presentation to: global packaging consolidation - … · global packaging consolidation: lead, ......

TRANSCRIPT

Presentation to:Presentation to:

Global Packaging Consolidation:Lead, Follow, or Get Out of the WayLead, Follow, or Get Out of the Way

March 11, 2010 Orlando, Florida

www.blaige.com

Page 2

Bl i & C p nBl i & C p n

Pure Focus. Premier Value.Pure Focus. Premier Value.SMSM

Blaige & CompanyBlaige & Company

Blaige & Company’s Pure Focus has resulted in its position as the largest specialty investment bank of its kind.

Our advantage is rooted in two unique and significant capabilities: Strategic and operational approach (rather than financial/transactional)

Pl i k i d h i l l Plastics, packaging, and chemicals only.

Blaige & Company’s senior advisory professionals have personallyg p y y p p ymanaged, owned, or visited over 600 plastic, packaging, and chemicaloperations in 40 countries and have completed over 150 value-enhancing transactions in plastics packaging and chemicalsenhancing transactions in plastics, packaging, and chemicals.

© Copyright 2010, All Contents Thomas Blaige & Co. LLC

Page 3

Major Themes Reflected in Packaging in Major Themes Reflected in Packaging in M&A in 2010M&A in 2010M&A in 2010M&A in 2010

© Copyright 2010, All Contents Thomas Blaige & Co. LLC

Page 4

M j r Th R fl t d in P k in M&A in 2010M j r Th R fl t d in P k in M&A in 2010Major Themes Reflected in Packaging M&A in 2010Major Themes Reflected in Packaging M&A in 2010Strategic Objectives Driving DealsStrategic Objectives Driving Deals

Mega DealsMega Deals Increasing CompetitionIncreasing Competition Mega DealsMega Deals –– Increasing CompetitionIncreasing Competition

Critical MassCritical Mass –– Raw Material Cost SavingsRaw Material Cost Savings

ReachReach –– Accommodate Global CustomersAccommodate Global Customers

CC M i l d P Fl ibiliM i l d P Fl ibili CrossoverCrossover –– Material and Process Flexibility Material and Process Flexibility

TalentTalent –– Scarcity of Management Talent Scarcity of Management Talent y gy g

CapitalCapital –– Tight Credit MarketsTight Credit Markets

© Copyright 2010, All Contents Thomas Blaige & Co. LLC

Page 5

Packaging Industry Packaging Industry Global ConsolidationGlobal ConsolidationGlobal ConsolidationGlobal Consolidation

© Copyright 2010, All Contents Thomas Blaige & Co. LLC

Page 6

P k in Ind tr Gl b l C n lid ti nP k in Ind tr Gl b l C n lid ti n

Packaging Converters = Squeezed

Packaging Industry Global ConsolidationPackaging Industry Global ConsolidationThe “Squeeze” Results from Upstream, Downstream and Competitive Pressure

S li C

Need for Differentiation

of ProductSupplier

ConsolidationCustomer

Globalization

Packaging Manufacturers and

Converters

Raw Materials Price Volatility

Customer Consolidation

MaturingMaturing Growth

© Copyright 2010, All Contents Thomas Blaige & Co. LLC

Page 7

P k in Ind tr Gl b l C n lid ti nP k in Ind tr Gl b l C n lid ti nPackaging Industry Global ConsolidationPackaging Industry Global ConsolidationEvolution across packaging types show that Flexible Packaging is due for Significant Consolidation

SegmentSegment 19801980 20102010

3 Leaders: 90% share 3 Leaders: 90% share (An h r O n St(An h r O n St G b inG b in))Glass (Bottles)Glass (Bottles) 19 competitors19 competitors (Anchor, Owens, St. (Anchor, Owens, St. GobainGobain))

Metal Metal //

4 Leaders: 80% share4 Leaders: 80% share(Food/Beverage (Food/Beverage Cans)Cans)

39 competitors39 competitors (Ball, Crown, Silgan, Rexam)(Ball, Crown, Silgan, Rexam)

Fl ibl (Pl ti )Fl ibl (Pl ti )4 Leaders: 34% share 4 Leaders: 34% share (A B i P i tp k S l d(A B i P i tp k S l dFlexible (Plastic) Flexible (Plastic)

PackagingPackagingMany competitorsMany competitors

(Amcor, Bemis, Printpack, Sealed (Amcor, Bemis, Printpack, Sealed Air)Air)

© Copyright 2010, All Contents Thomas Blaige & Co. LLC

Page 8

P k in Ind tr Gl b l C n lid ti nP k in Ind tr Gl b l C n lid ti n

Entrepreneurial Companies (Regional)

Packaging Industry Global ConsolidationPackaging Industry Global ConsolidationConsolidation Squeezing the “Middle Market”

p p ( g )Energetic, creative, responsive

Below competitive radarDesignated laboratory for new ideas, products, markets

Consolidators (Global) Purchasing power (sourcing)Purchasing power (sourcing)

Production scaleDistribution controlPersonnel resources

Research & development and capital funding

© Copyright 2010, All Contents Thomas Blaige & Co. LLC

Page 9

P k in Ind tr Gl b l C n lid ti nP k in Ind tr Gl b l C n lid ti nPackaging Industry Global ConsolidationPackaging Industry Global ConsolidationThe “Leaders,” “Followers,” and “Others”The “Leaders,” “Followers,” and “Others”

Top Consolidators Static Participants Consolidatees(“Leaders”) (“Others”) (“Followers”)

• 20% of universe• Rapidly gaining share

A i i i i d

• 60% of universe• Share erosion

M d l i

• 20% of universe• Rapidly losing share

R i d di i• Aggressive acquisitions and divestitures

• Market domination via best acquisitions, selective

• Mergers and selective acquisitions

• Pursue niche leadership

• Restructuring and divestitures • Sell at maximum Price

divestitures

© Copyright 2010, All Contents Thomas Blaige & Co. LLC

Page 10

M&A Activity in the Global Packaging M&A Activity in the Global Packaging MarketsMarketsMarketsMarkets

© Copyright 2010, All Contents Thomas Blaige & Co. LLC

Page 11

M&A Activity in the Global Packaging Markets 2002M&A Activity in the Global Packaging Markets 2002--20092009M&A Activity in the Global Packaging Markets 2002M&A Activity in the Global Packaging Markets 2002--2009 2009 1,308 Packaging Transactions Analyzed by Blaige & Company1,308 Packaging Transactions Analyzed by Blaige & Company

Packaging Segments

Metal2%

Glass1%

Plastic72%

Fiber25%

Source: Blaige & Co. Proprietary Research

© Copyright 2010, All Contents Thomas Blaige & Co. LLC

Page 12

M&A Activity in the Global Packaging Markets 2002M&A Activity in the Global Packaging Markets 2002--20092009M&A Activity in the Global Packaging Markets 2002M&A Activity in the Global Packaging Markets 2002--2009 2009 1,308 Packaging Transactions Analyzed by 1,308 Packaging Transactions Analyzed by BlaigeBlaige & Company& Company

Plastic Packaging Fiber Packaging Metal and Glass Packaging

Metal53%

Glass47%

Flexible48%Rigid

52%

Corrugated26%

Folding Carton24%

52%Label20%

Diversified16%

Integrated / Paper Making

14%

45 Transactions 3% of Packaging

323 Transactions 25% of Packaging

940 Transactions 72% of Packaging 3% of Packaging

transactions25% of Packaging

transaction72% of Packaging

transactions

© Copyright 2010, All Contents Thomas Blaige & Co. LLC

Page 13

M&A Activity in the Global Packaging MarketsM&A Activity in the Global Packaging Markets

2009 Plastic Packaging M&A is active in all flexible and rigid plastics segments M&A Activity in the Global Packaging Markets M&A Activity in the Global Packaging Markets

Other Machinery &

Injection Molding

20%

11%y

Tooling10%

Blow Molding7%20% 7%

Thermoforming6%

Distribution4%

Foam4%

143 Transactions

Film & Sheet38%

Source: Blaige & Co.© Copyright 2010, All Contents Thomas Blaige & Co. LLC

143 Transactions

Page 14

M&A Activity in the Global Packaging MarketsM&A Activity in the Global Packaging Markets

Plastic packaging deals nearly triple from 50 deals in 2002 to 143 in 2009.• Both flexible and rigid sectors are active

M&A Activity in the Global Packaging Markets M&A Activity in the Global Packaging Markets

Plastic Packaging Accounts for 30% of All Plastics DealsPlastic Packaging Accounts for 30% of All Plastics Deals

Both flexible and rigid sectors are active

Global Plastic Packaging M&A ActivityGlobal Plastic Packaging M&A Activity160

143Average = 118 deals

6%ng

Dea

lsn

g D

eals

59 4152 72

87 96100

120

140125

115126

138 140

103

143Average = 118 deals

CA

GR

1

Pac

kagi

nP

acka

gin

66 74 74 6653 43 47

19

60

20

40

60

80

50

3143 47

0

20

2002 2003 2004 2005 2006 2007 2008 2009

Flexible Rigid

Source: Blaige & Co.© Copyright 2010, All Contents Thomas Blaige & Co. LLC

Page 15

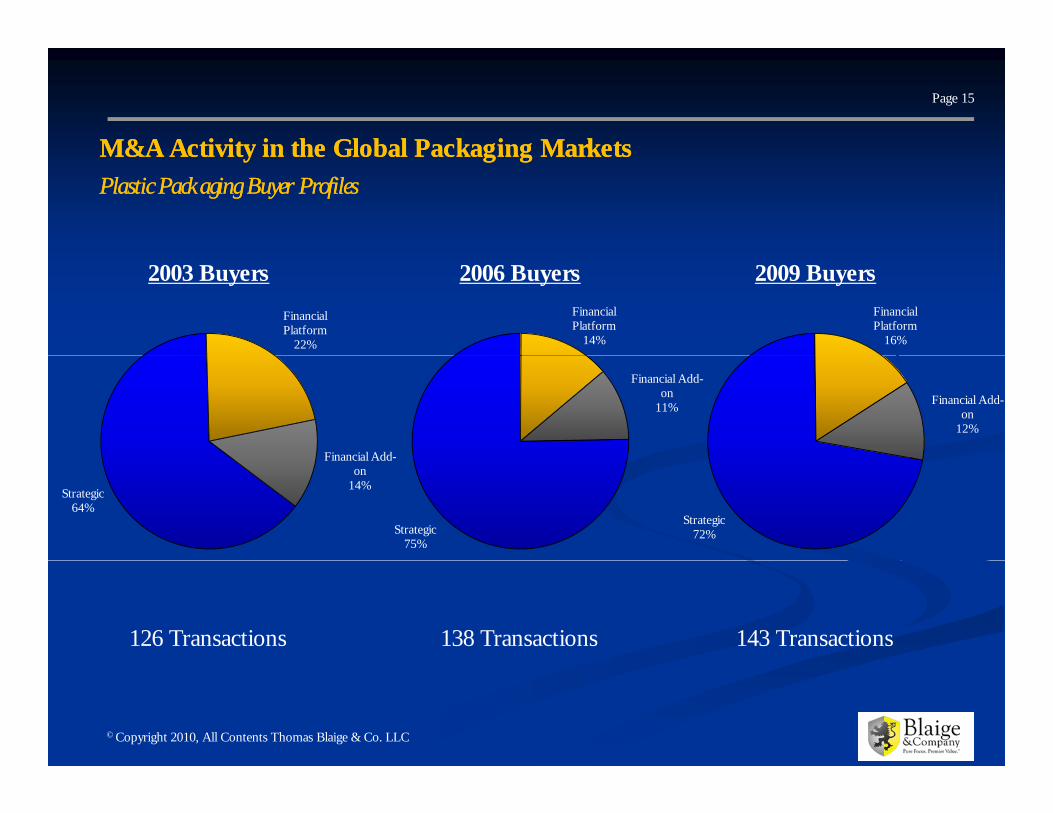

M&A Activity in the Global Packaging MarketsM&A Activity in the Global Packaging MarketsM&A Activity in the Global Packaging Markets M&A Activity in the Global Packaging Markets

Plastic Packaging Buyer ProfilesPlastic Packaging Buyer Profiles

2003 Buyers 2009 Buyers

Financial Platform

16%

Financial Platform

22%

2006 Buyers

Financial Platform

14%

Financial Add-on

12%

Financial Add-

Financial Add-on

11%

Strategic72%

Strategic64%

Financial Add-on

14%

Strategic75%

143 Transactions126 Transactions 138 Transactions

© Copyright 2010, All Contents Thomas Blaige & Co. LLC

Page 16

M&A Activity in the Global Packaging MarketsM&A Activity in the Global Packaging MarketsM&A Activity in the Global Packaging Markets M&A Activity in the Global Packaging Markets

Plastic Packaging Seller ProfilesPlastic Packaging Seller Profiles

2009 Sellers2003 Sellers 2006 Sellers

Private Sellers54%

Corporate Divestitures

35%Private Sellers

57%

Corporate Divestitures

38%Private Sellers

Corporate Divestitures

35%

Financial Sellers11%

57%

Financial Sellers5%

62%

Financial Sellers3%

126 Transactions 143 Transactions138 Transactions

11% 5%

© Copyright 2010, All Contents Thomas Blaige & Co. LLC

Page 17

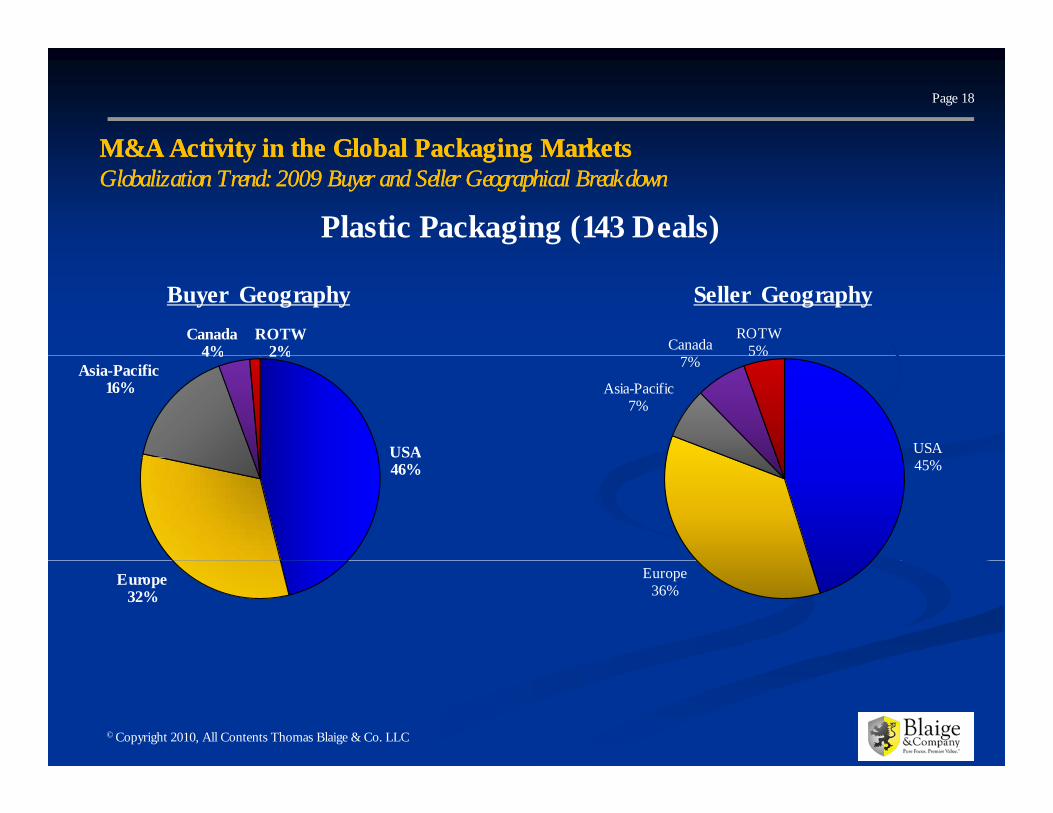

M&A Activity in the Global Packaging MarketsM&A Activity in the Global Packaging MarketsM&A Activity in the Global Packaging Markets M&A Activity in the Global Packaging Markets

Plastic Packaging Geography Profile: Growth in International and CrossPlastic Packaging Geography Profile: Growth in International and Cross--Border TransactionsBorder Transactions

2009 G h2009 Geography

International /

U.S. / U.S.34%

International50%

U.S. / International

16%

143 Transactions

16%

© Copyright 2010, All Contents Thomas Blaige & Co. LLC

143 Transactions

Page 18

M&A Activity in the Global Packaging MarketsM&A Activity in the Global Packaging Markets

Plastic Packaging (143 Deals)

M&A Activity in the Global Packaging Markets M&A Activity in the Global Packaging Markets Globalization Trend: 2009 Buyer and Seller Geographical BreakdownGlobalization Trend: 2009 Buyer and Seller Geographical Breakdown

Seller GeographyBuyer Geography

Canada4%

ROTW2% Canada

ROTW5%

USA

Asia-Pacific16%

4% 2%

USA

Asia-Pacific7%

7%5%

46% 45%

Europe32%

Europe36%

© Copyright 2010, All Contents Thomas Blaige & Co. LLC

Page 19

M&A Activity in the Global Packaging MarketsM&A Activity in the Global Packaging Markets

Key 2008 2009Number I

Percent I

M&A Activity in the Global Packaging Markets M&A Activity in the Global Packaging Markets 2009 Film & Sheet Activity is Very Strong 2009 Film & Sheet Activity is Very Strong –– Particularly in the U.S.Particularly in the U.S.

Total Deals

U.S. Participation Deals

U.S. Only Deals

yIncrease Increase

All Segment Deals 76 88 12 16%

U.S./U.S. + U.S./International 25 39 14 56%

U.S./U.S. 12 31 19 158%y

Non-U.S. Only Deals

Non-U.S. Participation Deals

Financial Deals

P k i D l

International/International + U.S./International 64 57 -7 -11%

International/International 51 49 -2 -4%

Private Equity/Financial Buyer or Seller 23 23 0 0%

T P d P k i P d 45 55 10 22%Packaging Deals

Non-Packaging Deals

Corporate Divestitures

Financial Divestitures

Target Produces Packaging Products 45 55 10 22%

Target Does Not Produce Packaging Products 31 33 2 6%

Corporate Seels Assets, Plant(s), Division, etc. 36 36 0 0%

Private Equity Sells Portfolio Company 4 2 -2 -50%

Automotive DealsMedical Deals

q y f p y

Target Produces Automotive Products 3 2 -1 -33%Target Produces Medical Products 4 10 6 150%

© Copyright 2010, All Contents Thomas Blaige & Co. LLC

Source: Blaige & Company Proprietary Research

Page 20

90100

Film & Sheet

Headline DealsAverage = 66 deals

Deal Activity

76

88

5262 58 43

41

4555

4050607080 Sigma Plastics completes 23rd deal since 1991

Ampac completes 10 deals since 2000 Bemis Co. completes 21st deal since 1990 Berry Plastics / Pliant Corporation31

64

74 74

6658

76

9 12 12 16 23 1731 3322

41

0102030

2002 2003 2004 2005 2006 2007 2008 2009

Berry Plastics / Pliant Corporation One Equity Partners / Constantia Packaging AG

31

2002 2003 2004 2005 2006 2007 2008 2009

Industrial Packaging

U.S./U.S.

2009 Buyers 2009 Geography

Financial

FinancialPlatform

13%Strategic Buyers78%

International/International

57%

34%

U.S./I i lF a c a

Add-On9%

78% International9%

Source: Blaige & Company© Copyright 2010, All Contents Thomas Blaige & Co. LLC

Page 21

6160

70

s

Deal ActivityHeadline Deals

YORK Label completes 9th deal sinceAverage = 38 deals

Label

28 30

51

3641

20

30

40

50

Tra

nsa

ctio

ns 2003 CCL completes 15 deals since 2003 Multi-Color Corp. completes 5 deals since

200322

0

10

20

2003 2004 2005 2006 2007 2008 2009

2003 Nashua sold to Cenveo in 2009

Financial

2009 Buyers 2009 Geography

Financial Add

Financial Platform

17%StrategicBuyers76%

International/International

45%

U.S./U.S.48%

Add-On7% U.S/

International7%

© Copyright 2010, All Contents Thomas Blaige & Co. LLC Source: Blaige & Company

Page 22

Packaging Industry Global Consolidation Packaging Industry Global Consolidation 2000’s Top 50 Flexible Packaging Companies* - Today

AEP Industries Inteplast Group Ltd.Sonoco High Density Film Products Division

Southern Film Extruders

g g yg g y

AET FilmsInternational Paper Co. Flexible Packaging

Spartech Corporation Pitt Plastics

Atlantis Plastics Custom & Stretch Films

Intertape Polymer Group Inc. Toray Plastics America Inc. Poly-Pak Industries

Bemis Co. Inc. Kama Corporation Transilwrap Co. Inc. InterfilmClopay Plastic Products Co. Klockner-Pentaplast of America Tredegar Film Products Corp. Smurfit-Stone Container Corp.Cryovac Division Mitsubish Polyester Film LLC Tyco Plastics and Adhesives Group Southern Film ExtrudersDow Chemical Inc. Nan Ya Plastics Corporation Vanguard Plastics Inc.DuPont Teejin Films Pactiv Corporation VPI LLCEssex Plastics Pechinery Plastic Packaging Inc. Winpak Ltd. E M bil Ch i l C FilExxonMobil Chemical Co. Films Business

Pliant Corporation Plassein Packaging Corp

Geon Engineered Films Poly America Inc. Heritage Bag Co.Glad Products Inc. Printpack Inc. Intex Plastics Corp.Great Pacific Enterprises Inc. Rexam Inc. HPG International Inc.H it B C R ld M t l C P k i B I

•Source: Plastics News and Blaige & Co.

Heritage Bag Co. Reynolds Metals Co. Packaging Bonar Inc.Honeywell Specialty Chemicals Sigma Plastics Group Fortune Plastics (Clondalkin)

Top 50 Total PercentageEliminated 16 32%Changed Ownership 6 12%U d M&A (A i iti

© Copyright 2010, All Contents Thomas Blaige & Co. LLC

Used M&A (Acquisition or Divestiture)

20 40%

Total 44 84%

Page 23

Packaging Industry Global Consolidation Packaging Industry Global Consolidation 2000’s Top 50 Label Converters Companies* - Today

g g yg g y

Avery Dennison (converting) National Label Company Hammer Lithograph The Label PrintersMoore North America Nashua Corporation Dot Label FB Johnston Groupp J pBrady Corporation Discount Labels Rittenhouse Stoffel SealsCCL Label Inc. L&E Packaging Belmark, Inc. Special Service PartnersStandard Register American Fuji Seal, Inc. Seal-It Sancoa InternationalWallace Computer Systems Spear Dow Industries (Screenprint)Mail Well Alcan Pkg (LawsonMardon) TimeMed Labeling SystemFort Dearborn Company Label Art Advanced Labelworx, Inc.Fleming Potter Company NorthStar Print Group LabeladGraphic Tech. (Nitto Denko) Mutli-Color Corporation Metro Label CompanyIntermec Technologies YORK Label Meyers Label CompanyIntermec Technologies YORK Label Meyers Label CompanyWS Packaging Superior Label Systems BeckettSmyth Companies Topflight Corporation Inland Printing CompanyMPI Label Systems Data-Label Outlook GroupWeber Marketing Systems Walle Corporation Best Label

•Source: Plastics News and Blaige & Co.

Top 50 Total PercentageEliminated 21 42%Changed Ownership 8 16%Used M&A (Acquisition or Divestiture)

4 8%

© Copyright 2010, All Contents Thomas Blaige & Co. LLC

)Total 33 66%

Page 24

Case Studies of Successful Consolidation Case Studies of Successful Consolidation and Growthand Growth

© Copyright 2010, All Contents Thomas Blaige & Co. LLC

Page 25

Case Studies of Successful Consolidation and GrowthCase Studies of Successful Consolidation and GrowthCase Studies of Successful Consolidation and GrowthCase Studies of Successful Consolidation and GrowthSigma Plastics Group Executes Aggressive and Unique Strategic Acquisition ProgramSigma Plastics Group Executes Aggressive and Unique Strategic Acquisition Program InvolvesInvolves strategicstrategic partnershipspartnerships wherebywhereby SigmaSigma acquiresacquires aa majoritymajority shareshare ofof qualityquality

filmfilm extrudersextruders andand helpshelps thethe owner/managersowner/managers buildbuild thethe businessbusiness withwith additionaladditionalfilmfilm extrudersextruders andand helpshelps thethe owner/managersowner/managers buildbuild thethe businessbusiness withwith additionaladditionalresourcesresources..

StrategyStrategy providesprovides maximummaximum upup--sideside forfor bothboth SigmaSigma PlasticsPlastics andand thethe remainingremaining equityequityholdersholders ofof thethe targettargetholdersholders ofof thethe targettarget..

Year Acquisitions Total2010 McNeely Plastics 12009 ISO Poly Films, Sante Fe Extruders, FlexSol 32007 Allied Extruders 12006 Mercury Plastics 12005 PCL Packaging Coastal Division, Filmtech 22004 Mid-Atlantic Bag, FlexSol NC plant, Republic Bag, Target Plastics 42003 Apple Plastics, Orange Plastics 22000 Poly Plastic Products 11999 Roll Pak U.S. stretch film business 11998 Biostar Films, Bio Industries, Aargus Plastics 31996 Essex Plastics 11994 South Eastern Plastics 11992 Great Eastern Plastics 11991 i C bid C di fil b i 1

© Copyright 2010, All Contents Thomas Blaige & Co. LLC

1991 Union Carbide Canadian films business 1Total 23

Page 26

Case Studies of Successful Consolidation and GrowthCase Studies of Successful Consolidation and GrowthCase Studies of Successful Consolidation and GrowthCase Studies of Successful Consolidation and GrowthBemis Co. successfully expands international presence with strategic acquisition.Bemis Co. successfully expands international presence with strategic acquisition. BemisBemis CoCo..’s’s AlcanAlcan Packaging’sPackaging’s FoodFood AmericasAmericas acquisitionacquisition isis thethe largestlargest toto datedate

Year Acquisitions Total2010 Alcan Packaging Food Americas Pending 12009 Huhtamaki Plásticos Rígidos Brasil Ltda and Huhtamaki Argentina S.A. 22005 Dixie Toga 12004 Masterpak S.A.'s Mexico flexible packaging operations 12003 Multi-Fix's pressure sensitive materials business 12002 Clysar, Walki Films 22001 Duralam 1

2000 Arrow Industries' flexible packaging operations, Viskase shrink films, Kanzaki 32000 p g g p , ,Specialty Papers' pressure sensitive materials business

3

1998 Interest in Dixie Toga, Techy International 21997 Paramount Packaging 11996 Perfecseal 11995 Banner Packaging 1g g1994 Fitchburg Coated Products, Hargo Healthcare Packaging 21993 Princeton Packaging's bakery packaging business 11990 Milprint 1Total 21

© Copyright 2010, All Contents Thomas Blaige & Co. LLC

Page 27

Case Studies of Successful Consolidation and GrowthCase Studies of Successful Consolidation and GrowthCase Studies of Successful Consolidation and GrowthCase Studies of Successful Consolidation and GrowthYORK Label/Diamond Castle pursue active acquisition strategyYORK Label/Diamond Castle pursue active acquisition strategy

YORKYORK LabelLabel hashas executedexecuted oneone ofof thethe mostmost successfulsuccessful acquisitionacquisition programsprograms inin thethek ik i ithith d blid bli ff ii 20052005packagingpackaging space,space, withwith aa doublingdoubling ofof revenuesrevenues sincesince 20052005

YORKYORK LabelLabel hashas completedcompleted 99 addadd--onon acquisitionsacquisitions sincesince 20032003

**BlaigeBlaige && CompanyCompany initiatedinitiated thethe SouthernSouthern AtlanticAtlantic LabelLabel transactiontransaction andand actedacted asas thethe BlaigeBlaige && CompanyCompany initiatedinitiated thethe SouthernSouthern AtlanticAtlantic LabelLabel transactiontransaction andand actedacted asas thetheexclusiveexclusive investmentinvestment bankerbanker advisoradvisor toto YORKYORK LabelLabel

Year Activity

2010 *YORK Label acquired Southern Atlantic Label2010 YORK Label acquired Southern Atlantic Label

2008YORK Label acquired Etiprak, S.A. and Etiquetas Industriales, LTDA under Wind Point; Diamond Castle Holdings purchased YORK Label from Wind Point Partners

2007 YORK Label acquired Cameo Crafts and Package Service Company

2006Wind Point Partners purchased YORK Holdings from Huron Capital and merged with Industrial Label Corporation to form YORK Label; acquired LSK Labels and Asheville, NC facility from Quality Assured Label

2002 YORK Holdings acquired by Huron Capital

© Copyright 2010, All Contents Thomas Blaige & Co. LLC

Page 28

Flexible Packaging Valuation MetricsFlexible Packaging Valuation Metrics

© Copyright 2010, All Contents Thomas Blaige & Co. LLC

Page 29

C bl A l i P bli l t d d C blComparables Analysis: Publicly-traded Comparables

Publicly-traded comparables trading at an average of approximately 0.8x Sales, 3.9xGross Profit, and 6.3x EBITDA.

LTM LTM LTM

Sales Gross Profit EBITDA

EV Mulitple ofCompany Ticker

Sales Gross Profit EBITDA

AEP Industries AEPI 0.6x 2.6x 5.2xAmcor Ltd. AMC.AX 0.7x 4.8x 8.2xBemis Company BMS 0.9x 5.0x 7.3xBemis Company BMS 0.9x 5.0x 7.3xPactiv Corporation PTV 1.3x 4.6x 5.4xSealed Air Corporation SEE 1.0x 3.3x 6.0xSpartech Corporation SEH 0.5x 4.3x 7.0xp pWinpak Ltd. WPK-T 0.9x 2.5x 5.0x

Mean Universe Value 0.8x 3.9x 6.3x

© Copyright 2010, All Contents Thomas Blaige & Co. LLC

Page 30

Comparables Analysis: Relevant Transaction ComparablesComparables Analysis: Relevant Transaction ComparablesSelect Publicly Disclosed Flexible Packaging Transactions

7.4x 7.6x8.0x

9.0x

10.0x

Mean = 6.2x

6.5x6.1x

5.2x

7.0x

4.5x 4.5x

7.0x

6.0x 5.9x 6.1x 6.0x

6.8x6.4x

6.0x

6.9x

6.0x

4.0x

5.0x

6.0x

7.0x

4.0x

Transactions reflect an average deal size in excess of $300 million

© Copyright 2010, All Contents Thomas Blaige & Co. LLC

Page 31

Comparables Analysis: Relevant Transaction ComparablesSelect Proprietary Transactions (18) Involving Blaige & Company’s Bankers

Unlike most publicly disclosed transactions, Blaige & Company’s proprietary universe of transactions coversb d f t ti i ith t p i l (“EV”) f d $100 illia broader range of transaction sizes, with a mean enterprise value (“EV”) of under $100 million.

16 0x

TEV Multiple to EBITDA (17 Observations)

13.6x

12.0x

14.0x

16.0x

Adj. Mean = 6.9x

7.0x6.1x

6.7x

9.6x

6.6x6.1x

7.5x6.7x

7.5x 7.7x7.0x 7.0x 7.0x 7.0x

5 8

8.0x

10.0x

6.1x 6.1x5.5x 5.8x

4.0x

6.0x

A B C D E F G H I J K L M O P Q R

© Copyright 2010, All Contents Thomas Blaige & Co. LLC

Note: The Adjusted Mean exclude the “A” data point

Page 32

C bl A l i R l T i C blComparables Analysis: Relevant Transaction ComparablesSelect Proprietary Transactions (18) Involving Blaige & Company’s Bankers

Unlike most publicly disclosed transactions, Blaige & Company’s proprietary universe of transactions coversa broader range of transaction sizes with a mean enterprise value (“EV”) of under $100 milliona broader range of transaction sizes, with a mean enterprise value ( EV ) of under $100 million.

TEV Multiple to Gross Profit (8 Observations)

6 0x

4.3x

5.0x5.4x

4 0 4 0 4 04.5x

5.0x

5.5x

6.0x

Mean = 4.1x

2 5x

4.0x 4.0x 4.0x

3.4x

3.0x

3.5x

4.0x

2.5x

2.0x

2.5x

B C D E F G M P

© Copyright 2010, All Contents Thomas Blaige & Co. LLC

Page 33

Comparables Analysis: Relevant Transaction ComparablesSelect Proprietary Transactions (18) Involving Blaige & Company Bankers

Unlike most publicly disclosed transactions, Blaige & Company’s proprietary universe of transactions coversb d f t ti i ith t p i l (“EV”) f d $100 illi

TEV Multiple to Revenue (18 Observations)

3.0x

a broader range of transaction sizes, with a mean enterprise value (“EV”) of under $100 million.

2.1x

1.7x

2.5x

2.0x

2.5xAdj. Mean = 0.9x

0.9x 0.8x 0.9x0.7x 0.7x

0.8x1.0x

1.2x

0.8x

1.4x

0.5x0.6x

0 4x

1.0x

1.5x

0.3x 0.3x0.4x

0.0x

0.5x

A B C D E F G H I J K L M N O P Q R

Note: The Adjusted Mean exclude the “N” data point

© Copyright 2010, All Contents Thomas Blaige & Co. LLC

Page 34

Comparables Analysis: Relevant Transaction ComparablesSelect Proprietary Transactions (18) Involving Blaige & Company Bankers

Unlike most publicly disclosed transactions, Blaige & Company’s proprietary universe of transactions coversb d f t ti i ith t p i l (“EV”) f d $100 illi

TEV Multiple to Pounds (15 Observations)

4.5x

a broader range of transaction sizes, with a mean enterprise value (“EV”) of under $100 million.

3.8x

3.0x3.5x4.0x

Adj. Mean = 0.7x

0.9x

1.8x

0.6x 0 6x0.9x

0.6x 0 5x 0.7x0.9x 0.7x 0.7x 0 6x

0.9x1.0x1.5x2.0x2.5x

0.3x0.6x 0.6x 0.6x 0.5x 0.6x

0.0x0.5x

A D F G H I J K L M N O P Q R

Note: The Adjusted Mean exclude the “N” data point

Page 35

SummarySummary

© Copyright 2010, All Contents Thomas Blaige & Co. LLC

Page 36

S rS rSummarySummary

Despite fragmentation, consolidation is active among largest players in past decadeDespite fragmentation, consolidation is active among largest players in past decade On v 75% f T p 50 Pl h v b n ff t d b M&AOn v 75% f T p 50 Pl h v b n ff t d b M&A On average, 75% of Top 50 Players have been affected by M&AOn average, 75% of Top 50 Players have been affected by M&A

–– 45% lost identity45% lost identity–– 15% changed ownership15% changed ownership–– 15% used M&A to achieve strategic goals15% used M&A to achieve strategic goals

Selected Sector Consolidation of 2000's Top 50 Companies

Sector

Lost Identity

Changed Ownership Used M&A Total

Flexible Packaging 32% 12% 40% 84%

p p

Flexible Packaging 32% 12% 40% 84%

Label Converters 42% 12% 8% 66%

© Copyright 2010, All Contents Thomas Blaige & Co. LLC

Page 37

K t S in C n lid ti nK t S in C n lid ti nKeys to Success in ConsolidationKeys to Success in Consolidation

Identify SituationIdentify Situation

–– Leader, Follower, or Other?Leader, Follower, or Other?

Adopt StrategyAdopt Strategy

–– Lead, Follow, Or Get Out of the WayLead, Follow, Or Get Out of the Way

E t St tE t St t Execute StrategyExecute Strategy

–– Create a Transaction Team and ExecuteCreate a Transaction Team and Execute

© Copyright 2010, All Contents Thomas Blaige & Co. LLC

Page 38

BlaigeBlaige & Company: Recently Completed Deals& Company: Recently Completed DealsBlaigeBlaige & Company: Recently Completed Deals& Company: Recently Completed Deals

has acquired the pharmaceuticalfolding carton division of

Exclusive representation of H.S. Crocker Co., Inc.

by Blaige & Company L.L.C.

has acquired

P & O Packaging, Ltd.a portfolio company of Pinecrest Capital Inc.

Exclusive representation of P & O Packaging, Ltd.

by Blaige & Company L.L.C.

p p y p

© Copyright 2010, All Contents Thomas Blaige & Co. LLC

Presentation to:Presentation to:

Global Packaging Consolidation:Lead, Follow, or Get Out of the WayLead, Follow, or Get Out of the Way

March 11, 2010 Orlando, Florida

www.blaige.com