public financial management & accountability in urban...

TRANSCRIPT

Ministry of Urban Development Ministry of Urban Development –– Government of IndiaGovernment of India

Public Financial Management & Public Financial Management & Accountability in Urban Local BodiesAccountability in Urban Local Bodies

Over the years there has been a decline of local self Over the years there has been a decline of local self government institutions in India in terms of inadequate government institutions in India in terms of inadequate devolution of powers and poor management and devolution of powers and poor management and governance.governance.

There has been a complete lack of financial viability and There has been a complete lack of financial viability and sustainability of local self government institutions sustainability of local self government institutions ((ULBsULBs).).

This has resulted in inadequate in service delivery at This has resulted in inadequate in service delivery at ground level.ground level.

Ministry of Urban Development Ministry of Urban Development –– Government of IndiaGovernment of India

Public Financial Management & Public Financial Management & Accountability in Urban Local BodiesAccountability in Urban Local Bodies

To arrest this decline government amended the To arrest this decline government amended the Constitution to recognize the importance of local self Constitution to recognize the importance of local self government institutions and ensure the devolution of government institutions and ensure the devolution of legislative, financial and administrative powers.legislative, financial and administrative powers.

The 74The 74thth Amendment mandated the constitution of Amendment mandated the constitution of ULBsULBsand the holding of regular elections.and the holding of regular elections.

It identified 18 functions to be devolved to It identified 18 functions to be devolved to ULBsULBs..

It mandated the constitution of State Finance It mandated the constitution of State Finance Commissions for recommending revenue sharing norms Commissions for recommending revenue sharing norms between states and between states and ULBsULBs..

Ministry of Urban Development Ministry of Urban Development –– Government of IndiaGovernment of India

Regulation of slaughter houses and tanneriesRegulation of slaughter houses and tanneries1818Public amenities including street lighting, parking lots, bus stPublic amenities including street lighting, parking lots, bus stops and public conveniencesops and public conveniences1717Vital statistics including registration of births and deathsVital statistics including registration of births and deaths1616Cattle pounds, prevention of cruelty to animalsCattle pounds, prevention of cruelty to animals1515Burials and burial grounds, cremations, cremation grounds and elBurials and burial grounds, cremations, cremation grounds and electric crematoriumsectric crematoriums1414Promotion of cultural, educational, and aesthetic aspectsPromotion of cultural, educational, and aesthetic aspects1313Provision of urban amenities and facilitiesProvision of urban amenities and facilities-- parks, gardens and playgroundsparks, gardens and playgrounds1212Urban poverty alleviationUrban poverty alleviation1111Slum improvement and upSlum improvement and up--gradationgradation1010

Safeguarding the interests of weaker sections society including Safeguarding the interests of weaker sections society including the handicapped and the handicapped and mentally retardedmentally retarded

99Urban forestry, protection of environment and ecologyUrban forestry, protection of environment and ecology88Fire servicesFire services77Public health, sanitation, conservancy and SWMPublic health, sanitation, conservancy and SWM66Water supplyWater supply-- domestic, industrial and commercialdomestic, industrial and commercial55Roads and bridgesRoads and bridges44Planning for economic and social developmentPlanning for economic and social development33Regulation of landRegulation of land--use and construction of buildingsuse and construction of buildings22Urban Planning including town planningUrban Planning including town planning11Functions listed in 12Functions listed in 12thth ScheduleScheduleNoNo

Ministry of Urban Development Ministry of Urban Development –– Government of IndiaGovernment of India

Public Financial Management & Public Financial Management & Accountability in Urban Local BodiesAccountability in Urban Local Bodies

Despite the 74Despite the 74thth Amendment, the situation did not change Amendment, the situation did not change on the ground because the Constitution did not mandate a on the ground because the Constitution did not mandate a time period for the implementation of this amendment.time period for the implementation of this amendment.

The implementation of the spirit of the Amendment was The implementation of the spirit of the Amendment was also hampered by the lack of political will of the states.also hampered by the lack of political will of the states.

The transfer of functions was not accompanied by the The transfer of functions was not accompanied by the transfer of funds and functionaries so it led to the tardy transfer of funds and functionaries so it led to the tardy implementation of the 74implementation of the 74thth Amendment. Amendment.

Ministry of Urban Development Ministry of Urban Development –– Government of IndiaGovernment of India

Public Financial Management & Public Financial Management & Accountability in Urban Local BodiesAccountability in Urban Local Bodies

To reverse this process of decay and decline of urban To reverse this process of decay and decline of urban governance, the Government of India conceived the governance, the Government of India conceived the Jawaharlal Nehru National Urban Reform Mission Jawaharlal Nehru National Urban Reform Mission (JNNURM).(JNNURM).

Basic thrust of JNNURM is planned development of Basic thrust of JNNURM is planned development of urban areas through improved urban governance. urban areas through improved urban governance.

Ministry of Urban Development Ministry of Urban Development –– Government of IndiaGovernment of India

Public Financial Management & Public Financial Management & Accountability in Urban Local BodiesAccountability in Urban Local Bodies

JNNURM is the flagship urban program of the JNNURM is the flagship urban program of the Government of India. Government of India.

The substance of the program is improvement of The substance of the program is improvement of governance through implementation of reforms. governance through implementation of reforms.

Total outlay of JNNURM is USD 12 Total outlay of JNNURM is USD 12 bnbn. or . or RsRs. 50,000 . 50,000 crorescrores approximate equal amount to be contributed by approximate equal amount to be contributed by states and states and ULBsULBs..

JNNURM grants are conditional on the implementation JNNURM grants are conditional on the implementation of reforms.of reforms.

PFMA reforms are a part of JNNURM.PFMA reforms are a part of JNNURM.

Double entry accrual based Double entry accrual based accounting systemaccounting systemEE--Governance: IT/GIS Governance: IT/GIS applicationsapplicationsProperty tax reform Property tax reform

using GISusing GISCollection efficiency : 85%Collection efficiency : 85%

Levy of reasonable user charges:Levy of reasonable user charges:Full recovery of O&MFull recovery of O&M

Internal budget earmarkingInternal budget earmarkingBasic services for poorBasic services for poor

Provision of seven basic services Provision of seven basic services to urban poorto urban poor…….at affordable .at affordable pricesprices

DecentralisationDecentralisation as per 74as per 74thth

Constitutional AmendmentConstitutional AmendmentRepeal of ULCRA*Repeal of ULCRA*Reform Rent Control Law*Reform Rent Control Law*EnactmentEnactment-- Public Disclosure Public Disclosure LawLawEnactmentEnactment-- Community Community Participation LawParticipation LawAssigning city planning and Assigning city planning and other municipal functions to other municipal functions to ULBULB

* * -- not mandatory for water supply, not mandatory for water supply, sanitation and prosanitation and pro--poor projectspoor projects

ULBState

Reform Agenda : Mandatory

ByeBye--laws revision: streamline approval process for constructionlaws revision: streamline approval process for constructionSimplify landSimplify land--use conversionuse conversion

-- Agriculture to NonAgriculture to Non--Agriculture useAgriculture useProperty Title Certification system in Property Title Certification system in ULBsULBsEarmarking for EWS/LIG: 20Earmarking for EWS/LIG: 20--25% land in housing projects25% land in housing projectsComputerisedComputerised registration of land & propertyregistration of land & propertyRevision of byeRevision of bye--laws: for compulsory rain water harvestinglaws: for compulsory rain water harvestingReRe--use of recycled wateruse of recycled waterAdministrative reformsAdministrative reformsStructural reformsStructural reformsEncouraging PPPEncouraging PPP

ULBs/ States

Reform Agenda : Optional

Ministry of Urban Development Ministry of Urban Development –– Government of IndiaGovernment of India

Public Financial Management & Public Financial Management & Accountability in Urban Local BodiesAccountability in Urban Local Bodies

Since PFMA is an integral part of JNNURM, the Since PFMA is an integral part of JNNURM, the MoUDMoUDrequested the World Bank to conduct a diagnostic study requested the World Bank to conduct a diagnostic study on the status of PFMA in on the status of PFMA in ULBsULBs..

This presentation is based on draft results of PFMA Study This presentation is based on draft results of PFMA Study on on ULBsULBs which was conducted by the World Bank under which was conducted by the World Bank under the guidance of the guidance of MoUDMoUD to provide inputs to JNNURM.to provide inputs to JNNURM.

Ministry of Urban Development Ministry of Urban Development –– Government of IndiaGovernment of India

Public Financial Management & Public Financial Management & Accountability in Urban Local BodiesAccountability in Urban Local BodiesFor the purpose of this study basic tenets of PFMA were For the purpose of this study basic tenets of PFMA were taken to comprise:taken to comprise:

Legislative FrameworkLegislative FrameworkAccounting (including Budgeting and Cash Accounting (including Budgeting and Cash Management)Management)AuditAuditInternal Control Internal Control ProcurementProcurement

In each area the study devised Benchmarks, assessed them In each area the study devised Benchmarks, assessed them against Policy and Progress to be able to gauge performance against Policy and Progress to be able to gauge performance under the JNNURM.under the JNNURM.

Benchmarks in different functional areas covered in Benchmarks in different functional areas covered in subsequent slides.subsequent slides.

Ministry of Urban Development Ministry of Urban Development –– Government of IndiaGovernment of India

Public Financial Management & Public Financial Management & Accountability in Urban Local BodiesAccountability in Urban Local Bodies

Legislative FrameworkLegislative Framework

Key Benchmark Key Benchmark : Prevailing rules and regulations should provide : Prevailing rules and regulations should provide an enabling environment for key aspects of PFMA.an enabling environment for key aspects of PFMA.Policy Policy : State Acts do exist but they are vague in specific : State Acts do exist but they are vague in specific requirements requirements Practice Practice : Requirements of State Municipal Acts often not adhered : Requirements of State Municipal Acts often not adhered to. to. Progress Progress : : MoUDMoUD suggests Model Municipal Law and crucial suggests Model Municipal Law and crucial changes to the rules that accompany Municipal Acts to ensure thachanges to the rules that accompany Municipal Acts to ensure that t they are comprehensive.they are comprehensive.MoUDMoUD mandated Disclosure Laws for mandated Disclosure Laws for ULBsULBs under JNNURM.under JNNURM.

Ministry of Urban Development Ministry of Urban Development –– Government of IndiaGovernment of India

Public Financial Management & Public Financial Management & Accountability in Urban Local BodiesAccountability in Urban Local BodiesAccounting, Planning and BudgetingAccounting, Planning and Budgeting

Key BenchmarkKey Benchmark : : Reliable financial information to be Reliable financial information to be available to decision makers that is based on cogent budgets available to decision makers that is based on cogent budgets that are consistent from one year to the next, are participatorythat are consistent from one year to the next, are participatoryand reflect the priorities of the peopleand reflect the priorities of the people

Policy Policy :: Most Municipal Acts do provide for annual Most Municipal Acts do provide for annual accounts. Budgeting is also required to be done. But, there is accounts. Budgeting is also required to be done. But, there is nothing to mandate participatory budgets or budgets that are nothing to mandate participatory budgets or budgets that are realistic and outcome based.realistic and outcome based.

Public Financial Management & Public Financial Management & Accountability in Urban Local BodiesAccountability in Urban Local Bodies

Accounting, Planning and Budgeting Cont..Accounting, Planning and Budgeting Cont..

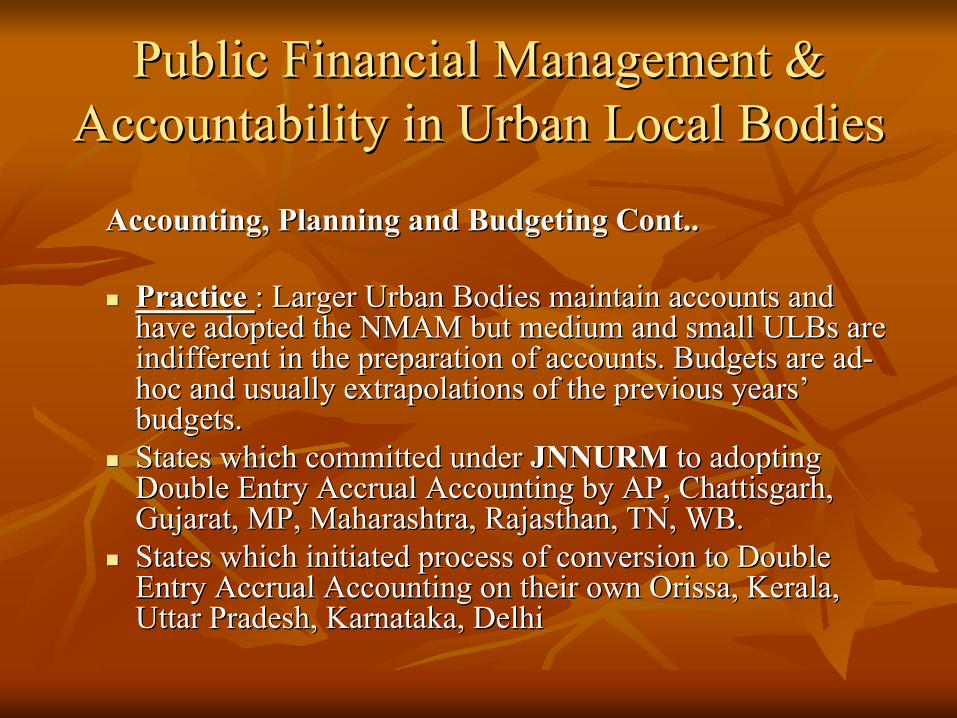

Practice Practice : Larger Urban Bodies maintain accounts and : Larger Urban Bodies maintain accounts and have adopted the NMAM but medium and small have adopted the NMAM but medium and small ULBsULBs are are indifferent in the preparation of accounts. Budgets are adindifferent in the preparation of accounts. Budgets are ad--hoc and usually extrapolations of the previous yearshoc and usually extrapolations of the previous years’’budgets.budgets.States which committed under States which committed under JNNURMJNNURM to adopting to adopting Double Entry Accrual Accounting by AP, Double Entry Accrual Accounting by AP, ChattisgarhChattisgarh, , Gujarat, MP, Maharashtra, Rajasthan, TN, WB.Gujarat, MP, Maharashtra, Rajasthan, TN, WB.States which initiated process of conversion to Double States which initiated process of conversion to Double Entry Accrual Accounting on their own Entry Accrual Accounting on their own Orissa, Kerala, Orissa, Kerala, Uttar Pradesh, Karnataka, DelhiUttar Pradesh, Karnataka, Delhi

Ministry of Urban Development Ministry of Urban Development –– Government of IndiaGovernment of India

Public Financial Management & Public Financial Management & Accountability in Urban Local BodiesAccountability in Urban Local BodiesAccounting, Planning and Budgeting ContAccounting, Planning and Budgeting Cont……

Progress Progress : Introduction of accrual accounting mandatory : Introduction of accrual accounting mandatory under JNNURM. under JNNURM.

But there are states which are still to initiate the conversion But there are states which are still to initiate the conversion to to double entry accounts like double entry accounts like Punjab, Bihar, HP, Jharkhand, Punjab, Bihar, HP, Jharkhand, Uttaranchal, Manipur, J&K, A P, Assam, Tripura, Mizoram, Uttaranchal, Manipur, J&K, A P, Assam, Tripura, Mizoram, Nagaland, Sikkim.Nagaland, Sikkim.

This study defines a discrete set of activities with time lines This study defines a discrete set of activities with time lines that would be required for that would be required for ULBsULBs to switch to full accrual and to switch to full accrual and to adopt participatory multi year outcome based budgeting.to adopt participatory multi year outcome based budgeting.

Ministry of Urban Development Ministry of Urban Development –– Government of IndiaGovernment of India

Public Financial Management & Public Financial Management & Accountability in Urban Local BodiesAccountability in Urban Local BodiesAudit Audit

Key Benchmark Key Benchmark : Providing assurance to stakeholders that : Providing assurance to stakeholders that money was used for the money was used for the puposespuposes intendedintended

PolicyPolicy : Municipal Acts require annual audits by the Local : Municipal Acts require annual audits by the Local Fund Auditors but no penal actions on non performanceFund Auditors but no penal actions on non performance

Practice Practice : Larger : Larger ULBsULBs or those that moved to the market for or those that moved to the market for funds are able to furnish have audited accounts, but the audit funds are able to furnish have audited accounts, but the audit quality is suspect. Medium and Small quality is suspect. Medium and Small ULBsULBs have a few have a few decades of audit arrearsdecades of audit arrears

Public Financial Management & Public Financial Management & Accountability in Urban Local BodiesAccountability in Urban Local Bodies

Audit Audit

ProgressProgress : : MoUDMoUD and the C&AG have started thinking and the C&AG have started thinking about ways to strengthen the Local Fund Audit offices about ways to strengthen the Local Fund Audit offices through the preparation of Manuals and guides. Other ways through the preparation of Manuals and guides. Other ways of building capacity of the LFA are also under of building capacity of the LFA are also under consideration like Certification Programs.consideration like Certification Programs.

Ministry of Urban Development Ministry of Urban Development –– Government of IndiaGovernment of India

Public Financial Management & Public Financial Management & Accountability in Urban Local BodiesAccountability in Urban Local Bodies

Internal ControlInternal Control

Key Benchmark :Key Benchmark : Clearly defined systems and procedures Clearly defined systems and procedures backed by policies to monitor activities of each department backed by policies to monitor activities of each department and function area. and function area.

PolicyPolicy : Most Acts governing : Most Acts governing ULBsULBs do not provide fordo not provide forinternal audit. internal audit.

ContCont……

Ministry of Urban Development Ministry of Urban Development –– Government of IndiaGovernment of India

Public Financial Management & Public Financial Management & Accountability in Urban Local BodiesAccountability in Urban Local Bodies

Internal Control ContInternal Control Cont……....PracticePractice : Larger Corporations are required to have internal : Larger Corporations are required to have internal audit carried out e.g. Chennai and audit carried out e.g. Chennai and KolkataKolkata..

ProgressProgress : : ULBsULBs need to have a separate department for need to have a separate department for Internal Audit and hire or train the necessary staff to conduct Internal Audit and hire or train the necessary staff to conduct the audit functions efficiently. the audit functions efficiently.

Audit Committees to be established.Audit Committees to be established.

Ministry of Urban Development Ministry of Urban Development –– Government of IndiaGovernment of India

Public Financial Management & Public Financial Management & Accountability in Urban Local BodiesAccountability in Urban Local Bodies

ProcurementProcurement

Key BenchmarkKey Benchmark : ULB procurement needs to be efficient : ULB procurement needs to be efficient and managed in a way to ensure and managed in a way to ensure increased competition, valueincreased competition, value--forfor--money and transparency. money and transparency.

Policy Policy : Legislation governing procurement in most cases is : Legislation governing procurement in most cases is defined, though it is very rudimentary and mostly based on defined, though it is very rudimentary and mostly based on lowest cost basis (L1 basis). Most state acts prescribe lowest cost basis (L1 basis). Most state acts prescribe ULBsULBs to follow State/PWD rules for the purpose of to follow State/PWD rules for the purpose of procurement. procurement.

Public Financial Management & Public Financial Management & Accountability in Urban Local BodiesAccountability in Urban Local BodiesProcurement ContProcurement Cont……

Practice Practice : No concept of value for money. No specialized : No concept of value for money. No specialized procurement procurement departrmentdepartrment. Limited transparency. In most . Limited transparency. In most ULBsULBs there is inadequate linkage of procurement with there is inadequate linkage of procurement with planning. planning. Departments need to be encouraged during the budget Departments need to be encouraged during the budget preparation to review and plan their tentative procurement preparation to review and plan their tentative procurement schedules and timeframes, so that budgets can be schedules and timeframes, so that budgets can be appropriately allocated. appropriately allocated.

Ministry of Urban Development Ministry of Urban Development –– Government of IndiaGovernment of India

Public Financial Management & Public Financial Management & Accountability in Urban Local BodiesAccountability in Urban Local Bodies

Procurement ContProcurement Cont…………..

Practice Practice : Most states still do not have any standard : Most states still do not have any standard documents directing procurement procedures and outlining documents directing procurement procedures and outlining the forms to be used at various stages of procurements. the forms to be used at various stages of procurements.

Lack of standardized procedures also results in delays in Lack of standardized procedures also results in delays in tendering processes and award. tendering processes and award.

Delays largely happen at the evaluation and approval stage Delays largely happen at the evaluation and approval stage since proposals are received in different formats making it since proposals are received in different formats making it difficult to evaluate. This can lead to substantial cost difficult to evaluate. This can lead to substantial cost overruns for the bidder and procurer. overruns for the bidder and procurer.

Public Financial Management & Public Financial Management & Accountability in Urban Local BodiesAccountability in Urban Local BodiesProcurement ContProcurement Cont…………..

Progress Progress : Many states have implemented the : Many states have implemented the Tender Transparency Act. Some progress is being Tender Transparency Act. Some progress is being made in this area through emade in this area through e--procurement. procurement.

Going forward Model guidelines and Tender Going forward Model guidelines and Tender documents need to be developed.documents need to be developed.

Ministry of Urban Development Ministry of Urban Development –– Government of IndiaGovernment of India

Public Financial Management & Public Financial Management & Accountability in Urban Local BodiesAccountability in Urban Local Bodies

The PFMA study presented a palette of discrete actions in The PFMA study presented a palette of discrete actions in the accounting and budgeting the accounting and budgeting alongwithalongwith timelines that the timelines that the JNNURM could pick up for inclusion.JNNURM could pick up for inclusion.

MoUDMoUD ((GoIGoI) has covered significant ground in the area ) has covered significant ground in the area of accounting and public disclosure through JNNURM of accounting and public disclosure through JNNURM but other areas such as Audit, Procurement and Internal but other areas such as Audit, Procurement and Internal Control still have some distance to cover.Control still have some distance to cover.