preparing the or budget: the nurse manager's responsibility

TRANSCRIPT

AORN J O U R N A L MARCH 1985, VOL 41. NO 3 -

Preparing the OR Budget THE NURSE MANAGER'S RESPONSIBILITY

Linda K. Groah, RN

king costs and increasing emphasis on cost containment have focused attention on the R budgeting process. Third-party payers and

health care consumers insist health care costs be controlled. In response, hospital administrators are pressuring nurse managers to control expenses. If costs are to be controlled effectively, the nurse manager and the staff in the operating room must be involved in the budgeting process. The old method-the nurse manager heard about the budget after it was completed by the accounting depart- ment-is no longer acceptable. The manager must participate in budget preparation and then use the budgeting data daily as a guide for decision making. Nuke manqers must thoroughly understand the budgeting process, be accountable for the services delivered, and be innovative in developing alternate methods of providing quahty care cost effectively.

The h a n d triangle has three components- forecasting, budget preparation, and controlling. This article will discus the first two components.

what is a Budget?

budget is a statement of estimated expenses and revenues for a specific time period. The A budget may be used to plan departmental

objectives and programs, motivate n m managers and staff to contain costs, and evaluate the nurse manager's performance. Budgets are developed by cost centers where expenses are allocated. For example, the operating rooms and the recovery rooms may be designated as two separate cost centers.

There are two types of budgets+pr&hg and capital. The operating budget consists of all expenses

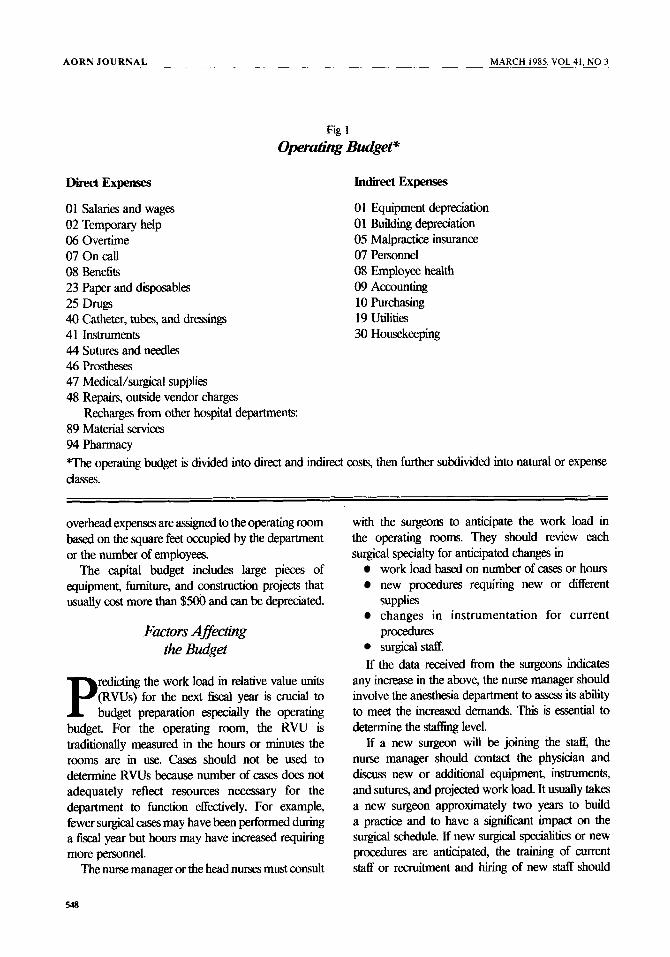

that are consumable and are used directly in patient care. Operating expenses tend to fluctuate with the number of surgical hours or cases, and they are divided into direct and indirect (overhead) expenses. The operating budget is further subdivided into natural or expense classes. Within these classes similar supply items and services are grouped together (Fig 1).

Direct expenses are those items that can be assigned directly to a department. These include salaries, medicaVsurgica1 supplies, repairs, and charges fiom other hospital departments. Indirect or

Linda K. Groah, RA? BA, CNOR, CNA, is the drector of nursing OR/PAR and assistant director of hospital cuiministration ai the University of California Hospitals and Clinics, San Francisco. She is also clinical inrmcctor at the University of Cal#omia School of Nursing, San Franciso. She received her diploma in nursing @om St Luke's School of Nuring and h a y a BA in Health Care Administration from St Maiy's Colkge, Moraga, Cal$

541

AORN JOURNAL MARCH 1985, VOL 41, NO 3

Fig 1

Operadihg Budget"

%ect Expenses

01 Salaries and wages 02 Temporary help 06 Overtime 07 On call 08 Benefits 23 Paper and disposables 25 Drugj 40 Catheter, tubes, and dressings 41 Instruments 44 Sutures and needles 46 Prostheses 47 Medical/surgical supplies 48 Repairs, outside vendor charges

89 Material services 94 Pharmacy *The operating budget is divided into direct and induect costs, then further subdivided into natural or expense ClasseS.

Recharges from other hospital departments:

Indirect Expenses

01 Equipment depreciation 01 Building depreciation 05 Malpractice insurance 07 Personnel 08 Employee health 09 Accounting 10 Purchasing 19 Utilities 30 Housekeeping

overhead expenses are assigned to the operating room based on the square feet occupied by the department or the number of employees.

The capital budget includes large pieces of equipment, fumIture, and construction projects that usually cost more than $500 and can be depreciated.

Factors Affecting the Budget

redicting the work load in relative value units (RVUs) for the next fiscal year is crucial to P budget preparation especially the operating

budget. For the operating room, the RVU is traditionally measured in the hours or minutes the rooms are in use. Cases should not be used to determine RVUs because number of cases does not adequately reflect resources necessary for the department to function effectively. For example, fewer surgical cases may have been perfomed during a fiscal year but hours may have increased requiring more personnel.

The nurse manager or the head nlllSeS must consult

with the surgeons to anticipate the work load in the operating rooms. They should review each surgical specialty for anticipated changes in

work load based on number of cases or hours new procedures requiring new or different supplies changes in instrumentation for current procedures surgicalstaff.

If the data received kom the surgeons indicates any increase in the above, the nurse manager should involve the anesthesia department to assess its ability to meet the increased demands. This is essential to determine the stafhg level.

If a new surgeon will be joining the staff, the nurse manager should contact the physician and discus new or additional equipment, instruments, and sutures, and projected work load. It usually takes a new surgeon approximately two years to build a practice and to have a s iwcant impact on the surgical schedule. If new surgical speaahties or new procedures are anticipata the training of current staff or recruitment and hiring of new staff should

548

AORN JOURNAL - MARCH 1985. VOL 41, NO 3

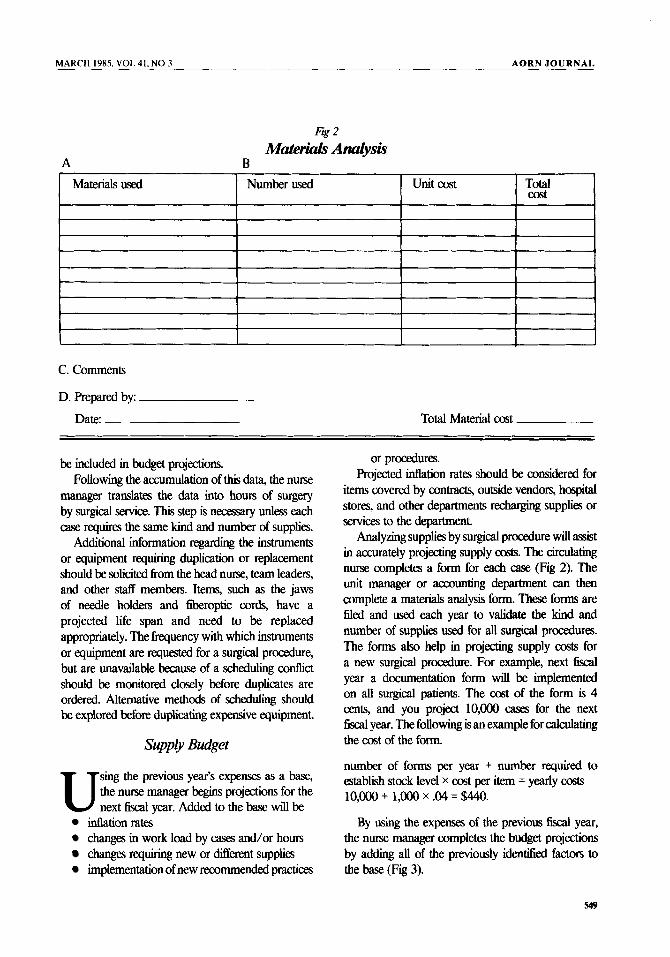

Fig 2 Materials Andy&

A B

C. Comments

D. Prepared by:

Date: Total Material cost

be included in budget projections. Following the accumulation of this data, the nurse

manager translates the data into hours of surgery by surgical service. This step is necessary unless each case requires the same kind and number of supplies.

Additional information regardmg the instruments or equipment requiring duplication or replacement should be solicited fiom the head nurse, team leaders, and other staff members. Items, such as the jaws of needle holders and fiberoptic cords, have a projected life span and need to be replaced appropriately. The frequency with which instruments or equipment are requested for a surgical procedure, but are unavailable because of a scheduling contlict should be monitored closely before duplicates are ordered. Alternative methods of scheduhng should be explored before duplicating expensive equipment.

Suppry Budget

sing the previous year’s expenses as a base, the n w manager begm projections for the U next fiscal year. Added to the base will be

inflation rates changes in work load by cases and/or hours changes requiring new or different supplies implementation of new recommended practices

or procedures. Projected inflation rates should be considered for

items covered by contracts, outside vendors, hospital stores, and other departments rechargmg supplies or services to the department.

Analyzing supplies by surgical procedure will mist in accurately projecting supply costs. The circulating nurse completes a form for each case (Fig 2). The unit manager or accounting department can then complete a materials analysis fom. These forms are filed and used each year to validate the kind and number of supplies used for all surgical procedures. The forms also help in projecting supply costs for a new surgical procedure. For example, next fiscal year a documentation form will be implemented on all surgical patients. The cost of the form is 4 cents, and you project l0,Ooo casg for the next fiscal year. The following is an example for calculating the cost of the form.

number of forms per year + number required to establish stock level x cost per item = yearly costs l0,Ooo + 1,Ooo x .04 = $440.

By using the expenses of the previous fiscal year, the nurse manager completes the budget projections by adding all of the previously idenaed factors to the base (Fig 3).

AORN JOURNAL MARCH 1985, VOL 41, NO 3

Fig 3 Supply hjection

Base + Inflation + Increase in +/- changes in supplies + Implementation = Total Year surgical cases of new nursing amount to

or types of procedures be budgeted cases per natural

C. Comments

D. Preparedby: Date: Total Mated Cost

Personnel Budget

he personnel budget consists of salaries and fringe benefits. The nurse manager is T responsible for developing a 6 g pattern

that will accurately reflect the projected work load. The personnel budget is expressed in full-time equivalents (FTEs). For example, one budgeted employee working 100% is one FTE; two par-time employees each workmg 50% equals one FTE.

The first step in planning the personnel budget is to determine the numbers of o p t i n g rooms to be available by day of the week and hours each day. This decision should be reached after collaborating with hospital administra tors, anesthesia department representatives, surgeons, and nurse managers. The nurse manager prepares historical data indicative of the total number of hours available for staffed operating room time versus the total number of hours for emergency procedures. Emergency procedure data should be analyzed by day of the week, and by shifts, ie, 7 AM to 3:30 PM, 3 to 11:30 PM, 11:30 PM to 7 AM. A 75% to 80% utilization of elective time is considered optimal and usually coIlstitutes justification for expansion of operating room hours.'

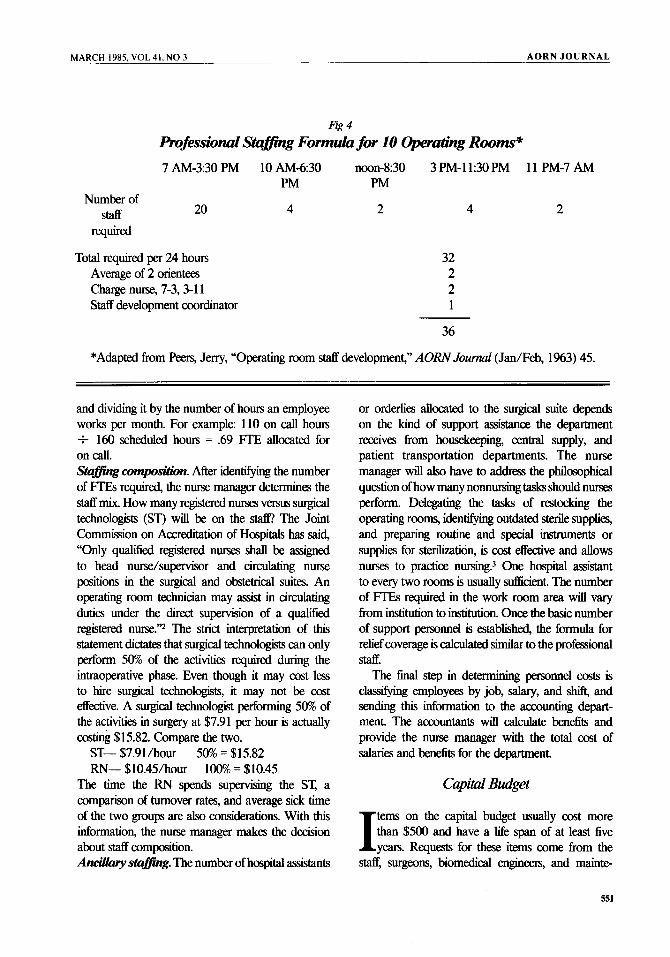

The stafjing formula in Fig 4 will assist in determining the minimum stafFng requirements for a 10-room operating suite in which 10 rooms are staffed 60m 7 AM to 3:30 PM, five rooms to 630 PM, three rooms to 8:30 PM, two rooms to 11:30 PM, and one room 11 PM to 7 AM. This formula provides minimual s W g only; it

does not consider the average number of FTEs in

orientation throughout the year. The 10 AM to 630 PM and 12 to 830 PM shifts provide lunch relief and coverage for cases that run late. Additional staff may be required based on patient needs or if other areas are to be staffed. For example, a room for local procedures may require a second circulator to monitor the patient; a total joint replacement may require two circulators-one to attend to the patient and one to assist the scrub nurse set up. Cardiac cases may require two scrub nurses during the entire procedure.

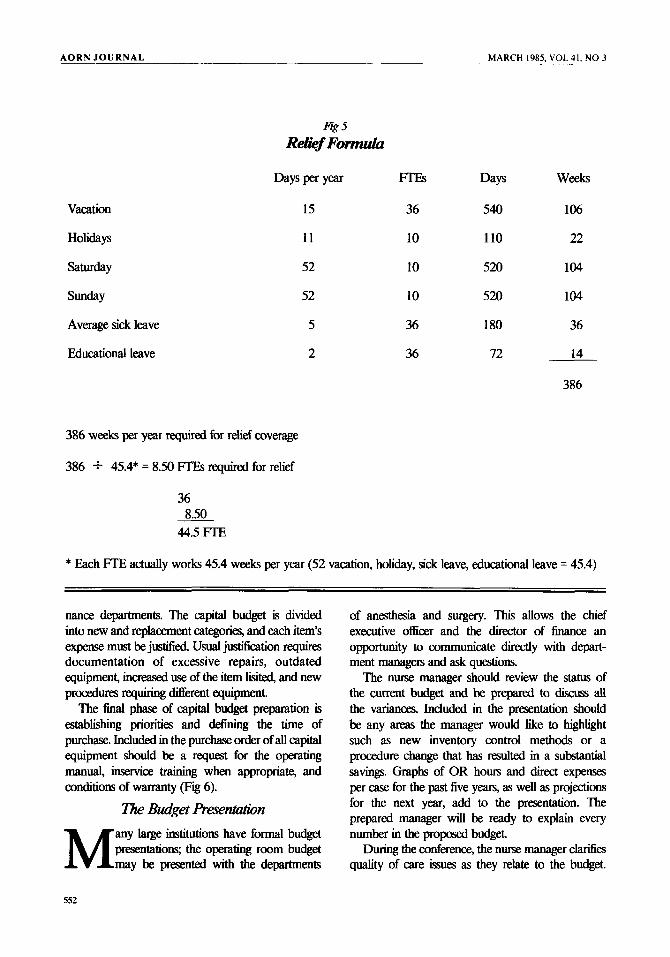

The nurse manager must calculate relief coverage for holidays, vacations, weekends, and sick days. For purposes of this formula, each employee will receive 15 days vacation and 1 1 holidays per year. If holidays and weekends are staffed, (instead of an on call arrangement) they must be included in the relief formula. Also, include guaranteed education days and an average number of sick days per professional employee. In calculating the average sick leave, all unusual days, such as long illnesses and maternity leaves, should be eliminated and the remaining number averaged (Fig 5). On C d Whether to staff the operating rooms during off hours or have an on call system is a decision for each nurse manager. In making this decision, the manager considers if an on call system would (a) be a soufce of dissatisfaction for the sk-5, (b) cost more in personnel hours and salary than providing regular staff, and (c) impact the next day's schedule if personnel were called out kequently. If the decision is made to provide an on call system, t h m hours are considered in the budget as FTES by tow the number of hours on call per month

550

MARCH 1985. VOL 41, NO 3 A O R N J O U R N A L

Number of Staff

Fig 4

hfesswnal S t a m g Formula for 10 Operading Rooms* 7 AM-3130 PM 10 AM430 noon-8:30 3 PM-11:30 PM 11 PM-7 AM

PM PM

20 required

Total required per 24 hours Average of 2 onentees Charge nurse, 7-3,3-11 Staff development coordinator

4 2

32 2 2 1

4 2

36

*Adapted from Peers, Jerry, “Operating room staff development,” AORN Journal (Jan/Feb, 1%3) 45.

and dividing it by the number of hours an employee works per month. For example: 110 on call hours t 160 scheduled hours = .69 FTE allocated for on call. Stumg (XlmpOSifiO. After idenhfymg the number of FIB required, the nurse manager determines the staff mix. How many registered rimes versus surgical technologists (ST) will be on the staff! The Joint Commission on Accreditation of Hospitals has said, “Only qualified registered nurses shall be assigned to head nurse/supenisor and circulating nurse positions in the surgical and obtetrical suites. An operating room technician may assist in circulating duties under the direct supervision of a qualified registered nurse.’? The strict interpretation of this statement dictates that surgical technologists can only perform 50% of the activities required during the intraoperative phase. Even though it may cost less to hire surgical technologists, it may not be cost effective. A surgical technologist performing 50% of the activities in surgery at $7.91 per hour is actually mting $15.82. Compare the two.

ST- $7.91/h0~1 50% = $15.82 RN- $10.45/h0~ 100% = $10.45

The time the RN spends supervising the ST, a comparison of turnover rates, and average sick time of the two groups are also considerations. With this information, the nurse manager makes the decision about staff composition. Ancillary stumg. The number of hospital assistants

or orderlies allocated to the surgical suite depends on the kind of support assistance the department receives from housekeeping, central supply, and patient transportation departments. The nurse manager will also have to address the philosophical question of how many nonnursing tasks should nurses perform. Delegating the tasks of restocking the operating rooms, idenhfymg outdated sterile supplies, and preparing routine and special instruments or supplies for sterilization, is cost effective and allows nurses to practice nursing? One hospital assistant to every two rooms is usually sdicient. The numkr of FTEs required in the work room area will vary from institution to institution. Once the basic number of support personnel is established, the formula for relief coverage is calculated similar to the professional Staff.

The final step in determining personnel mts is clmdyhg employees by job, salary, and shift, and sending this information to the accounting depart- ment. The accountants will calculate benefits and provide the nurse manager with the total oost of salaries and benefits for the department.

Capital Bdget

tems on the capital budget usually cost more than $500 and have a life span of at least five I years. Requests for these items come from the

staff, surgeons, biomedical engineers, and mainte-

551

A O R N J O U R N A L MARCH 1985. VOL 41. NO 3

Vacation

Holidays

Saturday

Sunday

Average sick leave

Educational leave

Fig 5 Relief Form&

Days per Year

15

11

52

52

5

2

m Days Weeks

36 540 106

10 110 22

10 520 104

10 520 104

36 180 36

36 72 14

386

386 weeks per year required for relief coverage

386 + 45.4* = 8.50 FTES required for relief

36

44.5 FTE 8.50

* Each FTE actually works 45.4 weeks per year (52 vacation, holiday, sick leave, educational leave = 45.4)

nance departments. The capital budget is divided into new and replacement categories, and each item’s expense must be justified. Usual justification requires documentation of excessive repairs, outdated equipment, i n d use of the item lisited, and new procedures requiring Merent equipment.

The final phase of capital budget preparation is establishing priorities and detining the time of purchase. Included in the purchase order of all capital equipment should be a request for the operating manual, inseMce training when appropriate, and conditions of warranty (Fig 6).

The Bua‘get Presentdon any large institutions have formal budget presentatiow the operating room budget M may be presented with the departments

of anesthesia and surgery. This allows the chief executive officer and the director of finance an opportunity to communicate directly with depart- ment managen and ask questions.

The n m manager should review the status of the current budget and be prepared to discuss all the varianm. Included in the presentation should be any areas the manager would like to highhght such as new inventory control methods or a procedure change that has resulted in a substantial savings. Graphs of OR hours and direct expenses per case for the past five years, as well as projections for the next year, add to the presentation. The prepared manager will be ready to explain every number in the propa4 budget.

During the conference, the nurse manager clarities quality of care issues as they relate to the budget.

552

MARCH 1985, VOL 41, NO 3 AORN J O U R N A L

Justifcation Comments

Fig 6 Operating & Recovery R m m

Cqital Budget Worksheet - Fiscal Year 19- to 19-

Administrative Comments/ Approval

Date: service:

Estimated cost

Submitted by:

Acquisition Period

If the institution manages by objectives, achievement of the current year‘s objectives and goals for the next year may be discussed. The nurse manager answers questions directly and in a nondefensive manner. Careful attention should be given to body language as well as verbal responses.

Before the presentation, the nurse manager should consider areas where compromises would be acceptable and not alter the quality of patient care or existing programs. The budget will either be approved as proposed or adjusted depending on the manager’s ability to communicate the p i b l e effects of each action. With this information and an open discussion of the requests, the chief executive officer can make a realistic decision about operating room budget requests.

Notes 1. Operating Room Resource UI&&K Chicago Area

Findings and Recommendations (Chicago: Chicago Hospital Council, 1976) 46.

2. Accredituhbn Manual for Hospitals (Chicago: Joint Commission on Accreditation of Hospitals, 1983) 117.

3. Linda Groah, Operating Room Nursing: The Perioperd’ve Role (Reston, Va: Reston Publishing, 1983) 68.

Predicting Heart Attacks in Emergency Patients A study in the January issue of Archives of Internal Medicine indicates that it may be possible to predict which patients with acute chest pain who come to the emergency room for treatment are at least risk for subsequent heart attacks.

After studying 5% patients, Thomas H. Lee, MD, and colleagues reported that if the patient has a normal electrocardiogram and no history of an- gina, but has stabbing pain and experiences pain when his chest is tapped, he is at least risk for a heart attack.

553