pradeep dubey 20

Post on 13-Sep-2014

1.491 views

DESCRIPTION

TRANSCRIPT

A SUMMER TRAINING REPORT

On“Market Segmentation in Sbi life Insurance”

At SBI Life Insurance Co Limited

Alakhnanda Tower 3rd Floor, City Centre, Gwalior (M.P)

Submitted ToJiwaji University

Gwalior For the partial fulfillment of the award of

Master of Business Administration (2011-2013)

Submitted By(Pradeep Dubey)

Prestige Institute of ManagementOpposite Deen Dayal Nagar, Bhind Road, Gwalior

Ph.0751-2470724, Fax-0751-470516Website: prestigegwl.org

1

DECLARATION

I am Pradeep Dubey, student of MBA IInd semester of Prestige Institute of

Management Gwalior; hereby declare that the Summer Training Report

entitled “Marketing Strategies Activity In Sbi life Insurance” in Gwalior

(M.P) is submitted by me in partial fulfillment of the requirement for the Master

of Business Administration Degree.

I assure that this summer training report is the result of my own efforts and that

any other institute for the award of any degree or diploma has not submitted it.

Place: Pradeep Dubey

Date: MBA-IInd sem.

2

Preface

Now days in this dynamic era Insurance is coming as an important tool for

reducing the effect of uncertainty and risks. It becomes an integral part and

indispensable part of human life. There are various types of Insurance Plans

to provide protection from loss and uncertainties.

So is a great opportunity for me to study on “People’s Perception and

awareness are concerning “Marketing Strategies Activity In Sbi Life

Insurance” in Gwalior (M.P). The purpose of this research is to know

awareness and importance among peoples regarding “Marketing Strategies

Activity in Sbi Life Insurance” in Gwalior (M.P)

.

Pradeep Dubey

M.B.A IInd sem

3

CERTIFICATE

This is to certify that Pradeep Dubey Student of MBA IInd Sem of Prestige

Institute Of management Gwalior, has successfully completed his Summer

training report. He has prepared this report entitled “Marketing Strategies

Activity In Sbi Life Insurance” under my direct supervision and guidance.

Prof. C K Dantre

(Faculty Guide PIMG)

4

ACKNOLEDGEMENT

Summer Training Report is a combined effort including this one also, so I

would like to thank to all who have helped me completion of this report

purposeful.

We would like to extend our heartfelt gratitude to Prof. Ashish Mehra for his

guidance throughout the project. Without his support and cooperation we would

have failed in our endeavors and targets in this project.

I also want to thank to Mr. Yog Mishra, Unit Manager in SBI LIFE Insurance

Co.Ltd. (Sales Dept.), Prof. C K Dantre my mentor and, coordinator assisting

me in completion of this project.

Further I would like to thanks to all of my Teachers, Staff Members, Library

Members, and Friends for their valuable support and advices which helps me a

lot to completing this project report purposeful.

Pradeep Dubey

M.B.A IInd sem

5

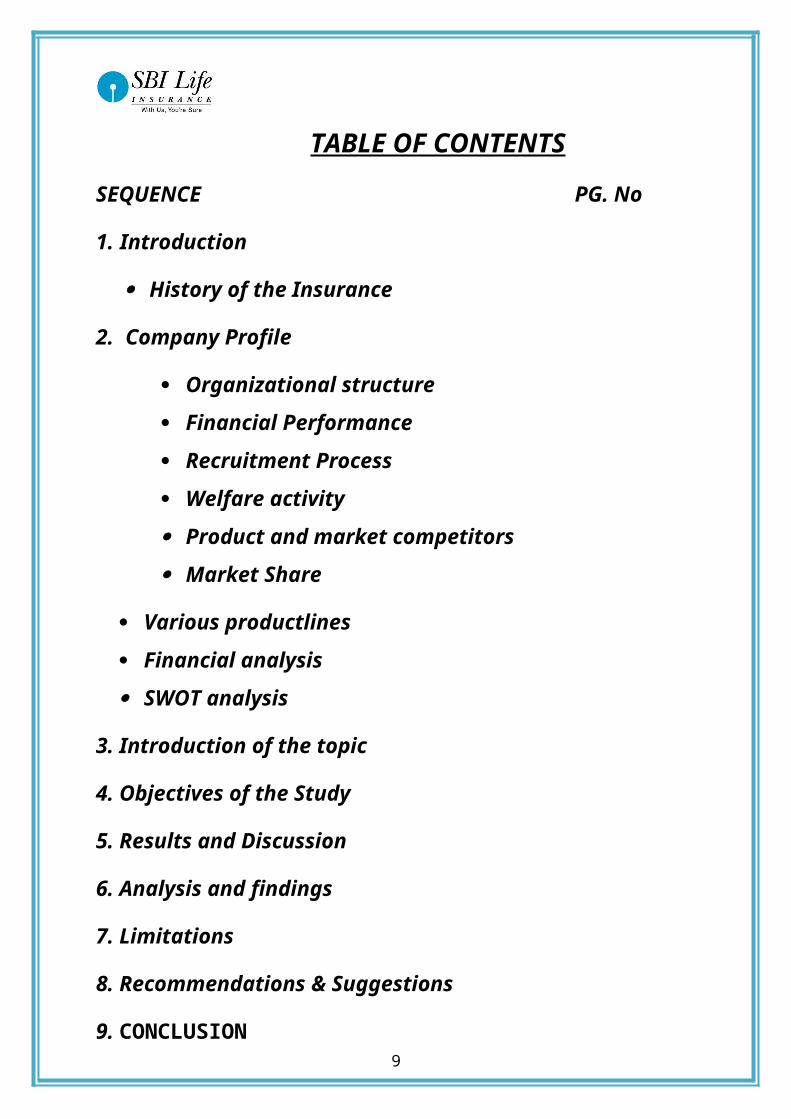

TABLE OF CONTENTS

SEQUENCE PG. No

1. Introduction

History of the Insurance

2. Company Profile

Organizational structure Financial Performance Recruitment Process Welfare activity Product and market competitors Market Share

Various productlines Financial analysis SWOT analysis

3. Introduction of the topic

4. Objectives of the Study

5. Results and Discussion

6. Analysis and findings

7. Limitations

8. Recommendations & Suggestions

9. CONCLUSION

Reference Annexure

6

History of Insurance: at a glance

Life Insurance in its modern form came to India from England in the year 1818. Oriental ife

Insurance Company started by Europeans in Calcutta was the first life insurance company on

Indian Soil. All the insurance companies established during that period were brought up with

the purpose of looking after the needs of European community and Indian natives were not

being insured by these companies. However, later with the efforts of eminent people like

Babu Muttylal Seal, the foreign life insurance companies started insuring Indian lives. But

Indian lives were being treated as sub-standard lives and heavy extra premiums were being

charged on them. Bombay Mutual Life Assurance Society heralded the birth of first Indian

life insurance company in the year 1870, and covered Indian lives at normal rates. Starting as

Indian enterprise with highly patriotic motives, insurance companies came into existence to

carry the message of insurance and social security through insurance to various sectors of

society. Bharat Insurance Company (1896) was also one of such companies inspired by

nationalism. The Swadeshi movement of 1905-1907 gave rise to more insurance companies.

The United India in Madras, National Indian and National Insurance in Calcutta and the Co-

operative Assurance at Lahore were established in 1906. In 1907, Hindustan Co-operative

Insurance Company took its birth in one of the rooms of the Jorasanko, house of the great

poet Rabindranath Tagore, in Calcutta. The Indian Mercantile, General Assurance and

Swadeshi Life (later Bombay Life) were some of the companies established during the same

period. Prior to 1912 India had no legislation to regulate insurance business. In the year 1912,

the Life Insurance Companies Act, and the Provident Fund Act were passed. The Life

Insurance Companies Act, 1912 made it necessary that the premium rate tables and periodical

valuations of companies should be certified by an actuary. But the Act discriminated between

foreign and Indian companies on many accounts, putting the Indian companies at a

disadvantage. The first two decades of the twentieth century saw lot of growth in insurance

business. From 44 companies with total business-in-force as Rs.22.44 crore, it rose to 176

companies with total business-in-force as Rs.298 crore in 1938. During the mushrooming of

insurance companies many financially unsound concerns were also floated which failed

miserably. The Insurance Act 1938 was the first legislation governing not only life insurance

but also non-life insurance to provide strict state control over insurance business. The demand

for nationalization of life insurance industry was made repeatedly in the past but it gathered

7

momentum in 1944 when a bill to amend the Life Insurance Act 1938 was introduced in the

Legislative Assembly. However, it was much later on the 19th of January, 1956, that life

insurance in India was nationalized. About 154 Indian insurance companies, 16 non-Indian

companies and 75 provident were operating in India at the time of nationalization.

Nationalization was accomplished in two stages; initially the management of the companies

was taken over by means of an Ordinance, and later, the ownership too by means of a

comprehensive bill. The Parliament of India passed the Life Insurance Corporation Act on the

19th of June 1956, and the Life Insurance Corporation of India was created on 1st September,

1956, with the objective of spreading life insurance much more widely and in particular to the

rural areas with a view to reach all insurable persons in the country, providing them adequate

financial cover at a reasonable cost.

Some of the important milestones in the life insurance Businesses in India are:

1818: Oriental Life Insurance Company, the first life insurance company on Indian soil

started functioning.

1870: Bombay Mutual Life Assurance Society, the first Indian life insurance company started

its business.

1912: The Indian Life Assurance Companies Act enacted as the first statute to regulate the

life insurance business.

1928: The Indian Insurance Companies Act enacted to enable the government to collect

statistical information about both life and non-life insurance businesses.

1938: Earlier legislation consolidated and amended to by the Insurance Act with the objective

of protecting the interests of the insuring public.

1956: 245 Indian and foreign insurers and provident societies are taken over by the central

government and nationalized. LIC formed by an Act of Parliament, viz. LIC Act, 1956, with

a capital contribution of Rs. 5 crore from the Government of India.

The General insurance business in India, on the other hand, can trace its roots to the Triton

Insurance Company Ltd., the first general insurance company established in the year 1850 in

Calcutta by the British.

8

Some of the important milestones in the general insurance Businesses in India are : 1907: The Indian Mercantile Insurance Ltd. set up, the first company to transact all classes of

general insurance business.

1957: General Insurance Council, a wing of the Insurance Association of India, frames a code

of conduct for ensuring fair conduct and sound business practices.

1968: The Insurance Act amended to regulate investments and set minimum solvency

margins and the Tariff Advisory Committee set up.

1972: The General Insurance Business (Nationalization) Act, 1972 nationalized the general

insurance business in India with effect from 1st January 1973

107 insurers amalgamated and grouped into four companies’ viz. the National Insurance

Company Ltd., the New India Assurance Company Ltd., the Oriental Insurance Company

Ltd. and the United India Insurance Company Ltd. GIC incorporated as a company.

Indian Insurance industry:

Indian Insurance comprised mainly two Players.

Life Insurer: the important are.

Life Insurance Corporation of India (LIC)

HDFC Standard Life Insurance Company Ltd.

Max New York Life Insurance Co. Ltd.

ICICI Prudential Life Insurance Company Ltd.

Kodak Mahindra Old Mutual Life Insurance Limited.

Birla Sun Life Insurance Company Ltd.

Tata AIG Life Insurance Company Ltd.

SBI Life Insurance Company Limited.

ING Vysya Life Insurance Company Private Limited.

Bajaj Allianz Life Insurance Company Limited.

9

MetLife India Insurance Company Pvt. Ltd.

Sahara India Insurance Company Ltd.

Aviva Life Insurance Co. India Pvt. Ltd.

General InsurerGeneral Insurance Corporation of India (GIC) GIC has four subsidiary companies namely:

The Oriental Insurance Company Limited.

The New India Assurance Company Limited.

National Insurance Company Limited.

United India Insurance Company Limited.

Royal Sundaram Alliance Insurance Company Limited.

Reliance General Insurance Company Limited.

TATA AIG General Insurance Company Ltd.

Bajaj Allianz General Insurance Company Limited

ICICI Lombard General Insurance Company Limited.

Cholamandalam General Insurance Company Ltd.

HDFC-Chubb General Insurance Co. Ltd.

10

Introduction

SBI LIFE – a joint venture between

74% 26%

SBI Life Insurance is a joint venture between the State Bank of India and Cardiff SA of

France. SBI Life Insurance is registered with an authorized capital of Rs 1000 core and a paid

up capital of Rs 350 carore. SBI owns 74% of the total capital and Cardiff the remaining 26%

State Bank of India enjoys the largest banking franchise in India. Along with its 7 Associate

Banks, SBI Group has the unrivalled strength of over 14,000 branches across the country, the

largest in the world. Cardif is a wholly owned subsidiary of BNP Paribas, which is The Euro

Zone’s leading Bank. BNP is one of the oldest foreign banks with a presence in India dating

back to 1860. It has 9 branches in the metros and other major towns in the country. Cardif is a

vibrant insurance company specializing in personal lines such as long-term savings, rotection

products and creditor insurance. Cardif has also been a pioneer in the art of selling insurance

products through commercial banks in France and 29 more countries.SBI Life Insurance’s

mission is to emerge as the leading company offering a comprehensive range of Life

Insurance and pension products at competitive prices, ensuring high standards of customer

ervice and world class operating efficiency. The company plans to make the insurance buying

process quick, simple and based on well-informed judgment. In 2004, SBI Life Insurance

became the first company amongst private insurance players to cover 30 lacks lives. The

company expects to carve a niche in the Indian insurance market through extensive product

innovation and aims to provide the highest standards of customer service through a

technological interface. To facilitate this, call centers have been already installed and help

lines will be installed and customers will have access to their accounts through the Internet or

through SBI branches. The company proposes to make available ready liquidity to its Life

Insurance policies by way of loans at SBI counters. This will make Life Insurance a liquid

asset in the financial portfolio of households. SBI Life Insurance is uniquely placed as a

11

pioneer to usher bank assurance into India. The company hopes to extensively utilize the SBI

Group as a platform for cross-selling insurance products along with its numerous banking

product packages such as housing loans, personal loans and credit cards. SBI’s access to over

100 million accounts provides a vibrant base to build insurance selling across every region

and economic strata in the country.

Group Corporate.

SBI Life extensively leverages the SBI Group as a platform for cross-selling insurance

products along with its numerous banking product packages such as housing loans and

personal loans. SBI’s access to over 100 million accounts across the country provides a

vibrant base for insurance penetration across every region and economic strata in the country

ensuring true financial inclusion.

12

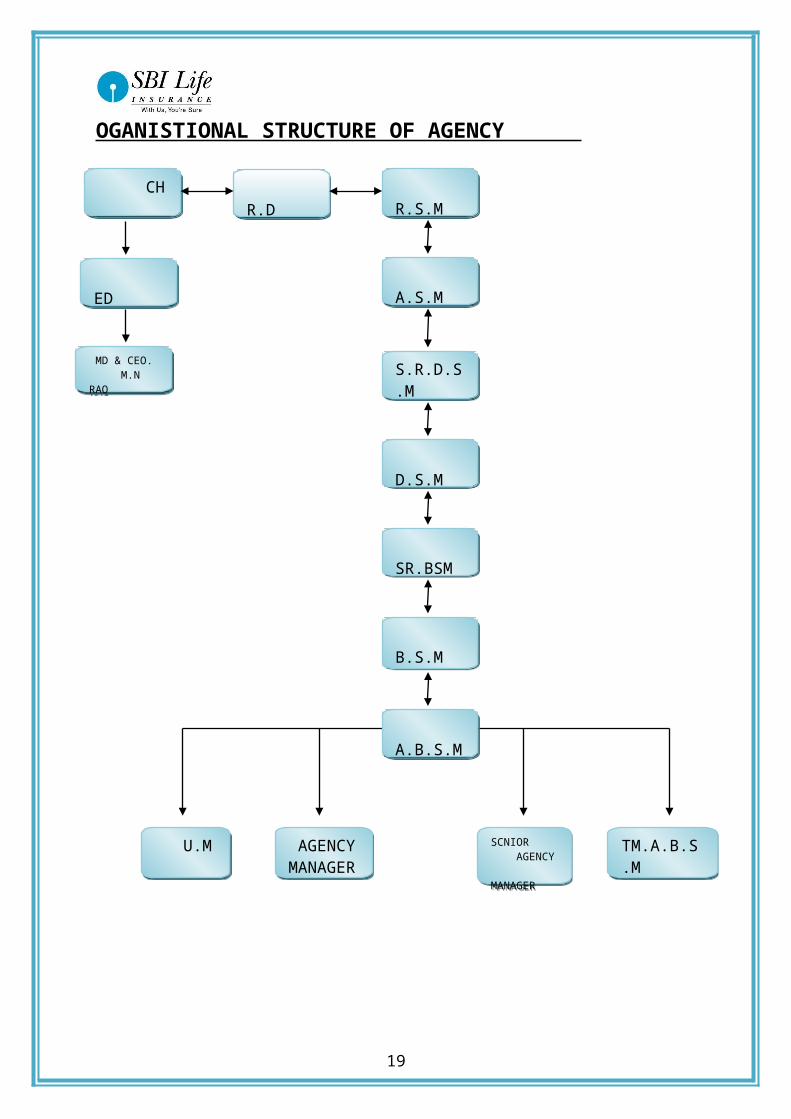

OGANISTIONAL STRUCTURE OF AGENCY

13

U.M AGENCY MANAGER

SCNIOR AGENCY MANAGER

TM.A.B.S.M

A.B.S.M

B.S.M

SR.BSM

R.S.M

A.S.M

D.S.M

S.R.D.S.M

MD & CEO. M.N RAO

ED

R.D CH

Management Style

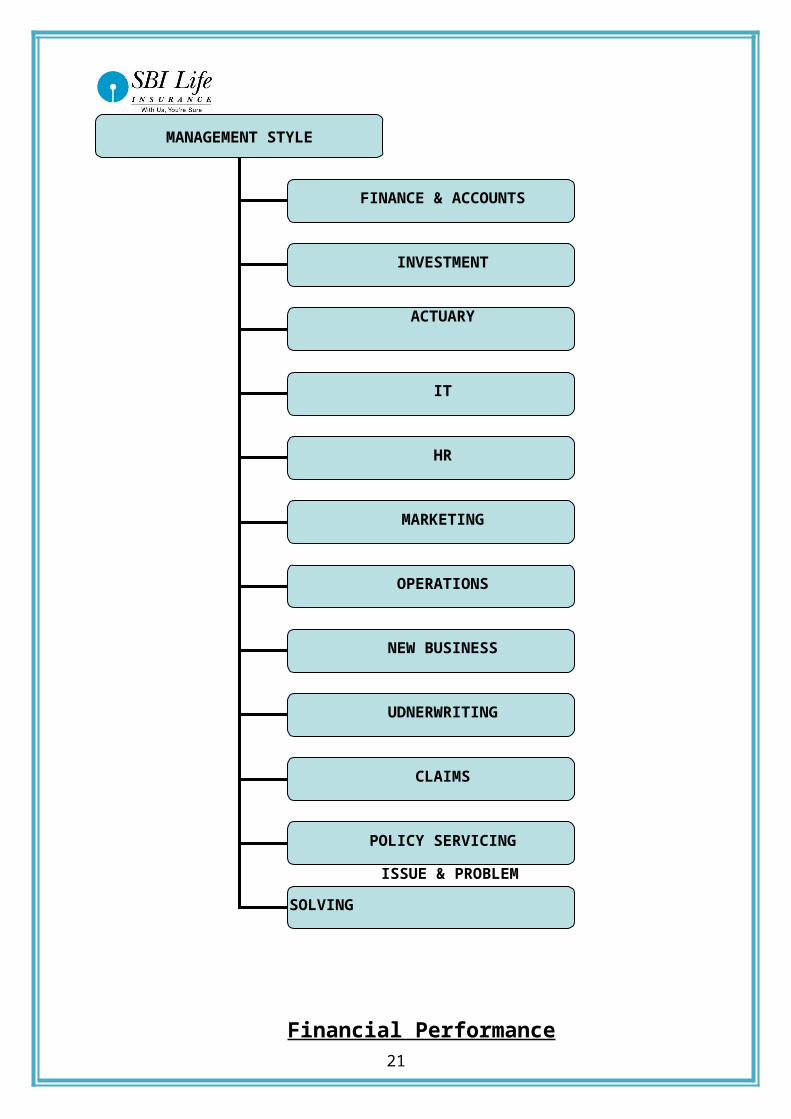

MANAGEMENT STYLE

FINANCE & ACCOUNTS

INVESTMENT

ACTUARY

IT

HR

MARKETING

OPERATIONS

NEW BUSINESS

UDNERWRITING

CLAIMS

POLICY SERVICING

ISSUE & PROBLEM SOLVING

14

Financial Performance

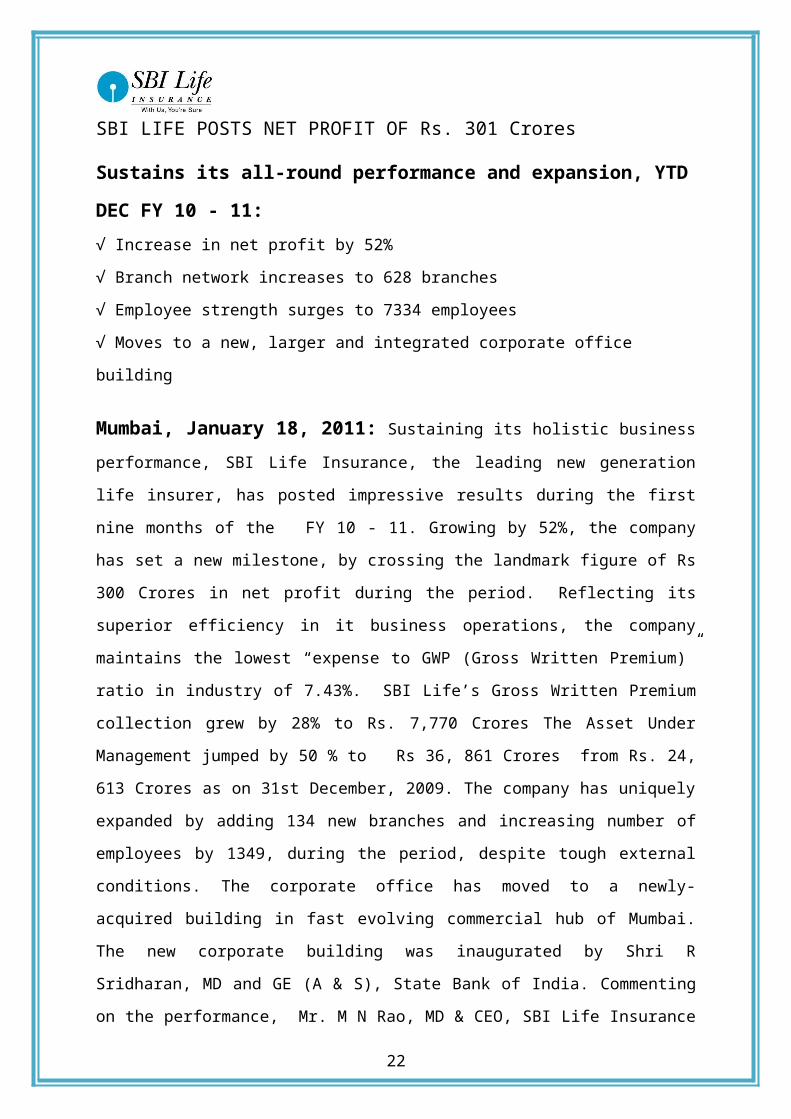

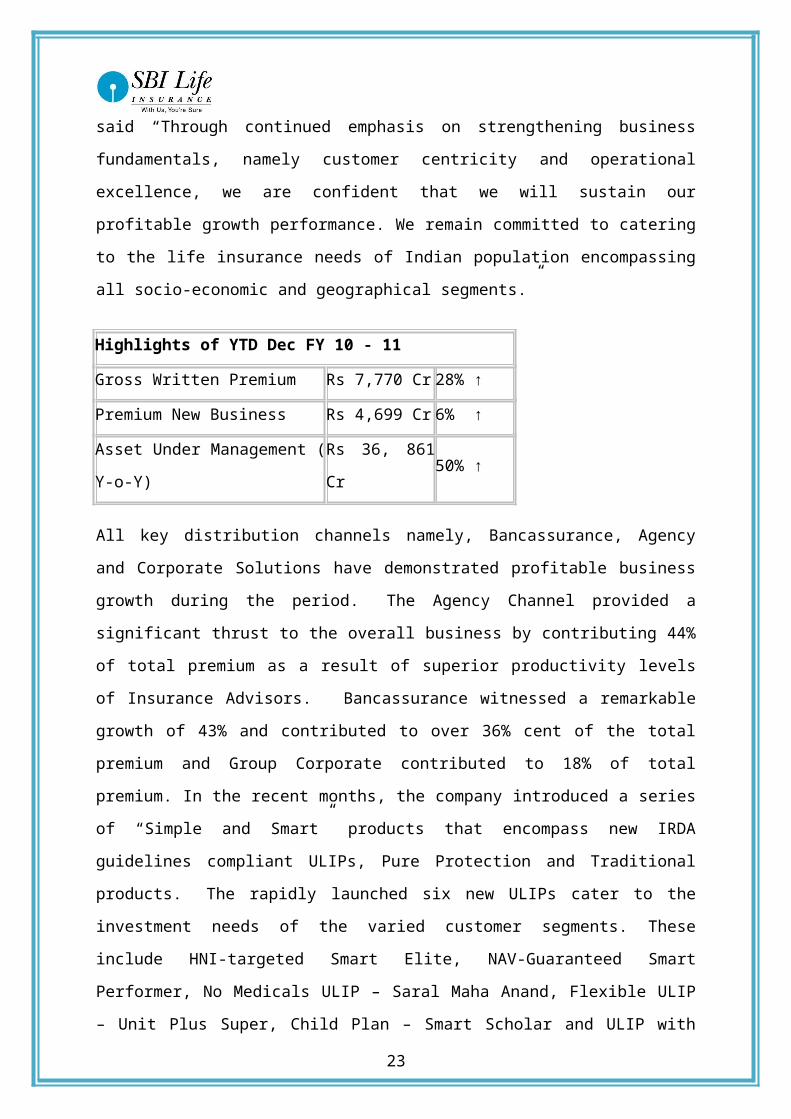

SBI LIFE POSTS NET PROFIT OF Rs. 301 Crores

Sustains its all-round performance and expansion, YTD DEC FY 10 - 11:√ Increase in net profit by 52%

√ Branch network increases to 628 branches

√ Employee strength surges to 7334 employees

√ Moves to a new, larger and integrated corporate office building

Mumbai, January 18, 2011: Sustaining its holistic business performance, SBI Life

Insurance, the leading new generation life insurer, has posted impressive results during the

first nine months of the FY 10 - 11. Growing by 52%, the company has set a new milestone,

by crossing the landmark figure of Rs 300 Crores in net profit during the period. Reflecting

its superior efficiency in it business operations, the company maintains the lowest “expense

to GWP (Gross Written Premium)” ratio in industry of 7.43%. SBI Life’s Gross Written

Premium collection grew by 28% to Rs. 7,770 Crores The Asset Under Management jumped

by 50 % to Rs 36, 861 Crores from Rs. 24, 613 Crores as on 31st December, 2009. The

company has uniquely expanded by adding 134 new branches and increasing number of

employees by 1349, during the period, despite tough external conditions. The corporate office

has moved to a newly- acquired building in fast evolving commercial hub of Mumbai. The

new corporate building was inaugurated by Shri R Sridharan, MD and GE (A & S), State

Bank of India. Commenting on the performance, Mr. M N Rao, MD & CEO, SBI Life

Insurance said “Through continued emphasis on strengthening business fundamentals,

namely customer centricity and operational excellence, we are confident that we will sustain

our profitable growth performance. We remain committed to catering to the life insurance

needs of Indian population encompassing all socio-economic and geographical segments.”

Highlights of YTD Dec FY 10 - 11

Gross Written Premium Rs 7,770 Cr 28% ↑

Premium New Business Rs 4,699 Cr 6% ↑

Asset Under Management ( Y-o-Y) Rs 36, 861 Cr 50% ↑

All key distribution channels namely, Bancassurance, Agency and Corporate Solutions have

demonstrated profitable business growth during the period. The Agency Channel provided a

15

significant thrust to the overall business by contributing 44% of total premium as a result of

superior productivity levels of Insurance Advisors. Bancassurance witnessed a remarkable

growth of 43% and contributed to over 36% cent of the total premium and Group Corporate

contributed to 18% of total premium. In the recent months, the company introduced a series

of “Simple and Smart” products that encompass new IRDA guidelines compliant ULIPs,

Pure Protection and Traditional products. The rapidly launched six new ULIPs cater to the

investment needs of the varied customer segments. These include HNI-targeted Smart Elite,

NAV-Guaranteed Smart Performer, No Medicals ULIP – Saral Maha Anand, Flexible ULIP

– Unit Plus Super, Child Plan – Smart Scholar and ULIP with Automatic Asset Allocation –

Smart Horizon. Innovatively-featured, non-ULIPs rolled out are No-Medicals, pure

protection plan – Saral Shield, HNI targeted, pure protection plan – Smart Shield and No

Medicals, traditional savings plan – Saral. One of the highlights towards achieving customer

service excellence has been the national launch of customer care initiative ‘SMS SOLVE”. A

first-of-its kind in the life insurance industry, the service allows customers to have their

grievances resolved in a simpler, paperless and faster manner. An innovative SMS-based

service, SMS SOLVE provides customers the ease of accessing SBI Life 24 X 7. Customers

are able to register their grievances about SBI Life’s service by merely sending SMS

‘SOLVE’ to 56161. Testifying its multi-dimensional excellence, the company has bagged

numerous recognitions and awards recently. Being adjudged the best, SBI Life’s annual

report has won Gold Shield from Institute of Charted Accountants of India (ICAI) for

excellence in Financial Reporting. Also, International Certification Services (ICS) has

awarded SBI Life "ICS Quality Champion Award - 2010" for continual improvement in the

Quality Process. NDTV Profit Business Leadership award and Best Life Insurer 2010,

Runner Up, award by Outlook Money are the other key media recognitions that have been

conferred to SBI Life. Retaining the ISO 9001:2000 Certification for superior claim process,

globally topping the prestigious international MDRT Table and reaffirmation of CRISIL

“AAA/Stable” rating are other key distinctions achieved by the company during initial

current financial year. As per the latest IRDA report, as of November 2010, the company has

a market share of 18.27% among private life insurers and a total market share of 5.10 %.

16

Management Philosophy

Vision : "To be the most trusted and preferred life insurance provider "

Mission"To emerge as the leading company offering a comprehensive range of life insurance and

pension products at competitive prices, ensuring high standards of customer satisfaction and

world class operating efficiency, and become a model life insurance company in India in the

post liberalization period".

Values • Trustworthiness

• Ambition

• Innovation

• Dynamism

• Excellence

17

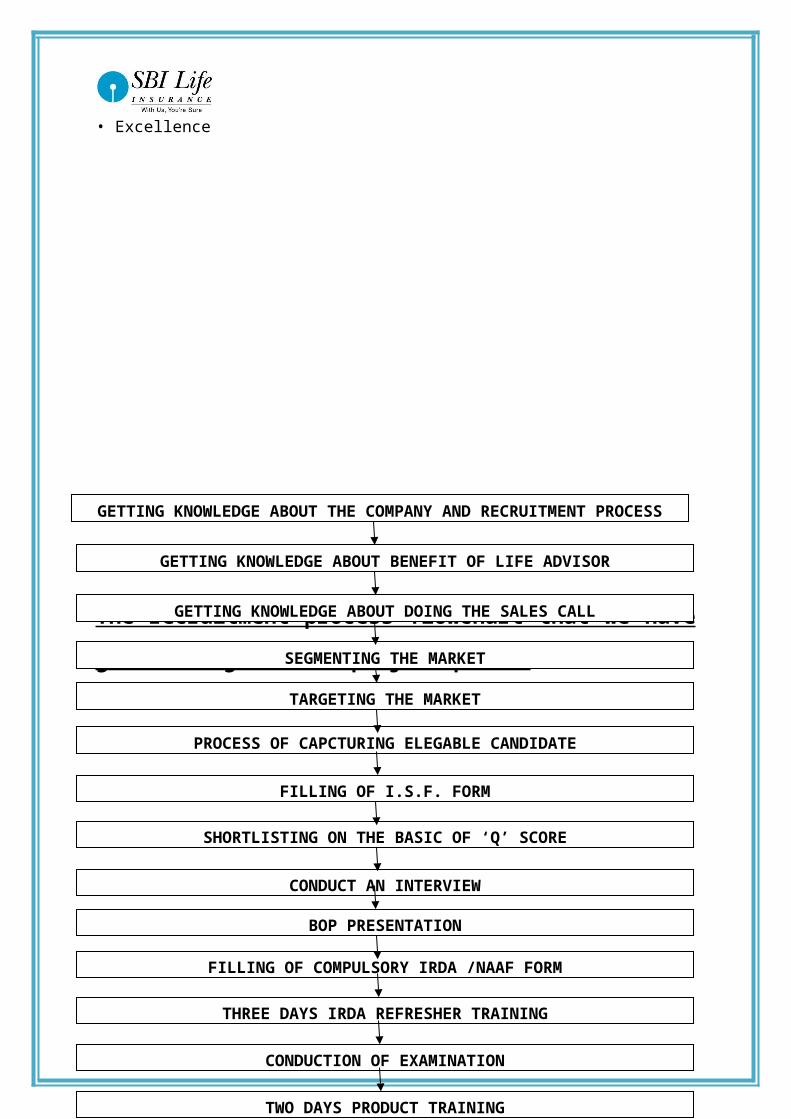

The recruitment process flowchart that we have gone through in

our project period

18

GETTING KNOWLEDGE ABOUT THE COMPANY AND RECRUITMENT PROCESS

GETTING KNOWLEDGE ABOUT BENEFIT OF LIFE ADVISOR

CONDUCTION OF EXAMINATION

TWO DAYS PRODUCT TRAINING

PROCESS OF CAPCTURING ELEGABLE CANDIDATE

THREE DAYS IRDA REFRESHER TRAINING

CONDUCT AN INTERVIEW

BOP PRESENTATION

FILLING OF COMPULSORY IRDA /NAAF FORM

FILLING OF I.S.F. FORM

SHORTLISTING ON THE BASIC OF ‘Q’ SCORE

TARGETING THE MARKET

SEGMENTING THE MARKET

GETTING KNOWLEDGE ABOUT DOING THE SALES CALL

Welfare Activities

Gift Drishti

One of our corporate ethos, enhancing our SBI Life brand value, is about

giving back to the society. In line with our Corporate Social Responsibility

(CSR) initiatives, the cause of supporting our Elderly Citizens was initiated.

Incidence of cataract blindness, annually at 3.28 million, is one of the most

prevalent health ailments suffered by old people, particularly in rural pockets of our country.

On the occasion of World Elder's Day on 1st October, CSR initiative - "Gift Drishti"

(Restoring vision) was launched in partnership with HelpAge India, a registered national

level voluntary body, working for the cause of disadvantaged aged persons. Restoring vision

is done through Intra Ocular Surgery (IOL). SBI Life employees made monetary

contributions to the cause. SBI Life donated twice the sum contributed by its employees. Eye

sight for thousands of elderly citizens was restored across the rural parts of the country.

Gift Drishti Camps

19

Read India Pledge

SBI Life undertook the Corporate Social Responsibility (CSR) initiative,

aimed at driving the cause to make children read and write. The campaign,

"Read India Pledge" sensitized general public towards the cause and urged

them to pledge & support the cause monetarily or by devoting time.The

campaign was partnered by Pratham, one of the leading child-cause related NGOs and Radio

Mirchi, a leading radio station.

Read India Camps

20

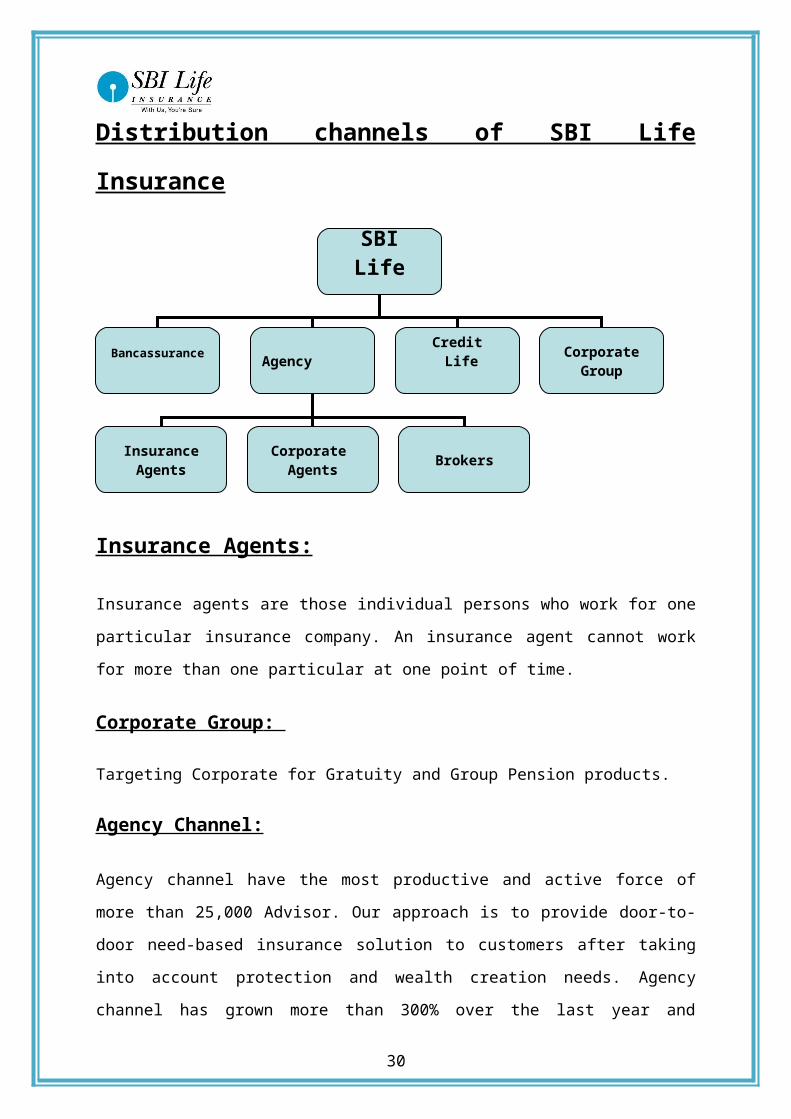

Distribution channels of SBI Life Insurance

Insurance Agents:

Insurance agents are those individual persons who work for one particular insurance

company. An insurance agent cannot work for more than one particular at one point of time.

Corporate Group :

Targeting Corporate for Gratuity and Group Pension products.

Agency Channel:

Agency channel have the most productive and active force of more than 25,000 Advisor. Our

approach is to provide door-to-door need-based insurance solution to customers after taking

into account protection and wealth creation needs. Agency channel has grown more than

300% over the last year and contributed more than 45% to the company’s new business

premium collection.

SBI Life

Bancassurance Agency Credit Life

Insurance Agents Corporate Agents Brokers

Corporate Group

21

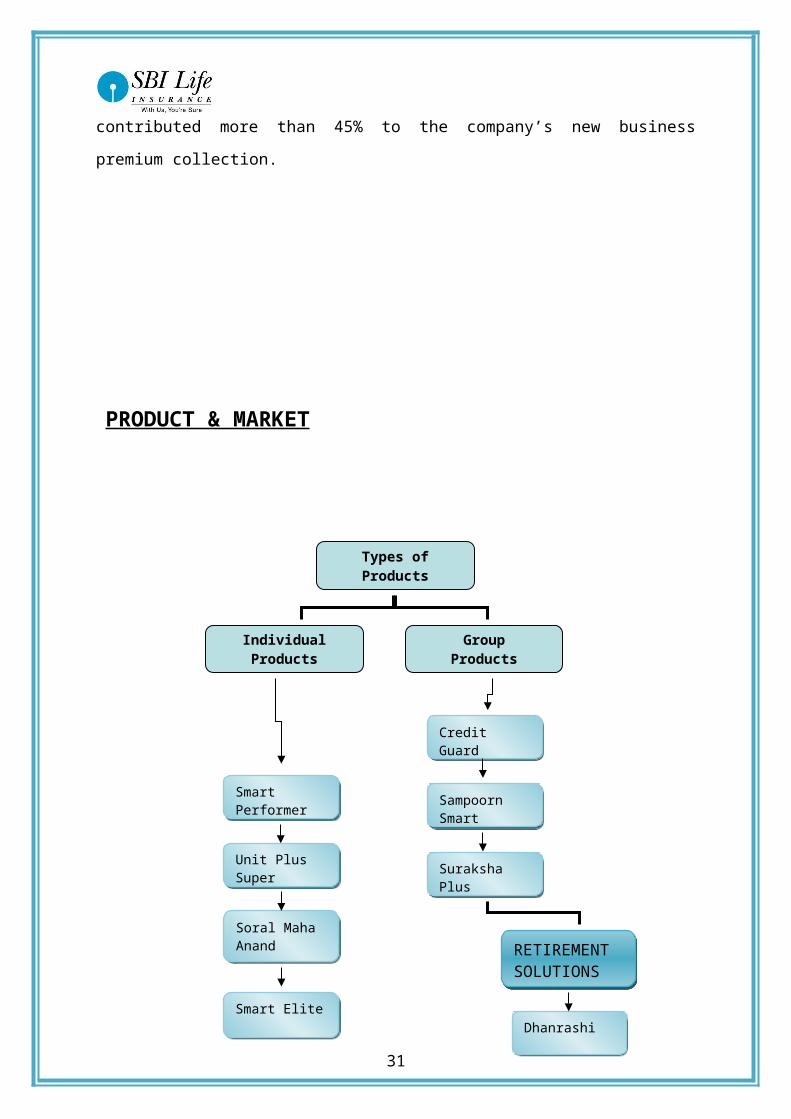

PRODUCT & MARKET

22

Types of Products

IndividualProducts

GroupProducts

RETIREMENT SOLUTIONS

Smart Performer

Unit Plus Super

Soral Maha Anand

Smart Elite

Smart Scholar

Smart Horizon

Credit Guard

Smart Weath Assare

Swarna Ganga

Dhanrashi

Swarna Jeevan

Cap Assure

Suraksha Plus

Sampoorn Smart

PROCESS OF INSURANCE OPERATION

A Without prejudice to the other express terms and conditions of this Agreement and all and

any implied rights of SBI Life Life Insurance after the termination of this Agreement, the

Advisor shall not:

Use for his own benefit or the benefit of any other person; or

Disclose to any person;

Through any failure to exercise all due care and diligence, cause or permit any

unauthorized disclosure of any trade secrets or confidential information of or relating to

SBI Life Life Insurance which he may have received, used or obtained during the term

of this Agreement. Any such trade secrets and confidential information shall at all times

remain the property of SBI Life Life Insurance.

a. For the purposes of this clause, trade secrets and/or confidential information shall

include, but not be limited to, lists of and information concerning customers,

Policyholders, employees, Advisors and agency managers of SBI Life life Insurance,

information relating to the working of any product, process, invention, improvement

or development carried on or used by SBI Life Life Insurance, information relating to

research projects, know-how, prices, rates, discounts, mark-ups, business strategies,

marketing, tenders and any price sensitive information concerning SBI Life Life

Insurance. For the avoidance of doubt, the obligation of confidentiality in this clause

extends to trade secrets and confidential information howsoever stored, whether in

hard copy documents, records or computer programs.

b. Access to SBI Life Life Insurance computer resources, electronic data and the like

may be given to and shall be utilized by the Advisor only for the purpose of carrying

out the duties embodied in the Agreement.

c. The forgoing provisions on confidentiality and non-disclosure also apply to

employees of both the parties to this Agreement and the sad parties assume liability

for the breach or violation in any manner by their employees.

23

SALES & MARKETING

Key Milestones

Financial Year 11-12: Awarded the most coveted NDTV Profit Business Leadership Award, twice in a row, 2010 &

2011.Awarded ‘Most Trusted Life Insurance Brand - II By The Economic Times, Brand

Equity and Nielsen, Most Trusted Brands 2011.

Globally topped the prestigious Million Dollar Round Table (MDRT) for having the aximum

number of MDRT members, for three years consecutively.

CRISIL reaffirmed its AAA / Stable rating to SBI Life, indicating highest financial strength

to meet policyholder obligations.

ICRA reaffirmed its iAAA rating indicating highest claims paying ability and a

fundamentally strong position.

Won one of the most prestigious quality distinction, IMC Ramkrishna Bajaj

National Quality Awards 2011- "Certificate of Merit"

Awarded Silver Shield by ICAI for Excellence in Financial Reporting for FY 2010

– 11 under the Insurance category

Won ‘Best Presented Accounts Award‘by The South Asian Federation of

Accountants (SAFA), in the Insurance Category for the Annual Report FY 2009-

10.

Financial Year 10-11:

SBI Life won the coveted Bloomberg UTV Financial Leadership Award 2011 - "Life

Insurer of the year".

Won the most coveted NDTV Profit Business Leadership Award 2010.

Globally topped the prestigious Million Dollar Round Table (MDRT) 2010 for having the

maximum number of MDRT members. Awarded the Gold Shield by Institute of Chartered

Accountants of India (ICAI) for Excellence in Financial Reporting. Won the ‘ICS Quality

24

Champion Award 2010’ for Continual Quality Improvement. Adjudged Best Life Insurer

2010 - Runner Up by Outlook Money

Launched an innovative customer care initiative - SMS ‘SOLVE’ for prompt

Grievance Redressal.

Appraised at Maturity level 3 of Capability Maturity Model Integration (CMMI)

Version 1.2 for its ISG Division.

ICRA reaffirmed ’iAAA’ rating to SBI Life, indicating highest claims paying ability and

meeting policyholders obligations.

CRISIL, country’s leading rating agency, reaffirmed its highest financial rating AAA/Stable

to SBI Life.

Financial Year 09-10:

Reported a robust Net Profit of Rs.276 Crores.

Crossed Rs.10,000 Crores in Gross Written Premium (GWP).

Ranked No.1, in New Business Premium, amongst private life insurance companies.

Assets under Management (AUM) grew by 96% to Rs.28, 551 Crores.

Globally topped the prestigious MDRT 2009 for having Maximum number of MDRT

Members.

ICRA reaffirmed iAAA rating to SBI Life indicating highest claims paying ability.

Awarded ISO Certification (ISO/IEC 27001:2005) for Information Security

Management System (ISMS).

Retained ISO 9001:2000 certificate for superior claim settlement process.

Financial Year 08-09:

Ranked among global top three in terms of number of Million Dollar Round Table

(MDRT) members.

Bagged the coveted personal finance award-Outlook Money NDTV Profit "Best Life

Insurer 2008".

CRISIL, country’s leading rating agency, reaffirmed its highest financial rating

AAA/Stable to SBI

Life. In 2007, SBI Life became the first life insurer in India to receive this rating from

CRISIL.

ICRA assigned iAAA rating indicating highest claims paying ability to SBI Life

Insurance

25

Retained ISO 9001:2000 certificate for superior claim settlement process.

Financial Year 07-08:

Ranked amongst global top five life insurance companies in the number of MDRT

members.

Rated as the ’The Most Trusted Private Life Insurer’ according to a survey conducted

by Brand quity in association with AC Nielsen ORG-MARG and the Economic Times

Intelligence Bureau.

Received the highest financial rating ’AAA’ from CRISIL.

Forayed into micro insurance with the launch of ’Grameen Shakti’ in Bhubaneshwar,

Orissa for the economically underprivileged sections of society.

Received ISO 9001: 2000 certification for superior claim settlement process.

Received CMMI Level 3 certification for IT processes and software development

capabilities.

Financial Year 06-07:

Second consecutive year of Profitability.

More than 6.40 Million lives covered Financial Year 05-06: Reported a robust net

profit of Rs. 2.02 Cr

MARKET SHARE 26

SBI LIFE LEADS GLOBALLY AT MILLION DOLLAR ROUND TABLE (MDRT) 2011

Mumbai, September 28, 2011 - SBI Life Insurance, the leading private life insurer, retains the

unique distinction of being the only Life Insurer from India, topping the prestigious Million

Dollar Round Table (MDRT) 2011 across the globe. For the third consecutive year, SBI Life

has reached the pinnacle of the international coveted league by having 2,661 MDRT

members in 2011. Amongst these, 200 have achieved Court of Table (COT) and 30 Top of

Table (TOT) membership statuses. SBI Life has been consistently featuring amongst the top

five insurers, worldwide, since last five years. Globally, the company ranked 5th in 2007, 3rd

in 2008, and 1st in 2009, 2010 and 2011. Reputation, standard of sales excellence and high

ethical standards are some of the key values that are associated with the MDRT brand. The

MDRT membership is an exclusive honor that is achieved by less than 1 percent of the

world's life insurance and financial services advisors. Life Insurance professionals aspire to

attain the privilege of being an MDRT member Mr. M. N. Rao, MD & CEO, SBI Life, said,

"Across the globe, both, Agent and Insurance Facilitator at bank, continue to be a reliable

source of personal financial advise. Our accomplishment on a global platform testifies the

professional approach followed by our distributors. We will continue to focus on equipping

them with relevant support to enable advisory-based delivery of life insurance solutions to

our customers." Mr. Rajiv Gupta, Executive Director, Marketing, SBI Life added "This

accomplishment resonates our commitment towards creating quality advisors who can be

looked upon as world-class benchmarks. Providing need based solutions, professional advice

and unmatched service will remain the focal delivery points for our Advisors ". An

opportunity to represent one of the most trusted brands in the country, superior training

program and attractive reward and recognition programmes are some of benefits availed by

SBI Life Insurance Advisors. Mr. Anand Pejawar, Executive Director, Marketing, SBI Life

added "In addition to highly productive Retail Agency Channel, our integrated bancassurance

approach continues to create value for Bank customers and Facilitators of our products. The

bank employee, involved in the sale of the insurance products, has rapidly evolved to deliver

holistic banking and insurance solutions to their customers making the bank truly a super

market for all financial requirements". During the first financial quarter ending June 2011,

SBI Life recorded a profit of Rs. 144 Crores, registering an impressive profit growth of 27%

over the corresponding period last year. The total premium of the company grew by 13 % to

Rs. 1935 Crores during the period. The new business premium collected, during the period,

stood at Rs. 892 Crores. Further, the Assets under Management grew by 33%, over the

corresponding period last year, to Rs. 40,070 Crore as on 30th June 2011. The company

27

continues to have the lowest expense to GWP (Gross Written Premium) ratio in industry of

10.14%. Uniquely, despite tough external conditions, SBI Life continues to expand its

presence. During the current financial year, the company has introduced 81 branches and

recruited 1657 employees. SBI Life ranks number one amongst private players, as per the

latest IRDA report, July 2011. The company has a market share of 21.6% among private life

insurers and a total market share of 6%.About MDRT: MDRT is an association of the world's

best life insurance sales (advisors) professionals. Founded in 1927, MDRT is an international,

independent association of nearly 36,000 of the world's leading life insurance and financial

services professionals from 76 nations and territories, representing over 450 companies.

MDRT members are recognized as skillful professionals who are considered to be among the

best in the industry, perform outstanding client service, and have achieved the highest

standard of sales excellence in the life insurance and financial services business.

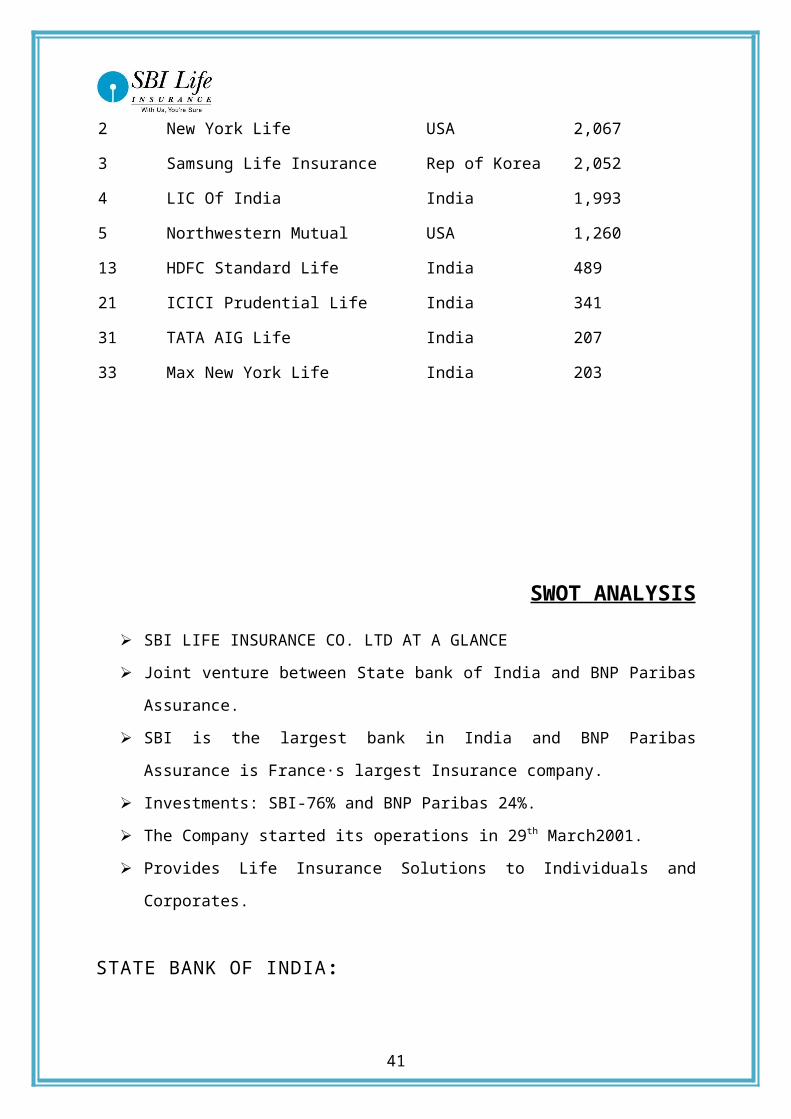

Rank Company Name Country 2010 Members

1 SBI Life Insurance India 2,661

2 New York Life USA 2,067

3 Samsung Life Insurance Rep of Korea 2,052

4 LIC Of India India 1,993

5 Northwestern Mutual USA 1,260

13 HDFC Standard Life India 489

21 ICICI Prudential Life India 341

31 TATA AIG Life India 207

33 Max New York Life India 203

SWOT ANALYSIS

SBI LIFE INSURANCE CO. LTD AT A GLANCE

Joint venture between State bank of India and BNP Paribas Assurance.

28

SBI is the largest bank in India and BNP Paribas Assurance is France·s largest

Insurance company.

Investments: SBI-76% and BNP Paribas 24%.

The Company started its operations in 29th March2001.

Provides Life Insurance Solutions to Individuals and Corporates.

STATE BANK OF INDIA: Largest and oldest banking franchise of India dating back to 1806 AD.

6 Associate Banks, 16000 Branches all over the country.

BNP PARIBAS ASSURANCE: 4thLargest Insurance Company in France.

The Insurance arm of BNP Paribas Bank, the largest bank of France.Operations in 41

countries around the world.

One of the oldest foreign banks with a presence in India dating back to1860 AD.

A worldwide leader in Creditor insurance products offering protection toover 50

million clients.

STRENGTHS

No.1 Private Life Insurance company in India (as on 2009-10).

Leverages the State Bank Group Relationship as a platform for cross-selling insurance

products.

As it sells its products through banc-assurance division of SBI,therefore less need on

spending money for establishing separate branch offices.

Market share of 18.34% among private life insurers and a total market share of

6.44%.

SBI·s access to over 100 million accounts across the country provides for a vibrant

base for insurance penetration in the country.

Growth at a rate of 40%.

IRDA has never banned any of SBI Life·s product.

Only private life insurance company to have posted profits (Rs 276 crores for they

earended March 31st, 2010) and declared bonus.

29

Solvency ratio of 2.2 and share capital of Rs.1000 Crore, SBI Life is one of the most

capita lefficient life insurance companies in the industry.

Continues to maintain the lowest´expense to GWP (Gross Written Premium)µ ratio in

industry of 6.5%

Globally topping the prestigious international MDR Table (Million DollarRound

Table ²30 Lacs collections by an agent in a year).

One of the market leaders in Unit Linked Plans by offering products asSmart ULIP,

UNIT +, UNIT +2, UNIT +3 etc.

Profitable business growth demonstrated by all key distribution channels.

Certifications of ISO 9001:2000, ISO 2700:2005 (Information security) AAA rating

by ICRA, CRISIL etc.

Superior Claims Settlement Process (certified by ISO 9001:2000).

Asset Under Management jumped by 96% to Rs 28,551 Crand New Business

Annualised Premium Equivalent (APE) by 37% to Rs.6, 358 Crores.

Restructured Customer Grievances Redressal Mechanism. Regional Directors and

Regional Channel Heads resolve customer complaints at local level.

Through ´My policy µ portal in www.sbilife.co.in,customers can view all policy

details including Payment Summary, Fund Value and Premium Calendar.

WEAKNESSES Less sales force than others (LIC·s 3 field advisor: SBI·s 1field advisor)

Low productivity of banc-assurance people.

People at top management/decision making level are from SBI. So,typical PSU

attitude in many aspects.

Hassle free online purchase of insurance policy is not available

Is less aggressive in generating business compared to other private life insurance

players.

Over dependence on the banc-assurance channels.

Less branch office compared to others.

OPPORTUNITIES

As only 12% of the 40 crores insurable population is insured, thus, a huge opportunity

to reach out to more people.

30

It has an edge over LIC as far as service is concerned. So, it can grab moremarket

share from LIC by giving it a tough competition.

Not so much requirement on establishment of Brand (already have a good brandimage

of SBI).

A huge revolutionary change (PARIBARTAN) in SBI is going to happen,so there is

an immense opportunity for SBI Life in future.

Huge market potentiality in Rural markets which has been untapped till now.

Higher market penetration by being more aggressive in banc-assurance channelof

distribution.

Huge opportunity to grab customers by being more active through otherdistribution

channels as mall-assurance, brokers etc..

Lower premium ULIP policy (<10000) can attract lower income segment market.

THREATS Huge competiti on from other pre-existing 22 players in the Life Insurance sector in

India.

ICICI Prudential, the market giantal ready pipped SBI Life to regaint opposition,

garnering new business worth Rs.303 crores (source Economic Times,26th May·10)

New entrants in the pipe line of the life insurance business.

New tie-ups of competitors with innovative distribution channels.The New Insurance

guidelines from September·10 onwards is really a big challenge or SBI Life·s bus

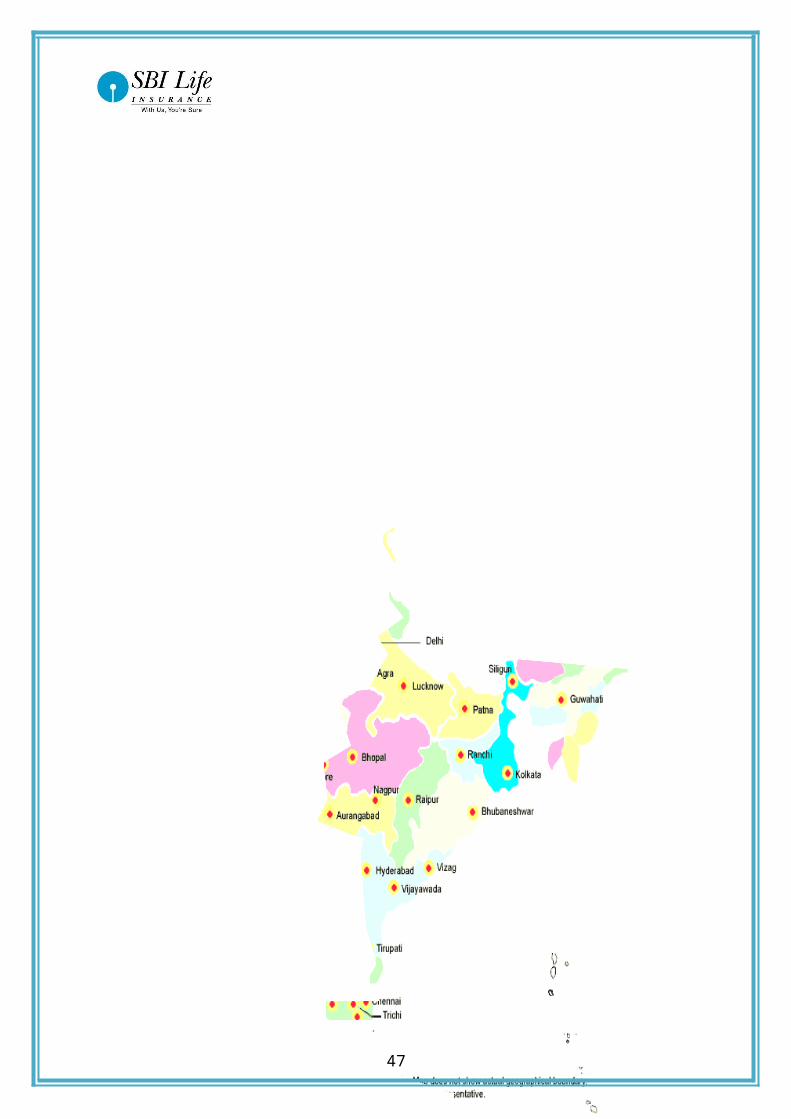

SBI LOCATION OF OFFICES:

SBI has a huge network of offices for providing service related to Insurance all overthe

country.

31

Location

Registered office:

SBI Life Insurance Co. Ltd. Central Processing Centre Kapas Bhawan, Sector 10, CBD

Belapur, Navi Mumbai 400614.Telephone No: 022-6645 6241

Email: [email protected]

Corporate Office:

SBI Life Insurance Co. Ltd, "Natraj", M.V. Road & Western Express Highway Junction,

Andheri (East), Mumbai - 400 069

Summer training office location

Branch office:

Sbi Life Insurance Co. Ltd. 3rd Floor, Alaknanda Tower, City Center.

474001. Gwalior (M.P) Tel.0 751- 4024 497

32

PROCESS OF CAREER GROWTH OF INSURANCE ADVISOR

As we were assigned to recruit life advisors, the very first thing that we required was

knowledge about benefits and opportunity because to motivate a prospective candidate to

33

become an Advisor, we need to convenience the Advisor about the opportunity and carrier

growth in SBI Life.

Benefit

Commission

Renewal Commission

Bonus

Quarterly gifts

ACER club membership facility

MDRT

Promotion factor for an agent

Domestic and International Conventions

Opportunity/

Advisor require no capital investment

They can chose there own working hour according to there convenience.

They are there own boss.

Unlimited earning potential

Represent a strong trusted brand.

OPPORTUNITY

Advisor requires no capital investment:- For starting any business we require a huge

infrastructure but here in SBI Life the Advisors do not require any capital investment other

than RS. 825 IRDA examination fees, which is very nominal and on return the Advisors get

free phone calling facility, Xerox facility etc. They can choose there own working hour

according to there convenience:- Advisor are free to work in there convenient hours because

the advisors working here comes from different profession like Doctor, Engineer, Student,

Medical Representative, contractor etc. They are there own boss:- There is no boss to give

you target rather you are your own boss and can work according to your pleasure and

earning requirement. Unlimited earning potential:- As the payment is made on commission

basis so there is no limit to earning. A person working hard can go to any limit with reward

and recognition in extra.

34

MARKETING STATEGIES & ACTIVITY

Marketing strategy consists of the analysis, strategy development, and implementation

activities in: “Developing a vision about the market(s) of interest to the organization,

selecting market target strategies, setting objectives, and developing, implementing, and

managing the marketing program positioning strategies designed to meet the value

35

requirements of the customers in each market target”. Strategic marketing is a market-driven

process of strategy development, taking into account a constantly changing business

environment and the need to deliver superior customer value. The focus of strategic

marketing is on organizational performance rather than a primary concern about increasing

sales. Marketing strategy seeks to deliver superior customer value by combining the

customer-influencing strategies of the business into a coordinated set of market-driven

actions. Strategic marketing links the organization with the environment and views marketing

as a responsibility of the entire business rather than a specialized function. Because of

marketing’s boundary orientation between the organization and its customers, channel

members, and competition, marketing processes are central to the business strategy planning

process. Strategic marketing provides the expertise for environmental monitoring, for

deciding what customer groups to serve, for guiding product specifications, and for choosing

which competitors to position against. Successfully integrating cross-functional strategies is

critical to providing superior customer value. Customer value requirements must be

transformed into product design and production guidelines. Success in achieving high-quality

goods and services require finding out which attributes of goods and service quality drive

customer value.

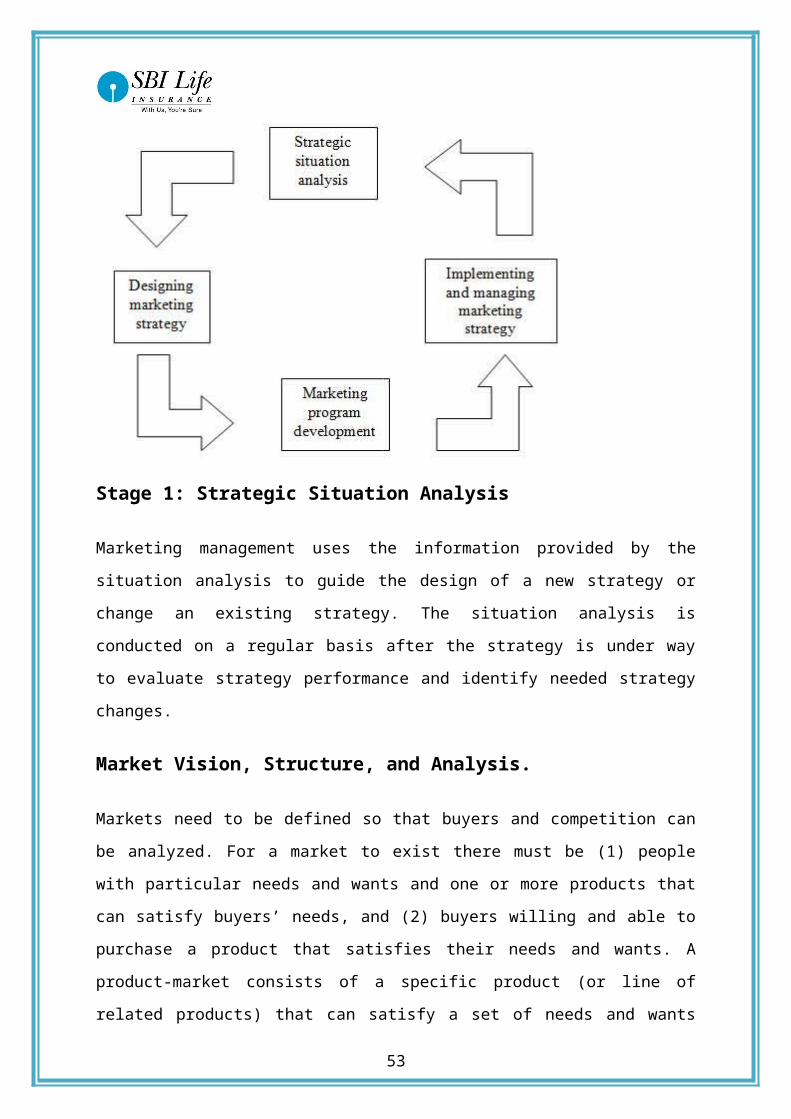

Marketing Strategy Process

The marketing strategy analysis, planning, implementation and management process is

described below. The strategic situation analysis considers market and competitor analysis,

market segmentation, and continuous learning about markets. Designing marketing strategy

examines customer targeting and positioning strategies, marketing relationship strategies and

planning for new products. Marketing program development consists of product, distribution,

price, and promotion strategies designed and implemented to meet the value requirements of

targeted buyers. Strategy implementation and management consider organizational design

and marketing strategy implementation and control.

36

Stage 1: Strategic Situation Analysis

Marketing management uses the information provided by the situation analysis to guide the

design of a new strategy or change an existing strategy. The situation analysis is conducted

on a regular basis after the strategy is under way to evaluate strategy performance and

identify needed strategy changes.

Market Vision, Structure, and Analysis.

Markets need to be defined so that buyers and competition can be analyzed. For a market to

exist there must be (1) people with particular needs and wants and one or more products that

can satisfy buyers’ needs, and (2) buyers willing and able to purchase a product that satisfies

their needs and wants. A product-market consists of a specific product (or line of related

products) that can satisfy a set of needs and wants for the people (or organizations) willing

and able to purchase it. The term product is used to indicate either a physical good or an

intangible service. Analyzing product-markets and forecasting how they will change in the

future are vital to business and marketing planning. Decisions to enter new product-markets,

how to serve existing product-markets, and when to exist in unattractive product-markets are

critical strategic choices. The objective is to identify and describe the buyers, understand their

preferences for products, estimate the size and rate of growth of the market, and find out what

companies and products are competing in the market. Evaluation of competitors’ strategies,

strengths, limitations and plans is also a key aspect of the situation analysis. It is important to

37

identify both existing and potential competitors. Competitor analysis includes evaluating each

key competitor. The analyses highlight the competition’s important strengths and

weaknesses. A key issue is trying to figure out what each competitor is likely to do in future.

Segmenting Markets. Market segmentation looks at the nature and extent of diversity of

buyers’ needs and wants in a market. It offers an opportunity for an organization to focus in

business capabilities on the requirements of one or more groups of buyers. The objective of

segmentation is to examine differences in needs and wants and to identify the segments (sub-

groups) within the product-market of interest. Each segment contains buyers with similar

needs and wants for the product category of interest to management. The segments are

described using the various characteristics of people, the reasons that they buy or use certain

products, and their preferences for certain brands of products. Likewise, segments of

industrial product-markets may be formed according to the type of industry, the uses for the

product, frequency of product purchase, and various other factors. Each segment may vary

quite a bit from the average characteristics of the entire product-market. The similarities of

buyers’ needs within a segment enable better targeting of the organization’s capabilities to

buyers with corresponding value requirements. And Marketing strategy is an ongoing process

of making decisions, implementing them, and tracking their effectiveness over time. In terms

of its time requirements, strategic evaluation is far more demanding than planning.

Evaluation and control are concerned with tracking performance and, when necessary,

altering plans to keep performance on track. Evaluation also includes looking for new

opportunities and potential threats in the future. It is the concerning link in the strategic

marketing planning process. By serving as both the last stage and the first stage (evaluation

before taking action) in the planning process, strategic evaluation assures that strategy is an

ongoing activity Key insurance marketing strategies will always include an in-depth review

of the a value of follow-up. All successful sales agents understand that consumers need to be

contacted again and again in order to make a vital connection. Also, great follow-up protocol

lets the potential customer know that good, solid customer service will be part of the over-all

package. Follow-up says to a consumer that they are important, thought of, and that their

business would be greatly appreciated. The consumer today not only wants a product at a

great price, they also want a personal relationship, especially when it comes to financial

system sales, such as various insurances. Letters and phone calls are gentle reminders that the

salesperson intends to serve with his or her whole heart. And, once a sale is secured, a thank

you call is strongly advised .consumers today value information. We live in the information

age, and the savvy, faithful customer is one that has knowledge about the products and

38

services offered. The next most valuable insurance marketing tips include the salesperson

being the source of financial information for the client. Newsletters, email updates, and

notifications will keep customers informed about issues surrounding insurance and other

financial programs. There are creative ways to approach these insurance marketing strategies.

Newsletters could include contests, special interest areas for kids, safety concerns, and

economic updates. There could even be an area for customer spotlights, or encouraging

testimonies of how the customers were helped through the office. Of course, all new products

and services should be showcased in any informative hard copy or e-mail communication.

Community marketing is another great way to get advertising and name recognition.

Successful networkers join local community agencies, such as the local Chamber of

Commerce, and sign up to help in activities. This is a great way to get name and photographs

listed in newspaper articles and other media avenues. Also, charity work cannot only be

greatly beneficial to the community and those served, but may also open doors to

communicating with other volunteers, who could be potential clients. People enjoy using

services extended by like-minded providers. Creating a sense of community is extremely

important to insurance marketing strategies. There are other insurance marketing tips and

resources available and insurance agents may find investigating several options to be

beneficial. Many marketing support companies offer email or publication updates, sharing

information and techniques that are proven to bring in success. Agents may want to browse

the Internet and find a few different insurance marketing tips programs to choose from. Not

only will these resources help keep salespersons abreast of the latest strategies, but these

support programs can also create a sense of community and an opportunity for agents to share

their own struggles and challenges with others in the field.

ACTIVITY

In the insurance industry there is a new way of thinking which determined the passage from

transactional marketing to a holistic marketing concept. In this paper five key elements of

holistic marketing are presented: relationship marketing, integrated marketing, internal

marketing, social responsibility marketing and international marketing. In order to be

successful insurance companies have to be able to convince their clients of the usefulness of

their products and of the solidity of their businesses. In the current crisis situation, trust is a

vital element for the insurance industry and even if on short term, liquidity is the target, as it

ensures survival, on long and medium term the objective has to be the consolidation of the

trust of consumers in insurance companies and the goal of the managers must be to win

39

customer loyalty. Keywords: holistic marketing in insurance, relationship marketing,

integrated marketing, internal marketing, social responsibility marketing, international

marketing, trust, customer loyalty, crisis Today the success of an insurance company is based

on the quality of the long term relationship established between the company and its

“partners”: customers, employees, broker dealers, banks, hedge funds etc. In the insurance

industry this new way of thinking determined the passage from transactional marketing to a

holistic marketing concept. The traditional transaction marketing focused on meeting

customers’ needs so that the company could obtain an immediate advantage. This approach

wasn’t always benefic for the insurance companies and for their clientsAn integrated

marketing is a must in the insurance industry. The insurance company must have a coherent

marketing mix in order to satisfy efficiently the needs of their clients. The marketing

department of the insurance company must coordinate and integrate all the activities included

in the marketing mix in order to maximize their joint effects: the insurance products and

services offered must be conceived as a solution for the needs of the client and the setting of

the premiums, distribution channels and company communications must be done in an

integrate perspective. The role of internal marketing is to ensure that everyone in the

insurance company embraces appropriate marketing principles. The internal marketing is the

task of hiring, training and motivating the employees who want to serve customers well.

Social responsibility marketing is a key element in the marketing activity of an insurance

company due to the specific of the product. The role of the insurance is to protect the insured

against different risks, but also to create benefic effects for the entire society. The marketing

activity in insurance has important causes and effects in the social, ethical and legal

environment. The social responsibility marketing activities demonstrate a corporate culture

that is designed to treat consumers fairly

OBJECTIVES OF THE STUDY40

The objective of the recruitment process is to obtain the number and quality of employees

that can be selected in order to help the organization to achieve its goals and objectives.

Following are other objectives of recruitment process-

1. Support the organization ability to acquire, retain and develop the best talent and skills.

2. Increase the effectiveness of various recruiting techniques.

3. This study provides the student a practical insight of various activities and functions of

the company.

4. The will also be able to develop in depth knowledge of Human Research sector. The study

is also required for the partial fulfillment of the requirement for the degree of M.B.A. as per

the curriculum

5. The study would help SBI to know the Employee`s attitude towards the company.

6. To know the latest trend of the company.

MEANING & DEFINITION

“The life insurance contract embodies an agreement in which broadly stated, the insurer

undertakes to pay a stipulated sum upon the death of the insurer to a designated beneficiary.”

--- J.H.MAGEE

“Life insurance contract may be defined whereby the insurer, in consideration of premium

paid either installment, undertakes to pay an annuity on the death of the insured of a certain

number of years.” --- R.S.SHARMA

“A contract of life assurance is that in which one party agrees to pay a given sum on the

happening of a particular event contingent upon the duration of human life in

consideration of immediate payment of a smaller sum by another.”

41

Insurance advisor

A life adviser is a broker or intermediary authorized to sell or advise on the policies of life

insurance and financial products, such as unit trusts. Typical examples of companies which

employ financial advisers are banks, insurance and life companies, general brokers, estate

agents and building societies The presence of a life insurance policy is essential in every

individual's financial portfolio. But at the same time, it is also important that the right

insurance products be bought and that too for the right reasons. With so many insurance

products vying for a place in the individual's portfolio, conducting a proper evaluation can

become quite a task. Taking the help of an insurance advisor/agent can help solve this

problem. An insurance advisor/agent can play the part of the direct link between the

insurance company and the insurance seeker i.e. you. He is the one who can help you select

the right policy i.e. one which can help you fulfill your insurance needs. But for this, it is

important that you connect with an expert and qualified insurance advisor/agent.

The task is to choose the good quality advisor those who are having the following quality.

•Confidence

•Self motivation And Persuasion

•Urge to be financiallyindependent

•Relationship skills

I have to recognize where a person (whom I meet to recruit him/her as an advisor) havingall

these characteristics or not .If some person is closed enough to these characteristicsthen. I

discussed the following support pattern.After getting all these information an advisor

basically asked about the workingenvironment. Then I discussed the working environment

and try to convince him/her that he/she has the potential to become an agent/advisor.

1. To be part of a world class sales team.

2. Work from his/her (advisor) own office or residence.

3. Work full time or part time.

4. Earn commission, bonus and incentives.

5. No upper limits on earnings.

6. Flexible career.Therefore the first and for most problem is to convinced that person those

whohaving enough patience to listen my companies idea/views.The role of the advisor is to

quite effective to search a good prospect.

42

FUNCTION OF ADVISORS:

Advisors provide on going financial advice for his /her client/prospect. In our official term

prospect is a person who can buy life insurance from us.The advisors study the prospects

needs and persuade them to buy a policy.Complete all formalities for proposal of new

insurance, including filling up forms.collecting premium. Arranging medical examination,

collecting proofs (of age/income), reports and information required by the underwriter.After

having sold a new insurance policy, the advisor has to ensure that the policy continues.

Without a lapse. Till it becomes a claim For that reason an advisor has to do the following:

1. Keep in touch with the policy holder to make sure that renewal premiums are paid in time.

2. Ensure that nominations are made or changed, if necessary

3. Assist in collecting claim amounts.As an advisor you contribute in bringing in new

business for the company offer world class pre and post sales service to the clients with the

support of theorganization.But an advisor to us means much more than a salesman or a,

saleswoman, at SBI LIFE recognize our advisors as the ambassadors of our organization in

the market place and we consider the advisor force would be our biggest differentiating factor

in thecoming years.That is why; we take a lot of care in recruiting and developing our advisor

force, so thatwe can maintain our standards of quality in service and salesmanship. The

competition and the customer awareness have forced the times to be a knowledgeoriented

marketplace. Appreciating the same we strive to get people with reasonablygood graduation

background as our advisors. We also acknowledge and recognize prior 11sales experience of

the persons; at the time of recruitment.The other function is to be of assistance to the policy

holder in case he/she needs a loanunder the policy.

ROLE OF AN ADVISOR:

1. Identify future clients/prospect

2. Making appointment.

2. Conduct financial review meeting with prospect.

4. Close sale.

5. Get referral

6. Provide service to clients/prospect.

7. Follow internal sales and reporting system.After analyzing the quality (which the company

is looking for), back office service(which the company is giving to that person). Functions to

43

be performed, role to be played .I used to describe the benefits which the advisor can get out

of his/her joiningas an advisor in SBI Life Insurance Company.

ROLE OF UNIT MANAGERS

In fulfilling his obligations under the Agreement, Advisor shall scrupulously adhere to,

follow and be bound by the Statutory provisions governing life insurance Advisors and more

particularly the code of conduct contained therein, as in force from time to time. Without

prejudice to the generalify of the obligations of the Advisor to SBI Life Life Insurance, the

Advisor shall:

a. Faithfully and diligently promote the business of SBI Life Life Insurace;

b. Ensure that any representation made and information provided is accurate;

c. Act diligently and carefully in providing any advice and ensure that such advice is

based on thorough analysis and take into account available alternatives;

d. Ensure that any advice is reasonable in view of the customer’s circumstances;

e. Not admit any liability or make any false, misleading, deceptive or reckless statement

to the customer in respect of life insurance generally or any particular product of SBI

Life Life Insurance;

f. Solicit proposals for insurance for SBI Life Life Insurance as SBI Life Life Insurance

may from time to time determine during the term of this Agreement;

g. Service the needs and requirements of customer introduced by self or assigned by

SBI Life life Insurance;

h. Meet the validation specified by SBI Life Life insurance including production and

persistency;

i. Attend all training, meetings and seminars arranged or required by SBI Life Life

Insurance and perform such other duties as requested by SBI Life Life Insurance;

j. Begin soliciting proposals for various insurance products at dates set by SBI Life

Life Insurance;

k. Be fully responsible and accountable for all its acts and omissions;

l. Obtain, maintain, renew and keep renewed the prescribed licences issued by the

IRDA and any other licence, approval or permission required of it for fulfilling the

obligations of an Advisor at all times during the term of this agreemet;

m. At all times during te term of this Agreement, act within the scope of such licences,

approvals and permissions and any applicable legislation ad in consonance with the

corporate image and objectives of SBI Life Life Insurance. The Advisor shall

44

promptly notify SBI Life Life Insurance of the loss of any suc licence, approval or

permission by it or by its certified persons;

n. Submit to SBI Life Life Insurance within the period of time specified by SBI Life

Life Insurance in writing from time to time, all proposals and initial premiums, for

products solicited by Adviosr and in any case within the time specified by 64VB(4)

of the Insurance Act, 1938 or any other statutory provisions applicable thereto. The

Advisor shall remit to SBI Life Life Insurance all monies collected in trust

immediately and without any deduction whatsoever.

o. Observe and be bound by the-

Statutory provisions, SBI Life Life Insurance Instructions including Advisor

manual, benefit illustration policy, cash acceptance policy, market conduct

guidelines, prevention of money laundering policy, the compliance manual

and the code of conduct that may be issued by SBI Life Life Insurance, in

writing, from time to time relating to the conduct of the business;

Monitoring, supervision and performance standards of the business and sales

practices used in relation to SBI Life Life Insurance products that may be

issued by SBI Life Life Insurance, in writing, from time to time;

p. Promptly deliver to SBI Life Life Insurance in good order and condition when

demanded all records, rate books, documents, manuals, computers (hardware and

software relating in any way to the life insurance business of SBI Life Life Insurance

and which were received from SBI Life Life Insurance, including those that have

been specifically entrusted to the Advisor pursuant to this Agreement. Advisor here

by acknowledges that such good, tangible and otherwise, and the exclusive property

of SBI Life Life Insurance;

q. Maintain and observe at all times the strictest secrecy and confidentiality, concerning

the business of SBI Life Life Insurance or of Policyholders or proposers of Life

Insurance or persons or companies from time to time dealing with SBI Life Life

Insurance at any time, either while the Agreement is in force or subsequent to its

termination;

r. Bear all expenses incurred in the performance of duties under this Agreement unless

otherwise specifically agreed to in writing by SBI Life Life Insurance;

s. Promptly disclose to SBI Life Life Insurance every fact and circumstance within his

knowledge relevant to the acceptance of the risk of business by SBI Life Life

Insurance and shall promptly and accurately relate to SBI Life Life Insurance every

45

fact disclosed to him relevant to the acceptance of such risk or business howsoever

the Advisor is aware of such matter;

t. Promptly notify SBI Life Life Insurance of receipt by it or service on it of any

complaint, demand, notice or claim made or to be made under a policy howsoever

the advisor is aware of such matter.

u. Record and reolve, within the standard turn around time of 7days from receipt, all the

complaints and requests/inquiries received from customers of Advisor and

statutory/regulatory bodies and forward a report of the complaints, requests and

inquiries of the past week with the relevant documentation containing details like

Date of Complaint, Policy older Name, Advisor name and Code No., MOA Name

and No., Nature of Complaint, Date of Complaint Forwarded to the concerned

function for resolution, Status (Resolved /Pending), Resolution date to SBI Life Life

Insurance at the specified email address on every Thursday of the next week.

v. Ensure that a strong needs analysis is carried out for every prospect during the sales

process;

w. Ensure strict adherence to the prevention of Money laundering and Terrorist

Financing Policy of SBI Life Life Insurance, the prevention of Money Laundering

Act, 2002, Rules thereunder and the IRDA Anti Money Laundering (‘AML’)

guidelines and modification thereto and employ adequate know Your Customer

(‘KYC’) standards as prescribed therein;

x. In the event of finding any adverse or suspicious change on the standing, integrity or

reputation of the customer/policyholder, Advisor should promptly disclose the same

to the Principal compliance officer of SBI Life Life Insurance in change of Anti

Money Laundering programme. In the event Advisor fails to comply with this

provision and/or exposes SBI Life Life Insurance to AML related risks, SBI Life Life

Insurance shall be entitled to terminate this Agreement with all attendant

consequences to the Advisor;

y. Act as a fiduciary, in good faith and I the best interests of SBI Life Life Insurance at

all times during the continuance of this Agreement; and

z. Declare his adherence to the code of sales and Business Conduct in the format

prescribed in Schedule ‘A’.

46

TRAINING AND COACHING OF ADVISORS

Refresher training is the basic given to the trainee advisors about what is insurance, types of

insurance, present scenario of life insurance in India and scope and career growth in

insurance with legal ideas related to insurance.

i. The applicant shall have to undergo at least 100 hours’ practical training in life or general

insurance business which may be spread over three to four weeks, where such applicant is

seeking license for the first time to act as an insurance agent.

ii. The training duration should be minimum 18 working days excluding Sundays and

holidays.

iii. No product training/market survey should be included into this hundred 100 hours

training. The product training, if any, to be given by the insurance company should be

over and above the minimum training hours prescribed by the Authority

iv. The attendance record of the trainees should be maintained at the Institute for necessary

inspection at any given point of time.

v. In case of short-fall of attendance, extra class may be permitted but the extra hours may

be specified separately with proper attendance and details of faculty.

vi. Every Institute should have at least one qualified permanent faculty who is an Associate

or Fellow from the Insurance Institute of India for each stream i.e. for Life and Non-Life.

vii. The attendance register of the faculty members should be maintained at the training

institutes.

viii. The record of the payment made to faculty should be maintained at the training institute

i.e. batch-wise payment detail should be maintained.

ix. The faculty should provide details of the other Institutes with whom they have been

empanelled as part-time/guest faculty.

47

x. Register should be maintained at the training institute giving details of batches completed,

strength of the each batch, number of candidates decertified, name of the sponsored

insurer and details of faculty who imparted the training with dates.

xi. The seating capacity of each class-room should not exceed 40.

xii. The fresh accreditation will be given on need basis after assessing the needs of the

particular city/town.

xiii. The initial approval will be for a period of 3 years and consideration of further renewal up

to 3 years would depend on the satisfactory compliance of requirements of accreditation.

xiv. The insurance companies would regularly send their officials to oversee the proper

conduct of the training at the institutes and would not sponsor candidates to those

institutes that are not maintaining the required standards of and facilities for the training.

xv. The training institute must display the certificate of accreditation to impart training issued

by the Authority at the training institute.

xvi. The Institute should not allow a franchisee to conduct courses on its behalf even if the

faculty is that of the Institute. The Institute should conduct the training on its own

premises or hired premises with proper infrastructure.

xvii. No marketing fee/consultancy fee payment is permitted for getting the training batches.

xviii. It will be the responsibility of the Insurance Company to check the status of the institute

before sponsoring any candidates for training.

xix. In case of mofussil areas or the cities where there are no accredited institutes and an

insurance company intends to appoint agents, it will be the responsibility of the insurance

company to conduct training.

xx. The Institutes must keep with them one set of records of the training at the place where

the training is being imparted.

48

xxi. The Institute should confine its activities only to the place/city for which it has been given

the approval. No training outside the said place/city is permitted.

xxii. The Institutes must submit a copy of the lease deed/rent agreement at the time of seeking

fresh accreditation/renewal/change of address of the institute.

xxiii. On successful completion of training the candidates get COT i.e. the Completion of

Training Certificate by SBI Life INSURANCE?

Basic aim of the insurance plan satisfies the following objectives:-

Protection of economic value of assets.

Mechanism to reduce impact of adverse events on value generating assets.

Types of insurance

Insurance is generally classified into three main categories:

1. Life Insurance.

2. Health Insurance.

3. General Insurance.

To get insurance an individual or an organization can approach to Insurance Company

directly, through Insurance agent of the concerned company or through intermediaries.

Life insurance or life assurance is a contract between the policy owner and the insurer,

where the insurer agrees to pay a sum of money upon the occurrence of the insured

individual's or individuals' death or other event, such as terminal illness or critical illness. In

return, the policy owner agrees to pay a stipulated amount called a premium at regular

intervals or in lump sums. There may be designs in some countries where bills and death

expenses plus catering for after funeral expenses should be included in Policy Premium.

NEED OF LIFE INSURANCE

49

. The functions of Insurance can be bifurcated into two parts:

1. Primary Functions

2.Secondary Functions

3. Other Functions

The primary functions of insurance include the following:

Provide Protection - The primary function of insurance is to provide protection against

future risk, accidents and uncertainty. Insurance cannot check the happening of the risk, but

can certainly provide for the losses of risk. Insurance is actually a protection against

economic loss, by sharing the risk with others.

Collective bearing of risk - Insurance is a device to share the financial loss of few

among many others. Insurance is a mean by which few losses are shared among larger

number of people. All the insured contribute the premiums towards a fund and out of which

the persons exposed to a particular risk is paid.

Assessment of risk - Insurance determines the probable volume of risk by evaluating

various factors that give rise to risk. Risk is the basis for determining the premium rate also.

Provide Certainty - Insurance is a device, which helps to change from uncertainty to

certainty. Insurance is device whereby the uncertain risks may be made more certain.

The secondary functions of insurance include the following:

Prevention of Losses - Insurance cautions individuals and businessmen to adopt suitable

device to prevent unfortunate consequences of risk by observing safety instructions;

installation of automatic sparkler or alarm systems, etc. Prevention of losses causes lesser

payment to the assured by the insurer and this will encourage for more savings by way of

premium. Reduced rate of premiums stimulate for more business and better protection to the

insured.

Small capital to cover larger risks - Insurance relieves the businessmen from security

investments, by paying small amount of premium against larger risks anduncertainty.

Contributes towards the development of larger industries - Insurance provides

50

development opportunity to those larger industries having more risks in their setting up. Even

the financial institutions may be prepared to give credit to sick industrial units which have

insured their assets including plant and machinery.

The other functions of insurance include the following:

Means of savings and investment - Insurance serves as savings and investment,

insurance is a compulsory way of savings and it restricts the unnecessary expenses by the

insured's For the purpose of availing income-tax exemptions also, people invest in insurance.

Source of earning foreign exchange - Insurance is an international business. The

country can earn foreign exchange by way of issue of marine insurance policies and various

other ways.

Risk Free trade - Insurance promotes exports insurance, which makes the foreign trade

risk free with the help of different types of policies under marine insurance cover.

51

LIMITATION

52

RECOMMENDATION AND SUGGESTIONS

Recommendations-

Following are suggestions made for the benefits and augmentation of the sound working of

the company –SBI life insurance

1. Need to train and develop life insurance agents with more comprehensive knowledge and

skills to counter every queries of the customer.

2. It is suggested that company should not left any stone unturned towards sound

advertisement and promotional measures on every section whether it is printed, media or air

via radio.

3. It is also suggested that skilled management graduates need to be places on sales and

marketing of financial services that can render their best ideas for the accomplishment of the