presentación de powerpoint - metro de santiago · metro - among the 14 leading subway systems in...

TRANSCRIPT

Empresa de Transporte de Pasajeros Metro S.A.

Investor Presentation

Metro at a glance

Key Investment Considerations

Financial Information

Metro Serves as the Backbone of Mass Transit in

Santiago

Metro owns and operates the entire underground

transportation system in Santiago, Chile

100% state-owned enterprise

Part of Transantiago, the city’s integrated public transport

system

To December 2014, 63% of all daily trips on public

transportation in Santiago use Metro

Current key subway network statistics:

o 103 kilometers of track and 108 stations on 5 lines

o 156 trains (1,093 cars)

o 2.4 million trips per workday

o 667.6 million passengers in 2014

Financial highlights:

o To December 2014 revenues of USD 464 million,

adjusted Ebitda and operating profit of USD 131

million and USD 9 million, respectively

o USD 6 billion in assets

o No subsidy required to generate an operating

surplus

Metro Overview Metro’s current network

3

Note: We define adjusted EBITDA as gross profit less administrative expenses plus depreciation and amortization

Metro’s Corporate History

2008, Metro

celebrates its 40th

anniversary

In 1968, President

Eduardo Frei

Montalva signed

the decree that

gave birth to Metro

In May 1975, the first

test trip took place

between “San Pablo”

station and “Estacion

Central” in Santiago.

Metro’s official

operations begin

In 1989, Metro

becomes a closed

stock corporation

and is registered

with the Chilean

Securities

Commission

(SVS). A board of

directors is

appointed to report

to its shareholders

Between 2010

and 2011

important

developments

begin at Metro,

with major line

extensions

2013-2018,

improvements to

existing lines and

construction of

lines 6 and 3

4

1997 Metro begins

operation of line 5

July 2011, Metro

announces the

construction of two

additional lines

In 2007, Metro

joins Transantiago,

the new integrated

transportation

system for the

capital city

In 2005, Metro

starts operating

lines 4 and 4A

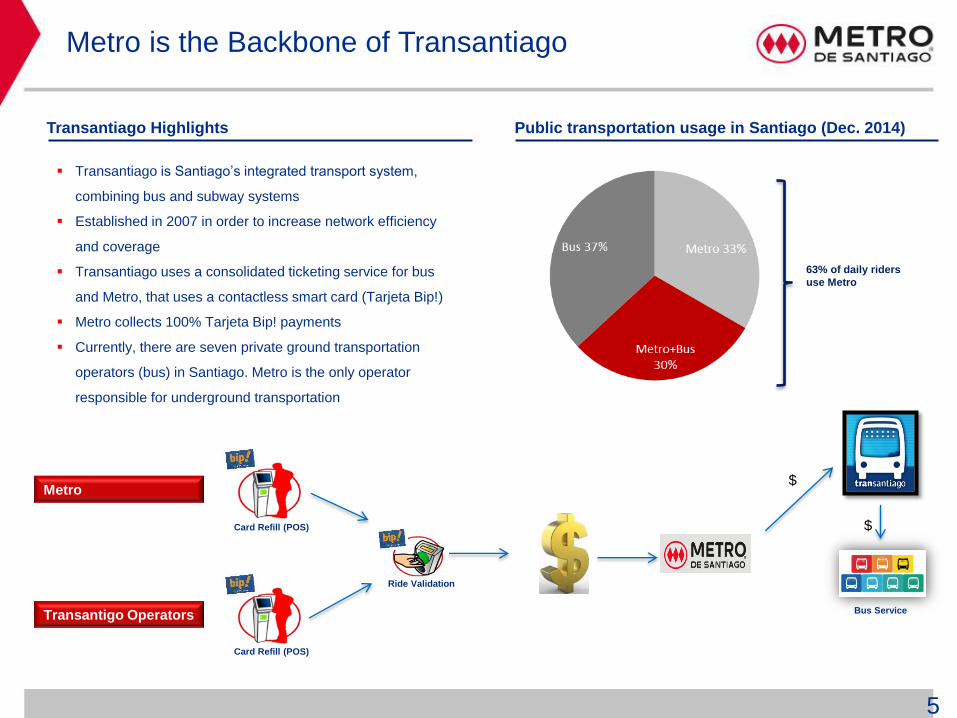

Metro is the Backbone of Transantiago

Transantiago is Santiago’s integrated transport system,

combining bus and subway systems

Established in 2007 in order to increase network efficiency

and coverage

Transantiago uses a consolidated ticketing service for bus

and Metro, that uses a contactless smart card (Tarjeta Bip!)

Metro collects 100% Tarjeta Bip! payments

Currently, there are seven private ground transportation

operators (bus) in Santiago. Metro is the only operator

responsible for underground transportation

Public transportation usage in Santiago (Dec. 2014)

Bus Service

Metro $

Transantiago Highlights

5

63% of daily riders

use Metro

$

Transantigo Operators

Card Refill (POS)

Card Refill (POS)

Ride Validation

Metro Grows Continuously to Serve Santiago

Project 63 & Network Strengthening Program (NSP) Planned layout for lines 6 and 3

6

Project 63, or the construction of new lines 6 & 3, is the

most significant undertaking and expansion effort in

Metro’s history

o 28 new stations and 37 kilometers of track

extensions

o Driverless trains

o Improved security by additional cameras in trains

and stations

o Overhead power line installation

o State-of-the-art information system for passengers

and workers

Total estimated investment of USD 2.8 billion

o 2/3 financed with government equity contributions

o 1/3 financed: Bond 144A/REG-S for USD 500

Million, Commercial Bank Facility Agreement for

USD 250 Million and ECA Multisource Facility

Agreement for USD 550 Million

126 new cars to be added to lines 1, 2 and 5 representing

a 20% increase in the total fleet for those lines

Air conditioning to be installed in all line 1 cars, and 60% of

line 2 and 5 cars

Refurbishment of NS74 trains (Metro’s oldest operating

trains), extending their useful life by 20 years (1/4 of the

current fleet)

New elevator access throughout the Metro network

Metro is upgrading the signaling system used on line 1

improve headway between trains

Metro Grows Continuously to Serve Santiago

Current and Upcoming Improvement Projects

7

Metro at a glance

Key Investment Considerations

Financial Information

Metro Benefits from Chile’s Growth and Stability

Source: World Bank and INE

(*) The International Rating Metro was recently ratified (04/17/15 Fitch, S & P 2/23/15)

The Government of Chile owns 100% of Metro

Ministerio

de Hacienda

State agency promoting

entrepreneurship and

innovation

Metro enjoys a stable economic backdrop

(po

pu

lati

on

in

mil

lio

ns

)

(po

pu

lati

on

in

mil

lio

ns

)

9

• Chile is the highest rated Latin American country

• Chile provides Metro with a stable political and regulatory

environment in an open economy with robust growth

• Unemployment and GDP figures 2011 – 2014:

17.2 17.3

17.5

16.0

16.5

17.0

17.5

18.0

2010 2011 2012

6.0 6.0 6.1

5.5

6.0

6.5

2010 2011 2012

Chile Santiago

• The Government of Chile regularly makes capital

contributions to Metro

• Demographics 2010 – 2012:

Chile’s Sovereign Credit Ratings

Agency Rating Outlook

Moody's Aa3 Stable

S&P AA- Stable

Fitch A+ Stable

Metro’s Credit Ratings

Agency Rating Outlook

Moody's - -

S&P (*) AA- Stable

Fitch (*) A Stable

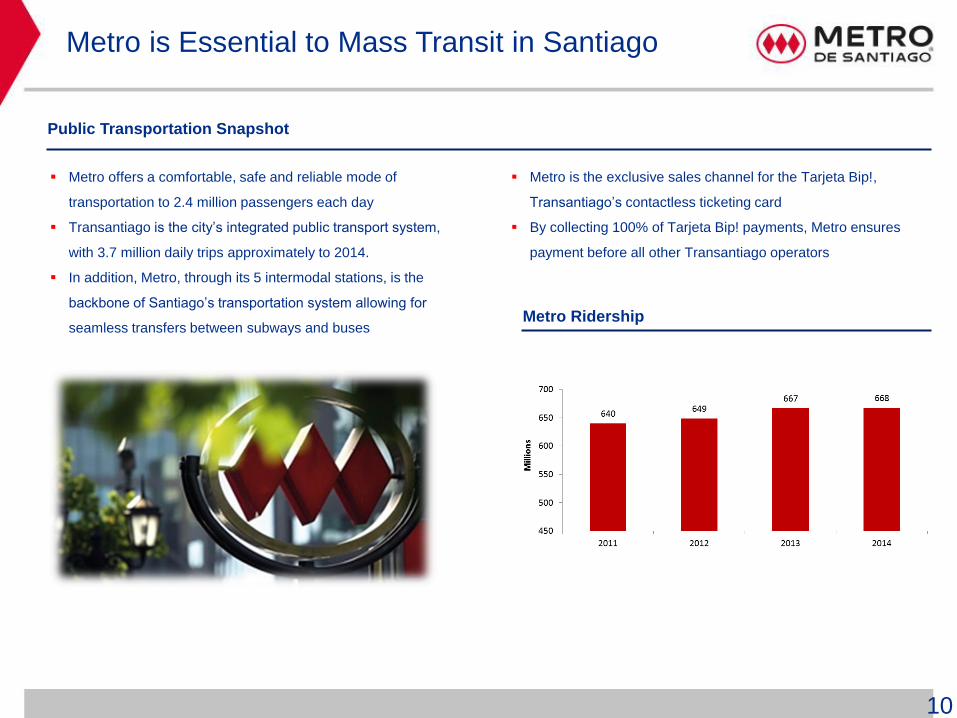

Metro is Essential to Mass Transit in Santiago

Metro offers a comfortable, safe and reliable mode of

transportation to 2.4 million passengers each day

Transantiago is the city’s integrated public transport system,

with 3.7 million daily trips approximately to 2014.

In addition, Metro, through its 5 intermodal stations, is the

backbone of Santiago’s transportation system allowing for

seamless transfers between subways and buses

Public Transportation Snapshot

10

Metro is the exclusive sales channel for the Tarjeta Bip!,

Transantiago’s contactless ticketing card

By collecting 100% of Tarjeta Bip! payments, Metro ensures

payment before all other Transantiago operators

Metro Ridership

Non-Fare Revenues Contribute Towards Higher

Margins

Non-Fare revenues

For december 2014, non-fare business accounts for 20% of Metro’s total revenue

Card Reloading (POS): Reloading service of Tarjeta Bip! at Metro ticket booths and load network surface

Intermodal: 5 intermodal stations

o Metro collects fees from bus companies for the use of these stations

Real Estate: Leasing of 340 stands and commercial spaces

Advertising: Over 10,000 advertising spaces on trains and stations

Services and Communications: 284 ATMs, 500 payphones, 18 cellular antennas, 57 kilometers fiber optics, among other services

11

Total Revenue Sources 2014

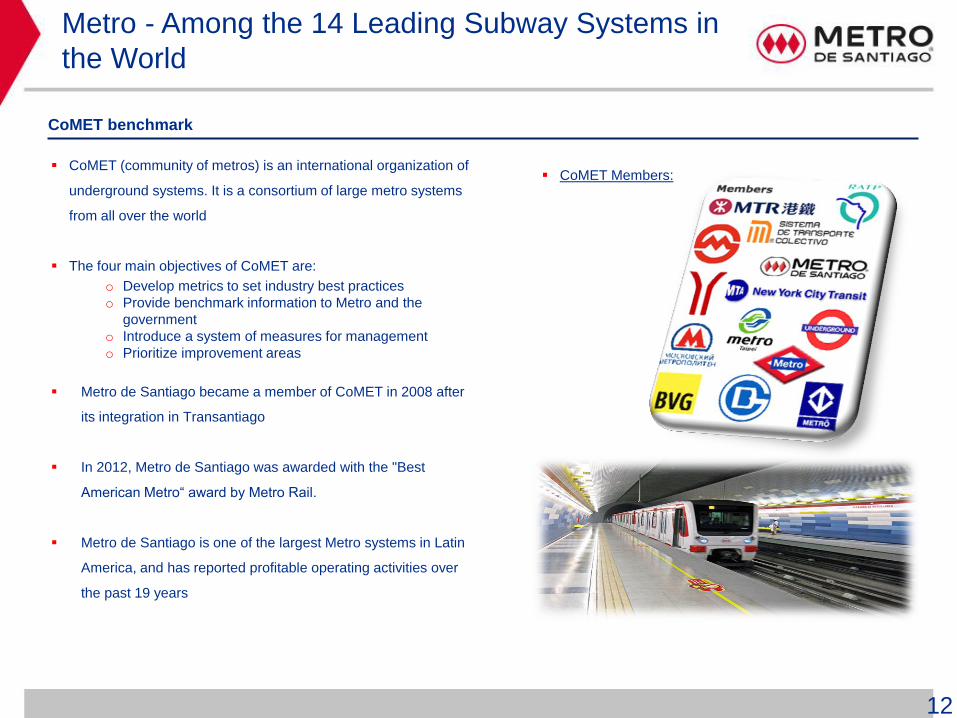

Metro - Among the 14 Leading Subway Systems in

the World

CoMET (community of metros) is an international organization of

underground systems. It is a consortium of large metro systems

from all over the world

The four main objectives of CoMET are:

o Develop metrics to set industry best practices

o Provide benchmark information to Metro and the

government

o Introduce a system of measures for management

o Prioritize improvement areas

Metro de Santiago became a member of CoMET in 2008 after

its integration in Transantiago

In 2012, Metro de Santiago was awarded with the "Best

American Metro“ award by Metro Rail.

Metro de Santiago is one of the largest Metro systems in Latin

America, and has reported profitable operating activities over

the past 19 years

CoMET benchmark

CoMET Members:

12

Metro at a glance

Key Investment Considerations

Financial Information

Total Revenues (USD Million) Adjusted Ebitda (USD Million)

Non-fare revenues (USD Million) Cost per Car-Km* (CLP Thousand)

Metro’s Solid Financial Metrics

14

Note: We define adjusted EBITDA as gross profit less administrative expenses plus depreciation and amortization

Figures have been converted from CLP to USD for the years 2014 & 2013 at a rate of CLP 606.75 & CLP 524.61 per USD 1 were used respectively; for the years ending 2012 & 2011 at a rate of CLP 479.96 & CLP 519.20

per USD 1 were used respectively

(*) Cost per Car-Km is calculated as (Cost of sale + admin. expenses) / Total of Car-Km

Debt to Capitalization* Interest Coverage (Adjusted Ebitda/Financial Expenses)

Shareholders’ Equity (USD Million) Debt/Equity

Metro’s Solid Financial Metrics (Cont’d)

Note: We define adjusted EBITDA as gross profit less administrative expenses plus depreciation and amortization

Figures have been converted from CLP to USD for the years 2014 & 2013 at a rate of CLP 606.75 & CLP 524.61 per USD 1 were used respectively; for the years ending 2012 & 2011 at a rate of CLP

479.96 & CLP 519.20 per USD 1 were used respectively

(*) Debt to Capitalization is calculated as Debt / (Debt + Equity)

15

Note: Figures in local currency (CLP) converted into USD (FX rate: 606.75 CLP / USD)

Figures may not add up due to rounding

Metro’s Debt Breakdown

Debt Structure (as of Dec. 2014)

Bonds (as of Dec. 2014)

Currency Breakdown (as of Dec. 2014)

Loans (as of Dec. 2014)

Total Bonds = USD 1,966MM Government Guaranteed = USD 875 MM

Non-Guaranteed = USD 1.091 MM

Total Debt = USD 2,481 MM Bonds = USD 1,966 MM

Loans = USD 500 MM

Total Loans = USD 500 MM Government Guaranteed = USD 136 MM

Non-Guaranteed = USD 364 MM

16

Derivatives = USD 1MM

Megaproject s withholding = USD 13 MM

Financial Information

(*) Adjusted Operating Profit = Gross Profit – Admin expenses (IFRS)

17

Note: Figures have been converted from CLP to USD for the years 2014 & 2013 at a rate of CLP 606.75 & CLP 524.61 per USD 1 were used

respectively; for the years ending 2012 & 2011 at a rate of CLP 479.96 & CLP 519.20 per USD 1 were used respectively

Balance Sheet 2011 2012 2013 2014

(USD Million) Current Assets 257 374 420 573

Non-Current Assets 5.196 5.830 5.555 5.226

Total Assets 5.453 6.204 5.975 5.800

Short-Term Liabilities 246 266 346 310

Long-Term Liabilities 2.338 2.459 2.158 2.363

Total Liabilities 2.583 2.725 2.503 2.674

Total Shareholders Equity 2.869 3.479 3.472 3.126

Total Shareholders Equity & Liabilities 5.453 6.204 5.975 5.800

Income Statement 2011 2012 2013 2014

(USD Million) Revenues 441 497 477 464

Cost of sales -379 -419 -414 -418

Gross Profit 62 78 63 46

Gross margin (%) 14,07% 15,68% 13,26% 9,82%

Admin expenses -39 -54 -48 -37

Net financial expenses -76 -88 -78 -66

Change in FX -84 65 -52 -95

Net Income -188 -52 -140 -216

Adjusted EBITDA 159 173 155 131

Adjusted Operating Profit (*) 23 11 15 9

Empresa de Transporte de Pasajeros Metro S.A.

Investor Presentation