private fund securities law exemptions: accredited...

TRANSCRIPT

Private Fund Securities Law Exemptions:

Accredited Investors, Qualified Purchasers,

Subscription Limits and More Navigating Exemptions Under the Investment Adviser,

Securities, Exchange and Investment Company Acts

Today’s faculty features:

1pm Eastern | 12pm Central | 11am Mountain | 10am Pacific

The audio portion of the conference may be accessed via the telephone or by using your computer's

speakers. Please refer to the instructions emailed to registrants for additional information. If you

have any questions, please contact Customer Service at 1-800-926-7926 ext. 1.

WEDNESDAY, APRIL 4, 2018

Presenting a live 90-minute webinar with interactive Q&A

Michael D. Belsley, Partner, Kirkland & Ellis, Chicago, IL

Brynn Rail, Counsel, Ropes & Gray, New York

Tips for Optimal Quality

Sound Quality

If you are listening via your computer speakers, please note that the quality

of your sound will vary depending on the speed and quality of your internet

connection.

If the sound quality is not satisfactory, you may listen via the phone: dial

1-888-450-9970 and enter your PIN when prompted. Otherwise, please

send us a chat or e-mail [email protected] immediately so we can address

the problem.

If you dialed in and have any difficulties during the call, press *0 for assistance.

Viewing Quality

To maximize your screen, press the F11 key on your keyboard. To exit full screen,

press the F11 key again.

FOR LIVE EVENT ONLY

Continuing Education Credits

In order for us to process your continuing education credit, you must confirm your

participation in this webinar by completing and submitting the Attendance

Affirmation/Evaluation after the webinar.

A link to the Attendance Affirmation/Evaluation will be in the thank you email

that you will receive immediately following the program.

For additional information about continuing education, call us at 1-800-926-7926

ext. 2.

FOR LIVE EVENT ONLY

4

4

April 4, 2018

Private Funds Securities

Law Exemptions –

Navigating the Maze

Webinar

Michael Belsley, Kirkland & Ellis LLP

Brynn Rail, Ropes & Gray LLP

5

5

Overview

This CLE webinar will discuss the exemption provisions of the

Investment Adviser Act, Securities Act, Exchange Act and Investment

Company Act that are relevant to private equity funds and venture capital

funds. The program will provide an in-depth analysis of each of the

exemption requirements, as well as the pros and cons of seeking

exemption from registration under these Acts.

6

6

Overview

I. Securities Act of 1933

II. Securities Exchange Act of 1934

III. Investment Company Act of 1940

IV. Investment Advisers Act of 1940

7

7

I. Securities Act of 1933

Prohibits the offering or sale of securities unless a registration statement

has been filed or an exemption is available.

“Securities” defined broadly to include stock and debt instruments.

Applies to transactions in securities involving the use of the U.S. mails or

interstate commerce.

A. Section 4(2) of the 1933 Act (the Statutory Private Placement

Exemption)

– Transactions not involving any public offering are not required to

be registered

– The 1933 Act does not define public offering

– No general solicitation or public advertising

8

8

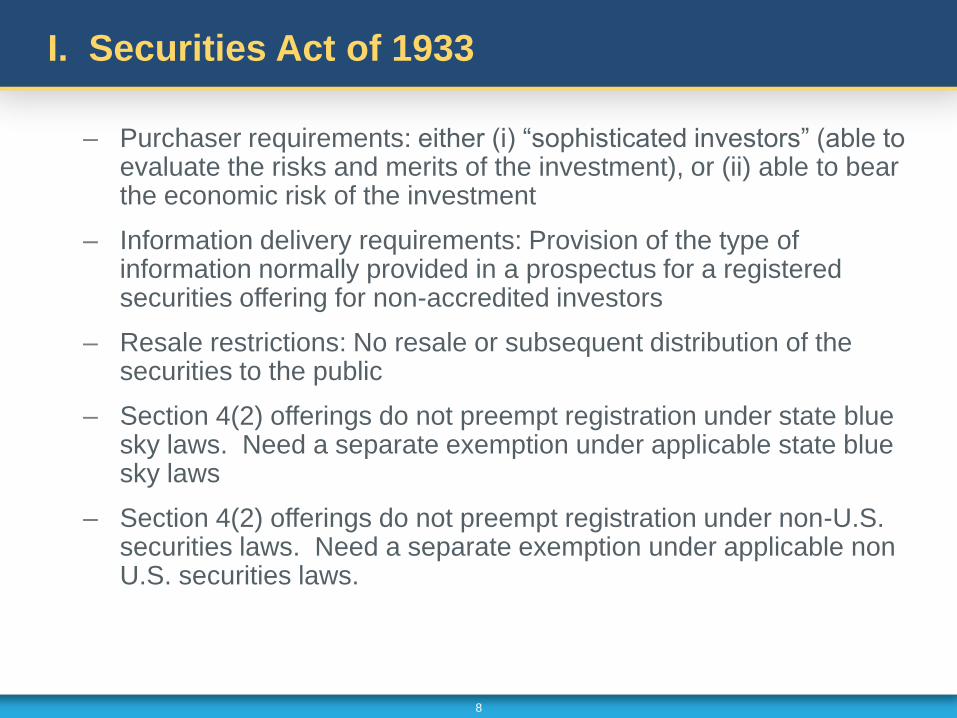

I. Securities Act of 1933

– Purchaser requirements: either (i) “sophisticated investors” (able to evaluate the risks and merits of the investment), or (ii) able to bear the economic risk of the investment

– Information delivery requirements: Provision of the type of information normally provided in a prospectus for a registered securities offering for non-accredited investors

– Resale restrictions: No resale or subsequent distribution of the securities to the public

– Section 4(2) offerings do not preempt registration under state blue sky laws. Need a separate exemption under applicable state blue sky laws

– Section 4(2) offerings do not preempt registration under non-U.S. securities laws. Need a separate exemption under applicable non U.S. securities laws.

9

9

I. Securities Act of 1933

B. Accredited investors

Categories of accredited investor (AI)

– individuals with a net worth in excess of $1,000,000 or annual

income in excess of $200,000 (or joint income with spouse in

excess of $300,000);

– a director, executive officer, or general partner of the issuer of the

securities being offered or sold, or any director, executive officer, or

general partner of a general partner of that issuer if organized as a

partnership;

– bank as defined in Section 3(a)(2) of the Securities Act, or a

savings and loan association or other institution as defined in

Section 3(a)(5)(A) of the Securities Act, whether acting in its

individual or fiduciary capacity;

10

10

I. Securities Act of 1933

– broker or dealer registered pursuant to Section 15 of the U.S.

Securities Exchange Act of 1934, as amended (the “Exchange

Act”);

– an insurance company as defined in Section 2(a)(13) of the

Securities Act;

– an investment company registered under the U.S. Investment

Company Act of 1940, as amended, and the rules and regulations

promulgated thereunder (the “Investment Company Act”);

– a business development company as defined in Section 2(a)(48) of

the Investment Company Act;

– a Small Business Investment Company licensed by the U.S. Small

Business Administration under Section 301(c) or (d) of the U.S.

Small Business Investment Act of 1958, as amended;

11

11

I. Securities Act of 1933

– a plan established and maintained by a state, its political subdivisions,

or any agency or instrumentality of a state or its political subdivisions,

for the benefit of its employees, if such plan has total assets in excess

of $5,000,000;

– an employee benefit plan within the meaning of Title I of the U.S.

Employee Retirement Income Security Act of 1974, as amended, and

the rules and regulations promulgated thereunder (“ERISA”), and:

the investment decision is made by a plan fiduciary, as defined in

Section 3(21) of ERISA, which is either a bank, savings and loan

association, insurance company or registered investment adviser,

the employee benefit plan has total assets in excess of

$5,000,000, or

such plan is a self-directed plan with investment decisions made

solely by persons that are “accredited investors”;

12

12

I. Securities Act of 1933

– a private business development company as defined in Section

202(a)(22) of the U.S. Investment Advisers Act of 1940, as

amended, and the rules and regulations promulgated thereunder

(the “Investment Advisers Act”);

– one of the following entities which was not formed for the specific

purpose of making an investment in the Partnership and which has

total assets in excess of $5,000,000:

a corporation, limited liability company or partnership,

an organization described in §501(c)(3) of the U.S. Internal

Revenue Code of 1986, as amended (the “Code”); or

a Massachusetts or similar business trust;

13

13

I. Securities Act of 1933

– a trust, with total assets in excess of $5,000,000, not formed for the

specific purpose of acquiring limited partner interests of the

Partnership, whose purchase of the limited partner interests

offered is directed by a person with such knowledge and

experience in financial and business matters as to be capable of

evaluating the merits and risks of an investment in such limited

partner interests; or

– an entity in which all of the equity owners are “accredited

investors.”

SEC Staff has previously proposed revising the definition and

thresholds of Accredited Investor, including in 2015, but the

recommendation has not been implemented

14

14

I. Securities Act of 1933

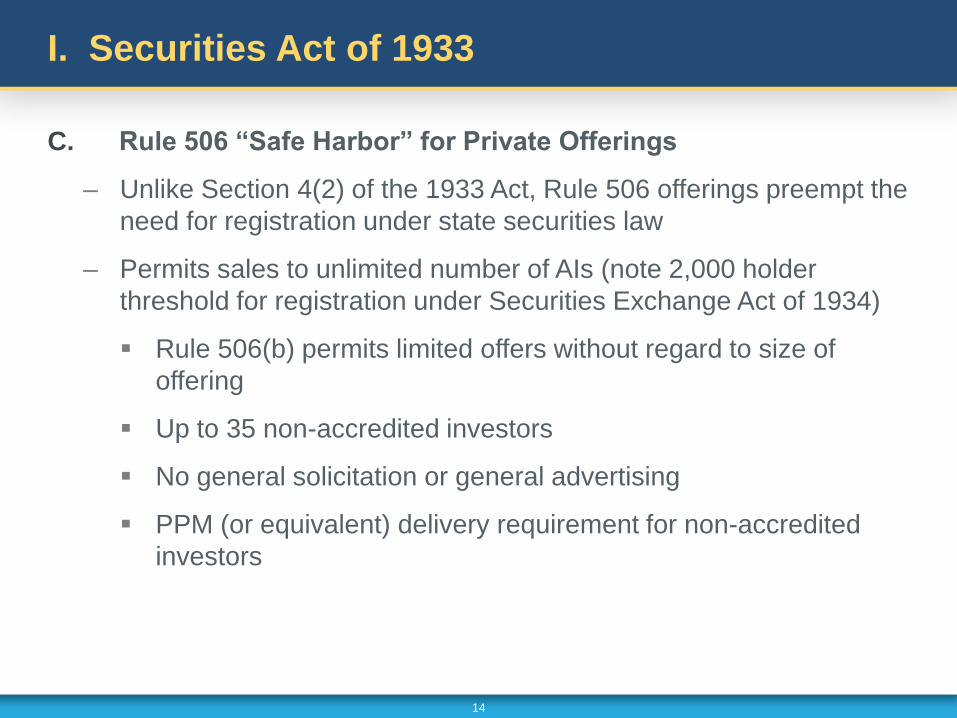

C. Rule 506 “Safe Harbor” for Private Offerings

– Unlike Section 4(2) of the 1933 Act, Rule 506 offerings preempt the

need for registration under state securities law

– Permits sales to unlimited number of AIs (note 2,000 holder

threshold for registration under Securities Exchange Act of 1934)

Rule 506(b) permits limited offers without regard to size of

offering

Up to 35 non-accredited investors

No general solicitation or general advertising

PPM (or equivalent) delivery requirement for non-accredited

investors

15

15

I. Securities Act of 1933

– Rule 506(c)—JOBS Act Provision

– Permits general solicitation of investors and general public

advertising

– No PPM delivery requirement

– Must verify AI status of investors

16

16

I. Securities Act of 1933

D. Significance of Rule 506(d) “disqualifying event” – the Bad

Actor Rule

– An offering is disqualified from relying on Rule 506(b) and 506(c) of

Regulation D if the issuer or any other person covered by Rule

506(d) has a relevant criminal conviction, regulatory or court order

or other disqualifying event that occurred on or after the effective

date of the rule amendments (i.e., September 23, 2013).

– For disqualifying events that occurred before September 23, 2013,

issuers may still rely on Rule 506, but must comply with the

disclosure provisions of Rule 506(e).

17

17

I. Securities Act of 1933

– Under the Rule, certain events are considered disqualifying events for bad actors. They include:

Certain criminal convictions

Certain court injunctions and restraining orders

Final orders of certain state and federal regulators

Certain SEC disciplinary orders

Certain SEC cease-and-desist orders

SEC stop orders and orders suspending the Regulation A exemption

Suspension or expulsion from membership in a self-regulatory organization (SRO), such as FINRA, or from association with an SRO member

U.S. Postal Service false representation orders

18

18

I. Securities Act of 1933

– Certain disqualifying events include a look-back period (for

example, a regulatory order that was issued within the last ten

years).

This look-back period is measured from the date of the disqualifying

event and not the date of the underlying conduct that led to the

disqualifying event.

19

19

I. Securities Act of 1933

E. General Solicitation

SEC Rule 502(c) does not define General Solicitation but does provide

examples of it.

(1) Any advertisement, article, notice or other communication

published in any newspaper, magazine, or similar media or

broadcast over television or radio

(2) Any seminar or meeting whose attendees have been invited by

any general solicitation or general advertising

20

20

I. Securities Act of 1933

F. Offerings under Regulation S Safe Harbor

– Regulation S provides an exclusion from registration under the

1933 Act for offerings made outside the United States

– Regulation S can be relied upon by both U.S. and foreign issuers

– The Regulation S safe harbor is non-exclusive, meaning that an

issuer that attempts to comply with Regulation S also may rely on

another exemption or safe harbor, such as Regulation D

– Deemed offshore if no directed selling efforts in U.S.

– Non-U.S. investors must receive the PPM and must sign the

Subscription Agreement outside the U.S.

21

21

II. Securities Exchange Act of 1934

Regulates securities exchanges operating in interstate commerce and

through the U.S. mails.

Requires registration with the SEC of issuers at certain thresholds and

broker-dealers

“Broker” is defined broadly as “any person engaged in the business of

effecting transactions in securities for the account of others”

“Engaged in the business” and “Effecting transactions” are not defined

terms

Unregistered entities receiving transaction-based compensation has

been an area of focus for the SEC for the last several years

22

22

II. Securities Exchange Act of 1934

A. Issuer exemption from broker-dealer registration

– Section 3a4-1 – the “Issuer’s Exemption” is a safe harbor for sales of securities by Officers, Employees and other Associated Persons of the Issuer

– Rule 3a4-1 is a “non-exclusive safe-harbor” under which an “associated person” of an issuer that performs limited securities sales for the issuer as prescribed by the rule would be deemed not to be a “broker” under Section 3(a)(4).

– Must meet the following preliminary conditions to rely on Rule 3a4-1:

The associated person must not be subject to a statutory disqualification, as defined in Section 3(a)(39) of the Exchange Act, at the time of his or her participation in the sale of the issuer’s securities

23

23

II. Securities Exchange Act of 1934

– In addition to satisfying each of the preliminary conditions, one of

the following three sets of conditions must be satisfied in order for

the safe harbor to apply:

Sales Restricted to Certain Classes of Purchasers or Certain

Transactions

Sales Duties Are Limited in Frequency and Proportion

Sales Duties Are Passive

– Safe harbor available limited to once every 12 months

24

24

II. Securities Exchange Act of 1934

– If the safe harbor does not apply, the SEC will apply a facts and circumstances based analysis. Factors include:

Transaction – based compensation: the single most important hallmark of broker status – any compensation relating to the success of the sale of the subject securities

Soliciting securities transactions (significant investor contact and negotiation)

Assisting in the structuring of the securities terms and transactions

Identifying potential purchasers

Taking or participating in orders for securities

Previous securities registration

Regular participation in the securities business

25

25

II. Securities Exchange Act of 1934

B. Investor limit

– 2,000 holder threshold for registration under Securities Exchange

Act of 1934

– Rule 12g3-2 provides an exemption if no class of fund securities

has 300 or more holders resident in the United States

26

26

III. Investment Company Act of 1940

A. Qualified Purchaser Fund Exemption

– Section 3(c)(7) of the Investment Company Act

– Requires all investors to be “qualified purchasers” or

“knowledgable” employees

– Qualified Purchaser Requirements

– Knowledgeable Employees

– Generally, if a natural person, must be an executive officer or

involved in the investment decisions

27

27

III. Investment Company Act of 1940

– More specifically, if a natural person, required to be:

An executive officer, director, trustee, general partner, advisory

board member, or person serving in a similar capacity, of the

fund or the fund’s affiliated investment manager; or

An employee (other than clerical and administrative personnel)

of the fund or the fund’s affiliated investment manager who

participates in the investment decisions and activities of such

fund manager for such fund or on behalf of another company for

at least 12 months.

– “Look through” Issues

28

28

III. Investment Company Act of 1940

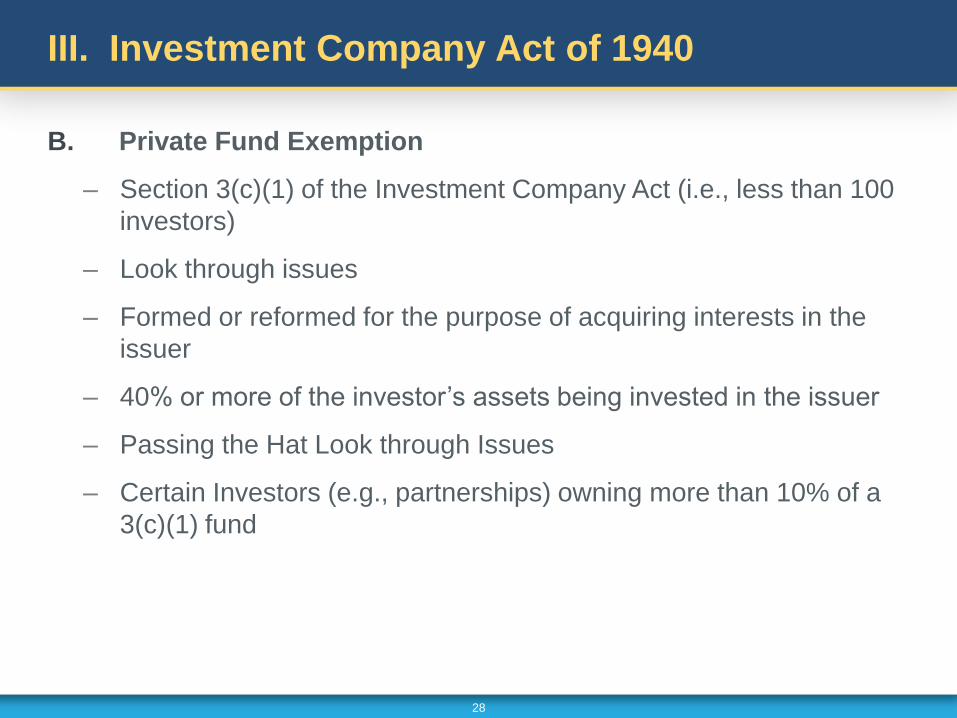

B. Private Fund Exemption

– Section 3(c)(1) of the Investment Company Act (i.e., less than 100

investors)

– Look through issues

– Formed or reformed for the purpose of acquiring interests in the

issuer

– 40% or more of the investor’s assets being invested in the issuer

– Passing the Hat Look through Issues

– Certain Investors (e.g., partnerships) owning more than 10% of a

3(c)(1) fund

29

29

IV. Investment Advisers Act of 1940

Prohibits “investment advisers” from engaging in interstate commerce in

connection with acting as an investment adviser unless registered or

exempt

Antifraud provisions intend to prevent advisers from defrauding or

deceiving clients

Imposes an implicit fiduciary duty on investment advisers

A. Qualified Clients

– The GP of a 3(c)(1) fund may not charge a performance based fee

(such as carried interest) in respect of an investor unless such

investor is a Qualified Client.

30

30

IV. Investment Advisers Act of 1940

– Categories of Qualified Client:

Net worth in excess of $2.1 million; or

Qualified Purchaser under Investment Company Act of 1940; or

Making a Commitment of at least $1 million

B. Exempt reporting advisers

– Under $25 million in Regulatory Assets Under Management

(“RAUM”)

SEC registration prohibited (with certain limited exceptions).

Home jurisdiction registration required at the state level unless

exempt under applicable state law.

Additional state registration preempted if adviser has no place

of business or fewer than 6 resident clients

31

31

IV. Investment Advisers Act of 1940

– Between $25 and $100 million in RAUM –Mid-sized Advisers

Federal registration generally not required (except BDC and

Registered Investment Company advisers)

State registration required unless exempt.

Additional state registration preempted if adviser has no place

of business or fewer than 6 resident clients, then required

unless exempt.

– Over $100 million in RAUM

SEC registration required unless exempt.

State registration required unless exempt or SEC registered.

32

32

IV. Investment Advisers Act of 1940

– Other exemptions

– Advisers who solely advise qualifying venture capital funds*

Foreign private advisers–limited to 15 U.S. clients/investors and

$25 million from U.S. clients

– Advisers who solely advise SBICs

– Advisers who solely advise private funds with aggregate RAUM

managed in the U.S. under $150 million*

*Subject to exempt adviser reporting on Form ADV

33

33

IV. Investment Advisers Act of 1940

– U.S. advisers--An investment adviser that only advises private funds with

its principal office and place of business in the U.S. is exempt from

registration if it:

Acts solely as an investment adviser to one or more qualifying private

funds; and

Manages private fund assets of less than $150 million.

Need to file a Form ADV as an exempt reporting advisor

– Non-U.S. advisers--an investment adviser with its principal office and

place of business outside of the U.S. is exempt from registration if it:

Has no client that is a U.S. person except for one or more qualifying

private funds; and

All assets managed by the investment adviser at a place of business in

the U.S. are solely attributable to private fund assets, the total value of

which is less than $150 million.

– Need to file a Form ADV as an exempt report advisor

34

QUESTIONS

35

THANK YOU Michael D. Belsley

Kirkland & Ellis

Partner, Chicago

312-862-2483

Brynn Rail

Ropes & Gray

Counsel, New York

212-596-9194