primer on asian bond markets

TRANSCRIPT

1

Primer on Asian Bond Markets

Hans J. Blommestein, OECD

and

S. Ghon Rhee, SKKU Business School

&

University of Hawaii

A Presentation at the 19th OECD Forum on Public Debt Management

November 25. 2009

2

Fast Growing LC Bond Markets

Average Annual Growth: 20% since 1997

However,

Size has yet to grow further:

Only 6% of World’s LC Bond Market

Growth of LC bond markets is attributed to

government bonds

3

Growing Importance of CB Bills:

Sterilization of Capital Inflow

China Japan Korea East Asia w/o China and Japan

T Bills 7.6% 3.3% 0% 7.6%

CB Bills 27.2% 13.8% 15.4% 23.8% T Bonds 65.1% 82.9% 84.6% 68.6%

As of 1st Quarter 2009

Source: ABM September 2009

4

Growing Importance of CB Bills:

Sterilization of Capital Inflow

As central banks rely on short-term debt instruments for sterilization with developing government bond markets

a. Drive up short-term interest ratesb. Encourage further capital inflow c. Heavy burden on government debt

servicing cost d. Make open market operations

more difficult

5

Cross-Border Investment in

Asian Bonds

Total Cross-Border Investments in LC Bonds

Worldwide: $16.3 trillion

Total Cross-Border Investment in Asian bonds:

$397 billion (less than 2.5%)

Japan: $223 billion

Rest of East Asian Economies: $174 billion

6

Intra-regional Investments

remain small

Source: IMF

Unit: US$ billion

EU15 $195.09 49.16%

United States 70.78 17.83%

Hong Kong 23.24 5.86%

Singapore 17.66 4.45%

Japan 13.13 3.31%

Korea 4.12 1.04%

Philippines 0.73 0.18%

Thailand 0.64 0.16%

Malaysia 0.35 0.09%

Indonesia 0.13 0.03%

Other Economies 71.00 17.89%

World 396.87 100.00%

7

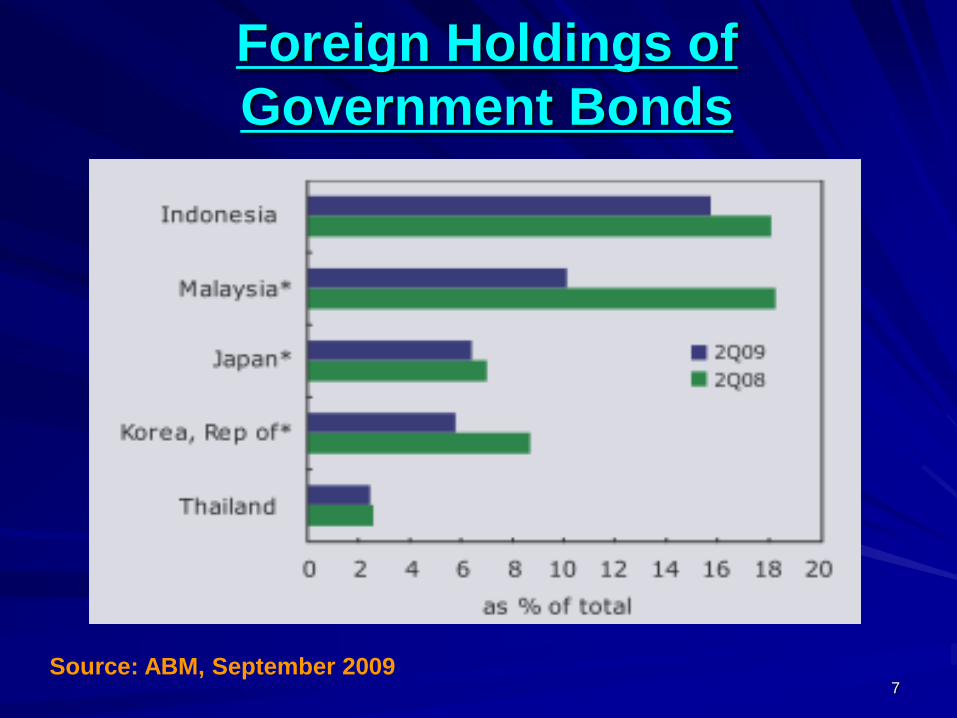

Foreign Holdings of

Government Bonds

Source: ABM, September 2009

8

Liquidity of Government Bond

Market Remains Major Concern

Source: ABM, September 2009

9

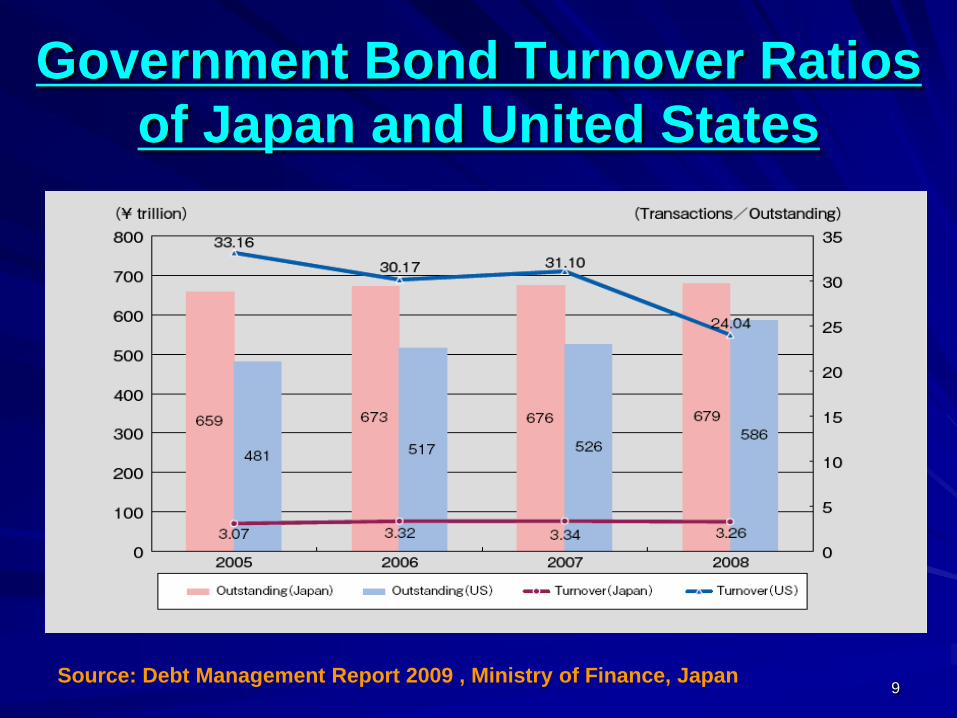

Government Bond Turnover Ratios

of Japan and United States

Source: Debt Management Report 2009 , Ministry of Finance, Japan

10Source: Debt Management Report 2009 , Ministry of Finance, Japan

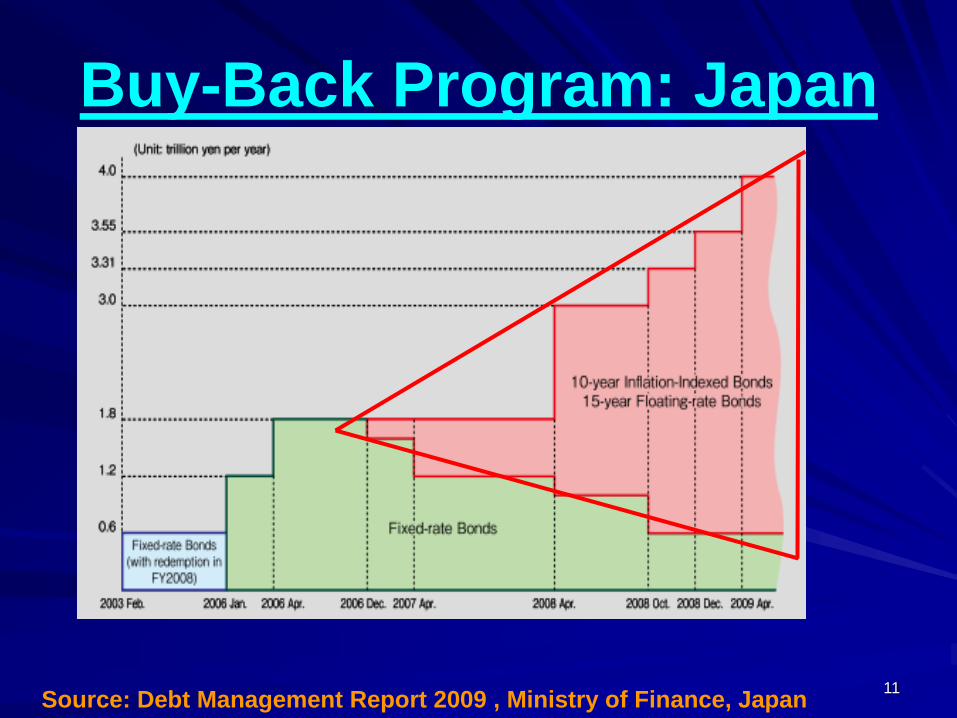

Liquidity-Enhancing Measures

during the Recent Crisis: Japan Buy-Back Program

¥4 trillion in 2009 for 15 Year Floating-Rate

Bonds and 10-Year Inflation-Indexed Bonds

Auctions for Enhanced-Liquidity

a. The same issues as outstanding JGBs were

additionally offered through this system

b. ¥ 6.3 trillion in 2009

Non-Price Competitive AuctionBuy limit for each JGB Market Participant is

raised from 10 % to 15 % for liquid JGBs

11

Buy-Back Program: Japan

Source: Debt Management Report 2009 , Ministry of Finance, Japan

12Source: Ministry of Strategy and Finance, Korea

Liquidity-Enhancing Measures

during the Recent Crisis:

Korea (I) Omnibus Account at ICSD

a. Exemption on Foreign Investor

Registration

b. No Need for Local Custodian

Account

c. OTC Trading Possible among

Foreign Investors

13Source: Ministry of Strategy and Finance, Korea

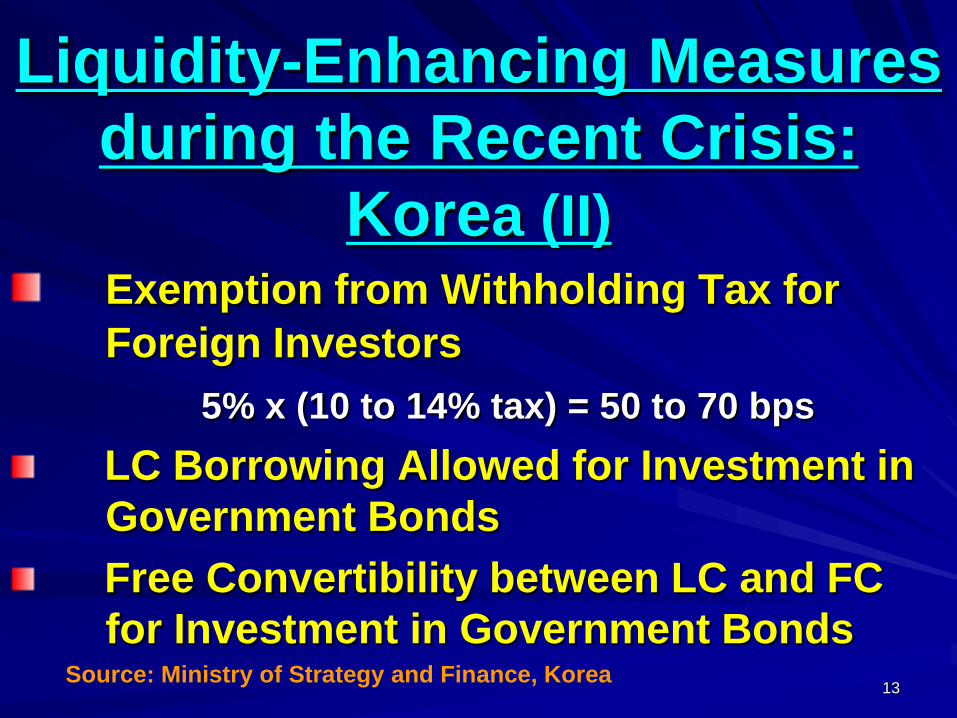

Liquidity-Enhancing Measures

during the Recent Crisis:

Korea (II)Exemption from Withholding Tax for

Foreign Investors

5% x (10 to 14% tax) = 50 to 70 bps

LC Borrowing Allowed for Investment in

Government Bonds

Free Convertibility between LC and FC

for Investment in Government Bonds

14Source: Ministry of Strategy and Finance, Korea

Liquidity-Enhancing Measures

during the Recent Crisis:

Korea (III)Conversion Offer (May 2009)

Swap of off-the-run KTBs with on-the-run KTBs

ETFs linked to KTBs (July 2009)

Buy-Back Program

Size is less than 5% of KTBs

15

Thank You

for Your Attention!