presentation by ca. sudha g. bhushan, taxpert professionals

TRANSCRIPT

Deposit and Remittances Foreign Exchange Management Act, 1999

Ghaziabad Branch || CIRC

Institute of Chartered Accountants of India

03rd June 2016

Presentation by: CA. Sudha G. Bhushan

Associate Director – Taxpert Professionals

09769033172 || 07738892291

– Current and capital Account transaction

– Residential Status

– Authorities under FEMA

– Balance Sheet and FEMA

– Various Entities under FEMA

FEW BASIC CONCEPTS

Account

By Person resident in India

Foreign Currency account in India

By Resident Individuals

By other

Account maintained

outside India

BY Resident Individuals

By Others

By Person resident outside

India

By NRI/PIOs

By others

Accounts under FEMA

Fo

reig

n E

xc

ha

ng

e M

an

ag

em

en

t (Fo

reig

n

cu

rren

cy a

cc

ou

nts

by a

pe

rso

n re

sid

en

t

in In

dia

Foreign Exchange Management

(Deposit) Regulations, 2016

Fo

reig

n E

xc

ha

ng

e M

an

ag

em

en

t (Fo

reig

n

cu

rren

cy a

cc

ou

nts

by a

pe

rso

n re

sid

en

t

in In

dia

Account

By person resident in India

Foreign Currency account in India

By Resident Individuals

By other

Account maintained

outside India

BY Resident Individuals

By Others

By Person resident outside

India

By NRI/PIOs

By others

Account By Person resident outside India

Foreign Exchange Management

(Deposit) Regulations, 2016

By Person resident outside India

FCNR(B) account

NRE account

NRO account

Special Non-Resident Rupee Account (SNRR account)

Escrow Account

Deposits by companies

Other

Unincorporated joint ventures (UJV)

shipping or airline company incorporated outside India

For Adjustment in export and import value

Foreign Exchange Management

(Deposit) Regulations, 2016

• Regulations – FEMA 5/2000-RB on Foreign

Exchange Management (Deposit) Regulations,

2000 amended from time to time.

REGULATORY FRAMEWORK

NRE A/C

SCHEDULE 1

FCNR - B A/c

SCHEDULE 2

NRO A/c

SCHEDULE 3

SNRR A/c Schedule 4

Escrow A/c

NON-RESIDENT (EXTERNAL) ACCOUNT

SCHEME (‘NRE ACCOUNT’)

NRIs and PIOs -eligible to open

Rupee Denominated

Savings, Current or fixed deposit

Can be opened by remittance of funds in free

foreign exchange.

Principal and interest both -

Repatriable

Interest lying to the credit of NRE

accounts - exempt from tax

Credits Debit

Inward remittance to India in permitted currency proceeds of account payee cheques, demand

drafts / bankers' cheques, issued againstencashment of foreign currency

transfers from other NRE / FCNR accounts sale proceeds of FDI investments interest accruing on the funds held in such

accounts interest on Government securities/dividends on

units of mutual funds purchased by debit to theNRE/FCNR(B) account of the holder, certain typesof refunds, etc.

local disbursements transfer to other NRE / FCNR accounts of person

eligible to open such accounts, remittance outside India, investments in shares / securities/commercial

paper of an Indian company, etc.

PERMISSIBLE DEBITS/CREDITS

NON RESIDENT (ORDINARY) RUPEE

ACCOUNT

NRIs and PIOsRupee

DenominatedSavings, Current or

Fixed Deposit

Can be opened jointly with residents

NON –Repatriable*

Interest lying to the credit of NRO

accounts is taxable *repatriable subject to conditions

Credits Debit

Proceeds of remittances from outside India through normal banking channels received in any permitted currency.

Any foreign currency, which is freely convertible, tendered by the account holder during his temporary visit to India.

Transfers from rupee accounts of non-resident banks. Legitimate dues in India of the account holder. This

includes current income like rent, dividend, pension, interest, etc.

Sale proceeds of assets including immovable property acquired out of rupee / foreign currency funds or by way of legacy /inheritance.

Resident individual may make a rupee gift to a NRI/PIO who is a close relative of the resident individual [close relative as defined in Section 6 of the Companies Act, 1956] by way of crossed cheque /electronic transfer. The amount shall be credited to the Non-Resident (Ordinary) Rupee Account (NRO) a/c of the NRI / PIO and credit of such gift amount may be treated as an eligible credit to NRO a/c.

All local payments in rupees including payments for investments in India subject to compliance with the relevant regulations made by the Reserve Bank.

Remittance outside India of current income like rent, dividend, pension, interest, etc. in India of the account holder.

Remittance up to USD one million, per financial year (April- March), for all bona fide purposes, to the satisfaction of the Authorised Dealer bank.

Transfer to NRE account of NRI within the overall ceiling of USD one million per financial year subject to payment of tax, as applicable

PERMISSIBLE DEBITS/CREDITS

FOREIGN CURRENCY NON RESIDENT

(BANKS) ACCOUNT

NRIs and PIOs are eligible to open

Denominated in Foreign Currency

Only in the form of term deposit

Accounts can be opened by remittance

of funds in free foreign exchange.

RepatriableRisk of foreign

exchange fluctuations borne by Bank

Credits Debit

Inward remittance to India in permitted currency proceeds of account payee cheques, demand

drafts / bankers' cheques, issued againstencashment of foreign currency

transfers from other NRE / FCNR accounts sale proceeds of FDI investments interest accruing on the funds held in such

accounts interest on Government securities/dividends on

units of mutual funds purchased by debit to theNRE/FCNR(B) account of the holder, certain typesof refunds, etc.

local disbursements transfer to other NRE / FCNR accounts of person

eligible to open such accounts, remittance outside India, investments in shares / securities/commercial

paper of an Indian company, etc.

PERMISSIBLE DEBITS/CREDITS – FCNR

(B) A/C

Any person resident outside India having business interest in

India

Non Interest Bearing

Debits and credits specific to the

business

NEW Schedule 4 RepatriableTransactions subject

to Taxes

Special Non-Resident Rupee Account -

SNRR account

Non resident or Resident together with non resident

Foreign Inward remittance through

Normal Banking channel

Operational for 6 months

NEW Schedule 5 Non interest bearing

Repatriable

(exchange risk to be born by Non

resident)

ESCROW ACCOUNT

LOAN AGAINST THE DEPOSIT

LOAN AGAINST DEPOSIT IN NRE A/C

loan

In India

In INR

To the account Holder

permitted

To third party Permitted

In Foreign Currency

To the account holder

Permitted

To third party Permitted

Outside India

To the account holder

Permitted

To third party Permitted

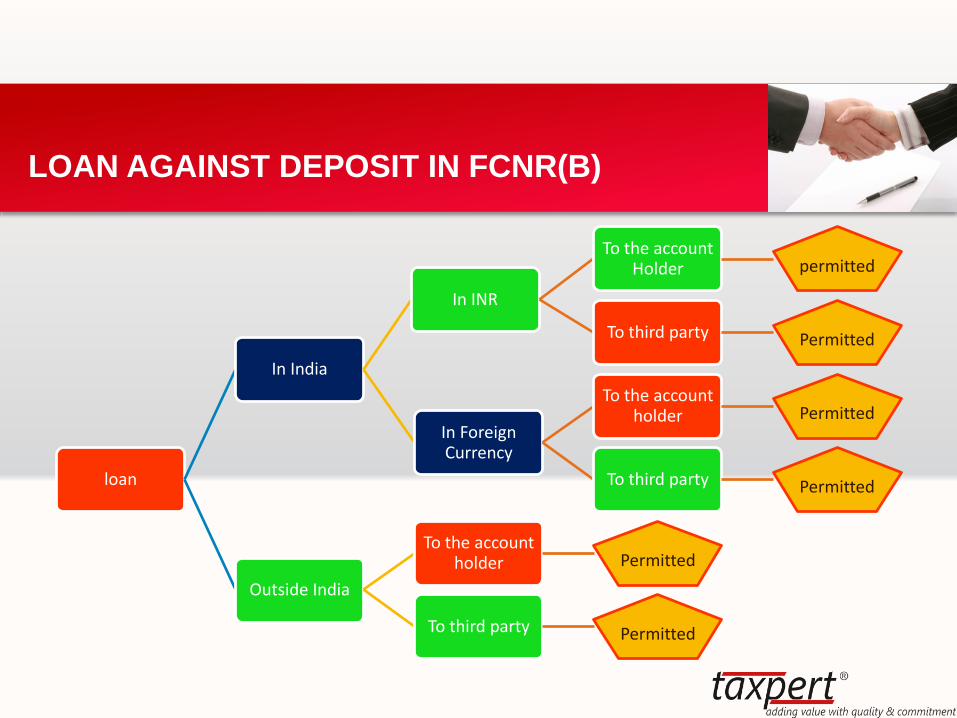

LOAN AGAINST DEPOSIT IN FCNR(B)

loan

In India

In INR

To the account Holder permitted

To third party Permitted

In Foreign Currency

To the account holder Permitted

To third party Permitted

Outside India

To the account holder Permitted

To third party Permitted

LOAN AGAINST DEPOSIT IN NRO A/C

loan

In India

In INR

To the account HolderPermitted subject

to extant Rules

To third partyPermitted subject

to conditions

In Foreign Currency

To the account holder Not Permitted

To third party Not Permitted

Outside India

To the account holder Not permitted

To third party Not Permitted

• i) Personal purposes or for carrying on business activities*

• ii) Direct investment in India on non-repatriation basis by way of contribution to the capital of Indian firms / companies

• iii) Acquisition of flat / house in India for his own residential use.

To the Account holder

• Fund based and / or non-fund based facilities for personal purposes or for carrying on business activities *.

To Third Party

• Fund based and / or non-fund based facilities for bonafide purposes.Abroad

*The loans cannot be utilised for the purpose of on-lending or for carrying on agriculture or plantation activities or for investment in real estate business.

PURPOSE OF LOAN –IN CASE OF NRE A/C

AND FCNR (B) A/C

• Personal requirement and / or business

purpose.*To the

account holder

• Personal requirement and / or business

purpose*To third

party

Resident individual to lend to a Non-resident Indian (NRI)/ Person of Indian Origin (PIO) close relative [means relative as defined in Section 6 of the Companies Act, 1956] by way of crossed

cheque /electronic transfer.

The loan amount should be credited to the NRO a/c of the NRI /PIO. Credit of such loan amount may be treated as an eligible credit to NRO a/c;

PURPOSE OF LOAN – NRO ACCOUNT

* The loans cannot be

utilised for the purpose

of on-lending or for

carrying on agriculture

or plantation activities or

for investment in real

estate business.

A Comparison

NRE Account is meant for foreign exchange earned outside India and transferred to India

NRO Account are meant to keep the money earned in India before or after becoming an NRI

Bank Accounts by Residents

• Save as otherwise provided in the Act or rules or regulations made

thereunder, no person resident in India shall open or hold or maintain a

Foreign Currency Account:

• Provided that a Foreign Currency Account held or maintained before the

commencement of these Regulations by a person resident in India with

special or general permission of the Reserve Bank, shall be deemed to be

held or maintained under these Regulations

• Provided further that the Reserve Bank, may on an application made to it,

permit a person resident in India to open or hold or maintain a Foreign

Currency Account, subject to such terms and conditions as may be

considered necessary. [RBI Notification No.FEMA 10 /2000-RB dated

3rd May 2000]

REGULATION

Account

By person resident in India

Foreign Currency account in India

By Resident Individuals

By other

Account maintained

outside India

BY Resident Individuals

By Others

By Person resident outside

India

By NRI/PIOs

By others

By Resident in India

Foreign Exchange Management

(Deposit) Regulations, 2016

Fo

reig

n E

xc

ha

ng

e M

an

ag

em

en

t (Fo

reig

n

cu

rren

cy a

cc

ou

nts

by a

pe

rso

n re

sid

en

t

in In

dia

Accounts

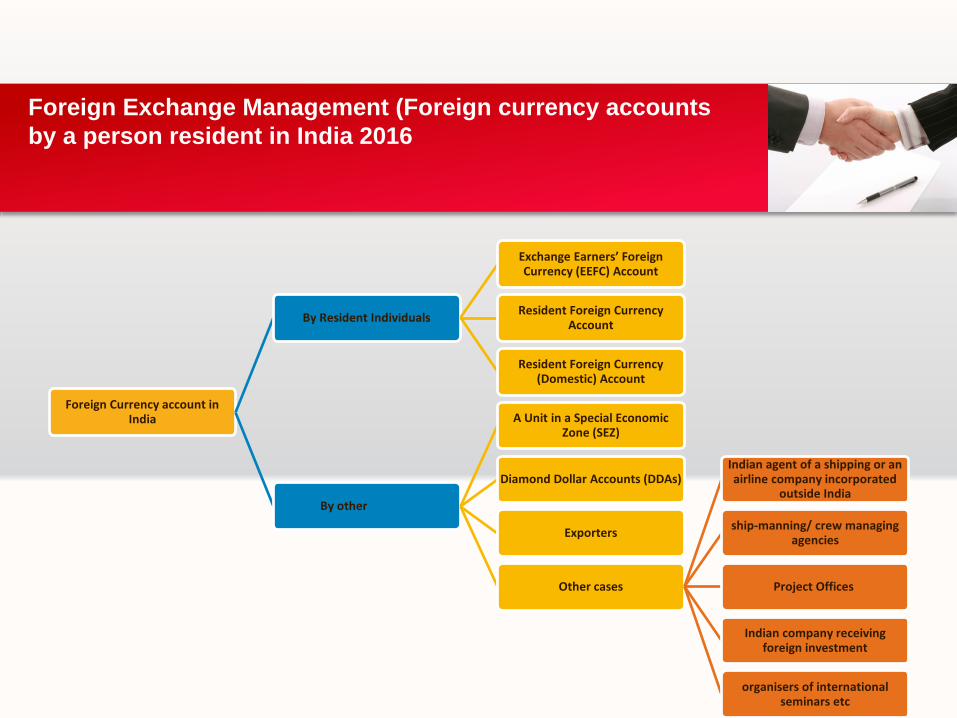

Foreign Exchange Management (Foreign currency accounts

by a person resident in India 2016

Foreign Currency account in India

By Resident Individuals

Exchange Earners’ Foreign Currency (EEFC) Account

Resident Foreign Currency Account

Resident Foreign Currency (Domestic) Account

By other

A Unit in a Special Economic Zone (SEZ)

Diamond Dollar Accounts (DDAs)

Exporters

Other cases

Indian agent of a shipping or an airline company incorporated

outside India

ship-manning/ crew managing agencies

Project Offices

Indian company receiving foreign investment

organisers of international seminars etc

Foreign Currency Account outside India

Others

office/ branch/ representative outside India

Exporters

External Commercial Borrowings (ECB)

For making Overseas Direct Investment

shipping or airline company incorporated in India

Life Insurance Corporation of India or General Insurance Corporation of India

Exhibition/ Trade fair

Resident Individual

On a visit to a foreign country

Abroad for studies

LRS

Salary

Foreign Exchange Management (Foreign currency accounts by a

person resident in India 2016

RESIDENT FOREIGN CURRENCY (DOMESTIC) ACCOUNT

RFRESIDENT FOREIGN

CURRENCY ACCOUNT

EXCHANGE EARNERS FOREIGN

CURRENCY ACCOUNTS

Type of Accounts

All categories of resident foreign exchange earners

can credit up to 100 per cent of their foreign exchange earnings to their EEFC Account with an

Authorised Dealer in India.

Funds held in EEFC account can be utilised for all permissible current account transactions and also for approved capital

account transactions

The account is maintained in the form of a non-interest bearing current account

EXCHANGE EARNERS FOREIGN

CURRENCY ACCOUNTS

Inward remittance through normal banking channels, other than remittances received on

account of foreign currency loan or investment received from abroad or received for meeting

specific obligations by the account holder;

Payments received in foreign exchange by a 100 per cent Export Oriented Unit or a unit in(a) Export Processing Zone or

(b) Software Technology Park or

(c) Electronic Hardware Technology Park for supply of goods to similar such units or to a unit in Domestic Tariff Area;

Payments received in foreign exchange by a unit in the Domestic Tariff Area for supply of goods

to a unit in the Special Economic Zone (SEZ);

Payment received by an exporter from an account maintained with an authorised dealer for the

purpose of counter trade.

Advance remittance received by an exporter towards export of goods or services;

Professional earnings including directors fees, consultancy fees, lecture fees, honorarium and

similar other earnings received by a professional by rendering services in his individual

capacity;

Re-credit of unutilised foreign currency earlier withdrawn from the account;

Amount representing repayment by the account holder's importer customer, of loan/advances

granted, to the exporter holding such account etc.

PERMISSIBLE CREDITS

Payment outside India towards a permissible current account transaction [in

accordance to the provisions of the Foreign Exchange Management (Current Account

Transactions) Rules, 2000]

Permissible capital account transaction [in accordance to the Foreign Exchange

Management (Permissible Capital Account Transactions) Regulations, 2000].

Payment in foreign exchange towards cost of goods purchased from a 100 percent

Export Oriented Unit or a Unit in(a) Export Processing Zone or

(b) Software Technology Park or

(c) Electronic Hardware Technology Park

Payment of customs duty in accordance with the provisions of the Foreign Trade Policy

of the Central Government for the time being in force.

Trade related loans/advances, extended by an exporter holding such account to his

importer customer outside India, subject to compliance with the Foreign Exchange

Management (Borrowing and Lending in Foreign Exchange) Regulations, 2000.

Permissible debits

Current or Savings or Term deposit accounts

A person resident in India

Free from all restrictions regarding utilisation of foreign

currency

opened to keep foreign currency assets which

were held outside India at the time of return

RFC Account

Permissible credits :

The foreign exchange received as:

pension of any other superannuation or other monetary benefits from the

employer outside India;

realised on conversion of the assets acquired, held or owned by such

person when he was resident in India or inherited from a person who was

resident in India

received or acquired as gift or inheritance from a person who was resident

outside India

RFC ACCOUNT

Permissible debits to the RFC account

The funds in RFC account are free from all restrictions regarding

utilization of foreign currency balances including any restriction on

investment outside India.

Foreign securities can also be acquired from RFC account.

The restriction of taking prior approval of government or prior

approval of RBI is not applicable to transactions undertaken out of

RFC account *

*However, the prohibited transactions as specified in Rule 3 of the Foreign Exchange Management (Current Account

Transactions) Rules, 2000 cannot be undertaken at all.

Regulations 5A of Foreign Exchange Management

(Foreign Currency Accounts by a Person Resident in India) Regulations, 2000

Resident Individual may open, hold and maintain

Current account

Does not bear any interest

No ceiling on the balances in the account

RESIDENT FOREIGN CURRENCY

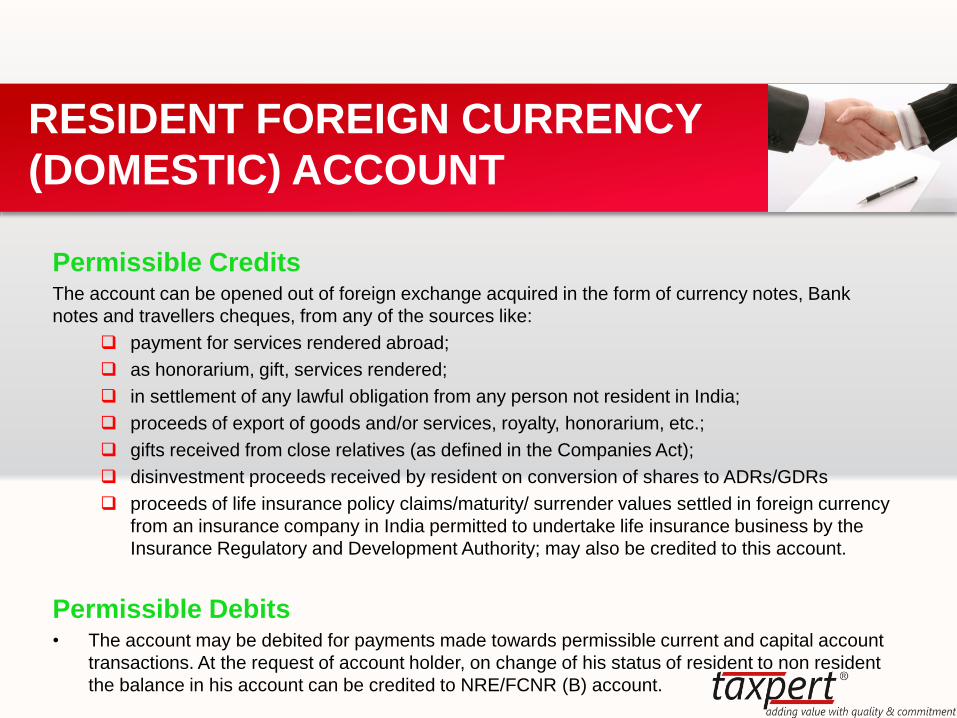

(DOMESTIC) ACCOUNT

Permissible CreditsThe account can be opened out of foreign exchange acquired in the form of currency notes, Bank

notes and travellers cheques, from any of the sources like:

payment for services rendered abroad;

as honorarium, gift, services rendered;

in settlement of any lawful obligation from any person not resident in India;

proceeds of export of goods and/or services, royalty, honorarium, etc.;

gifts received from close relatives (as defined in the Companies Act);

disinvestment proceeds received by resident on conversion of shares to ADRs/GDRs

proceeds of life insurance policy claims/maturity/ surrender values settled in foreign currency

from an insurance company in India permitted to undertake life insurance business by the

Insurance Regulatory and Development Authority; may also be credited to this account.

Permissible Debits• The account may be debited for payments made towards permissible current and capital account

transactions. At the request of account holder, on change of his status of resident to non resident

the balance in his account can be credited to NRE/FCNR (B) account.

RESIDENT FOREIGN CURRENCY

(DOMESTIC) ACCOUNT

REMITTANCES

Remittance

For Capital Account Transactions

Schedule I

Person resident In India

Schedule II

Person resident outside India

For Current Account Transactions

Schedule I

Prohibited

Schedule II

approval from the GOI

Schedule III

Approval from RBI

Liberalised Remittance Scheme

USD 250,000 per F.Y

Subsumes limits under CAT

Permissible capital Account transactions

Permissible current a/c

transactions

by CA. Sudha G. Bhushan

REM

ITTA

NC

ES

Non Resident Indian

From the funds in NRE account

Freely repatriable on request

Transfer from NRO account or Current Income subject

to applicable Taxes

From the funds in NRO account

Under Certificate from CA

Form 15CA/15CB

Remittance limited to USD 1 million per financial year

RESIDENT

In GeneralAs per FEM (Current

Account Transactions) Rules,2000

Schedule III of CA Rules specifies the limits of

remittance

Under Liberalisedremittance scheme

USD 2,50,000* per financial Year (April – March)

LRS facility subsumes limits specified in Sche III of CA

Rules

Foreign NationalFrom the funds in NRO

accountRetiring from

employment/inheritanceRemittance limited to USD 1

million per financial year

Taxpert Professionals Private Limited – Mumbai | New Delhi| Kolkata | Bangalore| Bhubaneswar

THANK YOU

Please feel free to call/mail me for further clarification.

CA.Sudha G. Bhushan

Taxpert Professionals Private Limited

Tel: +91 9769033172 || 07738892291

E-mail : [email protected]

Visit us at: www.taxpertpro.com