practical issues in entering the china market and …...practical issues in entering the china...

TRANSCRIPT

Practical Issues in Entering the China Market and Sourcing From China

September 29, 2010 Approved for 3.6 hours of Missouri CLE

8 - 8:30 Registration and Continental Breakfast Tab

Speaker Biographies 1 8:30 - 9:15 Is a Long Distance Relationship Right for You? 2

Sourcing from and Exporting to China Linda Tiller, Partner, Husch Blackwell LLP

Ms. Tiller will cover selected legal issues and provide practical advice related to sourcing from China, such as U.S. import laws, sourcing methods, contracting issues, quality control, and China-specific export controls.

9:15 - 10 Legal Issues Relating to Entering the China Market 3

Fang Shen, Associate, Husch Blackwell LLP

Ms. Shen will discuss entering the China market through contractual arrangements, covering issues such as distributor arrangements, manufacturing and licensing agreements, compliance with local laws, foreign exchanges, payments, Incoterms, and the Foreign Corrupt Practices Act.

10 - 10:15 Break 10:15 - 11 Foreign Direct Investment in China 4

Lawrence Shu, Partner, Hylands Law Firm, Shanghai, China

Mr. Shu will discuss the process of a foreign company establishing a business entity in China, covering issues such as common entity choices, joint ventures, registration procedure, key issues for a U.S. business to understand (concepts of registered capital, overall investment amount, etc.), and industry guidance.

11 - 11:45 What You Have to Know for Doing Business 5

in China Lidong Pan, Partner, Wang Jing & Co., Guangzhou, China

Mr. Pan will cover areas such as labor contract law, IP protection, importation regulations affecting foreign companies, the new tax laws and how they work with the special economic zones, old tax holidays and other key issues.

Visa Challenges for Chinese Business Visitors handout 6

About Husch Blackwell LLP 7

PAN Lidong,

Partner, Attorney at Law in China and New York

Areas of practice: corporate law, cross-boarder investment, employment law, intellectual

property (trademark and copyright), insurance law, commercial litigation and arbitration,

disputes of cargo transportation, international trade and Customs law issues

Office: Guangzhou

Email: [email protected], Tel.: 86 20-87690107

Academic qualifications:

1994 Sun Yat-sen (Zhongshan) University Law School

1997 Sun Yat-sen (Zhongshan) University Law School (Master of Laws)

2004 Washington University in St. Louis School of Law (Master of laws, insurance,

banking & commercial law)

Professional qualifications:

1998 Licensed lawyer (PRC)

2004 New York State Bar

Languages:

Chinese (Mandarin, Cantonese) and English

Experience:

Mr. Pan was trained at a Guangzhou law firm from 1994 to 1996. He then worked in the

Claims Department for AIU Insurance (a member of AIG) Guangzhou Branch until

1997, and between 1997 and 1998 as civil servant at the Hong Kong and Macao Affairs

Division of the Foreign Affairs Office, Shenzhen Municipal Government. He joined

Wang Jing & Co. and practiced as attorney at law in 1998. From August to November

2004, he was interned at the United States District Court of Southern Illinois and at the

offices of Keesal, Young & Logan in Long Beach, California.

Mr. Pan has acted as legal counsel to companies on cooperate matters, providing and

drafting legal opinion in general legal matters, corporate documents and regulations on

internal management, mergers, acquisitions, divestment, establishment of branches, stock

equity and credits. He also acts as legal counsel to companies on intellectual property

matters, advising on strategy and protection in of intangible properties in China, and

handling disputes and litigation of know-how, copyright and trademark. He has

represented many clients in commercial and maritime arbitration and litigation, in disputes

of international trade and PRC Customs matters. He has acted for a number of insure

companies in handling insurance investigations and insurance-coverage disputes. As

approved by China Insurance Regulatory Commission, Mr. Pan has been retained as

person responsible for legal affairs by CITIC-Prudential Life Insurance Company Ltd. He

frequently advised foreign clients on the establishment of employment contracts and

company internal labor/management rules, and has been involved in employment

negotiations, labor arbitration and the litigation of employment disputes.

Mr. Pan has been a speaker on arbitration and litigation, corporate, employment law,

commercial or IP law at numerous symposiums, including several organized by the

German, Italian, Japanese, Singapore and US chambers of commerce. He has also

attended several court hearings as expert witness on PRC law in lawsuits of maritime,

Customs issues, cargo transportation and international trade in Singapore, Russia and

Hong Kong.

He has also published a number of essays including Enforcement of Arbitral Awards and

Court Judgments in PRC, Mainland Courts to Enforce Hong Kong Judgments, Legal

Aspects of PRC Domestic Transactions, Corporate Acquisitions and Mergers, Issues for

Corporate Counsel in the Sale/Purchase of a Business, and The TRIPS Agreement and

IPR Laws of the PRC.

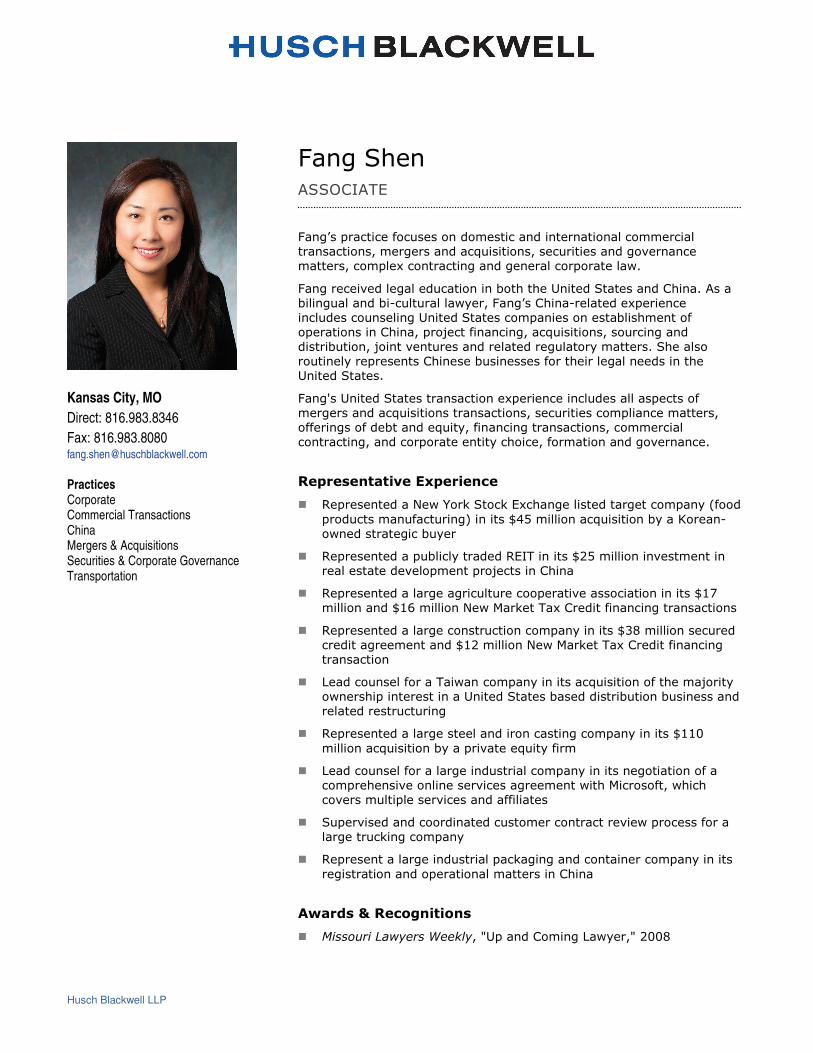

Husch Blackwell LLP

Kansas City, MO

Direct: 816.983.8346

Fax: 816.983.8080 [email protected]

Practices Corporate Commercial Transactions China Mergers & Acquisitions Securities & Corporate Governance Transportation

�������������� ��

���������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������� !���

���������������������������������"��������#����������������������!�����"�������������"�$����������� %����������������$���������������������������������������#������������������������������"������������������������������������&������������������������������������������������"�������&�����������������������������������%��������!������������������%��������������������"���������������������������������������#������������!���

����'��#�������������������������������������������������������������������������������������������������������������������������������������������������"�����������%���������������������������������������������������������������������%���������������������������������!�

�������������� ��������

� (�������������)� �*��+�����+������������������������������%�,�����

����������������������-��������./0���������������������"%���1�����$� ��������������"�%���

� (���������������"����%��������(�� ��������.20��������������������������������������������������&��������������

� (��������������������������������������������������������������.34�������������.35���������)� �6��+��� ���������������������������������

� (��������������������������������������%��������.78��������������������������������������.32���������)� �6��+��� ��������������������������������

� 9������������������ �� ���������%�����������������������������&����%�� ����������������������#�������������"�����������"������"����������������������������������

� (������������������������������������������������%��������.33:�

��������������������"%����������������%������

� 9�����������������������������������������%����������������������������������������������������������������� ����6���������� ���������������������������������������������

� �������������������������������������������������� �������������������������+����������%�

� (�������������������������������+��������������������������%��������

����������������������������������������������

��������������������

� ��������������� �������;#�������������9� %���;�2::8�

������������������������������������

� ��������<�����������������������������9� ��������������������������

� �������������<�����������������1���������%�

� 1���������%�6������������<��������������

�������������

� ���������"������������������=�������1���������%��<�����6��"����2::4$��������

� =�������1���������%��������������� ��������������<�����6��"����2::5$��������

� ���������%���������������� �����������<�����6��"����2::5$��������

���������

� 6���������2::7�

� #!�!�>���������������?�������>�����������6���������2::7�

� @�����'��(���"��������������3AA5�

���������

� B!>!��#��������%����6��������$�1���������%�� �����������������2::7�

� 99!<!��<��������9� ��@��������#��������%����������� �����������������3AA8�

��������������������������

� �������� ����C�>����������������������������@��������D�������������������������������6�%�2::4�

� �������C���*���@������������ ����9�����6�E�F�G� ����������9�����>����������"��������������������������B������������������D�42��������������230��2::7�

� ����+����C9�����������������������������������������D��������������� ����������������=�������1���������%��

6�����2:3:�

� ����+����C�����������������������(��������%�����������>�����<�����������������D�?�������?����� ��������������6�%�2::A�

� ����+�����C��������9� ����������� ������������������9��"����%�D� ��������������9� %���������������������6�������������9��������������!��6�%�2::8�

� ����+�����C�������������@������%�@�������������������D�6�� ������������������ �����������������������)�"!��>����"���2::4�

� ����+����C(��������������������������������9�����(��+�������>���>���������?����������D���������������������������������������������������!��6�%�2::4�

� ����+����C ���3:�?�%�����������������������%������������9����������(��������������D������)���=��"�����������@�������������@�!�������2::5�

����������

� 6������������������������

1

SHANGHAI OFFICE OF HYLANDS LAW FIRM

No. 1028, West Beijing Road, Xing Ye Tower, Suite 1805

Jing’an District, Shanghai 200041

Tel:+86-21-5256 9939 Fax: +86-21-5256 9930

www.hylandslaw.com

ATTORNEY’S BIOGRAPHY

LAWRENCE SHU

Partner

Member of the PRC Bar

Languages: Chinese and English

Education: � M.Jur., Oxford University

� LL.M., K.U. Leuven

� Master in Law, Nanjing University

� B.A., Southeast University

Email: [email protected]

Phone: + 86-21-5256-9939

Cell Phone: + 86 139 1664 8626

Fax: + 86-21-5256-9930

Practice Areas Foreign direct investment, merger & acquisition, general

corporate, and banking and investment.

Profile Mr. Shu worked as an engineer in China before he started his

legal practice. The unique background in both law and

engineering as well as the legal education both in civil law and in

common law facilitate his deep communication with clients from

various industries and jurisdictions so as to have a thorough

understanding of their real business needs.

Mr. Shu has provided efficient and high quality legal services to a

large number of multi-national companies, foreign investment

enterprises, hi-tech enterprises, commercial banks and

non-banking financial institutions. He is adept at providing

legal solutions for transaction structure design and conducting

complicated commercial negotiations.

Mr. Shu is the author of numerous books and articles, including

book of “Chinese Business Law” (one of the co-authors),

2

published by C.H. Beck in the Continental Europe and

co-published by Hart Publishing in the U.K. and the U.S. in

2010.

Mr. Shu is the member of various professional organizations such as

Chinese Bar Association, TerraLex and AIJA. He is the committee

member of Oxford China Scholarship Fund. He is also a guest

lecturer in Chinese law at University of Freiburg, Germany.

Husch Blackwell LLP

Kansas City, MO

Direct: 816.983.8223

Fax: 816.983.8080 [email protected]

Practices Customs & Trade International Mergers & Acquisitions Commercial Transactions

������������� ������

���������������������������������������������������������������������������������������� ������������� ������ �!��"����� ������!���������������������#��������� $�����������%�������#������ �����������#��

&�����������������"������ ��������� �������������'������������������� ����#������������������%�����'������������#���������������������"�����!�(�%����������������!��) ������ ������!����� ����)�������*�����&������������� $������������������������+���������������� �� ��#��������� ���� ��������������������������&� ����� ������ �!�,�������%� ������������!���������)��������������#���&������%�������������-��������'��� ����������������#�����������.������������������/����

%��&� ��������!���#�������������������&� ���������+��

�������������� ��������

� 0��������� ����������'������������������� ��������)�"�������� ���������$������������������������%�����

� %� ����������������� ���������*������ ���������������#�����#����&���� ����������� �������������

� �����������������1����� �����#��� ������#�������������� ��� ��

�������� ���#�������������������

� 2�����&����������������3������������������#���������������������1�"� ���������������(�%�������� �������

� %� ��������&� �������������)������#�������������������������������������������

������������������������������������

� ��������4�������������������-������� �������

� �������������-������� �������

� ������������1�����������-������� �������

� 1��������-������� ������!������������������������

���������

� 1�������!�5667�

� '����� ������������!�5665�

� (�%����������������������������!�5668�

���������

� 2�'�!��������#��/�����#����(��&�����������% ���!�5669�0�����������������

1����������-�����'���:��;���������������� ���������������� ���� ������������������ ��!��������������

� -�%�-���!�(��&����������1��������)��������!�56<7�

1

© Husch Blackwell LLP

Is a Long Distance Relationship Right for You?

Sourcing From and Exporting to China

September 29, 2010

Linda [email protected]

816.983.8223

Trade Statistics(U.S. Census Bureau)

31.618.413.1Mexico3

40.633.37.3China2

40.821.119.7Canada1

Total Trade (7/2010) [billions]

Imports (7/2010) [billions]

Exports (7/2010) [billions]

CountryRank

2

Agenda

• Sourcing from China– Importing into the U.S.

–Sourcing Structures

–Contract Terms

–Tips

• Exporting to China–Lists to check

–The China Rule

–Validated End-User Program

Common Import Pitfalls

• Tariff Classification

• Country of Origin Determination/Marking

• Assists

• Antidumping/Countervailing Duties

• Special Certifications

– Consumer Product Safety Commission

– Lacey Act

• Counterfeit components

3

Common Import Pitfalls

• Tariff Classification

–Determines the amount of duties

– Importer of Record is responsible for proper tariff classification

– Importer must exercise “Reasonable Care” to properly classify imported products

Common Import Pitfalls

• Country of Origin– Every foreign good imported into the U.S. for consumption must be marked with the country of origin so that the ultimate purchaser knows where the product originated.

– For textiles, COO determined by tariff shift rules (similar to those in U.S. free trade agreements).

– For non-textiles, COO is the country in which the product was last “substantially transformed” into a new and different item.

– Imported goods that are not properly marked are subject to seizure or redelivery to Customs and Border Protection (CBP), plus the costs of marking under CBP supervision, plus a marking penalty of 10% of the entered value of the goods.

4

Common Import Pitfalls

• “Assists”– Definition: Any of the following if supplied directly or indirectly, and free of charge or at reduced cost, by the buyer of imported merchandise for use in connection with the production or the sale for export to the United States of the foreign merchandise:• (i) Materials, components, parts, and similar items incorporated in the imported merchandise.

• (ii) Tools, dies, molds, and similar items used in the production of the imported merchandise.

• (iii) Merchandise consumed in the production of the imported merchandise.• (iv) Engineering, development, artwork, design work, and plans and sketches that are undertaken elsewhere than in the United States and are necessary for the production of the imported merchandise.

- Value of the “Assist” is added to the entered value of the imported merchandise and duties are assessed on it.

- Suggestion – If feasible, have the Chinese manufacturer purchase the components, materials, etc. and simply add it to the selling price.

Common Import Pitfalls

• Antidumping/Countervailing Duties

– Numerous Chinese-origin products are subject to AD/CVD orders (79 AD/12 CVD).

– AD/CVD orders impose additional duties on imported products to “level the playing field.”

– Additional duties could range from .1% to 300+% of the entered value of the goods.

– Rates can be manufacturer/exporter specific so know who you are buying from.

– CHECK THE AD/CVD ORDER LIST!• International Trade Administration - http://trade.gov/ia/

5

Import – Special Certifications

• Consumer Product Safety Commission– China exports more than $250 Billion in consumer products to the U.S. each year

– Consumer Product Safety Improvement Act of 2008 established requirements for testing and compliance certifications for any “consumer” product and for any product directed at children

– Violations could result in seizure and destruction or export of the products

– April 2010 - CBP and CPSC signed MOU which will give CPSC the capability to conduct import safety risk assessments and perform targeting work using CBP’s Automated Commercial System.

Import – Special Certifications

• Lacey Act– Makes it unlawful to import, export, transport, sell, receive, acquire, or purchase in interstate or foreign commerce any plant, with some limited exceptions, taken or traded in violation of the laws of the United States, a U.S. State or a foreign country.

– USDA identified a list of products and the associated Harmonized Tariff Schedule (HTS) numbers which requires filing a Plant Product Declaration Form (PPQ 505) with the import.

6

Counterfeit Goods/Components

• Enforcement of intellectual property rights is a priority trade issue of CBP. (http://www.cbp.gov)

• Counterfeit goods (or goods with counterfeit components) are subject to seizure and forfeiture at the U.S. border.

• Protect your marks and your imported goods:– If you have a recorded trademark/copyright, register it with CBP.

– If you are importing a product that includes a component trademarked/copyrighted by some other party, be sure that the component is genuine.

Sourcing from ChinaGetting Started

• Quality Control is key!– Supplier choice is critical!

• Considerations in selecting a factory– Location• Access to raw materials?• Costs to get finished goods to port?

– Expertise• Do they specialize in your type of product?• Do they have technical resources?

– Size• Too big? Too small?

• Recommendation: VISIT THE FACTORY!

7

Sourcing Structures

• Contract directly with the factory

• Use a sourcing agent– Full-service independent sourcing agent• Confirm whether it is a Buyer’s Agent or a Seller’s Agent

– Set up a PRC representative office to handle

• Use a trading company– Trading companies usually specialize in a particular type of product, but work for the factories so you may not know or have any control over which factory is producing

Manufacturing Contract

• Written Agreements should:– be clear and concise

– include all agreed upon terms

• Remember: – Entering into a contract in China is just the beginning (some say it is just the beginning of the negotiations).

– Constant oversight and mutual cooperation is required from the time the Agreement is signed until the product is delivered.

– If you simply issue a purchase order and expect perfect product and delivery without being engaged, you will likely be extremely disappointed.

8

Manufacturing ContractKey Terms

• Quality Control, Testing, Monitoring– Be specific– Require written reports– Joint Inspection– Independent inspector– Rules of Inspection

• Setoff Rights• Subcontracting– Generally not a good idea– If it will be required to complete the product, specify the terms

Manufacturing ContractKey Terms

• Dispute Resolution -- Arbitration VS Litigation– Arbitration

• In China– Over 200 arbitration institutions in China– Chinese International Economic and Trade Arbitration Commission

– Hong Kong International Arbitration Center– International Chamber of Commerce

• Outside China– China is a signatory to the New York Convention so enforces foreign arbitral awards

- Litigation• In China

– In the past, this was the last resort, but in recent years the Chinese courts have gained popularity

• Outside China– Difficult to get enforced in China

9

Manufacturing ContractKey Terms

• Dispute Resolution - Arbitration VS Litigation

- Evaluate the type of disputes that may arise

• E.g. - Quality issue and manufacturer has no assets outside of China; remedy = money damages

• E.g. – Manufacturer is using your intellectual property to manufacture and sell product to India in violation of Agreement; remedy = injunction.

• E.g. – Manufacturer refuses to return your molds after termination – You don’t need $$ - you need the molds returned; remedy = court order for return of the molds.

Manufacturing ContractKey Terms

• Specify Governing Language

– If contract will be in printed in more than one language, specify which language governs.

– Governing language may depend on whether disputes will be resolved by arbitration or in a Chinese court.

– Recommendation: Governing language should be Chinese if you want to enforce in a Chinese court.

10

Manufacturing ContractKey Terms

• Labor Matters

– Include provision prohibiting forced, convict, or child labor.

– Include a right to inspect the factory to actually confirm that labor matters comply with the contract.

Sourcing from ChinaTips

• How to encourage long-term reliability from Suppliers– Work closely at the beginning to establish acceptable performance.

– Keep monitoring quality (get written signed records and don’t lower your standards).

– Dump the worst factories.

– Give regular business to those that perform.

– Understand that the best factories receive a reasonable premium on prices.

– Don’t switch suppliers for a few pennies, but keep them in competition with at least one other factory to avoid unreasonable quotations.

11

Sourcing from ChinaTips

• Practical Recommendations

– Order 2nd quarter products in 4th quarter of the previous year (Chinese New Year is in Jan/Feb and everyone goes on vacation)

– Build in plenty of time for completion (e.g. don’t expect delivery of an order for 350,000 in the same time as you would expect delivery of 70,000)

– Establish a process for quality control and inspection [hire an in-country agent if necessary]

Export – Lists to Check

• Denied Persons ListA list of individuals/entities that have been denied export privileges. Any dealings with a party on this list that would violate the terms of its denial order is prohibited.

• Unverified ListA list of parties where Bureau of Industry and Security (BIS) has been unable to verify the end-user in prior transactions. Being on this list is a “Red Flag” that should be resolved before proceeding with the transaction.

• Entity ListA list of parties whose presence in a transaction can trigger a license requirement under the Export Administration Regulations (EAR). The list specifies the license requirements that apply to each listed party. These license requirements are in addition to any license requirements imposed on the transaction by other provisions of the EAR.

12

Export – Lists to Check

• Specially Designated Nationals ListA list compiled by the Treasury Department, Office of Foreign Assets Control (OFAC). OFAC’s regulations may prohibit a transaction if a party on this list is involved. In addition, the Export Administration Regulations require a license for exports or reexports to any party in any entry on this list that contains any of the suffixes "SDGT", "SDT", "FTO", "IRAQ2" or "NPWMD".

Export – Lists to Check

• Debarred ListA list compiled by the State Department of parties who are barred under the International Traffic in Arms Regulations (ITAR) from participating directly or indirectly in the export of defense articles, including technical data or in the furnishing of defense services for which a license or approval is required by the ITAR. (22 CFR §127.7)

• Nonproliferation SanctionsSeveral lists compiled by the State Department of parties that have been sanctioned under various statutes. The Federal Register notice imposing sanctions on a party states the sanctions that apply to that party. Some of these sanctioned parties are subject to a general policy of denial. (15 CFR §744.19).

13

Export – “The China Rule”

• Export license to China is required for a targeted list of items that are intended for a “military end use” (i.e. incorporated into a military item). (§744.21)

• Involves 20 product categories and associated technologies and software, as described in 31 entries on the Commerce Control List.

• Items subject to the military end-use control include aircraft and aircraft engines, avionics and inertial navigation systems, lasers, depleted uranium, underwater cameras and propulsion systems, certain composite materials, and some telecommunications equipment for space communications or air defense.

Export – “The China Rule”

• Validated End-User (VEU) program

–Certain Chinese companies that qualify (i.e.“trusted customers”) with a track record of responsible civilian use of U.S.-controlled technology will be able to receive certain controlled items without individual export licenses.

14

QUESTIONS?

Linda Tiller

Husch Blackwell LLP

4801 Main Street, Suite 1000

Kansas City, MO 64112

DD: 816.983.8223

Cell: 913.339.8430

1

© Husch Blackwell LLP

Legal Issues Relating to Entering the China Market

Fang Shen

Husch Blackwell LLP

© Husch Blackwell LLP

Road Map

• Overview of Forms of Market Entry

• Distribution Agreement

• Manufacturing Contract

• Other common issues

2

© Husch Blackwell LLP

Forms of Market Entry

• Employee? Sales representative? Independent contractor?

• Distribution Agreement

• Manufacturing Contract

• Franchise Agreement (allowed, but not the focus of today's discussion)

• Setting up your own operation (representative office, WFOE, or JV) to be covered later

© Husch Blackwell LLP

Forms of Market Entry

• What is the most effective method of entering the market?

• What tax issues are created?

• What liability issues are out there?

3

© Husch Blackwell LLP

Distribution Agreement

© Husch Blackwell LLP

Facts• MoInc is a Missouri company with headquarters

in Kansas City. MoInc makes and sells animal health care products. MoInc desires to expand its market in China.

• MoInc’s VP-International attended several trade shows and identified BeijingInc, a company that currently makes and distributes similar products in China. BeijingInc has offices in Beijing and several other major cities in northern and western China, but not southern China.

• After a few initial visits both are very interested in having BeijingInc serve as MoInc’s distributor in China and to market and sell MoInc’s products

4

© Husch Blackwell LLP

Question

What are the key issues that MoInc will need to consider in the contracting process?

© Husch Blackwell LLP

Due Diligence

• Existence and operation

• Business scope

• Financial strength

• Trustworthiness

5

© Husch Blackwell LLP

Exclusivity?

• Goes both ways

• Geographical consideration

• Competitive consideration

© Husch Blackwell LLP

Key Provisions

• Specify the geographic area, market, segment or scope of distribution

• Include specific performance requirement

• What else do you want to control (e.g., limit on resale price mark up)?

6

© Husch Blackwell LLP

Term and Termination

• Statutory restrictions

• Be specific about term and termination rights

• Comply with notice requirement and put termination in writing

© Husch Blackwell LLP

Manufacturing (and Often Licensing)

Agreement

7

© Husch Blackwell LLP

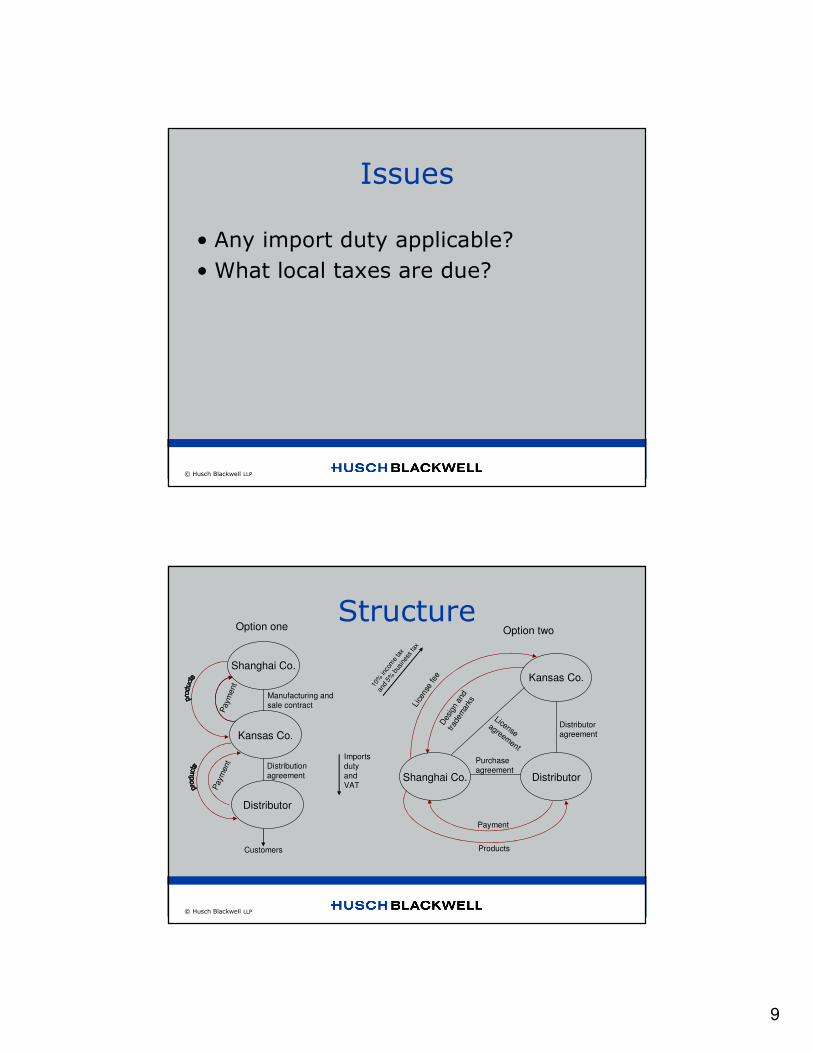

Facts• KansasCo is a Kansas company that

manufactures a range of measuring and precision devices that are commonly used in industrial manufacturing, farming, and construction

• It started selling its products in China three years ago. Since then KansasCo has seen the overall demand for its products increase in China, but at the same time local competition has also grown.

© Husch Blackwell LLP

Facts• To produce more products quickly to supply the

China market and bring down the cost, KansasCo started discussion with a Chinese company called ShanghaiCo. ShanghaiCo currently manufactures similar products under its own brand names.

• KansasCo would like to have ShanghaiCo manufacture the products under KansasCo's design and brand name. The products will then be shipped to KansasCo's existing distributor in China for sale to customers.

8

© Husch Blackwell LLP

Question

What are the key issues that KansasCo will need to consider in the contracting process?

© Husch Blackwell LLP

Structure

Shanghai Co.

Kansas Co.

Distributor

Kansas Co.

DistributorShanghai Co.

Option one Option two

Manufacturing and

sale contract

Paym

ent

Distribution

agreement

Customers

Paym

ent

Distributor

agreement

License agreem

ent

Payment

Products

Lice

nse

fee

Des

ign

and

trad

emar

ks

Purchase

agreement

9

© Husch Blackwell LLP

Issues

• Any import duty applicable?

• What local taxes are due?

© Husch Blackwell LLP

Structure

Shanghai Co.

Kansas Co.

Distributor

Kansas Co.

DistributorShanghai Co.

Option one Option two

Manufacturing and

sale contract

Paym

ent

Distribution

agreement

Customers

Paym

ent

Distributor

agreement

License agreem

ent

Payment

Products

Lice

nse

fee

Des

ign

and

trad

emar

ks

Purchase

agreement

Imports

duty

and

VAT

10%

inco

me

tax

and

5% b

usin

ess

tax

10

© Husch Blackwell LLP

Protection of Intellectual Property

• Registration of the contract?

• What are the IP rights important for your business?

• Think about China when you register your patents in the U.S.

• Are your trademarks registered in China?

• Is your domain name registered in China?

• Restrict access to sensitive information to the smallest possible group of individuals

© Husch Blackwell LLP

Other Common Issues

11

© Husch Blackwell LLP

Local Licensing and Registration Requirements

• Mandatory Product Certification Requirement– New regulations effective September 2010

– Requiring certification by the State Administration of Quality Supervision, Inspection, and Quarantine for products that potentially pose hazards to human, animal, plant or environment health or safety

– Catalogue of specific products is currently in the works; past examples from previous catalogue included electric cables and wires, circuit switches, surge protectors, etc.

• Certain products may be subject to licensing requirement by industry regulatory authority: e.g., elevator, medical equipment

• Manufacturer Registration Requirement: e.g., Food Safety Law

© Husch Blackwell LLP

Payment Methods

• Payment methods: cash only, progress payments, L/C, document collection, open account.

• L/C– A promise given by buyer’s bank that they will pay for the goods if the

seller can provide a set of documents in strict compliance with clauses

of the L/C

– Usually operate under the Uniform Customs and Practices by the ICC

– Rule of “strict compliance” : “The issuing bank must examine a

presentation to determine, on the basis of the documents alone,

whether or not the documents appear on their face to constitute a

complying presentation.” (UCP Art. 14, Standard for Exam. Of Docs)

12

© Husch Blackwell LLP

Foreign Exchange

• Currency

• Exchange rate fluctuation protection

• Foreign Exchange control complications (e.g., missing documentation, suspicious fee)

© Husch Blackwell LLP

WHAT ARE INCOTERMS?

• “Incoterms” stands for “International Commercial Terms” – they are the international standard delivery terms published by the ICC. They are widely used in international transactions

• They are currently being revised and the most recent version will come into force January 1, 2011

• Each term defines at which point transaction responsibilities and costs related to the delivery, transportation, insurance, export and import documentation, are divided between the seller and the buyer

13

© Husch Blackwell LLP

EX-WORKS and FOB are the two most commonly used terms

COMMON INCOTERMS

© Husch Blackwell LLP

EX-WORKS– Delivery is at the Seller’s Premises (e.g., Ex-Works

seller factory, St. Louis, Missouri)

– Goods suitably packed for export

– Seller notifies buyer when goods are ready

– Buyer loads arriving vehicle – Seller often exceeds Incoterm responsibility

– Buyer contracts for the freight from seller’s door to buyer’s door, buyer’s risk and responsibility from the seller’s door all the way to the buyer’s door

– Insurance not mentioned, but common sense dictates that parties should work this into the contract or Buyer should arrange

– Buyer handles all export processes & paperwork

– Buyer handles all import entry documentation

14

© Husch Blackwell LLP

FOB– Seller arranges for pre-carriage to the port

– Seller delivers when the goods are loaded on board the ship at the seaport in the seller’s country (e.g., FOB Long Beach, CA)

– Goods must pass the ship’s rail

– Seller’s responsibility to load vessel

– Seller handles all export processes & paperwork

– Buyer contracts for freight from seaport in seller’s country to his location, and it is the buyer’s risk and

responsibility from the seaport in the seller’s country until he receives the goods

– Insurance not mentioned

– Buyer handles import documentation

© Husch Blackwell LLP

INCOTERMS – TWO KEY POINTS

• Best if, (1) each party’s responsibilities match its realistic capabilities and (2) control and liabilities go together if (1) each party's responsibilities match its realistic capabilities and (2) control and liabilities go together

• Make sure the INCOTERM works with payment method

15

© Husch Blackwell LLP

Local Law Compliance

• Safety standard?

• Packaging and labeling requirements?

• Any other industry requirement?

© Husch Blackwell LLP

Dispute Resolution

• Court v. arbitration

• Where?

16

© Husch Blackwell LLP

Unfair Competition Practice

• What you are doing needs to be legal under both U.S. law and Chinese law

• Unfair competition law– Price or rate fixing

– Kickbacks or bribes

– Exchange of cost or price information with competitors

– Require suppliers to buy your product in order to sell to you

© Husch Blackwell LLP

FCPA Overview• Prohibits bribery of foreign officials, foreign

political parties or candidates to obtain or retain business

• Covers any U.S. person and any “domestic concern” organized under the laws of the United States or its agents

• Who is an official? Any officer or employee of a government or of a government-owned entity, any foreign political party or official, any candidate for foreign political office, any official of a public international organization, and any other person while “knowing” that the payment or promise to pay will be passed on to one of the above.

17

© Husch Blackwell LLP

Don’t Ignore the Facts!• “Willful blindness,” “deliberate ignorance” and

taking a “head-in-the-sand” attitude constitutes knowledge under the statute

• A company is not immune if the payment is made by a third party, such as an agent or consultant

• Liability may flow to a company if it: (1) authorizes an agent or third party to make improper payments to foreign officials or (2) makes payments to an agent or third party with actual or constructive knowledge that all or a portion of money will be paid directly or indirectly to foreign officials

© Husch Blackwell LLP

China Specific

• Sponsorship of overseas children’s study/work

• Travel expenses

• Excessive “license fee”

1

Foreign Direct Investment in China

Hylands Law Firm, China

Lawrence Shu

1. General FDI Policy

- FDI Guidance Catalogue

- FDI Provisions

- Exceptions to FDI Categorization

- Special Restrictions under FDI Provisions

- Summary

2. General FDI Concepts

- FDI Vehicles

- Capitalization of FIEs

- Forms of Capital Contribution

- Timetable for Capital Contribution

- External Loans

- Government Approvals

- Business Scope

Road Map

Hylands Law Firm

2

3. Representative Office

- Nature and Function

- Scope of Activities

- Streamlined Registration Procedures

4. Joint Venture

- Nature and Function

- EJV vs. CJV

- Establishment Procedures

5. Wholly Foreign Owned Enterprise

- Nature and Function

- Case Study – FICE Establishment

Road Map

Hylands Law Firm

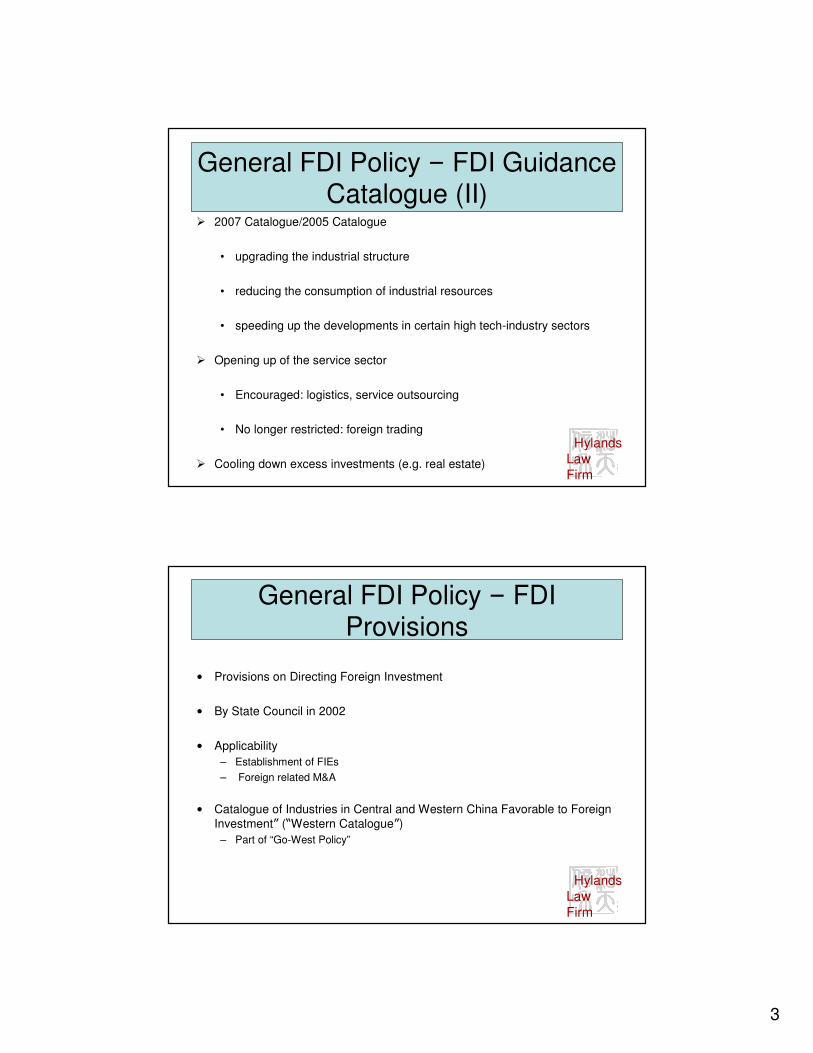

General FDI Policy – FDI Guidance Catalogue (I)

� Catalogue of Industries for Guiding Foreign Investment (“Guidance Catalogue”)

� Four categories of industry sectors: “encouraged”, “restricted”, “prohibited”and “permitted”

� Each category provides a difference level of treatment

� Updated in regular intervals: the most recent edition by NDRC and MOFCOM in Oct of 2007

Hylands Law Firm

3

� 2007 Catalogue/2005 Catalogue

• upgrading the industrial structure

• reducing the consumption of industrial resources

• speeding up the developments in certain high tech-industry sectors

� Opening up of the service sector

• Encouraged: logistics, service outsourcing

• No longer restricted: foreign trading

� Cooling down excess investments (e.g. real estate)

General FDI Policy – FDI Guidance Catalogue (II)

Hylands Law Firm

General FDI Policy – FDI Provisions

• Provisions on Directing Foreign Investment

• By State Council in 2002

• Applicability

– Establishment of FIEs

– Foreign related M&A

• Catalogue of Industries in Central and Western China Favorable to Foreign Investment” (“Western Catalogue”)

– Part of “Go-West Policy”

Hylands Law Firm

4

General FDI Policy – Exceptions to FDI Categorization

• General principles subject to several exceptions

• Exceptions based on high-priority political concerns

• Examples of Exceptions:

– "Permitted" or "restricted" projects in Western Catalogue;

– "Permitted" projects that export all of their products;

– “Restricted” projects that export at least 70% of products.

Hylands Law Firm

General FDI Policy – Special Restrictions under FDI Provisions

• If only EJVs or CJVs are allowed, a WFOE may not be established;

• If the Chinese side is required to hold a majority share, one or more Chinese shareholders together must hold more than 51% share;

• If the Chinese side is required to hold a relative majority share, the combined shares of all Chinese investors must be greater than the share of each foreign investor.

• E.g. sole Chinese investor (40%) + two foreign investors each (30%)

Hylands Law Firm

5

General FDI Policy – Summary

• FDI Provisions and Guidance Catalogue: a leading role in guiding FDI

• Categorization of investment: basis of solid investment plan

• Practical advise on categorization issue

– One of the first question from client

– Not easy to answer – 3 reasons

– Sufficient communication with client & early consultation with gv’t needed

– Room of negotiation

• Economic policy more favorable

• Further opening up widely expected

Hylands Law Firm

General FDI Concepts – FDI Vehicles

• Basically four kinds of FDI vehicles:

– RO (“Representative Office”);

– CJV (“Contractual Joint Venture” or “Cooperative Joint Venture”);

– EJV (“Equity Joint Venture”) and

– WFOE (“Wholly Foreign-owned Enterprise”).

• CJV, EJV and WFOE collectively called Foreign Investment Enterprises (FIEs)

Hylands Law Firm

6

General FDI Concepts –Capitalization of FIEs (I)

• Concept of registered capital

– Total amount of capital contributions subscribed to by investors

– Investors’ equity in a FIE

• Concept of total investment

– Registered capital + external borrowings

• Minimum capital requirement

– To satisfy needs of future operation

– No general requirement on minimum amount for FIE

– Special requirement for specific industries

– Local difference

– General principle: being sufficient for preparation & initial operation

Hylands Law Firm

General FDI Concepts –Capitalization of FIEs (II)

• Registered capital/total investment ratio

At least 33.3% or US$ 12 million(whichever is higher)

> US$ 30 million

At least 40% or US$ 5 million(whichever is higher)

> US$ 10 million and ≤US$ 30 million

At least 50% or US$ 2.1 million(whichever is higher)

> US$ 3 million and ≤US$ 10 million

At least 70%≤ US$ 3 million

Registered Capital/Total InvestmentTotal Investment Amount

Hylands Law Firm

7

General FDI Concepts – Forms of Capital Contribution

• A variety of forms (inc. cash, machinery, equipment and intangible property)

• Foreign party: assets from FIEs previously invested in

– By early recoupment of investment, liquidation, share transfer, capital reduction, etc.

– Subject to SAFE approval

• Chinese party: right to use a site

• Restrictions on in-kind contribution

– Technology contribution ≤ 20% (may be increased for encouraged projects)

– Valuation: major block in JV negotiations

Hylands Law Firm

General FDI Concepts – Timetable for Capital Contribution

• One lump sum or in installments

• Timetable be specified in JV contract and AOA

• Paid in one lump sum:

– w/i 6 months

• Paid in installments:

– First installment of 20%, w/i 3 months

– Balance, w/i 2 years

Hylands Law Firm

8

General FDI Concepts – External Loans

• Borrowing funds from Chinese or foreign bank permitted

• Shareholder loans

– From foreign party, permitted

– From Chinese party, no sufficiently broad business scope in most cases

• SAFE registration

• External loans ≤ (total investment – registered capital)

Hylands Law Firm

General FDI Concepts –Government Approvals (I)

• MOFCOM/COFTEC approval on FIE establishment

– Final right to approve a FIE

– Local counterparts: COFTEC

– Approval levels: amount of total investment & presence location

• NDRC ratification on FDI projects

– Major and restricted projects be ratified and filed

– Project Ratification Procedures by NDRC

Hylands Law Firm

9

General FDI Concepts –Government Approvals (II)

• Whether shall be ratified by NDRC:– Category of project

– Total investment amount

be ratified by the local NDRC of provincial level; andthis ratification right cannot be delegated down to lower level bodies

% 50 Mrestricted6

be ratified by the local NDRC% 100 Mencouraged or permitted

5

after the NDRC ratification, be submitted to the State Council for final verification

≥ 100 Mrestricted4

after the NDRC ratification, be submitted to the State Council for final verification

≥ 500 M encouraged or permitted

3

be ratified by NDRC≥ 50 Mrestricted2

be ratified by NDRC≥ 100 Mencouraged or permitted

1

Ratification RequirementsTotal Investment Amount (US$)

Category of Project

General FDI Concepts –Government Approvals (III)

• Timetable for ratification

– 30 day window

– A great improvement

• NDRC verification document

– Basis for other procedures (land, FIE establishment, equipment import, tax benefits)

– Other gov’t dep. not to proceed till verification is obtained

• Department in charge

– SoE: department in charge

– In a JV project, consent from such department is fundamental

Hylands Law Firm

10

General FDI Concepts – Business Scope

• Limited scope of approved operation

• Generally impossible to obtain a general scope of business

• Typically restricted to a specific category of manufacturing or service

• Broader scope of business on a case-by-case basis– prohibiting business activities that are prohibited by PRC laws, regulations and

state policies regarding foreign investment industries;

– prohibiting business activities that require special approval prior to obtaining the special approval; and

– permitting any and all business activities that are not subject to special approval as provided by PRC laws and regulations and are not classified as "restricted" according to PRC foreign investment industry regulations.

• Expansion of business scope Hylands Law Firm

Representative Office – Nature and Function

• Nature of Rep Office

– Most basic form of foreign business presence

– Permanent base + liaison

– Not a independent legal entity, but a liaison office

– Establishment process: relatively simple

– No capital investment requirement

• Scope of Activities

– Quite restricted and must be specifically approved

– Prohibited from engaging in “direct business operations”

• No precise definition

• Determined on a case-by-case basis

• No direct business activities with a view to making profits

Hylands Law Firm

11

Representative Office – Scope of Activities

• Permitted activities

– Basic types of activities w/i business scope

– Coordinate visits and exchanges of personnel

– Conduct negotiations on behalf of parent company

– Conduct activities in relation to its own office adm

• Consequences of exceeding limitations on activities

– Penalties

• Fines up to RMB 20k

• Suspension of business activities

– In practice, somewhat discretionary & on a case-by-case basis

• Remedy situation w/o sanction

• Appropriate penalties based on the amount invested or income generated

Hylands Law Firm

Representative Office – Streamlined Registration Procedures

• Sponsor

– Usually through a local Chinese sponsor

– Service companies act as sponsors (e.g. FESCO)

– Lately, w/o engagement of sponsor allowed in certain cities

• Streamlined registration procedures

– Substantially simplified by a regulation in 2004

– Previous two steps consolidated into one-step procedure

– Two-step regime still apply to certain industries

• E.g. banking, insurance, securities, transportation, legal service

• Some adm streamlining

– Normally takes 5-15 days in Shanghai

Hylands Law Firm

12

Hylands Law Firm

Representative Office – Post AIC-Registration Matters

7 daysCustomsCustoms Registration(only required if import samples)

7

5 daysBank Designated by ClientBank Account Opening6

1 day Branch of State Administration of Foreign Exchange (“SAFE”)

Foreign ExchangeRegistration Certificate

5

3 daysStatistics BureauStatistics Registration Certificate4

30 days Foreign Taxation Department of Shanghai Taxation Bureau

Tax Registration Certificate3

3 day Public Security BureauChop Carving and Record Registration

2

7 daysMunicipal Administration for Quality and Technology Supervision

Organization Code Certificate1

Estimated Timetable

Authority in ChargeItems

Joint Venture – Nature and Function

• Overview– Definition– Often used in a “restricted” sector– Still important role– Two types of JV: EJV & CJV

• EJV– Separate entity – Profit-sharing in proportion to investment

• CJV– Organized by means of contract; 2 types of CJV– “Purely contractual” CJV

• A purely contractual arrangement• Cannot protect the partners from venture’s liability• Rare animal in today’s market

– “Legal person” CJV• A separate LLC• Shares more characteristics of an EJV

Hylands Law Firm

13

Joint Venture – EJV vs. CJV (I)

• Principal differences bet EJVs & CJVs– EJV: the earliest form of LLC

– CJV: the evolutionary LLC

– CJV may provide more flexibilities in the aspects of• Investment form

• Profits/risks distribution

• Operation management

• Investment recoupment

• EJVs vs. CJVs – investment form– EJV

• In cash or other in-kind contributions

• Debt/equity ratio and timing of contribution

– CJV• “cooperative conditions”

– Access to or use of certain assets

– Rights that are not assigned formally

Hylands Law Firm

Joint Venture – EJV vs. CJV (II)

• EJV vs. CJV – operation management

– EJV

• Substantially as a corporation in Western jurisdictions

• Also shares characteristics of a partnership

• No concept of Shareholders Meeting

– CJV

• Board of director OR joint management office

• Management to be delegated to a third party (e.g. hotel industry)

• EJV vs. CJV – distribution of management rights & profits

– EJV

• Profits/losses in proportion to respective percentage of equity contribution

• Management rights allocated by percentage of contribution

– CJV

• Not conform strictly to the ratio of capital contribution

• More flexible, not tied to the value of contributions Hylands

Law Firm

14

Joint Venture – EJV vs. CJV (III)

• EJV vs. CJV – recoupment of investment

– EJV

• Recouped from distributable profits & liquidated investor’s returns

– CJV

• Accelerated recovery possible

• Subject to the condition that fixed assets be reverted to Chinese partner

• Typically funded by excess cash flow generated by accelerated assets depreciation

Hylands Law Firm

Joint Venture – EJV vs. CJV (IV)

Accelerated recovery of investment is possible

From distributable profits and liquidated investors’returns

Recoupment of Investment

Not tied to the value of contributions, but set by contract

By percentage of equity contribution

Distribution of management rights and profits/losses

- Board of directors model; or- Delegation of management to a third

party with gov’t approval

Board of directors modelOperation management

- capital contributions; and - cooperative conditions (e.g. market

access rights, undertakings to supply certain services or cooperation, access to or use of certain assets)

Capital contributions as required by law (e.g. cash/ permitted in-kind contributions; debt/equity ratio; timing of contribution)

Form of investment

- Non-legal person: “purely contractual”CJV

- LLC: “legal person” CJV

LLCLegal form

CJVEJV

15

Hylands Law Firm

Wholly Foreign Owned Enterprise

• Most popular foreign investment vehicle– accounting now for more than half of foreign investment

– Popularity will grow

• Three factors– difficulties experienced with JVs

– growing confidence

– more industry sectors opened up

• Appropriate where there is no legal requirement or business reason to involve a Chinese partner

• Usually as a company with limited liability

• Compared to JVs, many similarities in a WFOE establishment project

Case Study: FICE Establishment

• Nature and Function of FICE

– WTO accession – to open trading & distribution sector

– FICE: recently established corporate structure

– Wholly foreign-owned businesses in the sectors of wholesale, retail & distribution

– Entry requirements lowered

– LLC

Hylands Law Firm

16

FICE Establishment – Business Activities of FICE

• Business activities of FICE

– Commission Agency: agents or brokers of goods

– Wholesaler: selling goods to retailers, industrial customers, commercial organizations or other wholesalers

– Retailer: selling goods for consumption and use by individuals• Retailing commodities

• Importing commodities directly

• Purchasing domestic products for export; and

• Other related businesses (e.g. product consultant).

– Franchisor: vesting in others the use of its trademark, trade name, or mode of management

– Open outlets or storesHylands

Law Firm

FICE Establishment – Project Background

• Project Background

– A German company

• which manufactures medical imaging systems, in particular, X-ray equipment

– A rep office already registered in Shanghai

– To set up a WFOE in Shanghai

• to import and distribute their Products to their customers in China (e.g PRC hospitals)

– FICE is a suitable investment vehicle

Hylands Law Firm

17

Hylands Law Firm

Issuance of Approval Certificate

TIMEFRAME: approx. 30 days upon submission of documents

STEP 5: Application for Certificate of Approval

TIMEFRAME: approx. 30 days upon submission of documents

STEP 4: Application for Medical Equipment Operation License

TIMEFRAME: approx. 3-5 days upon submission of documents

STEP 3: Company name reservation

TIMEFRAME: approx. 15 days upon submission of documents

STEP 2: Registration of tenancy

TIMEFRAME: depending on the work efficiency and cooperation of client

STEP 1: Feasibility study

FICE Establishment – Procedures for FICE Establishment

Hylands Law Firm

TIMEFRAME: approx. 1 to 2 months

Issuance of business license by AIC (= formal legal existence of company)

STEP 7: Additional formalities after issuance of business license

� Registration with Public Security Bureau

� Application of Tax Registration Certificate with the tax authorities

� Finance Registration with the Finance Bureau

� Opening of bank accounts

� Customs registration

TIMEFRAME: approx. 1 to 2 weeks

STEP 6: Application for Business License

FICE Establishment – Procedures for FICE Establishment

18

HYLANDS LAW FIRM

Nanjing19th Floor, Tower E, Deji Plaza

No. 188 Changjiang Road

Nanjing 210018

P.R. China

Tel: (+86) (25) 8682 7100

Fax: (+86) (25) 8682 7103

Shanghai

Suite 1805, Xingye Tower1028 West Beijing RoadJing‘an DistrictShanghai 200041P.R. China

Tel.: (+86) (21) 5256 9939Fax: (+86) (21) 5256 9930

Beijing5A1, 5th Floor, Hanwei PlazaNo. 7 Guang Hua RoadChao Yang DistrictBeijing 100004P.R. China

Tel.: (+86) (10) 6561 2460Fax: (+86) (10) 6561 0548

Contact Person

Lawrence Shu

Tel.: (+86) (21) 5256 9939Fax: (+86) (21) 5256 9930Email: [email protected]

Hylands Law Firm

1

PAN LidongAttorney at LawChina and New York

Wang Jing & Co., Law Firm

Email: [email protected]

Contents

� I Labor Laws-Labor

� II Intellectual Property Protection-IP

� III Importing Goods to China

(Wine as case study)

� IV Enterprise Income Tax Law -EIT

2

I. Labor-Labor Laws in China

� Labor Law of the People’s Republic of China (which come into

force as of January 1,1995)

� Labor Contract Law of the People’s Republic of China, (which

is promulgated and come into force as of January 1, 2008)

� Law of the People’s Republic of China on Labor Dispute Mediation and Arbitration, (which is promulgated and be effective

as of May 1, 2008 )

� Regulation on the Implementation of the Employment Contract Law of the People’s Republic of China, (which is

promulgated and be effective as of September 3, 2008)

I. Labor-Labor Laws in China

� Labor Contract Law provides more protections to employee, such as open-ended labor contracts, double financial compensation for illegal termination of labor contracts;

� After the promulgation of Labor Contract Law and Law of the People’s Republic of China on Labor Dispute Mediation and Arbitration, Labor cases in Shenzhen has increased 198% than one year before. As the enterprises fail to keep records and adjust it’s internal regulations and management to employees, 60%-70% enterprises of the enterprises involving labor cases lose the cases.

3

1.1 Labor-Enter into Labor Contract

� Employers have to enter into written labor contracts with employees.

Three types of labor contracts:

� Fixed-term labor contracts

� Open-ended labor contracts

� Labor contracts that set the completion of

specific tasks as the term to end contracts

1.2 Labor- Open-ended Labor Contract

Unless the employee proposes to conclude a fixed-term labor contract a open-ended labor contract shall be concluded in the following circumstance:

1) The employee has already worked for the employer for 10 full years consecutively;

2) The labor contract is to be renewed after two fixed-term labor contracts have been concluded consecutively;

Failing to sign a written labor contract

after the lapse of one full year of work

open-ended labor contracts.

4

1.3 Labor-Liability for failing enter into a

contract pursuant to Labor Contract Law

Labor Contract Law Article 82

If an employer fails to conclude a written labor contract with an employee after the lapse of more than one month but less than one year as of the day when it started using him, it shall pay to the worker his monthly wages at double amount.

If an employer fails, in violation of this Law, to conclude with an employee a open-ended labor contract, it shall pay to the employee his monthly wage at double amount, starting from the date on which a open-ended labor contract should have been concluded.

1.4 Labor-how to terminate a labor contract

legally

Labor Contract Law Article 39

Where an employee is under any of the following circumstances, his employer may dissolve the labor contract:

1. the employee does not meet the recruitment conditions during the probation period;

2. The employee seriously violates employer’s rules;

3. The employee causes any severe damage to the employer because he seriously neglects his duties or seeks private benefits;

4. The employee simultaneously enters an employment relationship with other employers and thus seriously affects his completion of the tasks of the employer, or the employee refuses to make the ratification after his employer points out the problem;

5. The labor contract is invalidated due to the circumstance as mentioned in Item (1), paragraph 1, Article 26 of this Law; or

6. The employee is under investigation for criminal liabilities according to law.

5

1.5 Labor-other matters shall be paid more

attention

� Add a non-competition clause into labor agreement, if necessary

� Make sure your employee manual comply with labor laws and regulations

� Financial Compensation for termination labor contractthe employer shall pay financial compensation

EXCEPT that

the employer offer equal or better conditions as the previous contract to renew but the employee rejects such offer.

Labor-CASE STUDY

Case: A and B has signed fix-

term labor contract for

two times consecutively,

now they prepare to

renew the contract

A individual

Company B

6

Labor-CASE STUDY

Analysis:

� B has to sign a open-ended labor

contract with A.

� If B fail to do so, A might Claim against B for compensation

II IP- Laws and Regulations

WIPO WIPO Copyright

TRIPS (WTO) Paris Convention

Berne Convention Madrid Agreement

Paten Cooperation Treaty

General Principles of Civil Law

Copyright, Trademark, Patent Laws

Unfair Competition Law

Criminal Law

Regulations, Rules, and SPC

opinions

with domestic IP offices or

through international systems

7

Conventions and International Organizations

�World Intellectual Property Organization since 1980. (WIPO)

�Paris Convention for the Protection of Industrial Property since

1985

�Madrid Agreement Concerning the International Registration of

Marks since 1989

�Berne Convention for the protection of Literary and Artistic Works

since 1992

�WIPO Copyright Treaty since 1992

�Convention of Producers of Phonograms Against Unauthorized

Duplication of Phonograms since 1993

�Patent Cooperation Treaty since 1994 (PCT)

�Agreement on Trade-related aspects of Intellectual Property Rights

since 2001. (TRIPs)

II IP- Laws and Regulations

General laws and rules on IPRs

�General Principles of Civil Law (1986) in which IP was

adopted as a civil right.

�Copyright Law: adopted in 1990, revised in 2001;

�Trademark Law: adopted in 1982, revised in 1993, 2001;

�Patent Law: adopted in 1984, revised in 1992, 2000;

�Law Against Unfair Competition (1993), with clauses on

unfair competition, anti-monopoly, commercial secrets.

�Criminal Law (1979); 1997 revision includes

more new crimes on IP violation

�Other administrative regulations on IP protection by Chinese

central and local governments.

II IP- Laws and Regulations

8

Registration of IPRs under Chinese Law

•Trademarks: China Trademark Office,

or via the WIPO (int’l applications)

•Patent: State Intellectual Property Office

or via the PCT (int’l applications)

•Copyright: Copyright Bureau

•Domain Names: CNNIC

•Customs Protection: General Customs

Administration

2.1 IP-Registration IP in China

2.2 IP-Remedies

Administrative Adjudication (AIC, Trademark Office, Patent Office)

Civil Litigation

Criminal Prosecution

9

Effect:

Compen-

sation

Evidence:

Cost:

Time:

Infringement stopped,

potential infringers

warned off, products

confiscated, license

revoked, fines imposed

No compensation

Evidence less stringent

Low investigation fees, no

court fees / security

Relatively quick

DisadvantagesAdvantages

Effect:

Compen-

sation

Evidence:

Cost:

Time:

Infringement stopped,

potential infringers warned

off

Compensation

possible

Evidence relatively stringent

Court fees, lawyer fees, etc

Lengthy proceedings; IP

jeopardized pending the suit

Provisional measures

(against security)

DisadvantagesAdvantages

10

Effect:

Comp-

ensation

Evidence:

Cost:

Time:

Infringement stopped,

potential infringers warned,

products, tools and unlawful

income confiscated, fines

imposed

No compensation to

claimant

Stringent evidence

High investigation feesno court fees / security

Case by case

DisadvantagesAdvantages

Effect:

Compen-

sation

Evidence:

Cost:

Time:

CivilCrim / Adm

Adm / CrimCivil

Civil / CrimAdm

Crim / CivilAdm / Crim

Crim / CivilAdm / Crim

DisadvantagesAdvantages

11

2.3 IP-Remedies CASE STUDY

Case on trademark:Wholesale dealers sold counterfeit industrial batteries

Company A reported Infringement to Administrative Authorities

Authorities took Administrative Action (confiscation & fines)

Dealers appealed against

Administrative Actions in Court

claiming illegal procedures

Company A assisted with

defense, appeal withdrawn

Company A initiated civil lawsuits

√ lawsuits—manufacturer

×lawsuit -dealer

2.4 IP- strategy

Civil Lawsuit

or

Criminal Prosecution

Prevention

Pre-action Investigation

Administrative Adjudication

12

III Importing Goods to China

(Wine as case study)

� Business Licenses and Permits

� Application for a Registered Chinese Wine Label

� Quality Inspection - CIQ

� Customs Procedures/Forms

� Taxes

� Customs Duties/Website

� Import VAT

� Consumption Tax

� Tax Rate Formulas for Imported Goods

� Tax Rate - Case Study

� Contract Registration

3.1 Business Licensesand Permits (Wine as case study)

� Must be a legally registered PRC enterprise;

� Approval of Business Scope: BOFTEC provides approval for

importation (and domestic sales), and the business scope must

include trading.

� Permit for Wine Sales and Correct Business Scope : AIC grants

permit and the business scope must include the wine sales.

� Import and Export Operations: The enterprise may import the

wine on its own (with the above approvals, permits, and correct

business scope) or consign a separate trading company as its

agent to import the wine.

13

3.2 Application for Registered

Chinese Wine Label (Wine as case study)

An application must be filed with the local inspection & quarantine authority (“CIQ”) to obtain a registered Chinese label. Application documents:

� Business License;� Inspection & Quarantine Report on the quality of the wine;� Photocopy of Permit for Production provided by the wine manufacturer and a

Chinese translation (issued in the country of origin);

� Photocopy of the Health and Sanitation Permit provided by the wine manufacturer and a Chinese translation (issued in the country of origin);

� Photocopy of the Wine Production Process provided by the manufacturer and a Chinese translation;

� Design sample of the wine label in Chinese.

After the abovementioned documents are ready, the CIQ will report to the State CIQ for examination and approval. Upon approval, a Certificate of Approval for a registered Chinese label will be granted. One label may only correspond to one type of wine.

3.3 Quality Inspection - CIQ

Quality Inspection and Customs Declaration of imported goods areconducted simultaneously. The goods will be released by the Customsupon issuance of the clearance certificate from the CIQ. Goods must then also pass the CIQ’s sampling inspection which is done for each shipment received. The CIQ duties include the following:

� Examining the documents relating to the goods, including Sanitation Certificate, Certificate of Origin, Certificate of Quality, etc. issued by the exporting country;

� Whether the package is in compliance with the accepted standards

� Whether the goods have obtained a registered Chinese label (for wine);

� Sampling inspection: To discern whether the goods are in compliance with the sanitation standards of the PRC for imported food, three bottles are selected from each label, within each shipment, for inspection. The process takes about one week to complete.

14

3.4 Customs Procedures

Procedure - Declaration——Inspection——ReleaseDeclaration: Declaration must be made to the Customs by the receiver within14 days of the arrival of the means of transport. Necessary documents include: contracts, invoices, packing list, freight list (cargo manifest), bills of lading, a power of attorney for Customs declaration (if imported by agents), license to import and export, a write-off bill for collection of proceeds in export, and perhaps others.Inspection: Customs may examine whether the goods are in conformity with the documents and impose penalties or delay release if they are not satisfied with the results of their Inspection.

Release: After the consigner or its agent pays in full any tax or duties, the goods will be released by Customs upon obtaining the clearance certificate issued by the CIQ.One common source of delays at Customs is in the determination of the dutiable value of the imported goodsFactors considered by Customs in determining the price include: packaging, label, brand name/trademark. Generally speaking, the grade of the wine is determined by a commercial specification, the brand name, the place of origin, the raw materials used, and the processing method involved in its production.

3.5 Customs Declaration Form

15

3.6 Taxes

Scope of taxable goods: goods being allowed to be imported

into or exported from PRC and entry articles

� Customs Duties

� Import VAT (value added tax)

� Consumption Tax (special goods)

3.7 Customs Duties

Rates:

� Different goods are subject to different tax rates

� The State Council has a Customs duty commission which is responsible for the adjustment and interpretation of taxable items, Customs codes, and Customs duty rates which are published in the Regulations of the People’s Republic of China on Import and Export Duties and the Table of Rates of Import Duties of Entry Articles.

Taxpayer:

� Consignee of imported goods

� Consignor of exported goods

� Owner of imported articles

16

3.8 Customs Website

(Tax Rates Listed)

3.9 Import VAT

Taxable items:

� Sale of Goods

� Processing Services

� Repair and Replacement Services

� Importation of Goods

Taxpayer:

Entities and individuals engaged in any of the abovementioned

operations within the territory of the PRC are considered

taxpayers of VAT.

17

3.9 Import VAT

Rate:

� 17%: Sale or importation of goods (most goods), including wine

� 13%: Food grains, tap water, edible vegetable oil, pesticides and other basic appliances necessary for the production and living of residents

� 0%: Export of goods (unless otherwise provided by the State Council)

Calculation:

� the VAT amount as indicated in the Import VAT Duty Paid Certificate (������������) issued by the Customs is the input tax amount which is allowed to be offset against or be deducted from the output tax amounts

� the payable tax amount = the output tax amount – the input tax amount

3.10 Consumption Tax (Wine as case study)

Scope: Consumption tax only applies to the importation of the following

commodities

� Cigarettes, wine and alcohol (including white wine, rice wine, beer,

other wines, and alcohol), cosmetics, precious jewelry and gems,

firecrackers, skyrockets, finished fuel, automobile tires, motorcycles,

cars, golf carts and golf equipment, top-grade watches, yachts,

wooden throwaway chopsticks, hardwood flooring

Rates: Different commodities are subject to different rates, ranging from 1%

to 45%.

18

3.11 Tax Rate Formulas for

Imported Goods

� Customs Duty: import duty = dutiable value X duty rate

(Dutiable value = total amount payable and actually paid by the buyer to the seller + the freight, the associated expenses, and the insurance premiumsincurred prior to the arrival and unloading of the goods at the destination within PRC).

Customs is entitled to examine the authenticity and exactness of the declared value and is entitled to consult with the related parties on the declared value and adjust the declared value if it deems that the value declared by the related parties is not correct.

� Consumption tax: composite taxable value = (dutiable value + Customs duty) / (1 – consumption tax rate);

payable amount of consumption tax = composite taxable value Xconsumption tax rate;

� VAT = (dutiable value + Customs duty + consumption tax) X VAT rate;

� Total taxable amount = Customs duty + consumption tax + VAT

3.12 Tax Rate - Case Study (Wine as case

study)

Enterprise A (domestic) imports wine with a dutiable value of RMB 1,000,000.

(Note: assuming that the Customs Duty rate is 14%, the VAT rate is 17% and the Consumption Tax rate is 10%)

� Customs Duty: RMB 1,000,000 X 14% = RMB140,000;

� Composite taxable value : (RMB 1,000,000 + RMB 140,000) / (1 - 10%) = RMB 1,266,667

� Consumption tax: RMB 1,266,667 X 10% = RMB 126.667

� VAT: RMB (1,000,000 + 140,000 + 126.667) X 17% = RMB 215,333;

� Total Tax = RMB140,000 + RMB126,667 + RMB215,333 = RMB 482,000

19

3.13 Contract Registration

Import enterprises must register contracts involving advance payments on the sales of exported goods and deferred payments regarding imported goods on the official website designated by the State Administration of Foreign Exchange (SAFE).

� The term “deferred payment” refers to a payment made through foreign exchange on a date stipulated in a COD (cash on delivery) import contract which is later than the date of the importation of the goods, as stipulated in the contract, or which is made on a date more than 90 days later than the date of the actual importation

� Deadlines for contract registration

1. Within 15 working days of execution of the contract; or

2. Within 15 working days, of the end of a 90 day period from the date when Customs approves the import goods declaration form.

IV Enterprise Income Tax Law

� Reasons for the Enterprise Income Tax Law (EIT)

� Tax Rates

� Taxable Income Amount and Deductions

� Changes in Preferential Tax Treatment

� Technology Transfer and R & D

� Advance Pricing Agreements and Investigations

20

4.1 EIT-Reasons for the EIT Law:

� Unify the income tax processes of both domestic enterprises and foreign invested enterprises

� Unify and standardize the procedures and criteria used for pre-tax deductions

� Implement a preferential tax policy: priority is being given to specific industries for preferential tax treatment and the prior practice of preferential treatment based on the region an enterprise is located is now secondary

4.2 EIT-Tax Rate

� General tax rate 25%- PRC registered enterprises

� Small/Low-profit enterprises 20% (enterprises must not have more than RMB 300,000 in annual taxes, no more than 100 employees, and assets exceeding RMB 30m)

- PRC registered enterprises� Specific New and Hi-tech enterprises 15%

(enterprises must meet standards regarding investment, employment of skilled workers, and levels of income to qualify as a New or Hi-tech enterprise)

- PRC registered enterprises� Withholding income tax: 10%

- Foreign registered enterprises

21

4.3 EIT-Taxable Income Amount and

Deductions

� Taxable amount of income = total amount of income each tax year = tax-free income = tax-exempt income = all deduction items = any remedies for the losses of the previous year(s)

� Tax-free income: proceeds not originating from business activities (Article 7 of the EIT )

Example: VAT rebates

� Tax-exempt income: preferential tax treatment provided for in specific situations (Article 26 of the EIT, Article 83 of the Regulation on the Implementation of the EIT)

Example: treasury debts, qualified dividends, profit distribution, and other returns on equity investments between domestic enterprises.

� Business entertainment expenses may also now be deducted up to a maximum of 0.5% (Article 43 of the EIT)

4.4 EIT-Changes in Preferential Tax

Treatment

Article 53 stipulates that specific

measures for preferential tax treatment

and the right to reduce or exempt tax

shall be subject to the approval of the

State Council. Local authorities have no right to reduce or exempt tax.

22

4.4 EIT-Changes in Preferential Tax

Treatment

Examples of Preferential Tax Treatment which have been cancelled:

1. Preferential tax rates of 15% and 24% in special economic zones, costal economic and technical development zones, and in the initial development of riverside cities, etc.