private and confidential leasing/asset finance training for ula prepared for uganda leasing...

TRANSCRIPT

Private and confidential

LEASING/ASSET FINANCE TRAINING FOR ULA

Prepared for Uganda Leasing AssociationDenis Owili

16/06/15

2Contents

BASICS OF LEASING/ASSET FINANCE

• What is Asset Finance

. Is asset Finance Leasing

. Types of Leases

. Benefits of Leasing

• Stakeholders for any given Lease

• Assets that can be leased

• Industry Practice in Uganda

3What is Asset Finance

Asset finance is a sustainable form of funding that can enable a business to purchase or refinance capital equipment such as commercial vehicles, print machinery or construction and plant, spreading the cost over an agreed period of time.

Demonstrating its power as a strategic tool for business growth, asset finance is now the fastest growing finance option on the market.

The assets must meet the following Criteria

identifiable by means of serial numbers, engine number, make, and model

acceptable in terms of risk, value, condition and use of the asset

obtainable by the bank, in a valid and unassailable legal title

unencumbered (that is free and clear of any other claims or prior liens)

purchased from a reputable dealer/supplier

moveable, tangible and be able to be repossessed

fully insurable.

Marketable or saleable

- easy to value and its market value must not be subject to wide fluctuations

- verifiable in terms of the ownership of the asset

Key points

Sustainable form of funding

purchase./refinance equipment

Strategic tool for business growth

4Is Asset Finance Leasing?

Hire Purchase

Sale & Lease Back

Finance Lease

Operating Lease

Hire Purchase product provides the flexibility to spread the cost of an asset over a fixed period. Hire Purchase offers you fixed monthly repayments so you can manage your budget effectively over the repayment term. Plus, when the repayment term is finished, you own the asset.

Sale and Lease Back is an innovative product that enables you to unlock the capital held in your existing assets. It is a simple yet effective way to finance a business that is aiming for expansion.

If a business wants to maximize the use of an equipment without the responsibility of owning it, a Finance Lease will give them the freedom and flexibility they need. Also referred to as a full-payout lease, it seeks to recover the full cost of the asset, along with interest, over the primary agreement term. The business will have full use of the asset for its useful life, being responsible for its maintenance and insurance.

For a flexible way to enjoy an asset, Operating Lease is a great solution. It allows the business full use without the burden of ownership. The lease period is for a fraction of the asset’s useful life, which means you only pay for the difference between the original purchase price and the residual value at the end of the agreement.

At the end of the lease term, the asset is returned tp the Lessor and are responsible for disposing of the asset along with recovering the residual value on which the agreement was based.

Explanatory Notes on each type of Asset FinanceTypes of Asset FinanceKey points

Key points

Key points

Key points

5Types of Leases

Leasing in its simplest form is a means of providing access to finance and may be defined thus:

‘a contract between two parties whereby one party (the lessor) provides an asset to another party (the lessee) for usage and possession for a specified period of time, in return for specified and agreed payments.’

What is Leasing?

6

Two types of Leasing

1. Financial Leasing

2. Operating Leasing

7What is Leasing?......................

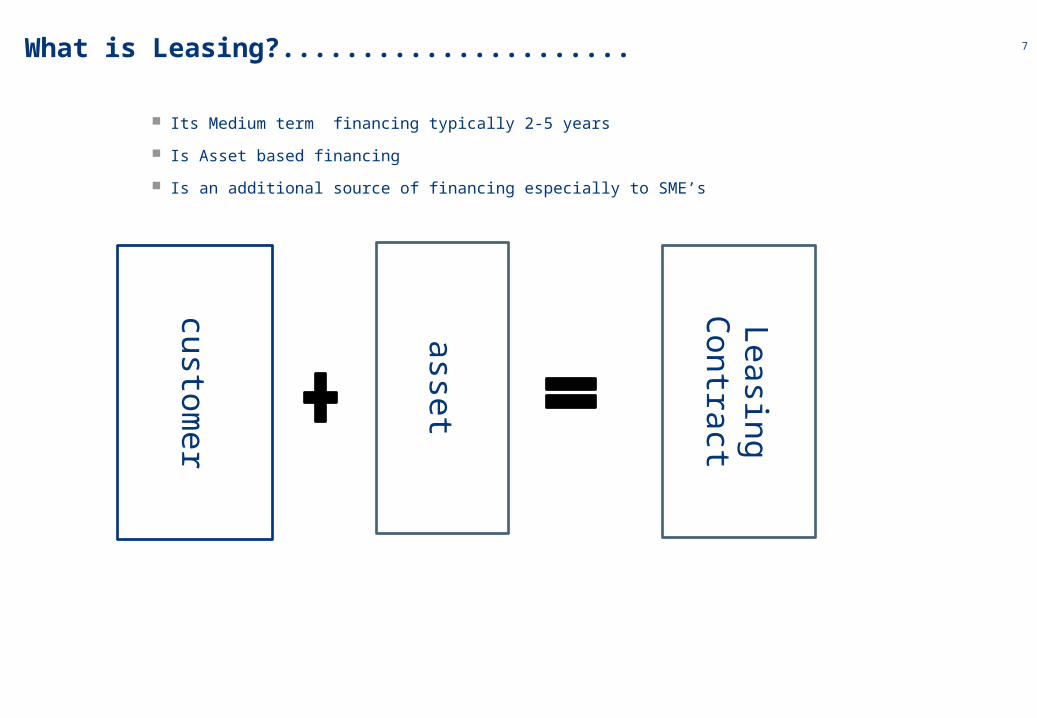

Its Medium term financing typically 2-5 years

Is Asset based financing

Is an additional source of financing especially to SME’s

customer

asset

Leasing Contract

8

What is financial Leasing?

LESSOR

(Leasing company)Pays the invoice from theequipment/vehicleSupplier

Legal ownershipof the asset(until the end of the lease)

LESSEE

(Customer)Use of the assetPossession of the asset

Fiscal benefitsassociated with the asset

9

Financial Leasing Process

Supplier

Lessee (client)

Lessor (Bank)

10Benefits of Leasing

There are tax benefits for Companies to finance their capital goods through Lease options. These are mainly manifested in the Operating lease scenarios. ROA improves,

The asset value is taken into consideration when assessing the collateral position of the client. This is an incentive to clients whose collateral value may not be adequate.

VAF forms a good lock in for clients and ensures loyalty to the bank. It’s a penetration product

The product provides for flexibility in terms of repayment structuring allowing for purchase, installation and commissioning of the equipment.

Preserves Existing Credit LinesVAF gives our client a new source of credit for present and future needs, while existing bank lines remain intact for other uses.

The value of equipment is realized when using it than when owning it.

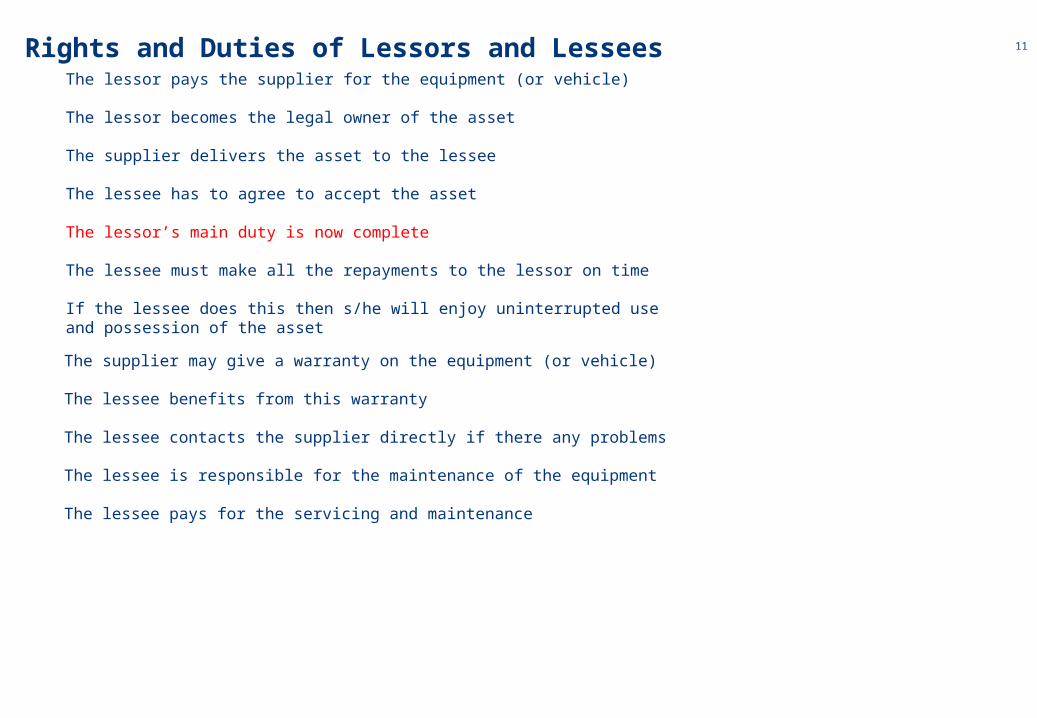

11Rights and Duties of Lessors and LesseesThe lessor pays the supplier for the equipment (or vehicle)

The lessor becomes the legal owner of the asset

The supplier delivers the asset to the lessee

The lessee has to agree to accept the asset

The lessor’s main duty is now complete

The lessee must make all the repayments to the lessor on time

If the lessee does this then s/he will enjoy uninterrupted useand possession of the asset

The supplier may give a warranty on the equipment (or vehicle)

The lessee benefits from this warranty

The lessee contacts the supplier directly if there any problems

The lessee is responsible for the maintenance of the equipment

The lessee pays for the servicing and maintenance

12

The lessee must insure the asset for the whole duration of the lease

Any damage caused to the asset must be remedied at the sole cost of the lessee (or insurer)

The lessee must allow reasonable access to the equipment if the lessor requests

Rights and Duties of Lessors and Lessees……………….

The lessee cannot pass or sell its obligations or rights to a third party

The lessor may transfer the lease contract to another party

BUT

The lessor may not sell (or pledge) the asset, only the lease contract

The new “lessor” must respect the terms and conditions of the lease contract

13Stakeholders for any given Lease

• Customers : Both Internal & External Customers

• Government

• Other internal departments such as IT, Risk, HR, Finance, Credit

• Vendors

Why are these stakeholders important in any given lease transaction?

Types of assets

• Office equipment

• Machinery and equipment

• Earthmoving equipment

• Commercial vehicles / Public transport

• Aviation

• Shipping and commercial fishing

• Medical equipment

• Agricultural equipment

• Yachts and motor boats

• Motor vehicles

Office equipment

• What type of equipment is to be financed?

• Will the equipment be used in the generation of business’ income?

• What will this equipment be used for and how will it support the business?

• Are there any other costs involved for aspects like installation and maintenance?

Considerations

Machinery and equipment

• Long term contracts or short variable jobbing contracts?

• Is purchasing adding value to the business?

• Luxury purchase or productive asset base?

• Generate sales or considered as an expense?

• Reputable supplier providing service back-up?

• Impact on production capacity

• Demand for goods and services

• Established market or not?

Considerations

Earthmoving equipment

• Core business?

• Composition of the fleet?

• Contracts on hand?

• Where is machine going to operate?

• Perform physical inspection

• Contract incoming funds period should match period of financing

Considerations

Commercial vehicles/Public transport

• Core business

• Type of goods

• Total distance to be travelled

• Length of hauls

• Condition of roads to be travelled

Considerations

Commercial vehicles/Public transport

• Maintenance of equipment

• Contract price per kilometer

• Composition of fleet

• Fleet insurance

• Management experience

Considerations

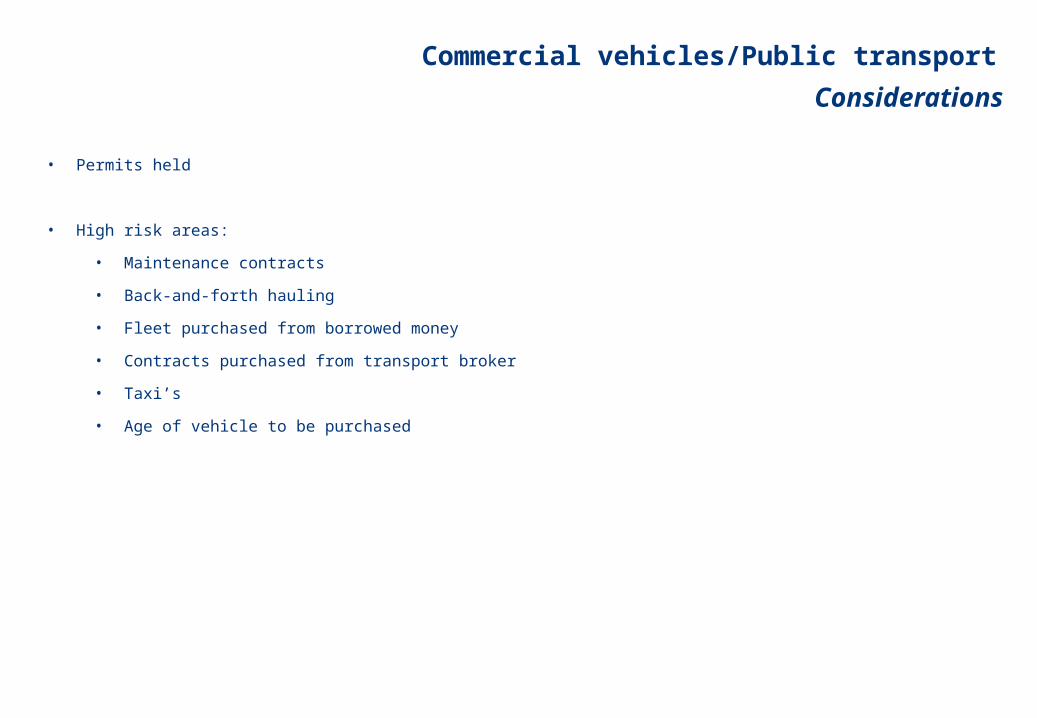

Commercial vehicles/Public transport

• Permits held

• High risk areas:

• Maintenance contracts

• Back-and-forth hauling

• Fleet purchased from borrowed money

• Contracts purchased from transport broker

• Taxi’s

• Age of vehicle to be purchased

Considerations

Aircrafts

• Service and spares back-up

• Certificates of airworthiness

• Service record

• Registration number

• Age vs. contract period

Considerations

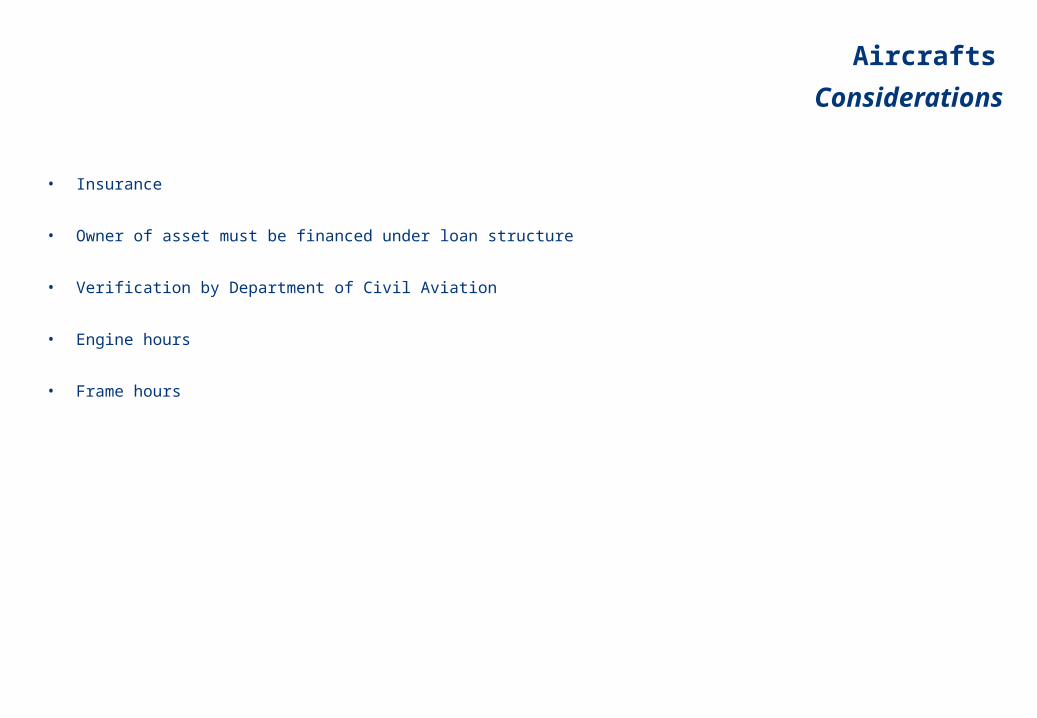

Aircrafts

• Insurance

• Owner of asset must be financed under loan structure

• Verification by Department of Civil Aviation

• Engine hours

• Frame hours

Considerations

Shipping/fishing

• Nautical consultant must evaluate vessel

• Marine mortgage

Considerations

Agricultural equipment

• What does farmer need goods for?

• Monthly repayments of non-productive and/or luxury goods

• Substantial upfront payment

• Payment frequency

Considerations

Used assets

• Stage of asset life cycle

• Cost of maintenance of used vs. new assets

• Older assets break down more often

• Effect on customer’s cash flow

• Parts availability

• Life span

Considerations

Used assets

• Condition

• Valuations from reputable valuator

• No finance higher than market value

• Must be insurable

• Establish ownership

Considerations

Industry Practice in Uganda

The Leasing Industry is currently not operating under any specific Leasing Law. Its is working with a Cock tail of laws including the Companies act, Income Tax Act, VAT Act

• The Industry is characterized by many different players. Currently known institutions financing assets are about 8 commercial

Banks and other independent leasing institutions.

• Banks are offering a cocktail of structures ranging from leases as well as term loans. • There is no statistics to verify the size of the leasing market and this is because the different players are not willing to share

their data

• Most of the institutions still offer balance sheet lending for finance leases as opposed to Cash flow lending which is the core of lease analysis.

• The banks offering lease transactions require the lessees to put an initial capital outlay ranging typically from 10% to about 35% of the equipment cost

• Lease repayments are structured over a 3 year period but to some extent range to about 5 years.

• Lessors have maintained good relationships with suppliers because this has proved to be a good source of business.

• There is a drive to tap into the Government leasing programmes. ULA has started sounding the drums and we hope that Gov’t will take the heed.

• The Courts of law are still “green” in the areas of leasing and so there is a need to fast track the leasing law so that the boundaries between Lessees and Lessors are well defined.

Industry Practice in Uganda................

• The repossession process is hitherto ad hoc. Most lessor’s take advantage of Court bailiffs, police and internal staff.

• The Lessee’s are often misinformed of their rights and obligations. This should clear once the leasing law is enacted into

force.• There are few skilled staff knowledgeable in the leasing business. Banks have began embracing lease training to up skill their

staff.

• The equipment and car industry is characterized by OEM’ representatives. Hence major equipment suppliers are agents of the OEM’s

• There is a dominance of used vehicles in the market. i.e. Total industry sales for new cars is approx. 2,000 vehicles whilst used cars is 50,000 cars. So where do you play in?

?