president, skf automotive market (710.22 kb)

TRANSCRIPT

SKF Capital Markets Day Automotive Market

• SKF Automotive Market • Market and SKF reality

• Strategy

• Application driven innovation • Core application/product

• Core capabilities

• Create and capture customer value • Competitiveness

• Success stories

• Summary

Agenda

© SKF Group

What’s on the automakers agenda?

3 November, 2015 Slide 3

Source: Prime research -World Car of the Year Study Global Automotive Trends 2014

Focusing efficiency for emission reduction

(Engine downsizing and component weight reduction)

Increasing standardization of platforms and modules

Increasing cost competition from continued flat net vehicle

pricing and consumer demand on higher value content

Hybrid and fully electric powertrains

Confidence in growth of compact affordable cars still strong

© SKF Group

Implications for SKF Automotive Market: a combination of opportunities and threats

Supplier profits pools for mechanical systems are squeezed

Smaller / affordable cars increase cost pressure on

component suppliers

Friction reduction driven by legislation and green agenda

Weight reduction holds great potential

E-commerce channel for after market sales,

efficient logistics supply chain enabler for success

3 November, 2015 Slide 4

Source: SKF analysis

© SKF Group

SKF Automotive Market business

3 November, 2015 Slide 5

Seals

Ball and Taper

bearings

Wheel &

suspension

bearings

Other*

5. ILJIN

4. SCH 3. NTN

2. NSK

1. SKF

9. OTHER 8. TIM

7. CHINESE

6. JTEKT

*) >10 Product lines

9. OTHER

8. ILJIN

7. TIM

6. JTEKT

5. NSK

4. NTN

3. SKF

2. CHINESE

1. SCH

Product portfolio

Auto bearings

market shares

Hub bearing unit

market shares Top customers

Sales by region

Latin America

India

China

Eastern Europe

Asia excl. China & India

Western Europe

North America

18.3 BSEK

2014

© SKF Group

Where we come from

• Pioneered with hub and suspension bearing units

• Leadership in deep groove ball bearings

• Strong manufacturing footprint of small tapered roller bearings

• Vehicle aftermarket penetration benefiting from global image

of SKF

3 November 2015 Slide 6

Strong heritage

We have built

on a market

leadership

…however

• Local technical support through global application engineering

• Global manufacturing footprint

• World coordinated sales to cope with global platform offer

© SKF Group

TURN AROUND PLAN to address cost

• Addressing market requirements with the right cost/performance positioning

• Developing the aftermarket business model to fit market needs and new channels

What are we doing differently?

• Refocusing product portfolio to fewer product lines aligned with core capabilities

FOCUSED ACTIVITIES

1

2

© SKF Group

Turn Around Plan launched

Productivity Taking advantage of the synergies we get

from our new simplified organizational structure

Manufacturing Focusing on ongoing restructuring projects

footprint

Application specific Reducing our cost by tailoring specifications to

performance usage needs

Supplier optimization Focusing on direct and indirect material, services and logistics

Manufacturing Focusing on World Class Manufacturing processes,

technologies such as intelligent grinding

1

2

3

4

5

Priorities

© SKF Group

Main activities in Turn Around Plan

3 November 2015 Slide 9

Productivity Staff reduction vs end 2014

Supplier optimization

• Vehicle aftermarket resourcing

program

• New suppliers approval program

• Inbound transport project

• Global indirect material

consolidated purchasing

Manufacturing

technologies

• Cold rolling

• Intelligent grinding

• Operational improvements

1

4

-5,0% -10,0%

-7,0%

2016

FC

2015

FC

2015

YTD

2014

Application specific

performance

• Differentiated material and

specification.

• Aftermarket wheel bearing

material

Manufacturing footprint

2

On-going restructuring Closed

• Component factory, France end 15

• Kit operation, Sweden end 15

• Seals Plant, US end 16

Further restructuring under development

3 5 Targeting 8%

© SKF Group

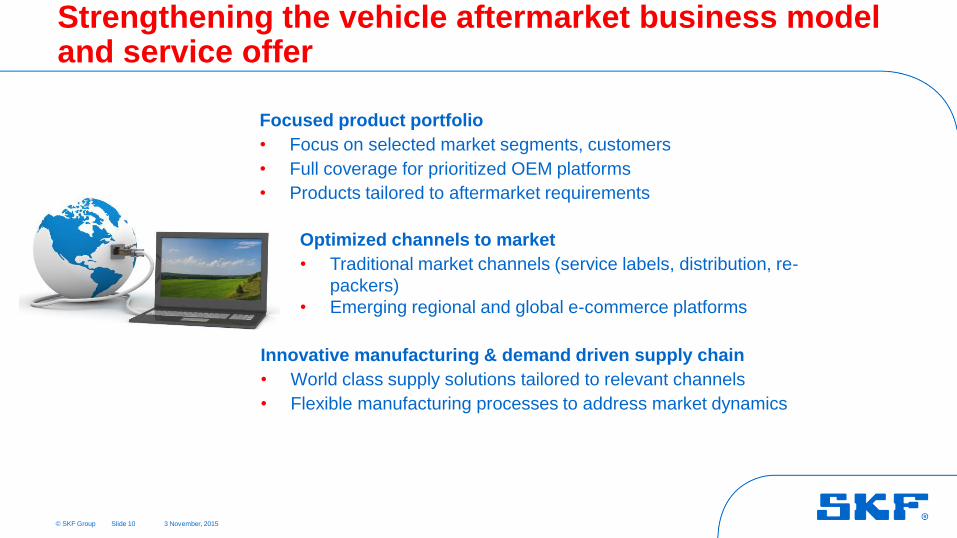

Strengthening the vehicle aftermarket business model and service offer

3 November, 2015 Slide 10

Optimized channels to market

• Traditional market channels (service labels, distribution, re-

packers)

• Emerging regional and global e-commerce platforms

Focused product portfolio

• Focus on selected market segments, customers

• Full coverage for prioritized OEM platforms

• Products tailored to aftermarket requirements

Innovative manufacturing & demand driven supply chain

• World class supply solutions tailored to relevant channels

• Flexible manufacturing processes to address market dynamics

© SKF Group

Product portfolio development

3 November, 2015 Slide 11

Core products

Future

Core capabilities

Today

• Performance and feature leadership of hub bearing units

• Friction management in SKF bearings (balls & tapers)

• Selected automotive special products

• Seals portfolio supporting bearing business and enabler for friction reduction

• Develop game changer products in wheel end

• New solutions for next generation powertrains

© SKF Group

We are….

… stretching our internal capabilities!

• To build up a more competitive structure

• Deployed around our core business

• Dedicated to a more focused agenda to deliver application driven solutions with higher competitiveness and differentiation potential.

From process experts to product innovators!

3 November, 2015 Slide 12