preventive servicing is good for business and affordable

TRANSCRIPT

243

HOUSING POLICY DEBATE VOLUME 18 ISSUE 2© 2007 METROPOLITAN INSTITUTE AT VIRGINIA TECH. ALL RIGHTS RESERVED.

Preventive Servicing Is Good for Business and Affordable Homeownership Policy Michael A. StegmanJohn D. and Catherine T. MacArthur Foundation

Roberto G. Quercia, Janneke Ratcliffe, and Lei DingUniversity of North Carolina at Chapel Hill

Walter R. DavisStatistics New Zealand

AbstractThis article documents the growing importance of preventive servic-

ing—businesspracticesthatemphasizeearlyinterventionindelinquencyanddefaultmanagementpracticesthatalsohelpfinanciallytroubledborrowersavoidforeclosure.Wesuggestthattheloanservicingsideoftheaffordablehousingdeliverysystemmaybeunderappreciatedandundercapitalized.

Weuseadatabaseofmorethan28,000affordablehousingloanstotestseveralpreventiveservicing–relatedpropositionsandfindthatafterwecon-trolforloanandborrowercharacteristics,thelikelihoodthatadelinquentmortgagor within this universe will ultimately default varies significantlyacrossservicers.Thissuggeststhatloanservicingisanimportantfactorindeterminingwhetherlow-andmoderate-incomeborrowerswhofallbehindin their mortgage payments will end up losing their homes through fore-closure.Italsosuggestsaneedforpolicymakerstoincorporatepreventiveservicingintoaffordablehomeownershipprograms.

Keywords:Affordability;Defaults;Mortgageservicing

IntroductionFavorabledemographics,unparalleledeconomicgrowth,andlowinter-

estratescombinedwithanaggressivelysupportivepublicpolicypropelledhomeownershipratesupwardduringthe1990stoahistorichighof69per-cent in2004,with“householdsofallages, incomes, racesandethnicities

HOUSING POLICY DEBATE

244 M.A.Stegman,R.G.Quercia,J.Ratcliffe,L.Ding,andW.R.Davis

joininginthehomebuyingboom”(JointCenterforHousingStudies2005,1). Home Mortgage Disclosure Act records verify an impressive increasein mortgages to low- and moderate-income families—38 percent between1993and1997,comparedwithanincreaseof27percentforloanstohigher-incomehouseholds(Quercia,McCarthy,andWachter2003).Thisgrowthinmortgagestolow-andmoderate-incomehouseholdswassupportedbythewidespreadintroductionof“affordable”mortgageproductsfeaturingflex-ibleunderwriting—including lowdownpayments,higherdebt ratios,andreducedcashreserves—combinedwith theuseofnontraditionalmeansofverifyingcreditworthiness(Querciaetal.2002).

Whatarobusteconomyandliberalizedunderwritingmakepossible,aneconomyindeclinecandiminish.Asthe2001recessiontookholdandwasfollowedbya“job-loss”recovery,thenumberoffinanciallystressedfamiliesgrew,andthenumberofhomeownersspending50percentormoreoftheirincomeformortgage,insurance,andutilitiesincreasedby1.2million(78per-cent)between1997and2003(Lipman2005).Suchhighhousingcostsinevi-tablyleadtomorevolatilepaymentpatternsforlow-andmoderate-incomehomeowners,whosehigherlevelofdebttoincomemakesthemmoresensi-tivethanhomeownersingeneraltoevenmodestdeclinesinthedemandforlabor.Thispartlyexplainswhydefaultratesformoreflexiblyunderwritten,higherloan-to-valueratio(LTV)government-backedloanstendtobesignifi-cantlyhigherthantheyareforconventionalmortgagesasawhole.1Areviewoftheliteratureonthewell-establishedrelationshipbetweenLTVsandpro-pensitytodefaultfoundthat“defaultdependsclearlyonloancharacteristics,mainlyhomeequity”(QuerciaandStegman1992,376).

Efforts to increase the homeownership rate by increasing the numberof new mortgagors can be successful only to the extent that these newhomeownerscanmaintaintheirtenure.AccordingtoarecentU.S.Depart-mentofHousingandUrbanDevelopment(HUD)study,“[P]oliciesthatpro-moteonlytemporaryspellsofhomeownershipwillhavelittleimpactonthenationalhomeownershiprate.Whatisimportantispromotingnewowner-shipspellsthataresustainable”(2004,v).

Ifthe1990swerethedecadeofaffordablehomeownership,thencurrenteconomicrealitiessuggestthatthe“newfrontierinsuccessfullendinginlow-andmoderate-incomecommunities justmaybe inpost-purchaseservices”(Meyer1997,4).Theseservicesincludecollectionsanddefaultmanagement

1Forexample,from1993to2000,therateofforeclosuresforFederalHousingAdminis-tration(FHA)loanswasatleasttwicethatofconventionalloansandthe90-daypast-dueratewasthreetosixtimeshigherforFHAloansthanforconventionalones(HUD2003).

HOUSING POLICY DEBATE

PreventiveServicingandAffordableHomeownershipPolicy 245

strategiesdesignedtokeepdelinquenthomeownersfromlosingtheirhomesthroughforeclosure.Thisarticlesuggeststhatwiththeproliferationofafford-ablelendingproducts,whichlayermortgagedefaultrisks,theservicingsideoftheaffordablehousingsystemhasbecomemorecriticalthanever.

Afterdiscussingwhatwemeanbypreventiveandsmart servicing,wewillreviewtheeconomicsoftheloanservicingbusiness.Then,usingadata-baseofmorethan28,000affordablehomeloansthatwearecollectingaspartofamultiyearevaluationofasecondarymortgagemarketdemonstra-tionundertakenbySelf-Help,a leadingcommunitydevelopmentfinancialinstitution,weempiricallytestseveralservicing-relatedpropositions:

1.That affordable mortgages can have a high likelihood of recoveryfromearly-stagedelinquency

2.Thatcertainborrower,loan,property,andpaymenthistoryattributesaffectcurerates(curemeansthattheborrowermakesupthemissedpayments)

3.Thatloanservicingplaysaroleindeterminingtheultimateoutcomeofdelinquencyspells

Preventive and smart servicing Inthisarticle,weusetheterm“preventiveservicing”todescribedelin-

quencymanagementpracticesthatemphasizeearlyinterventionanddefaultmanagementpracticesthathelpfinanciallytroubledborrowersavoidfore-closure(Oliveretal.2001).2“Smartservicingtools”meanstechnologiesthatenablepreventiveservicing,including“modelingsoftwareandscriptedmenuoptionstoengagecollectorandborrower”(Fields2001,27). Intheeffec-tivemanagementofnonperformingloans,collectionseffortsaresupportedbysmartsystemsthatprioritizecollectionscallsandidentifylossmitigationpathwaysappropriatetoeachcase.

Thekeytoeffectiveandefficientpreventiveservicingisinknowingwhichborrowerstocontactatwhichtime,andsuccessinavoidingforeclosureoftendepends on early intervention. For example, in a 2001 review of FederalHousingAdministration(FHA) loans,oneservicerhadasuccessrate thatexceeded45percentforworkoutsprocessedwithinthefirsttwomonthsofdelinquency,butonlya10percentsuccessrateiftheworkoutwasprocessed

2Forafulldiscussionofalternativestoforeclosure,seeCuttsandGreen(2005).

HOUSING POLICY DEBATE

246 M.A.Stegman,R.G.Quercia,J.Ratcliffe,L.Ding,andW.R.Davis

aftersevenmonths(HUD2002).Deloitte,theconsultingfirm,estimatesthatorganizationsthatadoptwhatitreferstoaspredictiveanalyticsandotherpreventiveservicingpractices“canenjoysubstantialbenefitsincludinga20percentimprovementinthedollarscollected,reductionsofupto30percentinoveralloperatingcosts,anddeclinesofupto20percentinrollrates(oraccounts rolling to the next stage of delinquency)” (Caldwell and Jordan2006,2).However,engagingadelinquentmortgagorquicklyissometimeseasiersaidthandone.Asacaseinpoint,whenCountrywideMortgagetriedtohelp300seriouslydelinquentChicago-areahomeownersavoid foreclo-sure,only38responded(Sichelman2001).Frustratedbysuchlowresponserates,thecompanysenta“teamoflossmitigationspecialists”tomeetwith61borrowers,and“despitethefactthat32ofthesecustomerswereinthelatestagesofforeclosure,Countrywidewasabletocreaterepaymentpro-gramsfor59oftheresidents”(Mozilo2000,18),dramaticallyunderscoringthepowerofpreventiveservicing.

Affordable mortgages, smart servicing, and mortgage economics Lendingprogramsdesignedtoincreasethehomeownershiprateforlow-

andmoderate-incomeborrowersthroughliberalizedunderwritingguidelinesalsoincreasethelikelihoodthatthosehomeownerswilldefault.Beginninginthelate1980sandcontinuingthroughthe1990s,lenders,mortgageinsur-ers,andsecondarymarketingagenciesrespondedtopolicygoalsandregula-torypressuresbyrelaxingtheguidelinesthatsometimesbarredlower-incomehouseholdsfromqualifyingforamortgage.Theseguidelinesevolvedtomin-imizetherequireddownpayment,reducetheborrower’sassetandcontribu-tionrequirements,raisetheallowablemonthlydebtpaymentsatparticularincomelevels,andloosencreditworthinessstandards.Whilethesefeaturesallowmorehouseholds tobuyhomes, theycan increase the riskofdelin-quencyanddefaultby40to400percent(Steinbach1995).Becauseoftheincreasedincidenceofdefaultandbecauselow-andmoderate-incomebor-rowerstypicallyhavelittlefinancialcushiontofallbackonintheeventofaneconomicsetback(BakuandSmith1998),callsto“implementhomebuyersupportstructuresdesignedtoensurelong-termhomeownership”pointthewaytopreventiveservicingmeasuresforthesehomeowners(Steinbach1995,39).

The smart servicing tools now in use canbe particularly effective fortheseborrowers.Thecombinationofearlyintervention,thetargetingofbor-rowersmostatriskofdefault,andworkoutoptionsthatallowborrowerstorecoverfromfinancialsetbacksallhelpservicersfocusresourcesonthose

HOUSING POLICY DEBATE

PreventiveServicingandAffordableHomeownershipPolicy 247

loansthatcanbenefitthemostfromintervention.Ineffect,flexibleguidelinesandpreventiveservicinghavethesameultimateaim:tobolstertheranksofhomeowners.

Becauseofthehighcostofdefaults,smartandpreventiveservicinggen-erallymakesgoodbusinesssenseforanymortgage.Forexample,theFHA-expectedlossperdefaultedloanrangesfrom30percentto40percentoftheloanamount,3 thussuggestingthatavoidingforeclosurecansaveasmuchas$60,000to$80,000onthemaximumFHAloaninstandard-costareas.Thoughmostconventionaloraffordablemortgagedefaultsdonotend inforeclosure,thosethatdocanbequitecostly.Forexample,CuttsandGreenciteFocardi’sfindingsthatforasampleofloansthatwentthroughthefullformalforeclosureprocess,thetotalcost,includinglostinterestduringdelin-quency, foreclosure costs, and disposition of the foreclosed property, ran$58,759andtookanaverageof18monthstoresolve,whilevoluntarytitletransferalternatives toforeclosurehadaveragecosts inexcessof$44,000andtooknearlyoneyeartoconclude(2005,352).

Ina1996article,AmbroseandCaponeillustratedhowinrisingmarkets“savingstothemortgageinvestorsandinsurersfrompreventingoneforeclo-sure(asuccessfulworkout)arelargeenoughtopaytheaddedcostsoffourworkouts”andthateveninsoftermarketswherepricesaredecliningbyasmuchas5percentayear,onesuccessfulworkoutcouldoffset thecostofmorethantwoadditionalworkouts(citedinCaponeandMetz2003,10).Sinceaffordablehousingmortgageswiththeirtypicallysmallerequitycush-ionsaremorelikelytodefault4andtoresultingreaterlossseverityfortheinvestororinsurer,thiscostbenefitequationshouldbeevenmorecompellingfortheaffordablesegment.

Thecostsofdefaultarelargelybornebytheholdersofcreditordefaultrisk (e.g., Fannie Mae, Freddie Mac, FHA, and mortgage insurers); thus,theystandtobenefitthemostfromtheuseofsmartandpreventiveservicing.Becausetheservicerhastherelationshipwiththeborrower,however,inves-torsandinsurersmustlooktothatentitytoimplementtheseloss-minimiz-ingpractices,whichareoftenlaborintensiveorrequireinvestmentsinnewtechnologiesandtraining—orboth.

3Forexample, the2005analysisofFHA’sMutualMortgage InsuranceFund indicatesthattheaveragelossseverityrateexperiencedbyFHAfrom2000to2004rangedfrom30.59percentonstreamlinedrefinanceadjustable-ratemortgagesto48.76percenton15-yearnon-streamlinedrefinancefixed-ratemortgages.From2002to2003,theaveragelossrateperclaimwas35percent(HUD2005).

4Forexample,amortgageinsurancecompanyfoundthatloanswithdownpaymentsof3percentoftheborrower’sownfundshadtwicethedefaultrateofloanswitha5percentdownpayment(Steinbach1995).

HOUSING POLICY DEBATE

248 M.A.Stegman,R.G.Quercia,J.Ratcliffe,L.Ding,andW.R.Davis

Servicer economics reliesonmaximizingefficiency,withconsolidationdrivenbytechnologyandeconomiesofscale.Between1989and2005,theshareofthemarketheldbythe5largestservicerswentfrom7percentto42percent,withthe25largestholding69percentofthemarket(InsideMort-gageFinance2006). Inthedrivetotakeadvantageofeconomiesofscale,productivitygainedsignificantly,fromaround700loansservicedperdirectfull-timeemployeein1992to1,229in2000,anincreaseofabout60percentinlessthan10years.Directservicingcostsperloanperyear,whichwere$80to$90inthelate1980s,wereshavedtolessthan$50in2000(Oliveretal.2001).

Ontherevenuesideoftheequation,thelargestsinglesourceofrevenueisservicingfees.Thestandardfeeforconventionalconforminghomeloansisonequarterof1percent(25basispoints)oftheoutstandingbalanceoftheloanannually.Ongovernment-backedloans,thefeeisgenerally44basispointsannually(Muolo2000),areflectionofloweraverageloanbalance,morereportingrequirements,andhighercostsassociatedwithservicingFHAandU.S.DepartmentofVeteransAffairs(VA)loans.

Some previous research indicates that servicing methods can make adifferenceinoutcomesforsubprimeborrowers.Alargeservicerexamined23,000 delinquency transitions over nearly four years—from current todelinquent,fromdelinquenttoforeclosureortocure,andfromforeclosuretocure—insubprime loansfromseveraldifferentservicers (Sjaastadetal.2005).Theanalysisvalidates thepredictivenessof such factorsas currentFICO(Fair,Isaac&Company)score,LTV,loanage,andpaymenthistoryforeachtransitiontype,yetaftercontrollingforthesefactors,theauthorscon-cludethat“servicerscanhavespecific,strongimpactsontransitionratesanddelinquencyduration times” in subprimemortgages (Sjaastadetal.2005,16).Thisservicereffectseemsreasonable,foroncealoanisclosed,theser-vicerhasanongoingrelationshipwiththeborrowerandisinapositiontoinfluenceoutcomes.

Toillustrate,whenaloanreaches60or90daysdelinquent,oneservicerpromptlyreferstheloantoaforeclosureattorney,asstatelawallows,andinsists that the borrower pay full arrearages and fees to halt foreclosure,somethingafinanciallytroubledborrowerusuallycannotdo.Anotherser-vicercontactstheborrower,exercisesforbearance,acceptspartialpayments,andactivelyhelpsformulateanalternativetoforeclosure.Inthefirstcase,thedelinquentloanquicklytransitionstoforeclosure,whileinthesecond,theborrowerremainsintheearly-delinquencystageuntileithercatchingupordefaulting severalmonths later.Delinquent loan servicingpractices aredifferentiatedbysuchfactorsasallocationofresources(bothstaffandtech-

HOUSING POLICY DEBATE

PreventiveServicingandAffordableHomeownershipPolicy 249

nology),theprocessinplacefornonperformingloans,investorpreference,andorganizationalcommitmenttolossmitigation,manyofwhicharecon-sideredinthisarticle.

Our literaturereviewfoundfewempiricalstudiesof theeconomicsofservicing affordable mortgage portfolios—those characterized by below-average loan balances and disproportionately large numbers of low- andmoderate-incomeborrowers—but there are scattered indications from theresearchandourexaminationoftheSelf-Helpportfolioofthespecialchal-lengesposedbythismarketsegment.

Over 30 years ago, the relationship between average loan size anddiscounted, net servicing revenue was found to be positive and nonlinear(McConnell1976). In2001, theaverageconventionalmortgage loanbal-ancewas$120,393(HMDA2001).TheaverageloanbalanceinSelf-Help’sprogram is substantially lower: $79,800. Thus, the annual servicing feesgeneratedontheaverageSelf-Helploanare34percentlowerthanthefeesfortheaverageconventionalloan($200versus$301).However,latefeesgener-atedby the increased incidenceofdelinquencymayoffset thisdifferentialsomewhat.5Morerecently,LindaSimmons,aStratmorGrouppartner,ana-lyzedalargepoolofmortgagedatafrom1999to2002andfound“astrongrelationship between portfolio composition and servicing costs” (DeZube2003,48).TheStratmorGroupfoundthatconventionalconformingloanscostanaverageof$48ayearforcoreservicingoverthestudyperiod,“whilegovernment-backedloanscameinat$98”(DeZube2003,48).Borrowerswho have affordable conventional loans have loan sizes and risk profilesmore like thoseofgovernment-backedborrowersandmay thereforehavesimilareconomics.

Onthepositiveside,affordablemortgagesmayexhibitslowerandlessvolatileprepaymentpatterns.Intheiranalysisoftheprepaymentratesasso-ciatedwithpoolsofFHA-insuredloans,DengandGabriel(2002)foundthatborrowerswithlowercreditscoresandhigherdefaultriskswerelesslikelytoprepaythanborrowerswithbettercredit.BytrackingFreddieMacloanspurchasedfrom1993to1997throughtheendof1999,VanOrderandZorn(2004) found that low-income and minority borrowers prepay mortgageloans less rapidlywhenconditionsare favorable forrefinancing. If indeedlow-andmoderate-incomemortgagesprepaymoreslowlythanothertypesofconventionalmortgages,theirservicingrevenuestreamwillbelongerandpotentiallymorevaluable.

5Latefees, incurredforpaymentsreceivedafterthe15thofthemonth,aretypically3percent to5percentof thepayment (sources includeCaliforniaRealEstateCenter.com2006andMortgageNewsDaily.com2005).

HOUSING POLICY DEBATE

250 M.A.Stegman,R.G.Quercia,J.Ratcliffe,L.Ding,andW.R.Davis

Tosummarize,thebusinesschallengesinservicingmortgagesoriginatedlargelyforCommunityReinvestmentAct(CRA)creditarecompoundedbytheirsmallersizeandhigherdelinquencyanddefaultrates.Althoughthesechallengesmaybeoffsettosomeextentbyslowerprepaymentpatterns,wearguethatthemortgageservicingindustryneedstoimplementthemosteffi-cientdefaultmanagement systemspossible tokeep costsdownwhile stillmeetinginvestorrequirementstominimizelosses.Webelievethatconsistentwith thepublicpolicygoalof sustaininghomeownership, investor/insurerandservicergoalsmightbealignedinthedevelopmentofsmartservicingtools.

The evolution of smart servicing tools6

Advancedinformationtechnologieswerefirstappliedtocollectionman-agementinthecreditcardindustryduringtheearly1990sasthepercent-ageofthosemakingminimumornomonthlypaymentsswelledalongwithaggregatedebtlevels.Thissectorwasafertiletestinggroundfordecisioningsystems that analyze thebehaviorpatternsof delinquent cardholders anddeterminewhois least likelytopaywithoutearlyintervention(Waggoner2002).

In a parallel fashion, first-generation automated mortgage servicingmodels,introducedinthemid-1990s,identifydelinquentmortgageaccountsthatarelikelytobenefitmostfromearlyintervention.Thesetools,suchasFreddieMac’sEarlyIndicatorSM(EI)andFannieMae’sRiskProfiler®(RP),useacombinationofborrowerinformationcontainedinthemortgageappli-cation, loan-specificpaymentpatterns,andupdatedcredit informationontheborrower(FannieMae2005a;FreddieMacn.d.).Personalcontactwiththeborrowerisnotrequiredtoproduceapropensityscore(Stanton2001).Thisapproach,whichoptimizesservicers’collectionbudgetsbyprioritizingcallschedules,isonlythefirstpartofsmartservicingsystems.

The second phase applies a combination of scripting systems such asFreddieMac’sEarlyResolutiontoaidservicerswhentheycontactborrowersandanalytic toolssuchasGE’smortgage insurancecompany’sLossMiti-gationOptimizer, FreddieMac’sWorkoutProspector®, andFannieMae’sWorkoutProfilerTMtoassesstheviabilityofforeclosurealternativesineachcase.Thesetoolsessentiallyapplyconsistentunderwritingmethodologytokeepborrowersintheirhomesbyassessingwhatoneindustryexpertreferstoasthe“threeCs”—capacity,collateral,andcommitment(Kehr2005).

6ThissectionisbasedlargelyonadraftpreparedforthisprojectbyStevenHornburg.

HOUSING POLICY DEBATE

PreventiveServicingandAffordableHomeownershipPolicy 251

Because investorsand insurersstandtogain themost fromaggressivelossmitigation,theyoftenservedascatalystsfortheinitialintroductionofutilitiesandtechnologyinthisareaandinvestedheavilyinthem.Today,suchtoolsareincreasinglybeingdevelopedorenhancedbythird-partysoftwarecompaniesandarebeingintegratedmoredirectlyintotheservicers’systems(Kehr2005).Whilemanyofthesetoolsgohandinhand,theycanbeusedindependentlyandwithmortgagesofmanydifferenttypes.

Havinglauncheditsownlossmitigationprogramin1996,FHAiscom-mittedtopreventiveservicingaswell.By2005,FHAofficialsaffirmedtheirbeliefthatthelossmitigationprogram“isbecomingthedominantapproachtoaddressadefault”(“FHACites90,000LossMitCases”2005,91).Thecost-effectivenessofpreventiveservicingisevident.In2002,FHApaidout$5.5 billion in claims on 64,000 foreclosures, while paying just $98 mil-liontohelpkeep73,000financiallytroubledborrowersintheirhomeswithrecastloans(Harney2002).By2005,thenumberoflossmitigationclaimspaid rose to90,000,withFHAavoidinganestimated$2billion in losses(“FHACites90,000LossMitCases”2005).

Instead of developing its own tools, FHA relies on servicers to applycommerciallyavailable smart servicing tools to its loans. Italso institutedasystemofscoringservicersandawardsfinancial incentives—$27millionin2005—foroutstandinglossmitigationperformance(“FHACites90,000LossMitCases”2005.FHAisnottheonlyinvestortoscoreorpayservicersforusingalternativestoforeclosure.FreddieMac’sServicerPerformancePro-filesusesuchindicatorsascurerates,workouts,andtimelinessofforeclosureto benchmark servicers (Melchiorre 1999). One servicer reported earning$25,000permonthfromlossmitigationincentives(O’Connor2003).Finan-cialincentiveshaveledsomeservicerstoseetheir“lossmitigationdepart-mentsmovefromcostcenterstoprofitcenters”(HUD2002,3).

Evidently, smartandpreventiveservicinghasbeenfinanciallyeffectivefor investors and insurers and even for servicers.Buthoweffectivehas itbeeninsustaininghomeownership?Throughaggressiveoutreachfeaturingacombinationofpreventiveandsmartservicing,FannieMaeanditsloanservicingpartnershelpednearly34,000financiallystrappedborrowersavoidforeclosurein2004alone;accordingtoKehr(2005),morethan92percentreceivedworkoutsthatallowedthemtostayintheirhomes.7Thesuccessoflossmitigationeffortsisoftengaugedbytheworkoutratio,whichgenerally

7Notallworkoutsresultinretainingthehome;otherstrategiesusedtoavoidforeclosureinvolvetheborrower’sgivinguporsellingthehomevoluntarily,suchasinthecaseofdeeds-in-lieuandpreforeclosuresales(Cornwell2003).

HOUSING POLICY DEBATE

252 M.A.Stegman,R.G.Quercia,J.Ratcliffe,L.Ding,andW.R.Davis

comparesthenumberofloansthatreceivesuccessfulworkoutswiththetotalnumberofloansthateithergetworkoutsorbecomerealestateowned(whenthetitleistransferredtothelenderthroughforeclosureorinlieuofforeclo-sure).Detailsofthismeasurecanvary;forexample,FreddieMacexcludesrepaymentplansintallyingworkouts,butFannieMaeincludesthem.

From1996to2000,FannieMae’sworkoutratiorosefrom32percentto53percent,whileFreddieMac’srosefrom26percentto38percent(Cordell2001;Cornwell2003).FHA’sworkoutrationearlydoubledfromlessthan15percentinlate1997toalmost30percentattheendof1999(Herbert,Gruenstein, and Burnett 2000) and over 50 percent by 2002 (Cutts andGreen2005).Moststrikingly,thenumberofFHAproblemloansthatwereresolvedusingahomeretentionworkoutincreasedsome88times,from770in1997to68,003in2003.AfterintroducingitsLossMitigationOptimizer,GE’smortgage insurancecompanyreportedalmostdoublingitscureratio—theshareofallloansforwhichthecompanyreceivesnotificationofdelin-quencybutthatlaterbecomecurrent(Venetis2001).8Afterimplementingacollectionscoringtool,oneservicerreporteda50percentincreaseinFHAandVAworkouts (Abraham1999); another claims thatworkouts tripledin the initialperiodafter a“BackInTheBlack” lossmitigation systemwasimplemented(O’Connor2003).From2000to2004,145,000FreddieMacborrowers,or“130familieseverybusinessday,”werekeptintheirhomeswithloanmodifications,repaymentplans,andforbearance(“Now,‘Afford-ableServicing’”2005,1).

PerhapstheclearestevidencecomesfromCuttsandGreen’s2005exami-nationofFreddieMac–ownedloansthatwentfrom60to120daysdelin-quentbetweenJanuaryandSeptember2001.Followingtheseloansfor18months,CuttsandGreen found thatusinga repaymentplan lowered theprobabilityoffailureby80percentforborrowerswithhigherincomesandby68percentforlow-andmoderate-incomeborrowers.

Clearly,then,thesetechnologiesandtoolshavehadanimpressiveimpactonthewaynonperformingmortgagesareservicedandonservicers’abilitytocost-effectivelykeepmoreborrowersintheirhomes.

Servicing issues and Self-Help data Inthissection,weuseauniquedatasetofmorethan28,000mortgages

madetolow-andmoderate-incomeborrowerstoexploretheimpactofvari-

8Notificationtypicallycomesat90days,however,itcouldbesooner,forexample,inthecaseofmonthlypaypolicies.

HOUSING POLICY DEBATE

PreventiveServicingandAffordableHomeownershipPolicy 253

ousfactorsondelinquencytransitions(fromdelinquenttoseriouslydelin-quentortocure)andtoisolatetheeffectsofservicing.

TheSelf-Helpsecondarymarketdemonstrationprogramisamultibil-lion-dollar initiativedesignedtoexpandhomeownershipopportunities forcreditworthy, low-income, low-wealth individuals who are not effectivelyservedbytheconventionalmarket.TheprogramisapartnershipamongtheFordFoundation;theCenterforCommunitySelf-Help,aNorthCarolina-basedcommunitydevelopmentorganization;andFannieMae,asecondarymarketentity.Thegoaloftheprogramistoprovidetangibleevidencethatlow-wealthborrowersare“bankable”andthatsecondarymarketactorscansignificantlyexpandtheirpurchaseofaffordablehousingloanswithoutcom-promisingeithertheirbalancesheetortheirsafetyandsoundness.

WithaFordFoundationgranttounderwriteasignificantportionofthecreditrisk,Self-Helppurchasesaffordablemortgages(CRAloans)thatcouldnototherwisebereadilysoldinthesecondarymarketbecauseoftheirper-ceivedhigherrisk.Self-HelpthensellstheloanstoFannieMaewhileretain-ingfullrecourse,meaningthatSelf-HelpisobligedtocoveranylossesFannieMaemayincurasaresultofdefaults.Self-Helpcontractswithparticipatingmortgagelenderstooriginateandsubservicetheloans.

Self-Help mortgage products feature flexible underwriting and typi-cally includeoneormoreof the followingfeatures:a lowdownpaymentornoneatall,lowerreserves,higherdebt-to-incomeratios,borrowerswithspottycreditrecordsornoestablishedcredit,andwaiverofprivatemortgageinsurance.

Dataforouranalysiscomefrom28,131loansthatweremadetolow-andmoderate-incomemortgagorsandpurchasedbySelf-HelpbeforeJanu-ary1,2003;theaverageoriginalbalancewas$79,800.Foreachloan,thedataincludeafullsetofloancharacteristics,someborrowercharacteristics,andthecompletepaymenthistoryfromthetimeofpurchasebySelf-Help.9

ThedatabaseisbeingcompiledaspartofourongoingmultiyearevaluationofSelf-Help’sprogramwiththeaimof

1.Measuring loan performance by tracking delinquency, default, andforeclosureratesoverthecriticalfirstfiveyearsofthemortgageterm

9Asmallnumberofmonthsaremissingfromthepaymenthistoryfile.Wehavedataon580,276loan-months,with532loan-monthsmissing.Weuseanalgorithmtofillinthelikelyvaluesforthemissingmonths.Forexample,ifmonth1waspaidontimeandmonth3waspaidontime,weassumethatmonth2wasalsopaidontime.Similarly,ifmonth1waspaidontimebutmonth3showsa60-daydelinquency,weassumethatmonth2waslate.Inthefewinstanceswhereaprecisedeterminationwasnotpossible,weimputedmonthssuchthatanydelinquencyspellwouldbeasshortaspossible.

HOUSING POLICY DEBATE

254 M.A.Stegman,R.G.Quercia,J.Ratcliffe,L.Ding,andW.R.Davis

2.Documentingthesocialandeconomicimpactsofhomeownershiponborrowers

3.Assessing to the extent practicable the impacts of the program onneighborhoodconditionsandhousingmarketdynamics

Aspartoftheevaluation,wearebuildingapanelofover2,700hom-eowners(asof2005)whoarebeinginterviewedinsixannualwavesrunningthrough2008.Someofthedescriptivedatacitedlaterinthearticlearefromourbaselinephoneinterviews,whichwereconductedbetweenlate2001and2003.Thisbaselinesurveygatheredinformationonthehomepurchaseandmortgageprocess,alongwithdemographicandeconomicdata.Coreques-tionsarerepeatedeveryyear,whiledifferentmodules(socialcapital,wealthandassets,financialbehaviorsandattitudes,senseofcommunity,andmoversurvey)areusedindifferentyears.

Who are these homeowners?

DemographicandothercharacteristicsoftheborrowersAlmost40percentofSelf-Helpborrowersareminoritiesand44percent

arewomen.Anestimated16percentaresingleparents.10Itisimportanttonotethathalfhadincomesbelow60percentofthelocalmedianhouseholdincomewhentheyclosedontheirloans(table1).Moreover,alittleover40percentofallSelf-HelpfamilieshadFICOscoresoflessthan660ornocreditscoreatall.ComparedwithborrowerswhoseconformingloanswereboughtbyFannieMaein1999,Self-Helphomeownersareabouttwiceaslikelytobeminorities,almostfivetimesaslikelytohaveincomesbelow60percentoftheareamedianincome,asdefinedbyHUD,andtwoandahalftimesaslikelytobefemale(CenterforCommunitySelf-Helpn.d.).

Datafromourbaselinesurveyof3,727Self-Helphomeowners,whichoccurredgenerallyaround12to24monthsafterhomepurchase,allowustolookatthefamilyandemploymentsituationsoftheseborrowersingreaterdetail.Asarule,Self-Helpfamilieshaveastrongcommitmenttotheworkforce; more than three-quarters of all sampled households with marriedcouplesorpartnershavetwowageearners.Moreover,16percentofallbor-rowersand10percentofallspousesorpartnerswhoworkhavemorethanonejob,includingpart-time,weekend,andeveningwork,and96percentofoursurveyedborrowersworkatleastfull-time(35ormorehoursperweek).Almost30percentaverageatleast50hoursofpaidworkperweek.

10ThisfigureisanestimatefortheentirepopulationofSelf-Helpborrowersbasedonthebaselinepanelsurvey.

HOUSING POLICY DEBATE

PreventiveServicingandAffordableHomeownershipPolicy 255

Table 1. Self-HelpLoans:DescriptiveStatisticsforLoansPurchasedbeforeJanuary1,2003(N=28,131)

Variable Percentage Median

Creditscore Nocreditscore 3.5 FICO620orlower 17.2 FICO621to660 21.0 FICO661to720 30.4 FICOabove720 28.0

Loancharacteristics LTV(%) 97.0 Back-endratio(%) 36.7 Ageofloanatpurchase(months) 11

Borrowercharacteristics Femaleborrower 44.0 Blackborrower 21.3 Hispanicborrower 16.6 Singleparenta 15.9 First-timehomebuyer 43.8 Incomeatorigination $29,472 IncomeasapercentageofAMI 59.7

Postpurchaseemploymenthistorya Currentunemployment(borrower) 3.1 Currentunemployment(spouse) 8.3 Currentlymorethanonejob(borrower) 16.1 Currentlymorethanonejob(spouse) 10.4 Anyunemploymentsincepurchase(borrower) 16.8 Anyunemploymentsincepurchase(spouse) 59.3 Currentlyworksfull-time(borrower) 95.9 Currentlyworksmorethan50hoursperweek(borrower) 27.8 Two-wage-earnerhouseholds 75.9 (amongmarried/partneredhouseholds)

Geography Rural 20.5 NorthCarolinaborrower 40.1 Californiaborrower 12.9 Oklahomaborrower 7.0 SouthCarolinaborrower 6.0 Ohioborrower 4.3 Virginiaborrower 3.9 Georgiaborrower 2.7 Texasborrower 2.6 Floridaborrower 2.5 Illinoisborrower 2.3 Otherstates 15.6

Source:Self-Helpdatabase,panelsurvey,andauthors’calculations.aThisestimateisbasedondatacollectedaspartofthebaselinepanelsurvey,afive-yearstudyofover3,700Self-Helpborrowers.AMI=areamedianincome(medianincomeofthemetropolitanstatisticalarea[MSA]orthestatefornon-MSAareas).

HOUSING POLICY DEBATE

256 M.A.Stegman,R.G.Quercia,J.Ratcliffe,L.Ding,andW.R.Davis

Despitethefactthatourinterviewswereconductedinthemidstoftheeconomicslowdown,wefoundlowunemploymentratesamongallborrow-ers(3.1percent),althoughmuchlargernumbersofborrowers(16.8percent)andtheirspousesorpartners(59.3percent)hadexperiencedatleastonespellofjoblessnesslastingaweekormoresinceclosingontheirloans(table1).11

Thephenomenonofhighlabormarketvolatilityandjobchurningamonglow-andmoderate-incomeborrowersduringperiodsofeconomicdecline,characterizedbycutbacksinovertimeandthelossofsecondjobsandpaidspousalwork,contributestohigherratesoflateandmissedmortgagepay-mentsamongalllow-andmoderate-incomefamilies.Thosewithsinglewageearnersareparticularlyaffected.Becausethesefamiliesaremorelikelythanotherstoloseincomeintermittentlyfromperiodicjobcutbacksandlayoffs,theyarealsomorelikelythanhigher-incomeborrowerstofallbehindintheirloanpaymentsandaremorelikelytohaveahardertimecatchingup.Thisputsevenmorepressureonservicerswhoseportfolioscontainlargenumbersofaffordablemortgagesandexplainswhytechnologythatenablesservicerstoidentifywhichborrowersaremostlikelytofallfartherbehindoncetheymissasinglepaymentcanbeavaluabledefaultmanagementtool.

ThedelinquencyexperiencesofSelf-HelpmortgagesAsofMarch2005,about2percentofallloansintheSelf-Helpportfo-

liohad reached foreclosure. In fact, comparedwith industrybenchmarks,Self-Help loans perform quite well. As of the first quarter of 2005, 3.03percentofSelf-Helploansweremorethan90daysdelinquentorinforeclo-sure,comparedwith1.89percentforallloans,5.15percentforFHAloans,and5.23percentforsubprimeloans(MortgageBankersAssociation2005).TakenincombinationwithSelf-Help’shistoricallossseverityrateofjust26percentoftheoriginal loanbalancecomparedwith37percentforsimilarFHAloans(HUD2005),thisperformancesuggeststhatSelf-Help’slossmiti-gationeffortsareeffective.

Consistent with preventive servicing’s emphasis on early intervention,only10percentofloansthatbecameatleast30daysdelinquenteventuallyreached foreclosure, comparedwithalmost30percent thatbecame60ormoredaysdelinquent.Forthosegoingover90days,morethan40percentreachedforeclosure.

Becausethisarticledealswithservicinganddefaultmanagementratherthanwithoriginationsandtheassessmentofinitialcreditrisk,wearemore

11Postpurchasejoblessnessamongspousesincludesthosewhoarenotinthelaborforce.

HOUSING POLICY DEBATE

PreventiveServicingandAffordableHomeownershipPolicy 257

interestedinexaminingtheoutcomesofSelf-Helploansoncetheybecome30dayspastduethanwearewithdeterminingthefactorsthatcauseloanstobecomedelinquentinthefirstplace.(TheanalysisofinitialdelinquencyandoverallSelf-HelploanperformanceisthesubjectofotherpapersproducedbytheCenterforCommunityCapitalism[Querciaetal.2002,forexample].)SincethefailurerateforaSelf-Helploanthatisover90daysdelinquentismorethanfourtimeshigherthanitisforonethatis30daysdelinquent,wefocusedonthetransitionswithinthisperiod.Fromthepaymenthistory,wewereabletodeterminewhenaloanbecamedelinquent,generatinga“delin-quencyspell.”BetweenSeptember1998andDecember2004,wetrackedtheperformanceof28,131Self-Help loansoriginatedbeforeDecember2003.Only21.2percent—or5,969loans—everexperiencedadelinquencyspell:15.7 percent experienced only relatively mild delinquency (a delinquencyspellof30or60days),and6.7percentexperiencedatleastonespelllastingatleast90days.

Theservicingchallengeassociatedwithaffordablelendingcanbemoregraphicallyillustratedbyexaminingthenumberofdelinquencyspellsgen-eratedbyeachloan.Astable2shows,alargeshareoftheever-delinquentloans(2,564outof5,969)generatedonlyonedelinquencyspelleach,last-inganaverageof2.5months,beforecuringordefaulting.Theremainderof these loans experienced two or more separate delinquency spells. Thisincludes1,403repeatedlydelinquentloanswithfourormorespells.Whileaccountingforabout5percentofallloans,thisgroupgeneratedoverhalfofalldelinquencyspells.

Adelinquencyspellcanbecuredorprogress toa90-daydelinquency(hereinafterreferredtoas“default”).Sincemostdelinquencyspellsresolve

Table 2.Numberof30-DayDelinquencies

Numberof AverageLength Loans Percentage ofDelinquency

Neverdelinquent 22,162 78.8

Onlyonedelinquency 2,564 9.1 2.50months

Twodelinquencies 1,246 4.4 2.66months

Threedelinquencies 756 2.7 2.57months

Fourdelinquencies 477 1.7 2.73months

Fiveormoredelinquencies 926 3.3 2.46months

Total 28,131 100 2.55months

Source:Self-Helpdatabaseandauthors’calculations.

HOUSING POLICY DEBATE

258 M.A.Stegman,R.G.Quercia,J.Ratcliffe,L.Ding,andW.R.Davis

12SincesomeloanswereoriginatedafterSeptember1998,theaveragelengthofobserva-tionforallloansisabout53months.

13Becausetheendingdateoftheobservationperiodwasarbitrarilydetermined,thestatusof“still30or60daysdelinquent”wasnotconsideredasanindependentoutcome.Besides,thereareveryfewspellsinthiscategory(2.6percent).

14Tomakesurethatalargenumberofearly-stagedelinquencieswerenotdrivenbypend-ing refinancing plans, we examined the number of delinquencies that ended in repayment.However,only234,orlessthan2percent,ofdelinquencyspellsendedinpayoff.

15Weuse90daysasaproxyfordefaultbecausecompleteddefaultsusuallylagsubstan-tiallyandthedataprovidemoreoccurrencesofdelinquenciesexceeding90days.Themeasure,then,istowhatextentloansmovetothemoreseverecategoryof“seriousdelinquency”ormorethan90dayslate.

16Some90-daydelinquentloanscuredandthensubsequentlybecamedelinquentagain.

onewayortheotherwithinsixmonthsandourobservationperiodlastedmorethansixyears,12nearlyallspells(97.4percent)achievedanoutcomeofeithercureordefaultbeforetheendoftheobservationperiod.Loansthatwerestilldelinquentattheendoftheperiodwereexcludedfromoursam-ple.13Oncealoanwascured,anysubsequentdelinquencygeneratedanewspell.Anobservationwasconsideredcurediftheloanwaspaidoffwhilestill30to60daysdelinquent.14

Asaresult,wehaveasampleof15,038delinquencyspellsthatweregen-eratedby5,886borrowersandendedineithercureordefaultbyDecember2004,foranaverageof2.6delinquencyspellsperloan.Some85percentofthesedelinquencyspellswerecured,while15percentendedindefault.15 The2,200defaultsweregeneratedby1,870loans,16representingjust7percentofallloanstrackedbut31percentofallever-delinquentloans(table2).Theother69percentofever-delinquentloansneverproceededbeyond60dayspastdue.Delinquencyspellsthatcuredordefaultedlastedanaverageof2.1monthsor4.1months,respectively.

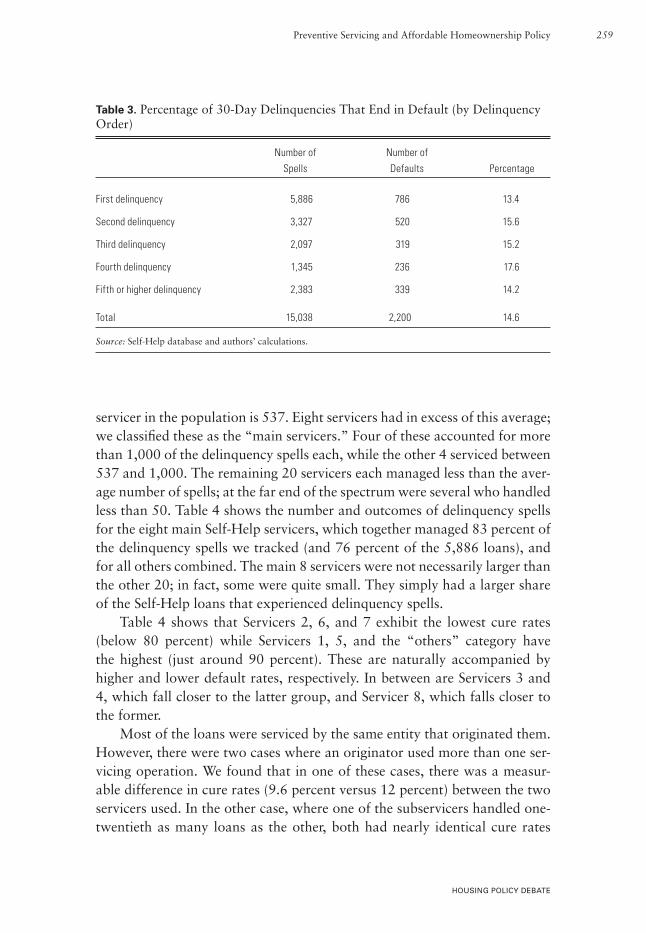

Astable3shows,13.4percentoffirst-timedelinquenciesendedindefault,andthisrategenerallyincreasedwiththenumberofpriordelinquencies,to17.6percentofthoseexperiencingafourthdelinquencyspell.Yetsomewhatsurprisingly, the default rate for borrowers experiencing a fifth or higherdelinquency spell dropped to 14.2 percent, nearly identical to the defaultrateamongloansexperiencingafirstspell.Thisfindingsuggestsaninflexionpointabovewhichthenumberofpreviousdelinquenciesexperiencedbyseri-allydelinquentborrowersdoesnotincreasethelikelihoodthatthecurrentspellwillendindefault.Infact,smartservicingtechnologiesseektoidentifythosefrequentlydelinquentborrowerswhoareunlikelytoactuallydefault,savingcollectionsresourcestofocusonother,higher-riskdelinquencies.

We want to determine the extent to which delinquency outcomes areaffectedbytheloanservicer.Theaveragenumberofdelinquencyspellsper

HOUSING POLICY DEBATE

PreventiveServicingandAffordableHomeownershipPolicy 259

servicerinthepopulationis537.Eightservicershadinexcessofthisaverage;weclassifiedtheseasthe“mainservicers.”Fouroftheseaccountedformorethan1,000ofthedelinquencyspellseach,whiletheother4servicedbetween537and1,000.Theremaining20servicerseachmanagedlessthantheaver-agenumberofspells;atthefarendofthespectrumwereseveralwhohandledlessthan50.Table4showsthenumberandoutcomesofdelinquencyspellsfortheeightmainSelf-Helpservicers,whichtogethermanaged83percentofthedelinquencyspellswetracked(and76percentofthe5,886loans),andforallotherscombined.Themain8servicerswerenotnecessarilylargerthantheother20;infact,somewerequitesmall.TheysimplyhadalargershareoftheSelf-Helploansthatexperienceddelinquencyspells.

Table4 shows thatServicers2,6,and7exhibit the lowestcure rates(below 80 percent) while Servicers 1, 5, and the “others” category havethehighest (just around90percent).Thesearenaturallyaccompaniedbyhigherandlowerdefaultrates,respectively.InbetweenareServicers3and4,whichfallclosertothelattergroup,andServicer8,whichfallsclosertotheformer.

Mostoftheloanswereservicedbythesameentitythatoriginatedthem.However,thereweretwocaseswhereanoriginatorusedmorethanoneser-vicingoperation.Wefoundthatinoneofthesecases,therewasameasur-abledifferenceincurerates(9.6percentversus12percent)betweenthetwoservicersused.Intheothercase,whereoneofthesubservicershandledone-twentiethasmany loansas theother,bothhadnearly identicalcurerates

Table 3.Percentageof30-DayDelinquenciesThatEndinDefault(byDelinquencyOrder)

Numberof Numberof

Spells Defaults Percentage

Firstdelinquency 5,886 786 13.4

Seconddelinquency 3,327 520 15.6

Thirddelinquency 2,097 319 15.2

Fourthdelinquency 1,345 236 17.6

Fifthorhigherdelinquency 2,383 339 14.2

Total 15,038 2,200 14.6

Source:Self-Helpdatabaseandauthors’calculations.

HOUSING POLICY DEBATE

260 M.A.Stegman,R.G.Quercia,J.Ratcliffe,L.Ding,andW.R.Davis

Table 4.Outcomesof30-DayDelinquenciesbyServicer

Percent90 Numberof Numberof Percent Days Loans Delinquencies Cured Delinquent

Servicer1 293 656 88.87 11.13

Servicer2 594 1,461 79.19 20.81

Servicer3 1,133 3,474 86.70 13.30

Servicer4 824 2,594 87.24 12.76

Servicer5 377 861 90.36 9.64

Servicer6 595 1,688 77.84 22.16

Servicer7 261 599 79.63 20.37

Servicer8 405 864 83.91 16.09

Others 1,404 2,841 89.02 10.98

Total 5,886 15,038 85.37 14.63

Source:Self-Helpdatabaseandauthors’calculations.Note:Eightmajorservicers(handlingmorethantheaveragenumberofdelinquencies)werechosenforinclusioninouranalysis.

(12.2percentand12.5percent).Inbothofthesecaseswithoneoriginatorandmultipleservicers,therewasonlyoneservicerwithalargeenoughnum-berofdelinquencyspellstobecountedamongthemainones;therestwereincludedintheotherscategory.Inallothercases,asingle,uniqueservicerwasmanagingaportfolioofloansoriginatedbythesamelender.

LogitregressionmodelTobetterisolatetheimpactsofdifferentservicingmethodsandotherrisk

factors,ourgoalinmodelingtheoutcomesofthe15,038delinquencyspellsistoidentifyfactorsthatpredictthelikelihoodthatagivendelinquencywillcureorworsenandgointodefault.Wemodelthebinaryoutcomesusingalogitregressionapproachwherethedependentvariableistheoddsofcureandthereferencecategoryisdefault.

(1)=

+=−

k

jijj

i

i Xpp

Log11

βα

HOUSING POLICY DEBATE

PreventiveServicingandAffordableHomeownershipPolicy 261

Here,Pi is theprobabilityof transition froma30-daydelinquency tocure,Χiisacolumnvectorofthecovariatemeasuresfordelinquencyspelli,andβisarowvectorofcoefficientsfortheoutcomeofcuring.Thismodelassumesthatoutcomesatanyonepointintimeareindependentofoutcomesinanypreviouspointintime.Tocontrolforthepotentialstatisticalprob-lemsassociatedwithrepeatedevents,themodelwasestimatedusingStata’slogitprocedurewithanadjustmenttothestandarderrorsforclusteringbyloan.17

Inadditiontoinvestigatingtheoutcomesforalldelinquencyspells,itisalsoimportanttolookattheoutcomesofthefirstdelinquencyspellstoelimi-natetheeffectofpossibledependenceamongdifferentspells.Itispossiblethatsomeservicerscouldtreatfirstdelinquenciesdifferentlyfromserialones.Tocheckthedifferentimpactofservicersontheoutcomeoffirstdelinquen-cies,weusedthesamemodeltorunaseparateregressiononfirstdelinquencyspells.

Werecognize thatdifferences incureanddefault ratesmaybedue todifferencesinthecompositionofeachportfolio.Table5profilestheloanshandledbythemaineightservicersandallothers.Thedifferencesarenota-ble:Servicer6’sportfoliohasthegreatestshareoflowcreditscoresandthelowest-incomeborrowers.LoanshandledbyServicer8haveespeciallyhighLTVs, while loans handled by Servicer 5 experienced the highest housingappreciationratesduringthestudyperiod.Astotheloansservicedby“oth-ers,”theonlyobviousdifferenceintermsofriskfactorsisintheirsomewhatbetterappreciationrates(7percentversus4percentforallbutServicer5).Borrowersservicedbytheotherscategoryalsohavehigherincomethanbor-rowershandledbymostofthemaineight.

Consequently,whenweestimatethelogitregressionmodel,wecontrolforvariousloanandborrowercharacteristicsthatmightaffectdelinquencyoutcomes.Controlvariablesinthemodelincludethefollowing:

1. Loan characteristics. Housing equity is a key factor in determiningdefault.Delinquentborrowerswithsubstantialaccumulatedequityhavemoreresourcestoavoidforeclosure,whilethosewithlittleornoequityhave less incentiveand lessability to retain theirhome.We includeadummyvariableforloanswithanLTVof95percentorhigher.Wealsoincludeloanageinmonthsatthetimeofdelinquencyandthenumber

17Theestimationusedthe“cluster”option,whichspecifiesthatobservationsareindepen-dentacrossgroups(loans)butnotnecessarilywithingroups(StataCorporation2003).Thisoptionaffectstheestimatedstandarderrorsandvariance-covariancematrixoftheestimator,butnottheestimatedcoefficients.

HOUSING POLICY DEBATE

262 M.A.Stegman,R.G.Quercia,J.Ratcliffe,L.Ding,andW.R.Davis

Table 5. LoanandBorrowerCharacteristicsbyServicer

MainServicers Variable All 1 2 3 4 5 6 7 8 Others Creditscore

Nocreditscore(%) 3.5 0.3 4.4 0.6 1.2 2.27 7.7 7.1 1.3 5.78

FICO620orlower(%) 17.2 7.8 23.1 25.1 23.8 9.42 46.5 26.4 15.5 11.43

FICO621to660(%) 21.0 17.6 26.5 20.4 23.7 20.61 21.3 35.1 20.2 19.41

FICO661to720(%) 30.4 33.7 29.1 26.8 29.9 37.22 15.2 22.4 36.5 30.88

FICOabove720(%) 28.0 40.6 17.0 27.1 21.5 30.49 9.3 9.2 26.6 32.50

Loancharacteristics

MedianLTV(%) 97.0 97.0 97.0 97.0 99.0 97.0 97.0 97.0 102.3 97.0

Medianback-endratio 36.7 37.7 37.5 35.4 36.6 37.3 34.9 37.1 37.2 37.0 (%)

Ageofloanat 11 13 3 23 18 9 5 2 9 12 purchase(months)

Estimated 4.3 4.2 3.3 3.4 3.6 13.4 4.1 4.0 4.4 7.0 appreciationrate(%)a

Borrowercharacteristics

Femaleborrower(%) 44.0 43.3 48.7 51.1 46.03 36.71 50.1 37.5 43.2 37.14

Blackborrower(%) 21.3 15.2 33.9 34.7 37.66 9.88 60.2 12.5 6.8 13.50

Hispanicborrower(%) 16.6 4.8 4.2 2.6 2.89 42.98 2.0 7.9 15.1 26.56

First-timehomebuyer 43.8 56.0 18.0 64.8 88.61 32.09 82.4 18.0 48.3 25.39 (%)

Incomeat 29,472 31,074 30,000 23,640 24,870 35,634 24,504 30,276 27,996 33,516origination($)(median)Incomeasa 59.7 61.3 64.3 57.0 58.1 61.2 48.2 52.8 59.8 61.8percentageofAMI(median)

Totalloansb 28,131 1,962 1,852 4,661 2,318 2,378 1,055 850 2,464 10,591

Source:Self-Helpdatabaseandauthors’calculations.Note:Totalsmaynotequal100percentbecauseofrounding.aTheestimatedannualhouseappreciationrateisbasedonthehousepriceatoriginationandtheupdatedhousepricesestimatedinDecember2005.bSelf-HelploanspurchasedbeforeJanuary1,2003.AMI=areamedianincome(medianincomeofthemetropolitanstatisticalarea[MSA]orthestatefornon-MSAareas).

HOUSING POLICY DEBATE

PreventiveServicingandAffordableHomeownershipPolicy 263

ofpreviousdelinquencies(ofcourse,thisvariableisnotincludedinthemodelfocusingonthetransitionoffirstdelinquencies).

2. Borrower characteristics. To control for underwriting and borrowerdifferences,we includeadummyforback-endratiosof38percentorhigher,18 incomeasapercentageofareamedian income,dummies forgenderandrace/ethnicity,andadummyforfirst-timehome-buyerstatus.Sincetheimpactofcreditscoreonloanperformancemightnotbelinear,wefollowindustrypracticeandpreviousliteraturebyalsoincludingasetofcreditscoredummyvariablesforborrowerswithnocreditscore,borrowerswithlowscores(below620),borrowerswithmoderatescores(620to659),andborrowerswithrelativelyhighscores (660to719).Thecategorywiththehighestscores(720orabove)issetasareferencegroup.

3. Economicconditions.Becausechangesinpropertyvaluesafterorigina-tioncanaffecthousingequity,weuseavariablefortheestimatedannualrate of appreciation, determined using the change between the valueofthehouseatoriginationandupdatedvaluesforeachpropertyasofDecember2005.Tohelp separate lender/servicereffects fromregionaleconomiceffects,wealsoincludedummyvariablesforthestateshavingthemostloansintheSelf-Helppopulationstudied:NorthCarolinaandCalifornia.

Totestfordifferencesamongservicers,weincorporatedummyvariablesforthemaineightSelf-Helpservicersintoourlogisticmodel.Wetreatdelin-quenciesservedby“others”asthereferencegroup.Theoddsratioestimatedfromthemodelistheoddsofcure(versusworsening)ofadelinquencyspellforoneservicerrelativetotheoddsofcurebyservicersintheotherscategory.Table4indicatedthatthereferencegroup(“others”)hadaveryhighcurerate (89.02percent);onlyServicer5hadahigher rate than this. Inotherwords,aftercontrollingforothercharacteristicsinourlogitmodel,wearecomparingthepracticesofmajorservicerswithsomeofthebestperformers(asthesimplefrequencytablesuggests).

Someoftheexplanatoryvariablesarehighlycorrelated.Generally,bor-rowerswithhighLTVshavelowercreditscores.BlackandHispanicborrow-ersalsohavelowercreditscoresandhigherLTVsthannon-Hispanicwhites.

18According to theSellingGuide createdbyFannieMae, its suggestedbenchmark fortotaldebt-to-incomeratiois36percentforstandardloansand38percentforcommunitylend-ingproducts(Allregs.com2006).NearlyallSelf-Helplendersallowahighermaximumratio,rangingfrom40percentto48percent.

HOUSING POLICY DEBATE

264 M.A.Stegman,R.G.Quercia,J.Ratcliffe,L.Ding,andW.R.Davis

PropertiesinCaliforniahavehigherhouseappreciationrates.Further,thereisasignificantcorrelationbetweentheloanagevariableandthenumberofpreviousdelinquencies.However,thesevariableshavebeenwidelyusedintheliterature,andacheckofvarianceinflationfactorsindicatesthatmulti-collinearityisnotparticularlyseriousamongindependentvariables.19Asaresult,thefinalmodelofthisanalysisincludesalltheseimportantvariablessuchascreditscores,LTV,race,gender,andstatedummies.

Tables6and7presenttheresultsofthelogitregressionmodel.Table6isbasedonalldelinquencyspells,whiletable7focusesonthetransitionoffirstdelinquencyspellsonly.20Apositivecoefficientmeansthattheoddsofcureincreaseastheindependentvariableincreases;anegativecoefficientmeansthattheoddsdecrease.Anoddsratiorepresentstheoddsofcurewhenanindependentvariableisequalto1relativetotheoddsofcurefortherefer-encecategory(forcategoricalvariables).Themodelfitisstrong.21Further,theeightservicervariableswerejointlysignificantatthe0.001level,whichsuggests that the introduction of these variables appreciably increases theexplanatorypowerofthemodel.

Ofprimary interest is the fact thataftercontrolling for loanandbor-rower characteristics, house appreciation rate, and regional dummies, wefindsignificantdifferencesintheoddsofcureamongservicers.Specifically,delinquenciesforServicers2,3,6,and7aresignificantlylesslikelytocurethantheyarefortheservicersintheotherscategory,whiletheoddsofcureforServicers1,4,5,and8arenotsignificantlydifferentfromthose“others.”Inotherwords,30-daydelinquenciesforServicers2,3,6,and7aresignifi-cantlymorelikelytoendindefaultthantheyareforservicersintheotherscategory.Theoddsofcure forServicers2,6,and7areabout40percentlowerthantheyareforservicersintheotherscategory,whiletheoddsareabout20percentlowerforServicer3.

19Varianceinflationfactorsareameasureofthemulticollinearityinaregressiondesignmatrix.Forthisstudysample,thevarianceinflationindicatorsformostvariablesarelessthan3(generallyconsideredacceptable).Theonlyexceptionsareseveralcategoricalcreditscorevariables.

20Thefinalstudysamplefortable6isreducedfrom15,308to13,878becauseofmissingdata.Thestudysamplefortable7is5,443.

21Toassessthepredictivequalitywiththemodelfocusingonallthespells,wefindthattheshareofcorrectlypredictedobservationswas87percentforcureand23percentfordefaultifwespecifythecutoffas>0.8(anestimatedprobabilityof>0.8forcurewouldbeassignedtobeapositiveoutcome).Theoverallshareofcorrectlyclassifiedobservationsis78percent.Ofcourse,ahighercutoffwouldleadtobetterspecificationfordefaultandpoorersensitivityforcure.Forexample,ifthecutoffissetas0.85,theshareofobservationsthatwerecorrectlypredicted is67percent for cureand47percent fordefault.Theoverall correctly classifiedshareis64percent.

HOUSING POLICY DEBATE

PreventiveServicingandAffordableHomeownershipPolicy 265

Table 6. LogisticRegressionResultsfortheOutcomesof30-DayDelinquencies:ProbabilityofCure

Variable Coefficient StandardError OddsRatio

Constant 1.423** 0.193

Nocreditscore –0.349* 0.102 0.705

FICObelow620 –0.046 0.119 0.955

FICO620to659 0.031 0.131 1.032

FICO660to719 0.036 0.136 1.036

LTV95orabove –0.087 0.069 0.917

Femaleborrower 0.128* 0.066 1.136

Blackborrower 0.076 0.071 1.079

Hispanic 0.301** 0.163 1.351

IncomeasapercentageofAMI 0.006** 0.002 1.006

Ageofloan(months) 0.004** 0.001 1.004

Numberofpreviousdelinquencies –0.028 0.014 0.973

Appreciationratea 0.028** 0.010 1.028

NorthCarolinaborrower 0.119 0.104 1.126

Californiaborrower –0.101 0.176 0.904

Servicer1 0.121 0.193 1.129

Servicer2 –0.610** 0.072 0.543

Servicer3 –0.222* 0.088 0.801

Servicer4 –0.213 0.099 0.808

Servicer5 0.088 0.157 1.093

Servicer6 –0.545** 0.068 0.580

Servicer7 –0.527** 0.086 0.590

Servicer8 –0.235 0.109 0.790

Modelfit

Wald_2 209.2**

df 22 Source:Self-Helpdatabaseandauthors’calculations.Note:Thestudysampleis13,878sinceanumberofobservationsweredroppedbecauseofmissingdata.aTheestimatedannualhouseappreciationrateisbasedonthehousepriceatoriginationandupdatedhousepricesestimatedinDecember2005.AMI=areamedianincome(medianincomeofthemetropolitanstatisticalarea[MSA]orthestatefornon-MSAareas).*p≤0.05.**p ≤0.01.

HOUSING POLICY DEBATE

266 M.A.Stegman,R.G.Quercia,J.Ratcliffe,L.Ding,andW.R.Davis

Table 7.LogisticRegressionResultsfortheOutcomesoftheFirst30-DayDelinquencies:ProbabilityofCure

Variable Coefficient StandardError OddsRatio

Constant 1.553** 0.26

Nocreditscore –0.375 0.164 0.687

FICOatorbelow620 –0.057 0.162 0.945

FICO620to659 0.005 0.175 1.005

FICO660to719 0.070 0.191 1.073

LTV95orabove –0.099 0.105 0.906

Femaleborrower 0.342** 0.125 1.408

Blackborrower 0.143 0.116 1.154

Hispanic 0.237 0.209 1.267

IncomeasapercentageofAMI 0.008** 0.003 1.008

Ageofloan(months) –0.003 0.002 0.997

Appreciationratea 0.026** 0.010 1.027

NorthCarolinaborrower 0.070 0.154 1.073

Californiaborrower 0.072 0.298 1.074

Servicer1 –0.199 0.184 0.820

Servicer2 –0.547** 0.118 0.578

Servicer3 –0.135 0.152 0.874

Servicer4 –0.085 0.174 0.919

Servicer5 0.216 0.292 1.241

Servicer6 –0.949** 0.066 0.387

Servicer7 –0.894** 0.081 0.409

Servicer8 –0.472** 0.115 0.624

Modelfit

Wald_2 161.4**

df 21

Source:Self-Helpdatabaseandauthors’calculations.Note:Thestudysampleis5,443sinceanumberofobservationsweredroppedbecauseofmissingdata.aTheestimatedannualhouseappreciationrateisbasedonhousepriceatoriginationandupdatedhousepricesestimatedinDecember2005.AMI=areamedianincome(medianincomeofthemetropolitanstatisticalarea[MSA]orthestatefornon-MSAareas).*p ≤0.05.**p≤0.01.

HOUSING POLICY DEBATE

PreventiveServicingandAffordableHomeownershipPolicy 267

Astothecontrolvariables,it isparticularlynoteworthythatvariablesthatarekeyindicatorsofdefaultriskatthetimeofunderwriting(basedoncreditscoreandLTV)generallydonotappeartobesignificantinpredictingwhetheranalreadydelinquentloanwilldefault.Theonlyexceptionisthatthereissomeevidencethatborrowerswithoutcreditscoresarelesslikelytobe cured.But someborrower characteristicsdomatter.Female,Hispanic,andhigher-incomeborrowersaremore likely tocure. Inparticular,delin-quentborrowerswhowereHispanichad39percentbetteroddsofcuring(versusworsening)thandelinquentborrowerswhowerewhite.Theevidencealsoindicatesthatolderloansaremorelikelytocure,suggestingthatexperi-encedborrowershandledelinquenciesbetterthannewonesdo.Fromamac-roeconomicstandpoint,locationineitherNorthCarolinaorCaliforniadidnothaveasignificanteffectonoutcomes,butthereisconsiderableevidencethatthehigherthehouseappreciationrate,themorelikelythatdelinquentloanswouldbecuredandthelesslikelythatborrowerswouldletthedelin-quencyproceed.

Whenwefocusonthefirstdelinquencyspell(table7),theresultsaregen-erallyconsistentwiththeresultsbasedonalldelinquencyspells.Firstdelin-quenciesforServicers2,6,and7arestilllesslikelytobecured,whilethecoefficientsforServicer3becomeinsignificant,likethoseofServicers4and5.ButthecoefficientforServicer8issignificantandnegativeinthismodel.AmongServicers2,6,7,and8,theoddsofcureareparticularlylow—about60percentlower—forServicers6and7.Thusitseemsthattherelativeoddsofcurefortheseservicers,whileworseforalldelinquencies,lagevenmoreforfirstdelinquencies.

Table 8 shows predicted cure and default rates by servicer. Using theresultsfromtable6(allspells),weestimatethatServicer2hasthe lowestpredictedcurerate(andthehighestpredicteddefaultrate),whileServicer1hasthehighestpredictedcurerate(andthelowestpredicteddefaultrate).Inotherwords,theprobabilitythatadelinquentloanservicedbyServicer2willdefaultisnearlydoublethatforServicer1(table8).

Thus there appear to be roughly two groups of servicers in terms ofoutcomes.DelinquencieshandledbyServicers2,3,6,and7havealowerprobabilityofcureandahigherprobabilityofdefault.Servicers1,4,5,and8,alongwiththeservicersintheotherscategory,havehighercureratesandalowerriskofdefault.22

22AlthoughServicer8hasalowercurerateforthefirst-30delinquencyspells,itsoverallcurerateisnotstatisticallydifferentfromthatofthe“others.”

HOUSING POLICY DEBATE

268 M.A.Stegman,R.G.Quercia,J.Ratcliffe,L.Ding,andW.R.Davis

From telephone interviews with the main servicers and supplementalinformation provided by Self-Help’s Servicing Manager, we learned thattherearesignificantdifferencesinthewaypersonnel,systems,andprocessesareappliedtononperformingloansbetweenthe30thand90thdayofdelin-quency—theperiod reflectedby theanalysis (Russell2005).Forexample,oneservicerhasonecollectorforevery15,000loansitservicesandusesnorisk-scoringsystematall.Thisisinstarkcontrasttotheservicersthathaveatleastonecollectorforevery5,000loansandusebothcollectionsscoringandforeclosurealternativeassessmentmodels,supportedbyscriptingsoftware.

Servicersuseanumberofdifferentcollectionsandlossmitigationtools.CollectionsscoringtoolsincludeFreddieMac’sEIandFannieMae’sRP.EIfeaturesbothascorethatprioritizescallstoborrowersintheearlystageofdelinquencyandamodulethatpredictstheshareofmoreadvanceddelin-quencies thatcouldresult ina loss (FreddieMacn.d.).RPusesborrower,loan,andpropertycharacteristicstosegmentloans(whethercurrentlydelin-quentornot)bylikelihoodofgoingmorethan60daysdelinquentwithinsixmonths. Investorshave laidout specific servicingproceduresbasedonscore—forexample,recommendingearliercontactforhigh-riskratherthanforlow-riskloans(FannieMae2005a,2005b).Toolstoassessalternativesto foreclosure includeFreddieMac’sWorkout Prospector®,which applies

Table 8. PredictedOutcomesofaTypical30-DayDelinquencybyServicer

Percentin Default(90 Percent Days Cured Delinquent)

Servicer1 90.41 9.59

Servicer2 81.94 18.06

Servicer3 87.00 13.00

Servicer4 87.10 12.90

Servicer5 90.13 9.87

Servicer6 82.89 17.11

Servicer7 83.13 16.87

Servicer8 86.84 13.16

Others 89.31 10.69 Source:Self-Helpdatabaseandauthors’calculations.Note:Basedonthelogitregressionmodelintable6.Additionalborrowerandloancharacteristicshavebeencontrolledfor.

HOUSING POLICY DEBATE

PreventiveServicingandAffordableHomeownershipPolicy 269

23Thisprogramwasdevelopedonathird-partyplatform.FreddieMacsoldittothethirdparty,ComputerSciencesCorporation,in2004(ComputerSciencesCorporation2004).

aconsistentapproachtoassess theviabilityof foreclosurealternatives foreach case (Cutts and Green 2005), and Workout ProfilerTM, part of Fan-nieMae’sHomeSaverSolutionNetworkTM(HSSN),aWeb-based,interac-tivemodelthatincorporatessuchdataasfinancialsituation,propertyvalue,andpaymenthistory(O’Connor2003).AnexampleofascriptingsystemisEarlyResolution®,23aprogramtotrainandguidepersonnelastheyinteractwithborrowerstodeterminethebestmethodtohelpthemkeeptheirhomes(O’Connor2003).

Servicersalsofollowdifferentstepstoaddressdelinquencies.Self-Helpsuggeststhatitssubservicersfollowaspecifictimelinethroughthedelinquencyprocess(figure1).ButwhileservicersgenerallyfollowedSelf-Help’smanual,thereweresomemarkeddeviationsinactualdelinquencymanagement.

Anotherareaofdifferentiationderives fromaSelf-Help-drivendelin-quencyinterventionprogram.Inthetraditionalprocess,theborrowermusttakesomeinitiativetogetintoalossmitigationplan,eitherbycontactingtheservicerorahousingcounselororbyfillingoutaninformationpacketthatcomes in themail fromtheservicer. In2002,Self-HelpbegantestingamoreproactiveapproachbyengagingBalance,anaffiliateofConsumerCreditCounselingofSanFrancisco,tocontactborrowersbytelephoneonthe45thdayofdelinquency.TheprogramwasactivatedwithServicers1,2,3,and6between2002andlate2003,aswellaswithoneotherthatisnotprofiledinthisarticle(Holder2005).BecauseSelf-Helpdeliberatelyphasedinservicersaccordingtowhereinterventionmighthavethemostimpact,itisnotsurprisingthatmostoftheparticipatingservicersfallinthelowercureratecategory.

ServicerprofilesProfilesofthedifferentstaffing,systems,andprocessesusedbythemain

Self-Helpservicersaredescribedinthefollowingparagraphs.Theseservicersand subservicers ranged in size from less than50,000 loans serviced to2million.Theyarelocatedinvariouspartsofthecountry,andtheirportfo-liosincludeloansfrommanydifferentstates.Theydonotfocusstrictlyonconventional,affordablemortgages,butratherservicearangeofmortgagetypes.Sowhilenotstatisticallyrepresentativeofallservicers,thesebriefcasestudiescharacterizeawiderangeofinstitutions,practices,andforeclosureprevention strategies.Whether oneof these strategies ismore effective or

HOUSING POLICY DEBATE

270 M.A.Stegman,R.G.Quercia,J.Ratcliffe,L.Ding,andW.R.Davis

Sour

ce:C

ente

rfo

rC

omm

unit

ySe

lf-H

elp

(200

3).

Fig

ure

1.S

elf-

Hel

pD

elin

quen

cyM

anag

emen

tT

imel

ine

inD

ays

Sche

dule

ear

lyde

linqu

ency

coun

selin

g

3060

90

7–10

16

20

45

50

10

5

Colle

ctio

nca

ll/pa

ymen

tre

min

der

notic

e

Follo

w-u

ple

tter

Late

pay

men

t no

tice

(a la

tefe

e is

usu

ally

asse

ssed

)

HUD

lette

r (su

gges

ts

coun

selin

g)

Loss

miti

gatio

nal

tern

ativ

esle

tter

Bre

ach/

dem

and

lette

r

Refe

r to

fore

clos

ure

(con

tinue

loss

m

itiga

tion)

Refe

r to

atto

rney

(fore

clos

ure

times

var

yby

sta

te)

HOUSING POLICY DEBATE

PreventiveServicingandAffordableHomeownershipPolicy 271

efficientthananothercannotbedeterminedfromthisanalysis,buttheextentofthedifferenceshintsatwhyoutcomesvary.

Servicers1,4,5,and8(highercurerates).Servicer1isamidsizeorgani-zation(between100,000and300,000loansservicedinall)thatusesEIfordelinquencyscoring.Thereisastrongcollectionsstaff,withonecollectorforevery4,000loansintheportfolio.ThisenablesspecializationsuchthattwocollectorsareassignedtoSelf-Helploans.TheyfollowSelf-Help’stimelineclosely.Intermsoflossmitigation,however,Servicer1hasonlyonespecial-isttoaddressitsportfolioofmorethan100,000loansanddoesnotuseaworkoutsystem.Self-Helprolledoutitsdelinquencyinterventionpilotwiththisservicer15monthsbeforetheendofthe53-monthobservationperiod,soitwouldhaveasomewhatlimitedimpactonourresults.

Servicer4isamega-servicer(morethan1millionloanshandled).Itaver-ages20,000 loansper collector; also, itoutsources certain calls for early-term,low-riskdelinquenciesandusesbothRPandEI.Affordablemortgagesarenotidentifiedperse,butinvestorprocessrequirementsarefollowedforall loans. Servicer 4 also averages about 20,000 to 25,000 loans per lossmitigationemployeeandusesaproprietaryworkoutsystembutnoscriptingtechnology.Thisisoneofonlytwoservicersthatreportedpayinganincen-tivetoitslossmitigationstaff,inthiscaseforworkoutsthatareapprovedorclosed.

Servicer5,alsoamega-servicer,usesbothRPandEIandhasaloans-to-collectorratiothatfallsatthehigherendoftherangeamongSelf-Help’sservicers. Staffmembers specialize by investor, not product type. For lossmitigation, the servicer uses the HSSN and supplements decision makingwithinternallydevelopedspreadsheets.Thisservicer’sprocessissomewhatunusualinthatitstartscollectionscallingonday1andsendsthelossmiti-gationalternatives letterveryearly—onthe30thday—eveninadvanceoftheHUDletter. (TheHUDlettergivestheborroweratoll-freenumbertocalltoobtainthename,number,andaddressofthenearestHUD-approvedcounselingagency.Thelossmitigationletterinformstheborrowerthatheor she may qualify for alternatives to foreclosure. The letter lists options(repaymentplan, loanmodification,deed in lieu, andpreforeclosure sale)andprovidesadescriptionofwhateachonemeans.)Thislikelyencouragesworkoutsearlyinthedelinquencytimeline.

Servicer 8 is small (less than 100,000 loans) and uses RP. Overall, itstaffsonecollectionspersonper6,000loans,withonecollectorassignedtoits2,000affordableloans(includingSelf-Help).Thelossmitigationemploy-ees—aboutoneforevery20,000loansintheportfolio—donotspecialize;WorkoutProfilerTMisusedforlossmitigation(Russell2005).Fromaprocess

HOUSING POLICY DEBATE

272 M.A.Stegman,R.G.Quercia,J.Ratcliffe,L.Ding,andW.R.Davis

standpoint,Servicer8takeslittleactionbetweentheinitialdelinquencyletterandthe60thday,whentheHUDletter,lossmitigationletter,andbreachlet-terareallsentwithinafewdaysofeachother(Holder2005).

Servicers2,3,6,and7(lowercurerates).Servicer2issmallandhasonecollectionspersonforevery15,000loansandnoriskscoringsystem.Thereisonlyonelossmitigationcounselor(forabout50,000loans),andtheHSSNisusedforworkouts.Staffmembersdonotspecializebyinvestororproducttype.Servicer2sendsouttheHUDlettertwoweekslaterthansuggested,butotherwisegenerallyfollowsSelf-Help’stimeline.Becauseofthelargenumberofdelinquenciesanditslimitedresources,Servicer2wasselectedasthefirstparticipantintheinterventionprogram.

Servicer3islarge(300,000to1millionloans)andusesbothRPandEI.Itemploysapproximatelyonecollectionspersonper10,000loans.Collec-torsdonotspecialize.Onthelossmitigationside,thereisonespecialistfor80,000loans,andtheHSSNisusedforworkouts.Servicer3basicallyfollowsSelf-Help’sinvestorrequirementsandbeganparticipatingintheinterventionprograminAugust2002,aboutmidwaythroughtheobservationperiod.

Servicer6isanotherlargeorganization.Theratioofloansservicedpercollector is between 5,000 and 10,000, while the ratio of loss mitigationspecialiststoloansisaboutoneper20,000.Servicer6usesRPbutnosmartworkoutsystem.HUDlettersarenotsent,butabreachletter issentveryearly(onthe35thday),andloansarereferredtoforeclosureearlieraswell.ThisservicerhasparticipatedinthedelinquencyinterventionprogramsinceJuly2003(thefinal18monthsoftheobservationperiod).

Servicer7fallsinthemega-servicercategory,averaging12,000loansperfull-timecollectionsemployee.Thisservicerreportshavingadedicatedteamforhigher-riskproducts;makingintroductorycallswhennewloansinthiscategory are added to theportfolio; paying staff incentives forworkouts;andusingRP,EI,multiplelossmitigationsystems,andascriptingsystem.Thisservicer’sactualprocessisdistinctinthatneitheraHUDletternoralossmitigationletterisautomaticallysent,andthebreachletterdoesnotgooutuntilthe90thday,sothereoftenappearstobelittlecommunicationwithdelinquentborrowersbetweenthe30thand90thdays.

Evidently, there is substantialvariation in the servicers’approaches toforeclosureprevention—somuch,infact,thatit isdifficulttodiscernbestpractices.WebelievethatthisvariationisnotconfinedtotheSelf-Helpser-vicers,butspeculatethatitiswidespread,particularlyassales,mergers,andconsolidationsresultintherealignmentofservicingplatformsandcultures.Further research into successful strategies for affordable mortgages could

HOUSING POLICY DEBATE

PreventiveServicingandAffordableHomeownershipPolicy 273

helpservicersdevelopmoreeffectivecombinationsofpeople,processes,andtechnology thatwouldhelpagreaternumberof troubledborrowerskeeptheirhomes.

ConclusionsTheunprecedentedgrowthinhomeownershipamonglow-andmoderate-

incomefamiliesduringthe1990smeantthatthebackendofthehome-buyingtransaction—loanservicingandpostpurchasedefaultmanagement—becamemuchmoreimportant.Althoughdelinquencyanddefaultratesincreasedastheeconomyfellintorecession,manymorefinanciallysqueezedhomeown-erswouldpossiblyhavelosttheirhomesifnotfortheinnovationsinloanservicingdiscussedinthisarticle.Atthiswriting,theloomingpossibilityofsofteninghousingmarketsandrisingforeclosures,andtheproliferationofaggressivemortgageproductswithadjustableratesandnegativeamortiza-tionsuggestthatthesetoolsmaybecomeevenmoreimportantinthenearfuture.Forexample,interest-onlyloans,onwhichnoprincipalpaymentsaremadetobringdownmortgagedebt,madeupnearlyone-thirdofmortgageoriginationsduring2004and2005(FishbeinandWoodall2006).Accordingtooneestimate,ofthe7.7millionhouseholdsthattookoutadjustable-ratemortgagestobuyorrefinancein2004and2005,“upto1millioncouldlosetheirhomesthroughforeclosureoverthenextfiveyearsbecausetheywon’tbeabletoaffordtheirmortgagepayments,andtheirhomeswillbeworthlessthantheyowe”(Knox2006,A1).

As mortgage products featuring more flexible underwriting standardsgaininpopularityandasmorelow-andmoderate-incomefamilies,immi-grants,andminoritiesjointhefirst-timehome-buyingmarket,theeconomicfortunesofmortgageinstitutionswillbeincreasinglytiedtotheeffectivenessoftheirloanservicingoperations.Clearly,themoreaggressivetheunderwrit-ing,themoreimportantpreventiveservicingbecomes.Whileclosecoordina-tionbetweencreditunderwritingpoliciesandservicingstrategiesisimportantfortheentireindustry(CaldwellandJordan2006),itisevenmoreimportantforaffordablehousingportfolios.

Althoughitisnotpossibletogeneralizeforallaffordablelendingpro-grams,earlyfindingsfromourevaluationoftheSelf-Helpsecondarymarketdemonstration program are nevertheless suggestive. A significant share ofSelf-Helpborrowersandcoborrowerswhobought theirhomesbefore theonsetofthe2000-01recessionhaveexperiencedmultiplespellsofjobless-nessandmissedhousingpaymentssincetakingouttheirloans.YetthevastmajorityofSelf-Helpborrowershavenevermissedapayment,andasmall

HOUSING POLICY DEBATE

274 M.A.Stegman,R.G.Quercia,J.Ratcliffe,L.Ding,andW.R.Davis

fraction account for a disproportionately large share of total delinquencyspellsanddefaults.

Againstthisoverallbackdrop,wefindthatevenaftercontrollingforloanand borrower characteristics and regional economic conditions, the oddsthata late-payingborrowerwillmanagetocatchuponpayments insteadofsinkingintoseriousdelinquencycanvaryasmuchas60percentbetweenservicers.Thissuggeststhatservicingstrategiesdomatter.

Weshouldalsonotethat,assuggestedbyindustrydataaswellasourowninterviews,defaultmanagementcostsdriveservicingprofits,andloanservic-ingremainsa labor-intensiveprocess,smart technologiesnotwithstanding.Someservicersweinterviewedstillvaluepersonnelovertechnology.Whilethismaybeawisechoiceintheshortrun,withoutthedecision-makingtech-nology thatwillbecomethe industrystandard,affordable lenderswill lagbehindindustrybenchmarksoverthelongterm,andmorelow-andmoder-ate-incomeborrowersthannecessarywilllosetheirhomes.

Withtherateofappreciationforhousingpricesslowing,therangeofcost-effectiveworkoutoptionsthatwouldenabledefaultedborrowerstoremainintheirhomesmaybenarrowing,sothatitbecomesevenmoreimportanttodiffusesmartservicingtechnologiesaswidelyaspossibleamongaffordablehousinglendersandservicers.Theevidencethatpreventiveservicingreallyworksshouldspurfoundationandgovernmentsupportforthedisseminationofbestpractices.Forexample,foundationandgovernmentgrantsforaccessandtrainingcouldacceleratetherateatwhichthesesmartservicingsystemsareadoptedbysmallerlendersandservicersofaffordablemortgages.Andthis,inturn,couldmaketheirpreventiveservicingeffortssmarterandmorecost-effective.

Finally,policyaimedataffordablehomeownershipshouldbemoresym-metrical;mortgageinnovationsthatlowerthecostofentrymustbematchedbysupportformoresophisticatedservicingsystems.Intheresearchrealm,thereisanurgentneedforsystematic,firm-levelstudiesofservicingpracticesforaffordablemortgages.Asthepresentstudysuggests,withoutbeingableto“unbundle”servicingactivitiesandobservehowfirm-levelpracticesareactuallyimplemented,definingbestpracticeswillbeimpossible.

AuthorsMichaelA.StegmanisthedirectorofPolicyfortheProgramonHuman

and Community Development at the John D. and Catherine T. MacAr-thur Foundation. Roberto G. Quercia is an associate professor of CityandRegionalPlanningattheUniversityofNorthCarolinaatChapelHill.

HOUSING POLICY DEBATE

PreventiveServicingandAffordableHomeownershipPolicy 275

Janneke Ratcliffe is the associate director of the Center for CommunityCapitalismattheUniversityofNorthCarolinaatChapelHill.LeiDingisaseniorresearchassociateattheCenterforCommunityCapitalismattheUniversityofNorthCarolinaatChapelHill.WalterR.DavisistheprincipalmethodologistatStatisticsNewZealand.

TheauthorsthankPhilipE.Comeau,AmyCrewsCutts,DebbieKehr,andMarquitaWebbfortheirhelpfulcommentsandsuggestionsandgrate-fullyacknowledgetheFordFoundationforitssupportofthisresearch.

References

Abraham,Jesse.1999.ALifePreserverforLoans.MortgageBanking59(9):56–65.

AllRegs.com.2006.FannieMaeSingle-FamilyGuides:2002SellingGuide.WorldWideWebpage<http://www.allregs.com>(accessedJuly10,2006).

Baku, Esmail, and Marc Smith. 1998. Loan Delinquency in Community LendingOrganizations:CaseStudiesofNeighborWorksOrganizations.HousingPolicyDebate9(1):151–75.

Caldwell, J.H., and Elizabeth Jordan, 2006. Unleashing the Power. DrivingProfits through Risk-Based Mortgage Collections. Deloitte. World Wide Web page<http://www.deloitte.com/dtt/cda/doc/content/US_FSI_UnleashingthePower_MBStudy.pdf>(accessedJuly11,2007).

CaliforniaRealEstateCenter.com. 2006. Mortgage Payment Behind? World Wide Webpage <http://www.Californiarealestatecenter.com/mortgage-payment-behind.htm>(accessedJuly11,2007).

Capone,CharlesA.Jr.,andAlbertMetz.2003.MortgageDefaultandDefaultResolu-tions:TheirImpactonCommunities.PaperpresentedattheFederalReserveBankofChi-cagoConferenceonSustainableCommunityDevelopment,Washington,DC.March27.

Center for Community Self-Help. 2003. Self-Help Servicing Manual, rev. January 1.Durham,NC.

CenterforCommunitySelf-Help.n.d.ComparisonofSelf-HelpBorrowerswithThoseforConformingLoansPurchasedbyGSEs.Unpublishedpaper.Durham,NC.

Computer SciencesCorporation. 2004.CSCAcquiresMortgage IndustryUtility fromFreddieMac:CompanyPlans toExpandDefaultManagement Services. Press release,February19.WorldWideWebpage<http://www.csc.com/solutions/managementconsult-ing/news/2599.shtml>(accessedJuly11,2007).

Cordell, Larry. 2001. Innovative Servicing Technology: Smart Enough to SustainHomeownershipGains?Paperpresentedatthe2001ConferenceonHousingOpportu-nity,sponsoredbytheResearchInstituteforHousingAmerica,Washington,DC.April26.

HOUSING POLICY DEBATE

276 M.A.Stegman,R.G.Quercia,J.Ratcliffe,L.Ding,andW.R.Davis

Cornwell,Ted.2003.FannieMaeSeesaContinuedRiseinWorkoutRatiosduring2003.NationalMortgageServicingNews27(25):7.

Cutts,AmyCrews,andRichardK.Green.2005.InnovativeServicingTechnology:SmartEnoughtoKeepPeopleinTheirHouses?InBuildingAssets,BuildingCredit:CreatingWealthinLow-IncomeCommunities,ed.NicolasP.RetsinasandEricS.Belsky,348–78.Washington,DC:BrookingsInstitutionPressandJointCenterforHousingStudies.

Deng,Yongheng,andStuartA.Gabriel.2002.EnhancingMortgageCreditAvailabilityamongUnderservedandHigherCredit-RiskPopulations:AnAssessmentofDefaultandPrepaymentOptionExerciseamongFHA-InsuredBorrowers.WorkingPaperNo.02–10.UniversityofSouthernCalifornia,MarshallSchoolofBusiness.

DeZube,Dona.2003.RunawayChurn.MortgageBanking63(5):46–52.

FannieMae.2005a.FannieMaeRiskProfiler®4.0UserGuide.Washington,DC.

Fannie Mae. 2005b. Servicing Changes to Risk Profiler®. Announcement No. 05–01.Washington,DC.

FHACites90,000LossMitCases.2005.NationalMortgageNews30(5):91.

Fields,RuthG.2001.RescuingLatepayers.MortgageBanking61(5):24–28.

Fishbein,AllenJ.,andPatrickWoodall.2006.ExoticorToxic?AnExaminationoftheNon-TraditionalMortgageMarketforConsumersandLenders.Washington,DC:Con-sumerFederationofAmerica.

Freddie Mac. n.d. EarlyIndicatorSM Version 5.0 Overview. World Wide Web page<http://www.freddiemac.com/service/earlyind/pdf/eiv5overview.pdf> (accessed February9,2006).

Harney,Kenneth.2002.It’sBetterNottoForeclose,Home-LoanGiantsFind.Washing-tonPost,November9.

Herbert,Christopher,DebbieGruenstein,andKimberlyBurnett.2000.AnAssessmentofFHA’sSingle-FamilyMortgageInsuranceLossMitigationProgram.CambridgeMA:AbtAssociatesInc.

Holder,Mary.2005.PersonalinterviewwiththeLossMitigationandServicingManageratSelf-Help,September24.

Home Mortgage Disclosure Act. 2001. Public Loan Origination Records. From com-puter-generatedtablesprovidedtoauthorsbyHaroldL.Bunce,deputyassistantsecretaryforEconomicAffairs,U.S.DepartmentofHousingandUrbanDevelopment,onJune12,2003.

InsideMortgageFinance.2006.The2006MortgageMarketStatisticalAnnual.Vol. I.ThePrimaryMarket.Bethesda,MD.

JointCenterforHousingStudies.2005.TheStateoftheNation’sHousing2005.Cam-bridge,MA.

HOUSING POLICY DEBATE

PreventiveServicingandAffordableHomeownershipPolicy 277

Kehr,Debbie.2005.Telephone interviewwith theDirectorofServicingOperationsatFannieMae,August30.

Knox,Noelle.2006.SomeHomeownersStruggletoKeepUpwithAdjustableRates.USAToday,April3,p.A1.

Lipman,BarbaraJ.2005.TheHousingLandscapeforAmerica’sWorkingFamilies2005.NewCenturyHousing5(1):1–56.

McConnell,JohnJ.1976.ValuationofaMortgageCompany’sServicingPortfolio.Jour-nalofFinancialandQuantitativeAnalysis11(3):433–53.

Melchiorre, Camillo T. 1999. Hitting Home Runs in Servicing. Mortgage Banking59(5):32–39.

Meyer, Laurence H. 1997. Models for Neighborhood Development and Reinvest-ment.SpeechattheAnnualMeetingonNeighborhoodHousingServicesofNewYorkCity, June 18. World Wide Web page <http://www.federalreserve.gov/BoardDocs/Speeches/1997/199706182.htm>(accessedJuly15,2007).

Mortgage Bankers Association. 2005. National Delinquency Survey: Second Quarter2005.Washington,DC.

MortgageNewsDaily.com.2005.ForeclosureHappens,ButThereAreSolutions.WorldWide Web page <http://www.mortgagenewsdaily.com/822005_Default_Mortgage.asp>(accessedJuly11,2007).

Mozilo,AngeloR.2000.LoanWorkoutPrograms:ABestBusinessPractice.MortgageBanking60(10):17–18.

Muolo,Paul.2000.TheRushtoBuyReceivables.U.S.Banker110(5):56–58.

Now,“AffordableServicing.”2005.NationalMortgageNews29(23):1,26.

O’Connor, Robert. 2003. Rescuing Borrowers at Risk. Mortgage Banking Magazine64(3):26–31.

Oliver,GeoffreyA.,TimothyDavis,BernadetteKogler,andJeffreyKlein.2001.ProfitableServicersintheNewMillennium.MortgageBanking61(9):32–41.

Quercia,RobertoG.,GeorgeW.McCarthy,andSusanM.Wachter.2003.TheImpactsofAffordableLendingEffortsonHomeownershipRates.JournalofHousingEconomics12(1):29–59.

Quercia,RobertoG.,andMichaelA.Stegman,1992.ResidentialMortgageDefault:AReviewoftheLiterature.JournalofHousingResearch3(2):341–79.

Quercia,RobertoG.,MichaelA.Stegman,WalterR.Davis,andEricStein.2002.Per-formanceofCommunityReinvestmentLoans:ImplicationsforSecondaryMarketPur-chases.InLow-IncomeHomeownership:ExaminingtheUnexaminedGoal,ed.NicolasP.RetsinasandEricS.Belsky,348–74.Washington,DC:BrookingsInstitutionPressandJointCenter forHousingStudies.Alsoavailableat<http://www.kenan-flagler.unc.edu/assets/documents/CC_reinvestment.pdf>.

HOUSING POLICY DEBATE

278 M.A.Stegman,R.G.Quercia,J.Ratcliffe,L.Ding,andW.R.Davis

Russell, Julie. 2005. An Exploration of Successful Default Management Strategies forAffordableHomeLoans.Master’sthesis.UniversityofNorthCarolinaatChapelHill.

Sichelman,Lew.2001.CompassionateServicing.MortgageBanking61(5):16–23.

Sjaastad, John E., Jason Vinar, Philip Jones, and Jeremy Prahm. 2005. DelinquencyDynamics:ServicerEffects.MarketPulse1:1–24.

Stanton,ThomasH.2001.Opportunities forReducingDelinquencies andDefaults inFederalHousingCreditPrograms:AReviewofNewTechnologiesandPromisingPrac-tices.JournalofPublicBudgeting,Accounting,&FinancialManagement13(2):157–92.

StataCorporation.2003.StataProgrammingReferenceManual,Release8.CollegeSta-tion,TX:StataPressPublications.