platts biofuels conference, geneva, april 13 2016 biofuels conference, geneva, april 13th 2016 dr...

TRANSCRIPT

© 2016 LMC International. All rights reserved. www.lmc.co.uk

Platts Biofuels Conference, Geneva, April 13th 2016 Dr Caroline Midgley

Table of Contents:

The RED amendments

The German GHG mandate

The Outlook for EU Biofuels

Conclusions

The 2015 amendments to the RED

© 2016 LMC International. All rights reserved. March 2016

Indirect Land Use Change (ILUC)

Note: These values were first published in October 2012 in the Commission’s proposal to amend the RED. They were subsequently adopted in the

2015 RED amendment for “reporting purposes” only.

• ILUC refers to the displacement of activity onto previously unused land.

• Accounting for ILUC aims to consider the full environmental impact of

biofuel production and usage.

• There is a potential environmental impact arising from the fact that

agricultural land which is used to produce biofuels has a broad variety of

previous uses, typically in crop production.

• Research suggests that ILUC is a more significant problem for biodiesel

than for ethanol.

The European Commission’s ILUC Penalties for Different Feedstocks

4

Feedstock group Estimated indirect land-use change emissions (gCO2eq/MJ)

Cereals and other starch rich crops 12

Sugars 13

Oil crops 55

© 2016 LMC International. All rights reserved. March 2016

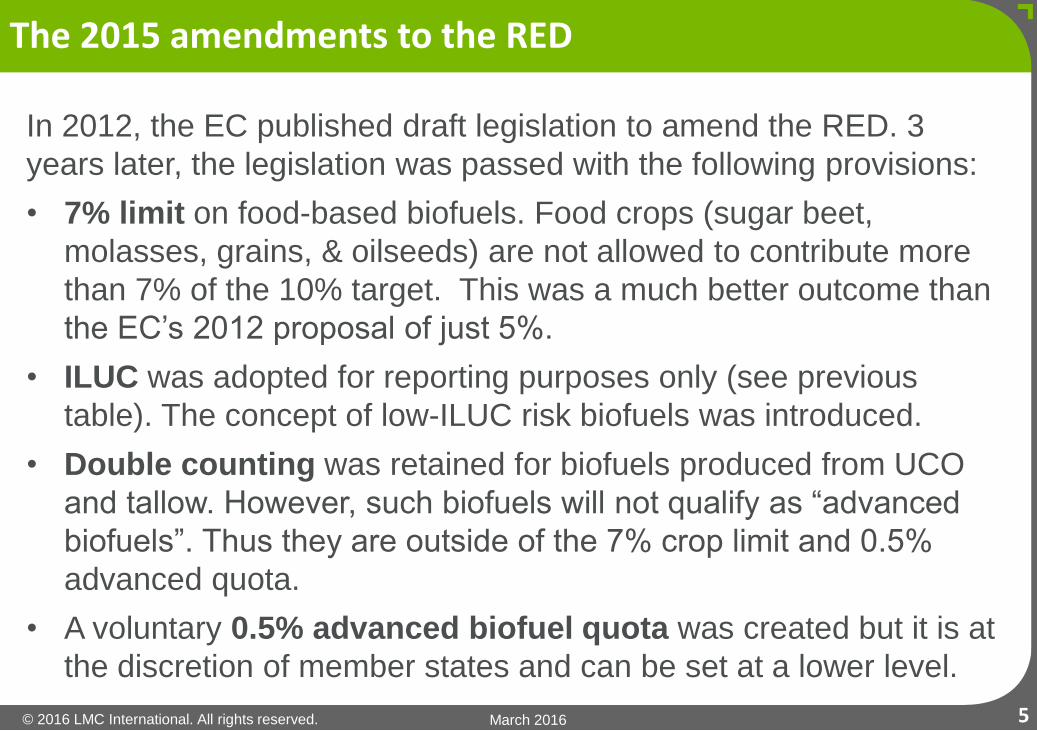

In 2012, the EC published draft legislation to amend the RED. 3

years later, the legislation was passed with the following provisions:

• 7% limit on food-based biofuels. Food crops (sugar beet,

molasses, grains, & oilseeds) are not allowed to contribute more

than 7% of the 10% target. This was a much better outcome than

the EC’s 2012 proposal of just 5%.

• ILUC was adopted for reporting purposes only (see previous

table). The concept of low-ILUC risk biofuels was introduced.

• Double counting was retained for biofuels produced from UCO

and tallow. However, such biofuels will not qualify as “advanced

biofuels”. Thus they are outside of the 7% crop limit and 0.5%

advanced quota.

• A voluntary 0.5% advanced biofuel quota was created but it is at

the discretion of member states and can be set at a lower level.

The 2015 amendments to the RED

5

© 2016 LMC International. All rights reserved. March 2016

• Biofuels qualifying as advanced will also count double towards

mandates. The directive contains a list of 20 qualifying feedstocks

(see next slide).

• A waste/residue must not be the principal product of a production

process and production must not be modified to create it.

• The GHG saving requirement of biofuels was amended, bringing

forward the implementation date of 60% GHG savings for new

plants (starting Oct 2015). The GHG saving requirement for

existing plants (operating prior to 2015) rises from 35% to 50%

from Jan 2018.

• Electric cars will now count 5 times towards mandates (instead

of 2.5 times previously).

• The Commission has indicated that post 2020, biofuels from

crops should not receive government support.

The 2015 amendments to the RED

6

© 2016 LMC International. All rights reserved. March 2016

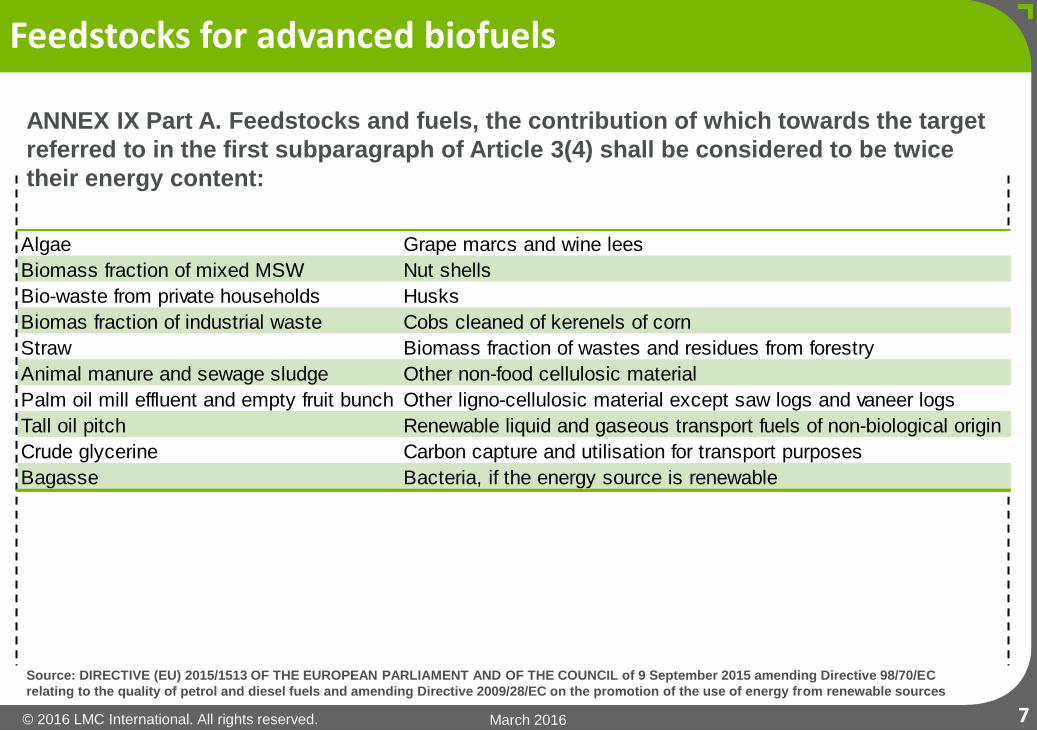

Feedstocks for advanced biofuels

ANNEX IX Part A. Feedstocks and fuels, the contribution of which towards the target

referred to in the first subparagraph of Article 3(4) shall be considered to be twice

their energy content:

Source: DIRECTIVE (EU) 2015/1513 OF THE EUROPEAN PARLIAMENT AND OF THE COUNCIL of 9 September 2015 amending Directive 98/70/EC

relating to the quality of petrol and diesel fuels and amending Directive 2009/28/EC on the promotion of the use of energy from renewable sources

7

Algae Grape marcs and wine lees

Biomass fraction of mixed MSW Nut shells

Bio-waste from private households Husks

Biomas fraction of industrial waste Cobs cleaned of kerenels of corn

Straw Biomass fraction of wastes and residues from forestry

Animal manure and sewage sludge Other non-food cellulosic material

Palm oil mill effluent and empty fruit bunch Other ligno-cellulosic material except saw logs and vaneer logs

Tall oil pitch Renewable liquid and gaseous transport fuels of non-biological origin

Crude glycerine Carbon capture and utilisation for transport purposes

Bagasse Bacteria, if the energy source is renewable

© 2016 LMC International. All rights reserved. March 2016

Based on the energy

share of ethanol and

biodiesel in transport

biofuel use has stagnated

since 2012.

According to the

Commission, the share of

renewables in transport

reached 5.7% in 2014

(including DC). The

original target was for

5.75% by 2010.

The energy share of

ethanol in the mix has

remained at close to 20%

Use of biofuels has stagnated since 2012

EU-27 Relative shares of fuel ethanol and biodiesel

8

2%

5%

9%

12%

15%

19%

22%

0

100

200

300

400

500

600

2008 2009 2010 2011 2012 2013 2014 2015

Gig

a J

ou

les

Ethanol Biodiesel % Share ethanol in biofuels Biofuels % Transport

The German GHG mandate

© 2016 LMC International. All rights reserved. March 2016

The German GHG mandate

• The quota rises from 3.5% GHG savings in 2015 to 4.0% in 2017

and 6% in 2020.

• The penalty for non-compliance is EUR 0.47/kg CO₂ equivalent.

• Data for 2015 suggests ethanol has not been disadvantaged by

the mandate (see table below)

• However, biodiesel consumption fell by 6.4% despite a 2.6%

increase in diesel consumption suggesting the GHG mandate

reduced demand by 9.0%.

Sales of Ethanol and Biodiesel in Germany, 2014 vs 2015

10

Units 2014 2015 % Change

Ethanol mn lts 1,445 1,413 -2.2%

Gasoline mn lts 25,427 24,896 -2.1%

Biodiesel 000 mt 2,288 2,141 -6.4%

Diesel 000 mt 36,403 37,367 2.6%

© 2016 LMC International. All rights reserved. March 2016

• This was because the GHG savings for biodiesel were higher

than expected, reducing the volume of biodiesel needed to meet

the mandate.

• The value of double counting biofuels is worth less in Germany

under the GHG mandate. The value of DC falls from a factor of 2

to 1.4 (with UCOME at 85% and RME at 60%).

• The market share of German producers improved in 2015 a result

of the mandate as local product has better GHG savings.

• The lesson from Germany is that it is difficult to anticipate future

reductions in CO2 savings and this results in a tendency to set

the mandate too low, reducing physical demand.

The German GHG mandate

11

The Outlook for EU Biofuels

© 2016 LMC International. All rights reserved. March 2016

• No EU wide biofuel mandates after 2020.

• The EU is seeking GHG reduction targets that will apply to all

renewables, not just transport.

• Thus it will be up to individual member states to provide specific

targets for biofuels.

• The RED revision of 2015 created a voluntary 0.5% mandate for

advanced biofuels, paving the way for 2G.

• Italy, Finland and Germany have already announced 2G

mandates. Denmark will decide in March 2016.

• Before the end of 2016, states must inform the Commission how

they intend to implement the revised RED.

• Only France has committed to raising mandates beyond 2020.

• Finland and Sweden have targets above 10% by 2020.

The outlook for EU biofuel policy

13

© 2016 LMC International. All rights reserved. March 2016

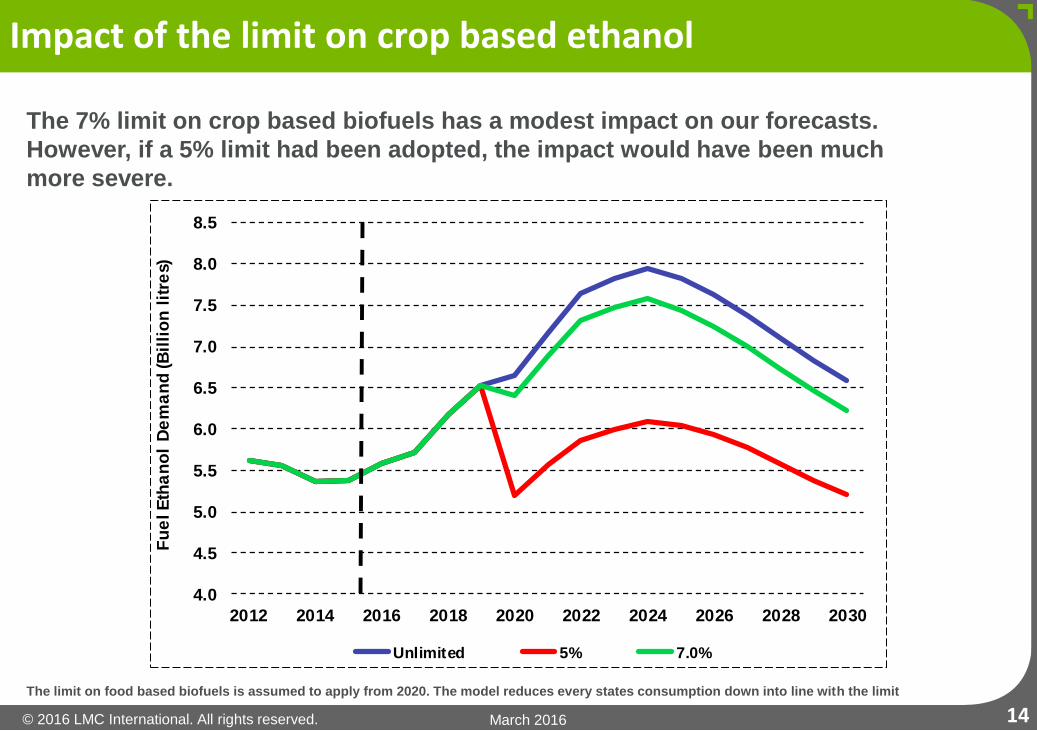

The 7% limit on crop based biofuels has a modest impact on our forecasts.

However, if a 5% limit had been adopted, the impact would have been much

more severe.

Impact of the limit on crop based ethanol

The limit on food based biofuels is assumed to apply from 2020. The model reduces every states consumption down into line with the limit

14

4.0

4.5

5.0

5.5

6.0

6.5

7.0

7.5

8.0

8.5

2012 2014 2016 2018 2020 2022 2024 2026 2028 2030

Fu

el E

tha

no

l D

em

an

d (B

illi

on

lit

res)

Unlimited 5% 7.0%

© 2016 LMC International. All rights reserved. March 2016

The current supply of waste-based ethanol

The EU can only produce around 220 million litres of waste-based ethanol (including

cellulosic ethanol), less than 5% of the fuel ethanol market.

15

Country Feedstock Company Plant Capacity (mn lts) Start-up Year

Denmark Straw Inbicon (Dong Energy) Kalundborg 5.4 2009

Odense 0.1 2005

Finland Bakery Waste St Lappeenranta 3.0 2007

MSW St Hämeenlinna 2.0 2010

Waste starch St Jokioinen 7.0 2011

France Biomass Tereos (Futurol) Bucy-le-long 8.0 2016

Germany Food Waste KWST Rockstedt 60.0 Prior to 2005

Straw Clariant Straubing 1.2 2012

Waste starch Wabio Bioenergie Bad Kostritz 10.0 2006

Ireland Whey Carberry Group Cork 10.0 Prior to 2005

Italy Straw Beta Renewables Crescentino 50.0 2013

Netherlands Waste starch Cargill Bergen Op Zoom 40.0 Prior to 2005

Spain Straw Abengoa Babilafuente, Salamanca 4.5 2007

Sweden Black liquor Domsjö Fabriker AB Domsjö 17.3 Prior to 2005

Grand Total 218.5

© 2016 LMC International. All rights reserved. March 2016

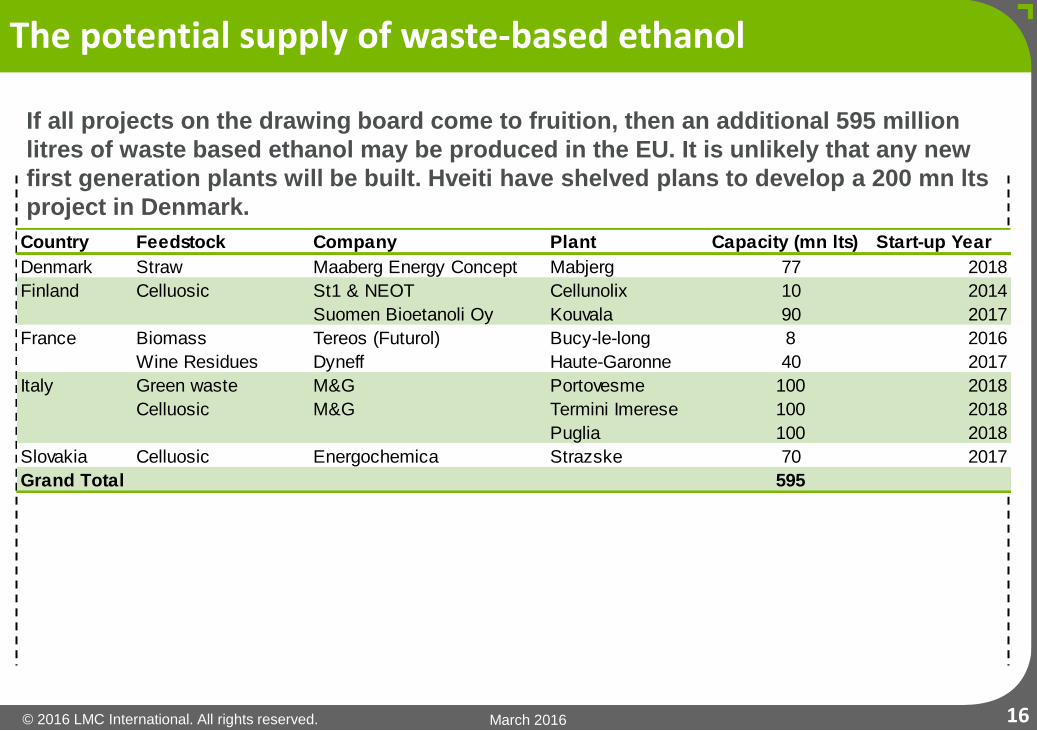

The potential supply of waste-based ethanol

16

Country Feedstock Company Plant Capacity (mn lts) Start-up Year

Denmark Straw Maaberg Energy Concept Mabjerg 77 2018

Finland Celluosic St1 & NEOT Cellunolix 10 2014

Suomen Bioetanoli Oy Kouvala 90 2017

France Biomass Tereos (Futurol) Bucy-le-long 8 2016

Wine Residues Dyneff Haute-Garonne 40 2017

Italy Green waste M&G Portovesme 100 2018

Celluosic M&G Termini Imerese 100 2018

Puglia 100 2018

Slovakia Celluosic Energochemica Strazske 70 2017

Grand Total 595

If all projects on the drawing board come to fruition, then an additional 595 million

litres of waste based ethanol may be produced in the EU. It is unlikely that any new

first generation plants will be built. Hveiti have shelved plans to develop a 200 mn lts

project in Denmark.

© 2016 LMC International. All rights reserved. March 2016

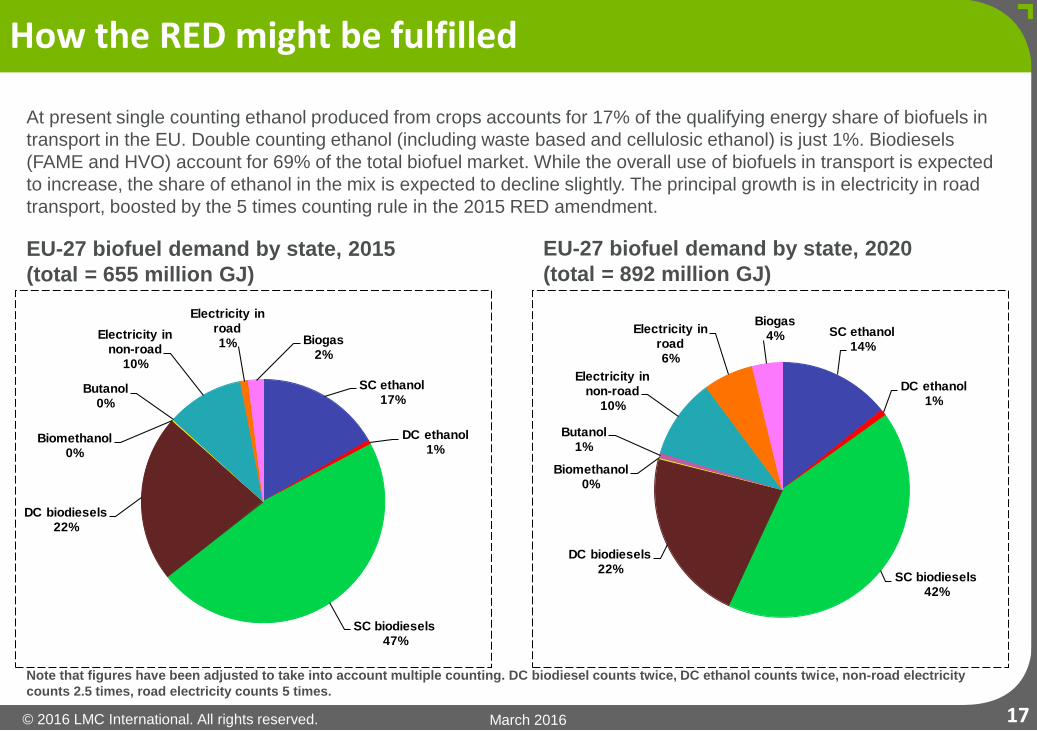

At present single counting ethanol produced from crops accounts for 17% of the qualifying energy share of biofuels in

transport in the EU. Double counting ethanol (including waste based and cellulosic ethanol) is just 1%. Biodiesels

(FAME and HVO) account for 69% of the total biofuel market. While the overall use of biofuels in transport is expected

to increase, the share of ethanol in the mix is expected to decline slightly. The principal growth is in electricity in road

transport, boosted by the 5 times counting rule in the 2015 RED amendment.

EU-27 biofuel demand by state, 2015

(total = 655 million GJ)

EU-27 biofuel demand by state, 2020

(total = 892 million GJ)

How the RED might be fulfilled

Note that figures have been adjusted to take into account multiple counting. DC biodiesel counts twice, DC ethanol counts twice, non-road electricity

counts 2.5 times, road electricity counts 5 times.

17

SC ethanol17%

DC ethanol1%

SC biodiesels47%

DC biodiesels22%

Biomethanol0%

Butanol0%

Electricity in non-road

10%

Electricity in road1% Biogas

2%

SC ethanol14%

DC ethanol1%

SC biodiesels42%

DC biodiesels22%

Biomethanol0%

Butanol1%

Electricity in non-road

10%

Electricity in road6%

Biogas4%

Conclusions

© 2016 LMC International. All rights reserved. March 2016

• From relatively simple beginnings in 2003, EU biofuel policy has

become highly complex as the European Parliament has

struggled to reconcile the demands of NGOs with those in the

industry.

• Implementation of the 2009 RED has taken far longer than the 18

months originally envisaged. It would not be surprising if

implementation of the 2015 revision was subject to similar delays.

• Policy was been implemented on a piecemeal basis with many

states delaying the implementation of sustainability requirements.

• The number of sustainability and certification schemes has

proliferated. This has greatly increased the administrative burden

on producers.

Conclusions

19

© 2016 LMC International. All rights reserved. March 2016

• The Commission’s announcement in 2011 that it would amend the

RED caused widespread uncertainty and put the market on hold

for 4 years. Finance for new 1G projects dried up, governments

refused to raise mandates and demand stagnated.

• The 2015 revision may put the market back on track but mandate

rises look set to remain on hold until 2017, the deadline for

announcing advanced biofuel mandates.

• The double counting policy largely benefited the biodiesel market

where waste oils (UCO/Tallow) could be converted into biodiesel

using existing technology.

• By contrast, large scale conversion of wastes and residues for

ethanol relies on the availability of cellulosic technology which is

still being commercialised.

Conclusions

20

© 2016 LMC International. All rights reserved. March 2016

• The trend is towards dropping ethanol or biodiesel specific

mandates in favour of GHG saving mandates. The lesson from

Germany is that accurately quantifying the GHG savings from

biofuels is key. As technology improves the GHG savings of

biofuels over time, such mandates will tend to reduce physical

demand for biofuels.

• More 2G capacity will be needed if states implement advanced

biofuel mandates. An EU wide 0.5% mandate would require 2.8

billion litres of cellulosic ethanol (replacing 0.5% of gasoline with

ethanol).

• It is looking increasingly likely that there will be no EU wide

targets for biofuels in transport after 2020. It will therefore be

down to individual member states to promote biofuels.

Conclusions

21

© 2016 LMC International. All rights reserved. March 2016

Singapore

16 Collyer Quay #21-00

Singapore 049318

Singapore

Tel: +65 6818 9231

This presentation and its contents are to be held confidential by the client, and are not to be disclosed, in whole or in part, in any

manner, to a third party without the prior written consent of LMC International.

While LMC has endeavoured to ensure the accuracy of the data, estimates and forecasts contained in this presentation,

any decisions based on them (including those involving investment and planning) are at the client’s own risk.

LMC International can accept no liability regarding information analysis and forecasts contained in this presentation.

© LMC International, 2016

All rights reserved

New York

1841 Broadway

New York, NY 10023

USA

T +1 (212) 586-2427

F +1 (212) 397-4756

Oxford

4th Floor, Clarendon House

52 Cornmarket Street

Oxford OX1 3HJ

UK

T +44 1865 791737

F +44 1865 791739

Kuala Lumpur

B-03-19, Empire Soho

Empire Subang

Jalan SS16/1, SS16

47500 Subang Jaya

Selangor Darul Ehsan

Malaysia

T +603 5611 9337

www.lmc.co.uk