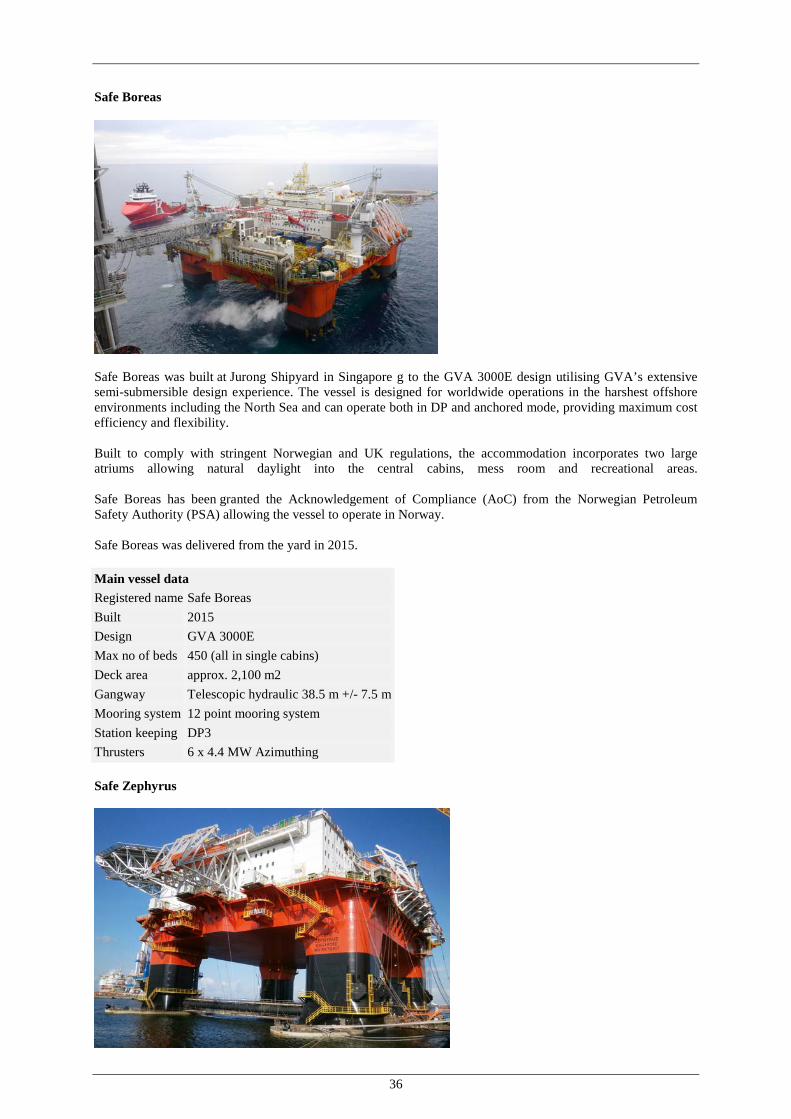

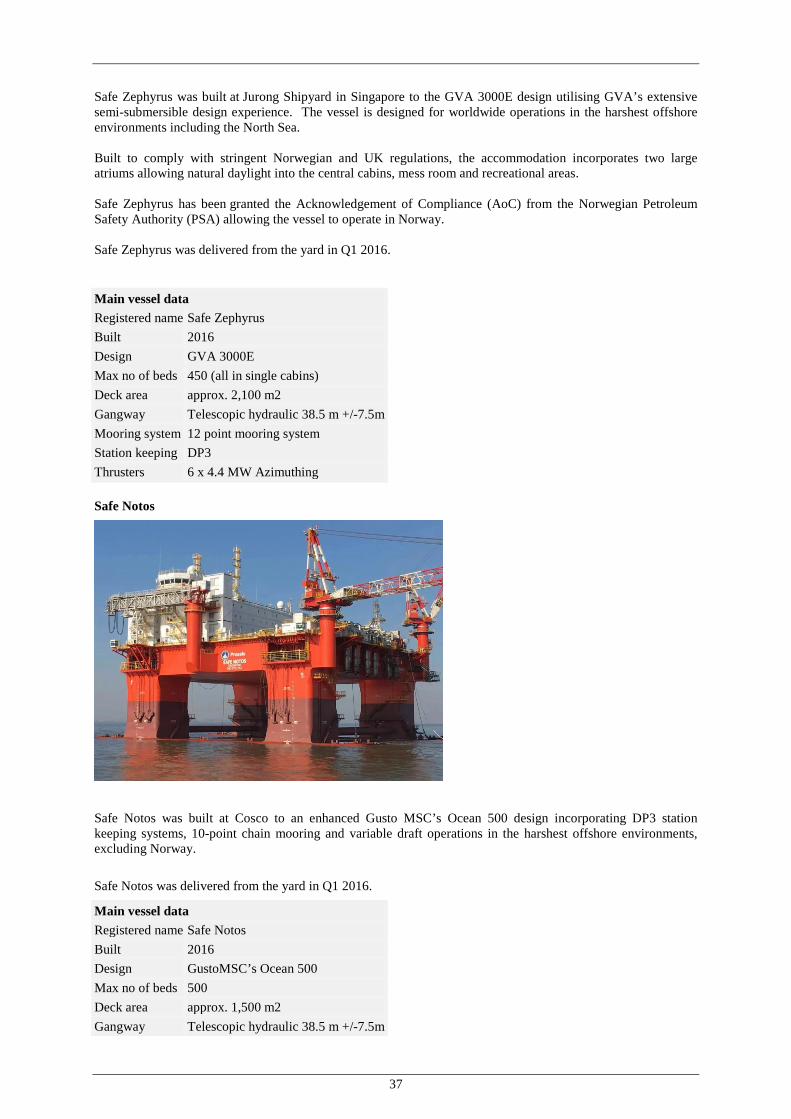

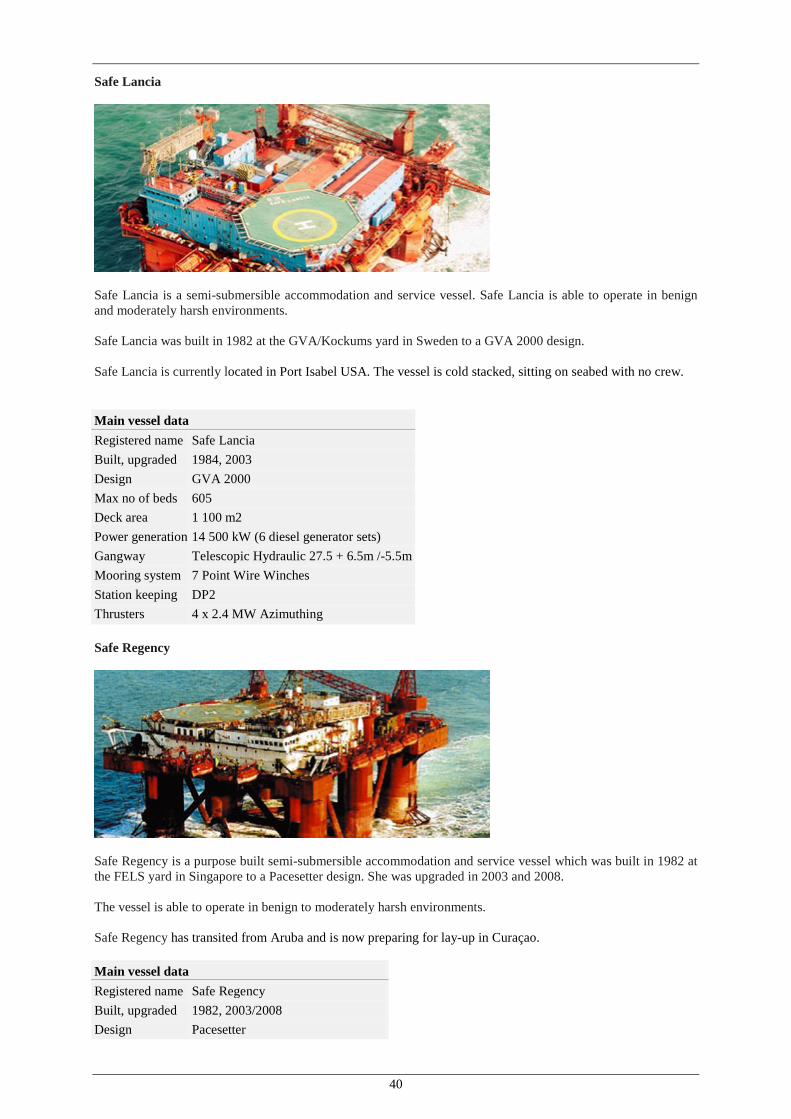

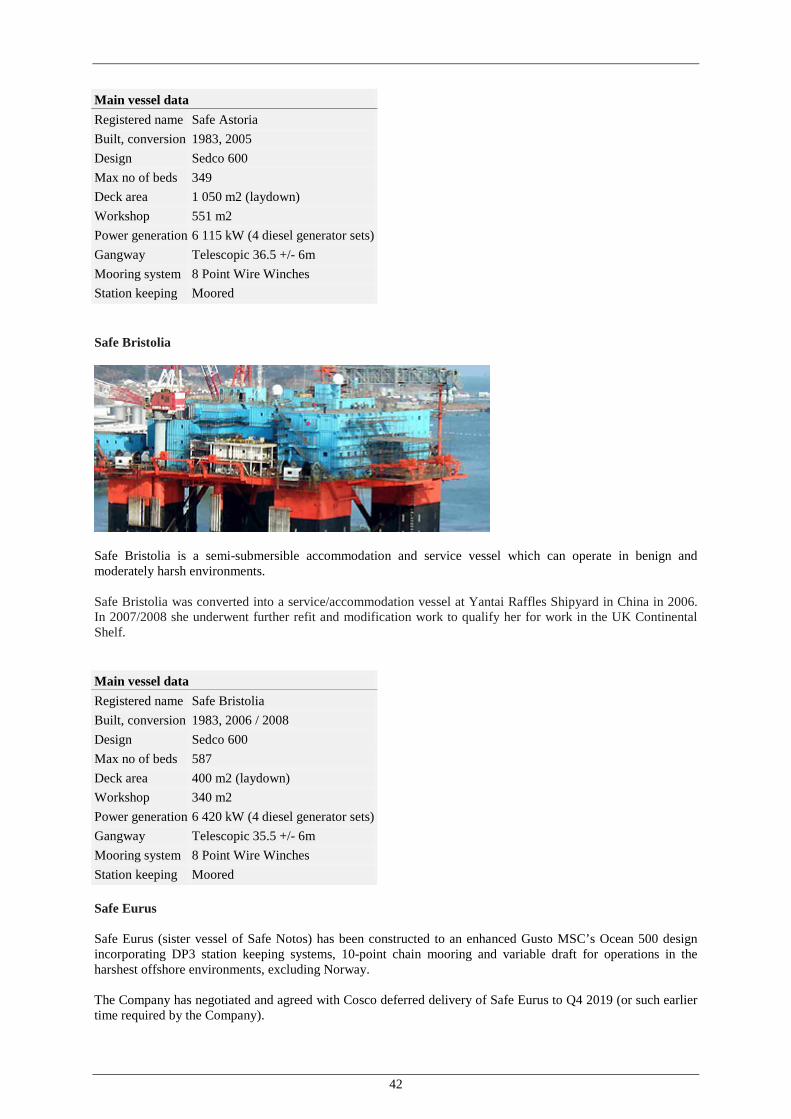

prospectus - seb group · prospectus. prosafe se (a european public limited liability company...

TRANSCRIPT

Prospectus

PROSAFE SE

(a European public limited liability company registered with the Registrar of Companies and Official Receiver

of the Republic of Cyprus, with the registration number SE4)

Subsequent Offering of up to 504,000,000 Offer Shares Subscription Price: NOK 0.25 per Offer Share

Subscription Period: From 17 October 2016 to 31 October 2016 at 16:30 Oslo time Listing of 4,376,600,000 new shares issued in a private placement (the “Private Placement Shares”), offering and listing of up to 504,000,000 shares to be issued in connection with the Subsequent Offering (the "Offer Shares"), listing of 1,400,839,757 new shares issued in connection with a bond conversion ("Bond Conversion Shares"), all with a nominal value of EUR 0.001 per share, and listing of convertible bonds ("New Convertible Bonds").

Prosafe SE (the “Company”, together with its subsidiaries the “Group”) is offering up to 504,000,000 Offer Shares in the Company with a nominal value of EUR 0.001 each at a subscription price of NOK 0.25 per Offer Share (the “Subsequent Offering”). Holders of the Company's shares (the “Shares”) as of 12 July 2016, as registered in the Norwegian Securities Depository (the “VPS”) as of 14 July 2016 who are not resident in a jurisdiction where such offering would be unlawful, or would (in jurisdictions other than Norway) require any prospectus filing, registration or similar action and who did not participate in the Private Placement (the “Eligible Shareholders”) are being granted non-tradable subscription rights (the “Subscription Rights”) that, subject to applicable law, provide preferential rights to subscribe for and be allocated Offer Shares in the Subsequent Offering. Eligible Shareholders will be granted 3.56 Subscription Rights for each Share held. Each Subscription Right will give the right to subscribe for one (1) Offer Share. The subscription period commences on 17 October 2016 and expires on 31 October 2016 at 16:30 CET (the “Subscription Period”). Subscription Rights that are not used to subscribe for Offer Shares before expiry of the Subscription Period will have no value and will lapse without compensation. The Company is not taking any action to permit a public offering of the Subscription Rights or the Offer Shares in any jurisdiction outside Norway. The Offer Shares are being offered only in those jurisdictions in which, and only to those persons to whom, offers of the Offer Shares (pursuant to the exercise of Subscription Rights or otherwise) may lawfully be made. For more information regarding restrictions in relation to the Subsequent Offering pursuant to this Prospectus, please see section 14. Investing in the Company's Shares, including the Offer Shares involves certain risks. See section 2 “Risk Factors”.

Managers

ABG Sundal Collier DNB Markets Nordea Markets Pareto Securities SEB

14 October 2016

IMPORTANT INFORMATION

For the definition of certain capitalised terms used throughout this Prospectus, please see Section 16 “Definitions and Glossary of Terms” which also applies to the front page.

Readers are expressly advised that the Shares are exposed to financial and legal risk and they should therefore read this Prospectus in its entirety, in particular Section 2 “Risk Factors”. The contents of this Prospectus are not to be construed as legal, financial or tax advice. Each reader should consult his, her or its own legal adviser, independent financial adviser or tax adviser for legal, financial or tax advice.

This Prospectus has been prepared by the Company in order to provide a presentation of the Group in connection with the listing of the Private Placement Shares, Bond Conversion Shares and the offer and listing of the Offer Shares , as defined and described herein. This Prospectus has been prepared to comply with the Securities Trading Act sections 7-2 and 7-3 and related legislation and regulations, including the Commission Regulation (EC) No. 809/2004 of 29 April 2004 implementing Directive 2003/71/EC of the European Parliament and of the Council as regards information contained in Prospectuses as well as the format, incorporation by reference and publication of such prospectuses and dissemination of advertisements. This Prospectus has been prepared solely in the English language.

The information contained herein is as of the date of this Prospectus and subject to change, completion and amendment without notice. In accordance with section 7-15 of the Securities Trading Act, any new circumstance, material error or inaccuracy relating to information included in this Prospectus, which may have significance for the assessment of the Private Placement Shares, Offer Shares, Bond Conversion Shares respectively, and arises between the date of this Prospectus and before the such Shares are listed on Oslo Børs, will be presented in a supplement to this Prospectus. Publication of this Prospectus shall not create any implication that there has been no change in the Company’s affairs or that the information herein is correct as of any date subsequent to the date of this Prospectus.

All inquiries relating to this Prospectus must be directed to the Company. No other person is authorised to give information or to make any representation in connection with the listing of the Private Placement Shares, Bond Conversion Shares or the offer and listing of the Offer Shares. If any such information is given or made, it must not be relied upon as having been authorised by the Company or by any of the employees, affiliates or advisers of any of the foregoing.

No action has been or will be taken in any jurisdiction other than Norway by the Company that would permit the possession or distribution of this Prospectus, any documents relating thereto, or any amendment or supplement thereto, in any country or jurisdiction where this is unlawful or specific action for such purpose is required. The distribution of this Prospectus in certain jurisdictions may be restricted by law. Persons into whose possession this Prospectus may come are required by the Company to inform themselves about and to observe such restrictions. The Company shall not be responsible or liable for any violation of such restrictions by prospective investors. The restrictions and limitations listed and described herein are not exhaustive, and other restrictions and limitations in relation to this Prospectus that are not known or identified at the date of this Prospectus may apply in various jurisdictions. This Prospectus serves as a listing prospectus as required by applicable laws and regulations only. This Prospectus does not constitute an offer to buy, subscribe or sell any of the securities described herein, and no securities are being offered or sold pursuant to it.

The securities described herein have not been and will not be registered under the US Securities Act of 1933 as amended (the “US Securities Act”), or with any securities authority of any state of the United States. Accordingly, the securities described herein may not be offered, pledged, sold, resold, granted, delivered, allotted, taken up, or otherwise transferred, as applicable, in the United States, except in transactions that are exempt from, or in transactions not subject to, registration under the US Securities Act and in compliance with any applicable state securities laws.

This Prospectus is subject to Norwegian law, unless otherwise indicated herein. Any dispute arising in respect of this Prospectus is subject to the exclusive jurisdiction of the Norwegian courts with Oslo District Court as legal venue in the first instance.

3

TABLE OF CONTENTS

1. EXECUTIVE SUMMARY ..................................................................................................................................................................... 5

2. RISK FACTORS .................................................................................................................................................................................. 14

2.1 STRATEGIC RISK .................................................................................................................................................................... 14 2.2 NON-STRATEGIC RISK ........................................................................................................................................................... 14 2.3 RISKS RELATED TO THE SHARES AND THE NEW CONVERTIBLE BONDS ................................................................. 16

3. STATEMENTS..................................................................................................................................................................................... 18

3.1 RESPONSIBILITY FOR THE PROSPECTUS .......................................................................................................................... 18 3.2 INFORMATION SOURCED FROM THIRD PARTIES ........................................................................................................... 19 3.3 NOTICE REGARDING FORWARD-LOOKING STATEMENTS ........................................................................................... 19

4. THE REFINANCING ........................................................................................................................................................................... 20

4.1 BACKGROUND ........................................................................................................................................................................ 20 4.2 THE MAIN TERMS OF THE REFINANCING ......................................................................................................................... 20 4.2.3.1. MAIN TERMS OF THE NEW CONVERTIBLE BONDS ........................................................................................................ 21 4.3 CONDITIONS FOR COMPLETION OF THE REFINANCING AND RESOLUTIONS .......................................................... 23 4.4 ADVISORS ................................................................................................................................................................................ 24

5. THE SUBSEQUENT OFFERING ........................................................................................................................................................ 26

5.1 GENERAL .................................................................................................................................................................................. 26 5.2 RESOLUTION REGARDING THE SUBSEQUENT OFFERING ............................................................................................ 26 5.3 ELIGIBLE SHAREHOLDERS AND RECORD DATE............................................................................................................. 26 5.4 OFFER SHARES AND SUBSCRIPTION RIGHTS .................................................................................................................. 26 5.5 SUBSCRIPTION PERIOD ......................................................................................................................................................... 27 5.6 SUBSCRIPTION PRICE ............................................................................................................................................................ 27 5.7 SUBSCRIPTION PROCEDURES AND SUBSCRIPTION OFFICE ......................................................................................... 27 5.8 FINANCIAL INTERMEDIARIES ............................................................................................................................................. 28 5.9 ALLOCATION ........................................................................................................................................................................... 29 5.10 PAYMENT FOR THE OFFER SHARES................................................................................................................................... 29 5.11 PUBLICATION OF INFORMATION RELATING TO THE SUBSEQUENT OFFERING ..................................................... 30 5.12 VPS REGISTRATION ............................................................................................................................................................... 30 5.13 DELIVERY AND LISTING OF THE OFFER SHARES ........................................................................................................... 30 5.14 SHARE CAPITAL FOLLOWING THE SUBSEQUENT OFFERING ...................................................................................... 30 5.15 TRANSFERABILITY OF THE OFFER SHARES .................................................................................................................... 30 5.16 EXPENSES AND NET PROCEEDS ......................................................................................................................................... 30 5.17 DILUTION ................................................................................................................................................................................. 31 5.18 SHAREHOLDERS’ RIGHTS RELATING TO THE OFFER SHARES .................................................................................... 31 5.19 INTEREST OF NATURAL AND LEGAL PERSONS .............................................................................................................. 31 5.20 MANAGERS AND ADVISOR .................................................................................................................................................. 31

6. PRESENTATION OF THE COMPANY AND ITS BUSINESS .......................................................................................................... 32

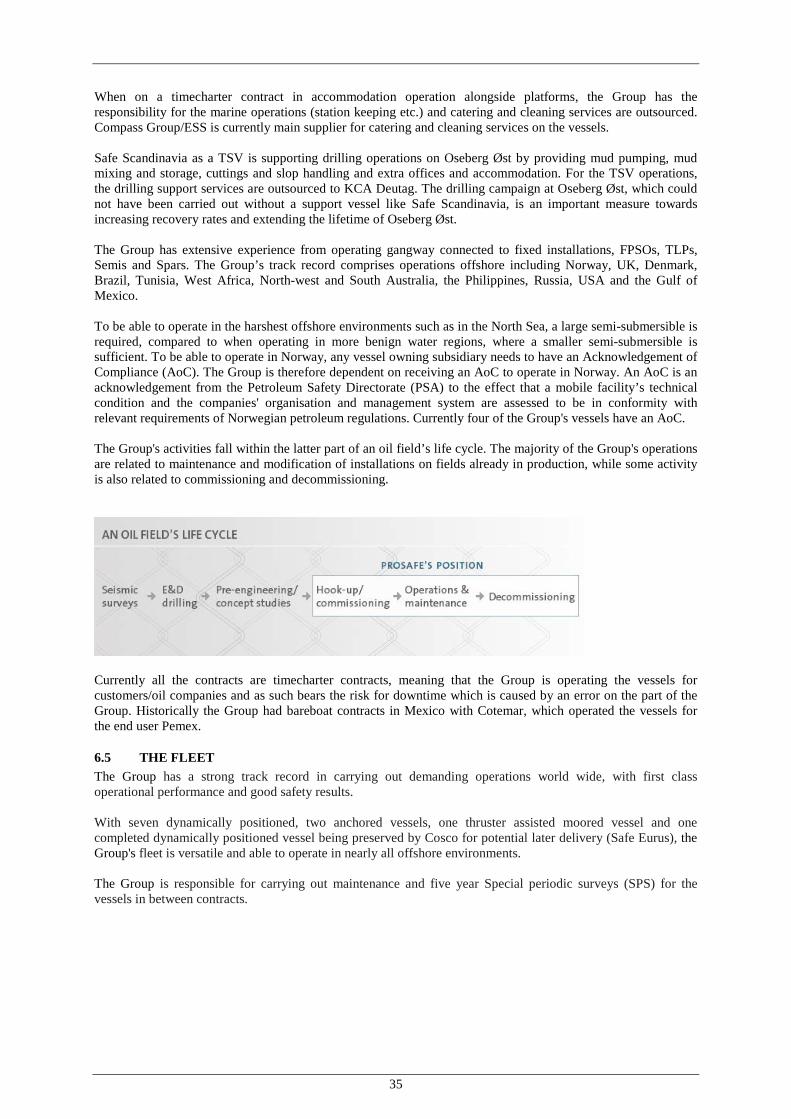

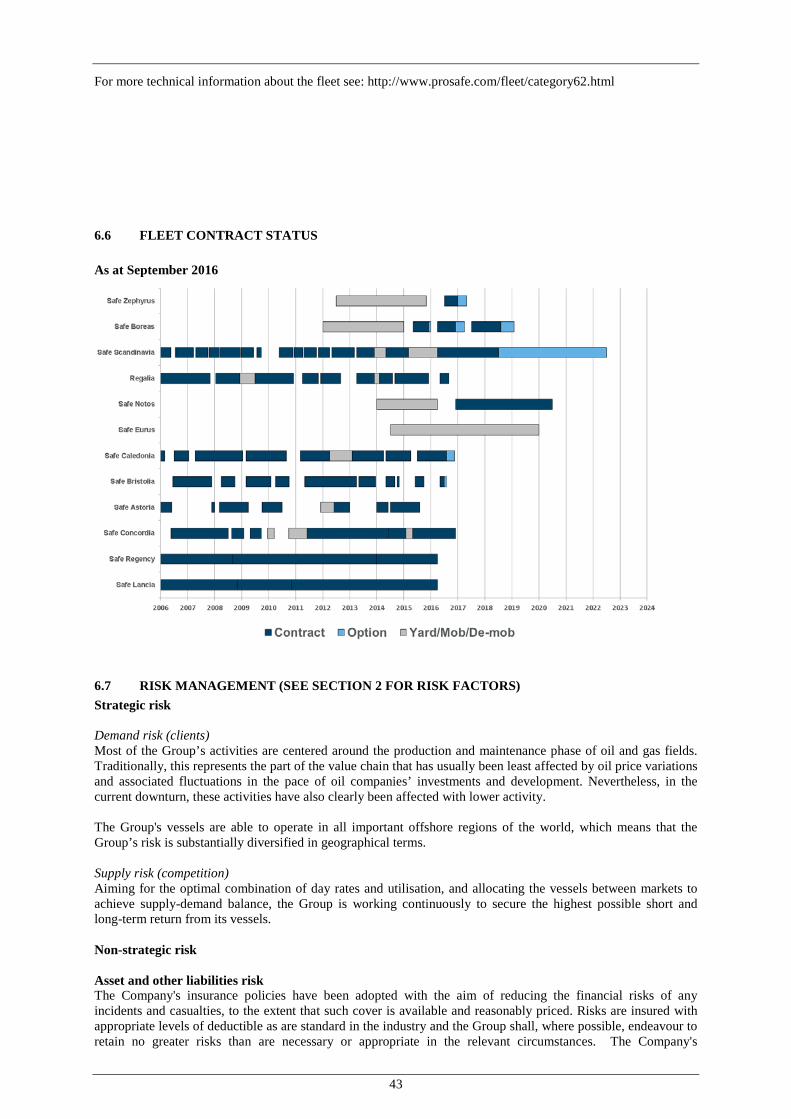

6.1 CORPORATE INFORMATION ................................................................................................................................................ 32 6.2 DESCRIPTION OF THE GROUP.............................................................................................................................................. 32 6.3 INTRODUCTION AND HISTORY ........................................................................................................................................... 33 6.4 PRINCIPAL ACTIVITIES ......................................................................................................................................................... 34 6.5 THE FLEET................................................................................................................................................................................ 35 6.6 FLEET CONTRACT STATUS .................................................................................................................................................. 43 6.7 RISK MANAGEMENT (SEE SECTION 2 FOR RISK FACTORS) ......................................................................................... 43 6.8 TREND INFORMATION .......................................................................................................................................................... 46 OUTLOOK ................................................................................................................................................................................................ 46 6.9 EMPLOYEES ............................................................................................................................................................................. 47

7. MARKET OVERVIEW........................................................................................................................................................................ 47

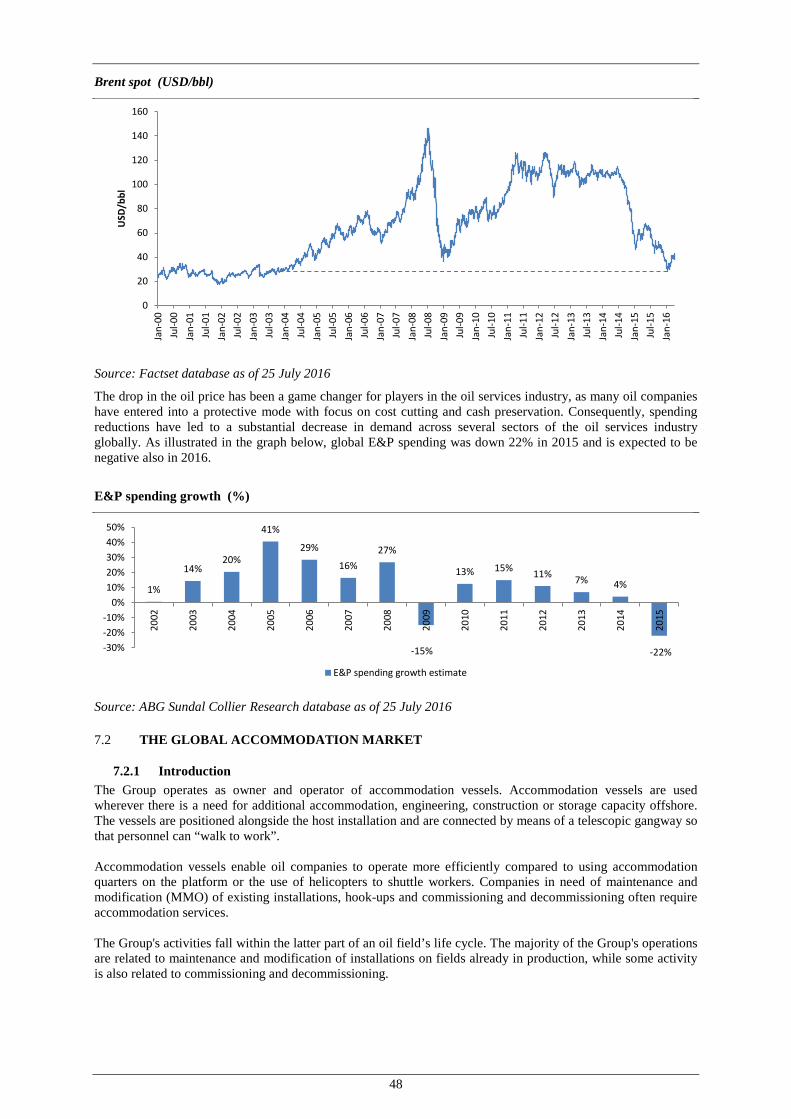

7.1 INTRODUCTION ...................................................................................................................................................................... 47 7.2 THE GLOBAL ACCOMMODATION MARKET ..................................................................................................................... 48

8. ORGANISATION, BOARD OF DIRECTORS AND MANAGEMENT ............................................................................................. 54

8.1 EXECUTIVE MANAGEMENT ................................................................................................................................................. 54 8.2 BOARD OF DIRECTORS ......................................................................................................................................................... 56

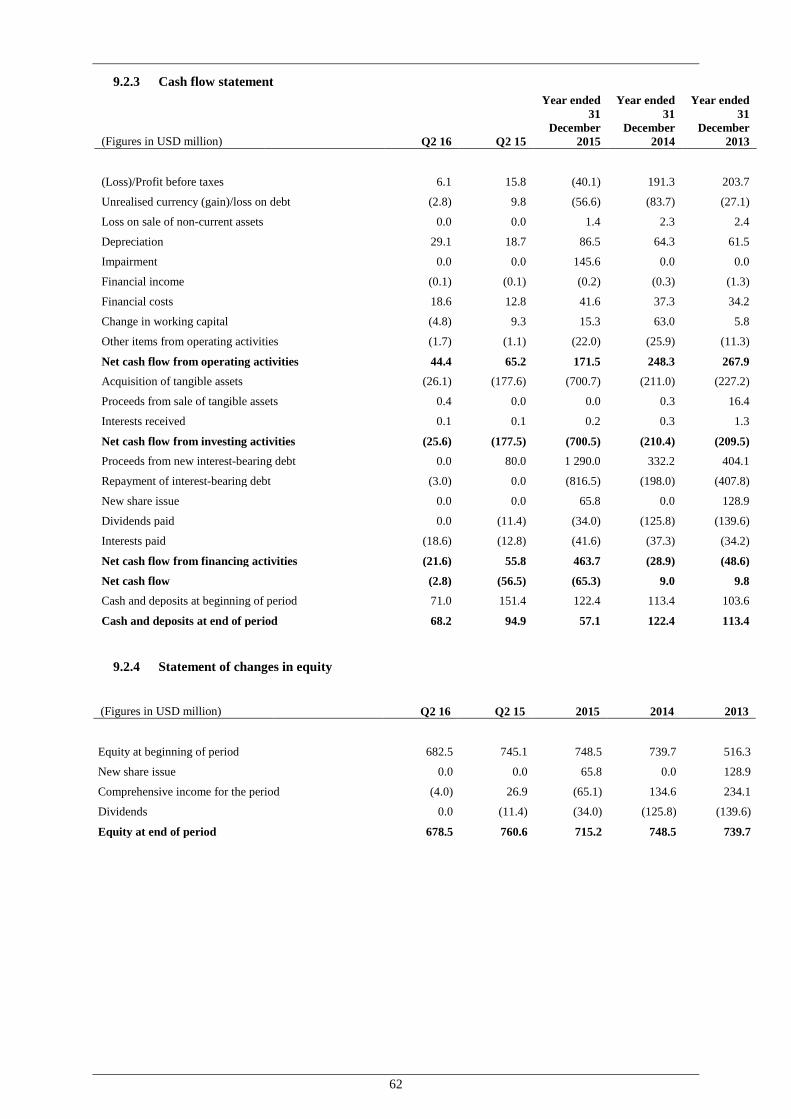

9. FINANCIAL INFORMATION ............................................................................................................................................................ 60

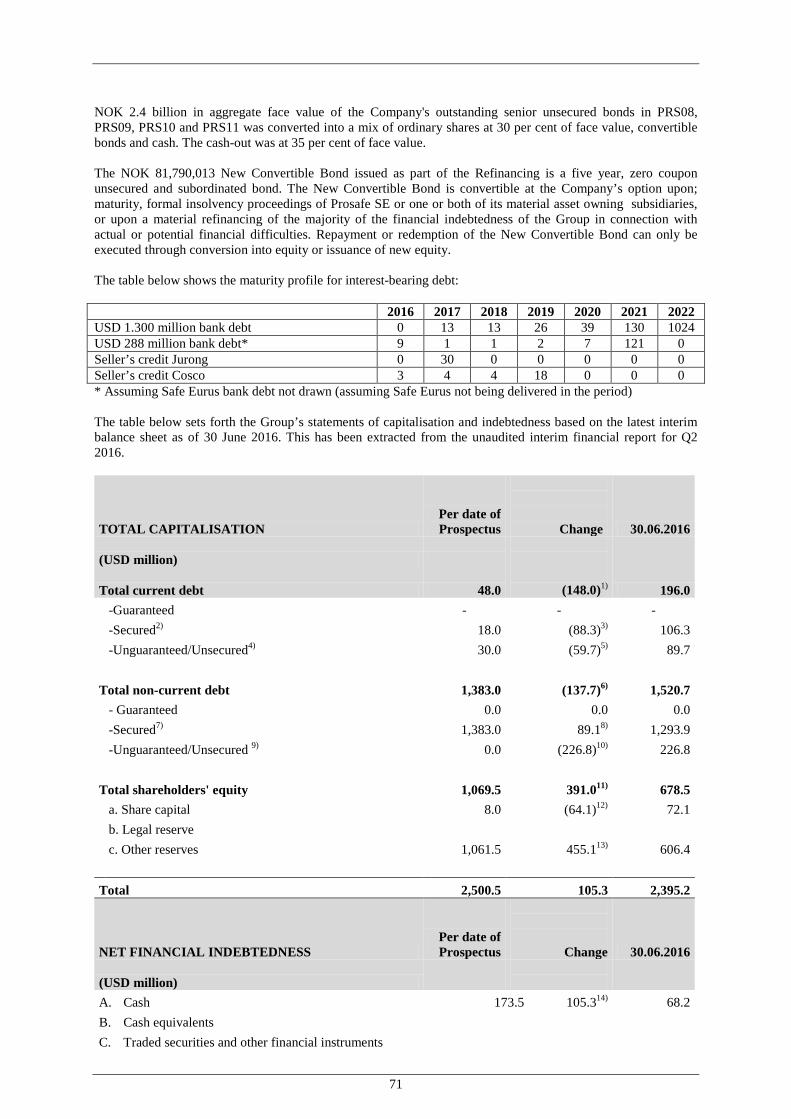

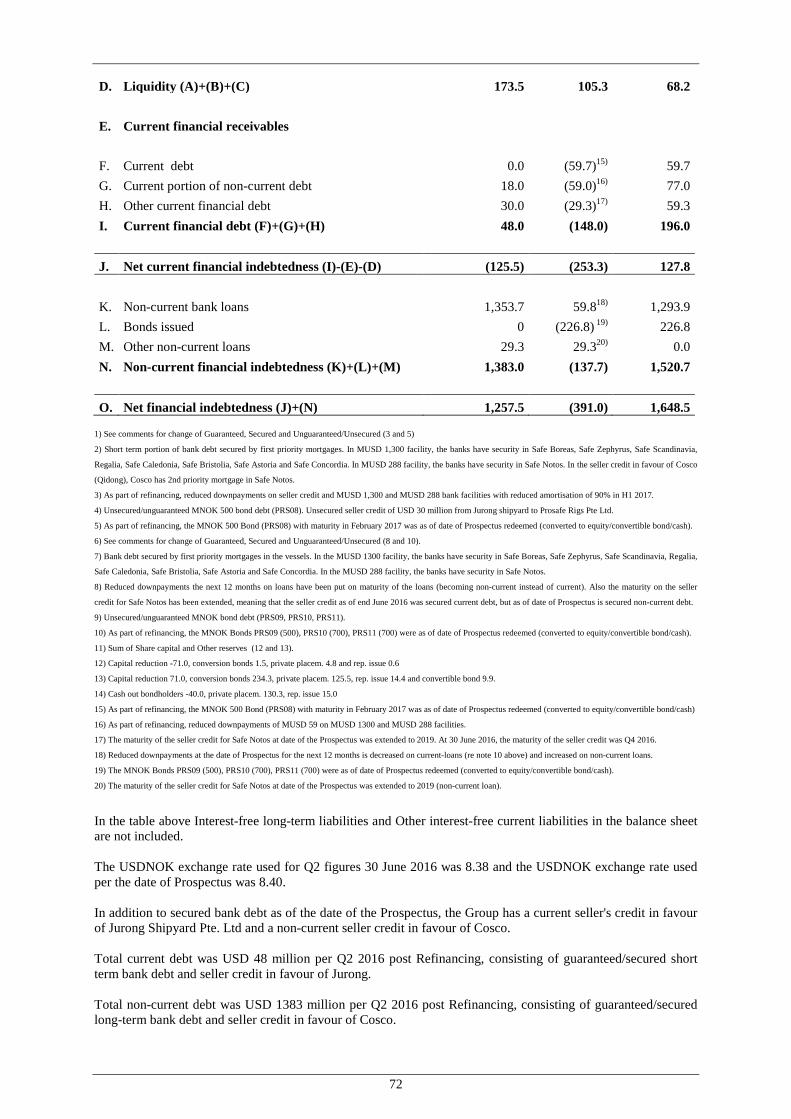

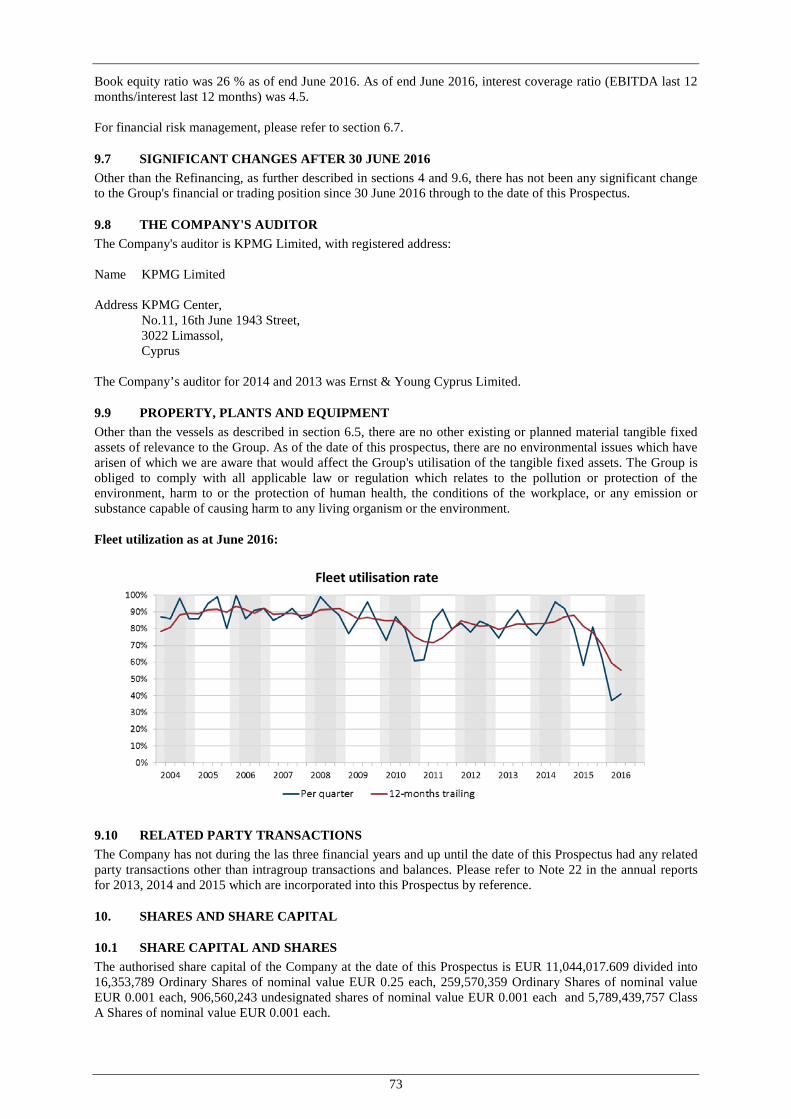

9.1 ACCOUNTING PRINCIPLES ................................................................................................................................................... 60 9.2 HISTORICAL FINANCIAL ACCOUNTS ................................................................................................................................ 60 9.3 OPERATING AND FINANCIAL REVIEW .............................................................................................................................. 63 9.4 INVESTMENTS ......................................................................................................................................................................... 68 9.5 WORKING CAPITAL ............................................................................................................................................................... 69 9.6 CAPITALISATION AND INDEBTEDNESS ............................................................................................................................ 69 9.7 SIGNIFICANT CHANGES AFTER 30 JUNE 2016 .................................................................................................................. 73 9.8 THE COMPANY'S AUDITOR .................................................................................................................................................. 73 9.9 PROPERTY, PLANTS AND EQUIPMENT .............................................................................................................................. 73 9.10 RELATED PARTY TRANSACTIONS ..................................................................................................................................... 73

10. SHARES AND SHARE CAPITAL ...................................................................................................................................................... 73

4

10.1 SHARE CAPITAL AND SHARES ............................................................................................................................................ 73 10.2 HISTORICAL DEVELOPMENT IN SHARE CAPITAL AND NUMBER OF SHARES ......................................................... 74 10.3 BOARD AUTHORISATION TO ISSUE SHARES ................................................................................................................... 74 10.4 BOARD AUTHORISATION TO REPURCHASE SHARES .................................................................................................... 74 10.5 OPTIONS AND WARRANTS ................................................................................................................................................... 74 10.6 OWN SHARES .......................................................................................................................................................................... 74 10.7 OWNERSHIP STRUCTURE ..................................................................................................................................................... 74 10.8 LISTING, SHARE REGISTRAR AND SECURITIES NUMBER ............................................................................................. 75 10.9 DIVIDEND ................................................................................................................................................................................. 75 10.10 SHAREHOLDER AGREEMENTS ............................................................................................................................................ 75

11. SHAREHOLDER MATTERS AND COMPANY AND SECURITIES LAW ..................................................................................... 75

11.1 SHAREHOLDERS RIGHTS ...................................................................................................................................................... 75 11.2 ADDITIONAL RIGHTS OF SHAREHOLDERS ...................................................................................................................... 76 11.3 LIMITATIONS ON THE RIGHT TO OWN AND TRANSFER SHARES ............................................................................... 77 11.4 GENERAL MEETINGS ............................................................................................................................................................. 77 11.5 ALTERATION OF CAPITAL.................................................................................................................................................... 77 11.6 PURCHASE OF OWN SHARES AND REDEMPTION ........................................................................................................... 78 11.7 VOTING RIGHTS ...................................................................................................................................................................... 78 11.8 PRE-EMPTION RIGHTS ........................................................................................................................................................... 79 11.9 REGULATION OF DIVIDENDS .............................................................................................................................................. 79 11.10 LIABILITY OF DIRECTORS .................................................................................................................................................... 80 11.11 DISTRIBUTION OF ASSETS ON LIQUIDATION .................................................................................................................. 80 11.12 SUMMARY OF CERTAIN PROVISIONS OF THE COMPANY’S CONSTITUTIONAL DOCUMENTS............................. 80 11.13 CYPRUS LAW DISCLOSURE OBLIGATIONS ...................................................................................................................... 81 11.14 APPLICABLE TAKEOVER BID REGULATIONS .................................................................................................................. 81 11.15 APPLICABLE SQUEEZE OUT AND SELL OUT REGULATIONS ....................................................................................... 82

12. TAXATION .......................................................................................................................................................................................... 84

12.1 CYPRUS TAXATION ............................................................................................................................................................... 84 12.2 NORWEGIAN TAXATION; OVERVIEW ............................................................................................................................... 90

13. LEGAL MATTERS .............................................................................................................................................................................. 92

13.1 DISPUTES – ACTUAL AND POTENTIAL DISPUTES .......................................................................................................... 92 14. SELLING AND TRANSFER RESTRICTIONS .................................................................................................................................. 93

14.1 GENERAL .................................................................................................................................................................................. 93 14.2 UNITED STATES ...................................................................................................................................................................... 94 14.3 EEA SELLING RESTRICTIONS .............................................................................................................................................. 95 14.4 NOTICE TO AUSTRALIAN ELIGIBLE SHAREHOLDERS ................................................................................................... 96 14.5 NOTICE TO CANADIAN ELIGIBLE SHAREHOLDERS ....................................................................................................... 96 14.6 NOTICE TO HONG KONG ELIGIBLE SHAREHOLDERS .................................................................................................... 96 14.7 NOTICE TO JAPANESE ELIGIBLE SHAREHOLDERS ......................................................................................................... 97 14.8 NOTICE TO SWISS ELIGIBLE SHAREHOLDERS ................................................................................................................ 97

15. ADDITIONAL INFORMATION ......................................................................................................................................................... 97

15.1 DOCUMENTS ON DISPLAY ................................................................................................................................................... 97 15.2 INCORPORATION BY REFERENCE ...................................................................................................................................... 97

16. DEFINITIONS AND GLOSSARY OF TERMS .................................................................................................................................. 99

APPENDIX 1 – SUBSCRIPTION FORM APPENDIX 2 – BOND AGREEMENT

5

1. EXECUTIVE SUMMARY

Summaries are made up of disclosure requirements known as “Elements”. These Elements are numbered in Sections A– E (A.1 – E.7) below. This summary contains all the Elements required to be included in a summary for this type of securities and the Company. Because some Elements are not required to be addressed, there may be gaps in the numbering sequence of the Elements. Even though an Element may be required to be inserted in the summary because of the type of securities and Company, it is possible that no relevant information can be given regarding the Element. In this case a short description of the Element is included in the summary with the mention of “not applicable”. Section A – Introduction and Warnings A.1 Warning This summary should be read as introduction to this Prospectus;

any decision to invest in the securities should be based on consideration of this Prospectus as a whole by the investor;

where a claim relating to the information contained in this Prospectus is brought before a court, the plaintiff investor might, under the national legislation of the Member States, have to bear the costs of translating this Prospectus before the legal proceedings are initiated; and civil liability attaches only to those persons who have tabled the summary including any translation thereof, but only if the summary is misleading, inaccurate or inconsistent when read together with the other parts of the Prospectus or it does not provide, when read together with the other parts of the Prospectus, key information in order to aid investors when considering whether to invest in such securities.

A.2 Consent to use of prospectus by financial intermediaries

Not applicable. The Prospectus will not be used for subsequent resale or final placement by financial intermediaries.

Section B - Company B.1 Legal and

commercial name The legal and commercial name of the Company is Prosafe SE

B.2 Domicile and legal form, legislation and country of incorporation

The Company is a European public limited liability company registered with the Registrar of Companies and Official Receiver of the Republic of Cyprus, with the registration number SE4.

B.3 Nature of current operations, principal activities /products and markets

The Group owns 10 semi-submersible accommodation vessels, one Tender support vessel (TSV) and has one semi-submersible accommodation vessel under construction. Safe Britannia, Jasminia and Safe Hibernia have recently been sold for scrap/recycling in the US. As of September 2016, five vessels are in operation, five vessels are off-hire and/or stacked, one vessel (Safe Notos) is in transit to Brazil and one vessel is at the yard (Safe Eurus). Accommodation vessels are used when there is a need for additional accommodation, engineering, construction or storage capacity offshore. Typically, these vessels will be utilised in connection with installation and commissioning of new facilities, upgrades, modifications and maintenance of existing installations, hook-ups of satellite fields to existing infrastructure, and decommissioning and removal of installations. Safe Scandinavia as a TSV is supporting drilling operations on Oseberg Øst by providing mud pumping, mud mixing and storage, cuttings and slop handling and extra offices and accommodation. The drilling campaign at Oseberg Øst, which could not have been carried out without a support vessel like Safe Scandinavia, is an important measure towards increasing recovery rates and extending the lifetime of Oseberg Øst. The Group's vessels have accommodation capacity (i.e. max number of beds) for 306-780 people depending on the type of vessel and offer high quality welfare and catering facilities, storage, workshops, offices, medical services,

6

deck cranes and lifesaving and fire fighting equipment. The vessels are positioned alongside the host installation and are connected by means of a telescopic gangway so that personnel can walk to work. The Group has extensive experience from operating gangway connected to fixed installations, FPSOs, TLPs, Semis and Spars. The Group’s track record comprises operations offshore including Norway, UK, Denmark, Brazil, Tunisia, West Africa, North-west and South Australia, the Philippines, Russia, USA and the Gulf of Mexico. The Group's activities fall within the latter part of an oil field’s life cycle. The majority of the Group's operations are related to maintenance and modification of installations on fields already in production, while some activity is also related to commissioning and decommissioning.

B.4a Recent trends The accommodation support segment is late cyclical by nature. Historically, more than three quarters of the work has been related to producing fields, whereas the remainder has been related to hook-up and commissioning of new fields. Accommodation support vessels are also used during decommissioning of offshore installations. The supply side is seeing significant growth in size during the period from 2012 to 2016 with the entry into the market of a number of new semi-submersible accommodation support vessels. However the growth is expected to be lower than earlier anticipated as a result of the extended down-cycle which may lead to both scrapping and delays or even cancellations of new builds. 2015 saw a continued slow-down in contracting activity and the gross value of charter contracts, including clients’ extension options, was reduced by approximately 13 % to USD 1,595 million (USD 1,843 million). The industry has seen deferral of several projects, as well as focus on cash preservation by way of contract renegotiations and contract cancellations. As all providers of oil services are dependent on oil companies’ cash flow, reductions of spending plans have led to a substantial decrease in demand for oilfield services, including accommodation support vessels. This has increasingly been evident in all geographical markets. Despite the current down-turn and the supply side growth, the longer term prospects are promising as it is expected that field life extensions continue through enhanced oil recovery efforts. Further, in the years ahead new fields will come on stream in parallel with decommissioning of old platforms gradually becoming an interesting source of demand. In Mexico, the Group's ultimate client Pemex has been cutting spending in order to adjust its budget to an oil price of USD 25 per barrel. This development has considerably affected the Group's operations in this region. Contracts for vessels operating in Mexico were either not being renewed or were cancelled or suspended, which means that currently the Group does not have any vessels operating in Mexico. Future demand might result from new fields being developed in deeper waters offshore Mexico longer-term or from maintenance and construction medium-term. The near and medium term outlook is also uncertain in Brazil. Even though accommodation support vessels are mostly used for safety and maintenance purposes on fields that are already producing, the financial situation of Petrobras has inevitably resulted in reduced activity and as a result cancellation

7

or renegotiation by Petrobras of contracts to preserve liquidity. The longer term outlook is, however, expected to present further opportunities. The general down turn in the market combined with in particular the non-extension of contracts in Mexico has led to reduced fleet utilisation and consequently reduced charter revenues for the Group. Total order backlog as of 31 December 2015 amounted to USD 997 million of which USD 598 million related to firm contracts and USD 399 million related to options. As of end 2015, secured utilisation for 2016 was 37%. For 2017 and 2018, secured utilisation was 19% and 16%, respectively. Market outlook remains uncertain in the near term, and although there are a number of prospects, 2017 is expected to be the low point in activity level. In general, the company sees the demand returning more to the traditional demand related to maintenance and modification projects with shorter lead times compared to hook-up projects. In 2016-17, approximately 40% of the market was related to maintenance and modifications and about 60% related to hook-up and commissioning work. The Company expects a slowdown of work relating to hook-ups in 2018-2020 as a result of few decisions being made in respect of development of new fields in 2015-2017. However the Company expects to see an improvement from 2021, as more plans for development and operation (PDO) are expected going forward. In general, in the coming years the Company anticipates the demand split reverting to that prior to 2015, when maintenance and modification work accounted generally to approximately 75% of the market and hook-up and commissioning work was approximately 25% of the market. Cost reductions in the E&P sector are expected to contribute to more projects becoming economically viable. Combined with continued focus on asset integrity and maintenance on offshore installations, the Company expects a market recovery from 2018 onwards. The Group has scrapped three vessels and it is likely that other suppliers’ vessels will be scrapped and/or exit the high-end market of the North Sea. As a consequence of this, the supply-demand environment is expected to become more balanced by 2020. With a high quality and versatile fleet and an unmatched operational track record in respect of accommodation operations worldwide, the Group should be well placed in this competitive landscape.

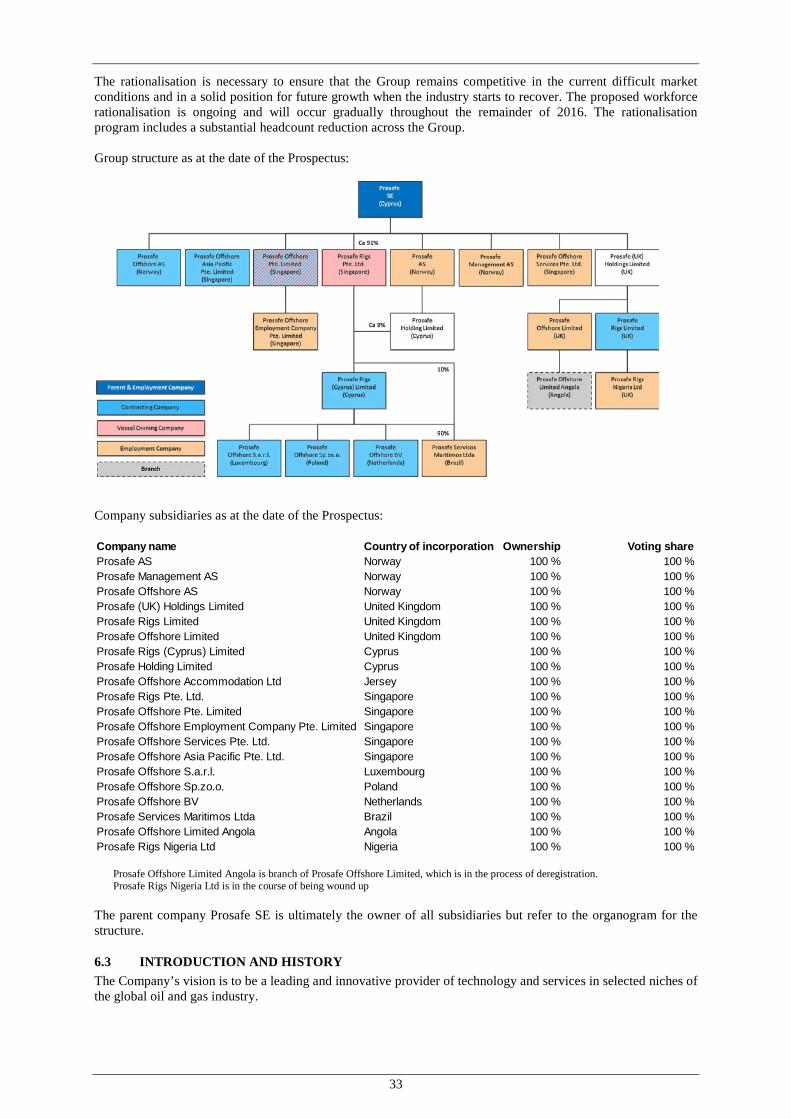

B.5 The Group The Company is the parent company of the Group and directly or indirectly owns 100 % of the shares in its subsidiaries, which own and operate the vessels. The parent company provides certain Group functions such as legal, insurance, accounting and internal audit.

B.6 Interests in the Company's capital and/or voting rights

As of the date of this Prospectus, as follows from the Company's shareholder register in the VPS, the following shareholders hold a notifiable ownership interest (i.e. over 5%) as of the date of the Prospectus:

Name of shareholder

Ordinary Shares

Class A Shares No. of Shares %

NORTH SEA STRATEGIC INVESTMENTS

47,940,903 1,500,000,000 1,547,940,903 25.6%

STATE STREET BANK AND TRUST

47,069,070 1,213,200,000 1,260,269,070 20.9%

* Ownership percentage of total Shares (i.e. both Class A Shares and Ordinary Shares)

Furthermore, pursuant to disclosures of large shareholdings to the market, the Company is aware that funds managed by Pareto Asset Management AS and

8

DNB Asset Management AS holds in aggregate 5.142% and 5.27% of the total Shares in the Company.

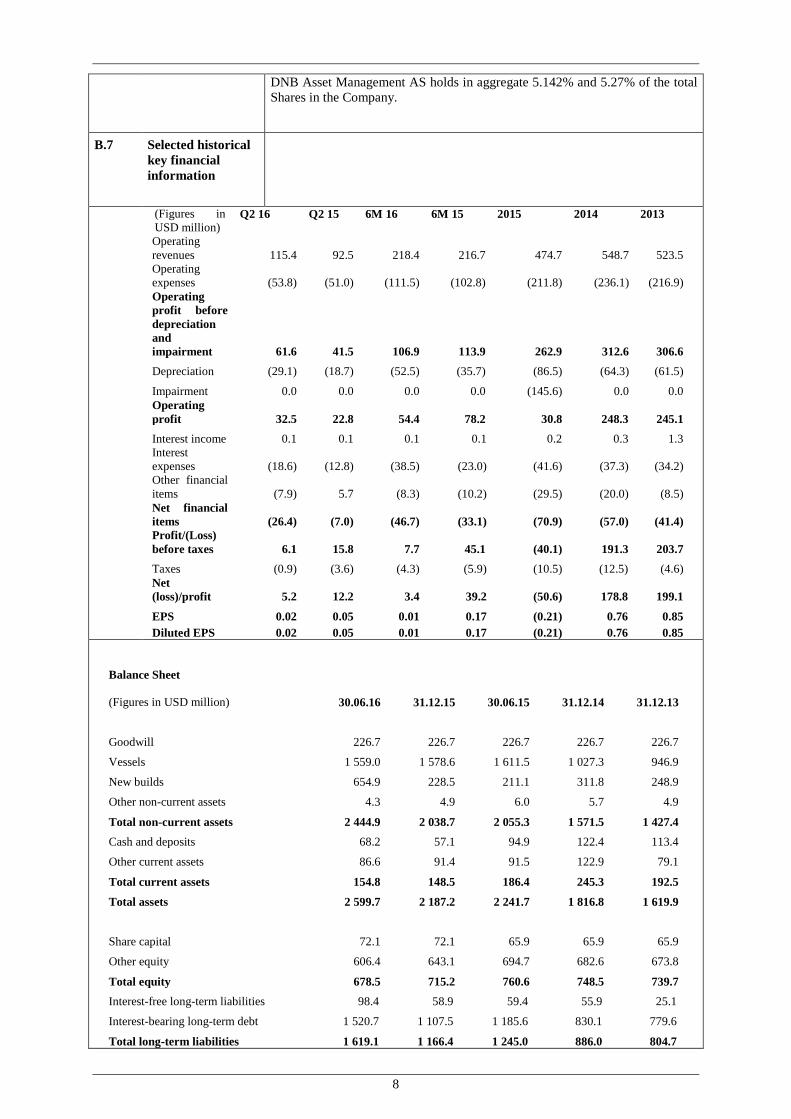

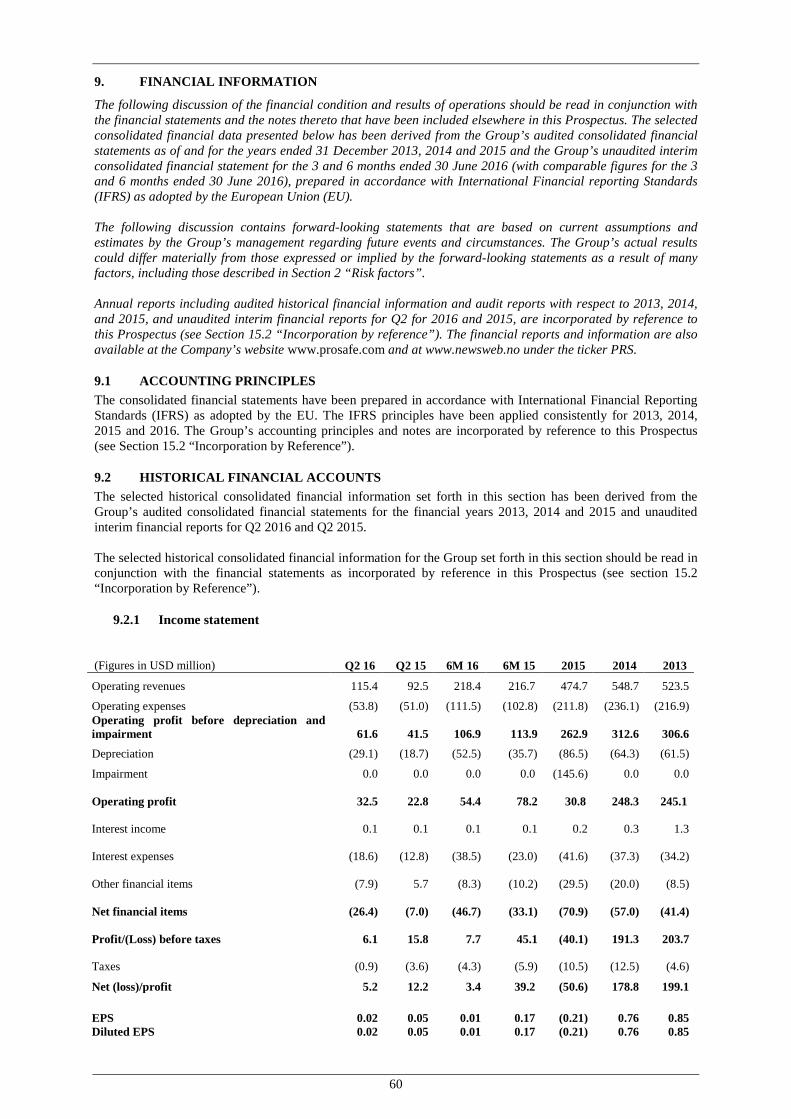

B.7 Selected historical key financial information

(Figures in USD million)

Q2 16 Q2 15 6M 16 6M 15 2015 2014 2013

Operating revenues 115.4 92.5 218.4

216.7 474.7 548.7 523.5

Operating expenses (53.8) (51.0) (111.5)

(102.8) (211.8) (236.1) (216.9)

Operating profit before depreciation and impairment 61.6 41.5 106.9 113.9 262.9 312.6 306.6 Depreciation (29.1) (18.7) (52.5) (35.7) (86.5) (64.3) (61.5) Impairment 0.0 0.0 0.0 0.0 (145.6) 0.0 0.0 Operating profit

32.5 22.8 54.4 78.2 30.8 248.3 245.1

Interest income 0.1 0.1 0.1 0.1 0.2 0.3 1.3 Interest expenses (18.6) (12.8) (38.5) (23.0) (41.6) (37.3) (34.2) Other financial items (7.9) 5.7 (8.3) (10.2) (29.5) (20.0) (8.5) Net financial items (26.4) (7.0) (46.7)

(33.1) (70.9) (57.0) (41.4)

Profit/(Loss) before taxes 6.1 15.8 7.7

45.1

(40.1) 191.3 203.7

Taxes (0.9) (3.6) (4.3) (5.9) (10.5) (12.5) (4.6) Net (loss)/profit 5.2 12.2 3.4

39.2 (50.6) 178.8 199.1

EPS 0.02 0.05 0.01 0.17 (0.21) 0.76 0.85 Diluted EPS 0.02 0.05 0.01 0.17 (0.21) 0.76 0.85

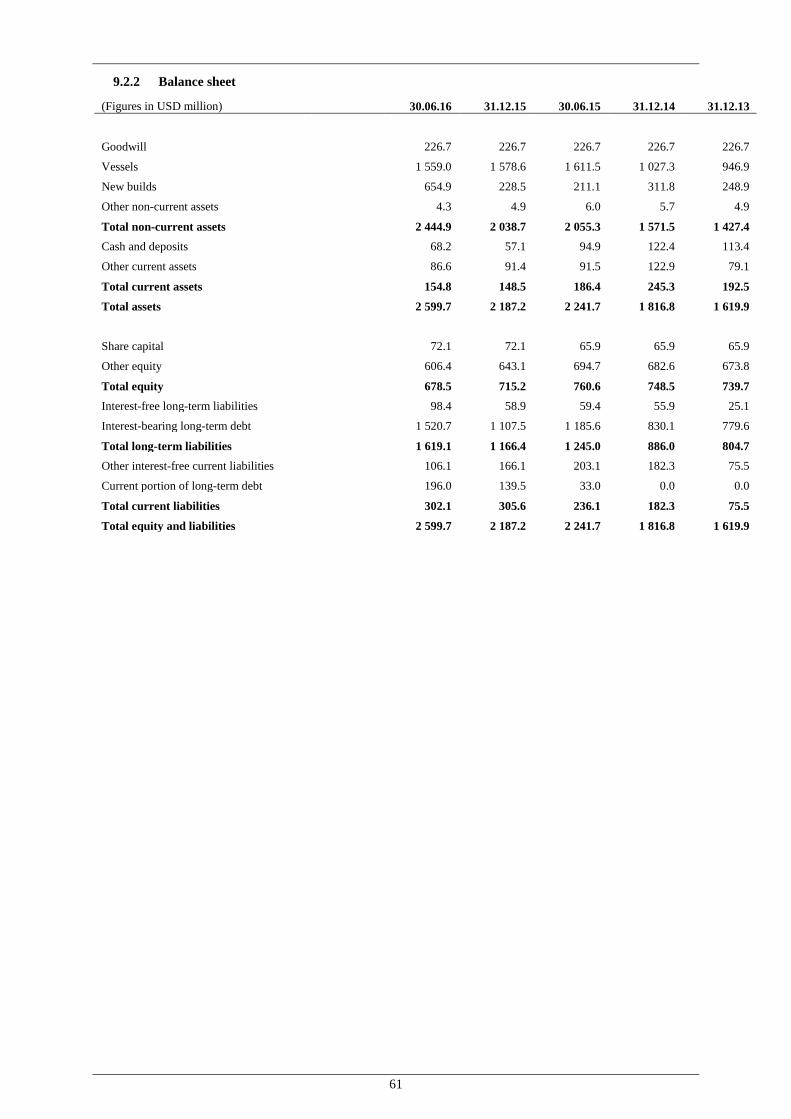

Balance Sheet (Figures in USD million) 30.06.16 31.12.15 30.06.15 31.12.14 31.12.13

Goodwill 226.7 226.7 226.7 226.7 226.7

Vessels 1 559.0 1 578.6 1 611.5 1 027.3 946.9

New builds 654.9 228.5 211.1 311.8 248.9

Other non-current assets 4.3 4.9 6.0 5.7 4.9

Total non-current assets 2 444.9 2 038.7 2 055.3 1 571.5 1 427.4 Cash and deposits 68.2 57.1 94.9 122.4 113.4

Other current assets 86.6 91.4 91.5 122.9 79.1

Total current assets 154.8 148.5 186.4 245.3 192.5

Total assets 2 599.7 2 187.2 2 241.7 1 816.8 1 619.9

Share capital 72.1 72.1 65.9 65.9 65.9

Other equity 606.4 643.1 694.7 682.6 673.8

Total equity 678.5 715.2 760.6 748.5 739.7 Interest-free long-term liabilities 98.4 58.9 59.4 55.9 25.1

Interest-bearing long-term debt 1 520.7 1 107.5 1 185.6 830.1 779.6

Total long-term liabilities 1 619.1 1 166.4 1 245.0 886.0 804.7

9

Other interest-free current liabilities 106.1 166.1 203.1 182.3 75.5

Current portion of long-term debt 196.0 139.5 33.0 0.0 0.0

Total current liabilities 302.1 305.6 236.1 182.3 75.5

Total equity and liabilities 2 599.7 2 187.2 2 241.7 1 816.8 1 619.9

B.8 Selected key pro forma financial information

Not applicable. The Prospectus does not contain any pro forma financial information.

B.9 Profit forecast or estimate

Not applicable. The Prospectus does not contain any profit forecasts or estimates.

B.10 Audit report qualifications

Not applicable. The audit reports do not include any qualifications.

B.11 Working capital The Board is of the opinion that the working capital of the Company is sufficient for the Group's present requirements in a twelve months perspective as from the date of this Prospectus.

B.17 Credit ratings Not applicable. No credit ratings have been assigned to the Company or the New Convertible Bonds at the request of or with the cooperation of the issuer in the rating process.

Section C - Securities C.1 Type and class of

securities The Ordinary Shares of the Company in the issued share capital are registered with ISIN CY0100470919. New shares to be issued as Ordinary Shares will be issued and registered with ISIN CY0100470919. New Shares issued as Class A Shares are registered with ISIN CY0106610914.

Please see element C.3 and C.4 for information on the interim separate class of Shares.

C.2 Currency of the securities issue

Norwegian kroner (NOK)

C.3 Number of shares in issue and nominal value

The Company’s issued share capital consists of 6,049,010,116Shares, of which 259,570,359 are Ordinary Shares of nominal value EUR 0.001 and 5,789,439,757 are Class A Shares of nominal value EUR 0.001.

As resolved by the extraordinary general meeting of the Company held on 23 August 2016, the Company has carried out a share capital reduction pursuant to which the nominal value of the issued Ordinary Shares was reduced from Euro 0.25 to Euro 0.001 after which the Class A Shares will, following the publication of this Prospectus, be converted into Ordinary Shares.

C.4 Rights attaching to the securities

The Shares have voting rights, the right to receipt of dividend when declared and a right to share in the return of capital available for distribution in a winding up of the Company. The Class A Shares have the same rights as the Ordinary Shares except that the Class A Shares are automatically convertible into Ordinary Shares following the completion of the Capital Reduction and publication of this Prospectus. Each Share gives the right to one vote at the Company's general meeting.

C.5 Transferability The Shares of the Company are freely transferable subject to local regulatory transfer restrictions.

The New Convertible Bonds are freely transferable

C.6 Admission to trading

The Ordinary Shares of the Company are listed on the Oslo Stock Exchange. Pending completion of the Capital Reduction and publication of this Prospectus, the Company has registered the Class A Shares on the N-OTC

C.7 Dividend policy Prosafe’s aim is that its shareholders receive a competitive return on their Shares through a combination of share price appreciation and a direct return in the form of dividends. As part of the agreed amendments to its credit facilities, Prosafe has agreed that

10

it will not issue any dividends, bond or complete any equity buy-back from 31 December 2015 unless all voluntary skipped amortisations have been prepaid or cancelled and a 12-month financial forecast has been provided which confirms compliance with original financial covenants (except for the equity ratio which must be a minimum of 35 %).

C.8 Rights attaching to the New Convertible Bonds

The New Convertible Bonds constitute subordinated unsecured obligations of the Company. The New Convertible Bonds are subordinated to the senior debt of the Company, however the New Convertible Bonds shall rank pari passu with similarly subordinated debt of the Company (save for such claims which are preferred by bankruptcy, insolvency, liquidation or other similar laws of general application), shall rank ahead of all amounts payable in respect of the share capital of the Company or other capital of the Company subordinated in rank to the New Convertible Bonds. Each Bondholder has the right to convert each New Convertible Bond into Shares at the Conversion Price in effect on the relevant Conversion Date. Furthermore, the bondholders shall have preferential allocation of common equity in line with holders of common equity. The New Convertible Bonds are convertible at the Company's option at the following times: • Maturity • Formal insolvency proceedings of the Company or one or both of its

material asset owning subsidiaries • Upon a material refinancing of the majority of the financial indebtedness of

the Group in connection with actual or potential financial difficulties.

C.9 Terms of the New Convertible Bonds

Please see Element C.8 for the rights attached to the New Convertible Bonds.

Conversion price……………………….

NOK 0.25

Conversion Date Date falling ten (10) Business Days after the Paying Agent has received an exercise notice pursuant to clause 13.4 of the Bond Agreement

Coupon rate………………………

Zero coupon

Issue date………………………

14 September 2016

Maturity date ...................... 23 August 2021

Interest payment……… The Company shall not pay any interest on the New Convertible Bonds

Bondholders’ representatives ....................

Nordic Trustee ASA.

C.10 Derivative component in the interest payments on New Convertible

Not applicable. There are no interest payments on the New Convertible Bonds.

C.11 Admission to trading of the New Convertible Bonds

The Company intends to apply for the New Convertible Bonds to be admitted to trading on the Oslo Stock Exchange.

| Section D - Risks

11

D.1 Key risks specific to the Company or its industry

• Demand and supply in the market in which the Company operates is

subject to cyclical movements in both the global economy and in regional economies. These movements may be driven by a number of factors such as political processes, changing trading patterns, changes in productivity, technological shifts, and monetary imbalances.

• Demand for the Company's services may be affected negatively by oil companies’ earnings. Changes in the oil price affect oil companies’ cash flows adversely impacting their willingness to invest in exploration and production. If the oil price drops significantly, oil companies may reduce spending, which in turn may lead to lower demand for accommodation vessels. Furthermore, in the long-term demand will depend on the oil companies’ replacement ratio. If oil companies fail to replace reserves, ultimately leading to lower production volumes, demand for accommodation vessels may also be reduced. The Company's customer base is fairly well diversified, although certain customers may, to a varying degree over time, make up substantial parts of the contract backlog. In line with industry practice, a contract normally contains early cancellation provisions for the customer in specific circumstances. Subject to termination not being due to a breach or negligence on the part of the Company, the effect on results in such cases will normally be wholly or partly offset by a financial settlement in the Group’s favour.

• Any significant increases in the fleet of available accommodation vessels and/or reduction of oil prices and consequent reduction of demand may affect utilization rates and/or day rates negatively, potentially adversely impacting the Company's financial results and cash flows.

• As the Company is partly financed by interest-bearing debt it is subject to credit risk. All its loans have a defined maturity date and there will always be a risk that debt cannot be fully refinanced. This could relate to Company specific factors, such as excessive leverage, falling asset values or low earnings/cash flow or it could have to do with macro-economic factors and the general development in the global credit markets. Failure to refinance debt may have a material adverse impact on the Company’s financial position. The Company's loan agreements contain various covenants. Breach of one or more of the covenants may lead to higher cost of debt or, ultimately, mandatory pre-payment of loans.

D.3 Key risks specific to the securities

• If there proves to be no active trading market for the Shares, the price of the Shares may be more volatile and it may be more difficult to complete a buy or sell order for Shares

• The trading price of the Shares could fluctuate significantly in

response to a number of factors.

• Shareholders may be diluted if they are unable to participate in future offering

• No liquid market currently exists for trading of the New Convertible Bonds and it is not possible to predict whether, if the New Convertible Bonds are listed on Oslo Børs, this may provide increased liquidity.

12

• Bondholders will bear the risk of fluctuation in the price of the Company's Shares

• The New Convertible Bonds are subordinated to all senior indebtedness of the Company.

Section E - Offer E.1 Proceeds and

expenses The gross proceeds from the Private Placement will amount to NOK 1,094 million with estimated expenses amounting to approximately NOK 40 million. Consequently, the net proceeds will be approximately NOK 1,054 million. The gross proceeds from the Subsequent Offering will amount to up to NOK 126 million with estimated expenses amounting to approximately NOK 5 million. Consequently, the net proceeds will, if the Subsequent Offering is fully subscribed, be approximately NOK 121 million.

E.2a Reasons for the issuance of new shares and use of proceeds

The negative development in the offshore oil service markets in 2015/16, coupled with an overspend and further delay in the start-up of the Safe Scandinavia Tender Support Vessel (“TSV”), suspension of additional Mexico contracts (including cancellation of a letter of intent for a new 4.5 year contract of ca USD 145 million for Safe Notos) and a consequent deterioration of the Group's contract backlog, as well as the unavailability of the bond market as a refinancing source, led to a situation where the Group's financial covenants would have been under pressure. The Company therefore engaged legal and financial advisors and initiated a review of the Company’s strategic options and funding situation.

Following discussions with key stakeholders, including secured bank lenders, major bondholders and shareholders, the Company announced on 7 July 2016, the terms of a comprehensive refinancing (the "Refinancing") for the purpose of improving the Company´s financial situation. The Refinancing comprised a solution involving new capital, amortization relief and covenant ease from senior lenders and conversion (equitization) of bond debt. The Refinancing will provide greater financial flexibility for the Company throughout the period until the end of 2020 including a solid liquidity buffer to weather a prolonged market downturn. The combined effect of the Refinancing is expected to improve the Company's liquidity by approximately USD 478 million over a five year period, and reduce the net interest bearing debt by approximately USD 395 million through 100% conversion of senior unsecured bonds, in addition to the contribution of new equity. The Refinancing will result in a substantial dilution of existing shareholders not participating in the Private Placement, and the contemplated Subsequent Offering will not fully compensate the dilutive effect for the remaining shareholders. Having considered available alternatives, the Board was however of the opinion that such deviation from the equal treatment principle was fair and necessary, given the challenging financial situation of the Company, the prevailing market conditions, the agreed terms of the Refinancing and the Company's need for certainty and flexibility when seeking to secure new equity. The proceeds from the Private Placement will be used to strengthen the Company's balance sheet, bond redemption and liquidity position as well as for general corporate purposes. USD 40 million of the proceeds from the Private Placement will be used to buy-back part of the Company's bonds.

E.2b Reasons for the issuance of new shares and use of proceeds from the New Convertible

Please see element E.2a

13

Bonds

E.3 Terms and conditions

The issuing of the Private Placement Shares, Bond Conversion Shares and Offer Shares were conditional on valid corporate resolutions being made to issue such Shares.

E.4 Interests material to the issue

The Managers and their affiliates have provided from time to time, and may provide in the future, investment and commercial banking services to the Company and its affiliates in the ordinary course of business, for which they may have received and may continue to receive customary fees and commissions. The Managers, its employees and any affiliate may currently own existing Shares in the Company. The Managers do not intend to disclose the extent of any such investments or transactions otherwise than in accordance with any legal or regulatory obligation to do so. The Managers will receive a success fee of a fixed percentage of the gross proceeds raised in the Subsequent Offering and, as such, have an interest in the Subsequent Offering.

E.5 Selling shareholders and lock-up

Not applicable. All Offer Shares will be newly issued Shares and no subscriber will be subject to lock-up.

E.6 Dilution As a consequence of the issuance of the Private Placement Shares and the Bond Conversion Shares, the shareholders who did not participate were diluted by approximately 96% (this does not take into account any Shares under the New Convertible Bond). The immediate dilution of ownership for shareholders not participating in the Subsequent Offering will be approximately 8% (given full subscription).

E.7 Estimated expenses charged to investor

Not applicable. No expenses will be charged to the investor by the Company.

14

2. RISK FACTORS

Investing in the Company involves inherent risks. Prospective investors should consider carefully, among other things, all of the information set forth in this Prospectus, and in particular, the specific risk factors set out below. An investment in the Shares is suitable only for investors who understand the risk factors associated with this type of investment and who can afford a loss of all or part of the investment. If any of the risks described below materialises, individually or together with other circumstances, they may have a material adverse effect on the Company’s business, operating results and financial condition, which may cause a decline in the value and trading price of the Shares that could result in a loss of all or part of any investment in the Shares. The order in which the risks are presented below is not intended to provide an indication of the likelihood of their occurrence nor of their severity or significance.

2.1 STRATEGIC RISK Unlike risks related to assets, operations, projects, legal compliance/legal and finance, where the Company seeks to reduce exposure as far as reasonably and practically possible, strategic risk is the only category that the Group actively accepts in order to generate a return for its shareholders. The Company will create shareholder value by allocating capital and resources to the commercial opportunities that yield the best return in relation to the risks involved within its specified strategic direction.

2.1.1 Macro risk Demand and supply in the market in which the Company operates is subject to cyclical movements in both the global economy and in regional economies. These movements may be driven by a number of factors such as political processes, changing trading patterns, changes in productivity, technological shifts, and monetary imbalances.

2.1.2 Demand risk (clients) Demand for the Company's services may be affected negatively by oil companies’ earnings. Changes in the oil price affect oil companies’ cash flows adversely impacting their willingness to invest in exploration and production. If the oil price drops significantly, oil companies may reduce spending, which in turn may lead to lower demand for accommodation vessels. Furthermore, in the long-term demand will depend on the oil companies’ replacement ratio. If oil companies fail to replace reserves, ultimately leading to lower production volumes, demand for accommodation vessels may also be reduced. The Company's customer base is fairly well diversified, although certain customers may, to a varying degree over time, make up substantial parts of the contract backlog. In line with industry practice, a contract normally contains early cancellation provisions for the customer in specific circumstances. Subject to termination not being due to a breach or negligence on the part of the Company, the effect on results in such cases will normally be wholly or partly offset by a financial settlement in the Group’s favour.

2.1.3 Supply risk (competition) Any significant increases in the fleet of available accommodation vessels and/or reduction of oil prices and consequent reduction of demand may affect utilization rates and/or day rates negatively, potentially adversely impacting the Company's financial results and cash flows.

2.2 NON-STRATEGIC RISK

2.2.1 Asset and other liabilities risk Operational risks may result in injury to personnel, damage or loss of a vessel, property, equipment and accidental discharges/ emissions to the natural environment. To mitigate these risks, most of the Group's assets, are insured at the estimated replacement cost taking into consideration applicable industry standards, regulations and all requirements set out in any finance facility documentation. Insurance is taken out with reputable international insurance companies and in accordance with good market practice. The Company's insurances cover its assets (both operated and non-operated vessels), third party liabilities, pollution and environmental risks, cargo and non-marine risks. However, insurance will not always provide full coverage of all risks resulting from operations and there can be no assurance that all risks can be adequately insured against all potential liabilities or that any insured sum will be paid which in turn may adversely affect the Company's financial position.

15

2.2.2 Operational risk In most of the Group’s contracts the day rate received will be subject to gangway uptime. Consequently, any operating failure leading to down time on the gangway connection may affect the Company's results negatively. Such downtime may be caused by human errors, breakdown of equipment or an otherwise difficult operating environment.

2.2.3 Health Safety and Environment risk The work processes onboard the Group’s vessels can be complex and may have to be undertaken in a potentially difficult environment. Consequently, there is a risk that personnel may be injured and/or equipment damaged. Furthermore, the business entails risk of accidental discharges/emissions to the natural environment.

2.2.4 Key personnel and crew risk The Company is operating in a complex industry. Although measures are taken to reduce dependency on any individual employee, the Company may in certain situations be dependent on the competency and experience of key personnel. Consequently, any such person leaving the Company may affect processes and operations negatively. Having a competent and experienced crew on the vessels is vital for achieving high operational standards. The competition for such key personnel is intense, and the loss of the services of one or more of these individuals without adequate replacements or the inability to attract new qualified personnel at a reasonable cost could have a material adverse effect. If increased competition for qualified personnel were to intensify in the future, the Company may experience increases in costs or limits on operations.

2.2.5 Hazard risk Given the nature of the Company's business, any operating failure or loss of asset integrity may cause serious accidents that could lead to critical damage and, ultimately, a total loss of the asset. This could have a severe impact on the Company's financial position.

2.2.6 Project execution and construction risk The Company will from time to time undertake larger projects related to new builds or upgrades of existing vessels. Such projects carry considerable risks related to cost overruns and delayed completion that may have a material adverse impact on the Company’s financial position.

2.2.7 Technical and unexpected repair costs risk Technical risk involves future demand for certain technical specifications and a supplier’s or yard’s ability to deliver in line with the specifications required. These future demands may have significant impact on the financial statements of the Group. The timing and costs of unexpected repairs on the Company’s vessels are difficult to predict with certainty and may be substantial. Many of these expenses, such as special survey and certain repairs for normal wear and tear are typically not covered by insurance. Large repair expenses could decrease the Company’s profits. In addition, repair time may result in a loss of revenue for the Company.

2.2.8 Regulatory risk The Company is involved in an industry that is highly regulated by different international and national Governmental bodies. Non-compliance with relevant regulations may lead to suspended operations, prosecutions and/or the imposition of fines which in turn may cause financial losses. Furthermore, in order to comply with changes to regulations the Company may, from time to time, incur substantial capital and operating costs. Such changes to regulations may also affect the Company's vessels. This could adversely impact the commercial and strategic position of the Company and affect its ability to expand or even maintain its current market position.

2.2.9 Legal proceedings and contractual disputes risk In the course of its activities, the Company may become involved in contractual and other disputes and legal proceedings where the final outcome is subject to uncertainties. Such proceedings may cause the Company to incur unforeseen expenses and could occupy a significant amount of management’s time and attention. Depending on the outcome, such proceedings may have a negative impact on the financial position and operations of the Company. For a description of current material disputes, please refer to section 13.1.

2.2.10 Interest rate risk The Company's fleet is partly financed by interest-bearing debt. Although the Company seeks to mitigate such risk by different hedging arrangements, increases in interest rates may have a material adverse impact on the Company's earnings and cash flows.

16

2.2.11 Currency risk The Company is exposed to several currencies. The bulk of revenues are in United States Dollars (USD) and vessels owned by the Company are valued and financed in USD. Accounts are therefore compiled in USD. During certain periods, however, depending on the country of operation, the Company will have contracts that yield GBP, NOK and BRL revenues, with a consequent reduction in net currency exposure. Operating expenses are mainly denominated in USD, GBP, NOK, SGD and BRL, but depending on the country of operation and nationality of the crew, operating expenses can also be in other currencies, such as EUR and SEK. Fluctuations in the mentioned currencies versus the USD may have significant impact on the financial statements of the Company.

2.2.12 Credit risk As the Company is partly financed by interest-bearing debt it is subject to credit risk. All its loans have a defined maturity date and there will always be a risk that debt cannot be fully refinanced. This could relate to Company specific factors, such as excessive leverage, falling asset values or low earnings/cash flow or it could have to do with macro-economic factors and the general development in the global credit markets. Failure to refinance debt may have a material adverse impact on the Company’s financial position. The Company's loan agreements contain various covenants. Breach of one or more of the covenants may lead to higher cost of debt or, ultimately, mandatory pre-payment of loans.

2.2.13 Counter-party risk The Company's clients are mostly reputable national oil companies, super majors, majors and larger independent oil companies. However, if a client should default on any obligation it could have a material negative impact on the Company's earnings and cash flows.

2.3 RISKS RELATED TO THE SHARES AND THE NEW CONVERTIBLE BONDS

2.3.1 There may not be a liquid market for the Shares Active, liquid trading markets generally result in lower price volatility and more efficient execution of buy and sell orders for investors. If there proves to be no active trading market for the Shares, the price of the Shares may be more volatile and it may be more difficult to complete a buy or sell order for Shares. Even if there is an active public trading market, there may be little or no market demand for the Shares, making it difficult or impossible to resell the shares, which would have an adverse effect on the resale price, if any, of the Shares. Furthermore, there can be no assurance that the Company will maintain its listing on Oslo Børs. A delisting from Oslo Børs would make it more difficult for shareholders to sell their Shares and could have a negative impact on the market value of the Shares.

2.3.2 Volatility of the share price The trading price of the Shares could fluctuate significantly, inter alia, in response to quarterly variations in operating results, general economic outlook, adverse business developments, interest rate changes, changes in financial estimates by securities analysts, matters announced in respect of competitors or changes to the regulatory environment in which the Company operates. Market conditions may affect the Shares regardless of the Company’s operating performance or the overall performance in the industry. Accordingly, the market price of the Shares may not reflect the underlying value of the Group’s net assets, and the price at which investors may dispose of their Shares at any point in time may be influenced by a number of factors, only some of which may pertain to the Company, while others of which may be outside the Company’s control. The market price of the Shares could decline due to sales of a large number of Shares in the Company in the market or the perception that such sales could occur. Such sales could also make it more difficult for the Company to offer equity securities in the future at a time and at a price that are deemed appropriate.

2.3.3 Shareholders may be diluted if they are unable to participate in future offerings The development of the Group’s business may, inter alia, depend upon the Company’s ability to obtain equity financing. Unless otherwise dis-applied by resolution of the general meeting, shareholders in Cypriot public companies such as the Company have statutory pre-emptive rights proportionate to the aggregate amount of the shares they hold with respect to new shares issued by the Company for cash. Shareholders that do not exercise granted pre-emptive rights may be diluted. Furthermore, shareholders may be unable to participate in future offerings, where the shareholders pre-emptive rights have been dis-applied in order to raise equity on short notice in the investor market, or for reasons relating to foreign securities laws or other factors, and as such have their shareholdings diluted.

17

2.3.4 Pre-emptive rights may not be available to U.S. holders and certain other foreign holders of the Shares

Under Cyprus law, prior to the Company’s issuance of any new Shares for consideration in cash, the Company must offer holders of the Company’s then issued Shares pre-emptive rights to subscribe and pay for a sufficient number of Shares to maintain their existing ownership percentages, unless these rights are waived at a general meeting of the Company’s shareholders. U.S. holders of the Shares may not be able to trade or exercise pre-emptive rights for new Shares unless a registration statement under the U.S. Securities Act is effective with respect to such rights or an exemption from the registration requirements of the U.S. Securities Act is available. The Company is not a registrant under the U.S. securities laws. If U.S. holders of the Shares are not able to trade or exercise pre-emptive rights granted in respect of their Shares in any rights offering by the Company, then they may not receive the economic benefit of such rights. In addition, their proportional ownership interests in the Company will be diluted. Similar restrictions may apply to other foreign holders of Shares, including, but not limited to shareholders in Australia, Canada, Hong Kong, Japan and Switzerland.

2.3.5 Holders of Shares that are registered in a nominee account may not be able to exercise voting rights as readily as shareholders whose Shares are registered in their own names with the Norwegian Central Securities Depository

Beneficial owners of the Company’s Shares that are registered in a nominee account (e.g., through brokers, dealers or other third parties) may not be able to vote for such Shares unless their ownership is re-registered in their names with the VPS prior to the Company’s general meetings. The Company cannot guarantee that beneficial owners of the Company’s Shares will receive the notice for a general meeting in time to instruct their nominees to either effect a re-registration of their Shares or otherwise vote for their Shares in the manner desired by such beneficial owners.

2.3.6 The transfer of Shares is subject to restrictions under the securities laws of the United States and other jurisdictions

The Company has not registered the Shares under the U.S. Securities Act or the securities laws of other jurisdictions than Norway and the Company does not expect to do so in the future. The Shares may not be offered or sold in the United States, nor may they be offered or sold in any other jurisdiction in which the registration of the Shares is required but has not taken place, unless an exemption from the applicable registration requirement is available, or the offer or sale of the Shares occurs in connection with a transaction that is not subject to these provisions. In addition, there can be no assurances that shareholders residing or domiciled in the United States will be able to participate in future capital increases or exercise subscription rights.

2.3.7 Liquidity of the New Convertible Bonds No liquid market currently exists for trading of the New Convertible Bonds and it is not possible to predict whether, if the New Convertible Bonds are listed on Oslo Børs, this may provide increased liquidity.

2.3.8 Bondholders will bear the risk of fluctuation in the price of the Company's Shares The market price of the New Convertible Bonds is expected to be affected by fluctuations in the market price of the Company’s Shares and it is impossible to predict whether the price of the Shares will rise or fall. Any decline in the price of the Shares may have an adverse effect on the market price of the New Convertible Bonds.

2.3.9 Risk related to subordination of the New Convertible Bond The New Convertible Bonds are subordinated to all senior indebtedness of the Company. Rights to receive payment on the New Convertible Bonds in a default situation will therefore be subject to all senior lenders first receiving due payment. Furthermore, the Company may always choose to settle its obligations under the New Convertible Bonds with delivery of Shares.

18

3. STATEMENTS

3.1 RESPONSIBILITY FOR THE PROSPECTUS We, the Board of Directors of Prosafe SE (the "Board"), hereby declare that, having taken all reasonable care to ensure that such is the case, the information contained in this Prospectus is, to the best of our knowledge, in accordance with the facts and contain no omissions likely to affect its import.

14 October 2016

The Board of Prosafe SE

Glen Ole Rødland Non-executive interim chairman

Roger Cornish Non-executive director

Nancy Ch. Erotocritou Non-executive director

Carine Smith Ihenacho Non-executive director

Anastasis Ziziros Non-executive director

19

3.2 INFORMATION SOURCED FROM THIRD PARTIES In certain sections of this Prospectus information sourced from third parties has been reproduced. In such cases, the source of the information is always identified. Such third party information has been accurately reproduced. As far as the Company is aware, and is able to ascertain from information published by the relevant third party, no facts have been omitted which would render the reproduced information inaccurate or misleading.

3.3 NOTICE REGARDING FORWARD-LOOKING STATEMENTS

Sections 6, 7 and 9 include “forward-looking” statements, including, without limitation, projections and expectations regarding the Company’s future financial position, business strategy, plans and objectives. All forward-looking statements included in this document are based on information available to the Company, and views and assessment of the Company, as of the date of this Prospectus. The Company expressly disclaims any obligation or undertaking to release any updates or revisions of the forward-looking statements contained herein to reflect any change in the Company’s expectations with regard thereto or any change in events, conditions or circumstances on which any such statement is based, unless such update or revision is prescribed by law.

When used in this document, the words “anticipate”, “believe”, “estimate”, “expect”, “seek to”, “may”, “plan” and similar expressions, as they relate to the Company, its subsidiaries or its management, are intended to identify forward-looking statements. The Company can give no assurance as to the correctness of such forward-looking statements and investors are cautioned that any forward-looking statements are not guarantees of future performance. Forward-looking statements are subject to known and unknown risks, uncertainties and other factors, which may cause the actual results, performance or achievements of the Company and its subsidiaries, or, as the case may be, the industry, to materially differ from any future results, performance or achievements expressed or implied by such forward-looking statements. Such forward-looking statements are based on numerous assumptions regarding the Company’s present and future business strategies and the environment in which the Company and its subsidiaries are operating or will operate. Factors that could cause the Company’s actual results, performance or achievements to materially differ from those in the forward-looking statements include, but are not limited to, those described in Section 2 “Risk Factors” and elsewhere in this Prospectus.

Given the aforementioned uncertainties, readers are cautioned not to place undue reliance on any of these forward-looking statements.

20

4. THE REFINANCING

4.1 BACKGROUND The negative development in the offshore oil service markets in 2015/16, coupled with an overspend and further delay in the start-up of the Safe Scandinavia Tender Support Vessel (“TSV”), suspension of additional Mexico contracts (including cancellation of a letter of intent for a new 4.5 year contract of approximately USD 145 million for Safe Notos) and a consequent deterioration of the Group's contract backlog, as well as the unavailability of the bond market as a refinancing source, led to a situation where the Group's financial covenants would have been under pressure. The Company therefore engaged legal and financial advisors and initiated a review of the Company’s strategic options and funding situation.

Following discussions with key stakeholders, including secured bank lenders, major bondholders and shareholders, the Company announced on 7 July 2016, the terms of a comprehensive refinancing (the "Refinancing") for the purpose of improving the Company´s financial situation. The Refinancing comprised a solution involving new capital, amortization relief and covenant ease from senior lenders and conversion (equitization) of bond debt. The Refinancing will provide greater financial flexibility for the Company throughout the period until the end of 2020 including a solid liquidity buffer to weather a prolonged market downturn. The combined effect of the Refinancing is expected to improve the Company's liquidity by approximately USD 478 million (approximately NOK 4,005 million) over a five year period, and reduce the net interest bearing debt by approximately USD 395 million (approximately NOK 3,310) through 100% conversion of senior unsecured bonds, in addition to the contribution of new equity. The Refinancing results in a substantial dilution of existing shareholders not participating in the Private Placement, and the contemplated Subsequent Offering will not fully compensate the dilutive effect for the remaining shareholders. Having considered available alternatives, the Board was however of the opinion that such deviation from the equal treatment principle was fair and necessary, given the challenging financial situation of the Company, the prevailing market conditions, the agreed terms of the Refinancing and the Company's need for certainty and flexibility when seeking to secure new equity.

4.2 THE MAIN TERMS OF THE REFINANCING