portfolio of advanced benefits work

DESCRIPTION

A collection of works and branding that I developed while employed at Advanced BenefitsTRANSCRIPT

Ad

van

ced

Ben

efit

s

MyAdvancedBenefits.com800.664.3482 | 208.664.3482

90 Day Navigation ProposalUpon appointment of your medical plan I will complete a full market analysis for all carriers and plans

available. With the best rates and plans available from the market I will put together a number of solutions

that show the integration of the following consumer driven health care concepts with a medical plan;

giving you the blueprint to your ultimate goal of lower premiums and enhanced benefits.

Health Saving Accounts • Health Reimbursement Arrangements Full Flexible Spending Accounts • Dual Option

Premium increases and forced benefits slashings have strong armed this communitie’s employers and

employees

The employee benefits world has seen more change than ever, making it a perfect time to revitalize.I can guarantee one of two things after 90 days:

1. I will earn your business with our solutions and customer service.

OR2. Your current broker works even harder for you.

Either way, you win!

Client Service Process:Your Employee Benefits need attention 365 days a year.

• 6 Month Review Meeting • 90 Day Pre-Renewal Meeting • Renewal Negotiations

• Employee Education Meetings • Post Renewal Stewardship Meeting • Year Round Quoting New Product/Carriers As They Become Available

Did you know:The following carriers are available in Idaho?

• Blue Cross of Idaho • Regence Blue Shield of Idaho• Pacific Source • Altius • Starmark

• Group Health (50 or more employees) • United Health Care

Health Care Reform and YouWhat are you doing to stay compliant with Health Care Reform? There are over 2000 pages that affect

you and your employees starting in 2010 through 2018.

Let our team of experts ensure you and your company are in compliance with these new laws!

About Advanced Benefits History, Profile and Qualifications

Advanced Benefits provides employee benefit consulting and insurance brokerage services to employers in the Inland Northwest. Our vision early on was to provide added value services wherever feasible in order to create a better experience in the management and use of today’s employee benefit programs.

Today, Advanced Benefits is comprised of over 20 full-time, industry-seasoned benefit professionals. Our collective experience exceeds 100 years and ranges the gamut of the insurance sales and service spectrum. Represented on the Advanced Benefits team are people whose resumes include positions with firms such as Blue Cross of Idaho, Premera Blue Cross, Blue Cross of California, New York Life Health Insurance Company, Metropolitan Life, American Fidelity, and Aetna.

Our scope of experience with employers runs wide. We serve groups of all sizes and all benefit platforms. We have extensive experience in managed care, PPO networks, self-funded plans, and extensive education and implementation of Consumer-Driven benefit options including HRAs and HSAs.

Collectively, our team of professionals spends numerous hours annually in Continuing Education programs to keep abreast of trends and changes with the potential to affect the strategic plans of our customers.

Advanced Benefits serves several hundred public and private employer clients across a broad spectrum of industries. This broad client base offers a balanced perspective when discussing benefit issues with committee members and/or employees whose background or spousal involvement is from the private perspective.

We specialize in serving the needs of employers with regards to group benefit plan consulting. However, our range of experience and training allows us to address, with objectivity (no selling), a host of ancillary coverages that may prove beneficial to your insurance committee and/or employees; including the areas of: supplemental insurance (Aflac-type policies), Medicare planning, long-term care, life and disability coverages.

In addition, Advanced Benefits’ staff can provide services to terminated or retired employees in the areas of Short-Term Coverage, Individual Coverage, and Medicare Supplement Coverage.

MyAdvancedBenefits.com800.664.3482 | 208.664.3482

Ahead of the CurvePartners make a difference!

Ad

van

ced

Ben

efit

s

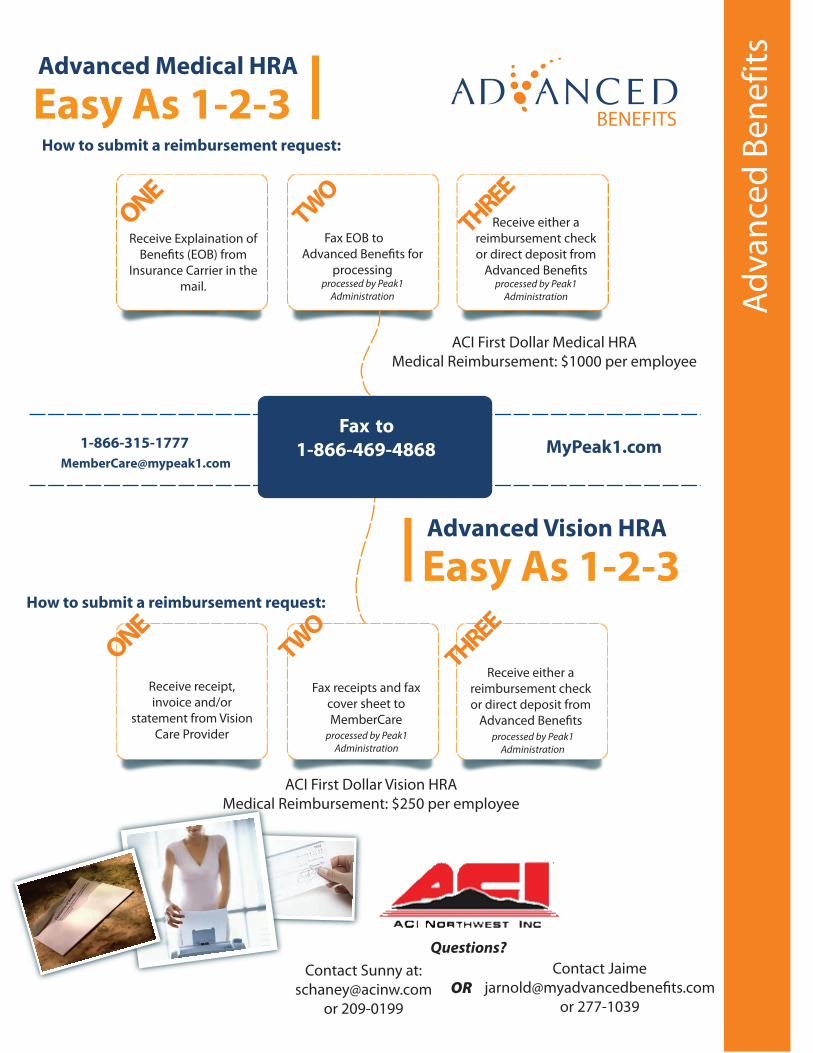

Advanced Medical HRA

Receive receipt, invoice and/or

statement from Vision Care Provider

Fax receipts and fax cover sheet to MemberCare

Receive either a reimbursement check or direct deposit from

Advanced Bene�ts

Advanced Vision HRA

Receive Explaination of

Insurance Carrier in the mail.

Fax EOB to

processing processed by Peak1

Administration

Receive either a reimbursement check or direct deposit from

processed by Peak1 Administration

processed by Peak1 Administration

processed by Peak1 Administration

ACI First Dollar Medical HRAMedical Reimbursement: $1000 per employee

ACI First Dollar Vision HRAMedical Reimbursement: $250 per employee

Questions? Contact Jaime

jarnold@myadvancedbene�ts.comor 277-1039

Contact Sunny at:[email protected]

or 209-0199OR

Ad

van

ced

On

e So

urc

e So

luti

on

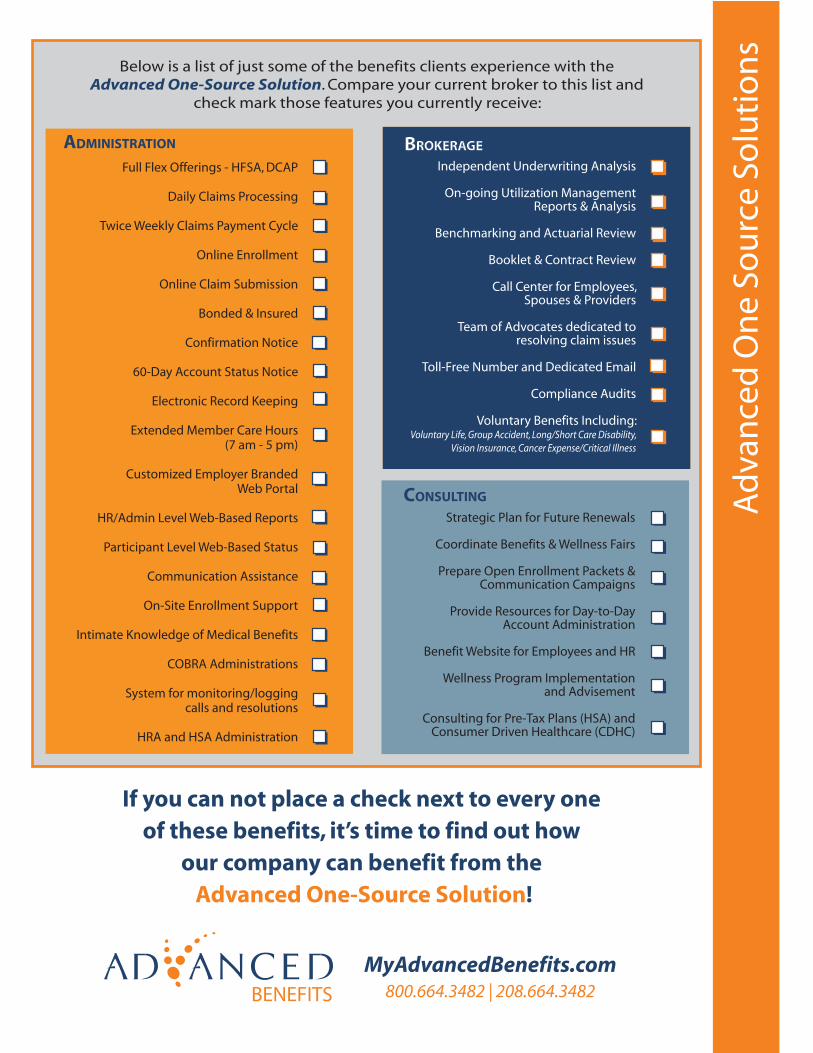

sSimplicity An integrated approach to ALL your benefit needs in one place!

We understand that employee benefits can be a challenging aspect of attracting and retaining the best

employees. At Advanced Benefits, we work hard to take the stress and confusion out of the equation for

you with our Advanced One-Source Solution. Bringing together all of the aspects of an effective

employee benefits solution under one roof gives our clients the most efficient and effective solutions

for their employees.

With over 20 employees and 100+ years of experience, Advanced Benefits works hard to ensure your

employees are getting the most out of the benefits you offer, while always making sure it is the best

solution for your company.

MyAdvancedBenefits.com800.664.3482 | 208.664.3482

Ad

min

istr

ati

on

Brokerage

Consulting

The Advanced One-Source Solution can enhance your current employee benefits

package in these important areas:

The Region’s Exclusive Members of the Bene�t Advisors Network, Smart PartnersTM: Through this membership we can provide you with unprecedented levels of access to the expertise, knowledge, strategies and proprietary tools from some of the most prestigious and progressive bene�t �rms in the United States.

Ad

van

ced

On

e So

urc

e So

luti

on

s

MyAdvancedBenefits.com800.664.3482 | 208.664.3482

ADMINISTRATION BROKERAGE

CONSULTING

Full Flex Offerings - HFSA, DCAP

Daily Claims Processing

Twice Weekly Claims Payment Cycle

Online Enrollment

Online Claim Submission

Bonded & Insured

Confirmation Notice

60-Day Account Status Notice

Electronic Record Keeping

Extended Member Care Hours (7 am - 5 pm)

Customized Employer Branded Web Portal

HR/Admin Level Web-Based Reports

Participant Level Web-Based Status

Communication Assistance

On-Site Enrollment Support

Intimate Knowledge of Medical Benefits

COBRA Administrations

System for monitoring/loggingcalls and resolutions

HRA and HSA Administration

Independent Underwriting Analysis

On-going Utilization Management Reports & Analysis

Benchmarking and Actuarial Review

Booklet & Contract Review

Call Center for Employees, Spouses & Providers

Team of Advocates dedicated to resolving claim issues

Toll-Free Number and Dedicated Email

Compliance Audits

Voluntary Benefits Including:Voluntary Life, Group Accident, Long/Short Care Disability,

Vision Insurance, Cancer Expense/Critical Illness

Strategic Plan for Future Renewals

Coordinate Benefits & Wellness Fairs

Prepare Open Enrollment Packets & Communication Campaigns

Provide Resources for Day-to-Day Account Administration

Benefit Website for Employees and HR

Wellness Program Implementation and Advisement

Consulting for Pre-Tax Plans (HSA) and Consumer Driven Healthcare (CDHC)

Below is a list of just some of the benefits clients experience with the Advanced One-Source Solution. Compare your current broker to this list and

check mark those features you currently receive:

If you can not place a check next to every one of these benefits, it’s time to find out how

our company can benefit from the Advanced One-Source Solution!

Ad

van

ced

Ben

efit

sThe Value of Smart Partners™ Advanced Benefits is excited to announce our membership in the Benefit Advisors Network. In being

accepted for membership, this prestigious national organizations has identified Advanced Benefits as the

“best of the best” benefits brokerage in the Northern Idaho region. We are excited to share with you how

this membership will benefit you through the BAN’s Smart Partners™ program.

Why should I work with a Smart PartnerTM?When you work with a member of Benefit Advisors Network, you benefit from the shared expertise of highly qualified benefit specialists, our Smart PartnersTM. From throughout the United States, each member is carefully selected, qualified and recognized as an expert in their marketplace.By combining the "best of the best" resources and tools in benefit planning, communication and administration, Benefit Advisors Network has developed an unparalleled suite of services and tools known as Smart Services.Smart PartnersTM are local business owners, not merely staffers or executives of a national conglomerate. They have firsthand knowledge of your local economy and culture as well as the unique issues in your marketplace.

Can a Benefit Advisors Network Smart PartnerTM cut through the “red tape”?Because of its outstanding national reputation and strength, Benefit Advisors Network has unparalleled clout with carriers. Many of these carriers have established special "pipelines" to help our members work through service issues and cut "red tape." And, because our members are recognized as the "best of the best" in the country, many carriers honor their experience and expertise by providing them with direct access to underwriters. That means our members are better able to offer you even more creative plan designs, value pricing, and savings.

What is the benefit of working with a Smart PartnerTM?Through their association with Benefit Advisors Network, Smart PartnersTM provide their clients with unprecedented levels of access to the expertise, knowledge, strategies and proprietary tools from some of the most prestigious and progressive benefit firms in the United States.

What are some of the services that a Smart PartnerTM provides?

Through collective resource sharing, Smart PartnersTM provide world class services and solutions (Smart Services) to their clients.

These services include:• Smart COBRA – Smart COBRA administers the continuation of group health coverage for qualified beneficiaries and handles it efficiently while maintaining compliance with all regulations.• Smart FSA – Smart FSA helps your company maximize its compensation packages in order to attract and retain quality employees, and to do so cost effectively.• Smart Wellness – Smart Wellness ensures that the administration of Population Health Management is as efficient and cost-effective as possible while freeing up your time and resources to focus on more strategic activities.• Smart Compliance – Smart Compliance was developed to help your company avoid the many common pitfalls of health and welfare compliance that impact productivity and profit.• Smart Payroll - Smart Payroll provides online payroll services and online human resources software with the ultimate in features and flexibility.

• Access to Industry Leaders such as; • Medical Director, Dr. David Rearick - specializing in wellness, population health management and claims analysis • Compliance Director, Peter Marathas, Esq. - specializing in ERISA and employment law • Pharmacy Director, Armand Dilanchian, R. Ph. - specializing in analysis of Rx claims and industry trends

• Professionally Conducted Monthly Webinar Series conducted for members and their clients• Compliance, Legislation and Trends Updates and Alerts including a Compliance Guide that is updated at least annually• Benchmarking Report – A Benefit Advisors Network branded compilation of Watson Wyatt and other studies

• Resource Library consisting of: • “Best of Breed” documents, resources and tools vetted through Benefit Advisors Network member committees • Regulatory compliance information and developments for HIPAA, ERISA and COBRA • Timely employer and employee communication materials • Health and wellness communication materials • Disease management communication

Partners Make A Difference!

Let us help you navigate the COBRA Compliance maze We provide the road map to COBRA compliance C

OB

RA

Ad

van

ced

Ben

efit

sSimplify COBRA Our years of experience enables you to rest easy

COBRA is burdensome and complex. It changes so often, most employers are just implementing the last

round of updates when a new round of requirements comes their way. The scary part is that if even

one piece of your compliance puzzle is missing, it can cost your organization literally tens-of-thousand

of dollars in fines and litigation. With more than 20 years of COBRA knowledge and service experience,

Advanced delivers solid liability protection.

BENEFITS• Reduced risk exposure

• Lower administrative costs

• Protection from costly litigation and federal regulatory fines

• Ability to prove compliance, if challenged

AT A GLANCE; Your COBRA Administration Process:

YOU:• Notify Advanced and insurer of insurance additions and deletions

US:• Send all required notices via First Class mail with proof of mailing for Election, Extension and Unavailability Notices• Receive COBRA Elections and Premium Payments• Notify Insurer or TPA of COBRA additions and deletions• Notify you when to add/delete COBRA participants• Provide simplified online submissions or Electronic Data Transfer (EDT specifications available)• Answer your COBRA questions• Satisfy the four required TAMRA criteria• Monitor COBRA regulations and legal opinions• Update procedures and notices as required• Track all required COBRA dates• Maintain proper documentation of notices• Become your advocate in a COBRA dispute• Provide reports for events submitted and notices sent• Provide toll-free customer and participant support• Provide HIPAA Certificates of Creditable Coverage

MyAdvancedBenefits.com800.664.3482 | 208.664.3482

MyAdvancedERC provides your company with

• Comprehensive descriptions of all your benefit plans.

• Forms needed to sign up for benefits, file claims, and more.

• Company Communication hub – post all news and information in one spot where everyone in your

company can read.

• Information to guide your employees through common life events, such as a birth of a new baby,

marriage, or buying a new home.

• And so much more!

Ad

van

ced

Ben

efit

s

MyAdvancedERC.com800.664.3482 | 208.664.3482

Learn Grow Advance

Your Benefits MyAdvancedERC is your one stop for benefit open enrollment forms, reimbursement forms, updating information and other common benefit needs. You can also get timely information from your company.

Life EventsGetting Married? Having a Baby? Buying a House? Let MyAdvancedERC help you with the forms and information you need to tackle all that life has to offer.

It’s Safe to Peek!Now you and your employees have one spotto look at for all your benefit docs and more ER

C

More Money, Added BenefitsAdvanced FSAs let employees increase their takehome pay while providing additional benefits FS

AA

dva

nce

d B

enef

itsMaximize Benefits Advanced FSA extends tax-advantaged dollars

An FSA with Advanced Benefits allows an employee to set aside a portion of their pre-tax earnings to

pay for qualified medical and/or dependent care expenses. Employees will see a significant tax savings

as the account is funded with pre-tax dollars from their paycheck.

By setting aside pre-tax money from their paycheck, employees will also end up with a lower taxable

amount and as a result, have more take home.

The types of FSA accounts that are available are:

• Medical Spending Account - reimburses for medical expenses not covered by insurance.

• Dependent Care Spending Account - reimburses for dependent care for children and/or a disabled

dependent so you and your spouse can work or be full-time students.

• Individually Owned Insurance - this account is to help employees whose spouse or children have

individual health insurance benefits from pre-tax reimbursement of health

premiums paid at home.

• Limited Purpose Spending Account - this account helps

employees who are enrolled in an HSA put additional

pre-tax dollars aside for vision and dental services

without disqualifying their HSA Plan.

Some of the benefits of an FSA with Advanced Benefits include:

• Increased employee satisfaction by

providing quick and accurate claims

reimbursement.

• Real people ready to answer

questions. You will not have to go

through multiple layers of

automated menus on the

phone to talk to us.

• An increased participation level

with easy to use debit cards and

online enrollment tools.

• 24-hour online access for

employees to monitor their

account.

• The entire funds are available to the

employee on either the first day of the

plan year, or the first time they make a

contribution into the plan.

MyAdvancedBenefits.com800.664.3482 | 208.664.3482

MyAdvancedBenefits.com800.664.3482 | 208.664.3482

FSA

Tax

Sav

ing

s C

alcu

lato

r

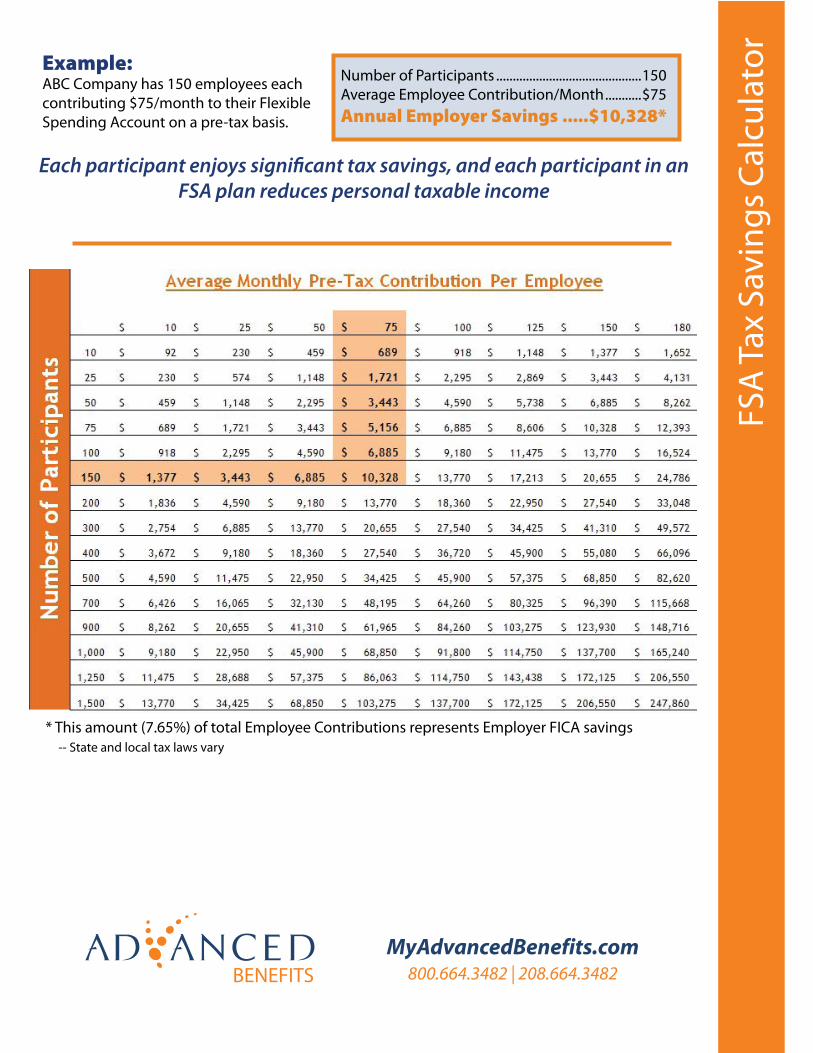

Number of Participants ............................................150Average Employee Contribution/Month ...........$75Annual Employer Savings .....$10,328*

Example:ABC Company has 150 employees each contributing $75/month to their Flexible Spending Account on a pre-tax basis.

FSA plan reduces personal taxable income

* This amount (7.65%) of total Employee Contributions represents Employer FICA savings -- State and local tax laws vary

Hea

lth

Car

e R

efo

rm S

um

mar

y

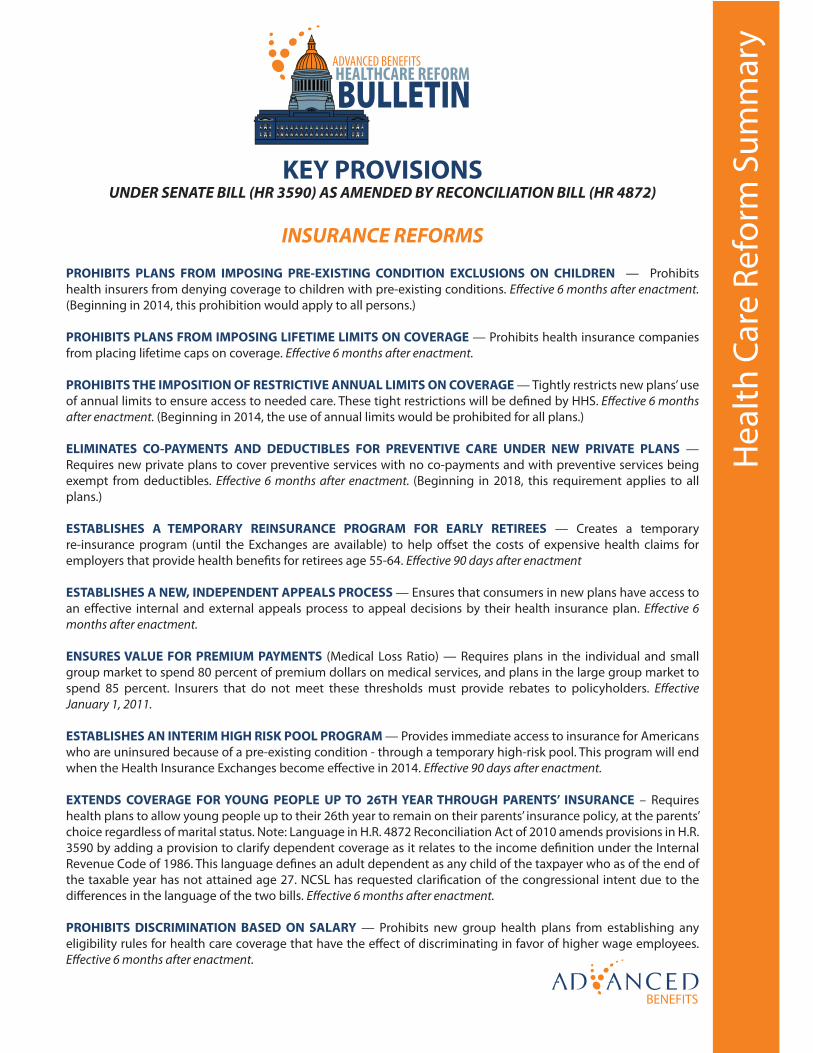

KEY PROVISIONS UNDER SENATE BILL (HR 3590) AS AMENDED BY RECONCILIATION BILL (HR 4872)

INSURANCE REFORMS

PROHIBITS PLANS FROM IMPOSING PRE‐EXISTING CONDITION EXCLUSIONS ON CHILDREN — Prohibits health insurers from denying coverage to children with pre‐existing conditions. E�ective 6 months after enactment. (Beginning in 2014, this prohibition would apply to all persons.)

PROHIBITS PLANS FROM IMPOSING LIFETIME LIMITS ON COVERAGE — Prohibits health insurance companies from placing lifetime caps on coverage. E�ective 6 months after enactment.

PROHIBITS THE IMPOSITION OF RESTRICTIVE ANNUAL LIMITS ON COVERAGE — Tightly restricts new plans’ use of annual limits to ensure access to needed care. These tight restrictions will be de�ned by HHS. E�ective 6 months after enactment. (Beginning in 2014, the use of annual limits would be prohibited for all plans.)

ELIMINATES CO-PAYMENTS AND DEDUCTIBLES FOR PREVENTIVE CARE UNDER NEW PRIVATE PLANS — Requires new private plans to cover preventive services with no co‐payments and with preventive services being exempt from deductibles. E�ective 6 months after enactment. (Beginning in 2018, this requirement applies to all plans.)

ESTABLISHES A TEMPORARY REINSURANCE PROGRAM FOR EARLY RETIREES — Creates a temporary re‐insurance program (until the Exchanges are available) to help o�set the costs of expensive health claims for employers that provide health bene�ts for retirees age 55‐64. E�ective 90 days after enactment

ESTABLISHES A NEW, INDEPENDENT APPEALS PROCESS — Ensures that consumers in new plans have access to an e�ective internal and external appeals process to appeal decisions by their health insurance plan. E�ective 6 months after enactment.

ENSURES VALUE FOR PREMIUM PAYMENTS (Medical Loss Ratio) — Requires plans in the individual and small group market to spend 80 percent of premium dollars on medical services, and plans in the large group market to spend 85 percent. Insurers that do not meet these thresholds must provide rebates to policyholders. E�ective January 1, 2011.

ESTABLISHES AN INTERIM HIGH RISK POOL PROGRAM — Provides immediate access to insurance for Americans who are uninsured because of a pre‐existing condition ‐ through a temporary high‐risk pool. This program will end when the Health Insurance Exchanges become e�ective in 2014. E�ective 90 days after enactment.

EXTENDS COVERAGE FOR YOUNG PEOPLE UP TO 26TH YEAR THROUGH PARENTS’ INSURANCE – Requires health plans to allow young people up to their 26th year to remain on their parents’ insurance policy, at the parents’ choice regardless of marital status. Note: Language in H.R. 4872 Reconciliation Act of 2010 amends provisions in H.R. 3590 by adding a provision to clarify dependent coverage as it relates to the income de�nition under the Internal Revenue Code of 1986. This language de�nes an adult dependent as any child of the taxpayer who as of the end of the taxable year has not attained age 27. NCSL has requested clari�cation of the congressional intent due to the di�erences in the language of the two bills. E�ective 6 months after enactment.

PROHIBITS DISCRIMINATION BASED ON SALARY — Prohibits new group health plans from establishing any eligibility rules for health care coverage that have the e�ect of discriminating in favor of higher wage employees. E�ective 6 months after enactment.

Hea

lth

Car

e R

efo

rm S

um

mar

y

KEY PROVISIONS UNDER SENATE BILL (HR 3590) AS AMENDED BY RECONCILIATION BILL (HR 4872)

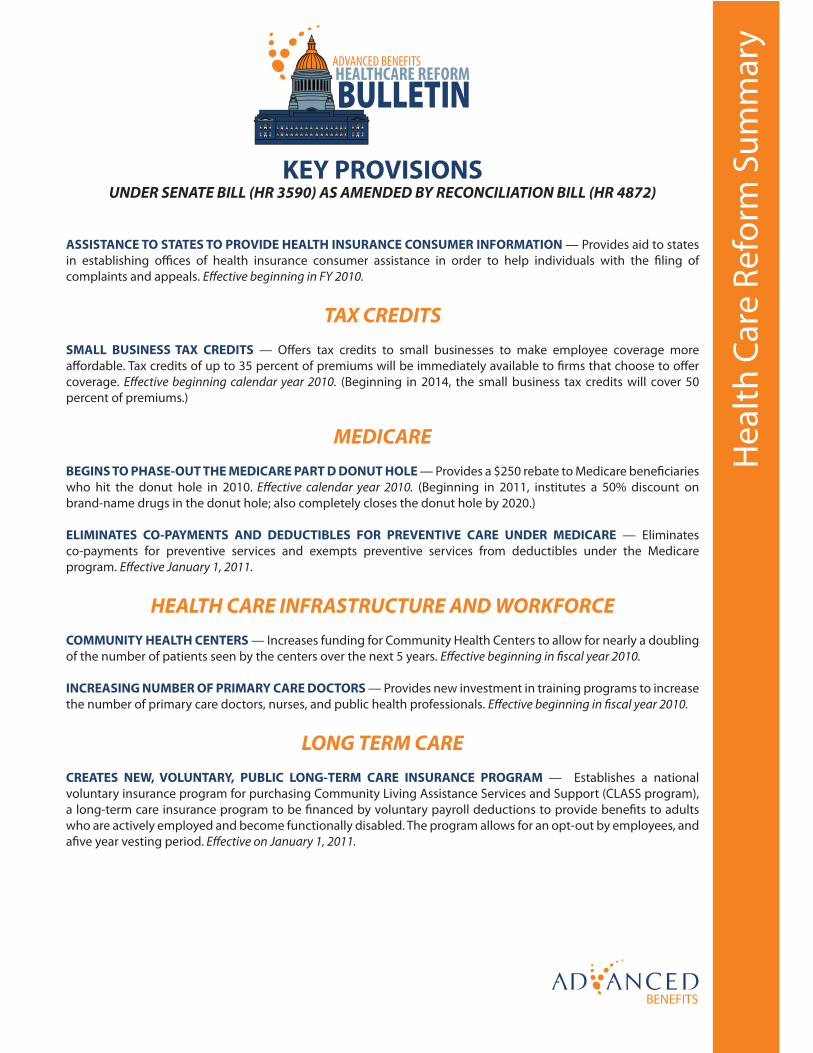

ASSISTANCE TO STATES TO PROVIDE HEALTH INSURANCE CONSUMER INFORMATION — Provides aid to states in establishing o�ces of health insurance consumer assistance in order to help individuals with the �ling of complaints and appeals. E�ective beginning in FY 2010.

TAX CREDITSSMALL BUSINESS TAX CREDITS — O�ers tax credits to small businesses to make employee coverage more a�ordable. Tax credits of up to 35 percent of premiums will be immediately available to �rms that choose to o�er coverage. E�ective beginning calendar year 2010. (Beginning in 2014, the small business tax credits will cover 50 percent of premiums.)

MEDICAREBEGINS TO PHASE-OUT THE MEDICARE PART D DONUT HOLE — Provides a $250 rebate to Medicare bene�ciaries who hit the donut hole in 2010. E�ective calendar year 2010. (Beginning in 2011, institutes a 50% discount on brand‐name drugs in the donut hole; also completely closes the donut hole by 2020.)

ELIMINATES CO-PAYMENTS AND DEDUCTIBLES FOR PREVENTIVE CARE UNDER MEDICARE — Eliminates co‐payments for preventive services and exempts preventive services from deductibles under the Medicare program. E�ective January 1, 2011.

HEALTH CARE INFRASTRUCTURE AND WORKFORCECOMMUNITY HEALTH CENTERS — Increases funding for Community Health Centers to allow for nearly a doubling of the number of patients seen by the centers over the next 5 years. E�ective beginning in �scal year 2010.

INCREASING NUMBER OF PRIMARY CARE DOCTORS — Provides new investment in training programs to increase the number of primary care doctors, nurses, and public health professionals. E�ective beginning in �scal year 2010.

LONG TERM CARECREATES NEW, VOLUNTARY, PUBLIC LONG‐TERM CARE INSURANCE PROGRAM — Establishes a national voluntary insurance program for purchasing Community Living Assistance Services and Support (CLASS program), a long‐term care insurance program to be �nanced by voluntary payroll deductions to provide bene�ts to adults who are actively employed and become functionally disabled. The program allows for an opt-out by employees, and a�ve year vesting period. E�ective on January 1, 2011.

Manage Costs and Promote Healthy Choiceswith an Advanced HRA

A Health Reimbursement Arrangement (HRA) administered by Advanced Benefits gives you a fresh

approach to your benefit package. Providing an HRA with a High Deductible Health Plan (HDHP) results

in a cost-efficient plan for employers and empowers the employee to take a more active role in their

health care benefits. An HRA encourages employees to begin making healthier choices when it comes

to their personal lifestyle.

An effective HRA design will enhance the benefit plan

and help employees make better health decisions.

Employers that encourage healthy choices

enjoy lower cost of insurance premiums

along with lower turnover and more

productive employees.

Advanced Benefits has a number

of HRA plan designs including:

• Standard HRA Enhance

your current benefit plan with

a Standard HRA designed to

reimburse 100% of eligible

expenses up to the total benefit

amount. Perfect for wellness plans,

vision expenses, and out of pocket

medical expenses.

• Deductible HRA Offer a competitive

benefits package while still increasing your

medical deductible. Add a Deductible HRA and

reimburse eligible expenses at 100% up to the total

benefit amount after a lower deductible is met.

• Coinsurance HRA Reduce out-of-pocket expenses for your employees with a Coinsurance HRA. Reimburse a

specified percentage, up to the total benefit amount, to assist employees with the cost of eligible expenses.

Let the experts at Advanced Benefits help you design the perfect HRA plan that meets your needs.

Ad

van

ced

Ben

efit

s

MyAdvancedBenefits.com800.664.3482 | 208.664.3482

Which is right for you?Together, we build the HRA that is right for you! H

RA

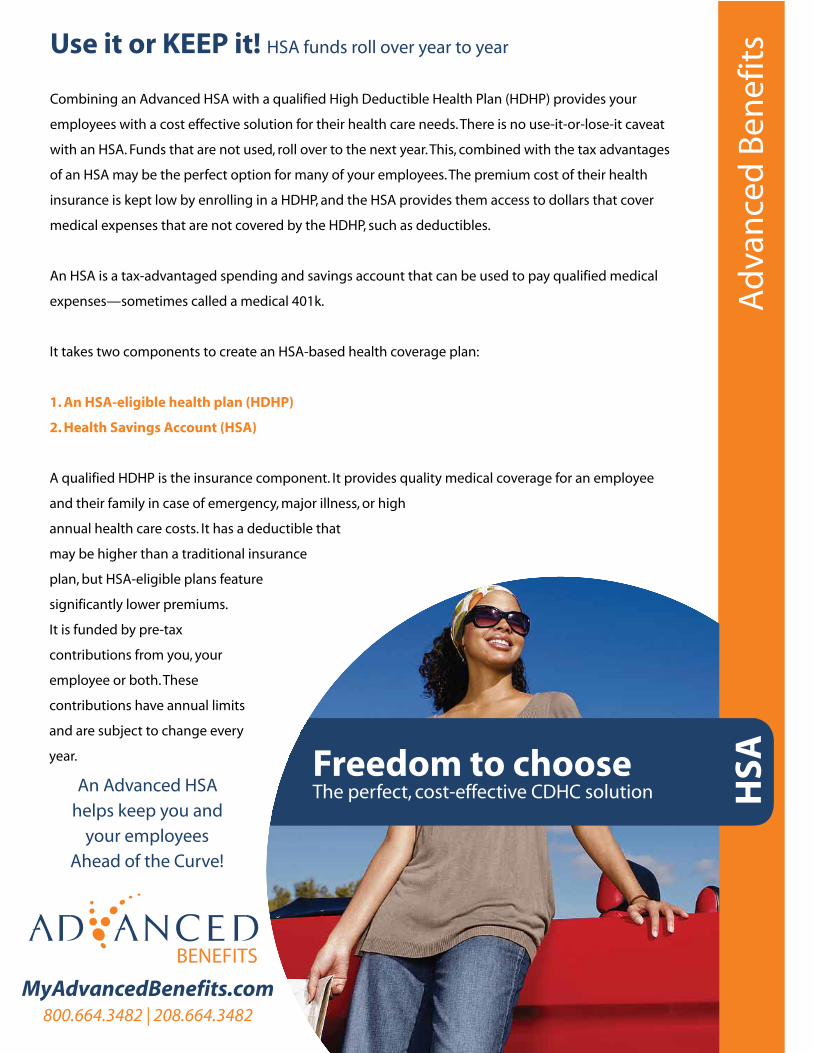

Freedom to chooseThe perfect, cost-effective CDHC solution

Ad

van

ced

Ben

efit

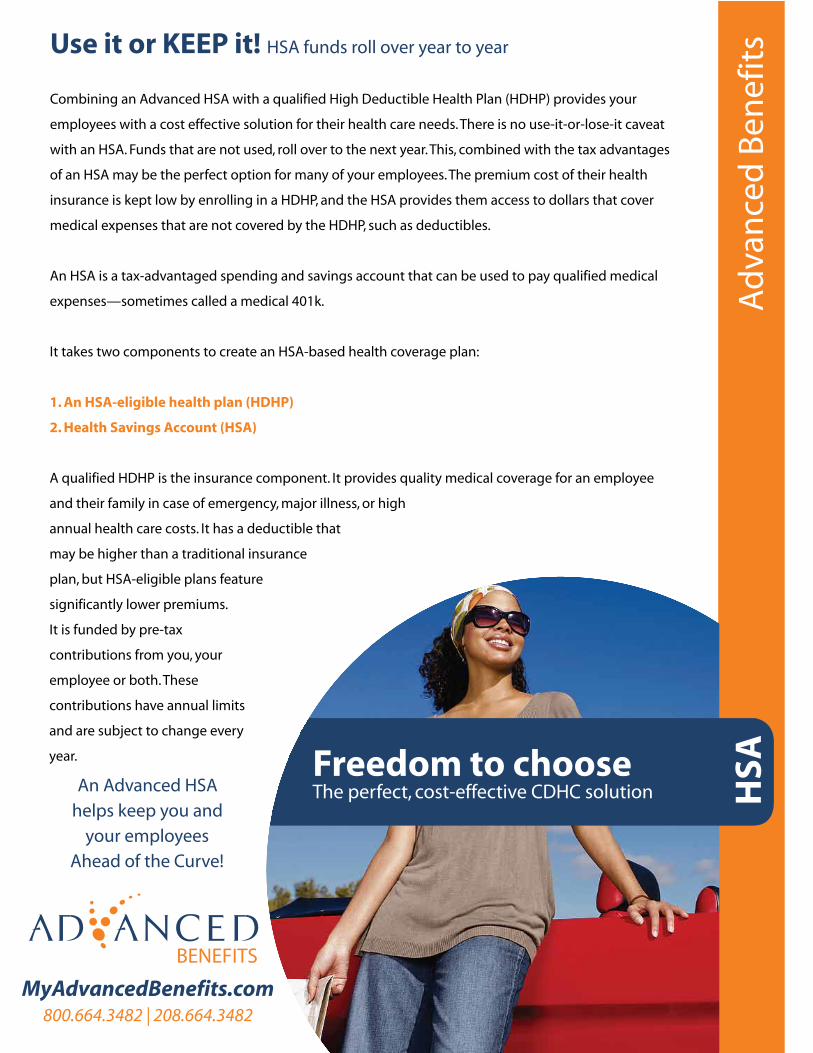

sUse it or KEEP it! HSA funds roll over year to year

Combining an Advanced HSA with a qualified High Deductible Health Plan (HDHP) provides your

employees with a cost effective solution for their health care needs. There is no use-it-or-lose-it caveat

with an HSA. Funds that are not used, roll over to the next year. This, combined with the tax advantages

of an HSA may be the perfect option for many of your employees. The premium cost of their health

insurance is kept low by enrolling in a HDHP, and the HSA provides them access to dollars that cover

medical expenses that are not covered by the HDHP, such as deductibles.

An HSA is a tax-advantaged spending and savings account that can be used to pay qualified medical

expenses—sometimes called a medical 401k.

It takes two components to create an HSA-based health coverage plan:

1. An HSA-eligible health plan (HDHP)

2. Health Savings Account (HSA)

A qualified HDHP is the insurance component. It provides quality medical coverage for an employee

and their family in case of emergency, major illness, or high

annual health care costs. It has a deductible that

may be higher than a traditional insurance

plan, but HSA-eligible plans feature

significantly lower premiums.

It is funded by pre-tax

contributions from you, your

employee or both. These

contributions have annual limits

and are subject to change every

year.

An Advanced HSA

helps keep you and

your employees

Ahead of the Curve!

HSA

MyAdvancedBenefits.com800.664.3482 | 208.664.3482

MyAdvancedBenefits.com800.664.3482 | 208.664.3482

Top 10 HSA Advantages

Fast

Fac

ts a

bo

ut

Ad

van

ced

HSA

s

Tax Savings - You can deduct your HSA deductions from your gross income on your

federal tax return, even if you do not itemize deductions. Many states also allow the deduction from

state income taxes.Earned Interest - Funds in your HSA grow with tax-deferred

interest.Portability - You own your account, so even if you change jobs, your

HSA funds go with you.Affordable Health Coverage - Use your Health Savings Account to

cover 100% of the cost of routine medical expenses like office visits, lab tests, and over-the-counter drugs.

Reduced Insurance Premiums - Your insurance premiums can be substantially lower when you change from a low-deductible plan to a high-deductible plan.Long-Term Savings - Because your funds can roll over from year to year, you can let the funds in your account grow tax-deferred. That's why HSAs have been referred to as the "Medical IRA."Retirement Bonus - After age 65, you may make withdrawals from your HSA for any reason without the 10% penalty imposed before age 65 for non-medical withdrawals. (Note: you'll still have to pay taxes on the money.)

Safety Net - There is no "use it or lose it" provision, so you can build up the savings in your HSA to use for major health events.

Coverage for the "Extras" - You can also use your HSA funds for programs not usually covered by other health plans, including dental,

optical, and much more.Empowerment - Take control of your routine healthcare decisions

you get to choose the healthcare and providers that you want.

Health Savings Accounts (HSA) are individually owned, tax-preferred savings accounts that can be funded to help offset eligible medical expenses or accumulated over time to supplement retirement savings. To have contributions made to an HSA, the account owner must have a qualifying High Deductible Health Plan in place. Not all high deductible plans meet this criteria.

Here a few key features of an HSA -

• HSAs must have a minimum deductible – In 2010 they these are set as $1,200 for individuals or $2,400 for families, indexed annually.• HSAs are employee-owned accounts – the full account balance moves with you if you leave employment.• HSA contributions can come from several sources – employer, employee-pretax payroll deduction, lump-sum, or any combination.• All HSA contributions are pre-tax and earnings accumulate tax-free or tax-deferred depending on how the money is spent.• HSA accumulations can be used tax-free for any IRS qualified medical expense, such as health plan deductibles and other out-of-pocket costs, dental, orthodontia, lasik surgery, over-the-counter medications, and more. • HSAs can accumulate year-over-year – there is never a threat of losing unspent balances.• For account owners 55 and older, additional “catch-up” contributions can be made.• HSAs have limits on contributions in any given calendar year – for 2010 they are $3,050 for individuals and $6,150 for families.• HSAs allow non-medical expense distributions, but account owner will be taxed and penalized (10%) on the funds withdrawn.• Early withdrawal penalty goes away for account owners 65 and older.

Why Choose an HSA?

HSA's provide a means for individuals and families

to take control of their health care plans.

Premium savings and other contributions

allow you to “self-insure” the small

expenses while maintaining high quality

catastrophic coverage for large claims –

if they occur!

• 100% of employee contributions are

free from federal, state (if applicable),

and other payroll taxes.

• Employer contributions, if any, are

free from taxation.

• Your HSA account can be invested

similar to a 401k and all earnings

grow tax-free or tax-deferred

depending on how the money is

eventually spent.

• You pay no taxes or penalties when

you use the money for qualified

expenses at anytime.

Freedom to chooseThe perfect, cost-effective CDHC solution

Ad

van

ced

Ben

efit

sUse it or KEEP it! HSA funds roll over year to year

Combining an Advanced HSA with a qualified High Deductible Health Plan (HDHP) provides your

employees with a cost effective solution for their health care needs. There is no use-it-or-lose-it caveat

with an HSA. Funds that are not used, roll over to the next year. This, combined with the tax advantages

of an HSA may be the perfect option for many of your employees. The premium cost of their health

insurance is kept low by enrolling in a HDHP, and the HSA provides them access to dollars that cover

medical expenses that are not covered by the HDHP, such as deductibles.

An HSA is a tax-advantaged spending and savings account that can be used to pay qualified medical

expenses—sometimes called a medical 401k.

It takes two components to create an HSA-based health coverage plan:

1. An HSA-eligible health plan (HDHP)

2. Health Savings Account (HSA)

A qualified HDHP is the insurance component. It provides quality medical coverage for an employee

and their family in case of emergency, major illness, or high

annual health care costs. It has a deductible that

may be higher than a traditional insurance

plan, but HSA-eligible plans feature

significantly lower premiums.

It is funded by pre-tax

contributions from you, your

employee or both. These

contributions have annual limits

and are subject to change every

year.

An Advanced HSA

helps keep you and

your employees

Ahead of the Curve!

HSA

MyAdvancedBenefits.com800.664.3482 | 208.664.3482

7:30 Sign in – Coffee/Tea/Juice

8:30 Opening Remarks • Dan Crawford - Managing Partner, Advanced Benefits

8:45 Engaging the Troops in the War on the High Cost of Benefits • Mark Fisher - Managing Partner, Advanced Benefits

9:30 Ready to Deploy: The Future of Local Healthcare • Rick McMaster, Executive Director, NIHN

10:15 Break

10:30 Healthcare Reform and your Company • Peter Marathas, Compliance Director, B.A.N.

11:15 Lunch

11:45 Protecting the Core of Your Business • Wade Larson, Director of Human Resources, NIC

12:30 Closing Remarks and Prize Giveaway

12:45 Adjourn

Please Do Not Forget To Turn In Your Surveys In The Box At The

Registration Table

The 2010 Business and Benefits Bootcamp is the

perfect training for all area businesses looking

for answers and guidance on...

*Topics and Speakers Subject To Change

Find out... How Healthcare Reform will affect your company today and in the future... How to thrive by

changing your corporate culture... and more!

Find out... How Healthcare Reform will affect your company today and in the future... How to thrive by

changing your corporate culture... and more!

Jaime Arnold

[email protected]. 208.277.1039

Fax. 208.664.3842

1299 West Riverstone DriveCoeur d’Alene, ID 83814

208.664.3482 | 800.664.3482

WHATHEALTH CARE REFORMMEANS

FOR YOURBUSINESS

Health care reform is now the law of the land. Andnearly every individual and business in the U.S. willbe affected by the new law’s provisions.

The Patient Protection and Affordable Care Act (the“Act,” as amended) overhauls the health care environ-ment in the U.S. The goal: to provide a minimum levelof health care coverage for eligible individuals. Forexample, the new law requires most U.S. citizens andlegal residents to have health insurance. Incomeeligible individuals and families will receive premiumtax credits to help pay for coverage. Those choosingnot to carry coverage will pay penalties.

The Act places new responsibilities on employers that,over time, may well change the nature of employer-provided health care. Employers choosing not to offertheir employees qualifying coverage will pay anadditional tax to help finance their employees’ healthcare. An exception applies for smaller businesses.

The new law’s provisions will generally go into effecton dates ranging from within a short time after the dateof enactment through 2018. For more details, see theCalendar of Effective Dates later in this publication.

The following pages summarize the key provisions ofthe Act that may affect your business. You will gaininsight as to how the new law applies in definedsituations and learn ways to plan for the new law’simpact. But keep in mind that the Act contains manycomplex rules and exceptions. Professional guidance isrecommended before applying anything you read hereto your individual or business situation.

Access to Coverage — The BasicsIt is important for business owners and executives tounderstand how the Act expands individuals’ access tohealth care insurance coverage, since those rules tie intothe provisions affecting employers’ responsibilities.Among other provisions, the new law:

2

• Generally requires most individuals to have at leasta minimum level of health care coverage (“minimumessential coverage”).

• Creates state-based American Health BenefitExchanges through which individuals without healthinsurance can buy coverage.

• Provides refundable premium tax credits and cost-sharing reductions to make health care more affordablefor individuals/families with income up to 400% of thefederal poverty level (for example, at 2010 levels, afamily of four with income up to $88,200).

• Imposes penalties on individuals who fail to carryminimum essential coverage. Exceptions apply(e.g., for those whose income is below thethreshold for filing a federal income-tax return).

• Allows personal or employer-provided healthbenefit coverage existing at the time of enactmentto stay in place under a “grandfather” provision.The Act considers the grandfathered coverage tomeet the law’s individual coverage mandate, ifrequirements are met.

Employer Shared Responsibility for HealthCare CoverageWhile the Act does not require employers to provideminimum essential health care coverage to employees,it strongly encourages them to do so. How? By offering“incentives” in the form of both carrots and sticks.

Small Business Exchange: The Act creates state-based exchanges (known as Small Business HealthOptions Program, or “SHOP,” Exchanges) throughwhich small businesses can pool together to spreadtheir financial risk and buy health care insurancecoverage for employees (and possibly save money bydoing so). SHOP Exchanges will generally beavailable to employers with up to 100 full-timeemployees until 2017, at which time states may allowlarger businesses to participate.

3

Your Planning: If you are a smaller employer, stayinformed about how your state is handling a SHOPExchange and, once the program is available,investigate whether the coverages offered can meetyour and your employees’needs at a reasonable cost.

Small Employer Health Insurance Tax Credit: TheAct offers small employers that purchase health insurancecoverage for employees a sliding-scale income-tax creditto help them pay for the plan. For purposes of the credit,a “small employer” is defined as one with no more than25 full-time (or full-time equivalent) employees andaverage annual wages of no more than $50,000 peremployee. The credit has two phases.

• For tax years 2010 through 2013, the law allows atax credit of up to 35% of the employer’s contri-bution toward employees’ coverage. In general, theemployer must contribute at least 50% of the totalpremium cost. Employers with 10 or feweremployees with average annual wages of less than$25,000 will be entitled to the full credit. The creditphases out for employers with more employeesand/or higher average wages.

• Starting in tax year 2014, eligible small businessesthat purchase coverage through a state-based SHOPExchange may qualify for a credit of up to 50% oftheir contribution toward the coverage. The employermust contribute at least 50% of the total premium cost.The credit will be available to a qualifying employerfor up to two tax years after 2013. Again, the fullcredit is available to employers with no more than 10employees who earn an average annual wage of lessthan $25,000 (adjusted for inflation), with a phaseoutas employee counts and/or average wages increase.

Example: Starting in 2010, Small Business, whichmeets the Act’s requirements, receives a 35% taxcredit to help pay for its health insurance plan. In2014, Small Business purchases coverage through aSHOP Exchange. The 50% credit will be available toSmall Business for two years, 2014 and 2015, only.

4

A small employer tax credit is available to qualifyingsmall tax-exempt employers, but at a reduced creditpercentage. The credit is taken against payroll taxes.

Observation: Be aware that certain employees (forexample, 2% S corporation shareholders andmore-than-5% owners of the employer) are notincluded in the definition of “full-time employee”for purposes of the small employer tax credit.Neither are seasonal workers who work 120 daysor less during the year. This can impact the amountof any credit your company may be entitled to.

Employer Penalty: The new law will exact a penalty oncertain larger employers that fail to provide adequateminimum essential health care coverage. An “applicablelarge employer” is defined as one having an average of atleast 50 full-time (or full-time equivalent) employees onbusiness days during the previous calendar year. (Definedseasonal workers don’t count.)

In general, the penalty applies where the employer offers:

• no minimum essential coverage,

• minimum essential coverage that is “unaffordable”(it costs the employee more than 9.5% of householdincome), or

• minimum essential coverage for which the plan’sshare of the total allowed cost of benefits provided toemployees (“actuarial value”) is less than 60%.

Large employers that (1) do not offer minimum essentialcoverage and (2) have at least one employee whoreceives a premium tax credit or cost-sharing reductionto help pay for individual coverage will incur anadditional “assessable payment” (read: tax). Theassessment is equal to $2,000 per full-time employee peryear (computed on a monthly basis). The Act excludesthe first 30 employees from the payment calculation.

Example: Sample Corporation has 65 full-timeemployees. It does not offer minimum essential healthcare coverage throughout the year. The amountpayable by Sample Corporation will be 35 (65 minus

5

30) employees multiplied by 1/12 of $2,000, or$5,833.33 a month, or $70,000 a year.

A penalty also applies to large employers that offerminimum essential coverage where that coverage iseither “unaffordable” or has an “actuarial value” of lessthan 60%. If at least one full-time employee receives apremium tax credit or cost-sharing reduction, theemployer will pay $3,000 for each employee receiving apremium credit or cost-sharing reduction or $2,000multiplied by the total number of full-time employees, ifthat amount is less.

Note that employers with fewer than 50 employees areexempt from the additional assessments imposed by theAct. Note too, that large employer grandfathered planscould be subject to a possible assessment if the coveragefalls within the penalty provisions.

Observation: The Act’s provisions may discouragebusinesses with fewer than 50 full-time employeesfrom expanding their payrolls to 50 or more. Toavoid dealing with new benefits, administrativecosts, and penalties, some employers may decide touse more independent contractors and contingentworkers rather than full-time employees.

Your Planning: For employers subject to potentialpenalty assessments, it will be important to considerthe options as to offering — or not offering — aqualifying health insurance plan. For someemployers, not offering insurance and paying theassessment may be a cheaper alternative to payingpremiums for employer-provided coverage. Makesure to consult a qualified professional to help youreview your choices and determine which makesthe most sense for your business.

Free Choice Vouchers: Employers that offer coverage totheir employees will be required to provide “Free ChoiceVouchers” to certain employees whose income is notmore than 400% of the federal poverty level. To qualifyfor a voucher, the employee’s required contribution tothe employer-provided coverage would have to exceed 8%

6

of household income (but not exceed 9.8% of income)and the employee must elect to enroll in a plan throughthe American Health Benefit Exchange.

The voucher amount will generally be the amount theemployer would have paid to cover the employee underthe employer’s plan. If the value of the voucher exceedsthe cost of the Exchange plan chosen by the employee,the employee keeps the excess. The employer won’t besubject to the additional assessment described earlierfor employees who receive vouchers.

Observation: In addition to the penalty assessmentsor Free Choice Voucher costs, some employerscould see premium costs rise. Lower-income healthyemployees could leave the higher-cost employerplan to secure coverage through an Exchange,leaving fewer healthy older employees in the plan.Plus, if the amount of the voucher the employerprovides is more than the cost of the Exchange-provided coverage, these opting-out employees mayreceive a windfall.

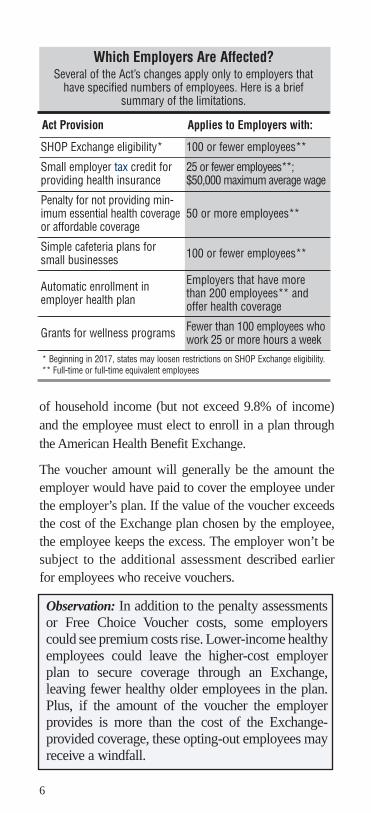

Which Employers Are Affected?Several of the Act’s changes apply only to employers that

have specified numbers of employees. Here is a briefsummary of the limitations.

Act Provision Applies to Employers with:

SHOP Exchange eligibility* 100 or fewer employees**

Small employer tax credit for providing health insurance

25 or fewer employees**; $50,000 maximum average wage

Penalty for not providing min-imum essential health coverageor affordable coverage

50 or more employees**

Simple cafeteria plans forsmall businesses 100 or fewer employees**

Automatic enrollment in employer health plan

Employers that have morethan 200 employees** andoffer health coverage

Grants for wellness programs Fewer than 100 employees whowork 25 or more hours a week

* Beginning in 2017, states may loosen restrictions on SHOP Exchange eligibility.** Full-time or full-time equivalent employees

7

Other Employer Coverage Information: The Actcontains several other important provisions affectingemployer-provided coverage. Among them:

•An employer with more than 200 full-timeemployees (or equivalents) will be required to auto-matically enroll employees in a health insurance planit offers. The employees may opt out of coveragealtogether or elect another plan offered by the employer.

• Most employers providing minimum essentialcoverage will be required to file information aboutthe coverage with the IRS. The filings will identifyindividual employees, number of months covered, thecoverage type, and the premium amount paid by eachemployee. Employers will also have to fileinformation about employee coverage with the U.S.Department of Health and Human Services. Failure-to-file penalties apply.

• Employers that provide health insurance coverage willhave to disclose the benefit’s cost on each employee’sannual Form W-2, Wage and Tax Statement. Thisprovision does not alter the tax-free treatment ofemployer-provided health coverage.

• Employers generally will have to provide employees,upon hire (or, for existing employees, by March 1,2013), a notice that describes the availability of andthe services provided by the American Health BenefitExchange and the eligibility requirements for buyinginsurance through the Exchange, as well as theconsequences if an eligible employee chooses to doso. Other employee notices may be required.

• Eligible small businesses will be able to establish“simple cafeteria plans” that allow them to offer tax-free health and other benefits to their employees. Anemployer is eligible to sponsor a simple cafeteria planif, during either of the preceding two years, thebusiness employed 100 or fewer employees on average(based on business days). Minimum contribution andeligibility/participation requirements apply.

8

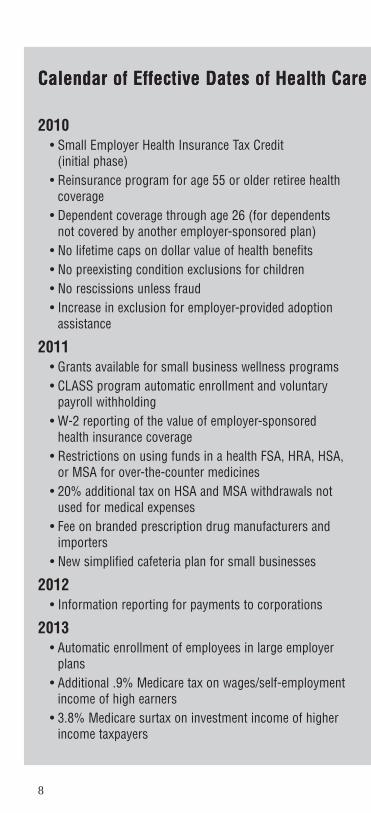

Calendar of Effective Dates of Health Care

2010• Small Employer Health Insurance Tax Credit

(initial phase)• Reinsurance program for age 55 or older retiree health

coverage• Dependent coverage through age 26 (for dependents

not covered by another employer-sponsored plan)• No lifetime caps on dollar value of health benefits• No preexisting condition exclusions for children• No rescissions unless fraud• Increase in exclusion for employer-provided adoption

assistance

2011• Grants available for small business wellness programs• CLASS program automatic enrollment and voluntary

payroll withholding • W-2 reporting of the value of employer-sponsored

health insurance coverage• Restrictions on using funds in a health FSA, HRA, HSA,

or MSA for over-the-counter medicines• 20% additional tax on HSA and MSA withdrawals not

used for medical expenses• Fee on branded prescription drug manufacturers and

importers• New simplified cafeteria plan for small businesses

2012• Information reporting for payments to corporations

2013• Automatic enrollment of employees in large employer

plans• Additional .9% Medicare tax on wages/self-employment

income of high earners• 3.8% Medicare surtax on investment income of higher

income taxpayers

Calendar of Effective Dates of Health Care

9

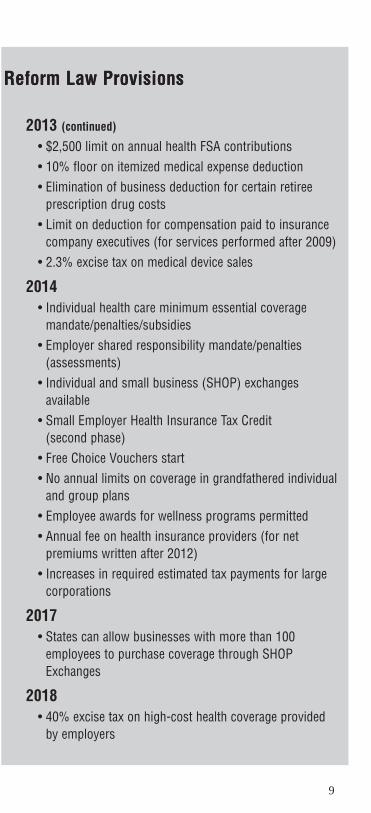

Reform Law ProvisionsReform Law Provisions

2013 (continued)

• $2,500 limit on annual health FSA contributions• 10% floor on itemized medical expense deduction• Elimination of business deduction for certain retiree

prescription drug costs• Limit on deduction for compensation paid to insurance

company executives (for services performed after 2009)• 2.3% excise tax on medical device sales

2014• Individual health care minimum essential coverage

mandate/penalties/subsidies• Employer shared responsibility mandate/penalties

(assessments)• Individual and small business (SHOP) exchanges

available• Small Employer Health Insurance Tax Credit

(second phase)• Free Choice Vouchers start• No annual limits on coverage in grandfathered individual

and group plans• Employee awards for wellness programs permitted• Annual fee on health insurance providers (for net

premiums written after 2012)• Increases in required estimated tax payments for large

corporations

2017• States can allow businesses with more than 100

employees to purchase coverage through SHOPExchanges

2018• 40% excise tax on high-cost health coverage provided

by employers

10

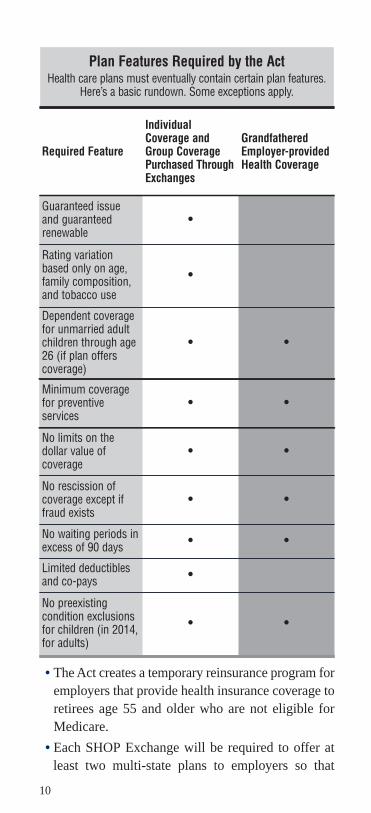

• The Act creates a temporary reinsurance program foremployers that provide health insurance coverage toretirees age 55 and older who are not eligible forMedicare.

• Each SHOP Exchange will be required to offer atleast two multi-state plans to employers so that

Plan Features Required by the ActHealth care plans must eventually contain certain plan features.

Here’s a basic rundown. Some exceptions apply.

Required Feature

IndividualCoverage andGroup CoveragePurchased ThroughExchanges

GrandfatheredEmployer-providedHealth Coverage

Guaranteed issueand guaranteedrenewable

•

Rating variationbased only on age,family composition,and tobacco use

•

Dependent coveragefor unmarried adultchildren through age26 (if plan offerscoverage)

• •

Minimum coveragefor preventiveservices

• •

No limits on thedollar value ofcoverage

• •

No rescission ofcoverage except iffraud exists

• •

No waiting periods inexcess of 90 days • •

Limited deductiblesand co-pays •

No preexistingcondition exclusionsfor children (in 2014,for adults)

• •

11

employers having employees in different states canobtain such coverage.

• The new law provides grants for up to five years(starting in 2011) to small employers that establishwellness programs. It also allows employers to offeremployees awards (premium discounts, waivers ofdeductibles or co-pays) of up to 30% of the cost ofcoverage for participation in a wellness program andmeeting certain health-related standards.

•The Act establishes a national, voluntary long-term careinsurance program for buying community livingassistance services and support (CLASS). The programwill provide individuals with specified functionallimitations a cash benefit of $50 a day or more topurchase services and support. The benefit vests over fiveyears. The CLASS program is not employer sponsoredor funded; however, it will require all employed adults tobe automatically enrolled in the program through work.If the employer elects, employees’ premium paymentsmay be made through payroll withholding. Employeescould opt out of the program.

Excise Tax on High-cost InsuranceThe Act imposes a 40% nondeductible excise tax onissuers (insurance companies and self-insured planadministrators) of high-end, public or private employer-sponsored health plans (so-called “Cadillac” plans). Thetax will generally apply to the extent annual premiums aremore than $10,200 for individual coverage and $27,500for family coverage. The threshold amounts are higher —$11,850 (individual) and $30,950 (family) — for planscovering employees engaged in certain high-risk profes-sions or retired individuals age 55 and older who are noteligible for Medicare. Standalone dental and vision plansare excluded in figuring the amount subject to tax.

New Restrictions on Health FSAs, HRAs,HSAs, and Archer MSAsThe Act imposes several new restrictions on health flexiblespending arrangements (FSAs), health reimbursementarrangements (HRAs), health savings accounts(HSAs), and Archer medical savings accounts (MSAs).

12

FSA Contributions: The Act places a $2,500 annuallimit on an employee’s salary reduction contributionsto a health FSA under a cafeteria plan. The limit willbe indexed for inflation.

Definition of Medical Expense: The new law generallyconforms the definition of medical expense for purposesof employer-provided health coverage to the definition forpurposes of the itemized deduction for medical expenses.As a result of this change, the cost of over-the-countermedicines will not be reimbursable with excludableincome through a health FSA, HRA, HSA, or MSAunless a physician prescribes the medicine.

Penalty Taxes: Withdrawals from HSAs before age65 that aren’t used for qualified medical expenses willbe subject to an additional tax of 20%, up from 10%under prior law. The new law also increases the addi-tional tax on MSA withdrawals not used for qualifiedmedical expenses from 15% to 20%.

Medicare Tax Increases for High EarnersThe Act imposes Medicare tax increases on higherincome taxpayers.

Additional Hospital Insurance Tax: Individual tax-payers who earn more than $200,000 a year, marriedtaxpayers filing jointly who earn more than $250,000,and married taxpayers filing separately who earn morethan $125,000 will face higher taxes on a portion of theirwages. These taxpayers will have to pay an additionalMedicare tax equal to .9% of their wages over therelevant threshold amount for their filing status. In effect,this change increases the Medicare tax rate on thoseearnings from 1.45% to 2.35%.

Observation: The rate increase applies only to theemployee portion of the Medicare tax. Theemployer portion of the Medicare payroll taxcontinues to be 1.45% of earnings (with no cap).Also, the threshold earnings amounts are notindexed to inflation.

13

Under a parallel provision, self-employed individualswill be liable for an additional tax of .9% on their self-employment income to the extent it exceeds theapplicable threshold amount. The additional self-employment tax is not deductible.

Note that employers only have to withhold the addi-tional .9% tax on an employee’s wages over $200,000.Employees will need to be made aware that, in certaincircumstances, their full liability for the additional taxmay not be covered through withholding.

Example: Linda works for Acme. She earns $100,000,and her husband Ted makes $210,000 at his job. Theircombined wages of $310,000 are $60,000 over the$250,000 threshold for joint filers. However, Acme isnot required to withhold any portion of the additionalMedicare tax from Linda’s salary, since it is under$200,000. And Ted’s employer withholds the additional.9% tax only on $10,000, the earnings in excess of$200,000. Since their employers don’t withhold enoughto cover all their additional Medicare tax liability,Linda and Ted should take the shortfall into account forestimated tax payment purposes.

Surtax on Investment Income: The new law alsoimposes a 3.8% surtax — called the “unearned incomeMedicare contribution” — on the investment income ofhigher income individuals, estates, and trusts. Forindividuals, the tax is equal to 3.8% of the lesser of (1)net investment income for the year or (2) the amount bywhich modified adjusted gross income (AGI) exceeds anannual threshold amount. The thresholds are the same asfor the additional Medicare tax on earnings (e.g.,$200,000 a year for individual taxpayers) and are notinflation-adjusted.

Example: David is single and has modified AGI of$230,000. Of that amount, $100,000 is net investmentincome. His liability for the unearned income Medicarecontribution tax is $1,140 — 3.8% of $30,000, theamount of his modified AGI in excess of $200,000.

14

Example: Abby, a single taxpayer, has modified AGIof $310,000 and net investment income of $100,000.Her unearned income Medicare contribution tax is3.8% of $100,000, the full amount of her netinvestment income, since that amount is less than$110,000 (the excess of modified AGI over$200,000, the threshold for her filing status).

Net investment income includes gross income frominterest, dividends, annuities, royalties, rents, netcapital gain, and income earned from passive trade orbusiness activities. However, the 3.8% surtax does notapply to qualified retirement plan and individualretirement account distributions.

Increased Floor on Medical DeductionUnder the new law, individuals generally will be ableto deduct their medical expenses as an itemizeddeduction only to the extent that their aggregateexpenses exceed 10% of adjusted gross income.However, a 7.5%-of-AGI floor will continue to applythrough 2016 if either the taxpayer or the taxpayer’sspouse is age 65 or over.

Retiree Prescription Drug Cost DeductionEmployers that receive federal subsidy payments forproviding prescription drug coverage to retireeseligible for Medicare Part D will no longer be able toclaim a business expense deduction for retireeprescription drug expenses to the extent of the subsidypayments received.

Observation: For companies that offer prescriptiondrug coverage to their retirees, taking away thededuction adds to the cost of providing the benefit.Large companies in particular could see asubstantial reduction in earnings stemming fromrecognizing the tax impact of the provision in theirfinancial statements.

Targeted Revenue RaisersThe new law includes several revenue raising provi-sions targeted at specific industries.

15

Insurance Company Executive Compensation:The Act places an annual cap on deductions that certaincompanies may claim for executive compensation andcertain other compensation paid. Where applicable, thededuction limit is $500,000 per individual.

Health Insurance Providers: Insurance companieswill be subject to an annual fee, allocated based onmarket share of net premiums written. The fee doesn’tapply to companies whose net premiums written are$25 million or less.

Pharmaceutical Manufacturers and Importers: TheAct also imposes an annual flat fee on businesses thatmanufacture or import branded prescription drugs forsale to, or in connection with, specified governmentprograms. The aggregate fee will be apportioned tocompanies according to market share.

Medical Device Manufacturers, Producers, andImporters: These companies will pay a 2.3% excisetax on the sale of taxable medical devices. Eyeglasses,contact lenses, hearing aids, and other IRS-specifiedmedical devices sold at retail establishments forpersonal use are exempted.

Other Business-related ProvisionsBusiness owners also may want to take note of theserevenue raising and miscellaneous tax provisionsincluded in the Act:

• Businesses that make payments aggregating $600or more in a year to a single corporation (other thana tax-exempt corporation) for the provision ofproperty or services will have to report thepayments on IRS information returns.

• Employers may continue to provide adoptionassistance as a tax-favored employee benefitthrough 2011. The new law increases the maximumavailable exclusion to $13,170 per eligible child(inflation-adjusted after 2010).

• Large corporations are subject to increases incertain required payments of estimated tax.

16

This publication is designed to provide accurate andauthoritative information in regard to the subject mattercovered. However, the general information herein is not intended to be nor should it be treated as tax, legal,or accounting advice. Additional issues could exist that would affect the tax treatment of a specific transaction and, therefore, taxpayers should seek advice from anindependent tax advisor based on their particularcircumstances before acting on any information presented.This information is not intended to be nor can it be usedby any taxpayer for the purposes of avoiding tax penalties.

HIRE Act Another new law, the Hiring Incentives to RestoreEmployment Act of 2010 (the HIRE Act), was enactedshortly before the health care reform law. Among otherprovisions, the HIRE Act:

• Relieves employers of the obligation to pay theemployer’s share of Social Security employment taxeson wages paid to employees hired after February 3,2010, and before January 1, 2011, if the law’srequirements are met. This “payroll tax holiday” isavailable for 2010 wages paid after March 18.

• Offers employers a tax credit for retaining the newlyhired workers for at least 52 consecutive weeks.(Other requirements apply.)

• Allows businesses to expense up to $250,000 of theirqualifying asset purchases in 2010 under Section179 of the tax code. The $250,000 expensing limitbegins to phase out when qualifying asset purchasesexceed $800,000.

SummaryHealth care reform will impact your business. To whatextent depends on a number of factors: your business’size, its current health care benefits, and the makeup ofits work force, to name just a few.

We hope this description of the Patient Protection andAffordable Care Act helps you gain a better understandingof the changes nearly every individual and business willface beginning in 2010 and over the next several years. It isimportant to consider how the law will affect your situation.We can help. Let our professionals be of service to you.

800.664.3482

Stay up-to-date on the Health Care Reform Law

by registering for ourHealth Care Reform

eBulletin atMyAdvancedBenefits.com

We are proud to support everyone

who is part of

MYADVANCEDBENEFITS.COM

800.664.3482

We are proud to support

everyone who is part of

We are proud to support

everyone who is part of

MyAdvancedBenefits.com

Leverage Having access to the right partners is vital to your company

When you choose Advanced Benefits as your employee benefits partner, you instantly gain access to

leverage the leading industry companies and experts from across the region. Advanced Benefits strives to

give your company innovative solutions from industry partners such as:

Ad

van

ced

Ben

efit

s

MyAdvancedBenefits.com

Partners Make A DifferenceLet us put our network of resources and relationships to work for your company today!

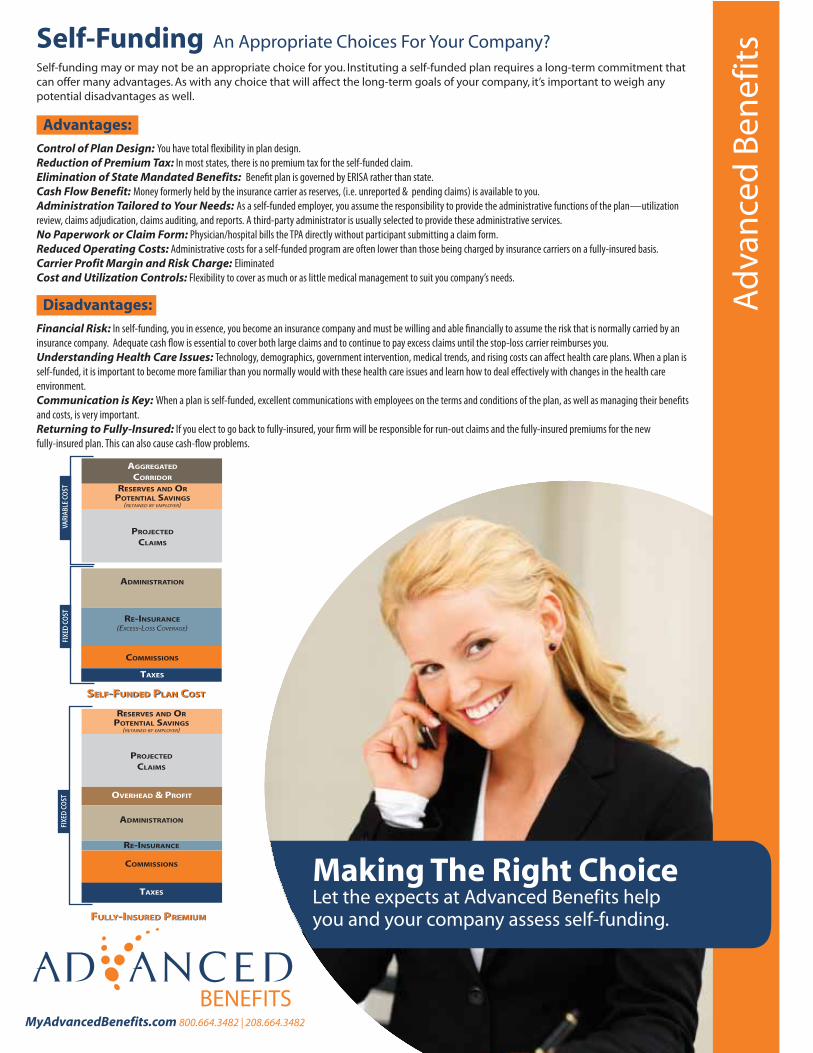

Making The Right ChoiceLet the expects at Advanced Benefits helpyou and your company assess self-funding.

Ad

van

ced

Ben

efit

s

TAXES

COMMISSIONS

RE-INSURANCE(EXCESS-LOSS COVERAGE)

ADMINISTRATION

PROJECTED

CLAIMS

RESERVES AND OR POTENTIAL SAVINGS

(RETAINED BY EMPLOYER)

AGGREGATED

CORRIDOR

TAXES

COMMISSIONS

RE-INSURANCE

ADMINISTRATION

PROJECTED

CLAIMS

RESERVES AND OR POTENTIAL SAVINGS

(RETAINED BY EMPLOYER)

OVERHEAD & PROFIT

Self-Funding An Appropriate Choices For Your Company?Self-funding may or may not be an appropriate choice for you. Instituting a self-funded plan requires a long-term commitment that can offer many advantages. As with any choice that will affect the long-term goals of your company, it’s important to weigh any potential disadvantages as well.

Advantages: Control of Plan Design: You have total �exibility in plan design.Reduction of Premium Tax: In most states, there is no premium tax for the self-funded claim.Elimination of State Mandated Benefits: Bene�t plan is governed by ERISA rather than state.Cash Flow Benefit: Money formerly held by the insurance carrier as reserves, (i.e. unreported & pending claims) is available to you.Administration Tailored to Your Needs: As a self-funded employer, you assume the responsibility to provide the administrative functions of the plan—utilization review, claims adjudication, claims auditing, and reports. A third-party administrator is usually selected to provide these administrative services.No Paperwork or Claim Form: Physician/hospital bills the TPA directly without participant submitting a claim form.Reduced Operating Costs: Administrative costs for a self-funded program are often lower than those being charged by insurance carriers on a fully-insured basis.Carrier Profit Margin and Risk Charge: Eliminated Cost and Utilization Controls: Flexibility to cover as much or as little medical management to suit you company’s needs.

Disadvantages: Financial Risk: In self-funding, you in essence, you become an insurance company and must be willing and able �nancially to assume the risk that is normally carried by an insurance company. Adequate cash �ow is essential to cover both large claims and to continue to pay excess claims until the stop-loss carrier reimburses you.Understanding Health Care Issues: Technology, demographics, government intervention, medical trends, and rising costs can a�ect health care plans. When a plan is self-funded, it is important to become more familiar than you normally would with these health care issues and learn how to deal e�ectively with changes in the health care environment.Communication is Key: When a plan is self-funded, excellent communications with employees on the terms and conditions of the plan, as well as managing their bene�ts and costs, is very important.Returning to Fully-Insured: If you elect to go back to fully-insured, your �rm will be responsible for run-out claims and the fully-insured premiums for the new fully-insured plan. This can also cause cash-�ow problems.