propinquity exploring global distribution...

TRANSCRIPT

Exploring Global Distribution Strategy

Propinquity works with asset managers to think through and optimize the delivery of their investment capabilities in the context of a complex and rapidly evolving competitive environment.

What Propinquity does

2

1. Who we are and what we do well

Guiding logic

• Successful asset managers align their activities with the perspective of sophisticated buyers of asset management products, anticipate their needs, and understand their motivations and evaluation processes.

• Context is important for positioning and focus – several unfolding themes are driving the future of the industry at an unprecedented rate and scale.

• What is immediately apparent and often taken at face value (fund flows, product launch trends, M&A activity, etc.) does not go far enough in explaining underlying implications. Nuances and subtleties make big differences.

3

1. Who we are and what we do well

Who we serve

• Propinquity serves boutiques selling their capabilities in a single jurisdiction and global managers with hundreds of products sold around the globe. Public and private. AuM range from de novo to $500+ billion.

• Our preferred clients are those managers who are good at what they do (though perhaps not positioned optimally), motivated to grow, are facing complex challenges and appreciate the value of thinking things through.

• Often there is need for a bridge: between investments and distribution, existing product range and evolving marketplace or across geographical/market borders.

4

1. Who we are and what we do well

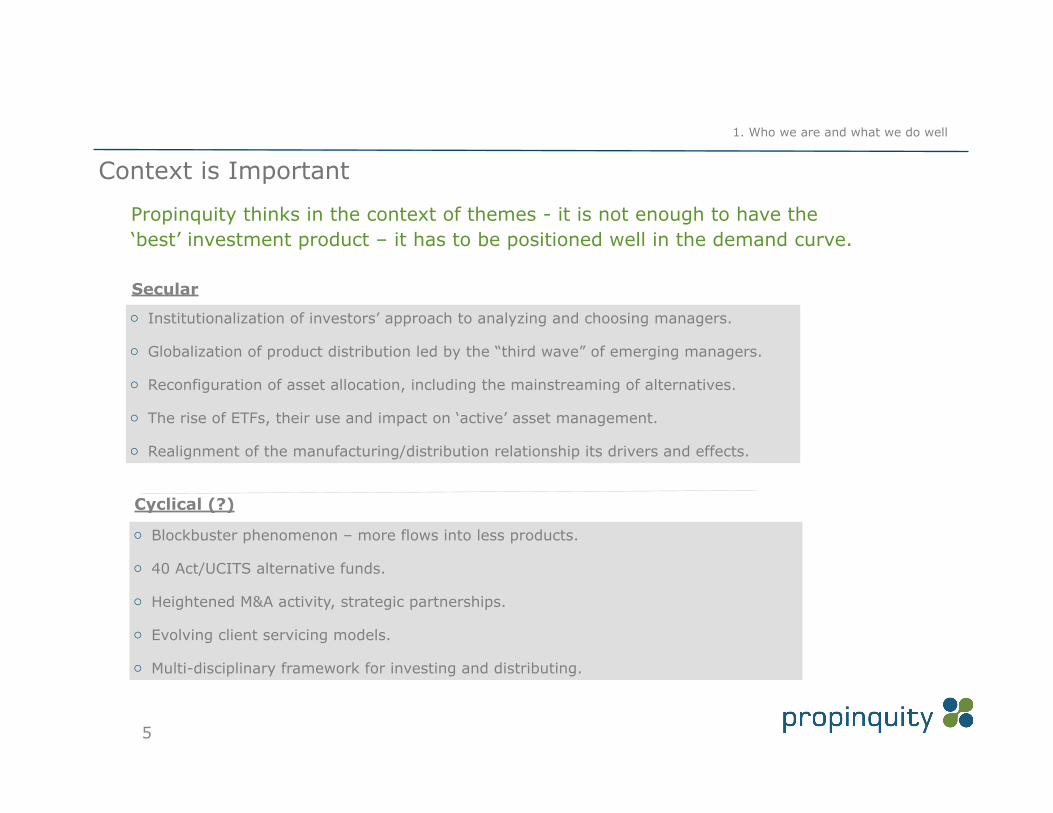

Context is Important

o Institutionalization of investors’ approach to analyzing and choosing managers.

o Globalization of product distribution led by the “third wave” of emerging managers.

o Reconfiguration of asset allocation, including the mainstreaming of alternatives.

o The rise of ETFs, their use and impact on ‘active’ asset management.

o Realignment of the manufacturing/distribution relationship its drivers and effects.

Secular

o Blockbuster phenomenon – more flows into less products.

o 40 Act/UCITS alternative funds.

o Heightened M&A activity, strategic partnerships.

o Evolving client servicing models.

o Multi-disciplinary framework for investing and distributing.

Cyclical (?)

Propinquity thinks in the context of themes - it is not enough to have the ‘best’ investment product – it has to be positioned well in the demand curve.

5

1. Who we are and what we do well

Exploring Global Distribution

6

Global Distribution - Overview

Opportunity - Asset management companies, for purposes of growth and diversification, are seeking opportunities to distribute their investment capabilities outside of their home markets.

Insight - While huge opportunities exist, an attempt to build global distribution can be a major drain on attention and budgets. The industry is littered with managers who have attempted and failed (sometime two and three times) to build and execute a strategy for global distribution. There are also ample cases of tremendous success. What follows are some basic thoughts on how Propinquity orients its clients to the challenge.

7

2. An area of focus - global distribution strategy

Finding the balance – matching near-term opportunities & resource requirements

“

Resources (Cost)

Near-Term Opportunity

Decent Opportunity,

Modest Resource Demand

Big Opportunity,

Big Resource Demand

Minimal Opportunity

Modest Resource Demand

Minimal Opportunity,

Big Resource Demand

Potential Opportunities

! Broaden & deepen distribution

! Increase AuM & margins

! Diversify client base

! Expand long-term opportunity set

Potential Costs

! Legal, set up, advice

! T&E

! Missed domestic opportunities

! Time, misalignment of interests

What are reasonable expectations & measures of success?

8

2. An area of focus - global distribution strategy

U.S. Managers – going international

! Well in excess of 100 U.S. firms distribute investment products outside of the U.S.

! No magic formula – successful managers play to their own strengths, demonstrate patience and

develop early wins before making sizable commitments of resources.

! Success has been reached through:

! segregated accounts

! proprietary cross border UCITS range

! sub-advisory engagements

! JV with local entities

! by taking meaningful ownership stakes and/or full acquisitions

* see matrix in appendix of this document

9

2. An area of focus - global distribution strategy

Match Opportunities with Patience and Budget:Thinking near to intermediate term – pick your spots (a global view)

MARKETS TO AVOID short-term but plan for long-term?:

! Over supplied, recently over-fished markets (Hong Kong, Singapore)

! Overly complex or ‘closed’ to external asset managers (Brazil, Mainland China)

! Unsophisticated investors (Direct Retail)

! Markets that are too small to matter (Numerous)

! Markets needing intense local support (Retail, platform, IFA)

! Markets that need extensive sales agreements/operational structuring (Retail, IFA)

! Retail sales (IFA, local banking, non-discretionary)

! Hyper-brand conscious (Asian retail)

! Very long lead times (Japan)

Topics in “()” are examples, not definitive.

10

2. An area of focus - global distribution strategy

The Global Manager: Franklin Templeton – not an overnight success

Offices/Representation: Franklin has 50 offices around the world (30 with on the ground research staff)

and 13 trading desks.

11

2. An area of focus - global distribution strategy

Global Financial Institutions (GFIs) as bridges for expansion of global distribution

! GFIs are increasingly networked – from the ‘center’ to a region to ‘local’ markets and other regions (e.g. Asian connection with MENA, LATAM and Switzerland & U.S.). Where are the clients and from where are they being serviced? Do all roads lead to London, New York, Frankfurt, Paris…?

US Europe Global

12

2. An area of focus - global distribution strategy

Learning from other’s mistakes – What doesn’t work?

In various iterations, one could point to a range of U.S. based firms that have either grown their

businesses at sub-scale/sub-optimal levels and/or failed (though many have re-entered). Typical

reasons include:

! Wrong product(s), wrong time.

! Lack of patience, resources. Wrong people/partners.

! Lack of commitment (perceived or real) throughout the organization to see the effort through

(from investment professionals, to operations/legal through to distribution personnel).

! Spreading efforts too thin – lack of focus.

! Overestimating the potential of a market vs. resource demand/commitment. Underestimating

the competition – both local and ‘cross-border.’

! Strategic over-commitment to single client type (global banks for instance).

13

2. An area of focus - global distribution strategy

What doesn‘t work? (cont.)

! Not properly laying the foundation before making a push (sales agreements, registration

requirements, etc.) – firing blanks.

! Not properly using/building bridges from current relationships.

! Trying to be all things to all people- ‘investor bandwidth.’

! Chasing hot money, getting and then losing hot money.

! Investment story lost in translation.

! Home office/international communication melt-down.

14

2. An area of focus - global distribution strategy

US Managers abroad

15

2. An area of focus - global distribution strategy

International Distribution - Decision Matrix

Option Cost Strength Weakness Opportunity ThreatHow to Implement/ Next Steps?

Timeframe to execute?

Mutually Exclusive

Do Nothing potential missed opportunity

No risk in failing. Resource conservation. Maintain focus on 'core' U.S. business. Avoid rocking the boat and risk.

Reliance on existing approach and a market that is both maturing and constricting margins. Giving up opportunties do something new, interesting and potential very profitable.

Solidify focus on evolving U.S. marketplace.

Miss the boat and get left behind. No rewind - markets will only become more mature and competitive.

Do nothing 0 days YES

Tactical/Light Touch - 'Fly in-Fly Out'

Low (relative), travel expenses, preparation time, time out of the office - likely to demand 1/2 FTE initially

Builds on existing relationships developed in the the U.S. (consultants). Allows for getting a toe in the water without a massive commitment. Potentially could identify some early wins that would demonstrate the validity/justify a more intense effort.

May not be necessarily effective. Investors want to see 'commitment'. Will a person without the experience/ knowledge in the markets be able to have impact while learning on the job?

Focus only on what is important, local presence could add a lot of noise and excitement with limited real unproven benefit- depends on the resources deployed! Gives tremendous flexibility to go where tactical opportunites present themselves (driven by consultant relations for instance).

Potential investors see a lack of commitment and get fatigued… Too slow to market and the currently strong performance cycle weakens.

Identify key markets/investors (primarily through developing consultant relations) and go to market quarterly or more often as needed - could be supplemented with placement agents/third party marketing.

ongoing (preparation of materials, database entries, etc. first)

NO. Could combine with use of 3PM.

Subadvisory Low (relative) - development would be similar to Fly in-Fly Out'

Quick to market, 'auto-pilot' approach. Works well when it works but run the risk of a dead end if the 'sponsor' of the fund/platform does not deliver. Distribution is the real key! Adding additional partners (or establishing own fund range) can make dificult bedfellows.

Lack of control, don't own the assets or the relationship. thinner margins (typically) opportunity cost. Is this the approach of a Tier 1 manager?

Building several such subadvisory relationships across different markets (geographic typically) can be very powerful. A great way to enter markets that an AMC otherwise would not have access to or the potential for building a business directly. A great way to explore business engagements on more equal footing (B to B) - also, what are the cross selling opportunties? - plenty of interest in U.S. distribution for non-U.S. entities

If the platform does not do well (not a going concern) or the distribution arm does not raise money and/or poorly represents AMC, run the risk of tarnishing brand and forward opportunity. Need to pick the right partners - difficult to 'unwind' - the engagement and wind-down gets public recognition.

Conduct search for subadvisory mandates in a variety of asset classes. This is done both top down (relationships) as well as bottom up on a product basis (looking to replace). There are very large pools of money in Europe (Nordics) and Asia (Japan) who work within such relations.

180 day exploration period.

NO

16

2. An area of focus - global distribution strategy

International Distribution - Decision Matrix (cont. 2)

Option Cost Strength Weakness Opportunity ThreatHow to Implement/ Next Steps?

Timeframe to execute?

Mutually Exclusive

Develop own UCITS-compliant fund range

Setup of 100k- 1MM depending upon complexity and service providers chosen - typically costs are allocated back to the fund. In addition, there are expenses related to registration in country and various regulatory hurdles/oversights.

Gives a brand presence. Pasively it is helpful to show up in databases etc. - ability to 'passively' gather assets, build a track record. It is the global brand usable across LatAm, Europe and Asia. Funds are far more accepted within institutions. Strategic flexibility. Consistent with route of large U.S. managers.

Cost, need for seed, committed…

Open ended - gives the option to take advantage as options arise, distribution is a secondary consideration (meaning, non-fixed as it is with a subadvisory mandate or using another's platform). Necessary for large DPM, FoFs markets and family offices in some cases. Also necessary for the cross border 'bridge relationships' w/ GFIs.

(Fixed) cost of maintaining, ability to execute?

Explore 2-3 service provider options to better understand the process and cost. Several 'full sevice' providers willing to assist as well as accountants and lawyers.

120 days NO

Establish Local Offices

Real Estate, personnel, taxes/legal, local business entity

Demonstrates 'commitment'. Provides a means to establish relationships and have boots on the group. London is by far the most common 'first stop'

Cost, is highly personality dependent - just having someone on the ground ensures nothing long-term. Would like be in a 'hub' (London for instance) so closer to local but not exactly.

Gives another (closer) stepping off point for local markets. May be necessary to do business in some markets (have a truly local office - although 'representative' in nature). Could be a point of common ground with investment teams who want to establish local research.

The ongoing expense can be a major drawback if revenues do not come in short order. Legal/ regulatory hassel & expense.

Decide on location, evaluate real estate and staffing needs.

120 days for local company formation, office, extended time to staff

NO

17

2. An area of focus - global distribution strategy

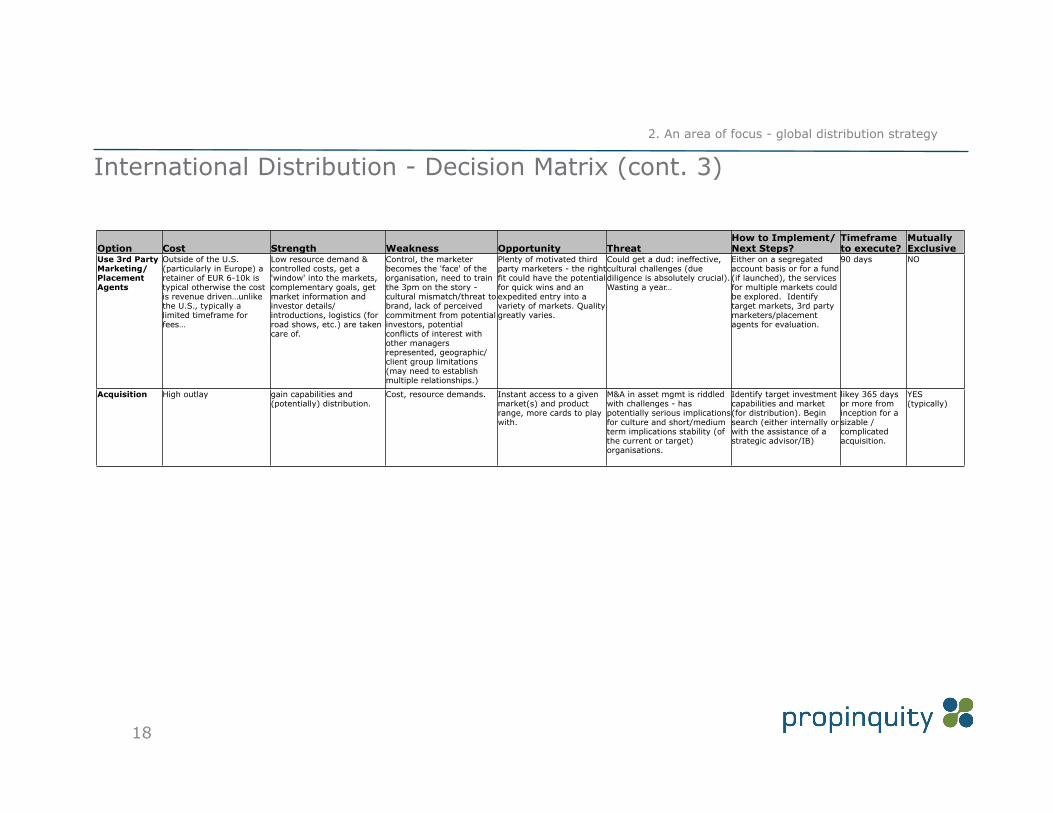

International Distribution - Decision Matrix (cont. 3)

Option Cost Strength Weakness Opportunity ThreatHow to Implement/ Next Steps?

Timeframe to execute?

Mutually Exclusive

Use 3rd Party Marketing/Placement Agents

Outside of the U.S. (particularly in Europe) a retainer of EUR 6-10k is typical otherwise the cost is revenue driven…unlike the U.S., typically a limited timeframe for fees…

Low resource demand & controlled costs, get a 'window' into the markets, complementary goals, get market information and investor details/introductions, logistics (for road shows, etc.) are taken care of.

Control, the marketer becomes the 'face' of the organisation, need to train the 3pm on the story - cultural mismatch/threat to brand, lack of perceived commitment from potential investors, potential conflicts of interest with other managers represented, geographic/client group limitations (may need to establish multiple relationships.)

Plenty of motivated third party marketers - the right fit could have the potential for quick wins and an expedited entry into a variety of markets. Quality greatly varies.

Could get a dud: ineffective, cultural challenges (due diligence is absolutely crucial). Wasting a year…

Either on a segregated account basis or for a fund (if launched), the services for multiple markets could be explored. Identify target markets, 3rd party marketers/placement agents for evaluation.

90 days NO

Acquisition High outlay gain capabilities and (potentially) distribution.

Cost, resource demands. Instant access to a given market(s) and product range, more cards to play with.

M&A in asset mgmt is riddled with challenges - has potentially serious implications for culture and short/medium term implications stability (of the current or target) organisations.

Identify target investment capabilities and market (for distribution). Begin search (either internally or with the assistance of a strategic advisor/IB)

likey 365 days or more from inception for a sizable /complicated acquisition.

YES (typically)

18

2. An area of focus - global distribution strategy

To Discuss:

Roland MeerdterManaging Partner+(1) 917 543 [email protected]

Last updated: January 2014

Copyright © 2014 Propinquity Advisors LLC. All rights reserved. No portion of this document can be used without permission.www.propinquityadvisors.com

Contact

19

2. An area of focus - global distribution strategy

Leadership

Roland J. Meerdter is Managing Partner of Propinquity. Prior to founding the firm in 2009, Roland was a Managing Director of Deutsche Bank. His primary role at DB was as global head of manager/fund research and due diligence. He was a member of the firm’s Global Investment Committee. Prior to joining DB in 1999, he was a research analyst with a multi-family office. He is sought for his advice and perspective on developments in the asset management industry. He earned a BA in philosophy (magna cum laude) from the University of Oregon. He has held the series 7 & 65 securities licenses.

20

1. Who we are and what we do well