powerpoint presentation · gm % % 37.6% 37.6% 37.6% 0.0ppt 100.0% (62.4)ppt summary total revenue...

TRANSCRIPT

BERTRAND MALLET CEO BELGIUM & LUXEMBOURG

Previously the

Group MD for EM

and Group

Strategy Director

Senior Bain

Consultant:

Retail and

Distribution focus

Inchcape Performance Management cycle

• Rigorous performance

management ingrained in

Inchcape’s culture through

timely implementation of key

processes - centrally, locally and

at every level of the organisation

• Leading indicators are

monitored on a daily basis

throughout the Group

Daily Customer Metrics

At a Daily level, the key areas of focus are leading indicators:

• Showroom & Web Traffic,

• Test Drives

• Conversion (Sales)

• Enquiries and Bookings (Aftersales)

Daily Customer Metrics

• This Dynamic information gives us clear and early insights,

thanks to the depth and breadth of the data:

• Global / regional / local focus enables us to differentiate

- national, regional or local trends

• Traffic / leads / test drives / offers - identify and differentiate

opportunities:

– Traffic building actions

– Dealer focus

– Attractiveness of commercial conditions

Weekly P&L / Cash

• On a weekly basis our scorecards provide detailed P&L and

Cash Flow forecasts for all entities, with a specific focus on

leading indicators such as

• Ordertake

• Delivery Momentum Versus monthly Rolling Forecasts

• Working Capital Level

• Corrective actions vs. deviations can be implemented

immediately (e.g. ordertake momentum, stock management,

etc…)

Belgium and Luxembourg MONTH

Prior

Week Week 9 Budget Var Budget Prior Year Var PY

CURRENT MONTH FORECAST Units

Orderbank end of month # units 5,580 5,362 5,567 (3.7)% 5,284 1.5%

No ageing analysis # units 0 0 - -

Orderbank month +1 # units 1,876 2,419 2,324 4.1% 2,096 15.4%

Orderbank month +2 # units 1,921 1,224 1,381 (11.4)% 1,668 (26.6)%

Orderbank month +3 # units 1,184 1,111 1,813 (38.7)% 1,421 (21.8)%

Orderbank month +4 # units 588 597 38 1471.1% 88 578.4%

Orderbank month +5 # units 11 11 11 0.0% 11 0.0%

NEW

Ordertake full month - External # units 2,400 2,409 2,178 10.6% 2,127 13.3%

Ordertake full month - Total # units 2,994 3,031 2,668 13.6% 2,520 20.3%

Volumes # units 3,036 2,831 3,035 (6.7)% 2,213 27.9%

Revenue £k 50,861 47,099 50,982 (7.6)% 35,939 31.1%

ASP £/unit 16,753 16,637 16,798 (1.0)% 16,240 2.4%

Gross profit £k 2,181 2,126 2,197 (3.2)% 1,666 27.6%

GPU £/unit 718 751 724 3.8% 753 (0.3)%

GM% % 4.3% 4.5% 4.3% 0.2ppt 4.6% (0.1)ppt

USED

Ordertake full month - External # units 50 53 43 23.3% 26 103.8%

Ordertake full month - Total # units 50 53 43 23.3% 26 103.8%

Volumes # units 167 175 167 4.8% 180 (2.8)%

Revenue £k 1,695 1,598 1,516 5.4% 1,761 (9.2)%

ASP £/unit 10,148 9,131 9,078 0.6% 9,781 (6.6)%

Gross profit £k 115 116 110 5.9% 161 (28.0)%

GPU £/unit 691 664 657 1.0% 896 (25.9)%

GM% % 6.8% 7.3% 7.2% 0.0ppt 9.2% (1.9)ppt

SERVICE

Hours # hours 7,785 7,903 8,005 (1.3)% 7,136 10.7%

Revenue £k 499 489 516 (5.2)% 426 14.8%

Recovery Rate £/hour 47.9 46.3 48.1 (3.8)% 45.6 1.5%

Gross Profit £k 270 265 282 (6.1)% 214 23.7%

GM % % 54.1% 54.2% 54.7% (0.6)ppt 50.3% 3.9ppt

BODYSHOP

Hours # hours 1,213 1,220 1,380 (11.6)% 1,324 (7.9)%

Revenue £k 212 214 224 (4.5)% 193 10.5%

Recovery Rate £/hour 96.0 96.2 90.7 6.1% 87.6 9.9%

Gross Profit £k 63 64 69 (7.6)% 62 2.4%

GM % % 29.6% 29.8% 30.8% (1.0)ppt 32.2% (2.4)ppt

PARTS

Revenue £k 6,062 5,585 6,276 (11.0)% 5,664 (1.4)%

Gross Profit £k 1,908 1,793 1,913 (6.3)% 1,779 0.8%

GM % % 31.5% 32.1% 30.5% 1.6ppt 31.4% 0.7ppt

AFTERSALES

Total Revenue £k 6,772 6,288 7,015 (10.4)% 6,283 0.1%

Total Gross Profit £k 2,240 2,122 2,264 (6.3)% 2,055 3.2%

GM % % 33.1% 33.7% 32.3% 1.5ppt 0 1.0ppt

OTHER

Revenue £k 596 596 596 0.0% 145 310.0%

Gross Profit £k 224 224 224 0.1% 145 54.1%

GM % % 37.6% 37.6% 37.6% 0.0ppt 100.0% (62.4)ppt

SUMMARY

Total Revenue £k 59,923 55,581 60,109 (7.5)% 44,128 26.0%

Revenue elim (-ve) £k (9,746) (9,294) (9,013) 3.1% (6,699) 38.7%

Revenue external £k 50,178 46,286 51,097 (9.4)% 37,429 23.7%

Revenue L4L £k 50,178 46,286 51,097 (9.4)% 37,429 23.7%

Gross profit £k 4,760 4,588 4,794 (4.3)% 4,029 13.9%

% Margin (% Ext Rev) % 9.5% 9.9% 9.4% 0.5ppt 10.8% (0.9)ppt

Expenses £k (4,014) (3,959) (4,047) 2.2% (3,703) (6.9)%

Operating profit £k 746 629 747 (15.9)% 326 92.8%

ROS% (% Ext Rev) % 1.5% 1.4% 1.5% (0.1)ppt 0.9% 0.5ppt

JV post acq P/L £k 0 0 0 - (14) (100.0)%

Finance Costs £k (47) (47) (48) 2.2% (50) 7.1%

PBT £k 700 582 699 (16.8)% 261 122.6%

Monthly Balance Scorecard

On a monthly basis our balance

scorecard monitors

• Customer Scores

• P&L

• Operational Effectiveness

• Capital Employed

(including Stock)

• Cash Flow indicators

Rolling Forecast

All items are reviewed along 3 dimensions:

Versus Targets

Versus Last Year

Versus Best In Class benchmark

The 3-dimensional benchmarking helps

to identify opportunities for growth, in

particular with regards to Network

League Table Management

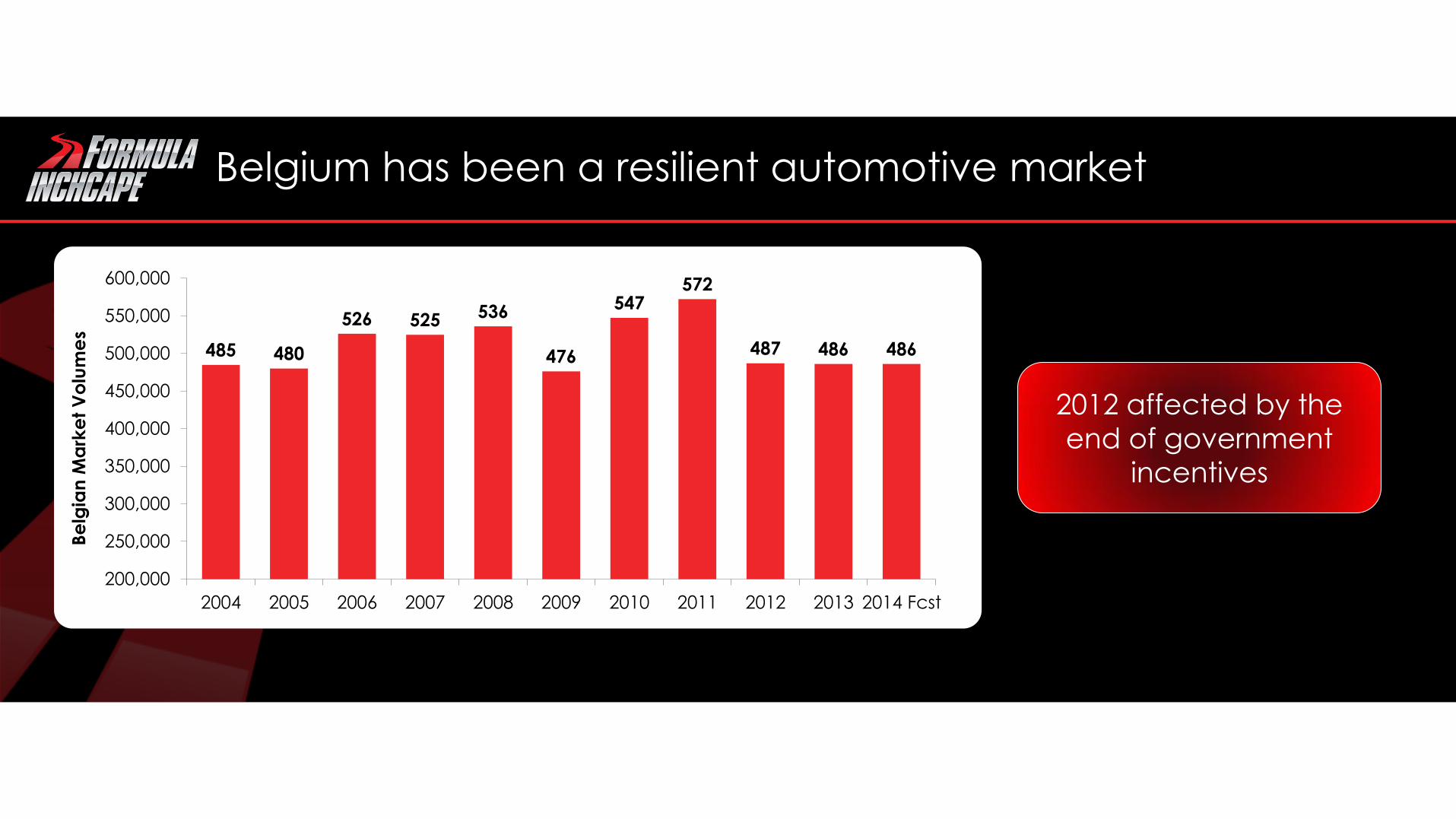

Belgium has been a resilient automotive market

485 480

526 525 536

476

547 572

487 486 486

200,000

250,000

300,000

350,000

400,000

450,000

500,000

550,000

600,000

2004 2005 2006 2007 2008 2009 2010 2011 2012 2013 2014 Fcst

Be

lgia

n M

ark

et

Vo

lum

es

2012 affected by the

end of government

incentives

Strong opportunity to grow share in core segments

• Constant stream of key new product launches in the next 3 years

• Hybrid as key competitive advantage in both private and fleet markets

• Improved value proposition at the heart of each segment

• Increased petrol demand across segments

• Improved diesel line-up thanks to partnership with BMW

The Share Growth Opportunity in Belgium

• Rigorous performance

management of the network

• A constant focus on customer

experience

• Successful marketing and sales

efforts, - We have an opportunity to

continue to grow Toyota and Lexus

market shares in Belgium 3.3%

3.6%

4.2%

2.0%

2.5%

3.0%

3.5%

4.0%

4.5%

2012 2013 2014 Q1

Ma

rke

t Sh

are

PC

Be

lgiu

m

Growth of Toyota Market Share

Product range significantly extended

H2 2012 H1 2013 H2 2013 H1 2014 H2 2014

NG Auris

MC Verso

NG Rav4

Auris TS

ProAce

NG Corolla

NG Aygo

MC Yaris

Verso 1,6d

IS 300h GS 300h NX 300h

NG Yaris H

NG Auris H Auris TS H

MC CT200h

MC Yaris H

Particular focus on

new Hybrid models

as well as a new

diesel powertrain

Excellent customer experience and loyalty in the Toyota network providing a strong platform for future growth

2008 2010 2012

#1 Hyundai Toyota Toyota

#2 Toyota Hyundai Peugeot

#3 Peugeot Peugeot Ford

#4 Nissan Nissan Citroën

Source: NCBS Survey

Best in class retailer recommendation High aftersales loyalty

0

10

20

30

40

50

60

70

80

90

100

Maintenance Quick fit Body repair Tyres

% lo

ya

lty

Our Hybrid strategy has been supported by strong and consistent communication

Example of Brussels Motorshow 2014

Strategy:

• Hybrid= affordable with the Hybrid

passport (€3,000 or Peace of mind)

• 360° integrated mass communication

during Brussels Motorshow

• Add Emotional element to

communication in order to change

the image of Hybrid driving ( Cool Driving)

0

10

20

30

40

50

60

70

80

Yaris Auris Auris TS Toyota PC

2013

Q1 2014

%

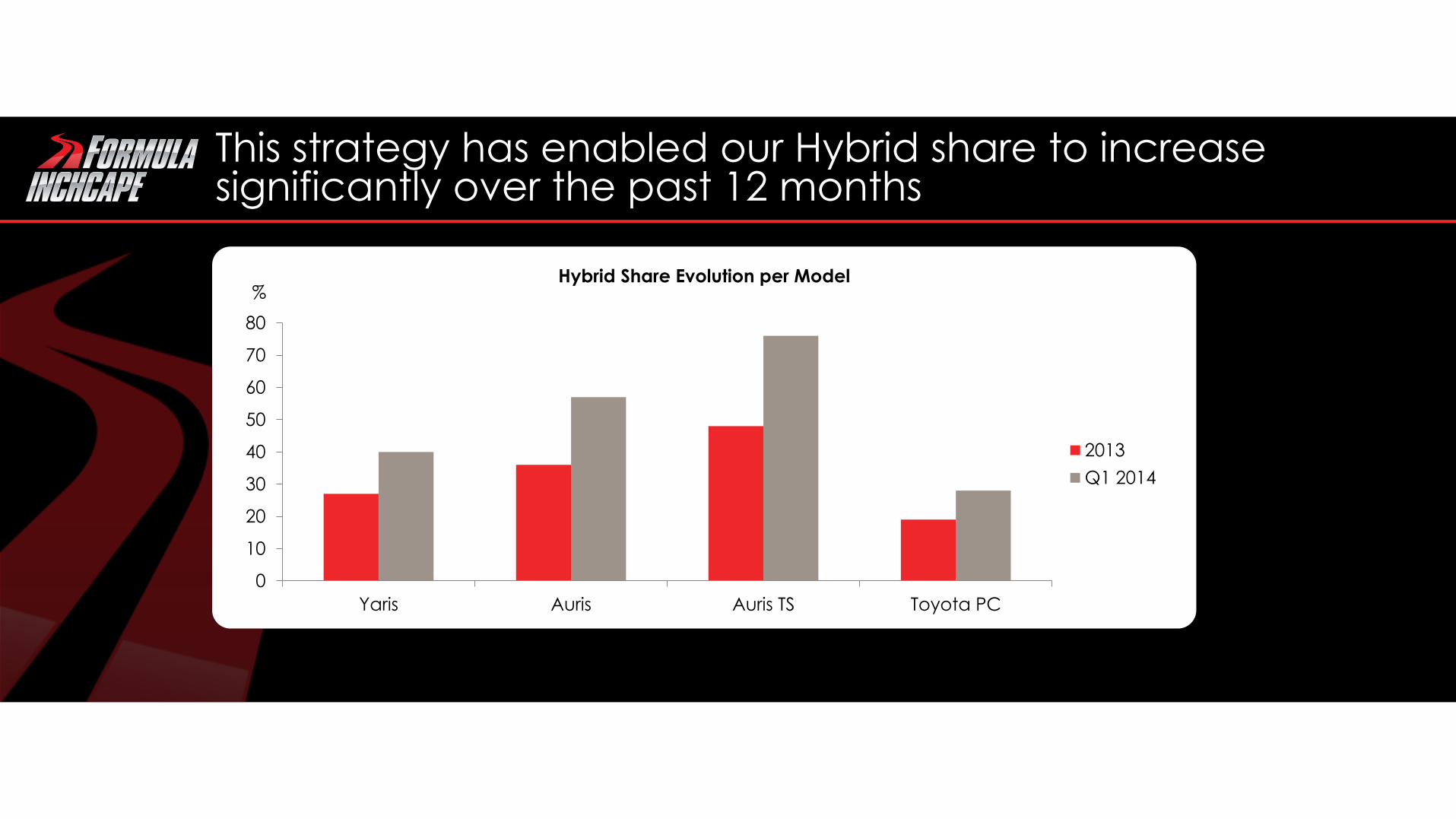

This strategy has enabled our Hybrid share to increase significantly over the past 12 months

Hybrid Share Evolution per Model

Profitable Revenue growth ahead in Toyota Belgium

Solid foundations of Toyota dealer

network

Differentiated customer

experience in Sales & Aftersales

Strength of Toyota brand Strong market positioning

Quality of product line up Market share growth in petrol,

diesel and hybrid

GEORGE ASHFORD CEO AUSTRALASIA

Previously the MD

of European Retail

and CEO of

Toyota Belgium

10 years of

experience at

Yum Restaurants

International

Inchcape performance management

As a scale distribution and retail business performance management is focused on:

• Driving effective management of the brand

• Driving site by site performance across

– Third party dealer network AND

– Inchcape network

• Leveraging scale to drive cost efficiencies across the group

Brand performance metrics

Brand performance metrics focus on:

• Long term health of the brand

• Effectiveness of each campaign

• Share performance

• Premiumisation

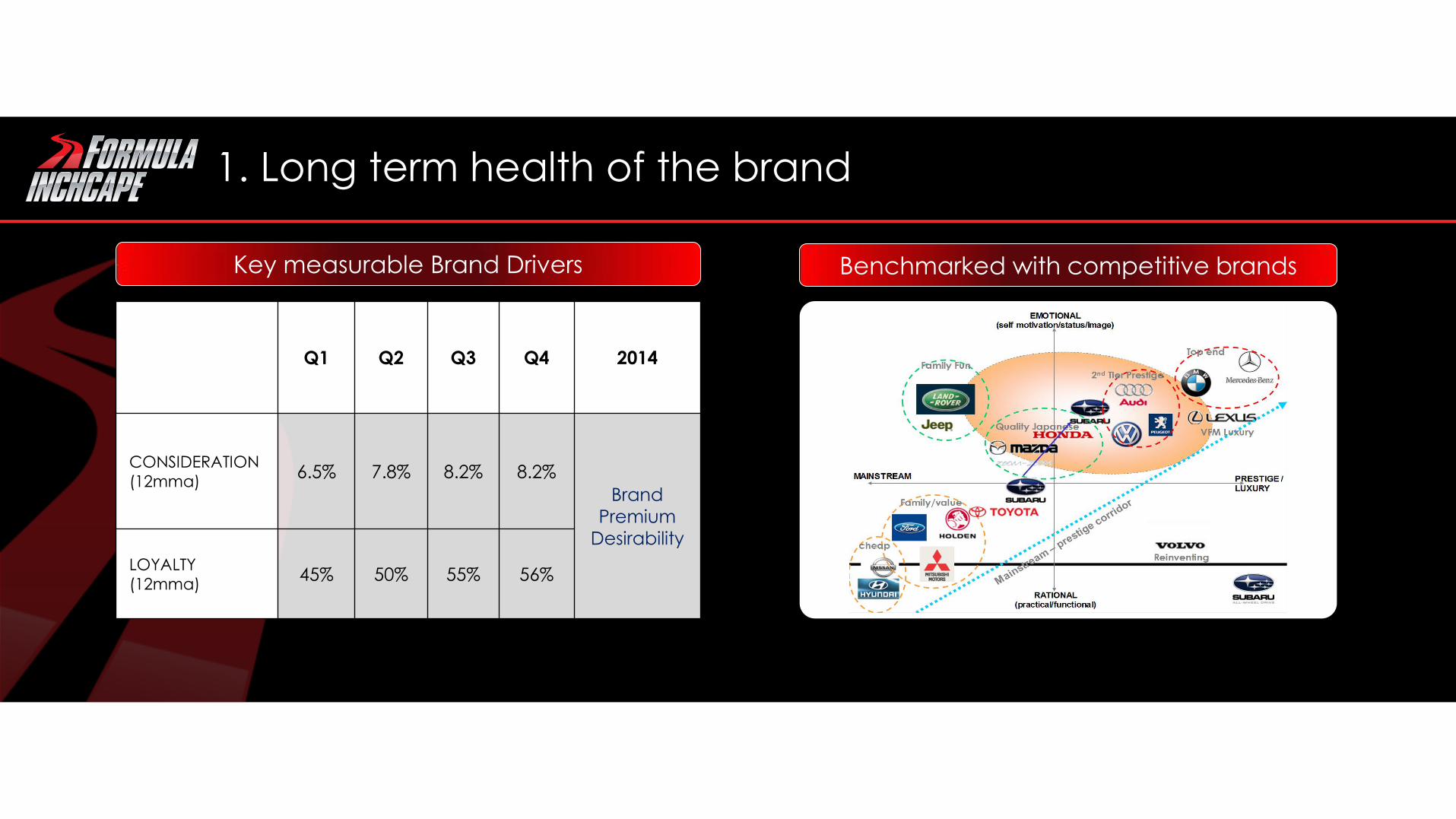

1. Long term health of the brand

Key measurable Brand Drivers

Q1 Q2 Q3 Q4 2014

CONSIDERATION

(12mma) 6.5% 7.8% 8.2% 8.2%

Brand

Premium

Desirability

LOYALTY

(12mma) 45% 50% 55% 56%

Benchmarked with competitive brands

2. Effectiveness of each campaign

Campaign Marketing Effectiveness Aligned “Go to market” process

Early bird reporting & ROI tracking

VEHICLE MARKET REVIEW - AUSTRALIA

VFACTS

SEGMENT MONTH % MONTH % MARKET % YTD % YTD % MARKET %

Mar-14 Mar-14 GROWTH Mar-14 Mar-14 GROWTH

MICRO 1,789 3.8 2,125 4.4 -336 -15.8 5,065 3.8 6,165 4.6 -1,100 -17.8

LIGHT 9,411 20.0 10,559 21.7 -1,148 -10.9 25,440 19.2 29,912 22.3 -4,472 -15.0

SMALL 21,512 45.7 22,414 46.1 -902 -4.0 63,122 47.7 60,679 45.3 2,443 4.0

MEDIUM 6,422 13.6 6,489 13.3 -67 -1.0 16,685 12.6 16,922 12.6 -237 -1.4

LARGE 4,350 9.2 3,494 7.2 856 24.5 11,972 9.0 10,358 7.7 1,614 15.6

UPPER LARGE 293 0.6 318 0.7 -25 -7.9 884 0.7 993 0.7 -109 -11.0

PEOPLE MOVERS 900 1.9 729 1.5 171 23.5 2,643 2.0 1,999 1.5 644 32.2

SPORTS 2,402 5.1 2,536 5.2 -134 -5.3 6,545 4.9 6,931 5.2 -386 -5.6

TOTAL PASSENGER 47,079 48.4 48,664 50.0 -1,585 -3.3 132,356 49.7 133,959 49.1 -1,603 -1.2

SUV 30,778 61.3 29,148 59.8 1,630 5.6 82,513 61.6 82,605 59.4 -92 -0.1

OTHER COMMERCIAL 19,410 38.7 19,588 40.2 -178 -0.9 51,501 38.4 56,484 40.6 -4,983 -8.8

TOTAL COMMERCIAL 50,188 51.6 48,736 50.0 1,452 3.0 134,014 50.3 139,089 50.9 -5,075 -3.6

TOTAL MARKET 97,267 100.0 97,400 100.0 -133 -0.1 266,370 100.0 273,048 100.0 -6,678 -2.4

SUBARU

PASSENGER 717 1.5 1,314 2.7 -597 -45.4 2,572 1.9 2,823 2.1 -251 -8.9

SUV 3,095 6.2 2,905 6.0 190 6.5 7,412 5.5 7,606 5.5 -194 -2.6

TOTAL SUBARU 3,812 3.9 4,219 4.3 -407 -9.6 9,984 3.7 10,429 3.8 -445 -4.3

3. Share performance : VFACTS

4. Premiumisation

XV DUALIS ASX TIGUAN $22,000

$40,000

$24,000

$26,000

$28,000

$30,000

$32,000

$34,000

$36,000

$38,000

Strong and sustained Premium grade/suffix mix Clear Model USP

Performance Management site by site applies same philosophy in third party and owned sites

Accelerate

Grow

Manage

High Octane Performance Management

Reduce Span of

Performance:

- Daily traffic and

conversion

- Weekly profitability and

stock control

- Monthly benchmarking

group wide, dealership

level

- Monthly Best Practice

Sharing

- Clear communication

Low performance

Best in class/

performance

potential

Middle Performance

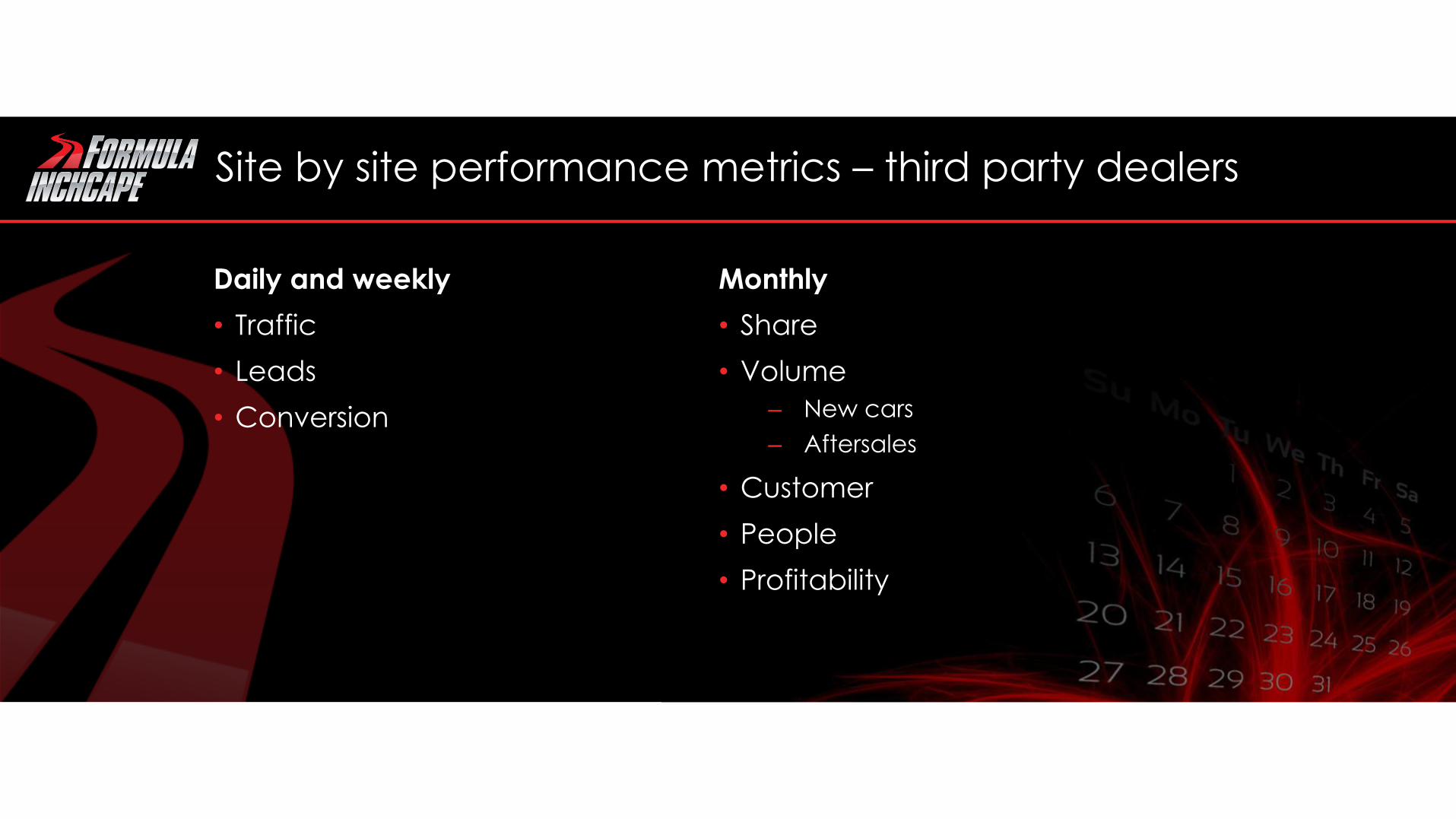

Site by site performance metrics – third party dealers

Daily and weekly

• Traffic

• Leads

• Conversion

Monthly

• Share

• Volume

– New cars

– Aftersales

• Customer

• People

• Profitability

Monthly Performance Measurement

Site by site performance metrics – Inchcape sites

Daily and weekly

• Traffic

• Leads

• Test drives

• Conversion

Weekly

• Profitability

• Customer

• Stock

Monthly

• OEM performance

• Sales funnel

• Customer

• People

• Stock

• Profitability

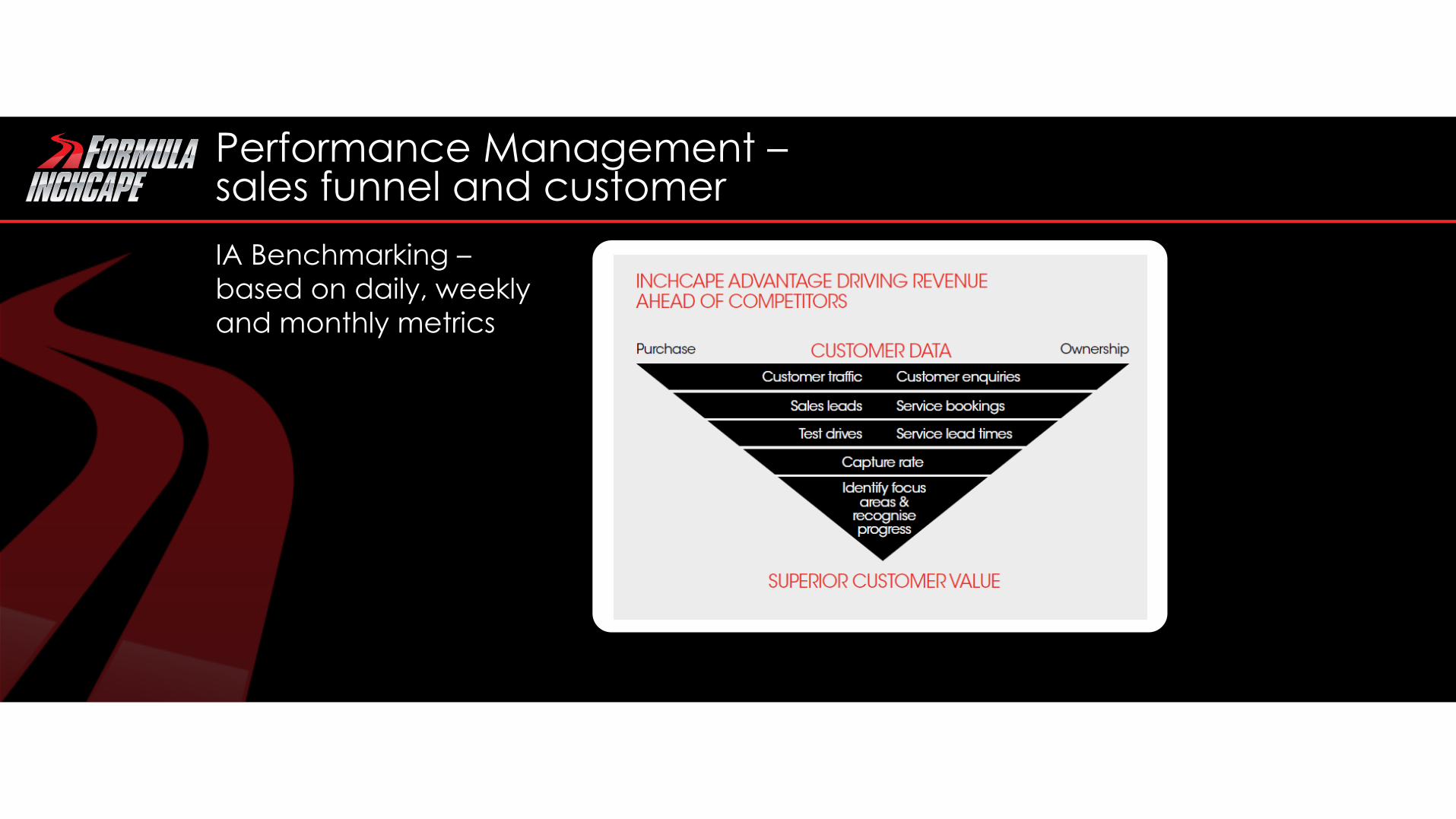

Performance Management – sales funnel and customer

IA Benchmarking –

based on daily, weekly

and monthly metrics

Performance Management

Weekly balanced scorecard – 3

dimensional approach:

Performance vs target, past year and YTD

IA Benchmarking – daily metrics

Monthly balanced scorecard –

3 dimensional approach:

Performance vs target, past year and Best in Class

Performance Management - people

Behavioural performance review and people planning

Jan and Feb • My Performance • My Behaviour • Leadership Skills • Values

• My Grow with Inchcape Plan

FULL YEAR REVIEW

Jan and Feb • My Performance • My Behaviour • Leadership Skills • Values

• My Grow with Inchcape Plan

FULL YEAR PLANNING -

Jul and Aug • My Performance • My Behaviour • Leadership Skills • Values

• My Grow with Inchcape Plan

MID YEAR REVIEW -

- Sales (Sales Consultants)

- Service (Service Advisors,

Workshop Controllers

MONTHLY REVIEW -

Performance Management – leveraging scale

Granular trend and benchmarking across

• Overheads

• Cost of sales

• Productivity

Delivering scale advantage through

• Supplier consolidation/negotiation

• Consolidation of back office functions

• Process re-engineering

Scale advantages realized

Supplier consolidation and negotiation

• Shipping

• F&I

Back office consolidation

• Shared services

• Centralized PDI

Process re-engineering

• Stock control

Performance Management ingrained in our culture

Centricity of Performance Management across the Group…

…and a relentless pursuit of high performance throughout Inchcape…

Delivering premium growth and premium returns

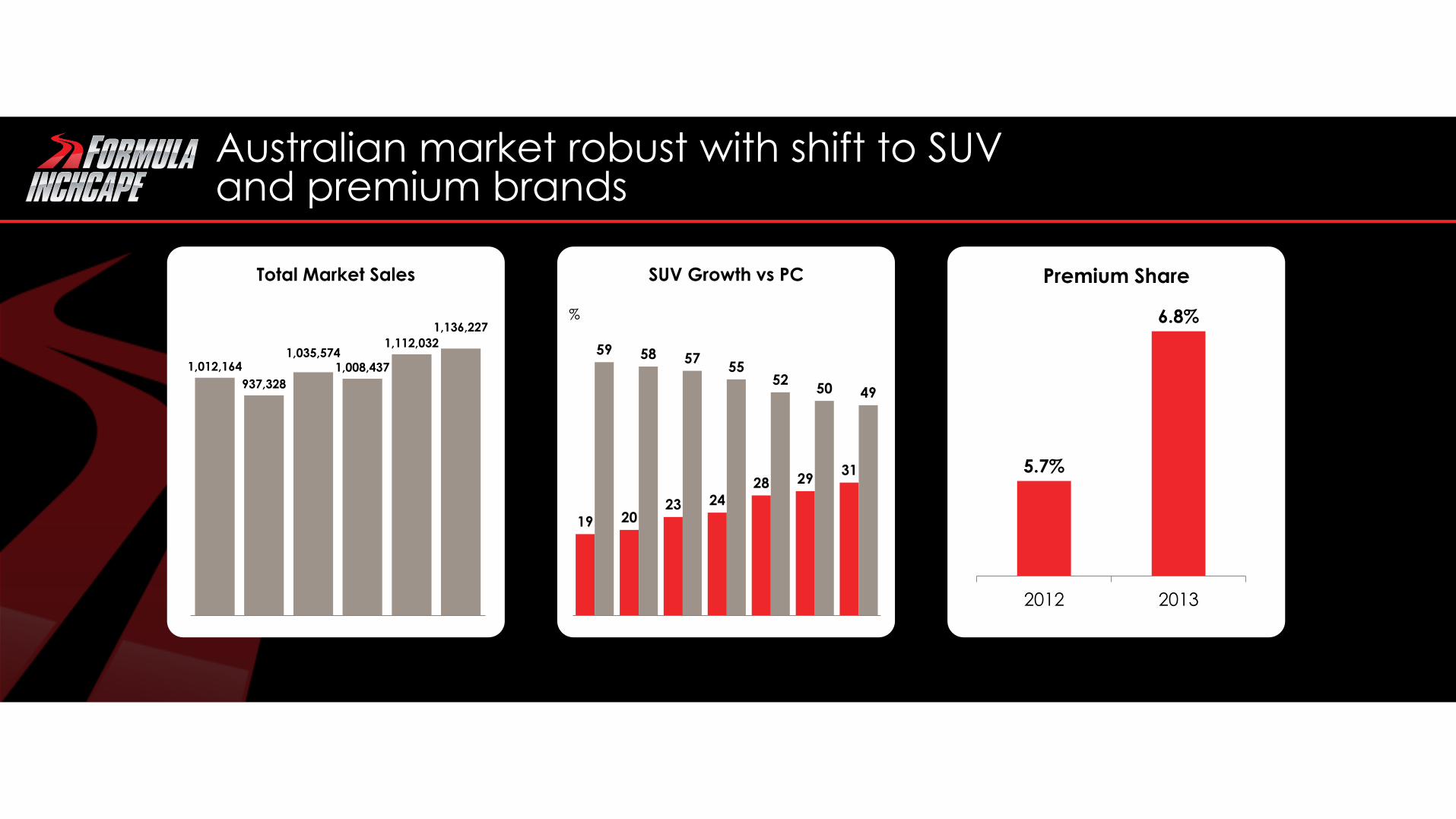

Australian market robust with shift to SUV and premium brands

1,012,164

937,328

1,035,574 1,008,437

1,112,032

1,136,227

Total Market Sales

19 20 23 24

28 29 31

59 58 57 55

52 50 49

SUV Growth vs PC

%

Premium Share

5.7%

6.8%

2012 2013

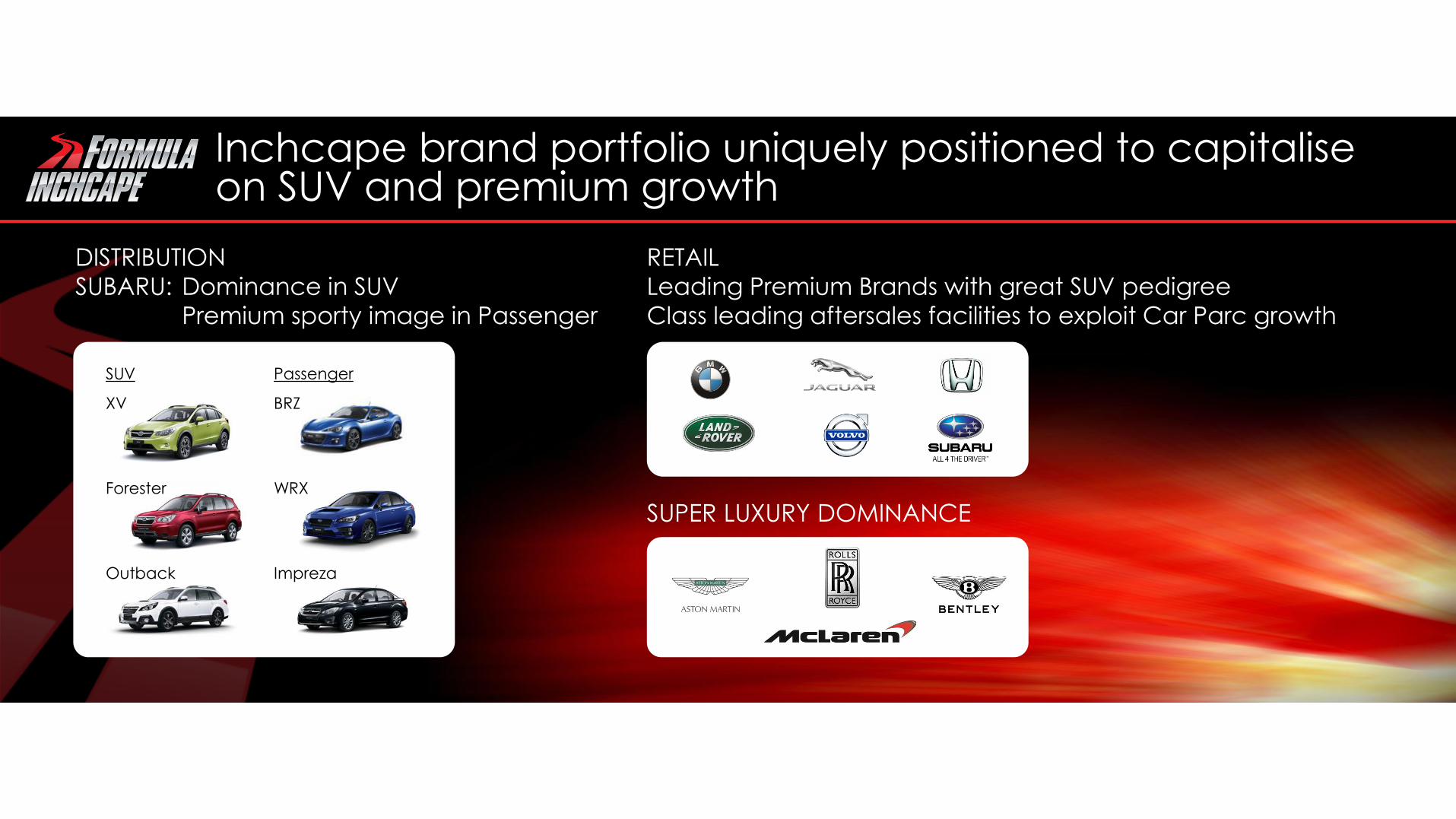

Inchcape brand portfolio uniquely positioned to capitalise on SUV and premium growth

DISTRIBUTION

SUBARU: Dominance in SUV

Premium sporty image in Passenger

RETAIL

Leading Premium Brands with great SUV pedigree

Class leading aftersales facilities to exploit Car Parc growth

SUV Passenger

XV

BRZ

Forester

WRX

Outback

Impreza

SUPER LUXURY DOMINANCE