powerpoint presentation · global deals peak in 2018, decline in 1h-2019 global vc, pe, and ma deal...

TRANSCRIPT

Fintech DecodedA biannual report tracking investment activity in Fintech companies

1H-2019

CONTENTS

01 GLOBAL

Global Fintech deals peak in 2018, decline in 1H-2019

Steep drop in early stage deal volume; deal activity resilient in late-stage VC

Median deal sizes continue to grow

02 AMERICAS

North America continues to witness surge in VC funding

Marginal decrease in median deal sizes

Mega deals boost funding in Lending and Payments

03 EUROPE

Fintech funding in Europe on track to reach record high in 2019

Lending, Insurance, and Business Solutions deals grow in value, but shrink in volume

Better funding activity in Payments and Financial Markets in 1H-2019 after slump in 2018

04 ASIA

VC funding deal activity drops to lowest level since 2014

Deal activity declines across stages, but most in early stage

All major Fintech verticals witness steep decline in funding

Executive Summary

Overall the VC funding activity in the Fintech sector has increased from $7.5 billion in 1H-2017 reaching

$11.1 billion in 1H-2019. Payments segment which has been the most significant contributor to Fintech

universe is showing signs of maturity as the late stage companies are attracting bulk of the funding.

Companies such as Margeta, N26 and Chime have each raised over $200 million in funding. Interestingly,

UK based start-up, Checout.com, raised $230 million in Series A funding at $2 billion post-money valuation

for expansion of Payments services in Latin America and Asia.

On the other hand, ‘financial markets’ vertical (companies focused on developing solutions for capital

market participants) has attracted majority of the funding in the early stages. Interestingly, Carta, raised

$300 million to build a stock market for private companies.

The funding activity in the technology enabled lending space has been declining Q-o-Q due to the

tightening of regulations in emerging markets such as China (world’s largest P2P lending market) where

the government has taken an initiative to crackdown P2P lending companies after the recent defaults.

However, the student lending platforms continue to attract VC funding. Companies such as SoFi and

Affirm have recently raised $500 million and $300 million respectively and are planning to offer wealth

management services to their borrowers.

Challenger banks and Neo-banks have prominently been on the investor’s radar due to their innovative

service delivery models. The funding is still at a nascent stage as regulations are shaping up. The concept

of branchless banking has sprung across the globe and we are seeing companies targeting banked and

unbanked customers offering product and service customization. These businesses are focused, providing

a step beyond the current banking system by leveraging technology to reduce operating costs, improve

service quality, and expand the customer reach.

Welcome to the first edition of Aranca’s

‘Fintech Decoded’ report, a bi-annual

publication where we highlight some major

trends in VC funding within broader

Fintech universe across key markets in

first half of 2019.

The outlook for the Fintech space

continues to be highly positive with the

rapid innovation in payments and

transformation in digital banking arena.

With increased regulatory pressure, deal

activity in first half of 2019 indicates

investors have become cautious in funding

businesses in sectors like lending and

crypto currency That said, astute investors

continue to back innovative companies

catering to targeted customer segments or

expanding into untapped geographies.

We hope you will find this edition an

interesting and informative read.

Fintech

In 1H-2019, investment

in Fintech companies

globally clocked

$38.8Bacross

688 deals

Global deals peak in 2018, decline in 1H-2019

Global VC, PE, and MA deal landscape in Fintech companies

57.4

96.8

76.2 71.1

141.0

38.8

39

1,206

1,491 1,503

1,6341,712

688

1,376

2014 2015 2016 2017 2018 2019*

Capital Invested ($B) Projected 2H19 Deal Count Projected 2019

January 01, 2014 – June 30, 2019

After a smashing 2018, which witnessed a

record number of mega deals ($100M+)

and super-size deals ($1B+), investment

activity (PE, VC, and M&A) in the global

Fintech landscape for 1H-2019 declined,

but remains higher than 2017 in terms of

the aggregate deal value. 1H-2019

registered the lowest number of deals

since 2014, yet median deal values

continue to surge, indicating a fairly strong

undercurrent for consolidation and maturity

in certain key segments

Currency in US$, unless specified

Data Source: Pitch Book, unless specified otherwise

Note: Please refer to the Methodology section at the end of the report to understand the Fintech universe and its constituents as defined

from perspective of this report as well as data analysis approach and 2019* calculation

Fintech

In 1H-2019, VC Funding

in Fintech companies

globally clocked

$11.1Bacross

603 deals

Consistent drop in deal volume; deal sizes continue

to grow

Global VC funding in Fintech companies

2.2 2.2 1.6 3.3 2.84.7

8.9

3.04.4

8.54.5

3.2 3.25.2 4.4 6.3 5.9

6.7

6.25.0 5.0 6.1

14

272 236 256 264 296 306 338 307 334 333293 306

356 332 330 347 379 396335 311 321

282

Q1 Q2 Q3 Q4 Q1 Q2 Q3 Q4 Q1 Q2 Q3 Q4 Q1 Q2 Q3 Q4 Q1 Q2 Q3 Q4 Q1 Q2

2014 2015 2016 2017 2018 2019

Capital Invested ($B) Ant Financial Deal Count

January 01, 2014 – June 30, 2019

1.5 1.81.3

2.0 2.2 2.0 2.2 1.9 2.2 2.02.5 2.2 2.1 2.5

3.2 3.03.9

4.8 4.9 4.7

3.5

5.0

Q1 Q2 Q3 Q4 Q1 Q2 Q3 Q4 Q1 Q2 Q3 Q4 Q1 Q2 Q3 Q4 Q1 Q2 Q3 Q4 Q1 Q2

2014 2015 2016 2017 2018 2019

Median Deal Size ($M)

Considering the last five quarters, the

number of VC-backed funding deals

declined for the fourth time in 2Q-2019 to

282 deals; a fall of 29% from the peak

value in Q1-2018. On the other hand,

median deal size trends continued to rise,

reaching $5.0M in 2Q-2019, more than

doubling from $2.2M just ten quarters ago.

Discounting the super-mega Ant Financial

deal, if the funding activity in terms of the

overall deal value in 1H-2019 holds for the

second half of the year, it is likely to be

another robust year for Fintech globally.

Data Source: Pitch Book, unless specified otherwise

Note: Please refer to the Methodology section at the end of the report to understand the Fintech universe and its constituents as defined

from perspective of this report as well as data analysis approach

Currency in US$, unless specified

0.81.0

1.3 1.21.6

0.5

0.5

2014 2015 2016 2017 2018 2019

3.25.6

7.7 8.210.3

3.6

3.6

2014 2015 2016 2017 2018 2019

5.3

12.6 11.7 9.7

26.0

7.1

7.1

2014 2015 2016 2017 2018 2019

426

503576 581

542504

213

2014 2015 2016 2017 2018 2019

512

366

477 482

577 648

256

2014 2015 2016 2017 2018 2019

269 268

159

194 203

246269

134

2014 2015 2016 2017 2018 2019

Steep drop in early stage; deal activity resilient in

late-stage VC

Global VC funding in Fintech companies January 01, 2014 – June 30, 2019

Decline in the angel/seed and early stage

VC funding in the 1H-2019 was too steep

to be considered a part of the usual

volatility in deal activity. Early-stage

funding activity in Fintech in 2Q-2019 has

been the lowest in the last eight quarters,

in terms of overall funding and the number

of deals. Late-stage deal activity continues

to remain strong as the number of mega

deals (>$100M) reached 26 in 1H-2019

alone, compared with 36 in entire 2018. In

fact, if this trend sustains, ignoring the Ant

Financial deal outlier, 2019 is likely to be

the best year for late-stage VC funding in

Fintech. These two trends arguably

indicate early signs of maturity. We believe

a huge untapped market potentially still

exists in Asia, particularly in India.

Capital Invested ($B) Projected 2H19 Deal Count ($M) Projected 2019

Angel/Seed Early Stage VC Later Stage VC

* * *

***

Currency in US$, unless specified

Data Source: Pitch Book, unless specified otherwise

Note: Please refer to the Methodology section at the end of the report to understand the Fintech universe and its constituents as defined

from perspective of this report as well as data analysis approach and 2019* calculation

Median deal sizes continue to grow

Global VC funding median deal size by funding stage

0.6 1.0 1.0 1.3 1.5 1.5

13.6

20.5

13.813.1

20.019.0

4.0 4.2 4.5 4.5

7.45.9

2014 2015 2016 2017 2018 2019

Angel/Seed Later Stage VC Early Stage VC

January 01, 2014 – June 30, 2019

Currency in US$, unless specified

Data Source: Pitch Book, unless specified otherwise

Note: Please refer to the Methodology section at the end of the report to understand the Fintech universe and its constituents as defined from perspective of this report as well as data analysis approach

Top 10 Global VC Funding Deals in Fintech

Top 10 VC funding deals in Fintech, Global

S.no Region Name VerticalsDeal

Size ($M)Key Investors

Post Money Valuation

($ B)

1 US SoFi Lending 500 Manhattan Venture Partners, Next Ventures 4.80

2 Germany N26 Payments 300Government of Singapore Investment Corporation,

Insight Partners3.50

3 US Affirm Lending 300 Baillie Gifford, Fidelity Management & Research 3.00

4 US Lemonade Insurance 300 OurCrowd, Annox Capital 2.10

5 US Carta Financial Markets 300 Alumni Ventures Group, Andreessen Horowitz 1.70

6 US Marqeta Payments 260 Coatue Management, Geodesic Capital 1.89

7 UK Checkout.com Payments 230 Blossom Capital, DST Global 2.00

8 US Chime Bank Payments 200 Coatue Management, Dragoneer Investment Group 1.30

9 Brazil Creditas Lending 200 SoftBank Group, Amadeus Capital Partners 0.73

10 US Divvy Business Solutions 200 New Enterprise Associates, Insight Partners 0.80

January 01, 2019 - June 30, 2019

Data Source: Pitch Book, unless specified otherwise

Note: Please refer to the Methodology section at the end of the report to understand the Fintech universe and its constituents as defined from perspective of this report as well as data analysis approach

6.1

9.68.1 7.7

13.7

6.8

6.8

2014 2015 2016 2017 2018 2019

1.4 6.810.5

7.2 6.1

1.2

14

1.2

2014 2015 2016 2017 2018 2019

1.62.4

1.7

3.8 3.5 3.0

3.0

2014 2015 2016 2017 2018 2019

831760

624675

616685

380

2014 2015 2016 2017 2018 2019

238

104

114

212 215201

238

52

2014 2015 2016 2017 2018 2019

287320

252294

363413

287

160

2014 2015 2016 2017 2018 2019

VC Funding: Europe completes strongest half year;

numbers plummet in Asia

Global VC funding (# of deals) in Fintech companiesJanuary 01, 2014 – June 30, 2019

Fintech VC funding in Europe is likely to

see the best year based on the robust deal

activity in 1H-2019. 1H-2019 witnessed

seven mega deals ($100 M+), the same as

those in the entire year in 2018. While

growth is seen across all stages, late-

stage VC funding in European Fintech

companies in the first six months of 2019

has already surpassed the entire amount

recorded in 2018, with the median deal

size reaching its highest peak. Fintech deal

activity in 1H-2019 in North America

continues to remain strong, with an

increase in late stage and a corresponding

decrease in early stage. Turmoil in China’s

P2P lending space dragged down the

overall Fintech funding in Asia to its lowest

since 2015.

Americas Asia Europe

Capital Invested ($B) Projected 2H19 Deal Count ($M) Projected 2019 Ant Financial ($B)

* * *

* * *

Currency in US$, unless specified

Data Source: Pitch Book, unless specified otherwise

Note: Please refer to the Methodology section at the end of the report to understand the Fintech universe and its constituents as defined

from perspective of this report as well as data analysis approach and 2019* calculation

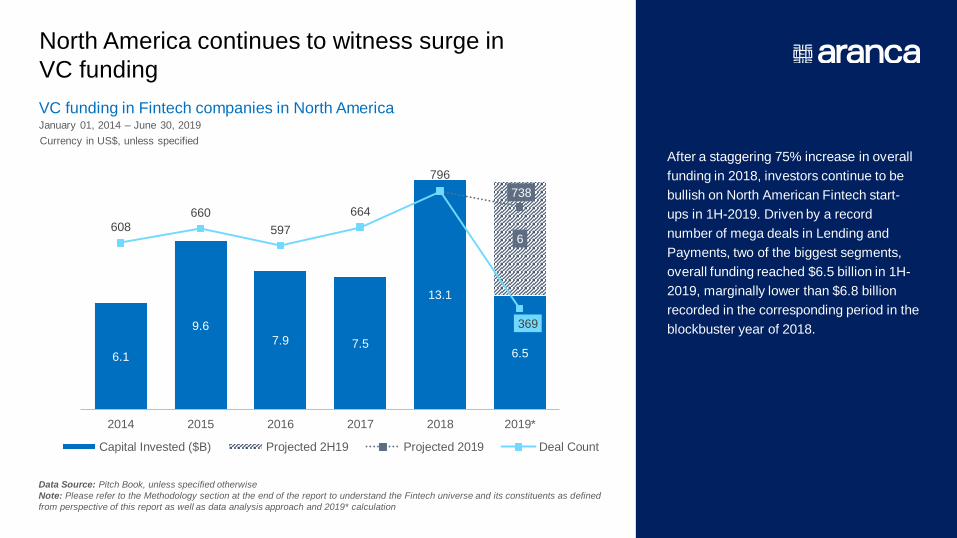

In 1H-2019, VC Funding

in Fintech companies in

North America clocked

$6.5Bacross

369 dealsFintech

North America continues to witness surge in

VC funding

VC funding in Fintech companies in North America

6.1

9.6

7.9 7.5

13.1

6.5

6

738

608

660

597

664

796

369

2014 2015 2016 2017 2018 2019*

Capital Invested ($B) Projected 2H19 Projected 2019 Deal Count

January 01, 2014 – June 30, 2019

After a staggering 75% increase in overall

funding in 2018, investors continue to be

bullish on North American Fintech start-

ups in 1H-2019. Driven by a record

number of mega deals in Lending and

Payments, two of the biggest segments,

overall funding reached $6.5 billion in 1H-

2019, marginally lower than $6.8 billion

recorded in the corresponding period in the

blockbuster year of 2018.

Currency in US$, unless specified

Data Source: Pitch Book, unless specified otherwise

Note: Please refer to the Methodology section at the end of the report to understand the Fintech universe and its constituents as defined

from perspective of this report as well as data analysis approach and 2019* calculation

304305 320280 295 322

152

2014 2015 2016 2017 2018 2019

280

189221

202242

334

140

2014 2015 2016 2017 2018 2019

140154

114 119 115127

140

77

2014 2015 2016 2017 2018 2019

0.5 0.6 0.6 0.7

1.0

0.3

0.3

2014 2015 2016 2017 2018 2019

1.42.6 3.1 2.6

5.5

1.9

1.9

2014 2015 2016 2017 2018 2019

4.16.3

4.2 4.3

6.6

4.2

4.2

2014 2015 2016 2017 2018 2019

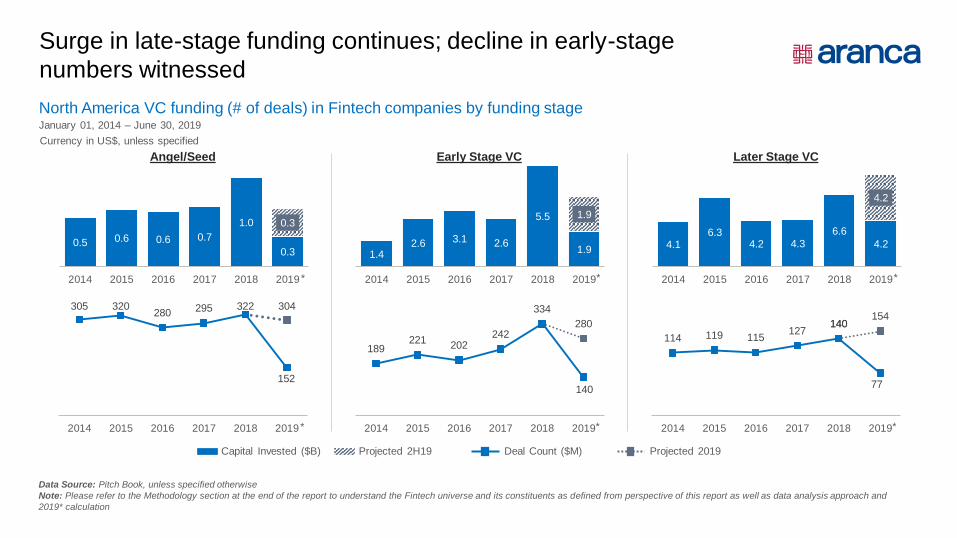

Surge in late-stage funding continues; decline in early-stage

numbers witnessed

North America VC funding (# of deals) in Fintech companies by funding stageJanuary 01, 2014 – June 30, 2019

Angel/Seed Early Stage VC Later Stage VC

Capital Invested ($B) Projected 2H19 Deal Count ($M) Projected 2019

* * *

* * *

Currency in US$, unless specified

Data Source: Pitch Book, unless specified otherwise

Note: Please refer to the Methodology section at the end of the report to understand the Fintech universe and its constituents as defined from perspective of this report as well as data analysis approach and

2019* calculation

Marginal decrease in median deal sizes

North America VC funding median deal size by funding stage

0.8 1.3 1.1 1.5 1.6 1.5

3.5

5.36.0 6.0

9.0

7.0

16.5

21.0

15.014.0

20.0

16.5

2014 2015 2016 2017 2018 2019

Angel/Seed Early Stage VC Later Stage VC

January 01, 2014 – June 30, 2019

Currency in US$, unless specified

Data Source: Pitch Book, unless specified otherwise

Note: Please refer to the Methodology section at the end of the report to understand the Fintech universe and its constituents as defined from perspective of this report as well as data analysis approach

Top 10 VC Funding Deals in North America

Top 10 VC funding deals in Fintech, North AmericaJanuary 01, 2019 - June 30, 2019

Data Source: Pitch Book, unless specified otherwise

Note: Please refer to the Methodology section at the end of the report to understand the Fintech universe and its constituents as defined from perspective of this report as well as data analysis approach

S.no Region Name VerticalsDeal

Size ($M)Key Investors

Post Money Valuation

($ B)

1 US SoFi Lending 500 Manhattan Venture Partners, Next Ventures 4.80

2 US Affirm Lending 300 Baillie Gifford, Fidelity Management & Research 3.00

3 US Lemonade Insurance 300 OurCrowd, Annox Capital 2.10

4 US Carta Financial Markets 300 Alumni Ventures Group, Andreessen Horowitz 1.70

5 US Marqeta Payments 260 Coatue Management, Geodesic Capital 1.89

6 US Chime Bank Payments 200 Coatue Management, Dragoneer Investment Group 1.30

7 US Divvy Business Solutions 200 New Enterprise Associates, Insight Partners 0.80

8 US Acoms Financial Markets 180 BlackRock, Comcast Ventures 0.87

9 USBranch

InternationalLending 170 B Capital Group, Foundation Capital 0.27

10 US Stripe Payments 140 DST Global, Proioxis Ventures 22.5

1.4

3.4

2.2 2.21.8 1.7

1.7

2014 2015 2016 2017 2018 2019

110 116106

125

99 97

58

2014 2015 2016 2017 2018 2019

1.2 0.91.3 1.3

2.01.4

1.4

2014 2015 2016 2017 2018 2019

111130

122113

102

122111

65

2014 2015 2016 2017 2018 2019

Mega deals boost funding in Lending and Payments

North America VC funding, Fintech - Lending and PaymentsJanuary 01, 2014 – June 30, 2019

While the total number of deals in Lending

did not increase drastically, a steep fall has

been witnessed in the Early Stage, with a

corresponding increase in the Late Stage.

Furthermore, the size of the mega rounds

keeps growing as the top four deals

contributed $1.10 billion of the $1.66 billion

funding in 1H-2019. A similar trend can be

observed in VC funding in Payments,

wherein six mega deals contributed $0.90

billion of the $1.45 billion received from 65

deals. Investors continued to be bullish on

North American Fintech start-ups in 1H-

2019.

Capital Invested ($B) Projected 2H19 Deal Count ($M) Projected 2019

Lending

Payments

*

* *

*

Currency in US$, unless specified

Data Source: Pitch Book, unless specified otherwise

Note: Please refer to the Methodology section at the end of the report to understand the Fintech universe and its constituents as defined

from perspective of this report as well as data analysis approach and 2019* calculation

Surge in Regtech VC funding: 2019 slated to be best year

North America VC funding, Fintech – Regtech

0.20.1

0.20.1

0.2 0.2

0.2

2014 2015 2016 2017 2018 2019

January 01, 2014 – June 30, 2019

25

36

16 1822

25 25

18

2014 2015 2016 2017 2018 2019

*

*

Currency in US$, unless specified

Data Source: Pitch Book, unless specified otherwise

Note: Please refer to the Methodology section at the end of the report to understand the Fintech universe and its constituents as defined from perspective of this report as well as data analysis approach and

2019* calculation

Capital Invested ($B) Projected 2H19 Deal Count ($M) Projected 2019

0.30.7

1.10.7

1.8

0.6

0.6

2014 2015 2016 2017 2018 2019

1.2

2.0

1.2 1.2

2.0

0.7

0.7

2014 2015 2016 2017 2018 2019

69

52

28

55 58

74 69

26

2014 2015 2016 2017 2018 2019

107 10692 92

86

102 107

53

2014 2015 2016 2017 2018 2019

Significant slowdown witnessed in funding in Insurance Tech

and Business Solutions

North America VC funding, Fintech – Insurance and Business SolutionsJanuary 01, 2014 – June 30, 2019

Insurance Business Solutions

Capital Invested ($B) Projected 2H19 Deal Count ($M) Projected 2019

*

*

*

*

Currency in US$, unless specified

Data Source: Pitch Book, unless specified otherwise

Note: Please refer to the Methodology section at the end of the report to understand the Fintech universe and its constituents as defined from perspective of this report as well as data analysis approach and

2019* calculation

In 1H-2019, VC Funding

in Fintech companies in

Europe clocked

$3.0Bacross

160 dealsFintech

Fintech funding in Europe to reach record high

in 2019

VC funding in Fintech companies in Europe

1.6

2.41.7

3.8 3.53.0

3.0

320

252

294

363413

287

160

2014 2015 2016 2017 2018 2019*

Capital Invested ($B) Projected 2H19 Projected 2H19 Deal Count

January 01, 2014 – June 30, 2019

Europe is witnessing staggering growth in

VC funding in Fintech, and 2019 may as

well be a blockbuster year based on robust

1H deal activity. While seven mega deals

($100M+) were registered in the first six

months, compared with the same number

recorded in the entire year in 2018, growth

is much more broad based, encompassing

all Fintech verticals and funding stages.

Median deal sizes have grown four times

since 2014, to around $4 million in 1H-

2019.

Currency in US$, unless specified

Data Source: Pitch Book, unless specified otherwise

Note: Please refer to the Methodology section at the end of the report to understand the Fintech universe and its constituents as defined

from perspective of this report as well as data analysis approach and 2019* calculation

96

124143

169157

96

48

2014 2015 2016 2017 2018 2019

152

101121

159

195

133

76

2014 2015 2016 2017 2018 2019

58

72

27 3035

61 58

36

2014 2015 2016 2017 2018 2019

0.10.2

0.40.3

0.2

0.1

0.1

2014 2015 2016 2017 2018 2019

0.71.1

0.81.3

1.7

1.0

1.0

2014 2015 2016 2017 2018 2019

0.8 1.20.5

2.21.6 1.9

1.9

2014 2015 2016 2017 2018 2019

Late-stage funding witnessed explosive growth in 1H-2019

Europe VC funding (# of deals) in Fintech companies by funding stageJanuary 01, 2014 – June 30, 2019

Angel/Seed Early Stage VC Later Stage VC

Capital Invested ($B) Projected 2H19 Deal Count ($M) Projected 2019

*

*

*

*

*

*

Currency in US$, unless specified

Data Source: Pitch Book, unless specified otherwise

Note: Please refer to the Methodology section at the end of the report to understand the Fintech universe and its constituents as defined from perspective of this report as well as data analysis approach and

2019* calculation

Median deal sizes in late-stage companies peak at record levels

Europe VC funding median deal size by funding stage

0.5 0.7 0.8 1.21.4 1.2

2.5 2.5 2.2 2.6

4.9 4.8

9.1

15.7

9.0

11.5 11.4

19.0

2014 2015 2016 2017 2018 2019

Angel/Seed Early Stage VC Later Stage VC

January 01, 2014 – June 30, 2019

Data Source: Pitch Book, unless specified otherwise

Note: Please refer to the Methodology section at the end of the report to understand the Fintech universe and its constituents as defined from perspective of this report as well as data analysis approach

Top 10 VC Funding Deals in Europe

Top 10 VC funding deals in Fintech, EuropeJanuary 01, 2019 - June 30, 2019

Data Source: Pitch Book, unless specified otherwise

Note: Please refer to the Methodology section at the end of the report to understand the Fintech universe and its constituents as defined from perspective of this report as well as data analysis approach

S.no Region Name VerticalsDeal

Size ($M)Key Investors

Post Money Valuation

($ B)

1 Germany N26 Payments 300Government of Singapore Investment Corporation,

Insight Partners3.50

2 U.K. Checkout.com Payments 230 Blossom Capital, DST Global 2.00

3 U.K. Iwoca Lending 196 Augmentum (London), Intesa Sanpaolo 0.10

4 Sweden Lendify Lending 160 Insight Investment, Anders Borg 0.09

5 U.K. Monzo Personal Finance 147 Latitude, Y Combinator 2.33

6 Germany Wefox Insurance 125 CreditEase, Mubadala Investment Company -

7 Germany Raisin Lending 117Goldman Sachs Principal Strategic Investments,

Orange Digital Ventures0.78

8 U.K. Starling Bank Payments 98 Merian Chrysalis Investment, Merian Global Investors 0.17

9 France PayFit Business Solutions 82 Bpifrance, Eurazeo -

10 U.K. GoCardless Payments 76 National Grid Partners, Adams Street Partners -

36 38

20

37

47 46

19

2014 2015 2016 2017 2018 2019

34

34

1116

28

44

34

17

2014 2015 2016 2017 2018 2019

4640

6166 75

65

46

20

2014 2015 2016 2017 2018 2019

0.1 0.10.2

0.30.4 0.3

0.3

2014 2015 2016 2017 2018 2019

0.0 0.00.1

0.40.5

0.4

0.4

2014 2015 2016 2017 2018 2019

0.3

1.4

0.5

1.0

0.50.7

0.7

2014 2015 2016 2017 2018 2019

Lending, Insurance, and Business Solutions deals grow in

value, but shrink in volume

Europe VC funding, Fintech – Lending, Insurance and Business Solutions January 01, 2014 – June 30, 2019

Capital Invested ($B) Projected 2H19 Deal Count ($M) Projected 2019

*

*

*

*

*

*

Currency in US$, unless specified

Business Solutions Insurance Lending

Data Source: Pitch Book, unless specified otherwise

Note: Please refer to the Methodology section at the end of the report to understand the Fintech universe and its constituents as defined from perspective of this report as well as data analysis approach and

2019* calculation

0.2 0.2 0.2

0.3 0.30.3

0.3

2014 2015 2016 2017 2018 2019

0.80.6

0.4

1.20.9 0.9

0.9

2014 2015 2016 2017 2018 2019

37

60

38

50

59 65

3730

2014 2015 2016 2017 2018 2019

51

6864 66 69 75

51

34

2014 2015 2016 2017 2018 2019

Better funding activity in Payments and Financial Markets in

1H-2019 after slump in 2018

Europe VC funding, Fintech – Financial Markets and Payments January 01, 2014 – June 30, 2019

Financial Markets Payments

Capital Invested ($B) Projected 2H19 Deal Count ($M) Projected 2019

* *

* *

Currency in US$, unless specified

Data Source: Pitch Book, unless specified otherwise

Note: Please refer to the Methodology section at the end of the report to understand the Fintech universe and its constituents as defined from perspective of this report as well as data analysis approach and

2019* calculation

In 1H-2019, VC Funding

in Fintech companies in

Asia clocked

$1.2Bacross

52 dealsFintech

VC funding deal activity drops to lowest level

since 2014

VC funding in Fintech companies in Asia

1.4

6.8

10.5

7.26.1

1.2

14.0

1.2

104

114

212 215201

237

52

2014 2015 2016 2017 2018 2019*

January 01, 2014 – June 30, 2019

Sharp decline in funding in Asian Fintech

companies was witnessed in 1H-2019 in

the key markets of China and India as the

number of deals plummeted. Turmoil in

China’s P2P lending vertical amid

tightening regulatory norms hit funding

activity across early-stage and late-stage

segments. After a record number of deals

in 2018, India witnessed a plunge in the

number of Fintech deals. The only silver

lining was continued growth in median deal

sizes. It would be interesting to see

whether deal activity rebounds in the

coming quarters.

Capital Invested ($B) Projected 2H19 Deal Count ($M) Projected 2019 Ant Financial ($B)

Currency in US$, unless specified

Data Source: Pitch Book, unless specified otherwise

Note: Please refer to the Methodology section at the end of the report to understand the Fintech universe and its constituents as defined

from perspective of this report as well as data analysis approach and 2019* calculation

16

46

74

87

5863

8

2014 2015 2016 2017 2018 2019

6055

10089

99

121

30

2014 2015 2016 2017 2018 2019

54

28

13

38 3944

54

14

2014 2015 2016 2017 2018 2019

0.20.2

0.20.1

0.3

0.1

0.1

2014 2015 2016 2017 2018 2019

1.01.7

3.7 4.0

2.4

0.50.5

2014 2015 2016 2017 2018 2019

0.3 4.86.7

3.1 3.30.6

14.0

0.6

2014 2015 2016 2017 2018 2019

Deal activity declines across stages, but most in early stage

Asia VC funding (# of deals) in Fintech companies by funding stageJanuary 01, 2014 – June 30, 2019

Angel Seeds Early Stage VC Later Stage VC

*

*

*

*

*

*

Capital Invested ($B) Projected 2H19 Deal Count ($M) Projected 2019 Ant Financial ($B)

Currency in US$, unless specified

Data Source: Pitch Book, unless specified otherwise

Note: Please refer to the Methodology section at the end of the report to understand the Fintech universe and its constituents as defined from perspective of this report as well as data analysis approach and

2019* calculation

Median deal sizes witness sharp decline from peak in 2018

Asia VC funding median deal size by funding stage

0.7 1.0 1.0 1.01.5

2.8

10.0

5.0

7.35.6

10.0

5.5

10.0

30.8

15.0

20.8

37.7

27.8

2014 2015 2016 2017 2018 2019

Angel/Seed Early Stage VC Later Stage VC

January 01, 2014 – June 30, 2019

Currency in US$, unless specified

Data Source: Pitch Book, unless specified otherwise

Note: Please refer to the Methodology section at the end of the report to understand the Fintech universe and its constituents as defined from perspective of this report as well as data analysis approach

Top 10 Global VC Funding Deals in Asia

Top 10 VC funding deals in Fintech, AsiaJanuary 01, 2019 - June 30, 2019

Data Source: Pitch Book, unless specified otherwise

Note: Please refer to the Methodology section at the end of the report to understand the Fintech universe and its constituents as defined from perspective of this report as well as data analysis approach

S.no Region Name VerticalsDeal

Size ($M)Key Investors

Post Money Valuation

($ B)

1 China Momo (Application Software) Payments 100Warburg Pincus, Goldman Sachs Merchant Banking

Division-

2 ChinaShanghai Dianrong Financial

Information ServicesLending 100 Affirma Capital, Dalian Finance Industry Investment Group -

3 Indonesia Akulaku Business Solutions 100 Ant Financial, Blue Sky Alternative Investments 0.45

4 China Wiseco Technology Lending 95 China Growth Capital, Green Pine Capital Partners -

5 India InCred Finance Lending 83 - -

6 Singapore GoBear Lending 80 Aegon, Walvis Group -

7 China Shuidichou Lending 74 Yuri Milner, Dianping.com -

8 India Acko General Insurance Insurance 65 Intact Ventures, RPS Ventures 0.30

9 China BangSun Technology RegTech 51 VT Ventures, Xinhu Zhongbao Company -

10 China Lupu Investment Financial Markets 45 Duane Kuang -

20

14

8

14

2320

7

2014 2015 2016 2017 2018 2019

33

16

25

52

40 40

33

8

2014 2015 2016 2017 2018 2019

78

3034

66 6959

78

15

2014 2015 2016 2017 2018 2019

0.1 2.0

5.1

2.5

0.60.1

0.1

2014 2015 2016 2017 2018 2019

0.3

1.71.2

2.6

1.30.2

0.2

2014 2015 2016 2017 2018 2019

0.8

2.1

3.4

1.01.8

0.40.4

2014 2015 2016 2017 2018 2019

All major verticals witness steep decline in funding

Asia VC funding, Fintech – Diverse VerticalsJanuary 01, 2014 – June 30, 2019

Capital Invested ($B) Projected 2H19 Deal Count ($M) Projected 2019

Business Solutions Payments Lending

* * *

* * *

Currency in US$, unless specified

Data Source: Pitch Book, unless specified otherwise

Note: Please refer to the Methodology section at the end of the report to understand the Fintech universe and its constituents as defined from perspective of this report as well as data analysis approach and

2019* calculation

Methodology

The underlying deal data used in the report was sourced from Pitchbook. Only transactions with a ‘Completed’ status were considered.

Fintech Data Selection Criteria

All transactions that were classified under the “Fintech” vertical by Pitchbook were selected. In addition, we also considered transactions based on search results that

included keys words such as Fintech, financial technology; finance technology, financial service technology, etc.

We also specifically reviewed the details such as original classification, business description, nature of deal, deal value for all transactions with deal value greater

than or equal to $1 billion using publicly available articles and/or company website. This was then used to make the reasonable judgment for their inclusion or

otherwise within the broader Fintech universe as well as the within different verticals/segments therein.

Categorization of Deal Type

For the purposes this report, our focus on Fintech deals is primarily three deal types as per Pitchbook classification: venture capital (VC), private equity (PE), and

mergers and acquisitions (M&As). All others deal types classifications including but not limited to “accelerator/incubator, secondary transaction, debt financed, publicly

listed, joint venture (JV), and others” are not included in the analysis of this report.

Venture Capital

For the purpose of this report, we observed the Deal Type and Deal Universe reported by Pitchbook for each deal. Based on Aranca’s analysis the deals tagged as

“early stage VC, late stage VC, angel (individual), restart-angel, seed round and Corporate” were classified as VC deals.

Venture Capital Stages

Angel/seed deals include deals tagged by Pitchbook as angel (individual) and seed round.

Early-stage deals include deals tagged by Pitchbook as early stage, which mostly include Series A and Series B companies. VC corporate deals with size less than $5

million that did not contain any specific tag for early or late stage (about 1% of total VC deals) within Pitchbook data were categorized as “early stage”.

Late-stage deals include deals tagged by Pitchbook as “late stage”, which typically represent Series C (and above) transactions. Furthermore, in absence of specific

classification, VC Corporate deals with size greater than or equal to $5 million (about 1% of total VC deals) were categorized as “late stage”.

In the report, Accelerator/Incubator is not a part of the VC universe.

Methodology (continued)

Categorization of Industry Segments

All Fintech deals have been classified under nine segments, namely, payments, lending, insurance, financial markets (wealth management and capital markets),

personal finance, business solutions, RegTech, real estate/mortgage, and Blockchain/crypto.

The companies have been classified based on the business description provided by Pitchbook or the company website.

1. Payments: Companies that provide money transfer and payment solutions, point-of-sale (PoS) systems, wallets, credit cards, etc.

2. Lending: Companies that provide loans or a marketplace for lending, working capital and any other type of business financing, crowdfunding, peer-to-peer (P2P)

lending, etc.

3. Insurance: Companies that provide insurance or provide technology/marketplace for all types of insurance products, insurance-enabling solutions, etc.

4. Financial Markets (Wealth Management and Capital Markets): Companies that provide portfolio management and advisory services, financial data and analytics,

trading or brokerage firms, investment management firms, etc.

5. Personal Finance: Companies that provide budget management apps, expense trackers, financial literacy apps, etc.

6. Business Solutions: Companies that provide business-process-enabling systems or technology such as accounting, payroll systems, and companies that do not

fall under any of the above categories

7. RegTech: Companies that provide solutions for risk management, regulatory compliance, assistance in audit, etc.

8. Real Estate/Mortgage: Companies that provide real estate advisory, rent payment solutions, any mortgage-related tech, etc.

9. Blockchain/Crypto: Companies offer Cryptocurrency/Blockchain related services or technology

2019 Full year calculation

The full year 2019 data provided in the charts is arrived at by annualizing 1H 2019 data and are not informed estimates. It is to facilitate better comparability with prior

years. Accordingly, the "dotted line" indicates 2019 full year annualized number of deals based on 1H 2019 actual data. The "shaded column area" indicates 2H 2019

capital invested based on 1H 2019 actual data.

Aranca is a trusted research & advisory partner to global companies, from the

hottest start-ups to the Fortune 500.

500+ strong team professional team

across multi-disciplinary domains

2500+ global Clients

80+ countries where we have delivered

projects

120+ sectors and sub-sectors

researched by our analysts

Business Research & Advisory

CXOs in Strategy, SBUs, Sales, Marketing, CI/MI, Innovation

Valuation & Financial Advisory

CFOs in Start-ups, PE//VC firms, Corporate M&A teams, mid-market cos.

Investment Research & Analytics

Brokerage, Hedge Funds, IRPs, I-Banks, AMCs, Investor Relations

Technology | IP Research & Advisory

R&D, Tech Scouting, Open Innovation, IP teams, Product Development

PRACTICE AREAS

Disclaimer

This document is for informational use only and may be

outdated and/or no longer applicable. Nothing in this

publication is intended to constitute legal, tax, or investment

advice. There is no guarantee that any claims made will

come to pass. The information contained herein has been

obtained from sources believed to be reliable, but Aranca

does not warrant the accuracy of the information. Consult a

financial, tax or legal professional for specific information

related to your own situation.

Bharat Ramnani, ACAHead of Valuations & Financial Advisory

Email: [email protected]

Ph: +91 22 3937 9999 Ext. 259

LinkedIn Profile

For additional details, please visit:

https://www.aranca.com/

https://www.linkedin.com/company/aranca

Bharat’s Client Service delivery experience of over 15 years

includes advising global clients across diverse strategic and

transaction advisory engagements, corporate finance and

business valuation situations. He has been instrumental in

building Aranca’s financial advisory services group, which

caters to wide spectrum of clientele including large corporate,

private equity & venture capital, family offices as well as

hundreds of high performing start-ups.

Bharat is a Chartered Accountant and holds an expert

designation in business valuation from American Society of

Appraisers.

Ashish RaneSenior Manager, Valuations and Financial Advisory

Email: [email protected]

Ph: +91 22 3937 9999 Ext. 390

LinkedIn Profile

Ashish has over 9 years of experience in Corporate Finance,

Transaction Advisory and Business Valuation and has

managed financial advisory engagements for over 300

Venture Capital firms focused on investments within the

Technology domain.

Ashish holds an MBA from New York’s Stern School of

Business and a Baccalaureate degree in Business and

Management Information Systems from Pennsylvania State

University.

www.aranca.com

If you have any questions about the information in the report, please reach out to Ashish Rane at [email protected]