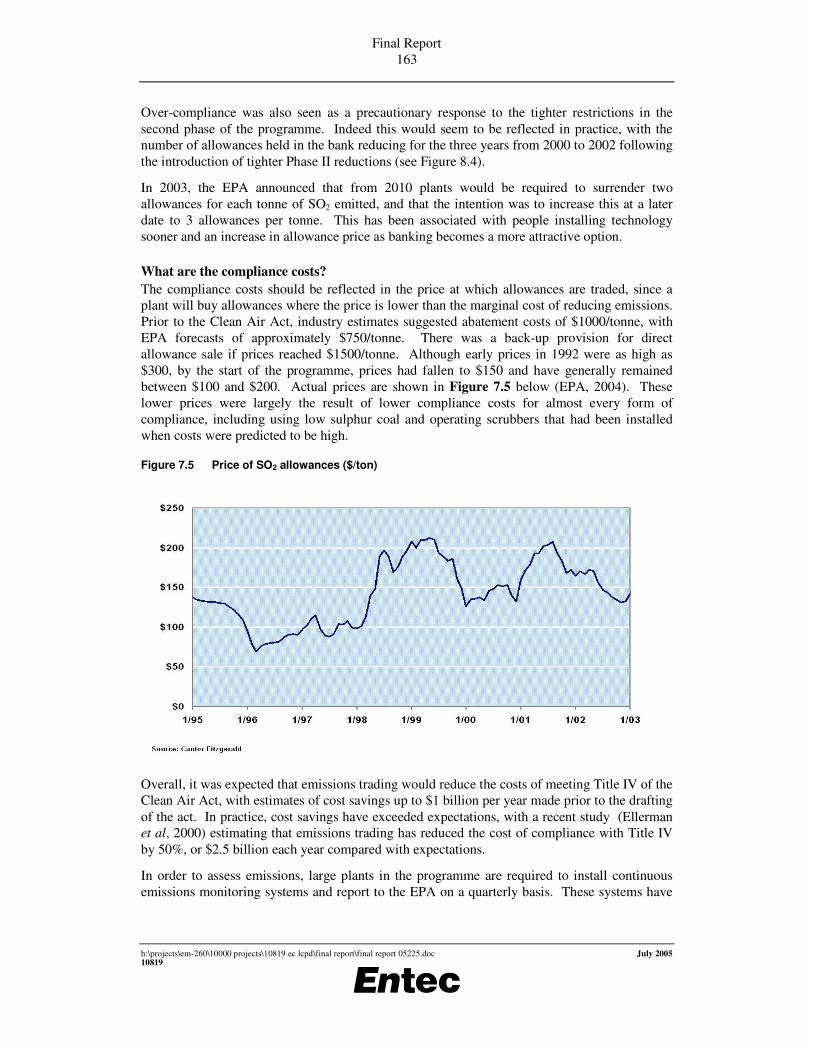

preparation of the review relating to the large combustion...

TRANSCRIPT

Preparation of the review relating to the Large Combustion Plant Directive

A Report for European Commission,

Environment Directorate General

Final Report

July 2005

Entec UK Limited

Certificate No. FS 13881

Report for DG ENV-C.4 European Commission B-1049 Brussels Belgium

Main Contributors Alistair Ritchie Katherine Wilson Ben Grebot Robin Smale (OXERA) Wojciech Orzeszek (Energoprojekt) Sabrina Dann Layla Twigger Ian Spencer Andriana Stavrakaki

Issued by

…………………………………………………………

Alistair Ritchie

Approved by

………………………………………… Iain Johnston

Entec UK Limited Windsor House Gadbrook Business Centre Gadbrook Road Northwich Cheshire CW9 7TN England Tel: +44 (0) 1606 354800 Fax: +44 (0) 1606 354810

10819

h:\projects\em-260\10000 projects\10819 ec lcpd\final report\final report 05225.doc

Preparation of the review relating to the Large Combustion Plant Directive

A Report for European Commission, Environment Directorate General

Final Report

July 2005

Entec UK Limited

Certificate No. EMS 69090

In accordance with an environmentally responsible approach, this document is printed on recycled paper produced from 100% post-consumer waste, or on ECF (elemental chlorine free) paper

Final Report i

h:\projects\em-260\10000 projects\10819 ec lcpd\final report\final report 05225.doc

July 2005

10819

Glossary

Al Aluminium

As Arsenic

B Boron

BaP Benzo(a)pyrene

BAT Best Available Techniques

BAU Business-As-Usual

BBAU Beyond Business-As-Usual

BC Brown Coal/Lignite

Be Beryllium

BREF BAT Reference Document

CAC Command And Control

CAFE Clean Air for Europe

CCGT Combined Cycle Gas Turbines

Cd Cadmium

CER Commission for Energy Regulation

CHP Combined Heat and Power

CLE Current Legislation

CLRTAP Convention on Long Range Transboundary Air Pollution

Co Cobalt

CO Combustion Optimisation

COALPRO Confederation of UK Coal Producers

COHPAC Compact Hybrid Particulate Technology

Cr Chromium

DLN Dry Low NOx

EEA European Environmental Agency

EGTEI Expert Group on Techno-Economic Issues

ELV Emission limit value

EPA Environmental Protection Agency

EPER European Pollutant Emission Register

ESI Electricity Supply Industry

ESP Electrostatic Precipitator

ETS Emissions Trading Scheme

Final Report ii

h:\projects\em-260\10000 projects\10819 ec lcpd\final report\final report 05225.doc

July 2005

10819

EURELECTRIC Union of the Electricity Industry

FF Fabric Filter

FGD Flue Gas Desulphurisation

FGC Flue Gas Conditioning

FOE Friends of the Earth

HC Hard Coal

Hg Mercury

IEA International Energy Agency

IIASA International Institute for Applied Systems Analysis

IPPC Integrated pollution prevention and control

LCP large combustion plant

LCPD Large Combustion Plant Directive

LNB Low NOx Burner

LPG Liquefied Petroleum Gas

LTC Long Term Contract

MBI Market Based Instrument

Mn Manganese

Mo Molybdenum

NAAQS National Ambient Air Quality Standards

NECD National Emission Ceilings Directive

NERP National Emission Reduction Plan

Ni Nickel

NOx Nitrogen Oxide

NSPS New Source Performance Standards

OFA Overfire Air

OGP International Association of Oil and gas Producers

OTC Ozone Transport Commission

PAH Polycyclic Aromatic Hydrocarbons

Pb Lead

PCC Potential Combustion Concentration

PFC Progressive Flow Control

PM Particulate Matter

PM2.5 Particulate matter of less than 2.5 µm diameter

PM10 Particulate matter of less than 10 µm diameter

PP Public Power

RACT Reasonably Available Control Technology

Final Report iii

h:\projects\em-260\10000 projects\10819 ec lcpd\final report\final report 05225.doc

July 2005

10819

RAE Royal Academy of Engineering

RAINS Regional Air Pollution Information and Simulation

RECLAIM Regional Clean Air Incentives Market

RTC RECLAIM Trading Credits

Sb Antimony

SCR Selective Catalytic Reduction

SDA Spray Drier Adsorption

Se Selenium

Si Silicon

SIP State Implementation Plan

SNCR Selective Non Catalytic Reduction

SO2 Sulphur dioxide

TP Transition Period

TSO Transmission System Operators

UBA Umweltbundesamt (Germany’s Federal Environmental Agency)

UCTE Union for the Co-ordination of Transmission of Electricity

UKCS UK Continental Shelf

UKOOA UK Offshore Operators Association

UNECE United Nations Economic Commission for Europe

V Vanadium

VOC Volatile Organic Compound

Zn Zinc

Final Report iv

h:\projects\em-260\10000 projects\10819 ec lcpd\final report\final report 05225.doc

July 2005

10819

Final Report v

h:\projects\em-260\10000 projects\10819 ec lcpd\final report\final report 05225.doc

July 2005

10819

Executive Summary

Introduction Entec UK has undertaken a project for the European Commission to support the review of Directive 2001/80/EC, referred to as the Large Combustion Plant Directive (LCPD). This is the final report of the project, which presents the findings of the collection and analysis of information on a range of aspects related to large combustion plant emissions, in accordance with the overall project objectives.

This project is being undertaken in conjunction with the wider Clean Air for Europe (CAFE) Programme. In line with the project objectives, this project addresses a number of specific aspects related to the large combustion plant sector in the EU. It is understood that the conclusions on the need for further measures in relation to the LCPD, however, will be dependent not only on the findings of this project but also on the findings of other activities under the CAFE Programme.

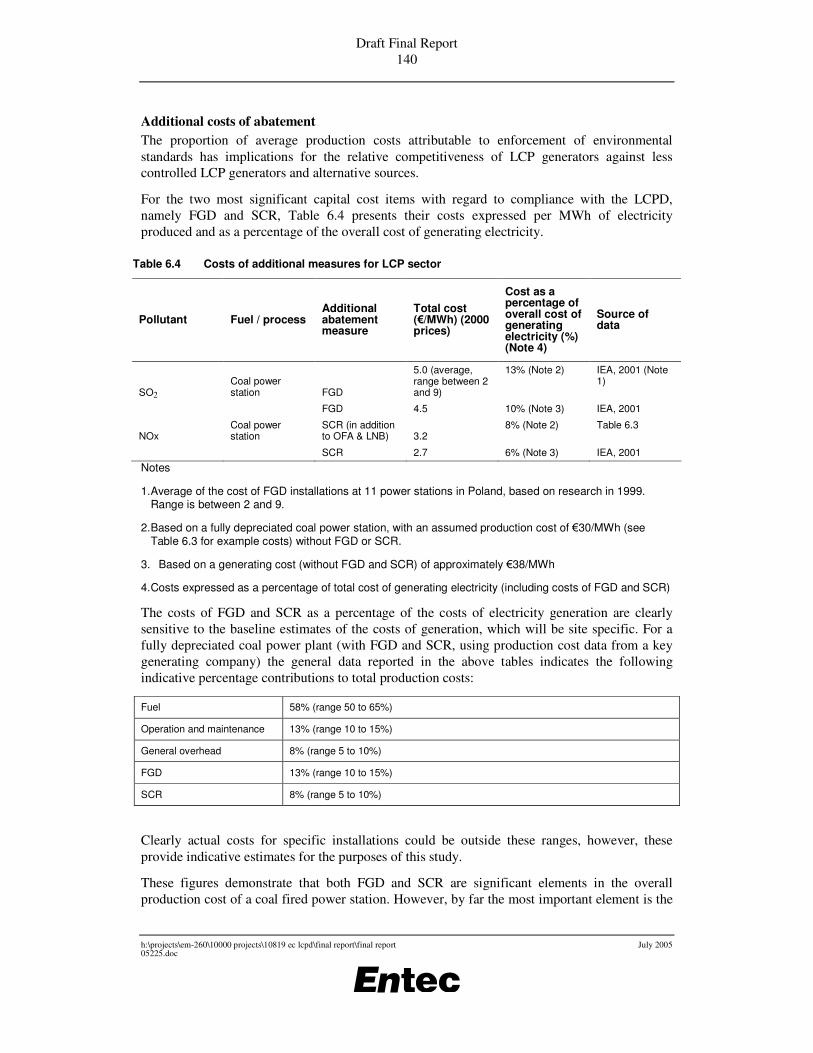

A summary of some of the key findings of this study is presented below.

Key policies affecting air pollutant emissions from large combustion plants Brief details of some of the key policies affecting emissions of air pollutants from large combustion plants in the EU are presented in Section 2. Clearly the Large Combustion Plant Directive (LCPD) itself is of most direct relevance, and this is discussed, including information on national emission reduction plans submitted so far under the LCPD and details of implementation of this directive in the new Member States. This is followed by sections that identify whether and to what extent some Member States go beyond the LCPD ELVs in their own national legislation; the requirements of ‘best available techniques’ (BAT) under the IPPCD and key air quality directives. Key summary points include:

• Under the LCPD, Member States had the option of choosing a national emission reduction plan for existing plants instead of ELVs. For those Member States that have so far submitted a national emission reduction plan to the Commission (including Czech Republic, Finland, France, Greece, Ireland, Netherlands, Slovenia1 and UK), the targets of these plans are presented together with current emission levels for comparison. Compliance with the targets in these plans will be achieved through a mixture of abatement, fuel switching and reductions in load factors and will be decided by the operating companies themselves, closer to the LCPD compliance deadline for existing plants of 1 January 2008.

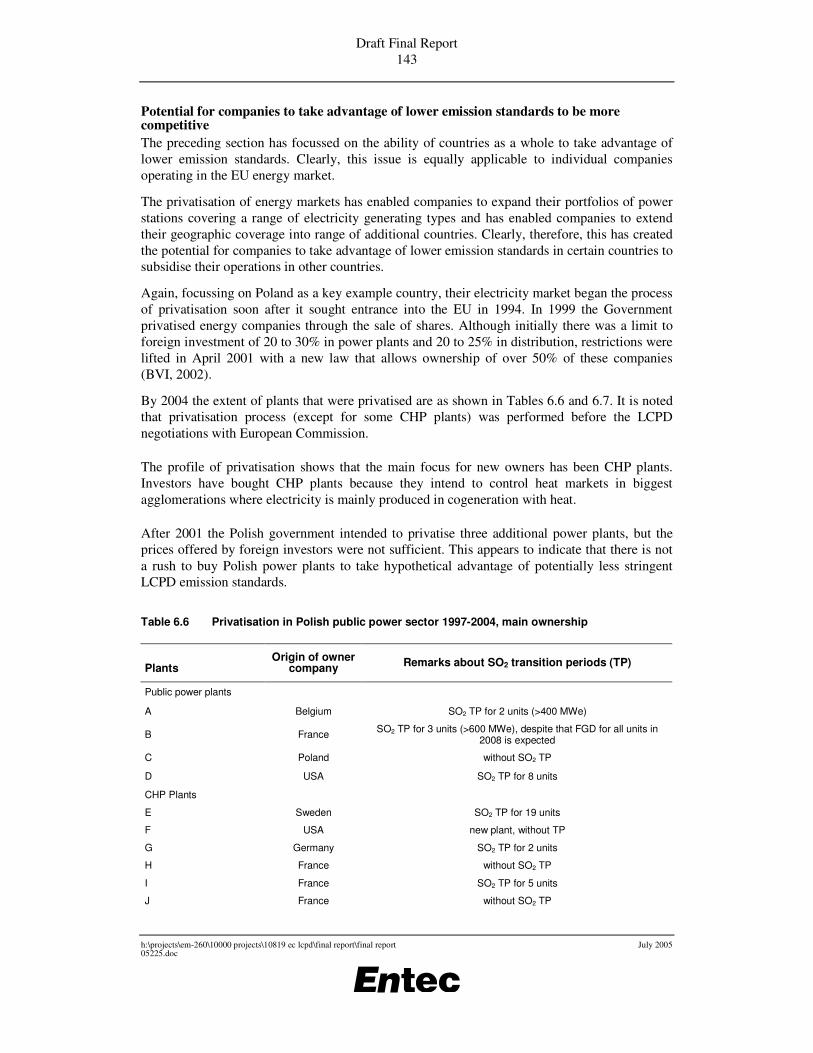

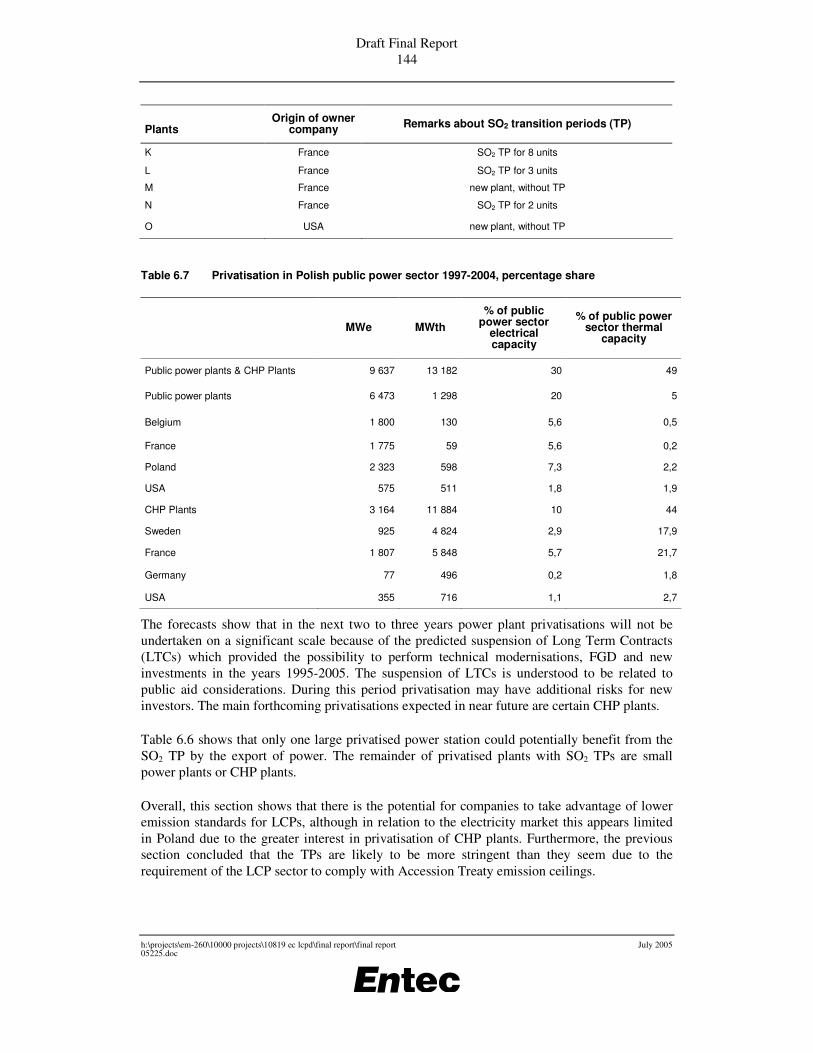

• Several new Member States have derogation allowances under the LCPD. Those with the most extensive derogation allowances, as well as the only countries with derogation allowances beyond 2008, include Estonia, Lithuania and Poland. Poland has, by far, the greatest number of plants with derogation allowances. However, Poland and Lithuania are also required to comply with conditions that set progressively tighter total emission ceilings for SO2 and NOx from the LCP sector.

1 Note that Slovenia withdrew its plan and opted for the ELV approach.

Final Report vi

h:\projects\em-260\10000 projects\10819 ec lcpd\final report\final report 05225.doc

July 2005

10819

As such, the true extent to which the derogation allowances are less stringent than the LCPD will be dependent on various factors, notably the projected fuel mixes for the electricity supply industry in these countries.

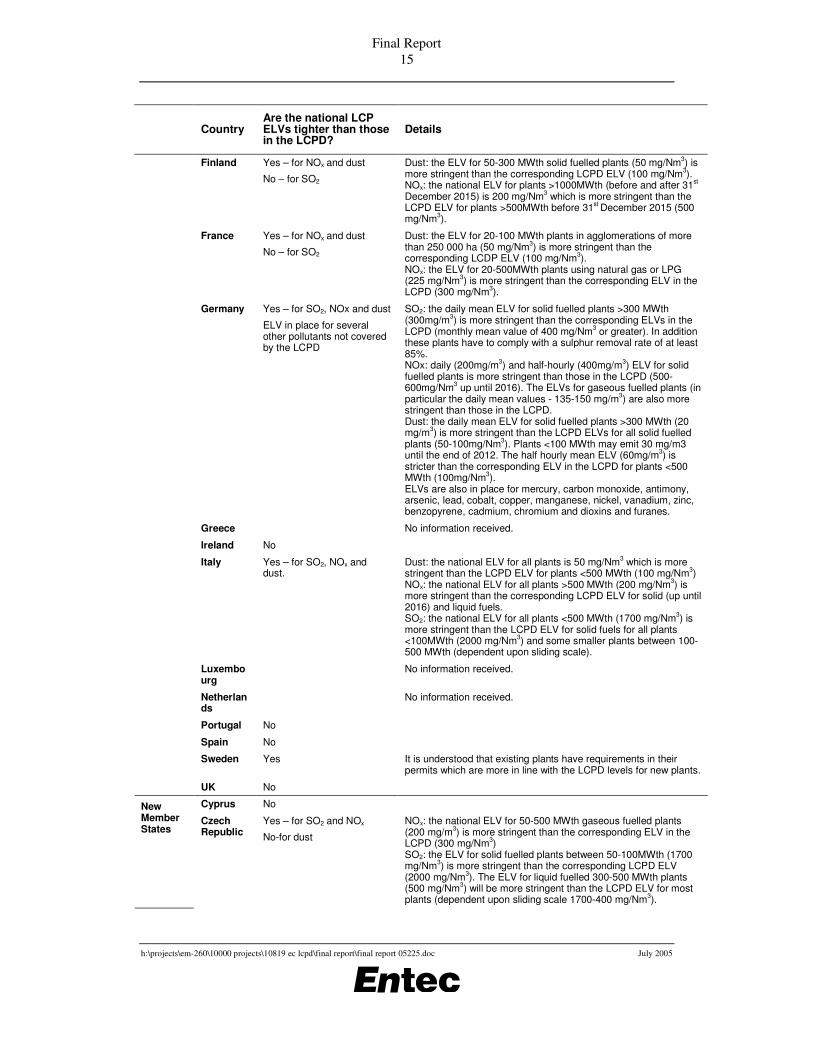

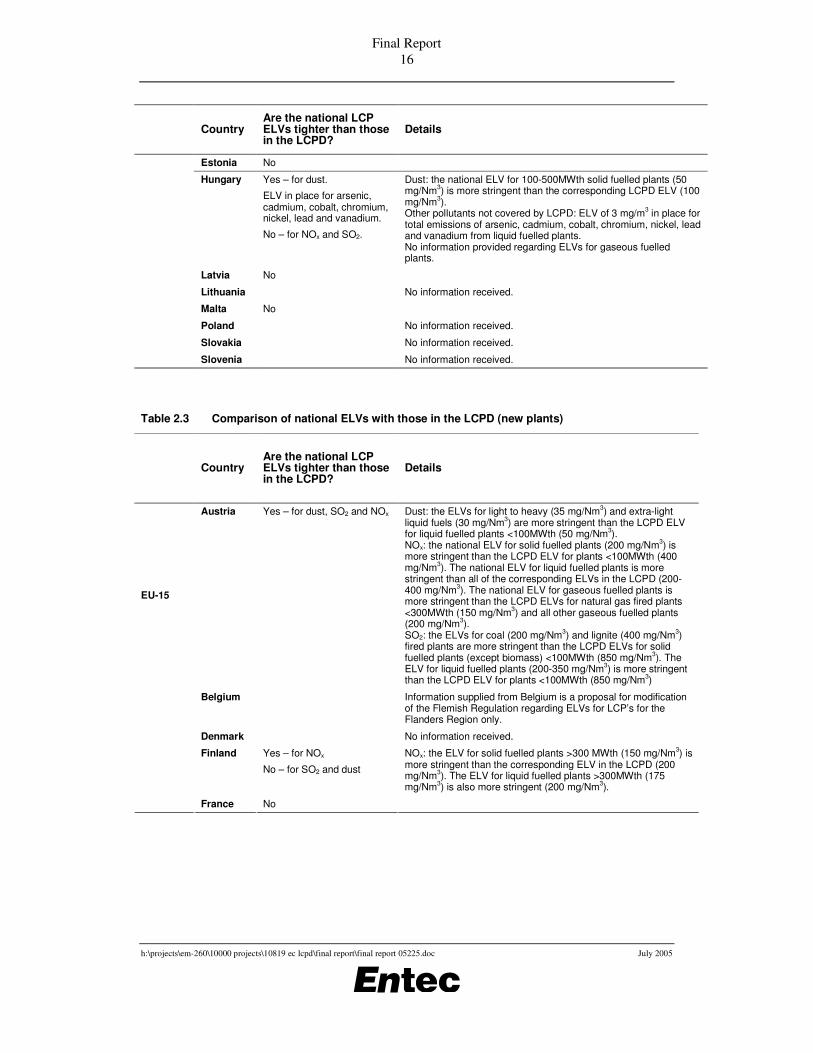

• Some Member States choose to set national ELVs for LCPs which go beyond those included in the LCPD. From a survey of Member States, it is clear that for existing plants many countries go further than the LCPD in terms of ELVs for at least one or more of the LCP pollutants of SO2, NOx or dust. In addition, a relatively small number of countries also impose ELVs for trace metals, with one country imposing ELVs for dioxins and PAHs. In contrast, for new plants most countries tend to set ELVs derived directly from the LCPD rather than going beyond it. For those countries that go beyond the LCPD for new plants, the additional stringency appears much less significant than for existing plants.

Large combustion plant emissions data Section 3 presents data on current and future emissions from LCPs across the EU25. The purpose of this section is to support conclusions on the quantity and profile of current emissions of key pollutants from LCPs, as well as an indication of the quantity and profile of future emissions of key pollutants expected under a ‘business as usual’ (BAU) scenario, incorporating the expected impact of agreed policies, including the current LCPD and IPPCD, to the extent that they have been taken into account in currently available modelling work.

By understanding the likely quantity and profile of future emissions from LCPs under a BAU scenario, it is then possible to give an indication of which types of LCPs and which pollutants may be of most interest in the event that any further reductions in emissions were required from the LCP sector. It is not within the scope of this study, however, to determine whether further reductions in LCP emissions would be required, in addition to those reductions expected under the BAU scenario.

Key summary points include:

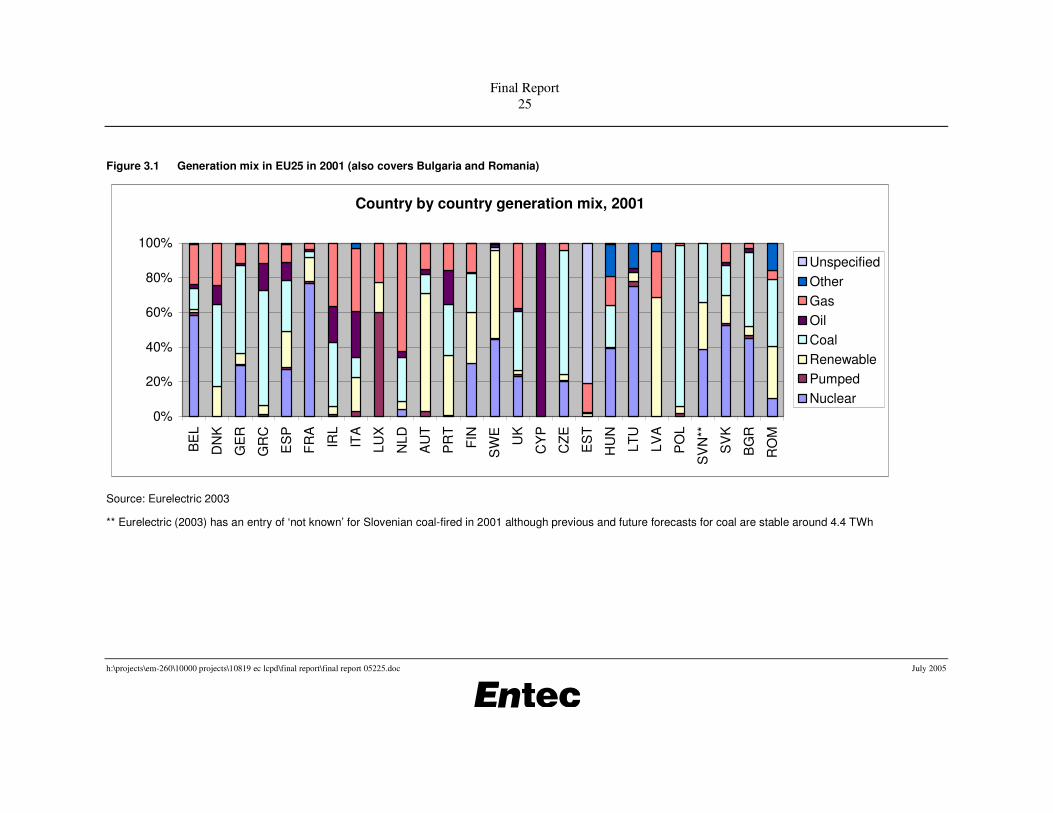

Fuel types and trends

• According to projections developed for the European Commission2, gas is projected to be the main energy source for electricity production beyond 2010. Overall, gas based electricity is predicted to grow from 16% of power generation in 2000 to 36% in 2030.

• Solid fuels are predicted to exhibit a continuous decline as an energy source for electricity production in the short / medium term, but later recover as a replacement fuel for nuclear both in absolute terms and as a share of total electricity generated. Overall the solid fuel share reduces from 32% in 2000 to 27% in 2030. Hard coal is projected to make a strong comeback in the long run, whereas this is not the case for lignite.

• Oil is becoming a more limited form for electricity production. Many of the existing oil fired plants are kept only as part of the reserve margin.

2 European Commission, 2003. European Energy and Transport Trends to 2030.

Final Report vii

h:\projects\em-260\10000 projects\10819 ec lcpd\final report\final report 05225.doc

July 2005

10819

Emissions data sources

• A key source of current emissions data for LCPs is given in the emissions inventories submitted by Member States (so far only EU15) under the requirements of the LCPD.

• Future (2010) emissions projections by Member States are incorporated in their projections developed to meet the requirements of the National Emission Ceilings Directive (NECD), however the data is usually aggregated within national totals hence the specific contributions from LCPs are not clear.

• The RAINS web model, which is being used to support the Commission’s CAFE programme, provides an important source of data with which to investigate projections of emissions for the LCP sector at an EU25 level. The main RAINS scenario referred to in this study is the ‘CP_CLE’ scenario, as agreed with the Commission. It has been selected because it provides data for each EU25 Member State, it incorporates assumptions on current legislative controls3 and climate measures, and its use will enable consistency with other studies undertaken for the Commission.

• The CP_CLE scenario uses energy projections developed from the PRIMES model. An equivalent scenario (also accounting for current legislative controls and climate measures) has been developed which uses national energy projections submitted by Member States. This ‘NAT’ scenario is only currently available for 10 Member States, but a comparison with the ‘CP_CLE’ scenario reveals significantly higher emissions for the public power sector under the ‘NAT’ scenario compared to the ‘CP_CLE’ scenario for many countries. Due to the clear sensitivity of energy projections in overall emissions estimations, it is therefore recommended that national energy projections are also taken into account when informing future policy developments affecting the LCP sector.

• It should be noted that the RAINS model does not have a specific sector for LCPs, with the best match given by the ‘Public Power’ (PP) sector. Overall this is thought to potentially underestimate LCP emissions because it excludes industrial boilers and process heaters (that are incorporated within various other sectors in the model), although this will be counteracted to some extent by the inclusion of plants <50MWth (ie not LCPs) within the PP sector. The match between LCPs is further complicated by the different definitions of ‘existing’ and ‘new’ plants between RAINS (based on PRIMES inputs with a cut-off year of 1995) and the LCPD (cut-off date of 1 July 1987).

• The ‘capacity controlled’ data (data on the percentage uptake of specific abatement measures for specific sector / fuel combinations) within the RAINS model is a significant variable affecting overall emissions and consultations between IIASA and Member States have sought to review and, where necessary, correct this and other key data within the model. However, due to the significance of these assumptions on emissions estimates, it is recommended that if using the RAINS model to inform policy developments affecting the LCP sector, then positive

3 Including the Large Combustion Plant Directive.

Final Report viii

h:\projects\em-260\10000 projects\10819 ec lcpd\final report\final report 05225.doc

July 2005

10819

confirmation is gained from Member States that the assumptions within the model represent best available data. For example, some general observations on the data include higher than expected levels of future uptake of SCR for coal, lignite and gas plants, which may lead to an underestimation in NOx emission projections.

• The European Pollutant Emissions Register (EPER) provides an additional source of data on emissions from LCPs. However, this data is likely to represent an underestimation because emissions from LCPs at some sites (eg petroleum refineries) are reported under separate sectors and the data is dependent on the completeness of reporting for each site. As such, the EPER emissions data is only used in this study when more robust data is not available.

• To supplement the abovementioned sources, Entec has gathered data at a plant level on emissions, activity levels, fuel types and abatement techniques for LCPs. This covers a large number of EU25 member states and focuses on the dominant LCP sector, namely the electricity supply industry. For each Member State information was sought on a representative plant in each of a number of categories (based on size, age and abatement levels), with plants considered as representative within a category where the capacity, activity rate (load factor) and level of emission control was broadly typical of the category as a whole.

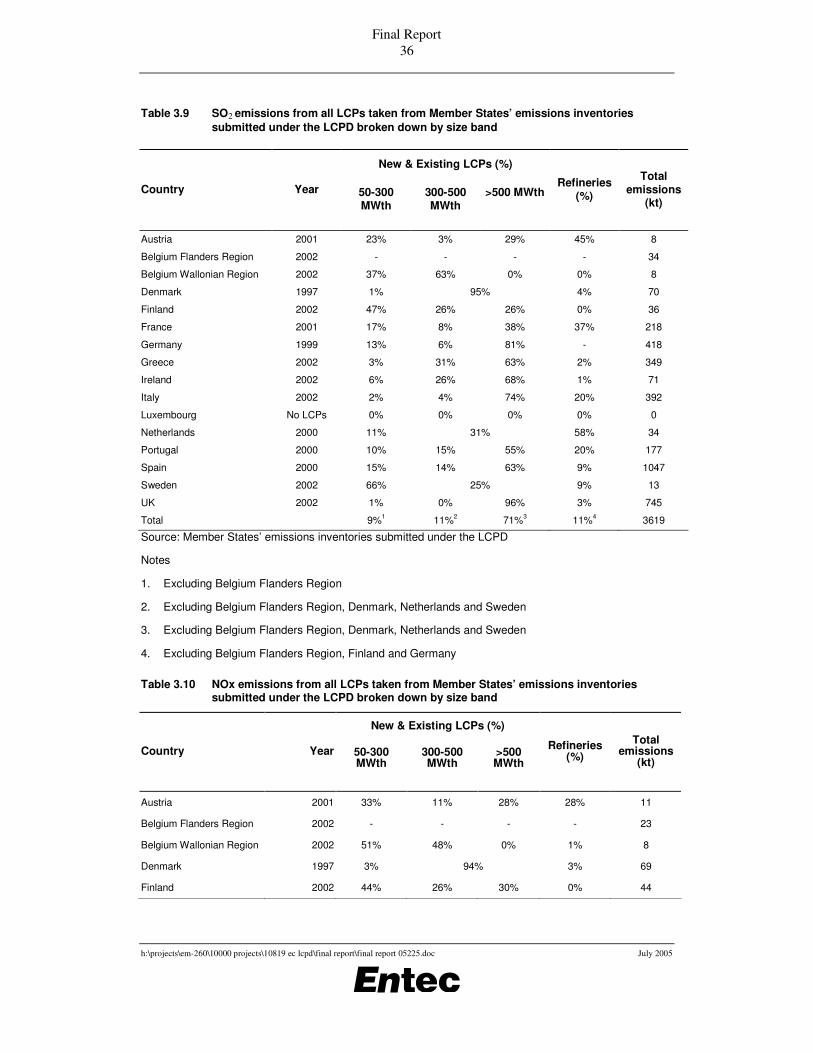

SO2 emissions

• According to the emission inventories submitted under the LCPD, total current SO2 emissions from LCPs in EU15 are in the region of 3600kt.

• Within this total, the majority is from plants >500MWth (71%), with 11% from 300-500MWth plants, 9% from 50-300MWth plants and 11% from petroleum refineries. However the proportionately tighter requirements in the LCPD on larger plants is expected to increase the relative contribution from smaller plants and petroleum refineries in the future.

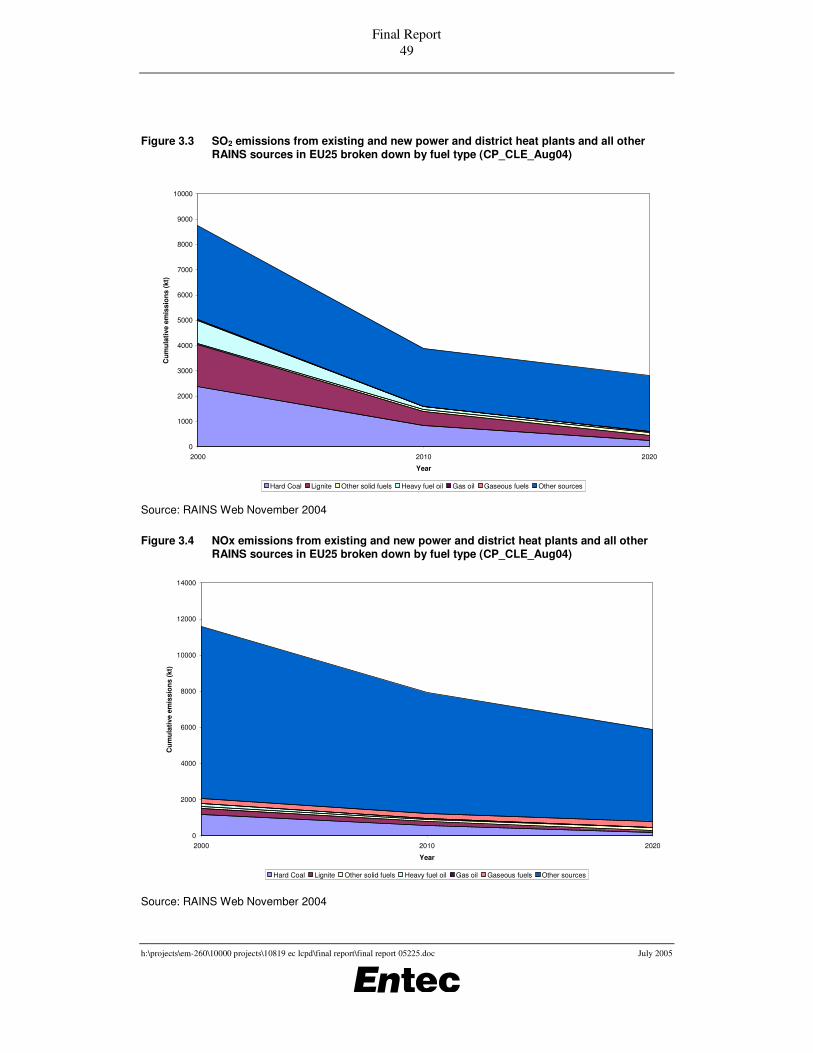

• According to the RAINS CP_CLE scenario, SO2 emissions from public power plants in EU25 are estimated to decline between 2000 and 2020 both in absolute terms (5015kt to 606kt) and relative terms in comparison to emissions from all RAINS sources (57% to 22%).

• Within the public power sector, the fuel types contributing greatest SO2 emissions by 2020 are hard coal (39% of emissions from public power) and lignite (33%).

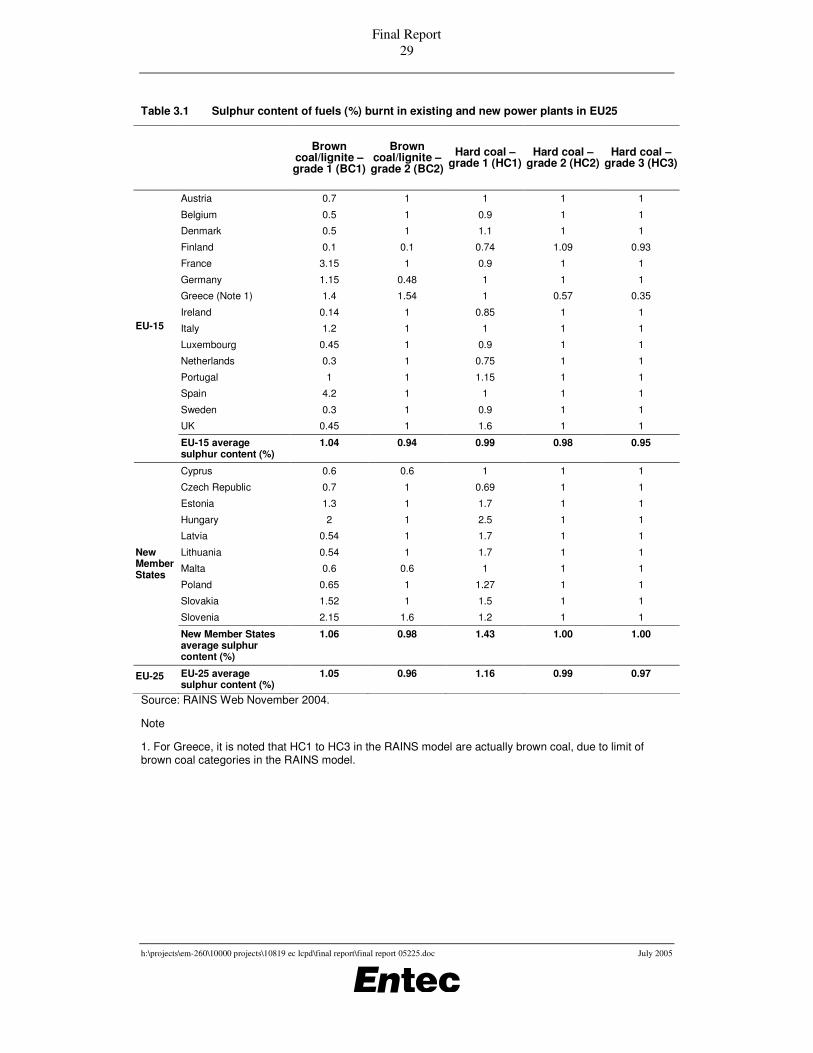

• The RAINS model estimates that the average level of sulphur in hard coal is 1.2% in EU25, and the average for lignite is 1.1%. However, the lower calorific value of lignite means that its sulphur content per unit energy is higher for lignite than hard coal. These sulphur levels are generally higher than levels for internationally traded coal.

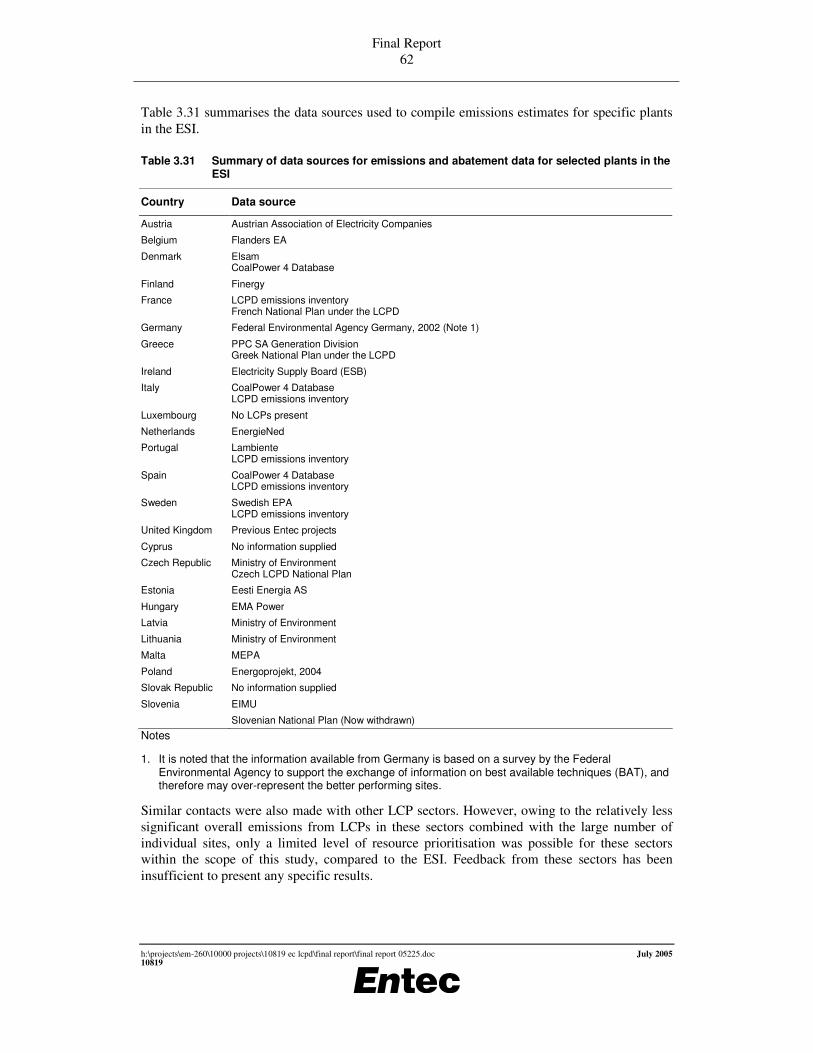

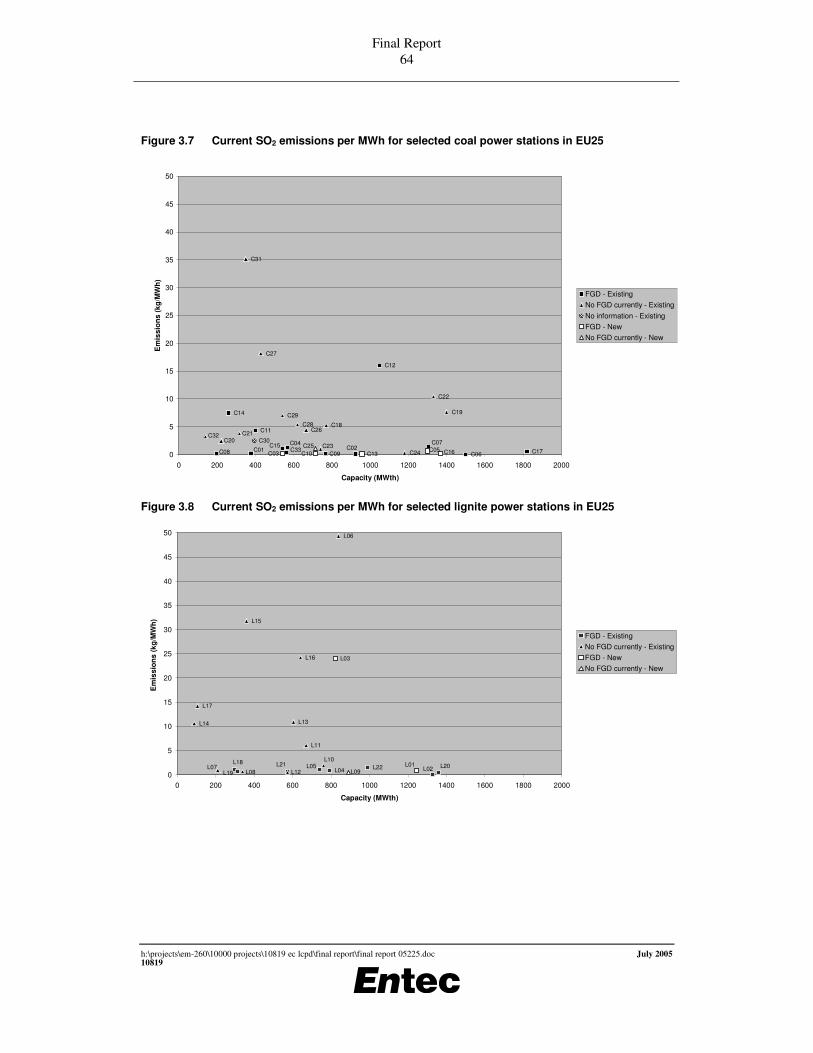

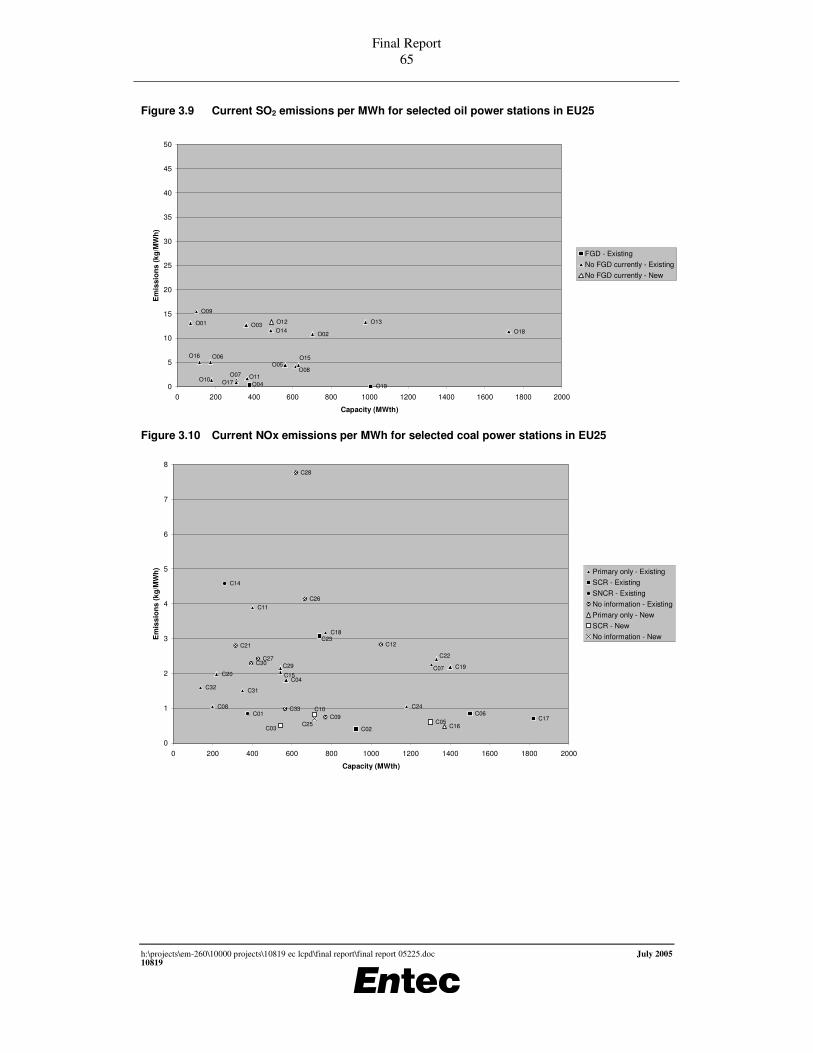

• Based on data gathered for this study from a number of selected power stations across the EU25, SO2 emissions per MWh of electricity produced are shown below:

Final Report ix

h:\projects\em-260\10000 projects\10819 ec lcpd\final report\final report 05225.doc

July 2005

10819

Fuel General range in current emissions (kg per MWh), selected power stations in EU25

FGD No FGD currently

Coal 0.1 to 5, some values higher 1 to 20, some values higher

Lignite 0.1 to 2, some values higher 1 to 35, some values higher

Oil 0.1 to 0.3 (limited data points) 1 to 15

NOx emissions

• According to the emission inventories submitted under the LCPD, total current NOx emissions from LCPs in EU15 are in the region of 1500kt.

• Within this total, the majority is from plants >500MWth (72%), with 10% from 300-500MWth plants, 12% from 50-300MWth plants and 7% from petroleum refineries. As for SO2, the proportionately tighter requirements in the LCPD on larger plants is expected to increase the relative contribution from smaller plants and petroleum refineries in the future.

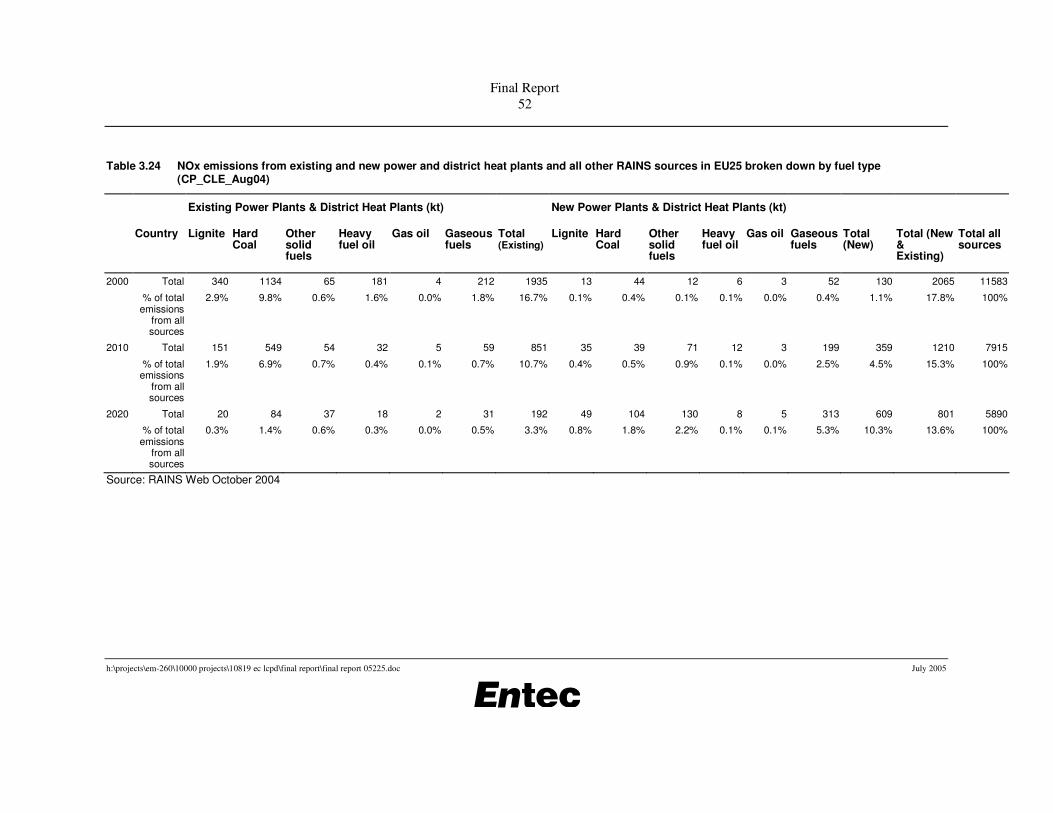

• According to the RAINS CP_CLE scenario, NOx emissions from public power plants in EU25 are estimated to decline between 2000 and 2020 both in absolute terms (2065kt to 801kt) and relative terms in comparison to emissions from all RAINS sources (18% to 14%).

• Within the public power sector, the fuel types contributing greatest NOx emissions by 2020 are gas (45% of emissions from public power) and hard coal (24%).

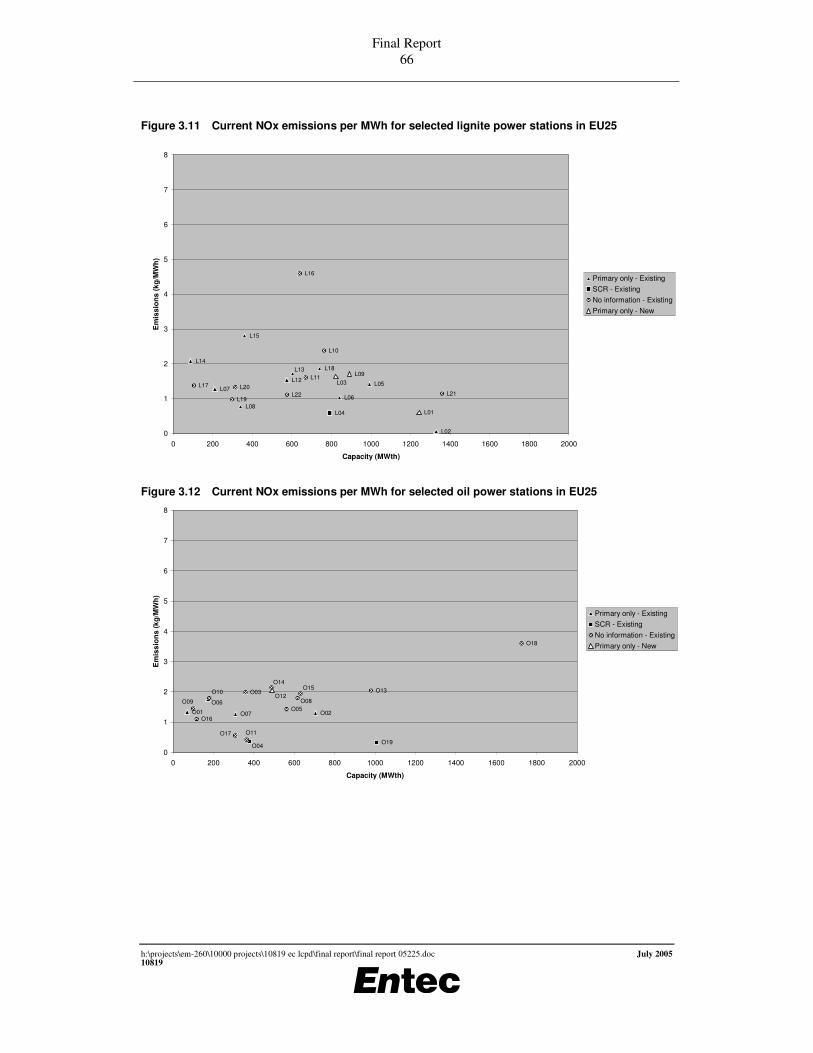

• Based on data gathered for this study from a number of selected power stations across the EU25, NOx emissions per MWh of electricity produced are shown below:

Fuel General range in current emissions (kg per MWh), selected power stations in EU25

SCR Primary measures only

Coal 0.4 to 1 1 to 4

Lignite No data (SCR not widely fitted to lignite plants)

0.5 to 3

Oil 0.3 to 0.4 (limited data points) 1 to 2

Dust and PM emissions

• Of the particle size fractions, PM2.5 is of most concern because it is associated with proportionately higher levels of trace metals and is more easily respirable than larger particle sizes.

• According to the RAINS CP_CLE scenario, PM emissions from public power plants in EU25 are estimated to decline between 2000 and 2020 both in absolute terms (249kt to 85kt for PM10 and 148kt to 55kt for PM2.5) and relative terms in

Final Report x

h:\projects\em-260\10000 projects\10819 ec lcpd\final report\final report 05225.doc

July 2005

10819

comparison to emissions from all RAINS sources (10% to 6% for PM10 and 9% to 6% for PM2.5).

• Within the public power sector, the fuel types contributing greatest PM10 and PM2.5

emissions by 2020 are hard coal (47% of PM10 emissions from public power and 44% of PM2.5 emissions) and lignite (40% of PM10 and PM2.5).

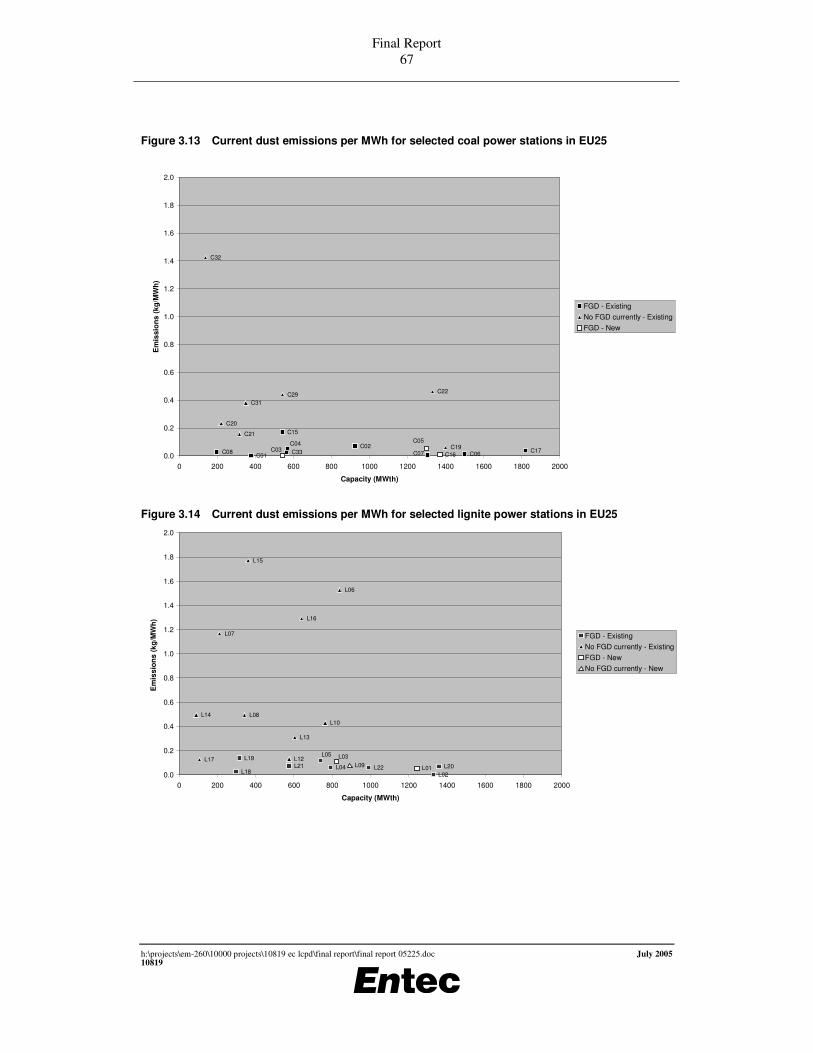

• Based on data gathered for this study from a number of selected power stations across the EU25, dust emissions per MWh of electricity produced are shown below:

Fuel General range in current emissions (kg per MWh), selected power stations in EU25

FGD No FGD currently

Coal 0.01 to 0.2 0.1 to 0.5

Lignite 0.01 to 0.2 0.1 to 2

Oil 0.02 (limited data) 0.01 to 1

• For dominant LCP sources of PM, namely large coal and lignite power stations, according to the RAINS model, a large proportion of plants are assumed to be fitted with more than 2 ESP fields which are assumed to achieve high levels of abatement of PM2.5 (99.0%), and 99.6% abatement of PM10.

• Of the PM that is emitted from these plants, the majority is expected to be PM2.5. As it is not generally possible to vary any ratio between fractional abatement efficiencies for coarse and fine PM in a practical way in ESPs (the dominant PM abatement technique by far in the power sector), lowering the amount of overall PM emissions will also lower the amount of PM2.5. Therefore, the requirement for any further reductions in PM2.5 emissions from such power stations could effectively be achieved through tighter overall dust emission standards.

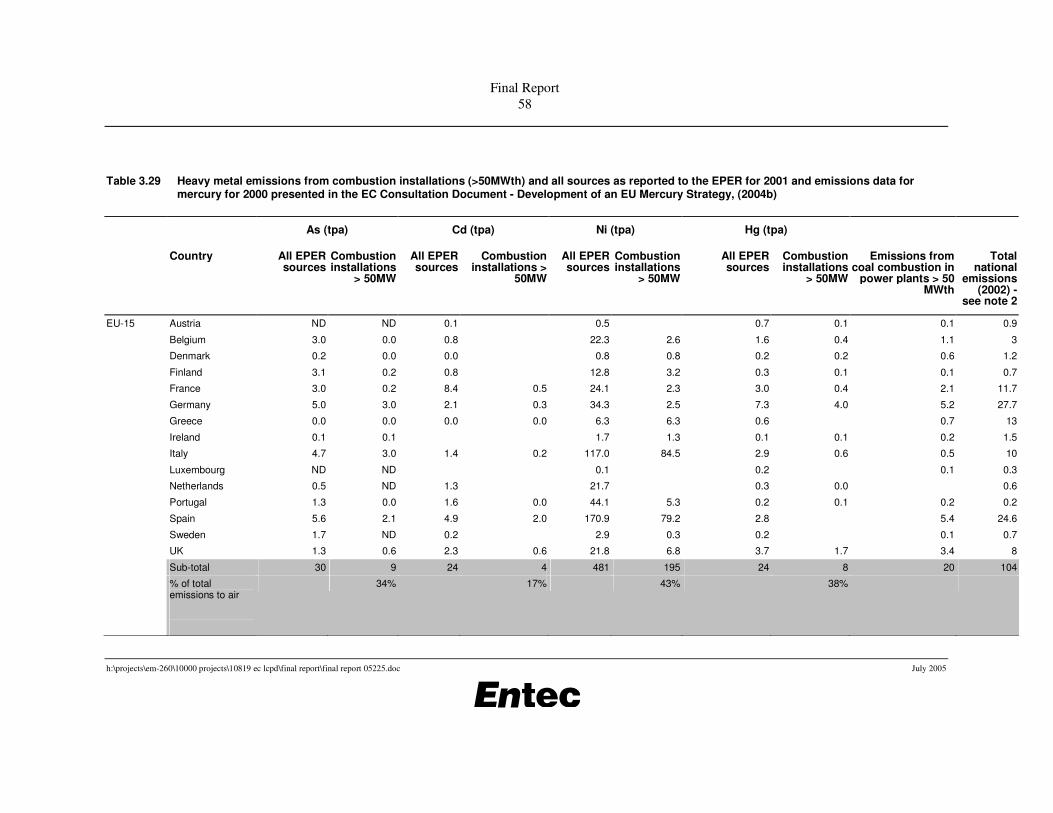

Heavy metal emissions

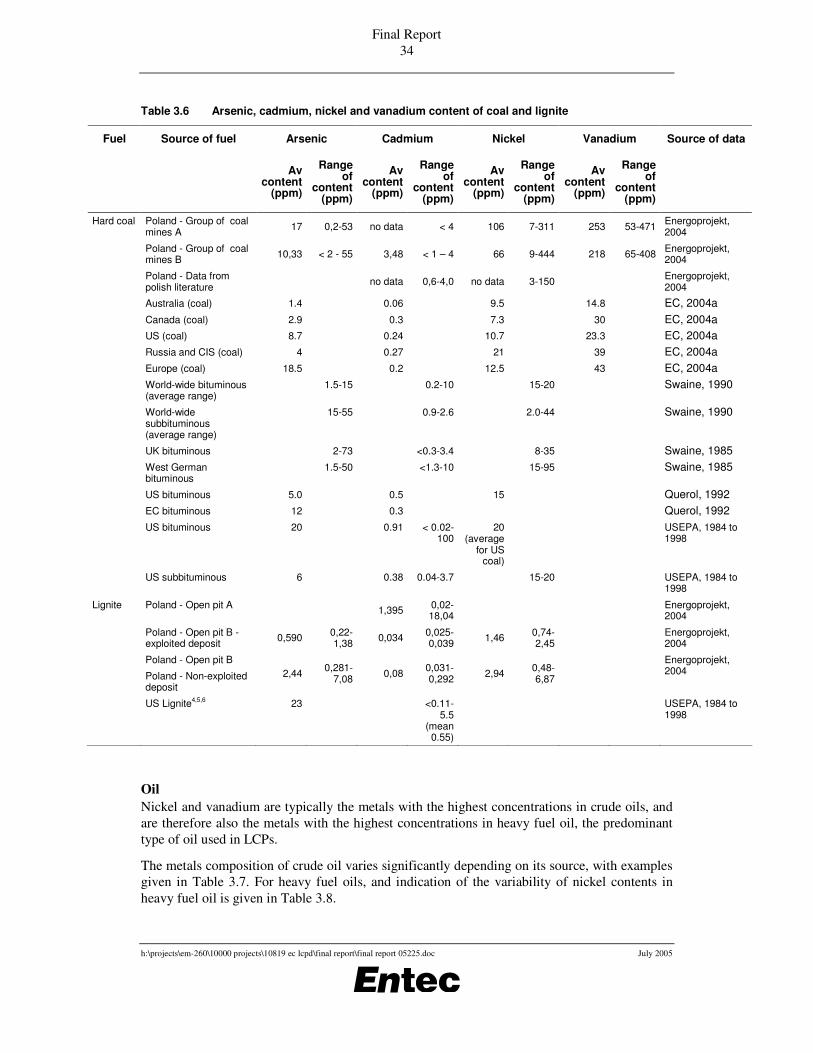

• Heavy metals in coal and lignite are normally several orders of magnitude higher than in oil (except occasionally for nickel and vanadium in heavy fuel oil) or natural gas.

• There can be significant variations in the concentration of mercury and other heavy metals in coal and lignite between different countries and between different mines within the same country.

• Key heavy metals in LCP emissions, with the exception of mercury, are associated with particulate matter. As such, measures focussed on particulate matter abatement will also be the most appropriate measures for abating those types of metals, and can achieve high levels of abatement (generally over 99% abatement is possible with ESPs and FGD). For these metals, dust emission standards can represent an effective proxy for the control of such metal emissions from LCPs. The use of dust emission standards in this way would also avoid the potential difficulties associated with direct heavy metal emission limit values, namely that there can be very significant variations in the heavy metals content of the same type of fuel, but from different mines or crude types.

Final Report xi

h:\projects\em-260\10000 projects\10819 ec lcpd\final report\final report 05225.doc

July 2005

10819

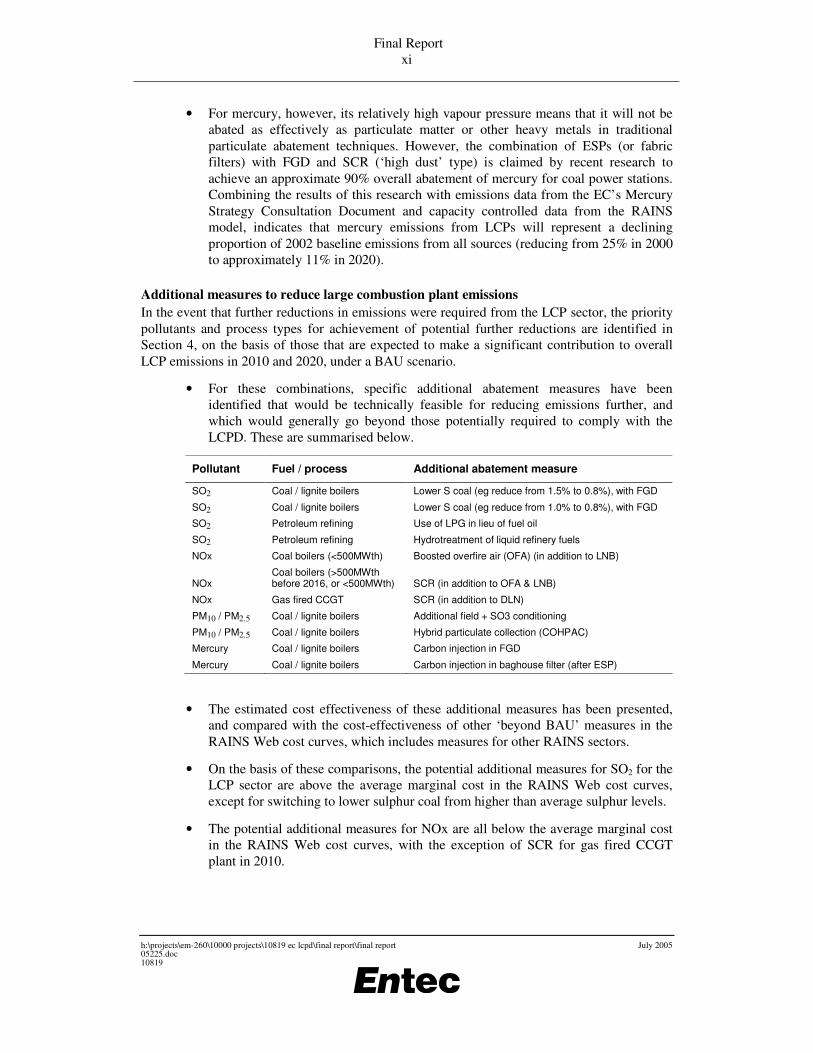

• For mercury, however, its relatively high vapour pressure means that it will not be abated as effectively as particulate matter or other heavy metals in traditional particulate abatement techniques. However, the combination of ESPs (or fabric filters) with FGD and SCR (‘high dust’ type) is claimed by recent research to achieve an approximate 90% overall abatement of mercury for coal power stations. Combining the results of this research with emissions data from the EC’s Mercury Strategy Consultation Document and capacity controlled data from the RAINS model, indicates that mercury emissions from LCPs will represent a declining proportion of 2002 baseline emissions from all sources (reducing from 25% in 2000 to approximately 11% in 2020).

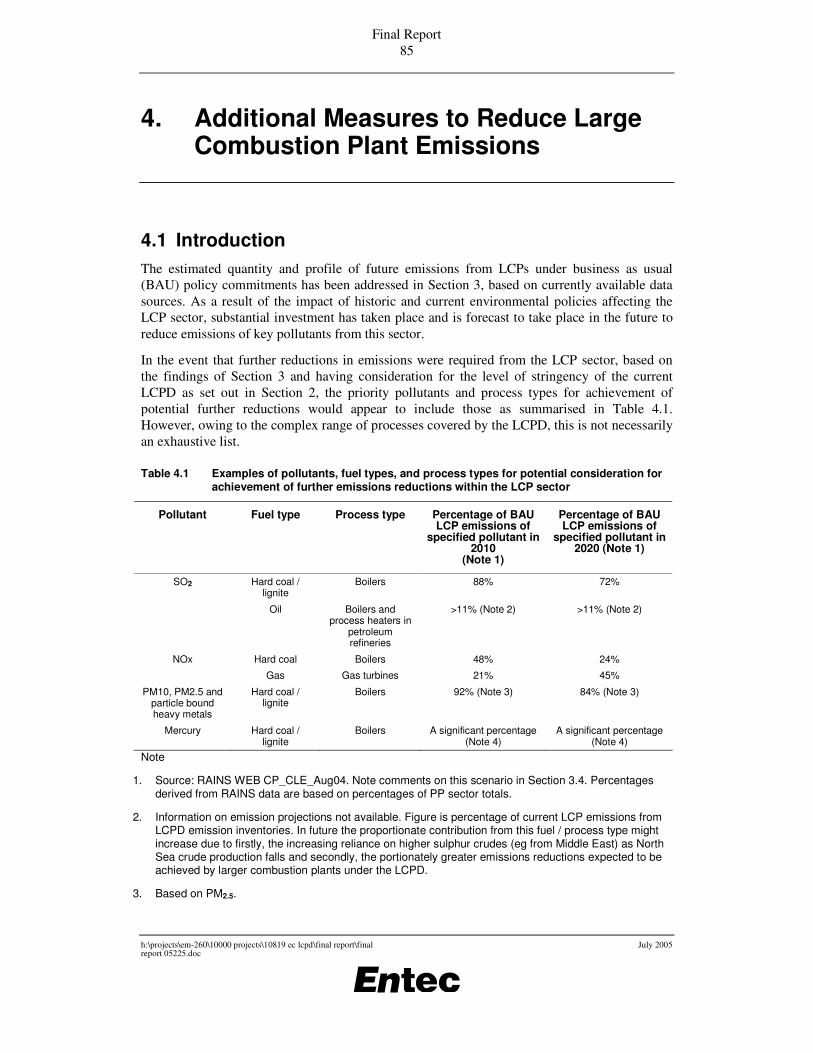

Additional measures to reduce large combustion plant emissions In the event that further reductions in emissions were required from the LCP sector, the priority pollutants and process types for achievement of potential further reductions are identified in Section 4, on the basis of those that are expected to make a significant contribution to overall LCP emissions in 2010 and 2020, under a BAU scenario.

• For these combinations, specific additional abatement measures have been identified that would be technically feasible for reducing emissions further, and which would generally go beyond those potentially required to comply with the LCPD. These are summarised below.

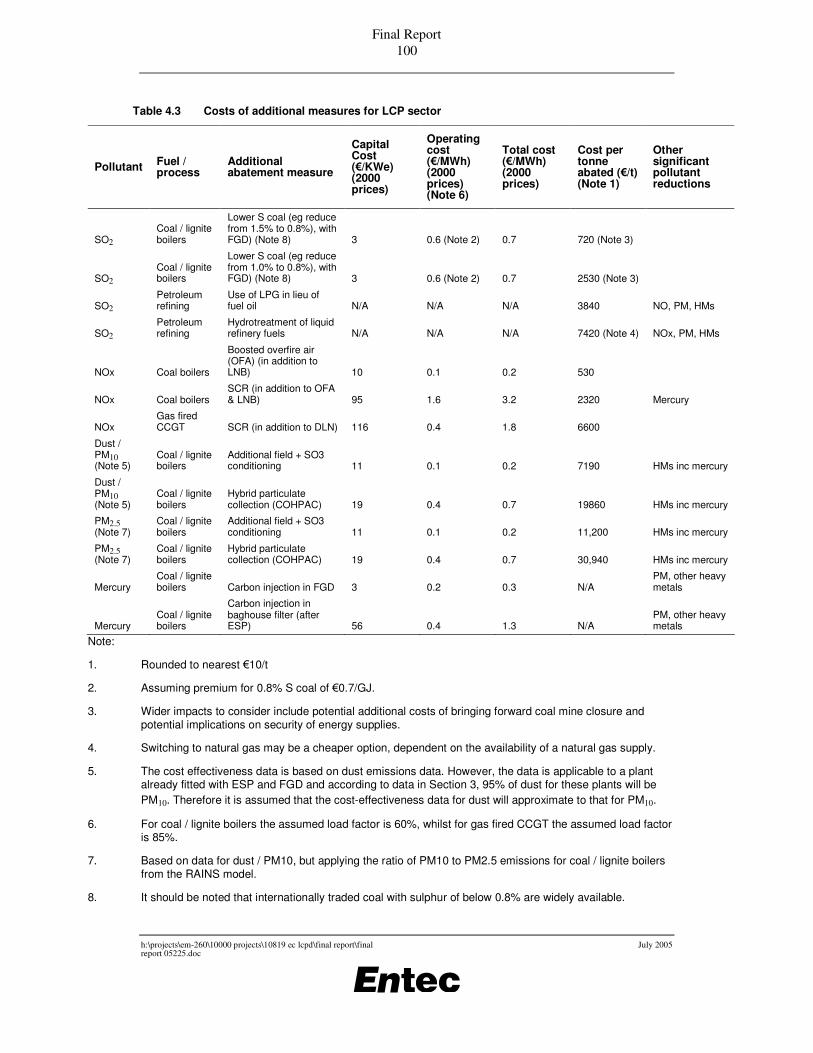

Pollutant Fuel / process Additional abatement measure

SO2 Coal / lignite boilers Lower S coal (eg reduce from 1.5% to 0.8%), with FGD

SO2 Coal / lignite boilers Lower S coal (eg reduce from 1.0% to 0.8%), with FGD

SO2 Petroleum refining Use of LPG in lieu of fuel oil

SO2 Petroleum refining Hydrotreatment of liquid refinery fuels

NOx Coal boilers (<500MWth) Boosted overfire air (OFA) (in addition to LNB)

NOx Coal boilers (>500MWth before 2016, or <500MWth) SCR (in addition to OFA & LNB)

NOx Gas fired CCGT SCR (in addition to DLN)

PM10 / PM2.5 Coal / lignite boilers Additional field + SO3 conditioning

PM10 / PM2.5 Coal / lignite boilers Hybrid particulate collection (COHPAC)

Mercury Coal / lignite boilers Carbon injection in FGD

Mercury Coal / lignite boilers Carbon injection in baghouse filter (after ESP)

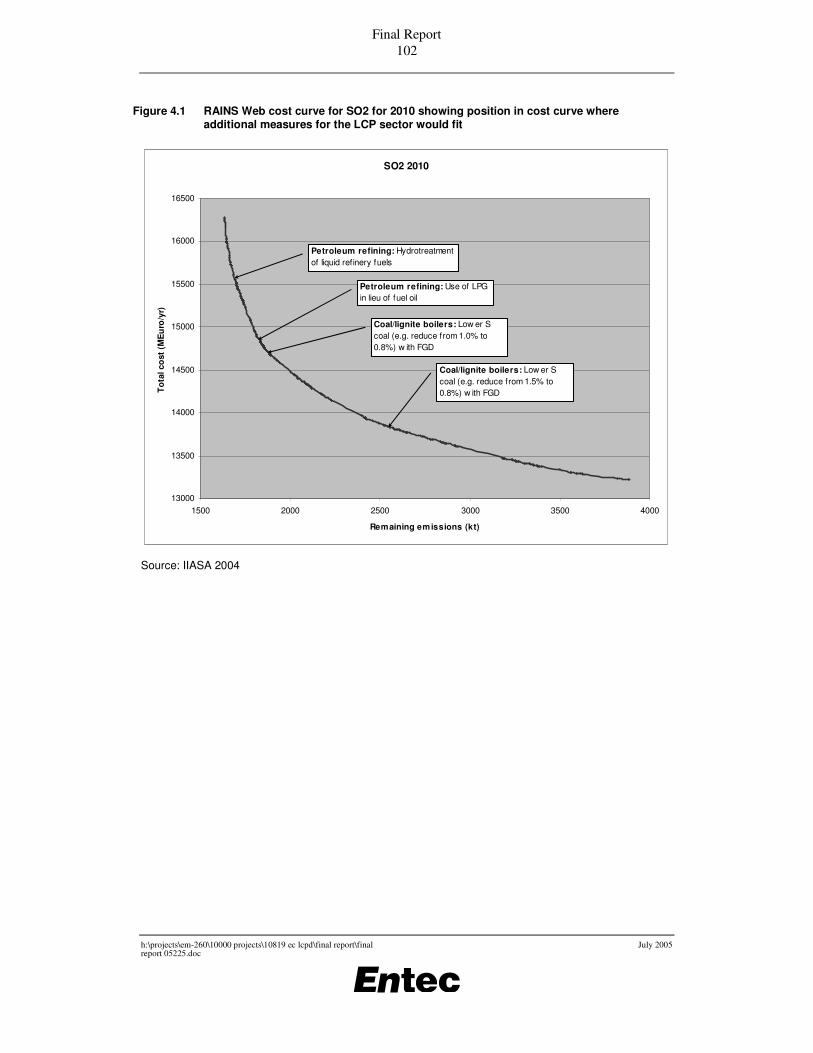

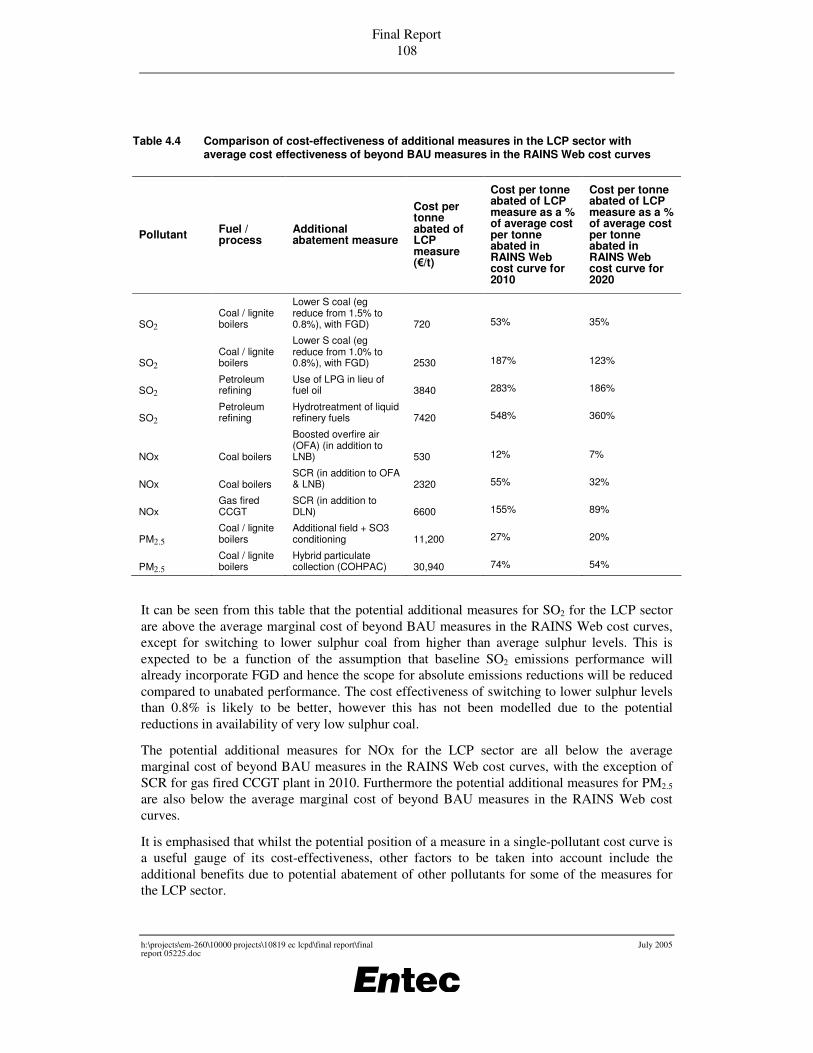

• The estimated cost effectiveness of these additional measures has been presented, and compared with the cost-effectiveness of other ‘beyond BAU’ measures in the RAINS Web cost curves, which includes measures for other RAINS sectors.

• On the basis of these comparisons, the potential additional measures for SO2 for the LCP sector are above the average marginal cost in the RAINS Web cost curves, except for switching to lower sulphur coal from higher than average sulphur levels.

• The potential additional measures for NOx are all below the average marginal cost in the RAINS Web cost curves, with the exception of SCR for gas fired CCGT plant in 2010.

Final Report xii

h:\projects\em-260\10000 projects\10819 ec lcpd\final report\final report 05225.doc

July 2005

10819

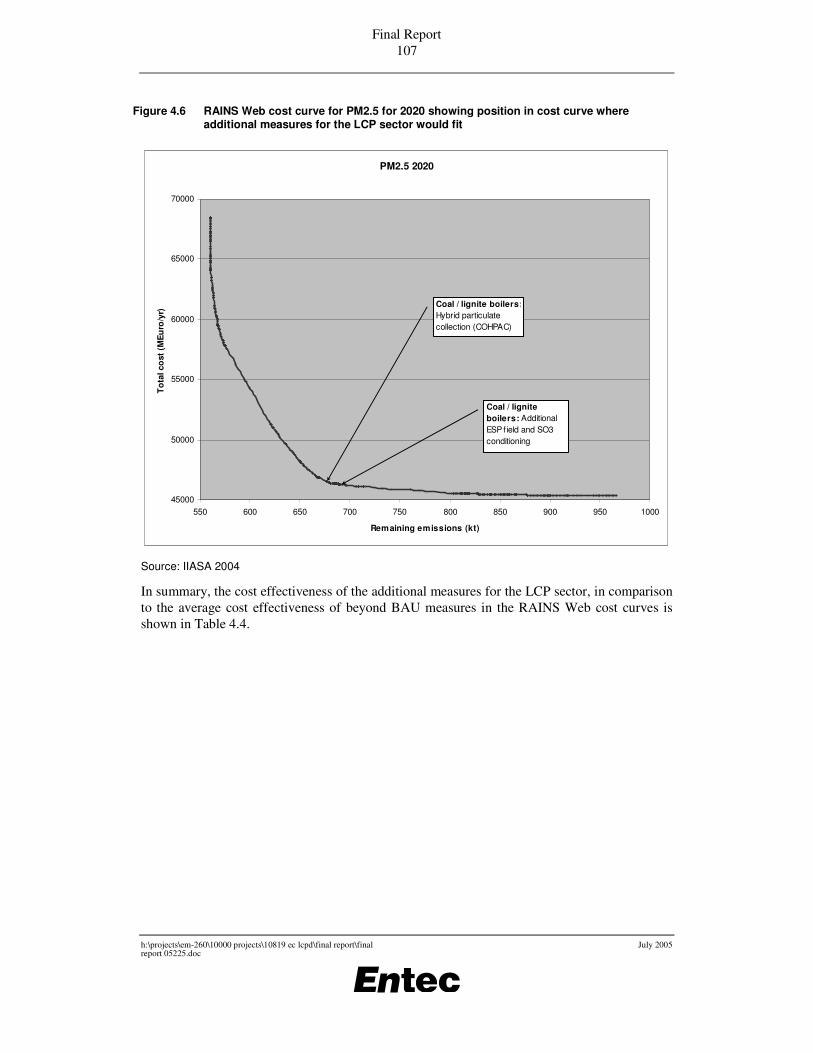

• Furthermore the potential additional measures for PM2.5 are also below the average marginal cost in the RAINS Web cost curves.

• It is emphasised that whilst the potential position of a measure in a single-pollutant cost curve is a useful gauge of its cost-effectiveness, other factors to be taken into account include the additional benefits due to potential abatement of other pollutants. This could be a significant issue for some of the measures for the LCP sector, including the PM2.5 and mercury measures and the SO2 measures for the petroleum refining sector.

• Furthermore, whilst the scope of this particular study does not extend to a cost-benefit analysis, it would clearly be necessary to consider the costs in more detail (including absolute costs and relevant wider economic impacts) and to quantify the health and environmental benefits of any potential emissions reductions in the event of further policy development related to potentially tighter standards in the LCP sector.

Assistance on possible end dates or of lower limit values for the NOx ELV derogation A brief section (Section 5.1) provides supporting information related to possible end dates or lower limit values for the derogation contained in footnote 2 to Annex VI A. This derogation allows operators of solid fuel LCPs >500MWth a less stringent NOX ELV if they do not operate for more than 2,000 hours per annum until 31/12/15 (ELV of 600 vs 500mg/Nm3) and 1,500 hours per annum after 01/01/16 (ELV of 450 vs 200mg/Nm3). Key summary points include:

• At the present time it is difficult to foresee a significant number of plants seeking to qualify for this low load factor derogation allowing less stringent NOx ELVs. This is due to economic constraints of operating at very low load factors combined with only a limited relaxation in emission standards (for the period to 2016). As such, plants covered by this derogation are expected to make only a relatively small contribution to overall NOx emissions from the LCP sector.

• Furthermore, until 2016, the slightly more relaxed ELV appears sensible in making provision for potential technical difficulties of older (and potentially low load factor) boilers fitting OFA. Beyond 2016, the less stringent ELVs should still trigger advanced primary NOx abatement measures, which would be an appropriate measure for very low load factor plants, rather than SCR.

• However, it would be recommended that a more accurate indication of the potential uptake of this derogation is sought in 2008, to assess how significant the derogation is in terms of emissions. Following this a further review could be undertaken of the potential need to tighten the ELVs from 2016 for low load factor plants, based on the information available at that time on achievable emission levels for advanced primary NOx measures (eg OFA, reburn, etc).

Potential inclusion of offshore gas turbines in the LCPD The current LCPD excludes from its scope gas turbines used on offshore platforms, although these are covered under the IPPC Directive. In contrast, onshore gas turbines licensed from 27 November 2002, and with a thermal input of at least 50MW, are included within the scope of the directive. A brief section (Section 5.2) provides supporting information related to the potential justification, if any, for inclusion of offshore gas turbines (of at least 50MWth) within

Final Report xiii

h:\projects\em-260\10000 projects\10819 ec lcpd\final report\final report 05225.doc

July 2005

10819

the scope of the directive. The focus is specifically concerned with NOx emissions, to be consistent with the pollutant of concern for gas turbines in the current LCPD, and to reflect the dominant LCPD pollutant from this type of plant. Key summary points include:

• According to industry estimates, projected NOx emissions from the offshore gas turbine sector are expected to represent a relatively small and decreasing share of overall NOx emissions from the EU25 LCP sector from 2010 to 2020, although there is greater uncertainty in the potential contribution to be made by new gas turbines.

• The available information indicates that the most applicable NOx abatement technology for offshore gas turbines is DLN.

• For dual fuel gas turbines, DLN does not appear to be proven at the current time for the offshore sector due to operational problems experienced in practice and by fuel constraints.

• For single fuel gas turbines, DLN does not appear to be proven where the field gas is of variable or inappropriate composition.

• Within the offshore sector, this technology is most applicable to new single fuel (gas fired) gas turbines using gas with a reasonably steady and acceptable composition. This technology is estimated to have a low range cost of approximately �310/t NOx abated. Whilst this is well below the average marginal cost for ‘beyond BAU’ NOx measures (according the RAINS Web cost curves described in Section 4), potential impacts of reduced reliability, higher maintenance and higher fuel consumption costs would increase this cost, although these elements are difficult to estimate, being very application specific.

• Furthermore, whilst retrofitting DLN technology has been undertaken in practice in a small number of offshore examples, experience shows it to be significantly more expensive than the application of this technology to new gas turbines (a low range estimate of the marginal cost is �1570/t) due to the potential requirement for modifications to other equipment and the potential impacts on production during the retrofitting period. Furthermore, it is possible that not all gas turbine types in operation will be upgradable to DLN technology.

Effects of differences between Community environmental standards for the LCP sector Section 6 investigates the effects of differences between the Community environmental standards for the LCP sector on competition in the energy market, focussing particularly on where there is expected to be a delay in meeting the LCPD requirements due to derogation allowances for new Member States. In addition, this section gives brief consideration to the effects of differences in standards on the environment. Key summary points include:

• The currently available capacity of European interconnection is reported to be insufficient to satisfy demand for exchange within a single market. However, ‘bottleneck’ congestion points have been identified and the Commission has put forward an action plan to address this issue. Further integration of administrative networks is also planned, with regionalised integration of markets expected to develop prior to full harmonisation within a single market.

Final Report xiv

h:\projects\em-260\10000 projects\10819 ec lcpd\final report\final report 05225.doc

July 2005

10819

• Domestic market conditions play an important role in allowing competition between domestic and import suppliers. These issues are addressed within the European Union by the implementation of Electricity Directive (2003/54/EC). Full supply market opening to non-household customers, allowing customers to choose their supplier is set for 2004.

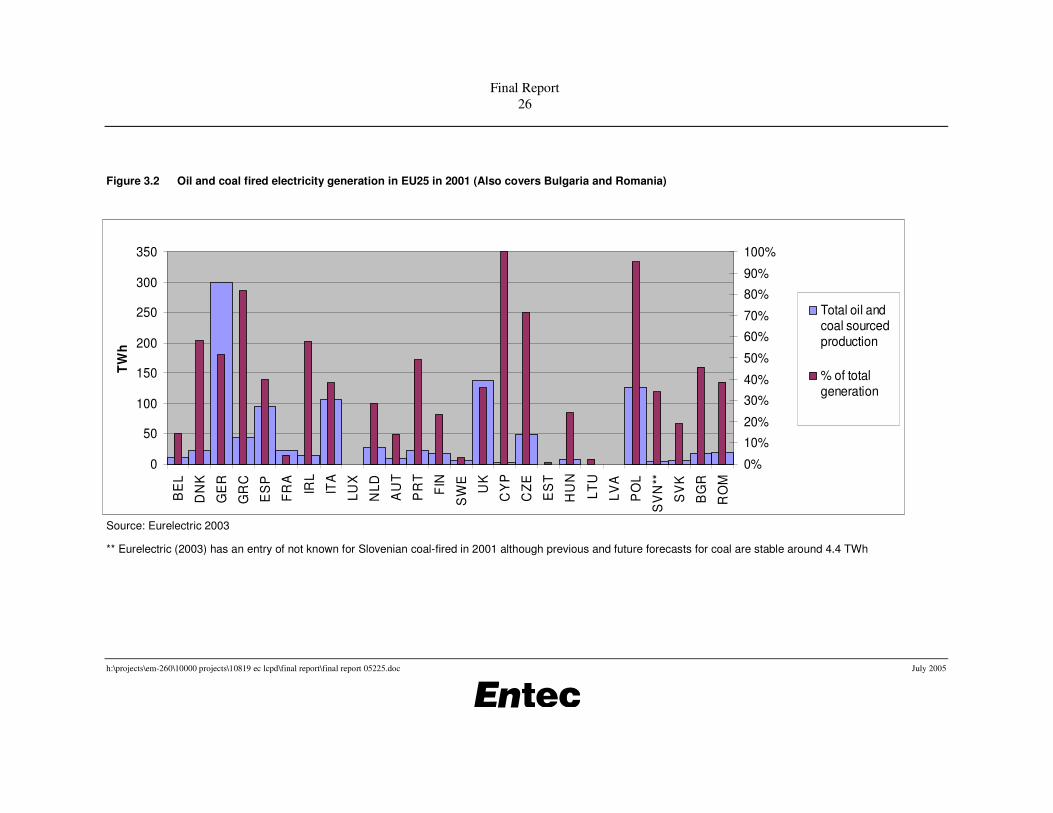

• The Member States with the greatest capacity to generate electricity from coal and oil fired plants (the key fuel types affected by the LCPD ELVs) are Germany, Greece, Spain, Italy, the UK, Czech Republic and Poland. Of these Member States, Poland appears to have greatest potential for export from power stations without flue gas desulphurisation (FGD).

• Whilst Poland has a transition period of 8 years for the SO2 requirements (and 2 years for the 2016 NOx requirements), it is roughly estimated that the associated Accession Treaty emission ceilings will have the effect of reducing this transition period to about 4 years. Therefore the length of time for which lower emission standards will apply is expected to be shorter than implied in the Accession Treaty. Furthermore, during this time, the scope for Poland to export electricity to countries with tighter standards is likely to reduce from current levels due to increased domestic demand for electricity and reductions in power plant capacity. The picture is expected to be broadly similar for other new Member States with derogation allowances, although on a less substantial scale to that of Poland.

• On the basis of this brief investigation, the overall situation is that whilst there is the potential for countries with derogation allowances to take advantage of lower emission standards, in practice the scope for this is expected to be relatively limited and declining in the future.

• Due to the multitude of policies affecting the environmental impact of air emissions from LCPs (including LCPD, IPPCD, Air Quality Daughter Directives, National Emission Ceilings Directive, etc) and the different options that operating companies have got in response to these policies, it is not possible to draw any broad conclusions on the effects of differences between the Community environmental standards for the LCP sector on the environment. Notwithstanding this, it is clear that the differences in LCP standards themselves are becoming smaller in time, between the best and the worst performing ‘old’ Member States, and between the ‘old’ and ‘new’ Member States.

Screening level analysis of the feasibility and desirability of market based instruments for SO2 and NOx in the EU LCP sector Section 7 briefly identifies key aspects of EU and US approaches to reducing emissions of SO2 and NOx in the LCP sector, and incorporates a selection of case studies of market-based instruments (MBIs) that have been applied in practice to reducing SO2 and NOx emissions in the LCP sector, mainly in the USA, but with one example in the EU. By drawing on these case studies and other information, specific consideration is then given to the feasibility and desirability of market based instruments for reducing emissions of SO2 and NOx in the EU’s LCP sector. Within the scope of this project, this is a screening level analysis, and hence the discussions deal in outline terms only. Key summary points include:

Final Report xv

h:\projects\em-260\10000 projects\10819 ec lcpd\final report\final report 05225.doc

July 2005

10819

• While there are numerous options for the introduction of MBIs to control SO2 and NOx emissions in the EU, the most likely options are (a) a tax, (b) an emissions permit trading scheme and (c) some hybrid permit trading scheme with upper, or upper and lower, limits to permit prices set by a tax and subsidy.

• Relative to command and control (CAC) measures, MBIs offer the potential for compliance cost savings, both in a static (current) sense and dynamically through time due to the stimulus to technological innovation. Auctioned permits and taxes also generate government revenues which can be hypothecated to various uses, but notably to reducing other distortionary taxes and to encouraging further environmental improvement. The scale of the ‘double dividend’ associated with the former option is currently debated. Overall, while MBIs will not always secure cost efficiency gains over CAC, the general rule is that they will.

• While, in principle, optimally designed taxes and tradable permit schemes secure the same cost-efficient outcomes, various practical issues affect the choice between them: (a) where tradable permits are given freely, there is no government revenue effect; and (b) in the context of uncertainty about abatement costs, the choice between them depends on the relative steepness of the damage and abatement cost curves.

• As far as tradable permit schemes are concerned, it will be essential to ensure that:

• variations in abatement costs by emitters are sufficient to secure the cost reductions from trading;

• there are sufficient participants in the market to signal the right information about cost savings. On the broader scale, ensuring that there is adequate liquidity in the market;

• an emissions trading scheme does not generate ‘hot spots’ of unacceptable environmental quality. In practice, the potential for such ‘hot spots’ should be minimised by the effect of the Air Quality Daughter Directives, as well as the requirement to comply with BAT under the IPPCD. However, it may be necessary for any scheme to operate with side constraints on deposition effects or ‘exchange rates’;

• permits do not become concentrated in the hands of a few polluters;

• there is a provision for banking permits (reserving them for future use) in order to reduce risks associated with over-compliance;

• the schemes are not ‘over-designed’ by central authorities, leaving industry to promote trading rules within the overall environmental constraint;

• new entrants are not seriously disadvantaged, either by allocating free permits or enabling part of the cap to be auctioned;

• an effective monitoring and compliance system is in place—especially an effective penalty system for non-compliance or misreporting.

• As far as a tax solution is concerned, the following issues also need to be addressed: devising an effective system for the use of revenues, including analysis of the

Final Report xvi

h:\projects\em-260\10000 projects\10819 ec lcpd\final report\final report 05225.doc

July 2005

10819

relative merits of reducing other taxes and recycling of revenues to industry in proportion to environmental achievement; and, as with a trading scheme, ensuring that sectoral competitiveness is preserved.

• A hybrid trading/tax scheme can be more efficient than a tax or tradable permit scheme alone if it is carefully designed to have a tax rate setting an upper limit to the permit price and a subsidy setting a lower limit.

• Additional comments in the LCPD context include:

• while an emissions cap is consistent with the LCPD, as illustrated by the national emission reduction plan option for existing plants, the LCPD caps under these plans are annual and hence would not permit banking. This suggests setting a cap for any trading scheme lower than the total emissions cap - a ‘cap within a cap’;

• while it is well known that pure emissions trading secures potentially significant cost reductions, they have the potential to give rise to unacceptable locational pollution. In the context of LCPs, however, the likelihood for this should be minimised by the requirement to comply with pre-existing policies including the Air Quality Daughter Directives; BAT under the IPPC Directive; and the requirements of the current LCPD. Additional options to address this potential issue, however, appear limited. For example movement towards a theoretically desirable ambient-based trading scheme is limited because of high transaction costs; and one option is to adopt an ‘exchange rate’ approach, although some of the evidence suggests that this will severely limit cost savings;

• at the practical level, setting common tax rates may be more politically difficult than devising a trading scheme.

Final Report xvii

h:\projects\em-260\10000 projects\10819 ec lcpd\final report\final report 05225.doc

July 2005

10819

Contents

1. Introduction 1

1.1 This report 1 1.2 Background 1 1.3 Project Scope and Objectives 1 1.4 Structure of the report 3

2. Key Policies Affecting Air Pollutant Emissions from Large Combustion Plants 5

2.1 Introduction 5 2.2 Large Combustion Plant Directive 5 2.2.1 Introduction 5 2.2.2 Information on national emission reduction plans under the

LCPD 6 2.2.3 Information on implementation of the LCPD in New Member

States 7 2.3 National large combustion plant emission limit values 14 2.4 Best Available Techniques for large combustion plants 18 2.4.1 Introduction 18 2.4.2 Background to Best Available Techniques 18 2.4.3 Reference Documents on Best Available Techniques 19 2.5 Ambient air quality limit values 20 2.6 Summary 21

3. Large Combustion Plant Emissions Data 23

3.1 Introduction 23 3.2 Fuel types 24 3.2.1 Introduction 24 3.2.2 Current fuel mix 24 3.2.3 Future trends in fuel mix 27 3.2.4 Sulphur contents of fuels 28 3.2.5 Heavy metals content of fuels 32 3.3 LCPD emission inventory data 35 3.4 RAINS model data 38

Final Report xviii

h:\projects\em-260\10000 projects\10819 ec lcpd\final report\final report 05225.doc

July 2005

10819

3.4.1 RAINS scenarios 38 3.4.2 Applicability to LCP sector 39 3.4.3 Assumptions of uptake of abatement measures 40 3.4.4 Emissions data in CP_CLE_Aug04 scenario 48 3.4.5 Emissions data in NAT_Aug04 scenario 55 3.5 EPER data 55 3.6 NECD and UNECE/EMEP data 60 3.7 Plant level data 61 3.7.1 Survey of emissions and abatement data for selected plants in

the ESI 61 3.7.2 Survey of gas turbine manufacturers 68 3.7.3 Work by the Swedish NGO Secretariat on Acid Rain on the

performance range of existing power plants 69 3.8 Other data 70 3.8.1 Particle size distribution 70 3.8.2 Projections of heavy metal emissions 73 3.9 Summary of emissions data 76 3.9.1 Fuel types and trends 76 3.9.2 Emissions data sources 77 3.9.3 SO2 emissions 78 3.9.4 NOx emissions 79 3.9.5 Dust and PM emissions 80 3.9.6 Heavy metal emissions 80 3.10 References 81

4. Additional Measures to Reduce Large Combustion Plant Emissions 85

4.1 Introduction 85 4.2 Additional measures for SO2 86 4.2.1 Existing coal / lignite boilers 86 4.2.2 Existing oil fired boilers and process heaters in the petroleum

refining sector 89 4.3 Additional measures for NOx 91 4.3.1 Existing coal boilers 91 4.3.2 New gas fired gas turbines 93 4.4 Additional measures for dust, PM10, PM2.5 and particulate

bound heavy metals 94 4.4.1 Existing coal / lignite boilers 94 4.5 Additional measures for mercury 95 4.5.1 Existing coal and lignite boilers 95 4.6 Costs of additional measures 99

Final Report xix

h:\projects\em-260\10000 projects\10819 ec lcpd\final report\final report 05225.doc

July 2005

10819

4.6.1 Cost effectiveness of additional measures 99 4.6.2 Comparison of costs of additional measures for LCP sector with

RAINS model costs for all other sectors 101 4.7 Summary 109 4.8 References 110

5. Analysis of Other Specific Provisions of the LCPD 113

5.1 Assistance on possible end dates or of lower limit values for the NOx ELV derogation 113

5.1.1 Introduction 113 5.1.2 Potential significance of NOx emissions from plants covered by

this derogation 113 5.1.3 Cost-effectiveness of various NOx abatement measures 114 5.1.4 Summary 115 5.2 Potential inclusion of offshore gas turbines in the LCPD 115 5.2.1 Introduction 115 5.2.2 Relative significance of NOx emissions from offshore gas

turbines 115 5.2.3 Additional abatement measures for offshore gas turbines 117 5.2.4 Summary 121 5.2.5 References 122 5.3 Monitoring aspects 122 5.3.1 Comments on measurement requirements 122 5.3.2 Comparison of reporting requirements under the EPER and

LCPD 124 5.3.3 References 125

6. Effects of Differences between Community Environmental Standards for the LCP Sector 127

6.1 Introduction 127 6.2 Effects on competition in the energy market 127 6.2.1 Introduction 127 6.2.2 Interconnection 130 6.2.3 Administrative network developments 133 6.2.4 Internal market conditions 134 6.2.5 EU generation mix 136 6.2.6 Potential for electricity trade between countries with different

environmental standards 136 6.2.7 Power generation costs 138 6.2.8 Impact of differences in electricity generation costs on

competition in the energy market 141

Final Report xx

h:\projects\em-260\10000 projects\10819 ec lcpd\final report\final report 05225.doc

July 2005

10819

6.2.9 Summary 145 6.3 Effects on the environment 145 6.4 References 146

7. Screening Level Analysis of the Feasibility and Desirability of Market Based Instruments for SO2 and NOx in the EU LCP Sector 149

7.1 Introduction 149 7.2 EU and US approaches to reducing emissions of SO2 and

NOx in the LCP sector 150 7.2.1 Introduction 150 7.3 EU approaches for reducing emissions of SO2 and NOx in

the LCP sector 151 7.3.1 Overview of EU approaches 151 7.3.2 Market-based instrument case study 1: Swedish NOx charge 153 7.4 US approaches for reducing emissions of SO2 and NOx in

the LCP sector 157 7.4.1 Overview of US approaches 157 7.4.2 Market-based instrument case study 2: US Acid Rain

Programme 160 7.4.3 Market-based instrument case study 2: Ozone Transport

Commission (OTC) NOx Budget Program and NOx SIP Call Trading Program 166

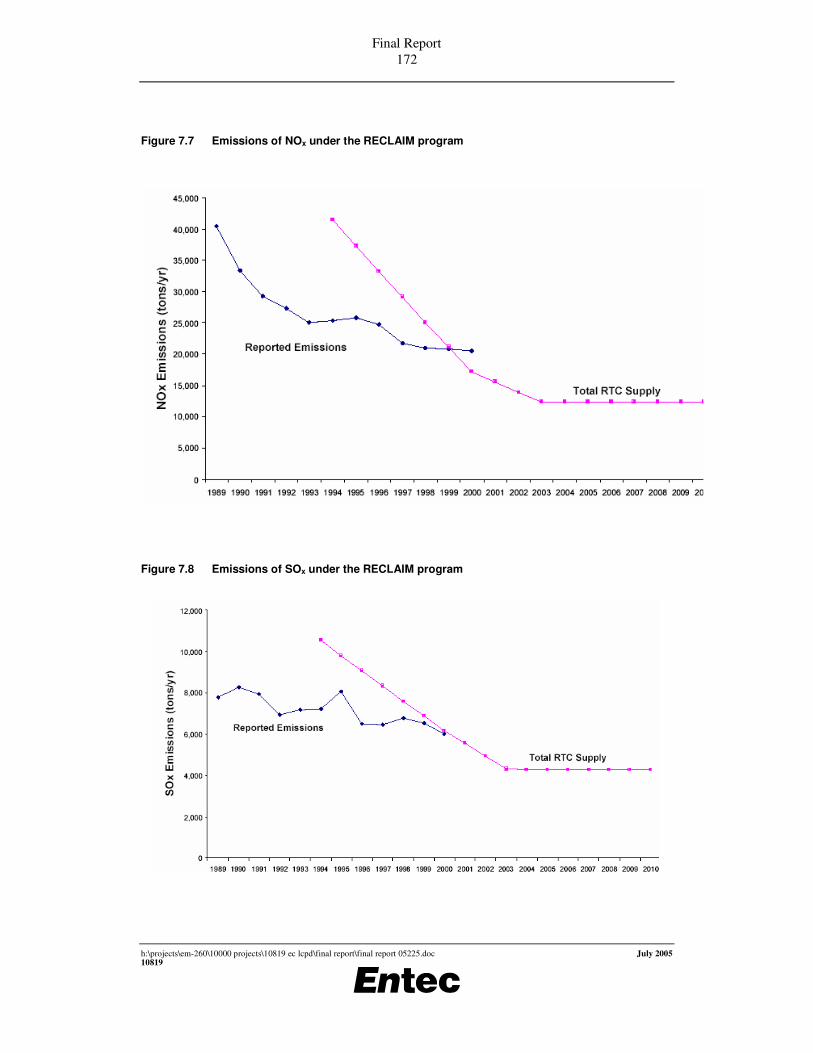

7.4.4 Market-based instrument case study 3: Regional Clean Air Markets Initiative (RECLAIM) 169

7.4.5 Assessment of the relative stringency of the US emission trading schemes compared to the LCPD 173

7.5 Screening level analysis of feasibility and desirability of market based instruments for SO2 and NOx in the EU LCP sector 174

7.5.1 Rationale for introducing trading or taxation 174 7.5.2 Introducing trading or taxation in addition to existing CAC

regulation 178 7.5.3 Hybrid tax and permit trading schemes 180 7.5.4 The potential need for further reductions in EU SO2 and NOx

emissions beyond business as usual reductions 181 7.5.5 The technical feasibility of achieving further SO2 and NOx

emissions reductions in the EU LCP sector beyond business as usual reductions 181

7.5.6 Preliminary considerations of key design issues for trading schemes 182

7.5.7 Preliminary considerations of key design issues for tax schemes 187

Final Report xxi

h:\projects\em-260\10000 projects\10819 ec lcpd\final report\final report 05225.doc

July 2005

10819

7.5.8 Cost-effectiveness of MBIs for the EU LCP sector compared with tightening CAC legislation 188

7.5.9 Summary 189 7.6 References 191

Table 1.1 Project tasks 2 Table 2.1 Implementation of the LCPD in New Member States (EC, 2004) 8 Table 2.2 Comparison of national ELVs with those in the LCPD (existing plants) 14 Table 2.3 Comparison of national ELVs with those in the LCPD (new plants) 16 Table 2.4 EU ambient air quality limit values in First Daughter Directive (1999/30/EC) 20 Table 3.1 Sulphur content of fuels (%) burnt in existing and new power plants in EU25 29 Table 3.2 Sulphur content of fuels (%) per unit energy (GJ/tonne) burnt in new (PP_NEW) and

existing (PP_EX) power plants in Europe (EU-15, New Member States and EU-25) 30 Table 3.3 Sulphur content of coal used in Europe 31 Table 3.4 Sulphur content of coal used by two companies for power production 32 Table 3.5 Mercury content of coal and lignite 33 Table 3.6 Arsenic, cadmium, nickel and vanadium content of coal and lignite 34 Table 3.7 Information on Crude Oils 35 Table 3.8 Range of Ni Content in Heavy Fuel Oils 35 Table 3.9 SO2 emissions from all LCPs taken from Member States’ emissions inventories submitted

under the LCPD broken down by size band 36 Table 3.10 NOx emissions from all LCPs taken from Member States’ emissions inventories

submitted under the LCPD broken down by size band 36 Table 3.11 SO2 emissions from LCPs at petroleum refineries taken from Member States’ emissions

inventories expressed per unit of crude capacity 37 Table 3.12 Hard coal, existing plants, grade 1, all boiler types except wet bottom (figures are

percentages of capacity controlled by FGD) 42 Table 3.13 Hard coal, existing plants, grade 1, wet bottom boilers (figures are percentages of

capacity controlled by FGD) 43 Table 3.14 Brown coal/lignite, existing plants, grade 1, all boiler types except wet bottom (figures are

percentages of capacity controlled by FGD) 43 Table 3.15 Heavy fuel oil, existing plants, all boiler types except wet bottom (figures are percentages

of capacity controlled by FGD) 44 Table 3.16 Hard Coal, existing plants, grade 1, all boiler types except wet bottom (figures are

percentages of capacity controlled by SCR) 44 Table 3.17 Hard coal, existing plants, grade 1, wet bottom (figures are percentages of capacity

controlled by SCR) 45 Table 3.18 Brown coal/lignite, existing plants, grade 1, all boiler types except wet bottom (figures are

percentages of capacity controlled by SCR) (Note 1) 45 Table 3.19 Heavy fuel oil, existing plants, all boiler types except wet bottom (figures are percentages

of capacity controlled by SCR) 46 Table 3.20 Natural gas (incl. other gases), new plants (figures are percentages of capacity controlled

by SCR) 46 Table 3.21 Hard coal, existing plants, grade 1, pulverized fuel (figures are percentages of capacity

controlled by ESPs with more than 2 fields) 46 Table 3.22 Brown coal/lignite, existing plants, grade 1, pulverised fuel (figures are percentages of

capacity controlled by ESPs with more than 2 fields) 47 Table 3.23 SO2 emissions from existing and new power and district heat plants and all other RAINS

sources in EU25 broken down by fuel type (CP_CLE_Aug04) 51 Table 3.24 NOx emissions from existing and new power and district heat plants and all other RAINS

sources in EU25 broken down by fuel type (CP_CLE_Aug04) 52 Table 3.25 PM10 emissions from existing and new power and district heat plants and all other RAINS

sources in EU25 broken down by fuel type (CP_CLE_Aug04) 53 Table 3.26 PM2.5 emissions from existing and new power and district heat plants and all other RAINS

sources in EU25 broken down by fuel type (CP_CLE_Aug04) 54 Table 3.27 Emissions from power and district heat plants in ‘NAT’ scenario expressed as a

proportion of emissions in ‘CP_CLE’ scenario 55 Table 3.28 SO2, NOx and PM10 emissions from combustion installations (>50MWth) and all sources

as reported to the EPER for 2001 56 Table 3.29 Heavy metal emissions from combustion installations (>50MWth) and all sources as

reported to the EPER for 2001 and emissions data for mercury for 2000 presented in the EC Consultation Document - Development of an EU Mercury Strategy, (2004b) 58

Table 3.30 Emissions of mercury in Poland in 2001 (from national submission to UNECE) 60 Table 3.31 Summary of data sources for emissions and abatement data for selected plants in the

ESI 62

Final Report xxii

h:\projects\em-260\10000 projects\10819 ec lcpd\final report\final report 05225.doc

July 2005

10819

Table 3.32 Information for land based gas turbines >50MWth licensed before 27 November 2002 68 Table 3.33 Information for land based gas turbines >50MWth licensed after 27 November 2002 69 Table 3.34 Particulate abatement efficiency for existing hard coal and lignite power stations 71 Table 3.35 Impact of different levels of particulate abatement on residual concentrations and size

fractions 71 Table 3.36 Proportion (%) of PM2.5 and PM10 in emissions from LCPs with or without abatement

technology (members of EURELECTRIC and VGB) 72 Table 3.37 Abatement efficiency of metals by traditional abatement techniques for LCPs 74 Table 3.38 Mercury emission projections from combustion installations (>50MWth) (tonnes) 75 Table 4.1 Examples of pollutants, fuel types, and process types for potential consideration for

achievement of further emissions reductions within the LCP sector 85 Table 4.2 Weighted average combustion related emissions (mg/Nm3) of SO2 for different European

areas 89 Table 4.3 Costs of additional measures for LCP sector 100 Table 4.4 Comparison of cost-effectiveness of additional measures in the LCP sector with average

cost effectiveness of beyond BAU measures in the RAINS Web cost curves 108 Table 5.1 Differences in marginal abatement costs for NOx control for plants at different load factors

(Note 1) 114 Table 5.2 Estimated number of existing UK offshore gas turbines (of at least 50MWth) and their

corresponding NOx emissions according to UKOOA 117 Table 5.3 Indicative capital costs of DLN technology for offshore gas turbines 120 Table 5.4 Marginal abatement costs of DLN for the offshore gas turbine sector 121 Table 5.5 Comments on measurement requirements 123 Table 5.6 EPER source categories relevant to LCPs 124 Table 6.1 Market liberalisation, EU and neighbouring countries 135 Table 6.2 Import-export trade balances for electricity* (TWh) 137 Table 6.3 Summary of costs of generating electricity (� per MWh) (Note 1) 138 Table 6.4 Costs of additional measures for LCP sector 140 Table 6.5 The Accession Treaty emission ceilings for Polish LCP sector 142 Table 6.6 Privatisation in Polish public power sector 1997-2004, main ownership 143 Table 6.7 Privatisation in Polish public power sector 1997-2004, percentage share 144 Table 7.1 Selection of some policies in the European Union and United States addressing

emissions of SO2 and NOx from LCPs 150 Table 7.2 SO2 and NOx emission limits under Standards of Performance for New Stationary Source

(Note 1) 158 Table 7.3 NOx emission limit values under Phase II of the Acid Rain Program 162 Table 7.4 Emission reduction requirements for OTC NOx Budget Program 167 Table 7.5 OTC NOx Budget Program state allocations and emissions (tons) 168 Table 7.6 Comparison between stringency of US emission trading schemes and the LCPD, based

on existing coal fired power station >500MWth 173 Table 7.7 Examples of additional measures to achieve further reductions in SO2 and NOx emissions

from the LCP sector 182 Figure 3.1 Generation mix in EU25 in 2001 (also covers Bulgaria and Romania) 25 Figure 3.2 Oil and coal fired electricity generation in EU25 in 2001 (Also covers Bulgaria and

Romania) 26 Figure 3.3 SO2 emissions from existing and new power and district heat plants and all other RAINS

sources in EU25 broken down by fuel type (CP_CLE_Aug04) 49 Figure 3.4 NOx emissions from existing and new power and district heat plants and all other RAINS

sources in EU25 broken down by fuel type (CP_CLE_Aug04) 49 Figure 3.5 PM10 emissions from existing and new power and district heat plants and all other RAINS

sources in EU25 broken down by fuel type (CP_CLE_Aug04) 50 Figure 3.6 PM2.5 emissions from existing and new power and district heat plants and all other RAINS

sources in EU25 broken down by fuel type (CP_CLE_Aug04) 50 Figure 3.7 Current SO2 emissions per MWh for selected coal power stations in EU25 64 Figure 3.8 Current SO2 emissions per MWh for selected lignite power stations in EU25 64 Figure 3.9 Current SO2 emissions per MWh for selected oil power stations in EU25 65 Figure 3.10 Current NOx emissions per MWh for selected coal power stations in EU25 65 Figure 3.11 Current NOx emissions per MWh for selected lignite power stations in EU25 66 Figure 3.12 Current NOx emissions per MWh for selected oil power stations in EU25 66 Figure 3.13 Current dust emissions per MWh for selected coal power stations in EU25 67 Figure 3.14 Current dust emissions per MWh for selected lignite power stations in EU25 67 Figure 3.15 Current dust emissions per MWh for selected oil power stations in EU25 68 Figure 4.1 RAINS Web cost curve for SO2 for 2010 showing position in cost curve where additional

measures for the LCP sector would fit 102 Figure 4.2 RAINS Web cost curve for SO2 for 2020 showing position in cost curve where additional

measures for the LCP sector would fit 103

Final Report xxiii

h:\projects\em-260\10000 projects\10819 ec lcpd\final report\final report 05225.doc

July 2005

10819

Figure 4.3 RAINS Web cost curve for NOx for 2010 showing position in cost curve where additional measures for the LCP sector would fit 104

Figure 4.4 RAINS Web cost curve for NOx for 2020 showing position in cost curve where additional measures for the LCP sector would fit 105

Figure 4.5 RAINS Web cost curve for PM2.5 for 2010 showing position in cost curve where additional measures for the LCP sector would fit 106

Figure 4.6 RAINS Web cost curve for PM2.5 for 2020 showing position in cost curve where additional measures for the LCP sector would fit 107

Figure 5.1 Application of various parts of the directive 122 Figure 6.1 Differences in environmental standards - a context for assessing effects on competition 129 Figure 6.2 Current trading Partnerships - physical energy flows (GWh), April - September 2003 131 Figure 6.3 Production of coal and lignite (2001) 139 Figure 7.1 Total and specific NOx emissions from boilers subject to the NOx charge (estimated for

1990) 155 Figure 7.2 Emissions of nitrogen oxides, 1980-2002 156 Figure 7.3 SO2 allowances traded, 1994-2002 161 Figure 7.4 Cumulative SO2 allowances transferred to the end of 2002 162 Figure 7.5 Price of SO2 allowances ($/ton) 163 Figure 7.6 SO2 emissions from acid rain sources, 1980 to 2002 165 Figure 7.7 Emissions of NOx under the RECLAIM program 172 Figure 7.8 Emissions of SOx under the RECLAIM program 172

Appendix 1 LCPD Emission Limit Values

Appendix 2 Details of Best Available Techniques from BAT Reference Documents Appendix 3 Mercury Contents of Coals Appendix 4 Emissions Data from RAINS Model Appendix 5 Emissions Data from Selected Plants

Final Report xxiv

h:\projects\em-260\10000 projects\10819 ec lcpd\final report\final report 05225.doc

July 2005

10819

Final Report 1

h:\projects\em-260\10000 projects\10819 ec lcpd\final report\final report 05225.doc

July 2005

10819

1. Introduction

1.1 This report Entec UK has undertaken a project for the European Commission (Contract No B4-3040/2003/360121/MAR/C1) to support the review of Directive 2001/80/EC, referred to as the Large Combustion Plant Directive (LCPD). This is the final report of the project, which presents the findings of the information collection and analysis that has been undertaken in relation to the overall project objectives.

1.2 Background Adopted in October 2001, the LCPD requires Member States to reduce emissions of sulphur dioxide (SO2), nitrogen oxides (NOX) and dust from power plants and other industrial facilities containing large combustion plants (LCPs). Reductions in emissions of the three pollutants of concern will yield reductions in acidification, ground level ozone and particulate matter, with subsequent improvements to human health and the environment.

The Directive also places a requirement for a review of its implementation and the potential for extension of the Directive’s requirements. In particular, Article 4(7) of the Directive specifies that “the Commission shall submit a report to the European Parliament and the Council in which it shall assess:

(a) the need for further measures;

(b) the amounts of heavy metals emitted by large combustion plants;

(c) the cost-effectiveness and costs and advantages of further emission reductions in the combustion plants sector in Member States compared to other sectors;

(d) the technical and economic feasibility of such emission reductions;

(e) the effects of both the standards set for the large combustion plants sector including the provisions for indigenous solid fuels, and the competition situation in the energy market, on the environment and the internal market;

(f) any national emission reduction plans provided by Member States in accordance with paragraph 6.

The Commission shall include in its report an appropriate proposal of possible end dates or of lower limit values for the derogation contained in footnote 2 to Annex VI A.”

1.3 Project Scope and Objectives The overall objective of the study is to contribute to the preparation of the review of the LCPD. The tasks undertaken have required the collection and analysis of information on a range of

Final Report 2

h:\projects\em-260\10000 projects\10819 ec lcpd\final report\final report 05225.doc

July 2005

10819

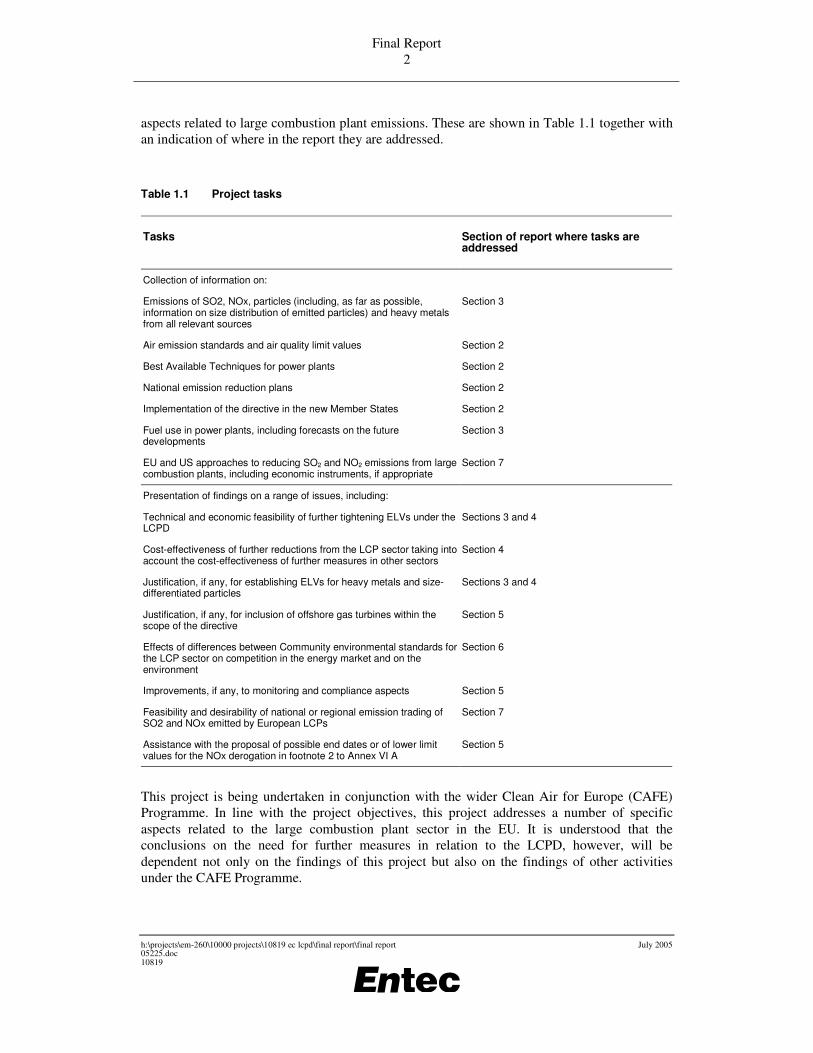

aspects related to large combustion plant emissions. These are shown in Table 1.1 together with an indication of where in the report they are addressed.

Table 1.1 Project tasks

Tasks Section of report where tasks are addressed

Collection of information on:

Emissions of SO2, NOx, particles (including, as far as possible, information on size distribution of emitted particles) and heavy metals from all relevant sources

Section 3

Air emission standards and air quality limit values Section 2

Best Available Techniques for power plants Section 2

National emission reduction plans Section 2

Implementation of the directive in the new Member States Section 2

Fuel use in power plants, including forecasts on the future developments

Section 3

EU and US approaches to reducing SO2 and NO2 emissions from large combustion plants, including economic instruments, if appropriate

Section 7

Presentation of findings on a range of issues, including:

Technical and economic feasibility of further tightening ELVs under the LCPD

Sections 3 and 4

Cost-effectiveness of further reductions from the LCP sector taking into account the cost-effectiveness of further measures in other sectors

Section 4

Justification, if any, for establishing ELVs for heavy metals and size-differentiated particles

Sections 3 and 4

Justification, if any, for inclusion of offshore gas turbines within the scope of the directive

Section 5

Effects of differences between Community environmental standards for the LCP sector on competition in the energy market and on the environment

Section 6

Improvements, if any, to monitoring and compliance aspects Section 5

Feasibility and desirability of national or regional emission trading of SO2 and NOx emitted by European LCPs

Section 7

Assistance with the proposal of possible end dates or of lower limit values for the NOx derogation in footnote 2 to Annex VI A

Section 5

This project is being undertaken in conjunction with the wider Clean Air for Europe (CAFE) Programme. In line with the project objectives, this project addresses a number of specific aspects related to the large combustion plant sector in the EU. It is understood that the conclusions on the need for further measures in relation to the LCPD, however, will be dependent not only on the findings of this project but also on the findings of other activities under the CAFE Programme.

Final Report 3

h:\projects\em-260\10000 projects\10819 ec lcpd\final report\final report 05225.doc

July 2005

10819

1.4 Structure of the report The structure of this report is as follows:

Section 2 presents brief details of some of the key policies affecting emissions of air pollutants from large combustion plants in the EU. Clearly the Large Combustion Plant Directive (LCPD) itself is of most direct relevance, and this is discussed, including information on national emission reduction plans submitted so far under the LCPD and details of implementation of this directive in the new Member States. This is followed by sections that identify whether and to what extent some Member States go beyond the LCPD ELVs in their own national legislation; the requirements of ‘best available techniques’ (BAT) under the IPPCD and key air quality directives.

Section 3 presents data on current and future emissions from LCPs across the EU25. The purpose of this section is to support conclusions on the quantity and profile of current emissions of key pollutants from LCPs, as well as an indication of the quantity and profile of future emissions of key pollutants expected under a ‘business as usual’ (BAU) scenario, incorporating the expected impact of agreed policies, including the current LCPD and IPPCD, to the extent that they have been taken into account in currently available modelling work.

In the event that further reductions in emissions were required from the LCP sector, the priority pollutants and process types for achievement of potential further reductions are identified in Section 4. This section goes on to present brief details of technically feasible additional abatement measures that could reduce emissions further. The cost effectiveness of these abatement measures is then presented and compared to the cost effectiveness of additional measures in other sectors.

Section 5 provides supporting information related to possible end dates or lower limit values for the NOx derogation contained in footnote 2 to Annex VI A; supporting information related to the potential inclusion of offshore gas turbines (of at least 50MWth) within the scope of the directive; and details on measurement and reporting aspects.

Section 6 investigates the effects of differences between the Community environmental standards for the LCP sector on competition in the energy market, focussing particularly on where there is expected to be a delay in meeting the LCPD requirements due to derogation allowances for new Member States. In addition, this section gives brief consideration to the effects of differences in standards on the environment.

Section 7 briefly identifies key aspects of EU and US approaches to reducing emissions of SO2 and NOx in the LCP sector, and incorporates a selection of case studies of market-based instruments (MBIs) that have been applied in practice to reducing SO2 and NOx emissions in the LCP sector, mainly in the USA, but with one example in the EU. By drawing on these case studies and other information, specific consideration is then given to the feasibility and desirability of market based instruments for reducing emissions of SO2 and NOx in the EU’s LCP sector. Within the scope of this project, this is a screening level analysis, and hence the discussions deal in outline terms only.

Summaries of the findings in each section are given at the end of the appropriate section, with an overall summary of key findings presented in the Executive Summary.

Final Report 4

h:\projects\em-260\10000 projects\10819 ec lcpd\final report\final report 05225.doc

July 2005

10819

Final Report 5

h:\projects\em-260\10000 projects\10819 ec lcpd\final report\final report 05225.doc

July 2005

10819

2. Key Policies Affecting Air Pollutant Emissions from Large Combustion Plants

2.1 Introduction The purpose of this section is to present brief details of the key policies affecting emissions of air pollutants from large combustion plants in the EU. This is not intended to represent an exhaustive coverage of key policies, but simply those that are required to be considered within the scope of this study.

Clearly the Large Combustion Plant Directive (LCPD) is of most direct relevance, and this directive is discussed in Section 2.2, including information on national emission reduction plans submitted so far under the LCPD and details of implementation of this directive in the new Member States. This is followed by sections that identify whether and to what extent some Member States go beyond the LCPD ELVs in their own national legislation; the requirements of ‘best available techniques’ (BAT) under the IPPCD and key air quality directives.

2.2 Large Combustion Plant Directive

2.2.1 Introduction Directive 2001/80/EC, referred to as the Large Combustion Plant Directive (LCPD), applies to combustion plants with a rated thermal input of 50MW or more. The LCPD is a complex directive that places requirements upon Member States to reduce emissions of sulphur dioxide (SO2), nitrogen oxides (NOx) and particulate matter (PM) from combustion plants within power plants, petroleum refineries, iron and steelworks and other industrial processes.

For existing plants (licensed before 1 July 1987), each Member State is able to choose between complying with emission limit values (ELVs) as set out in part A of Annexes III to VII or implementing a national emission reduction plan as defined in Article 4(6). The compliance date for existing plants is 1 January 2008.

In comparison to the ELV approach, the targets of the national emission reduction plan are defined as follows: “The national emission reduction plan shall reduce the total annual emissions of nitrogen oxides (NOx), sulphur dioxide (SO2) and dust from existing plants to the levels that would have been achieved by applying the emission limit values [in part A of Annexes III to VII]…to the existing plants in operation in the year 2000,.… on the basis of each plant’s actual annual operating time, fuel used and thermal input, averaged over the last five years of operation up to and including 2000”.

An operator of an existing plant may be exempted from compliance with the ELVs and from inclusion in a national emission reduction plan if a written undertaken was submitted to the competent authority by 30 June 2004, not to operate the plant for more than 20,000 operational hours starting from 1 January 2008 and ending no later than 31 December 2015.

Final Report 6

h:\projects\em-260\10000 projects\10819 ec lcpd\final report\final report 05225.doc

July 2005

10819

All new plants (those licensed from 1 July 1987) are required to comply with ELVs at the present time. Those licensed before 27 November 2002 are required to comply with those set out in part A of Annexes III to VII, whilst those licensed from 27 November 2002 are required to comply with the more stringent ELVs set out in part B of Annexes III to VII.

The ELVs are presented in Appendix 1 of this report. For plants with multi-firing units, the specific ELVs are set as described in Article 8.

The obligations of the LCPD are without prejudice to Directive 96/61/EC concerning integrated pollution prevention and control (IPPC Directive) as discussed in Section 2.4 and Directive 96/62/EC on ambient air quality assessment and management (Air Quality Framework Directive) as discussed in Section 2.5.

2.2.2 Information on national emission reduction plans under the LCPD As outlined in the above section, Member States have the option for existing plants to implement a national emission reduction plan, instead of implementing ELVs.

The requirements of a national emission reduction plan are set out in Article 4(6) of the LCPD. In particular, plans should “comprise objectives and related targets, measures and timetables for reaching these objectives and targets, and a monitoring mechanism”.

The Commission published a recommendation4 on the guidelines to assist a Member State in the preparation of a plan, together with the publication of a guidance document and associated summary.

According to the LCPD, EU15 Member States were to communicate their national emission reduction plans to the Commission no later than 27 November 2003. Following receipt of the plans, the Commission is to undertake an evaluation of the plans against the requirements of the directive, and communicate with the Member State as appropriate.

At the time of writing, 8 Member States have so far submitted national emission reduction plans to the Commission. These include:

• Czech Republic;

• Finland;

• France;

• Greece;

• Ireland;

• Netherlands;

• Slovenia; and

• UK.

Slovenia subsequently withdrew its plan and opted for the ELV approach.

4 Commission Recommendation of 15/01/2003.

Final Report 7

h:\projects\em-260\10000 projects\10819 ec lcpd\final report\final report 05225.doc

July 2005

10819

In addition, Spain is also known to be submitting a plan and some additional Member States may also be submitting plans.

At this stage, it is not possible to fully determine exactly which types of measures will be fitted to which specific plants in these countries. In general these will comprise a mixture of abatement, fuel switching and reductions in load factors and will be decided by the operating companies themselves, closer to the compliance deadline.

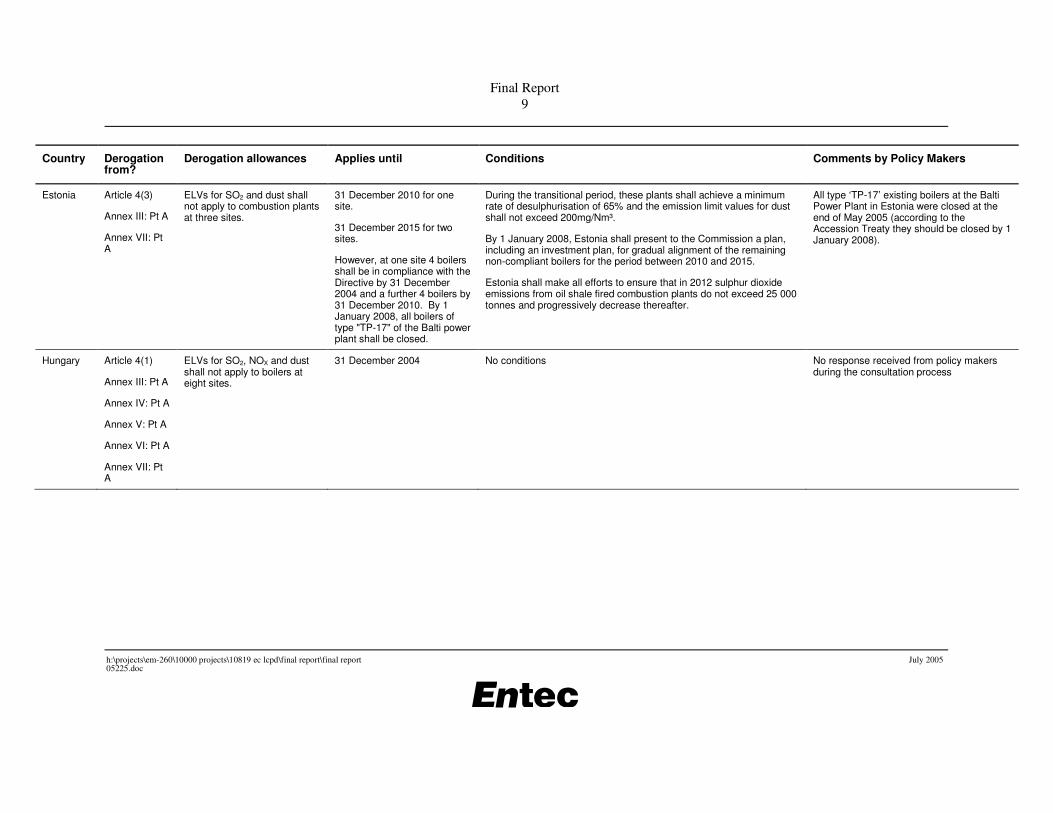

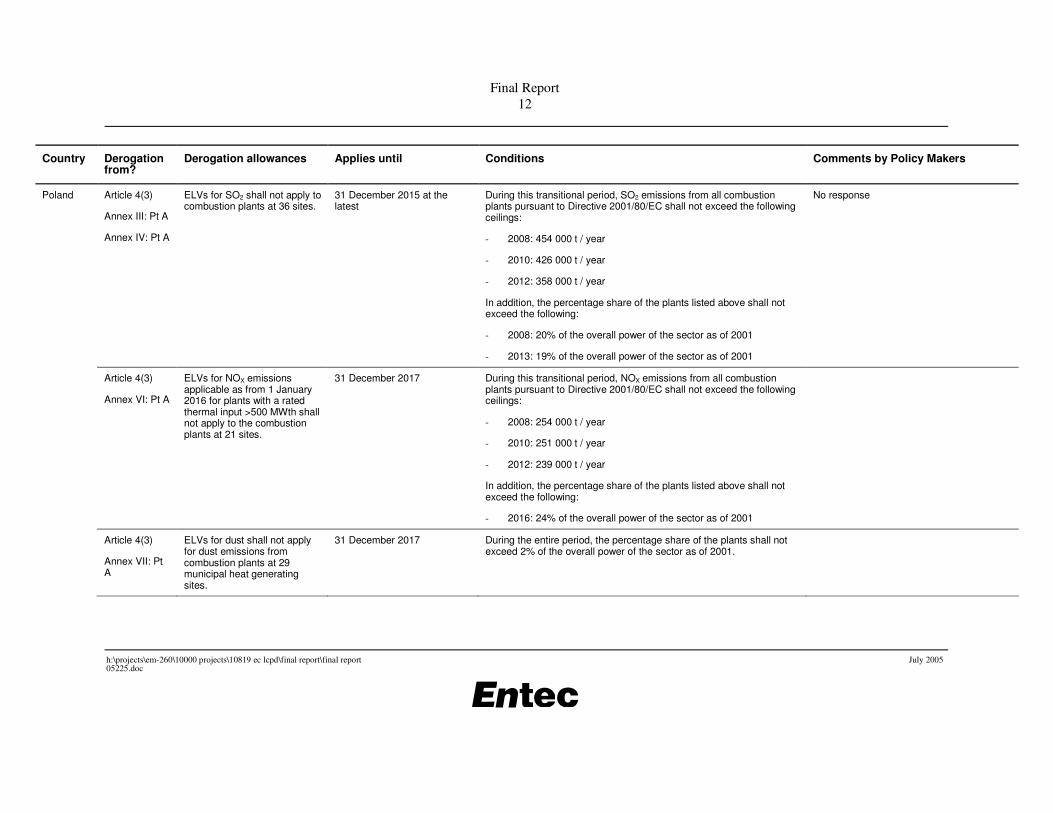

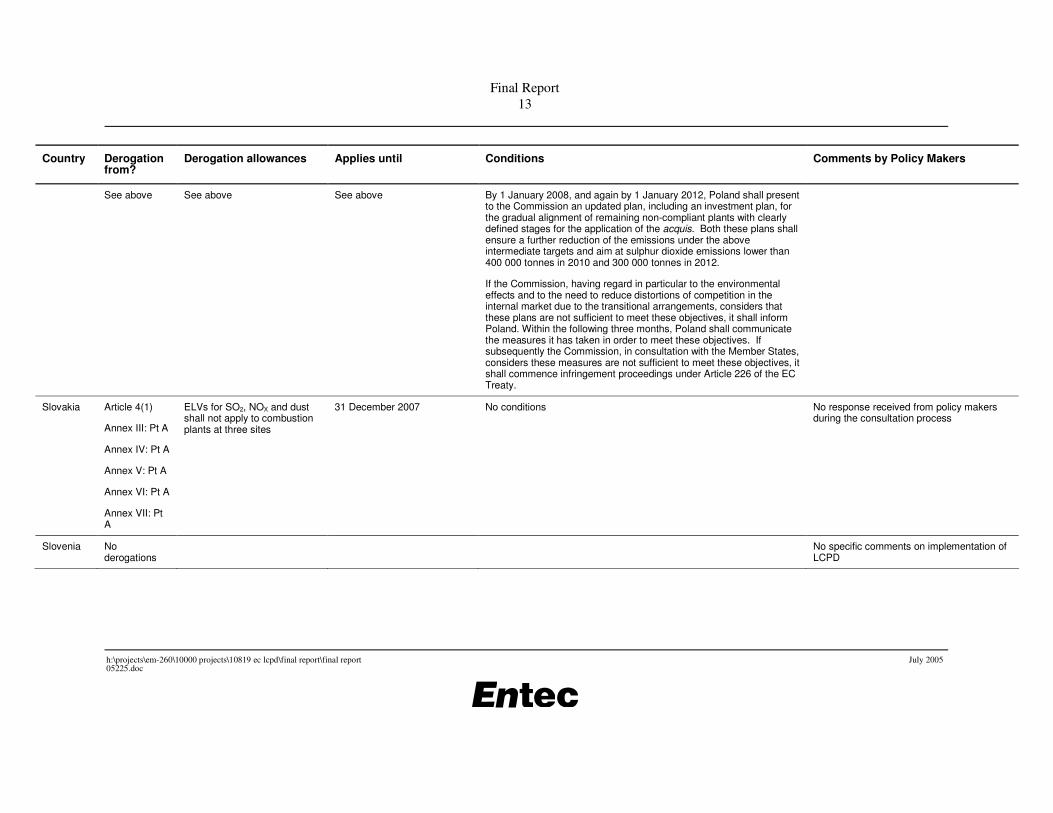

2.2.3 Information on implementation of the LCPD in New Member States The Commission has provided detailed information on the Transition Periods and Treaty Provisions (EC, 2004) associated with the implementation of the LCPD in New Member States. This information is summarised in Table 2.1 below, in addition to views and comments provided by the policy makers in these countries.

Final Report 8

h:\projects\em-260\10000 projects\10819 ec lcpd\final report\final report 05225.doc

July 2005

Table 2.1 Implementation of the LCPD in New Member States (EC, 2004)

Country Derogation from?

Derogation allowances Applies until Conditions Comments by Policy Makers

Cyprus Article 4(3)

Annex IV: Pt A

ELVs of 1 700 mg/Nm³ for SO2 shall apply to the boilers in operation in September 2002 at two combustion plants.

One of the following conditions materialises:

- there is an upgrade or a significant change to these boilers;

- natural gas becomes available on the island;

- Cyprus becomes an exporter of electricity; or

- the currently operating boilers are closed.

During the application of the ELVs, Cyprus shall report to the Commission, by 31 March each year after accession, on:

- the fuel quality used;

- annual total emissions of SO2 ; and

- the estimated contribution of these emissions to the emissions in neighbouring countries.

No comments to make on problems foreseen with LCPD implementation. They generally feel that Cyprus will be able to comply under the existing derogation conditions.

Czech Republic

Article 4(1)

Annex III: Pt A

ELVs for SO2 shall not apply to boilers at two sites

31 December 2007 No conditions As of yet the Czech Republic has not been expecting any trouble concerning the Directive implementation with the exemption of the two already negotiated and agreed transitional periods for two new sources.

Final Report 9

h:\projects\em-260\10000 projects\10819 ec lcpd\final report\final report 05225.doc

July 2005

Country Derogation from?

Derogation allowances Applies until Conditions Comments by Policy Makers

Estonia Article 4(3)

Annex III: Pt A

Annex VII: Pt A

ELVs for SO2 and dust shall not apply to combustion plants at three sites.

31 December 2010 for one site.

31 December 2015 for two sites.

However, at one site 4 boilers shall be in compliance with the Directive by 31 December 2004 and a further 4 boilers by 31 December 2010. By 1 January 2008, all boilers of type "TP-17" of the Balti power plant shall be closed.

During the transitional period, these plants shall achieve a minimum rate of desulphurisation of 65% and the emission limit values for dust shall not exceed 200mg/Nm³.

By 1 January 2008, Estonia shall present to the Commission a plan, including an investment plan, for gradual alignment of the remaining non-compliant boilers for the period between 2010 and 2015.

Estonia shall make all efforts to ensure that in 2012 sulphur dioxide emissions from oil shale fired combustion plants do not exceed 25 000 tonnes and progressively decrease thereafter.

All type ‘TP-17’ existing boilers at the Balti Power Plant in Estonia were closed at the end of May 2005 (according to the Accession Treaty they should be closed by 1 January 2008).

Hungary Article 4(1)

Annex III: Pt A

Annex IV: Pt A

Annex V: Pt A

Annex VI: Pt A

Annex VII: Pt A

ELVs for SO2, NOX and dust shall not apply to boilers at eight sites.

31 December 2004 No conditions No response received from policy makers during the consultation process

Final Report 10

h:\projects\em-260\10000 projects\10819 ec lcpd\final report\final report 05225.doc

July 2005

Country Derogation from?

Derogation allowances Applies until Conditions Comments by Policy Makers

Latvia No derogations

Difficulties highlighted include:

• the lack of BAT Reference documents and BAT documents about energy efficiency, as well it is not defined which measures are considered as BAT.

• how to identify and assess energy efficiency measures – indicators, benchmarks, methods for energy efficiency assessments, tools to measure, monitoring.

• economic reasons of the BAT implementation for existing plants.

• technical problems related to installation of monitoring equipment on the stacks of the existing plants, where several boilers are connected to one stack

Lithuania Article 4(3)

Annex IV: Pt A

Annex VI: Pt A

ELVs for SO2 and NOX shall not apply for the combustion plants at four sites

31 December 2015 During this transitional period, total SO2 and NOX emissions relating to electricity generation at these plants as well as the Lithuanian Thermal Power Plant, shall not exceed the following ceilings:

- 2005: 28 300 t SO2 / year; 4 600 t NOx / year

- 2008: 21 500 t SO2 / year; 5 000 t NOx / year

- 2010: 30 500 t SO2 / year; 10 500 t NOx / year

- 2012: 29 000 t SO2 / year; 10 800 t NOx / year