potential for power trade in western part of south asia

TRANSCRIPT

Potential for Power Trade in Western Part of South Asia :Techno-Economic Rationale

SOUTH ASIA REGIONAL INITIATIVE FORENERGY INTEGRATION (SARI/EI)

Report is prepared by:

SARI/EI Project Secretariat, IRADe

Mr. V. K. Kharbanda, Project Director Mr. Rajiv Ratna Panda, Head-Technical

August, 2016

DISCLAIMER:

This study is made possible by the support of American people through the United States Agency for International Development (USAID). The content of this study do not necessarily reflect the views of USAID of the United Sates Government.

Integrated Research and Action for Development (IRADe) does not guarantee the accuracy of the data included in this publication and accepts no responsibility for any consequences of their use. By making any reference to a particular geographic area, or by using the term “country’’ in this document, IRADe does not intend to make any judgement as to the legal or other status of any area.

The information/data as existed in public domain and obtained/collected from the various primary and secondary sources as on July, 2016 has been used on an “as-is” basis without any independent verification by IRADe. IRADe shall not be responsible in any manner whatsoever for any error or omissions, or for the results obtained from the use of this information and provides no assurance regarding the accuracy, timeliness, adequacy, comprehensiveness and/ or completeness of such information. IRADe shall not be liable for any losses and damages arising as a result of any inaccuracy or inadequacy or incomprehensiveness or incompleteness of such information.

Any changes and updating made in data/information after July, 2016 has not been incorporated as a part of this study. This study analysis and report concluded in the month of August, 2016. The report and its findings do not necessarily reflect the views of SARI/EI Project Secretariat. The report can be considered as a base document for further analysis and the reports aims to stimulate further discussion and analysis for accelerating Cross Border Electricity Trade in the South Asian Region.

© Integrated Research and Action for Development (IRADe) 2016.

All rights reserved. Do not copy or quote without prior permission. No part of this report can be reproduced or utilized in any form or by any means, electronic or mechanical, including photocopying, recording, or by any information storage and retrieval system, without prior permission (for seeking permission contact [email protected]) in writing from Integrated Research and Action for Development.

IRADe-SARI-08 (August 2016)

Potential for Power Trade in Western Part of South Asia :Techno-Economic Rationale

SOUTH ASIA REGIONAL INITIATIVE FORENERGY INTEGRATION (SARI/EI)

August 2016

iii

Contents

Abbreviations v

Preface 01

1 Introduction 02

2 South Asian Cross Border Energy Trade 03

3 CountryProfile 09

4 CBET PotentialinWesternPartofSouthAsia 20

5 Techno-EconomicRationale 24

WayForward 31

Bibliography 32

Acknowledgements 33

FigureFigure1: PowerSectorProfile 03

Figure2: LoadSheddinginBangladesh 06

Figure3: PowerPurchaseCostinBangladesh 06

Figure4: BhutanGDPGrowth 07

Figure5: ElectricityExporttoIndia 07

Figure6: PeakDemand-SupplyScenarioinIndia 09

Figure7: EnergyAvailabilityScenarioinIndia 10

Figure8: PeakDemandandEnergyRequirementForecast-India 10

Figure9: Demand-SupplyScenarioinPunjab(India)(GW) 11

Figure10:Punjab(India)EnergyAvailability 11

Figure11:EnergyConsumptionProfile-Punjab(India) 12

iv

Potential for Power Trade in Western Part of South Asia : Techno-Economic Rationale

Figure12:PowerTradingArrangementinIndianMarket 13

Figure13:IndianPowerMarket-STPriceTrends 13

Figure14:PakistanPowerSectorProfile 14

Figure15:GenerationmixofPakistan 14

Figure16:EnergyMixbyFuelinPakistan 15

Figure17:PakistanDemand-Supply 15

Figure18:Fuel-wiseGenerationTariffinPakistan2015 17

Figure19:GenerationTariffsforFuturePlants 17

Figure20:Afghanistan’sInstalledCapacity(MW)-2016 18

Figure21:Afghanistan’sEnergySupplyScenario 19

Figure22:PowerTradingPotentialbetweenIndiaandPakistan(2018-2034) 21

Figure23:CASA1000Project 22

Figure24:Pakistan–IndiaInterconnection 24

Figure25:Stage1–200MWTransferCapacityinRadialMode 25

Figure26:Stage2–500MWHVDCSub-station 25

Figure27:ImplementationSchedule 26

TablesTable1: EnergyResourcePotentialinSouthAsia 04

Table2: SouthAsianRegionInterconnections 05

Table3: PakistanGenerationAdditionbyFY2020 16

Table4: CASATariff 17

Table5: ReferenceCostofSimilarProjects 26

Table6: InterconnectionProjectEstimatedCost 26

Table7: PowerTariffsinIndia 28

Table8: Cost-BenefitoftheProject 29

v

Potential for Power Trade in Western Part of South Asia : Techno-Economic Rationale

AC AlternatingCurrent

ADB AsianDevelopmentBank

APPC AveragePowerPurchaseCost

BDT BangladeshiTaka

BPDB BangladeshPowerDevelopmentBoard

BU BillionUnits

CAGR CompoundAnnualGrowthRate

CASA CentralAsiaSouthAsia

CBET Cross-BorderElectricityTrade

CEA CentralElectricityAuthority

D/C DoubleCircuit

EPS ElectricPowerSurvey

FO FurnaceOil

GW Gigawatt

GWh GigawattHours

HSD HighSpeedDiesel

HVAC HighVoltageAlternatingCurrent

HVDC HighVoltageDirectCurrent

IEX IndianEnergyExchange

IPP IndependentPowerProducers

kM Kilometer

kV Kilovolt

MW Megawatt

Abbreviations

vi

Potential for Power Trade in Western Part of South Asia : Techno-Economic Rationale

MWh MegawattHour

NTDC NationalTransmissionandDispatchCompanyLtd

NTPC NationalThermalPowerCorporation

PEPCO PakistanPowerElectricCompany

PPA PowerPurchaseAgreements

PXIL PowerExchangeIndiaLimited

SAARC SouthAsianAssociationforRegionalCooperation

SAFTA SouthAsianFreeTradeArea

SEC SAARC Energy Centre

SPV SpecialPurposeVehicle

T/L TransmissionLine

TWh TeraWatthouror1BillionkWh

USD UnitedStatesDollars

WBSEDCLWestBengalStateElectricityDistributionCompany

01

Potential for Power Trade in Western Part of South Asia : Techno-Economic Rationale

SouthAsiaRegionalInitiativeforEnergyIntegration(SARI/EI),aprogramofUSAIDbeingimplementedbyIntegratedResearchandActionforDevelopment(IRADe),aimstopromotetheintegrationofenergysystemsandalsotoenhanceCross-BorderElectricityTrade(CBET)amongtheSouthAsiancountries.Theprogramfocusesonthreekeyoutcomesfortheoverallsocio-economicprogressoftheregion:

y Harmonisation/coordinationofpolicy,regulatory,andlegalissues

y Advancement of transmission systems interconnections

y EstablishmentofSouthAsiaRegionalElectricityMarkets

TheeightSouthAsiannations(Afghanistan,Bangladesh,Bhutan,India,theMaldives,Nepal,Pakistan,andSriLanka)collectivelyaccountforoverone-fifthoftheworld’spopulation.All theSouthAsiancountries are currently facing power and energy shortages which is negatively impacting theireconomy. Adequate supply of energy is a pre-requisite for all the development pursuits in SouthAsiarangingfromeconomicprogresstoscientificresearch,education,healthcare,qualityoflife,andprosperityintheregion.Intherecentpast,SouthAsiahasbeenoneofthefastestgrowingregionsintheworld,withanaverageannualgrowthrateof6percentasmeasuredbyGDPpercapita.Despitethisimpressivemacroeconomicgrowth,theenergysectorintheSouthAsianregionhasnotbeenabletokeeppace,andcontinuestoexperiencechronicproblemslikeshortageofsupplyandpoorqualityofservice.Giventhisdilemmatheonlylong-termsolutionisthesustainedincreaseinregionalenergycooperationandadvancing/acceleratingCBETamongSouthAsiannations.

TheintegrationofpowergridandCBETtotheextentof2300MWintheeasternpartofSouthAsiaisalreadyestablished,betweenBangladesh-India(600MW),Bhutan-India(1416MW),andNepal-India(~500MW),thoughthereisahugepotentialofCBETintheregionandtradeislikelytoenhanceinfuture.

Therefore,theintegrationofpowersysteminthewesternpartofSouthAsiawillbeanimportantstepinthedirectionofadvancing/acceleratingCBETintheSouthAsiaRegion.ThefutureprospectsforCBETare immense; fromacompletely integratedSouthAsiangrid,wherepowercouldbe tradedacrosstheregion,subsquentelytoapaninter-regionalintegrationbetweenCentralAsianandSouthEastAsia.

Thisstudyreportdescribesthecurrent landscapeandevaluatesthefutureoptionsofpotential forpowertradeinwesternpartofSouthAsia.

Preface

02

Potential for Power Trade in Western Part of South Asia : Techno-Economic Rationale

1.1 Objective of the StudySouthAsiaRegionalInitiativeforEnergyIntegration(SARI/EI)programofUSAIDisworkingtowardspromotingthedevelopmentofintegratedregionalpowermarketinSouthAsiatofacilitatepowertradeamongsttheSAARCcountries.ThepasteffortsunderthisprogramhavebroughtaboutarecognitionofthebenefitsofCross-BorderElectricityTrade(CBET)intheregionformeetingelectricityrequirementsofrespectivecountriesandalsoaddressingtheenergysecurityoftheregion.

This study is an endeavor to complement the increasingacceptanceofCBET in theSouthAsianregionforsustainabledevelopmentofthepowersectorintheregion.WithinSouthAsia,therehavebeenseveralsuccessful initiatives for interconnectionon theeasternside, involving India,Bhutan,BangladeshandnowNepal.AtrulyintegratedSouthAsianregionalpowergridwillberealisedoncethereisconnectivityonthewesternsideofSouthAsiainvolvingIndia,PakistanandAfghanistan.

AkeyelementofintegratingthepowersysteminthewesternpartofSouthAsiaistheIndia–Pakistaninterconnection,whichhasbeenthesubjectofvariousstudiessince1990sandseveralpre-feasibilitystudieshavebeenundertakeninthepasttoidentifythemostsuitableconnectivitybetweenthetwocountries.Thisreportevaluatestheprofiles/optionsforpowertransmissioninterconnectionandpowertradingopportunitiesamongthewesternpartofSouthAsiancountriesinthechangingcontextandprovidesconclusionsonthepotentialforpowertradebasedonthetechno-economicrationaleofthepossiblealternatives.

1 Introduction

03

2.1 BackgroundThe regional cooperation offers an ideal platform to achieve sustainable growth through sharingofavailablenatural resources in the region. In thecontextofenergysector, it isapplicable to theSAARCmembercountries,wherethereisavastdiversityofavailableenergyresources,particularlyhydropowerandrenewable,whicharestillunderdevelopment.Thefigure-1providesasnapshotofpowersystemsinSouthAsia:

Figure 1: Power Sector Profile

India

Bangladesh

Bhutan

Sri Lanka

Maldives

India

Nepal

Bhutan

Bangladesh

Afghanistan

Maldives

Sri LankaUnder developed Hydro potential

• Fragmented and very small power systems

• Diesel dependent• Limited possibility of

interconnection

• Small power system with high gas dependence

• Interconnected with India• Declining Gas reserves

• Largest energy consumer and supplier in region

• Large coal reserves• Dependent on import of oil & gas• Interconnections with Nepal,

Bhutan and Bangladesh

• Very small power system• Large hydro potential• Net exporter of power

to India

• Small power system• Under-utilized hydro potential• Net importer now but

potential to export in future

Pakistan• Mid-sized power system• Gas and Oil dependent• Proposed interconnection with

Central Asia & Afghanistan• Small power system• Proposed

interconnection with Central Asia and Pakistan

Theregionisendowedwithlimitedfossilfuelsbutamplehydroresources.Inadditiontotheconventionalenergyresources,therearehugerenewableenergyresourcessuchassolarandwind,asshownintable-1onnextpage.

Thedominanceofcertainfueltypes–coalinIndia,gasinBangladesh,petroleuminPakistan,hydropower inBhutanandNepal- leadstoover-dependenceontheseresourcesatacountry levelandleavesthemvulnerabletosupplysiderisks.Thereisaneedtohavediversityinenergysupplymixaswellasimprovetheenergyaccessforthelargepopulationinthesecountrieswhoaredeprivedofthebenefitsofelectricity.Thereisalsoaneedtobalancetheconventionalsourceswiththerenewableenergyresourcesformanagingtheclimatechangeeffectsinthesub-continent.

Allthecountriesintheregionarefacingsimilarchallengesofrisingcostofelectricitysupplyandhasanurgentneedtoimprovetheaccesstoelectricityforalargesectionofpopulation.Therearehuge

2South Asian Cross Border Energy Trade

04

Potential for Power Trade in Western Part of South Asia : Techno-Economic Rationale

Table 1: Energy Resource Potential in South Asia

Country/ Fuel Source

Coal (Million Tonnes)

Oil (Million Barrels)

Natural Gas

(Trillion Cubic Feet)

Biomass (Million Tonnes)

Hydropower (MW)

Solar (kwh/sq m/day)

Wind (MW)

Afghanistan 440 NA 15 18–27 25,000 NA Limited

Bhutan 2 0 0 27 30,000 2.5-5 4,825

Bangladesh 884 12 8 0.08 330 3.8-6.5 Limited

India 90,085 5,700 39 139 1,50,000 4-7 151,918

Maldives 0 0 0 0.06 0 NA NA

Nepal NA 0 0 27 83,000 3.6-6.2 3,000

Pakistan 17,550 324 33 - 59,000 5.3 24,000

SriLanka NA 150 0 12 2,000 NA 25,000

Total 1,08,961 6,186 95 223-232 3,49,000

Source:BackgroundPaperonCross-BorderElectricityTradeinSouthAsia:KeyPolicy,RegulatoryIssues/ChallengesandtheWayForward,Jan2016-IRADe

opportunitiesforoptimisationofresourcesthroughinterconnectedpowersystemsacrosstheregionwhichcanaddressthesechallenges.Theregionalenergytradehasthepotentialtodeliversignificanteconomicbenefitsaswellasimprovethereliabilityofpowerinanenvironmentfriendlymanner.

Thedominanceofcertainfueltypes–coalinIndia,gasinBangladesh,petroleuminPakistan,hydropower inBhutanandNepal- leadstoover-dependenceontheseresourcesatacountry levelandleavesthemvulnerabletosupplysiderisks.Thereisaneedtohavediversityinenergysupplymixaswellasimprovetheenergyaccessforthelargepopulationinthesecountrieswhoaredeprivedofthebenefitsofelectricity.Thereisalsoaneedtobalancetheconventionalsourceswiththerenewableenergyresourcesformanagingtheclimatechangeeffectsinthesub-continent.

All thecountries in the regionare facingsimilar challengesof risingcostof electricity supplyandhasanurgentneedto improvetheaccesstoelectricity fora largesectionofpopulation.Therearehuge opportunities for optimisation of resources through interconnected power systems acrossthe region which can address these challenges. The regional energy trade has the potential todeliver significanteconomicbenefitsaswell as improve the reliabilityofpower inanenvironment friendlymanner.

2.2 Key CBET Initiatives in South Asian RegionOver the past decade, there has been a growing realisationamongst the SAARC nations, onthe importance of improving the energy situation in their respective geographies and the rolewhich the regional Cross Border Energy Trade can play in meeting their individual electricityneeds. The agreement for a South Asian Free Trade Area (SAFTA), signed in 2004, envisioned a transition towardsa commonmarket. TheSAARCEnergyCentre (SEC); established in 2006as aSpecialPurposeVehicle(SPV)withitsbaseinIslamabad,Pakistan;alsohasafocusonregionalenergysectorcooperationinSouthAsia.Further,theSAARCInter-governmentalFrameworkAgreementonEnergy(electricity)Cooperation,signedamongSAARCmemberstates,laysthefoundationfordeeperpowersectorcooperationandenhancingCBETintheregion.

05

Potential for Power Trade in Western Part of South Asia : Techno-Economic Rationale

ThekeyinitiativesforpowertradinginSouthAsiahavepredominantlybeenthebilateralarrangementsbetweencountries.ThebilateralarrangementsbetweenIndia-BhutanandIndia-Nepalforgenerationand transmission system have provided opportunities to unleash the huge hydropower potentialavailable inbothBhutanandNepal.ThiscleansourceofenergycanbeusedtomeetthegrowingelectricitydemandinSouthAsia.Morerecently,thedevelopmentandgrowthintheIndia-Bangladeshpowertradehasopenednewavenuesforacollaborativeregionalmarket.Thetable-2belowillustratestheexistingandproposedinterconnectionsforCBETbetweenSouthAsiancountries.

Table 2: South Asian Region Interconnections

Interconnection Key Features

Bhutan–India y Totalexportcapacityofaround1,416MWfromTala,ChukhaandKurichhu y TransmissionandassociatedinfrastructureforPunasangchhuI&II(2220MW)andMangdechu(720MW)HEPsunderconstruction

y Capacityof10,000MWforexporttoIndiatobedevelopedinBhutanundertheUmbrellaAgreementsignedbetweenthetwocountries

Bangladesh–India y 500MWpowerisbeingsuppliedfromIndiavia400kVBehrampur-BheramaralinewithHVDCstationatBheramara

y 400kV(chargedat132kV)Tripura–Comillatransmissionlinetotransfer100MWpowertoBangladeshinradialmode

y AugmentationofHVDCbacktobackstationcapacityatBheramaraby500MWunder construction

Nepal–India y Multipleinterconnectionsat11kVto132kVwithcapacityofaround150MW y 400kVMuzaffarpur-Dhalkebarline(currentlychargedat220kV)willultimatelyhavecapacityofaround1000MW

2.3 CBET Experience in South Asia

2.3.1 BANGLADESH – INDIA ELECTRICITY TRADE

ThecrossborderelectricitytradebetweenBangladeshandIndiawasinitiatedinOctober2013withthecommissioningofBheramara(Bangladesh)–Baharampur(India)400kVback-to-backHVDClinkof500MWcapacitycomprisingoffollowingelements:

y Bangladeshside:27kmofBaharampur(India)–Bheramara(Bangladesh)400kVdoublecircuitline,a3kmloop-in,loop-outofIshurdi–KhulnaSouth230kVdoublecircuitlineatBheramaraanda500MWHVDCback-to-backstationand230kVswitchingstationatBheramara

y Indiaside:71kmofBaharampur(India)–Bheramara(Bangladesh)400kVdoublecircuit line,a3kmloop-in, loop-outofFarakka–Jeerat400kVsinglecircuit lineatBaharampurand400kVswitchingstationatBaharampur

Bangladeshpowersectorhadfacedseveralchallengesintherecentpast.Theseincluded:

y Hugepowerdeficit,whichislikelytocontinueinthemedium-term,duetogrowingdemandandlimitedaccesstonewgenerationsourcesintheshorttomedium-term

y Increased procurement cost of power due to reduced availability of gas which resulted independenceonpetroleum/oilbasedgeneration

y Rising demand for electricity combinedwith the need to improve energy access for the largesectionofpopulation

06

Potential for Power Trade in Western Part of South Asia : Techno-Economic Rationale

TheBangladesh–IndiainterconnectionhasbeenbeneficialtoBangladeshinsolvingseveralprevailingproblemsbeingfacedbyitspowersector:

1. Reduced load shedding due to increased availability of power from India

TheBangladeshutilitieshadtoresorttoloadsheddingforallcategoriesofconsumersduetoreducedgenerationcapacity.Theadditionof500MWfromimportofIndianpowerhasimprovedtheoverallloadsheddingsituationsince2013.

Figure 2: Load Shedding in Bangladesh

6,454 6,7657,518

8,3499,268

10,283

4,606 4,890

6,066 6,4347,356 7,817

1,459 1,335 1,058 1,048 932307

0

2,000

4,000

6,000

8,000

10,000

12,000

FY 10 FY 11 FY 12 FY 13 FY 14 FY 15

Max Demand (MW) Max Peak Generation (MW) Max Load Shedding (MW)

Source:BPDBAnnualReport2014-15

2. Reduction in power purchase cost

ThetariffofpowerimportedfromIndiaislowerthantheaveragepowerpurchasecostinBangladesh.Hence,theoverallprocurementcostofpowerforBangladeshPowerDevelopmentBoard(BPDB),whoisthesoleprocurerofpowerinBangladesh,hasreducedastheimportfromIndiaisatalowerratethantheAveragePowerProcurementCost(APPC).TheestimatedsavingsfromtheenergytransferwouldbearoundUSD500Millionperyear(Shahi2014).

Figure 3: Power Purchase Cost in Bangladesh

4.73

6.32

8.90

3.62

5.62

-

123456789

10

BPDB IPP Rental PublicPlants

Import from India

Avgpower purchase cost: 6.27 Tk/KWh

Taka

/Uni

t

Source:BPDBAnnualReport2015

In addition, India and Bangladesh have recently commissioned the 27 km 400 kV double circuittransmissionlinefromComillainBangladeshtoTripurainIndiaalongwithassociatedworksatComilla

07

Potential for Power Trade in Western Part of South Asia : Techno-Economic Rationale

(132kVbayextensionand18km132kVtransmissionline)toimport100MWpowerfromPalatanapowerstationinTripurainradialmode.TheestimatedprojectcostofextensionoftransmissionlineisBDT1,720Million(USD22Million).

Thebenefitsofthecrossbordertradehasbeenrecognisedbyboththecountriesandhasresultedinproposaltorampupthetransmissioncapacity.TheAsianDevelopmentBank(ADB)financedtheprojecttoaugmenttheexistingBheramaraHVDCStationCapacitybyadditional500MWtofacilitateoverall1000MWofpowertransferbetweenBangladeshandIndiathroughtheexistinginterconnection,whichiscurrentlyunderimplementationandislikelytobecompletedby2019.

2.3.2 BHUTAN - INDIA ELECTRICITY TRADE

Bhutan has a huge hydro potential but has limited demand. TheCrossBorder Energy Trade has providedBhutananaccesstogrowingIndianpowermarket.Sinceyear2003,hydropowerdevelopmenthassignificantlycontributedtoBhutan’sGDPasshowninthefigurebelow:

Figure 4: Bhutan GDP Growth

5%

10%

15%

20%

25%

30%

35%

40%

0

0.5

1

1.5

2

2.5

3

FY 2000

FY 2001

FY 2002

FY 2003

FY 2004

FY 2005

FY 2006

FY 2007

FY 2008

FY 2009

FY 2010

FY 2011

FY 2012

FY 2013

FY 2014

FY 2015

FY 2016

Gro

wth

(%)

GD

P (U

SD

Bill

ion)

GDP (USD Billion) Percentage growth

TalaHydro (1020 MW)

-10%

-5%

0%

Source:IMFEstimates

Figure 5: Electricity Export to India (USD Million)

30.00 30.01 30.3 30.4 30.6 30.7

17.01%

14.40%

10.74% 11.52%10.19% 10.14%

30.10

30.08

30.06

30.04

30.02

30.00

29.98

29.962010 2011 2012 2013 2014 2015

Export (USD Million) Export (% of GDP)

Source:BhutanPowerSectorReport

08

Potential for Power Trade in Western Part of South Asia : Techno-Economic Rationale

TheenergysaleswithinBhutanhasreachedthreetimesoverpastonedecadeandhasalsoledtodevelopmentofenergyintensiveindustrieslikeCement,IronandSteel,Carbide,etc.TheelectricityaccesshasimprovedinBhutan(76percentin2012)asaresultofhydropowerdevelopment.

The electricity exports to India have alsobeen steadily risingover the last decade. In addition tocontributingtotheGDP(morethan10percent),thedevelopmentofhydropowerpotentialhasalsoindirectlycontributedtotheoveralldevelopmentofBhutaneseeconomy.

2.4 Case for CBET in Western Part of South AsiaIn South Asia, the power systems in India-Bangladesh-Bhutan-Nepal have been interconnectedoverpastdecadeasaresultofseveralbilateralinitiatives.Thishasopenedupopportunitiesfortheevolutionofaneasternsub-regionalgridwithinSouthAsia.ThehugehydropowerpotentialinBhutan(estimatedcapacitydevelopedtobe11GWby2020)andNepal(economicpotentialisestimatedtobe42GW),canbedevelopedandtransmittedtoloadcenterstomeettheexponentiallyincreasingelectricitydemandinBangladeshandIndia.

On itswestern side, Pakistan already has limited connectivity to Iran’s power systemand is alsoan integral part of the CASA 1000 scheme. Under this scheme,over 3 Terawatt hours (TWh) ofhydroelectricityisproposedtobetransferredduringthesummermonthsfromCentralAsiancountriesofKyrgyzRepublicandTajikistantoPakistanthroughAfghanistaninSouthAsia.Currently,thereisnoconnectivityforpowertransferbetweenPakistanandIndia.TheinterconnectiononthewesternsideinvolvingIndia,PakistanandAfghanistanisimportantfortheoverallevolutionoftheSouthAsianregionalgrid.

The interconnectionbetweenPakistanand Indiahas thepotential tobringaboutan integration inthepowersystemsofCentralAsiancountriesandSouthAsiancountries.ThehydropowerpotentialinthesecountriescancomplementthepredominantlycoalbasedthermalpowergenerationinIndiatocreateastablepowersystem,whichismutuallybeneficialtotheconstituentsofboththeregions.According to ADB report (2013)1, the benefits fromCASA 1000 project in conjunctionwith India-Pakistan interconnectioncanyield substantivesavingsexceedingUSD1Billion,primarily throughreductioninunservedenergyinAfghanistan,PakistanandIndia.

Intheshort tomedium-term,the interconnectionbetweenPakistanandIndiacanbenefitPakistanandpossiblyAfghanistaninmeetingthegenerationdeficitatacompetitiveprice.Inthelong-term,theinterconnectedsysteminSouthAsiawillprovideopportunitiesforthenewcapacityadditionswithinPakistantoseekpowerdeficientmarketsinSouthandCentralAsia.TheSouthAsianregionalgridwillimprovetheelectricityaccessforthepopulationwhiledrivingthedevelopmentofefficientanddiversegenerationcapacities.

1 RDTA 7529: South Asian Regional Power Exchange Study – Final Report

09

Potential for Power Trade in Western Part of South Asia : Techno-Economic Rationale

Inthefollowingsection,thecurrentandfutureprofilesofpowersectorinIndiaandPakistanhavebeenassessedtounderstandandevaluatethepowertradingpotentialbetweenthetwocountries.

3.1 INDIAIndia’spowergenerationcapacitycurrentlystandsat303GW(June,2016)andhasfourthrankintheworld.This isasignificant increasefrom145GWattheendofFY2006,withaCompoundAnnualGrowthRate(CAGR)of7.7percent.TheenergymixforIndiaisdominatedbycoalwhichaccountsfor59percentofthetotalinstalledcapacity.ThesupplysituationinIndiahasdrasticallyimprovedoverthelasttwoyears.Thepeakdemandsupplydeficithasprogressivelycomedownoverlast5yearsandIndiaislikelytohavepeaksurplusduringFY2017.Thecoalsupplyhasalsoimprovedwithsurpluscoalcapacitybeingavailable.ThedominanceofcoalinIndia’senergyportfolioislikelytocontinueintheforeseeablefutureaswell.RenewableEnergyhasbeenoneofthefastestgrowingsegmentsofthepowersector,accountingfor17.6percentofthecurrentinstalledcapacity.ThegrowthinRenewableEnergyislikelytocontinueoveralong-termperiod,giventheambitioustargetswhichhavebeensetforsolarandwindsegments.

3.1.1 DEMAND-SUPPLY SCENARIO – PAN INDIA

The peak demand supply scenario has improved in India over the last few years as a result ofacceleratedgenerationcapacityadditionsandacomplementaryslowdowninthedemandgrowth.ForFY2017,thesituationislikelytoturnwithpeaksurplusof2.57percentasshowninthefigurebelow:

Figure 6: Peak Demand-Supply Scenario in India

119 122130

135 136

148153

160

104 110 116 123 130 141 148 157

-12.7%

-9.8%-10.6%

-9.0%

-4.5% -4.7%

-3.2%

-1.6%

-14%

-12%

-10%

-8%

-6%

-4%

0%

-

20

40

60

80

100

120

140

160

180

FY 2010 FY 2011 FY 2012 FY 2013 FY 2014 FY 2015 FY 2016 FY 2017

GW

Peak Demand Peak Supply Gap (%)

-2%

Source:MinistryofPower,GovernmentofIndia

3 Country Profile

10

Potential for Power Trade in Western Part of South Asia : Techno-Economic Rationale

Asimilartrendisalsoseenintheelectricitygenerationandavailability.India’selectricitydeficithasgraduallydecreasedover thepastdecade, from~10percent in2010to2.1percent in2016.Thecountryislikelytoexperienceenergysurplusduring2016-17asshowninthefigurebelow

Figure 7: Energy Availability Scenario in India

831 862 937

996 1,002 1,069 1,114

1,143

747 788 858 909 960 1,031 1,091 1,135

-10.11%

-8.50% -8.46% -8.73%

-4.23%-3.57%

-2.11%

-0.70%

-12%

-10%

-8%

-6%

-4%

-2%

0%

-

200

400

600

800

1,000

1,200

1,400

FY 2010 FY 2011 FY 2012 FY 2013 FY 2014 FY 2015 FY 2016 FY 2017

TW

h

Energy Requirement Energy Availability Surplus/ (Deficit)

Source:MinistryofPower,GovernmentofIndia

The 18th Electric Power Survey (EPS) report has analysed the future demand-supply and energysituationforIndia.ThereportestimatesthatIndia’speakdemandwouldbearound541GWinyear2032andelectricalenergyrequirementofaround3,700TWhasillustratedinthefigurebelow.

Figure 8: Peak Demand and Energy Requirement Forecast - India

200283

401

5421355

1905

2710

3710

0

500

1000

1500

2000

2500

3000

3500

4000

0

100

200

300

400

500

600

FY 2017 FY 2022 FY 2027 FY 2032

Pea

k D

eman

d (G

W)

Ene

rgy

Req

uire

men

t (T

Wh)

Peak Demand (GW) Energy Requirement (TWh)

Source:18thEPSReport,CentralElectricityAuthority

11

Potential for Power Trade in Western Part of South Asia : Techno-Economic Rationale

3.1.2 DEMAND-SUPPLY SCENARIO – PUNJAB (INDIA)

PunjabhasoneofthehighestpercapitaelectricityconsumptionstatesinIndiaandhasbeenabletoachieve100percentelectrificationwithinthestate.Thepeakdemandsupplygapforthestatehasbeenprogressivelycomingdownoverthelastfiveyearsasshownbelow:

Figure 9: Demand-Supply Scenario in Punjab (India) (GW)

-24.3%

-14.8% -15.6%

-21.2%

-12.2% -12.0%

-3.8% -3.1%-4.3%

-8.9%

-

2.00

4.00

6.00

8.00

10.00

12.00

14.00

16.00

FY 2010 FY 2011 FY 2012 FY 2013 FY 2014 FY 2015 FY 2016 FY 2017 FY 2018 FY 2019

Peak Demand Peak Supply Surplus/deficit

-30%

-25%

-20%

-15%

-10%

-5%

0%

Source:PFAReportsonPunjab

Theenergyavailability–requirementscenarioinPunjabhasbeenimprovingovertheyears.Asfarasenergyrequirementandthesupplyscenarioisconcerned,Punjabhasshowntremendousimprovementsince 2010. The state has attained surplus energy due to generation capacity additions over thepastfewyears.Theenergydeficithasdecreasedgraduallyfrom6,449GWhin2010toanegligibleshortagein2016.Thescenarioislikelytoimprovefurther,withtheadditionofthermalpowerprojectsinthestate.ThePowerFinanceCorporation(PFC)reportonPunjabforecastshugeenergysurpluswithinthestateinthecomingyearsasshownbelow:

Figure 10: Punjab (India) Energy Availability (TWh)

-13.9%

-6.0%-3.1%

-5.4%-1.6% -1.0%

36.8%

48.7%46.0%

37.2%

-16%

-6%

4%

14%

24%

34%

44%

54%

-10.00

20.00

30.00

40.00

50.00

60.00

70.00

80.00

90.00

100.00

FY 2010 FY 2011 FY 2012 FY 2013 FY 2014 FY 2015 FY 2016 FY 2017 FY 2018 FY 2019

Energy Requirement Energy Availability Surplus/ deficit

TWh

Source:PowerFinanceCorporationreportonPunjab

12

Potential for Power Trade in Western Part of South Asia : Techno-Economic Rationale

Punjab has a typical demand variation due to high agriculture load and the requirement is at itspeakduringthepaddyseason(JunetoSeptember).Around47percentofthetotalannualenergyrequirement isconsumedduring these fourmonthsand the requirementsignificantlydropsduringthe remaining part of the year. The state has surplus energy during the non-paddyperiod,whichis tradedthroughbilateralarrangementswithotherstates.The followingfigureshowsthemonthlyenergyprofileofPunjab(India):

Figure 11: Energy Consumption Profile - Punjab (India)

3.00

4.35

5.45

6.35 6.21

5.48

3.93

2.67

3.21 3.07 3.02 2.88

0.00

1.00

2.00

3.00

4.00

5.00

6.00

7.00

Apr-15 May-15 Jun-15 Jul-15 Aug-15 Sep-15 Oct-15 Nov-15 Dec-15 Jan-16 Feb-16 Mar-16

TW

h

Requirement (TWh)

Source:CEAReports

TherearesignificantopportunitiesfortradingthesurplusenergyavailablewiththestateofPunjabinfuture.ThissurpluscouldbeabsorbedwithintheNorthernRegioninIndiaorcanbetradedwithutilitiesinotherregionsaswell.

3.1.3 PRICING TRENDS IN INDIAN MARKET

ThepowermarketinIndiahasvariouscontractingarrangementsavailable,whichcandeterminethepriceoftransactionsbasedonopenmarketmechanism,asshowninfigure12.

ThepowerpricesinIndianmarketsareregulatedasperpurchasebythestatedistributioncompaniesareconcerned.Thegeneratorscanenterintolong-termPowerPurchaseAgreements(PPA)withthebuyerssuchasthedistributioncompaniesorpowertraders.Thepowerutilitiescanalsoenterintomediumtolong-termPPAstosellanysurplusenergyavailablewiththem.Thelicensedtraderscanactasintermediariestobuyandsellpowerbothinthemedium-termandlong-termmarkets.Inaddition,thetwoIndianexchangesviz.IndianEnergyExchange(IEX)andPowerExchangeIndiaLimited(PXIL)allowforshort-termandmedium-termpowertransactionstobebasedonthedemandandsupplybetweenthebuyersandsellers.For the internationalpowertrade, thereareseveraloptionswhichhavebeenimplementedinIndiancontext.ThesaleofpowerfromgeneratingstationsinBhutanistransactedthroughPTCIndiaLtd.whichisalicensedtrader.Morerecently,thesaleof80MWofpowerfromIndiatoNepalwasimplementedthroughNVVN,anotherlicensedpowertrader.Similarly,whenBangladeshPowerDevelopmentBoard(BPDB)contractedfor500MWofpowerinthefirstphase,250MWwasaffectedthroughPTCIndiaLtdfora3yearperiodandremaining250MWwassoldfromNTPCplants.ThepowersoldbyPTCIndiaLtd.wassourcedfromsurpluspoweravailablewithWestBengalStateElectricityDistributionCompany(WBSEDCL),justacrosstheIndia-Bangladeshborder.

13

Potential for Power Trade in Western Part of South Asia : Techno-Economic Rationale

Figure 12: Power Trading Arrangement in Indian Market

Long TermPower Purchase Agreements

Upto 25 Years

Medium Term

Power Exchanges (2)

Balancing Market

Real Time

Short Term

3 months-3 years

• Contingency Transaction• Day Ahead Transaction• Collective Transaction• Bilateral Transaction

Intraday -3 months

Bilateral TransactionsOver the Counter Trading (OTC)Licensed traders (47)

OTC Intraday-3 months

1. Intra-day2. Day Ahead Market (DAM)3. Day Ahead Contingency (DAC)4. Daily5. Weekly

Deviation Settlement Mechanism(DSM)

89% -91%

5% -6%

2% -3%

2% -3%

Themarketpriceforpoweronthepowerexchangehasbeenrangeboundoverlast5yearsasthedemandhasbeensuppressedandtheutilitieshavenotbeenprocuringpowerfromshort-termmarketduetostrictmonitoringbytheregulatorsonthepowerprocurementcosts.Thepricingtrendsforthetransactionsdoneby theTraders,PowerExchange–DayAheadMarketandTermAheadMarket,DSM–realtimeenergychargesforsixyearsisshownbelow:

Figure 13: Indian Power Market - ST Price Trends

8.09

7.37

6.43 6.66 6.60 6.58 6.32

5.43

7.63

5.34 5.49 5.65

4.46

5.38

4.18 3.85

-

1

2

3

4

5

6

7

8

9

FY 10 FY 11 FY 12 FY 13 FY 14 FY 15 FY 16 FY 17

Pric

ing

(US

cen

ts/

kWh)

Power Traders Power Exchange (DAM+TAM)

Source:CERCMonthlyMonitoringReports

3.2 PAKISTANThe installed generation capacity in Pakistan has increased at amodest CAGR of 1.55 per centbetween theperiodFY2011andFY2015.Theelectricitygenerationduring the sameperiodhasgrownatCAGRof2percent.ThepowersectorprofileofPakistanisshownfigure14.

14

Potential for Power Trade in Western Part of South Asia : Techno-Economic Rationale

Figure 14: Pakistan Power Sector Profile

23.34 23.49 23.73 23.73 24.82

100.58 99.30 98.66 105.70 109.06

-

20

40

60

80

100

120

-

10

20

30

FY 2011 FY 2012 FY 2013 FY 2014 FY 2015

TWh(GW

)

Installed Capacity (GW) Generation (TWh)

Source:StateofindustryReport,2015

Pakistan’spowersectorhasahighdependenceonliquidfuelsforpowergeneration.About35percentofitsinternalgenerationcamefromDiesel/HSD/FO,followedby30.9percentfromhydroand29.5percentfromdomesticgas.Itisexpectedthatthecontributionofliquidfuelswouldgraduallydecreaseby2020.Atthesametime,theproportionofdomesticgasisexpectedtodecreaseto18percentby2034andwillbereplacedbynuclearandhydrowhichwouldcontributearound7percentand35percentrespectivelyby2034.

Figure 15: Generation mix of Pakistan (2014)

RE,0.2%

DomesticGas, 29.5%

DomesticCoal, 0.1%

Diesel/HS/D/FO,35.2%

ImportedCoal, 0.0%

LNG, 0.0%

Hydro,30.9%

Nuclear, 4.0%

ThetotalenergygenerationinPakistanisexpectedtoincreaseto198TWhagainsttheoveralldemandof370TWhin2034.2Thiswouldmean,around172TWhwouldhavetobemetthrough importofelectricityfromothercountries.

2 USAID report on Assessment of the Electricity Trading Potential in the South Asian Region, May 2016

15

Potential for Power Trade in Western Part of South Asia : Techno-Economic Rationale

Figure 16: Energy Mix by Fuel in Pakistan

28

91

5 - - -

-

-

27

- - -

-

-

53

38 29 25

-

33 52

59 65 70

-

4

13

13 13 13

0

0

18

18 18 18

30

27

36

36 36 36

-

1

5

12 26 36

FY 2011 FY 2015 FY 2020 FY 2025 FY 2030 FY 2034

TWH

Diesel/HSD/FO LNG Coal (Imported) Hydro Nuclear Coal (Domestic) Gas (Domestic) RE

Source:SARI/EIreportonAssessmentoftheElectricityTradingPotentialintheSouthAsianRegion,May2016

3.2.1 DEMAND SUPPLY SCENARIO

TherehavebeensevereenergyshortagesinPakistansince2006.Thiscanbeattributedtolackofadequategenerationcapacityadditionstomeetthegrowingdemandandchallengesinmaintainingsomeoftheexistingaginggeneratingstations.Thesituationhascausedhugedemandsupplygapresultinginload-sheddingofelectricityasshownbelow:

Figure 17: Pakistan Demand-Supply

1213 13 13 12

14 13 1312

14

17 17 17

1213

1416

17 18 18 19 19 1921

2223

0.2 0.2

(10.00)

(5.00)

-

5.00

10.00

15.00

20.00

25.00

GW

2015

-16

2014

-15

2013

-14

2012

-13

2011

-12

2010

-11

2009

-10

2008

-09

2007

-08

2006

-07

2005

-06

2004

-05

2003

-04

-5.4-4.4-4.0

-5.3-6.6

-5.3-5.0-4.2-5.0

-2.5-1.2

Available Capability Computed Peak Demand Surplus/(Deficit)

Source:NTDCPresentationSAARCPerspectiveWorkshop,Oct2015

Theincreaseindemandsupplygapisattributedtoseveralfactorslike,reducedavailabilityfromtheexistingthermalstations,onaccountoffuelsupply-depletioninnaturalgas,delaysindevelopingthehydroprojects–lessthan15percentofthetotalhydropotentialof60GWhasbeendevelopedsofar.Theincreasedusageoffurnaceoilandhighspeeddieselalsoledtoexponentialincreaseingenerationcostwhichalsoadverselyaffectedtheaffordabilityofgeneration.

16

Potential for Power Trade in Western Part of South Asia : Techno-Economic Rationale

Thegovernmenthas initiatedaprogramme,withtheassistanceofChina,wheretheenergysectorhasbeengivenhighprioritytoovercomeenergyshortages.TheChina-PakistanEconomicCorridor(CPEC) is expected to add 10,400 MW to the grid on priority basis. The projects include coal,hydro andwind.Not only that, it will augment supplies in amajorway, butwill also significantlychange the energy mix, replacing expensive oil and resulting in reduction in the average cost ofgeneration.

ThesituationissimilarintheprovinceofPunjab,whichisalsothemostpopulousprovinceinPakistanandalsocontributesto68percentofthetotalconsumptioninthecountry.Thedemandisgrowingattherateofaround6-8percentperannumwiththedemand-supplygapestimatedataround4GW.Thegeneration,transmission,distributionandretailsupplyofelectricityinPakistanisundertakenbyPakistanPowerElectricCompany(PEPCO)withsignificantcontributiontogenerationfromvariousIndependentPowerProducers(IPPs).

The demand-supply gap will, however, remain almost the same in short to medium-term due tosuppresseddemandinthesystem,whichisexpectedtogrowatarateoffourtofivepercent.However,inthelong-runthesituationmayreverseandPakistancanbecomepowersurplusifitcanachieveitsambitioustargetsofadding17000MWpowergenerationcapacityunderCPEC.ThissituationmayallowPakistantoexportsurpluspowertoIndiaorotherSouthAsiancountriesconnectedtoIndianpowertransmissiongrid.

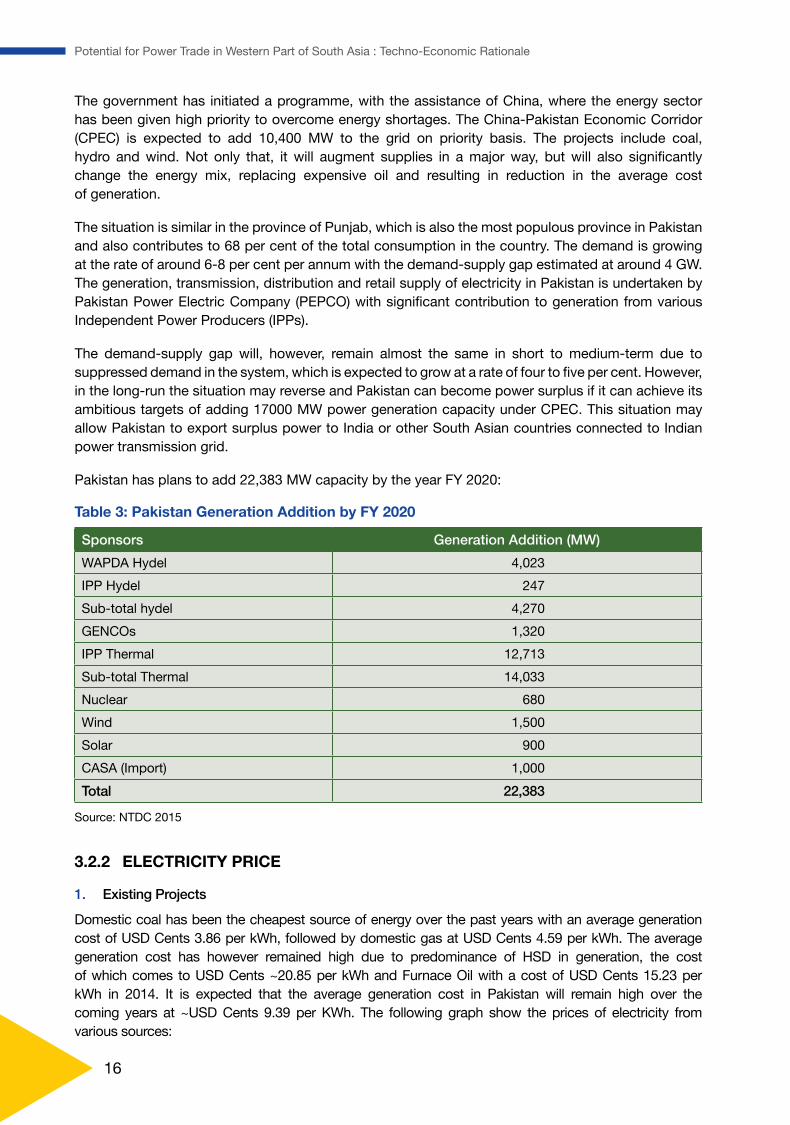

Pakistanhasplanstoadd22,383MWcapacitybytheyearFY2020:

Table 3: Pakistan Generation Addition by FY 2020

Sponsors Generation Addition (MW)

WAPDAHydel 4,023

IPPHydel 247

Sub-totalhydel 4,270

GENCOs 1,320

IPPThermal 12,713

Sub-totalThermal 14,033

Nuclear 680

Wind 1,500

Solar 900

CASA(Import) 1,000

Total 22,383

Source:NTDC2015

3.2.2 ELECTRICITY PRICE

1. Existing Projects

DomesticcoalhasbeenthecheapestsourceofenergyoverthepastyearswithanaveragegenerationcostofUSDCents3.86perkWh,followedbydomesticgasatUSDCents4.59perkWh.Theaveragegeneration cost has however remained high due to predominance of HSD in generation, the costofwhichcomestoUSDCents~20.85perkWhandFurnaceOilwithacostofUSDCents15.23perkWh in 2014. It is expected that the average generation cost in Pakistan will remain high over thecoming years at ~USDCents 9.39 perKWh. The following graph show the prices of electricity from varioussources:

17

Potential for Power Trade in Western Part of South Asia : Techno-Economic Rationale

Figure 18: Fuel-wise Generation Tariff in Pakistan (2015)(U

S c

ents

/ kW

h)

1.14

4.29 4.59

7.85 9.57

11.96

16.35

9.72

-

2.00

4.00

6.00

8.00

10.00

12.00

14.00

16.00

18.00

Nuclear Coal Gas Mixed Import Iran FO HSD

Fuelwise Av Generation

Source:StateofIndustryReport2015

2. Future Plants

TheCASA–1000isscheduledtodeliverthepoweratalevelisedtariffrangingfromUScents9.38toUScents10.88perkWhdependingonthecountryofsupplyasshowninthetablebelow:

Table 4: CASA TariffAllfiguresinUSCentsperkWh

Component Energy from Tajikistan

Energy from Kyrgyz

Energy from non-member country

Transmission Tariff 2.98 2.98 2.98

Energy Tariff 5.15 5.15 5.15

AfghanTransitFee 1.25 1.25 1.25

TajikistanfeeforKyrgyzenergy - 0.1 -

Non-member country charge - - 1.5

Total 9.38 9.48 10.88

Source:NEPRAPakistan

WithinPakistan,varioussourcesoffuelarebeingexploredtoreplacethecostlyoilbasedgeneration.Thefollowingfigureshowstherangeofgenerationtariffsforthefutureprojectsbasedonfuelsused:

Figure 19: Generation Tariffs for Future Plants

8.25 8.64 9.36

15.09

9.29 9.67 10.07

15.77

Domestic Coal Imported Coal LNG HSD

(US

cen

ts/

kWh)

Source:NEPRAPakistan

18

Potential for Power Trade in Western Part of South Asia : Techno-Economic Rationale

3.3 AFGHANISTANAfghanistan is rebuilding its energy sector and it has made ‘providing sustainable energy to itspopulation’afocusofitsdevelopmenteffortswiththesupportofinternationalcommunity.Currently,only43percentofthepopulationisestimatedtohaveaccesstoelectricity,withaverageper-capitauseof73kWhperyear.Eventhislowper-capitalevelofelectricityaccessconcealsasignificanturban-ruraldisparity,asitisestimatedthatonly23percentofsuppliedelectricityreachestheruralareas.

The Afghan energy sector not only suffers from limited power generation capacity but also itstransmissionanddistributionsystemsareoutdated.Theruralpopulationismostlydependentonmicro-hydroorPVbasedsolarpowerprojects.Thedependenceonthetraditionalbiomass(woodanddung)isstillveryhigh,ataround85percentofprimaryenergy,whichadverselyimpactstheenvironment.It is supplementedby theuseofdieselgenerators inoff-gridareasaswell as tocompensate forpoweroutages.Lackofaccesstoaffordableenergyislimitingtheeconomic,socialandeducationalopportunities,particularlyforthepoorandthoseinruralareas.

TheinstalledcapacityofAfghanistan’spowersystemwas566MWin2016.Thiscomprisedof53percenthydro,35.34percentdieselorHFObasedthermalpowerplants,0.2percentsolarandsmalldieselgeneratorsetsconstitutedabout12percent.However,duetopoliticalinstabilityandconflictsin the last twodecades,generationcapacityadditionhavebeen limitedandmajorityofelectricityconsumption(77percentoftotalconsumption, i.e.4,454GWh)ismetthroughpowerimportfromneighbouringcountries.

Afghanistancomprises10isolatedgridsorislandssuppliedbydifferentpowersystemsthrough220kVand110kVlinks.DifferentpartsofAfghanistanimportspowerfromIran,Tajikistan,Turkmenistan,and Uzbekistan. Currently, there are five transmission lines that are used for power import fromTurkmenistan,UzbekistanandTajikistanandthreelinesforimportofpowerfromIran.

Figure 20: Afghanistan’s Installed Capacity (MW) - 2016

Solar, 1, 0%Diesel Gensets, 65,12 %

Thermal, 200, 35%

Hydro,300,53%

Source:CAREC:StudyforPowerSectorFinancingRoadMap;DABSreportonAfghanistanPowerSectorOverview

3.3.1 DEMAND SUPPLY SCENARIO

Currently, Afghanistan’s energy demand-supply gap is around 50 per cent and the same trend isexpectedtocontinuetill2020.Therelianceontheimportofpowerfromneighboringcountrieswouldcontinue and the country is set to further gain from intra-regionalCBETprojects likeCASA-1000ProjectwhichwillenabletohavelinkswithPakistanandwilltransfercentralAsia’shydropowertoPakistan.

19

Potential for Power Trade in Western Part of South Asia : Techno-Economic Rationale

Figure 21: Afghanistan’s Energy Supply Scenario

-

1,000

2,000

3,000

4,000

5,000

6,000

2012 2013 2014 2015 2016 2017 2018 2019 2020 2021 2022 2023 2024 2025 2026 2027 2028 2029 2030 2031 2032

Total Capacity (MW) Peak Load (MW)

Source:AfghanistanPowerMasterPlan2013(ADB)

AccordingtotheAfghanistanPowerSectorMasterPlan,2013,thetotaldemandinAfghanistanwillincreaseonanaverageby5.7percentperannum to reach18,400GWh in2032.The totalpeakdemandin2032isexpectedtostandataround3,500MW.Thetotalcapacity(includingimportsfromneighbouringcountries)islikelytoincreasefrom1,270MWin2013to5,659MWin2032.Inenergyterms,thesituationislikelytoimprovewiththecommissioningofCASAInterconnectionin2020.ThefollowingfigureprovidesthepeakdemandandsupplyscenarioforAfghanistan.

3.3.2 TRANSMISSION INTERCONNECTIONS

Thefollowinginterconnectionsareinoperationorhavebeenproposed3

1. Interconnection with Tajikistan

Theexisting220kVdoublecircuitimportlinefromTajikistanisdesignedforaratingofabout600MW.Further,TajikistanwillbeprovidingpowertoAfghanistanthroughtheCASA-1000link.

2. CASA-1000

The Central Asia South Asia Electricity Transmission and Trade Project (CASA-1000), coveringAfghanistan,KyrgyzRepublic,PakistanandTajikistan,willputinplacethecommercialandinstitutionalarrangementsaswellastheinfrastructurerequiredfor1,300MegaWatts(MW)ofelectricitytrade.ThetotalprojectcostasperWorldBankreportisestimatedatUSD1.17billion.TheCASA-1000electricitytransmissionsystemwillhelptransformtheregionandsignifiesanimportantsteptowardrealizingtheplannedCentralAsia-SouthAsiaRegionalElectricityMarket(CASAREM).

3. Interconnection with Turkmenistan

TurkmenistanInterconnectionProjectisproposedtobedevelopedinthreestages.Thefirstphaseisunderimplementationandinvolvesconstructionofa500kVlinefromAtamyrat(TKM)toSheberghan(AFG)viaAndkhoy(AFG).Thiswillallowtheimportof300MWonthe220kVlevelthroughouttheyearandcompletionisexpectedby2017.Thesecondphase;foranadditional200MWoffirmcapacitysummingupto500MW,byupgradingto500kV,includingaback-to-backconverteratPul-e-Chomri;wouldbeavailableby2020.Inthethirdphase;anadditional500MWsummingupto1000MW,byaddingasecondback-to-backconverteratPul-e-Chomri;isscheduledfor2025.

3 Afghanistan Power Sector Master Plan Addendum Report (2014)

20

Potential for Power Trade in Western Part of South Asia : Techno-Economic Rationale

4.1 Past StudiesOverthelastdecade,severalpre-feasibilitystudieshavebeenconductedforthecrossborderenergytrade interconnectionbetween India andPakistan andalso for interconnectionwithCentralAsiancountries.Thesestudieshaveassessedthetechnical,financialandeconomicfeasibilityofthepowertradeinwesternpartofSouthAsia.Someofthekeyhighlightsofthesestudiesinclude:

1. CASA-1000ProjectCentralAsia-SouthAsiaRegionalPowerConnectivity:TheideaofCentralAsia–SouthAsiaTransmissionInterconnectionProject(CASA-1000)wasconceivedin2008totransmit1300MWofsurpluselectricity(MaytoSept)fromexistinghydelresourcesinTajikistanandKyrgyzRepublicthroughAfghanistantoPakistan.Outof1300MWofexpectedpower,300MWisreservedforAfghanistanand1000MWwillbeconsumedbyPakistan.

2. TheADB2013report4suggeststhattheshort-termpowertransfersbetweenIndiaandPakistanalsohasasignificanteconomicpotential.According to the report, the fuelcostsavings forasingleyearalonecanfundthedevelopmentoftransmission.Theestimatedinterconnectioncostfora200MWtransmissionlineof45kmlengthat220kVwouldbeUSD50millionandgoinguptoUSD150millionfor400kV5inlong-term,(2012estimate).Theannualbenefitsestimatedforthe400kVinterconnectionwasUSD491million,whichincludesfuelcostsavings.

3. TheWorldBankPolicyResearchPaper6publishedinJune2015showsthatthegridinterconnectioncapacitypotentialbetweenIndiaandPakistanwouldbe14,900MWbytheyear2040inano-carbonconstraint scenario. In this scenario, theenergy transfer fromPakistan to Indiawouldbe300TWhandenergy transfer from India toPakistanwouldbe397TWhduring theperiod2015-40.Inafullregionaltradingscenariowithcarbonconstraints,theinterconnectioncapacitypotentialwouldbe11,000MWby2040,whiletheexportfromPakistanduringtheperiod2015-40wouldbe314TWh,asagainstanimportof225TWhbyPakistanfromIndia.

4. TheSARI/EI/IRADereportonAssessmentoftheElectricityTradingPotentialintheSouthAsianRegion(May2016)estimatesthetradingpotentialbetweenIndiaandPakistantobeinexcessof44TWhfrom2021onwards,withIndiabeingthenetexporterofpowerfortheforecastperiodupto2034asshowninthefigureonnextpage:

4CBET Potential in Western Part of South Asia

4 ADB Report: RETA – Study on South Asia Regional Power Exchange (Jun 2013)5 similar to Bangladesh line, HVDC back to back6 World Bank Policy Research Paper: How Much Could South Asia Benefit from Regional Electricity Cooperation and Trade? –

Govinda Timilsina et al (2015)

21

Potential for Power Trade in Western Part of South Asia : Techno-Economic Rationale

Figure 22: Power Trading Potential between India and Pakistan (2018-2034)

- - -

44 55

65 75

84 93

102 111

120 129

139 150

161 172

FY 18 FY 19 FY 20 FY 21 FY 22 FY 23 FY 24 FY 25 FY 26 FY 27 FY 28 FY 29 FY 30 FY 31 FY 32 FY 33 FY 34

TWh

Source:SARI/EIreportonAssessmentoftheElectricityTradingPotentialintheSouthAsianRegion,May2016

4.2 Power Trade Potential In Western Part of South AsiaSalientfeaturesemergingfromtheanalysisofpowersectorsinIndia,PakistanandAfghanistanaregivenbelow:

1. Shortterm(2017to2020)

• India is likely to become energy surplus with the state of Punjab (India) being surplus in peak capacity and energy at least for 8 months.

• Pakistan will have overall energy deficit and will continue to depend on high-cost units like diesel/FO/HSD etc., to meet its demand in absence of sufficient transmission links with neighboring countries.

• Afghanistan will continue to be the net importer of electricity from the Central Asia and will have to rely on high-cost domestic generation from oil-based plants. Lack of interconnections with Pakistan will limit the potential of power export from South Asian region.

• Electricity trade can start between Pakistan and India with export of upto 200 MW power by India in the short-term. The trading of electricity is constrained by the lack of transmission infrastructure between the two countries. A phased approach for the interconnection needs to be considered.

2. Mediumterm(2021to2025)

• Development of CASA 1000 interconnection project will facilitate greater imports of electricity by Afghanistan from Central Asia, and possibly from South Asia.

• The electricity trading between India and Pakistan could increase with augmentation of interconnections and can be increased to 500 MW in the medium-term. Pakistan could also act as transit for export of power from India to Afghanistan.

3. Long-term(Beyond2025):

• Pakistan can also trade its surplus power to India or other South Asian countries if its ambitious target of power generation is realised.

• For incremental demand, Pakistan may rely on imports rather than building its own capacity, as importing coal-based power from India could work out to be economical than generation from an imported coal based power plant in Pakistan.

22

Potential for Power Trade in Western Part of South Asia : Techno-Economic Rationale

• Afghanistan can explore electricity import options from South Asia in addition to the already planned capacities in Central Asian region. More transmission interconnections through Pakistan could be planned which would link with the rest of the South Asian region.

4.3 Interconnection Options

4.3.1 INDIA - PAKISTAN

ThereareseveraloptionsforinterconnectionbetweenIndiaandPakistanwhichhavebeenidentifiedsince1990s.Thekeyamongstthemare:

y 400kVACtransmissionlinebetweenAmritsar(Punjab,India)andLahore(Punjab,Pakistan)andback-to-backHVDCsub-stationinPakistan-CostEstimatesasperstudyfundedbyWorldBankin2012-13:US$119.4million

y 220kVACtransmissionlinebetweenPatti(India)–Dinanath(Pakistan)interconnection(250MW)

y AC transmission line betweenMundra (Gujarat, India) andKarachi(Pakistan) and back-to-backHVDCsub-stationinPakistan

All recent studies indicate that interconnectionbetween theprovincesofPunjaboneither sideofborderwouldbemostappropriate, taking intoconsideration factors likedemand–supplyscenario,costof interconnectionetc.The400kVACtransmission linebetweenAmritsar (Punjab, India)andLahore(Punjab,Pakistan)andback-to-backHVDCsub-stationinPakistanhasbeenproposedaspertheWorldBankpre-feasibilitystudycarriedoutin2012-13.Thefollowingelementsofinterconnectionhavebeenproposed:

y 400/220 kV HVDC Back-to-back Convertor Station inPakistan

y 400kVD/CTransmissionLinefromBalachaknearAmritsarto Pakistan-India Border

y 400 kV D/C Transmission Line (approx. 10 km) fromConvertor Station to Pakistan-India Border

y 220kVD/CTransmissionLinefromGhaziRoadtoConvertorStation

4.3.2 AFGHANISTAN - PAKISTAN

1. CentralAsiaSouthAsia(CASA1000)Project

TheCASA-1000projectwillinclude:

y 500kVAClinefromDatka(intheKyrgyzRepublic)toSugd-500(477kilometresawayinTajikistan)

y 1300MWAC-DCConvertorStationatSangtuda(Tajikistan)

y 750 kilometre High Voltage DC line from Sangtuda(Tajikistan)toNowshera(Pakistan)

y 1300MWDC-ACConvertorStationatNowshera

Hydropowerplants(HPP)inKyrgyzstanandTajikistanwillsupplytheelectricityforCASA-1000.Theprojectcostisestimatedto Source: Central Asia - South Asia Electricity Transmission And Trade

(CASA-1000) Project Feasibility Study Update Report SNC Lavlin-

Pak

ista

n 500k

V H

VD

C -

750

km -

1300

MW

500k

V H

VAC

- 4

77km

-100

0MW

Peshawar

Kabul300MW

1300MW

Tajikistan Internal AC Grid

AC/DC Converter Station

Sangtuda

Khoudjand

Datka

Tajik

ista

nA

fgah

inis

tan

Kyr

gyza

tan

Figure 23: CASA 1000 Project

23

Potential for Power Trade in Western Part of South Asia : Techno-Economic Rationale

beUSD1.16BillionandisbeingsupportedbytheWorldBankGroup,IslamicDevelopmentBank,UnitedStatesAgencyforInternationalDevelopment(USAID),USStateDepartment,UnitedKingdomDepartment for InternationalDevelopment (DFID),AustralianAgency for InternationalDevelopment(AusAID)andotherdonorcommunities.

TheproposedCASA1000transmissionhastheflexibilityofbidirectionalflowsonthesystem.Asaresult,AfghanistansystemcanprovidepowertoPakistanincaseTajikistan/Kyrgyzsystemisunabletoprovidethefull1,300MWofexportpower.Similarly,AfghanistancanimportpowerfromPakistanincaseofneed.

2. Turkmenistan-Afghanistan-Pakistan500kVLine(TAP-500)

TheproposedTurkmenistan-Afghanistan-Pakistan500kVLine (TAP-500)projectwill facilitateyear-roundpower export fromTurkmenistan tobothAfghanistan andPakistan.By2020, Turkmenistanexpectstogenerate3,500MWofexcesspowertobeavailableforexport.ThetripartiteagreementhasbeensignedbythethreeheadofstatesinDecember2015.

24

Potential for Power Trade in Western Part of South Asia : Techno-Economic Rationale

5.1 Proposed Interconnection Between India and Pakistan

5.1.1 TECHNICAL ASSESSMENT

The proposed connection is required to have back-to-back HVDC sub-station, to make theasynchronousconnectionbetweenIndiaandPakistan,whichoperateondifferentfrequencies.Theprojectislikelytotakeupto36-40monthsforimplementation,astheconstructionofHVDCback-to-backstationshallhavelongergestationperiodofabout36months,whilethetransmissionnetworkcanbecompleted in about24months.The following technical interfacehasbeenconsidered forcarryingoutthetechno-economicanalysisfor400kVACtransmissionlinebetweenAmritsar(Punjab,India)andLahore(Punjab,Pakistan)andback-to-backHVDCsub-stationinPakistan:

y 400 kV D/C Transmission Line (approximately 26 kms) from Balachak near Amritsar (India) toPakistan -India Border

y 400kVD/CTransmissionLine(approximately10kms)fromConvertorStationinLahoretoPakistan-India Border

y 400/220kVHVDCback–to–backSubstationinLahoreforasynchronousinterconnectionmode

y 220kVD/CTransmissionLinefromGhaziRoadtoConvertorStation

y CostEstimatesasperstudyfundedbyWorldBankin2012-13:US$119.4million

Figure 24: Pakistan – India Interconnection

Source:NTDCL,Pakistan

5 Techno-Economic Rationale

25

Potential for Power Trade in Western Part of South Asia : Techno-Economic Rationale

Apossibleoptionwouldbetoconnectthesystemsinradialmodeat220kVvoltagelevelintheinterimperiod tillcommissioningofHVDCsub-station.TheconnectionwithHVDC linkbetweenBalachaksub-stationinAmritsar,Punjab(India)andGaziRoadsub-stationinLahore(Pakistan)isshownintheFigure25below.

The following stages of development of the interconnection have been considered for economicanalysis

1. Stage 1 -Supply of power to Lahore from India in radial mode

Underradialmodeofoperation,aportionofLahoreGridshallhavetobeisolatedandconnectedtoIndianGridthroughthe400kVdoublecircuittransmissionline,whichwouldinitiallybechargedat220kV.Around150-200MWloadcanbesegregatedforsupplyofpowerfromIndiaasshownbelow:

Figure 25: Stage 1 – 200 MW Transfer Capacity in Radial Mode

BalachakSub-station

Gazi Road Sub-station

400 kV Line charged at 220 kV

India-Pakistan Border

Lahore, Pakistan Amritsar, India

Load ~ 200 MW

Connection in radial mode

Disconnection from Lahore Grid

200 MW power transfer

2. Stage2:Developmentof500MWHVDCback-to-backsub-station

The construction of back-to-back HVDC sub-station would enhance the power transfer capacitybetweenthetwocountriesto500MWwithinthreetofouryears.

Figure 26: Stage 2 – 500 MW HVDC Sub-station

IndiaPakistan

PGCILSystem

PSTCL

Power Exchange (IEX/ PEX)

Power Trader

PSPCL

NTDCTransmission

System

500 MW B-B HVDC

S/S

LESCO

400 kV Transmission Line

500 MW Power Transfer

26 km10 km

BalachakS/S

400 kV and 220 kV AC Switchyard

India-Pakistan Border

26

Potential for Power Trade in Western Part of South Asia : Techno-Economic Rationale

5.1.2 COST ESTIMATION FOR INDIA PAKISTAN INTERCONNECTION

Thecapitalcostfortheprojecthasbeenestimated,basedontheprevailingtrendsinSouthAsianmarket.Therecentbenchmarkcostsfromtheregionhavebeenconsidered.

Table 5: Reference Cost of Similar Projects

Project Estimated Cost (USD Million)

India-BangladeshHVDCBlock–I

y 125kmof400kVdoublecircuit(D/C)T/LbetweensubstationsatBaharampur(India)andBheramara(Bangladesh)

y 400kVswitchingstationatBaharampur y 500MWback-to-backHVDCsub-stationatBheramara

USD193Million(excludesIndiansidetransmissionlinecost)*

India-BangladeshHVDCBlock-II

y 500MWback-to-backHVDCsub-station

USD144Millionin2015

CASA-1000

y 500kVHVACT/LfromKyrgyztoTajikistan(477km) y ±500kVHVDCT/LfromTajikistantoPakistanviaAfghanistan(750km)

y 300MWHVDCsubstationatKabulinAfghanistan y 1300MWHVDCconvertorstationatTajikistan y 1300MWHVDCconvertorstationatPeshawar

USD1.17Billionincluding208millionIDC

*Revisedcostestimates2015

ThetotalcostofinterconnectionincludingIDCandcontingencyfortwostagesisshownintheTablebelow:

Table 6: Interconnection Project Estimated Cost

Cost of Proposed Interconnection USD Million

Stage I 16.9

Stage II 108.1

Total 125.0

5.1.3 IMPLEMENTATION SCHEDULE

Theprojectcanbecompletedin54monthsbuttherearechallengesintheimplementationgiventhecomplexitiesinprocurementandimplementationduetothevaryingrequirementsinbothcountries.

Thepre-awardstagecomprisingofstudies,finalisationofspecificationsandtenderdocuments,awardofEPC-turnkeyContractscouldtakeupto18months.TheexecutiontimeforStageIisexpectedtobe24monthsposttheawardofcontract.TheStageIIislikelytotake36monthstocompletefromtheawarddate.Indicativetimelinesfortheproposedprojectisshownbelow.

Figure 27: Implementation Schedule

Appointment of Consultant

Issuance of RfP

M0 M12

Award of Turnkey Contract

M18 M42

Stage I: 400 kV D/C line Ready

Stage II: HVDC Converters ready

M48

Stage II: System

M54

Studies Completed

M8

27

Potential for Power Trade in Western Part of South Asia : Techno-Economic Rationale

5.1.4 COST-BENEFIT ANALYSIS

1. EconomicrationaleoftheProject

TheSouthAsiancountriesarenet importersof fossil fuelssuchascoal,oilandoilproducts fromoutside the region. Considerable benefits could be derived from tapping hydropower potential inBhutan,IndiaandNepalandfromutilisingthedifferingseasonalloadcharacteristicsofthecountriesintheregion.Theinterconnectionofpowertransmissionofthesecountrieshasbeenapriorityinthepastfewyearsinordertoutilisetheresourcesavailableintheregion.Regionalinterconnectivitycouldhelpcountriesmanagepowershortages,avoidpoweroutagesandimprovesystem-wideefficiency.Currently,IndiaimportspowerfromBhutanandexportspowertoNepalandBangladesh.TheIndia–Pakistancrossborderproject,whenimplemented,willprovideasuccessfulexampleofpowertradingbetweentwocountriesintheregion,contributetowardsmeetingthegoalofprovidingpowertoall,andbringeconomicbenefitstotheregion.

Pakistanhasexperiencedrapidlygrowingenergyneedstosustainitsgrowth,particularlyintheindustrysector.LackofgenerationcapacityadditionsandchallengesinoperatingtheexistinggeneratorduetofuelshortageshaveresultedinelectricitysalesinPakistannotmatchingthedemand.Peakdeficitofover5,000MWwasrecordedin2015.Thegovernmenthasplannedseveralinitiativestominimisepowershortagesbyplanninghydropowercapacityadditions,relyingonimportedgasandpetroleumandbypreparingprojectsbasedon importedcoal.Sourcingpower from theSouthAsia region isanotheroptionthatcanprovideafastandefficientmechanismtooffsetshortages.TheelectricalgridinterconnectionfacilitybetweenIndiaandPakistanwillpartiallyalleviatethecurrentpowercrisisbyproviding200–500MWofpowerfromIndia.TheprojectwillfacilitateimportsofcheapandreliablepowerfromIndiaforuseinPakistan,asignificantpartofthedemandbeingattributedtoindustrialactivities.

InPakistan,around30percentofelectricityisproducedfromgas-basedpowerplantsand35percent from petroleum products (Diesel and FO). The delays in capacity installation programmehasforcedelectricityutilitiestoresorttoloadsheddingincludingindustrialconsumerswhichhavebeenusingcaptivegenerationfacilities.Thedependenceonimportedcoalbasedplantsisalsoincreasing.

2. Keyassumptions

India-Pakistan Electrical Grid Interconnection will allow an exchange of power between the twocountries.Itwillinitiallyfacilitatethetransmissionof200MWofpowerfromIndiatomeetexistingandfuturedemandsinPakistan.Thiswillbeincreasedto500MWwithestablishmentofHVDCstation.Thisisthebasecasewhichhasbeenusedfortheanalysis.

Theprojectcostandthebenefitsfortheproposedinterconnectionhasbeenworkedoutbasedonfollowingassumptions:

y Allcostsareexpressedinconstant2016prices.Thecapitalcostestimatesincludecontingenciesandfinancialchargesduringconstruction.

y TheprojectcostincludesinvestmentandmaintenancecostsofPakistantoIndiatransmissionline,costofotherassociatedfacilitiesandannualpaymentstotheIndianentitiesfordeliveryofpowertoPakistan.Thepublishedreportshavebeenrelieduponfordata.

y Theprojectwillbefundedbymulti-lateralagenciesandwillbeownedbythetransmissionlicenseesintherespectivegeographies.

y PowerwillbeavailableforsaletoPakistanfromthesurpluswithPunjabstateinIndiaandalternatelythroughthemedium-termcontractingwiththelicensedpowertradersinIndia.Intheshort-termperiod,powercouldbepurchasedfromthepowerexchange(s)inIndiatomeetanyshort-fallinenergy.

28

Potential for Power Trade in Western Part of South Asia : Techno-Economic Rationale

y TheavailablepowerfromIndiawouldbeusedforreplacingthecostlierfuelswithinPakistanvizHSD/FO and imported coal. The additional powerwould be available for sale to the industrialconsumersincaseenergydeficitsituationprevailsinthemedium-term.

y Noenvironmentalandsocialcostsorbenefitshavebeenquantifiedorusedfortheinterconnectionproject.

y Theinformation/dataasexistedinpublicdomainandobtainedandcollectedfromvariousotherprimaryandsecondarysourcesasonJuly,2016.

3. EconomicAnalysis

Aperiodof25yearshasbeenassumedfortheeconomicanalysisandastandard12percentdiscountratewasusedtocalculatethelevelisedtariff.Capitalcostswerespreadoverthefirst3yearsbasedonconstructioncycleofsimilarprojects.Capacityutilisationofthetransmissionlineswasassumedtobe85percentinestimatingthequantityofpowertransmitted.

ThefollowingtableshowsthepricecomparisonbetweenvariousoptionsforprocurementofadditionalpowerfortheperiodFY19toFY34.ThelevelisedcostofpowerprocurementfromIndiaincludingthetransmissiontariffforIndiansystemandthetransmissionchargesfortheproposedinterconnectionhavebeencomparedwiththepowergenerationtariffsinPakistan.

FortheIndiansystem,thefollowingpowertariffshavebeenassumedforthebaseyear(2016)

Table 7: Power Tariffs in India

Indian power market tariff Tariff (US cents/kWh)

LongtermPPA 6.32

PowerExchange 5.49

PowerTraders 6.22

ForPakistan,whilehydropoweristhemosteconomicsourceofelectricity,domesticgasisnextlowcostresource,theavailabilityofwhichislimited.TheFurnaceOil-basedandHSD-basedgenerationisthecostliest.PakistanalsohassizablecoalreservesinTharregion,butcurrentlythereareconstraintsincoalproduction.Thedevelopmentofdomesticcoalfieldswill take timeandthedependenceonimportedcoalislikelytoincreaseinordertoreplacetheoil-basedgeneration.

ThefeasibilityoftheinterconnectionhasbeenassessedfromtheperspectiveofbothPakistanandtheregion.TheEconomicInternalRateofReturn(EIRR)ofthetransmissionprojecthasbeencalculatedassumingadedicatedtransmissionlinetoevacuatepowerfromadesignatedplant.

Theresourcecostsavingshavebeenconsideredforthebasecaseasdiscussedabove.Theresourcecost savingswere basedon the assumption that oil-basedgeneratorswould be used alongwithimported coal-based plants in the absence of the project. In the base case, the resource costsavingswereused toestimate thebenefits.The levelisedcostofgeneration for importedcoalhasbeen conservatively estimated at 9.70US cents per kWh for the base-case calculation. With thePakistan–India transmissionnetwork inplace,Pakistanwill be in aposition to import power fromIndia at a relatively cheaper cost in short to medium-term. The tariff for the power from tradersin India is based on the available power in short to medium-term and the trading margin andtransmission charges for delivery of power are based on theCERC-approved tariffmethodology.Marketbasedpowerpurchasecosts formediumandshort-termpower supplyareconsidered. InFY2016, the total tariffworksout toabout INR4.2perkWh.A2percentannualescalation rate hasbeenconsidered.

29

Potential for Power Trade in Western Part of South Asia : Techno-Economic Rationale

Theeconomiccost–benefitanalysisindicatesthatthebasecaseresultsinanEIRRof22.14percent.TheprojectislikelytogiveabenefitofUSD210Millionagainstthetotalcostof125Million.TheB/Cratioof theprojectworksout tobe1.68.Theproject iseconomicallyviable in thebasecase.Thefollowingtableshowsthecostsandbenefits:

Table 8: Cost-Benefit of the Project(AllfiguresinUSMillion)

Year Capital Cost & Operating Cost

Cost of Power Purchase

Total Cost Gross Benefit

Net Benefit

2017-18 25.04 - 25.04 - (25.04)

2018-19 51.16 - 51.16 - (51.16)

2019-20 27.51 90.11 117.62 115.16 (2.46)

2020 - 21 0.98 204.63 205.61 257.05 51.44

2021 - 22 1.00 165.97 166.98 204.92 37.94

2022 - 23 1.02 134.63 135.65 163.36 27.71

2023 - 24 1.04 109.21 110.25 130.23 19.98

2024 - 25 1.06 88.59 89.65 103.82 14.16

2025-26 1.09 71.87 72.95 82.76 9.81

2026-27 1.11 58.30 59.41 65.98 6.57

2027-28 1.13 47.30 48.43 52.60 4.16

2028-29 1.15 38.38 39.53 41.93 2.40

2029-30 1.18 31.14 32.32 33.43 1.11

2030 - 31 1.20 25.27 26.47 26.65 0.18

2031 - 32 1.23 20.50 21.73 21.24 (0.49)

2032 - 33 1.25 16.64 17.89 16.93 (0.95)

2033 - 34 1.28 13.50 14.78 13.50 (1.28)

2034 - 35 1.31 10.96 12.26 10.76 (1.50)

2035-36 1.33 8.89 10.22 8.58 (1.64)

2036-37 1.36 7.22 8.58 6.84 (1.74)

2037-38 1.39 5.86 7.24 5.45 (1.79)

2038-39 1.42 4.75 6.17 4.35 (1.82)

2039-40 1.45 3.86 5.30 3.47 (1.84)

2040 - 41 1.48 3.13 4.61 2.76 (1.85)

2041 - 42 1.51 2.54 4.05 2.20 (1.85)

2042 - 43 1.54 2.06 3.60 1.76 (1.85)

2043 - 44 1.57 1.67 3.25 1.40 (1.85)

2044 - 45 1.51 1.36 2.86 1.12 (1.75)

AsensitivityanalysishasbeenundertakenbasedonthesaleofpowertotheindustrialconsumersintheLahorearea.ThelevelisedtariffofUScents11.72perkWhhasbeenassumedbasedonthe

30

Potential for Power Trade in Western Part of South Asia : Techno-Economic Rationale

existingapplicabletariff fortheindustrialcategoryfortheanalysis.ThisgivesasignificantlyhigherEIRRandB/Cratio(3.33).Theprojectissensitivetocostescalationsandlowerlevelsofutilisation. A10percentcostincreasewouldgiveanEIRRof17.1percentandautilisationbelow75percentwillresultinnegativeEIRR.

ThesurpluspowersituationinNorthernIndiaislikelytocontinueandgiventherelativelysmallquantumofpowerrequirement,theriskofoutageonaccountoflackofpoweravailabilityisremote.

GiventhedevelopmentofthetradingmarketinIndiaaswellasthelevelofmarginalcostofelectricityinPakistan,itisnotexpectedthatthelinewillremainunutilisedoveritslifeoncebuilt.Overall,theanalysis shows that theproject is economically viable andprovides stable benefits under variousscenarios.

5.2 CASA 1000 Interconnection between Afghanistan and PakistanThetechno-commercialanalysisfortheCASA1000projectwasassessedbySNCLavalinandFinalFeasibilityStudyReportsubmittedinFebruary2011.

SNCLavalin was commissioned to prepare a feasibility study, in two phases, for the regionalinterconnection.ThefinalPhase1reportwassubmittedinDecember2007andthePhase2report,inJanuary2009.

Thekeyexcerptsfromthefeasibilityreportareasbelow:

5.2.1 TECHNICAL ASSESSMENT

TheHVDClinkbetweenTajikistan,AfghanistanandPakistaniscomprisedof1,300MWconvertersinTajikistanandPakistan,a300MWconverterinAfghanistananda1,300MW,750kmtransmissionline.TheCASAprojectalso includesanHVACtransmission linebetweentheKyrgyzRepublicandTajikistan,477kmlongandratedat1,000MW.

Theprojectisbasedontheexpectationthatsufficientsurpluspowerisavailableinthecountriesinthenorthtorepresentasubstantialpotentialfortradewiththecountriesinthesouth.Moreover,thecostofelectricityinthesendingcountriesisbelowthelong-runmarginalcostinthereceivingcountries,providingajustifiablerationaletoinvestinthetransmissioninterconnection.

5.2.2 COST ESTIMATES

AccordingtoSNCLavalinestimates,thecostoftherecommendedprojectisUSD873Million(Feb2011reportestimates),excludingInterestDuringConstruction(IDC). IDCamountstoanadditionalUSD80million.Theprojectisfoundtobeeconomicallyviablebasedona10percentdiscountratewithaBenefit/Costratioof1.3percentandanEIRRof15.6percent.

31

Potential for Power Trade in Western Part of South Asia : Techno-Economic Rationale

TheoverallCBETpotentialfortheSouthAsiaisverylarge.Theeasternpartoftheregionhasseensignificant developments in creation of the transmission infrastructure which has the potential oflinkingwithSouthEastAsiathroughMyanmar.Thewesternpartoftheregionisstilltowitnesssimilardevelopments.

A potential linking of Afghanistan–Pakistan and Indian grids could facilitate development of aninterconnectedsystembetweenCentralAsiaandSouthAsiawhichwouldbenefit thecountries intheseregions.

The current techno-commercial analysis is focusedon the India-PakistanCrossBorder ElectricityTrade,butthesamecouldbeextendedtocoverthewholeofwesternregionincludingAfghanistan.

Withthedevelopmentof India-Pakistan interconnection, IndiacanexportpowertoPakistan intheshort-term,since the later is experiencing huge power shortage. In the long-term, Pakistan canbecomesurplusandexporttoIndiabecauseofitsaggressivepowergenerationadditionaswellaslikelyconnectivitytotheCentralAsiansystem.Eitherway,theSouthAsianregionissettobenefitfromtheoptimalsourceofpowergeneration.

TheincumbentcountriesinthewesternpartofSouthAsianregioncouldformajointcommitteetoevaluatetheelectricitytradepotential.Thenodalagenciesfromrespectivecountriescouldbeidentifiedandgiventheresponsibilitytoworkoutvarioustechno-commercialissues.Adetailedfeasibilitystudyfortheidentifiedinterconnectionscouldbetakenupimmediatelytofinalisethecostsandalignment.

Various technical issueswouldneed tobe looked for viz. harmonisationofgridconnectioncode,operatingparametersetc.TheCASA1000Project,whichwouldestablishthelinkbetweenAfghanistanandPakistan,couldestablishbenchmarksfortheintegratedoperation.

Way Forward

32

Potential for Power Trade in Western Part of South Asia : Techno-Economic Rationale

1. Central Asia - South Asia Electricity Transmission and Trade (CASA-1000) Project FeasibilityStudyUpdateReport–SNCLavalin,Feb2011

2. EnergyTrade inSouthAsiaOpportunitiesandChallenges–ADB(Dec2011)-PriyanthaD.C.Wijayatunga,HerathGunatilake,P.N.Fernando

3. Cross-BorderPowerTradinginSouthAsia:ATechnoEconomicRationale-PriyanthaWijayatunga,D.ChattopadhyayandP.N.Fernando;August2015

4. StudyonaSouthAsiaRegionalPowerExchange–ADB(June2013)

5. PerspectiveTransmissionPlanforTwentyYears(2014-2034)(Aug2014)-GovernmentofIndia,MinistryofPower,CentralElectricityAuthority,PGCILandPOSOCO

6. SouthAsiaRegionalWorkshoponCompetitiveElectricityMarkets–Design,Implementation&BenefitsColombo,SriLanka,(Mar2014)-MuhammadWaseemYounas,SohailMumtazBajwa

7. SAARCPerspectiveWorkshoponthePast,PresentandFutureofHighVoltageDC(HVDC)PowerTransmission,Lahore,Pakistan(Oct2015)-MuhammadWaseemYounas

8. TheEnergyCooperationInSouthAsiaUnderSaarcUmbrella,The6thJapan-SAARCSymposium(March2013),Kathmandu,Nepal-Dr.MuhammadPervaz

9. SecuringIndia’sEnergyFuture(Oct2012),ColonelDevindarKumar,

10. Cross-BorderElectricityTradeinSouthAsia:KeyPolicy,RegulatoryIssues/ChallengesandtheWayForward-WorkshopontheSustainableDevelopmentofPowerSectorandEnhancementof Electricity Trade in the South Asian Region, New Delhi, India (Jan 2016), SARI/EI ProjectSecretariat,IRADe,Dr.JyotiParikh,Mr.V.K.Kharbanda,Mr.RajivRatnaPanda

11. Modelling, Investment Planning and Optimisation for the Design of a Polygeneration EnergySystem,Elsevier(2007)–PeiLiu,DimitriosI.GerogiorgisandEfstratiosN.Pistikopoulos

12. DevelopingaRegionalPowerMarketinSouthAsia,9thCapacityBuildingProgrammeforOfficersoftheElectricityRegulatoryCommissions–(Nov2015),AnoopSingh

13. CentralElectricityAuthorityWebsite(http://www.cea.nic.in/)

14. IndiaEnergyExchangeWebsite(http://www.iexindia.com/)

15. NationalElectricPowerRegulatoryAuthorityWebsite(http://www.nepra.org.pk/)

16. NationalTransmissionandDispatchCompanyLtdPakistanWebsite(http://www.ntdc.com.pk/)

17. LahoreElectricSupplyCompanyWebsite(http://www.lesco.gov.pk/)

Bibliography

33

Wearegratefultoallthestakeholderswhohaveprovidedtheirvaluableinputs/suggestioninpreparingandfinalizingReporton“PotentialforPowerTradeinWesternPartofSouthAsia:Techno-EconomicRationale”.

We are grateful to United States Agency for International Development (USAID) for its generoussupport.Wewould like toexpressoursincere thanks toMs.MonaliZeyaHazra,RegionalEnergyManagerandCleanEnergySpecialistfortheirvaluableinputsandsuggestions.

WesincerelythankDr.KiritS.Parikh,FormerMember,PlanningCommission,India,andChairman,IRADeandDr.JyotiParikh,ED,IRADefortheirvaluablesuggestionsandguidanceallalong.

WealsothankMr.RajivRatnaPanda,Head-TechnicalatSARI/EIProjectSecretariatforallhisvaluableanalyticalandtechnicalinputsandsuggestionsinpreparationofthisreport.

WewouldliketothankSARI/EIconsultantviz.Mr.TusharSudandMr.RajneeshSharmaofDeloitteToucheTohmatsuIndiaLLP(DTTLLP),forpreparingandfinalisingthisreport.

WealsoliketothankMr.Nikhil,ResearchAssistant,IntegratedResearchandActionforDevelopment(IRADe)forprovidinghissupportinreportwritingcopyeditinganddesigningofthereport.

Wealsoacknowledgeandexpressourappreciationforallthoseindividualswhosenamescannotbepennedherebutwhohaveofferedvaluableinsightsandgeneroussupportthroughoutthisexercise.WehopethatthisreportwillinitiatethoughtprovokingdiscussionamongSAcountrygovernments,electricity regulators of South AsianCountries, Policy and decisionmakers, developers/investors,financialinstitutionsandwillserveasavaluableresourcedocumentforpromotingCBETinPanSouthAsiaRegion.

Acknowledgements

34

ABOUT SARI/EI

Over the past decade, USAID’s South Asia Regional Initiative/Energy (SARI/E) has been advocating energy cooperation in South Asia via regional energy integration and cross border electricity trade in eight South Asian countries (Afghanistan, Bangladesh, Bhutan, India, Pakistan, Nepal, Sri Lanka and the Maldives). This fourth and the final phase, titled South Asia Regional Initiative for Energy Integration (SARI/EI), was launched in 2012 and is implemented in partnership with Integrated Research and Action for Development (IRADe) through a cooperative agreement with USAID. SARI/EI addresses policy, legal and regulatory issues related to cross border electricity trade in the region, promote transmission interconnections and works toward establishing a regional market exchange for electricity.

ABOUT USAID