profit & loss conference, economists' panel singapore oct. 2014

TRANSCRIPT

Asia: regional resilience, internal dispersionProfit & Loss Singapore 2014Naomi FinkCEO, Europacifica Consulting

2What to expect when expectations are everything The “taper tantrum” in September showed the

sensitivity of global markets to Fed actions

However, the Fed is also gauging market expectations to time its actions – withdrawal will happen, but when minimum damage may be done

It is inevitable that withdrawal of liquidity will slow activity in some sectors (e.g. commodities, high yield bonds) but some sectors will do better than others… expect greater dispersion.

The question is where does Asia sit in the global context, how vulnerable is it to global expectations for inflation and growth? How will greater dispersion affect Asian currencies?

3

Asia’s relative advantages External position; Surplus-holding Asia still has the luxury of

gradualism in fiscal and monetary consolidation; domestic output gaps are closing gradually, thus policy should remain comparatively accommodative vs. the Fed’s; fiscal positions are not as extreme as Europe’s.

China: China’s investment-consumption shift is likely to be relatively positive for exporters of consumer goods, though negative for raw materials exporters.

Financial sector health, policy leeway: Private sector leverage is one risk, but the financial system is sound, and corporate lending is moderate vs the 1990’s (pre Asia crisis). Ability to loosen Macro-Prudential Policies gives some leeway if strains arise.

Debt/equity mix: A better debt-equity balance than other regions and a trend toward rising equity trading volumes lend capital market support.

Regional integration can help buffer the weaker portions of ASEAN (Indonesia, Thailand) with export diversification boosting productivity

4

Increasing equity interest in Asia is a relative boon

Source: World Federation of Exchanges, IMF

• Growing Asian volume of share trading, lower debt/equity ratios

5

Improving productivity in Asia (unlike Australia)

Source: FRED

6

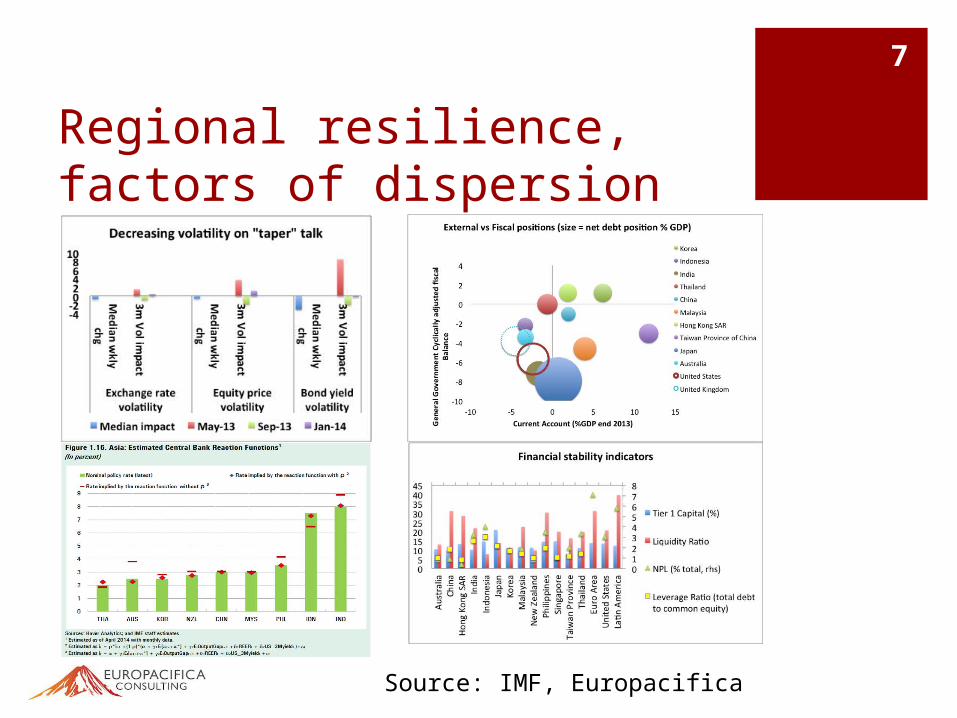

Regional resilience, factors of dispersion Asian asset markets have more recently showed reduced

volatility in comparison to the “Taper tantrum” of September 2013 at times where withdrawal expectations escalate

Asian financial institutions appear sound – their Tier 1 capital is at global (US, European) standards; while their liquidity ratios are slightly lower, NPL balances are much lower than in the rest of the world. Relative financial conditions will be an intra-regional dispersion factor.

External surplus positions in many large Asian economies provide a buffer, while fiscal deficits tend mostly to be slighter than in the US, UK, Australia.

Aside from India, monetary policy rules appear consistent, even without considering serial correlation.

7

Regional resilience, factors of dispersion

Source: IMF, Europacifica

8

One big contingency: competitive conditions! Weaker currencies are exporter boons, and providing risk

aversion is contained, may support capital inflows into stock markets where productivity (and profitability) gradually picks up.

The connection between capital inflows and credit growth (IMF, REO 2014) may prove a drag; then again, flows into stocks vs bonds might prove supportive of Asian economies with well-capitalized equity markets (Singapore, Thailand).

Inflation remaining contained thanks not only to a gradually closing output gap but also to weaker commodity prices is also one contingency.

Continued structural improvement: subsidies for technological development in industry (Malaysia) a longer-term positive to prolong TFP advantage

Trade before capital: regional integration initiatives such as the AEC can help expand goods/services trade in regional currencies, paving the way for increased local-currency capital flows (ASEAN).

9

Long-term valuation (PPP)

Source: World Bank WDI, FRED, XE

24%

56%

36%

16%

42%

12% 50%

1%

0.87 6.1235 12079

107 3.274

1.27513 61.46

32.41

10

Marginal factors for OECD and regional currencies AUD: Over-valued and inflated by a long run of commodity strength;

badly-diversified. Sell.

JPY: Relatively looser policy means weakness vs USD but this will help competitiveness, hence output.

IDR: Relatively bearish among ASEAN currencies thanks to high inflation, external deficit, reform uncertainty.

INR: Bearish vs. ASEAN – alongside weaker fundamentals, could fall behind as ASEAN ramps up productivity.

MYR: Bullish, though likely to under-perform USD. Positive fundamentals and promising reforms. High credit growth remains a risk, however.

SGD: Bullish; likely to under-perform USD; high credit growth remains a risk but positive productivity may help in the long-run.

THB: Hurt by politics and uncertainty ahead of 2015/16 elections but current account position may give it an advantage over IDR.

11

Summary of key views Risk tolerance is likely to be a pre-requisite for Fed liqudiity withdrawal

(which is now strategic). This in turn is likely to push the dollar higher on interest rate differentials, not flight to quality

Sectors most inflated by cheap liquidity – such as commodities – are likely to be the worst-hit. We are bearish on the Australian dollar and comparatively unproductive Australia.

Asian currencies are likely to decline vs. an appreciating dollar, but are likely to weather volatility relatively well thanks to positive fundamentals.

Expect divergence between external surplus holders and debtors, high vs low inflation areas: We like Malaysia and Singapore, remain bearish on Indonesia and India, and look for Thailand to out-perform Indonesia.

Greater integration in the ASEAN region is likely to breed advantages in trade competitiveness, productivity and regional resilience. We would be long ASEAN currencies vs INR.

The link between capital market volatility and domestic credit remains one risk; success of Chinese investment-consumption rebalancing another.

Disclaimer

12

These materials have been prepared by Europacifica Consulting (“Europacifica”), for informational purposes only. The materials are only available for distribution under such circumstances as may be permitted by applicable law and is not intended for use by any person in any jurisdiction which restricts the distribution of this report. Europacifica and/or any person connected with it may make use of or may act upon the information contained in these materials prior to distribution to its customers. Neither the information nor the opinion expressed herein constitute or are to be construed as an offer or solicitation to buy or sell financial products or services. This report has been prepared solely for informational purposes and does not attempt to address the specific needs, financial situation or investment objectives of any specific recipient. This report is based on information from sources deemed to be reliable but is not guaranteed to be accurate and should not be regarded as a substitute for the exercise of the recipient’s own judgment. This report is based upon the author’s own views. Historical performance does not guarantee future performance. Europacifica or its officers, from time to time, may have interest and/or investment in the relevant securities mentioned herein or related instruments and/or may have a position or holding in such securities or related instruments as a result of engaging in such transactions. Furthermore, Europacifica may have or have had a relationship with or may provide or have provided consulting services to any company mentioned herein. All views herein (including any statements and forecasts) are subject to change without notice and neither Europacifica or its officers or affiliates is under any obligation to update these materials. The information contained herein has been obtained from sources Europacifica believed to be reliable but Europacifica does not make any representation or warranty nor accept any responsibility or liability as to its accuracy, timeliness, suitability, completeness or correctness. Europacifica, its officers and affiliates and the information providers accept no liability whatsoever for any loss or damage of any kind arising out of the use of all or any part of this report. Europacifica retains copyright to this report and no part of this report may be reproduced or re-distributed without the written permission of Europacifica Europacifica expressly prohibits the distribution or re-distribution of this report to Private Customers, via the Internet or otherwise and Europacifica, its officers or affiliates accept no liability whatsoever to any third parties resulting from such distribution or re-distribution. Copyright © 2014 Europacifica Consulting, Pasadena, California.www.europacifica.com