private equity europe 26 september 2007 confidentialpresentation to: vittorio pignatti morano, vice...

TRANSCRIPT

Private Equity Europe

26 September 2007

Confidential Presentation to:

Vittorio Pignatti Morano, Vice Chairman

What is Private Equity?

Private Equity funds are pools of capital managed by professional investors who make equity investments in private companies

Private Equity funds align the economic interests of three key players:– Investors looking for higher risk / return equity exposure – Companies seeking financing to complement or replace traditional sources of capital– The investment professionals / venture capitalists

Types of Private Equity– Corporate Buyouts

• Merchant Banking• Co-Investment• Infrastructure

– Venture Capital– Fund of Funds– Real Estate– Mezzanine Products

The performance of the fund is defined by the investment’s internal rate of return (“IRR”); the IRR of a fund is the return on the investment

1

Private Equity Returns

Private Equity has outperformed public equity over the last 10 and 20 years

Net IRRs Ending 31 December 2006

20-Year 10-Year

___________________________1. Historical trends do not imply, forecast or guarantee future results. Thomson Venture Economics’ US Private Equity Performance Index is based on the latest (31 December 2006) quarterly statistics from Thomson Venture Economics’ Private Equity Performance Database analysing the cash flows and returns for 1,860 US venture capital and private

equity partnerships with a capitalisation of over $679bn. Sources are financial documents and schedules from limited partner investors and general partners. All returns are calculated by Thomson Venture Economics from the underlying financial cash flows. Returns are net to investors after management fees and carried interest.2. Source: Bloomberg, LP. Represents quarterly total returns for the period. S&P 500 & Dow Jones exclude dividend reinvestment. NASDAQ and Russell 2000 exclude dividends.

13.9%

9.2%9.9% 10.2%

9.2%

0%

3%

6%

9%

12%

15%

(% )

PE Index S&P 500 Dow Jones NASDAQ Russell 2000(1) (2) (2) (2) (2)

11.0%

6.7% 6.8% 6.5%

8.1%

0%

3%

6%

9%

12%

15%

(% )

PE Index S&P 500 Dow Jones NASDAQ Russell 2000(1) (2) (2) (2) (2)

2

Strong Industry Growth

The market for LBOs has increased more than ten times in the last five years

29 33

57 53

40

20 22

47

94

130

233

0

50

100

150

200

250

1996 1997 1998 1999 2000 2001 2002 2003 2004 2005 2006

($bn)

Total US Leveraged Buyout Volume

___________________________Source: S&P Global Leveraged Loan Review 4Q06. Historical trends do not imply, forecast or guarantee future results.

3

Increasing Deal Sizes

The average size of an LBO reached over $1bn in 2006

0.5

0.4 0.4 0.4 0.4 0.4

0.5

0.7 0.7

1.0

1.3

0.0

0.4

0.8

1.2

1.6

1996 1997 1998 1999 2000 2001 2002 2003 2004 2005 2006

($bn)

Average LBO Size

___________________________Source: S&P Global Leveraged Loan Review 4Q06. Historical trends do not imply, forecast or guarantee future results.

4

Globalisation of Private Equity

The industry has expanded outside the US

69%

52%

17%

38%

14%10%

0%

20%

40%

60%

80%

100%

2000 2005

(% )

North America Europe Asia + Other

Funds Raised

___________________________Source: International Financial Services London (ESFL) estimates based on Thomsan, PwC and EVCA data.

Investments

68%

40%

17%

43%

15% 17%

0%

20%

40%

60%

80%

100%

2000 2005

(% )

North America Europe Asia + Other

5

Global Fundraising EnvironmentRapid growth of private equity in recent years is capturing the attention of many investors who have never invested in the asset class

___________________________Source: Thomson Financial, through December 31, 2006. Includes Buyout and Mezzanine funds.

$47

$71

$99$88

$114$103

$71 $66

$94

$203

$352

0

50

100

150

200

250

300

350

400

1996 1997 1998 1999 2000 2001 2002 2003 2004 2005 2006

($ billions)

North America Europe Other

Commitments to Global Private Equity Partnerships

6

European Fundraising Environment

As in the U.S., 2006 was a record year for private equity fundraising in Europe

___________________________1. Source: Thomson VenturExpert.

€ 61.8

€ 53.5

€ 16.7

€ 23.7

€ 19.1

€ 52.6

€ 60.7

€ 27.0

€ 21.1€ 18.4

€ 8.3

0

10

20

30

40

50

60

70

1996 1997 1998 1999 2000 2001 2002 2003 2004 2005 2006

($ billions)

Commitments to Asian Private Equity Partnerships1Observations

Fundraising has predominately been in the buyout space as traditional venture capital investing is relatively less important

The list of the largest funds raised in Europe in 2006 is dominated by:

– Pan-European funds, headquartered in London; or

– Nordic funds headquartered in Stockholm Many investors believe middle-market European funds, which

tend to be most often country-specific, are more likely to generate outsized returns

Fund Name Location Year Amount (€mm)

Permira IV London 2006 11,000

Cinven IV London 2006 6,500

3i Europe Partners V London 2006 5,000

EQT V Stockholm 2006 4,250

CVC European Equity Partners IV London 2006 4,200

Charterhouse Capital Partners VIII London 2006 4,000

Terra Firma Capital Partners III London In Market 4,000

Nordic Capital Fund VI Stockholm 2006 1,900

TDR Capital Fund II London 2006 1,750

Altor Equity Partners II Stockholm 2006 1,150

10 Largest European Funds Ever Raised

7

Evolution of the Buyout Market

Bull Market

Recession

Resurgence

Growing

Developing

Recession

Late ’90s 2000–2002 2003–2007Late ’80sEarly to Mid ’80s Early ’90sStrong Good Poor Good StrongExcellent

VintagePerformance

Loan Market

Under Exploited Balance Sheets

Underperforming Economy

DevelopingHY Market

More Sophisticated

Financial Engineering

Growing M&A

Limited Equity

Increasing Deal Size

Recapitalisation Through Equity

Markets

Multiple Contraction

HLT Regulation

Abundant Fundraising

EconomicBoom

Overheated Stock Market

Tech / Telecom Bubble

Non US Buyouts

Focus on Growth Investments

Valuation Decline

Tight Credit

Management Focus

Increased Equity

Robust Credit Market

Club Deals

Strategic Buyers Less Relevant

Low Interest Rates

Sarbanes-Oxley

Globalisation of Business

Mega Buyouts

Growing Level of Sophistication

8

Lehman Brothers Private Equity Fund Performance

Fund Performance1

Asset Class Invested Capital Period Gross IRR

Merchant Banking $3.5 billion 1989 – 2007 37%

Venture Capital $699 million 1996 – 2007 28%

Real Estate $4.7 billion 2000 – 2007 33%

European Mezzanine $1.2 billion 2002 – 2007 17%

CDO Opportunity $556 million 2002 – 2007 25%

Fund of Fund Investments $2.9 billion 1997 – 2006 32%

First quartile performance in aggregate since inception of each asset class

___________________________Source; Lehman Brothers Inc. Past performance is not necessarily indicative of future results. There can be no assurance that future funds will achieve comparable results. 1. Returns are expressed in US Dollars. All returns are as of March 31, 2007 except for the Fund of Fund Investments return, which is as of 12/31/2006. Gross internal rates of return (IRRs) do not reflect the management fees, carried interest, taxes, transaction costs and other expenses to be borne by

investors in each fund, which in the aggregate are expected to be substantial.

9

Current Areas of Interest in Private Equity

1. Secondary Investments

– Purchase of limited partnership interests from original investors

– Access to relatively mature private equity investments often at favorable prices

– Reduces the J-curve effect by hastening the time until portfolio investment gains are realized

– Improved visibility pertaining to the underlying partnership portfolio companies

2. Co-Investment

– Direct investment in private equity transactions

– Selectivity in deals

– Reduced GP fees

– Lower fees and the immediacy of capital calls contribute to truncation of the J-curve

– Beneficiary of limited “club deals”

3. Mezzanine

– Through mezzanine debt, investors can acquire buyout equity exposure without paying high premiums

– Historically, mezzanine debt has offered equity-like returns with fixed-income-like risk levels

– Mezzanine also offers good diversification benefits vs. high yield (i.e., historical correlation = zero)

10

Current Areas of Interest in Private Equity (cont’d)

4. Large Cap Buyouts

– Mega cap deals (greater than $5 billion) can have less competition than the middle market and small market

– This is largely an historically untapped market

– Resale of subsidiaries to strategic buyers

– Strategic buyers emerging in Asia and the Persian Gulf

5. Infrastructure

– Hybrid investment between private equity and fixed income

– Illiquidity risk premium plus long duration

– Long-dated contracts

– Inelastic demand

– Municipalities, electric utilities

6. Distressed Debt in private equity

– Slow deployment of capital from date of subscription

– Opportunistic investment as distressed situations arise

– Effective counterbalance and diversification to LBO equity investments

11

2008 – 2010 Opportunities

Real Estate – Asia, Emerging Europe

Mezzanine – Europe, U.S.

Buyouts – mid-cap globally

Secondary investments

Infrastructure investments – globally

12

0x

2x

4x

6x

8x

10x

12x

14x

2004 2005 2006 2007 YTD

EB

ITD

A m

ult

iple

<$1 B $1-5 B $5+ B

Mega Caps And Mezzanine

___________________________

Source: Factset, Lehman Brothers

LBOs: EBITDA Multiples

Attractive Risk Adjusted Performance Of Mezzanine Investing

Source: Thomson, Bloomberg, Lehman; As of 12/06; Mezzanine data represents 25 th %ile returns

0%

5%

10%

15%

20%

25%

Return Risk Return Risk Return Risk Return Risk Return Risk

Mezzanine Debt US Large Cap Equity US Fixed Income High Yield LBO

3yrs

5yrs

7yrs

10yrs

13

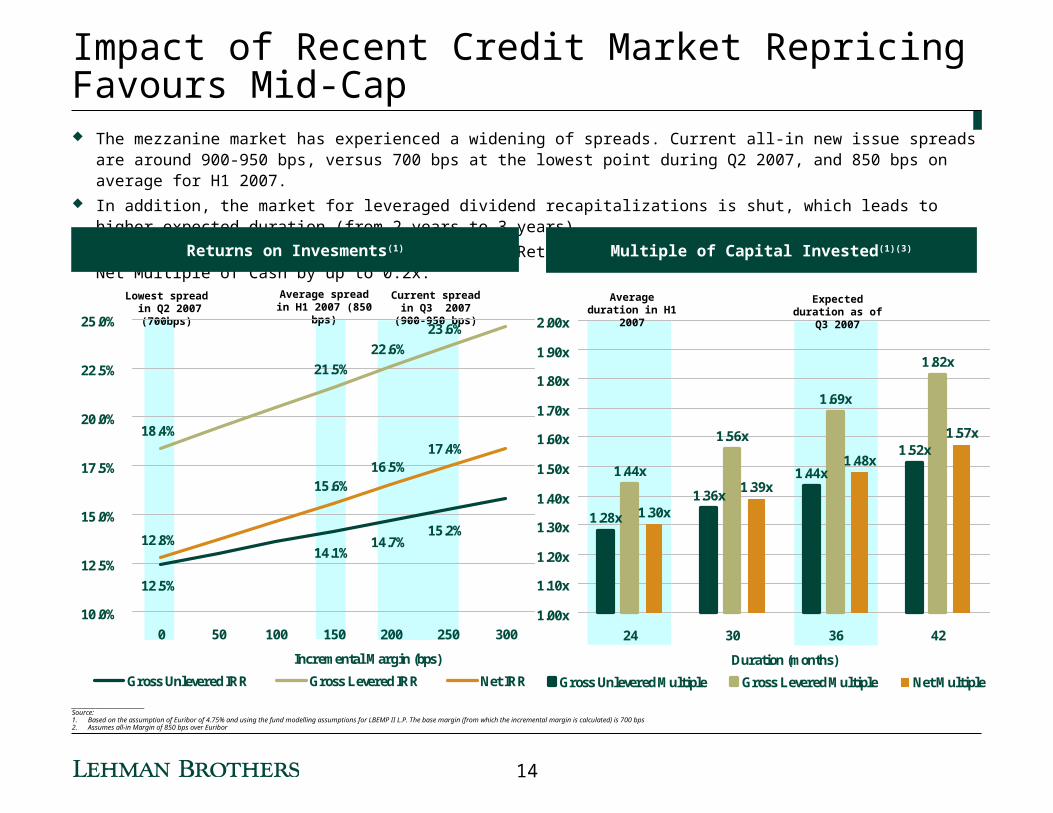

Impact of Recent Credit Market Repricing Favours Mid-Cap The mezzanine market has experienced a widening of spreads. Current all-in new issue spreads are around 900-950 bps, versus 700 bps at

the lowest point during Q2 2007, and 850 bps on average for H1 2007. In addition, the market for leveraged dividend recapitalizations is shut, which leads to higher expected duration (from 2 years to 3 years). As a result, on a Fund basis, projected Net Returns to investors are higher by 3% - 5% and Net Multiple of Cash by up to 0.2x.

Returns on Invesments(1)

___________________________Source: 1. Based on the assumption of Euribor of 4.75% and using the fund modelling assumptions for LBEMP II L.P. The base margin (from which the incremental margin is calculated) is 700 bps2. Assumes all-in Margin of 850 bps over Euribor

Multiple of Capital Invested(1)(3)

1.28x

1.36x

1.44x

1.52x

1.44x

1.56x

1.69x

1.82x

1.30x

1.39x

1.48x

1.57x

1.00x

1.10x

1.20x

1.30x

1.40x

1.50x

1.60x

1.70x

1.80x

1.90x

2.00x

24 30 36 42

Duration (months)

Gross Unlevered Multiple Gross Levered Multiple Net Multiple

Lowest spread in Q2 2007 (700bps)

Average spread in H1 2007 (850 bps)

Current spread in Q3 2007 (900-950 bps)

Average duration in H1 2007

Expected duration as of Q3 2007

12.5%

14.1%14.7%

15.2%

18.4%

22.6%

23.6%

12.8%

15.6%16.5%

17.4%

21.5%

10.0%

12.5%

15.0%

17.5%

20.0%

22.5%

25.0%

0 50 100 150 200 250 300

Incremental Margin (bps)

Gross Unlevered IRR Gross Levered IRR Net IRR

14

DisclaimerThis presentation (the "Presentation") is being furnished on a confidential basis to a limited number of sophisticated institutions on a "one-on-one" basis for informational and discussion purposes only and does not constitute an offer to sell or a solicitation of an offer to purchase any security in Lehman Brothers European Mezzanine Partners II ("Fund II"). Any such offer or solicitation shall be made only pursuant to the confidential private placement memorandum relating to Fund II, as amended or supplemented from time to time (the "Memorandum"), which describes the risks relating to an investment in Fund II as well as other important information about Fund II and Lehman Brothers.

This Presentation is qualified in its entirety by all of the information set forth in the Memorandum, including without limitation the notice to investors set out at the front of the Memorandum and the section headed "Risk Factors and Conflicts of Interest". The Memorandum must be read carefully in its entirety prior to investing in Fund II. This Presentation does not constitute a part of the Memorandum.

This Presentation is based on or derived from information which is believed to be reliable and no representation is made that it is accurate or complete. Past performance is no indication of future results. No reliance should be placed on the contents of this Presentation by any person who may subsequently decide to enter into a transaction with Lehman Brothers.

Investors should determine for themselves the relevance of the information contained in this Presentation and any subsequent decision to invest in Fund II should be based on such investigation as they themselves deem necessary. An investment in Fund II is suitable only for sophisticated investors and requires the financial ability and willingness to accept the high risks and lack of liquidity inherent in such a transaction.

The distribution of this Presentation in certain jurisdictions may be restricted by law. This Presentation is only directed at persons to whom it may lawfully be distributed and any investment activity to which this Presentation relates will only be available to such persons. It is the responsibility of any potential investor to satisfy itself as to the full compliance of the applicable laws and regulations of any relevant jurisdiction, including obtaining any governmental or other consent and observing any other formality prescribed in such jurisdiction.

This Presentation is proprietary to Lehman Brothers and may not be disclosed to any third party or used for any purpose without the prior written consent of Lehman Brothers.

15