private placement investor presentation

TRANSCRIPT

PRIVATE PLACEMENTINVESTOR PRESENTATION

08 April 2021

2© Avance Gas

IMPORTANT INFORMATION (I/II)

THIS PRESENTATION AND ITS CONTENTS ARE CONFIDENTIAL AND NOT FOR DISTRIBUTION OR RELEASE, IN WHOLE OR IN PART, DIRECTLY OR INDIRECTLY, IN OR INTO THE UNITED STATES OF AMERICA (INCLUDING ITS TERRITORIES AND POSSESSIONS, ANY STATE OF THE UNITED

STATES OF AMERICA AND THE DISTRICT OF COLUMBIA) (THE "UNITED STATES"), AUSTRALIA, CANADA, THE HONG KONG SPECIAL ADMINISTRATIVE REGION OF THE PEOPLE'S REPUBLIC OF CHINA OR JAPAN, OR ANY OTHER JURISDICTION IN WHICH THE DISTRIBUTION OR RELEASE

WOULD BE UNLAWFUL. THIS PRESENTATION IS NOT AN OFFER OR INVITATION TO BUY OR SELL SECURITIES IN ANY JURISDICTION.

This presentation and its appendices (collectively the "Presentation") has been produced by Avance Gas Holding Ltd. ("Avance Gas" or the "Company", together with its subsidiaries the "Group") with assistance from DNB Markets, a part of DNB Bank ASA (the "Manager"), solely for

information purposes in connection with a contemplated offering of shares by the Company in a private placement (the "Private Placement").

The Presentation is intended for information purposes only, and does not itself constitute, and should not be construed as, an offer, invitation or recommendation to purchase, sell or subscribe for any securities in any jurisdiction and neither the issue of the information nor anything

contained herein shall form the basis of or be relied upon in connection with, or act as an inducement to enter into, any investment activity. Prospective investors in the Private Placement are required to read the offering material and other relevant documentation which is released in

relation thereto for a description of the terms and conditions of the Private Placement.

The Presentation and its contents is strictly confidential and by reviewing it, you are acknowledging its confidential nature, and are agreeing to abide by the terms of this disclaimer. For the purposes of this notice, "Presentation" means and includes this document and its appendices,

any oral presentation given in connection with this Presentation, any question and answer session during or after such oral presentation and any written or oral material discussed or distributed during any oral presentation meeting. The Presentation may not be copied, distributed,

reproduced, published or passed on, directly or indirectly, in whole or in part, or disclosed by any recipient, to any other person (whether within or outside such person's organisation or firm) or published in whole or in part, by any medium or in any form for any purpose or under any

circumstances.

The Company strongly suggests that each recipient seeks its own independent advice in relation to any financial, legal, tax, accounting or other specialist advice. In particular, nothing herein shall be taken as constituting the giving of investment advice and these materials are not

intended to provide, and must not be taken as, the exclusive basis of any investment decision or other valuation and should not be considered as a recommendation by the Company (or any of its affiliates) or the Manager that any recipient enters into any transaction. These materials

comprise a general summary of certain matters in connection with the Group. These materials do not purport to contain all of the information that any recipient may require to make a decision with regards to any transaction. Any decision as to whether or not to enter into any

transaction should be taken solely by the relevant recipient. Before entering into such transaction, each recipient should take steps to ensure that it fully understands such transaction and has made an independent assessments of the appropriateness of such transaction in the light

of its own objectives and circumstances, including the possible risks and benefits of entering into such transaction.

Neither the Company or the Manager have taken any steps to verify any of the information contained herein. No representation or warranty (express or implied) is made as to, and no reliance should be placed on, any information, including projections, estimates, targets and opinions,

contained herein, and no described herein. liability whatsoever is accepted as to any errors, omissions or misstatements contained herein, and, accordingly, none of the Company or the Manager or any of their parent or subsidiary undertakings or any such person's officers or

employees accepts any liability whatsoever arising directly or indirectly from the use of the Presentation. This Presentation speaks only as of 8 April 2021, and the views expressed are subject to change based on a number of factors, including, without limitation, macroeconomic and

equity market conditions, investor attitude and demand, the business prospects of the Group and other specific issues. These materials and the conclusions contained herein are necessarily based on economic, market and other conditions, as in effect on, and the information

available to the Company and the Manager as of, their date. These materials do not purport to contain a complete description of the Group or the markets in which the Group operates, nor do they provide an audited valuation of the Group. The analyses contained in these materials

are not, and do not purport to be, appraisals of the assets, stock or business of the Group or any other person. Moreover, these materials are incomplete without reference to, and should be viewed and considered solely in conjunction with, the oral briefing provided by an authorised

representative of the Company in relation to these materials. None of the Company, and/or the Manager undertakes any obligation to amend, correct or update this Presentation or to provide any additional information about any matters.

3© Avance Gas

IMPORTANT INFORMATION (II/II)

An investment in the Company involves significant risk, and several factors could adversely affect the business, legal or financial position of the Company or the value of its securities. The recipient should carefully review the chapters on "Risk Factors" in the Presentation for a

description of certain of the risk factors that will apply to an investment in the Company’s securities.

This Presentation may contain certain forward-looking statements relating to the business, financial performance and results of the Company and/or the industry in which it operates. Forward-looking statements concern future circumstances and results and other statements that are

not historical facts, sometimes identified by the words "believes", "expects", "predicts", "intends", "projects", "plans", "estimates", "aims", "foresees", "anticipates", "targets", and similar expressions. Any forward-looking statements contained in this Presentation, including

assumptions, opinions and views of the Company or cited from third party sources are solely opinions and forecasts which are subject to risks, uncertainties and other factors that may cause actual events to differ materially from any anticipated development. None of the Company,

the Manager or any of their parent or subsidiary undertakings or any such person's officers or employees provides any assurance that the assumptions underlying such forward-looking statements are free from errors nor does any of them accept any responsibility for the future

accuracy of the opinions expressed in this Presentation or the actual occurrence of the forecasted developments. None of the Company or the Manager assume any obligation to update any forward-looking statements or to conform any forward-looking statements to our actual

results.

These materials are not intended for distribution to, or use by, any person in any jurisdiction where such distribution or use would be contrary to local laws or regulations. By accepting these materials, each recipient represents and warrants that it is able to receive them without

contravention of an unfulfilled registration requirements or other legal or regulatory restrictions in the jurisdiction in which such recipients resides or conducts business. The Company does not accept any liability to any person in relation to the distribution or possession of these

materials in or from any jurisdiction.

The Company has not authorized any offer to the public of securities or has undertaken any action to make an offer of securities to the public requiring the publication of an offering prospectus, in any member state of the European Economic Area (the "EEA"). This Presentation is

directed at persons in member states of the EEA, who are "qualified investors" within the meaning of Article 2(e) of Prospectus Regulation (Regulation (EU) 2017/1129).

The securities of the Company have not been and will not be registered under the US Securities Act of 1933 (the "Securities Act") or with any securities regulatory authority of any state or jurisdiction of the United States and may not be offered, sold, resold, pledged, delivered,

distributed or transferred, directly or indirectly, into or within the United States unless registered under the Securities Act or pursuant to an applicable exemption from, or in a transaction not subject to, the registration requirements of the Securities Act or in compliance with any

applicable securities laws of any state or jurisdiction of the United States. Accordingly, any offer or sale of securities will only be offered or sold (i) within the United States or to U.S. Persons, only to qualified institutional buyers as defined under Rule 144A under the Securities Act

("QIBs") in offering transactions not involving a public offering and (ii) outside the United States in offshore transactions in accordance with Regulation S. Any purchaser of securities in the United States, or to or for the account of U.S. Persons, will be deemed to have been made

certain representations and acknowledgements, including without limitation that the purchaser is a QIB.

These materials are exempt from the general restriction (in section 21 of the Financial Services and Markets Act 2000 ("FSMA")) on the communication of invitations or inducements in investment activity pursuant to the FSMA (Financial Promotion) Order 2005 as amended (the "Order")

on the ground that in the United Kingdom, these materials are being directed at a restricted number of persons who are: (A)(i) persons having professional experience in matters relating to investments, i.e., investment professionals within the meaning of Article 19(5) of the Order; (ii)

high net worth entities falling within the meaning of Article 49(2)(a) to (d) of the Order; or (iii) any other person to whom it can otherwise be lawfully distributed, and (B) "Qualified Investors" as defined in section 86 of the FSMA (persons meeting criteria "A" and "B" are referred to herein

as "Relevant Persons").

This Presentation is subject to Norwegian law, and any dispute arising in respect of this Presentation is subject to the exclusive jurisdiction of Norwegian courts with Oslo city court (Nw: Oslo tingrett) as exclusive venue.

TRANSACTION HIGHLIGHTS

5© Avance Gas

TRANSACTION HIGHLIGHTS

• Private placement of up to ~$70m and plans to increase the newbuilding program from four to six dual fuel 91k VLGCs

• Attractive average purchase price of 78.9m (70% of purchase price payable at or close to delivery date)

• Superior earnings power (c. 30% premium vs a non eco VLGC) and significantly reducing environmental emissions

6x dual fuel VLGC newbuildings withsuperior earnings power

Significant operating leverage and cash flow

potential

Leading VLGC operator with industry low G&A

Compelling near term market fundamentals

• Leading operator of modern VLGCs with a fleet of 13 VLGCs on the water and 6 newbuilds (including the two options)

• Modern, energy efficient fleet and lean and efficient operating structure with industry leading G&A

• Tier 1 sponsor through the Seatankers system

• Balanced vessel supply with moderate VLGC order book and aging fleet - 20-25% of fleet to dry dock annually in 2020-22

• Oil price rebound expected to increase Middle East exports and fuel vessel demand into high season

• Higher oil prices also leave upside potential to US LPG production and export forecasts

• Low cash break even and significant operating leverage enabling for a proforma cash yield of ~27% at current 1yr t/c rates

• No dry-dockings before 2023 and no debt maturities before 2024

• Strong balance sheet enabling attractive dividend capacity

6© Avance Gas

BACKGROUND FOR THE TRANSACTION

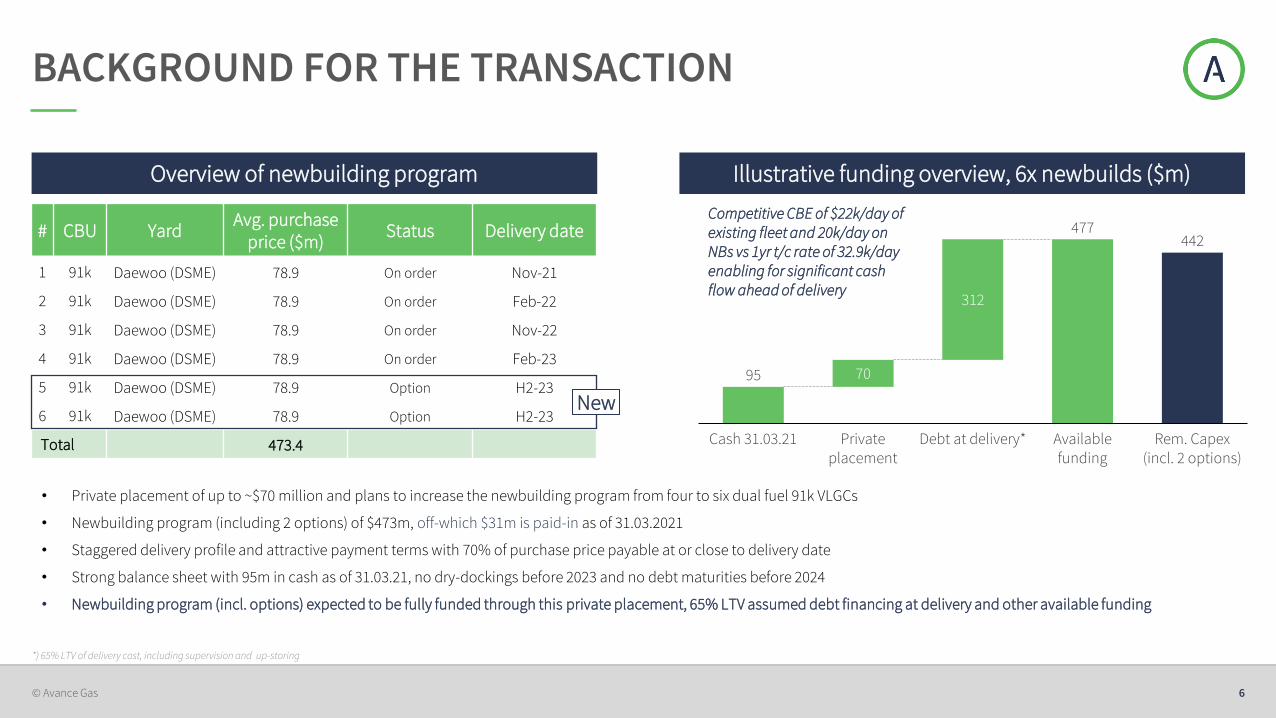

Overview of newbuilding program Illustrative funding overview, 6x newbuilds ($m)

• Private placement of up to ~$70 million and plans to increase the newbuilding program from four to six dual fuel 91k VLGCs

• Newbuilding program (including 2 options) of $473m, off-which $31m is paid-in as of 31.03.2021

• Staggered delivery profile and attractive payment terms with 70% of purchase price payable at or close to delivery date

• Strong balance sheet with 95m in cash as of 31.03.21, no dry-dockings before 2023 and no debt maturities before 2024

• Newbuilding program (incl. options) expected to be fully funded through this private placement, 65% LTV assumed debt financing at delivery and other available funding

95

477442

70

312

Private placement

Cash 31.03.21 Debt at delivery* Available funding

Rem. Capex (incl. 2 options)

# CBU YardAvg. purchase

price ($m)Status Delivery date

1 91k Daewoo (DSME) 78.9 On order Nov-21

2 91k Daewoo (DSME) 78.9 On order Feb-22

3 91k Daewoo (DSME) 78.9 On order Nov-22

4 91k Daewoo (DSME) 78.9 On order Feb-23

5 91k Daewoo (DSME) 78.9 Option H2-23

6 91k Daewoo (DSME) 78.9 Option H2-23

Total 473.4

New

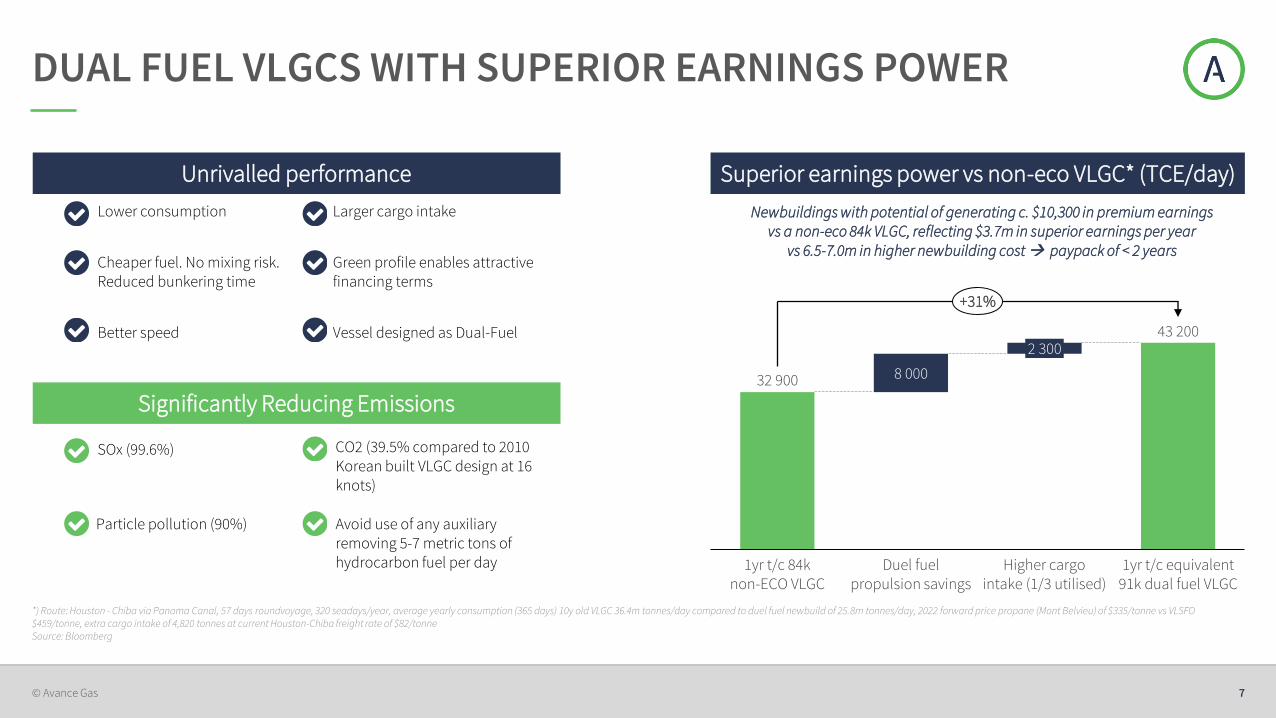

Competitive CBE of $22k/day of existing fleet and 20k/day on NBs vs 1yr t/c rate of 32.9k/day enabling for significant cash flow ahead of delivery

*) 65% LTV of delivery cost, including supervision and up-storing

7© Avance Gas

• SOx (99.6%)

•

DUAL FUEL VLGCS WITH SUPERIOR EARNINGS POWER

Unrivalled performance Superior earnings power vs non-eco VLGC* (TCE/day)

Lower consumption

Cheaper fuel. No mixing risk.Reduced bunkering time

Better speed

Larger cargo intake

Green profile enables attractive financing terms

Vessel designed as Dual-Fuel

Significantly Reducing Emissions

CO2 (39.5% compared to 2010 Korean built VLGC design at 16 knots)

32 900

43 200

8 000

1yr t/c 84k non-ECO VLGC

Duel fuel propulsion savings

1yr t/c equivalent 91k dual fuel VLGC

2 300

Higher cargo intake (1/3 utilised)

+31%

Newbuildings with potential of generating c. $10,300 in premium earnings vs a non-eco 84k VLGC, reflecting $3.7m in superior earnings per year

vs 6.5-7.0m in higher newbuilding cost → paypack of < 2 years

*) Route: Houston - Chiba via Panama Canal, 57 days roundvoyage, 320 seadays/year, average yearly consumption (365 days) 10y old VLGC 36.4m tonnes/day compared to duel fuel newbuild of 25.8m tonnes/day, 2022 forward price propane (Mont Belvieu) of $335/tonne vs VLSFO $459/tonne, extra cargo intake of 4,820 tonnes at current Houston-Chiba freight rate of $82/tonneSource: Bloomberg

Avoid use of any auxiliary removing 5-7 metric tons of hydrocarbon fuel per day

Particle pollution (90%)

8© Avance Gas

*) Cash flow calculated based on CBE rates subtracted from X-axis TCE rates, adding $14,900/v/d for newbuilds with LPG propulsion and $4,300 /v/d for scrubber fitted vessels. Cash flow yield calculated on fully delivered and annualized cash flow basis divided by pro-forma market cap of $420million based on pre-money market cap of $350 million and ~$70 million capital raise **) Premium for dual fuel based on Houston - Chiba via Panama Canal, 57 days roundvoyage, 320 seadays/year, average yearly consumption (365 days) 10y old VLGC 36.4m tonnes/day compared to duel fuel newbuild of 25.8m tonnes/day, 2022 forward price propane (Mont Belvieu) of $335/tonne vs VLSFO $459/tonne, extra cargo intake of 4,820 tonnes at current Houston-Chiba freight rate of $82/tonne. 1/3 of higher order intake utilised. Premium for scrubber benefits based on Houston -Chiba via Panama Canal, 57 days round voyage, 320 seadays/year, average yearly consumption (365 days) 10y old VLGC 36.4m tonnes/day, 2022 forward price VLSFO (Singapore) of $459/tonne vs HSFO (Singapore) $331/tonneSource: Bloomberg, Clarksons SIN

STRONG CASH FLOW AND DIVIDEND POTENTIAL

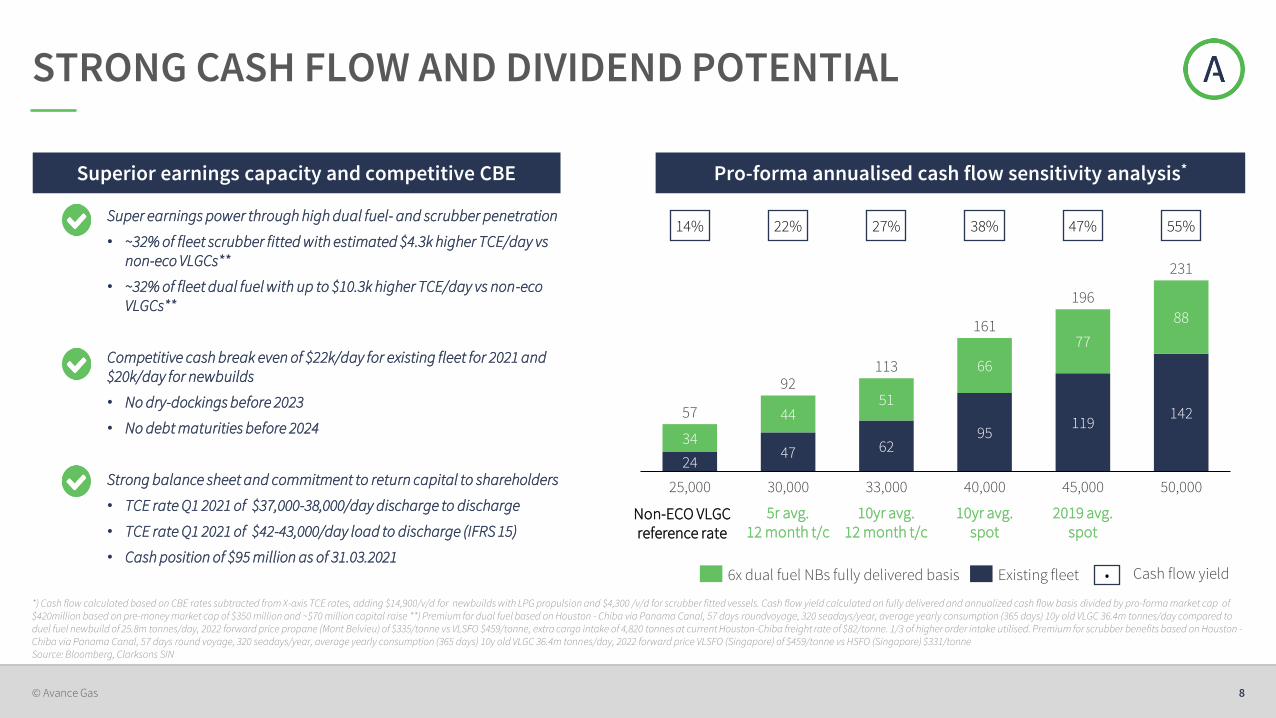

Superior earnings capacity and competitive CBE Pro-forma annualised cash flow sensitivity analysis*

2447 62

95119

142

34

4451

66

77

88161

25,000 40,000 45,00030,000 33,000

57

50,000

92113

196

231

14% 22% 27% 38% 47%

6x dual fuel NBs fully delivered basis Existing fleet

10yr avg. 12 month t/c

10yr avg. spot

2019 avg. spot

5r avg. 12 month t/c

55%

• Cash flow yield

Super earnings power through high dual fuel- and scrubber penetration

• ~32% of fleet scrubber fitted with estimated $4.3k higher TCE/day vs non-eco VLGCs**

• ~32% of fleet dual fuel with up to $10.3k higher TCE/day vs non-eco VLGCs**

Competitive cash break even of $22k/day for existing fleet for 2021 and $20k/day for newbuilds

• No dry-dockings before 2023

• No debt maturities before 2024

Strong balance sheet and commitment to return capital to shareholders

• TCE rate Q1 2021 of $37,000-38,000/day discharge to discharge

• TCE rate Q1 2021 of $42-43,000/day load to discharge (IFRS 15)

• Cash position of $95 million as of 31.03.2021

Non-ECO VLGC reference rate

9© Avance Gas

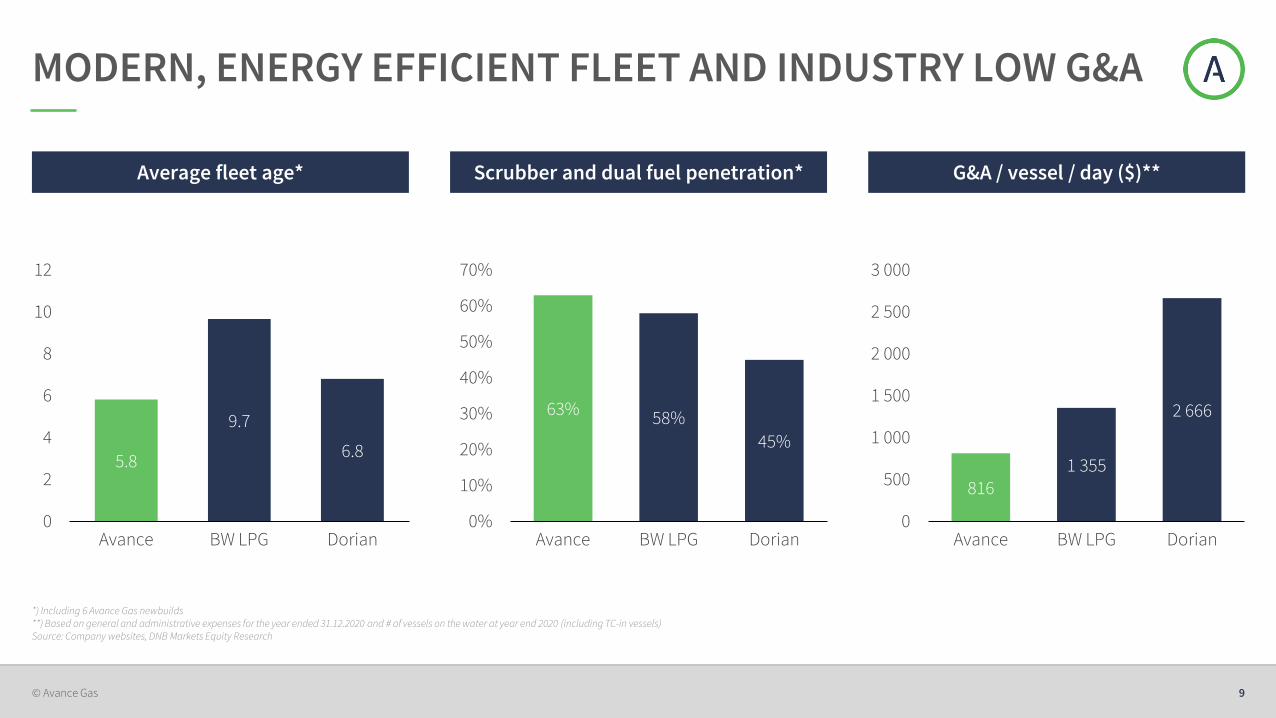

*) Including 6 Avance Gas newbuilds **) Based on general and administrative expenses for the year ended 31.12.2020 and # of vessels on the water at year end 2020 (including TC-in vessels)Source: Company websites, DNB Markets Equity Research

MODERN, ENERGY EFFICIENT FLEET AND INDUSTRY LOW G&A

8161 355

2 666

0

500

1 000

1 500

2 000

2 500

3 000

DorianBW LPGAvance

5.8

9.7

6.8

0

2

4

6

8

10

12

DorianBW LPGAvance

Scrubber and dual fuel penetration*Average fleet age* G&A / vessel / day ($)**

63% 58%

45%

0%

10%

20%

30%

40%

50%

60%

70%

DorianAvance BW LPG

10© Avance Gas

Source: Clarksons SIN

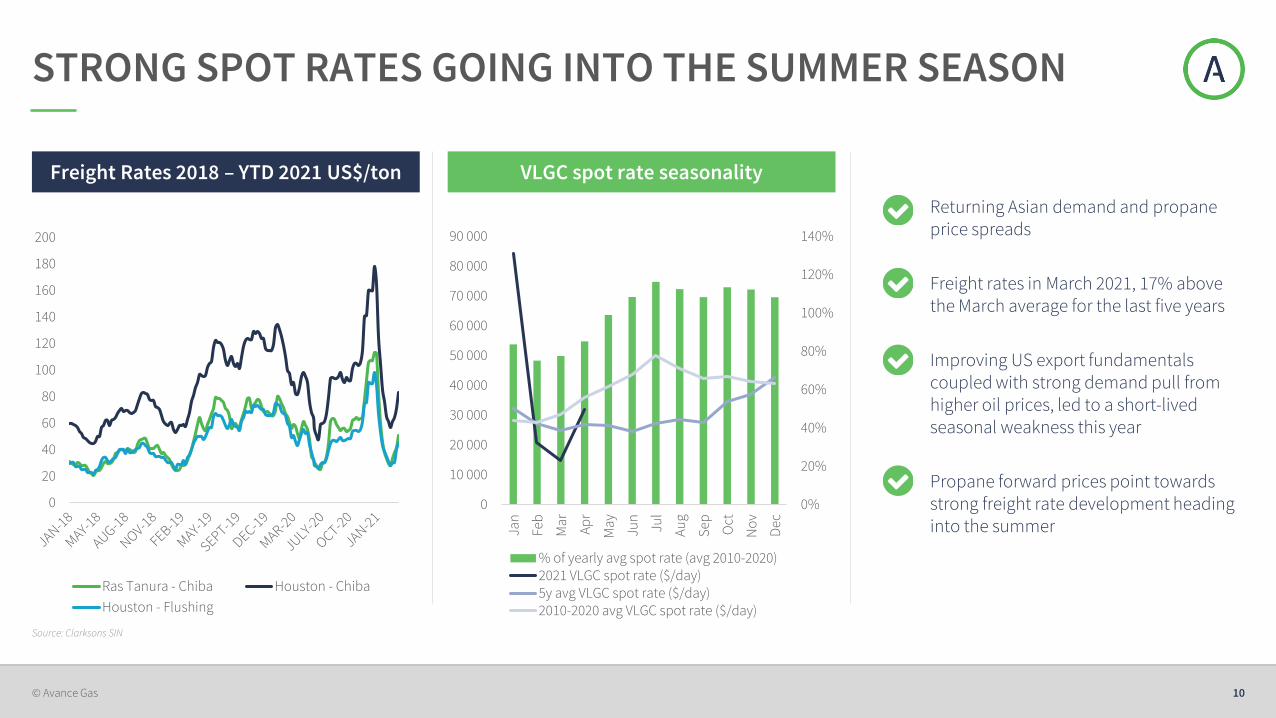

STRONG SPOT RATES GOING INTO THE SUMMER SEASON

Freight Rates 2018 – YTD 2021 US$/ton VLGC spot rate seasonality

Returning Asian demand and propane price spreads

Freight rates in March 2021, 17% above the March average for the last five years

Improving US export fundamentals coupled with strong demand pull from higher oil prices, led to a short-lived seasonal weakness this year

Propane forward prices point towards strong freight rate development heading into the summer

0

20

40

60

80

100

120

140

160

180

200

Ras Tanura - Chiba Houston - Chiba

Houston - Flushing

0%

20%

40%

60%

80%

100%

120%

140%

0

10 000

20 000

30 000

40 000

50 000

60 000

70 000

80 000

90 000

Jan

Feb

Mar

Ap

r

May

Jun

Jul

Au

g

Sep Oct

No

v

Dec

% of yearly avg spot rate (avg 2010-2020)2021 VLGC spot rate ($/day)5y avg VLGC spot rate ($/day)2010-2020 avg VLGC spot rate ($/day)

11© Avance Gas

COMPELLING MARKET FUNDAMENTALS

Supply Production and demand Avance Gas outlook

Moderate orderbook and aging fleet

14% of global fleet above 20 years

Increased US exports for 2021 and improving arbitrage fundamentals

Oil price rebound expect to increase US production forecast

Increasing demand in India, China and South Korea

Plans to increase newbuilding program from four to six dual fuel 91k VLGCs with superior earnings power, taking an important step towards de-carbonisation and contributing to a greener shipping industry

TCE rate Q1 2021 of $37,000-38,000/day discharge to discharge, with significant operating leverage in to the summer season

Strong fundamentals and fully tradeable fleet creating significant cash flow potential

20-25% of fleet to dry dock annually in 2020-22

MARKET UPDATE

50%

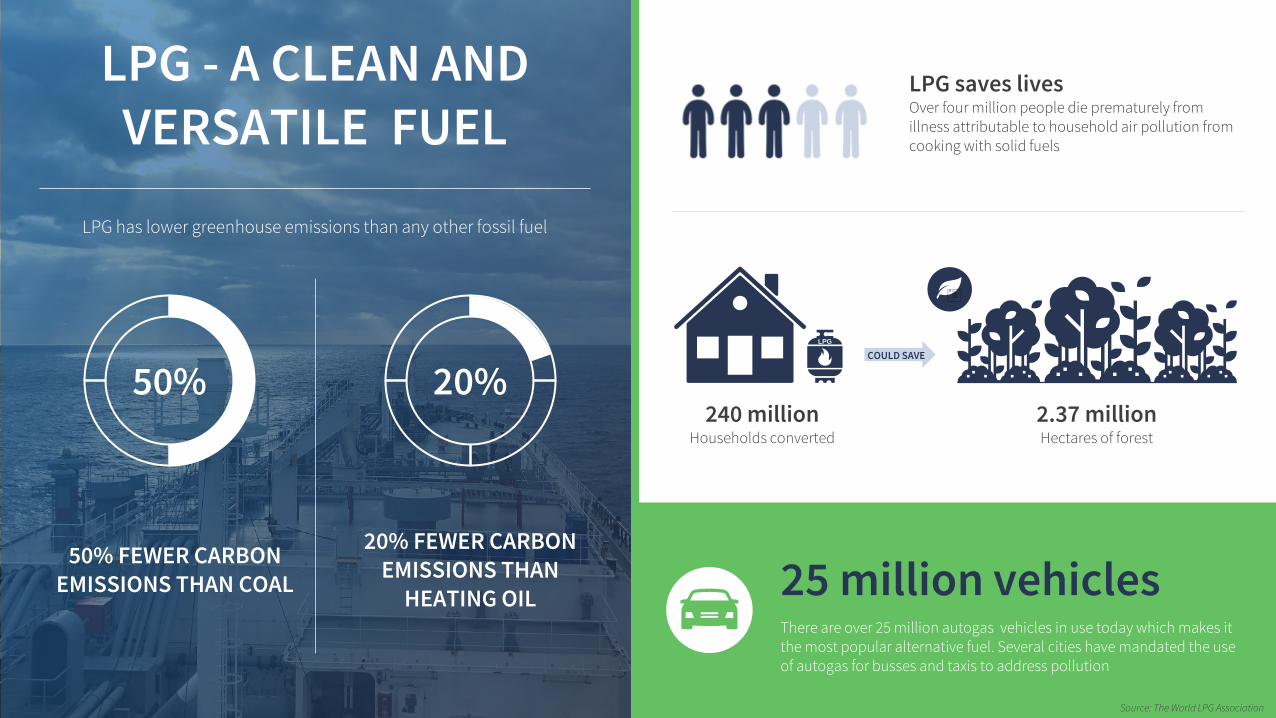

50% FEWER CARBONEMISSIONS THAN COAL

LPG - A CLEAN AND VERSATILE FUEL

25 million vehiclesThere are over 25 million autogas vehicles in use today which makes it the most popular alternative fuel. Several cities have mandated the use of autogas for busses and taxis to address pollution

LPG saves livesOver four million people die prematurely from illness attributable to household air pollution from cooking with solid fuels

LPG has lower greenhouse emissions than any other fossil fuel

20% FEWER CARBONEMISSIONS THAN

HEATING OIL

Source: The World LPG Association

20%

LPG

COULD SAVE

240 millionHouseholds converted

2.37 millionHectares of forest

14© Avance Gas

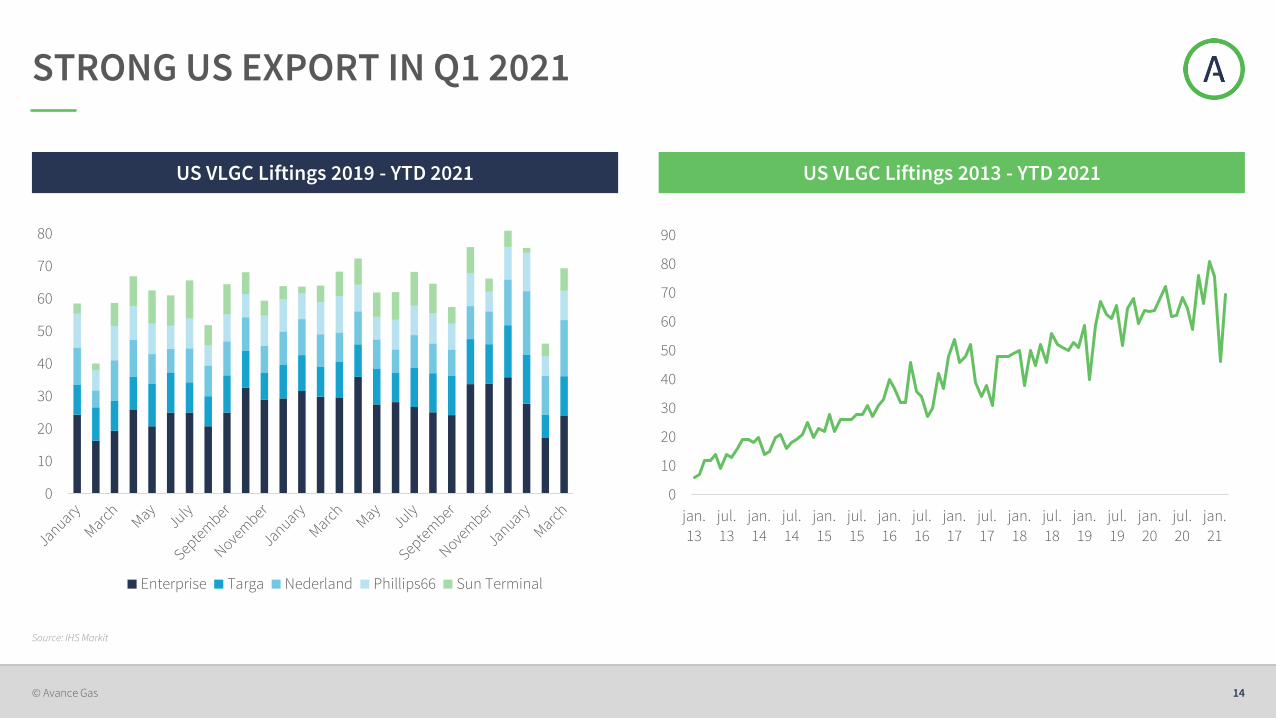

Source: IHS Markit

STRONG US EXPORT IN Q1 2021

US VLGC Liftings 2019 - YTD 2021 US VLGC Liftings 2013 - YTD 2021

0

10

20

30

40

50

60

70

80

Enterprise Targa Nederland Phillips66 Sun Terminal

0

10

20

30

40

50

60

70

80

90

jan.

13

jul.

13

jan.

14

jul.

14

jan.

15

jul.

15

jan.

16

jul.

16

jan.

17

jul.

17

jan.

18

jul.

18

jan.

19

jul.

19

jan.

20

jul.

20

jan.

21

15© Avance Gas

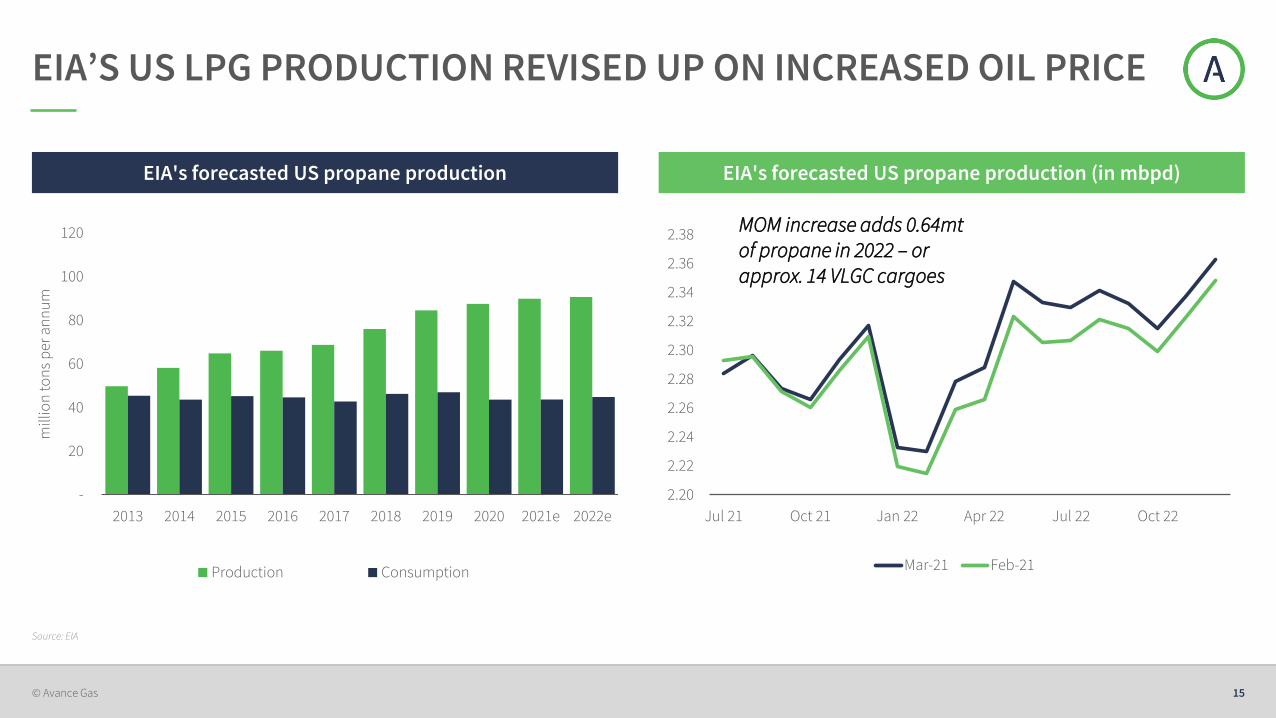

Source: EIA

EIA’S US LPG PRODUCTION REVISED UP ON INCREASED OIL PRICE

EIA's forecasted US propane production EIA's forecasted US propane production (in mbpd)

2.20

2.22

2.24

2.26

2.28

2.30

2.32

2.34

2.36

2.38

Jul 21 Oct 21 Jan 22 Apr 22 Jul 22 Oct 22

Mar-21 Feb-21

MOM increase adds 0.64mt of propane in 2022 – or approx. 14 VLGC cargoes

-

20

40

60

80

100

120

2013 2014 2015 2016 2017 2018 2019 2020 2021e 2022e

mill

ion

to

ns

per

an

nu

m

Production Consumption

16© Avance Gas

Source: IHS Markit

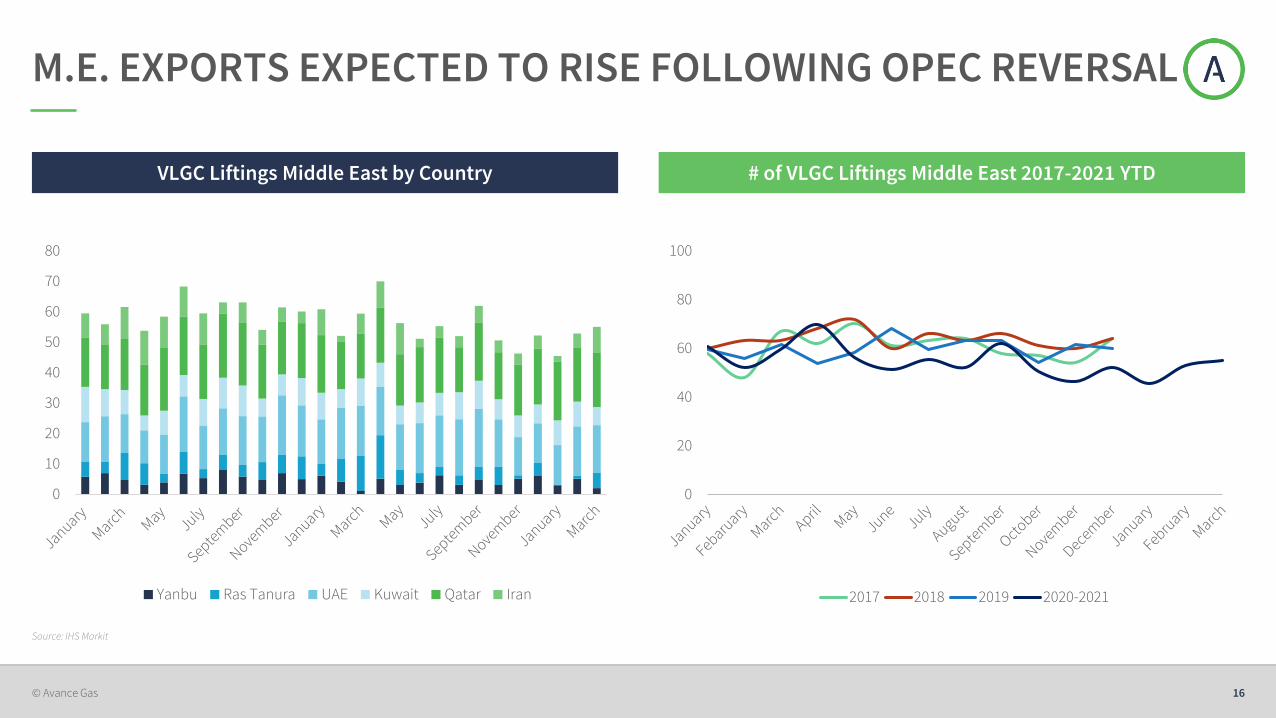

M.E. EXPORTS EXPECTED TO RISE FOLLOWING OPEC REVERSAL

VLGC Liftings Middle East by Country # of VLGC Liftings Middle East 2017-2021 YTD

0

10

20

30

40

50

60

70

80

Yanbu Ras Tanura UAE Kuwait Qatar Iran

0

20

40

60

80

100

2017 2018 2019 2020-2021

17© Avance Gas

GROWTH IN ASIAN LPG DEMAND EXPECTED TO CONTINUE

Source: Fearnleys, IHS Markit

VLGC Imports China VLGC Imports India ~80% of global demand in Asia

~70% of Asian demand is non industrial

India and Indonesia imports up by 15-20% year-on-year

Cooking / heating – residentialPDH and industrial

2mmts + new PDH demand

-

5

10

15

20

2015 2016 2017 2018 2019 2020

Mill

to

ns

-

5

10

15

20

2015 2016 2017 2018 2019 2020

Mill

to

ns

18© Avance Gas

Source: Clarksons SIN

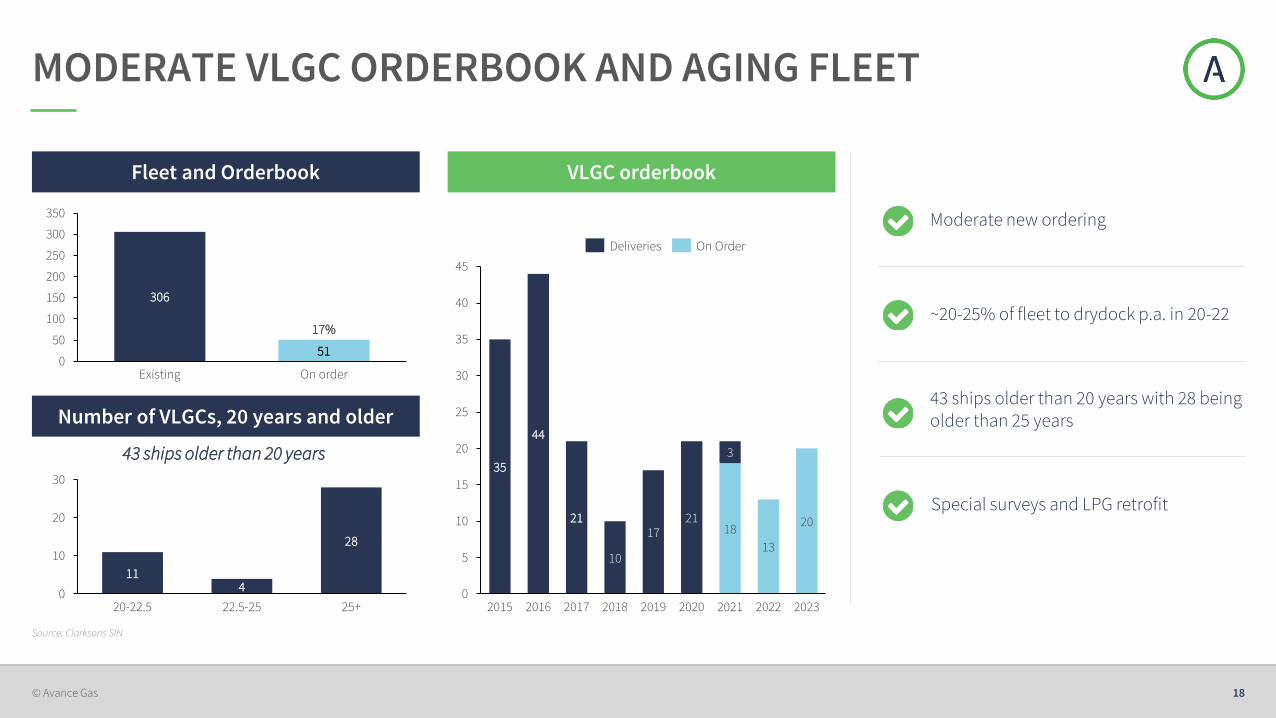

MODERATE VLGC ORDERBOOK AND AGING FLEET

Fleet and Orderbook VLGC orderbook

Number of VLGCs, 20 years and older

Moderate new ordering

~20-25% of fleet to drydock p.a. in 20-22

43 ships older than 20 years with 28 being older than 25 years

Special surveys and LPG retrofit

306

510

50

100

150

200

250

300

350

Existing On order

17%

114

28

0

10

20

30

22.5-2520-22.5 25+

35

44

21

10

1721

18

13

20

3

0

5

10

15

20

25

30

35

40

45

202120202015 2016 20192017 2018 2022 2023

Deliveries On Order

43 ships older than 20 years

COMPANY UPDATE

20© Avance Gas

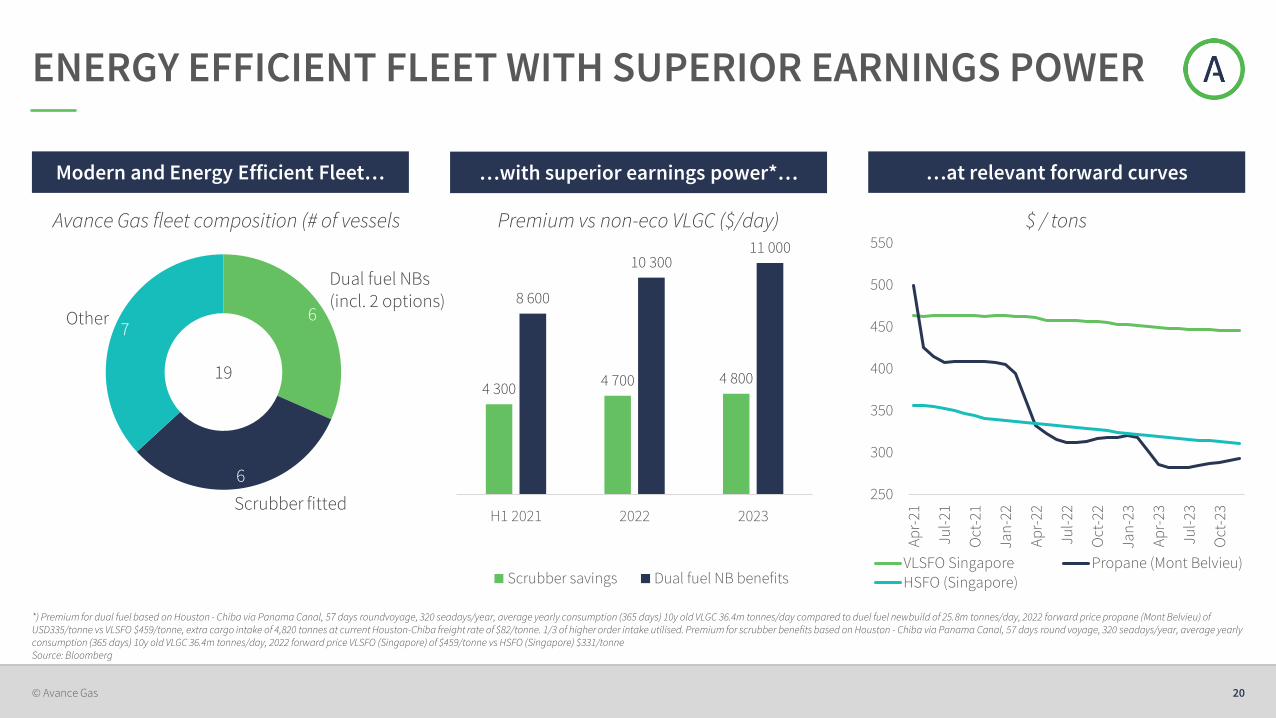

ENERGY EFFICIENT FLEET WITH SUPERIOR EARNINGS POWER

Modern and Energy Efficient Fleet… …with superior earnings power*… …at relevant forward curves

6Other

Dual fuel NBs (incl. 2 options)

6

Scrubber fitted

7

19

Premium vs non-eco VLGC ($/day)

*) Premium for dual fuel based on Houston - Chiba via Panama Canal, 57 days roundvoyage, 320 seadays/year, average yearly consumption (365 days) 10y old VLGC 36.4m tonnes/day compared to duel fuel newbuild of 25.8m tonnes/day, 2022 forward price propane (Mont Belvieu) of USD335/tonne vs VLSFO $459/tonne, extra cargo intake of 4,820 tonnes at current Houston-Chiba freight rate of $82/tonne. 1/3 of higher order intake utilised. Premium for scrubber benefits based on Houston - Chiba via Panama Canal, 57 days round voyage, 320 seadays/year, average yearly consumption (365 days) 10y old VLGC 36.4m tonnes/day, 2022 forward price VLSFO (Singapore) of $459/tonne vs HSFO (Singapore) $331/tonne Source: Bloomberg

250

300

350

400

450

500

550

Ap

r-21

Jul-

21

Oct

-21

Jan

-22

Ap

r-22

Jul-

22

Oct

-22

Jan

-23

Ap

r-23

Jul-

23

Oct

-23

VLSFO Singapore Propane (Mont Belvieu)HSFO (Singapore)

4 3004 700 4 800

8 600

10 30011 000

H1 2021 2022 2023

Scrubber savings Dual fuel NB benefits

Avance Gas fleet composition (# of vessels $ / tons

21© Avance Gas

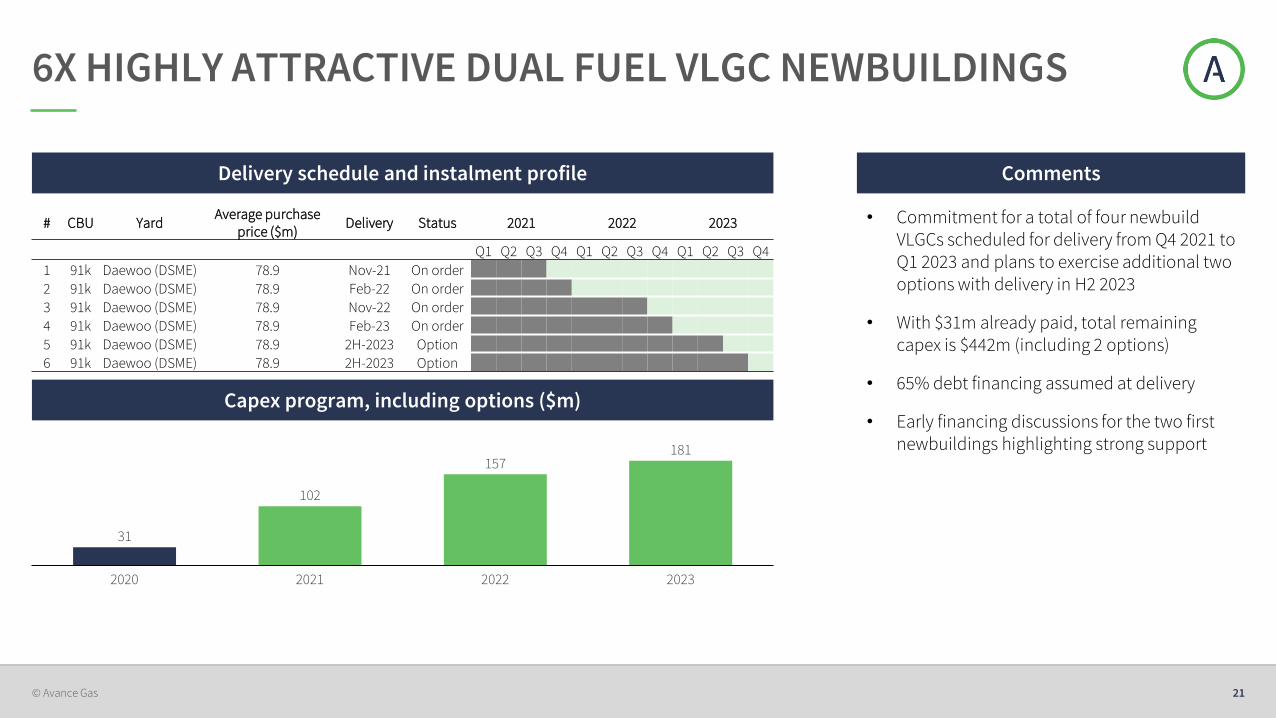

6X HIGHLY ATTRACTIVE DUAL FUEL VLGC NEWBUILDINGS

Delivery schedule and instalment profile Comments

• Commitment for a total of four newbuild VLGCs scheduled for delivery from Q4 2021 to Q1 2023 and plans to exercise additional two options with delivery in H2 2023

• With $31m already paid, total remaining capex is $442m (including 2 options)

• 65% debt financing assumed at delivery

• Early financing discussions for the two first newbuildings highlighting strong support

Capex program, including options ($m)

31

102

157181

2020 20222021 2023

# CBU YardAverage purchase

price ($m)Delivery Status 2021 2022 2023

Q1 Q2 Q3 Q4 Q1 Q2 Q3 Q4 Q1 Q2 Q3 Q4

1 91k Daewoo (DSME) 78.9 Nov-21 On order 1 1 1 2 2 2 2 2 2 2 2 2

2 91k Daewoo (DSME) 78.9 Feb-22 On order 1 1 1 1 2 2 2 2 2 2 2 2

3 91k Daewoo (DSME) 78.9 Nov-22 On order 1 1 1 1 1 1 1 2 2 2 2 2

4 91k Daewoo (DSME) 78.9 Feb-23 On order 1 1 1 1 1 1 1 1 2 2 2 2

5 91k Daewoo (DSME) 78.9 2H-2023 Option 1 1 1 1 1 1 1 1 1 1 2 2

6 91k Daewoo (DSME) 78.9 2H-2023 Option 1 1 1 1 1 1 1 1 1 1 1 2

22© Avance Gas

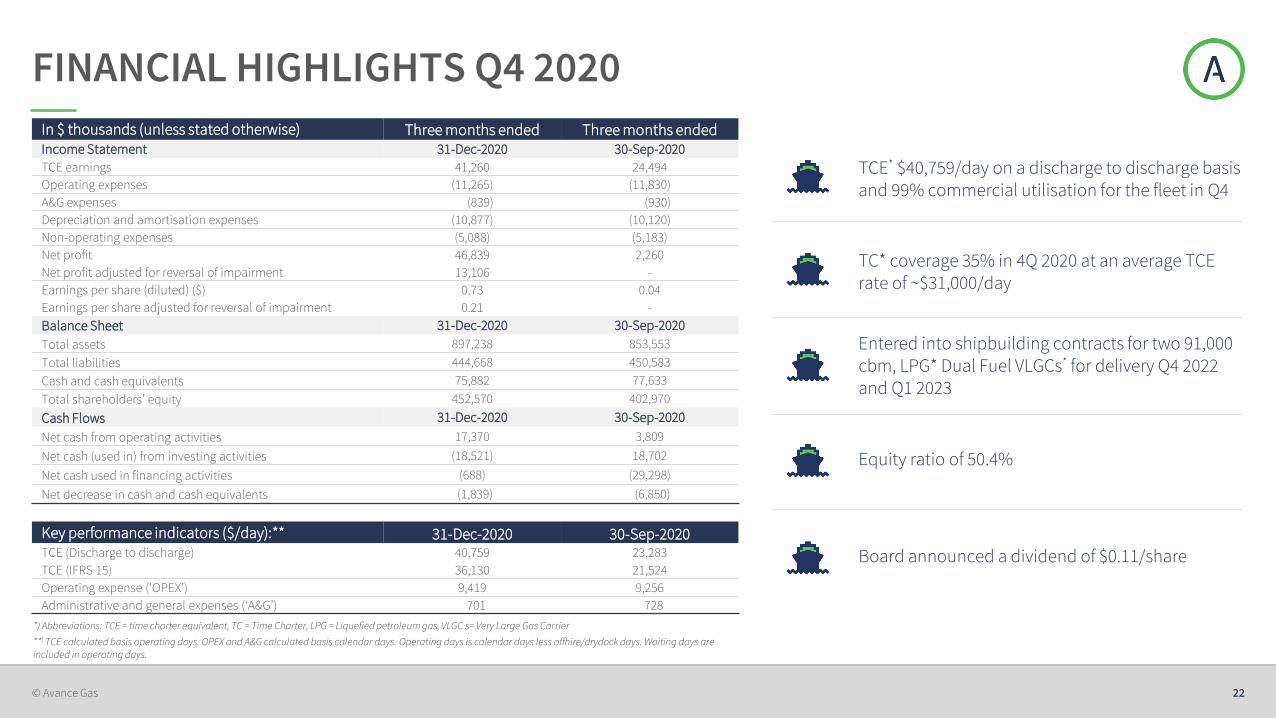

FINANCIAL HIGHLIGHTS Q4 2020In $ thousands (unless stated otherwise) Three months ended Three months endedIncome Statement 31-Dec-2020 30-Sep-2020

TCE earnings 41,260 24,494

Operating expenses (11,265) (11,830)

A&G expenses (839) (930)

Depreciation and amortisation expenses (10,877) (10,120)

Non-operating expenses (5,088) (5,183)

Net profit 46,839 2,260

Net profit adjusted for reversal of impairment 13,106 -

Earnings per share (diluted) ($) 0.73 0.04

Earnings per share adjusted for reversal of impairment 0.21 -

Balance Sheet 31-Dec-2020 30-Sep-2020

Total assets 897,238 853,553

Total liabilities 444,668 450,583

Cash and cash equivalents 75,882 77,633

Total shareholders’ equity 452,570 402,970

Cash Flows 31-Dec-2020 30-Sep-2020

Net cash from operating activities 17,370 3,809

Net cash (used in) from investing activities (18,521) 18,702

Net cash used in financing activities (688) (29,298)

Net decrease in cash and cash equivalents (1,839) (6,850)

Key performance indicators ($/day):** 31-Dec-2020 30-Sep-2020TCE (Discharge to discharge) 40,759 23,283

TCE (IFRS 15) 36,130 21,524

Operating expense (‘OPEX’) 9,419 9,256

Administrative and general expenses (‘A&G’) 701 728

TC* coverage 35% in 4Q 2020 at an average TCE rate of ~$31,000/day

Entered into shipbuilding contracts for two 91,000 cbm, LPG* Dual Fuel VLGCs* for delivery Q4 2022 and Q1 2023

TCE* $40,759/day on a discharge to discharge basis and 99% commercial utilisation for the fleet in Q4

Board announced a dividend of $0.11/share

**) TCE calculated basis operating days. OPEX and A&G calculated basis calendar days. Operating days is calendar days less offhire/drydock days. Waiting days are included in operating days.

Equity ratio of 50.4%

*) Abbreviations: TCE = time charter equivalent, TC = Time Charter, LPG = Liquefied petroleum gas, VLGC s= Very Large Gas Carrier

23© Avance Gas

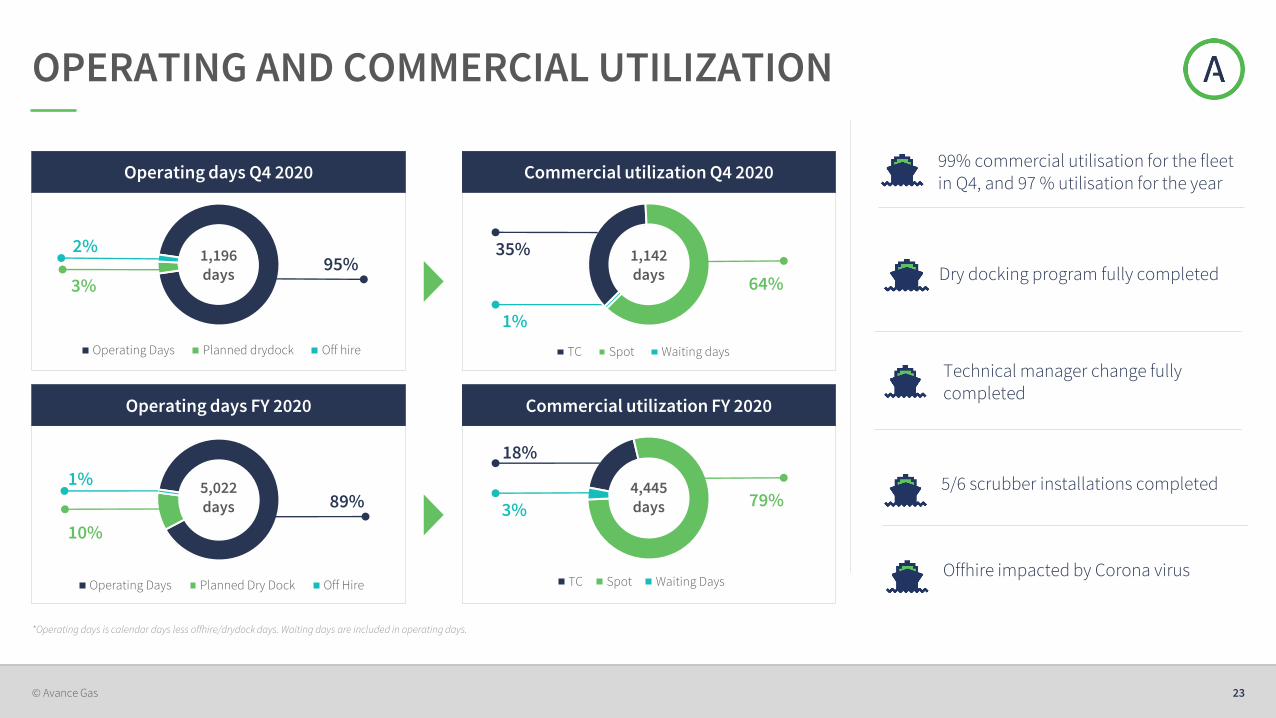

1%

Operating Days Planned Dry Dock Off Hire

10%

OPERATING AND COMMERCIAL UTILIZATION

99% commercial utilisation for the fleet in Q4, and 97 % utilisation for the year

Operating Days Planned drydock Off hire

1,196days

TC Spot Waiting days

1,142days

5,022days

TC Spot Waiting Days

4,445days

95%2%

3% 64%

35%

79%3%

18%

89%1%

*Operating days is calendar days less offhire/drydock days. Waiting days are included in operating days.

Operating days Q4 2020 Commercial utilization Q4 2020

Operating days FY 2020 Commercial utilization FY 2020

Dry docking program fully completed

5/6 scrubber installations completed

Technical manager change fully completed

Offhire impacted by Corona virus

24© Avance Gas

FY 2021 – ESTIMATED CBE AND OUTLOOK

Estimated CBE* ($/day) FY ** 2021

OPEX A&G Interest Paid Installments

$22,000per day

$4,000

$9,300$7,800

$900

Outlook – 2021

*) CBE = Cash break-even‘**) FY = Financial year

TC coverage of 25% at an average rate of $30,000/day

No schedule dry dockings – fully tradeable fleet

Strong long term fundamentals and significant free cash flow generation potential

Enhancing the green profile of the Avance Gas fleet while increasing its competitiveness with adding six dual fuel VLGCs to the fleet

25© Avance Gas

Avance Gas has set up an ESG reporting framework, including climate accounting, based on internationally recognized standards and methodologies

Avance Gas Shipping industry and emissions

ESG reporting

Three UN Sustainable Development Goals

ESG REPORTING

RISK FACTORS

27© Avance Gas

RISK FACTORS (I/XI)

An investment in the Offer Shares involves inherent risk. Before making an investment decision, investors should carefully consider the risk factors and all information contained in this Presentation. The risks and uncertainties described below are the principal known risks anduncertainties faced by the Group as of the date hereof that the Company believes are the material risks relevant to an investment in the Offer Shares. An investment in the Offer Shares is suitable only for investors who understand the risks associated with this type of investment and whocan afford to lose all or part of their investment. The absence of negative past experience associated with a given risk factor does not mean that the risks and uncertainties described herein should not be considered prior to making an investment decision in respect of the Offer Shares. Ifany of the following risks were to materialise, individually or together with other circumstances, they could have a material adverse effect on the Group and/or its business, results of operations, cash flows, financial condition and/or prospects, which may cause a decline in the value andtrading price of the Offer Shares, resulting in the loss of all or part of an investment in the same.

The order in which the risks are presented does not reflect the likelihood of their occurrence or the magnitude of their potential impact on the Group's business, results of operations, cash flows, financial condition and/or prospects. The risks mentioned herein could materialiseindividually or cumulatively. This information is as of the date of this Presentation.

1. Risks related to the industry in which the Group operates

The Group's business, financial condition and results of operations depend on the level of activity in the LPG industry

The Group's financial performance depends on the continued growth in global and regional shipments of liquefied petroleum gas ("LPG"). The level of activity in the LPG industry is affected by a number of factors, including, but not limited to the following factors:

• Worldwide demand for and production of LPG;

• Increase in the cost of LPG relative to the cost of naphtha and other competing feedstocks;

• The availability of additional sources of LPG closer to the areas of LPG consumption (reduction in tonne-miles);

• The availability of alternative energy sources;

• Expectations regarding future energy prices;

• Government laws and regulations, including environmental protection laws and regulations;

• Weather conditions;

• Political and military conflicts;

• Negative global or regional economic or political conditions, particularly in LPG consuming regions, which could reduce energy consumption or growth in energy consumption; and

• Technological changes that could make other sources of energy more competitive than LPG.

If the demand for LPG products and LPG shipping does not grow, or decreases, the Group's business, cash flows, financial condition, results of operations and/or prospects could be materially and adversely affected.

A worsening in global economic conditions could materially and adversely affect the Group's business, financial condition and results of operations

Demand for LPG products fluctuates with changes in global economic activity, which in turn affects demand for LPG ships. Slowdowns in global economic activity, such as the ongoing Covid-19 pandemic, and particularly in LPG consuming regions, may materially and adversely impactthe LPG industry, including, among other things:

28© Avance Gas

RISK FACTORS (II/XI)

• Reducing the demand for LPG products and LPG shipping and hence charter rates or the availability of new charters for ships;

• Decreasing the market values of ships;

• Reducing the availability of financing for ships; and

• Reducing the liquidity in an already slow second-hand market for the sale of ships.

Any of the above events could materially and adversely affect the Group's business, cash flows, financial condition, results of operations and/or prospects.

The state of the global financial markets may materially and adversely impact the Group's ability to obtain financing

A worsening in the credit markets may have a material adverse effect on the Group's ability to obtain additional financing on favourable terms or at all, and could have a material adverse effect on the Group's business, cash flows, financial condition, results of operations and/orprospects, and may also negatively impact the Group's operations by affecting the solvency of its suppliers and/or customers, which could lead to disruptions in the delivery of supplies, cost increases for supplies, accelerated payments to suppliers, customer bad debts or reducedrevenues.

A large increase in the number of VLGCs on order could lead to an increase in the global VLGC fleet, which may lead to a reduction in LPG freight rates and have a material adverse impact on the Group's business, financial condition and results of operations

If the number of LPG ships delivered exceeds the number of ships being recycled, the global ship capacity will increase. If the demand for ships does not increase correspondingly with the future increase in the number of ships, freight rates and ship utilisation could materially decline.Lower utilisation and freight rates due to an over-supply of LPG ships could have a material adverse effect on the Group's business, cash flows, financial condition, results of operations and/or prospects. Prolonged periods of low utilisation and charter hire, which the LPG market hasexperienced in the past, could also have a material adverse effect on the value of the Group's ships.

Competition within the LPG shipping industry could have a material adverse effect on the Group's ability to market its services

The Group's ships are employed in a highly competitive market that is capital intensive and fragmented. Competition for charters is intense, and at times the Group may potentially compete against other ship owners who have greater resources than the Group. Competition for LPGshipping depends on price, location, size, age, condition and the acceptability of the ship and its operators to prospective charterers. Due in part to the fragmented nature of the market, competitors with greater resources could enter and operate larger fleets that may be able to offerlower charter rates and higher quality ships than the Group is able to offer. The Group's operations may be materially and adversely affected if its current competitors or new market entrants introduce new offerings with better features, performance, prices or other characteristics thanthe Group can offer.

Increases in bunker fuel prices and other operating costs may significantly increase the Group's operating costs

In accordance with industry practice, the Group is responsible for voyage expenses, including bunker fuel costs, when operating its LPG ships. Increases in the cost of bunker fuel are subject to a number of economic, natural and political factors affecting the level of crude oil prices inglobal markets that are beyond the Group's control, including worldwide demand and supply imbalances, political instability and natural disasters in oil-producing regions. An increase in the cost of bunker fuel could significantly increase operating costs for the Group's ships, whichcould have a material adverse effect on the Group's results of operation to the extent that it is not able to increase its freight rates to recover bunker fuel cost increases from its customers. Other operating expenses, such as for example crew costs, may also fluctuate and affect the Group'sprofitability.

Charter rates may fluctuate substantially and if rates stay low for a prolonged period, the Group's revenues and cash flows may be adversely affected

The Group operates its ships predominantly in the spot market where charter rates and cargo availability fluctuates significantly and where seasonality can adversely impact the Groups earnings from time to time. Being dependent on the spot market may leave the Group particularlyvulnerable to short or long term swings in the freight market.

The spot charter market may fluctuate significantly based upon LPG supply and demand. In addition, VLGC spot rates are highly seasonal. The successful operation of the Group's ships in the competitive and highly volatile spot market depends on, among other things, obtainingprofitable spot charters, which depends greatly on ship supply and demand, and minimising, to the extent possible, time spent waiting for charters and time spent travelling unloaded to pick up cargo.

If charter rates are low when the Group is seeking a new charter, it may only be able to enter into new charters at unprofitable rates. Prolonged periods of low charter hire rates or low ship utilisation could also have a material adverse effect on the value of the Group's ships.

29© Avance Gas

RISK FACTORS (III/XI)

The Group may not be able to obtain supplies and services when needed, at an acceptable cost, or at all

The Group relies, and will in the future rely, on a significant supply of consumables, spare parts and equipment to operate, maintain, repair and upgrade its fleet of ships. Cost increases, delays or unavailability could negatively impact the Group's operations and result in down-time dueto delays in the repair and maintenance of the Group's ships.

The Group's operations may be affected by political, governmental and economic instability which may adversely affect the Group's business

The Group's operations may be affected by political, governmental and economic conditions, such as trade wars, in countries where the Group engage in business. Any disruption caused by these factors could adversely affect the Group's business, including by reducing the levels of oiland gas exploration, development and production activities in these areas. In addition, political instability, trade wars, terrorist or other attacks, war or international hostilities may contribute to further world economic instability and uncertainty in global financial markets, which mayadversely affect the LPG industry and the Group's business. In particular, terrorist attacks, or the perception that LPG facilities and carriers are potential terrorist targets, could materially and adversely affect expansion of LPG infrastructure and LPG shipping.

2. Risks related to the Group

The Group may not be able to successfully implement its strategies

The Group's strategy is to contribute to consolidation of the VLGC industry; grow the fleet; have a chartering strategy focused on spot market exposure; and maintain a strong balance sheet with attractive financing terms. Maintaining and expanding the Group's operations and achievingits other objectives involve inherent costs and uncertainties and there is no assurance that the Group will achieve its objectives or other anticipated benefits. Further, there is no assurance that the Group will be able to undertake the contemplated activities within its expected time frame,that the cost of any of the Group's objectives will be at expected levels or that the benefits of its objectives will be achieved within the expected timeframe or at all. The Group's strategy may also be affected by factors beyond its control, such as the speed of the economic recovery in itsmarket and the availability of acquisition opportunities in the market. Any failures, material delays or unexpected costs related to implementation of the Group's strategies, including the amount already invested, could have a material adverse effect on its business, financial condition,results of operations, cash flows and/or prospects.

Due to the Group's undiversified exposure towards the LPG market, adverse developments in the LPG shipping industry would have a significantly greater impact on the Group's financial condition, results of operations and cash flows than if the Group maintained a more diverse fleet ofships

The Group relies exclusively on the cash flow generated from spot trades and charters for its LPG ships. Due to the Group's lack of diversification, an adverse development in the LPG shipping industry would have a significantly greater impact on the Group's business, financial condition,results of operations, cash flows and/or prospects than if the Group maintained a more diverse fleet of ships.

The Group's earnings and business are subject to risk caused by counterparties in contracts, including credit risk, and failure and misrepresentation of such counterparties causing them not to meet their obligations could cause loss to the Group or otherwise materially and adverselyaffect the business of the Group

The ability of each counterparty to perform its obligations under a contract with the Group will depend on a number of factors that are beyond the Group's control and may include, among other things:

• General economic conditions;

• The condition of the maritime and other industries to which the counterparty is exposed;

• The overall financial condition of the counterparty;

• Charter rates received for specific types of ships; and

• Various expenses.

The Group's ships may from time to time be chartered out on time charters. In depressed market conditions, charterers may no longer need a ship that is currently under time charter or may be able to obtain a comparable ship at lower rates. As a result, charterers may seek to re-negotiate the terms of their existing time charters or avoid their obligations under those contracts. Future contracts could permit a customer to terminate its contract early subject to the payment of a termination fee. Such fee may not fully compensate for the loss sustained by the Group.Should a counterparty fail to honour its obligations under its agreements with the Group, the Group could sustain significant losses, which could have a material adverse effect on the Group's business, financial condition, results of operations, cash flows and/or prospects. Further, theGroup's shipping services are subject to the risks associated with having limited customers for its services.

30© Avance Gas

RISK FACTORS (IV/XI)

The market value of the Group's current ships and those it acquires in the future may decrease, which could, among other things, cause the Group to be in non-compliance with its loan covenants or to incur losses if it decides to sell them following a decline in their market values

The market value of ships are both cyclical and volatile, and may fluctuate due to a number of different factors, including, but not limited to:

• General economic and market conditions affecting the LPG shipping industry, including competition from other shipping companies;

• Availability of credit and other forms of financial liquidity;

• Charterers' preferences with respect to ship design, types, sizes and ages of available ships;

• The availability of other modes of transportation;

• Increases in the supply of ship capacity;

• Prevailing charter and freight rates;

• The cost of LPG newbuildings;

• Changes to governmental, laws and regulations, including environmental protection laws and regulations and or class rules; and

• The need to upgrade ships as a result of charterer requirements, technological advances in ship design or equipment or otherwise, such as IMO 2020.

A decline in the fair market values of the Group's ships could result in the Group not being in compliance with its loan covenants.

The Group's credit facilities include covenants pursuant to which the minimum fair market value of the Group's existing fleet financed under its credit facilities shall at all times cover at least 130% of the outstanding facility amounts, in addition to a covenant under a sale leasebackagreement entered into in December 2020 pursuant to which the minimum fair market value of the vessel shall at all times cover at least 115% of the outstanding amount. Consequently, a decline in the market value of the Group's ships financed under the credit facilities may lead to abreach of such covenants, which again may lead to the Group being required to provide cash or other security to the lenders or reduce the outstanding and available amount under the facilities to restore the ratio to its required level, or to sell ships, or the lenders may accelerate the loansunder the facilities. As a result, the Group's business, financial condition, results of operations, cash flow and/or prospects could be materially and adversely affected.

In addition, a decline in the fair market values of the Group's ships may result in impairment adjustments in the Group's financial statements, which would adversely affect its financial results, and if for any reason the Group find it necessary to sell any of its ships at a time when prices aredepressed, the Group could incur a significant loss.

The Group may not be able to keep pace with technological developments in the LPG shipping market

Future technological developments for LPG ships may result in substantial improvements in ships equipment functions and performance. As a result, the Group's future success and profitability may be dependent in part upon its ability to:

• Maintain existing ships and related equipment and services;

• Cost effectively address the increasingly sophisticated needs of its customers; and

• Anticipate changes in technology and industry standards and respond to technological developments on a timely basis.

If the Group is not successful in timely responding to technological developments or changes in industry standards, on a cost-effective basis, this could have a material adverse effect on the Group's business and/or prospects.

31© Avance Gas

RISK FACTORS (V/XI)

3. Risks related to the Group's operations

The Group's operating and maintenance costs may not necessarily fluctuate in proportion to changes in operating revenues

The Group's operating and maintenance costs will not necessarily fluctuate in proportion to changes in operating revenues. Operating revenues may fluctuate as a function of changes in supply and demand for LPG shipping services, which in turn affect charter rates. In addition,equipment maintenance costs fluctuate depending upon the type of activity the ship is performing and the age and condition of the equipment. In a situation where a ship faces longer idle periods, reductions in costs may not be immediate as some of the crew may be required toprepare ships for stacking and maintenance in the stacking period. Should ships be idle for a longer period, the Group may seek to redeploy crew members, who are not required to maintain the ships, to active units to the extent possible. However, there can be no assurance that theGroup will be successful in reducing its costs.

The Group's business involves numerous operating hazards and the Group's own insurance may not be adequate to cover the Group's losses

The operations of the Group's ships are subject to hazards inherent in the industry where it operates, service down time on its ships, equipment defects, fires, explosions and pollution. These hazards can cause personal injury or loss of life, severe damage to or destruction of property andequipment, pollution or environmental damage, claims by employees, third parties or customers and suspension of operations. The operation of the Group's ships is also subject to hazards inherent in marine operations, such as capsizing, sinking, grounding, collision, damage fromsevere weather and marine life infestations. Operations may also be suspended because of machinery breakdowns, acts of piracy, abnormal conditions, and failure of subcontractors to perform or supply goods or services, or personnel shortages.

Damage to the environment could also result from the Group's operations, particularly through spillage of fuel, lubricants or other chemicals and substances used in operations, or extensive uncontrolled fires. Although the Group carries protection and indemnity insurance, all risks maynot be adequately insured against, and any particular claim may not be paid. Any claims covered by insurance would be subject to deductibles, and since it is possible that a large number of claims may be brought, the aggregate amount of these deductibles could be material.

The Group may be unable to procure adequate insurance coverage at commercially reasonable rates in the future. For example, more stringent environmental regulations have led in the past to increased costs for, and in the future may result in the lack of availability of, insuranceagainst risks of environmental damage or pollution. Any uninsured or underinsured loss could harm the Group's business, financial condition and operating results. In addition, the Group's insurance may be voidable by the insurers as a result of certain of the Group's actions, such as theGroup's ships failing to maintain certification with applicable maritime self-regulatory organisations.

The Group's insurance coverage will not in all situations provide sufficient funds to protect the Group from all liabilities and losses that could result from its operations. The amount of the Group's insurance cover may be less than the related impact on enterprise value after a loss. TheGroup's coverage includes policy limits. As a result, the Group retains the risk for any losses in excess of these limits. Any such lack of reimbursement may cause the Group to incur substantial losses and costs. In addition, the Group could decide to retain substantially more risk in thefuture. Moreover, no assurance can be made that the Group has, or will maintain in the future, adequate insurance against certain risks.

If a significant accident or other event occurs and is not fully covered by the Group's insurance or any enforceable or recoverable indemnity from, or claim against, a third party, it could adversely affect the Group's business, financial position, results of operations, cash flows and/orprospects.

The Group's ships are exposed to technical risk and down-time or off-hire

In respect of both the ships operating in the spot market and the ships from time to time chartered out under time charter arrangements, the Group carries the costs and risks of operational and technical problems. In respect of ships operating in the spot market, ship down-time couldincrease the Group's costs and will reduce its earnings. In respect of ships chartered out under time charter arrangements, ship down-time may result in increased costs, as well as off-hire (i.e. non-payment of daily charter hire under the time charter). Any ship down-time or off-hire couldadversely affect the Group's business, financial condition, results of operations, cash flows and/or prospects.

Failure to secure future employment for the Group's ships could have a material adverse effect on the Group's results of operation, cash flow and financial condition

No assurance can be given as to whether future employment for the Group's ships can be secured on terms, rates and with charterers, which are acceptable. Failure to secure future employment for the Group's ships could have a material adverse effect on the Group's business, results ofoperation, cash flows, financial condition and/or prospects.

32© Avance Gas

RISK FACTORS (VI/XI)

The required maintenance and dry-docking of the Group's ships could be more expensive and time consuming than originally anticipated

Maintenance and dry-dockings of the Group's ships require significant capital expenditures and result in loss of revenue while such ships are out of service. Any significant increase in either the number of days ships are out of service due to such maintenance or dry-dockings or in the costsof any repairs carried out could have a material adverse effect on the Group's profitability and cash flows. The Group may not be able to precisely predict the time required to maintain or dry-dock any of its ships and unanticipated problems may arise. General increases in demand fordry-docking services in the shipping industry could result in increased costs, delays or unavailability related to dry-docking for the Group's ships. If a ship is dry-docked longer than expected or if the cost of repairs or maintenance is greater than budgeted, the Group's results of operations,financial condition and cash flows could be materially and adversely affected. Generally, ships dry-dock every five years. Avance Gas has during the course of 2020 drydocked eight ships, as scheduled.

Failure to obtain or retain highly skilled personnel could have a material adverse effect on the Group's operations

The successful development and performance of the Group's business depends on the Group's ability to attract and retain skilled professionals with appropriate experience and expertise. Any loss of the services of any of the senior management or key personnel could have a materialadverse effect on the Group's business and operations. Obtaining charters with leading industry participants depends on a number of factors, including the ability to man ships with suitably experienced, high-quality masters, officers and crews. In recent years, the limited supply of andincreased demand for well-qualified crew has created upward pressure on crewing costs, which the Group bears both in respect of its ships operating in the spot market and its ships that from time to time are chartered out under time charters. Increases in crew costs may adverselyaffect the Group's profitability. In addition, if the Group cannot retain sufficient numbers of quality on-board seafaring personnel, the Group's fleet utilisation will decrease, which could have a material adverse effect on the Group's business, financial condition, results of operations, cashflows and/or prospects.

The Group may face labour disruptions that could interfere with its operations and have a material adverse effect on the Group's business, financial condition, result of operations, cash flows and/or prospects

If not resolved in a timely and cost-effective manner, industrial action or other labour unrest could prevent or hinder the Group's operations from being carried out normally and could have a material adverse effect on the Group's business, financial condition, results of operations, cashflows and/or prospects.

The Group uses information technology systems to communicate with its ships and conduct its business, and disruption, failure or security breaches of these systems could materially and adversely affect its business and results of operations

The Group uses information technology ("IT") systems in order to communicate with its ships and achieve its business objectives. The Group uses industry accepted security measures and technology such as access control systems to securely maintain confidential and proprietaryinformation maintained on its IT systems, and market standard virus control systems. However, the Group's portfolio of hardware and software products, solutions and services and its enterprise IT systems may be vulnerable to damage or disruption caused by circumstances beyond itscontrol, such as catastrophic events, power outages, natural disasters, computer system or network failures, computer viruses, cyber-attacks or other malicious software programmes. The failure or disruption of the Group's IT systems to perform as anticipated for any reason coulddisrupt the Group's business and result in decreased performance, significant remediation costs, transaction errors, loss of data, processing inefficiencies, down-time, litigation, and the loss of suppliers or customers. A significant disruption or failure could have a material adverse effecton the Group's business and results of operations.

The ageing of the Group's fleet may result in increased operating costs in the future and a less competitive fleet

In general, the cost of maintaining a ship in good operating condition increases with the age of the ship. As the Group's fleet ages, the Group will incur increased costs. Older ships are typically less fuel efficient and more costly to maintain than more recently constructed ships due togradual improvements in engine technology and other design features. Cargo insurance rates increase with the age of a ship, making older ships less desirable to spot customers and charterers. Governmental regulations and safety or other equipment standards related to the age ofships may also require expenditures for alterations or the addition of new equipment to the Group's ships and may restrict the type of activities in which the Group's ships may engage. The Group cannot assure that, as the Group ships age, market conditions will justify those expendituresor enable the Group to operate its ships profitably during the remainder of their useful lives.

Avance Gas is a holding company and is dependent upon cash flow from subsidiaries to meet its obligations

The Group currently conducts its operations through, and most of the Group's assets are owned by, Avance Gas' subsidiaries. As such, the cash that the Group obtains from its subsidiaries is the principal source of funds necessary to meet its obligations. Contractual provisions or laws, aswell as the Group's subsidiaries' financial condition, operating requirements, restrictive covenants in its debt arrangements and debt requirements, may limit the Group's ability to obtain cash from subsidiaries that it requires to pay its expenses or meet its current or future debt serviceobligations.

The inability to transfer cash from the Group's subsidiaries may mean that the Group may not be permitted to make the necessary transfers from its subsidiaries to meet its obligations. A payment default by the Group, or any of the Group's subsidiaries, on any debt instrument would havea material adverse effect on the Group's business, financial condition, results of operations, cash flows and/or prospects.

33© Avance Gas

RISK FACTORS (VII/XI)

The Group's financial condition may be materially and adversely affected if the Group fails to successfully integrate acquired assets or businesses, or is unable to obtain financing for acquisitions on acceptable terms

The Group believes that acquisition opportunities may arise from time to time, and that any such acquisition could be significant. At any given time, discussions with one or more potential sellers may be at different stages. However, any such discussions may not result in theconsummation of an acquisition transaction, and the Group may not be able to identify or complete any acquisitions or make assurances that any acquisitions the Group makes will perform as expected or that the returns from such acquisitions will support the investment required toacquire or develop them. The Group cannot predict the effect, if any, that any announcement or consummation of an acquisition would have on the trading price of the Shares.

Any future acquisitions could present a number of risks, including:

• The risk of using management time and resources to pursue acquisitions that are not successfully completed;

• The risk of failing to identify material problems during due diligence;

• The risk of over-paying for assets;

• The risk of failing to arrange financing for an acquisition as may be required or desired;

• The risk of incorrect assumptions regarding the future results of acquired operations;

• The risk of failing to integrate the operations or management of any acquired operations or assets successfully and timely; and

• The risk of diversion of management's attention from existing operations or other priorities.

In addition, the integration and consolidation of acquisitions requires substantial human, financial and other resources, including management time and attention, and may depend on the Group's ability to retain the acquired business' existing management and employees or recruitacceptable replacements. Ultimately, if the Group is unsuccessful in integrating any acquisitions in a timely and cost-effective manner, the Group's business, financial condition, results of operations, cash flows and/or prospects could be materially and adversely affected.

Seasonal fluctuations could have a material adverse effect on the Group's business, financial condition, results of operations and cash flows

The export volumes coming out of the Middle East LPG market, which has historically been the Group's primary market, have traditionally been lower during the late fourth and the beginning of the first calendar quarters than at other times of the year. This is mainly because of lowerproduction in combination with somewhat higher local demand. Due to US Gulf increasing its share in global exports, the last years have seen lower exports in the second and third quarters, and hence the historical seasonal patterns have become less clear.

4. Risks related to laws, regulations and litigation

The Group may be subject to litigation and disputes that could have a material adverse effect on the Group's business, financial condition, results of operations and cash flows

The Group may in the future be involved from time to time in litigation and disputes. The operating hazards inherent in the Group's business may expose the Group to, amongst other things, litigation, including personal injury litigation, environmental litigation, contractual litigation withcustomers, intellectual property litigation, tax or securities litigation, and maritime lawsuits including the possible arrest of the Group's ships, as well as other litigation and disputes that arises in the ordinary course of business.

The Group is currently not involved in any litigation and disputes. However, it may in the future be involved in litigation matters from time to time. Avance Gas cannot predict with certainty the outcome or effect of any claim or other litigation matter. The ultimate outcome of any litigationmatter and the potential costs associated with prosecuting or defending such lawsuits and claims, including the diversion of the management's attention to these matters, could have a material adverse effect on the Group's business, financial condition, results of operations, cash flowsand/or prospects.

Laws and regulations could hinder or delay the Group's operations, increase the Group's operating costs, reduce demand for its services and restrict its ability to operate its ships or otherwise

The Group is subject to complex laws and regulations, including environmental regulations that can adversely affect the cost, manner or feasibility of doing business. The operation of the Group's ships is subject to government oversight and regulation in the form of internationalconventions, sanctions, national, state and local laws and regulations in force in the jurisdictions in which the ships operate, as well as in the country or countries of their registration. Because such conventions, laws and regulations are often revised, the Group cannot predict the ultimatecost of complying with such conventions, laws and regulations or the impact thereof on the re-sale prices or useful lives of the Group's ships. The Group may also incur additional costs in order to comply with other existing and future regulatory obligations, including, but not limited to,costs relating to: air emissions, including greenhouse gases; the management of ballast waters; maintenance and inspection; development and implementation of emergency procedures; and insurance coverage or other financial assurance of the Group's ability to address pollutionincidents. In addition, environmental or other legislation establishing additional regulation or restrictions on LPG production and transportation, including the adoption of climate change legislation or regulations, or legislation in the United States placing additional regulation orrestrictions on LPG production from shale gas could result in reduced demand for LPG shipping.

34© Avance Gas

RISK FACTORS (VIII/XI)

A change in tax laws of any country in which the Group operates from time to time, or complex tax laws associated with international operations which the Group may undertake from time to time, could increase the effective tax rate of the Group

The Group will from time to time conduct operations through various subsidiaries in countries throughout the world and the Group's ships will have voyages to and from, and will call on ports, in countries throughout the world. The Group may, for example, be exposed to tax liability incountries where its ships operate, computed on the basis of a percentage of its charter revenue and the number of days spent in that country. The Group and its shareholders may also become subject to Controlled Foreign Corporations (CFC) taxation. Tax laws and regulations are highlycomplex and subject to interpretation and change. For example, if Norwegian shareholders control a company (i.e. directly or indirectly own or control at least 50% of the shares or the capital of the company) resident in a low tax jurisdiction, such Norwegian shareholders may be subjectto Norwegian taxation according to the Norwegian Controlled Foreign Corporations regulations (Norwegian CFC-regulations). Such taxation could apply with respect to certain of the Group's subsidiaries if the Group becomes subject to the control of Norwegian shareholders. If AvanceGas' Norwegian shareholders are subject to Norwegian CFC taxation, such Norwegian shareholders are taxed in Norway on their proportionate share of the net profits generated by the relevant foreign company, calculated according to Norwegian tax regulations.

A loss of a major tax dispute or a successful tax challenge to the Group's operating structure from time to time or other disputes related to or challenges to the Group's tax payments could result in an increase in the Group's effective tax rate

From time to time the Group's tax payments may be subject to review or investigation by tax authorities of the jurisdictions in which the Group operates from time to time. If any tax authority successfully challenges the Group's operational structure, intercompany pricing policies, thetaxable presence of its subsidiaries in certain countries, or if the Group loses a material tax dispute in any country, or any tax challenge of the Group's tax payments is successful, its effective tax rate could increase substantially.

Compliance with environmental laws or requirements may have an adverse effect on the Group's results of operations

The shipping industry is affected by extensive and changing international conventions and national, state and local laws and regulations governing environmental matters in the jurisdictions in which the Group's vessels operate and such vessels are registered. Such regulatory measuresmay include, for example, the adoption of cap and trade regimes (emission trading), carbon taxes, increased efficiency standards and incentives or mandates for renewable energy. Recent and upcoming changes in regulatory requirements include, but are not limited to, (i) the IMOSulphur Cap ("IMO 2020"), which provides for a significant reduction of sulphur content of the marine fuels used by certain vessels, such as the Group's vessels, and (ii) the IMO Ballast Water Management Convention (the "BWM Convention"), which sets out limitations on the amount ofviable organisms allowed to be discharged with a vessel's ballast water, (iii) the Energy Efficiency Design Index and Energy efficiency Existing Ship Index and (iv) IMO 2030.

Compliance with changes in laws and regulations relating to climate change could increase the costs of operating and maintaining the Group's vessels and could require the Group to install new emission controls, as well as acquire allowances, affect the resale value or useful lives of thevessels, lead to increased impairment charges, require reductions in cargo capacity, ship modifications or operational changes or restrictions. Further, such changes could lead to decreased availability of insurance coverage or increased policy costs for environmental matters or result inthe denial of access to certain jurisdictional waters or ports or detention in certain ports, require taxes to be payable in relation to the Group's greenhouse gas emissions or require the Group to administer and manage a greenhouse gas emissions program. Regulation of vessels,particularly in the areas of safety and environmental impact, may change in the future and require the Group to incur significant capital expenditures and/or additional operating costs in order to keep the Group's vessels in compliance.

Increasing scrutiny and changing expectations from investors, lenders and other market participants with respect to the Group's Environmental, Social and Governance policies may impose additional costs on the Group or expose the Group to additional risks

The Company will require additional capital in the future in order to finance newbuilds, take advantage of business opportunities and due to unforeseen liabilities or net cash flow shortfalls. Increasing scrutiny and changing expectations from investors, lenders and other marketparticipants with respect to the Group's Environmental, Social and Governance policies may restrict the availability of debt finance to the Company. The resulting lack of available credit and/or higher financing costs and more onerous terms may materially impact the performance ofcertain investments with a potential adverse impact on both working capital and term debt availability and on exit options.

5. Risks related to financing and market risk

The Private Placement may not be sufficient and the Group may require additional capital in the future in order to execute its growth strategy or for other purposes, which may not be available on favourable terms, or at all

No assurance can be given that the Private Placement will be sufficient and that the Group will not require additional funds in order to execute its growth strategy, or for other purposes. The Group's business is capital intensive and, to the extent the Group does not generate sufficient cashfrom operations together with the cash proceeds from the Private Placement, the Group or its subsidiaries may need to raise additional funds through public or private debt or equity financing to fund capital expenditures. Adequate sources of funds may not be available, or available atacceptable terms and conditions, when needed or may not be available on acceptable terms. If the Group raises additional funds by issuing additional equity securities, the existing shareholders may be significantly diluted. If funding is insufficient at any time in the future, the Group maybe unable to fund maintenance requirements and acquisitions, take advantage of business opportunities or respond to competitive pressures, any of which could materially and adversely impact the Group's business, results of operations, cash flows, financial condition and/orprospects. Such development could also have a material adverse effect on the value of the Shares.

35© Avance Gas

RISK FACTORS (IX/XI)

The Group's existing or future debt arrangements could limit the Group's liquidity and flexibility in obtaining additional financing, in pursuing other business opportunities or corporate activities or Avance Gas' ability to declare dividends to its shareholders

The Group's credit facilities and bank loan contain certain covenants and event of default clauses, including cross default provisions and restrictive covenants and performance requirements, such as loan-to-fleet value requirements and change of control provisions, which may affect theoperational and financial flexibility of the Group. The satisfaction of these restrictive covenants and performance requirements may be outside of the Group's control. Such restrictions could affect, and in many respects limit or prohibit, among other things, the Group's ability to paydividends, incur additional indebtedness, create liens, sell assets, or engage in mergers or acquisitions. These restrictions could further limit the Group's ability to plan for or react to market conditions or meet extraordinary capital needs or otherwise restrict corporate activities. There canbe no assurance that such restrictions will not materially and adversely affect the Group's ability to finance its future operations or capital needs.

The Group's future cash flows may be insufficient to meet all of its debt obligations and contractual commitments. To the extent that the Group is unable to repay its indebtedness as it becomes due or at maturity, the Group may need to refinance its debt, raise new debt, sell assets orrepay the debt with the proceeds from equity offerings.

Additional indebtedness or equity financing may not be available to the Group in the future for the refinancing or repayment of existing indebtedness, and the Group may not be able to complete asset sales in a timely manner sufficient to make such repayments.

Interest rate fluctuations could affect the Group's cash flow and financial condition

The Group has incurred, and may in the future incur, significant amounts of debt. The Group is exposed to interest rate risk primarily in relation to its long-term borrowings issued at floating interest rates. If the Group were to hedge some or all of its interest rate exposure, there can be noassurance that such hedging arrangements will be effective. As such, movements in interest rates could affect the Group's cash flow and financial condition.

Fluctuations in exchange rates could affect the Group's cash flow and financial condition

The Group has currency exposure to both transaction risk and translation risk related to its operating and administrative expenses.

Transaction risk arises when future commercial transactions or recognised assets or liabilities are denominated in a currency that is not the entity's functional currency. The Group is exposed to transaction risks due to fluctuations in exchange rates as it receives revenue primarily in USD,but a portion of its operating and administrative and general expenses are in local currencies. In certain markets where the Group operates, it may experience currency exchange losses when revenue is received and expenses are paid in non-convertible currencies or when the Groupdoes not hedge an exposure to the relevant foreign currency.

Translation risk arises due to the conversion of amounts denominated in foreign currencies to USD, the Group's reporting and functional currency. One of the Group's subsidiaries has NOK as its reporting and functional currency. Consequently, any change in exchange rates between itsoperating subsidiary's functional currency and USD affect its consolidated income statement and balance sheet when the result of that operating subsidiary is translated into USD for reporting purposes.

6. Risks related to the Shares

The price of the Shares may fluctuate significantly

The trading price of the Shares could fluctuate significantly in response to a number of factors beyond the Group's control, including, but not limited to, quarterly variations in operating results, adverse business developments, changes in financial estimates and investmentrecommendations or ratings by securities analysts, or any other risk discussed herein materialising or the anticipation of such risk materialising.