property and casualty insurance (pre-license)

TRANSCRIPT

Property and Casualty Insurance (Pre-License)

Module 1: Property Insurance

Lesson 1: Insurance Terms and Related Concepts

Purpose of Insurance

The purpose of insurance is to spread risk amongst others and provide a

practical solution to economic uncertainties and unexpected losses.

For test purposes, insurance is defined as a social device for handling risk

by transferring it.

Parts of the Insurance Contract

Since an insurance policy is a legal contract, it must be very specific about the

agreements between the insured and the insurer. To do this, most policies

contain five parts:

� Declarations: These can usually be found on the first page of the

policy.

• It contains information such as the name of the insured,

address, amount of coverage, description of the property, and

the cost of the policy.

� Insuring Agreements: This is the �heart� of the policy as it states

what is to be covered or, in other words, the losses for which the insured

will be indemnified.

• The insuring agreement also describes the type of property

covered and the perils against which it is insured.

� Conditions: This part of the contract describes the responsibilities

and obligations of both the insurance company and the insured. In

other words, everyone knows what they have to do.

� Exclusions: Describes the losses for which the insured is not covered.

If an excluded loss occurs, the insured will not be indemnified.

� Definitions: This section clarifies the meaning of certain terms

used in the policy.

Insurable Interest

Before a person can benefit from insurance, that person must have a chance of

financial loss or have a financial interest in the property. The insured must have

an insurable interest in his/her home or any subject of the insurance. It is

important to note that it is at the time of a loss when the insured must have an

insurable interest as it relates to property and casualty insurance.

Risk

A risk is the uncertainty or chance of a loss

Types of Risks

1. Speculative Risk: This risk implies that an individual has the potential

of improving his/her financial position and also has the potential

of being placed in a worse financial position by losing something. The

best example of speculative risk is GAMBLING. Therefore, insurance

policies will NOT protect speculative risks.

2. Pure Risk: On the other hand, this risk is what insurance is all

about. It covers losses only, and does not imply that the insured can

�make money� after a covered loss. The goal of insurance is to place

the insured back into his/her financial position just prior to the loss.

Obviously, in the case of life insurance, the deceased cannot be replaced,

but instead, the insurance will provide financial stability to the family or

loved ones. In property and casualty, dollars are provided to replace

the lost/damaged property.

Hazard

A hazard is any factor or situation that increases or contributes to the probability

that a peril will occur, so as to increase the chance of a loss.

Types of Hazards

� Physical Hazard: A visible or tangible condition of the premises that

increases the chances of a peril occurring such as faulty wiring, slippery

floors, icy roads, gasoline cans, etc.

� Moral Hazard: Concerns the insured�s attempting to defraud the

insurance company through intentional and deliberate destruction of the

property, such as arson.

� Morale Hazard: Has to do with the insured�s indifference, carelessness,

laziness or lack of concern for the property, such as leaving your keys in

the car, smoking in bed, or exceeding the speed limit.

Peril

A peril is the immediate, specific cause of a loss. For example, if a home is

destroyed by a fire, the fire is a peril.

Policy Perils

� Property and casualty insurance policies are written in one of two ways

concerning the perils covered. The first are named perils and the

second type is known as all risk or open perils.

• Named perils lists the specific perils that it will cover.

Obviously, in order for the insured to collect, the specific loss

must be covered or the insured will not recover.

• On the other hand, an all risk or open perils policy covers all

risk of loss or all perils, except those that are specifically

excluded.

Loss

A loss is an unintended or unforeseen reduction or destruction of financial or

economic value. If an insured�s building burned to the ground, this event would

be considered a total loss because the value of the ashes would be drastically

different than the value of the building before the loss.

� Direct Loss is a loss which occurs directly through an �unbroken chain

of events� as a result of an insured peril. This is done without any

intervening cause.

� Indirect or consequential loss is a loss or damage which results

from a hazard or peril, but the loss was not actually caused by that hazard

or peril. These are losses which result from the actual physical loss itself.

• Example: A fire burns a clothing store to the ground. The

direct loss from the fire peril would be the total destruction

to the building and its contents. The indirect loss from the

fire peril would be the inability of the clothing store owner to

conduct business following the fire loss.

Proximate Cause of a loss is an action that, in a natural and continuous

sequence, produces the loss. This sequence is unbroken by any other factors or

events.

Example: Everyone eating catfish in a restaurant gets ill. Even though

these patrons did something else after leaving the restaurant, the fact is,

they were served food that was the proximate cause of the injury

(sickness).

Deductibles

In order to avoid minor claims, companies usually write deductibles into their

property contracts. This means that the insured must pay some portion of the

loss. Just like in health insurance, the insured will pay the deductible first, and

then the insurance company will pay the remainder of the claim within covered

limitations.

Indemnity

All property and casualty insurance contracts are contracts of indemnity and their

purpose is to make the insured �whole again�, or pay he/she back. The purpose

is to put the insured back into the same financial positions as he/she was, prior to

the insured loss.

Actual Cash Value (ACV)

Many losses are settled with the insurance company

on an actual cash value basis. This is usually

calculated by determining what the item would cost to replace (replacement cost)

and subtracting an amount for depreciation (use).

� The formula is ACV = Replacement Cost � (minus) Depreciation

� If the insured were paid the full replacement cost without deducting

anything for having used the insured item, the principle of indemnity

would be violated.

Replacement Cost (RC)

This is the exact amount of settlement needed to replace damaged or destroyed

property at the point the loss occurred, with one of like kind and quality. As

Example: Billy Bob bought a Z28 Camaro three years ago for $22,000.

Today, it has a book value of $7,000. According to the principle of indemnity, the

depreciation is not a factor, this represents a departure from indemnity rules.

Limit of Liability

These limits represent the maximum amount the insurance company will pay for

a loss. Within this framework, the principle of indemnity and applicable policy

conditions are used to determine the exact reimbursement, in the event of a loss.

The limits of liability are found on the Declarations page.

Coinsurance

This feature encourages policyholders to insure property to value. Coinsurance

is found in many property policies in order to require policy holders to carry

adequate insurance on their property at the time of loss. A coinsurance clause is

an agreement between the insurer and insured in which:

� The insurer agrees to charge a reduced premium rate for coverage.

� The insured agrees to carry a specified percentage of the replacement

cost of the building.

A typical coinsurance clause of a property policy will state that an insured has to

satisfy an 80% level. This means that the insured must carry insurance equal to

at least 80% of the value of the insured property.

If the coinsurance clause is satisfied, partial losses will be paid in full. If the

coinsurance clause is not satisfied, partial losses will be subject to a penalty

payment.

Extensions of Coverage

Extensions of coverage are really additional coverages that would apply in an

insurance policy. These may have reduced or separate limits of liability or require

the insured to meet certain policy requirements before they apply.

Additional Coverages

These are similar to extended coverages, as they offer some additional policy

coverage under certain conditions. Some examples will be discussed in later

chapters of this workbook.

Accident vs. Occurrence

Property and casualty contracts are usually written in two ways:

Accident

An accident is a sudden, unexpected, unforeseen event resulting in

financial loss.

� Examples

•Man trips on a cracked sidewalk.

•A truck hits a car.

•Lightening strikes a house, causing a fire.

Occurrence (very close to an accident)

An occurrence is a sudden, unexpected, unforeseen event resulting in

financial loss, including repeated and continuous exposure to conditions.

� Examples

• Industrial waste gradually pollutes a river.

•An insured worker gradually becomes ill due to repeated

handling of asbestos on the job.

Cancellation

Either the insured or insurer may cancel provided coverage. Each property and

casualty policy details the reasons for which the insurer can cancel the policy. Of

course, these reasons must be in compliance with individual state laws. While

the insurance company must give some specified written notice required by the

state, the insured, on the other hand, can request immediate cancellation,

without any notice.

If the insurance company cancels the policy, any unearned premium will be

returned on a pro rata basis. There is no allowance for deductions, such as

service fees. This allows the insured to get back all of the money which has not

been used or applied to premium cost.

If the insured cancels the policy any unearned premium will be returned on a

short rate basis (with deductions made for servicing the policy, etc.) With the

short rate basis, the insurance company can recoup some of the costs of

underwriting and policy processing.

If either the insured or the insurance company cancels the policy on its effective

date, this is known as a flat cancellation, with no return of premium or service

fees.

Nonrenewal

This is the act of terminating an insurance policy after the specified policy period.

Nonrenewal is a notice given by the insurance company to the insured, indicating

the intention not to renew the policy upon the normal termination date. There

may be, however, some limitations on the insurance company for nonrenewal.

Vacancy and Unoccupancy

Vacancy refers to a building which is unfurnished and not being used as a

dwelling or for a business.

Unoccupancy refers to a building which is furnished, but not being used as a

dwelling or for business.

� Insurance policies treat these differently, so make sure you

understand the differences and analyze the questions carefully.

Right of Salvage

When an insurance company settles a claim, it owns a right to salvage the

property that has only been partially damaged or been destroyed, but still has a

salvage value.

� The insurance company can reduce its losses in the matter by selling

the salvage to a salvage dealer.

� It may determine whether or not property will be repaired, replaced

or cash will be provided.

� In situations where an insured property is not completely destroyed,

the insurance company may take possession of it and receive its

salvage value when it has replaced or has made a cash settlement

to the insured party.

Abandonment

An insured cannot be allowed to abandon the insured property and then demand from the insurance company to be paid in full. The insurance company, by

contract, has the right to settle the loss by payment, repair or outright

replacement of the property involved.

Liability

Liability insurance is meant to protect people against financial loss arising out of

liability claims by transferring the burden of financial loss from the insured to the

insurance company.

Negligence

Negligence is also known as an unintentional Tort (act). Failure to do what a

reasonable person would do under similar circumstances.

� Was there a legal duty to act or not to act?

� Was there a breach of that duty?

� Was there injury or damage to another person?

� Was the act the proximate cause of the damages?

If all the questions can be answered with a yes, then a case for negligence can

be made and typically, insurance companies will pay for the covered losses.

(Compared to intentional acts, which would probably NOT be covered)

Lesson 1 Review Questions 1. The purpose of insurance is to: A. Pay for all losses. B. Spread risk amongst others. C. Guarantee against any possible losses. D. Share risks with all the other insureds. 2. Which of the following is NOT a part to a legal contract? A. Declarations B. Insuring agreement C. Exclusions

D. Ex part fixio 3. Which part of a legal contract states the losses for which the insured will be indemnified? A. Declarations B. Insuring agreement C. Exclusions D. Definitions 4. Which of the following must an insured have at the time of loss? A. A car B. An open checking account C. An insurable interest in the property D. A certified page of Declarations 5. Which type of risk is insured against? A. Speculative risk B. Pure risk C. Grand Victoria losses D. Hazard risks 6. Which of the following is NOT a hazard? A. Physical B. Moral C. Mental D. Morale 7. If a home is destroyed by a fire, the peril is: A. The evil match B. The evil gasoline C. The fire D. The charcoal 8. Which of the following lists the perils that a policy will cover? A. Direct B. Named C. All risk D. Open 9. An action, through an unbroken series of events, that can be determined to be the immediate or actual cause of the loss is the: A. Proximate cause B. Negligent cause C. Indemnity cause D. Peril cause

10. Property and casualty insurance contracts are contracts of: A. Proximate cause B. Negligent cause C. Indemnity D. Total reimbursement 11. How much is the ACV, if the replacement cost of the property insured is $100,000 and depreciation is $5,000? A. $100,000 B. $105,000 C. $ 95,000 D. $110,000 12. Which of the following is NOT true regarding a coinsurance feature of a policy? A. The insurer agrees to charge an increased premium rate for coverage. B. The insured agrees to carry a specified percentage of the replacement cost of a building. C. A typical coinsurance clause usually requires an 80% coinsurance. D. The insurer agrees to charge a decreased premium rate for coverage. 13. What refers to a building which is unfurnished and not being used as a dwelling or a business? A. Vacancy B. Unoccupancy C. Salvage D. Renewal 14. Which of the following is defined as a sudden, unexpected, unforeseen event resulting in financial loss? A. Occurrence B. Accident C. Coverage D. Negligence 15. Which of the following is true regarding the cancellation of a property policy? A. The insured alone cannot cancel the policy. B. The insurer alone cannot cancel the policy. C. Both the insurer and insured must cancel the policy at the same time. D. Either the insurer or insured can cancel the policy. 16. If an insurance company cancels the policy, any unearned premium will be returned on a: A. Full basis B. Pro rata basis

C. Short rate basis D. Retroactive basis 17. If the insured cancels the policy, any unearned premium will be returned on a: A. Full basis B. Pro rata basis C. Short rate basis D. Retroactive basis 18. What is the term given to the act of terminating an insurance policy after the specified policy period? A. Nonrenewal B. Vacancy C. Salvage D. Renewal 19. What refers to a building which is furnished, but not being used as a dwelling or for business? A. Salvage B. Vacancy C. Unoccupancy D. Abandonment 20. Which of the following is known as an unintentional tort? A. Proximate cause B. Liability C. Negligence D. Abandonment

Lesson 1 Review Answers

1. (B) The purpose of insurance is to spread risk amongst others and is intended to provide a practical solution to economic uncertainties and unexpected losses. It can also be defined as a social device for handling risk by transferring it. 2. (D) A legal insurance contract includes Declarations (name of the insured, address, amount of coverage, description of the property, cost of the policy); Insuring agreement (what is to be covered); Conditions (responsibilities and obligations of both the insurance company and the insured); Exclusions (losses for which the insured is not covered); and Definitions (clarifies the meaning of certain terms). 3. (B) The Insuring Agreement is the portion of the insurance contract that identifies what losses the insured will be covered for; in other words, the losses for which the insured will be indemnified.

4. (C) At the time of loss, the insured must have an insurable interest in the property. It is important to note that it is at the time of a loss when the insured must have an insurable interest as it relates to property and casualty insurance, whereas in Life and Health policies, an insurable interest must be present at the time of the application. 5. (B) Only pure risks can be insured against. Insurance contracts are contracts of indemnity, not profit makers. The goal of insurance is to place the insured back into his/her financial position just prior to the loss. 6. (C) Moral, morale and physical hazards are all types of hazards dealing with property and casualty insurance. Mental hazards are not considered in P&C coverage. 7. (C) Since a peril is the immediate, specific cause of loss, in the circumstance that a house is destroyed by fire, the fire is the peril. Regardless if a match or gasoline started the fire, they are not ultimately was destroyed it. 8. (B) Perils that are covered in a policy are called Named perils. These are the specific perils that, in order for the insured to collect, must be covered or the insured will not recover. 9. (A) A proximate cause of a loss is an action that, in a natural and continuous sequence, produces the loss. This sequence is unbroken by any other factors or events. For example, everyone eating catfish in a restaurant gets ill. Even though these patrons did something else after leaving the restaurant, the fact is, they were served food that was the proximate cause of the injury (sickness). 10. (C) P&C contracts are indemnity contracts, meaning their purpose is to make the insured �whole again�, or pay he/she back. The purpose is to put the insured back into the same financial positions as he/she was, prior to the insured loss. 11. (C) Actual Cash Value (ACV) is determined by the replacement cost less depreciation. In this case, the replacement cost ($100,000) minus the depreciation ($5,000) equals an ACV of $95,000. 12. (A) A coinsurance clause is an agreement between the insurer and insured in which the insurer agrees to charge a reduced premium rate for coverage. This means that the insured must carry insurance equal to at least 80% of the value of the insured property. If the coinsurance clause is satisfied, partial losses will be paid in full. If the coinsurance clause is not satisfied, partial losses will be subject to a penalty payment. 13. (A) Vacancy refers to a building which is unfurnished and not being used as a

dwelling or for a business. 14. (B) An accident is a sudden, unexpected, unforeseen event resulting in financial loss. This is opposed to an occurrence, which is similar in definition except it includes repeated and continuous exposure to conditions. Accident: A truck hits a car. Occurrence: waste gradually pollutes a river 15. (D) Either the insured or insurer may cancel provided coverage. Each property and casualty policy details the reasons for which the insurer can cancel the policy. Of course, these reasons must be in compliance with individual state laws. While the insurance company must give some specified written notice required by the state, the insured, on the other hand, can request immediate cancellation, without any notice. 16. (B) If the insurance company cancels the policy, any unearned premium will be returned on a pro rata basis. There is no allowance for deductions, such as service fees. This allows the insured to get back all of the money which has not been used or applied to premium cost. 17. (C) If the insured cancels the policy any unearned premium will be returned on a short rate basis (with deductions made for servicing the policy, etc.) With the short rate basis, the insurance company can recoup some of the costs of underwriting and policy processing. 18. (A) Nonrenewal is the act of terminating an insurance policy after the specified policy period. Nonrenewal is a notice given by the insurance company to the insured, indicating the intention not to renew the policy upon the normal termination date. There may be, however, some limitations on the insurance company for nonrenewal. 19. (C) Unoccupancy refers to a building which is furnished, but not being used as a dwelling or for business. Vacancy, on the other hand, refers to a building which is unfurnished and not being used as a dwelling or for a business. 20. (C) An unintentional tort is known as negligence. This is failure to do what a reasonable person would do under similar circumstances. If a case for negligence can be made, typically insurance companies will pay for the covered losses.

Lesson 2: Types of Policies

Personal Lines

Personal lines are types of insurance written for individuals, rather than

businesses, for which the term commercial lines apply.

Dwelling and Contents

The Dwelling policy provides protection for individuals and families against loss

to their dwelling and personal property.

� The Dwelling policy provides more limited Property coverage than the

Homeowners� policy, which will be reviewed in another Chapter.

� The unendorsed (not part of a basic policy) Dwelling policy provides

Property coverage only, while the Homeowners policy provides a package

of Property and Liability coverage.

Dwelling property forms are used to provide coverage for the following types of

personal residences:

� One, two, three and four family homes and apartment houses.

� Dwellings up to five roomers or boarders.

� Permanently installed mobile homes or trailers.

� Insure homes that do not qualify for Homeowners insurance such as

rentals.

� The Dwelling policy covers the named insured and his or her spouse, as

long as the spouse lives in the same household as the insured.

Basic Form (DP-1)

This Basic Form provides the following coverages:

� Coverage A � Dwelling

•Dwelling.

•Structures attached to the dwelling.

•Materials and supplies used to repair the dwelling or other

structures.

� Coverage B � Other structures

• Insures buildings on the premises, but not in contact with the

dwelling.

•Cannot be used for commercial, manufacturing or farming.

� Coverage C � Personal Property

• Insured�s personal property.

•Personal property belonging to the insured�s guests or

servants.

•The following items are NOT covered:

� Money, coins and securities.

� Paper and computerized accounting records.

� Software media.

� Credit cards.

� Animals including birds and fish.

� Aircraft.

� Motor vehicles other than motorized equipment used to

maintain the property.

� Boats, other than rowboats and canoes.

� Coverage D � Fair Rental Value

• If the loss to the dwelling makes it uninhabitable, and the

insured cannot collect the rent he or she would have been

able to receive if the loss had not occurred.

•10% of the insurance on the dwelling is available for this

coverage.

Perils Insured Against

A peril is the cause of the loss such as fire, wind or vandalism.

� Perils that are automatically covered under the Basic form are fire,

lightning and internal explosion.

� Internal explosion is an explosion that occurs in an insured covered

building or in a building containing covered personal property.

� Typical losses covered would include the explosion of a furnace,

stove or hot water heater.

� Steam explosions are excluded if the equipment is owned, leased or

operated by the insured.

Extended Coverage Perils

The insured may choose to be covered against a list of additional perils

that are sometimes called the Extended Coverage perils. While these perils

are already printed in the DP-1 form, no coverage applies until the insured

pays the additional premium.

The following Extended Coverages (EC) can be added on:

� Windstorm: Direct action of the wind, including objects hurled

by the air that cause damage.

� Civil Disorder: An uprising or disturbance by a large number of

persons.

� Smoke: Only smoke from a hostile fire would be covered. This EC

broadens the smoke peril to any sudden, accidental damage from smoke.

� Hail: Direct action of hail to the insured�s property.

� Aircraft: Damage caused by aircraft, including self-propelled

missiles, spacecraft, helicopter, etc. This includes the falling of

an aircraft or parts of an airplane.

� Vehicles: Provides protection for any damage caused by a vehicle,

unless it is owned by the insured. Also, does not include

damage to fences or driveways.

� Explosion: Covered, whether they originate inside or outside

the building including:

•Bursting water pipes

•Electrical arching

•Rupture, bursting or pressure reduction devices

•Steam boilers or pipes

� Riot: Direct loss caused by striking employees. Riot and civil

commotion are very close in definition.

Volcanic Eruption

Losses caused other than by earthquake, land

shock waves or tremors.

This peril covers damage caused by the eruption of

a volcano, including

the ensuing lava flow and airborne particles.

Vandalism and Malicious Mischief (V&MM)

Includes any willful and malicious damage or destruction, except theft and

glass breakage. These acts must be intentional to be covered. This coverage

is included automatically with the DP� 2 Broad Form.

Test Clue: Try using the Acronym � W C S H A V E R to help remember the above Extended Coverage Perils.

Other Coverages

In addition to insuring against the listed perils, the Dwelling Basic form

provides the additional following coverages:

� Other Structures: This provides up to 10% of Coverage A to

cover losses of other structures. (Basic policy coverage)

� Debris Removal: Pays for the expense of removing debris resulting

from a loss that is covered by the policy.

� Property Removed: Covers loss to property that occurs while

the property is being removed to protect it from a covered peril.

� Reasonable Repairs: This pays for the reasonable costs to

make necessary repairs to protect property from further damage

following a covered loss.

� Improvements, Alterations and Additions: Provides coverage

for insureds who are tenants for improvements or alterations to

the dwelling made at the tenant�s expense. Up to 10% of the

coverage C limit is available.

� Fire Department Service Charge: Pays up to $500 for fire

department charges incurred when the fire department is called.

NO deductible applies.

� Worldwide Coverage: Provides 10% of the Coverage C limit

for personal property while it is located anywhere in the world

such as clothes taken on a vacation.

� Rental Value: Provides 10% of Coverage A limit for loss of fair

rental value, payable at 1/12th of the 10% limit for each month

the described location is unfit for its normal use. (Basic policy

coverage)

Exclusions under DP-1 (What�s not covered)

� Water damage in general, including flooding, water backups into

a building or seeping from below the ground.

� Losses resulting from earth movement, except for direct loss by

fire or explosion resulting from earth movement.

� Losses due to power disruption occurring away from the insured�s

location.

� War.

� Nuclear hazard.

� Losses caused by the insured or by someone else at the insured�s

direction.

� Replacing regular glass with safety glass.

� Losses resulting from ordinances or laws that require more expensive

reconstruction or demolition.

How Will Losses Be Paid, Settled or Treated? (Terms to

know)

Loss Settlement

Covered property losses are valued at actual cash value, but not to exceed

the amount necessary to repair or replace.

Our Option

Gives the insurer the right to repair or replace damaged property with the

equivalent property within 30 days of receiving the insured�s statement

of loss.

Pair or Set

This clause in a policy will explain how a claim should be handled when

one item of a pair or set is damaged. Loss of an article which completes

a pair or set is handled as a unique claims settlement problem.

The following options may be used when these circumstances arise:

� Repair or replace any part to restore the pair or set to its value before

the loss.

� Settle by paying the difference between the actual cash value of the

set before and after the loss.

Deductibles

This clause is located in the Declarations and states

that only the amount

of loss over the deductible will be paid, up to the

limit of liability.

Other Insurance

If a loss is also covered by other insurance, the insurance company will

pay only its proportion of the loss.

Loss Payment

The loss will be paid within 30 days after reaching an agreement with the

insured.

Recovered Property

If the insured or insurer recovers property on which the insurer has made

loss payment, the other party must be notified. The insured may have the

property returned, in which case, the loss payment will be adjusted, or allow

the company to have it.

For Those Who Want Additional Dwelling Coverage

Example: Let�s assume that Diane owns a pair of earrings designed especially for her. Each earring is worth $1,000, but the pair is worth $5,000. Assume that one earring was destroyed by fire. Her loss is

What if the coverage under the Basic Form (DP-1) isn�t enough? What if insured

wants additional protection? Well, for those who want broader Dwelling

coverage, there are two other Dwelling forms available. They are:

� Broad form (DP-2)

� Special form (DP-3)

Coverage E (Additional Living

Expenses Found in DP-2 and DP-3)

� Pays for additional living expenses after a covered

loss

� Includes reasonable motel, dining, laundry and transportation expenses

� Covered for the time needed to repair or replace the damaged property or

become settled elsewhere in permanent quarters

� Coverage E can be added to the DP-1 by endorsement (extra premium)

Broad Form (DP-2)

While the Basic form named specific perils, so does the Broad form (DP-2). It

includes all those in DP-1, as well as some additional perils. Some of the

additional perils included in the DP-2 are as follows:

Important Note: All three Dwelling forms, DP-1, DP-2 and DP-3 provide the basic policy coverages with Coverage A, B, C and D. However, DP-2 and DP-3 also provide an additional coverage known as Coverage E.

� Burglar damage

� Ice and snow weight

� Glass breakage

� Accidental discharge

� Falling objects

� Freezing of pipes

� Electrical damage

� Collapse

� Tearing apart

Note the acronym to help you remember: BIGAFFECT

Additional Coverage Definitions

Burglar Damage

This covers damage done to the property, but not to any property stolen.

Ice

Protection is provided from falling objects such as ice, snow and sleet. Damage

to the insured building and/or contents due to their weight is covered.

Coverage does not extend to the following:

� Awnings

� Fences

� Patios

� Pavements

� Swimming pools

� Foundations

� Retaining walls

� Bulkheads

� Wharves

� Docks

� Piers

Glass Breakage

All building glass, as long as the insured premises has not been vacant for 30

consecutive days or more immediately before the loss.

Accidental Discharge

Accidental discharge of water and steam from plumbing, heating, air-conditioning

or fire protective sprinkler systems, or of a household appliance.

This does not include losses due to continuous leakage or seepage. No

coverage for a building unoccupied for more than 30 consecutive days

immediately before the loss or to the system or appliance causing the water or

steam escaping.

Falling Objects

Covers damages to the exterior of the insured premises and its contents, if the

falling object first damages the roof or exterior wall. Damage to the falling object

itself is not covered. Outdoor antennas, wiring, equipment, awnings and

fences are not covered.

Freezing of Pipes

Losses are not covered if the dwelling is vacant, unoccupied or being

constructed, unless the insured has taken reasonable care to:

� Maintain heat in the building

� Shut off the water supply and drain the system

Electrical Damage

Coverage from sudden and accidental electrical current.

Collapse

The collapse peril covers risk of direct physical loss to covered property involving

collapse of a building or any part of it caused by:

� Perils insured against in the policy

� Hidden decay

� Insect damage

� Weight of contents

� Weight of rain or snow collected on the roof

� Use of defective materials

Collapse coverage does not cover damage due to:

•Settling

•Cracking

•Shrinking

•Bulging

•Expansion

The following structures and �things� are excluded from coverage:

•Awnings

•Fences

•Patios

•Swimming pools

•Underground pipes, drains and septic tanks

•Foundations

Tearing Apart

Sudden and accidental tearing apart, cracking, burning or bulging of

steam or hot water heating systems, air-conditioning, or automatic fire protective

sprinkler systems, or hot water heaters. This peril does not include

loss caused by freezing, except as provided in the peril of freezing.

Additional Available Coverage with DP-2 and DP-3 (Not

available with DP-1)

� Trees, shrubs and other plants: Pays up to 5% of the Coverage A limit

for damage to trees, shrubs, plants or lawns caused by a specified list of

perils. There is a $500 maximum for damage to any one tree, shrub or

plant.

� Collapse: Pays for the collapse of the dwelling caused by a specified list

of perils.

� Glass or Safety Glazing Material: Pays for the breakage of glass or

safety glazing material and damage to covered property caused by glass

breakage.

Special Form (DP-3)

This is an all risk or open perils policy, unlike DP-1 and DP-2, which are written

on specific perils. DP-3 is defined by its exclusions. If a peril is not specifically

excluded, then it is included for coverage. If contents (Personal Property) are

covered under DP-3, they are insured against the same perils as provided under

the DP-2. In other words, DP-3 provides All Risk or Open Perils coverage on

the dwelling and other structures, and Broad Form coverage on personal

property or contents.

REVIEW CHART ON DWELLING PROPERTY FORMS

(Perils covered for Dwelling Owner)

DP-1 Basic Form

DP-2 Broad Form

DP-3

Special Form

FIRE

LIGHTNING

INTERNAL

EXPLOSION

plus

EXTENDED COVERAGE

• Windstorm • Civil commotion • Smoke • Hail • Aircraft • Vehicles • Volcanic eruption • Explosion • Riot • Vandalism • Malicious

i hi f

FIRE

LIGHTNING

INTERNAL

EXPLOSION

plus

EXTENDED COVERAGE

plus

BROAD FORM

ADDITIONAL PERILS • Burglar damage • Ice & snow

weight • Glass breakage • Accidental

discharge

ALL RISK ON

DWELLING

with

BROAD FORM (DP-2)

PERILS ON

PERSONAL

PROPERTY

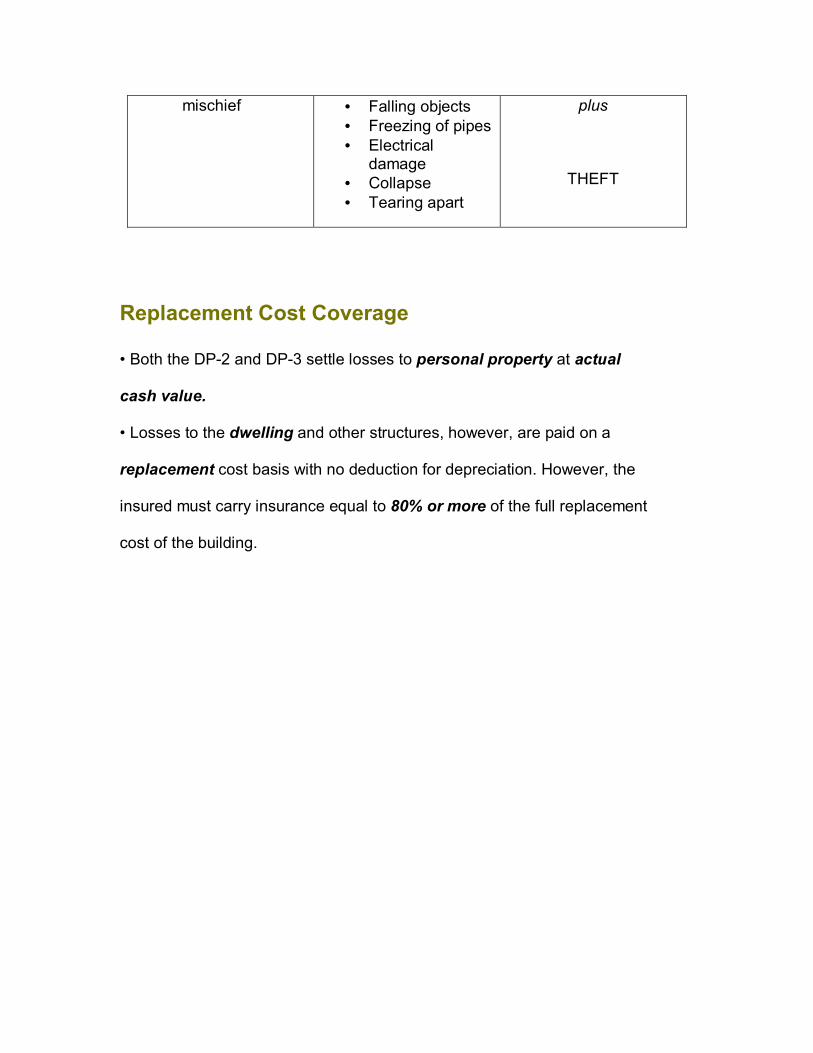

mischief

• Falling objects • Freezing of pipes • Electrical

damage • Collapse • Tearing apart

plus

THEFT

Replacement Cost Coverage

� Both the DP-2 and DP-3 settle losses to personal property at actual

cash value.

� Losses to the dwelling and other structures, however, are paid on a

replacement cost basis with no deduction for depreciation. However, the

insured must carry insurance equal to 80% or more of the full replacement

cost of the building.

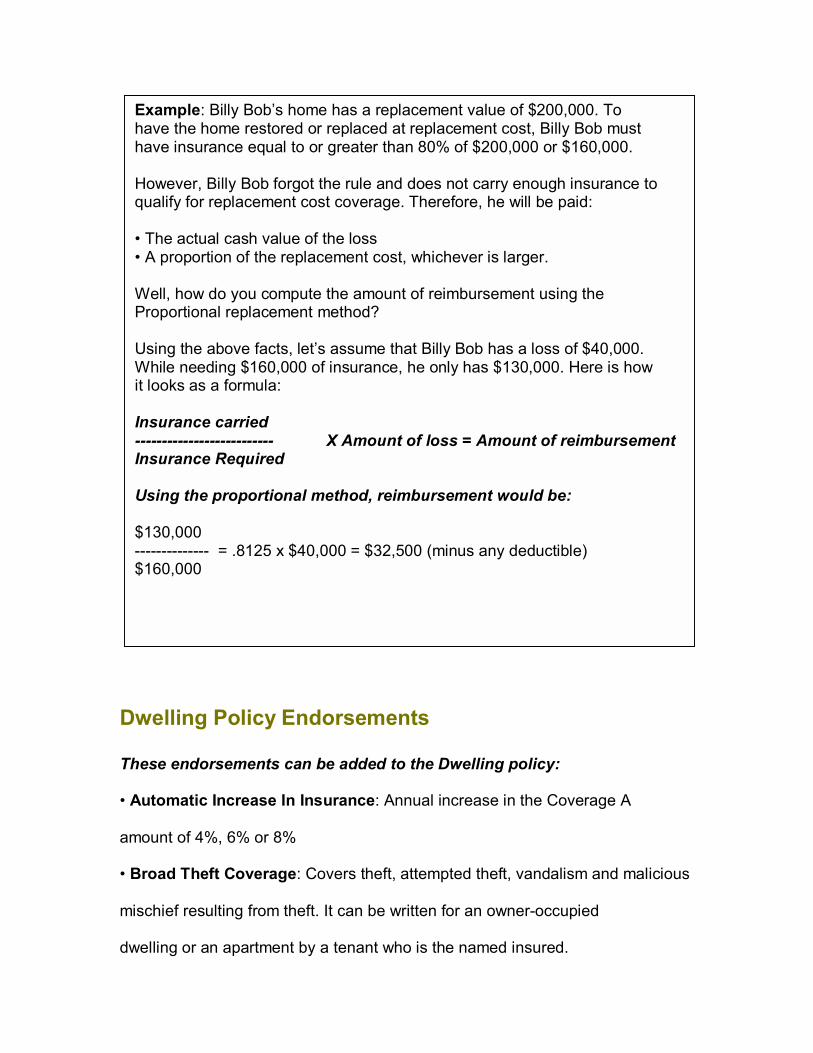

Dwelling Policy Endorsements

These endorsements can be added to the Dwelling policy:

� Automatic Increase In Insurance: Annual increase in the Coverage A

amount of 4%, 6% or 8%

� Broad Theft Coverage: Covers theft, attempted theft, vandalism and malicious

mischief resulting from theft. It can be written for an owner-occupied

dwelling or an apartment by a tenant who is the named insured.

Example: Billy Bob�s home has a replacement value of $200,000. To have the home restored or replaced at replacement cost, Billy Bob must have insurance equal to or greater than 80% of $200,000 or $160,000. However, Billy Bob forgot the rule and does not carry enough insurance to qualify for replacement cost coverage. Therefore, he will be paid: � The actual cash value of the loss � A proportion of the replacement cost, whichever is larger. Well, how do you compute the amount of reimbursement using the Proportional replacement method? Using the above facts, let�s assume that Billy Bob has a loss of $40,000. While needing $160,000 of insurance, he only has $130,000. Here is how it looks as a formula: Insurance carried -------------------------- X Amount of loss = Amount of reimbursement Insurance Required Using the proportional method, reimbursement would be: $130,000 -------------- = .8125 x $40,000 = $32,500 (minus any deductible) $160,000

Property is covered while it is on or off the premises.

� Dwelling under Construction: When the intended occupant of a dwelling

under construction is the named insured, this endorsement is attached

to the Dwelling policy to provide coverage.

•The limit of liability that applies at any given time is a percentage of

the policy limit based on the value of the partially completed dwelling.

•The available policy limit increases as construction of the dwelling

progresses.

Personal Liability

The insured may purchase Personal Liability and Medical Payments to

Others Coverage as an endorsement to the Dwelling policy. These coverages

can also be purchased as a separate policy. You also need to know that these

coverages are very similar to those provided in the Liability section of the

Homeowners policy, which will be covered in the next Section.

Personal Liability � Coverage L

� Coverage for damages that the insured becomes legally obligated

to pay because of bodily injury or property damage caused by an

occurrence for which there is coverage.

� The insurer will also defend the insured against such claims at its

own expense, even if the suit is groundless or fraudulent.

� The policy limit is $100,000.

Medical Payments to Others � Coverage M

� The insurance company will pay all necessary medical expenses

incurred within three years of an accident that causes bodily injury.

� Coverage applies to injuries:

•While the injured party is on the insured location with the

insured�s permission.

•Sustained while the injured party is off the insured location, if

the injury arises out of a condition:

! On the insured location.

! Caused by an animal in the insured�s care.

! Caused by the activities of the insured.

� There is a policy limit of $1,000 per person.

� The insured does not have to be legally liable for coverage to apply.

� Coverage does not apply to any injury sustained by the insured or

the insured�s family members.

Homeowner (HO forms)

Homeowners policies allow property owners to select the contract that most

closely fits their needs and their ability to pay. There are five Homeowners

policies. While each has some unique characteristics, they all share at least one

common attribute. Each package contains property (fire) and casualty

(personal liability and theft). This places the needs of the consumer into one

contract, thus creating a multi-line policy.

In the modern Homeowners contract, Section I contains the property coverages

and Section II provides coverage for legal liability. Section I will vary according to

the HO form, while section II will be identical in all forms.

The five Homeowners forms are:

� HO-2 Broad

� HO-3 Special

� HO-4 Tenant (or contents) Form

� HO-6 Condominium or unit owner

� HO-8 Modified Coverage

HO-2 (Broad form)

� Provides broad coverage for direct physical loss caused by:

•Fire

•Lighting

• Internal Explosion

•Extended Coverage Perils (EC)

•Vandalism & Malicious Mischief (VMM)

•Broad Form Additional Perils ( BIGAFFECT )

HO-3 (Special form)

� Provides open peril coverage for direct physical loss caused by:

•All Risk or Open perils on the dwelling and other structures.

•HO-2 perils on the personal property (contents).

•Theft.

HO-4 (Tenants form)

� Designed for tenants of apartments.

� Provides broad coverage for personal property.

� Similar coverage to the HO-2s and HO-3s broad coverage for personal

property.

� No coverage for the dwelling.

HO-6 (Condominium form)

� Like the HO-4, the HO-6 is designed to insure personal property of

condominium owners.

� Similar coverage to that provided under the HO-2, HO-3 and HO-4.

� Provides very limited dwelling coverage.

HO-8 (Modified Coverage form)

� Designed for older homes.

� Replacement values may far exceed market values.

� Basic coverage on the dwelling and personal property.

� Similar to the DP-1 with EC perils and V&MM coverage.

� Has restrictions on valuation of losses.

� Generally not available today.

REVIEW CHART ON HOMEOWNERS PROPERTY FORMS

(Perils covered for Homeowners)

HO-2 Broad Form

HO-3 Special Form

HO-4 Tenant or Renter

HO-6 Condominium

unit owner

• Fire • Lightning • Internal

explosion

plus

EXTENDED COVERAGE

plus

BROAD FORM

ADDITIONAL PERILS:

Burglar damage Ice & snow

weight Glass breakage

Accidental discharge

Falling objects Freezing of pipes

Electrical damage

Tearing apart

ALL RISK ON DWELLING

with

BROAD FORM

perils on personal property

plus

THEFT

BROAD FORM ON PERSONAL

PROPERTY ONLY

Same as HO-4

with BROAD FORM ON PERSONAL

PROPERTY ONLY

BROADER

ADDITIONS AND ALTERATIONS

Policy Sections of an HO Policy

Section I � Property

Section l (Property) of a Homeowners policy subdivides the property insured into

four distinct coverages:

� Coverage A � Dwelling

� Coverage B � Other Structures

� Coverage C � Personal Property

� Coverage D � Loss of Use

Coverage A � Dwelling

� Covers the dwelling, structures attached to the dwelling as well as materials

and supplies located on or next to the dwelling which is being used for

construction, alteration or repair.

Example: The insured installs built-in cabinets, vanities and wall to wall carpet.

These items are generally not considered contents and would be covered

only as alterations and additions to the dwelling.

Coverage B � Other Structures

� Provides protection for structures on the premises which are detached from

the dwelling. (e.g., tool shed and garage).

� Coverage does not apply to land or structures used for business or rented to

anyone other than a tenant of the dwelling unless it is a garage.

� HO-4 does NOT include Coverage A or Coverage B since renters and

tenants can only insure their personal property.

� HO-6, the Condominium form, includes limited Coverage A for:

o Alterations, appliances, fixtures and improvements that are part

of the building containing the residence premises.

o Property that is the insured�s responsibility under a condo association

agreement.

o Items of real property pertaining solely to the residence premises.

o Structures other than the personal residence owned solely by

the insured at the location of the residence premises.

� The standard Coverage A limit for the HO-6 is $1,000.

Coverage C � Personal Property

� Provides protection for personal property, which is owned or used by the

insured anywhere in the world.

� Coverage is extended to personal property at a secondary residence.

� Coverage for personal property is available for property owned by others as

well as guests or residence employees at the insured�s option if the premises

is occupied by the owner, guests or residence employee.

� Coverage is up to 10% of the Coverage C limit or $1,000, whichever is

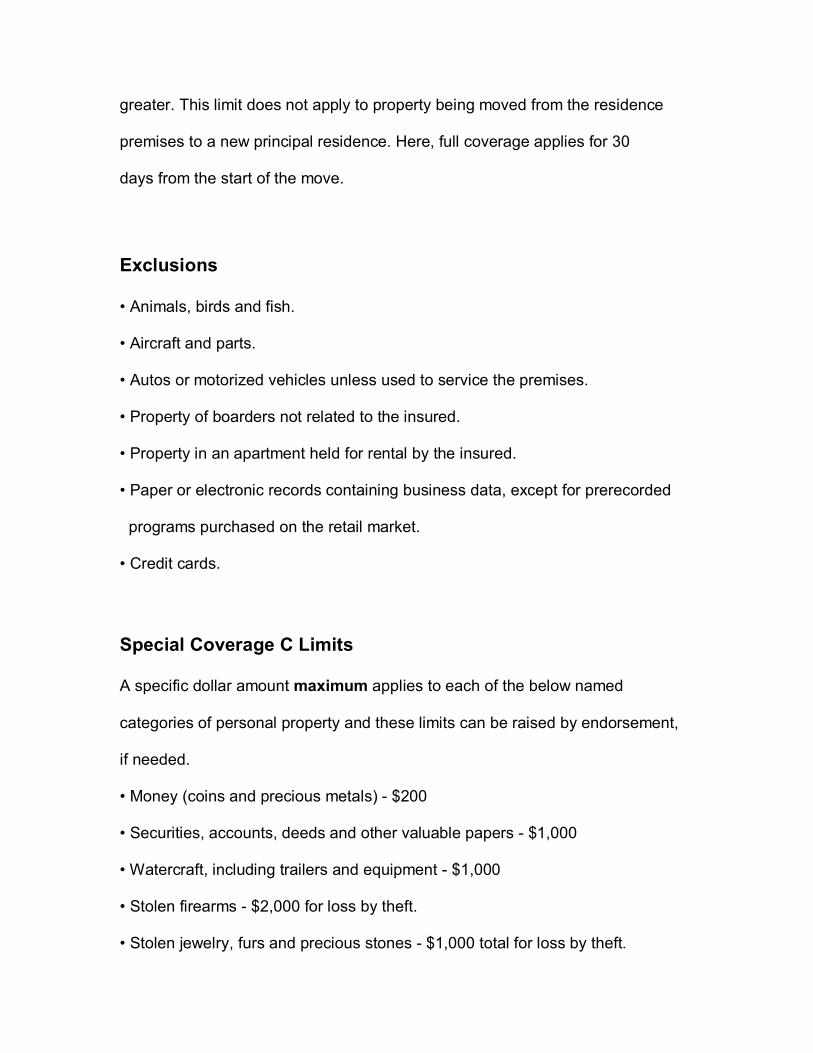

greater. This limit does not apply to property being moved from the residence

premises to a new principal residence. Here, full coverage applies for 30

days from the start of the move.

Exclusions

� Animals, birds and fish.

� Aircraft and parts.

� Autos or motorized vehicles unless used to service the premises.

� Property of boarders not related to the insured.

� Property in an apartment held for rental by the insured.

� Paper or electronic records containing business data, except for prerecorded

programs purchased on the retail market.

� Credit cards.

Special Coverage C Limits

A specific dollar amount maximum applies to each of the below named

categories of personal property and these limits can be raised by endorsement,

if needed.

� Money (coins and precious metals) - $200

� Securities, accounts, deeds and other valuable papers - $1,000

� Watercraft, including trailers and equipment - $1,000

� Stolen firearms - $2,000 for loss by theft.

� Stolen jewelry, furs and precious stones - $1,000 total for loss by theft.

� Stolen silverware, goldware or pewterware - $2,500

� Property on the premises used for business purposes - $250

� Loss of portable electronic apparatus in, on or away from autos. This

would include a car phone or portable CD player provided the device can

be operated by both the vehicle�s power and other power sources - $1,000

Coverage D � Loss of Use

This coverage reimburses for additional living expenses and fair rental value

when the insured premises is unfit to live in. The coverage pays the additional

costs related to living elsewhere and the fair rental value of the insured premises.

Coverage D limits are written as a percentage of Coverage A under the HO-2,

HO-3 and HO-8; and a percentage of Coverage C under the HO-4 and HO-6.

Note: Other additional coverages available include:

� Inflation Guard Endorsement, which automatically increases the

coverages under A, B, C and D on a regular periodic basis

� Replacement Cost for Personal Property that will pay for the full cost

of the repair or replacement of the damaged personal property, as a rider

to all HO policies.

Property Not Available for Replacement Cost:

•Antiques and fine art

•Souvenirs and collector items

•Articles outdated or obsolete

•Articles not in good condition

Section l � Additional Coverages:

All Homeowners forms provide additional coverages in addition to the major

Section l � Coverage A through D, but costing no additional premium, unless

otherwise noted.

� Debris removal: If a covered peril causes a loss, pays for removal of debris.

Debris removal is included in the limit of liability applying to the damaged

property. If that limit is exceeded, then an additional 5% of the limit of liability

is paid.

� Cost of reasonable repairs: Pays to protect the property temporarily from

further damage.

� Trees, shrubs and plants: Pays, if on the residence premises for losses

caused by covered perils � up to 5% but no more than $500 per tree, shrub or

plant.

� Fire department service charges: Pays up to $500 when the fire department

is called to fight a covered peril.

� Property removed: Covers property against direct loss from any peril while

being removed from a premise endangered by a covered peril, and for up to

30 days while removed.

� Credit card forgery and counterfeit money: Pays up to $500 due to the

theft or unauthorized use of an insured check or negotiable instrument. Also

covered is protection against forgery of any check as well as losses sustained

because of unknowingly accepting counterfeit currency.

� Loss assessment: Pays up to $1,000 charged by a corporation or association

for a direct insured loss to property owned by all members collectively.

� Landlord�s furnishings: Pays up to $2,500 for the insured�s (as landlord)

appliances, carpeting and other household furnishings in an apartment on the

residence premises.

Section l � Additional Coverages Exclusions:

•Ordinance or law

•Earth movement

•Water damage

•Power failure

•Neglect

•War

•Nuclear hazard

• Intentional loss by, or directed by an insured with the intent to cause

loss

Earthquake Coverage

Earthquake coverage for homes can be added by endorsement, as HO policies

generally exclude coverage for these losses. Costs are based on construction

of the home. Frame houses are less expensive than masonry.

Section l � Additional Conditions of the Policy

� Limits of liability is the maximum amount the insurance company will pay for a

particular loss or for losses sustained during a period of time. This is also

known as the Policy Limit and Limits of Coverage.

� After a loss the insured must notify the company or agent promptly, notify the

police in the event of a theft, notify the credit card company, take reasonable

steps to protect the insured property from further damage, make reasonable

and necessary repairs to protect the property, keep records of repairs, prepare

an inventory of damaged personal property, cooperate with the company

by showing damaged property and records and submit a proof of loss

within 60 days of the insurer�s request.

� Loss settlement rules in which personal property losses are settled on an

actual cash value (ACV) basis while buildings insured under Coverages A

and B are settled on a replacement cost basis subject to an 80% coinsurance

requirement.

� Loss to a pair or set

� Glass replacement with safety glazing materials

� Appraisal

� Pro Rata Liability for other insurance

� Suit against insurer requires that all policy provisions have been complied

with and the suit is stated within one year of the date of loss

� Abandonment of Property not allowed by the insured

� Mortgage clause acknowledges the insurable interest of the mortgagee

(holding the mortgage). The mortgagee�s insurable interest in a dwelling is

the amount of money owed by the insured on the dwelling.

� No Benefit to Bailee (holder of goods)

� Nuclear Hazards excluded

� Recovered Property can be kept or turned over to the insurance company.

Section II � Liability

Now that you�ve become familiar with Section I property coverages, it�s time to

learn about one of the other major areas of risk known as liability.

Just imagine the various exposures to liability a home owner has, such as

damages arising from the home itself or the front yard when a visitor slips and

falls, or a dead tree falls on your neighbor�s new home and the roof collapses.

Homeowners can be held liable for actions of children and pets. How about going

to a football game and it starts to rain? You open your umbrella and one of the

metal tips on the end of the umbrella pokes the person in the next seat, injuring

an eye.

The insured is covered for his/her responsibility as a home owner to the general

public through Coverage E - Personal Liability and Coverage F - Medical

Payments to Others.

Coverage E Covers bodily injury or property damage if someone gets hurt on

your property and the insured is found liable. Minimum limit of liability is

$100,000, but may be increased with additional premiums. Coverage is for non-

business activities.

Conditions include the insured�s location, personal activities of the insured on or

off the insured premises, and actions of an employee who lives at the insured

location in the course of employment. The insured includes the named insured

and all related residents of the same household and residence under 21 in the

care of any member of the named insured�s family.

Coverage E � Personal Liability

� Bodily injury (BI) liability includes bodily harm, disease or sickness

even if it results in death.

� Property damage applies to the physical injury or destruction to tangible

(real) property, including the loss of such property.

� Property Damage (PD) liability.

� Above arising out of insured�s personal, non-business activities that occur

anywhere.

� Provides a legal defense at the insurer�s choice, even if the suit is

groundless, false or fraudulent.

� Coverage E also applies for bodily injury or property damage arising

from insured locations including:

•Premises described in the Declarations.

•Residences newly acquired.

•Vacant land owned or rented by the insured.

• Insured�s land on which a residence is being built.

•Locations where an insured is temporarily residing.

•Locations an insured is renting for non-business use.

•Cemetery plots or burial vaults.

Coverage F - Medical Payments to Others

Coverage F pays for medical expenses incurred within 3 years due to bodily

injury to individuals who do not live at the residence. The expenses are paid,

regardless of whether or not the insured is liable for the injury. The maximum

medical limit of liability is $1,000, but limits may be increased by paying more

premium.

This coverage pays for the necessary medical expenses accrued within a three

year time frame from the date of the accident by a guest or others who may be

injured on the insured�s premises or as a direct result of an insured�s personal

activities.

Coverage F is not limitless but will generally pay for injuries:

� Sustained while the injured party is on an insured location with any insured�s

permission

� Sustained while the injured party is off the insured location if the injury

arises out of a condition:

•On the insured premises.

• Involving an activity of the insured.

•Caused by a residence employee (i.e. live in maid) in the course

of his/her employment.

•Caused by an animal owned by or in the care of any insured.

Coverages E and F Exclusions

� BI and PD arising out of the rental of any part of the premises, except

for the rental of part of an insured location as a residence.

� Liability for injury or damage that is expected or intended by the insured.

� BI or PD arising out of business pursuits or the rendering of or failure

to render professional services.

� BI that is covered under a Workers Compensation policy.

� Liability arising out of ownership, maintenance, use, loading, or

unloading of aircraft, watercraft and motor vehicles.

� Liability arising out of war and war-like acts, such as insurrection and

rebellion.

� Liability arising out of sexual molestation, corporal punishment or

physical or mental abuse.

� Liability arising out of the transmission of a communicable disease by

an insured.

� Liability arising out of the use, sale, manufacture, delivery, transfer, or

possession of a controlled substance (not legitimate RX drugs).

Section II - Comprehensive Personal Liability Additional

Coverage

� Claims expenses for the cost of investigating a claim, premiums for

bonds required in a suit the company decides to defend, reasonable

expenses incurred by the insured, interest on judgment which accrues

after the entry of the judgment. Expenses are paid in addition to the

limit of liability.

� First Aid Expenses incurred by an insured to others, but will not pay

first aid expenses for first aid to the insured.

� Damage to Property of Others - company will pay the replacement

cost of property of others damaged by an insured up to $500 per

occurrence.

� Loan Assessment - $1,000 per occurrence for the insured�s share or

assessment as a member of a group of property owners including liability

for an act of a director, officer or trustee

Section II Conditions

These will apply to both Sections I and II:

� There is coverage only during the policy period.

� No coverage for insureds who intentionally conceal or misrepresent

any material fact relating to insurance coverage.

� Waivers must be in writing to be effective.

� The following cancellation rules apply:

• Insurance company can cancel, for any reason, with 10 days

written notice to the insured during the first 60 days.

• Insured can cancel at any time.

•After 60 days the company may only cancel for the following

reasons:

! Material misrepresentation by the insured (requires a

30 day notice).

! Substantial change in risk insured (requires a 30 day

notice).

! Nonpayment of premium (requires a 10 day notice).

Endorsements

On this subject of endorsements, keep in mind that a homeowners policy is put

together for the average homeowner, whatever that is. However, from time to

time, homeowners develop special needs. To meet these needs, there are a

number of endorsements that can be attached to the Homeowners policy to

modify coverage under Sections I and/or II.

Section I Endorsements

�Scheduled Personal Property: This endorsement provides a separate

schedule of insurance for one or more of nine categories of valuable

property such as:

•Jewelry

•Cameras, projectors, films and equipment

•Golf equipment

•Furs

•Musical instruments

•Silverware

•Coins

•Fine arts

•Postage stamps

� Personal Property Coverage Endorsement (HO-15)

•Attaches to the HO-3 to insure personal property on an open

peril basis.

•This endorsement can only be used with the HO-3.

� Personal Property Replacement Cost: Policy will reimburse losses

to personal property on a replacement cost basis rather than actual

cash value. This is done in the same way that Homeowners forms

reimburse loss to dwellings.

� Permitted Incidental Occupancies: Overrides the exclusions under

the Homeowners forms that apply to the insured�s business activities

conducted on the residence premises.

•This basically eliminates the exclusion for using another

structure for business purposes

• It also eliminates the $2,500 limit for business property on the

residence premises with regard to furniture, supplies and

equipment used in the business listed in the endorsement

•Also, eliminates the Section II exclusion of liability and medical

payments coverage in connection with business pursuits for the

described business.

� As none of the Homeowners forms cover earthquakes, the insured

must purchase an Earthquake endorsement.

� Home Day Care Coverage: Extends Homeowners coverage to this

type of business. The premium for this coverage is based on the number

of children the insured cares for.

Section II Endorsements

� Business Pursuits Endorsement: Provides liability coverage for a

business conducted away from the residence premises.

� Personal Injury Endorsement: Modifies the definition of bodily injury

to include personal injuries such as libel, slander, false arrest, invasion

of privacy and malicious prosecution.

Mobile Homes Coverage

Due to their high exposure to risk and loss, mobile homes are excluded from

homeowner policies, with the exception of the availability of the MH-200

endorsement, which can be added to an HO-2 or HO-3 policy.

If the mobile home is permanently fixed on a foundation, then a dwelling policy

can be used. Because of depreciation, losses are always based on actual cash

value and not replacement value.

The mobile home package policy offers the Broad form of All Risk coverage for

the following:

� Mobile home, all equipment

� Built in accessories

� Additional structures such as awnings, carports and shelters

� Collision (optionally available)

� Additional living expenses

Note: Mobile home coverage is available under Homeowners policies, if

the home is at least 10 x 40 feet and designed for year round living.

Lesson 2 Review Questions 1. Which lines are written for individuals rather than businesses? A. Commercial B. Personal C. BOP D. CPP 2. Which type of policy provides the most Property coverage? A. Dwelling policy B. Unendorsed policy C. Homeowners policy D. Basic form policy 3. Which of the following is NOT covered by Dwelling property forms? A. Four family homes B. Dwellings up to seven roomers or boarders C. Permanently installed mobile homes D. Three family homes 4. Which of the following is NOT one of coverages offered in the DP-1 Basic form? A. Coverage A � Dwelling B. Coverage B � Other structures C. Coverage C � Personal property D. Coverage D � Casualty liability 5. Which of the following would provide coverage for a non-attached garage? A. Coverage A B. Coverage B

C. Coverage C D. Coverage D 6. Which of the following items are NOT covered under Coverage C? A. Money B. Television C. Couch D. Table 7. Coverage D � Fair Rental Value, provides what percent of the insurance on the dwelling for this coverage? A. 5% B. 10% C. 15% D. 20% 8. Which of the following perils are NOT automatically covered under the Dwellings Basic form? A. Fire B. Steam explosions from equipment owned and operated by a third party. C. Steam explosions from equipment leased by the insured. D. Wind 9. All of the following are Extended Coverage Perils (EC) which can be added onto a Dwelling policy EXCEPT: A. Windstorm B. Civil commotion C. Fire D. Smoke 10. Which of the following is NOT an additional coverage on the Dwelling Basic form? A. Other structures B. Debris removal C. Improvements D. Lightening 11. Which of the following are Not exclusions under a DP-1 form? A. War B. Fire C. Nuclear hazard D. Floods 12. Covered property losses are valued at actual cash value, but not to exceed the amount necessary to repair or replace, is known as: A. Loss Settlement

B. Our Option C. Pair or Set D. Repair Option 13. The clause in a policy that explains the rules regarding the loss of one item in a set is known as the: A. Loss Settlement B. Our Option C. Pair or Set D. Repair Option 14. After reaching an agreement with the insurer, a loss will be paid for within how many days? A. 10 B. 15 C. 30 D. 90 15. To increase the coverage of the Basic for DP-1, an insured could purchase additional coverage using which of the following Broad forms? A. DP-1 B. DP-2 C. DP-3 D. DP-4 16. All of the following are included as additional perils found in the DP-2 form EXCEPT: A. Burglar damage B. Electrical damage C. Fire D. Tearing apart 17. Ice coverage extends to which of the following? A. Dwelling B. Awnings C. Patios D. Swimming pool 18. The Collapse Peril covers risk of direct physical loss to covered property involving collapse of a building or any part of it caused by: A. Settling B. Shrinking C. Bulging D. Hidden decay 19. Which of the following additional coverages are available with the DP-2

and DP-3? A. Materials and supplies used to repair the dwelling B. Trees C. Structures attached to the dwelling D. Personal property 20. Broad forms additional perils are found under which form? A. DP-1 B. DP-2 C. DP-3 D. DP-4 21. Both the DP-2 and DP-3 settle losses to personal property at: A. Replacement value B. Actual cash value C. Depreciated value D. Replacement value plus depreciation 22. Bob�s home has a replacement value of $160,000. To have the home restored or replaced at replacement cost, Jo Bob must have insurance equal to or greater than 80% of the replacement value. However, Bob forgot the rule and does not carry enough insurance to qualify for replacement cost coverage. Assuming he only has insurance coverage for $100,000, and has a loss of $20,000, how much will the insurance company reimburse Bob? A. $20,000 B. $16,000 C. $15,625 D. $12,500 23. Personal liability under Dwelling Coverage is covered under which of the following coverages? A. Coverage A B. Coverage B C. Coverage L D. Coverage M 24. Medical Payments to Others under Dwelling Coverage is paid under which of the following coverages? A. Coverage A B. Coverage B C. Coverage L D. Coverage M 25. Homeowners forms are identified by which of the following abbreviations?

A. MO B. HO C. HP D. HF 26. Which Homeowners form provides broad form coverages? A. HO-2 B. HO-3 C. HO-4 D. HO-6 27. Which Homeowners form provides Special form coverages? A. HO-2 B. HO-3 C. HO-4 D. HO-6 28. Which of the Homeowners forms is designed for tenants? A. HO-2 B. HO-3 C. HO-4 D. HO-6 29. Which of the Homeowners forms is designed for condominiums? A. HO-2 B. HO-3 C. HO-4 D. HO-6 30. Which HO form is designed for older homes? A. HO-2 B. HO-3 C. HO-4 D. HO-8 31. With HO forms, which Section provides coverage for Property? A. 1 B. 2 C. 3 D. 4 32. Which coverages in Section 1 of a Homeowners policy provides coverage for Other Structures? A. A B. B C. C

D. D 33. Coverage C in Section 1 provides coverage for personal property: A. Only in the United States B. Only in the State of residence C. Anywhere in the world D. Only outside the United States 34. Personal property coverage is up to what percent of the Coverage C limit? A. 10% B. 15% C. 25% D. 50% 35. Money can be covered under Special Coverage C to a limit of: A. $100 B. $200 C. $500 D. $1,000 36. A proof of loss must be submitted to the insurance company within how many days of the insurer�s request? A. 10 B. 25 C. 30 D. 60 37. Under Section II of a Homeowners policy, Personal liability is covered by which Coverage? A. A B. F C. E D. M 38. Under Section II of a Homeowners Policy, Medical payments to others are covered under which Coverage? A. A B. F C. E D. M 39. Endorsements are meant to: A. Decrease coverage B. Increase coverage C. Keep coverage the same

D. Decrease then increase every 30 days 40. Which of the following HO forms attach to HO-3 for additional personal property coverage? A. HO � 2 B. HO � 6 C. HO � 15 D. HO � 18

Lesson 2 Review Answers 1. (B) Personal lines are written for individuals. Commercial lines are written for businesses. 2. (C) While both a Homeowners and Dwelling policy provide property coverage, the Dwelling is a more limited policy. The Dwelling policy provides protection for individuals and families against loss to their dwelling and personal property. Homeowners policies extend protection to include property (fire) and casualty (personal liability and theft). This places the needs of the consumer into one contract, thus creating a multi-line policy. 3. (B) Dwelling property forms cover dwellings up to five roomers, not seven. This form also covers three- and four-family homes, permanently-installed mobile homes and rentals not coverable by homeowners. 4. (D) DP-1 offers the following coverage: Coverage A - Dwelling; Coverage B � Other Structures; Coverage C � Personal Property; Coverage D � Fair Rental Value. There is no coverage for casualty liability in DP-1. 5. (B) Since a non-attached garage is considered another structure, it would be covered under Coverage B � Other Structures. 6. (A) Under Coverage C, money, coins and securities are not covered. Also excluded are: paper and computerized accounting records; software media; credit cards; animals including birds and fish; aircraft; motor vehicles other than motorized equipment used to maintain the property; boats, other than rowboats and canoes. 7. (B) If the loss to the dwelling makes it uninhabitable, and the insured cannot collect the rent he or she would have been able to receive if the loss had not occurred, 10% of the insurance on the dwelling is available for this coverage. 8. (B) Damage due to steam explosions are excluded in the Dwellings Basic policy, if the equipment is owned, leased or operated by the insured. 9. (C) Extended Coverage Perils (EC) that can be added to a Dwelling policy

include windstorm, civil disorder, smoke, hail, aircraft, vehicle, explosion and riot. Fire is a named peril under the Basic form, and would not need to be added as an EC. Use the acronym WCSHAVER to remember EC perils. 10. (D) Lightening is covered under the Basic form, not the Additional coverages form. Additional coverages include: other structures; debris removal; property removed; reasonable repairs; improvements, alterations and additions; fire department service charge; worldwide coverage; and rental value. 11. (B) Fire is covered under Dwellings Basic. War, nuclear hazard and floods are all excluded under DP-1. 12. (A) Covered property losses are valued at actual cash value, but not to exceed the amount necessary to repair or replace. This is known as loss settlement. 13. (C) The Set or Pair clause will explain how a claim should be handled when one item of a pair or set is damaged. Loss of an article which completes a pair or set is handled as a unique claims settlement problem. Options include repair or replace any part to restore the pair or set to its value before the loss, or settle by paying the difference between the actual cash value of the set before and after the loss. 14. (C) The loss will be paid within 30 days after reaching an agreement with the insured. 15. (B) While the Basic form named specific perils, so does the Broad form (DP-2). It includes all those in DP-1, as well as some additional perils. Some of the additional perils included in the DP-2 are burglar damage, ice and snow weight, glass breakage, accidental discharge, falling objects, freezing of pipes, electrical damage, collapse, and tearing apart. 16. (C) Fire is covered under the Basic form, while burglar damage, electrical damage and tearing apart are included in the DP-2 Broad form. 17. (A) Protection is provided from falling objects such as ice, snow and sleet. Damage to the insured building and/or contents due to their weight is covered. Coverage does not extend to awnings, fences, patios, pavements, swimming, pools, foundations, retaining walls, bulkheads, wharves, docks and piers. 18. (D) The collapse peril covers risk of direct physical loss to covered property involving collapse of a building or any part of it caused by perils insured against in the policy, hidden decay, insect damage, weight of contents, weight of rain or snow collected on the roof, or use of defective materials. 19. (B) Additional coverage available with DP-2 and DP-3 include trees, collapse

and glass or safety glazing material. 20. (B) Broad forms Additional Perils are found in DP-2. They include burglar damage, ice and snow weight, glass breakage, accidental discharge, falling objects, freezing of pipes, electrical damage, collapse, and tearing apart. 21. (B) Both DP-2 and DP-3 forms settle losses to personal property at Actual Cash Value (ACV). This is found by subtracting depreciation from the replacement cost. 22. (C) If Bob carried $100,000 of insurance, but the coinsurance value required $128,000 (or 80% of the $160,000 replacement value), this would amount to $100,000 divided by the insurance required of $128,000, or .78125. That amount, times the loss of $20,000, equals the reimbursement of $15,625. 23. (C) Personal liability is covered under Coverage L. It is for damages that the insured becomes legally obligated to pay because of bodily injury or property damage caused by an occurrence for which there is coverage. The insurer will also defend the insured against such claims at its own expense, even if the suit is groundless or fraudulent. The policy limit is $100,000. 24. (D) Medical Payments to Others is under Coverage M (think Medical = M). The insurance company will pay all necessary medical expenses incurred within three years of an accident that causes bodily injury. Coverage does not apply to any injury sustained by the insured or the insured�s family members. 25. (B) Homeowners forms can be identified by the abbreviation HO. 26. (A) Broad form HO coverages are found in HO-2. Provides broad coverage for direct physical loss caused by fire, lighting, internal explosion, extended coverage perils (EC), vandalism & malicious mischief (VMM), and broad form additional perils ( BIGAFFECT ) 27. (B) Special forms coverage is provided under HO-3. It provides open peril coverage for direct physical loss caused by: all risk or open perils on the dwelling and other structures, HO-2 perils on the personal property (contents), and theft. 28. (C) HO-4 is designed for tenets of apartments. It provides broad coverage for personal property. Similar coverage to the HO-2s and HO-3s broad coverage for personal property. The dwelling itself is not covered. 29. (D) Like the HO-4, the HO-6 is designed to insure personal property of condominium owners. Similar coverage to that provided under the HO-2, HO-3 and HO-4. Provides very limited dwelling coverage.