probable advantages and disadvantages of branch … branch unit banking banking banking arkansas...

TRANSCRIPT

PROBABLE ADVANTAGES AND DISADVANTAGES OF BRANCH BANKING

FOR THE STATE OF KANSAS

by

ROBERT MELVIN DEAVER

B. A., Kansas State University, 1965

A MASTER'S REPORT

submitted in partial fulfillment of the

requirements for the degree

MASTER OF ARTS

Department of Economics

KANSAS STATE UNIVERSITYManhattan, Kansas

1966

Approved by:

Major Professor

ir-D

MI960"Q 3l$S table of contents

CD-Page

LIST OF TABLES , . iv

Chapter

I. INTRODUCTION 1

The Changing Nature of Kansas and Possible Need ForChanges in Kansas Banking Laws

The Growth of Branch Banking in Both Kansas and theUnited States

II. THE DIFFERENT FORMS OF BANKING 6

Unit, Correspondent, Branch, Group, and Chain BankingThe Different Types of Branch Banking

III. THE 'DUAL" BANKING SYSTEM IN THE UNITED STATES 13

The "Dual" Banking SystemFederal Banking LawKansas Banking Law

IV. BRANCH BANKING IN OTHER STATES 19

The ExtentSome Banking Laws in Other States

V. BRANCH BANKING STUDIES 25

Horvitz StudiesArizona—New Mexico Study

VI. ADVANTAGES AND DISADVANTAGES OF BRANCH BANKING FORKANSAS 34

The "Traditional" Arguments Given For and AgainstBranch Banking

Growth in the Number of Suburban Banks in WichitaSince 1950

More Extensive Branch Banking for Kansas

ii

TABLE OF CONTENTS (continued)

CONCLUSIONS , 42

ACKNOWLEDGMENTS 44

REFERENCES 45

iii

LIST OF TABLES

Table H§»

1. Urban Versus Rural Population in Kansas for the "euro

1940, 1950, and 1960 1

2. Population Growth in Wichita and Topeka--Selected Years . . 2

3. Number of Branch Banking Systems and Unit Banks in the

United States by Selected Years from 1900-1962 4

4* Commercial Banks and Branches in Kansas by SelectedYears from 1919-1964 5

5. Banks in Kansas, 1953-1962 14

6. Classification of States by Branching Law 19

7. Number of Commercial Banks and ConcentrationDecember 31, 1962 20

8. The Banking Laws of Some States Permitting LimitedDegrees of Branch Banking ..... 24

9. Growth in the Number of Wichita Banks (1950 to 1965) ... 39

iv

CHAPTER I

INTRODUCTION

The Changing Nature of Kansas and Possible Need

For Changes in Kansas Banking Laws

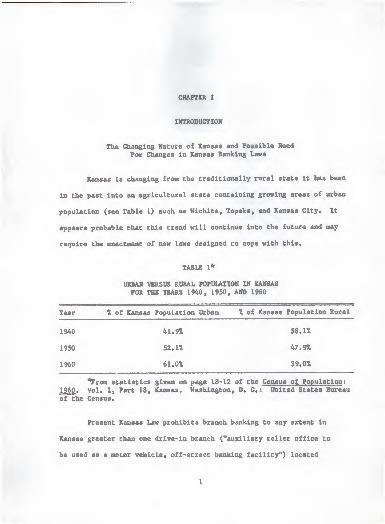

Kansas is changing from the traditionally rural state it has been

in the past into an agricultural state containing growing areas of urban

population (see Table 1) such as Wichita, Topeka, and Kansas City* It

appears probable that this trend will continue into the future and may

require the enactment of new laws designed to cope with this*

TABLE 1*

URBAN VERSUS RURAL POPULATION IN KANSAS

FOR THE YEARS 1940, 1950, AND 1960

Year X of Kansas Population Urban I of Kansas Population Rural

1940 41.91 58.11

1950 52.1% 47.91

1960 61.0% 39.0X

*Prom statistics given on page 18-12 of the Census of Population ;

1960 . Vol. I, Part 18, Kansas. Washington, D. C. : United States Bureau

of the Census.

Present Kansas Law prohibits branch banking to any extent in

Kansas greater than one drive-in branch ("auxiliary teller office to

be used as a motor vehicle, off-street banking facility") located

within 2,600 feet of the bank which operates it. 1 Some of the city

bankers in Kansas feel that this law is too restrictive on then and

places then in a "squeese." They suggest that, although this law

may be adequate for the rural areas in Kansas, it does not give the

banks in the major urban areas of Kansas sufficient leeway to deal

with their probleaa. As the major cities in Kansas are growing (see

Table 2). and more and more people are moving to the suburbs, "these

banks feel that they must move along with their customers or lose

valuable accounts.'..2

TABLE 2*

POPULATION GROWTH IN WICHITA AND TOPEKA—SELECTED TEARS

-:,

.,,)':,

";i:

Year

City 1940 1950 1960 1965

Wichita

Topeka

114,966

67,833

168,279

78,791

254,698

119,484

approx. 275,000

approx. 127,500

*?rom statistics given on page 18-28 of the Census of Population ;

I960 . Vol. I, Part 18, Kansas. Washington, D. C. : United States Bureau

of the Census; and from statistics given in the Rand McNally International

Bankers Directory, The Bankers Blue Book (Chicago, Illinois: Rand McNally& Company, Final 1965 Edition).

Wichita is the outstanding example of this phenomenon in Kansas.

In 1950, there were 6 banks in Wichita; in 1965, there were 14 banks in

Section 1, Chapter 72 of Senate Bill No. 105 (from the Laws of

Kansas—1957)—Banks and Banking. Approved April 5, 1957.

2United States House of Representatives, Banking Concentration

and Small Business (4 Staff Report to the Select Committee on SmallBusiness. 86th Congress, 2nd Session, December 23, 1960), p. 48.

3

Wichita--an Increase of 8 banks (133 1/3 per cent). 1 Seven of the eight

new banks since 1950 were suburban banks, 2 and it seems reasonable to

assume that the existing downtown banks could have efficiently handled

a portion of this growing suburgan business, if they had been permitted

to do so under a more liberal banking law in Kansas. Some of the city

banks feel that the present banking law is tending to "stifle" the

growth of the downtown banks in the three main metropolitan areas of

Kansas; and yet, they are afraid to "speak out" for fear of antagonizing

the small banks in Kansas and losing correspondent business from them.

Small banks usually fear—and perhaps with some basis—that large

"monopolistic banking empires" would be built as a result of banking laws

which would be liberal enough to permit city banks to buy up large num-

bers of small, rural banks in areas of the state far distant, both econ-

omically and geographically, from the buying city banks. The rational

answer to this problem would seem to be a more liberal banking law

for the three major metropolitan areas in Kansas and yet a retention

of the present banking law for the rest, or more rural part, of Kansas.

Later, as cities such as Salina, Hutchinson, and Lawrence grow and

develop, perhaps a third area of banking law could be created which

would meet their needs—somewhat more restrictive than that for the

major metropolitan areas and yet more liberal than for the rural areas.

Rand McNally International Bankers Directory, The Bankers BlueBook (Chicago, Illinois: Rand McNally & Company), Final 1950 andPinal 1965 Edition.

HThe 8th bank was The Wichita State Bank, a new downtown bank(across the river, and about % mile from the other downtown banks).

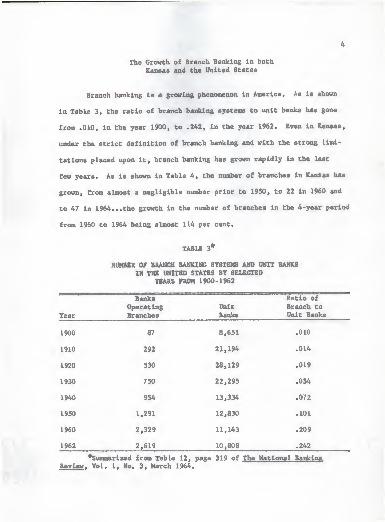

The Growth of Branch Banking in both

Kansas and the United States

Branch banking is a growing phenomenon in America. As is shown

in Table 3, the ratio of branch banking systems to unit banks has gone

from .010, in the year 1900, to .242, in the year 1962. Even in Kansas,

under the strict definition of branch banking and with the strong limi-

tations placed upon it, branch banking has grown rapidly in the last

few years. As is shown in Table 4, the number of branches in Kansas has

grown, from almost a negligible number prior to 1950, to 22 in 1960 and

to 47 in 1964... the growth in the number of branches in the 4-year period

from 1960 to 1964 being almost 114 per cent.

TABLE 3*

NUMBER OF BRANCH BANKING SYSTEMS AND UNIT BANKS

IN THE UNITED STATES BY SELECTEDYEARS FROM 1900-1962

Year

BanksOperatingBranches

Unit

Banks

Ratio Of

Branch toUnit Banks

1900 87 8,651 .010

1910 292 21,194 .014

1920 530 28,129 .019

1930 750 22,295 .034

1940 954 13,334 .072

1950 1,291 12,830 .101

1960 2,329 11,143 .209

1962 2,619 10,808 .242

^Summarised from TableReview. Vol. 1, No. 3, March

12,1964.

page 319 of The National Banking

TABLE 4'

Year

1919

1934

1946

1950

1960

1964

COMMERCIAL BANKS AND BRANCHES IN KANSASBY SELECTED YEARS FROM 1919-1964

Banks Branches

1,304

752

614

612

587

594

1

22

47

Total

1,304

752

615

612

609

641

Summarized from Table 3, p. 25 of The Banking Structure inEvolution , The Administrator of National Banks, United StatesTreasury, 1964.

In the United States branch banking "is growing in both relative

and absolute importance." 1 Today, branches of banks make up "nearly

one-half of all commercial banking offices in this country. This is

in contrast to earlier periods when, as recently as 1949, branches of

banks accounted for less than one-quarter of the total number of bank-

ing offices."2

iLeland J. Pritchard, Money and Banking (Boston, Massachusetts:Houghton Mifflin Company, 1964), p. 132.

'Ibid.

CHAPTER II

THE DIFFERENT FORMS OF RANKING

Unit, Correspondent, Branch, Group, and Chain Banking

In spite of the inroads branch banking has made on our banking

structure in the United States, we are still considered to have a unit

banking system. We have more than 10,000 banks (see Table 3), while in

England and Wales five banks and their branches account for three-

fourths of the banking resources—and branch offices* Canada, for

instance, has only eleven chartered banks, three of which "dominate

the field of commercial banking." 1

A unit bank can be defined as a single-bank corporation which

operates only one banking office and is not related to other banks,

either through ownership or control. A unit bank is not controlled

by another bank, person, group, or corporation: and it does not itself

control other banks.

Correspondent banking acts as a supplement to the unit banking

system. It works in the following manner: smaller, outlying banks main-

tain "non- interest bearing accounts" with their city correspondent banks.

Hf. H. Steiner, Eli Shapiro, and Ezra Solomon, Money and Banking .

An Introduction to the Financial System (New York: Holt, Rinehart andWinston, Inc., 1958), p. 86.

Pritchard, p. 131.

7

In return for this, these city correspondent banks provide check clearing

services, aid in buying and selling bonds, banking and technical infor-

mation, and other services for these smaller banks. If the customer of

a small bank wants trust services, a larger loan than the "loan limit"

of the smaller bank, or other services which the smaller bank wouldn't

otherwise be able to provide on its own; this bank is able to provide

these things through the aid of its larger, city correspondent bank.

Branch banking exists when a single banking corporation, having

one group of directors and one charter, directly owns and operates more

than one banking office...with each local office being supervised by a

manager appointed by the officers of the bank. 2 Once a branch banking

corporation exists, there are two ways in which it can expand* It can

expand by buying up, or emerging with, existing banks; or it can expand

by forming de novo * or new branches.

The following passage from, Biography of a Bank, The Story of the

Bqnk of AffWrl^fi gives a good description of the workings branch banking:

Loans are made direct by the branches, except in instances wherethe amount is unusually large or the branch manager wishes to secure

the advice of the head office credit department. The customers of

the branch deal with the local officers, and only in extraordinarycircumstances are they brought into contact with the head officedepartments. Each branch has a general lending limit fixed by the

bank's finance committee. Within this limit each branch may lend

and report without previous consultation with the head office.

These limits vary with the proven credit capacity of the various

Banking and Monetary Studies , edited by Deane Carson (Homewood,Illinois: Richard D. Irwin, Inc., 1963), pp. 301-302.

2W. H. Steiner, Eli Shapiro, and Ezra Solomon, p. 87.

branch loaning officers. ... All applications for unfixed lines

of credit in excess of the lending limit of a given branch are

promptly considered and acted upon by the proper central credit

department and proper advice and instructions issued. The broad

fundamental policies respecting credits are outlined by the general

executive committee and application is then made by the credit

department.

*

Each branch of a branch banking corporation carries on the same

kind of activities performed by unit banks; however, trust, investment,

and other kinds of specialized banking services are usually limited to

the main office and to the larger branches. In communities too small to

support a full-scale bank, a branch may be little more than a "teller's

window" limited to receiving and paying deposits and taking applications

for loans. In other communities where there is a need for some banking

services, but not on a full-time basis, branch offices operating on a

part-time basis are capable of taking care of the banking needs ...and

although branches located in quite small communities may have only the

minimum of facilities, they are able to arrange through the head office

2for all types of banking services.*

Group banking refers to an arrangement by which two or more

separately incorporated banks are under the control of a holding company,

or separate corporation. 3 This holding company controls banks that have

, , I I , | | ||

- . . . . i —

.

t

Marquis James and Bessie Rowland James, Biography of a Bank ,

The Story of Bank of America (New York: Harper & Brothers, 1954),

p. 90.

2Gerald C. Fischer, Bank Holding Companies (New York: Columbia

University Press, 1961), p. 47.

"

Tinancial Institutions » edited by Roland I. Robinson (Homewood,

Illinois: Richard D. Irwin, Inc., 1960), p. 136.

9

separate charters and boards of directors. 1 According to Gerald C.

Fischer in his book, Bank Holding Companies , "economies and efficiencies"

exist in group banking, but not to the degree that they exist in branch

banking. According to Fischer:

Many of the problems of the small bank owner can be solved through

the formation of a group of cooperating banks. The marketability

of shares can be improved, specialists can be employed, elaborate

machinery can be installed at the headquarters to serve the members,

and numerous other advantages of a sizable branch system can be en-

joyed without the considerable sacrifice of local autonomy whichoccurs in a branch system.

2

From the banks that Fischer had analyzed for his study, he came to

the conclusion that, "The group system has been able to offer considerable

financial gain to the stockholder of a small bank. The holding company's

shares, when an exchange of stock occurred, were usually more marketable,

provided a higher rate of return on book value, and resulted in a tax

saving for the owners. "3

According to the Federal Bank Holding Company Act of 1956, a bank

holding company is defined as any company owning 25 per cent or more of

the voting shares of two or more banks or which in any manner controls

the election of a majority of directors of two or more banks. Holding

companies are required to register with the Board of Governors of the

Federal Reserve System and to obtain consent to acquire more than 5 per

cent of the voting stock of any bank. No bank holding company is permitted

Marquis James and Bessie Rowland James, p. 298.

rischer, p. 141.

3Ibid . . p. 140.

10

to acquire ownership or control in any company other than a bank. 1

Chain banking is quite similar to group banking, except that the

control of two or more banks is held by one individual, or by a group

of individuals, through interlocking directorstes--the same man, or

men, sitting on several boards of directors. Chain banking has pri-

marily been a development in agricultural areas and has achieved its

greatest significance "in a few middle western states where branch

banking is prohibited."2

According to Mr. Carl A. Bowman, Executive Secretary of the Kansas

Bankers Association, chain banking "isn't significant in the state of

Kansas."3 Mr. Bowman said that, primarily, only two chain banking systemi

operate in the state of Kansas~"the Chandler banks" and those owned by

a man named "C. H. Goppert"--but that they don't significantly influence

banking in Kansas. According to Mr. Bowman, one of the major advantages

of chain banking, as it exists in Kansas, is that it has certain ad-

vantages in buying securities—for example, in being able to buy munici-

pal bonds in larger blocks.

^

Satellite or affiliate banking is somewhat similar to chain

banking, but according to Mr. A. K. Davis, President of the American

Financial Institutions , p. 137.

Ibid., p. 139.

3From an interview with Mr. Bowman in June of 1966.

4Ibid.

11

Bankers Association, it "has some resemblance to chain banking but

control is somewhat looser." 1

Branch banking, group (or holding company) banking, and chain

(and affiliate) banking are similar to each other in that they are all,

"devices whereby several banks are brought under a single control. "2

In states where branch banking is prohibited by law, these other forms

have a tendency—when not prohibited by law—to come into existence.

According to Mr. Carl Bowman, there are 33 one-bank holding com-

panies in Kansas. They are permitted by Federal and State law—and are

not covered by the Federal Bank Holding Company Act of 1956—because

they affect only one bank. The advantage of these, according to Mr.

Bowman, is that they are a way in which a young banker can gain control

of a bank- -for example, through the use of an Insurance Agency as a

holding company. Again, as with chain banking, these aren't a par-

ticularly "significant" influence in Kansas banking, said Mr. Bowman. 3

The Different Types of Branch Banking

Branch banking may vary greatly in its scope or extent. Branch

banking may be nation-wide, such as it is in Canada or in England; it

may be state-wide, as it is in California; or it may be limited to a

—^——^—^—^—^—— .... ...r ,--, . , ,|inin , M a ia a, nm M , m i , lt _x . i n » i mijwii» u ,±. ..

Hte Must Keep Building (Address of Archie K. Davis, President, TheAmerican Bankers Association, before the Midwinter Meeting of the OhioBankers Association, Sheraton Columbus Hotel, Columbus, Ohio, Friday Noon,February 18, 1966.)

2United States House of Representatives, Banking Concentration and

Small Business (A Staff Report to the Select Committee on Small Business.86th Congress, 2nd Session, December 23, 1960), p. 2.

^rom the interview with Mr. Bowman in June of 1966.

12

geographic, or economic region within a state. Several of the possible

geographic limitations to branch banking within a state are as follows:

branch banking within the "city limits" of the major cities of a state;

branch banking within, say, 15 miles of the city limits of the major

cities of a state 1 or branch banking, 'within the head-office county

or counties contiguous to it. "2

Branching may be limited to certain "regions" within a state.

A state legislature may divide a state into regions- -within which banks

are permitted to branch and merge, subject to certain restrict ions- -using

geographic and economic factors as criteria in establishing the borders

for these regions. For example, in New York State, 1934 legislation

divided the state into 9 banking regions, or districts, designed to

work in this manner. 3

The Monopolistic Character of Branch Banking (An Address given

in 1965 by John F. McCarthy, President, Illinois Bankers Association.)

Pritchard, p. 133.

3New York State Banking Department, Branch Banking. Bank Mergers

and The Public Interest (January, 1964), p. 8.

CHAPTER III

THE "DUAL' 1 BANKING SYSTEM IN THE UNITED STATES

The "Dual" Banking System

The "Dual Banking System" in the United States, with the co-

existence of national banks and of banks chartered by the SO states,

is unique among the nations of the world. 1 This system "springs

from the continuing conflict between Federal power and States rights

which has characterized American politics over the years."2

Table 5 gives a comparison between the number of national banks

and state banks in Kansas during recent years--1953 to 1962.

In the United States, as of December 31, 1958, only 34 per cent

of the total number of commercial banks were national banks, and yet

they held over 50 per cent of all commercial bank deposits. Thus,

although national banks are of a larger average size in the nation as

a whole, the larger number of state banks exists because, "State regu-

lations, in general, permit more freedom in the use of funds and an

enhanced earning position when compared with national regulation."3

united States House of Representatives, Banking Concentration andSmall Business (A Staff Report to the Select Committee on Small Business.86th Congress, 2nd Session, December 23, 1960), p. 1.

2Ibid.

financial Institutions , pp. 128-129.

13

14

TABLE 5W

BANKS IN KANSAS, 1953-1962(DECEMBER 31)

Year National Banks State Banks Total

1953 172 434 606

1954 170 432 602

1955 170 431 601

1956 170 428 598

1957 169 426 595

1958 169 424 593

1959 169 424 593

1960 167 420 587

1961 167 423 590

1962 168 425 593

Froi

, Int.

a Table 1. page 19, An Evaluation of Commercial Banking in

Kansas ernal Report to the Kansas Bankers Association, by Philip B.

Hartley and Robert D. Schrock.

Federal Banking Law

Generally speaking, national banks operating within a given state

are subject to the same limitations and restrictions as the state banks

operating within that state in respect to branch banking. Thus, in a

state where branch banking is permitted by the state law, national banks

may establish and operate branches to the same extent that the state

banks are permitted to do so. In a state where branch banking is pro-

hibited by the state law, national banks are held to the same restrictions

as the state banks... and thus are not permitted to establish branches.

The following are the major provisions of federal laws relating

to the establishment of branches—as a result of the Federal Reserve

Act of 1913, the McFadden Act of 1927, the Banking Acts of 1933 and

1935, and various rulings of the Board of Governors and the Comptroller

of the Currency:

15

1. Both national and state member banks may establish branches

in their main office cities if the laws of the state specifically

authorise state banks to establish such branches. They may also

establish state-wide systems if state law allows, with the proviso

that member banks must meet the minimum capital requirements fixed

by federal law. The effect of this provision is to make total

capital requirements much more onerous than is required by most

state laws.

2. The approval of the Comptroller of the Currency for national

banks and the approval of the Board of Governors for state member

banks is required before any branch may be moved or established.

3. State banks that are insured by the FDIC but are not members

of the Federal Reserve may not establish or move a branch without

the consent of the FDIC, but there is no other quantitative re-

striction by the FDIC. 1

Therefore, in summary, a national bank generally, "has the same

right to establish branches as it would if it were a state bank, except

that there are special requirements as to capital and the approval of

the Comptroller of the Currency is required."2

Kansas Banking Law

As stated previously in this paper, present Kansas Law prohibits

branch banking to any extent in Kansas greater than one drive-in branch

located within 2,600 feet of the branch which operates it. This is an

oversimplification of the banking law in Kansas, so at this point it

seems appropriate to give complete quotations of the portions of Kansas

law pertaining to branch banking and bank holding companies. The follow-

ing deals with the establishment of bank branches in Kansas:

Fritchard, p. 133.

2Gavin Spofford, Guideposts for Banking Expansion (New Brunswick,

New Jersey: Rutgers University Press, 1961), p. 157.

16

SECTION 1. Section 9-1111 of the General Statutes of 1949 ishereby amended to read as follows: Sec. 9-1111. The generalbusiness of every bank shall be transacted at the place of busi-ness specified in its certificate of authority, and it shall beunlawful for any bank to establish and operate any branch bank,or branch office or agency or place of business: Provided, Thatany bank domiciled in this state may, or two (2) or more suchbanks may jointly establish and maintain not more than one (1)

detached or attached auxiliary teller office to be used as amotor vehicle off-street banking facility, such office to belocated within two thousand six hundred (2,600) feet of the pre-mises specified as its place of business in its certificate ofauthority, but not within fifty (SO) feet of another nonpartici-pating bank or auxiliary teller office thereof: Provided, how-ever, That the services of such teller office be limited to re-ceiving deposits of every kind and nature, cashing checks ororders to pay, issuing exchange, and receiving payments payableat the bank.

i

The following is the Kansas Law pertaining to bank holding

companies

:

9-504. Bank holding companies; prohibited acts; definitions.For the purpose of this act, the following definitions shallgovern:

(a) "Bank holding company" means any company: (1) Whichdirectly or indirectly owns, controls, or holds with power tovote, twenty-five percent (251) or more of the voting shares oftwo (2) or more banks or of a company which is or becomes a bankholding company by virture of this act; (2) which controls inany manner the election of a majority of the directors of eachof two (2) or more banks; or (3) for the benefit of whose share-holders or members twenty-five percent (251) or more of the vot-ing shares of each of two (2) or more banks or a bank holdingcompany is held by trustees; and for the purposes of this act,any successor to any such company shall be deemed to be a bankholding company from the date as of which such predecessor com-pany became a bank holding company. Notwithstanding the fore-going (A) no bank shall be a bank holding company by virtueof its ownership or control of shares in a fiduciary capacity,except where such shares are held for the benefit of the share-holders of such bank.

2

^The Laws of Kansas . Chapter 72, Senate Bill No. 105, Section 1,Approved April 5, 1957.

2 c1959 Supplement to General Statutes of Kansas 1949 . $ 9-504.

17

9-505. Same; unlawful acta. It ehall be unlawful for any bank

holding company, aa defined in aection 1 (9-504) hereof: (1) To

take any action which reaulta in a company becoming a bank holding

company as defined in this act; (2) for any bank holding company

to acquire direct or indirect ownership or control of any voting

shares of any bank if, after such acquisition, such company will

directly or indirectly own or control more than twenty-five percent

(251) of the voting sharea of two or more banks; (3) for any bank

holding company or subsidiary thereof, other than a bank, to ac-

quire all or substantially all of the assets of a bank; or (4)

for any bank holding company to merge or consolidate with any other

bank holding company. Notwithstanding the foregoing, this prohi-

bition shall not apply to: (A) Shares acquired by a bank, (1)

in good faith in a fiduciary capacity, except where such shares

are held for the benefit of the shareholder of such bank, or (2)

in the regular course of securing or collecting a debt previously

contracted in good faith, but any shares acquired after the date

of enactment of this act in securing or collecting any such pre-

viously contracted debt in excess of the number of shares permitted

under the terms hereof as hereinbefore set forth shall be disposed

of within a period of two years from the date on which they were

acquired; or (B) additional shares acquired by a bank holding com-

pany in a bank in which auch bank holding company owned or controlled

a majority of the voting shares prior to such acquisition. 1

Thus, in essence, the Kansas Law pertaining to bank holding com-

panies "restricts the expansion of existing bank holding companies and

forbids the organisation of new companies."2

In 1961, a bill pertaining to branch banking was before the House

of Representatives and Senate of the state of Kansas, but it failed to

pass. It was introduced on February 10, 1961, in the House of Repre-

sentatives as a bill which would extend the 2,600 foot limitation to

3,600 feet (other distances were proposed before the bill was killed,

one for 6,500 feet). This proposed extension of the distance for

auxiliary teller offices was intended to be statewide. On March 30, 1961,

1959 Supplement to General Statutes of Kansas 1949 . 5 9-505.

2Fischer, p. 169.

18

the Senate Banking Committee "reported that; the limitation be left

at 6^500 feet for banks in Wyandotte and Johnson counties (as based

on amounts relating to population and total assessed taxable tangible

valuation) and for all other counties jthej limit be 2,600 fee."

On April 5, a vote of 19-19 in the Senate killed this bill.

Even if the Senate had passed this measure, it "would. . .have been

subject to concurrency by the House in the Senate amendments or non-

concurrence 1,7 which would have thrown the bill into conference pro-

cedures between the two houses."2

Hfhe Kansas Banker , published monthly by the Kansas BankersAssociation, Topeka, Kansas, April, 1961, p. 15.

2Ibid.

CHAPTER IV

BRANCH BANKING IN OTHER STATES

The Extent

Kansas Laws restrict branch banking to such a great extent--to

"auxiliary teller offices" instead of full fledged branches capable

of performing numerous other banking services—that, when considered

with other states, Kansas is grouped with those which in effect have

unit banking. Under somewhat general criteria, the following is a

classification of the 50 states according to their banking laws:

TABLE 6*

CLASSIFICATION OF STATES BY BRANCHING LAW

(1963)

AlaskaArizonaCaliforniaConnecticutDelawareHawaiiIdahoMaineMarylandNevadaNorth CarolinaOregonRhode IslandSouth CarolinaUtahVermontWashington

AlabamaGeorgiaIndianaKentuckyLouisianaMassachusettsMichiganMississippiNew JerseyNew MexicoNew YorkOhioPennsylvaniaSouth DakotaTennesseeVirginiaWisconsin

Statewide Limited'

Branch Branch UnitBanking Banking Banking

ArkansasColoradoFloridaIllinoisIowaKansasMinnesotaMissouriMontanaNebraskaNew HampshireNorth DakotaOklahomaTexasWest VirginiaWyoming

*From Appendix A, page 341, Paul M. Horvitz"Branch Banking and the Structure of Competition,"Review , Vol. 1, No. 3 (March, 1964).

19

and Bernard Shull,The National Banking

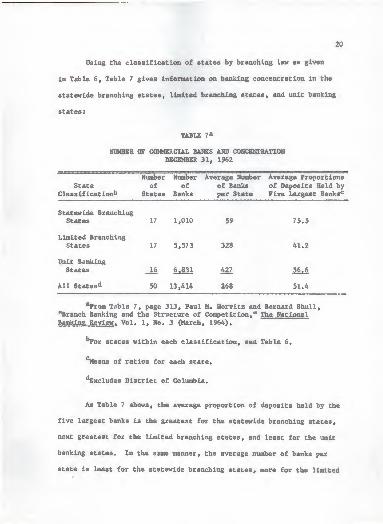

Using the classification of states by branching law as given

in Table 6, Table 7 gives information on banking concentration in the

statewide branching states, limited branching states, and unit banking

states

:

TABLE 7*

NUMBER OF COMMERCIAL BANKS AND CONCENTRATIONDECEMBER 31, 1962

Statewide BranchingStates 17 1,010 59

Limited BranchingStates 17 5,573 328

Unit BankingStates 16 6,831 127

All States'* 50 13,414 268

Number Number Average Number Average ProportionsState of of of Banks of Deposits Held by

Cla8sificationb States Banks per State Five Largest Banksc

75.5

41.2

51.4

aFrom Table 7, page 313, Paul M. Horvitz and Bernard Shull,"Branch Banking and the Structure of Competition," The NationalBanking Review . Vol. 1, No. 3 (March, 1964).

"For states within each classification, see Table 6.

cMeans of ratios for each state.

"Excludes District of Columbia.

As Table 7 shows, the average proportion of deposits held by the

five largest banks is the greatest for the statewide branching states,

next greatest for the limited branching states, and least for the unit

banking states. In the same manner, the average number of banks per

state is least for the statewide branching states, more for the limited

21

branching states, and greatest for the unit banking states.

At this point> the reader may want to refer again to Table 3 on

page 4 of this paper, which shows the increase in the number of banks

operating branches and the increase in the ratio of branch to unit

banks in the United States.

Some Banking Laws in Other States

In this paper we have divided the state banking laws into three

categories: statewide branch banking, limited branch banking, and unit

banking. The Kansas banking law, previously given in this paper, is an

example of a state law permitting only unit banking. It limits branch-

ing to such an extent that only "auxiliary teller offices" are permitted

instead of "true" branches; thus, in effect, only a unit banking system

exists in Kansas. Texas is an even better example of a state having a

unit banking system than Kansas. In Texas "an express prohibition of

branch banking is contained in the constitution of the State, as well

as in the statutes." 1 The following is the applicable part of the

Texas Constitution: "...Such body corporate (banking corporation)

shall not be authorized to engage in business at more than one place

which shall be designated in its charter...."2 The relevant part

of the Texas Civil Statutes is: "No State, national or private bank

^United States House of Representatives, Banking, Concentrationand Small Business , p. 32.

Texas Constitution, art. 16, sec. 16. (from, Banking Concen-

tration and Small Business , p. 32).

22

shall engage in business in more than one place, maintain any branch

office, or cash checks or receive deposits except in its own banking

house."1

California is a good example of a state which permits statewide

branch banking. The following is the portion of California Law which

pertains to its branch banking:

500. When authorised by the superintendent as provided in thischapter, a bank or trust company, pursuant to a resolution of itsboard of directors, may establish and maintain one or more branchoffices within the State.

501. The request for authority to establish a branch office shallbe set forth in an application in such form and containing such in-formation as the superintendent may require and shall be accompaniedby an application fee of one hundred dollars ($100) for each newbranch office.

502. Before opening a branch office a bank or trust companyshall have and shall thereafter maintain as long as the branch isoperated, for each branch so opened paid-up capital in additionto the paid-up capital required by Chapter 3 of this division,equal to the following:

(a) If the branch office will be located in the city inwhich the head office of the bank is located or in a city inwhich the bank has already established a branch office, fiftythousand dollars ($50,000).

(b) If the branch office is to be located elsewhere, theamount required by Chapter 3 of this division to open a newbank in the place in which the branch will be located, exclu-sive of the amount required for a trust department.

(c) If the branch is to engage in no other banking businessthan the trust business, fifty thousand dollars ($50,000).503. The superintendent may give or withhold his approval of an

application in his discretion but he shall not approve an applicationuntil he has examined into the matters referred to in subdivisions0>)» (c), and (f) of Section 361 and until he has ascertained to hissatisfaction that the following are true:

(a) That the public convenience and advantage will be pro-moted by the establishment of the proposed branch office.

(b) That the bank or trust company has the capital requiredby Chapters 3 and 4 of this division.

2

LArt. 342-903, Vernon's Civil Statutes of Texas, Anno, (from,

Banking Concentration and Small Business , p. 33).

'State of California, Banking Law and Related Acts . December 31,1962, pp. 17-18, Chapter 4, Article 1, ^500 to 503.

23

507. When authorized by the superintendent a bank or trust

company may change the location of a branch office from one loca-

tion to another in the same vicinity. 1

The concepts of "unit banking" and '•statewide branch banking" are

fairly clear-cut because they represent the two extremes; but between

these two extremes the possibility exists for many different forma,

and degrees, of branch banking. Table 8 gives some of these various

forms which branch banking may take, as they exist in the United States

(this listing of states isn't intended to coincide exactly with the list

of "Limited Branch Banking" states, as given in Table 7, page 20 of this

paper)

:

1Ibid . . p. 18,^507,

24

TABLE 8*

THE BANKING LAWS OF SOME STATES PERMITTING

LIMITED DEGREES OF BRANCH BANKING

(1959)

Alabamal New Mexico6

Arkansas2 New York7

Georgia3 North Dakota^

Indiana1 Ohio2

Iowa^ Pennsylvania2

Kentucky1 Tennessee 1

Massachusetts 1 Utah1

Michigan2 Virginia1

Mississippi5 Alaska^

New Jersey1 Hawaii8

1Permits branches within the city and county of head office.

Permits branches within city, county, or county contiguous to

county of head office.

3Permits banks in certain classes of cities to establish brancheswithin limits of city of head office.

Sennits only "offices," "agencies," or "stations" for limitedpurposes, as distinguished from branches.

Permits branches within 100-mile radius of head office.

Permits banks to establish branches within the county or countycontiguous to the county in which the parent bank is located, or withina certain distance of the parent bank.

Permits banks to establish branches within the limits of thebanking district in which the parent bank is situated.

aPermits branches within certain zones.

From Table XVII, page 35, United States House of Representatives,Banking Concentration and Small Business , A Staff Report to the SelectCommittee on Small Business, 86th Congress, 2nd Session (December 23,1960).

CHAPTER V

BRANCH BANKING STUDIES

Horvitz Studies

Paul M. Horvitz of Boston University is a Senior Economist in the

Department of Banking, Office of the Comptroller of the Currency, Wash-

ington, D. C. He has published material on such topics relating to

branch banking as, "Economies of Scale in Banking," "Branch Banking

and the Structure of Competition," and "The Impact of Branch Banking

on Bank Performance"--the last two of which he has done in conjunction

with Bernard Shull, another Senior Economist in the Department of Bank-

ing. Some of the conclusions and findings given in these articles will

be reported here without an attempt being made to explain the studies

and statistics used to arrive at these conclusions. From the descrip-

tions given of these studies, it appears that they were carefully

thought out and interpreted; and generally, the tone of their "find-

ings" supported the case for statewide branch banking.

The major results and findings in the article, "Branch Banking

and the Structure of Competition," by Horvitz and Shull are as follows:

over the last decade branch banking has been associated with a de-

clining number of banks, and there are far fewer banks in the branch

banking states than in the unit banking states. In recent years,

though, the decline in the number of banks has slowed down despite

25

26

the continued rapid expansion of branch banking. In the non-

metropolitan areas of the United States, on the average, there are

no fewer competitors in the branch banking states than in the unit

banking states in the most important banking markets—especially, the

local market. Banking concentration is typically higher in the

metropolitan areas of branch banking states than it is in the metro-

politan areas of unit banking states, but it is very high in both,

and there is no evidence that the difference is economically signi-

ficant. The economic barriers to entry in banking are low in com-

parison to such barriers in manufacturing, and they are probably

somewhat lower under branch banking than under unit banking. 1

In this article, they stated that:

Our analysis suggests that neither in terms of number of com-

petitors, nor concentration..., nor in terms of the condition of

entry (potential competition) have the structures of local bank-

ing markets been adversely affected by branch banking in the

United States. The weight of evidence suggests that, to the con-

trary, market structures are adversely affected by restrictions

on branch banking.

2

The results of one of their studies, reported in this article,

showed that there is a tendency for economies of scale to increase

(for the costs of a bank to decline) until it reacht? a size of,

"2-5 million in deposits. Costs are then relatively constant until

the very large size of $100-500 million is reached."3 It was their

1Paul M. Horvitz and Bernard Shull, "Branch Banking and theStructure of Competition," The National Banking Review , Vol. 1, No. 3

(March, 1964), pp. 340-341."

2Ibid . , p. 341.

3Ibid. . p. 307.

27

view, though, that "economies of scale do not pose a serious barrier

to entry in banking," 1 and that "the most important barrier to entry

in banking is found not in the economic factors, but in the regulatory

policy and procedure."2

According to them, there is a danger of overestimating the number

of actual competitors in banking. "There is a natural tendency in a

country where free trade is the norm to look at numbers of firms and

ignore geographic barriers that keep them from competing."-* Many small

banks in the United States are:

...locked in sanctuaries protected against outside competition;

they can neither grow to an efficient size nor disappear throughfailure. Over one-half the banks in the United States have less

than $5,000,000 in deposits, and nearly one-quarter have less

than $2,000,000. There is, further, some evidence to suggestthat the unit banks absorbed through merger in branch bankingcommunities have generally been the relatively inefficient ones.

Horvitz and Shull also present an argument for branch banking

which rests upon the unbalanced banking needs of some communities.

They say that even if a unit bank could be operated as efficiently

as the branch of a large bank, the branch would be better suited to

certain types of communities, because many smaller communities or

suburban areas present the need for a very unbalanced banking business.

Paul M. Horvitz and Bernard Shull, "Branch Banking and the Structureof Competition," p. 308.

2Ibid . . p. 310.

3Ibid . . p. 330.

4Ibid . . p. 318.

Some wealthy suburban communities may generate sizable time deposits

and personal checking accounts, but they may have almost no demand for

business loans. In contrast, other residential areas may provide a

substantial demand for installment and mortgage loans, but an inadequate

deposit volume. The branch system, "provides for mobility of funds and

can shift excess reserves for lending through other outlets of the system.

Thus there are offices of some branch banks which have loan-to-deposit

ratios of over 100 percent."1

It is necessary for unit banks to maintain some reasonable balance

between total loans and total deposits, and there must also generally be

some balance in the loan portfolio between real estate, consumer loans,

and commercial loans. "Thus entry to a potential unit banker looks at-

tractive only in an area in which a sufficient volume and diversified

acomposition of business appears available."*

They also give another reason why entry by a new branch may be

easier than entry by a new bank:

The new branch can draw upon a reservoir of trained management

personnel developed by the large branch system. ..In addition...

the branch can benefit in its early months from the service of

experienced, specialised personnel who can be transferred tem-

porarily to the new branch.

3

The main results and conclusions of another article by Paul

Horvits and Bernard Shull, "The Impact of Branch Banking on Bank

^Paul M. Horvitz and Bernard Shull, "Branch Banking and the

Structure of Competition," p. 337.

2Ibid., p. 337.

3Ibid., pp. 337-338.

29

Performance," are as follows: "Host recent studies of economies of

scale have found that branch banks tend to have higher operating costs

than unit banks of similar size."1 Most evidence suggests that unit

banks can attain minimum optimum size at substantially lower asset sizes

than branch banks. Branching has the advantage of permitting growth by

way of geographic extension, but it has the disadvantage of raising the

minimum optimum size of banks* The diseconomies of branching can be

overcome, though, by growth as long as fairly extensive branching is per-

mitted in a particular state. 2

They give in the favor of the efficiency of branch banking the

fact that:

It has generally been confirmed that branch banks as a group

devote a larger proportion of their resources to loans than unit

banks as a group. Unit banks must generally have higher ratios

of liquid to total assets than branch banks.

3

It is their conclusion that, "branch banking is likely to result

in a somewhat greater convenience of banking facilities in moderate

and large sized non-metropolitan areas. "^ The results of some of their

studies suggest that, "branch banks are more apt to satisfy the hetero-

geneity of consumer demands than are unit banks, and in medium and large

size communities to provide more convenience in the form of more offices."'

''Paul M. Horvitz and Bernard Shull, "The Impact of Branch Bankingon Bank Performance," The National Banking Review , Vol. 2, No. 2 (December,

1964), p. 145.

2Ibid .

3Ibld . , p. 146.

4Ibid . . p. 149.

5Ibid., p. 155.

They say that one important difference between branch banking systems

and unit banks is in the rang* of services provided. Branch banking

systems "clearly outstrip" unit banks in the variety of produce offered

and in the convenience provided by multiple offices- -in towns large

enough to make more than one banking office a convenience. 1

Also, branch banking appears to influence bank performance in

other ways. According to Horvitz and Shull, the existence of "permissive

branching legislation" has an effect on the performance of unit banks

—

"unit banks in branch banking states generally have higher loan-asset

ratios and higher ratios of time-to-total deposits, and... they pay

higher rates of interest on time deposits than unit banks in unit bank-

ing states."2

Arizona—New Mexico Study

The article, "Branch Banking and Economic Growth in Arizona

and New Mexico," originated as a thesis entitled, "The Branch Banking

Question in Arizona and New Mexico: A Comparative Study," written

and submitted by Mr. Paul D. Butt in partial fulfillment of the require-

ments for his degree of Master of Business Administration at the Uni-

versity of New Mexico. It was begun in 1958 and completed in the spring

of 1959. As with the Horvitz studies, the results of Mr. Butt's work

will be given here without an attempt being made to explain the studies

and statistics used in arriving at them.

1Paul M. Horvitz and Bernard Shull, "the Impact of Branch Bankingon Bank Performance," p. 178.

2lbid.

31

This study examined the "validity of two opposing philosophies"

concerning branch banking. It was based upon comparisons of economic

activity between 1947 and 1959 in Arizona and New Mexico, one of which

permits unlimited branch banking, while the other has a system of branch

banking, "so limited as to constitute little more than unit banking."

The success of the banking operations in these two states was measured,

by the relative contribution of each system to its state's econ-

omic progress, with the contributions being measured in turn (1)

by the extent to which bank funds were used in earning assets,

(2) by the magnitude of interest costs to borrowers, (3) by the

availability of banking facilities, (4) by a comparison of bank

failures.

2

Mr. Butt summarised the banking laws of the two states somewhat

as follows: Arizona permits unlimited branch banking, and the only

qualifications for the opening of a branch are those of meeting the

standards of public convenience and advantage and of possessing mini-

mum amounts of capital and surplus. New Mexico permits a form of

limited branch banking such that, "a branch may be opened either in

the same county in which the parent bank is located, in an adjacent

county if there is no bank located in such county, or within a radius

of 100 miles of the home bank provided that the county in which the

branch is to be located has no bank already in operation."3 But ac-

cording to Mr. Butt, "No matter what it is called, the limited branch

^Paul D. Butt, "Branch Banking and Economic Growth in Arizona and

New Mexico," New Mexico Studies in Business and Economics: No. 7 , Bureau

of Business Research, The University of New Mexico, Albuquerque, New

Mexico (1960), p. 1.

2lbld .

3Ibid . . p. 2.

32

banking system in New Mexico is, for all practical purposes, really a

system of unit banking," and, "certainly, the primary advantages to be

obtained from branch banking are not present in any of the state's

systems."1

The following are, in my own words, the conclusions reached by

Mr. Butt as reported in his study:

1. The economic growth and development of Arizona exceeded that

of New Mexico over the period studied (from 1947 to 1959) , and the evi-

dence strongly supports the contention that during this period the un-

limited branch banking system of Arizona contributed more to Arizona's

economic development.''

2. Throughout the period analyzed, Arizona's banks kept a

higher proportion of their funds invested in loans and discounts; and

the average interest cost to the user of bank funds in Arizona was

lower than in New Mexico, yet the Arizona banks actually earned higher

returns on capital. 3

3. Banking facilities expanded more rapidly in Arizona,

and they were more widely available than in New Mexico—with the

unlimited branch banking system apparently being the chief contri-

buting force.

1Paul D. Butt, p. 2.

2Ibid.

.

PP< , 1 and 18.

3Ibid.

.

P. 21.

4Ibid.

33

4. Stability of branch banking seems to have been greater than

that of unit banking because of the wider economic and geographic

diversification of loans under unlimited branch banking. 1

5. Mr. Butt recommended, upon the basis of the evidence pre-

sented in his thesis, that a law be enacted in New Mexico which would

permit unlimited branch banking, since this system—he felt—would be

the kind most advantageous in New Mexico both to the consumer and to

the general economy. 2

Paul D. Butt, p. 21,

2Ibid.

CHAPTER VI

ADVANTAGES AND DISADVANTAGES OF BRANCH BANKING FOR KANSAS

The "Traditional" Arguments Given For and

Against Branch Banking

The discussion of branch banking in this paper thus far has been

based upon the results of studies, the opinions of experts, and thoughtful

analysis. The subject of branch banking is highly controversial, and

often the arguments given in favor of, or against, branch banking are

emotionally charged and are based upon few real facts. Although some

of these arguments may not be of great value in the quest for the "cor-

rect" or "right" answers concerning branch banking (the "correct" or

"right" answers must, of necessity, be based upon studies and empirical

observations), even so, many prominent men high in financial circles

use, and believe in, these arguments. Thus, no study of branch banking

would be complete without outlining briefly some of these arguments; and

so, the following is a brief list of the "disadvantages" commonly listed

as going along with branch banking (along with which will be a few re-

marks as to their faults or validity):

1. Independent unit banks know the needs of their community

better, and can meet these needs on a more personal basis, than the

branches of large branch banking systems. These locally owned and

Hf. H. Steiner, Eli Shapiro, and Ezra Solomon, p. 90.

34

35

controlled banks are more responsive Co local needs, and the management

of these banks will be more enterprising In promoting local projects.

*

2. Branch banking "fosters monopoly." There may be some degree

of truth In this, but It appears likely that "the competition between

rival branch organizations of large size might be more effective in

providing good banking services than would competition among a large

number of smaller unit banks. "2

3. "The single-office independent bank is likely to have a more

flexible management. Decisions can be made locally on the spot without

waiting for the approval of a distant main office. "3

4. It is difficult for a supervisory authority to adequately

examine a branch banking system. This seems to have been somewhat

solved, though, by a plan used in California whereby "state examiners

audit a random sample of the branch offices simultaneously. "^

3. If a large branch system were not competently managed and

were to fail, the "ensuing disaster" would be very widespread. "In

fact, the failure of a large branch banking system may imperil the

banking structure of a nation."5

Pritchard, p. 134.

^Financial Institutions , p. 134.

3Pritchard, p. 134.

Tinancial Institutions , p. 135.

5Ibid.

36

6. With branch banking "loans made to local borrowers will be

administered by bankers not especially interested in local welfare or

keenly aware of local credit needs." 1 It would be a short-sighted

branch banking system that would, knowingly, pursue this policy; be-

cause the welfare and growth of the system as a whole would be de-

pendent upon the welfare and growth of each of the local branches

—

and their local communities—making up the branch banking system.

7. There is less chance of competition among the branches of

branch banking systems with respect to service charges, interest rates

on time deposits, and services rendered to customers than is true of

independent unit banks. 2 The Horvitz studies reported in this paper

suggest that this usually isn't the case.

The following are some of the "advantages" commonly given for

branch banking:

1. Branch banking provides safety resulting from a wide diversi-

fication of assets. Branch banking systems are less likely to fail be-

cause they are spread over many localities; and, because of their size,

they are able to achieve a better diversification of assets than unit

banks .

3

2* Small unit banks are often too small to supply all of the

specialized banking services that are needed in their community. The

financial Institutions , p. 134.

2Pritchard, p. 134.

Financial Institutions , p. 133.

37

branches of a large banking system are better able to supply these

services. 1

3. A branch office can be established more quickly and at a

lower capital cost than a unit bank. Statistics seem to uphold the

validity of this argument. 2

4. Branch banking promotes a better distribution and mobility

of credit and banking resources. 3 "Not only does this mean a better

accomodation of local loan demands but [also it] results in an over-all

reduction in interest rates. '**

5. The loan limits of many small unit banks may be too small to

meet the needs of their largest borrowers and, although they are able

to make these loans with the aid of their larger city correspondent

banks, the branch banks of large branch banking systems are faster

and more efficient at handling these loan needs. 5

The above have been only a few of the arguments which have been

put forward in favor of, and against, branch banking. Other than where

the validity or falsehood of these arguments has been pointed out (as

based upon studies or empirical evidence, for example by Horvitz)...it

is hard to say whether these arguments are valid or not. The facts just

Pritchard, p. 134.

^Financial Institutions , p. 134.

3Ibid . . p. 133.

Pritchard, pp. 134-135.

5Ibid. . p. 134.

aren't available, and this ought to prove a fruitful field for further

research.

Growth in the Number of Suburban Banks

in Wichita Since 1950

Wichita appears to be the best example in Kansas of a growing

metropolitan area in which a number of new suburban banks have been

chartered (to see the population growth in Wichita, refer to Table 2,

on page 2 of this paper). From Table 9, it can be seen that in 1950,

there were 6 banks in Wichita (all of them downtown banks), while in

1965, there were 14 banks in Wichita (seven of the eight new banks being

suburban banks).

The idea presented in Chapter I of this paper was that, under

more liberal banking laws in Kansas, it seems likely that the existing

downtown banks in Wichita could have efficiently handled a portion of

this growing suburban business by means of establishing suburban branches.

It also seems reasonable to assume that some of these suburban areas

would have presented somewhat of an unbalanced banking situation--"un-

balanced banking needs"--as discussed in the summary of the Horvitz

Studies in this paper. If this unbalanced banking situation indeed

existed, the results of the Horvitz Studies suggest that branch banking

would be more efficient at handling this situation than unit banking.

Although Wichita is the best example of suburban bank growth,

perhaps a similar trend could be found in Topeka and in metropolitan

Kansas City, Kansas. Included here is information only on the growth

of suburban banking in Wichita (Table 9) for the following reasons:

39

TABUE 9*

GROWTH IN THE NUMBER OF WICHITA BANKS

(1950 to 1965)

Banks: Suburban (S), or

Downtown (D); and Year

Chartered, eg: (1906)

Deposits, In Thousands of Dollars

(All Statements as of June 30th)

1965 1955 1950

(S) Boulevard State Bank (1954) 12,949

(S) Central State Bank (1962) 5,938

(S) East Side National Bank (1955) 7,050

(D) Pirst National Bank (1876) 104,620

(D) Fourth National Bank (1887) 214,678

(D) Kansas State Bank (1934) 28,969

(S) National Bank of Wichita (1964) 2,616

(S) Parklane National Bank (1962) 4,732

(S) Seneca National Bank (1961) 5,190

(D) Southwest National Bank (1915) 20,220

(D) Stockyards National Bank (1910) 21,072

(S) Twin Lakes State Bank (1965) «

(D) Union National Bank (1906) 57,202

(D) Wichita State Bank (1953) 9,203

5,267

105,911

172,198

19,341

13,684

5,350

25,216

3,784

90,820

121,455

8,541

9,004

4,500

16,303

*The Twin Lakes State Bank had 882 thousand dollars of deposits

as of December 31, 1965.

*Prom statistics given in the Rand McNally International Bankers

Directory, The Bankers Blue Book (Chicago, Illinois: Rand McNally &Company), Final 1950 Edition, Final 1955 Edition, and Final 1965 Edition.

40

The population growth in Topeka, although extremely rapid, has been

somewhat slower than the population growth in Wichita. In beginning

to compile a table similar to the one for Wichita (Table 9) for Topeka,

it was found that the banking situation isn't as clear-cut in Topeka

and that several bank mergers have somewhat confused the situation as

far as presenting the banking information for Topeka in an orderly and

meaningful table. The city of Kansas City is located on a state line,

and it appeared that any suburban banking information gathered on it

would have had doubtful value.

More Extensive Branch Banking for Kansas

The question of whether branch banking- -and if so, to what degree-

would be a benefit to Kansas is a difficult one to answer. Not enough

data and research directed specifically at the possibility of branch

banking in Kansas is available, so the only way to attempt to answer

this question is to draw inferences from studies that have been done

in other states.

From the Horvitz Studies of branch banking throughout the United

States and from the study which compared Arizona and New Mexico, it appears

that branch banking of some degree would be a benefit to Kansas. The

problem comes in trying to find the proper form and proper degree of

branch banking for Kansas. It seems that a minimal change in Kansas

Banking Laws should include provisions for branching within the city

limits (including the "suburbs") of the major cities in Kansas--Wichita,

Topeka, and Kansas City... and later, perhaps some of the other cities

in Kansas after they have reached a certain size.

41

The Arizona-New Mexico Study pointed out that a great deal is at

stake for a state... the "economic growth." If the banking system in

Kansas is a handicap to its economic growth in relation to that of

other states, something should be done about it. As was stated in,

An Evaluation of Commercial Banking in Kansas, Internal Report to the

Kansas Bankers Association , in a somewhat different context, "While

many Kansas communities possess adequate banking facilities and will

continue to do so for some time, other communities experiencing a

change in both population and the level and nature of economic acti-

vity currently pose a real question as to whether the general public

is enjoying the maximum level of banking services." 1

1Philip B. Hartley and Robert 0. Schrock, An Evaluation ofCommercial Banking in Kansas, Internal Report to the Kansas BankersAssociation (Lawrence, Kansas, January, 1964) , p. 142.

42

CONCLUSIONS

Although several of the major cities in Kansas appear to have

some need for branch banking, it appears likely that if the branch

banking question were to come up in Kansas , the rural areas would op-

pose any movement toward branch banking. There appears to be a mildly

growing sentiment among the city bankers of the larger city banks in

Kansas in favor of branch banking, but these city bankers seem reluctant

to speak out on the matter. They are afraid that if they come out in -

favor of branch banking they stand to lose correspondent banking business

from the smaller banks in the rural areas of Kansas.

If the branch banking question were to develop in Kansas, it

seems likely that these small rural banks would oppose branch banking.

As a matter of self-interest they would probably fear the possibility

that, under statewide branch banking laws, large city banks could build

"empires" by buying up banks in all parts of the state. Although they

might be somewhat "hazy" about how it could occur, these small rural

banks would perhaps fear that, through their size, the large banking

systems, which could grow up under liberal banking laws, would have

an "unfair advantage" and would have tools at their disposal which

would put smaller banks into a "squeeze."

One of the major advantages of branch banking appears to be

that it can provide banking services for a community which has an

unbalanced banking situation. Some communities, or suburban areas,

might have the potential for large amounts of deposits and yet almost

no demand for loans. Other communities might have a sizable demand

43

for loans but not an adequate deposit volume to support these loans.

Branch banking appears to be the answer to this problem. The branches

of the same bank existing in these two areas might be able to balance

each other out* while a single, independent unit bank would have a

difficult time existing, or coming into existence, in either of these

areas.

Thus, branch banking might be of benefit to suburban areas and

shopping centers- -if unbalanced banking situations exist. In the same

manner, it might be of service to rural areas and small communities which

otherwise wouldn't be able to support a bank. If Kansas is to strive for

maximum economic growth, and for the best possible banking services for

its people, branch banking may provide some of the answers.

44

ACKNOWLEDGMENTS

The author wishes to express his sincere gratitude to Mr. Carl A.

Bowman and The Kansas Bankers Association, Professor Donald F. DeCou,

Professor Merton L. Otto, and Professor John 0. Rees for the valuable

suggestions and time given by them during the preparation of this

report

.

REFERENCES

Books

Alhadeff, David A. Monopoly and Competition in Banking . Berkeley,

California: University of California Press, 1954.

Banking and Monetary Studies . Edited by Deane Carson. Homewood,

Illinois: Richard D. Irwin, Inc., 1963.

Cartinhour, Gaines T. Branch. Group, and Chain Banking . New York:

The Macmillan Company, 1931.

Chapman, John M. and Wexterfield, Ray B. Branch Banking . New York:

Harper & Brothers Publishers, 1942.

Collins, Charles Wallace. The Branch Banking Question . New York:

The Macmillan Company, 1926.

Financial Institutions . Edited by Roland I. Robinson. Homewood,

Illinois: Richard D. Irwin, Inc., 1960.

Fischer, Gerald C. Bank Holding Companies . New York: Columbia

University Press, 1961.

Hogenson, Palmer T. Tha Economics of Group Banking . Washington,

D. C. : Public Affairs Press, 1955.

James, Marquis and James, Bessie Rowland. Biography of a Bank. The

Story of Bank of America . New York: Harper & Brothers, 1954,

Lamb, W. Ralph. Group Banking . New Brunswick, New Jersey: Rutgers

University Press, 1962.

Pritchard, Leland J. Money and Banking . Boston, Massachusetts:Houghton Mifflin Company, 1964.

Rand McNally Bankers Directory. The Bankers Blue Book . Chicago,Illinois: Rand McNally & Company, Final 1950 Edition.

. Chicago,Illinois: Rand McNally & Company, Final 1955 Edition.

45

Rand McNally Bankers Directory. The Bankers Blue Book . Chicago,Illinois: Rand McNally & Company, Final 1965 Edition.

Spofford, Gavin. Guideposts for Banking Expansion . New Brunswick,New Jersey: Rutgers University Press, 1961.

Steiner, W. H. ; Shapiro, Eli; and Solomon, Ezra. Money and Banking .

An Introduction to the Financial System. New York: Holt,Rinehart and Winston, Inc., 1958.

Public Documents

Federal Deposit Insurance Corporation. Assets. Liabilities, and CapitalAccounts Commercial and Mutual Savings Banks. June 30. 1965 .

Report of Call No. 72.

General Assembly of the Commonwealth of Pennsylvania. Branch Banking .

Joint State Government Commission, Harrisburg, Pennsylvania,1957.

General Statutes of Kansas . (The sections giving present Kansas BankingLaw were furnished by the Kansas Bankers Association, Tocek*t,Kansas.)

New York State Banking Department. Branch Banking. Bank Mergers and ThePublic Interest . January, 1964.

_. Branch Banking, Bank Mergers and ThePublic Interest- -A Summary Report . January, 1964.

State of California. Banking Law and Related Acts . December 31, 1962.

United States Bureau of the Census. United States Census of Population :

I960 . Vol. I, Characteristics of the Population, Part 18,Kansas. Washington, D. C. : U. S. Government Printing Office,1963.

United States House of Representatives. Banking Concentration and SmallBusiness . A Staff Report to the Select Committee on SmallBusiness. 86th Congress, 2nd Session, December 23, 1960.

United States Treasury—The Administrator of National Banks. The BankingStructure in Evolution . Washington, D. C. , 1964.

United States Treasury- -The Administrator of National Banks. Studies inBanking Competition and the Banking Structure. Washington, D. C,January, 1966.

47

Periodicals

"The Case for the Satellite Branch," Banking. Journal of the American

Bankers Association , Vol. LVII, No. 10 (April, 1965), pp. 52,

& 98-102.

Horvitz, Paul M. "Economies of Scale in Banking," Private Financial

Institutions , Englewood Cliffs, New Jersey: Prentice-Hall,

Inc., 1963, pp. 1-54.

; and Shull, Bernard. "Branch Banking and the Structure

of Competition," The National Banking Review , Vol. 1, No. 3

(March, 1964), pp. 301-341.

« "The Impact of Branch Banking on

Bank Performance," The National Banking Review , Vol. 2, No. 2

(December, 1964), pp. 143-188.

"Kansans in Washington Want One-Bank System," The Wichita Eagle ,

March 23, 1966, Sec. A, p. 10, cols. 1 & 2.

The Kansas Banker . Published Monthly by the Kansas Bankers Association,

Topeka, Kansas (April, 1961), pp. 13 & 15.

Other Sources

Bankers Against Monopoly Banking- -A Committee of the Illinois Bankers

Association. Facts About Banking and the Public Interest . Chicago,

Illinois: The Illinois Bankers Association.

Banking Education Committee- -The American Bankers Association. The Story

of American Banking . New York: The American Bankers Association,

1963.

Bank of America Annual Report. 1965 . Bank of America (Headquarters

in Los Angeles, California).

Butt, Paul D. "Branch Banking and Economic Growth in Arizona and New

Mexico," New Mexico Studies in Business and Economics: No. 7 .

Bureau of Business Research, The university of New Mexico,Albuquerque, New Mexico, 1960.

"Establishing A Branch," A Bank Director's Job . Reprinted from articleswhich originally appeared in, Banking, Journal of the AmericanBankers Association , from April, 1956 through April 1964,

pp. 57-59.

48

Hartley, Philip B. and Schrock, Robert D. An Evaluation of Commercial

Banking in Kansas, Internal Report to the Kansas Bankers

Association . Lawrence, Kansas, January, 1964.

The Monopolistic Character of Branch Banking . An Address given in 1965

by John F. McCarthy, President, Illinois Bankers Association.

New York State Bankers Association. Planning Ahead for CommercialBanking . (405 Lexington Avenue, New York, New York),

September, 1963.

We Must Keep Building. Address of Archie K. Davis, President, The

American Bankers Association, before the Midwinter Meeting

of the Ohio Bankers Association, Sheraton Columbus Hotel,

Columbus, Ohio, Friday Noon, February 18, 1966.

PROBABLE ADVANTAGES AND DISADVANTAGES OF BRANCH BANKING

FOR THE STATE OF KANSAS

ROBERT MELVIN DEAVER

B. A., Kansas State University, 1965

AN ABSTRACT OF A MASTER'S REPORT

submitted in partial fulfillment of the

requirements for the degree

MASTER OF ARTS

Department of Economics

KANSAS STATE UNIVERSITYManhattan, Kansas

1966

Kansas i« changing from the traditionally rural state it has been

in the past into an agricultural state containing growing areas of urban

population. It appears probable that this trend will continue into the

future and may require the enactment of new laws designed to cope with

this. Present Kansas law prohibits branch banking to any greater extent

in Kansas than one drive-in branch located within 2,600 feet of the bank

which operates it. It is felt by some that this present law it too

restrictive.

Seven of the eight new banks chartered in Wichita between 1950 and

1965 were suburban banks. In some cases suburban areas provide an un-

balanced banking situation. Por example, an unbalanced banking situation

exists in an area which has a high potential for deposits and yet almost

no demand for loans. Similarly, an unbalanced banking situation exists

in an area which has a sizable demand for loans but not an adequate de-

posit potential to support these loans. Branch banking may be the

answer to this problem; the branches of a branch banking system exist-

ing in these two types of unbalanced banking areas might be able to

balance each other out, but a single unit bank would have a difficult

time existing, or coming into existence, in either of these areas.

Thus, it seems reasonable to assume that the existing downtown banks

in Wichita could have efficiently handled a portion of the growing

suburban banking business in Wichita by establishing branches, if they

had been permitted to do so under a more liberal banking law in Kansas.

Branch banking might be able to benefit suburban areas and shopping

centers in Kansas in which unbalanced banking situations exist; and, in

the same manner, it might be able to aid rural areas and small communities

which otherwise wouldn't be able to support a bank. If Kansas is to

strive for maximum economic growth, and for the best possible banking

services for its people, branch banking may be able to provide ac

of the answers.