privatisation commission · strategic sales, and capital market ... wherein management of pses is...

TRANSCRIPT

Volume 01 March 2015

Privatisation CommissionNEWSLETTER

PAGE-5MissionStatement

PAGE-6History ofPrivatisation

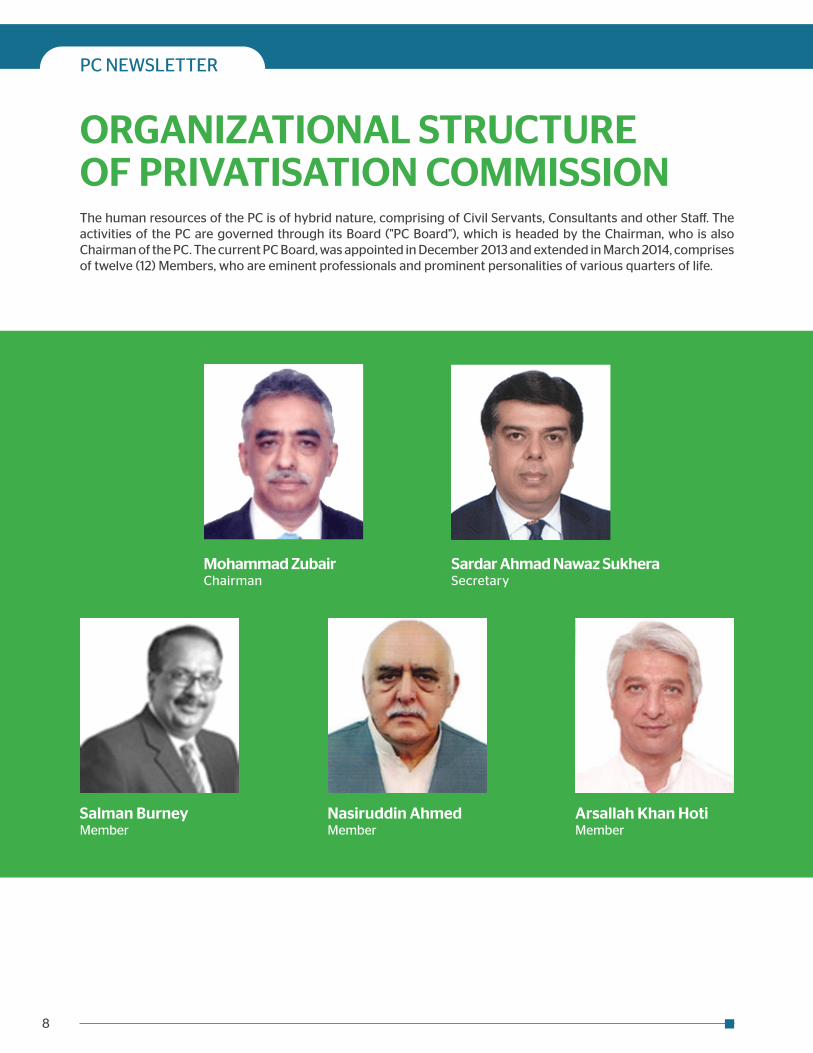

PAGE-8Organizational Structure ofPrivatisation Commission

PAGE-19PC News

PAGE-22IFR Asia’s Issuer of the Year

Message from theMinister for Finance, Revenue, Economic

Affairs, Statistics and Privatisation

Pakistan’s privatisation program is focused on attracting private sector capital and managerial expertise through the divestment of identified public sector entities (“PSEs”) in a transparent manner. The program includes the divestment of PSEs in the oil and gas, power, and financial sectors through capital market transactions, and other modes, which will enhance the attractiveness and visibility of Pakistan as a favoured investment destination. In doing so, the Privatisation Commission will deepen the country’s capital markets through foreign and domestic direct and portfolio investment, and will mobilise the savings of Pakistanis by providing an opportunity to take ownership in successful businesses.

The major benefits of the privatisation are to:

• Generate revenue for debt retirement and poverty alleviation;

• Improve the PSE's provision of services to the general public; and

• Provide better facilities to the general public after improvement of PSEsby private sector involvement;

The following benefits will also accrue in the power sector:

• Enhanced capital formation for the domestic power sector outside theGovernment's budget and without sovereign guarantees;

• Improved power sector efficiency through competition, accountability,managerial autonomy, profit incentives, and deregulation.

• Rationalized prices and subsidies while maintaining certain sociallydesirable policies such as rural electrification and low-income lifelinetariff rates.

The Privatisation Commission Newsletter is a valuable addition to the Privatisation Commission's efforts to disseminate useful information to other government departments, and the general public.

Mohammad Ishaq DarMinister

2

3

Message from theChairman,Privatisation Commission

Privatisation is an important policy tool for generating growth and addressing structural imbalances by removing artificial barriers, attracting investment, and opening-up the economy to competition. Pakistan’s privatisation program is part of the Government of Pakistan’s economic reforms agenda, which along with deregulation, restructuring, and good governance, seeks to enhance growth and productivity in the economy by harnessing the private sector’s capital and managerial expertise as an engine of growth. Privatisation will continue to be implemented in a transparent manner, to bring the Government out of running businesses, and to create space for the private sector leading to a sustainable economy and a prosperous Pakistan.

The Government of Pakistan attaches a high priority to private sector development and endeavors to provide a level playing field by encouraging local as well as foreign direct investment. The Government believes that the private sector is the engine of growth and the Government should only be an impartial umpire rather than a market participant. Previously, the privatisation process suffered a setback due to global financial crisis of 2007-2009. However, one of the most important achievements of the Privatisation Commission during the tenure of current Government is the revival of the privatisation program, after a six year gap. So far, three capital market transactions have been successfully concluded, and about a dozen strategic sales are currently being processed.

The Privatisation Commission is seeking to turn loss making PSEs to profitability by equipping them with state-of-the-art technologies, through the introduction of Public Private Partnerships, strategic sales, and capital market transactions, which will lead to provision of improved services to the public in general.

The Privatisation Commission Newsletter, in addition to the Privatisation Commission’s website and periodic announcements, helps to ensure that the general public and all stakeholders are aware of the Privatisation Commission’s activities and accomplishments.

Mohammad ZubairChairman

4

The Government of Pakistan is committed to pursuing privatisation as a core element of its economic reform agenda. The privatisation program aims to reduce Pakistan’s fiscal burden, improve service delivery to the people of Pakistan, facilitate more competition in the economy, and strengthen Pakistan’s capital markets.

Pakistan was one of the first countries in the region to initiate the deregulation and liberalization of its economy, and to start privatisation. Between 1991 and 2008, proceeds of PKR 476 billion were raised from 167 privatisation transactions, which included important privatisation successes in the industrial, telecom and financial sectors. The latter two sectors, in particular, have been major contributors to the national exchequer.

The present Government restarted the privatisation program in 2013, after a six year gap. A ‘Program for Early Implementation’ was approved by the Cabinet Committee on Privatisation on 3 October 2013, listing thirty one PSEs for privatisation. Eight further PSEs were added to this list in June 2014.

The focus of the program is to attract private capital investment, benefit from the private sector’s skill-set and experience, and make it the engine of economic growth for Pakistan. In order to achieve this, the current program is modelled around the concept of Public Private Partnerships, wherein management of PSEs is transferred to strategic investors along with a 26% equity stake. The program also includes divestments through strategic sales and capital markets to enhance the attractiveness and visibility of Pakistan as a favoured investment destination.

During the present Government, the Privatisation Commission has successfully completed three capital market offerings, namely United Bank Limited, Pakistan Petroleum Limited and Allied Bank Limited, raising gross proceeds of ~PKR 68 billion including foreign exchange of over USD 350 million. Global debt and equity offerings by the Government of Pakistan have been acknowledged internationally as is evident from the award of ‘Issuer of the Year’ given to Pakistan by IFR Asia. Furthermore, the United Bank Limited transaction also received the “Best Deal Award” for Pakistan by The Asset, one of Asia’s most prestigious corporate ranking journals. These achievements have improved the standing of our domestic capital markets and put Pakistan firmly back on the global equity markets map.

The Privatisation Commission is vigorously pursuing the implementation of the remaining program with work on over 30 PSEs being done concurrently.

However, success of the privatisation program is contingent upon the support of all the stakeholders, including the various Government agencies, departments, organizations, regulatory authorities and, most importantly, the people of Pakistan.

I am confident that all stakeholders will play their part and contribute fully towards ensuring the success of the ongoing privatisation and the fulfilment of the program’s objectives.

Message from theSecretary,Privatisation Commission

Sardar Ahmad Nawaz SukheraSecretary

PC NEWSLETTER

5

Privatisation is an open, fair and transparent process,

for the benefit of the people of Pakistan,

in the right way, to the right people, at the right time.

Mission Statement

6

Pakistan's privatisation program is an important economic reform policy tool for generating growth and erasing structural inefficiencies by removing barriers and opening up the economy to competition. The program is part of the economic & structural reforms agenda, and along with deregulation and good governance, seeks to enhance the growth and productivity of Pakistan’s economy by harnessing the private sector as its engine of growth. It takes an integrated approach to enhance the private sector’s role and goes beyond just the sale of public assets to the private sector. Though good governance, sensible regulation, and market competition, the Government of Pakistan ("GOP") will foster conditions that will insentivise the private sector to invest, and provide goods and services efficiently.

Pakistan had initiated a significant program of deregulation and decontrol in 1960s, when such policies were neither fashionable nor common in many emmerging markets. After the announcement of an “Industrial Investment Policy”, the industrial sector was partially deregulated.

After the announcement of Economic Reforms Order 1972, the GOP took over 32 industrial units under ten basic categories i.e.; iron and steel, basic metals, heavy engineering, heavy electrical machinery, assembly and manufacture of motor vehicles, tractor assembly and manufacture, heavy and basic chemicals, petrochemical, cement and public utilities including oil, gas and electricity. In September 1973 another 26 industrial units were nationalized, including vegetable oil, life insurance, shipping and petroleum making companies, followed by cotton and rice export trade. In 1974, banks were nationalized, which later extended to 3000 flour mills, rice husking and cotton grinning industries. However, most of the small rice and cotton units were denationalized and the government only retained large rice mills. Only textile and sugar sector remained untouched. The public sector entities (“PSEs”), eventually exhibited the following characteristics:

Mismanagement and over-staffing

Inappropriate and costly investments

Poor coverage and quality of services

High debt and fiscal losses

Corruption

“The Transfer of Managed Established Order 1978” induced denationalization policy except for sugar and a tractor plant, and the same were transferred to private sector. Two further attempts of denationalization in 1985 and 1989 had little success. Nevertheless, the Government succeed in divesting 10% shares of Pakistan International Airlines (“PIA”) via an initial public offering in 1988.

The GOP is committed to getting itself out of the business of running businesses and creating space for the private sector to play a vital role in the development process and in realizing the dream of a prosperous Pakistan. The Government initiated the privatisation program afresh and offered 108 PSEs out of 128 and in less than 18 months, 66 PSEs were privatised. Thus, in 1991, Pakistan formally institutionalized the privatisation activity by establishing the Privatisation Commission (“PC”).

Many organizational changes took place so that by the end of 1993, there was one Commission to manage the privatisation of industrial units, banks and financial institutions, another Commission for privatisation of the power sector, while separate committees looked after the privatisation of telecommunications, transport and shipping companies. All of these activities were subsequently amalgamated into one Privatisation Commission by the end of 1993.

Later, on 28 September 2000, the Privatisation Commission Ordinance 2000 was promulgated, and the Privatisation Commission was converted into a body corporate, which strengthened its legal authority for implementing the GOP’s Privatisation Policy.

HISTORY OF PRIVATISATION

PC NEWSLETTER

7

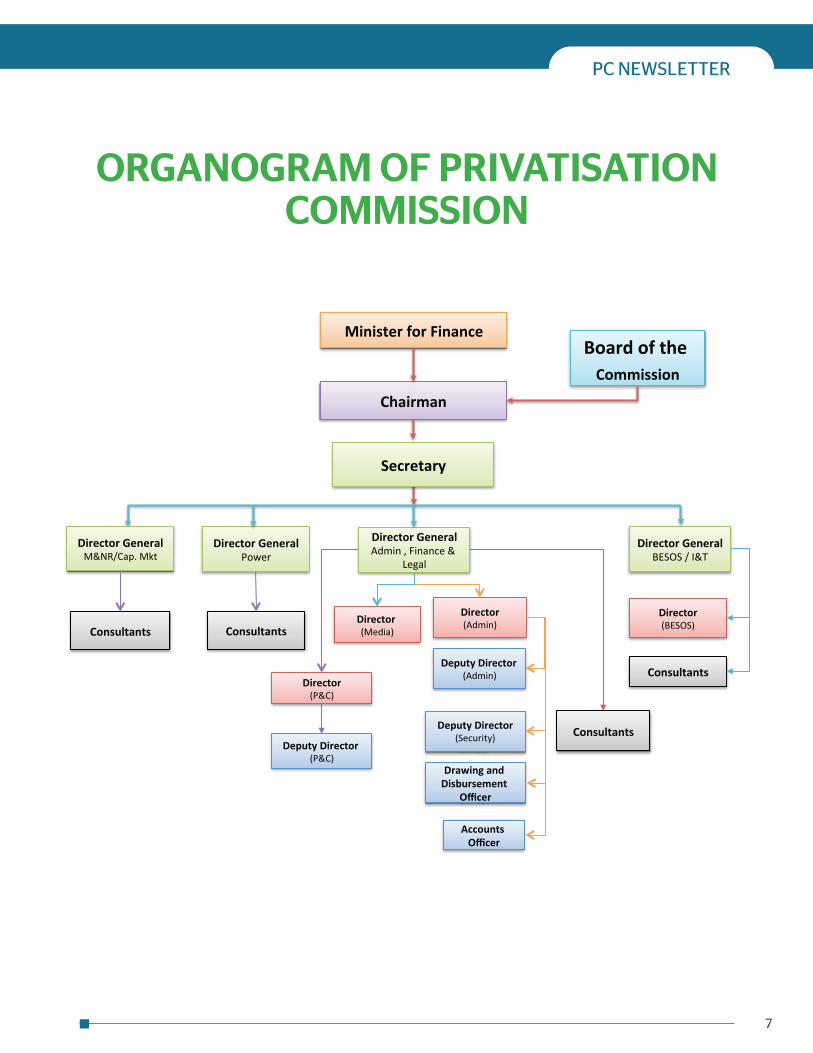

ORGANOGRAM OF PRIVATISATION COMMISSION

Secretary

Legal

Officer

Deputy Director(Security)

Officer

Power

Consultants (BESOS)

Consultants

Mkt

8

ORGANIZATIONAL STRUCTURE OF PRIVATISATION COMMISSIONThe human resources of the PC is of hybrid nature, comprising of Civil Servants, Consultants and other Staff. The activities of the PC are governed through its Board ("PC Board"), which is headed by the Chairman, who is also Chairman of the PC. The current PC Board, was appointed in December 2013 and extended in March 2014, comprises of twelve (12) Members, who are eminent professionals and prominent personalities of various quarters of life.

Sardar Ahmad Nawaz SukheraSecretary

Mohammad ZubairChairman

Salman BurneyMember

Nasiruddin AhmedMember

Arsallah Khan HotiMember

PC NEWSLETTER

PC NEWSLETTER

9

Zafar IqbalMember

Aziz NishtarMember

Mr. Khurram SchehzadMember

Mr. Yawar Irfan KhanMember

Nauman K. DarMember

Shahid ShafiqMember

Engr. M. A. JabbarMember

Naseer Ahmad AkhtarMember

Ashfaq Yousuf TolaMember

Zafar Iqbal SobaniMember

Zaffar A. KhanMember

10

CAREER SUMMARY• Appointed as Minister of State / Chairman Privatization Commission on 18th December to date.

• Appointed as Chairman, Board of Investment on 12th July, 2013 to 17th December, 2013.

• Part of PML- N Economic, Tax Reforms Media Committees, 2012-2013.

• Worked for Leading American IT Company IBM: 1981 to 2007 including key International Assignments inParis, Rome, Milan and Dubai.

• Chief Financial Officer, IBM Middle East / Africa Region 2004 – 2007.

• Chief Financial Officer, IBM Pakistan – 1998 – 2003.

• Financial Controller & CFO, IBM Middle East based in Dubai – 1995 – 1997.

• Financial Operations Officer, IBM Southern Europe based in Milan, Italy – 1993 – 1995.

• Accounting & Treasury Manager, IBM Pakistan – 1990 – 1992.

• Treasury & Investment Operations Manager IBM Africa based in Paris, France – 1988 – 1990.

AWARDS / RECOGNITIONS• Awarded Administrative Achievement Award for best employee IBM Pakistan – 1981.

• Awarded Presidents Award for best performance in IBM Europe – 1997.

• Attended IBM Convention in Naples, Italy for outstanding performance – 1993.

• Awarded IBM Europe / Middle East / Africa Region Certificate for outstanding performance during 2002.

• Several Other Awards and Recognitions achieved during the course of career with IBM.

EDUCATIONMaster’s in Business Administration (MBA) from the Institute of Business Administration (IBA).

OTHER ACHIEVEMENTS• Elected on the Board of Directors of IBA, Karachi as their Student Representative – 1980.

• Taught Financial Management at the Institute of Business Administration, Karachi in the evening campus –1981 – 1986.

• Remained on board of the American Business Council in financial advisory capacity during the period2004 – 2007.

• Member of the Overseas Investors Chamber of Commerce and Industry 2004 – 2007.

• Regularly contributed articles on business subjects in leading Pakistani papers since 2007.

Mohammad ZubairChairman, Privatisation Commission

PC NEWSLETTER

11

Mohammad ZubairChairman, Privatisation Commission

Naseer A. Akhtar is the President and CEO of InfoTech Group, Pakistan’s leading information and communication technology firm with offices in Pakistan, Singapore, United Kingdom, Ghana, and United Arab Emirates. He has over 30 years of professional experience and is a sought after mentor and speaker on such topics like global trade, policy and market positioning, and has been honoured with numerous industry awards.

Prior to InfoTech, Mr. Akhtar was Managing Director of South Technology & Services (Private) Ltd; Managing Director of South Express (Private) Ltd.; managing director of Avimatics; a Regional Manager of ITC Group Pakistan; and Operations Manager of A.A. Turki Group (Saudi Arabia). Mr. Akhtar was recently the past Chairman of Pakistan’s industry association P@SHA and was also a member of the Board of Investment’s Advisory Committee on ICT; Chairman of Pakistan Software Houses Association; Director of the Pakistan Software Export Board; and Member of the Corporate Advisory Committee of the National University of Science & Technology during his professional career.

Mr. Akhtar has a Bachelor’s degree in Science in Mathematics and Physics from the University of Punjab, Lahore; a foundation in science in pre-engineering from Government College, Lahore; and a certificate for independent directors from the Institute of Chartered Accountants of Pakistan.

Sardar Ahmad Nawaz Sukhera is an officer of the Pakistan Administrative Service and joined the Privatisation Division/ Commission on April 08, 2014.

He joined the Civil Service of Pakistan in 1985 and over the course of his career, has held various Secretariat, Field and Staff assignments. Before joining the Privatisation Division, he was serving as Chief Executive Officer of the Small & Medium Enterprises Development Authority of Pakistan (SMEDA). He has held field assignments of Deputy Commissioner in Faisalabad (1995-96) and Sheikhupura (2000-01) Districts and was District Coordination Officer, Sheikhupura (2001). Staff jobs done by him include Principal Secretary to the Governor Punjab (2008-11), PSO to Chief Minister, Punjab (1994-95) and Faculty Member at the National School of Public Policy (2011-12). In the Secretariat of Government of the Punjab, he has held assignments of Secretary (Implementation & Coordination) (2005-08), Additional Finance Secretary (Budget & Development) (2003-05), Chief, External Capital Assistance (1996-97), besides having been Project Director of the Technical Education Project (1998-99), which was an ADB Funded Project.

He earned his MPA degree from Harvard University (1994), and Master of Arts (Development Economics) from Williams College (1993). He also holds a Bachelor of Science (Hons.) degree in Economics, specialising in Industry & Trade, from the London School of Economics (1983). Earlier, he completed his schooling at the Aitchison College, Lahore.

He has attended executive courses in Investment Appraisal & Management, Infrastructure in Market Economy, and Public-Private Partnership for Infrastructure Development at Harvard University, and Budgeting & Financial Management in Public Sector at Duke University.

He has also taught economics at the undergraduate level at Harvard University (1993-94). His research paper on ‘Kalabagh Dam – contentious issues and ways of reproachment’ was published in the National Institute of Public Administration Papers (2004), and his master thesis at Williams College was on ‘Peace Dividend and Social Sector Spending- a case study of India and Pakistan’.

Sardar Ahmad Nawaz SukheraSecretary, Privatisation Commission

Naseer Ahmad AkhtarMember, Board of Privatisation Commission

12

Engr. Memon Abdul Jabbar is Chief Executive of Qaim Automotive Mfg. Pvt. Ltd., and is Chairman of the Karachi Tools & Dies Mold Centre. He has over 30 years of experience across a wide range of industries and sectors including engineering; light, medium and heavy industries; power generation; cement; steel; shipyards; and international trade.

Engr. Jabbar is also a Director of the National Fertilizer Corporation; Director of the Pakistan Standard Quality Control Authority; Director of the Sindh Board of Investment Sindh, Govt. of Sindh; Director of the Public Private Partnership Policy Board Govt. of Sindh and of the Sindh Public Procurement Regulatory Authority Govt. of Sindh Advisory Committee Federal Tax Ombudsman. He was also Chairman of the North Sindh Urban Services Corporation; Vice President Federation of Pakistan Chambers of Commerce and Industry; Chairman WTO Resource Centre and R&D Committees FPCCI; Chairman SITE Association of Industry Karachi; and life time member FPCCI/SAARC CCI.

Engr. Jabbar has a Bachelor’s degree in Engineering (Electrical), and has completed postgraduate studies in power systems. He is a certified safety engineer, and certified director of companies as per SECP Rules 2013.

Engr. M. A. JabbarMember, Board of Privatisation Commission

Mr. Nasiruddin Ahmed has over 40 years of experience, particularly in government, where was recently a member of the National Electric Power Regulatory Authority (“NEPRA”) for a term of four years. He served as Cabinet Secretary, until attaining superannuation, and as Principal Secretary to the Prime Minister. His long and distinguished career in government included work in several ministries / divisions inter alia Production, Interior, Economic Affairs, and the Cement Corporation of Pakistan.

He served in Baluchistan as provincial secretary of various departments including Finance, S&GAD, Agriculture, Environment, Education, Forest and as chairman of the Baluchistan Development Authority. He was also posted to the Federal Government and served as Member Finance in Pakistan Agriculture Research Council (PARC), and as Additional Secretary Ministry of Food Agriculture and Livestock.

Mr. Ahmed has a Master’s in Social Sciences in Project Planning and Monitoring, and Local Government Finances.

Mr. Zafar Iqbal is a Chartered Accountant and a senior partner of a firm of Chartered Accountants with offices at Lahore and Faisalabad. He has over 25 years of professional experience in audit & assurance, taxation and corporate matters, and has experience in project restructuring and evaluation, monitoring and designing of MIS, accounting, and financial systems with a wide-range of clients including the Punjab Government.

Mr. Iqbal is a member of the Accounting & Auditing Standards Committee, a fellow member of the Institute of Chartered Accountants of Pakistan, and a committee member of its Small and Medium Practices Committee and Quality Assurance Board. He is also a fellow member of the Institute of Corporate Secretaries of Pakistan. During his professional career, he was a director of Zarai Taraqiati Bank (ZTBL), and a member of the Northern Regional Committee of Institute of Chartered Accountants of Pakistan. Mr. Iqbal completed his Chartered Accountancy with the Institute of Chartered Accountants of Pakistan.

Nasiruddin AhmedMember, Board of Privatisation Commission

Zaffar IqbalMember, Board of Privatisation Commission

PC NEWSLETTER

PC NEWSLETTER

13

Mr. Zafar Iqbal Sobani is Managing Director of Habib Metro Pakistan (Pvt.) Limited and Makro–Habib Pakistan Limited, and also manages the House of Habib Group’s new business development initiatives. He has over 30 years of professional experience capital markets, management and cost accounting, and the power sector. Prior to joining the House of Habib Group, Mr. Sobani was Chief Executive of Hub Power Company, and Chief Executive of Liberty Power Tech, which is an independent power producer under the 2002 Power Policy. Before this, he spent 19 years as Director of Finance with Century Paper & Board Mills, and five years with BOC Pakistan Limited (now known as Linde Pakistan). Although he started his career in auditing with A.F. Ferguson, he also worked for Ernst & Young Saudi Arabia.

Mr. Sobani is a director of the Board of Institute of Capital Market Pakistan. He was most recently the chairman of the Quality Control Board of the Institute of Chartered Accountant of Pakistan and was president of the Institute of Chartered Accountants of Pakistan. Prior to joining the PC Board, he was a member of the Privatisation Board from 2006 through 2007. Mr. Sobani is a Chartered Accountant specialising in cost and management accounting.

Zafar Iqbal SobaniMember, Board of Privatisation Commission

Mr. Zaffar A. Khan is an adjunct professor at the Institute of Business Administration where he teaches human resource management, and he also teaches at the Pakistan Institute of Corporate Governance. Mr. Khan has over 35 years of professional experience at Engro (previously Exxon) having worked in Pakistan, Hong Kong, United States and Singapore, where he held numerous posts including that of CEO.

Mr. Khan has also served on a number of boards where he is currently a board member of Shell Pakistan, Unilever Pakistan, International Industries, Askari Bank, Acumen Fund Pakistan, and the Pakistan Centre for Philanthropy. Previously, Mr. Khan served as Chairman of Pakistan Telecommunication Company Limited, the Karachi Stock Exchange, Pakistan International Airlines, United Bank, and the State Bank of Pakistan. Mr. Khan has also served as President of Overseas Chamber of Commerce & Industries & several Government of Pakistan committees such as the Economic Advisory Committee, Pay & Pension Committee, and the National Environment Quality Standard.

Mr. Khan completed the Advanced Management Program from the University of Hawaii and has completed courses from the Harvard Business School and INSEAD. He is a recipient of Sitara-e-Imtiaz.

Zaffar Ahmad KhanMember, Board of Privatisation Commission

Mr. Aziz Nishtar is an advocate and legal consultant at Nishtar & Zafar, and has over 28 years of experience in consulting, corporate law, domestic and international tax planning, public private partnerships, joint venture, and government advisory particularly in policy, legislative, and statuary issues regarding taxation and commercial law.

Mr. Nishtar was tax counsel with Engro Corporation and has advised on transaction, legal structures and tax efficiency. He also worked at Tax Analysts. Inc. as a news editor and staff writer; was Assistant Commissioner at the Federal Board of Revenue; Assistant Director at the Export Promotion Bureau; Corporate Planning Officer at Pakistan International Airlines and was an assistant director at the Agriculture Development Bank. Mr. Nishtar has also worked as an advisor to UNICEF, the Sindh Child Protection Authority; Asian Development Bank; Government of Sindh on public procurement policy; IATA; and assisted Barrister Zafarullah Khan.

Mr. Nishtar is a member of the Islamabad High Court Bar Association; member of the Islamabad District Bar Association; member of the Karachi Tax Bar Association; and was admitted to the practice of law in all High Courts in Pakistan. Mr. Nishtar has an LLM in Taxation and Corporate Law from Harvard Law School.

Aziz NishtarMember, Board of Privatisation Commission

14

Mr. Arsallah Khan Hoti is currently the general secretary of PML (N) and a member of the KPK assembly. He has extensive professional experience having served as Managing Director with Shaf Industry and Textile Mill, and as a graduate gemologist with Khyber Exports Ltd. He also has experience in the United Kingdom having worked as a managing director for Savory Healthcare Ltd. He was also a Managing Director of Crescent Ltd.

Mr. Hoti was Director of the Society for Dialogue and Action, and holds memberships and is a committee member of Manifesto Committee PML (N); FATA Reform Committee NDI (National Democrat Institute); and of the Provincial Central Committee KPK. Mr. Hoti has an MBA in marketing from the American University, London.

Arsallah Khan HotiMember, Board of Privatisation Commission

Mr. Salman Burney is the CEO of Glaxo Smith Kline Pakistan, and has regional management responsibility for Iran and Afghanistan. He has extensive experience in chemicals and fibres, agrochemicals and seeds, and in the pharmaceutical industry. Having started his career with ICI and helped develop business lines in chemicals and fibres, he served as Regional Personnel Manager for Africa and Middle East, and as its General Manager for agrochemicals and seeds.

Mr. Burney is former President of the Overseas Investors’ Chamber of Commerce & Industry, and has chaired the Pharma Bureau, and was President of Pakistan Society for Training & Development. Mr. Salman Burney has a degree in economics from Cambridge University, and was a founding trustee of the Oxford & Cambridge Society Educational Trust.

Salman BurneyMember, Board of Privatisation Commission

Shahid Shafiq has extensive senior management experience having served as Chief Executive of Trading Company; country representative of Exxon Mobil Petrochemicals; and as CEO of a textile-spinning mill.

Mr. Shafiq holds memberships in the Board of Governors, IBA, Karachi; Lady Ouffer in Hospital; Executive Committee of Chiniot Islamia School and College; Management Association of Pakistan; Sindh Club; Karachi Boat Club; and Gymkhana. He holds an MBA from the Institute of Business Administration, and is a Gold Medal awardee.

Shahid ShafiqMember, Board of Privatisation Commission

Mr. Nauman K Dar is President and CEO of the Habib Bank Limited, and has extensive experience in the financial services sector. Prior to Habib Bank, Mr. Dar was Vice President at Citibank and Head of Risk Management for East Africa, and was Managing Director at Bank of America. He also holds memberships in the Institute of Directors UK; Institute of Bankers, Pakistan; Pakistan Banks Association; Pakistan Business Council; and the Bretton Woods Committee.

Mr. Dar has an MBA in finance from the University of California, and has taken courses from INSEAD, Harvard Business School, and International Institute of Finance.

Nauman K DarMember, Board of Privatisation Commission

PC NEWSLETTER

PC NEWSLETTER

15

Mr. Ashfaq Yousaf Tola is the senior partner of Naveed Zafar Ashfaq Jaffery & Co. Chartered Accountants. He has the expertise of tax planning and advisory, assurance and business advisory services, international mergers &acquisitions, corporate finance and investment advisory, due diligence and forensic audits, financial product designing and launching, and public listing and ccorporate aaffairs. He was also a partner with Nasir Javed Maqsood Imran Ashfaq, Chartered Accountants, and Principal Strategic Officer at Stallion Textiles; CEO of Fincon; and Chief Internal Auditor at National Development Leasing Corporation, and was a trainee student at A.F. Ferguson & Co., Chartered Accountants.

Mr. Tola holds professional memberships with the Institute of Chartered Accountants of Pakistan, and the Institute of Cost and Management Accountants of Pakistan.

Ashfaq Yousaf TolaMember, Board of Privatisation Commission

Mr. Khurram Schehzad is CEO of Lakson Investments, and has extensive experience in investment research, corporate finance advisory, funds advisory and portfolio management. Previously he served as Vice President at Arif Habib Group, overseeing equity brokerage as well as group research (domestic &international), extending coverage from equities to commodities, real estate, manufacturing (cements, fertilizers, steel, energy and dairies) in direct coordination with the group chair. He also served as Head of Financial and Economic Research at Invest Capital Markets Limited, where he also managed a discretionary/non-discretionary portfolio of equities and fixed income investments for institutional clients. Mr. Schehzad was also Assistant Portfolio Manager at First Capital Investment Management Limited, and has served as a Financial Advisor and Research Consultant to financial brokerages and local business newspapers, on freelance basis. Mr. Schehzad was ranked as one of the Top Analysts in Pakistan (ranked by CFA Pakistan)

Mr. Schehzad is also an Executive Committee Member at the Federal Board of Investment, and served as one of panel judges to the leading local business schools. He is a guest speaker and frequently quoted in both local and international newspapers on financial sector issues.

Mr. Schehzad is currently pursuing a Ph.D. in financial economics. He is a finalist for the Chartered Financial Analyst (CFA) Program, and has an MBA in Finance (Gold Medal/Summa cum laude), and a Bachelor’s degree in Economics, Banking and Management from the University of Karachi.

Khurram SchehzadMember, Board of Privatisation Commission

Mr. Yawar Irfan Khan is a Director of the Lahore Transport Company, director of Oil and Gas Development Company Limited, and Director of the Benazir Income Support Programme. He has over 25 years of experience in marketing, small industries, industrial development, management, international business and trade, tourism, and social sector. Previously, Mr. Khan served as Chairman of the Punjab Chief Minister’s Task Force for Industrial Development, and as Managing Director of the Punjab Small Industries Corporation. He was also Joint Secretary for the Marketing Association of Pakistan, Lahore Chapter.

Mr. Khan is also active in the social and charitable services in the health and education sectors. He was Chairman of the Asifa Irfan Foundation Trust; board member of the Pakistan School of Fashion Design-Lahore; Member of the Board of Governors of the Government Chuna Mandi College for Women in Lahore; Member Citizen of the Police Liaison Committee for Lahore District, and lifetime member of the SAARC Chamber of Commerce and Industry.

Mr. Khan graduated from Government College, Lahore and has a Master’s in Business Administration.

Muhammad Yawar Irfan KhanMember, Board of Privatisation Commission

16

The PC Board, held 22 meetings during 2014-15 and approved the initiation of various strategic sales/ divestments. In doing so, the PC Board approved the appointment of financial advisors, transaction structures, bid prices, offering prices, etc. A glimpse of such decisions are as under:-

Description of Decisions Date of Meeting

Approved initiation of HEC, PIA, NPCC, HBL, UBL, ABL, PPL & OGDCL 8 – 9 January 2014

Approved initiation of FESCO, LESCO & NPGCL (GENCO -III) 20 February 2014

Briefing for PC Board Members & other issues 2 April 2014

Approved appointment of Financial Advisors for OGDCL, PPL & UBL and extended submission of EOIs date for NPCC, FESCO, LESCO, NPGCL & PIA

22 April 2014

Approved transaction structure of UBL and recommended to CCoP 9 May 2014

Approved transaction structure of PPL Offering & Floor Price of UBL Offering and recommended to CCoP

10 June 2014

Approved Strike Price of UBL Offering and recommended to CCoP 11 June 2014

Approved Floor Price of PPL Offering and recommended to CCoP 25 June 2014

Approved Strike Price of PPL Offering and recommended to CCoP 28 June 2014

Approved pre-qualification of Bidders for HEC; approved FAs for NPCC, NPGCL, FESCO, PIA and initiation of HBL Divestment

22 July 2014

Approved Transaction Structure of OGDCL Offering 12 September 2014

Approved Floor Price of OGDCL Offering and recommended to CCoP 5 November 2014

Approved Strike Price of OGDCL Offering and recommended to CCoP 8 November 2014

Approved appointment of FA for ABL divestment 14 November 2014

Approved Transaction Structure for ABL divestment 26 November 2014

Approved Floor Price of ABL Offering and recommended to CCoP; approved to reinitiate HEC strategic sale

9 December 2014

Approved Strike Price of ABL Offering and recommended to CCoP and appointment of FA for HBL divestment.

11 December 2014

Approved appointment of Financial Advisors for FESCO & LESCO; approved Transaction Structure of NPCC Transaction and recommended to CCoP

23 January 2015

Approved pre-qualification of Interested Parties for HEC Transaction; approved Transaction Structure of HBL Transaction and recommended to CCoP

4 February 2015

Approved Reserve Price of HEC strategic sale and recommended to CCoP 9 March 2015

Mandated the Chairman & Secretary, PC to finalize deal with the sole bidder for acquisition of HEC 10 March 2015

Approved Bid Price of HEC strategic sale and recommended to CCoP 24 March 2015

Decisions of the Board of the Privatisation Commission

PC NEWSLETTER

17

CABINET COMMITTEE ON PRIVATISATIONThe Cabinet Committee on Privatisation ("CCOP") was established along with the PC in 1991. It has been functioning continuously except for the brief period from September 1998 to February 2000, when the PC Board headed by the Prime Minister was formulated.

The mandate of the CCOP is to formulate rules for streamlining the functioning of the PC and also serves as a forum for strategic decisions on privatisation and monitoring progress. All major privatisation decisions are placed for approval of the Cabinet through this Committee.

Initially, the CCOP was headed by the Minister for Finance. Then, on 21 September 2004, the Prime Minister reconstituted the CCOP to be chaired by him. However, from 15 November 2008, it was headed by the Advisor to PM on Finance, Revenue, Economic Affairs and Statistics. Currently, it is headed by the Minister for Finance, Revenue, Economic Affairs and Statistics.

CompositionThe following table shows the current composition of the CCOP:

1. Minister for Finance, Economic Affairs, Revenue, Statistics and Privatisation

Chairman

2. Minister for Commerce & Textile Industry

Member

3. Minister for Industries and Production

Member

4. Minister for Law Justice and Human Rights

Member

5. Minister for Planning and Development

Member

6. Minister for Petroleum and Natural Resources

Member

7. Minister for Ports and Shipping Member

8. Minister for Privatisation Member

9. Minister for Water and Power Member

Apart from the above mentioned Members, following can also be invited by Special Invitation.

1. Minister for Planning, Development & Reforms

2. Governor, State Bank of Pakistan

3. Chairman, Privatisation Commission

4. Chairman, Security Exchange Commission of Pakistan

5. Chairman, Board of Investment

6. Secretary, Communications Division

7. Secretary, Finance Division

8. Secretary, Industries and Production

9. Secretary, Petroleum and Natural Resources Division

10. Secretary, Planning & Development Division

11. Secretary, Ports and Shipping Division

12. Secretary, Privatisation Division

13. Secretary, Textile Industry Division

14. Secretary, Water and Power Division

15. Secretary, Board of Investment

* Issued by Cabinet Division vide notification No 5/4/2013-com dated 20.06.2013

Terms of Reference• Formulate the Privatisation Policy for approval of

the Government / Cabinet.

• Approve the PSEs to be privatised on therecommendation of the PC or otherwise.

• Take policy decisions on inter-ministerial issuesrelating to the privatisation process.

• Review and monitor the progress of privatisation.

• Instruct the PC to submit reports/information/data relating to the privatisation process or anymatter relating thereto.

• Take policy decisions on matters pertainingto privatisation, restructuring, deregulation,regulatory bodies and Privatisation Fund Account.

• Approve the reference price in respect of the PSEs being privatised.

• Approve the successful bidders.

• Consider and approve the recommendations ofthe PC on any matter.

• Assign any other task relating to privatisation tothe PC.

* Issued by Cabinet Division vide notification No 5/4/2007-com dated 27.03.2009

18

COUNCIL OF COMMON INTERESTSArticle 153 of the Constitution of Islamic Republic of Pakistan provides for a Council of Common Interests ("CCI") comprising the Chief Ministers of the Provinces and an equal number of members from the Federal Government. The CCI, headed by the Prime Minister of Pakistan, is exclusively responsible to the Parliament.

The CCI formulates and regulates policies in relation to matters in Part II of the Federal Legislative List and exercise supervision and control over related institutions.

Decisions of the CCI are expressed in terms of opinion of the majority. The public entities/ interests etc. contemplated to be privatized are brought before CCI for its approval before submission of summary to the Cabinet.

The present (as of February 2014) composition of CCI is as under:

i. The Prime Minister Chairman

ii. Chief Minister, Baluchistan Member

iii. Chief Minister, Punjab Member

iv. Chief Minister, Sindh Member

v. Chief Minister, Khyber Pakhtunkhwa Member

vi. Pir Syed Sadaruddin Shah Rashadi (by name)

Minister for Overseas Pakistanis & Human Resource Development

Member

vii. Lt. General (Rtd.) Abdul Qadir Baloch (by name)

Minister for States and Frontier Regions

Member

viii. Sardar Muhammad Yousaf (by name)

Minister for Religious Affairs and Interfaith Harmony

Member

* Issued by Cabinet Division vide notification No 2(50)/2013-CCI, dated 08.02.2014

Terms of ReferenceCases relating to formulation and regulation of policies in relation to the following matters and supervision and control over the related institutions shall be submitted to the CCI:

a. Railways

b. Mineral oil and natural gas, liquids and substances declared by Federal law to be dangerouslyinflammable.

c. Development of industries, where developmentunder Federal control is declared by Federal lawto be expedient in the public interest; institutions, establishments, bodies and corporationsadministered or managed by the FederalGovernment immediately before the 14th August, 1973, including Water and Power DevelopmentAuthority and the Pakistan IndustrialDevelopment Corporation; all undertaking,projects and schemes of such institutions,establishments, bodies and corporations;industries, projects and undertaking ownedwholly or partially by the Federal Govt. or by acorporation set up by the Federation.

d. Electricity.

e. Major ports, powers of the ports authoritiestherein.

f. All regulatory authorities established underFederal Law.

g. Fees in respect of any of the matters specifiedabove but not including fees taken in any court.

h. Inter provincial matters and co-ordinations.

i. Legal, medical and other professions.

j. Standards in Institutions for higher educationand research, scientific and technical institutions.

k. Offenses against law with respect to any of thematters specified above.

l. Inquiries and statistics for the purposes of any ofthe matters specified above.

m. Matters incidental or ancillary to any of thematters specified above.

n. Complaints as to interference with water supplies (Article 155 of the Constitution).

o. Implementation of the directions given by theparliament for action by the Council (Article154(4) of the Constitution)

Approval of Privatisation ProgramThe CCI in 1997 and 2006 approved a broad-based privatisation program including PSEs in various sectors like banking & finance, oil & gas, power, infrastructure, transport, industries & production etc.

Moreover, post 18th Amendment to the Constitution, the PC in 2011 and 2014, sought approval of the CCI for the privatisation of all GENCOs & DISCOs.

Moreover, only the new cases are submitted to CCI for decision, as the previous decisions of CCI remain valid.

PC NEWSLETTER

PC NEWSLETTER

1918

PC NEWS

20

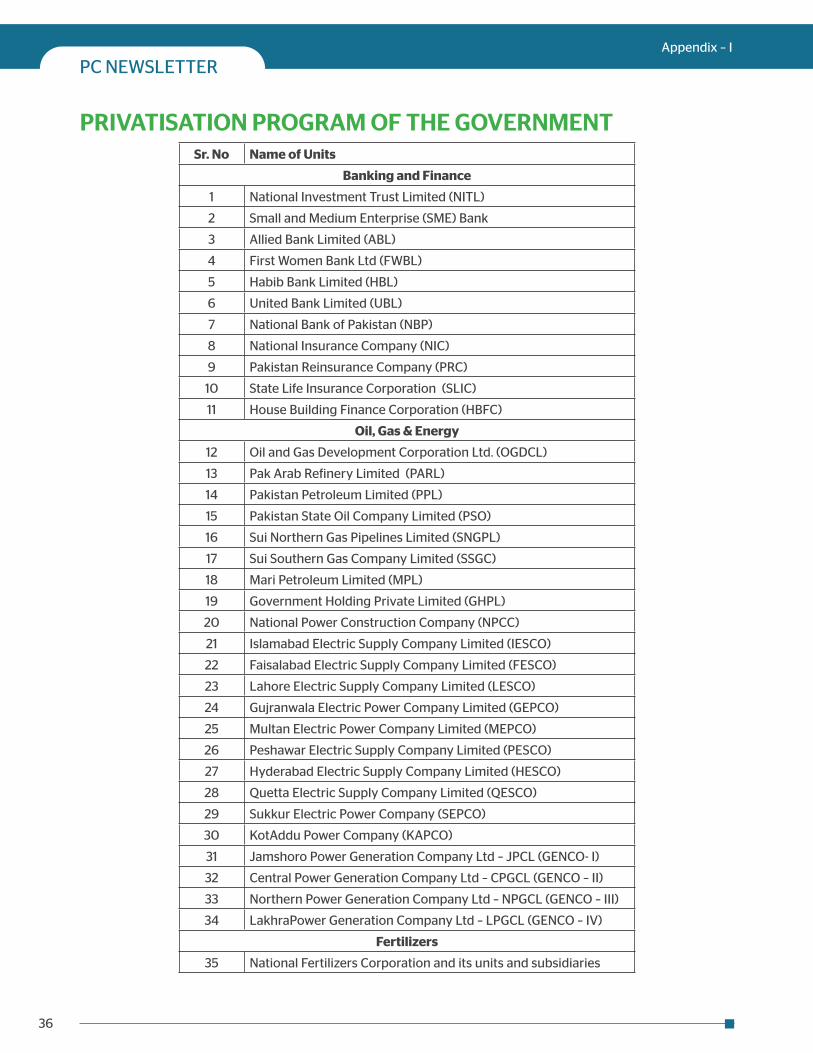

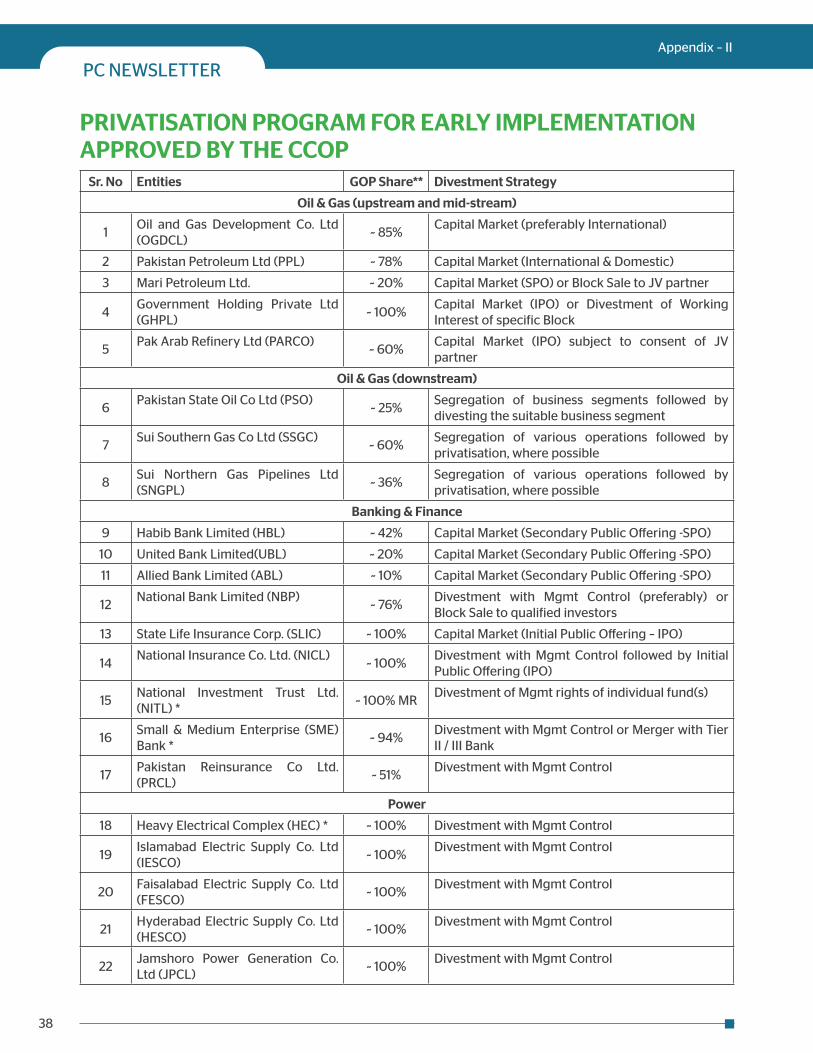

PRIVATISATION PROGRAMPrivatisation is a high priority area for the present Government as part of its overall economic reforms agenda. The scope of the PC includes PSEs in the power, oil & gas, banking & insurance, infrastructure & transport, telecom, real estate and industrial sectors. The CCI in 1997, 2006, 2011 & 2014 had approved a broad-based privatisation program of the entities falling in the purview of Federal Legislative List, Part-II. Moreover, the CCOP in October 2013 and June 2014approved a broad-based (Appendix-I) as well as priority privatisation program (Appendix-II).

To harness the private sector’s capital and managerial potential the program was modeled around the concept of Public Private Partnerships ("PPP") wherein the management is to be transferred to investors through sale of 26% shares and strategic sales. The program also focused on divestments through the capital markets to enhance the attractiveness and visibility of Pakistan as a favored investment destination.

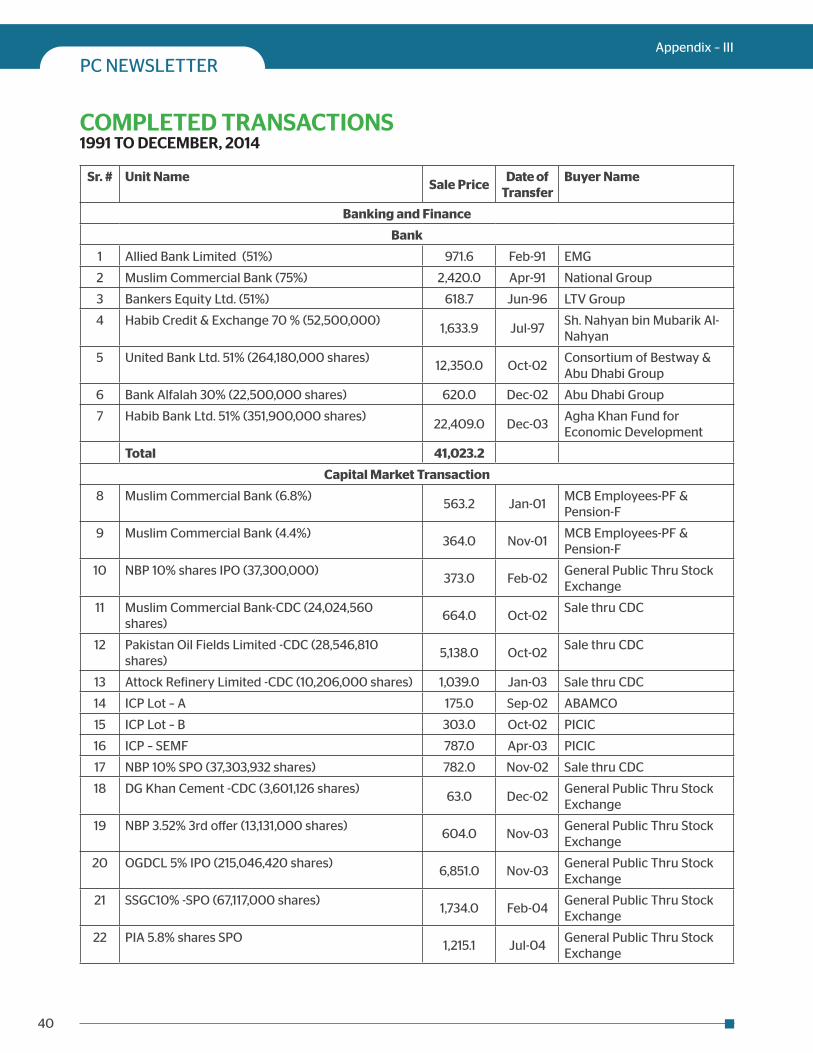

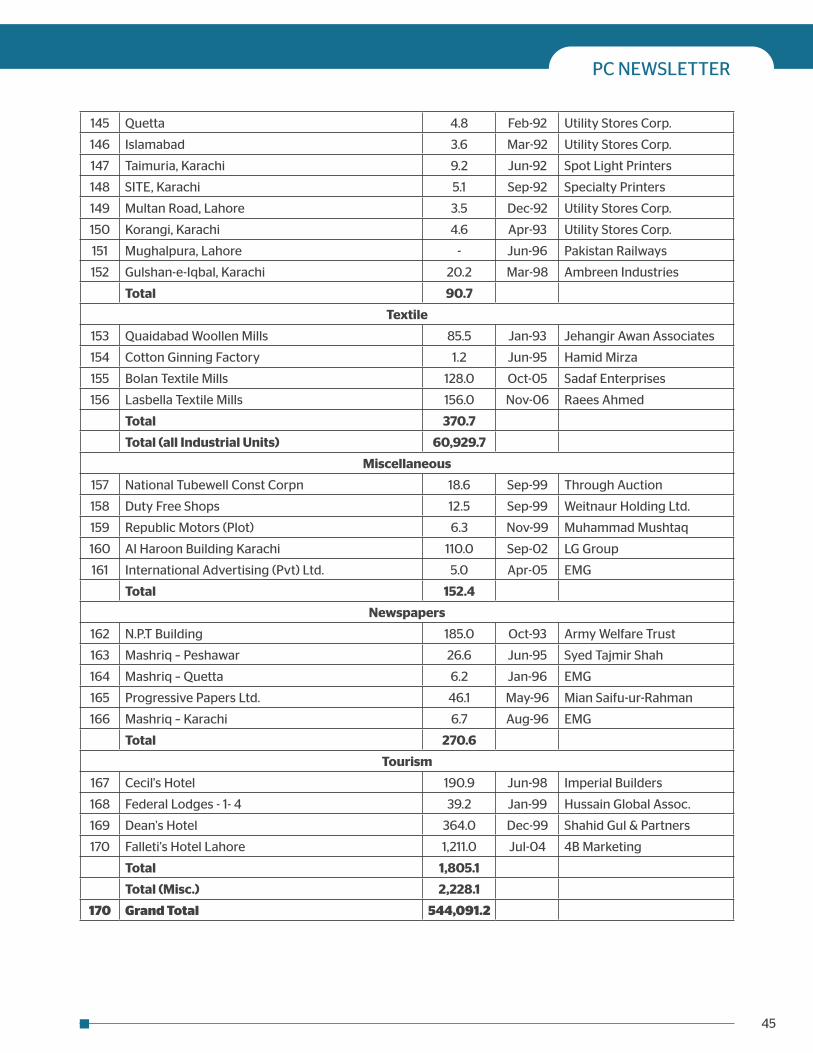

ACHIEVEMENTS OF PRIVATISATION COMMISSIONSince its inception in 1991, the PC has completed 170 transactions for PKR 544.091 billion (Appendix-III). During this phase, the PC completed many high-valued market transactions (about 35% of total proceeds) apart from asset/ strategic sales (about 65% of total proceeds). Banking, telecommunication and industrial sector privatisations are the hallmarks of the program, as they had contributed about 90% of the total proceeds.

Achievements during the tenure of current GovernmentSubsequent to the approval of the CCoP in October 2013, the PC initiated various strategic sales and divestment of shares of various PSEs. In June 2014, two (02) Capital market transactions were accomplished. The first one was of United Bank Limited, which re-initiated the privatisation program after a lapse of almost eight years, which was followed by divestment of Pakistan Petroleum Limited shares. In December 2014, residual shares of Allied Bank Limited were divested.

Moreover, following strategic sales/ divestments are in pipeline:-

Sr. # Unit Mode of Transaction

Oil & Gas Sector

1 Oil & Gas Development Co. Ltd. ("OGDCL") Local & Int’l Capital Market Transactions

Banking & Finance

2 Habib Bank Limited ("HBL") Capital Market (Secondary Public Offering -SPO)

Power Sector

3 Heavy Electrical Complex ("HEC") Divestment with Management Control

4 National Power Construction Corp. ("NPCC") Divestment with Management Control

5 Faisalabad Electric Supply Co. Ltd ("FESCO") Divestment with Management Control

6Northern Power Generation Co. Ltd. ("NPGCL" – GENCO - III) - Thermal Power Station – (TPS) Muzaffargarh (1350 MW)

Divestment with Management Control

7 Lahore Electric Supply Company Limited ("LESCO") Divestment with Management Control

8Islamabad Electric Supply Company Limited ("IESCO")

Divestment with Management Control

Industries, Transport & Real Estate

9 Pakistan International Airlines Corp ("PIA")Restructuring followed by divestment of 26% GoP equity stakes to strategic partner with Management control

PC NEWSLETTER

PC NEWSLETTER

21

KEY HIGHLIGHTS OF CAPITAL MARKET TRANSACTIONS

UNITED BANK LTD ("UBL") TRANSACTION

• One of the Largest Capital Market Transactionin Pakistan raising over PKR 38 billion includingForeign Exchange of over USD 310 million for theGovernment of Pakistan (GoP)

• Total demand of over PKR 63 billion (~USD 632million) generated at selling price of PKR 158 pershares i.e. Demand of ~394 million shares againstthe offer size of ~242 million shares

• Generated robust international demand of overUSD 500 million (equivalent of PKR 50 billion) atthe selling price of PKR 158 per share

• Generated domestic demand of over PKR 12billion at the selling price of PKR 158 per share

• Over 30 international equity fund managers/qualified institutional buyers (QIB’s) participatedand successfully allocated ~81% of total offer sizeof ~ 242 million shares

• Over 200 domestic institutional and high networth individuals (HNWIs) participated andsuccessfully allocated ~19% of the total offer sizeof ~ 242 million shares

PAKISTAN PETROLEUM LIMITED ("PPL") TRANSACTION

• One of the largest ever domestic secondarypublic offering: GOP divested approximately 5%GOP shareholding in PPL raising PKR 15.3 billionor USD 155 million.

• Via domestic book building mechanism: PPLtransaction was the largest domestic bookbuilding ever conducted in the history of thecountry.

• First ever GOP offering through book building:PPL’s SPO was the first time the Governmentutilized the domestic book building mechanismto offer shares to the local investors. Historically,the government has used GDRs for internationaltransactions and public offer through balloting for local transactions.

• First transaction where deal price was higherthan market price: The offering price determinedvia book building for PPL was PKR 219 per sharewhich was at a premium of 7% to the floor price,a premium of 2.4% to June 25, 2014 closing price(floor price was set on June 25, 2014) and 0.5%premium to the last day (June 27, 2014) closingprice (PKR 217.94). This was the first instance inthe history of Pakistan’s capital markets whereoffering price was higher than the market price.

• Oversubscribed by 2.04x: Domestic and foreigninvestors bought aggressively which resulted inoversubscription of 2.04 times. Participation ofdomestic investors in PPL was significantly higher than the recently conducted offering of UBL,which signifies the trust domestic investors havein the capital markets and the future progress ofthe country.

• Demand in excess of PKR 30 billion: Bids in excess of PKR 30 billion were received, surpassing thecumulative demand for all the domestic capitalmarket transactions concluded in the last 2-3years.

ALLIED BANK LTD (ABL) TRANSACTION

• Generated a total demand of over ~PKR 21 billion

• Demand from Foreign Investors exceeded ~USD30 million

• Oversubscribed by 1.4 x i.e. generated a demandof ~185 million shares against the offer size of ~131million shares

• Offering price at ~2.5% discount, to the closingprice on that day beating the Asia Region discount benchmarks for precedent transactions

• Over 325 domestic and international investorsparticipanted areas including Peshawar, Multan,Faisalabad, Rawalpindi in addition to theconventional three cities of Islamabad, Lahore &Karachi

• Upbeat demand/ allocation from individualinvestors i.e. ~40% due to lowering minimum bidsize from PKR 1 million to PKR 500,000.

22

IFR Asia’sIssuer of the YearIslamic Republic of

Pakistan

M a n y A s i a n

i s s u e r s raised funds

with ease in 2014, but only

one capped a remarkable

turnaround with offerings in both the

debt and equity capital markets. For putting itself

firmly back on the global markets map, the Islamic

Republic of Pakistan is IFR Asia’s Issuer of the Year.

Issuer of the YearThe Islamic Republic of Pakistan

embarked on ambitious capital-raising plans in 2014, presenting investors

throughout the international markets with an optimistic turnaround growth story. This

allowed Pakistan’s new government to do two things, the country of 180 million had not been

able to do in about seven years: price a US dollar bond and sell shares in the capital markets.

In April, the sovereign printed a USD 2 billion offering bonds at tenors of five and 10 years in April and, in June, it

launched a PKR 38 billion (USD 370 million) offer for sale in United Bank and a PKR 15.3 billion (USD 155 million) stake sale

in Pakistan Petroleum.

These transactions were no mere showpieces. They were vital to Pakistan’s future. The proceeds helped increase foreign-exchange

reserves and cut the fiscal deficit, two improvements required under a USD 6.7 billion conditional support package agreed with the International

Monetary Fund in late 2013, just months after pro-business Prime Minister Nawaz Sharif came to office.

Pakistan had been forced to turn to the IMF to avert a balance-of-payments crisis in November 2008, after a run on the PKR, amid the global crisis, left it frozen out

of the international capital markets. However, the IMF ended its support in 2011 after Pakistan showed little sign of economic reform, and the final USD 3.7 billion of a USD

11.3 billion rescue package was never disbursed.

Having regained the IMF’s support 2013, the GOP needed to show real progress in improving its fiscal position. It also needed to convince investors that the reform-minded

prime minister could maintain stability in the face of severe political and economic challenges.

Pakistan tested the waters with a USD 100 million 360-day loan in December 2013, its first syndicated facility in 15 years, and increased the size to USD 172.5 million after six other

lenders joined leads Credit Suisse, Standard Chartered and Pakistan’s United Bank Limited.

A mandate for a US dollar sovereign bond followed in early January 2014, as the GOP set out to take advantage of the global hunt for yield, which had led money managers lower and lower down

the credit spectrum.

Days before the mandate, B1/B+/BB– rated Sri Lanka had priced a successful USD 1 billion five-year bond, hinting at the extent of global demand. Pakistan, however, with its far lower ratings of Caa1/B– and a bigger

target size, needed to work hard to attract a similar response.

When bookrunners Bank of America, Merrill Lynch, Barclays, Citigroup and Deutsche Bank started marketing the USD 2 billion deal around the end of March, they had many data points with which to impress investors. The

IMF had just increased to 3.1% from 2.8% its growth forecast for Pakistan in the 2013–14 fiscal year, and the GOP had just announced an ambitious plan to privatise more than 60 PSEs to help fill a hole in its budget.

PC NEWSLETTER

23

Pakistan’s outstanding dollar bonds were also trading at all-time low yields. The 6.875% June 2017 notes – the country’s last global issue before the crisis – dipped below 7% in February for the first time since they were launched in 2007, quite a recovery from yields of over 15% in early 2012.

The results were striking. The USD 1 billion five-year bond priced to yield 7.25%, and the USD 1 billion 10-year tranche printed at 8.25%.

The rate on the 10-year bonds was particularly low. Just days before Pakistan came to market, B+/B rated Zambia printed a USD 1 billion 10-year offering at 8.625%. Investors clearly valued Pakistan’s prospects, despite the lower rating.

“In broad terms, Pakistan’s credit fundamentals have improved since the new government came into office last year,” said Agost Benard, associate director of sovereign ratings, at Standard & Poor’s. “Given a B– rating, Pakistan’s current conditions are fairly benign, and the improved macroeconomic setting was what enabled the government to launch a bond this year.”

Fund managers in the US, the UK and Europe bought the majority of both tranches, signalling a strong vote of confidence in the country.

PrivatisationIt was only a matter of weeks before Pakistan was back in the international markets, this time with a share offering of Karachi-listed United Bank. In June, the country disposed of its 19.8% stake in the bank, raising PKR 38 billion, the government’s first equity offering since it sold a 7.5% stake in Habib Bank for PKR 12 billion in 2007.

It was a crucial first step towards the government target to raise PKR 198 billion through privatisation in the fiscal year ending 30 June 2015, and the first of 65 PSEs earmarked for partial privatisations over the next five years.

There was a lot riding on this transaction, something Mohammad Zubair, chairman of the privatisation commission, knew well. Before investors could really be convinced of the viability of Pakistan’s privatisation plan, the PC had to convince bankers, advisers, lawyers and accountants that the country was serious. Pakistan had hired equity advisers in the recent past, only to have those planned deals go nowhere.

“I went to New York and London within two months of taking the job (to talk to the financing community),” said Zubair, who was appointed in December 2013. “This was the first indication for them that we were serious about this. If we couldn’t convince them, obviously we couldn’t do this.”

Arif Habib, Credit Suisse and Elixir Securities were eventually named joint lead managers.

Because the bank was already listed, and the government held a minority stake, it was easier to garner political support for the trade.

“Pakistan restarted its privatisation program with the less controversial deals, and it’s a smart move,” said Ali Naqvi, head of equities for Asia Pacific at Credit Suisse. “They sought to sell companies that were already partially privatised – and at smaller stakes.”

In the end, foreign investors bought almost 80% of the 241.9 million shares on offer.

“Investors liked the story a lot because the banking sector is growing and, with more stock from the sale, the name would become more liquid,” Naqvi said.

Additonally, money managers, including Templeton Asset Management, Wellington Management, Everest Asset Management, Lazard, BlackRock and Morgan Stanley, participated despite reports of militant attacks at the country’s main airport days before the deal closed.

“It was actively participated by the major funds,” Zubair said. “When we went around on the roadshows, we were able to sell the Pakistan story – Pakistan as a place to invest. There is interest in our economic momentum.”

Professional teamThe transaction also put the country in good stead for what would come next.

“United Bank’s story is good, and the government delivered on execution like a professional team,” Credit Suisse’s Naqvi said. “Because of that, we were able to generate a well-oversubscribed order book. Then, once it was listed, the stock did well, which was good news for the rest of the privatisation plans.”

United Bank priced at PKR 158 in early June and on August 5 it hit a 2014 high of PKR 202. That was good news because Pakistan had plans to sell takes in Allied Bank and Habib Bank.

The GOP did not waste any time building on the success of the United Bank sale. Weeks afterwards, it sold a 5% stake in Pakistan Petroleum for PKR 15 billion, its second capital markets privatisation of the year and one that was heavily marketed to domestic investors.

“We went around the country to places where the privatisation commission would never have gone (in the past) to drum up interest – even among people who never would have participated,” Zubair said. “We wanted to spread the idea of privatisation around the country to everyone in the country.”

It sold 70.1 million shares at PKR 219 each in a mainly domestic deal that was twice covered, with a handful of foreign investors also taking part.

Not every deal was a success, however. Oil and Gas Development Corp decided to pull its offering of up to PKR 69.8 billion in global depositary receipts, owing a weak response from investors as oil prices tanked globally. Zubair said the country would try to sell the deal again in 2015.

As ever, it is difficult to disentangle the fiscal benefits of privatisation from politics. Indeed, one way the government sought to put Pakistan in a positive light locally was to show citizens how much international investor interest there was for its companies.

“That was another challenge. We had to say to people: ‘Look, Pakistan’s not falling apart. These financial institutions participating in UBL is a great thing for us. This is positive momentum’,” Zubair said.

24

Heavy Electrical Complex ("HEC")The Cabinet Committee on Privatisation in its meeting held on 26 March 2015, under the chairmanship of Senator Ishaq Dar, Federal Minister for Finance, approved strategic sale of 97% shares of Heavy Electrical Complex (HEC) to Cargill Holdings Ltd. for PKR 905 million, far in excess of the reserve price set by the Privatization Commission Board and the Cabinet Committee on Privatization. The Government of Pakistan retains 3% of the shares.

Cargill’s offer also assumes liabilities of PKR 435 million, PKR 250 million in cash ‘up front’ and, in addition, another PKR 30 million to cover employee gratuity and provident fund obligations. Finally, Cargill will forego tax benefits associated with five years of losses amounting to PKR 190 million.

Cargill also has stated its intention to market abroad thereby earning, in time, foreign exchange.

“The net to the Government of Pakistan is PKR 905 million,” said Mohammad Zubair, Chairman, Privatization Commission (PC) while briefing the CCOP. Zubair added that in three previous attempts agreement with a qualified investor had not been possible.

In 2006-07, four investors initially expressed interest, two interested parties pre-qualified, but neither put up ‘earnest money.’

In 2011-12, four parties expressed interest, however, none met pre-qualification criteria apart from one which failed to deposit the earnest money after conducting due diligence.

Again, in 2013 three parties pre-qualified, only two conducted due diligence, but neither deposited the earnest money required after conducting the due diligence due to the weak condition of the company.

“The earlier failed attempts to privatize the company is a statement of HEC’s poor condition,” Zubair said. “We are pleased to have a qualified buyer of Cargill’s calibre and have agreed to such favourable terms”, Zubair remarked.

Finance Minister Ishaq Dar on this occasion said that he had always advocated observance of complete transparency in the privatization process and desired that employees interest should be accorded due importance. These principles are to be followed in letter and spirit in all transactions to be carried out by the PC, the Minister added.

Habib Bank Limited ("HBL")The CCOP and the Board of the Privatisation Commission approved the transaction structure for the divestment of the residual GOP shares in the HBL on 4 February 2015.

A team comprising of Chairman, Secretary and Transaction Manager, Privatisation Commission and management team of HBL is currently conducting roadshows at Karachi, Hong Kong, Singapore, London, New York and Dubai. They will have One to One meetings with the potential investors to market the transaction. The transaction is likely to be concluded in April 2015.

Expected Capital Market/ Strategic Sales

25

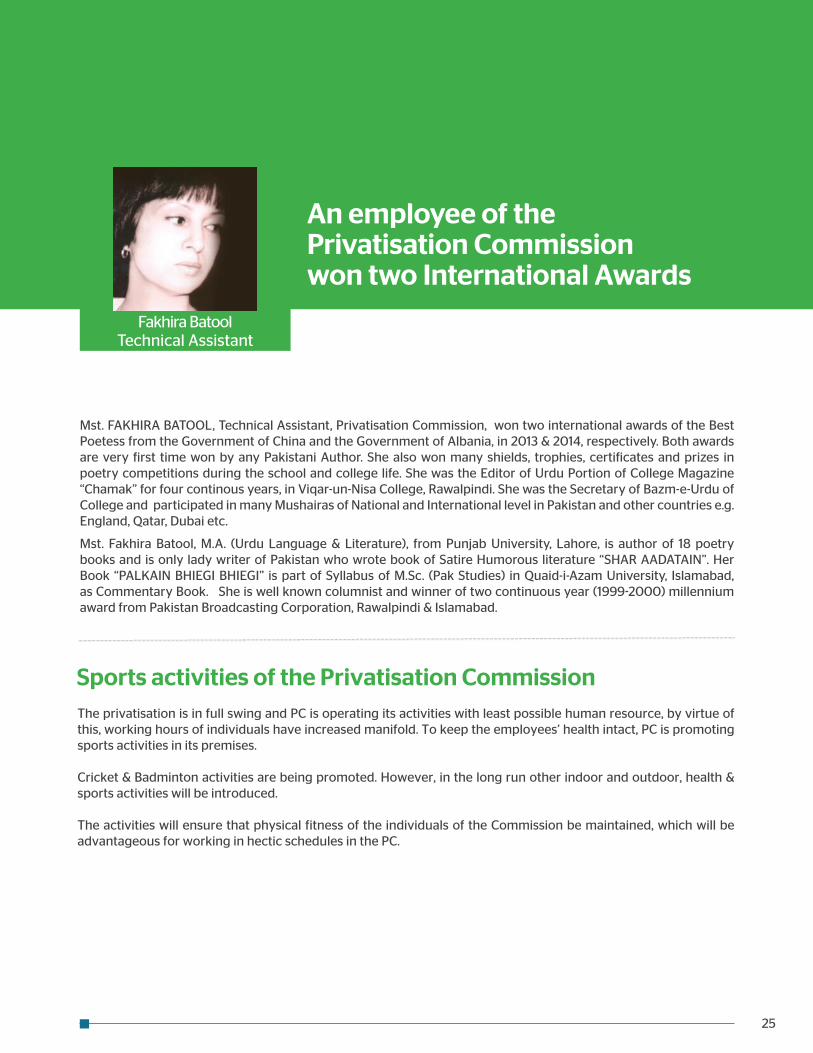

Mst. FAKHIRA BATOOL, Technical Assistant, Privatisation Commission, won two international awards of the Best Poetess from the Government of China and the Government of Albania, in 2013 & 2014, respectively. Both awards are very first time won by any Pakistani Author. She also won many shields, trophies, certificates and prizes in poetry competitions during the school and college life. She was the Editor of Urdu Portion of College Magazine “Chamak” for four continous years, in Viqar-un-Nisa College, Rawalpindi. She was the Secretary of Bazm-e-Urdu of College and participated in many Mushairas of National and International level in Pakistan and other countries e.g. England, Qatar, Dubai etc.

Mst. Fakhira Batool, M.A. (Urdu Language & Literature), from Punjab University, Lahore, is author of 18 poetry books and is only lady writer of Pakistan who wrote book of Satire Humorous literature “SHAR AADATAIN”. Her Book “PALKAIN BHIEGI BHIEGI” is part of Syllabus of M.Sc. (Pak Studies) in Quaid-i-Azam University, Islamabad, as Commentary Book. She is well known columnist and winner of two continuous year (1999-2000) millennium award from Pakistan Broadcasting Corporation, Rawalpindi & Islamabad.

An employee of thePrivatisation Commission won two International Awards

Fakhira BatoolTechnical Assistant

Sports activities of the Privatisation CommissionThe privatisation is in full swing and PC is operating its activities with least possible human resource, by virtue of this, working hours of individuals have increased manifold. To keep the employees’ health intact, PC is promoting sports activities in its premises.

Cricket & Badminton activities are being promoted. However, in the long run other indoor and outdoor, health & sports activities will be introduced.

The activities will ensure that physical fitness of the individuals of the Commission be maintained, which will be advantageous for working in hectic schedules in the PC.

26

PC NEWSLETTER

27

28

PC NEWSLETTER

29

Articles

30

By: Mr. Asad Rasool

Pakistan was one of the first countries in the region to initiate deregulation and liberalization of the economy and start the privatisation process. There have been some important privatisation successes in the industrial, telecommunications and financial sectors, since the start of this process in the early 1990s. As a consequence, the telecom sector contributed ~PKR 245 billion to the national exchequer during FY 2013-14, whereas the 4 large privatized commercial banks, namely Muslim Commerical Bank ("MCB"), Habib Bank Limited ("HBL"), United Bank Limited ("UBL") & Allied Bank Limited ("ABL"), paid ~PKR 36 billion in income tax alone during 2013. The privatisation program has been instrumental in mobilizing both foreign direct investment ("FDI") and local savings. In view of its strategic importance, privatisation is a core element of the economic revival program of the present Government. List of entities included in the program, duly approved by the Council of Common Interests, is placed at Appendix-I.

Key components of the overall framework for privatisation include a transparent process, an enhanced overall socio-economic environment, investment climate, market conditions and improvement in the country’s risk profile and corporate governance. The outcomes envisaged include reduced fiscal burden, improved service delivery and creation of shareholder value. Individual privatisation transactions are considered on an entity specific basis with the objective of increasing competition, protecting employees and consumer interests, and meeting strategic, economic and social needs.

In order to harness the private sector’s capital and managerial potential, the privatisation program is modeled around the concept of Public Private Partnership ("PPP") wherein management will be transferred to investors, preferably through sale of 26% share, subject to various factors including sectoral dynamics, entity’s size & economic status, and investors’ interest. The program also includes divestments through strategic sales and capital market to enhance the attractiveness and visibility of Pakistan

as a favored investment destination. Program for Early Implementation, approved by the Cabinet Committee on Privatisation on October 03, 2013 and amended thereafter, is placed at Appendix-II.

Since the restarting the privatisation program by the present Government in 2013, after a gap of almost six year, the Commission has successfully completed three capital market offerings, namely UBL, PPL and ABL, raising gross proceeds of ~PKR 68 billion including foreign exchange of over USD 350 million, compared to proceeds of PKR 476 billion raised by completion of 167 transactions between 1991 and 2008. Global debt and equity offerings by the GOP have been acknowledged internationally, as is evident from the award of ‘Issuer of the Year’ given to Pakistan by IFR Asia. Furthermore, the UBL transaction also received the “Best Deal Award” for Pakistan by The Asset, one of Asia’s most prestigious corporate ranking journals. This has put Pakistan firmly back on the global markets map besides improving the standing of domestic capital markets.

The PC has completed one of the five planned transactions during FY 2014-15, namely the ABL offering. Details of the FY 2014-15 Plan are as follows:

Privatisation Flows in FY 2014-2015

PC NEWSLETTER

PC NEWSLETTER

31

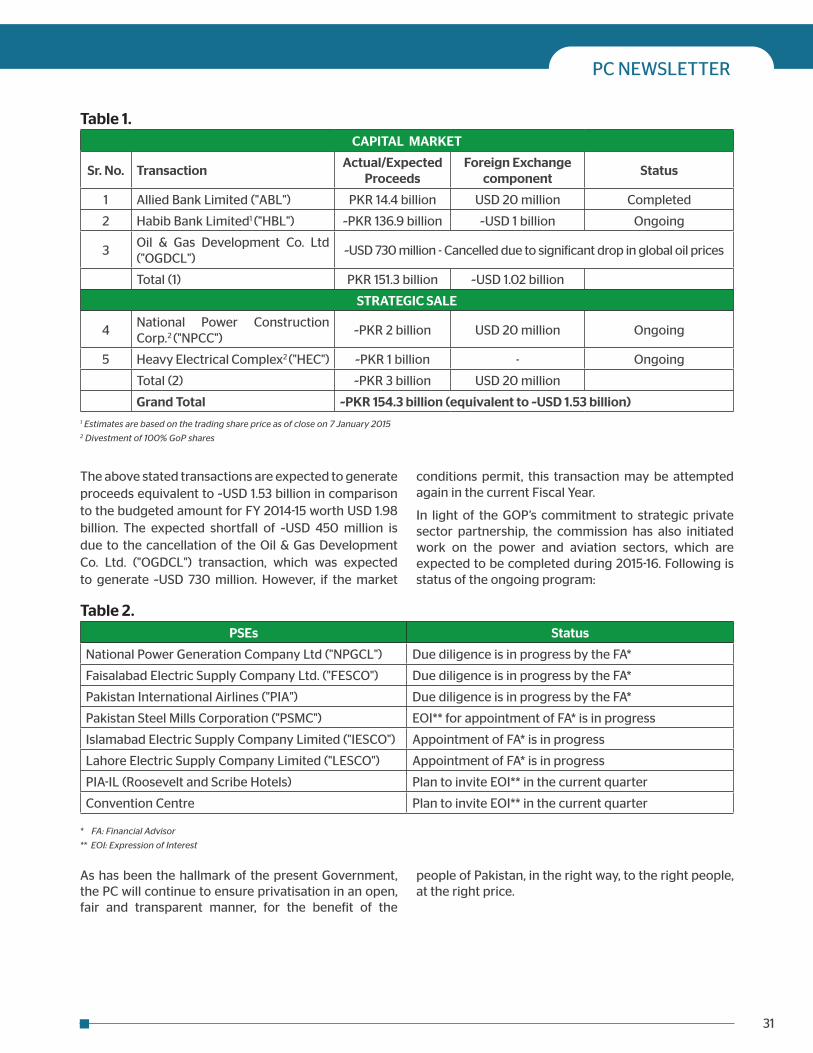

Table 1.CAPITAL MARKET

Sr. No. TransactionActual/Expected

ProceedsForeign Exchange

componentStatus

1 Allied Bank Limited ("ABL") PKR 14.4 billion USD 20 million Completed

2 Habib Bank Limited1 ("HBL") ~PKR 136.9 billion ~USD 1 billion Ongoing

3Oil & Gas Development Co. Ltd ("OGDCL")

~USD 730 million - Cancelled due to significant drop in global oil prices

Total (1) PKR 151.3 billion ~USD 1.02 billion

STRATEGIC SALE

4National Power Construction Corp.2 ("NPCC")

~PKR 2 billion USD 20 million Ongoing

5 Heavy Electrical Complex2 ("HEC") ~PKR 1 billion - Ongoing

Total (2) ~PKR 3 billion USD 20 million

Grand Total ~PKR 154.3 billion (equivalent to ~USD 1.53 billion)1 Estimates are based on the trading share price as of close on 7 January 20152 Divestment of 100% GoP shares

The above stated transactions are expected to generate proceeds equivalent to ~USD 1.53 billion in comparison to the budgeted amount for FY 2014-15 worth USD 1.98 billion. The expected shortfall of ~USD 450 million is due to the cancellation of the Oil & Gas Development Co. Ltd. ("OGDCL") transaction, which was expected to generate ~USD 730 million. However, if the market

conditions permit, this transaction may be attempted again in the current Fiscal Year.

In light of the GOP’s commitment to strategic private sector partnership, the commission has also initiated work on the power and aviation sectors, which are expected to be completed during 2015-16. Following is status of the ongoing program:

As has been the hallmark of the present Government, the PC will continue to ensure privatisation in an open, fair and transparent manner, for the benefit of the

people of Pakistan, in the right way, to the right people, at the right price.

Table 2.PSEs Status

National Power Generation Company Ltd ("NPGCL") Due diligence is in progress by the FA*

Faisalabad Electric Supply Company Ltd. ("FESCO") Due diligence is in progress by the FA*

Pakistan International Airlines ("PIA") Due diligence is in progress by the FA*

Pakistan Steel Mills Corporation ("PSMC") EOI** for appointment of FA* is in progress

Islamabad Electric Supply Company Limited ("IESCO") Appointment of FA* is in progress

Lahore Electric Supply Company Limited ("LESCO") Appointment of FA* is in progress

PIA-IL (Roosevelt and Scribe Hotels) Plan to invite EOI** in the current quarter

Convention Centre Plan to invite EOI** in the current quarter

* FA: Financial Advisor

** EOI: Expression of Interest

32

By: Dr. Kabir Sidhu

Normative Objectives of Islamic and Conventional EconomicsIslam does not claim to have invented the market based system, however, it took measures to enhance and improve its spirit and its efficiency with its ethical approach. Islamic economic philosophy articulates that markets do not simply provide a platform for exchange. It enables participants to maximise profit subject to promoting falah and collective social welfare in the society. Quran articulates, “Eat not up your property amongst yourselves by vanities: but let there be trade with mutual consent”.

Shariah subscribes to “exchange with mutual consent” as the most basic denominator in any transaction and an equitable form of distribution of wealth in the society. Centuries later, Adam Smith, a major proponent of laissez-faire and the father of modern economics also based his free market philosophy on a similar proposition, which he called “trade by mutual consent to mutual advantage.” Both parties gain and wealth is created. Exchange appears to be the fundamental concept and common denominator both in Islamic economics and conventional economics.

The aggregate or cumulative effect of the exchanges with mutual consents lead to fair price formation mechanism and facilitates resource allocation in the economy. It represents natural equilibrium of forces of demand and supply which distributes wealth equitably in the society. Most legal and regulatory frameworks across the globe aim to facilitate smooth interplay of market forces, uninterrupted natural equilibrium devoid of exploitation in the economy. The society reaps the benefit in the form of optimum competition resulting in better quality products and services to the public in general.

Pakistani Markets and Privatisation Policy It is a sad fact that the presence of the PSEs in almost every segment of Pakistani market distorts the forces of demand and supply disrupting the natural equilibrium. There is no doubt that most of the Pakistani markets are distorted and to some extent manipulated. It undermines the integrity of the markets and investors depart in search of safer heavens.

The PSEs are operating in oil and gas, electricity, aviation, banking and many other fields. The result is poor and despicable quality service to the public. The

Government as the market player as well as the umpire is the root of all problems in free market economy. The PSEs receive preferential services and are not subject to normal forces of demand and supply. They are generally run by the bureaucrats and has no fear of regulatory measures being imposed upon them by their fellow bureaucrats heading the regulators. Government as market players and as regulators undermines all principles of economics in running the country. The PSEs negates the normal forces of demand and supply and undermines the dynamic of the market. These PSEs neither learn from the market nor do they try to innovate to remain profitable and competitive. They know they will be taken care of by the government. Thus they end up creating their own culture which is almost impossible to change.

This calls in question that the entire legal, regulatory and structural framework of various segments of the markets need to completely revamped to bring it in alignment with the free market economy in 21st century. This is the ambitious task that has been entrusted to the PC.

The common theme of critics on privatisation attempt to create a false perception that Pakistan is falling apart with the willy-nilly sale of PSEs in a less then transparent manner. They mercilessly criticise the current privatisation policy of deregulation, liberalisation, public private partnership and revamping of the legal and regulatory framework in the key areas of oil, gas and electricity as a dictation from the US, World Bank and IMF. They often equate it with selling the family silver. The reality is quite the contrary. It’s the need of the time to increase competition in all segments of the market to bring foreign investment and ensure sustainable economic development.

For the last decade or so, terrorism has hampered the foreign investment in the country so much so that the domestic investor is fleeing with their capital to more stable and secure destinations. The first step in the direction to revive the economic stagnation is government and opposition’s recent consensus in terrorism policy which sends out the message to the international investors that “it means business.” The second step is the ongoing privatisation policy. Markets and investors communicate in their own language. In aggregate, the local and international market response cannot be instigated or dictated. This is obvious from the reception of issuances of Sukuk worth USD. 2 billion

1 “Eat not up your property amongst yourselves by vanities: but let there be trade with mutual consent” Al-Quran 4:29.

Economic Objectives and Privatisation in Pakistan

PC NEWSLETTER

PC NEWSLETTER

33

By: Anjum Nazir

As brief review in context of banks and financial institutions in Pakistan

IntroductionFor any country well-functioning financial sector is necessary for enhancing the efficiency of intermediation, which is achieved by mobilizing domestic savings, channeling them into productive investment by identifying and funding good business opportunities, reducing information, transaction, and monitoring costs and facilitating the diversification of risk. This results in efficient allocation of resources, contributing to a more rapid accumulation of physical and human capital, and faster technological progress, which in turn lead to higher economic growth.

NationalizationPakistan’s financial sector suffered a major setback with nationalization of domestic Banks under the Banks Nationalization Act 1974. The Pakistan Banking Council was formed to supervise the nationalized commercial

banks. By 1990s, the banking sector was suffering from, over-staffing and branches, massive non-performing loans, poor customer services and product ranges, political interference and personnel issues. Pakistan’s banking sector was rooted in a failure of governance and lack of financial discipline owing to undue political interference in the financial intermediation process, especially in the NCBs and DFIs. NCDs and DFIs were the major source of bad loans accounting for the 90% of the bad loans in the entire system and were the main loss makers.

PrivatisationThis led the Government to initiate the privatisation process in the early 1990s as part of economic reforms program and in 1991, the PC was established for disposing PSEs. The mission statement of PC clearly shows the objectives of privatisation. Privatisation process of the financial sector in the country commenced with MCB and ABL in 1991.

Privatisation coupled with the banking reforms were aimed to strengthen the sources of governance and

as well as the domestic offerings of UBL and ABL. The markets response was loud and clear to the surprise of all our critics. Keen investor’s interest and subsequently two international awards for the recent domestic capital market offerings endorse our privatisation policy and establish Pakistan as a favourable place of investment.

One of the objectives of privatisation policy is to ensure sustainable, social economic infrastructure development through public private partnership by divesting strategic management. United Kingdom was one of the first countries to start the private finance initiative across a broad range of sectors (transport, education, health, prisons, defence, leisure, government offices, environment, housing, courts, technology and others). About 80% of the projects were completed on time and within the budget compared with the 30% in the private sectors. Public and private sectors collaborate on the basis of a clearly defined sharing of the tasks and the risks to achieve the benefit of added value and increased efficiency. Project related risks are transferred to the private entity. This enables the government to focus on policy, strategy and monitoring role rather than service delivery. Another example is china who became the world player by privatising the public property. Similarly, China reduced the state owned enterprises from 1.4 million to 468,000 between

1995 – 2001, as part of its structural reforms.

The critics also advocate the sale of PSEs is against the national interest and technically they should be revived by restructuring first and then resold at higher price. It ignores the fact that these institutions almost cost PKR 500 billion to the tax payers annually. The government loses revenue and the potential tax it can collect from privatised PSEs. It also distorts the overall market deterring the potential market players from entry.