plenary: global trends impacting international tax ... · plenary: global trends impacting...

TRANSCRIPT

Plenary: global trends impacting international tax planning and a US tax update Tom Calianese, Ernst & Young LLP James Sauer, Ernst & Young LLP Gerrit Groen, Ernst & Young LLP

Page 2 Global Tax Desk Day | New York | 20 March 2013

Disclaimer

► Ernst & Young refers to the global organization of member firms of Ernst & Young Global Limited, each of which is a separate legal entity. Ernst & Young LLP is a client-serving member firm of Ernst & Young Global Limited located in the US.

► This presentation is © 2013 Ernst & Young LLP. All rights reserved. No part of this document may be reproduced, transmitted or otherwise distributed in any form or by any means, electronic or mechanical, including by photocopying, facsimile transmission, recording, rekeying, or using any information storage and retrieval system, without written permission from Ernst & Young LLP. Any reproduction, transmission or distribution of this form or any of the material herein is prohibited and is in violation of US and international law. Ernst & Young LLP expressly disclaims any liability in connection with use of this presentation or its contents by any third party.

► Views expressed in this presentation are not necessarily those of Ernst & Young LLP.

Your presenters

► Tom Calianese Ernst & Young LLP Iselin, NJ

► James Sauer Ernst & Young LLP New York, NY

► Gerrit Groen Ernst & Young LLP New York, NY

Agenda

► US developments ► Legislative update ► Technical developments

► International developments ► Developments in tax policy ► Organisation for Economic Co-operation and

Development (OECD) base erosion and profit shifting (BEPS) report

► EU update

US developments

Page 7 Global Tax Desk Day | New York | 20 March 2013

Elements of key US tax reform proposals

President’s Framework for Business Tax Reform (September

2012) and FY 2013 budget blueprint (February 2012)

Sen. Enzi’s United States Job Creation and International

Tax Reform Act (February 2012)

Chairman Camp’s Discussion Draft (October 2011)

Wyden-Coats Bipartisan Tax Fairness and Simplification Act

(April 2011)

Deficit Commission*

Report (December 2010)

Overview

Deficit and debt impact Revenue-neutral (business sector) Revenue-neutral Revenue-neutral Revenue-neutral

Reduces debt held by the public to 60% of gross domestic product (GDP) by 2014 and 40% by 2037

Corporate taxes

Corporate tax rate 28%. 25% effective rate for manufacturing (lower rate for advanced) 35% 25% 24% 28%

Business tax expenditures

Eliminatesexpenditures for specific industries, with exceptions. Identifies tax bias for debt finance and taxing large flow-through business as issues

Not addressed Eliminates unspecified tax expenditures

Reduces many business tax expenditures. Limits deductibility of interest to real (non-inflationary) interest only

Eliminates all business tax expenditures

Research and development tax credit

Makes permanent. Increases the alternative simplified credit to 17% Not addressed Not addressed Not extended Repealed

Accelerated depreciation Moves toward economic depreciation Not addressed Not addressed

Limits depreciation allowances to accelerated depreciation system (as proxy for economic depreciation)

Eliminates or modifies, details not specified

International taxation Retains worldwide system. Imposes minimum tax on overseas profits

Territorial tax system with 95% deduction for the post-2012 foreign-source portion of dividends received from controlled foreign corporations (CFCs)

Territorial system, with 95% deduction for the foreign-source portion of dividends received from CFCs

Repeals tax deferral of active foreign earnings. Reinstitutes per-country foreign tax credit. Includes repatriation holiday with reinvestment requirements

Territorial system, current taxation of passive foreign income retained

Transition relief Not addressed 10.5% elective tax on pre-effective date foreign earnings, which could be spread over up to eight years

5.25% mandatory tax on pre-effective date foreign earnings (spread over up to eight years) future distribution taxed at 1.25%

Not addressed

Transition relief not discussed. Revenue estimate suggests little or no transition

* President’s National Commission on Fiscal Responsibility and Reform (co-chaired by Erskine Bowles and former Sen. Alan Simpson (R-WY))

Page 8 Global Tax Desk Day | New York | 20 March 2013

Key considerations for companies

► Companies have a lot at stake under a base-broadening, rate-reducing tax reform

► Any revenue-neutral reform means winners and losers across industries and within industries

► Details of provisions may matter enormously ► Still early in the debate ► What can companies do?

► Follow details of debate ► Understand and model effects of potential reforms on company ► Take advantage of opportunities for planning/minimizing risks ► Work through trade associations and company coalitions/groups to

influence the debate and frame issues

Planning for legislative change

Page 10 Global Tax Desk Day | New York | 20 March 2013

Legislative change — key aspects of planning Managing/harvesting attributes ► Accessing high-tax pools before deemed inclusion date ► Accessing deficits/hovering deficits ► Earnings and profits (E&P) and tax-pool planning

► Accounting method elections ► Triggering built-in losses ► Section 304 transactions

► Utilization of foreign tax credit (FTC) carryforwards ► Accelerating foreign taxes without E&P (e.g., withholding

taxes (WHT))

Page 11 Global Tax Desk Day | New York | 20 March 2013

E&P planning — Section 304

Facts ► CFC HoldCo acquires all of the shares of CFC2

from CFC1 for US$1,000x cash. Results ► CFC HoldCo’s acquisition of the CFC2 stock

from CFC1 is a Section 304 transaction that results in dividend income to CFC1 to the extent of the earnings and profits of CFC HoldCo first and then of CFC2.

► Dividend received by CFC1 should not give rise to Subpart F income if an exception applies (e.g., Sec. 954(d)(6)).

► Low-taxed E&P of CFC Holdco (and CFC2 thereafter) has been migrated to CFC1.

Considerations ► What happens to CFC1’s basis in CFC2 stock? ► Consider Notice 2001-45 to determine whether it

is a listed transaction or substantially similar under individual facts; if so, then requires disclosure under Treas. Reg. 1.6011-4 on Form 8886.

USP

CFC HoldCo

(low-taxed)

CFC2

CFC1 CFC2 stock

US$1,000x cash

CFC2 (low- taxed)

B = US$1,000x V = US$1,000x

CFC3 (high- taxed)

Page 12 Global Tax Desk Day | New York | 20 March 2013

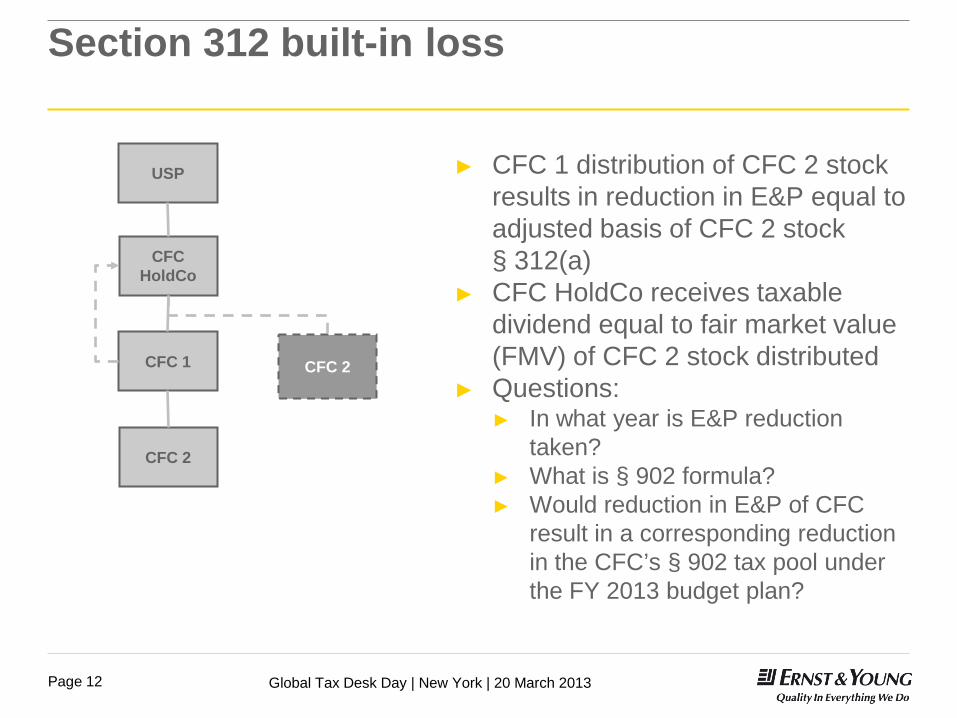

Section 312 built-in loss

► CFC 1 distribution of CFC 2 stock results in reduction in E&P equal to adjusted basis of CFC 2 stock § 312(a)

► CFC HoldCo receives taxable dividend equal to fair market value (FMV) of CFC 2 stock distributed

► Questions: ► In what year is E&P reduction

taken? ► What is § 902 formula? ► Would reduction in E&P of CFC

result in a corresponding reduction in the CFC’s § 902 tax pool under the FY 2013 budget plan?

CFC 2

USP

CFC HoldCo

CFC 1

CFC 2

Page 13 Global Tax Desk Day | New York | 20 March 2013

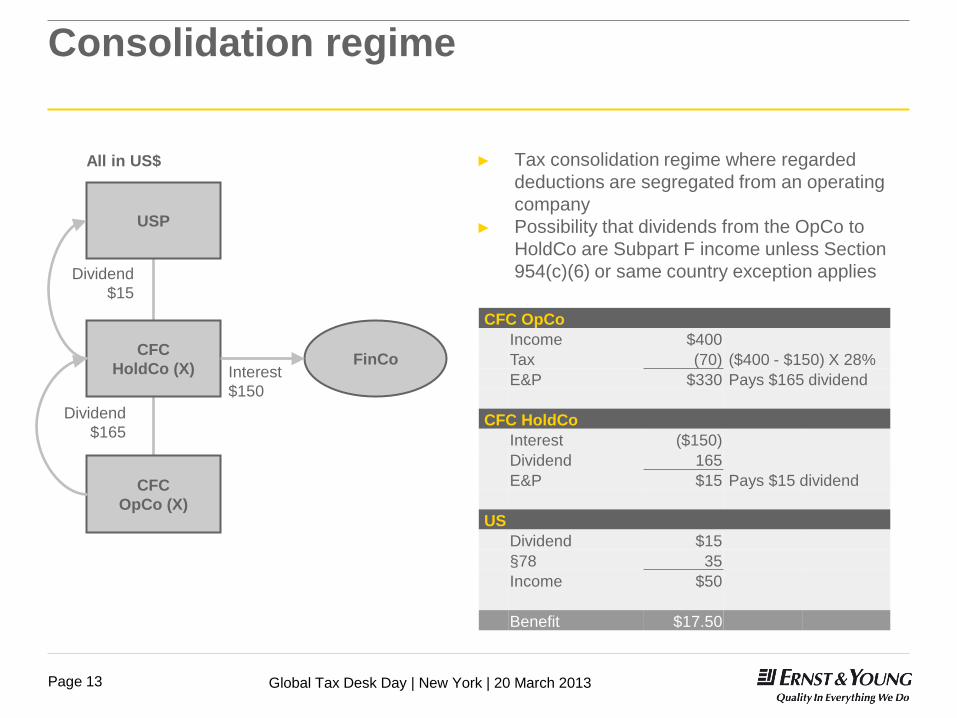

Consolidation regime

► Tax consolidation regime where regarded deductions are segregated from an operating company

► Possibility that dividends from the OpCo to HoldCo are Subpart F income unless Section 954(c)(6) or same country exception applies

Interest $150

Dividend $165

Dividend $15

CFC HoldCo (X)

USP

CFC OpCo (X)

FinCo

CFC OpCo Income $400 Tax (70) ($400 - $150) X 28% E&P $330 Pays $165 dividend

CFC HoldCo Interest ($150) Dividend 165 E&P $15 Pays $15 dividend

US Dividend $15 §78 35 Income $50

Benefit $17.50

All in US$

Page 14 Global Tax Desk Day | New York | 20 March 2013

US tax planning with subsidiaries in Italy Acquisition of Italian target

Overview 1. Italian HoldCo is leveraged by its EU parent company 2. Target contributes its business in NewCo 3. HoldCo purchases NewCo stock (assumed by FY 2013) 4. NewCo elects for step-up on its own assets 5. HoldCo and NewCo elect for tax consolidation/merger Anticipated Italian tax analysis ► Leverage must have business purpose ► Interest deductible within 30% earnings before interest,

taxes, depreciation and amortization (EBITDA) of HoldCo ► 30% EBITDA of Target may be used under tax consolidation

► Interest paid should be exempt from WHT ► E.g., one-year holding period, EU Co as interest-

beneficial owner ► Contribution of business is non-taxable

► Registration tax issue to be managed ► Target is subject to 1.375% effective corporate income

tax (CIT) upon sale of NewCo ► NewCo elects for step-up by paying 16% substitute tax ► NewCo will benefit from 31.4% amortization (Italian

corporate income tax ((IRES) 27.5% + Italian regional production tax (IRAP) 3.9%)

Anticipated US tax analysis ► US creditability of Italian 16% tax may be achieved under

certain circumstances

2. Contribution

Existing Co (ITA)

NewCo (ITA)

4. Step-up

Target (ITA)

NewCo (ITA)

3. Sale

Top US Co

EU Co

1. Loan

Seller (ITA)

5. Tax consolidation/merger

Page 15 Global Tax Desk Day | New York | 20 March 2013

US tax planning with subsidiaries in Italy Migration of Italian IP

Overview ► OpCo contributes, in exchange for shares, a

research and development (R&D) division including the intangible property (IP) to a New IPCo Srl (FY1)

► New IPCo Srl makes a step-up election on IP (FY2) ► Sale of any residual IP or final amortization (FY5) ► Further developments of IP will be owned by foreign

Principal/IPCo which remunerates New IPCo at cost plus for R&D

Anticipated Italian tax analysis ► Contribution is tax-free ► Step-up election requires 16% tax payment in three

annual instalments (30% - 40% - 30%) and allows amortization at 31.4% (IRES 27.5% + IRAP 3.9%)

► Tax amortization of IP should offset royalty income ► Sale of any residual IP with no capital gain Anticipated US tax analysis ► US creditability of Italian 16% tax may be achieved

under certain circumstances

USA Inc

SubCo (EU)

Principal/IPCo (e.g., CH or Lux)

3. Sale of IP

New IPCo Srl (Italy)

1. Contribution

2. Step-up election

OpCo (Italy)

Holdings (Italy)

Collateral consequences of the foreign group technical taxpayer rules

Page 17 Global Tax Desk Day | New York | 20 March 2013

Collateral consequences of foreign consolidated group tax payments

Issue ► Tax liability of a foreign consolidated group is allocated among its

members pursuant to Reg.1.901-2(f)(3) in proportion to each member’s allocable share of the group’s income.

► Each member is treated as having legal liability under foreign law for its portion of the group taxes.

► US tax principles apply to determine tax consequences if one person remits a tax that is the legal liability of another person. Reg. 1.901-2(f)(3)(iv).

► Raises possibility of deemed distributions and/or contributions to the extent (i) parent is not reimbursed or (ii) is reimbursed without appropriate arrangements in place that treat parent as acting on behalf of subsidiaries and subsidiaries as reimbursing parent for tax payments made on their behalf.

Page 18 Global Tax Desk Day | New York | 20 March 2013

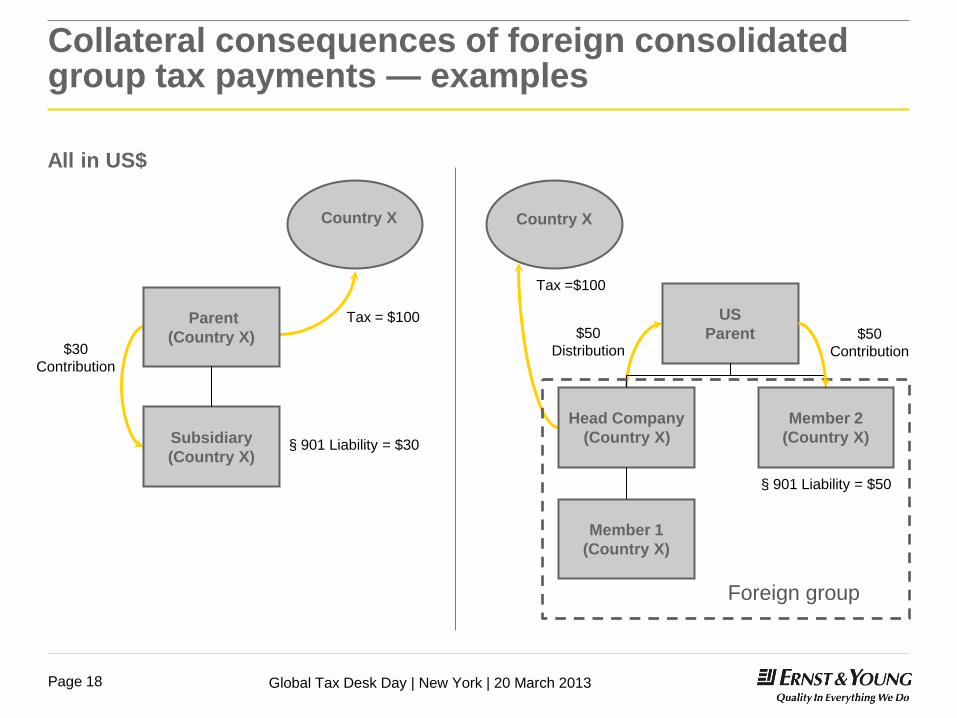

Collateral consequences of foreign consolidated group tax payments — examples

US Parent

Head Company (Country X)

Member 2 (Country X)

$50 Distribution

Member 1 (Country X)

$50 Contribution

Foreign group

Country X

Tax =$100

Parent (Country X)

Country X

Tax = $100

Subsidiary (Country X)

§ 901 Liability = $30

§ 901 Liability = $50

$30 Contribution

All in US$

Page 19 Global Tax Desk Day | New York | 20 March 2013

Collateral consequences of foreign consolidated group tax payments

► Reimbursements to parent by members ► Reimbursements to agent or other person for payment by agent of

liability of principal should not be treated as giving rise to a contribution or distribution. ► Principle has been applied to payment to parent for member’s portion

of consolidated tax liability. See Rev. Rul. 73-605; GCM 39367; and Beneficial Corp. v. Commissioner (18 T.C. 396 (1952)).

► Must a formal agency or lending arrangement be in place? ► Preamble to final regulations (TD 9576) suggests so:

► “... a shareholder’s payment of a corporation’s tax on a corporation’s reimbursement of a shareholder for paying its tax liability will not result in a deemed capital contribution and deemed dividend treatment if arrangements are in place that treat the shareholder’s payment of the tax as pursuant to a lending or agency arrangement.”

► Otherwise, risk of deemed contributions/distributions upon payment of tax by parent company and further distribution/contribution upon reimbursement.

Page 20 Global Tax Desk Day | New York | 20 March 2013

Collateral consequences of foreign consolidated group tax payments (cont.)

► Treatment of tax losses ► Treas. Reg. 1.901-2(f)(3)(iii)(C) requires allocation of net loss of a

member to other members proportionally to income of other members unless mandatory provisions under foreign law require other allocation.

► No provision allows for reimbursement by parent or other members to member with net loss.

► Under Beneficial Corp. and Dynamics Corp. v. United States (392 F.2d 241), if one member reimburses another for net loss contributed to group, it is not treated as reimbursement for value and gives rise to distribution/contribution. See also GCM 39367.

► But, in case of potential triangular distribution/contribution via common shareholder, consider authorities on whether shareholder benefits. See Sammons v. Commissioner (472 F.2d 449 (5th Cir. 1972)) and Gulf Oil Corp. v. Commissioner (89 TC 1010).

Page 21 Global Tax Desk Day | New York | 20 March 2013

Collateral consequences of foreign consolidated group tax payments (cont.)

► Steps to take to reduce risk of distribution/contribution: ► Consider having group members enter into a tax-funding

agreement or other reimbursement agreement ► Local approaches to allocating liability may differ from the

approach in the technical taxpayer regulations ► Allocation of losses of group members ► Intercompany deductible payments

► Agreement will need to be carefully drafted to ensure it follows technical taxpayer tax liability allocation method, while coordinating with specifics of local rules

► Consider treatment under local law of different categories of income with different statutory rates and categories of deductions that are specially allocable to certain income (e.g., capital gains and losses)

International developments

Page 23 Global Tax Desk Day | New York | 20 March 2013

Developments in tax policy

Expanded jurisdictions

Convergence/ alignment of tax systems

Increased tax competitiveness

Common themes

Response to global scrutiny

4

1

3 2

► Reduction in headline corporate tax rates ► Incentives for IP development/R&D activities ► Conclusion of tax treaties for key markets ► Extended availability of ruling processes

► Major governments shaping debate

► OECD and EU input ► Differing responses between

hub and destination territories

► Consistency in transfer-pricing methodologies ► Increased diligence/scrutiny in ruling processes ► EU Common Consolidated Corporate Tax Base (CCCTB) ► Wider adoption of International Financial Reporting

Standards (IFRSs) ► General Anti-Avoidance Rules (GAARs)

► Tax residency and beneficial ownership

► Permanent establishment

► Anti-haven rules/blacklists

Global attention on corporate tax

Page 25 Global Tax Desk Day | New York | 20 March 2013

OECD report on BEPS

► The OECD report “Addressing Base Erosion and Profit Shifting” was released on 12 February 2013 ► Project being driven by the governments of several key OECD

member countries, including the US, UK, Germany, France and Australia

► Origins in discussions in the G20 and also are closely linked with the G8

► Due to high-level government interest in this project, the work is being conducted on an accelerated timetable, and the recommendations that come out of it will have the strong endorsement of OECD member countries

► Focuses on the same international tax issues that are the subject of hearings and headlines in the US, UK and elsewhere

Page 26 Global Tax Desk Day | New York | 20 March 2013

“Key pressure areas”

► The OECD BEPS report is mainly a background document that sets the stage for future work of the OECD.

► The report identifies the following “key pressure areas”: ► International mismatches in entity and instrument characterization ► Application of treaty concepts to profits derived from the delivery of digital

goods and services ► Tax treatment of related-party debt financing, captive insurance and other

intra-group financial transactions ► Transfer pricing, particularly in relation to the shifting of risks and

intangibles, artificial splitting of ownership of assets among legal entities within a group, and transactions among related-party entities that would rarely take place among independent entities

► The effectiveness of anti-avoidance measures, in particular GAARs, CFC regimes, thin capitalization rules and rules to prevent tax-treaty abuse

► The availability of harmful preferential regimes

Page 27 Global Tax Desk Day | New York | 20 March 2013

Next steps

► The action plan to be issued by the OECD in the summer: ► Identify actions needed to address BEPS ► Set deadlines ► Identify resources needed

► While this project will not trigger immediate changes in law and treaties, the deep and broad political support means it is time to think about the longer-term implications of the report, including the potential impact it could have on tax reform developments in the US and elsewhere.

Page 28 Global Tax Desk Day | New York | 20 March 2013

European Commission (EC) Action Plan

► On 6 December 2012, the EC published “An Action Plan to Strengthen the Fight Against Tax Fraud and Tax Evasion.” This included two recommendations: ► An EU-common approach to identification of tax havens

► Encouragement to apply certain measures in relation to third countries that adopt tax practices incompatible with minimum standards of good governance.

► Coordinated common actions by Member States to resolve double deductions and double non-taxation cases ► Member States should ensure through their Double Taxation

Agreements (DTAs) that double non-taxation does not occur, e.g., by inclusion of “subject to tax provisions.”

► Member States should adopt GAARs.

Page 29 Global Tax Desk Day | New York | 20 March 2013

Summary

► Potential US tax reform could lead to changes in the approach to international tax planning.

► OECD and EC reports provide a framework for developments in international approach to tackling tax avoidance.

► What does this mean on a country-by-country level? ► Mature markets ► Emerging markets

Questions?

Contacts

► Tom Calianese

Ernst & Young LLP Iselin, NJ +1 732 516 4490 [email protected]

► James Sauer

Ernst & Young LLP New York, NY +1 212 773 1161 [email protected]

► Gerrit Groen Ernst & Young LLP New York, NY +1 212 773 8627 [email protected]

Ernst & Young

Assurance | Tax | Transactions | Advisory About Ernst & Young Ernst & Young is a global leader in assurance, tax, transaction and advisory services. Worldwide, our 167,000 people are united by our shared values and an unwavering commitment to quality. We make a difference by helping our people, our clients and our wider communities achieve their potential. Ernst & Young refers to the global organization of member firms of Ernst & Young Global Limited, each of which is a separate legal entity. Ernst & Young Global Limited, a UK company limited by guarantee, does not provide services to clients. For more information about our organization, please visit www.ey.com. Ernst & Young LLP is a client-serving member firm of Ernst & Young Global Limited operating in the US. © 2013 Ernst & Young LLP. All Rights Reserved. ED None 1301-1013589 BOS