premier oil plc · premier oil plc (incorporated in scotland with registered number sc234781) 4 for...

TRANSCRIPT

Proof10:3.4.09

THIS DOCUMENT AND ANY ENCLOSURES WITH IT ARE IMPORTANT AND REQUIRE YOUR IMMEDIATE

ATTENTION. If you are in any doubt as to the action you should take, you are recommended to seek your own personal financial

advice immediately from your stockbroker, bank manager, solicitor, accountant, fund manager or other appropriate financial adviser

authorised pursuant to FSMA if you are in the United Kingdom or from another appropriately authorised independent financial

adviser if you are in a territory outside the United Kingdom.

Subject to the restrictions set out below, if you sell or transfer or have sold or transferred all of your Existing Ordinary Shares

(other than ex-rights) before 21 April 2009 (the ‘‘ex-rights date’’), please send this document and any Provisional Allotment

Letter, duly renounced, if and when received, as soon as possible to the purchaser or transferee, or to the stockbroker, bank or

other agent through whom the sale or transfer was effected, for onward delivery to the purchaser or transferee. This document

and/or the Provisional Allotment Letter should not, however, be distributed, forwarded to or transmitted in or into any

jurisdiction where to do so might constitute a violation of local securities law or regulations, including, but not limited to

(subject to certain exceptions), the Excluded Territories. Please refer to paragraphs 7 and 8 of Part VIII of this document if you

propose to send this document and/or the Provisional Allotment Letter outside the United Kingdom. If you sell or transfer part

only of your Existing Ordinary Shares, instructions regarding split applications will be set out in the Provisional Allotment

Letter. If you have sold or transferred Existing Ordinary Shares (other than ex-rights) held in uncertificated form, or have sold

or transferred American Depositary Shares (other than ex-rights), in each case before the ex-rights date, a claim transaction will

automatically be generated by Euroclear UK which, on settlement, will credit the appropriate number of Nil Paid Rights to the

purchaser or transferee.

This document, which comprises a prospectus relating to the Rights Issue and a circular relating to the Acquisition, has been

prepared in accordance with the Prospectus Rules made under section 73A of FSMA and has been approved as such by the

FSA in accordance with section 85 of FSMA. A copy of this document has been filed with the FSA in accordance with

paragraph 3.2.1 of the Prospectus Rules. This document has also been made available to the public in accordance with

paragraph 3.2.1 of the Prospectus Rules. This document can also be obtained on request from the Company’s Registrar, Capita

Registrars.

The Directors, whose names appear on page 19 of this document, the Proposed Director and Premier accept responsibility for

the information contained in this document. To the best of the knowledge of the Directors, the Proposed Director and Premier

(who have taken all reasonable care to ensure that such is the case), the information contained in this document is in

accordance with the facts and contains no omission likely to affect the import of such information.

Applications have been made to the UK Listing Authority and to the London Stock Exchange for the maximum number of

New Ordinary Shares that may be issued to be admitted to the Official List of the UK Listing Authority and to be admitted to

trading on the main market for listed securities of the London Stock Exchange. It is expected that, subject to the conditions to

the Rights Issue being satisfied or, where permitted, waived and subject also to the timing of the satisfaction or waiver of the

conditions, Admission will become effective and that dealings on the London Stock Exchange in the New Ordinary Shares (nil

paid) will commence at 8.00 a.m. (London time) on 21 April 2009.

The distribution of this document and/or the accompanying documents, and/or the transfer of Nil Paid Rights, Fully Paid

Rights and/or New Ordinary Shares, into jurisdictions other than the United Kingdom may be restricted by law and therefore

persons into whose possession this document and/or the accompanying documents come should inform themselves about and

observe any such restrictions. Any failure to comply with any such restrictions may constitute a violation of the securities laws

of such jurisdictions.

Premier Oil plc(Incorporated in Scotland with registered number SC234781)

4 for 9 Rights Issue at 485 pence per share to raise approximately £171 million,Acquisition of the entire issued share capital of ONSL (in administration) (or

of the ONSL Assets) and Notice of Extraordinary General Meeting

Deutsche BankFinancial Adviser, Global Co-ordinator, Joint Sponsor, Joint Bookrunner, Underwriter

and Joint Broker

Oriel Securities LimitedJoint Sponsor, Joint Broker, Co-Lead Manager and Underwriter

Barclays Capital, HSBC, RBC Capital MarketsJoint Bookrunners and Underwriters

For a discussion of certain risk factors which should be taken into account when considering whether to vote in favour of the

Resolutions please refer to the section entitled ‘‘Risk Factors’’ on pages 9 to 17 of this document. Your attention is drawn to the

letter from the chairman of Premier in Part I of this document, recommending you to vote in favour of the Resolutions to be

proposed at the Extraordinary General Meeting. You should read this document in its entirety and consider whether to vote in

favour of the Resolutions in light of the information contained in, or incorporated by reference into, this document.

Notice of an Extraordinary General Meeting, to be held at 10.00 a.m. on 20 April 2009 at the offices of Deutsche Bank,

Winchester House, 1 Great Winchester Street, London EC2N 2DB, is set out at the end of this document. Shareholders will find

enclosed a Form of Proxy for use at the Extraordinary General Meeting. Shareholders are requested to complete and return the

Form of Proxy whether or not they intend to be present at the meeting. To be valid, Forms of Proxy should be completed and

signed in accordance with the instructions printed thereon and returned by post or by hand so as to reach the Registrar as soon as

possible and, in any event, by no later than 10.00 a.m. on 18 April 2009. Return of a Form of Proxy will not preclude a

Shareholder from attending and voting at the Extraordinary General Meeting. All Shareholders on the register of members of

Premier at the close of business on 1 April 2009 have been sent this document.

Certain information in relation to Premier is incorporated by reference into this document. Capitalised terms have the meanings

ascribed to them in Part XVIII of this document. Certain abbreviated terms that are commonly used in the oil and gas industry

and which appear in this document are also defined in Part XVIII of this document.

No person has been authorised to give any information or make any representations other than those contained in this

document and, if given or made, such information or representations must not be relied on as having been so authorised. The

delivery of this document shall not, under any circumstances, create any implication that there has been no change in the

affairs of Premier since the date of this document or that the information in it is correct as of any subsequent time.

Deutsche Bank AG is authorised under German Banking Law (competent authority: BaFin - Federal Financial Supervisory

Authority) and authorised and subject to limited regulation by the FSA. Oriel, Barclays, HSBC and Royal Bank of Canada

Europe Limited (which trades as RBC Capital Markets) are authorised and regulated by the FSA. Each of Deutsche Bank and

Oriel is acting for Premier and no one else in connection with the Acquisition and the Rights Issue and will not regard any

other person (whether or not a recipient of this document) as a client in relation to the Acquisition or the Rights Issue, and

will not be responsible to anyone other than Premier for providing the protections afforded to its client or for providing advice

in relation to the Acquisition or the Rights Issue. Each of Barclays, HSBC and RBC Capital Markets are acting for Premier

and no one else in connection with the Rights Issue and will not regard any other person (whether or not a recipient of this

document) as a client in relation to the Rights Issue or the Acquisition and will not be responsible to anyone other than

Premier for providing the protections afforded to their respective clients or for providing advice in relation to the Acquisition

or the Rights Issue.

Apart from the responsibilities and liabilities, if any, which may be imposed on Deutsche Bank, Oriel, Barclays, HSBC and

RBC Capital Markets by FSMA or the regulatory regime established thereunder or under the regulatory regime of any other

jurisdiction where exclusion of liability under the relevant regulatory regime would be illegal, void or unenforceable, none of

Deutsche Bank, Oriel, Barclays, HSBC and RBC Capital Markets accept any responsibility whatsoever for the contents of this

document, including its accuracy, completeness or verification, or for any statement made or purported to be made by any of

them, or on behalf of them, in connection with the Company, the Nil Paid Rights, the Fully Paid Rights, the New Ordinary

Shares, the Rights Issue or the Acquisition. Each of Deutsche Bank, Oriel, Barclays, HSBC and RBC Capital Markets

accordingly disclaim all and any liability whether arising in tort, contract or otherwise (save as referred to above) which it

might otherwise have in respect of such document or any such statement.

Deutsche Bank, Oriel, Barclays, HSBC and RBC Capital Markets may, in accordance with applicable legal and regulatory

provisions and subject to the Underwriting Agreement, engage in transactions in relation to Nil Paid Rights, Fully Paid Rights,

the Ordinary Shares or related instruments for their own account for the purpose of hedging their underwriting exposure or

otherwise. Except as required by applicable law or regulation, Deutsche Bank, Oriel, Barclays, HSBC and RBC Capital Markets

do not propose to make any public disclosure in relation to such transactions.

Subject to the passing of the Resolutions, it is expected that Qualifying Non-CREST Shareholders (other than, subject to

certain exceptions, Shareholders in the United States and other Excluded Territories) will be sent a Provisional Allotment Letter

on 20 April 2009, and that Qualifying CREST Shareholders (other than, subject to certain exceptions, Shareholders in the

United States and other Excluded Territories) will receive a credit to their appropriate stock accounts in CREST in respect of

the Nil Paid Rights to which they are entitled on 20 April 2009. The Nil Paid Rights so credited are expected to be enabled for

settlement by Euroclear UK as soon as practicable after Admission. For further details, see Part VIII of this document.

This document does not constitute an offer to sell or the solicitation of an offer to acquire New Ordinary Shares or to take up

entitlements to Nil Paid Rights in any jurisdiction in which such an offer or solicitation is unlawful. None of the Nil Paid

Rights, the Fully Paid Rights, the New Ordinary Shares nor the Provisional Allotment Letters has been or will be registered

under the US Securities Act of 1933, as amended, or under the applicable securities laws of any state of the United States, any

province or territory of Canada, Australia, the State of Israel, New Zealand, Dubai International Finance Centre or the

Republic of South Africa. Accordingly, unless a relevant exemption from such requirements is available, neither the New

Ordinary Shares nor the Provisional Allotment Letters may, subject to certain exceptions, be offered, sold, taken up, renounced

or delivered, directly or indirectly, within the United States, Canada, Australia, the State of Israel, New Zealand, Dubai

International Finance Centre or the Republic of South Africa or in any country, territory or possession where to do so may

contravene local securities laws or regulations. Shareholders who believe that they, or persons on whose behalf they hold

Ordinary Shares, are eligible for an exemption from such requirements should refer to Part VIII of this document to determine

whether and how they may participate in the Rights Issue. Overseas Shareholders and any person who is resident in or a

citizen or national of any country outside the United Kingdom and any person (including, without limitation, nominees,

custodians and trustees) who has a contractual or other legal obligation to forward this document or a Provisional Allotment

Letter to a jurisdiction outside the United Kingdom should read paragraphs 7 and 8 of Part VIII of this document. Holdings

of Existing Ordinary Shares in certificated and uncertificated form will be treated as separate holdings for the purpose of

calculating entitlements under the Rights Issue.

The contents of this document are not to be construed as legal, business or tax advice. Each Shareholder should consult his,

her or its own legal adviser, financial adviser or tax adviser for legal, financial or tax advice.

Unless otherwise specified, this document contains certain translations of US Dollars into amounts in Pounds Sterling (and of

Pounds Sterling into amounts in US Dollars) for the convenience of the reader based on the exchange rate of US$1.00 =

£0.6787 or £1 = US$1.4734 (as applicable), being the relevant exchange rates on 24 March 2009 (the latest practicable date

prior to the date of the Announcement). These exchange rates were obtained from Bloomberg.

All information on reserves and production in this document is unaudited information and is sourced as set out in paragraph

17 of Part XVI of this document.

The contents of Premier’s website do not form part of this document.

2

c100191pu010Proof10:3.4.09B/LRevision:0OperatorPutA

TABLE OF CONTENTS

Page

SUMMARY 4

RISK FACTORS 9

EXPECTED TIMETABLE OF PRINCIPAL EVENTS 18

DIRECTORY 19

RIGHTS ISSUE STATISTICS 21

PART I LETTER FROM THE CHAIRMAN OF PREMIER OIL PLC 22

PART II INFORMATION ON PREMIER 34

PART III INFORMATION ON ONSL 51

PART IV KEY INFORMATION 59

PART V SUMMARY OF THE PRINCIPAL TERMS OF THE ACQUISITION 65

PART VI SUMMARY OF THE COMPANY VOLUNTARY ARRANGEMENT

PROCEDURE FOR ONSL 68

PART VII SOME QUESTIONS AND ANSWERS ON THE RIGHTS ISSUE 70

PART VIII TERMS AND CONDITIONS OF THE RIGHTS ISSUE 77

PART IX INFORMATION CONCERNING THE NEW ORDINARY SHARES 95

PART X OPERATING AND FINANCIAL REVIEW 97

PART XI FINANCIAL INFORMATION ON PREMIER 124

PART XII FINANCIAL INFORMATION ON ONSL 125

PART XIII UNAUDITED PRO FORMA FINANCIAL INFORMATION 158

PART XIV COMPETENT PERSON’S REPORT 162

PART XV UNITED KINGDOM TAXATION 223

PART XVI ADDITIONAL INFORMATION 226

PART XVII DOCUMENTATION INCORPORATED BY REFERENCE 249

PART XVIII DEFINITIONS 250

NOTICE OF EXTRAORDINARY GENERAL MEETING 256

3

c100191pu010Proof10:3.4.09B/LRevision:0OperatorPutA

SUMMARY

The following information should be read as an introduction to and in conjunction with the full text

of this document. Any investment decision relating to Premier, the Rights Issue, the Acquisition or

the Enlarged Group should be based on a consideration of this document as a whole, including the

documents incorporated by reference. Investors should therefore read this entire document and notrely solely on this summary. In particular, investors should not rely on the summarised financial

information in this summary and should read the financial information contained in the remainder of

this document.

Civil liability will attach to those persons responsible for this summary (including any translation of

this summary) in any member state of the European Economic Area, but only if the summary ismisleading, inaccurate or inconsistent when read together with the other parts of this document.

Where a claim relating to the information contained in this document is brought before a court in a

member state of the European Economic Area, the plaintiff might, under the national legislation of

the member state where the claim is brought, be required to bear the costs of translating this

document before the legal proceedings are initiated.

1. Introduction

Premier announced on 25 March 2009 that it had (through its wholly-owned subsidiaries, POGL and

POEL) reached conditional agreement with Oilexco Inc. and ONSL to acquire ONSL or the ONSL

Assets for a maximum consideration of approximately US$505 million (approximately £343 million).

Premier proposes to fund the Acquisition and associated costs by way of:

* a 4 for 9 rights issue of New Ordinary Shares at a price of 485 pence per share to raise gross

proceeds of approximately £171 million (approximately US$252 million);

* New Credit Facilities comprising a US$175 million 18-month acquisition bridge facility, a

US$225 million 3-year revolving credit facility and US$63 million and £60 million 3-year letter

of credit facilities; and

* Premier’s existing cash resources.

2. Information on Premier and ONSL

Premier is an oil and gas exploration and production company. It is the Group’s ultimate parent

company. The Group was founded 75 years ago and has current interests in 11 countries around the

world and significant operations in the North Sea (UK and Norway), Asia and the Middle East. It

has a reserve and resource base of 382 mmboe, which is currently producing around 36,500 boepd (asof the year ended 31 December 2008).

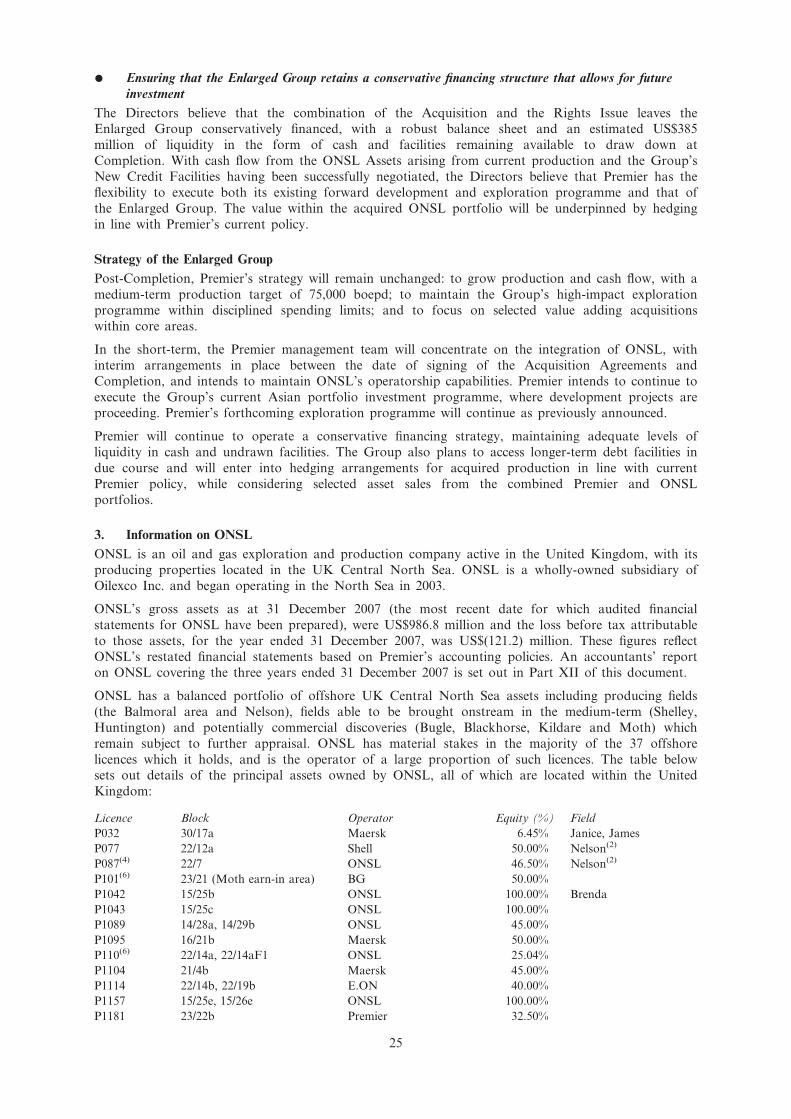

ONSL is an oil and gas exploration and production company active in the UK, with its producing

properties located in the UK Central North Sea. ONSL is a wholly-owned subsidiary of Oilexco Inc.

and began operating in the North Sea in 2003. ONSL was placed into administration by its lending

banks on 7 January 2009. Since that date, ONSL’s Administrators have continued to operate thebusiness, which has continued to generate positive current cash flow from ongoing operations.

ONSL’s total production for the year ending 31 December 2009 is expected by Premier to be

approximately 13,700 boepd. As at 31 December 2008, ONSL had total 2P reserves and contingent

resources of approximately 60 mmboe, of which 40 mmboe is expected to be bookable to 2P reserves

by Premier.

3. Background to and reasons for the Acquisition

The Directors believe that the Acquisition is an opportunity with a compelling strategic, operational

and financial rationale, and will contribute significantly to the achievement of Premier’s strategic

objectives. The Acquisition will provide the Enlarged Group with a greater presence in the North Sea,

strengthening the Group’s existing operations in that area by adding a material package of assets

comprising existing producing fields, development projects of existing discovered reserves and a

portfolio of exploration prospects, together with high-quality UK operatorship capabilities.

The Directors believe that particular benefits of the Acquisition will include:

* Balancing the Enlarged Group by delivering critical mass in a second core area, the North Sea

* Enhancing the Group’s reserves, current production and cash flow

* Offering significant overlap with Premier’s existing North Sea assets and infrastructure

4

c100191pu010Proof10:3.4.09B/LRevision:0OperatorPutA

* Strengthening exploration and appraisal portfolio with acquired North Sea acreage

* Strengthening operational flexibility via significant equity and operatorship positions

* Improving Premier’s portfolio of potential development projects

* Allowing Shareholders to benefit from a compelling acquisition valuation

* Ensuring that the Enlarged Group retains a conservative financing structure that allows for

future investment

The Directors also believe that the cash flows from the acquired producing fields of ONSL

complement, and will assist in, the funding of Premier’s previously announced development capital

expenditure requirements for its three developments in Asia.

4. Summary operating and financial information on Premier

The operating and financial information set out below has been extracted from Premier’s statutory

accounts for the three years ended 31 December 2008, which are incorporated by reference into this

document, as explained in Part XI of this document. The information set out below does not

constitute statutory accounts for any company within the meaning of section 435 of the Companies

Act 2006.

2P Reserves

(mmboe)

Production

(kboepd)

Profit after tax

(US$m)

Operating cash flow

(US$m)

2008 2007 2006 2008 2007 2006 2008 2007 2006 2008 2007 2006

228 212 152 36.5 35.8 33.0 98.3 39.0 67.6 352.3 269.5 244.8

5. Current trading and prospects of Premier

Despite volatile markets and the sharp downturn in economic activity, the Directors consider that theGroup is in a strong position to maintain its growth profile. Already in 2009, the Group has

progressed a number of critical contracts which are now at the centre of its development projects.

Premier is about to embark on an extensive exploration and appraisal campaign, which has the

potential to have a material impact on the Group. The quality of the Group’s producing assets,

underpinned by its financial position, secures its forward cash flows and allows it to progress its

exploration and development programmes that could bring very significant upside.

6. Principal terms of the Acquisition

Under the terms of the Acquisition, Premier (through its wholly-owned subsidiaries, POGL and

POEL) has agreed to acquire either: (i) the Shares; or (ii) the Assets. Premier has proceeded initially

with the Share Acquisition. Completion under the Share Acquisition Agreement is conditional upon,

inter alia, the approval of the Company Voluntary Arrangement (as more fully described in Part VI

of this document). The total consideration payable to Oilexco Inc. (acting through the Receiver)

under the Share Acquisition Agreement is US$1. However, in addition, POGL will also fund the

payment by ONSL of a settlement amount of US$505 million (the ‘‘Settlement Amount’’) tocompromise certain debts and liabilities owed to ONSL’s secured and unsecured creditors.

Appropriate adjustments will be made to the Settlement Amount to account for certain payables,

receivables and other items.

If the CVA is not approved, Premier (through POEL) will continue the Acquisition under the Asset

Acquisition Agreement, which has been entered into conditionally upon termination of the ShareAcquisition Agreement. The consideration payable by POEL under the Asset Acquisition Agreement

is US$415 million. Similar adjustments will be made to the consideration to account for certain

payables, receivables and other items.

Both of the Acquisition Agreements are conditional upon (i) Admission; and (ii) the approval byShareholders of the Acquisition at the EGM.

Both of the Acquisition Agreements contain a break fee in an amount of US$5.05 million in favour

of ONSL. The break fee is payable only if: (i) the Resolutions are not passed by Shareholders at the

EGM; or (ii) Admission does not take place by 14 June 2009.

Certain operating assets owned by ONSL are subject to pre-emption rights in favour of third parties.

If a third party exercises its right of pre-emption in respect of an asset, such asset will not form part

of the Acquisition and the consideration will be reduced accordingly.

5

c100191pu010Proof10:3.4.09B/LRevision:0OperatorPutA

Under the terms of the Acquisition Agreements, if ONSL’s interest in one or more of the Balmoral

field interest, the Brenda field interest, the Nicol field interest or the Huntingdon field interest is

forfeited, revoked or terminated, or notice of forfeiture, revocation or termination is given before

Completion, POGL and/or POEL may terminate the Share Acquisition Agreement or the AssetAcquisition Agreement (as applicable) at its discretion.

7. Principal terms and conditions of the Rights Issue

The New Ordinary Shares will be offered by way of rights at 485 pence per share to Qualifying

Shareholders (other than, subject to certain exemptions, Excluded Overseas Shareholders) on the basis

of:

4 New Ordinary Shares for every 9 Existing Ordinary Shares

The Rights Issue Price represents a discount of approximately 49% to the Closing Price for an

Existing Ordinary Share of 952 pence on 24 March 2009 (the latest practicable date prior to the date

of the Announcement).

The New Ordinary Shares will, when issued and fully paid, rank pari passu in all respects with the

Existing Ordinary Shares. The Rights Issue has been fully underwritten by the Underwriters and isconditional upon:

(a) both the Acquisition Agreements not having been terminated, and the Acquisition not ceasing to

be capable of Completion in accordance with the terms of the Acquisition Agreements prior to

Admission;

(b) the Resolutions being passed at the EGM;

(c) Admission becoming effective by not later than 8.00 a.m. on 21 April 2009 (or such later time

and/or date as Premier and the Underwriters may agree (being not later than 8.00 a.m. on 6

May 2009)); and

(d) the Underwriting Agreement having become unconditional in all respects (save for conditionsrelating to Admission) and not having been terminated in accordance with its terms prior to

Admission.

The Rights Issue will result in dilution of 31% if existing Shareholders do not take up their rights

under the Rights Issue.

Application has been made to the UK Listing Authority and to the London Stock Exchange for theNew Ordinary Shares to be admitted to the Official List of the UK Listing Authority and to be

admitted to trading on the main market for listed securities of the London Stock Exchange. It is

expected that Admission will become effective and that dealings in the New Ordinary Shares will

commence on the London Stock Exchange, nil paid, at 8.00 a.m. on 21 April 2009.

8. Use of proceeds of the Rights Issue

The proceeds of the Rights Issue will be used to fund part of the consideration for the Acquisition,

together with transaction and acquisition costs. The Rights Issue is not conditional on Completion. In

the event that the Rights Issue proceeds but Completion does not take place, the Directors’ currentintention is that the net proceeds of the Rights Issue will be invested on a short-term basis while the

Directors consider how best to return the proceeds of the Rights Issue (after the deduction of

acquisition and transaction costs) to Shareholders. However, if, before Admission, the Acquisition

Agreements have both terminated or the Acquisition ceases to be capable of Completion, the Rights

Issue will not proceed.

9. New Credit Facilities

Premier has entered into the New Credit Facilities comprising a US$175 million 18-month acquisition

bridge facility, a US$225 million 3-year revolving credit facility and US$63 million and £60 million 3-year letter of credit facilities. The New Credit Facilities are conditional on Completion of the

Acquisition and are described in paragraph 12(f) of Part XVI of this document.

10. Risk factors

Shareholders should consider carefully the following risks, which are not the only risks facing

Premier, ONSL and the Enlarged Group:

6

c100191pu010Proof10:3.4.09B/LRevision:0OperatorPutA

Risk factors relating to Premier, ONSL and the Enlarged Group

* failure to access new oil and gas reserves could slow oil and gas production growth and

replacement of reserves;

* the assumptions on which estimates of hydrocarbon reserves or resources have been based may

prove to be incorrect, particularly where uncertified data is used;

* failure to successfully integrate a strategic business acquisition (such as the Acquisition) may

adversely affect the business of the Enlarged Group;

* intense competition in the oil and gas business environment (including as a result of the scarcity

of vital services and capital equipment) may lead to increased costs and reduced available

growth opportunities;

* production plans may be adversely affected by a wide range of factors which are not within the

control of Premier or, following the Acquisition, the Enlarged Group;

* failure to comply with potentially complex and stringent health and safety laws and regulationsmay give rise to significant liabilities;

* fluctuation of hydrocarbon prices may affect Premier’s or, following the Acquisition, the

Enlarged Group’s financial position;

* Premier or, following the Acquisition, the Enlarged Group may be adversely affected by

political, economic, legal, regulatory or social changes in certain countries, including by the

significant influence of certain governments over the oil and gas industry;

* there can be no assurance that the proceeds of insurance applicable to covered risks will be

adequate to cover uninsured hazards;

* conditions in the credit markets could prevent Premier from refinancing its facilities on

acceptable terms or at all in the longer-term.

Risk factors relating to the Acquisition

* the implementation of the Acquisition is subject to the satisfaction of a number of conditions

and there is no guarantee that these conditions will be satisfied; if the conditions are not

satisfied, the proceeds of the Rights Issue will not be used for the purchase price for the

Acquisition;

* as Premier has received no representations, warranties or other indemnities in connection with

the Acquisition, it does not have any recourse against any person for defects in title or third

party rights, or for any undiscovered liabilities or obligations connected with the acquired Shares

or Assets (as applicable);

* there may have been a significant deterioration in the value of ONSL’s business since it wasplaced into administration;

* certain Assets are subject to pre-emption rights which, if exercised, will preclude Premier from

acquiring such Assets;

* accumulated tax losses within ONSL may be less than anticipated;

* if the Acquisition proceeds by way of a Share Acquisition there may be objections by creditors

to the CVA which, ultimately, could lead to a court unwinding the CVA;

* the invalid appointment of, or conferral of powers to, a receiver or an administrator gives rise

to a risk that the purchase of the ONSL Shares (in the case of the Receiver) or the ONSL

Assets (in the case of the Administrator) could be challenged, and Premier would have no

recourse to the Receiver or the Administrators (as applicable) should any liability arise on acontract entered into by such officer.

Risk factors relating to the terms of the New Credit Facilities

* Premier could be required to refinance the US$175 million 18-month acquisition bridge facility

at a significantly increased cost to the Enlarged Group;

* the covenants and other restrictions applicable to the New Credit Facilities could restrict the

Enlarged Group’s business, flexibility or ability to undertake strategic or significant transactions.

7

c100191pu010Proof10:3.4.09B/LRevision:0OperatorPutA

Risk factors relating to the Rights Issue and the New Ordinary Shares

* Premier’s share price could be the subject of significant price fluctuations due to a change in

sentiment in the market;

* an active market in Nil Paid Rights may not develop on the London Stock Exchange during the

trading period;

* the market price of the Ordinary Shares may decrease, reducing the discount at which the New

Ordinary Shares are available to Qualifying Shareholders; and

* if Shareholders do not take up the offer under the Rights Issue, their proportionate ownership

and voting interests in Premier will be reduced.

8

c100191pu010Proof10:3.4.09B/LRevision:0OperatorPutA

RISK FACTORS

You should carefully consider the risks and uncertainties described below, in addition to the other

information in this document. The risks and uncertainties described below represent all of those known to

the Directors as at the date of this document which the Directors consider to be material. However,

these risks and uncertainties are not the only ones facing the Group and/or the Enlarged Group;

additional risks and uncertainties not presently known to the Directors, or that the Directors currently

consider to be immaterial, could also impair the business of the Group and/or the Enlarged Group. If

any or a combination of these risks actually occurs, the business, financial condition and operating

results of the Group and/or the Enlarged Group could be adversely affected. In such case, the market

price of the Ordinary Shares could decline and you may lose all or part of your investment.

No statement contained in the risks and uncertainties described below should be taken as qualifying the

statement as to the sufficiency of working capital set out in paragraph 3 of Part IV of this document.

1. Risk factors relating to Premier, ONSL and the Enlarged Group

Reserves replacement

Future oil and gas production will depend on Premier’s or, following the Acquisition, the Enlarged

Group’s access to new reserves through exploration, negotiations with governments and other owners

of known reserves, and acquisitions. Failures in exploration or in identifying and finalisingtransactions to access potential reserves could slow Premier’s or the Enlarged Group’s oil and gas

production growth and replacement of reserves. This, in turn, could have an adverse affect on the

turnover and profits of Premier or the Enlarged Group.

In addition, the results of appraisal of discoveries are uncertain and may involve unprofitable efforts,not only from dry wells, but also from wells that are productive but uneconomic to develop.

Appraisal and development activities may be subject to delays in obtaining governmental approvals or

consents, shut-ins of connected wells, insufficient storage or transportation capacity or other

geological and mechanical conditions all of which may variously increase Premier’s or, following the

Acquisition, the Enlarged Group’s costs of operations.

Exploration activities are capital intensive and inherently uncertain in their outcome. There is

therefore a risk that Premier or, following the Acquisition, the Enlarged Group will undertake

exploration activities and incur significant costs in so doing with no assurance that such expenditure

will result in the discovery of hydrocarbons, whether or not in commercially viable quantities. If

exploration activities prove unsuccessful over a prolonged period of time, Premier or the Enlarged

Group may not, after 12 months from the date of this document, have sufficient working capital to

continue to meet their obligations and their ability to obtain additional financing necessary to

continue operations may also be adversely affected.

Estimation of reserves, resources and production profiles

The estimation of oil and gas reserves, and their anticipated production profiles involves subjective

judgments and determinations based on available geological, technical, contractual and economic

information. They are not exact determinations. In addition, these judgments may change based on

new information from production or drilling activities or changes in economic factors, as well as from

developments such as acquisitions and dispositions, new discoveries and extensions of existing fieldsand the application of improved recovery techniques. Published reserve estimates are also subject to

correction for errors in the application of published rules and guidance.

The reserves, resources and production profile data contained in this document are estimates only and

should not be construed as representing exact quantities. They are based on production data, prices,costs, ownership, geophysical, geological and engineering data, and other information assembled by

Premier or ONSL (as applicable). The estimates may prove to be incorrect and potential investors

should not place undue reliance on the forward-looking statements contained in this document

concerning Premier’s or ONSL’s reserves and resources or production levels.

If the assumptions upon which the estimates of Premier’s or ONSL’s hydrocarbon reserves, resources

or production profiles have been based prove to be incorrect, Premier or, following the Acquisition,

the Enlarged Group may be unable to recover and produce the estimated levels or quality of

hydrocarbons set out in this document and Premier’s or the Enlarged Group’s business, prospects,

financial condition or results of operations could be materially adversely affected.

9

c100191pu020Proof10:3.4.09B/LRevision:0OperatorPutA

Business acquisitions – integration and other issues

Part of Premier’s strategy is or, following the Acquisition, part of the Enlarged Group’s strategy will

be to increase oil and gas reserves through strategic business acquisitions. Risks commonly associatedwith acquisitions of companies or businesses include the difficulty of integrating the operations and

personnel of the acquired business, problems with minority shareholders in acquired companies, the

potential disruption of Premier’s or the Enlarged Group’s own business, the possibility that

indemnification agreements with the sellers may be unenforceable or insufficient to cover potential

liabilities and difficulties arising out of integration. Furthermore, the value of any business Premier or

the Enlarged Group acquires or invests in may be less than the amount it pays. (These risks may also

apply to the Acquisition itself).

Currency fluctuations and exchange controls

Premier operates and, following the Acquisition, the Enlarged Group will operate in a number of

different countries and territories throughout the world. Premier is, or the Enlarged Group will be,

subject to risks from changes in currency values and exchange controls. The Enlarged Group’s

exposure to such risks will be increased by the Acquisition, as ONSL has a greater exposure to costs

in Pounds Sterling. Changes in currency values and exchange controls could have an adverse effect on

Premier’s or the Enlarged Group’s results of operations and financial position.

Competition

Premier operates or, following the Acquisition, the Enlarged Group will operate in a very challenging

business environment and competition for access to exploration acreage, gas markets, oil services andrigs, technology and processes, and human resources is intense. Competitors include companies with,

in many cases, greater financial resources, local contacts, staff and facilities than those of Premier or

the Enlarged Group. Competition for exploration and production licences as well as other regional

investment or acquisition opportunities may increase in the future. This may lead to increased costs in

the carrying on of Premier’s or the Enlarged Group’s activities and reduced available growth

opportunities. Any failure by Premier or the Enlarged Group to compete effectively could adversely

affect Premier’s or the Enlarged Group’s operating results and financial condition.

Third party contractors and providers of capital equipment

In particular, Premier has or, following the Acquisition, the Enlarged Group will have an interest in

contracts or leases, services and capital equipment from third-party providers. Such equipment and

services can be scarce and may not be readily available at the times and places required. In addition,

the costs of third-party services and equipment have increased significantly over recent years and may

continue to rise. Scarcity of equipment and services and increased prices may, in particular, result

from any significant increase in regional exploration and development activities which in turn may be

the consequence of increased or continued high prices for oil or gas. The scarcity of such equipment

and services, as well as their potentially high costs, could delay, restrict or lower the profitability andviability of Premier’s or the Enlarged Group’s projects and therefore have a material adverse affect

on Premier’s or the Enlarged Group’s business.

Production

The delivery of Premier’s production plans depends or, following the Acquisition, the delivery of the

Enlarged Group’s production plans will depend on the successful continuation of existing field

production operations and the development of key projects. Both of these involve risks normally

incidental to such activities including blowouts, oil spills, explosions, fires, equipment damage or

failure, natural disasters, geological uncertainties, unusual or unexpected rock formations, abnormalpressures, availability of technology and engineering capacity, availability of skilled resources,

maintaining project schedules and managing costs, as well as technical, fiscal, regulatory, political and

other conditions. Such potential obstacles may impair Premier’s or the Enlarged Group’s continuation

of existing field production and delivery of key projects and, in turn, Premier’s or the Enlarged

Group’s operational performance and financial position (including the financial impact from failure to

fulfil contractual commitments related to project delivery).

Premier or, following the Acquisition, the Enlarged Group may face interruptions or delays in the

availability of infrastructure, including pipelines and storage tanks, on which exploration and

production activities are dependent. The production performance of the reservoirs and wells may also

be different to that forecast due to normal geological or mechanical uncertainties. Such interruptions,

delays or performance differences could result in disruptions or changes to Premier’s or the Enlarged

10

c100191pu020Proof10:3.4.09B/LRevision:0OperatorPutA

Group’s existing production and projects, lower production and increased costs, and may have an

adverse effect on Premier’s or the Enlarged Group’s profitability.

Health, Safety, Environment and Security (‘‘HSES’’)

The range of Premier’s or, following the Acquisition, the Enlarged Group’s operated and joint

venture production operations globally means that Premier’s HSES risks cover, and the Enlarged

Group’s HSES risks will cover, a wide spectrum. These risks include major process safety incidents;

failure to comply with approved policies; effects of natural disasters and pandemics; social unrest;civil war and terrorism; exposure to general operational hazards; personal health and safety; and

crime. The consequences of such risks materialising can be injuries, loss of life, environmental harm

and disruption to business activities. Depending on cause and severity, the materialisation of such

risks may affect Premier’s or the Enlarged Group’s reputation, operational performance and financial

position.

In addition, failure by Premier or, following the Acquisition, the Enlarged Group to comply with

applicable legal requirements or recognised international standards may give rise to significant

liabilities. HSES laws and regulations may over time become more complex and stringent or the

subject of increasingly strict interpretation or enforcement. The terms of licences may include more

stringent HSES requirements. The obtaining of exploration, development or production licences and

permits may become more difficult or be the subject of delay by reason of governmental, regional or

local environmental consultation, approvals or other considerations or requirements. These factorsmay lead to delayed or reduced exploration, development or production activity as well as to

increased costs.

Reputation

It is important for maintaining Premier’s or, following the Acquisition, the Enlarged Group’s licencesto operate and ability to secure new resources that Premier or the Enlarged Group should maintain

strong and positive relationships with the governments and communities in the countries where its

business is conducted. Premier’s business principles govern or, following the Acquisition, will govern

how Premier and the Enlarged Group conduct their affairs. Failure – real or perceived – to follow

these principles, or any of the risk factors described in this document materialising, could harm

Premier’s or the Enlarged Group’s reputation, which could, in turn, impact Premier’s or the Enlarged

Group’s licence to operate, financing and access to new opportunities.

Human resources

Premier’s key human resources are or, following the Acquisition, the Enlarged Group’s key human

resources will be essential for the successful delivery of projects and continuing operations. Loss of

personnel to competitors or inability to attract quality human resources could affect Premier’s or theEnlarged Group’s operational performance and growth strategy.

Hydrocarbon prices

Historically, hydrocarbon prices have been subject to large fluctuations in response to a variety of

factors beyond Premier’s or ONSL’s control. Factors that influence these fluctuations includeoperational issues, natural disasters, weather, political instability or conflicts, economic conditions or

actions by major oil-exporting countries. Price fluctuations can affect Premier’s business assumptions,

investment decisions and financial position or, following the Acquisition, could affect the Enlarged

Group’s business assumptions, investment decisions and financial position. In particular, lower

hydrocarbon prices may reduce the economic viability of Premier’s or the Enlarged Group’s projects,

result in a reduction in revenues or net income, impair Premier’s or the Enlarged Group’s ability to

make planned expenditures and could materially adversely affect Premier’s or the Enlarged Group’s

business, prospects, financial condition and results of operations.

Current and future financing

Premier and, following the Acquisition, the Enlarged Group will require new financing to refinance

existing facilities (all of which have a term or an unexpired term of more than 12 months from thedate of this document) and may, in the longer-term, require additional financing to fund future

exploration and development plans. This financing may not be available or, if available, may not be

available on favourable terms. The ability of Premier or the Enlarged Group to arrange such

financing in the future will depend in part upon the prevailing capital market conditions, as well as

the business performance of Premier or the Enlarged Group. There can be no assurance that Premier

11

c100191pu020Proof10:3.4.09B/LRevision:0OperatorPutA

or the Enlarged Group will be successful in its efforts to arrange additional financing on satisfactory

terms. If adequate funds are not available, or are not available on acceptable terms, Premier or the

Enlarged Group may not be able to take advantage of opportunities, or otherwise respond to

competitive pressures and remain in business.

Political, economic, legal, regulatory and social uncertainties

Premier operates or, following the Acquisition, the Enlarged Group will operate in some countries

where political, economic and social transition is taking place. Changes in politics, laws and

regulations can affect Premier’s or could affect the Enlarged Group’s operations and earnings. Such

circumstances include forced divestment of assets; limits on production; import and exportrestrictions; international conflicts, including war; civil unrest and local security concerns that threaten

the safe operation of Premier’s or the Enlarged Group’s facilities; price controls, tax increases and

other retroactive tax claims; expropriation (including ‘‘creeping’’ expropriation) and nationalisation of

property; terrorism; outbreaks of infectious diseases; cancellation of contract rights; and

environmental regulations. It is difficult to predict the timing or severity of these occurrences or their

potential effect. If such risks materialise they could affect the employees, reputation, operational

performance and financial position of Premier or the Enlarged Group.

Premier operates or, following the Acquisition, the Enlarged Group will operate in countries which

have transportation, telecommunications and financial services infrastructures that may present

logistical challenges not associated with doing business in more developed locales.

Either Premier or the Enlarged Group may have difficulty ascertaining its legal obligations and

enforcing any rights which it may have. Certain governments in other countries have in the past

expropriated or nationalised property of hydrocarbon production companies operating within their

jurisdictions. Sovereign or regional governments could require Premier or the Enlarged Group to

grant to them larger shares of hydrocarbons or revenues than previously agreed to. Furthermore, it

may be expensive and logistically burdensome to discontinue hydrocarbon exploration and/or

production operations in a particular country should economic, political, physical or other conditionssubsequently deteriorate. All of these factors could materially adversely affect Premier’s or the

Enlarged Group’s business, results of operations, financial condition or prospects.

Joint ventures and partners

Inherently, oil and gas operations globally are conducted in a joint venture environment. Many of

Premier’s and ONSL’s major projects are operated by a partner in the relevant joint venture. Theability of Premier and ONSL to influence their partners will sometimes be limited due to their

percentage ownership in non-operated development and production operations. Non-alignment on

various strategic decisions in joint ventures may result in operational or production inefficiencies or

delay.

Governmental involvement in the oil and gas industry

The governments of countries in which Premier currently operates or may operate or, following theAcquisition, the Enlarged Group will or may operate have exercised and continue to exercise

significant influence over many aspects of their respective economies, including the oil and gas

industry. Any government action concerning the economy, including the oil and gas industry (such as

a change in oil or gas pricing policy or taxation rules or practice, or renegotiation or nullification of

existing concession contracts), could have a material adverse effect on Premier or the Enlarged

Group. Furthermore, there can be no assurance that these governments will not postpone or review

projects or will not make any changes to laws, rules, regulations or policies, in each case, which could

materially adversely affect Premier’s or the Enlarged Group’s financial position, results of operationsor prospects.

Uninsured hazards

Premier or, following the Acquisition, the Enlarged Group may be subject to substantial liability

claims due to the inherently hazardous nature of their business or for acts and omissions of sub-

contractors, operators or joint venture partners. Any indemnities Premier or the Enlarged Group mayreceive from such parties may be difficult to enforce if such sub-contractors, operators or joint

venture partners lack adequate resources. There can be no assurance that the proceeds of insurance

applicable to covered risks will be adequate to cover expenses relating to losses or liabilities.

Accordingly, Premier or the Enlarged Group may suffer material losses from uninsurable or

uninsured risks or insufficient insurance coverage.

12

c100191pu020Proof10:3.4.09B/LRevision:0OperatorPutA

Counterparties

Premier has entered into or, following the Acquisition, the Enlarged Group will be subject to

agreements with a number of contractual counterparties in relation to the sale and supply ofhydrocarbon production volumes. Therefore, Premier is, or the Enlarged Group will be, subject to the

risk of delayed payment for delivered production volumes or counterparty default. Such delays or

defaults could materially adversely affect Premier’s or the Enlarged Group’s business, results of

operations and cash flows.

Licensing and other regulatory requirements

Countries in which Premier currently operates or may operate or, following the Acquisition, the

Enlarged Group will or may operate are subject to licences, regulations and approvals ofgovernmental authorities, including those relating to the exploration, development, operation,

production, marketing, pricing, transportation and storage of oil and gas, taxation, environmental,

and health and safety matters.

Premier has or the Enlarged Group will have limited control over whether or not necessary approvals

or licences (or renewals thereof) are granted, the timing of obtaining (or renewing) such licences or

approvals, the terms on which they are granted or the tax regime to which Premier or the EnlargedGroup or the assets in which Premier or the Enlarged Group has interests will be subject. As a result,

Premier or the Enlarged Group may have limited control over the nature and timing of exploration

and development of oil and gas fields in which Premier or the Enlarged Group has or seeks interests.

There can be no assurance that Premier or the Enlarged Group will not in the future incur

decommissioning charges since local or national governments may require decommissioning to be

carried out in circumstances where there is no express obligation to do so, particularly in case of

future licence renewals.

Licence withdrawal and renewal

It is possible that in the future Premier or, following the Acquisition, the Enlarged Group may be

unable or unwilling to comply with the terms or requirements of a licence in circumstances that

entitle the relevant authority to suspend or withdraw the terms of such licence. Moreover, some of

the exploration and production licences which are held by Premier or will be held by the Enlarged

Group expire or may expire before the end of what Premier estimates or the Enlarged Group may

estimate to be the productive life of the licenced fields. There can be no assurance that extensions willbe granted in relation to such licences. Any failure to receive such extensions or any premature

termination, suspension or withdrawal of licences may have a material adverse effect on Premier’s or

the Enlarged Group’s reserves, business, results of operations and prospects.

Credit market conditions and credit ratings

Recent events in the credit markets have significantly restricted the supply of credit, as financial

institutions have applied more stringent lending criteria or exited the market entirely. If current

market conditions continue, it will be more costly and more difficult for Premier or, following theAcquisition, the Enlarged Group to refinance its debt as it falls due in the longer-term.

In addition, it has become and may become more costly to raise new funds to take advantage of

opportunities.

Macroeconomic risks could result in an adverse impact on Premier’s or, following the Acquisition, theEnlarged Group’s financial condition

One of the principal uncertainties for Premier and the Enlarged Group at present is the extent to

which the global economic slowdown currently being experienced may feed through into Premier’s or,

following the Acquisition, the Enlarged Group’s major operations, and the timing of that impact. The

links between economic activities in different markets and sectors are complex and depend not only

on direct drivers such as the balance of trade and investment between countries, but also on domestic

monetary, fiscal and other policy responses to address macroeconomic conditions.

2. Risk factors relating to the Acquisition

General risks relating to the Acquisition

Conditions of the Acquisition

The implementation of the Acquisition is subject to the satisfaction (or waiver, where applicable) of a

number of conditions, including:

13

c100191pu020Proof10:3.4.09B/LRevision:0OperatorPutA

* for the Share Acquisition Agreement, completion of the agreed CVA process with unsecured

creditors; and

* for the Asset Acquisition Agreement, successful completion of the relevant pre-emption processes

applicable to some of the Assets.

There is no guarantee that these (or other) conditions will be satisfied (or waived, if applicable), in

which case the Acquisition will not be completed. The conditions are more fully described in Part V

of this document. If the Rights Issue has become unconditional but the Acquisition has not, the

Company will raise proceeds in the Rights Issue that may not subsequently be used to pay the

purchase price for the Acquisition if the Acquisition does not complete.

No warranties in connection with the Acquisition

As is customary in the case of purchases from sellers in administration or receivership, Premier has

received no representations, warranties or other indemnities of any kind in connection with the

Acquisition. Premier will therefore acquire the ONSL Shares or Assets (as applicable) pursuant to theAcquisition, together with any potential risks and liabilities associated with them, without having any

recourse against any person for defects in title to those ONSL Shares or Assets or for any

undiscovered liabilities or obligations connected with such ONSL Shares or Assets. If any such issues

arise after Completion, Premier could be left without full ownership of the ONSL Shares or Assets,

or with ownership of the ONSL Shares or Assets but with unexpected additional liabilities or

obligations, and with no ability to reclaim any of the consideration it has paid.

Deterioration in the value of ONSL’s business

ONSL was placed into administration on 7 January 2009. During the course of the administration,

the value of ONSL’s business may have fallen significantly due to the negative market perception ofthe administration process. The effects of such perception may include suppliers withdrawing lines of

credit and insisting that purchases are on cash on delivery terms or prepaid; customers refusing to

pay their invoices on time; customers seeking alternate suppliers; customers insisting on discounts on

outstanding debts and any new orders placed; a lack of new business; a fall in employee morale and

productivity; and the departure of skilled and senior employees essential to the business. This may

have negative consequences for the business of the Enlarged Group and its prospects following

Completion.

Certain of the Assets are subject to pre-emption rights

A number of the Assets held by ONSL are held pursuant to joint operating agreements and willtherefore be subject to pre-emption rights held by joint venture partners of ONSL if Premier acquires

such Assets pursuant to the Asset Acquisition Agreement. Premier would only be able to acquire

these Assets following compliance with the relevant contractual pre-emption process, which may

typically take a period of between 30 and 90 days or more to implement. If the joint venture partners

choose to exercise their rights, Premier will not be able to acquire such Assets at all. If all of the

Assets still subject to pre-emption are pre-empted, this could mean a reduction in the benefits of the

Acquisition for Premier, and will also mean that part of the proceeds of the Rights Issue will not be

required for use in payment of the purchase price.

If the Acquisition proceeds by way of Share Acquisition or Asset Acquisition the Bugle asset

(governed by P815 Licence) is also subject to a right of pre-emption under the relevant joint venture

agreement.

Assets subject to third party rights

While Premier has carried out a due diligence exercise in relation to ONSL, the Assets may be

subject to undisclosed third party rights (including, among others, fixed or floating charges, hire

purchase agreements and retention of title claims). If, at the conclusion of ONSL’s administration,

Premier has not procured the formal release of any such rights (or the purported release is in any

way invalid), beneficiaries may be entitled to exercise their rights over such Assets. Post-Acquisition,there is a risk that Premier will be prevented from dealing freely with the Assets or that its use of the

Assets will be restricted and/or made subject to Premier paying the relevant beneficiary a fee for such

use.

The Enlarged Group’s success will be dependent upon its ability to integrate ONSL

The Enlarged Group may encounter numerous integration challenges in connection with the

Acquisition, including challenges which are not currently foreseeable. In addition, the Enlarged

14

c100191pu020Proof10:3.4.09B/LRevision:0OperatorPutA

Group’s management and resources may be diverted away from its core business activities due to

personnel being required to assist in the integration process. This integration process may take longer

than expected, or difficulties relating to the integration, of which the Board is not yet aware, may

arise. This could adversely affect the implementation of the Enlarged Group’s plans, and the EnlargedGroup may not be successful in addressing risks or problems encountered in connection with the

integration and failure to do so may adversely affect its business or financial condition. In addition,

there is a risk that synergy benefits may fail to materialise, or they may be materially lower than have

been estimated which may have a material adverse affect on the financial condition of the Enlarged

Group.

Risks relating to the Acquisition proceeding by way of Share Acquisition

Objections to the CVA

While the Share Acquisition Agreement is conditional upon both the CVA being approved at a

creditors’ meeting and a 28 day objection period for creditor complaints having passed, there is still a

risk that the decision of the creditors to approve the CVA could be subsequently challenged after

Completion. A creditor entitled to vote at the creditors’ meeting (but who did not receive notice of

such meeting) may apply to the court and challenge the decision of the meeting. If the court issatisfied that the approval of the CVA unfairly prejudices such a creditor, it has the power to revoke

or suspend any decision of the creditors’ meeting and/or direct that a further meeting of the creditors

takes place. If successful, revocation or reconsideration of the approval of the CVA after the

completion of the Share Acquisition Agreement could, in theory, result in the unwinding of the CVA

and the resurrection of ONSL’s original debt obligations (which would therefore fall to be payable by

Premier); or that the CVA would stand, and ONSL would be required to compensate the affected

creditor in cash to the value of the affected claim.

Ongoing relations with suppliers

Certain of the contracts being terminated pursuant to the CVA, and certain of the liabilities being

compromised under the CVA, relate to suppliers to ONSL that have ongoing relationships with

ONSL or other members of the Group. In such cases, while the historic position may be dealt with

as part of the CVA, the ongoing relationships may be adversely affected in such a manner as could

impact on the business of the Enlarged Group going forward, in particular where the Enlarged

Group has limited choices of suppliers to fulfil the relevant role.

Appointment of receiver

The purchase of all the ordinary shares of ONSL is expected to occur through a Receiver appointed

by Royal Bank of Scotland. If this appointment is in any way invalid, or if the Receiver does not

have the right to deal with the property of Oilexco Inc., or has not obtained any required approval

(including any approval of any Canadian court that may be required) or authorisation of any third

party, there is a risk that the Share Acquisition could be challenged by creditors of Oilexco Inc. and

found to be invalid or not to convey any interest in the ONSL Shares to Premier.

Liability of Receiver

While the Business Corporations Act (Alberta) provides that a receiver must deal with any propertyin its possession or control in a commercially reasonable manner, as is customary in the case of

purchases from sellers who are subject to the Companies Creditors Arrangement Act (Canada), the

Share Acquisition Agreement expressly excludes the personal liability of the Receiver. Premier will

therefore have no recourse to the Receiver should any liability arise on any contract entered into by

the Receiver in the exercise of their rights pursuant to any applicable documents.

Taxation

As a result of its significant historical expenditures on exploration, appraisal and development of its

assets, ONSL has accumulated substantial UK tax losses which are potentially available to shelterfuture profits from UK tax if the Acquisition proceeds by way of the Share Acquisition.

As described in the risk factor entitled ‘‘No warranties in connection with the Acquisition’’ on page14, Premier has received no representations, warranties or other indemnities in connection with the

Acquisition. It is possible that the accumulated tax losses will be less than anticipated if HMRC

successfully challenges losses claimed in past tax returns that are still open (2007) or yet to be filed

(2008), either by reason of the eligibility of the actual expenditure, anti-avoidance provisions or by

challenging other aspects of the relevant tax returns.

15

c100191pu020Proof10:3.4.09B/LRevision:0OperatorPutA

Risks relating to the Acquisition proceeding by way of Asset Acquisition

Appointment of the Administrators

ONSL’s Administrators were appointed on 7 January 2009. If this appointment is in any way invalid,or if the Administrators have dealt with ONSL’s property without obtaining the necessary approvals

or authorisations, there is a risk that the Asset Acquisition could be challenged by ONSL’s creditors

and members.

Liability of the Administrators

As is customary in the case of purchases from sellers in administration, the Asset Acquisition

Agreement expressly excludes the personal liability of the Administrators. Premier will therefore have

no recourse to the Administrators should any liability arise on any contract entered into by the

Administrators in the exercise of their functions.

3. Risk factors relating to the terms of the New Credit Facilities

The covenants contained in the New Credit Agreements include financial and other covenantsincluding restrictions on the ability of the Enlarged Group to incur additional financial indebtedness,

grant security, make acquisitions or disposals, enter into mergers and repurchase shares as well as

covenants related to the Acquisition. These could restrict the Enlarged Group’s activities or flexibility

or ability to undertake strategic or significant transactions.

The Company has also entered into certain refinancing obligations in connection with the

US$175 million 18-month acquisition bridge facility. These include an obligation on the Company, if

required by the financiers at any time after the period commencing four months after Completion and

where the Company has not been able to demonstrate that the bridge facility will be refinanced byother means, to take steps to issue debt securities to refinance the bridge facility. If the Company is

unable to carry out such a refinancing (having taken all practicable steps within its control) the

bridge facility will not become repayable prior to its scheduled maturity date on 24 September 2010.

However, the costs of the bridge facility (both in terms of applicable margin and fees) will increase

over time so long as it remains outstanding and is not refinanced. In addition, the refinancing

arrangements referred to above could require the Company, in refinancing the bridge facility, to do so

at a significantly increased cost to the Enlarged Group.

4. Risk factors relating to the Rights Issue and the New Ordinary Shares

Premier’s share price will fluctuate

The market price of the New Ordinary Shares (including the Nil Paid Rights and the Fully Paid

Rights) and/or the Ordinary Shares could be subject to significant fluctuations due to a change in

sentiment in the market regarding the New Ordinary Shares (including the Nil Paid Rights and the

Fully Paid Rights) and/or the Ordinary Shares (or securities similar to them). Such risks depend on

the market’s perception of the likelihood of completion of the Rights Issue, and/or may occur in

response to various facts and events, including any variations in the Group’s operating results,

business developments of the Group and/or its competitors. Stock markets have, from time to time,experienced significant price and volume fluctuations that have affected the market prices for

securities and which may be unrelated to the Group’s operating performance or prospects.

Furthermore, the Group’s operating results and prospects from time to time may be below the

expectations of market analysts and investors. Any of these events could result in a decline in the

market price of the New Ordinary Shares (including the Nil Paid Rights and the Fully Paid Rights)

and/or the Ordinary Shares and investors may, therefore, not recover their original investment.

The sale of Ordinary Shares could have an adverse effect on the market price of the Ordinary Shares.Furthermore, it is possible that Premier may decide to offer additional shares in the future. An

additional offering could also have an adverse effect on the market price of the Ordinary Shares.

An active trading market in the Nil Paid Rights may not develop

An active trading market in the Nil Paid Rights may not develop on the London Stock Exchange

during the trading period. In addition, because the trading price of the Nil Paid Rights depends on

the trading price of the Ordinary Shares, the Nil Paid Rights price may be volatile and subject to the

same risks as noted elsewhere in this document.

16

c100191pu020Proof10:3.4.09B/LRevision:0OperatorPutA

Calculation of the issue price of the New Ordinary Shares

The issue price of the New Ordinary Shares has been calculated by reference, among other things, to

the Closing Price. The market price of the Ordinary Shares may subsequently decrease, reducing thediscount at which the New Ordinary Shares are available to Qualifying Shareholders (other than,

subject to certain exemptions, Excluded Overseas Shareholders).

Dilution of ownership

If Shareholders do not take up the offer of New Ordinary Shares under the Rights Issue their

proportionate ownership and voting interests in Premier will be reduced and the percentage that theirshares will represent of the total share capital of Premier will be reduced accordingly. Even if a

Shareholder elects to sell his unexercised Nil Paid Rights, or such Nil Paid Rights are sold on his

behalf, the consideration he receives may not be sufficient to compensate him fully for the dilution of

his percentage ownership of Premier’s share capital that may be caused as a result of the Rights

Issue.

17

c100191pu020Proof10:3.4.09B/LRevision:0OperatorPutA

EXPECTED TIMETABLE OF PRINCIPAL EVENTS

Each of the times and dates in the table below is indicative only and may be subject to change.

2009

Date of this document 3 April

Record Date for Rights Issue 6.00 p.m. on 16 April

Latest time and date for receipt of Forms of Proxy for

the Extraordinary General Meeting

10.00 a.m. on 18 April

Extraordinary General Meeting 10.00 a.m. on 20 April

Dispatch of Provisional Allotment Letters 20 April

Dealings expected to commence in New Ordinary Shares, nil paid, on the

London Stock Exchange and Existing Ordinary Shares marked ‘‘ex-rights’’

8.00 a.m. on 21 April

Nil Paid Rights and Fully Paid Rights enabled in CREST as soon as

practicable after

8.00 a.m. on 21 April

Recommended latest time and date for requesting withdrawal of Nil Paid

Rights or Fully Paid Rights from CREST

4.30 p.m. on 29 April

Recommended latest time and date for depositing renounced Provisional

Allotment Letters, nil paid or fully paid, into CREST

3.00 p.m. on 30 April

Latest time and date for splitting Provisional Allotment Letters, nil paid and

fully paid

3.00 p.m. on 1 May

Latest time and date for acceptance, delivery of Nil Paid Rights, payment in full

for rights taken up in CREST and registration of renunciation of ProvisionalAllotment Letters

11.00 a.m. on 6 May

Commencement of dealings in New Ordinary Shares fully paid on the London

Stock Exchange

8.00 a.m. on 7 May

New Ordinary Shares in uncertificated form credited to stock accounts in

CREST

8.00 a.m. on 7 May

Expected date of dispatch of definitive share certificates for New Ordinary

Shares in certificated form

8.00 a.m. on 14 May

Expected date of Completion of the Acquisition May

Notes:

(1) Reference to times in this document are to London time unless otherwise stated.

(2) The dates set out in the expected timetable of principal events above and mentioned throughout this document and in theProvisional Allotment Letters may be adjusted by Premier in which event details of the new dates will be notified to the FSA,London Stock Exchange and, where appropriate, the Shareholders.

(3) If you have any queries on the procedure for acceptance and payment, you should contact the Registrar on 0871 664 0321 or fromoutside the United Kingdom on +44 20 8639 3399. Calls to the 0871 664 0321 number cost 10 pence per minute (including VAT)plus your service provider’s network extras. Different charges may apply to calls from mobile telephones and calls may berecorded or randomly monitored for security and training purposes. Please note that the Registrar cannot provide financial adviceon the Rights Issue or as to whether or not you should take up your rights under the Rights Issue.

18

c100191pu020Proof10:3.4.09B/LRevision:0OperatorPutA

DIRECTORY

Registered Office 4th Floor

Saltire Court20 Castle Terrace

Edinburgh EH1 2EN

Directors Sir David John KCMG, Chairman

Simon Lockett, Chief Executive

Tony Durrant, Finance Director

Robin Allan, Director of Business Development

Neil Hawkings, Operations Director

John Orange, Senior Independent Non-Executive Director

Michel Romieu, Independent Non-Executive Director

David Lindsell, Independent Non-Executive Director

Professor Dr. David Roberts, Independent Non-Executive Director

Joe Darby, Independent Non-Executive Director

Company Secretary Stephen Huddle

Financial Adviser Deutsche Bank AG

Winchester House

1 Great Winchester Street

London EC2N 2DB

Global Co-ordinator, Joint Sponsor,

Joint Bookrunner, Underwriter and

Joint Broker

Deutsche Bank AG

Winchester House

1 Great Winchester Street

London EC2N 2DB

Joint Sponsor, Joint Broker, Co-

Lead Manager and Underwriter

Oriel Securities Limited

125 Wood Street

London EC2V 7AN

Joint Bookrunners and Underwriters Barclays Bank PLC

5 The North Colonnade

Canary Wharf

London E14 4BB

HSBC Bank plc

8 Canada Square

London E14 5HQ

Royal Bank of Canada Europe Limited

71 Queen Victoria Street

London EC4V 4DE

Solicitors to the Joint Sponsors and

Underwriters

Clifford Chance LLP

10 Upper Bank Street

London E14 5JJ

Registrar and Receiving Agent Capita Registrars Limited

The Registry

34 Beckenham RoadBeckenham

Kent BR3 4TU

Auditors and Reporting Accountants Deloitte LLP

2 New Street Square

London EC4A 3BZ