public disclosure authorized inancial olivia...

TRANSCRIPT

CONFIDENTIAL FOR RESTRICTED USE ONLY (NOT FOR USE BY THIRD PARTIES)

FINANCIAL SECTOR ASSESSMENT

BOLIVIA AUGUST 2012 FINANCIAL AND PRIVATE SECTOR DEVELOPMENT VICE PRESIDENCY LATIN AMERICA AND THE CARIBBEAN REGION VICE PRESIDENCY

THE WORLD BANK A joint IMF-World Bank mission visited La Paz during March 2 to March 15, 2011, for an update of the Financial Sector Assessment Program (FSAP) conducted in 2004.1 As agreed with the authorities, the FSAP Update focused on (i) banking system issues, including financial soundness indicators, stress testing, competition and efficiency, regulations, supervision, resolution, and safety nets; (ii) payments systems; (iii) access to financial services in rural areas and fostering credit to the productive sector; and (iv) assess compliance with Basel Core Principles. This report summarizes the main findings of the mission and the policy priorities identified, focusing on financial development issues.

1 The mission was composed of Luisa Zanforlin (IMF, MCM mission co-chief), Aquiles A. Almansi (WB, FPDPO mission co-chief), Gregorio Impavido (IMF, MCM), Torsten Wezel (IMF, MCM), Richard Munclinger (IMF, MCM), Pierre-Laurent Chatain (WB, FPDPO), Juan Buchenau (WB, LCSPF), Ceu Pereira (WB), José Tuya (IMF expert), Javier Bolzico (IMF expert), and Ilka Funke (WB expert).

Pub

lic D

iscl

osur

e A

utho

rized

Pub

lic D

iscl

osur

e A

utho

rized

Pub

lic D

iscl

osur

e A

utho

rized

Pub

lic D

iscl

osur

e A

utho

rized

i

Contents Page

I. Overall Assessment and Main Recommendations .............................................................................................. 3

II. Financial Sector Structure and Performance ...................................................................................................... 6 A. Banks and Specialized Credit Entities (SCEs) ..................................................................... 6 B. Insurance Sector .................................................................................................................. 12 C. Capital Markets ................................................................................................................... 13 D. Pensions .............................................................................................................................. 14

III. Payments System ............................................................................................................................................ 16

IV. Financial Inclusion ......................................................................................................................................... 17

V. Financial Regulation and Supervision ............................................................................................................. 20 A. Banking regulation and supervision ................................................................................... 21 B. Regulatory framework for specialized credit entities ......................................................... 23 C. Insurance Regulation and Supervision ............................................................................... 24 D. Pension supervision ............................................................................................................ 24 E. Securities Supervision ......................................................................................................... 25

VI. Financial Safety Net ....................................................................................................................................... 25 A. Exceptional Liquidity Assistance ....................................................................................... 25 B. Bank Resolution Scheme .................................................................................................... 26 C. The Financial Restructuring Fund ...................................................................................... 27

VII. Appendixes ................................................................................................................................................... 28 A. Appendix I. Tables ............................................................................................................. 28

Figures Figure 1. Bank Concentration and Competition ..................................................................................... 8 Figure 2. Average Banking Sector Returns-on-Equity for Selected Countries ...................................... 9 Figure 3. Average Banking Sector Net Interest Margin for Selected Countries .................................... 9 Figure 4. Total Loans By Type of Lender ............................................................................................ 11

Tables Table 1. Bolivia: 2011 FSAP Update Main Recommendations ............................................................ 5 Table 2. Bolivia: Banks Revenue, Costs, and Return on Average Assets, 2003–10 .............................. 7 Table 3. Bolivia: Total Liquid Assets of the Financial Sector ............................................................. 10 Table 4. Bolivia: Insurance Market Summary Indicators ..................................................................... 13 Table 5. Bolivia: Insurance Market Profitability .................................................................................. 13 Table 6. Bolivia: Private Pension System Summary Indicators ........................................................... 15 Table 7. Bolivia: Pension Portfolio Distribution .................................................................................. 15 Table 8. Bolivia: Financial Penetration Indicators ............................................................................... 18 Table 9. Bolivia: Financial Sector Structure ........................................................................................ 28 Table 10. Bolivia: Financial Soundness Indicators .............................................................................. 29

ii

Glossary ACH: Automated Clearing House for Direct Debits and Transfers AFP Pension Fund Administrator APS: Pensions and Insurance Authority ASFI: Financial System’s Supervisory Authority ASOBAN: Association of Private Banks of Bolivia BCB: Central Bank of Bolivia BDP: Bank of Productive Development BOL: Boliviano CAR: Capital Adequacy Ratio CCC: Checks Clearing House CPI: Consumer Price Index CPISIPS: Core Principles for Systemically Important Payment Systems COMA: BCB’s Open Market Operations Committee DPF: Bank-issued Certificate of Deposit DVP: Delivery versus payment EDV: Central Securities Depository ELA: Emergency Liquidity Assistance FFP: Private Financial Fund FIU: Financial Intelligence Unit FRF: Financial Restructuring Fund GPI: Gross Premium Income HHI: Hirschman-Herfindahl Index IFD: Development Financial Institutions IBNR: Incurred but not reported LBFI: Banking Law LIP: Integrated Payments Settlement System MELID: Differed operations settlement mechanism MELOR: Delayed operations settlement mechanism MFI: Microfinance Institution NEP: Net Earned Premium NIR: Net International Reserves NPL: Nonperforming loan NPS: National Payments System OMO: Open Market Operations RAL: Fund of required liquid assets ROA: Return on Assets ROE: Return on Equity RTGS: Real Time Gross Settlement System SAFI: Mutual Fund Administrator SIPAV: High-Value Payments system SPT: Treasury accounts TRE: Reference Interest Rate UPR: Unearned premium reserves

3

I. OVERALL ASSESSMENT AND MAIN RECOMMENDATIONS

1. Bolivia’s recent macroeconomic performance has been favorable, although inflation has become a concern. An export boom, led by the hydrocarbon and mining sectors, has supported strong economic growth since 2004. Sustained external and fiscal surpluses have allowed for unprecedented accumulation of international reserves. Currency appreciation and policy measures have significantly reduced the dollarization of the economy. Inflationary pressures rekindled in late 2010 and early 2011, turning real interest rates negative. The authorities, however, stepped up efforts to reduce domestic liquidity, quickly bring real interest rates to positive levels.

2. The institutional and legal framework in Bolivia is undergoing a profound transformation. The 2009 Constitution increased the role of the state in the economy, requiring the review of a large number of laws, which has not yet been completed. Developmental policy objectives inspired changes in the prudential framework supporting credit to key sectors. A new pension law required the consolidation of the existing two private pension funds into a single state-managed fund.

3. Banks have strengthened their financial position but recent rapid credit growth may have increased risks. Following distress in the early 2000s, banks have restructured loans and shed nonperforming assets, while enjoying good profitability. Banks appear relatively efficient and indicators of competition are only slightly below those in the rest of Latin America (although they also face the competition of non-bank MFIs, which play a large role in the Bolivian financial system, but are not included in the standard competition indicators). The system’s capital adequacy ratio (CAR) stood at 12 percent at end 2010, in excess of the regulatory minimum of 10 percent. Credit quality indicators appear strong, with low nonperforming loans (NPLs) and high provisioning coverage, but lending to the private sector, which averaged 16 percent growth since 2007, accelerated to 18 percent in 2010 due to low interest rates and policy measures promoting lending to certain sectors, should be expected to increase credit risk.

4. Credit risks are compounded by the structure of the loan portfolios of Bolivian banks. The loan portfolio is either indexed to a variable reference interest rate (TRE) or denominated in foreign currency (FX), and a sharp increase in interest rates or a depreciation of the boliviano, including in response to the recently observed inflationary pressures, would increase the loan service burden on largely unhedged borrowers. In addition, a significant share of loans is secured by possibly overvalued real estate. Finally, the quality of underwriting and risk-management is limited by weaknesses in data collection and financial statements.

4

5. Liquidity in the system is abundant but unevenly distributed, with close to a fifth of deposits owned by the public pension fund. Deposit-taking institutions other than commercial banks suffer from limited access to the interbank market, and lack of assets eligible for emergency liquidity assistance (ELA). Close to 20 percent of banks’ deposits belong to the new publicly managed pension fund, leaving bank liquidity highly dependent on its investment decisions.

6. While significantly reduced, the current level of dollarization in the financial system continues to pose challenges. Partial dollarization leaves banks exposed to sudden shifts in depositor sentiment that might lead to a sudden increase in FX liabilities. This risk is compounded by new regulations limiting the ability of banks to hold assets abroad, thus constraining the active management of FX positions. A new regime on minimum reserve requirements introduced in January 2012 will, however, contribute to reduce the system’s partial dollarization by gradually increasing the types of foreign-currency denominated deposits subject to an additional 45 per cent requirement

7. Progress has been made in strengthening the supervisory framework, but more work is needed, including implementing recently enacted legislation. Supervisory arrangements have been clarified; presidential decrees allowing forbearance were amended, and, among other, new requirements have been issued for managing liquidity, credit, and exchange rate risks. However, the system still lacks a deposit insurance scheme and the regulatory and supervisory frameworks for anti-money laundering and combating the financing of terrorism (AML/CFT) should be strengthened as planned. Finally, recent legislation merits amendment to: (i) strengthen the operational and budgetary independence of supervisors; (ii) reintroduce legal protection for supervisors; and (iii) avoid using prudential measures to direct credit to key sectors of the economy.

8. Regulatory measures were introduced to foster access to financial services, but stronger attention needs to be placed on lowering the costs of delivering services. The government introduced regulatory reforms aiming at stimulating productive sector credit and enhancing consumer protection. Going forward, it is suggested to introduce a framework for innovative delivery channels (smaller service points, nonbank agents and mobile banking solutions). Furthermore, efforts could be undertaken to strengthen the payments system and credit bureau infrastructure, reforming the movable collateral and factoring regime, introducing leasing, and clearly and narrowly defining the mandate of public financial institutions to remove potential competitive distortions. A survey to assess the use of financial services would be recommended to better target the measures.

The main FSAP recommendations are reported in Table 1.

5

Table 1. Bolivia: 2011 FSAP Update Main Recommendations

2 ASFI: Financial Sector Supervisory Authority; APS: Pension and Insurance Supervisory Authority; FRF: Financial Restructuring Fund; FIU: Financial Intelligence Unit. 3 High priority recommendations are indicated as “Short term.”

Recommendations2 Horizon3

Macro prudential Keep real lending rates positive to avoid unsound credit growth. Short term

Supervisory Framework Appoint ASFI’s executive director officially and specify in the law the conditions for

dismissal. Short term

Align ASFI’s APS’ internal capacity and resources with their growing workload and responsibilities.

Short term

Restore full legal protection for ASFI staff in performing their duties. Short term

Commercial Banking Sector

Ensure that classification and provisioning requirements are based solely on credit risk considerations.

Short term

Eliminate limits on total foreign investments as a share of capital. Short term

Add market risk (interest rate and foreign exchange) to capital requirements. Short term

Complete work on operational and interest rate risk guidance. Short term

Make the financing of terrorism a criminal act. Short term

Provide the FIU with adequate human resources. Medium term

The ASFI should increase the intensity, frequency, and coverage of supervision in financial institutions, including formalizing the on-site inspection cycle.

Short term

Establish clear cooperation mechanisms between the FIU and ASFI. Short term

Improve the operations of the credit bureaus. Short term

Microfinance

Promote partial credit guarantee schemes, registries for movable assets. Medium term

Specify the mandate of public financial institutions. Medium term

Carry out financial literacy and promotion campaigns. Short term

Insurance

Update the legal framework. Medium-term

Conduct a study on adequacy of reserves and reinsurance arrangements. Short term

Increase the frequency of on-site inspection to a one-year cycle. Medium term

Pensions Strengthen selection criteria standards for public pension fund directors. Short term

Auction all insurance risk to insurance providers. Short term

Maintain the current strong investment framework. Short term

Payment Systems Enact a Payments System Law. Medium term

Formalize cooperation with ASFI. Short term

Establish criteria to access payment system and eliminate discretion. Medium term

Supervise all institutions offering money-transfer services. Short term

Safety nets Include a deposit insurance scheme in the FRF framework. Short term

6

II. FINANCIAL SECTOR STRUCTURE AND PERFORMANCE

A. Banks and Specialized Credit Entities (SCEs)

9. Main players in the financial system are the commercial banks, the public pension fund, and a variety of non-bank deposit-taking institutions. About 50 percent of the financial system’s assets are held by commercial banks; 28 percent by the new public pension fund; and 18 percent by other deposit-taking institutions, including private financial funds (fondos financieros privados, FFP), credit associations (mutuales) that provide mortgage financing; credit cooperatives (cooperativas), and mutual and development financing institutions (IDFs), which are in the process of being brought under formal supervision.4

10. Commercial banks are largely domestically owned. Foreign ownership in the banking sector is limited, with only one large foreign bank holding close to 15 percent of total assets.5 There are two public banks: the fifth largest commercial bank, Banco Unión, and a small second-tier bank, Banco de Desarrollo Productivo (BDP), holding 6 percent and 1.5 percent of total bank assets respectively. Some banks are part of financial groups that include an insurance company, a brokerage company, and an asset management fund, but nonbanking activities typically represent less than 10 percent of the groups’ assets.

11. Bolivia has a vibrant microfinance industry, with the vast majority being supervised or in the process of being brought into regulatory oversight. The microfinance and specialized credit industry currently represents 20 percent of total credit. Microfinance lending is mostly undertaken by regulated FFPs and MFI-banks. The largest microfinance institution, a fully licensed bank, accounts for 8 percent of domestic credit (up from less than 3 percent in 2003). Other deposit-taking institutions, such as the cooperatives and the mutual credit associations are historically specialized by loan type but are becoming increasingly diversified.6

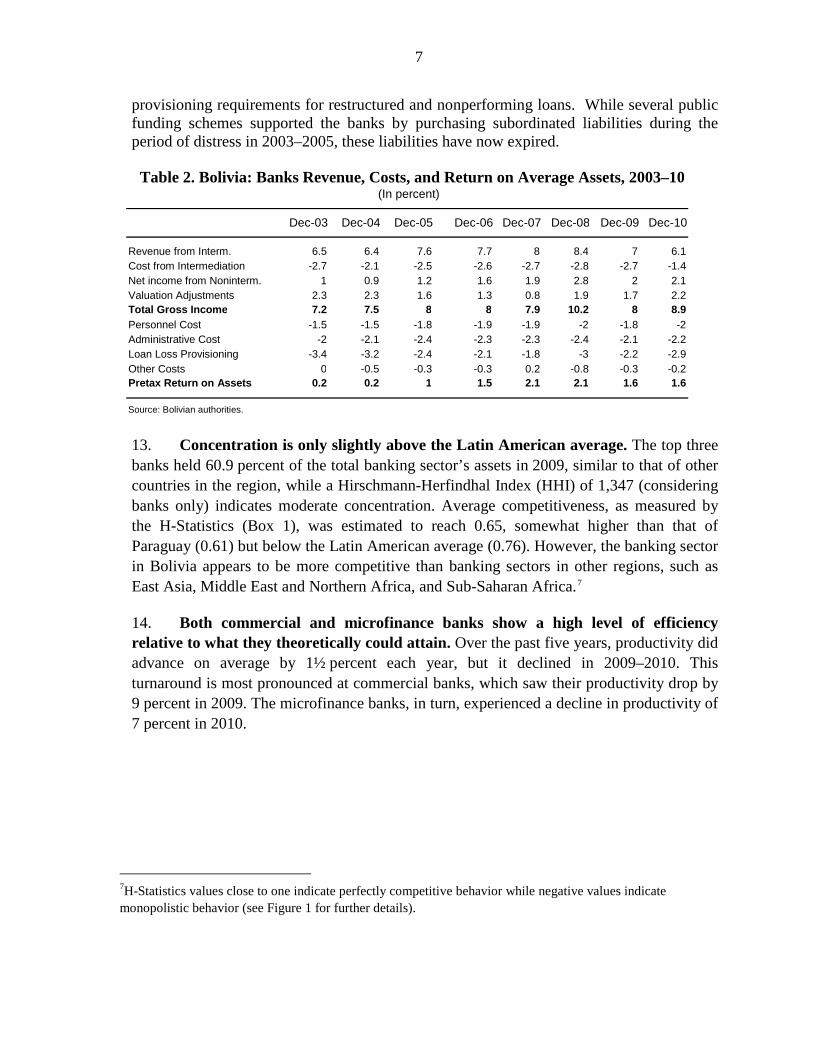

12. Following deep distress in 2003–04, strong economic performance has allowed the banking sector to improve profitability and strengthen its capital base. Not directly affected by the international crisis, the banking sector has remained profitable and net-interest margins have been stable since 2008, in line with other countries (Table 2, Figures 2 and 3). Banks have restructured their corporate loan portfolios and complied with

4ASFI is the supervisor for commercial banks and other deposit-taking institutions. 5The estimated Hirschmann-Herfindhal Index (HHI) is 1,347. 6FFPs have traditionally directed their activities to SMEs. Mutual credit associations have exclusively financed mortgage housing, and cooperatives have focused on consumer loans.

7

provisioning requirements for restructured and nonperforming loans. While several public funding schemes supported the banks by purchasing subordinated liabilities during the period of distress in 2003–2005, these liabilities have now expired.

13. Concentration is only slightly above the Latin American average. The top three banks held 60.9 percent of the total banking sector’s assets in 2009, similar to that of other countries in the region, while a Hirschmann-Herfindhal Index (HHI) of 1,347 (considering banks only) indicates moderate concentration. Average competitiveness, as measured by the H-Statistics (Box 1), was estimated to reach 0.65, somewhat higher than that of Paraguay (0.61) but below the Latin American average (0.76). However, the banking sector in Bolivia appears to be more competitive than banking sectors in other regions, such as East Asia, Middle East and Northern Africa, and Sub-Saharan Africa.7

14. Both commercial and microfinance banks show a high level of efficiency relative to what they theoretically could attain. Over the past five years, productivity did advance on average by 1½ percent each year, but it declined in 2009–2010. This turnaround is most pronounced at commercial banks, which saw their productivity drop by 9 percent in 2009. The microfinance banks, in turn, experienced a decline in productivity of 7 percent in 2010.

7H-Statistics values close to one indicate perfectly competitive behavior while negative values indicate monopolistic behavior (see Figure 1 for further details).

Dec-03 Dec-04 Dec-05 Dec-06 Dec-07 Dec-08 Dec-09 Dec-10

Revenue from Interm. 6.5 6.4 7.6 7.7 8 8.4 7 6.1 Cost from Intermediation -2.7 -2.1 -2.5 -2.6 -2.7 -2.8 -2.7 -1.4 Net income from Noninterm. 1 0.9 1.2 1.6 1.9 2.8 2 2.1 Valuation Adjustments 2.3 2.3 1.6 1.3 0.8 1.9 1.7 2.2 Total Gross Income 7.2 7.5 8 8 7.9 10.2 8 8.9 Personnel Cost -1.5 -1.5 -1.8 -1.9 -1.9 -2 -1.8 -2 Administrative Cost -2 -2.1 -2.4 -2.3 -2.3 -2.4 -2.1 -2.2 Loan Loss Provisioning -3.4 -3.2 -2.4 -2.1 -1.8 -3 -2.2 -2.9 Other Costs 0 -0.5 -0.3 -0.3 0.2 -0.8 -0.3 -0.2 Pretax Return on Assets 0.2 0.2 1 1.5 2.1 2.1 1.6 1.6

Source: Bolivian authorities.

Table 2. Bolivia: Banks Revenue, Costs, and Return on Average Assets, 2003–10 (In percent)

8

Figure 1. Bank Concentration and Competition Some evidence of monopolistic competition was observed in the banking sector. The H-Statistics developed by Panzar and Rosse (1987) assigns a value to the level of competition between agents in specific industrial groups by measuring the elasticity of interest revenue to a change in costs. Values close to 1 indicate perfectly competitive behavior while negative values indicate monopolistic behavior. In all other cases, commonly referred to as monopolistic competition, the H Statistic will take a value between zero and 1. The estimated long run value of the H-statistics for Bolivia was 0.65 (for 2003–10), which compares to a score of 0.61 recently computed for Paraguay (using the same methodology). If compared to results of recent cross-country study (WB Policy Research W.P. No. 5363), Bolivia’s banking sector would appear to be less competitive than the average of Latin America (0.76 in that study) but still more competitive than banking systems in other regions, such as East Asia, Middle East and Northern Africa, and Sub-Saharan Africa. However, competition appears to have declined recently, as the H-Statistic for the sub-period of 2007–10 was estimated to be close to zero.

0

10

20

30

40

50

60

70

80

90

100

0

10

20

30

40

50

60

70

80

90

100

Arge

ntin

a

Ecua

dor

Para

guay

Boliv

ia

Hon

dura

s

Vene

zuel

a

Gua

tem

ala

Peru

Jam

aica

Banking Concentration Indices in Latin America(Index)

Sources: World Bank.

9

Figure 2. Average Banking Sector Returns-on-Equity for Selected Countries

Source: FinStats/Bankscope-Bureau Van Dijk

Figure 3. Average Banking Sector Net Interest Margin for Selected Countries

Source: FinStats/Bankscope-Bureau Van Dijk

10

15. Large short-term deposits represent the largest share of commercial banks’ liabilities. Deposits still represent the largest source of banks’ funding, amounting to 80 percent of total liabilities, as the interbank and the securities markets remain very small. In addition, more than half of the deposits are concentrated in accounts larger than US$200,000, corresponding to less than 2 percent of the total bank accounts. Deposits of pension fund administrators, (Administradoras de Fondos de Pensiones, AFPs) represent about 20 percent of total bank deposits.

16. Bank liquidity averages 29 percent of liabilities. If combined with assets eligible for emergency liquidity assistance (ELA), system liquidity averages 43 percent (Table 3). 8 The reserve requirement for domestic currency deposits is 13 percent; however, since the increase in the local-currency loan portfolio above the June 2009 level can be deducted from the computational base, the effectively required reserves are only 6 percent.

17. SCEs have lower liquidity levels than the commercial banks. Own liquidity is as low as 12 percent for mutuales and 16 percent for cooperatives, even after combining with assets eligible for BCB’s refinancing.

Table 3. Bolivia: Total Liquid Assets of the Financial Sector

18. In 2010, widespread rumors triggered two quickly contained episodes of rapid deposit withdrawal. One was related to fears of unsoundness of a particular bank; the other involved the entire banking sector and lead to an outflow of about 3 percent of total deposits in two days.

19. Banking system liquidity is considerably dependent on the investment decisions of the new public pension fund. Total direct deposits and Banks’ Certificates of Deposit (DPFs) owned by the preexisting private pension funds amount to 35 percent of total pension assets, or around 20 percent of bank deposits.

8Under current provisions, total eligible assets for ELA amount to US$1,259, representing 14 percent of total deposits and 12 percent of Net International Reserves (NIR).

Repo Other Total liquidity TotalImmediate Invest. RAL securities Repo through BCB liquidLiquidity 1/ Abroad 70 percent BCB-TGN Securities Operations assets Deposits Coverage

Banks 1861.8 204.1 376.1 904.3 160.8 1441.2 3507.1 7739 45.3Mutuales 22.7 29.6 70 90.9 190.5 213.2 425 50.2Cooperatives 36.2 36.8 15.9 52.7 88.9 443 20.1FFPs 127.6 27.9 0.7 16.1 44.7 172.3 683 25.2Total 2048.3 204.1 470.5 975.1 283.7 1729.2 3981.6 9290 42.9

Source: Bolivian authorities1/ As of March 2011.

11

20. Credit by commercial banks has picked up significantly in the past year, supported by high liquidity and changes in the regulatory environment. Rapid credit growth (Figure 4 could lead to even more rapid accumulation of credit risk. This might particularly be the case for household credit, where the scarcity of data constrains the banks’ ability to screen borrowers. In the corporate sector, according to a credit bureau, financial statements are not drafted following consistent accounting principles, and are not available for many SMEs.

21. Loan concentration in the commercial banking sector tends to be high. Reflecting the same patterns of deposits (see below), more than 35 percent of total bank loans are extended to 0.3 percent of borrowers, providing limited credit-risk diversification. Exposures to the real estate sector are significant in some financial institutions, while real estate prices have been reportedly increasing rapidly.9 However, loan-to-value ratios remain within prudent standards.

22. A significant share of private sector credit continues to be extended in foreign currency, a reflection of the high FX-deposit base. The authorities have been adjusting the regulatory and prudential framework to discourage FX lending by reducing the

9Unfortunately there is no real estate index, nor data on housing prices. However, indicators of activity in the real estate sector have been rising rapidly: the index of construction activity has been growing at a rate above 10 percent for the last two years and total banks’ loans to the construction and real estate sector have been growing close to 20 percent in the past three years.

0

1

2

3

4

5

6

7

0

10

20

30

40

50

60

70

80

2005 2006 2007 2008 2009 2010

Commercial Banks Other financial institutions Total Loan (secondary axis)

In percent of GD P

In billions of U .S. dollars

Figure 4. Total Loans By Type of Lender

Source: Bolivian authorities.

12

allowable net open position in FX, and the share of foreign assets in total assets. The authorities have also introduced higher provisioning requirements for foreign currency loans vis-à-vis domestic currency loans, so as to prompt the banking sector to internalize the risks of extending FX loans to un-hedged domestic borrowers. Despite a significant reduction from levels above 90 percent, foreign currency and FX-indexed loans still represent close to 50 percent of private sector credit.

23. The maturity mismatch between interest-sensitive assets and liabilities is limited. The short-term nature of the deposit base has led banks to extend loans on a floating rate basis. In this way, increases in deposit interest rates tend to be matched by increases in the interest rate on loans, as they are based on the TRE. Such loans may, however, generate significant increases in debt service if the TRE responds to recently observed inflationary trends, weakening the financial performance of borrowers.

B. Insurance Sector

24. The insurance market is small and highly concentrated. With US$255 million in gross premium income (GPI) in 2010, it is one of the smallest insurance markets in the region. Nonlife and life companies operate in the market with a penetration of 0.9 percent and 0.3 percent of GDP respectively, and insurance density of only US$16 and US$5 per capita. About 60 percent of the market is controlled by three companies, part of financial conglomerates, while one-third of the market is represented by small family-owned companies.

25. Loss ratios are low and, on average, the sector is profitable, although efficiency could be improved. On average, companies report 16 percent ROEs. The ratio of payout on claims is very low (average loss ratio of 46 percent), while underwriting costs are very large (especially for family owned companies), with an average expense ratio of 50 percent (Table 5). This implies an average underwriting profitability of 2 percent and an overall profitability (when investment income is added) of about 6 percent of net earned premiums. Similarly to other emerging markets, Bolivian insurance companies are highly dependent on yields of invested assets.

26. Investments are concentrated in short-term government debt, with substantial maturity mismatches in the life business. Reflecting the structure of securities traded in the formal markets, short duration fixed-income instruments account for 35 percent and 76 percent of nonlife and life company assets, respectively. This implies substantial maturity mismatches in the life business. Real estate, equities, and DPFs together account for less than 10 percent of nonlife and life company assets.

13

C. Capital Markets

27. Securities markets do not represent a significant source of private sector financing. The institutional investor base largely consists of domestic pension funds. There are seven investment companies and four insurance companies operating in the stock exchange representing about 5 percent of market capitalization. The high degree of informality of the economy restricts private sector issuance to a handful of large corporations, although in the past year specialized credit entities have successfully tapped

2005 2006 2007 2008 2009 2010 Average

Loss Ratio 1/ 47 49 51 48 46 42 47 Expense Ratio 2/ 53 49 49 51 52 50 51 Combined Ratio 3/ 100 98 100 99 98 92 98 Investment Income/NEP 4 3 4 6 5 3 4 Profits/NEP 4 6 4 7 6 11 6 ROE 4/ Na na na 15 14 18 16 Source: Bolivian authorities and Fund staff calculations. 1/ Defined as Net Incurred Claims (NIC) over Net Earned Premiums (NEP). 2/ Defined as Net Expenses (NEX) over Net Earned Premiums (NEP). 3/ Defined as ((NIC+NEX)/NEP). 4/ Return on Equity

Table 5. Bolivia: Insurance Market Profitability

2004 2005 2006 2007 2008 2009 2010

Penetration: 1.8 1.8 1.6 1.2 1.1 1.2 1.2 Life 0.8 0.8 0.7 0.3 0.3 0.3 0.3 Non Life 1.1 1 0.9 0.9 0.9 0.9 0.9

Density (in U.S. dollars): 18 18 19 16 19 21 20 C2 1/:

Life Na 74 73 59 56 57 55 Non Life Na 62 61 59 52 48 46

HHI 2/: Life Na 3,724 3,720 2,302 2,174 2,212 2,250 Non Life Na 2,294 2,288 2,322 2,040 1,990 1,940

Source: Staff computations based on Bolivian authorities' data. 1/ C2 represents the two largest companies assets over total assets. 2/ Hirschman-Herfindahl Index

Table 4. Bolivia: Insurance Market Summary Indicators

14

the market. Overall, private sector issuance represents less than 5 percent of total issues, with public sector-issued instruments representing the bulk of the new issues market.

28. The equities market is shallow and concentrated on papers issued by public sector enterprises. There were 82 companies listed on the Stock Exchange at end 2010, including investment funds and special purpose vehicles for securitization deals of which only 56 are registered to issue securities. Market capitalization stands at US$3 billion or barely 15 percent of GDP, and it is among the lowest of the region. The petroleum sector accounts for 35% of the total equity market. The small free float of most companies leads to high illiquidity, with yearly turnover representing 0.3 percent of the market capitalization.

29. Debt instruments represent by far the largest share of both issuances and traded volume on the stock exchange. Government and central bank securities10 still represent the largest share of outstanding debt, but a decline in issuances by the government and BCB has led bank-issued CDs (DPFs) to dominate the debt market turnover. The strong demand for such securities by pension funds has been the main driver of this development. Although corporate debt issues increased in recent years, the corporate debt market remains relatively small.

D. Pensions

30. The Bolivian pension system follows a multi pillar design, typical of other countries in the region. It includes a social pension in pillar zero and mandatory defined contribution plans in the second pillar. Second pillar pension funds cover only 14 percent of the labor force. The small coverage reflects the large size of the informal sector in the economy.

31. The reform, approved in December 2010, significantly changed the institutional framework. The new public institution will manage the old individual account, annuity and disability funds, together with a new social pension fund aimed at increasing replacement rates of low income earners. The reform increases the investments required in non-credit-rated SMEs to 5 percent of the portfolio and modifies pension variable annuities by introducing annual re-pricing of the annuities as a function of investment and mortality performance.

32. Investment portfolios are concentrated in domestic fixed-income assets. Pension fund portfolios are invested in public sector securities and DPFs traded on the stock exchange (Table 7). Although allowed, no FX investments have been made due to the

10Letras del Tesoro, Bonos del Tesoro, etc.

15

absence of valuation rules for foreign assets and the requirement that this be made through the BCB.

Pension funds provide various types of insurance with potential important intra and intergenerational transfers. Pension funds directly provide disability insurance and variable annuities, insuring inflation and longevity risk outside the solvency framework designed for insurance companies. The reform modified pension variable annuities by introducing annual

re-pricing of the annuities as a function of investment and mortality performance.

2005 2006 2007 2008 2009 2010 1/

Funds' Administrators 2 2 2 2 2 2 Contributors (in thousands of U.S. dollars) 497 508 510 513 558 584 Percent of labor force 12.3 13.3 13.3 12.8 13.4 13.5 Retired (in thousands) 4 9 13 20 25 29 Disability (in thousands) 5 6 8 9 10 11 Assets under management 2/ 2,060 2,299 2,910 3,885 4,626 5,311 In percent of GDP 22 20 22 23 27 30

Source: Bolivian authorities. 1/ As of October 2010. 2/ Individual Accounts.

Table 6. Bolivia: Private Pension System Summary Indicators

2005 2006 2007 2008 2009 2010

Government Paper 70 74.8 72.4 68.5 62.7 56.7 Long Term Bonds 12.8 8.9 8.1 7.8 6.7 10.1 Bank Bonds (Traded) 0 0 0 0.5 0.7 1 Municipal Bonds 0 0 0 0.2 0.2 0.2 Closed Funds 0 0.2 1 1.1 1.2 1.4 DPFs (Traded) 1/ 6.8 11.1 14.6 14.3 20 24.5 Other Fixed Income 0.7 0.4 0.4 3.8 4.8 4.6 Shares 6.3 0.1 0 0 0 0 Time Deposits 2.5 2.7 2.2 0 0 0 Cash 0.9 1.9 1.2 3.7 3.7 1.5 Memo item:

Total Assets Under Management (in millions of US$) 2,060 2,299 2,910 3,885 4,626 5,467

Source: Bolivian Authorities. 1/ "Depositos a Plazo Fijo": term deposits.

Table 7. Bolivia: Pension Portfolio Distribution (In percent)

16

III. PAYMENTS SYSTEM

33. Bolivia has made significant progress in modernizing its NPS over the last several years. A major improvement was the Real Time Gross Settlement System (RTGS) launched in 2004. This system has contributed to a better integration between BCB, the banks, and other financial institutions, and it is processing a growing share of large-value payments. Known as SIPAV, it is the backbone of the payment system, and it provides settlement services for the Checks Clearing House (CCC), the Automated Clearing House for Direct Debits and Transfers (ACH) for credit transfers and direct debits, the Treasury accounts (SPT), and securities (EDV). Due to the volumes it settles, and its unique position as sole entity to provide settlement in central bank accounts, SIPAV is considered a systemically important payment system.

34. SIPAV is broadly in observance of most Core Principles for Systemically Important Payment Systems (CPISIPS), but some key issues are yet to be adequately addressed. Its legal basis is BCB Resolution 131/2009, which includes the main features characterizing modern and safe payment systems: settlement finality, recognition of the digital signature and the certification process, and enforceability of security interests provided under collateral arrangements. Although Resolution 131/2009 also provides for BCB’s ability to oversee SIPAV, and to recognize the use of digital signatures, the absence of a Payments System Law as the legal basis for these two important features is an important gap with respect to Core Principle I. However, BCB has started drafting such a Law. Access to SIPAV is restricted to entities either supervised by ASFI, or discretionarily authorized by BCB’s Board of Directors (and consequently not bound to “objective and publicly disclosed criteria,” as required by Core Principle IX). There is presently no formal consultation mechanism, such as a National Payments Council, to ensure that all parties are consulted and informed on decisions affecting the design and operations of the NPS, and there is no formal cooperation mechanism with ASFI. Finally, BCB’s oversight is not yet fully separated from the system’s operation.

35. BCB is working on a new payments system, LIP (Sistema de Liquidación Integral de Pagos), which would improve the inter-connection between the various subsystems of the NPS. This new system would be partly RTGS, partly netting with queues, and would allow all components of the NPS to operate on the same technical platform, thus improving liquidity management for non-RTGS systems, and further improving their safety.

36. BCB considers CCC systemically important because it is the only existing clearing house for checks. CCC is managed by Administradora de Cámaras de Compensación y Liquidación (ACCL), a private company owned by banks and Association of Private Banks of Bolivia (ASOBAN). Since checks are used mainly for commercial transactions between companies, the average value cleared at BCB is rather high (averaging between US$3800 and US$5550 in 2005 -9), which implies that checks are not

17

primarily retail payment instruments. It is foreseen that the volume cleared at CCC will over time be transferred to either the Automated Clearing House for Direct Debits and Transfers (ACH), or to SIPAV, albeit at a slow pace. ACH, the automated clearing house for transfers and direct debits also managed by ACCL, started its operations in 2006, but its volumes still remain low despite efforts to promote its usage.

37. Central Securities Depository (EDV), a private entity, is the sole central securities depositary in Bolivia. It handles government and corporate securities, and it provides Delivery versus payment (DVP) services, settling at the RTGS in T+0. In order to manage credit risk, the system has introduced the “Mecanismo de Liquidación de Operaciones Retrasadas” (MELOR) and “Mecanismo de Liquidación de Operaciones Diferidas” (MELID), but a liquidity facility (like that of loans against RAL holdings for SIPAV) does not yet exist.

38. While transactions with credit cards have remained stagnant, the use of debit cards has been steadily increasing. Administradora de Tarjetas de Crédito (ATC) and LINKSER are the two networks managing credit and debit card transactions. Both entities are expected to join SIPAV in the short term. They are technically interoperable, but there is no sharing of POSs and ATMs infrastructure, and cardholders are discouraged to use the competing network.

IV. FINANCIAL INCLUSION

39. The government has a strong focus on increasing the access to financial services, particularly in rural areas and for small and micro-enterprises in the productive sectors. Over the past few years, the government actively promoted these areas through (i) the definition of norms for the consolidation of hitherto unregulated cooperatives and Instituciones Financieras de Desarrollo (IFDs); (ii) issuing regulations to stimulate the opening of branches in rural areas, to facilitate credit to the productive sector, and to enhance consumer protection; (iii) providing dedicated funding sources for credit to the productive sector through its second tier bank; and (iv) distributing conditional cash transfers through financial entities. This process has been accompanied by an ongoing dialogue between the government and the different stakeholders in the area of productive credit/rural finance.

40. Partly as a result of government measures, Bolivia’s core indicators of financial access showed a significant improvement over the last three years. The number of branches of formal financial institutions increased by 484 (66 percent) since 2007. This growth was fueled by a rapid expansion of branches of microfinance banks and finance companies (+85 percent), which, by April 2010, accounted for 55 percent of all branches in the formal financial system (up from 45 percent in 2007). The expansion of the branch network contributed to a substantial growth in deposit accounts, by 80 percent in the period during 2007 and 2010, reaching over 4.8 million by end November 2010. In the

18

same period, the number of borrowers in the formal financial system increased by 17 percent. However, a significant shift in the composition of the borrower base took place, away from clients with loans above US$100,000 (declining 25 percent) and clients with loans below US$1,000 (increasing 18 percent), towards micro- and small clients with loans between US$1 to US$30,000 (increasing 47 percent). The number of ATMs in the system has also increased significantly (42 percent), but according to a 2009 survey of the BCB, only 10 percent of the population uses electronic payments, with the vast majority continuing to rely on cash as sole means of payment. In addition to the formal financial system, NGOs and closed cooperatives account have a larger presence in the urban periphery and rural areas, and cater to approximately 350 000 depositors, and 450 000 borrowers. About 15 percent of the adult population has a loan from the formal financial system, while an estimated additional 10 percent has a loan from financial institutions in the transition phase to becoming regulated.

41. Bolivia has now bridged some of the distance in financial penetration rates with respect to its regional peers (Table 8). This overall level of penetration is close to the regional average in Latin America, and well above the 1.2 branches reported for Sub-Saharan Africa. In addition, bank accounts per adult are comparatively high, considering Bolivia’s income level, although there is still a gap with respect to the rest of Latin America. Bolivia also continues to lag behind its peers (in the region and within the same income bracket) with regard to the availability of ATMs and Point of Sales (POS), according to the Financial Access Base (2009).

42. Several barriers must be overcome to further increase the outreach of the formal financial system to hitherto underserved segments of the population. In particular, the following barriers were identified: a) lack of information on the actual use of financial services, b) lack of financial education and cultural factors blocking the use non-cash payment instruments, c) low population density (9 inhabitants per square kilometer) and deficient infrastructure (roads, energy, communications), d) little integration along value chains, lack of conventional financial reporting practices, and business relationships

Number of Number of Country/ Branches per Country/ Deposit Accounts Region 10,000 Adults Region per Adult

Latin America 2.5 Pakistan 0.2 Middle East and Northern Africa 2.3 Paraguay 0.3

East Asia and Pacific 2.1 Nicaragua 0.5 Bolivia 2 Bolivia 0.8 Sub-Saharan Africa 1.2 Latin America 1.9

Source: World Bank.

Table 8. Bolivia: Financial Penetration Indicators

19

based on personal trust rather than written contracts, creating significant information asymmetries that are costly to overcome, and e) limited availability of guarantees, particularly for rural borrowers who cannot use their land as collateral.

43. Affordability does not appear to be a significant issue. Deposit accounts have low minimum deposit requirements, and interest rates for microcredit and consumer credit of 18 percent or less are comparatively low for the region. While longer loan maturities are available in the market, most of the loan portfolio is short term.

44. A survey of the use of financial services, and of perceptions by their users and non-users, would help the authorities define adequate policies and track their impact. This survey could be conducted by the National Statistics Institute under the guidance of the financial sector authorities. The information thus gathered would also be of use for financial entities to design adequate products and services. The authorities should also consider including, on a regular basis, a small financial sector module in the household survey, in order to monitor results and fine-tune reform measures.

45. The supply of loans to the productive sector could be improved by following the proposals made at the ASFI workshop on access to finance in 2010. Some proposals are aimed at improving conditions for the credit-risk management in the productive sector through a) establishment of partial credit guarantee schemes, b) introduction of legislation and registries for the use of movable assets as collateral, c) improvements in the operations of credit bureaus, d) the design and introduction of sustainable insurance products for agriculture (e.g. index-based insurance contracts) and of other micro-insurance products, and e) the establishment of an appropriate legislation for leasing. In addition, it seems advisable to assess options to improve the capacity of rural firms and farms to use their land (or its usufruct) as collateral for small to medium sized investment loans. ASFI should also continue ongoing efforts to define the characteristics of SME loans, while leaving sufficient flexibility to financial entities to define the types of assets that may be used as collateral for such firms. These measures should be accompanied by actions to improve the accounting practices of MSMEs, as well as reform measures to foster value chains in the country.

46. Access to financial services in rural/remote areas could be further expanded by improving the reach of the retail payments system. As a key component in this effort, it is advisable to enhance the regulatory requirements for the operation of smaller service points, non-bank agents, and mobile-banking in the country, to lower the cost of these services.11 The government should also define positive incentives for the entire financial system for the opening of points of service in strategically important locations. Earlier experiences of Fondesif in Bolivia and in other countries (e.g. Bansefi in Mexico) should

11Banking through mobile telephones.

20

be taken into account. Existing policies to channel government payments (such as “renta dignidad”) through financial institutions should continue to involve large segments of the financial system, and options for non-cash delivery of these payment should be explored (such as debit cards, or the direct payment into accounts) to facilitate the introduction of innovative payment delivery channels. These efforts should be complemented by financial literacy campaigns.

47. The mandate of public financial institutions should be clarified and narrowly focused on existing market gaps. Banco Unión has increasingly assumed the role of a development bank in the country, providing first-tier retail financial services to targeted segments of the population, and handling all government payments, including the government to person payments. The latter has the potential to distort the market, and to require the setting up of public sector service points in areas already sufficiently covered by the private financial system. BDP, which has an array of funds for on-lending at its disposition, could play an important role in facilitating the availability of long-term funding, in developing new markets (e.g. along value chains that are not yet fully developed), and in providing partial credit guarantees. In order to prevent public bank failures or contingent liabilities as experienced in other countries, a clear mandates for both institutions needs to be defined and a monitoring and evaluation system should be set up for these institutions to regularly assess their effectiveness in achieving their policy mandate.

48. All actions to promote access to finance should be part of a comprehensive strategy to be managed and monitored by the financial sector authorities, building on their existing coordination and, if needed, involving other government entities. The efforts to expand the reach of the financial system should be coordinated with broader government efforts to improve road infrastructure, the supply of electricity and the delivery of conditional cash transfers.

V. FINANCIAL REGULATION AND SUPERVISION

49. The supervision framework is strong, but the new constitution approved in 2009 has changed the operational framework of supervisory authorities. The coordination of financial policies with the Ministry of Finance mandated by the new constitution has steered the regulatory framework and supervisory practices towards the support of social policies. Some modifications in the prudential framework have reduced the risk-adjusted cost of lending to certain sectors.

50. Prudential requirements should reflect the actual risk of losses and should not be used to promote alternative policy objectives. Regulatory changes skewing the incentives to lend to specific sectors may lead originators to underestimate actual risks and extend credit to unworthy borrowers.

21

51. Legal protection of supervisors, while discharging their functions, is essential to ensure operational independence. The legal protection of supervisors has been lifted since the enactment of the law on combating corruption and illicit enrichment. Consequently, civil, administrative, and criminal actions can be brought against ASFI and APS staff during performance of their duties. Legal protection of staff against claims from third parties would strengthen the operational independence of the agency subject to careful consideration on how the burden of proof is allocated between the parties. Under certain conditions, the agencies should be in a position to reclaim some damages from staff.

52. Strategic decisions will have to be made to provide all supervisory authorities with more resources and training for their staff, to align capacity and resources to growing workload and responsibilities. ASFI’s mandate and scope of work has been significantly extended including for the compliance with AML/CFT regulations. The insurance supervisory authority has only 24 professionals on the supervisory payroll, including one of the four registered actuaries in the country. As a consequence of low salary levels, the average turnover for mid-level staff is very high and, as a result, only three staff members have more than ten years of experience.

A. Banking regulation and supervision

53. Since the previous FSAP in 2004, Bolivia has moved toward aligning its regulatory and supervisory framework with international standards. In 2004, the institutional framework for the supervision of banks suffered from several weaknesses: (i) lack of clarity in the objectives and attributions of the agencies involved; (ii) potential for government interference; (iii) limited independence of the supervisory agencies; and (iv) dubious effectiveness of the coordination mechanism in place. Bolivian authorities have taken action to address several of these problems. In particular:

• The former bodies that were granted overlapping and superseding attributions in the area of financial regulation and oversight no longer exist,12 bringing greater clarity to the supervisory arrangements: ASFI is now the authority to supervise deposit taking and capital market institutions, while APS supervises insurance and pension institutions.

• New requirements for liquidity, credit, and exchange risks were passed. Presidential decrees that gave banks more time to bring their provisions to the adequate level were amended. These changes have reinforced risk-management standards in the banking industry as well as the methodologies for valuation of loans and financial investments.

12 The Ministry of Financial Services and the General Superintendency of the System of Financial Regulation (SIREFI) no longer exist.

22

• Risk supervision practices were improved through the adoption of a new inspection manual that provides detailed guidance to bank examiners during their on-site inspections. A rich offsite system allows ASFI staff to collect a significant quantity of data that are being used for on-going surveillance. The supervisory authority has also reorganized its internal structure to implement a more risk-oriented supervision.

54. Compliance with international standards for effective banking supervision has improved in several areas, but there is room for further progress. Out of the 25 Basel Core Principles, seven principles were given a compliant rating, and 12 principles were found largely compliant. Bolivia has been found materially non compliant for BCP 13 that relates to market risks. Persistent deficiencies in the areas of (i) country risk: (ii) interest risks; and (iii) integrity (AML/CFT) justified a noncompliant rating. In comparison with the 2004 FSAP, improvement in the ratings has been reached in various areas. In the areas of capital adequacy and problem assets/provisioning, ratings shifted from Materially Non Compliant (MNC) to Largely Compliant (LC). For liquidity and internal control principles, the improvement was even greater (from MNC to C) and in the case of corrective measures, the rating was upgraded from non compliant to largely compliant.

55. Despite notable accomplishments, there is still room for improvements in several areas:

• ASFI’s executive director and his last two predecessors have been appointed “ad interim,” following ongoing government reorganizations. In addition, there is no provision in the law that stipulates under which conditions he can be dismissed. Formal appointment and legal protection from arbitrary dismissal would reinforce ASFI autonomy.

• Non-prudential factors have been added to regulatory provisioning levels. Loans to the productive sector are subject to reduced provisioning to encourage lending to the sector. If the loans do not perform, provisions are established in line with the treatment of all other loans. The exception is for performing loans. Although the exception is limited, it is important that credit quality judgments focus on credit worthiness.

• ASFI’s internal risk oversight processes need to be furthered by adopting a risk-based approach. So far, there has been an increased focus on credit, liquidity, and corporate governance risks, but other important aspects—including operational, interest rate, and reputational risks—have yet to be considered. In developing regulations, it is important to maintain close collaboration with the industry to enhance the effectiveness of regulations.

56. Integrity of the Bolivian financial sector is a matter of concern, and authorities are encouraged to address persistent deficiencies in the national AML regime.

23

Bolivia’s AML regulatory and supervisory regime is very weak. Money laundering is not an offense “per se” (because it requires a “precedent” offense), and terrorist financing had not yet been criminalized at the time of the FSAP mission. It was, however, criminalized by Law 170 in September 2011. The FIU suffers from insufficient autonomy, capacity, and resources and does not have enforcement powers. Because of persistent strategic deficiencies in its AML regime, the Financial Action Task Force (FATF) decided in February 2011 to maintain Bolivia under close scrutiny. 13

57. ASFI’s mandate has been extended to include not only banks, but also securities and newly supervised entities (casas de cambios, remittances, development finance companies (IFDs), and 62 cooperativas societarias). In addition, entities that are currently not regulated will soon fall under ASFI scrutiny. Moreover, the implementation of IFRS in banks and the possible migration toward consolidated supervision will create additional pressure. Supervision of compliance with AML/CFT regulations will also merit the recruitment of additional and well qualified staff.

B. Regulatory framework for specialized credit entities14

58. The regulatory framework for banks and specialized credit entities is largely identical. The LBFI (Law 1488) and its regulations place restrictions for specialized credit entities on foreign trade operations, capital investments in securitization companies, the administration of investment funds and factoring and leasing operations. Additionally, SCEs need permission to issue current accounts and credit cards, and finance companies and IFDs can also apply for authorization to invest in financial service auxiliaries. Those permissions have so far not been issued. These distinctions are common in many countries, but nevertheless can lead to cheaper funding sources for banks than their competitors, a competitive edge with regard to credit card issuance, and an advantage over clients with export/import business.

59. Small institutions face relatively high administrative burdens. Regulations on the bulk and frequency of information to be submitted, which have been frequently changed in the past year, have imposed a significant burden on the small financial institutions. The list of information required on a regular basis from the various financial entities is particularly long and cumbersome. ASFI requires the monthly transmission of complete borrower information per financial entity. ASFI could consider whether frequent and extensive reporting is justified for all institutions. However, the requested data allows ASFI to develop a substantive picture of the financial health of each financial institution.

13 Bolivia was also excluded from the Egmont Group in 2008.

14 In Spanish “Intermediarios No Bancarios.”

24

C. Insurance Regulation and Supervision

60. A modernization of the insurance regulatory framework would help address some important deficiencies. The main insurance law passed in 1999 has not been updated since then. It does not include, among others, corporate governance rules for insurers (a project currently pursed by the authorities), information disclosure and supervision of sales channels, especially brokers, the calculation methodology of incurred but not reported (IBNR) claim reserves for nonlife insurers, a special supervision regime for intervened companies, and intervention and liquidation of insurers in general.

61. The surveillance function is well-designed, although additional information could be required. A manual to conduct financial analysis of companies has been developed based on the Mexican experience. This is supported by a well-developed system of early warning ratios and prudential forms on, among others, minimum capital requirement and solvency margin, reserves adequacy, quality of reinsurance arrangements, underwriting performance, income, assets, and compliance with investment rules. Both the frequency and type of information received is adequate, although consideration should be given to request information on premiums and claims on a policy-by-policy level. In addition, companies should be required to file information on trends of claims over time to strengthen the analysis of the adequacy of claims’ reserves.

62. Intervention powers and the regulatory framework for exit are detailed in the main law but are not fully developed. The law provides for adequate intervention powers for the authority, including fines, admonitions, and the ability to restrict commercial activities in individual lines of business, transfer policies to other companies, intervene, remove management, and revoke the license. However, the insurance law does not grant the supervisor powers to force restructuring. In addition, there is no manual defining a special supervisory regime for companies at risk of being insolvent, nor are there manuals to guide supervisory action during forced intervention and liquidation.

63. The newly created insurance supervisor (APS) should have budgetary independence and the capacity to retain talented staff. During the mission, the directorate for insurance supervision was being merged with the pension supervisory authority to form a new Authority for Pension and Insurance Supervision (APS). The legal capacity for prudential norms and supervisory intervention that was provided by the legal department in ASFI would need to be reconstituted in APS. In addition, supervisory staff will enter the much lower salary scale used for civil servants. Finally, the insurance operational budget of US$4 million will be used to subsidize pension supervision that lost its source of financing with the recent pension reform.

D. Pension supervision

64. A strong focus on transparency should dispel any concerns about the operations and operational framework of the new public pension system. A special

25

decree would be required to strengthen selection standards for the public pension fund directors (contained in the new law). In addition, the existing strong investment framework—requiring at least 95 percent of assets to be invested in tradable securities—should be maintained (as currently planned by the authorities) to ensure that disclosure requirements are respected and that the new fund assumes investment risks with full information.

E. Securities Supervision

65. The regulatory pillars for the stock exchange and market participants have been completed but need to be modernized. The stock exchange regulation was approved in 2005, and the regulatory framework for mutual funds administrators (SAFIs) and securities brokers was approved in 2004. ASFI supervises the EDV. ASFI also regulates the credit rating agencies and issuances of equity and fixed-income securities, open funds, and closed-end funds, including securitization vehicles. ASFI does not regulate derivative contracts.

66. Securities have to be submitted to ASFI for approval prior to public offer, a process usually plagued by delays. It currently takes up to five months to obtain certification. Streamlining procedures and administrative requirements, and increasing the number of dedicated staff, would help reduce the delays and increase private sector recourse to securities markets. ASFI also reviews new securities for consumer protection purposes.

VI. FINANCIAL SAFETY NET

A. Exceptional Liquidity Assistance

67. The ELA function of the BCB is broadly flexible and well-designed. In cases of illiquidity, the BCB can provide loans guaranteed by RAL (authorizing banks to use their reserves) and loans secured by eligible collateral. The BCB’s COMA determines the assistance conditions for the ELA, which will be provided at penalty rates, for a limited time, and against collateral, with no pre-defined intervention limit.

68. Rules on collateral eligibility limit the BCB´s capacity to provide ELA.15 Bank loans are de facto not eligible for ELA, because the BCB would lose any senior claim to the collateral received in guarantee if the institution is liquidated.16 This implies that under

15Resolution BCB 037/2003. 16Art. 131 of Law 1488.

26

the current framework, BCB can only provide liquidity up to 4 percentage points of total liabilities to the cooperatives.

69. To enhance the BCB’s intervention capacity, existing regulations should be modified to ensure that all financial institutions can access sufficient liquidity in case of emergency. In particular, the following amendments to the current framework would increase BCB capacity to perform ELA functions: (i) broaden the scope of collateral eligible for refinancing operations to senior participation notes issued by trusts funded by high quality loans; (ii) amend Art.131 of LBFI Law to ensure that BCB would maintain a senior claim on collateral guaranteeing liquidity operations in those cases the financial institution is subsequently deemed insolvent and liquidated; (iii) subsequently to such amendment, further broaden the collateral eligible for refinancing operations to include high quality loans; and (iv) create a liquidity fund to complement the BCB resources available for the ELA function.

70. The authorities have decided to de-centralize the BCB treasury operations to service remote areas. With only one treasury in La Paz and limited physical amount of FX notes, the BCB incurs a high operational risk in case of runs in remote areas of the country. This limitation became evident during the run in December 2010. As a result, the authorities decided to de-centralize treasury operations in three cities to reduce operational risk in case of emergency.

B. Bank Resolution Scheme

71. The legal framework for bank resolution is largely in line with best practices. The LBFI gives ASFI the legal powers—and the adequate tools—to carry out bank resolution, using good-bank/bad-bank structures. This involves a special purpose vehicle (trust) designed to liquidate good assets and transfer deposits to a sound financial institution, which receives a claim on the liquidation value of the good assets recovered. The system has worked well in the past. Minor changes could be introduced in the legislation to streamline its operational aspects, removing provisions requiring equivalence of excluded asset and liabilities. To support the resolution procedure, the law stipulates that the Financial Restructuring Fund (FRF) can provide funds under "the least cost rule", albeit under some limitation (see below). Since 2001 ASFI has applied successfully the resolution procedure to small intermediaries, but there has been no experience with medium and large intermediaries.

72. There is no specific provision in the bank resolution framework, neither in the FRF nor in the ELA framework, for systemic situations. The authorities should consider whether it would be useful for Bolivia to extend the safety net to banks facing systemic distress.

73. Bank resolution processes are complex and require skilled and trained personnel for proper implementation. While there is an ASFI team that focuses on bank

27

resolution, high staff turnover has diminished the overall operational expertise within ASFI.

C. The Financial Restructuring Fund

74. The FRF is a bank resolution instrument, not a deposit insurance fund. FRF is a fund managed by the BCB, which invests its resources in safe and liquid instruments. The Ministry of Finance, the BCB, and ASFI each appoint a member of the Board, thereby ensuring coordination by the three agencies. Regulations provide that FRF can contribute up to 30 percent of the preferred obligations of an intervened financial intermediary to support the transfer of deposits to another institution during a resolution procedure (see above).17 However, if no receiving bank is found for the deposits, the bank falls into forced liquidation and FRF cannot compensate depositors.

75. The new constitution may weaken FRF’s effectiveness if its resources are insufficient to support a transfer of deposits. Existing FRF resources are insufficient to provide the legal maximum support of 30 percent of a resolution procedure of any top four intermediaries of the system, nor of two medium-sized entities, and the new Constitution explicitly prohibits the BCB, together with all public entities and institutions, from assuming the debts of banks or private financial institutions.

76. The financial safety net needs to be strengthened. It currently has no provisions on (i) bank resolution in cases of systemic distress; (ii) the functions of the Financial Restructuring Fund (FRF); or (iii) ELA functions for cases of systemic distress.

77. An explicit deposit insurance scheme, managed by the FRF, would enhance the crisis management framework. The supervisory framework is sufficiently strong, and corrective actions are sufficiently enforceable, to support a deposit insurance system. FRF’s resources and governance would seem adequate for this purpose. Expanding the functions of the FRF to become a full deposit guarantee fund for retail depositors would reduce uncertainties and strengthen the bank resolution framework.

17The FRF resources can be used for any regulated financial institution.

28

VII. APPENDIXES

A. Appendix I. Tables

Table 9. Bolivia: Financial Sector Structure

Number of Institutions

Total Assets (US$)

Share of System

Percent of GDP

Deposit-taking institutions - - Commercial banks 12 9,263,024,762 51.3 51.5 Open cooperatives 24 570,551,875 3.2 3.2 Mutual credit associations 8 912,317,852 5.0 5.1 FFPs 6 581,090,396 3.2 3.2 Entities in process of regularization 77 659,949,976 3.7 3.7 Closed cooperatives 63 406,494,634 2.2 2.3 Development finance institutions 14 253,455,342 1.4 1.4 Institutional investors - - Brokerage companies 9 133,196,799 0.7 0.7 Mutual funds administrators (SAFI) 8 15,228,996 0.1 0.1 Pension funds 2 1/ 5,240,696,834 29.0 29.1 Insurance companies 14 690,472,669 3.8 3.8 Total 18,066,530,159 100.0 100.0

Source: Bolivian authorities and Fund staff estimates.

1/ Prior to the December Pension Reform.

29

Table 10. Bolivia: Financial Soundness Indicators 2005 2006 2007 2008 2009 2010 Capital adequacy Bank regulatory capital to risk-weighted assets* 14.6 13.3 12.6 13.7 13.3 11.9 Regulatory tier 1 capital to risk-weighted assets NA 12.5 11.8 12.98 12.8 11.7 Capital to total assets 11.3 10.0 9.0 9.3 8.7 8.4

Asset Quality Bank nonperforming loans to total loans* 11.3 8.7 5.6 4.3 3.5 2.2 Bank provisions to nonperforming loans 85.9 106.5 132.4 153.7 165.7 189.4 High risk loans to total loans 23.9 18.5 12.6 9.3 7.3 4.8 Provisions to high risk loans 40.7 45.7 54.5 67.3 75.7 98.9 Nonperforming loans net of provisions to capital 12.5 5.0 -4.2 -7.7 -7.7 -9.6 High risk loans net of provisions to capital 77.7 58.1 32.4 15.4 8.7 0.3

Earning and profitability Bank return on assets 0.6 0.9 1.9 1.7 1.7 1.3 Bank return on equity 6.4 8.6 21.2 20.3 20.6 17.3 Interest income to gross Income 64.1 70.2 95.4 91.9 59.5 56.4 Non-interest expenses to gross income 11.7 3.2 -27.6 -42.3 11.0 4.7

Liquidity Liquid Assets (Disponibilidades) to total deposits 14.0 16.7 15.1 14.7 24.6 21.5 Foreign currency loans to total loans 92.9 84.8 81.5 68.9 62.7 55.1

Source: Bolivian authorities and Fund staff estimates.