policy considerations in developing a dual...

TRANSCRIPT

ISLAMIC FINANCE INTELLECTUAL DISCOURSE 20TH OCTOBER 2016 NOVOTEL MELAKA

POLICY CONSIDERATIONS IN DEVELOPING A DUAL FINANCIAL SYSTEM IN MALAYSIA

Rustam Mohd Idris

Islamic Banking & Takaful

Department

2

Disclaimer

This document is solely for the use of the participants of the Islamic Finance

Intellectual Discourse (18 – 20 October 2016)

All information in this document shall not be circulated, copied or reproduced in

whole or in part, nor publicly referred to or discussed unless with the prior written

approval from Bank Negara Malaysia (BNM) or the information has been officially

released by BNM to the public.

The information was not prepared with the specific consideration of any particular

individual or entity.

Any views expressed in this document are those of the author and are not

necessarily those of BNM. While every care is taken in the preparation of the

information, no responsibility can be accepted by BNM for any errors and any

liability for any loss or damage arising from the use of, or reliance on, the

information contained in this document.

Where we are now…

How we reach to this level…

What’s next …

What are the policy considerations…

3

Islamic AuM:

RM132.4 billion Market share: 19.8%

Outstanding:

RM749 billion Global market share: 54.3%

Contribution:

RM6.8 billion Domestic market share: 12.9%

Asset:

RM685.4 billion Domestic market share: 26.8%

IF has entered its third decade of development…

All figures as at end 2015 .

Takaful

Islamic

banking

Sukuk

Islamic

fund

4

Source : BNM’s Financial Stability & Payment System

Report 2015

Source : BNM’s Financial Stability & Payment System

Report 2015

Sources : Zawya Islamic, Thompson Reuters

Source : Bi-Annual Bulletin of Malaysian Islamic

Capital Market

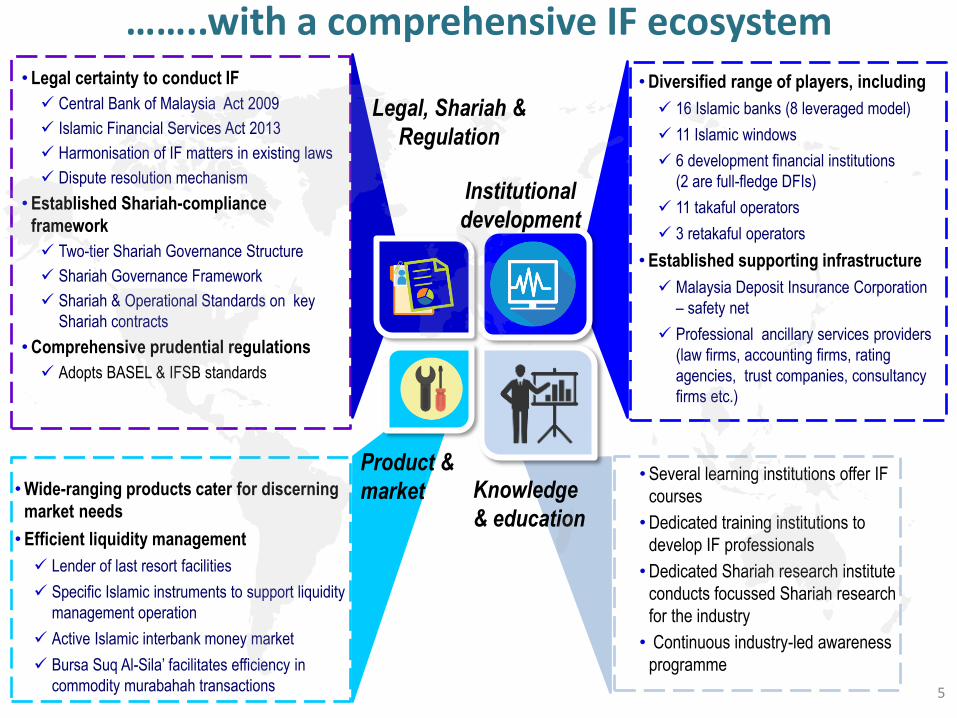

……..with a comprehensive IF ecosystem • Legal certainty to conduct IF

Central Bank of Malaysia Act 2009

Islamic Financial Services Act 2013

Harmonisation of IF matters in existing laws

Dispute resolution mechanism

• Established Shariah-compliance

framework

Two-tier Shariah Governance Structure

Shariah Governance Framework

Shariah & Operational Standards on key

Shariah contracts

• Comprehensive prudential regulations

Adopts BASEL & IFSB standards

• Diversified range of players, including

16 Islamic banks (8 leveraged model)

11 Islamic windows

6 development financial institutions

(2 are full-fledge DFIs)

11 takaful operators

3 retakaful operators

• Established supporting infrastructure

Malaysia Deposit Insurance Corporation

– safety net

Professional ancillary services providers

(law firms, accounting firms, rating

agencies, trust companies, consultancy

firms etc.)

• Wide-ranging products cater for discerning

market needs

• Efficient liquidity management

Lender of last resort facilities

Specific Islamic instruments to support liquidity

management operation

Active Islamic interbank money market

Bursa Suq Al-Sila’ facilitates efficiency in

commodity murabahah transactions

• Several learning institutions offer IF

courses

• Dedicated training institutions to

develop IF professionals

• Dedicated Shariah research institute

conducts focussed Shariah research

for the industry

• Continuous industry-led awareness

programme

Knowledge

& education

Product &

market

5

Institutional

development

Legal, Shariah &

Regulation

Sustained growth… Is

lam

ic b

anki

ng

, tak

afu

l &

Isla

mic

wea

lth

man

agem

ent

Sh

aria

h c

om

plia

nt

secu

riti

es

685.4 132.4 35.7

Sources : BNM’s Financial Stability & Payment System Report 2015,

Securities Commission Dec 2015

6

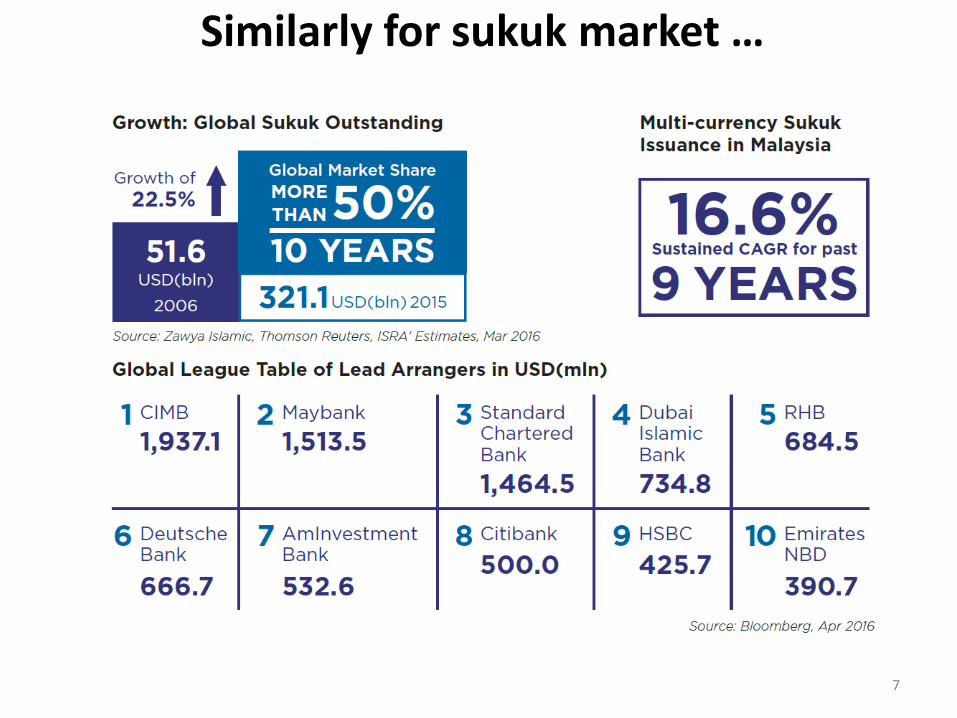

7

Similarly for sukuk market …

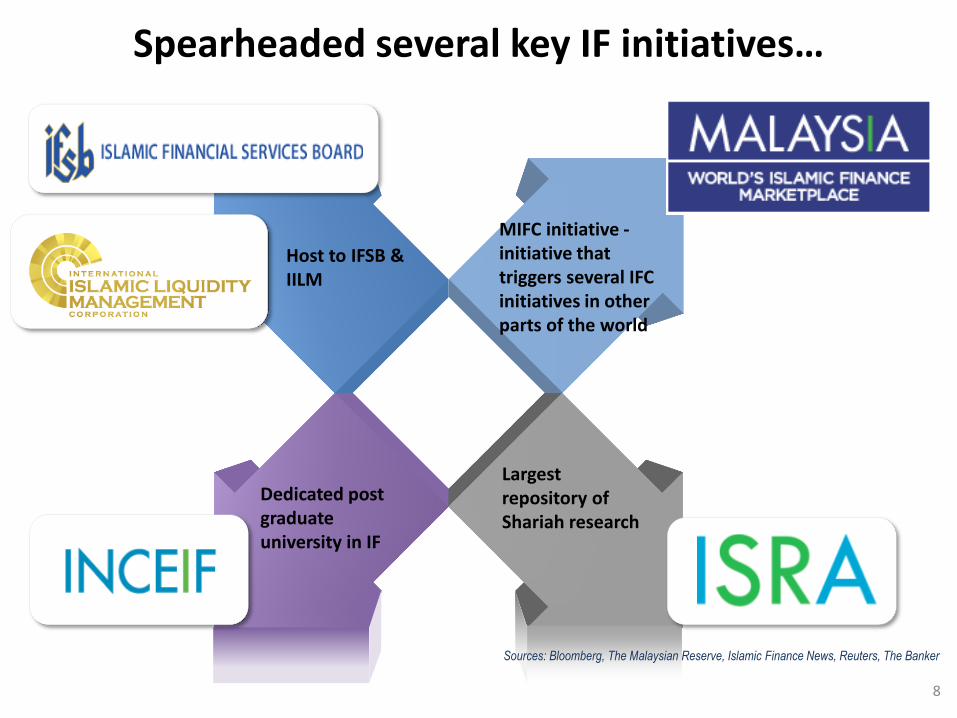

8

MIFC initiative - initiative that triggers several IFC initiatives in other parts of the world

Dedicated post graduate university in IF

Largest repository of Shariah research

Host to IFSB & IILM

Spearheaded several key IF initiatives…

Sources: Bloomberg, The Malaysian Reserve, Islamic Finance News, Reuters, The Banker

Where we are now…

What’s next …

What are the policy considerations…

How we reach to this level…

9

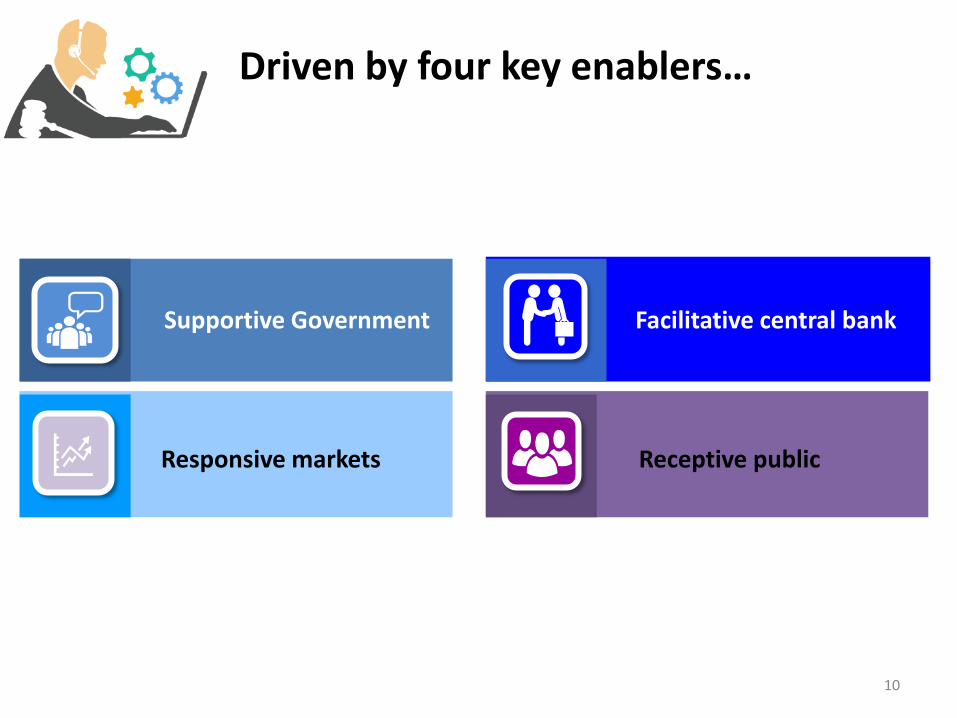

10

Supportive Government Facilitative central bank

Responsive markets Receptive public

Driven by four key enablers…

Government of Malaysia has been very supportive

National Agenda

Enabling legal environment

Provides enabling legal environment through:-

11

• GII, Islamic Treasury Bills, sovereign sukuks

• Dedicated legislation & IF provision in conventional legislation

• Non- discriminatory policy through tax neutrality framework

• Dedicated High Court & i-Arbitration for IF

Continuous sukuk issuance

12

Islamic Finance is one of BNM’s

key agenda

• Consistent facilitator of IF agenda since 80s Firm believer of financial inclusion & viability of IF’s

contribution to national growth

• Strong advocate of financial stability Regulator & supervisor of licensed IFIs Comprehensive regulatory / supervisory oversight for IFIs Comprehensive prudential policies to achieve stability &

compliance.

• Develop Islamic money markets & liquidity instruments

• Dedicated department (JPIT) to deliver IF mandates

13

• Strong buy in from markets due to its economics' viability & commercial considerations

• Consistent outreach programmes to create awareness

• Effective distribution of IF products & services

• Innovative in designing new products

Markets that are responsive

14

Malaysian population is a very important determinant that

ensures success of IF

• Strong acceptance from Malaysian population • Initial objective to cater for Muslim religious needs

evolved into commercial consideration. • Non-Muslim becomes important component of IF’s

growth.

14

Where we are now…

What’s next …

How we reach to this level…

What are the policy considerations…

15

16

Implications to financial

stability Phased in approach

Comprehensive and

structured framework

Shariah compliance as key

oversight

4 main principles in formulating policy considerations….

17

Dual role of BNM • The appropriateness for the Islamic bank to be placed under BNM • Issue of treatment between Islamic bank vs conventional bank

Possible disruption of the banking system • Possibility of a large migration of funds from conventional

banks into Islamic bank.

Effects on foreign investments • Possible concerns on Foreign Direct Investments

Pressure for more Islamic banks • Demand for more Islamic banks • Possible conversion of existing banks, especially

Government-owned bank

Containing the fear of non-Muslim • Racial harmony – non Muslims may view that the

establishment of an Islamic bank is an attempt to impose Islamic principles on the entire economic system.

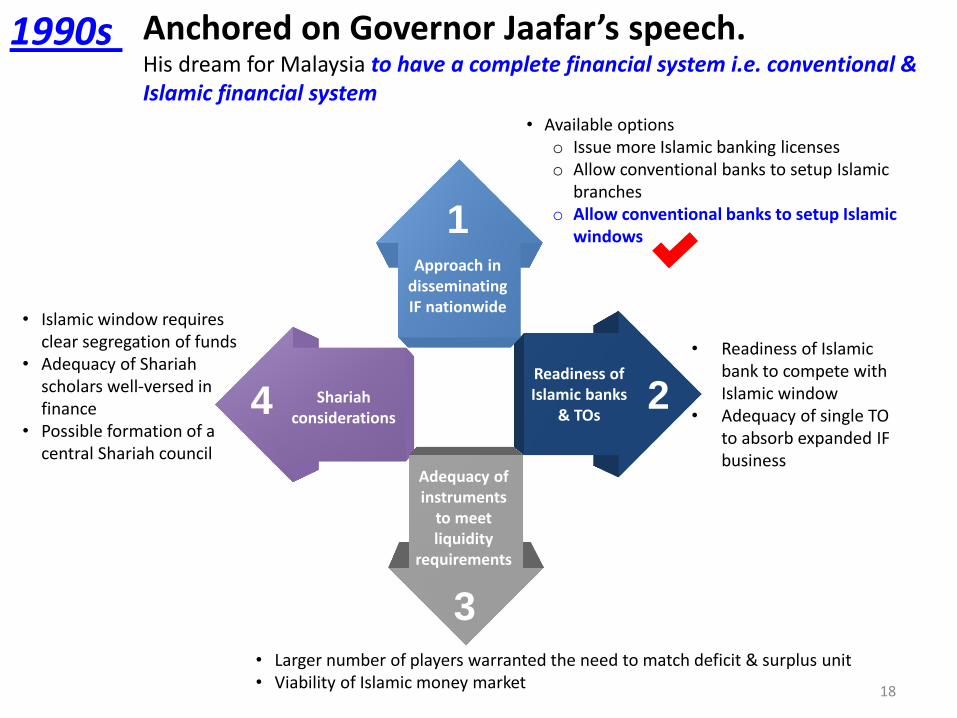

1980s What were the concerns then?

These concerns were addressed – establishment of 1st Islamic bank becomes a reality.

18

1

2 4

Approach in disseminating IF nationwide

• Available options o Issue more Islamic banking licenses o Allow conventional banks to setup Islamic

branches o Allow conventional banks to setup Islamic

windows

1990s Anchored on Governor Jaafar’s speech. His dream for Malaysia to have a complete financial system i.e. conventional & Islamic financial system

Adequacy of instruments

to meet liquidity

requirements

• Larger number of players warranted the need to match deficit & surplus unit • Viability of Islamic money market

Shariah considerations

• Islamic window requires clear segregation of funds

• Adequacy of Shariah scholars well-versed in finance

• Possible formation of a central Shariah council

Readiness of Islamic banks

& TOs

• Readiness of Islamic bank to compete with Islamic window

• Adequacy of single TO to absorb expanded IF business

1

2

3

19

1990s Some key initiatives & outcomes

Formation of SAC.

Nation wide dissemination from 40 branches to 1000 branches

Establishment of Islamic money market

Separate system for fund segregation

Market share increase from virtually nil to 5%

Increase in number of takaful operators

20

Institutional capacity enhancement

2000s : Policy considerations guided by FSMP Realising a comprehensive Islamic financial system

• Benchmarking • Enhance knowledge & expertise • Strong management team

Financial Infrastructure development

• number of Islamic banks & TOs to stimulate competition • Deepen Islamic financial market • 20% market share by 2010

Regulatory framework development

• Strengthen regulatory framework for Islamic banks & TOs

• Establish an effective legal structure

• Codified dual financial system in CBoM Act 2009

21

2000s : Some key initiatives & outcomes

Development of new market & financial infrastructure

• Sukuk dominates IF growth

• Bursa Suq As-Sila

Creating strong & highly capitalized Islamic banks & TOs • Liberalising policy for

foreign players • Transformation of

windows to subsidiaries

Positioning Malaysia as an Islamic financial center (formation of MIFC)

Strengthened legal & Shariah framework • New CBoM Act • SAC as apex • SGF

Capacity building • Transformation of

IBFIM • Establishment of

INCEIF & ISRA

Establishment of multilateral institutions in Malaysia

22

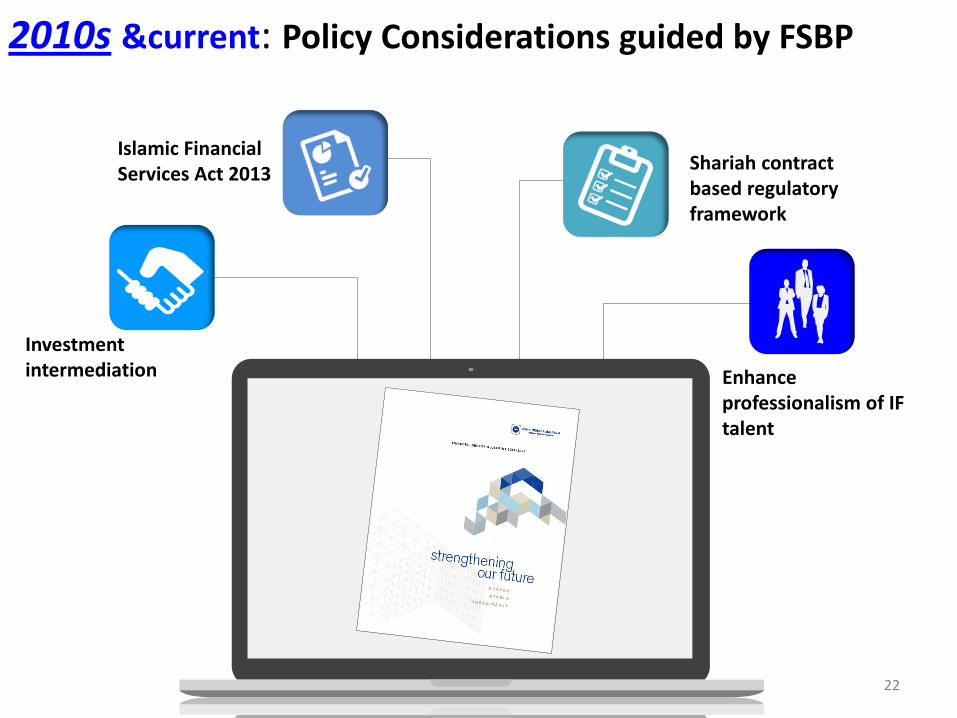

2010s ¤t: Policy Considerations guided by FSBP

Islamic Financial Services Act 2013

Investment intermediation Enhance

professionalism of IF talent

Shariah contract based regulatory framework

Islamic Financial

Services Act 2013

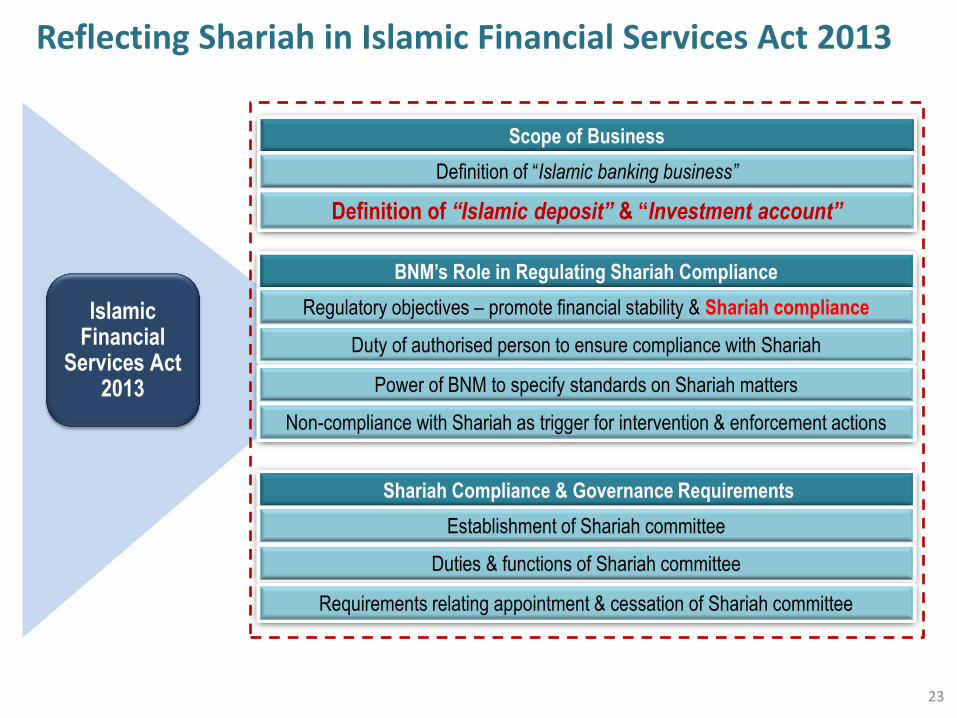

Scope of Business

Definition of “Islamic banking business”

Definition of “Islamic deposit” & “Investment account”

BNM’s Role in Regulating Shariah Compliance

Regulatory objectives – promote financial stability & Shariah compliance

Duty of authorised person to ensure compliance with Shariah

Power of BNM to specify standards on Shariah matters

Non-compliance with Shariah as trigger for intervention & enforcement actions

Shariah Compliance & Governance Requirements

Establishment of Shariah committee

Duties & functions of Shariah committee

Requirements relating appointment & cessation of Shariah committee

Reflecting Shariah in Islamic Financial Services Act 2013

23

Financial Stability

Shariah Compliance

Efficient Payment System

Monetary Stability

Developmental Role

Formation of strategic initiatives aimed to institute a

comprehensive financial infrastructure supported by key

ancillary institutions through holistic developmental plans

Regulatory Role

Formulation of comprehensive regulatory framework,

institutional & infrastructure building with effective &

efficient consumer protection

Supervisory Role

Development and implementation of a sustainable,

progressive and robust Shariah supervision framework to

ensure the safety and soundness of financial institutions

in accordance with Shariah

Clarity of BNM’s role under IFSA that include Shariah

24

Protection of depositors, investment account holders & policyholders

• Preventing mismanagement of public funds

Preserve sound Islamic financial system

Preserve sanctity of Shariah conducts

Objective: Ensure financial stability

Defined regulatory framework for IF anchored on two regulatory objectives

1

To preserve public confidence • Setting minimum standards that all industry players

must adhere to

2

To correct market imperfections • Protecting consumer interests e.g. issues on

information asymmetry, monopolistic or non-competitive behavior

3

Need to moderate the problem of moral hazard

• Counter the negative effects of safety net arrangements such as tendency for excessive risk taking by industry players

4

Understand the fundamental • Shariah as backbone of Islamic finance • Specific approach taken to ensure compliance with

Shariah principles

1

Appreciate the uniqueness • Recognise unique structures of Islamic finance • Identify distinctive risks for Islamic finance

2

Recognise the environment • Understand local industry, customise regulatory &

supervisory approach to nature of Islamic finance • Resolve pressing & emerging system-wide issues

3

Acknowledge the challenge • Identify pre-requisites for sustainable system e.g.

human capital, infrastructure, capacity & capability • Balancing the need for prudential regulation & strategic

aspiration

4

25

FSMP & FSBP has facilitated in transforming IF into a modern, advanced & comprehensive IF ecosystem

Financial Sector Masterplan

(2001-2010)

Financial Sector Blueprint

(2011-2020)

26

• Ensures Malaysian Law is facilitative for IF

transactions for greater certainty

• Made recommendations for the amendment of

relevant laws – Rules of High Court, Land laws

Legal & Shariah Development

• Authority for the ascertainment of

Islamic law for IF industry

• Decision of SAC is binding on IFIs,

court, arbitration & BNM

Dato’ Dr. Mohd Daud Bakar

SAC Chairman

Tun Abdul Hamid

Former Chief Justice of Malaysia/

Chairman of LHC

LAWS OF MALAYSIA

Act 701

CENTRAL BANK OF MALAYSIA ACT 2009

LAWS OF MALAYSIA

Act 799

ISLAMIC FINANCIAL SERVICES ACT 2013

“The financial system in Malaysia shall consist of the

conventional financial system and the Islamic financial

system.” Section 27, Central Bank of Malaysia Act 2009

“The principal regulatory objectives of this Act are to

promote financial stability and compliance with Shariah…”

Section 6, Islamic Financial Services Act 2013

________________________ _______________________

Dedicated judge to adjudicate

Islamic finance cases

27

Shariah Resolutions in IFaims to

be an essential guide and

reference point for the Islamic

financial community.

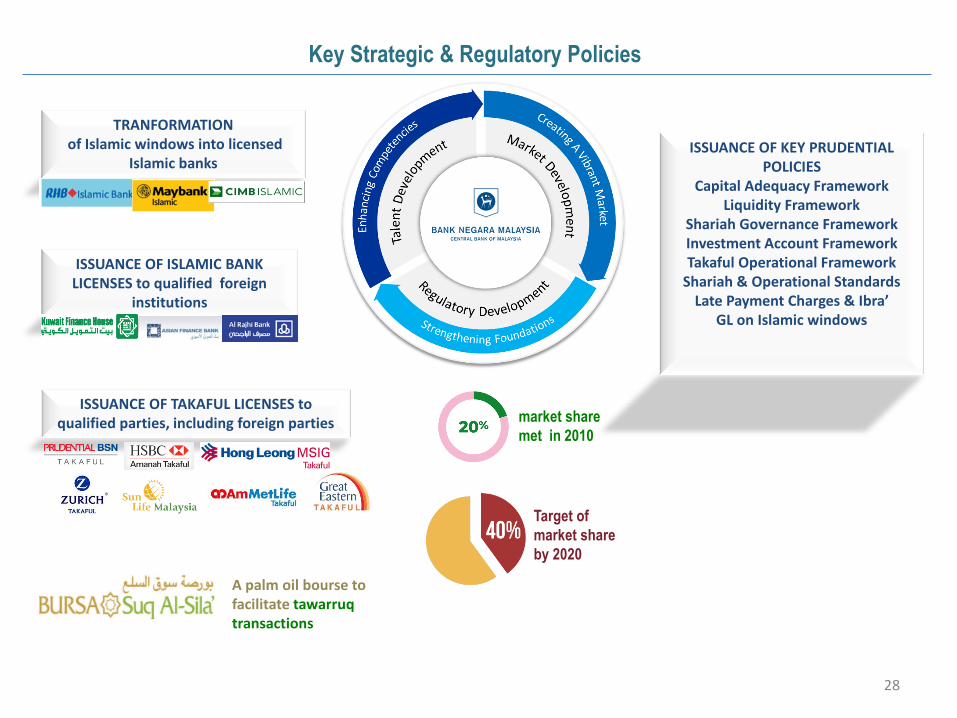

Key Strategic & Regulatory Policies

TRANFORMATION of Islamic windows into licensed

Islamic banks

ISSUANCE OF ISLAMIC BANK LICENSES to qualified foreign

institutions

ISSUANCE OF TAKAFUL LICENSES to qualified parties, including foreign parties

ISSUANCE OF KEY PRUDENTIAL POLICIES

Capital Adequacy Framework Liquidity Framework

Shariah Governance Framework Investment Account Framework Takaful Operational Framework

Shariah & Operational Standards Late Payment Charges & Ibra’

GL on Islamic windows

Target of

market share

by 2020

market share

met in 2010

A palm oil bourse to facilitate tawarruq transactions

28

Capacity Building & Talent Development

• Promotes applied research in the area of Shariah &

IF. Recognised by Thomson Reuters as the top

global contributor in dedicated IF researches (2011-

2013)

• An industry-owned institute to enhance

technical skills & knowledge of IF

practitioners

• Trained more than 30% of total IF industry

workforce

• Robust KMC

• 63 titles published & more than 11,000 books

stored

Association for Shariah advisers & Shariah

officers to enhance professionalism

Professional body responsible to promote

highest standard of professional practice

amongst IF practitioners.

SHARIAH LEADERSHIP EDUCATION

Specialised programs to educate

Shariah advisers on banking & finance

29

International Initiatives

• Malaysia play host to IILM & supported via the IILM

Corporation Act 2011

• An international corporation that facilitates cross-

border Islamic liquidity management through

issuance of sukuk.

• Outstanding sukuk issued as at end Dec 2015 - USD

1.85 bil amount of

• Malaysia play host to IFSB supported via IFSB Act

2002

• An international standard-setting organisation that

formulate standards for IFIs globally

• Issued 24 standards & guiding principles

• Several regulators including BNM have adopted

IFSB standards

30

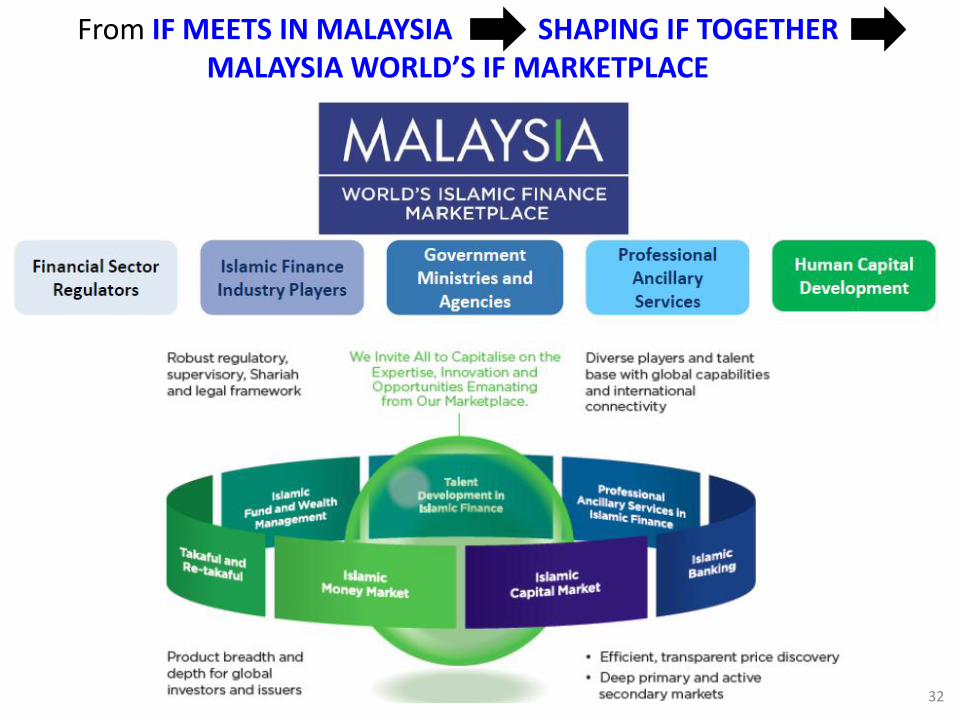

• Malaysia has earned its position as an

international marketplace for Islamic

finance.

“Malaysia's Islamic finance marketplace is open to global industry players and market participants to collaborate with and mutually benefit from a highly conducive business environment of innovation, expertise and deal flow.”

Malaysia’s MIFC initiative… greater international integration and inter-linkages on Islamic finance Established in 2006

31

CAPITAL MARKETS BANKING TAKAFUL TALENT DEVELOPMENT

PROFESSIONAL SERVICES

David Cameron Former Prime Minister of the United Kingdom October 2013

Mark Mobius, Ph.D Executive Chairman, Templeton Emerging Markets Group March 2015

32

From IF MEETS IN MALAYSIA SHAPING IF TOGETHER MALAYSIA WORLD’S IF MARKETPLACE

32

Where we are now…

How we reach to this level…

What are the policy considerations…

What’s next …

33

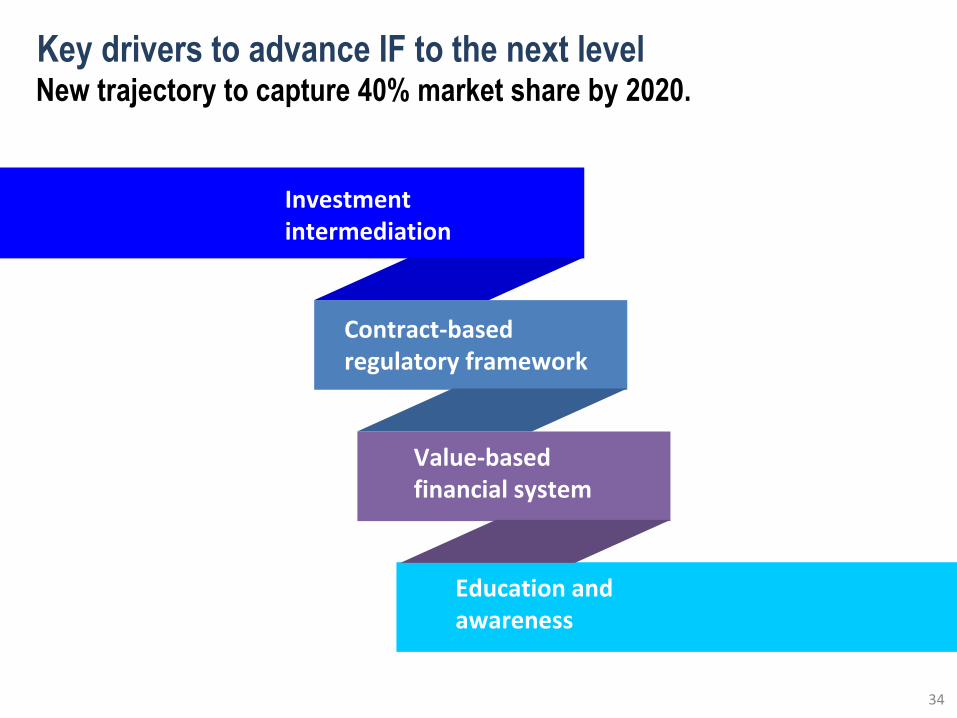

Key drivers to advance IF to the next level

Value-based financial system

Contract-based regulatory framework

Investment intermediation

Education and awareness

34

New trajectory to capture 40% market share by 2020.

Value-based financial system

Contract-based regulatory framework

Investment intermediation

Education and awareness

Enhancing role of Islamic banks to further

strengthen its intermediary functions &

promote risk sharing

• To reduce reliance on banking activities as main

source of finance for IFIs, the latest regulation, IFSA

2013, introduced Investment Account (IA) as an

alternative source of funding

i. IFSA redefines Islamic deposit and IA for greater

clarity

IA demonstrated strong exponential growth

since its inception in July 2015 (110%

growth after a year from RM32.3 billion to

RM67.8 billion)

Industry-led digital innovation led to the

development of the IA Platform (IAP) -

bridge investors with prospective ventures

to facilitate efficient operationalisation of IA

35

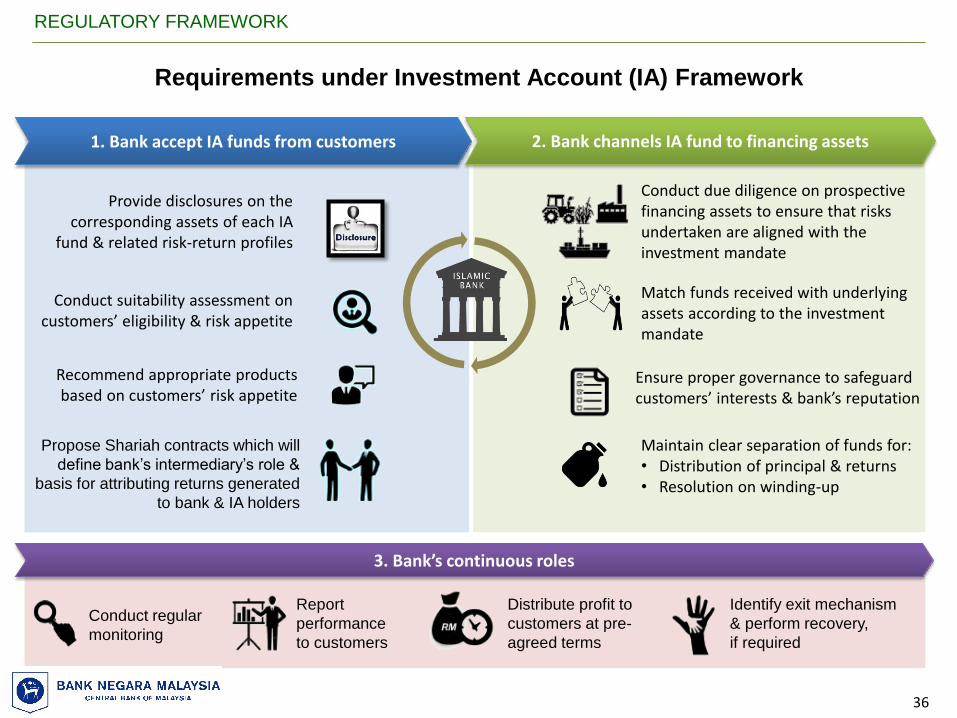

1. Bank accept IA funds from customers 2. Bank channels IA fund to financing assets

Conduct suitability assessment on customers’ eligibility & risk appetite

Provide disclosures on the corresponding assets of each IA

fund & related risk-return profiles

Recommend appropriate products based on customers’ risk appetite

Conduct due diligence on prospective financing assets to ensure that risks undertaken are aligned with the investment mandate

Ensure proper governance to safeguard customers’ interests & bank’s reputation

Maintain clear separation of funds for: • Distribution of principal & returns • Resolution on winding-up

REGULATORY FRAMEWORK

36

3. Bank’s continuous roles

Conduct regular

monitoring

Report

performance

to customers

Distribute profit to

customers at pre-

agreed terms

Identify exit mechanism

& perform recovery,

if required

Match funds received with underlying assets according to the investment mandate

Propose Shariah contracts which will

define bank’s intermediary’s role &

basis for attributing returns generated

to bank & IA holders

Requirements under Investment Account (IA) Framework

Key features

• Centralised platform channelling funds from investors to viable entrepreneurial projects

• Incorporates robust disclosure regime

• Operates on secured internet-based architecture

Industry-led initiative on Investment Account Platform facilitates efficient operationalisation of

IA by bridging investors with prospective ventures

37

Initiatives to advance Islamic finance to the next level

Value-based financial system

Contract-based regulatory framework

Investment intermediation

Education and awareness

Contract-based regulatory framework

to reflect underlying Shariah tenets of

the respective contracts

• The framework supports the effective application of

Shariah contracts in the offering of Islamic financial

products and services

• The diverse spectrum of Shariah contracts provides

the opportunity for Islamic banks to expand their

product offerings beyond the traditional debt-based

products

• To increase dynamic offerings of Islamic banks that

can effectively match the diverse needs of customers

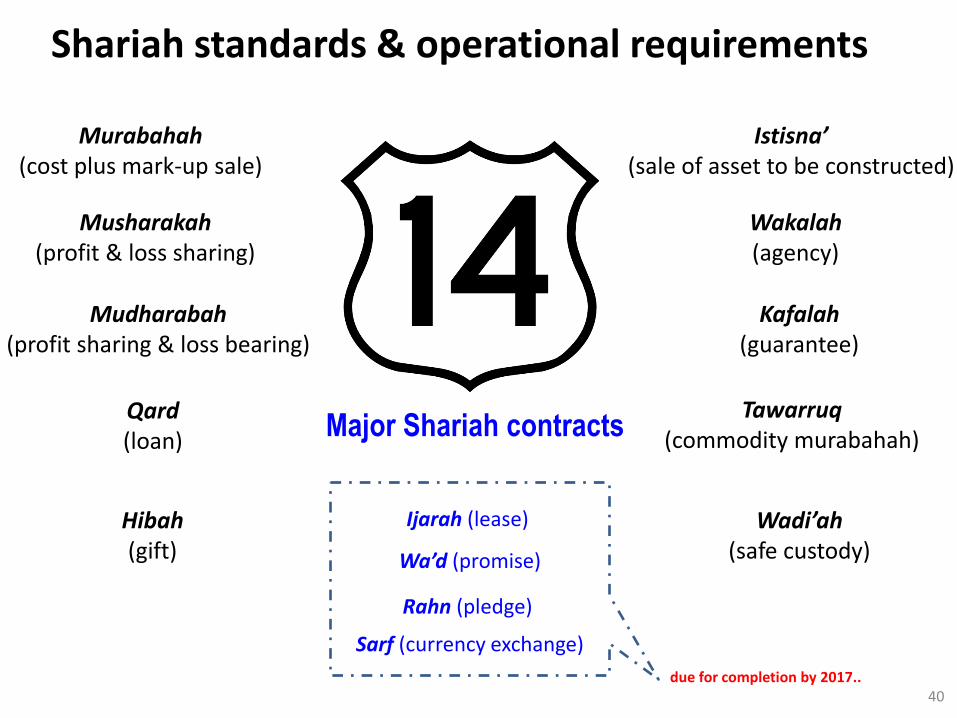

• 14 Shariah Standards have been developed to

facilitate the implementation of Shariah & operational

requirements 38

Shariah contract-based regulatory framework for Islamic finance

IFSA reflects Shariah contracts specificities and

enables issuances of -

Towards achieving value propositions of Islamic finance

Financial intermediation that serves real economy

Distinct risk and reward profiles based on Shariah contracts

Supports effective application of Shariah contracts

in Islamic banking business

39

Islamic banks conduct financial intermediation functions using various Shariah contracts

Islamic financial system

Compliance with fundamental requirements of respective Shariah contracts

Shariah Standards Practice Guides

Strengthen risk management, legal, accounting and other operational aspects of applying Shariah Standards

40

Shariah standards & operational requirements

Major Shariah contracts

Murabahah (cost plus mark-up sale)

Musharakah (profit & loss sharing)

Qard (loan)

Mudharabah (profit sharing & loss bearing)

Hibah (gift)

Istisna’ (sale of asset to be constructed)

Wakalah (agency)

Kafalah (guarantee)

Tawarruq (commodity murabahah)

Wadi’ah (safe custody)

Ijarah (lease)

Wa’d (promise)

Rahn (pledge)

Sarf (currency exchange)

due for completion by 2017..

Initiatives to advance Islamic finance to the next level

Value-based financial system

Contract-based regulatory framework

Investment intermediation

Education and awareness

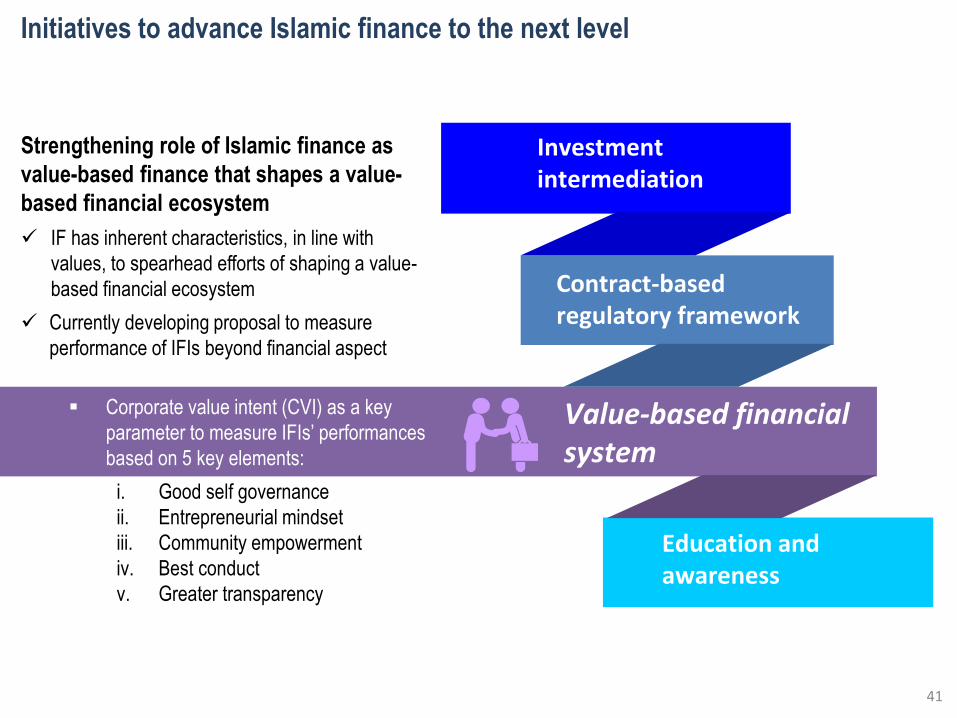

Strengthening role of Islamic finance as

value-based finance that shapes a value-

based financial ecosystem

IF has inherent characteristics, in line with

values, to spearhead efforts of shaping a value-

based financial ecosystem

Currently developing proposal to measure

performance of IFIs beyond financial aspect

Corporate value intent (CVI) as a key

parameter to measure IFIs’ performances

based on 5 key elements:

i. Good self governance

ii. Entrepreneurial mindset

iii. Community empowerment

iv. Best conduct

v. Greater transparency

41

Efficient waqf &sadaqah

management

Opportunity for Islamic banks to

give back to society

Alternative funding sources for

waqf land development

Increase in size of waqf & sadaqah collected

Expand range of cash waqf & sadaqah products

Finance more social projects that are impactful to community

Community empowerment initiative Linking Islamic finance through waqf and sadaqah

Potentials for Islamic finance

Desired outcomes

42

4 innovative solutions currently being offered by Islamic banks

1) Wakaf Selangor-Mumalat is a cash waqf collaboration

channelled for education and health benefits

2) Bank Islam introduced e-donation terminals in mosques

3) Affin Barakah Charity account-i is a deposit product where

earned profit/dividend (hibah) can be donated

4) Maybank Islamic collaborating with Majlis Agama Islam Perak

(MAIP) to collect cash waqf from the public

Note – Community empowerment initiative is referring to social finance

Initiatives to advance Islamic finance to the next level

Value-based financial system

Contract-based regulatory framework

Investment intermediation

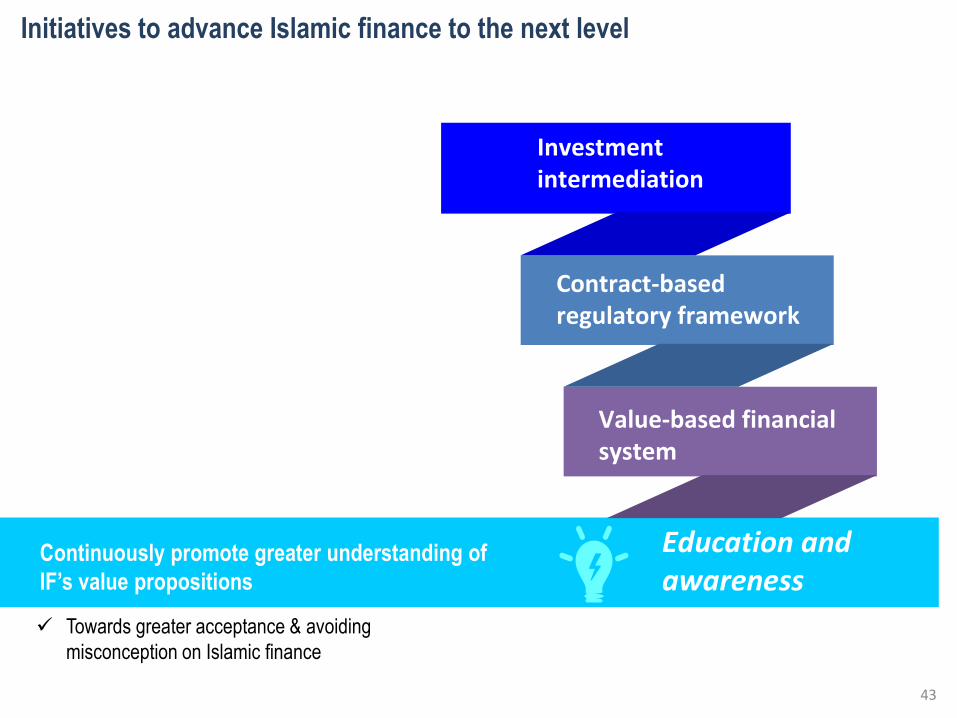

Education and awareness

Towards greater acceptance & avoiding

misconception on Islamic finance

Continuously promote greater understanding of

IF’s value propositions

43

44

45

Educator’s Manual for Murabahah Standard – Pilot project

A collaborative effort BNM,ISRA and IBFIM.

To assist the teaching faculty to infuse relevant practical elements of murabahah into the current academic syllabus.

The principles, pillars and components of murabahah including the recommended best practices are deliberated in an illustrative and attractive format

It exposes the students and academicians to the operational aspects and practical application of murabahah.

Universiti Sains Islam Malaysia (USIM) and Universiti Islam Antarabangsa Malaysia (UIAM) have agreed to adopt the Educator's Manual in their teaching syllabus

Educator’s Manual of other Shariah contracts will be issued in gradual

Disclaimer: While every care is taken in the preparation of this publication, no responsibility can be accepted for any errors.

Copyright: All or any other portion of this presentation may be reproduced provided acknowledgement of the source is made.

Notification of such use is required. All rights reserved. 46