project idbi

DESCRIPTION

project idbiTRANSCRIPT

PROJECT REPORT ON

WORKING CAPITAL FINANCE-“HOW WORKING CAPITAL LENDS WORK”

SUBMITTED BY:

MANVI JAIN

PGDM FINANCE

ITM COLLEGE, KHARGHAR

The Indian banking can be broadly categorized into nationalized (government owned), private banks and specialized banking institutions.The Reserve Bank of India acts a centralized body monitoring any discrepancies and shortcoming in the system. Since the nationalization of banks in 1969, the public sector banks or the nationalized banks have acquired a place of prominence and has since then seen tremendous progress. The need to become highly customer focused has forced the slow-moving public sector banks to adopt a fast track approach. The unleashing of products and services through the net has galvanized players at all levels of the banking and financial institutions market grid to look anew at their existing portfolio offering..The Indian banking has finally worked up to the competitive dynamics of the ‘new’ Indian market and is addressing the relevant issues to take on the multifarious challenges of globalization.. Private banks have been fast on the uptake and are reorienting their strategies using the internet as a medium The Internet has emerged as the new and challenging frontier of marketing with the conventional physical world tenets being just as applicable like in any other marketing medium.The Indian banking has come from a long way from being a sleepy business institution to a highly proactive and dynamic entity. This transformation has been largely brought about by the large dose of liberalization and economic reforms that allowed banks to explore new business opportunities rather than generating revenues from conventional streams (i.e. borrowing and lending). The banking in India is highly fragmented with 30 banking units

contributing to almost 50% of deposits and 60% of advances. Indian nationalized banks (banks owned by the government) continue to be the major lenders in the economy due to their sheer size and penetrative networks which assures them high deposit mobilization. The Indian banking can be broadly categorized into nationalized, private banks and specialized banking institutions.The Reserve Bank of India act as a centralized body monitoring any discrepancies and shortcoming in the system. It is the foremost monitoring body in the Indian financial sector. The nationalized banks (i.e. government-owned banks) continue to dominate the Indian banking arena. Industry estimates indicate that out of 274 commercial banks operating in India, 223 banks are in the public sector and 51 are in the private sector. The private sector bank grid also includes 24 foreign banks that have started their operations here. Under the ambit of the nationalized banks come the specialized banking institutions. These co-operatives, rural banks focus on areas of agriculture, rural development etc.,

Phases of Indian Banking System Without a sound and effective banking system in India it cannot have a healthy

economy. The banking system of India should not only be hassle free but it should

be able to meet new challenges posed by the technology and any other external

and internal factors.

For the past three decades India’s banking system has several outstanding

achievements to its credit. The most striking is its extensive reach; it is no longer

confined to only metropolitans or cosmopolitans in India. In fact, Indian banking

system has reached even the remote comers of the country. This is one of the

main reasons of India’s growth process.

The government’s regular policy for Indian bank since 1969 has paid rich

dividends with the nationalisation of 14 major private banks of India.

The first bank in India, though conservative, was established in 1786. From 1786

till today, the journey of Indian Banking System can be segregated into three

distinct phases.

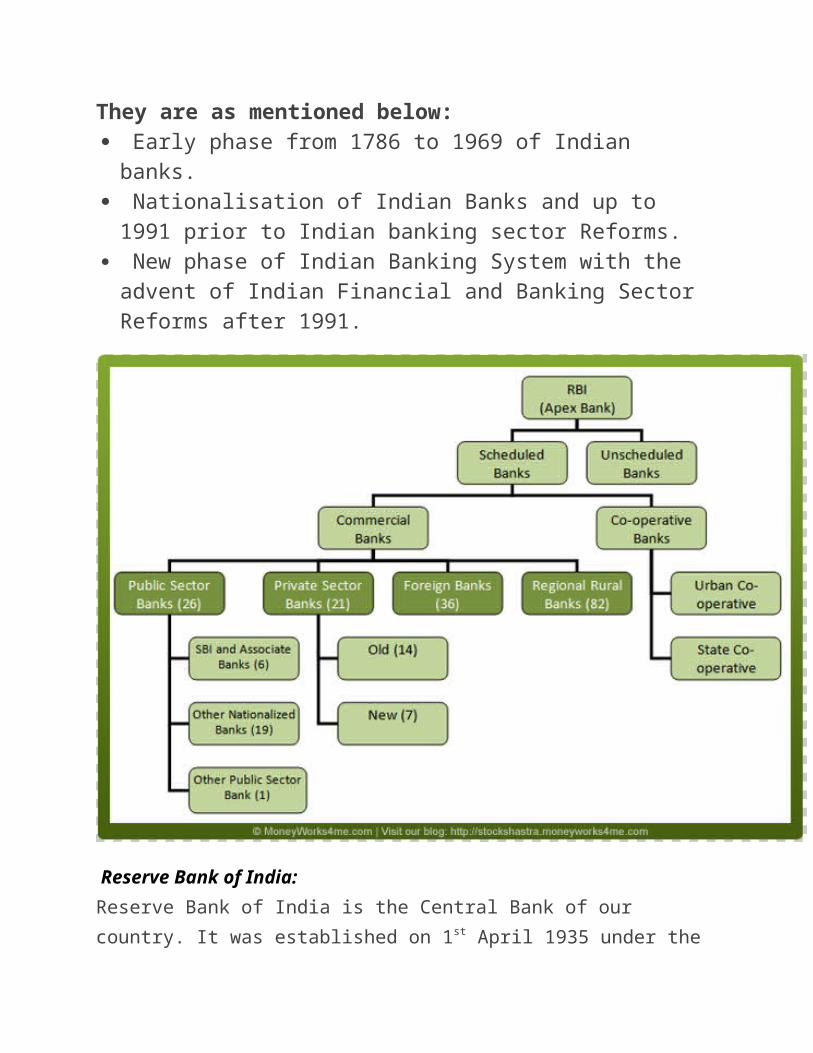

They are as mentioned below: Early phase from 1786 to 1969 of Indian banks. Nationalisation of Indian Banks and up to 1991 prior to Indian

banking sector Reforms. New phase of Indian Banking System with the advent of Indian

Financial and Banking Sector Reforms after 1991.

Reserve Bank of India:

Reserve Bank of India is the Central Bank of our country. It was established on

1st April 1935 under the RBI Act of 1934. It holds the apex position in the banking

structure. RBI performs various developmental and promotional functions.

It has given wide powers to supervise and control the banking structure. It

occupies the pivotal position in the monetary and banking structure of the

country. Central bank is known as a banker’s bank. They have the authority to

formulate and implement monetary and credit policies. It is owned by the

government of a country and has the monopoly power of issuing note.

1. Scheduled Banks :- Under RBI Act of 1934, banks were classified as scheduled and non-scheduled banks. The scheduled banks are those which are entered in second schedule of RBI Act of 1934. They are eligible for certain facilities. All commercial banks (India and foreign, regional rural banks) and state co-operatives are scheduled banks.

A scheduled must have a paid up capital and reserves of not less than Rs. 5 lakhs. It must also satisfy RBI that it affairs are not conducted in a manner detrimental to the interest of its depositors.

2. Non-Scheduled Banks :-Non-scheduled Banks are those which have not been included in the second

Schedule of RBI Act. The number of non-scheduled banks is declining as many of them are attaining the status of scheduled banks in 2008.The scheduled commercial banks consist of public sector banks, private sector Banks and Foreign Banks. As on march 2009, there are 27 public sector banks consisting of SBI and its 8 associated banks, 19 nationalised banks and IDBI Ltd. There are 7 new private sector banks, 15 old private sector banks in India. Besides there are 86 RRBs in 2008-09.

I. Co-operative Bank:

Co-operative bank was set up by passing a co-operative act in 1904. They are

organised and managed on the principal of co-operation and mutual help. The

main objective of co-operative bank is to provide rural credit.

The cooperative banks in India play an important role even today in rural co-

operative financing. The enactment of Co-operative Credit Societies Act, 1904,

however, gave the real impetus to the movement. The Cooperative Credit

Societies Act, 1904 was amended in 1912, with a view to broad basing it to enable

organisation of non-credit societies.

II. Commercial Banks:

Commercial bank is an institution that accepts deposit, makes business loans and

offer related services to various like accepting deposits and lending loans and

advances to general customers and business man.

These institutions run to make profit. They cater to the financial requirements of industries and various sectors like agriculture, rural development, etc. it is a profit making institution owned by government or private of both.

I. Public Sector Banks :-Public sector Banks have a dominant position in terms of business. They

accounted for 71.9% of assets, 76.6% of deposits, 75.3% of advances and 69.9% of investments of all scheduled commercial banks as at end of March 2009. Among the public sector banks, the state Bank of India and associates had 16,294 branches and nationalized banks had 39,703 branches as on June 30, 2009.

a) State Bank Of India And Its Associate Banks :- On 1st July, 1955, on the recommendation of Rural Credit Survey Committee, the Imperial Bank of India was converted in to State Bank of India. RBI acquired its 92% shares, thus SBI had the distinction of becoming the first state owned commercial bank in the country.

The State Bank of India (Associate banks) Act was passed in 1959 and this paved the way for creating State Bank Group. Besides functioning as a commercial bank, SBI ushered a new era of mixed banking system in the country. It proved that financing to agriculture and other priority sectors could be a viable commercial activity. On 19th July, 1969, 14 major commercial banks were nationalized and 6 more were nationalized in 1980. Over the years SBI and its associates have expanded their business. On June 30, 2009, they accounted for 20% of total branches of all commercial banks. The share of banking business with them was roughly 30%. In 1993, SBI Act was amended to enable it to have access to capital market.

b) Other Nationalised Banks :-The second category of public sector is 19 commercial banks, of which 14

were natioalised on July 19, 1969. This changed the banking structure. Each one of these 14 banks had deposits of Rs. 50 crore or more. The nationalization was justified by government because major banks have a larger social purpose. In December 1969, Lead bank Scheme was formulated which played an important role in transforming these profit maximizing institutions in to catalysts of local development. On April 15, 1980 six more private owned commercial were nationalized. The purpose was to promote the welfare of the people in conformity with the policy of the state. With natioalisation, The share of private sector in the entire banking declined to just 9%. In 1993 New Bank of India merged with Punjab National Bank. As a result, the no. of public sector banks (other than state Bank and its associates) declined to 19. As on June 30, 2009, the total number of branches of 19 nationalised banks was 39,661.

c) Regional Rural Banks (RRBs) :-The RRBs came to be set up under the act of 1976. They were set up to save

the poor rural people from the grip of money lenders and traders. The Working Group on Rural Banks recommended the setting up of RRBs as part of multi-agency approach to rural credit. A RRB is sponsored by a public sector bank which also subscribes to its share capital. As on June 30, 2006, there were 196 RRBs with a network of 14,500 branches.

The RRBs meet the credit requirements of weaker sections, small and marginal farmers , landless labourers, artisians and small entrepreneurs. RRBs have been excellent in meeting the credit needs of rural poor.

II. Private Sector Banks :-In Private sector small scheduled commercial banks and seven newly

established banks with a network of 8,965 branches are operating. To encourage competitive efficiency, the setting up of new private bank is now encouraged. Presently, the total number of banks in private sector is 22 (15 old and 7 new). In 2008-09 new private sector banks accounted for 19.6% of total banking assets.

III. Foreign Banks :-For a long time a majority of foreign banks have been operating in India. On

30th June 2009, the country had 32 foreign banks with 295 branches located mainly in big cities. Apart from financing of foreign trade, these banks have performed all functions of commercial banks and they have an advantage over Indian banks because of their vast resources and superior management. In 2008-09, foreign banks accounted for 8.5% of total banking assets. At the end of September, 2010, 34 foreign banks were operating in India. In India, foreign banks practices have been held in suspicion. The unfair competition with Indian banks, their practice of drawing funds from London Money Market for financing India’s foreign trade and their gross irregularities in securities scam have been a cause of concern. With growing strength of Indian banks have improved their practices and have stopped discriminatory policies

Categories of BankingWhen we talk about banks, we are talking about several different types of financial institutions, conducting different kinds of business. Some banks are very large and carry out many different functions, others are more specialised. Some have operated for hundreds of years and some have taken on new kinds of business quite recently.

Not all banks carry out the same range of activities. Banking activities can be generally divided into the following types:

Central Banking The duty of central banks is to maintain financial stability, otherwise a country's economy will not operate properly. Central banks act as regulators of their country's interest rates by controlling the amount of money in circulation and buying and selling currencies. They amass reserves and act as lenders of last resort, should another bank get into trouble. They exist as a separate entity from all the other banks.

Retail Banking Retail banks are the high street banks we are all familiar with. They take deposits from individuals, provide saving facilities and pay interest on these accounts. They also lend money to individuals, in the form of loans and overdrafts, and charge interest on the money they lend. They provide a range of other financial services.

Commercial Banking Commercial banks, or divisions of banks, provide banking services to businesses, from small companies through to corporate banking directed at large corporations. They help companies raise finance to expand their businesses and to maintain their cashflow by lending them money. They provide a wide range of other financial services.

Investment Banking Investment banks distribute and underwrite (guarantee the sale of) share and bond issues; they trade securities on the financial markets and advise corporations oncapital market activities such as mergers and acquisitions. Investment banks originally developed in the USA and these banks have now taken over many roles that were previously carried out by UK merchant banks.

Meaning of Working Capital Management

The management of current assets, current liabilities and inter-relationship between them is termed as working capital management. “Working capital management is concerned with problems that arise in attempting to manage the current assets, the current liabilities and the inter-relationship that exist between them.”

Working capital is the investment in current assets. Without this investment, we can not operate our fixed assets properly. For getting good profits from fixed assets, we need to buy some current assets or pay some expenses or invest our money in current assets. For example, we keep some of cash which is the one of major part of working capital. At any time, our machines may need repair. Repair is revenue expense but without cash, we can not repair our machines and without machines, our production may delay. Like this, we need inventory or to invest in debtors and other short term securities.

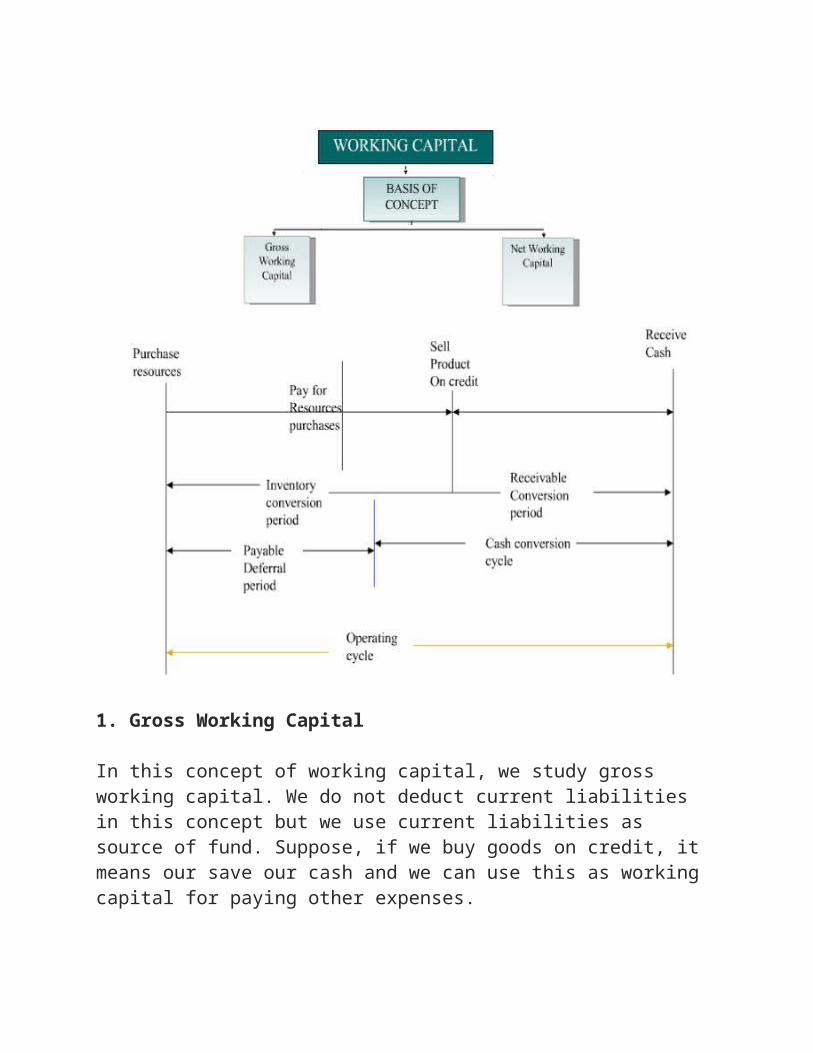

On the basis of Concept, we can divide our working capital into two parts:

1. Gross Working Capital

In this concept of working capital, we study gross working capital. We do not deduct current liabilities in this concept but we use current liabilities as source of fund. Suppose, if we buy goods on credit, it means our save our cash and we can use this as working capital for paying other expenses.

2. Net Working Capital

Under this concept we use net working capital. For this, we first deduct all our current liabilities from our current assets. Excess of current assets over current liabilities will be current assets. We have to maintain minimum level of working capital in our business for operation of business activities. This concept is also used for preparation of balance sheet. In the vertical form of balance sheet, we show excess of current assets over current liabilities.

Operating Cycle Concept of Working Capital

In this concept of working capital, we make the operating cycle. In this cycle, we calculate inventory conversion period. To know this, we can estimate when we need cash for buying our inventory. We also calculate debtor or receivable conversion period. To know this, we can estimate when we receive cash from our debtors.

If inventory conversion period is less than debtor conversion period, we have to manage other sources for buying our inventories. If we buy good on credit, we also take care creditors' conversion period.

Working Capital Management StrategiesWorking capital management directly affects the firm’s long term growth and survival. A company may be profitable and it may have sufficient assets, but short of liquidity may endanger its goodwill. Management should make sure that they have adequate working capital so as to manage its daily activities and upcoming operational expenses. There is high risk and uncertainty involved in managing the working capital since your debtors may not pay you at the time when you have to pay to your suppliers. At the same

time, management cannot keep excess capital as it leads to opportunity loss of the excess capital blocked and shortage of it can lead to irreparable damage to the company in terms of lost suppliers due to delay in payments or lost customers due to not meeting the demands as and when required which may also result in poor returns, high amount of bad debts and low market value of shares. Effective working capital management allows the company to invest in future growth, repay its current liabilities as and when they become due and reduce financing costs. Thus, working capital management will involve managing cash, inventories, receivable and short term financing.

Current assetsA current asset is an item on an entity's balance sheet that is either cash, a cash equivalent, or which can be converted into cash within one year. Examples of current assets are:

Cash Investments Prepaid expenses Accounts receivable Inventory

These items are typically presented in the balance sheet in their order of liquidity, which means that the most liquid items are shown first. The preceding example shows current assets in their order of liquidity.

Creditors are interested in the proportion of current assets to current liabilities, since it indicates the short-term liquidity of an entity. In essence, having substantially more current assets than liabilities indicates that a business should be able to meet its short-term obligations.

Non current assets

Non-current assets are assets other than current assets, while current assets are assets which are expected to be realized in next 12 months or within normal operating cycle of a business.

Following are the major types of non-current assets:

1. Property, Plant and Equipment

2. Intangible Assets 3. Long-term Investments

There are certain alternative terms used to refer to non-current assets, for example fixed assets, long-term assets, long-lived assets etc.

Current liability

A current liability is an obligation that is 1) due within one year of the date of a company's balance sheet and 2) will require the use of a current asset or will create another current liability. If a company's operating cycle is longer than one year, current liabilities are those obligation's due within the operating cycle.

Current liabilities are usually presented in the following order:

1. the principal portion of notes payable that will become due within one year

2. accounts payable

3. the remaining current liabilities such as payroll taxes payable, income taxes payable, interest payable and other accrued expenses

The parties who owed the current liabilities are referred to as creditors. If the creditors have a lien on company assets, they are known as secured creditors. The creditors without a lien are referred to as unsecured creditors.

The amount of current liabilities is used to determine a company's working capital (current assets minus current liabilities) and the company's current ratio (current assets divided by current liabilities).

Non current liabilitiesNon-current liability is a liability not due to be paid within 12 months during the normal course of business. Non-current liabilities are also called long-term

liabilities. In accounting, non-current liabilities are shown on the right wing of the balance sheet representing the sources of funds, which are generally bounded in form of capital assets.Non-current liabilities include (according to the IFRS): Non-current provisions for employee benefits Other long-term provisions Trade and other non-current payables Deferred tax liabilities Other long-term financial liabilities Other non-current non-financial liabilities

All liabilities are divided into non-current liabilities and current liabilities. Non-current liabilities often referred aslong-terms debts.Non-current liabilities are very important source of entity's long-tem financing (acquisition of fixed and other non-current assets).

Working capital gap

In order to reduce the dependence of businesses on banks for working capital, ceiling on bank credit to individual firms has been prescribed. Accordingly, businesses have to compute the current assets requirement on the basis of stipulations as to size. So, flabby inventory, speculative inventory cannot be carried on with bank finance. Normal current liabilities, other than bank finance, are also worked out considering industry and geographical features and factors. Working capital gap is the excess of current assets as per stipulations over normal current liabilities (other than bank assistance). Bank assistance for working capital shall be based on the working capital gap, instead of the current assets need of a business. This type of financing assistance by banks was introduced on the basis of recommendations of Tandon Committee.

Analysis of balance sheet

Balance sheet analysis can be defined as an analysis of the assets, liabilities, and equity of a company. This analysis is conducted generally at set intervals of time, like annually or quarterly. The process of balance sheet analysis is used for deriving actual figures about the revenue, assets, and liabilities of the company.

Goal of Balance Sheet AnalysisThe balance sheet analysis is helpful for the investors, investment bankers, share brokers, and financial institutions, for verifying the profitability of investment for a specific company.

How to perform a Balance Sheet Analysis

It is not a difficult task to perform a Balance Sheet Analysis. The main steps include: The primary step involves adding up liabilities and the paid up equity share

capital. The sum must tally with the sum of total assets. After the process of tallying is done, contrast the total assets with total liabilities. However, this evaluation does not include the issued shares’ amount in the liabilities. If the total assets are exceeding the total liabilities, the financial standing and performance of the company is considered to be good.

The next step involves looking at the current assets and liabilities. Sometimes, it is considered as a good sign to have more unsecured liabilities.

Another important step is calculating the ROA by dividing the net income by assets. Producer companies feature a high ROA unlike the real estate and leasing companies which feature a low ROA.

The fourth step involves special concern for copyrights and patents. It is important to consider the ratio between invested amount for research and the consequent returns.

Next step involves calculating the debt asset ratio by dividing total liabilities by total assets. A lower liability dimension reflects a better performance by the company.

Another step includes estimating the receivables turnover ratio which signifies the relation between investment in sales and money receivable. A better financial status is reflected in high amount of money receivables.

Another important ratio is the inventory turnover ratio which indicates the company’s capability of producing goods with available assets.

The final step includes analyzing other features of company including goodwill, credit ratings, and current projects. This analysis is helpful in evaluating the company activities in near future.

By analysing the balance sheet you can assess a company’s liquidity, how much its leveraged, its return on investment, and more.

Working Capital

Working capital should always be a positive number. It is used by lenders to evaluate a company’s ability to weather hard times. Often, loan agreements specify a level of working capital that the borrower must maintain.

Working Capital = Total Current Assets - Total Current Liabilities

The current ratio, quick ratio and working capital are all measures of a company’s liquidity. In general, the higher these ratios are, the better for the business and the higher degree of liquidity.

Debt/Worth Ratio

The debt/worth ratio (or leverage ratio) is an indicator of a business’ solvency. It is a measure of how dependent a company is on debt financing (or borrowings) as compared to owner’s equity. It shows how much of a business is owned and how much is owed.

The debt/worth ratio is computed as follows:

Debt/Worth Ratio = Total Liabilities

Net Worth

ANALYSIS OF RATIOS

Ratio analysis is a process of determining and interpreting relationships between the items of financial statements to provide a meaningful understanding of the performance and financial position of an enterprise. Ratio analysis is an accounting tool to present accounting variables in a simple, concise, intelligible and understandable form.

Classification or types of Ratios:

1) Liquidity Ratio

2) Financial Structure Ratio

3) Activity Ratio

4) Profitability Ratio

5) Coverage Ratio

1) Liquidity Ratio(Short Term Solvency):

It measures the short-term solvency, i.e., the firm’s ability to pay its current dues. They comprise of Current Ratio and Liquid Ratio.

Current Ratio or Working Capital Ratio is a relationship of current assets to current liabilities. Current Assets are the assets that are either in the firm of cash or cash equivalents or can be converted into cash or cash equivalents in a short time (say, within a year’s time) and Current Liabilities are repayable in a short time. It is calculated as follows:

Current Ratio = Current Assets

Current Liabilities

Significance:

The objective of calculating Current Ratio is to assess the ability of the enterprise to meet its short-term liabilities promptly. It shows the number of times the current assets can be converted into cash to meet current liabilities. As a normal rule current assets should be twice the current liabilities. Low ratio indicates inadequacy of the enterprise to meet its current liabilities and inadequate working Capital. High Ratio is an indication of inefficient utilization of funds. An enterprise should have a reasonable current ratio. Although there is no hard and fast rule yet a current ratio of 2:1 is considered satisfactory.

Current Ratio is calculated at a particular date and not for a particular period.

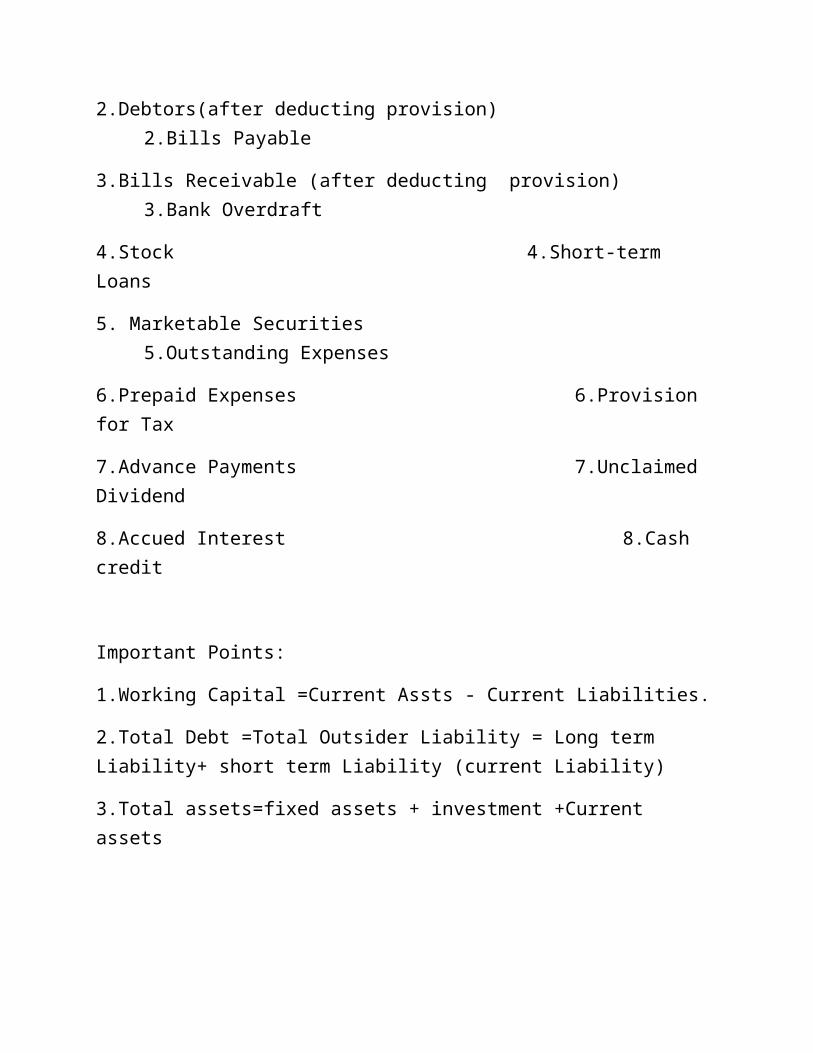

The following items are included in current assets and Current Liabilities:

Current Assets Current Liabilities

1.Cash and Bank Balance 1.Creditors

2.Debtors(after deducting provision) 2.Bills Payable

3.Bills Receivable (after deducting provision) 3.Bank Overdraft

4.Stock 4.Short-term Loans

5. Marketable Securities 5.Outstanding Expenses

6.Prepaid Expenses 6.Provision for Tax

7.Advance Payments 7.Unclaimed Dividend

8.Accued Interest 8.Cash credit

Important Points:

1.Working Capital =Current Assts - Current Liabilities.

2.Total Debt =Total Outsider Liability = Long term Liability+ short term Liability (current Liability)

3.Total assets=fixed assets + investment +Current assets

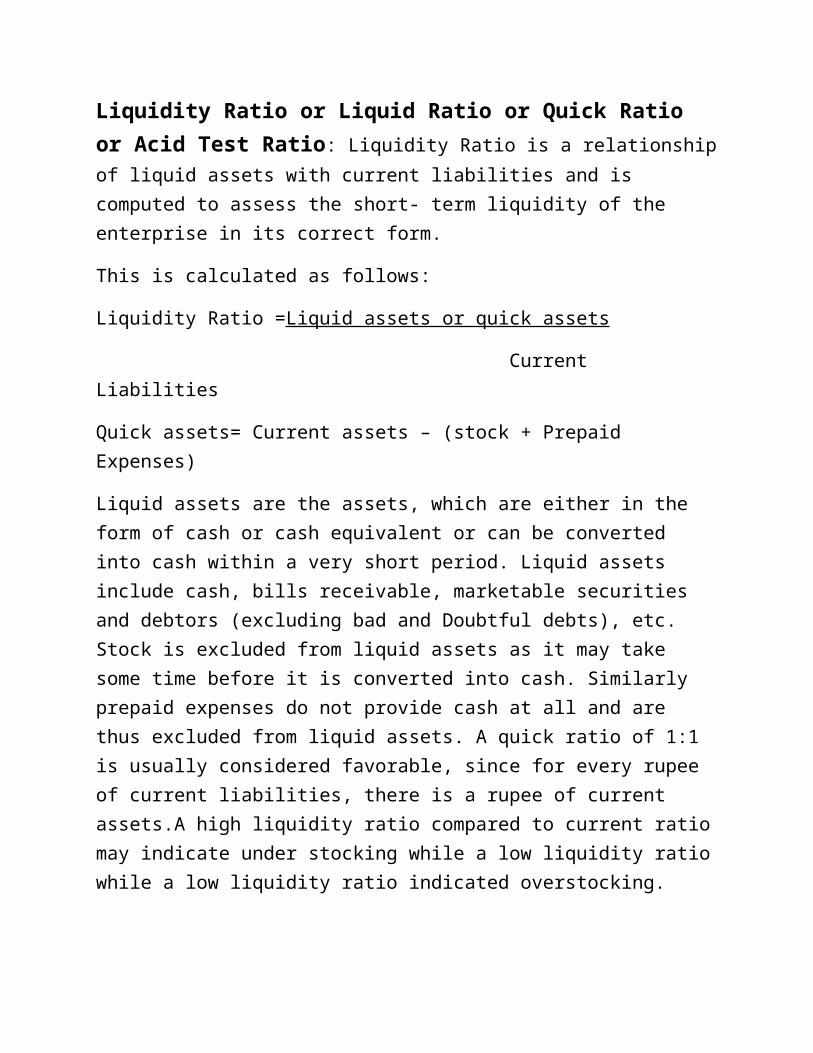

Liquidity Ratio or Liquid Ratio or Quick Ratio or Acid Test Ratio: Liquidity Ratio is a relationship of liquid assets with current liabilities and is computed to assess the short- term liquidity of the enterprise in its correct form.

This is calculated as follows:

Liquidity Ratio =Liquid assets or quick assets

Current Liabilities

Quick assets= Current assets – (stock + Prepaid Expenses)

Liquid assets are the assets, which are either in the form of cash or cash equivalent or can be converted into cash within a very short period. Liquid assets include cash, bills receivable, marketable securities and debtors (excluding bad and Doubtful debts), etc. Stock is excluded from liquid assets as it may take some time before it is converted into cash. Similarly prepaid expenses do not provide cash at all and are thus excluded from liquid assets. A quick ratio of 1:1 is usually considered favorable, since for every rupee of current liabilities, there is a rupee of current assets.A high liquidity ratio compared to current ratio may indicate under stocking while a low liquidity ratio while a low liquidity ratio indicated overstocking.

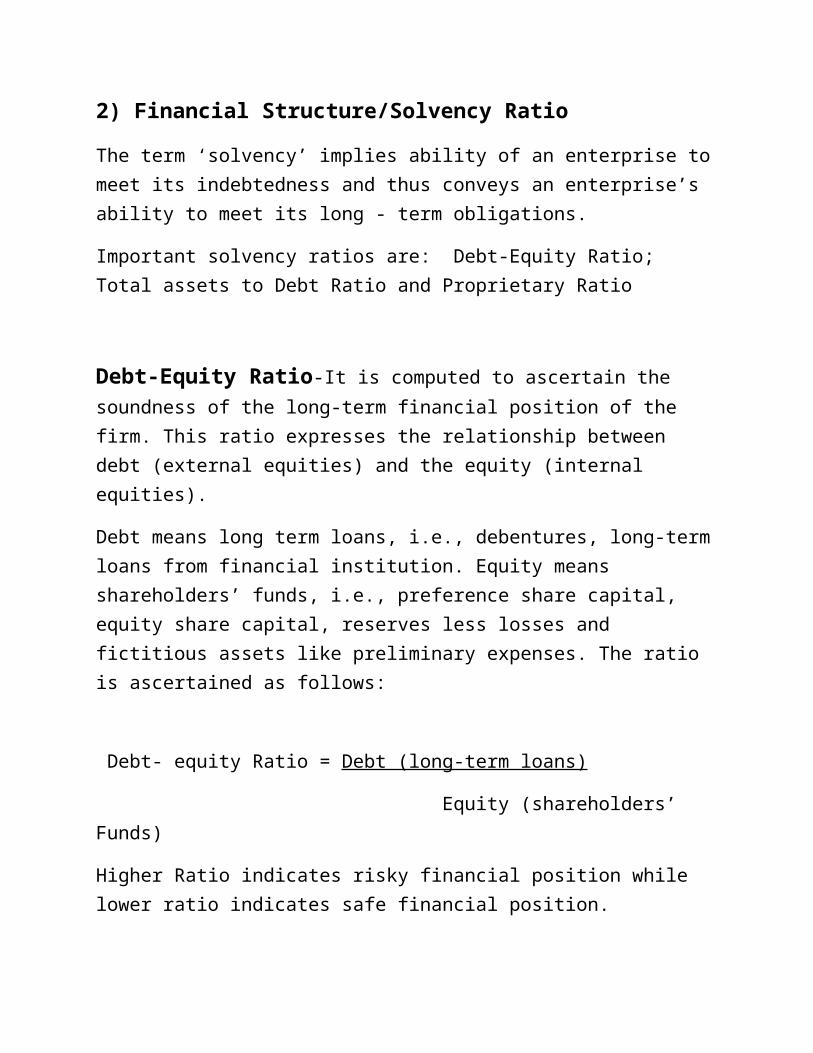

2) Financial Structure/Solvency Ratio

The term ‘solvency’ implies ability of an enterprise to meet its indebtedness and thus conveys an enterprise’s ability to meet its long - term obligations.

Important solvency ratios are: Debt-Equity Ratio; Total assets to Debt Ratio and Proprietary Ratio

Debt-Equity Ratio-It is computed to ascertain the soundness of the long-term financial position of the firm. This ratio expresses the relationship between debt (external equities) and the equity (internal equities).

Debt means long term loans, i.e., debentures, long-term loans from financial institution. Equity means shareholders’ funds, i.e., preference share capital, equity share capital, reserves less losses and fictitious assets like preliminary expenses. The ratio is ascertained as follows:

Debt- equity Ratio = Debt (long-term loans)

Equity (shareholders’ Funds)

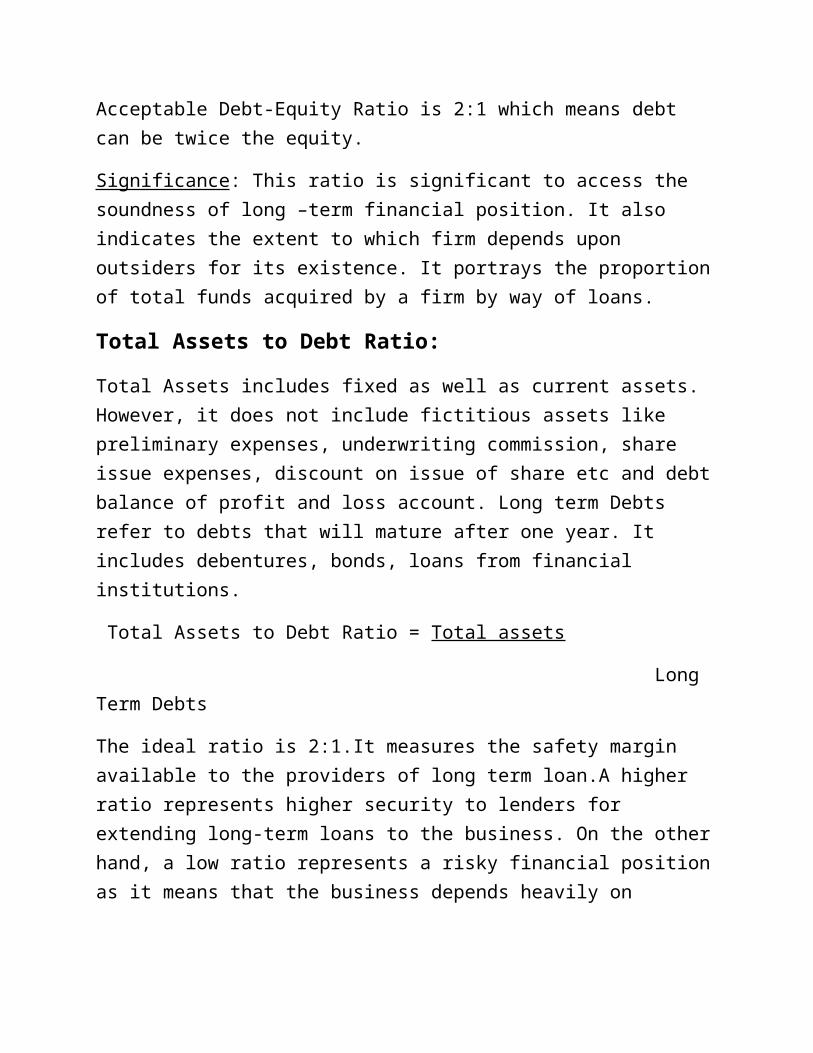

Higher Ratio indicates risky financial position while lower ratio indicates safe financial position. Acceptable Debt-Equity Ratio is 2:1 which means debt can be twice the equity.

Significance: This ratio is significant to access the soundness of long –term financial position. It also indicates the extent to which firm depends upon outsiders for its existence. It portrays the proportion of total funds acquired by a firm by way of loans.

Total Assets to Debt Ratio:

Total Assets includes fixed as well as current assets. However, it does not include fictitious assets like preliminary expenses, underwriting commission, share issue expenses, discount on issue of share etc and debt balance of profit and loss account. Long term Debts refer to debts that will mature after one year. It includes debentures, bonds, loans from financial institutions.

Total Assets to Debt Ratio = Total assets

Long Term Debts

The ideal ratio is 2:1.It measures the safety margin available to the providers of long term loan.A higher ratio represents higher security to lenders for extending long-term loans to the business. On the other hand, a low ratio represents a risky financial position as it means that the business depends heavily on outside loans for its existence. In other words, investment by the proprietors is low.

Proprietary Ratio:

It establishes the relationship between proprietor’s funds and total assets. Proprietors fund means share capital + reserves + surplus, Both of capital and revenue nature. Loss and fictitious assets are deducted. This ratio shows the extent to which the shareholders own the business. The difference between this ratio and 100 represents the ratio of total liabilities to total assets. It is computed as follows:

Proprietary Ratio = Proprietor’s funds or share holders’ funds

Total assets (excluding fictitious assets)

Higher the ratio the better it is for all concerned.

Proprietary Ratio highlights the general financial position of the enterprise. This ratio is of great importance to the creditors to ascertain the proportion of shareholders’ funds in the total assets employed in the firm.

A high ratio indicates adequate safety for creditors, but a very high ratio indicates improper mix of proprietor’s fund and loan funds, which results in lower return on investment. It is because on loans funds, interest is deductible as an expense, thus the enterprise does not pay income tax thereon.

A low ratio indicates inadequacy or low safety cover for the creditors. It may lead to unwillingness of creditors to extend credit to the enterprise.

Nature of facilities

Credit facilities can be funded of non-funded. The funded limits are those where outlay of the bank’s funds is involved.non funded based are those where the bank endorses the commitment or promise made by the borrower and the bank need to meet only if the borrower fails to honour it.

Fund based limits

Fund based limits are generally granted by way of overdrafts, cash credit and bill purchased/discounted.usually the security offered, the purpose, size of advance, repayment ters and requirements of customer decide the type of facility to be granted .

Overdraft and cash credit-

Both cash credit and overdraft are operating accounts through which a borrower if he or she desire can withdraw funds as and when needed up to the credit limit given by the banker to him or her. Under this the borrower can repay the amount anytime, and interest will be charged on amount borrowed and not on the credit limit sanctioned by the bank to the borrower.

This form of borrowing is extremely useful to the borrower because under this borrower can draw the amount as and when required by him and also he has to pay only interest on the amount which he has withdrawn and not on full amount which is sanctioned therefore providing flexibility to the borrower. The difference between cash credit and overdraft is that while under cash credit the security is inventory of the company while under overdraft security is generally the fixed assets of the company (sometimes bank give overdraft facility to the company without any security which is called clean overdraft facility).

Cash credit can of two types, one is key cash credit, in which the possession of goods will be with the banks and other is open cash credit, in which the possession of goods will be with the borrower and not with the bank.

Non fund based limits-

The credit facilities given by the banks where actual bank funds are not involved are termed as 'non-fund based facilities'. These facilities are divided in three broad categories as under:

Letters of credit Guarantees Co-acceptance of-bills/deferred payment guarantees.

Units for the above facilities are also simultaneously sanctioned by banks while sanctioning other fund based credit limits. Facilities for co-acceptance of bills/deferred payment guarantees are generally required for acquiring plant and machinery and may, technically be taken as a substitute for term loan which would require detailed appraisal of the borrower's

needs and financial position in the same manner as in case of any other term loan proposal

LETTER OF CREDIT

Letter of credit is, a method of settlement of payment of a trade transaction and is widely used to finance purchase of machinery and raw material etc. It contains a written undertaking given by the bank on behalf of the purchaser to the seller to make payment of a stated amount on presentation of stipulated documents and fulfilment of all the terms and conditions incorporated therein. All letters of credit in India relating to the foreign trade i.e., export and import letters of credit are subject to provisions of 'Uniform Customs & Practice for Documentary Credits' (UCPDC). These provisions neither have the status of law or automatic application but parties to a letter of credit bind themselves to these provisions by specifically agreeing to do so. These provisions have almost universal application and help to arrive at unambiguous interpretation of various terms used in letters of credit and also set the obligations, responsibilities and rights of various parties to a letter of credit

GUARANTEE

A contract of guarantee can be defined as a contract to perform the promise, or discharge the liability of a third person in case of his default. The contract of guarantee has three principal parties as under: (1) Principal debtor - the person who has to perform or discharge the liability and for whose default the guarantee is given.

(2) Principal creditor - the person to whom the guarantee is given for due fulfilment of contract by principal debtor. Principal creditor is also sometimes referred to as beneficiary.

(3) Guarantor or Surety - the person who gives the guarantee.

Bank provides guarantee facilities to its customers who may require these facilities for various purpose. The guarantees may broadly be divided in two categories as under :

Financial guarantees - Guarantees to discharge financial obligations to the customers.

Performance guarantees - Guarantees for due performance of a contract by customers.

Trade finance

It signifies financing for trade, and it concerns both domestic and international trade transactions. A trade transaction requires a seller of goods and services as well as a buyer. Various intermediaries such as banks and financial institutions can facilitate these transactions by financing the trade.

While a seller (or exporter) can require the purchaser (an importer) to prepay for goods shipped, the purchaser (importer) may wish to reduce risk by requiring the seller to document the goods that have been shipped. Banks may assist by providing various forms of support. For example, the importer's bank may provide a letter of credit to the exporter (or the exporter's bank) providing for payment upon presentation of certain documents, such as a bill of lading. The exporter's bank may make a loan (by advancing funds) to the exporter on the basis of the export contract.

Other forms of trade finance can include Documentary Collection, Trade Credit Insurance, Factoring or forfeiting. Some forms are specifically designed to supplement traditional financing.

Trade finance products

Letter of credit : It is an undertaking/promise given by a Bank/Financial Institute on behalf of the Buyer/Importer to the Seller/Exporter, that, if the Seller/Exporter presents the complying documents to the Buyer's designated Bank/Financial Institute as specified by the Buyer/Importer in the Purchase Agreement then the Buyer's Bank/Financial Institute will make payment to the Seller/Exporter.

Bank guarantee : It is an undertaking/promise given by a Bank on behalf of the Applicant and in favour of the Beneficiary. Whereas, the Bank has agreed and undertakes that, if the Applicant failed to fulfill his obligations either Financial or Performance as per the Agreement made between the Applicant and the Beneficiary, then the Guarantor Bank on behalf of the Applicant will make payment of the guarantee amount to the Beneficiary upon receipt of a demand or claim from the Beneficiary.

Collection and discounting of bills : It is a major trade service offered by the Banks. The Seller's Bank collects the payment proceeds on behalf of the Seller, from the Buyer or Buyer's Bank, for the goods sold by the Seller to the Buyer as per the agreement made between the Seller and the Buyer.

Methods of Working capital assessment

• Operating Cycle Method • Turnover Method.• MPBF method (II method of lending) for limits of Rs 6.00 crores and above • Cash Budget method - Based on procurement and cash inflow) . It is

mainly used for Seasonal Industries (Sugar/ Rice Mills/Textiles/Tea/ Tobacco/Fertilizers) Contractors & Real Estate Developers , Educational Institutions, etc.

Operating Cycle Method

Meaning of operating cycle:

It begins with acquisition of raw materials and ends with collection of receivables.

Stages:

• 1)Raw materials (RM/RM consumption)2)Work-in-process (WIP/COP)

3)Finished Goods (FG/COS)4)Receivables (Debtors/Credit sales)

Less:

• Creditors (creditors/purchases)

Turnover Method :(originally suggested by Nayak Committee for SSI units)

The WC requirements may be worked out on the basis of Naik Committee recommendations for working capital limit upto Rs.6 crores from the banking system, on the basis of minimum of 20% of their projected annual turnover for new as well as existing units, beyond which WC be computed on the basis of WC cycle, after fixing stipulated margins , on each component of the WC. In case of borrowers desiring facilities under Naik Committee recommendations and having a WC cycle of more than 3 months in a year, the WC requirements will be funded after assessing his requirements on the basis of his WC cycle, after fixing proper margins.

Computation:

MPBF Method (Tandon’s II method of lending)

• Working capital gap : Current assets – current liabilities (other than bank borrowings)

• Minimum stipulated net working capital= 25% of current assets (excluding exports receivables)

• Actual projected NWC

Cash budget method

Working Annual Turnover as projected by BorrowerTurnover as accepted by BankCapital Requirement (25% of B)Minimum margin required (5% of B)Actual Margin available (CA - CL)Item C - item DItem C - item EMin. WC Finance - F or G, whichever is less

Credit monitoring assessment(CMA)

Credit management is the management of the credit portfolio of banks and financialinstitutions.Credit management is no longer a rule-of-thumb game .In a highly competitive andderegulated environment, banks and financial institutions have to evolve better systems and procedures to manage the credit needs of highly demanding customers, particularly in the corporate and retail sectors. The developments of the past decadehave totally changed the perspective of management of credit

Stages of credit monitoring:

1.stock statements

2.insurance

3.operations in the account

4.inspection of security

5.Review and renewal of limit

6.balance confirmation

Applicable to seasonal industry(such as tea, sugar)

Specific industry (such as Information Technology and software)

Based on Peak Deficit projected as per cash flow statement

CONCLUSION:I conclude that it was overall a good experience for me.i got to learn much about the working capital finance which was my project topic. I got to know more about the functioning and working of the company. to have a personal contact with the company guide and other people of the company. gained such a vast practical knowledge in this project work. It was great to make contacts with the corporate people and this was a great opportunity for me.