment of income of the securitisation trust wherein the income would be directly taxable in the hands of its investors. The securitisation trust shall be required to deduct tax at source @25% in case of payment to resident investors which are individual or HUF and @30% in case of others excluding non-residents. In case of payments to non-resident investors, TDS shall be at the rates in force.

nIt is proposed to amend section 10 of the IT Act to provide units located in an International Financial Services Centre for exemption from tax on capital gains to the income arising from transaction undertaken in foreign currency on a recognised stock exchange even when STT is not paid in respect of such transactions. However, MAT shall be chargeable @9%. Further, DDT shall not be applicable.

nPresumptive taxation scheme extended to professionals having gross receipts up to Rs. 50,00 000 with profit deemed to be 50%.

nThe threshold limit of gross receipts for applicability of tax audit in case of professionals, increased from Rs. 25,00,000 to Rs. 50,00,000.

nDeduction under section 80JJAA of the IT Act for additional wages is now available to all assessees who are subject to tax audit.

nConcessional tax rate of 10% for Indian residents on royalty income on gross basis from worldwide exploitation of patents developed and registered in India.

nDividend distributed by SPVs out of its income to the REITs / InvITs, not to suffer DDT.

nNon-banking financial companies shall be eligible for deduction to the extent of 5% of its income in respect of provision for bad and doubtful debts.

nIn order to provide clarity, it is proposed to insert a new section 35ABA in the IT Act to provide for tax treatment of spectrum fee. The spectrum fee will be allowed as a deduction in equal installments over the period for which the right to use spectrum remains in force.

Back to Content

RSM 3INDIA BUDGET 2016 - Key Aspects

Executive Summary

nSection 43B of the IT Act is proposed to be amended to include payments made to Indian Railways for use of Railway assets within its ambit.

nOne time window provided for domestic taxpayers to declare undisclosed income or such income represented in the form of any asset by paying tax @30%, surcharge @7.5% and penalty @ 7.5%, aggregating to 45% of the undisclosed income. Declarants will have immunity from prosecution.

nDirect Tax Dispute Resolution Scheme 2016 proposed to be introduced for tax arrears and specified tax where the assessee has the option to settle the case by paying tax, interest and penalty as under:– Where the appeal is pending before the CIT(Appeals), pay tax

arrears along with interest up to date of assessment and no penalty where tax arrears are less than Rs. 10,00,000 whilst 25% penalty where tax arrears exceed Rs. 10,00,000.

– Where appeal is pending before any appellate authorities and tax was determined pursuant to retrospective amendments, only tax amount to be paid and immunity from interest, penalty and prosecution.

nExisting penalty provisions of section 271(1)(c) are rationalized and new section 270A is introduced where it is proposed to levy a penalty @50% of taxes payable on the underreporting of income and @200% of taxes payable on the misreporting of income.

nPetitions of the tax payers seeking waiver of interest and penalty to be disposed off within a year.

nThe AO to grant stay of demand once assessee pays 15% of the disputed demand, while the appeal is pending before CIT(Appeals).

nGovernment to pay interest at 9% p.a. for delay in giving effect to Appellate Order beyond 90 days.

nAs per the Budget speech, section 14A read with rule 8D is proposed to be amended wherein disallowance would be limited to 1% of the average monthly value of investments yielding exempt income, but not exceeding actual expenditure claimed.

nDividend income of more than Rs.10,00,000 p.a. would be liable to tax @10% of gross amount of dividends in the hands of Individuals / HUFs / Firms despite the fact that DDT is already paid by companies declaring such dividends.

nTax to be collected at source @1% on purchase of luxury cars exceeding value of Rs.10,00,000 and purchase of goods and services in cash

Back to Content

RSM 4INDIA BUDGET 2016 - Key Aspects

Executive Summary

exceeding Rs.2,00,000.nSTT in case of ‘Options’ increased from 0.017% to 0.05%.nIn addition to existing conditions for availing tax neutral conversion from

Company to LLP, value of total assets as per books in any preceding 3 years not to exceed Rs.5,00,00,000.

nThe time limit for assessment, reassessment, re-computation has been advanced by 3 months.

nGAAR to be effective from 1 April 2017.

nThe tax rebate under section 87A has been increased from Rs. 2,000 to Rs. 5,000 for Individuals having income up to Rs. 5,00,000.

nWithdrawal up to 40% of the corpus at the time of closure to be tax exempt in the case of National Pension Scheme (NPS) and the Annuity fund which goes to legal heir will also be exempt.

nIn case of superannuation funds and recognized provident funds, including EPF, the same norm of 40% of corpus to be tax free will apply in respect of corpus created out of contributions made on or after 1 April 2016.

nHigher rate of TDS for non-provision of PAN in case of non-residents, not to apply where alternative documents are provided by such non-residents.

nEqualization levy of 6% proposed on payment (exceeding Rs.1,00,000 p.a.) made to non-residents not having a PE, in respect of online advertising or space for digital advertising, in case of B2B transactions.

nAny income accruing or arising to a foreign company on account of storage of crude oil in a facility in India and sale of crude oil therefrom to any person resident in India shall not be included in the total income.

nApplicability of rules of POEM for determining the status of residency of a foreign company deferred by 1 year. (Applicable w.e.f. FY 2016-17)

nBased on OECD Action plan 13 of BEPS, it is proposed to provide specificreporting regime in respect of Country by Country reporting and also a standardized master file for all group members of Multinational Enterprises. Penal implications introduced for non-compliance.

nTime limit for assessment, reassessment, re-computation has been advanced by 3 months

nTo facilitate the “Stand Up India Scheme” at least 2 projects per bank

1.3 Personal Taxation

1.4 Proposals for Non-residents

1.5 Proposal for Transfer Pricing

1.6 Other Proposals

Back to Content

RSM 5INDIA BUDGET 2016 - Key Aspects

Executive Summary

branch to be approved. This will benefit at least 2,50,000 entrepreneurs.nGovernment to contribute 8.33% for all new employees (where basic

salary is less than Rs.15,000 p.m.) enrolling in EPFO for the first 3 years of their employment. Budget provision of Rs. 1,000 crore for this scheme.

nAmendments in Companies Act to improve enabling environment for start-ups.

nReforms in FDI policy in the areas of Insurance and Pension, ARC, SEs. Further, 100% FDI allowed through FIPB route in marketing of food products produced and manufactured in India.

nTo continue with the ongoing reform programme and ensure passage of the GST bill and Insolvency and Bankruptcy law.

nNew model Shops and Establishments Bill to be circulated to the state governments.

nEffective service tax rate to increase from 14.5% to 15% (including Swachh Bharat Cess) in view of the proposal to levy an additional cess @ 0.5% as Krishi Kalyan Cess w.e.f. 1 June 2016 on all or any of the taxable services.

nExemption to construction and maintenance in relation to various projects, contracts etc., which was removed w.e.f. 1 April 2015 has been restored and given retrospective exemption.

nRate of interest rationalized @24% in case of amount collected but not paid and @15% in all other cases, as against the present rate of 18% to30%, as the case may be.

nLegal services provided by a senior advocate to an advocate or partnership firm of advocates made liable to service tax.

nRationalization of abatement to construction of complex, building civil structure or part thereof @70% as against existing rate of 70% and 75% as the case may be.

nServices provided by mutual fund agent/distributor to mutual fund/asset management company to be liable as forward charge.

nOne Person Company whose aggregate value of services during previous financial year is up to Rs. 50,00,000 or HUF shall be required to pay service tax as per the due date as applicable to individual or partnership firms.

nThe limitation period for issuance of show cause notice is proposed to be increased from 18 months to 30 months.

nAmendment in CENVAT Credit Rules, 2004 particularly relating to

2.0 INDIRECT TAXES2.1 Service Tax

Back to Content

RSM 6INDIA BUDGET 2016 - Key Aspects

Executive Summary

apportionment of credit between exempted and non-exempted final products/services.

nAmendment in provisions relating to Input Service Distributor (ISD) including extension of this facility to transfer input services credit to outsourced manufacturers under certain circumstances.

nBanking and other financial institution to have an option of reversing CENVAT credit in respect of exempted services on actual basis, in addition to an option of reversal of 50% of CENVAT credit.

nLevy of service tax and excise duty/CVD to be mutually exclusive on informational technology software.

nIt is clarified that point of taxation in case of new levy on services will be as per Rule 5 of Point of Taxation Rules, 2011 and that that transactions other than those falling under two scenarios specified in Rule 5 shall be liable to new levy.

nThe optional service tax rate in case of single premium annuity policies is being rationalized @1.4% of the total premium charged, where the amount allocated for investment is not intimated to policy holder.

nIndirect Tax Dispute Resolution Scheme, 2016 is proposed to be introduced w.e.f. 1 June 2016 for Service Tax, Excise and Customs assessee who has filed an appeal before Commissioner (Appeals) and is pending for adjudication as on 1 March 2016.

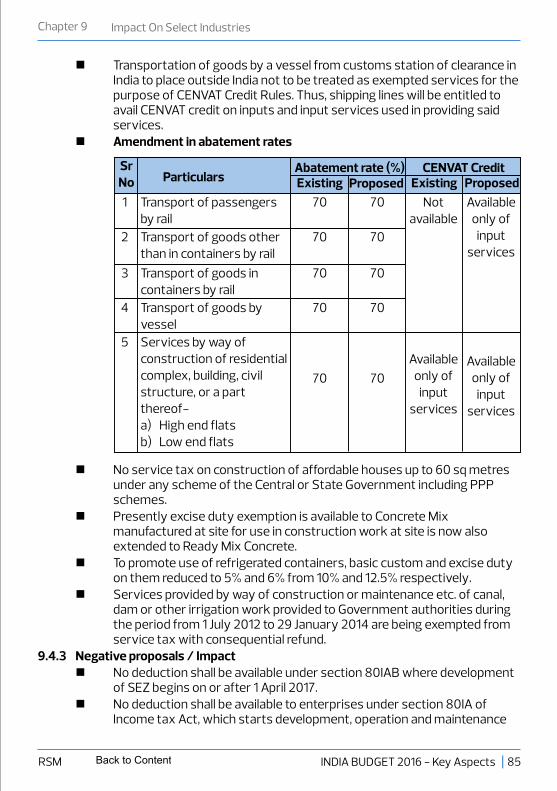

nTransportation of goods by a vessel from customs station of clearance in India to place outside India, not to be treated as exempted services for the purpose of CENVAT Credit Rules.

nIt is proposed to levy service tax on transportation of goods by a vessel from outside India up to the customs station in India w.e.f. 1 June 2016.

nNo change in general effective rate of Basic Excise Duty (‘BED’).nInfrastructure Cess as duty of excise ranging from 1% to 4% is being

imposed on motor vehicles (depending upon type of motor vehicle) falling under chapter heading 8703.

nExcise duty of 1% without input tax credit or 12.5% with input tax credit on articles of jewellery (excluding silver jewellery, other than studded with diamonds and some other precious stones) with a higher exemption and eligibility limits of Rs. 6 crores and Rs. 12 crores respectively.

nExcise duty on ready-made garments with retail price of Rs. 1,000 or more, raised to 2% without CENVAT credit or 12.5% with CENVAT credit

nBED on refrigerated containers reduced from 12.5% to 6%.nOption for revising periodical returns to be provided to central excise

2.2 Excise Duty

Back to Content

RSM 7INDIA BUDGET 2016 - Key Aspects

Executive Summary

assesses.nChanges in excise duty rates on certain inputs in sectors like information

technology hardware, capital goods, defense production, textiles, mineral fuels & mineral oils, chemicals & petrochemicals, paper, paperboard and newsprint, maintenance repair and overhauling of aircrafts and ship repair.

nReduction in number of returns under central excise by an assessee above a certain threshold from 27 to 13.

nExemption from excise duty on ready mix concrete manufactured at construction sites.

nRate of duty increased from 9% to 9.5% in case of refined gold bars manufactured from gold dore bar, silver dore bar, gold ore or concentrate, silver ore or concentrate, copper ore or concentrate. Excise duty exemption under the existing area based exemptions on refined gold is withdrawn.

nFor refined silver manufactured from silver ore or concentrate, silver dore bar, or gold dore bar, the excise duty exemption under the existing area based exemptions is being withdrawn – rate of duty to increase from 8% to 8.5%.

nNo change in peak rate of Basic Custom Duty (BCD).nBCD on import of imitation jewellery is increased from 10% to 15%.nInterest rate for delayed payment of customs duty has been reduced

from 18% p.a. to 15% p.a.nImport of Printed Circuit Boards (PCBs) of mobile phones and tablet

computers subjected to Customs Duty.nSpecial Additional Duty (SAD) to be levied on import of inputs and raw

materials used in manufacture of personal computers and tablets.nSelf–declaration sufficient for availing duty exemptions to import goods

at concessional rate to be used in manufacture of excisable goods.nCustoms baggage declaration to be filed only by passengers carrying

dutiable or prohibited goods.nCVD increased on gold dore bars from 8% to 8.75%.nCVD increased on silver dore from 7% to 7.75%.

nGas transported through a common carrier pipeline or transport or distribution system and which becomes comingled or fungible, introduced in the system in one state and taken out from the pipeline in the other state is deemed to be sold in the inter-state trade.

2.3 Customs

2.4 Central Sales Tax

Back to Content

RSM 8INDIA BUDGET 2016 - Key Aspects

Chapter 1 Introduction

1.1 Background

In the midst of an uncertain global economic outlook, India is emerging as the new ‘global economic hotspot’. The Indian economy is estimated to grow at 7.6% in FY 2015-16 and is expected to grow at 7% to 7.75% in FY 2016-17, making it the fastest growing major economy in the world. Further, India’s other macroeconomic parameters like inflation; fiscal deficit and current account balance have exhibited distinct signs of improvement. The World Economic Forum has said that India’s growth is ‘extraordinarily high’.

The Union Budget 2015 is primarily driven with the objective of accelerating investment in infrastructural sector, fiscal consolidation and reducing litigation. The total investment in infrastructure sector is projected at a whopping Rs. 2,21,000 crores. The fiscal deficit for FY 2015-16 is expected to be at 3.9% of GDP which is expected to come down to 3.5% for FY 2016-17.

The most striking feature of the Budget is the concerted effort at reducing litigation and ease of doing business. The Budget contains “The Direct Tax Dispute Resolution Scheme 2016” which would permit the taxpayers whose appeals are pending before the first appellate authority to pay the tax and interest up to the date of assessment where disputed tax is up to Rs. 10 lacs. In cases where disputed tax exceeds Rs. 10 lacs, 25% of the minimum penalty leviable shall be payable. There will be no further penalty or prosecution nor interest for the period after assessment. The total disputed amount in litigation is estimated at Rs.5.50 lac crores with over 3 lac cases. The Budget also contains “The Income Declaration Scheme 2016” which will provide a window to the taxpayers who have not paid full taxes in the past to ensure compliance by paying 45% of declared income as tax and penalty. This will result in no further interest or penalty or prosecution. The scheme will be open from June 2016 to September 2016 and will be subject to specified conditions. In the case of tax disputes due to retrospective changes of law (such as Vodafone for indirect transfer of shares), it is proposed to permit the settlement of dispute subject to the payment of tax which will ensure complete immunity from interest, penalty and prosecution. This can help restore confidence of international investors.

There is a widespread disappointment on the tax rates. In the last Budget 2015, a roadmap to lower the corporate tax rates over 4 years from 30% to 25% was announced with the phasing out of the tax exemptions. However, the corporate tax rate has been kept unchanged at 30% plus applicable surcharge and cess

Back to Content

Chapter 1 Introduction

RSM 9INDIA BUDGET 2016 - Key Aspects

resulting in effective tax rate of 34.608%. The only relief is for specific manufacturing companies set up after 1 April 2016 where a lower rate (i.e. 25% plus applicable surcharge and cess) and Specified small companies having annual turnover of less than Rs. 5 cores (i.e. 29% plus applicable surcharge and cess) would apply, although MAT shall be applicable to them. In turn, it has proposed phased elimination of deductions and exemptions including sunset clause for setting up of SEZ units, infrastructure facilities and developers of SEZs. The Minimum Alternate Tax (MAT) and Dividend Distribution Tax (DDT) rates have remained unchanged at 21.3416% {(18.5%+12% surcharge) x3% cess} and 20.358% {(15%+12% surcharge) x3% cess with grossing up} respectively.

The personal tax rates have remained unchanged except for high income tax payers wherein the surcharge on income-tax is proposed to be increased from 12% to 15% in case income exceeds Rs. 1,00,00,000. This will result in maximum marginal rate of 35.535% {(30%+15% surcharge thereon)+3% cess} for FY 2016-17 as against 34.608% {(30%+12% surcharge thereon)+3% cess} at present. It is also proposed to tax any income by way of dividend in excess of Rs. 10,00,000 in the case of an individual, HUF or a firm who is resident in India @ 10% on gross basis. However, HNIs can heave a sigh of relief that the much talked about long term capital gains tax exemption period for shares sold on the stock exchange continues at 1 year and has not been increased to 3 years. The limit for deduction under Section 80C of Rs. 1,50,000 remains unchanged. Section 80C provides for tax deduction in respect of investment in eligible savings such as Provident fund, ELSS, life insurance premium, housing loan repayment, 5 year bank deposits, NSC, ULIP to promote growth.

Certain Foreign Direct Investment reforms have been announced in areas of Insurance and Pension, Asset Reconstruction Companies, Stock Exchanges, etc. 100% FDI will be allowed through FIPB route in marketing of food products produced and manufactured in India. To incentivize Sovereign Gold Bond and Gold monetization scheme, the capital gains on redemption and interest thereon is proposed to be exempt under the IT Act.

The determination of tax residency of foreign company on the basis of Place of Effective Management (POEM) is proposed to be deferred by 1 year. It is hoped that the Income Computation and Disclosure Standards (ICDS) would also be deferred as per recommendation of the Easwaran Committee. To meet with the commitment to BEPS initiative of OECD and G-20, the Finance Bill, 2016 has included the provision for requirement of country by country reporting for companies with consolidated revenue of more than Euro 750 million. General Anti Avoidance Rules (GAAR) would be effective from 1 April 2017 as proposed earlier. A new provision (section 35ABA) is proposed to be introduced to provide

Back to Content

RSM 10INDIA BUDGET 2016 - Key Aspects

Chapter 1 Introduction

clarity for amortization of spectrum fees. For a foreign company engaged in business of mining of diamonds, it is proposed that, no income shall be taxed from the activities confined to display of uncut and unassorted diamonds in a Special Notified Zone.

It is proposed to promote employment generation, incentive available under Section 80JJAA of the IT Act will be available not only to assessees deriving income from manufacture of goods in a factory but to all assessees who are subject to statutory audit under the Act. Thus, a deduction of 30% of the emoluments paid to such employees can be claimed for 3 years for employees whose monthly emoluments do not exceed Rs.25,000. Also, no deduction will be admissible in respect of employees for whom the Government is paying the entire EPS contribution.

Deduction up to 100% of the profits is proposed to be allowed for 3 out of 5 years for start-ups setup during April 2016 to March 2019. Deduction up to 100% of profits is proposed to be allowed to an undertaking in housing project for flats upto 30 sq. metres in 4 metro cities and 60 sq. metres in other cities, approved between June 2016 and March 2019 and completed within 3 years. However, MAT / AMT will apply in both the cases.

Under the existing provisions of the Income-tax Act, tax treatment for the National Pension System (NPS) referred to in section 80CCD is Exempt, Exempt and Tax (EET). It is proposed that withdrawal up to 40% of the corpus at the time of retirement shall be tax exempt in the case of National Pension Scheme. In case of superannuation funds and recognized provident funds, including employees provident Fund, 40% of corpus created out of contributions made on or from 1.4.2016 shall be tax exempt upon withdrawal. It may be pointed out that presently withdrawals from recognized Provident Funds are generally exempt from tax altogether whereas withdrawals from NPS are taxable entirely.

It is proposed to provide for presumptive taxation regime for professionals having gross receipts upto Rs. 50,00,000 per annum wherein profit of 50% shall be deemed to be his income.

Effective service tax rate (including Swachh Bharat Cess) and the proposed additional levy @ 0.5% as Krishi Kalyan Cess effective 1 June 2016 on the taxable services, would result in effective service tax rate to 15%. This will have far reaching implications. Excise duty of 1% without input tax credit or 12.5% with input tax credit is proposed on articles of jewellery (excluding silver jewellery, other than studded with diamonds and some other precious stones) with a higher exemption and eligibility limits of Rs. 6 crores and Rs. 12 crores respectively.

Back to Content

RSM 11INDIA BUDGET 2016 - Key Aspects

Chapter 1 Introduction

A Committee shall be formed to review the implementation of the FRBM Act and give its recommendations on the way forward. As mentioned in the Budget Speech, the Government shall also endeavour to continue with the ongoing reform programme and ensure passage of the Constitutional amendments to enable implementation of the Goods and Service Tax, the passage of Insolvency and Bankruptcy law and other important reform measures which are pending before the Parliament. Amendments in Companies Act are proposed to improve enabling environment for start-ups. Comprehensive central legislation to deal with illicit deposit taking schemes is proposed to be introduced. A new model Shops and Establishments Bill is proposed to be circulated to the state governments and the passenger road transport segment is proposed to be revamped with reforms.

The Budget is a serious Policy Statement for putting India back on the path of long term sustained economic growth and stable tax regime.

In this booklet compiled by us, we intend to offer a broad outline of the highlights of the Union Budget 2016 presented on 29 February 2016. We have discussed the significant proposals of general interest in respect of direct taxes. In respect of indirect taxes and other policy initiatives, only the highlights have been briefly enumerated. Preceding the budget proposals are the macro indicators of Indian economy which provide a backdrop to the legal and financial proposals.

This booklet is not an offer, invitation or solicitation of any kind and it does not purport to be comprehensive, or to render legal, economic or financial advice. This booklet should not be relied upon for taking actions or decisions without appropriate professional advice as the facts of each case have to be studied and the legal position analysed properly before taking any action or decision in the matter. Further, this booklet contains only the proposals and amendments as given in the Finance Bill, 2016, which may be modified before it receives the approval and assent of the Parliament and the President. The proposals regarding direct taxes would become effective from AY 2017-18 (FY 1 April 2016 to 31 March 2017), unless otherwise specified. In this booklet, the terms 'IT Act', 'the Rules' and 'the Bill' are used for the "Income-tax Act, 1961", ''Income-tax Rules, 1962'' and "Finance Bill, 2016" respectively.

While all reasonable care has been taken in preparation of this booklet, we accept no responsibility for any errors it may contain or for any omissions or otherwise or for any loss, howsoever caused or sustained, by the person who relies on it.

1.2 Scope and Limitations

Back to Content

RSM 12INDIA BUDGET 2016 - Key Aspects

Chapter 2 Indian Economy – An Overview

2.1 India At A Glance – The Macro-Economic Perspective

GDP - 2015lUS$ 8 trillion in terms of Purchasing

Power Parity (PPP) - 3rd largest in the world

Rapid AdvancementlIndia hailed as a 'bright spot' amidst a

slowing global economy by IMFlThe World Economic Forum has said that

India's growth is 'extraordinarily high’

GDP Growth Rate

l7.6% for FY 2015-16 (Advance Estimate)l7% to 7.75% for FY 2016-17 (Projection)

Demography l1.271 billion (2015) with more than 65%

population aged under 35 yearslWorld’s largest diaspora of 16 million

Forex ReserveslForex Reserves of US$ 350 billion

Exchange Ratel1 US$ = INR 68.616 (as on 29 February

2016)

Market Capitalization (as on 29 February 2016)lUS$ 1.25 trillion

Political SystemlFederal Republic with Parliamentary

democracylLargest Democracy in the world.

2.2 General Review

The global economic outlook is currently very uncertain due to weak growth of world output, declining prices of a number of commodities, turbulent financial markets and volatile exchange rates. In spite of such unsupportive macroeconomic landscape, India has grown at 7.6% in FY 2015-16 and is expected to grow at 7% to 7.75% in 2016-17, making it the fastest growing major economy in the world. Further, India’s other macroeconomic parameters like inflation, fiscal deficit and current account balance have exhibited distinct signs of improvement. As a result, India is emerging as the new ‘global economic hotspot’.

GDP Growth

5.1

2014-15 2015-162013-142012-13 2016-17*

* Projection

6.97.2 7.6 7.759

87654321

0

Back to Content

The year 2015-16 continues to experience moderation in general price levels in the country following the global trend of declining commodity and producers prices. Headline inflation based on the Consumer Price Index, dipped to 4.9% during 2015-16 (April-January) as against 5.9 % in 2014-15. Similarly, headline Wholesale Price Index inflation was -2.8% in 2015-16 (April-January) as compared to 2.0% in 2014-15.

During 2015-16 (April-January), India’s exports declined year-on-year by 17.6 % to US$ 217 billion owing to sluggish global demand and low global commodity prices. In keeping with the global trends of slow growth, imports have also declined by 15.5 % in 2015-16 (April-January) to US $ 324 billion. Lower imports of petroleum, oil and lubricants were the main reasons for the decline in total imports this year so far. In spite of the decline in exports during 2015-16, India’s BoP position remained comfortable.

During 2015-16 (April-January), the average exchange rate of the Rupee depreciated to INR 65.04/US$ as against INR 60.92/US$ in 2014-15 (April-January).

While 2014-15 saw the Indian equity markets witnessing a dream run to reach an all-time high of 29448.95, 2015-16 has seen substantial erosion with the BSE Sensex reaching a year low of 23,002 as on 29 February 2016.

The new foreign Trade Policy for the period 2015-20, announced on 1 April 2015 focuses on supporting both manufacturing and services exports and improving ease of doing business. It aims to increase India’s exports to US$ 900 billion by 2019-20 and it also provides the road map by the government to align it with the ‘Make in India’ and ‘Digital India’ programmes and to ease trade.

The Indian economy has made substantial improvements in its macroeconomics fundamentals and impressive strides in reducing in key areas, pursuit of fiscal prudence and consolidation, focus on price stability and the resultant benign price situation and comfortable level of external current account.

Chapter 2 Indian Economy – An Overview

RSM 13INDIA BUDGET 2016 - Key AspectsBack to Content

Chapter 2 Indian Economy – An Overview

RSM 14INDIA BUDGET 2016 - Key Aspects

Absolute values % change over previous periodItems 2013-14 2014-15 2015-16

2.3 India – Key Economic Indicators

2013-14 2014-15 2015-16

Gross Domestic Product(Rs. thousand crore)

2R 1R 1AE-At constant market prices 9,839 10,552 11,35 6.6 7.2 7.6GVA at basic prices

2R 1R AE(2011-12 prices) 9,084 9,727 10,438 6.3 7.1 7.31At constant market prices

(US $ billion – Annual Average exchange rate) 1,626 1,726 1,745 -4.1 6.1 1.1Food grains production

a(million tons) 265 252 253 3.1 -4.9 0.5Index of industrial production

b(Base: 2004-05 = 100) 172 176 182 -0.1 2.8 3.1Electricity generation

b(billion KWH) 1175 1274 1330 6.0 8.4 4.4Wholesale Price Index

c(Average) 177 181 176 6.0 2.0 -2.8Imports

P(US $ billion) 450 448 379 -8.3 -0.5 -15.5Exports

P(US $ billion) 314 310 256 4.7 -1.3 -17.6Foreign exchange reserves

d(in US $ billion) 304 341 349 4.2 12.3 2.3Average exchange rate

e(Rs/US $) 60.51 61.14 65.03 11.2 1.0 6.4Gross fiscal deficit

f g(of GDP) 4.5 4.0 3.9

1 Calculated based on available figures.2R Second Revised Estimates1R First Revised EstimatesAE Advance Estimatesa 2nd Advance Estimatesb April-December 2015-16c April-January 2015-16

d As at end-January 2016le April-January 2015-16f Provisional Actualsg Budget EstimateP Provisionalna Not available

Back to Content

RSM 15INDIA BUDGET 2016 - Key Aspects

Chapter 3 TAX RATES

3.1 Individuals, HUFs, AOPs and BOIs

3.1.1 Tax rates

The Bill proposes certain marginal modifications to the tax structure for individuals, HUFs, AOPs and BOIs. Consequently, the effective proposed and present tax rates for the FYs 2016-17 and 2015-16, in case of individuals, HUFs, AOPs and BOIs are as follows:

Income Slabs(Rs.)

Income Slabs(Rs.)

ProposedTax Rates

Tax Rates

FY 2016-17 FY 2015-16

Nil

10.30% [tax rate 10% plus education cess 3% thereon] of income exceeding Rs. 2,50,000

Rs. 25,750 plus 20.60% [tax rate 20% plus education cess 3% thereon] of income exceeding Rs. 5,00,000

Rs. 1,28,750 plus 30.90% [tax rate 30% plus education cess 3% thereon] of income exceeding Rs. 10,00,000

0 - 2,50,000#

2,50,001# - 5,00,000*

5,00,001 - 10,00,000

10,00,001 - 1,00,00,000

Nil

10.30% [tax rate 10% plus education cess 3% thereon] of income exceeding Rs. 2,50,000

Rs. 25,750 plus 20.60% [tax rate 20% plus education cess 3% thereon] of income exceeding Rs. 5,00,000

Rs. 1,28,750 plus 30.90% [tax rate 30% plus education cess 3% thereon] of income exceeding Rs. 10,00,000

0 - 2,50,000#

2,50,001# - 5,00,000*

5,00,001 - 10,00,000

10,00,001 - 1,00,00,000

Rs. 32,58,920 plus 34.608% [(tax rate 30% plus surcharge 12% thereon) plus education cess 3% thereon] of income exceeding Rs. 1,00,00,000

1,00,00,001^ and aboveRs. 32,58,920 plus 35.535% [(tax rate 30% plus surcharge 15% thereon) plus education cess 3% thereon] of income exceeding Rs. 1,00,00,000

1,00,00,001^ and above

# Basic exemption income slab in case of a resident individual of the age of 60 years or more (senior citizen) & resident individual of the age of 80 years or more (very senior citizens) at any time during the previous year, continues to remain the same at Rs. 3,00,000, Rs. 5,00,000 respectively. The tax for other slabs will change accordingly.

Back to Content

Chapter 3 TAX RATES

RSM 16INDIA BUDGET 2016 - Key Aspects

* A resident individual having income upto Rs. 5,00,000 is entitled to a rebate of tax payable [excluding education cess] or Rs. 5,000 (Rs. 2,000 in FY 2015-16) whichever is less.

^ Marginal relief is available to ensure that the additional income tax payable, including surcharge of 15% on the excess of income over Rs. 1,00,00,000 is limited to the amount by which the income is more than Rs. 1,00,00,000. However, no marginal relief shall be available in respect of the education cess.

3.1.2 Proposed tax incidence

The proposed incidence of income-tax for FY 2016-17 on individuals, senior citizens and very senior citizens, having different income levels can be exemplified as follows:

* The tax incidence for HUFs, AOPs and BOIs will be same as that of individuals.

3.2.1 Domestic companies

The Bill proposes to reduce the corporate tax rate to 29% [plus applicable surcharge and education cess thereon], in case of company having total turnover or gross receipts in FY 2014-15 upto Rs.5,00,00,000.

Further, the Bill proposes the tax rate of 25% in case of newly setup domestic company registered on or after 1 March, 2016 engaged solely in the business of manufacture or production of article or thing and not claiming any specified. benefit/deduction.

3.2 Companies

AnnualIncome (Rs.)

Tax Liability (Rs.)

Individuals(including women)*

Senior Citizens

Very SeniorCitizens

2,50,000 - - -

3,00,000 - - -

4,00,000 10,300 5,150 -

5,00,000 20,600 15,450 -

8,00,000 87,550 82,400 61,800

10,00,000 1,28,750 1,23,600 1,03,000

25,00,000 5,92,250 5,87,100 5,66,500

50,00,000 13,64,750 13,59,600 13,39,000

1,00,00,000 29,09,750 29,04,600 28,84,000

1,50,00,000 51,22,963 51,17,040 50,93,350

Back to Content

Chapter 3 TAX RATES

RSM 17INDIA BUDGET 2016 - Key Aspects

Except for the above, there are no changes proposed in the corporate tax rates for FY 2016-17. The effective tax rates and MAT rates for other domestic companies for FYs 2016-17 and 2015-16 are as follows:

Marginal relief is available to ensure that the additional income-tax payable, including surcharge of 7% on the excess of income over Rs. 1,00,00,000, is limited to the amount by which the income is more than Rs. 1,00,00,000. Similarly, marginal relief is available to ensure that the additional income-tax payable, including surcharge of 12% on the excess of income over Rs. 10,00,00,000, is limited to the amount by which the income is more than Rs. 10,00,00,000. However, no marginal relief shall be available in respect of the education cess.

3.2.2 Foreign companies

No changes are proposed in the tax rate and surcharge. As such, the effective tax rates for foreign companies for FYs 2016-17 and 2015-16 are as follows:

DomesticCompany

Effective Tax Rates

FY 2016-17 FY 2015-16 FY 2016-17

Having total income exceeding Rs.

10,00,00,000

Effective MAT Rates

FY 2015-16

34.608% [(tax rate 30% plus

surcharge 12% thereon) plus

education cess 3% thereon]

34.608% [(tax rate 30% plus

surcharge 12% thereon) plus

education cess 3% thereon]

21.3416% [(tax rate 18.5% plus surcharge 12% thereon) plus

education cess 3% thereon]

21.3416% [(tax rate 18.5% plus surcharge 12% thereon) plus

education cess 3% thereon]

Having total income exceeding Rs.

1,00,00,000 but not exceeding Rs. 10,00,00,000

33.063% [(tax rate 30% plus surcharge 7% thereon) plus

education cess 3% thereon]

33.063% [(tax rate 30% plus surcharge 7% thereon) plus

education cess 3% thereon]

20.38885% [(tax rate 18.5% plus surcharge 7% thereon) plus

education cess 3% thereon]

20.38885% [(tax rate 18.5% plus surcharge 7% thereon) plus

education cess 3% thereon]

Having total income upto Rs.

1,00,00,000

30.90% (tax rate 30% plus

education cess 3% thereon)

30.90% (tax rate 30% plus

education cess 3% thereon)

19.055% (tax rate 18.5% plus

education cess 3% thereon)

19.055% (tax rate 18.5% plus

education cess 3% thereon)

Foreign CompanyEffective Tax Rates

FY 2016-17 FY 2015-16

Having total income exceeding Rs. 10,00,00,000

43.26% [(tax rate 40% plus surcharge 5% thereon) plus education cess 3% thereon]

Having total income exceeding Rs. 1,00,00,000 but not

exceeding Rs. 10,00,00,000

42.024% [(tax rate 40% plus surcharge 2% thereon) plus education cess 3% thereon]

Having total income upto Rs. 1,00,00,000

41.20% (tax rate 40% plus education cess 3% thereon)

Back to Content

Chapter 3 TAX RATES

RSM 18INDIA BUDGET 2016 - Key Aspects

Marginal relief is available to ensure that the additional income-tax payable, including surcharge of 2% on the excess of income over Rs. 1,00,00,000, is limited to the amount by which the income is more than Rs. 1,00,00,000.

Similarly, marginal relief is available to ensure that the additional income-tax payable, including surcharge of 5% on the excess of income over Rs. 10,00,00,000, is limited to the amount by which the income is more than Rs. 10,00,00,000. However, no marginal relief shall be available in respect of the education cess.

3.2.3 Tax on Dividend / Income distributed by domestic companies

No changes are proposed in the DDT rates for FY 2016-17 (the effective DDT rates for FY 2016-17 and 2015-16 are tabulated below). However, the Bill proposes to tax dividend at the rate of 10% in the hands of recipient i.e. individual, HUF or Firm, who is resident in India if dividend received is in excess of Rs.10,00,000. The rate (plus surcharge and education cess thereon) is on gross basis on the amount of dividend.

The effective DDT rates for FY 2016-17 and 2015-16 are as follows:

No changes are proposed in the tax rates. The effective tax rates for partnership firms/LLPs for FYs2016-17 and 2015-16 are as follows:

Marginal relief is available to ensure that the additional income-tax payable, including surcharge of 12% on the excess of income over Rs.1,00,00,000, is limited to the amount by which the income is more than Rs.1,00,00,000. However, no marginal relief shall be available in respect of the education cess.

3.3 Partnership Firms/LLPs

Dividend DistributionTax Rate

Effective Tax Rates

FY 2016-17 FY 2015-16

Rate of DDT on the amount of dividend received by the

shareholders

20.3576% [(tax rate 15% plus surcharge 12% thereon) plus education cess 3% thereon considering the grossing up

provisions]

PartnershipFirms / LLPs

Effective Tax Rates

FY 2016-17 FY 2015-16

Having total income exceeding Rs. 1,00,00,000

34.608% [(tax rate 30% plus surcharge 12% thereon) plus education cess 3% thereon]

Having total income upto Rs. 1,00,00,000

30.90% (tax rate 30% plus education cess 3% thereon)

Back to Content

Chapter 3 TAX RATES

RSM 19INDIA BUDGET 2016 - Key Aspects

3.4 AMT on Non-corporate Assessees

3.5 Tax on Dividend Distributed by Mutual Funds

AMT continues on non-corporate assessees such as partnership firms, sole proprietorships, AOPs, HUFs, BOIs, etc. AMT is to be calculated on adjusted total income (if the adjusted total income of such person exceeds Rs. 20,00,000) if the regular income tax payable by such person is less than AMT. No change has been proposed in the AMT rates. However, surcharge rate for assessees other than firms is proposed to be increased from 12% to 15% in case the total income exceeds Rs. 1,00,00,000. As such, the effective tax rates for FYs 2016-17 and 2015-16 are as follows:

Marginal relief is available to ensure that the additional income-tax payable, including surcharge of 12% / 15% (as applicable) on the excess of income over Rs. 1,00,00,000, is limited to the amount by which the income is more than Rs. 1,00,00,000. However, no marginal relief shall be available in respect of the education cess.

No change has been proposed in the income distributed by mutual funds. However, surcharge rate for Individuals, HUF, AOP, BOI etc. is proposed to be increased from 12% to 15% in case the total income exceeds Rs. 1,00,00,000. As such, the effective tax rates for FYs 2016-17 and 2015-16 are as follows:

Non-corporateassessee

Effective AMT Rates

FY 2016-17 FY 2015-16

Individuals, HUF, AOP, BOI etc. having total income exceeding

Rs. 1,00,00,000

21.9133 % [(tax rate 18.50% plus surcharge 15% thereon) plus education cess 3% thereon]

21.3416% [(tax rate 18.50% plus surcharge 12% thereon) plus education cess 3% thereon]

Firms / Others - having total income exceeding

Rs. 1,00,00,000

21.3416% [(tax rate 18.50% plus surcharge 12% thereon) plus education cess 3% thereon]

Having total income upto Rs. 1,00,00,000

19.055% (tax rate 18.50% plus education cess 3% thereon)

42.07%* (considering the grossing up

provisions)

52.92%* (considering the grossing up

provisions)

40.52%* (considering the grossing up

provisions)

52.92%* (considering the grossing up

provisions)

Income distributed by a money market mutual fund or a liquid mutual fund to- an Individual or a HUF

- others

Type of IncomeEffective Tax Rate

FY 2016-17 FY 2015-16

Back to Content

Chapter 3 TAX RATES

RSM 20INDIA BUDGET 2016 - Key Aspects

* The tax rates are inclusive of surcharge of 15% and education cess of 3% for Individual and HUF and surcharge of 12% and education cess of 3% thereon for others i.e. company, Firm, local authorities and co-operative society.

No change being proposed, the effective tax rate for distributed income of domestic companies for buy-back of shares for FY 2016-17 and FY 2015-16 are as follows:

The bill proposes that tax on distributed income by Securitization Trust would not be applicable from 1 June 2016 and the same would be included as income in the hands of the investor directly.

3.8.1 Co-operative societies

No change is proposed in the tax rate. As such, the tax rates for co-operative

3.6 Tax on Distributed Income of Domestic Company for Buy-back of Shares:

3.7 Tax on distributed income by Securitization Trust:

3.8 Other Entities

Rate of TaxEffective Tax Rates

FY 2016-17 FY 2015-16

On the distributed income of domestic company

23.072%* [(tax rate 20% plus surcharge 12% thereon) plus education cess 3% thereon]

Type of IncomeEffective Tax Rate

FY 2016-17 FY 2015-16

42.07%* (considering the grossing up

provisions)

52.92%* (considering the grossing up

provisions)

40.52%* (considering the grossing up

provisions)

52.92%* (considering the grossing up

provisions)

Income distributed by a mutual fund (including debt fund) other than a money market mutual fund or a liquid mutual fund to-an Individual or a HUF

- others

6.12%* (considering the grossing up provisions)

6.12%* (considering the grossing up provisions)

Income distributed by a mutual fund to non-residents (not being company) under infrastructure debt scheme

Back to Content

Chapter 3 TAX RATES

RSM 21INDIA BUDGET 2016 - Key Aspects

societies for FYs 2016-17 and 2015-16 are as follows:

Marginal relief is available to ensure that the additional income-tax payable, including surcharge of 12% on the excess of income over Rs. 1,00,00,000, is limited to the amount by which the income is more than Rs. 1,00,00,000. However, no marginal relief shall be available in respect of the education cess.

3.8.2 Local authorities

No change is proposed in the tax rate. As such, the tax rates for local authorities for FYs 2016-17 and 2015-16 are as follows

Marginal relief is available to ensure that the additional income-tax payable, including surcharge of 12% on the excess of income over Rs. 1,00,00,000 is limited to the amount by which the income is more than Rs. 1,00,00,000. However, no marginal relief shall be available in respect of the education cess.

It is proposed to insert a new section 115BBF of the IT Act to provide that if the total income of the eligible assessee includes any income by way of royalty in respect of a patent developed and registered in India, then such royalty shall be taxable at the rate of 10% (plus applicable surcharge and cess) on the gross amount of royalty. No expenditure or allowance in respect of such royalty income shall be allowed under the IT Act.

An eligible assessee means a person resident in India, who is the true and first inventor of the invention and whose name is entered on the patent register as the patentee in accordance with Patents Act, 1970.

3.9 Taxation of Income from Patents

Income slab(Rs.)

Effective Tax Rates

FY 2016-17 FY 2015-16

0 - 10,000 10.30%

10,001 - 20,000 Rs. 1,030 plus 20.60% of income exceeding Rs. 10,000

20,001 - 1,00,00,000 Rs. 3,090 plus 30.90% of income exceeding Rs.20,000

Above 1,00,00,000 Rs. 34,57,339 plus 34.608% of income exceeding Rs. 1,00,00,000

Local authoritiesEffective Tax Rates

FY 2016-17 FY 2015-16

Having total income exceeding Rs. 1,00,00,000

34.608% [(tax rate 30% plus surcharge 12% thereon) plus education cess 3% thereon]

Having total income up to Rs. 1,00,00,000

30.90% (tax rate 30% plus education cess 3% thereon)

Back to Content

Chapter 4 G-20 Countries - Comparative Corporate And Personal Tax Rates

RSM 22INDIA BUDGET 2016 - Key Aspects

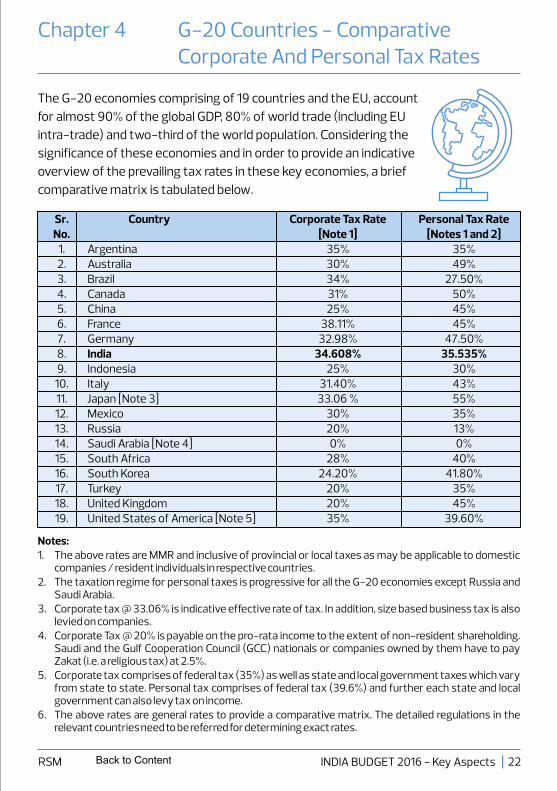

The G-20 economies comprising of 19 countries and the EU, account for almost 90% of the global GDP, 80% of world trade (including EU intra-trade) and two-third of the world population. Considering the significance of these economies and in order to provide an indicative overview of the prevailing tax rates in these key economies, a brief comparative matrix is tabulated below.

Notes:1. The above rates are MMR and inclusive of provincial or local taxes as may be applicable to domestic

companies / resident individuals in respective countries.2. The taxation regime for personal taxes is progressive for all the G-20 economies except Russia and

Saudi Arabia.3. Corporate tax @ 33.06% is indicative effective rate of tax. In addition, size based business tax is also

levied on companies.4. Corporate Tax @ 20% is payable on the pro-rata income to the extent of non-resident shareholding.

Saudi and the Gulf Cooperation Council (GCC) nationals or companies owned by them have to pay Zakat (i.e. a religious tax) at 2.5%.

5. Corporate tax comprises of federal tax (35%) as well as state and local government taxes which vary from state to state. Personal tax comprises of federal tax (39.6%) and further each state and local government can also levy tax on income.

6. The above rates are general rates to provide a comparative matrix. The detailed regulations in the relevant countries need to be referred for determining exact rates.

Sr. Country Corporate Tax Rate Personal Tax Rate [Note 1] [Notes 1 and 2]

2. Australia 30% 49%3. Brazil 34% 27.50%4. Canada 31% 50%5. China 25% 45% 6. France 38.11% 45%7. Germany 32.98% 47.50%8. India 34.608% 35.535%9. Indonesia 25% 30%

10. Italy 31.40% 43%11. Japan [Note 3] 33.06 % 55%12. Mexico 30% 35%13. Russia 20% 13%14. Saudi Arabia [Note 4] 0% 0%15. South Africa 28% 40%16. South Korea 24.20% 41.80%17. Turkey 20% 35%18. United Kingdom 20% 45%19. United States of America

No.

[Note 5] 35% 39.60%

1. Argentina 35% 35%

Back to Content

RSM 23INDIA BUDGET 2016 - Key Aspects

Chapter 5 Tax Incentives For Businesses

The IT Act provides for far reaching tax holidays and other tax incentives for businesses. We have briefly enumerated below, the significant tax holidays and incentives available to businesses along with the nature of deductions, eligibility criteria, quantum of deduction and period for which the deductions are available. The tax holidays and incentives are subject to fulfillment of specified conditions. The Finance Bill 2016 has set-out a plan to gradually phase out exemptions, deductions and incentives in order to bring down the rate of corporate tax to 25% as announced in Budget Speech 2015. The changes proposed by the Finance Bill, 2016 are highlighted in BOLD font.

(As updated up to the Finance Bill, 2016)

Section Details of Exemption / Deduction ^ Period Quantum of Deduction

10AA First 5 yearsNext 5 years

Next 5 years+

100%50%50%

New eligible unit set up in SEZ on or after 1 April 2005nExemption is available to the entrepreneur as referred

to in Section (2j) of SEZ Act, 2005 for profits derived from export of articles or things or services, manufactured, or produced or provided by an eligible unit.

nThe profits and gains derived from on-site development of computer software (including services for development of software) outside India shall be deemed to be the profits and gains derived from the export of computer software outside India.

nThe benefit is also available to units engaged in cutting and polishing of precious and semi-precious stones.

nThe deduction under this section is to be computed in the same proportion, which the export turnover of the eligible unit bears with the total turnover of the said unit.

nThe eligible units availing these deductions will be subject to MAT / AMT @ 18.50% (plus applicable surcharge and education cess)

nMAT / AMT paid shall be allowed to be carried forward upto 10 years and credit of MAT / AMT paid shall be available for set-off against the tax as per normal provisions in subsequent years.

nIn case deduction has been claimed under section 10AA for the specified business mentioned in section 35AD(8)(c), no deduction under section 35AD shall be available in the same or any other assessment year in respect of such specified business.

Back to Content

Chapter 5 Tax Incentives For Businesses

RSM 24INDIA BUDGET 2016 - Key Aspects

Section Details of Exemption / Deduction ^ Period Quantum of Deduction

nIt is proposed that no deduction shall be available to units commencing manufacture or production of article or thing / providing services on or after 1 April 2020.

+ The deduction is allowed only on creation of a specified reserve, which is required to be utilized for specified purposes.

33AB Available for every AY

Up to 40% of profits or amount

deposited, whichever is

less

Tea / Coffee / Rubber / development allowancenDeduction is available to assessee engaged in the

business of growing and manufacturing tea, coffee or rubber in India.

nFor claiming the deduction, the amount has to be deposited in a special account with NABARD or any Deposit Account opened by the assessee and approved by the Tea Board or Coffee Board or Rubber Board within 6 months from the end of the financial year or before the due date of furnishing the return of income, whichever is earlier.

nThe amount has to be utilized by the assessee for specified purposes.

33ABA Available for every AY

Up to 20% of profits or amount

deposited, whichever is

less.

Site Restoration Fund – Petroleum or Natural GasnDeduction is available to assessee engaged in the

business of prospecting for, or extraction or production of petroleum or natural gas or both in India and in relation to which the Central Government has entered into an agreement with such assessee.

nFor claiming the deduction, the amount has to be deposited in a special account with SBI opened by the assessee and approved by the Ministry of Petroleum and Natural Gas before the end of the financial year.

nThe amount has to be utilized by the assessee for specified purposes.

Section

32(1)(iia)

Additional DepreciationnGeneral rate of depreciation for plant and machinery is 15% (other than certain specified

types of plant and machinery).nAn assessee engaged in the business of manufacture or production of any article or

thing or in the business of generation or generation and distribution or transmission of power can claim the additional depreciation of 20% on the cost of new plant and machinery (other than ships and aircraft) which are acquired and installed after 31 March 2005.

nFurther, higher additional depreciation @ 35% (instead of above 20%) in respect of the actual cost of eligible new machinery or plant acquired and installed by a manufacturingundertaking or enterprise which is set up in the notified backward area of the State of

Eligibility Criteria, Quantum and Period of Deduction ^

Back to Content

Chapter 5 Tax Incentives For Businesses

RSM 25INDIA BUDGET 2016 - Key Aspects

Section

Andhra Pradesh or Telangana or Bihar or West Bengal on or after the 1 April 2015 and ending before the 1 April 2020. The eligible machinery or plant is mentioned in existing proviso to section 32(1)(iia) of the IT Act.

nThe above additional depreciation shall be allowed only to the extent of 50% (i.e. 10% or 17.5%) if the machinery is put to use for a period less than 180 days in the year of its acquisition and installation and the balance 50% shall be allowed in the immediate next year.

Eligibility Criteria, Quantum and Period of Deduction ^

32AC(1A)

(1B)

(2)

Investment in new plant or machinerynWhere a company is engaged in the business of manufacture or production of an article

or thing, acquires new assets in any financial year exceeding Rs. 25,00,00,000 and such assets are installed before 31 March 2017, then there shall be allowed a deduction of 15% of the actual cost of such new assets over and above the normal depreciation under section 32 of the IT Act in the year in which such assets are installed.

nThe said deduction is available for investment made in new plant and machinery up to 31 March 2017.

nIn case any new asset is sold or otherwise transferred within a period of 5 years, the deduction allowed above shall be deemed to be the income chargeable under the head ‘Profits and Gains of business or profession’ of the financial year in which such new asset is sold or otherwise transferred (In addition to taxability of gains on transfer of such new asset).

32AD Investment in new plant or machinery in certain statesnAdditional investment allowance of an amount equal to 15% of the cost of new asset

acquired and installed by an assessee, if:I. It sets up an undertaking or enterprise for manufacture or production of any article

or thing on or after 1 April 2015 in any notified backward areas in the State of Andhra Pradesh or Telangana or Bihar or West Bengal; and

ii. The new assets are acquired and installed for the purposes of the said undertaking or enterprise during the period 1 April 2015 to 31 March 2020.

nThe above deduction will be allowed over and above the existing deduction under section 32AC of the IT Act.

nIn case any new asset is sold or otherwise transferred within a period of 5 years, the deduction allowed above shall be deemed to be the income chargeable under the head ‘Profits and Gains of business or profession’ of the financial year in which such new asset is sold or otherwise transferred (In addition to taxability of gains on transfer of such new asset).

35AC Expenditure on eligible projects or schemenDeduction is available for expenditure incurred for promoting social and economic

welfare.nAny assessee can claim deduction as under:

nIt is proposed that no deduction shall be available for expenditure incurred on or after 1 April 2017.

To whom payment should be madeAssessee Direct ExpenditureCompany Public sector company, or a local authority

or to an association or institution approved by the National Committee for carrying out any eligible project or scheme

A company can also directly incur expenditure in respect of eligible project and scheme

Others Same as above Not permitted

Back to Content

Chapter 5 Tax Incentives For Businesses

RSM 26INDIA BUDGET 2016 - Key Aspects

Section Eligibility Criteria, Quantum and Period of Deduction ^

35AD Deduction in respect of expenditure on specified businessesnAny expenditure of capital nature (other than expenditure incurred on the acquisition of

any land or goodwill or financial instrument) incurred, wholly and exclusively, during the year for specified business shall be allowed as deduction subject to the specified provisions.

nSpecified business and the year (in which the operations to be commenced) for availing deduction under this section are tabulated as under:

Specified BusinessSr. No

Specified year of Commencement

1 Setting up and operating a cold chain facility From 1 April 2009 onwards *2 Setting up and operating a warehousing facility for

storing agricultural produceFrom 1 April 2009 onwards *

3 Laying and operating a cross-country natural gas or crude or petroleum oil pipeline network for distribution, including storage facilities being an integral part of such network

From 1 April 2007 onwards

4 Building and operating a hotel of 2 star or above category as classified by the Central Government anywhere in India

From 1 April 2010 onwards **

5 Building and operating a hospital with at least 100 beds for patients anywhere in India

From 1 April 2010 onwards *

6 Developing and building a housing project under a scheme for slum redevelopment or rehabilitation framed by the Central or State Government, as the case may be, and which is notified by the Board in this behalf in accordance with the guidelines as may be prescribed

From 1 April 2010 onwards

7 The Business of developing and building a housing project under a scheme for affordable housing framed by the Central Government or a State Government, as the case may be, and notified by the Board in this behalf in accordance with the guidelines as may be prescribed

From 1 April 2011 onwards *

8 Production of fertilizers in India through a new plant or a newly installed capacity in an existing plant

From 1 April 2011 onwards *

9 Setting up and operating an inland container depot or a container freight station notified or approved under the Customs Act, 1962

From 1 April 2012 onwards

10 Bee-keeping and production of honey and beeswax From 1 April 2012 onwards

11 setting up and operating a warehousing facility for storage of sugar

From 1 April 2012 onwards

12 Laying and operating a slurry pipeline for transportation of iron ore

From 1 April 2014 onwards

13 Setting up and operating a semiconductor wafer fabrication manufacturing unit, if such unit is notified by the Board in accordance with the prescribed guidelines

From 1 April 2014 onwards

* Specified business referred at Sr. No. 1, 2, 5, 7 and 8 in the above table commencing operations on or after 1 April 2012 shall be eligible for deduction of 150% of capital expenditure

Back to Content

35CCA Deduction for payment towards rural development programmesn100% Deduction is allowed subject to fulfillment of certain conditions for any sums paid to:

i. An association or institution for carrying out any programme of rural developmentii. An association or institution for training of persons for implementation of rural

development programmeiii. National Fund for Rural Developmentiv. National Urban Poverty Eradication Fund

35CCC Weighted deduction of expenditure incurred on agriculture extension projectnThis section provides for weighted deduction of 150% of the expenditure incurred on

agricultural extension project. The conditions for eligibility of agricultural extension project have been provided under Rule 6AAD and Rule 6AAE of the IT Rules.

nFurther, where a deduction under this section is claimed and allowed for any assessment year, in respect of any expenditure on agricultural extension project, no deduction shall be allowed in respect of such expenditure under any other provisions of the IT Act for the same or any other assessment year.

nIt is proposed that no deduction shall be available for expenditure incurred on or after 1 April 2017.

35CCD Weighted deduction of expenditure incurred on skill development projectnAny expenditure (not being expenditure in the nature of cost of any land or building)

incurred on skill development project shall be eligible for weighted deduction of 150% in the hands of a company. The conditions of eligibility of skill development project have been provided under Rule 6AAF to Rule 6AAH of the IT Rules.

Chapter 5 Tax Incentives For Businesses

RSM 27INDIA BUDGET 2016 - Key Aspects

Section Eligibility Criteria, Quantum and Period of Deduction ^

incurred. It is proposed that deduction shall be restricted to 100% of capital expenditure incurred on or after 1 April 2017.** Where the assessee builds a hotel of 2 star or above category as classified by the Central Government and subsequently, while continuing to own the hotel, transfers the operation thereof to another person, the said assessee shall be deemed to be carrying on the ‘specified business’ of building and operating hotel as referred at Sr. No. 4 in the above table, with retrospective effect from AY 2011-12.nAny asset, in respect of which a deduction is claimed and allowed under this section, shall

be used only for the specified business for a period of 8 years beginning with the financial year in which such asset is acquired or constructed.

nWhere such asset is used for any purpose other than the specified business, then, the total amount of deduction so claimed and allowed in any financial year in respect of such asset (after reducing the depreciation allowable under section 32 of the IT Act on deduction allowed under section 35AD of the IT Act), shall be deemed to be income of the assessee chargeable under the head ‘Profits and gains of business or profession’.

nWhile computing AMT, adjusted total income shall be increased by the deduction claimed under section 35AD of the IT Act as reduced by the amount of depreciation allowable under section 32 of the IT Act.

nIn case deduction has been availed under section 35AD of the IT Act on account of capital expenditure incurred for the purposes of specified business in any assessment year, no deduction under section 10AA of the IT Act or under the provisions of Chapter VI-A or under any other provisions of the IT Act shall be available in the same or any other assessment year in respect of such specified business.

Back to Content

Chapter 5 Tax Incentives For Businesses

RSM 28INDIA BUDGET 2016 - Key Aspects

Section Eligibility Criteria, Quantum and Period of Deduction ^

nFurther, where a deduction under this section is claimed and allowed for any assessment year in respect of any expenditure on skill development project, no deduction shall be allowed in respect of such expenditure under any other provisions of the IT Act for the same or any other assessment year.

nIt is proposed that no deduction shall be available for expenditure incurred on or after 1 April 2020.

Section Details of Deduction ^

35(1)(i)

35(1)(ii)

35(1)(iia)

35(1)(iii)

35(1)(iv)

35(2AA)

35(2AB)

Proposed Quantum of deduction of

sum paid / expenditure

incurred

ExistingQuantum of deduction of

sum paid / expenditure

incurred

Weighted deduction on various expenditure incurred on scientific researchAny expenditure (not being in nature of capital expenditure) laid or expended on scientific research related to business carried on by the assessee.Any sum paid to an approved research association, (which has its object of undertaking scientific research) or to a university, college or other institution to be used for scientific research. Any sum paid to an approved company to be used by it for scientific research. Such approved company will not be entitled to claim weighted deduction under section 35(2AB) of the IT Act. However, deduction to the extent of 100% of the sum spent as revenue expenditure on scientific research, which is available under section 35(1)(I) of the IT Act will continue to be allowed.Any sum paid to approved research association (which has its object of undertaking research) or university, college or other institution to be used for research in social science or statistical research.Any capital expenditure (other than expenditure on land and building) incurred on scientific research related to the business carried on by the assessee.Any sum paid to a National Laboratory or a University or an Indian Institute of Technology or a specified person with a specific direction that the said sum shall be used for scientific research undertaken under a programme approved by the prescribed authority, Any expenditure incurred up to 31 March 2017 (other than expenditure on cost of land and building), on in-house research and development facility, as approved by the prescribed authority, incurred by the company, engaged in the business of bio-technology or manufacture or production of article or thing (except those specified in the Eleventh Schedule).

100%

175%

125%

125%

100%

200%

200%

100%

150%*100%**

100%***

100%***

100%

150%*100%**

150%*100%**

Back to Content

Chapter 5 Tax Incentives For Businesses

RSM 29INDIA BUDGET 2016 - Key Aspects

Section Details of Deduction ^ Proposed Quantum of deduction of

sum paid / expenditure

incurred

ExistingQuantum of deduction of

sum paid / expenditure

incurred

Deduction under the said section shall be allowed only if the company enters into an agreement with the prescribed authority for co-operation in such research and development facility and fulfills prescribed conditions with regard to maintenance and audit of accounts and also furnishes prescribed reports.

* From FY 2017-18 to FY 2019-20 ** From FY 2020-21 onwards*** From FY 2017-18 onwards

Section Eligibility Criteria, Quantum and Period of Deduction54G Capital gains arising on transfer of plant, machinery, land, building or any rights in land /

building effected in course of or in consequence of the shifting of an industrial undertaking situated in an urban area to any area (other than an urban area) shall be eligible for exemption. This exemption shall be least of the following:

nAmount of capital gains;nAmount of capital gains utilized within a period of 1 year before or 3 years after the

date of transfer of the above assets, for purchase of new plant and machinery, land and building and for shifting expenses, subject to specified conditions.

Exemptions from Capital Gains in certain cases ^

54GA Capital gains arising on transfer of plant, machinery, land, building or any rights in land / building effected in course of or in consequence of the shifting of an industrial undertaking situated in an urban area to any SEZ shall be eligible for exemption. This exemption shall be least of the following:

nAmount of capital gains;nAmount of capital gains utilized within a period of 1 year before or 3 years after the

date of transfer of the above assets, for purchase of new plant and machinery, land and building and for shifting expenses, subject to specified conditions.

54GB nLong term capital gains shall be exempt in the hands of an individual or an HUF on sale of a residential property (house or plot of land) on or before 31 March 2017 in case of re-investment of the net consideration in the equity of a newly start-up SME company in the manufacturing sector and the SME company utilizes the said funds for purchase of new plant and machinery, subject to the certain conditions.

nIt is proposed to amend section 54GB so as to provide that long term capital gains arising on account of transfer of a residential property before 31 March 2019 shall not be charged to tax if such capital gains are invested in subscription of shares of a company which qualifies to be an eligible start-up.

nIndividual or HUF should hold more than 50% shares of the company and such company should utilize the amount invested to purchase new asset (including computers or computer software for technology driven eligible start-up) before due date of filing of return by the investor.

nEligible start-up and eligible business shall have the same meanings as assigned in section 80-IAC(4).

Back to Content

Chapter 5 Tax Incentives For Businesses

RSM 30INDIA BUDGET 2016 - Key Aspects

Section Eligibility Criteria, Quantum and Period of Deduction

Exemptions from Capital Gains in certain cases ^

54EC nCapital gain on transfer of a long term capital asset shall be exempt from tax, if an assessee invests, within a period of 6 months from the date of transfer of a long-term capital asset, the capital gains in the specified asset. The specified asset must be held for a period of 3 years from the date of its acquisition. This exemption shall be least of the following:– Investment in specified assets viz. bonds issued by NHAI and the RECL. The

investment is restricted up to Rs. 50,00,000 per assessee per financial year. – Amount of capital gains.

nFurther, the exemption in respect of capital gains upon aforesaid investments made during the financial year in which the original asset or assets are transferred and in the subsequent financial year shall not exceed Rs. 50,00,000.

Section Eligibility Criteria, Quantum and Period of Deduction / Exemption ^

10(34)/ 10(35)

Dividend referred to in section 115-O and income received in respect of units of mutual fund or shares shall not be included in the total income of assessee (other than individual, HUF and firm earning dividend income from shares exceeding Rs. 10,00,000 in a financial year).

10(34A)

Any income arising to an assessee, being a shareholder on account of buy back of shares as referred in section 115QA (not being listed on a recognized stock exchange) by the company shall not be included in the total income of assessee.

10(38) Capital gain arising from transfer of long term capital asset being an equity share in a company or a unit of an equity oriented fund or unit of a business trust, on which securities transaction tax is charged, is exempt from tax. However, this exemption is not available for computation of MAT.

54EE nCapital gain on transfer of a long term capital asset shall be exempt from tax, if an assessee invests the capital gains in the specified assets within a period of 6 months from the date of transfer of a long-term capital asset.

nThis exemption shall be least of the following:- Investment in specified assets viz. a unit or units, issued before the 1 April, 2019 of

fund notified by the Central Government. - Rs. 50,00,000 per assessee per financial year - Amount of capital gains.

nFurther, the exemption in respect of capital gains upon aforesaid investments made during the financial year in which the original asset or assets are transferred and in the subsequent financial year shall not exceed Rs. 50,00,000.

nThe specified asset must be held for a period of 3 years from the date of its acquisition. Further, in a case an assessee takes any loan or advance on the security of such specified asset, he shall be deemed to have transferred such specified asset on the date on which such loan or advance is taken.

9(1)(i) -Explan-

ation (1)(e)

It is proposed to provide that in the case of a foreign company engaged in the business of mining of diamonds, no income shall be taxed from the activities which are confined to the display of uncut and unassorted diamond in any special notified zone by the Central Government.

Back to Content

Chapter 5 Tax Incentives For Businesses

RSM 31INDIA BUDGET 2016 - Key Aspects

Section Eligibility Criteria, Quantum and Period of Deduction / Exemption ^It is further proposed that any long term capital gains arising out of transaction undertaken on a recognised stock exchange located in any International Financial Services Centre and where the consideration for such transaction is paid or payable in foreign currency shall also be exempt under the said section. Further, MAT under section 115JB shall be applicable at the concessional rate of 9% plus applicable surcharge and cess.

10(48A)

It is proposed to provide that any income accruing or arising to a foreign company on account of storage of crude oil in a facility in India and sale of crude oil therefrom to any person resident in India shall not be included in the total income subject to approval of Central Government.

115BBD

Any dividend declared, distributed or paid by the specified foreign company to Indian company shall be taxable at a concessional tax rate of 15%.

115BBF It is proposed to provide that any royalty income earned by resident patentee in India in respect of a patent developed and registered in India shall be taxable at the concessional rate of 10% (plus applicable surcharge and cess) on the gross amount of royalty.

115-O In computing DDT liability, dividend declared by the domestic holding company to its shareholders shall be reduced to the extent of:

i. Dividend received from the domestic subsidiary company during the year on which DDT has already been paid by subsidiary under this section.