preparing for the new lease accounting standard

TRANSCRIPT

Copyright © 2015 PowerPlan, Inc. All rights reserved. CONFIDENTIAL AND PROPRIETARY.

Graphics Line to go in this area. Unauthorized use, disclosure, or reproduction is strictly prohibited.

Preparing for the New

Lease Accounting StandardRick Fisher & Will Davis

PowerPlan, Inc.

Copyright © 2015 PowerPlan, Inc. All rights reserved. CONFIDENTIAL AND PROPRIETARY.

Graphics Line to go in this area. Unauthorized use, disclosure, or reproduction is strictly prohibited.

Field OperationsCFO Office

Lease Accounting will require collaboration and integration of business and system processes across the organization

IRS: Reduced income taxes;

audit trail

Regulators: Profitable rate case

State & Local Governments:

Reduced income & property

taxes; audit trail

Debt Holders: Improved cash flow;

forecasting covenant compliance

Joint Ventures: Master Limited

Partnership K-1 filings

SEC: GAAP, IFRS; Proper asset

valuation; SOX compliance

FINANCIAL CENTRIC VIEWGeneral Ledger, Procurement, HR, Treasury, Fixed Assets, Accounts Receivable…

ASSET MAINTENANCE CENTRICConstruction WIP, Project Management, In-Service Dates, Maintenance, RetirementGeospatial data…

TaxManagement

Budget and Project

Management

AssetAccounting

Management

Asset Management

Planning

Regulatory Management

Integration Management

Copyright © 2015 PowerPlan, Inc. All rights reserved. CONFIDENTIAL AND PROPRIETARY.

Graphics Line to go in this area. Unauthorized use, disclosure, or reproduction is strictly prohibited.

Introductions

3

Will DavisProfessional Services

Rick FisherSolution Consulting

Copyright © 2015 PowerPlan, Inc. All rights reserved. CONFIDENTIAL AND PROPRIETARY.

Graphics Line to go in this area. Unauthorized use, disclosure, or reproduction is strictly prohibited.

Agenda

Lease Standard overview

Lease accounting lifecycle

Example lease agreement

Proposed adoption timeline

4

Copyright © 2015 PowerPlan, Inc. All rights reserved. CONFIDENTIAL AND PROPRIETARY.

Graphics Line to go in this area. Unauthorized use, disclosure, or reproduction is strictly prohibited.

February 25, 2016 – FASB releases Topic 840

Initially proposed in February 2006

Many iterations and tons of feedback

After diverging, IASB released a similar standard in January 2016

January 2019 mandatory adoption date

2 year lookback period

January 13, 2016

IASB releases

IFRS 17 Leases

February 25, 2016

FASB

releases final

standard

January 2017

Lookback period

for comparable

financials

January 2019

Standard effective

for most public

companies

Copyright © 2015 PowerPlan, Inc. All rights reserved. CONFIDENTIAL AND PROPRIETARY.

Graphics Line to go in this area. Unauthorized use, disclosure, or reproduction is strictly prohibited.

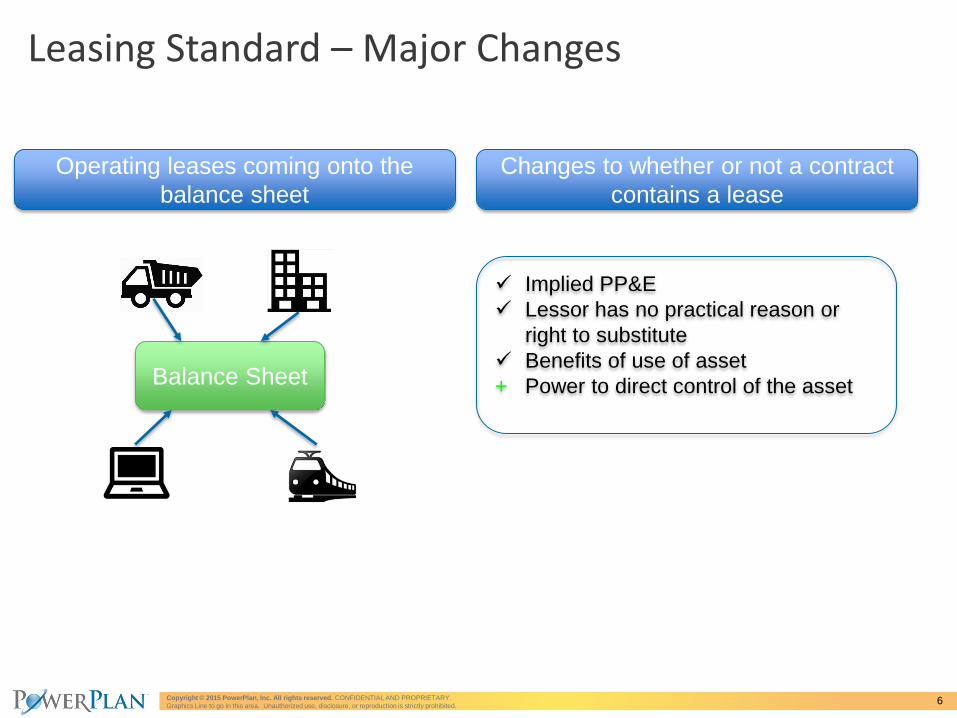

Leasing Standard – Major Changes

6

Operating leases coming onto the

balance sheet

Balance Sheet

Changes to whether or not a contract

contains a lease

Implied PP&E

Lessor has no practical reason or

right to substitute

Benefits of use of asset

+ Power to direct control of the asset

Copyright © 2015 PowerPlan, Inc. All rights reserved. CONFIDENTIAL AND PROPRIETARY.

Graphics Line to go in this area. Unauthorized use, disclosure, or reproduction is strictly prohibited.

Life Exceeds

75%Economic Life

NPV of Payments

>90%Fair Market Value

Transfer of

Ownership at

End of TermBPO

OR

Today Result

• 90%+ lease dollars are operating

• 95%+ lease records are operating

• Very few leases on balance sheet

CapitalFront Loaded

Expense

OperatingStraight-line

Expense

Balance Sheet

Copyright © 2015 PowerPlan, Inc. All rights reserved. CONFIDENTIAL AND PROPRIETARY.

Graphics Line to go in this area. Unauthorized use, disclosure, or reproduction is strictly prohibited.

Transfer of

Ownership at

End of TermBPO

OR

FinanceFront Loaded

Expense

OperatingStraight-line

Expense

Leases < 1 Year

Balance Sheet

Rental Expense

Specialized in

Nature+

Future

Life Exceeds

Economic Life

NPV of Payments

Fair Market Value

Major Portion Substantially All

Copyright © 2015 PowerPlan, Inc. All rights reserved. CONFIDENTIAL AND PROPRIETARY.

Graphics Line to go in this area. Unauthorized use, disclosure, or reproduction is strictly prohibited.

ASSET ACCOUNTING• Capital accounting for most leases• Depreciation forecasting• Transitioning leased assets to owned• Lease vs. buy decisions

TAX• Property tax responsibilities• Front loaded expense impacts

income taxes• Book/ tax differences• Potential for a 315 and 481a

adjustment for change in accounting

BUDGETING• Interest and amortization affects

O&M budgets• Capital approval processes

REGULATORY• Leases in rate base• Income statement treatment• Regulated assets and liabilities

LESS

EE A

CC

OU

NTI

NG

What are the Ripple Impacts

from Lessee Accounting?

Copyright © 2015 PowerPlan, Inc. All rights reserved. CONFIDENTIAL AND PROPRIETARY.

Graphics Line to go in this area. Unauthorized use, disclosure, or reproduction is strictly prohibited.

How to interpret removal of bright-line tests?• “Substantially all”• “Major Part”

Earnings impact?• Above the line vs. below the line• Capital leases included in EBITDA but have adverse EPS impacts at the start of the term

Will the IRS make any changes? • IRS still deliberating on future treatment• Monitor cutoff dates of leases to know if they are eligible for automatic changes in

accounting methods

Will FERC make changes?• Regulatory treatment is still up in the air• Will capital lease expense continue to follow payments? • Will regulatory assets / liabilities be required for FERC / GAAP differences?

Will State Commissions make changes?• How will states interpret FERC’s decisions when it comes time for rate cases?• Will more states include capital leases in rate base?

Lease vs. Buy decision criteria?

10

What Will Drive My Lease Adoption Strategy?

Copyright © 2015 PowerPlan, Inc. All rights reserved. CONFIDENTIAL AND PROPRIETARY.

Graphics Line to go in this area. Unauthorized use, disclosure, or reproduction is strictly prohibited.

Need not re-assess whether expired or existing contracts contain leases

Need not reassess capital vs. operating leases

Need not reassess initial direct costs incurred on lease contracts

Practical Expedients for Transition

11

• Scope out existing leases

Potential Lessee Benefits

• More or less capital leases

• Expense impacts

• EBITDA & EPS impacts

• Reduce capital leases dollars due

to internal costs

• Increase capital lease dollars and

front-loaded expense Non-lease components can be

included as lease costs by class of underlying asset

Copyright © 2015 PowerPlan, Inc. All rights reserved. CONFIDENTIAL AND PROPRIETARY.

Graphics Line to go in this area. Unauthorized use, disclosure, or reproduction is strictly prohibited.

LEASE ACCOUNTING LIFECYCLE

12

Copyright © 2015 PowerPlan, Inc. All rights reserved. CONFIDENTIAL AND PROPRIETARY.

Graphics Line to go in this area. Unauthorized use, disclosure, or reproduction is strictly prohibited.

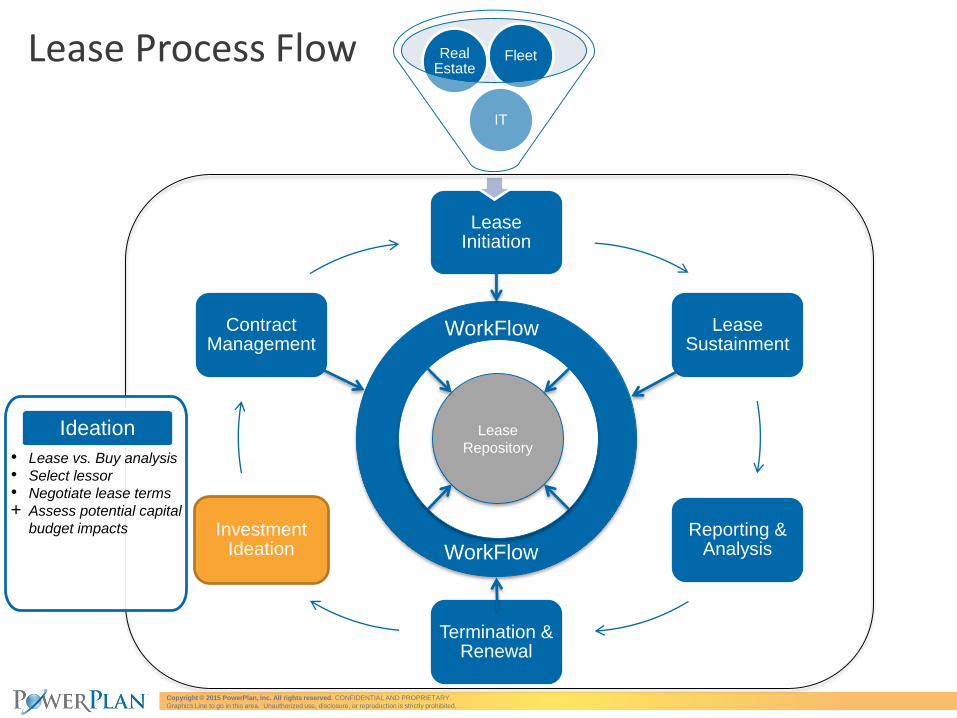

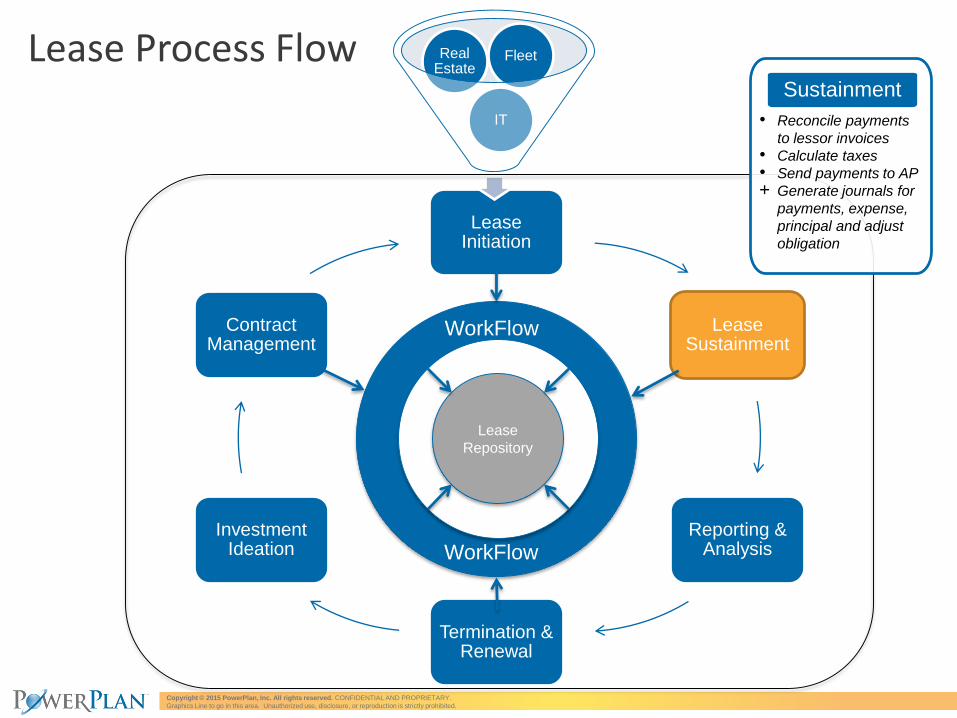

Lease Initiation

Lease Sustainment

Reporting & Analysis

Termination & Renewal

Investment Ideation

Contract Management

Lease Process Flow

1313

IT

Real Estate

Fleet

Lease

Repository

WorkFlow

WorkFlow

Copyright © 2015 PowerPlan, Inc. All rights reserved. CONFIDENTIAL AND PROPRIETARY.

Graphics Line to go in this area. Unauthorized use, disclosure, or reproduction is strictly prohibited.

Lease Initiation

Lease Sustainment

Reporting & Analysis

Termination & Renewal

Investment Ideation

Contract Management

Lease Process Flow

IT

Real Estate

Fleet

Lease

Repository

WorkFlow

WorkFlow

Ideation

• Lease vs. Buy analysis

• Select lessor

• Negotiate lease terms

+ Assess potential capital

budget impacts

Copyright © 2015 PowerPlan, Inc. All rights reserved. CONFIDENTIAL AND PROPRIETARY.

Graphics Line to go in this area. Unauthorized use, disclosure, or reproduction is strictly prohibited.

Lease Initiation

Lease Sustainment

Reporting & Analysis

Termination & Renewal

Investment Ideation

Contract Management

Lease Process Flow

IT

Real Estate

Fleet

Lease

Repository

WorkFlow

WorkFlow

Contracts

• Store contracts in a

centralized repository

+ Check all contracts for

embedded leases

+ Route leases through

capital approvals in an

auditable system of

record

Copyright © 2015 PowerPlan, Inc. All rights reserved. CONFIDENTIAL AND PROPRIETARY.

Graphics Line to go in this area. Unauthorized use, disclosure, or reproduction is strictly prohibited.

Lease Initiation

Lease Sustainment

Reporting & Analysis

Termination & Renewal

Investment Ideation

Contract Management

Lease Process Flow

IT

Real Estate

Fleet

Lease

Repository

WorkFlow

WorkFlow

Initiation

+ Consolidate all leases for

reporting and

management

+ Determine capital lease

classification

+ Calculate schedules

+ Integrate with field leasing

systems

+ Automate balance sheet

additions

Copyright © 2015 PowerPlan, Inc. All rights reserved. CONFIDENTIAL AND PROPRIETARY.

Graphics Line to go in this area. Unauthorized use, disclosure, or reproduction is strictly prohibited.

Lease Initiation

Lease Sustainment

Reporting & Analysis

Termination & Renewal

Investment Ideation

Contract Management

Lease Process Flow

IT

Real Estate

Fleet

Lease

Repository

WorkFlow

WorkFlow

Sustainment

• Reconcile payments

to lessor invoices

• Calculate taxes

• Send payments to AP

+ Generate journals for

payments, expense,

principal and adjust

obligation

Copyright © 2015 PowerPlan, Inc. All rights reserved. CONFIDENTIAL AND PROPRIETARY.

Graphics Line to go in this area. Unauthorized use, disclosure, or reproduction is strictly prohibited.

Lease Initiation

Lease Sustainment

Reporting & Analysis

Termination & Renewal

Investment Ideation

Contract Management

Lease Process Flow

IT

Real Estate

Fleet

Lease

Repository

WorkFlow

WorkFlow

Reporting

• Future minimum

lease payments

+ Leasing standard

impact forecasting

+ Balance sheet

account balances

+ Capital lease vs.

operating lease

expense

Copyright © 2015 PowerPlan, Inc. All rights reserved. CONFIDENTIAL AND PROPRIETARY.

Graphics Line to go in this area. Unauthorized use, disclosure, or reproduction is strictly prohibited.

Lease Initiation

Lease Sustainment

Reporting & Analysis

Termination & Renewal

Investment Ideation

Contract Management

Lease Process Flow

IT

Real Estate

Fleet

Lease

Repository

WorkFlow

WorkFlow

Expire/Renew

Track bargain

purchase options and

renewals

+ Automate end of life

retirements

+ Manage early

terminations

Copyright © 2015 PowerPlan, Inc. All rights reserved. CONFIDENTIAL AND PROPRIETARY.

Graphics Line to go in this area. Unauthorized use, disclosure, or reproduction is strictly prohibited.

Example Lease Agreement

3 year lease – paid monthly in arrears• Year 1 - $500,000 per month

• Year 2 - $700,000 per month

• Year 3 - $1,000,000 per month

Fair market value of asset - $27,500,000

NPV of payments - $24,613,492

Capitalization percent = 89.50%

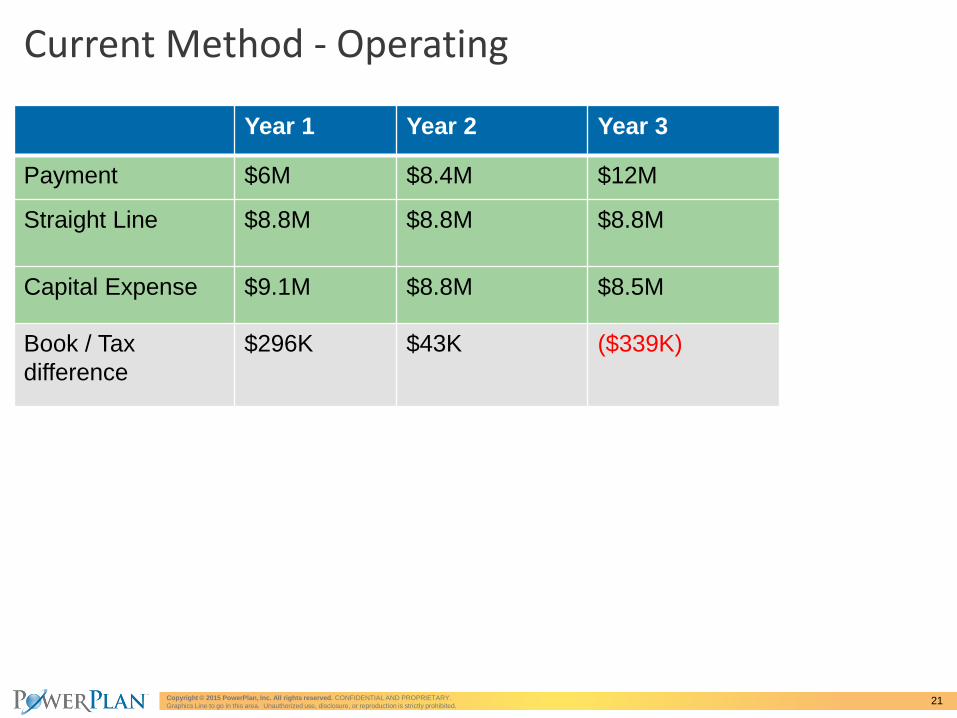

Current treatment – Operating Lease

20

Copyright © 2015 PowerPlan, Inc. All rights reserved. CONFIDENTIAL AND PROPRIETARY.

Graphics Line to go in this area. Unauthorized use, disclosure, or reproduction is strictly prohibited.

Year 1 Year 2 Year 3

Payment $6M $8.4M $12M

Straight Line $8.8M $8.8M $8.8M

Capital Expense $9.1M $8.8M $8.5M

Book / Tax

difference

$296K $43K ($339K)

Current Method - Operating

21

Copyright © 2015 PowerPlan, Inc. All rights reserved. CONFIDENTIAL AND PROPRIETARY.

Graphics Line to go in this area. Unauthorized use, disclosure, or reproduction is strictly prohibited.

-200000

0

200000

400000

600000

800000

1000000

1200000

1 2 3 4 5 6 7 8 9 10 11 12 13 14 15 16 17 18 19 20 21 22 23 24 25 26 27 28 29 30 31 32 33 34 35 36

Current Treatment - Operating

22

Straight-lined

operating lease

expense

Expense if

recognized on basis

of payment

Book / Tax

Difference

Copyright © 2015 PowerPlan, Inc. All rights reserved. CONFIDENTIAL AND PROPRIETARY.

Graphics Line to go in this area. Unauthorized use, disclosure, or reproduction is strictly prohibited.

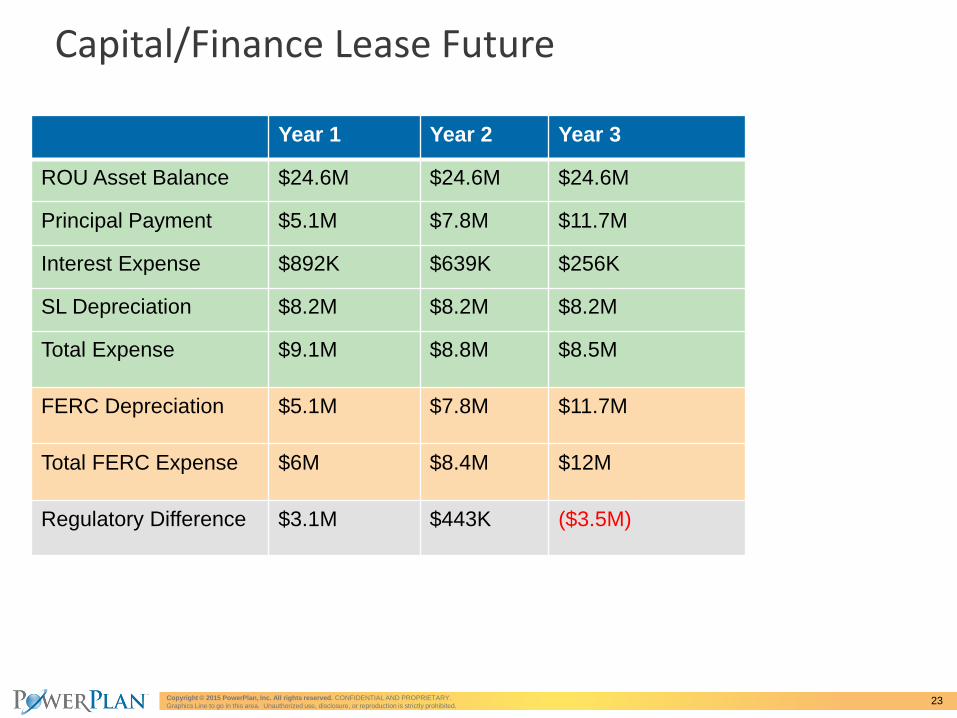

Capital/Finance Lease Future

23

Year 1 Year 2 Year 3

ROU Asset Balance $24.6M $24.6M $24.6M

Principal Payment $5.1M $7.8M $11.7M

Interest Expense $892K $639K $256K

SL Depreciation $8.2M $8.2M $8.2M

Total Expense $9.1M $8.8M $8.5M

FERC Depreciation $5.1M $7.8M $11.7M

Total FERC Expense $6M $8.4M $12M

Regulatory Difference $3.1M $443K ($3.5M)

Copyright © 2015 PowerPlan, Inc. All rights reserved. CONFIDENTIAL AND PROPRIETARY.

Graphics Line to go in this area. Unauthorized use, disclosure, or reproduction is strictly prohibited.

Future - Capital Lease

24

-400000

-200000

0

200000

400000

600000

800000

1000000

1200000

1 2 3 4 5 6 7 8 9 10 11 12 13 14 15 16 17 18 19 20 21 22 23 24 25 26 27 28 29 30 31 32 33 34 35 36

Total GAAP

Expense

Total FERC

Expense

Regulatory

Difference

Copyright © 2015 PowerPlan, Inc. All rights reserved. CONFIDENTIAL AND PROPRIETARY.

Graphics Line to go in this area. Unauthorized use, disclosure, or reproduction is strictly prohibited.

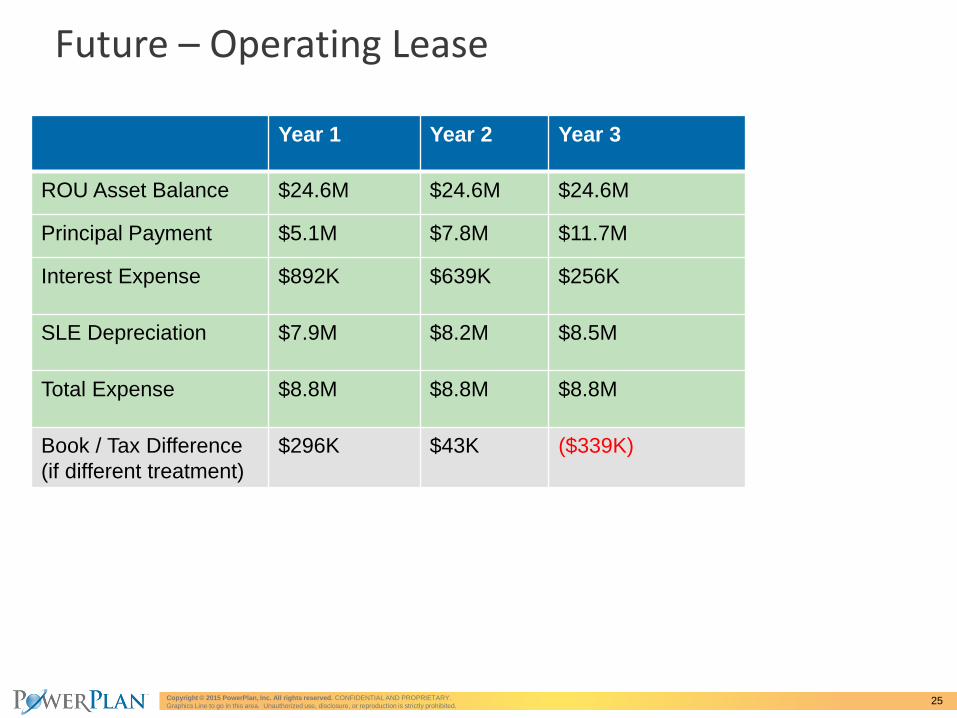

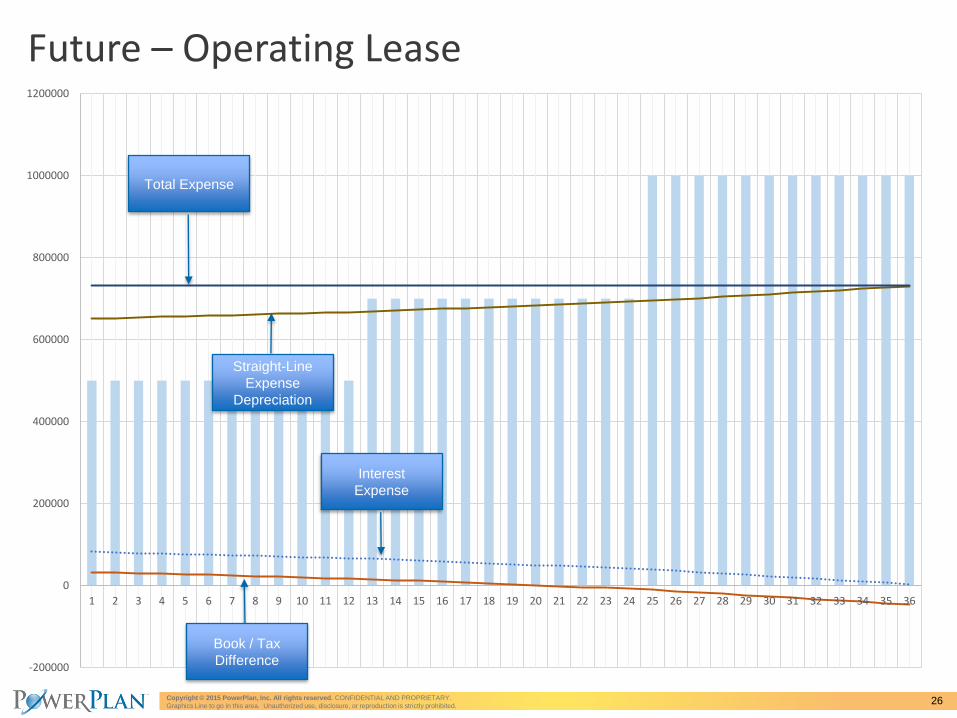

Future – Operating Lease

25

Year 1 Year 2 Year 3

ROU Asset Balance $24.6M $24.6M $24.6M

Principal Payment $5.1M $7.8M $11.7M

Interest Expense $892K $639K $256K

SLE Depreciation $7.9M $8.2M $8.5M

Total Expense $8.8M $8.8M $8.8M

Book / Tax Difference

(if different treatment)

$296K $43K ($339K)

Copyright © 2015 PowerPlan, Inc. All rights reserved. CONFIDENTIAL AND PROPRIETARY.

Graphics Line to go in this area. Unauthorized use, disclosure, or reproduction is strictly prohibited.

-200000

0

200000

400000

600000

800000

1000000

1200000

1 2 3 4 5 6 7 8 9 10 11 12 13 14 15 16 17 18 19 20 21 22 23 24 25 26 27 28 29 30 31 32 33 34 35 36

Future – Operating Lease

26

Total Expense

Straight-Line

Expense

Depreciation

Interest

Expense

Book / Tax

Difference

Copyright © 2015 PowerPlan, Inc. All rights reserved. CONFIDENTIAL AND PROPRIETARY.

Graphics Line to go in this area. Unauthorized use, disclosure, or reproduction is strictly prohibited.

PROPOSED ADOPTION TIMELINE

27

Copyright © 2015 PowerPlan, Inc. All rights reserved. CONFIDENTIAL AND PROPRIETARY.

Graphics Line to go in this area. Unauthorized use, disclosure, or reproduction is strictly prohibited.

Proposed Adoption Timeline

Consolidate Leases• Review existing contracts • Check AP for recurring payments• Reach out to operating units• Gather details for leasing standard

like renewal options, bargain purchase options, etc.

Change Management• How will you educate the organization on the new processes around entering into a lease agreement?

2 Year Lookback• You will need to report on leases in effect 2017

in 2019

Implement System• Automate Lease Accounting and Asset Creation• Guarantee Compliance• Automate Conversion of Operating Leases

Lease Standard Effective!

Forecast Balance and Income Sheet Impact• Balance Sheet – Assets, obligations, and depreciation coming onto balance sheet• Income Statement – P&L impacts of front loaded expense• Statements of Cash Flows – Cash flow from financing activities vs. operations

Assign Owner

Who will own leases going forward?

Capital Process Integration• How will the new leased assets be managed?• What will the capital approval process look like?• What system or tools will you be using to track leases and

their assets?• How will you add existing operating leases to the balance

sheet?

2016 2017 2018 2019

Copyright © 2015 PowerPlan, Inc. All rights reserved. CONFIDENTIAL AND PROPRIETARY.

Graphics Line to go in this area. Unauthorized use, disclosure, or reproduction is strictly prohibited.

Will Davis

Professional Services – Accounting Practice

Copyright © 2015 PowerPlan, Inc. All rights reserved. CONFIDENTIAL AND PROPRIETARY.

Graphics Line to go in this area. Unauthorized use, disclosure, or reproduction is strictly prohibited.

Key Takeaways

Accounting groups will be responsible for many more aspects of the leasing lifecycle

Keep in mind the ripple effects of lease changes on other areas

It is not too early to start preparing!

Reach out to PowerPlan if you have any questions

Copyright © 2015 PowerPlan, Inc. All rights reserved. CONFIDENTIAL AND PROPRIETARY.

Graphics Line to go in this area. Unauthorized use, disclosure, or reproduction is strictly prohibited.

SAFE HARBORCertain sections of this document contain forward-looking statements that are based on assumptions regarding the products'

features and capabilities and the adoption of PowerPlan, Inc. by customers. Actual events or results may differ materially from

those described in this document due to a number of risks and uncertainties. These potential risks and uncertainties include,

among others, customer acceptance of PowerPlan solutions, customer demand for PowerPlan solutions, the ability to satisfy

changing customer needs, market demand in general for PowerPlan products and the introduction of new products by competitors

or the entry of new competitors into the markets for PowerPlan products.

Words such as “believe,” “estimate,” expected," "planned," "intends," "anticipated" “may,” “will,” “expect,” and “project” and similar

expressions as they relate to the Company are intended to identify such forward-looking statements. The Company undertakes no

obligation to publicly update or revise any forward looking statements. All forward-looking statements are subject to various risks

and uncertainties that could cause actual results to differ materially from expectations. Forward-looking statements are made

pursuant to the safe harbor provisions of the Private Securities Litigation Reform Act of 1995, as amended. PowerPlan is not

obligated to undertake any obligation to update these forward-looking statements to reflect events or circumstances after the date

of this document. Readers are cautioned not to place undue reliance on these forward-looking statements, which speak only as of

their dates.

31