planning to succeed - the definitive eguide for building company financial forecasts mark ostryn...

TRANSCRIPT

8/14/2019 Planning to Succeed - The Definitive eGuide for Building Company Financial Forecasts Mark Ostryn DRAFT 180708

http://slidepdf.com/reader/full/planning-to-succeed-the-definitive-eguide-for-building-company-financial 1/94

K2

C

owledge20 pty ltd

m

HE DMP

FT

This is

ommearkostr

I hope t

you –

FINITNY FI

ORECRACK

a very

ts are t n@kno

at it’s

ark Os

IVE EANC

O

ASTIING

arly dra

uly wel ledge

f some

tryn Jul

GUIDIAL FTRY

G, FIOUR

ft and

ome at 020.co

value to

2008

E FORREC

NANBUSI

.

BUILSTS‐

INGESS

INGARK

& FAGRO

TTH

8/14/2019 Planning to Succeed - The Definitive eGuide for Building Company Financial Forecasts Mark Ostryn DRAFT 180708

http://slidepdf.com/reader/full/planning-to-succeed-the-definitive-eguide-for-building-company-financial 2/94

June 1,2008

FORECASTING, FINANCING & FAST TRACKING YOUR BUSINESS GROWTH

2 | P a g e

© 2008. Knowledge 2020 Pty Ltd. Please do not reproduce without prior permission, which will usually begranted. Contact Mark Ostryn 02 8005 1240 http://www.knowledge2020.com The above text containsgeneric financial information that does not constitute financial advice

TABLE OF CONTENTS

1 INTRODUCTION ......................................................................................................................................... 5

2 STRATEGIC VISION ..................................................................................................................................... 7

2.1 WHYFORECAST................................................................................................................................................ 8 2.2 PROFILE OF SUCCESS........................................................................................................................................... 9 2.3 MAKING FORECASTING EFFECTIVE....................................................................................................................... 11 2.4 UNDERSTANDING CUSTOMERS .................................................................................................................. 12

2.4.1 MARKET SEGMENTATION ...................................................................................................................... 13 2.5 REALISTIC ASSUMPTIONS ........................................................................................................................... 14 2.6 GETTING STARTED WITH YOUR FORECAST.............................................................................................................. 15

3. REVENUES ................................................................................................................................................ 19

3.1 PRODUCTSALES.............................................................................................................................................. 20 3.2 PRICING........................................................................................................................................................ 22 3.3 GEOGRAPHICALEXPANSION ........................................................................................................................... 25 3.4 NEW PRODUCTREVENUES ............................................................................................................................. 26 3.5 BUSINESSSEGMENTS....................................................................................................................................... 27 3.6 ALLIANCES, PARTNERSHIPS, LICENSING AND DISTRIBUTION AGREEMENTS .............................................. 27

3.6.1 Licensing ................................................................................................................................................ 28 3.6.2 STRATEGIC ALLIANCES ........................................................................................................................... 30 3.6.3 DISTRIBUTION CHANNELS ...................................................................................................................... 30

3.7 FRANCHISING ............................................................................................................................................. 31 3.7.1 Being a Franchisor ................................................................................................................................. 31 3.7.2 Being a Franchisee ................................................................................................................................. 33

3.8 PROJECT MANAGEMENT ............................................................................................................................ 33 3.9 CONSULTANCY ........................................................................................................................................... 34 3.10 OTHERINCOME.............................................................................................................................................. 34

3.10.1 Grants & financial Assistance ........................................................................................................... 34 3.10.2 Intellectual Property Income ............................................................................................................ 35

4. COSTS ....................................................................................................................................................... 37

4.1 COST OF SALE................................................................................................................................................. 38 4.1.1 Refunds, Warranties and Guarantees .................................................................................................... 38 4.1.2 Loyalty & Awards Programmes ............................................................................................................. 39

4.2 OPERATING EXPENSES/ OVERHEADS ................................................................................................................ 40 4.2.1 Marketing .............................................................................................................................................. 41

8/14/2019 Planning to Succeed - The Definitive eGuide for Building Company Financial Forecasts Mark Ostryn DRAFT 180708

http://slidepdf.com/reader/full/planning-to-succeed-the-definitive-eguide-for-building-company-financial 3/94

June 1,2008

FORECASTING, FINANCING & FAST TRACKING YOUR BUSINESS GROWTH

3 | P a g e

© 2008. Knowledge 2020 Pty Ltd. Please do not reproduce without prior permission, which will usually begranted. Contact Mark Ostryn 02 8005 1240 http://www.knowledge2020.com The above text containsgeneric financial information that does not constitute financial advice

4.2.2 Information Technology ......................................................................................................................... 46 4.2.3 Employee / Personnel Costs ................................................................................................................... 49 4.2.4 Administrative Costs .............................................................................................................................. 53 4.2.5 Legal Costs ............................................................................................................................................. 54 4.2.6 TAXes ..................................................................................................................................................... 55

5. BALANCE SHEET, WORKING CAPITAL & CAPITAL EXPENDITURE ................................................................. 59

5.1 BUSINESSCHALLENGES – MANAGING YOURCASHFLOW ....................................................................................... 60 5.1.1 Managing Working Capital ........................................................................................................................ 61

5.2 BUSINESS GROWTH – INVESTING INTHEFUTURE ....................................................................................... 66 5.2.1 Manufacturing challenges .................................................................................................................... 67 5.2.2 Research & DeveloPment challenges .................................................................................................... 68

5.3 LIMITS TO GROWTH – CAN YOU GROW TOO QUICKLY? ............................................................................. 69 5.4 DEPRECIATION& AMORTISATION....................................................................................................................... 69

5.4.1 INTANGIBLE ASSETS & AMORTISATION ................................................................................................ 70

6 FINANCING .............................................................................................................................................. 71

6.1 DEBT ........................................................................................................................................................... 72 6.2 EQUITY ....................................................................................................................................................... 73

6.2.1 RETAINED PROFITS ................................................................................................................................. 74 6.2.2 Share capital issued ............................................................................................................................... 74 6.2.3 Dividends declared & paid ..................................................................................................................... 75 6.2.4 Reserves ................................................................................................................................................. 75

7 REPORTING & ANALYSIS ................................................................................................................................. 76 7.1 CASH FLOW & CASH MANAGEMENT FORECASTING.............................................................................................. 76

7.1.1 CASH FLOW AND INVESTORS ................................................................................................................. 79 7.2 RATIOANALYSIS ........................................................................................................................................... 80 7.3 VARIANCE ................................................................................................................................................... 81 7.4 SCENARIO ANALYSIS ......................................................................................................................................... 82 7.5 FINANCIALRISK MANAGEMENT .................................................................................................................... 84

8. ACQUIRING OR SELLING – VALUATION & OTHER CHALLENGES .................................................................. 87

8.1 INCREASING YOUR BUSINESS VALUATION ................................................................................................. 89 8.2 MERGERS& ACQUISITIONS............................................................................................................................... 89

8.2.1 Vertical Integration ................................................................................................................................ 91 8.3 DUE DILIGENCE ........................................................................................................................................... 92 8.4 EXITING YOUR BUSINESS ............................................................................................................................ 93

9 REVIEWING YOUR FORECAST .................................................................................................................... 94

8/14/2019 Planning to Succeed - The Definitive eGuide for Building Company Financial Forecasts Mark Ostryn DRAFT 180708

http://slidepdf.com/reader/full/planning-to-succeed-the-definitive-eguide-for-building-company-financial 4/94

June 1,2008

FORECASTING, FINANCING & FAST TRACKING YOUR BUSINESS GROWTH

4 | P a g e

© 2008. Knowledge 2020 Pty Ltd. Please do not reproduce without prior permission, which will usually begranted. Contact Mark Ostryn 02 8005 1240 http://www.knowledge2020.com The above text containsgeneric financial information that does not constitute financial advice

8/14/2019 Planning to Succeed - The Definitive eGuide for Building Company Financial Forecasts Mark Ostryn DRAFT 180708

http://slidepdf.com/reader/full/planning-to-succeed-the-definitive-eguide-for-building-company-financial 5/94

June 1,2008

FORECASTING, FINANCING & FAST TRACKING YOUR BUSINESS GROWTH

5 | P a g e

© 2008. Knowledge 2020 Pty Ltd. Please do not reproduce without prior permission, which will usually begranted. Contact Mark Ostryn 02 8005 1240 http://www.knowledge2020.com The above text containsgeneric financial information that does not constitute financial advice

1 INTRODUCTION

Entrepreneurship has its glamour. However behind the world of intense negotiations, last minute deals and garage visionaries madegood lie the less glamorous concepts that you must get right – cashflow, working capital, pricing strategy etc.

This eBook is all about financial forecasting. It addresses the truism“failing to plan is planning to fail”. A forecast is simply a translation of

the vision and strategy of your company into financial numbers. Manyentrepreneurs and managers find this process tedious and intimidating.

External support is not always there for you. This eBook is here to assist you.

Your company must be self ‐sustaining over the short term and profitable over the long term. Itmust generate sufficient cash to pay the bills and maintain increasing levels of sales.

I wrote this having spent many years working with fast growing dynamic Small & MediumEnterprises. These dynamic companies continually faced the longer term financial issues whichwould help determine their success.

Most businesses use adequate to good Management Accounting packages such as MYOB, andQuicken. These tools are perfect for audit and for a historical review of the enterprise. Butwhat of the future? How are key expansion questions such as the following answered?

• What is our company worth today? How can we increase its value in the future?• Can we afford to fund our growth? Will our need for ever increasing amount of

working capital sink our company?• Should we purchase? Should we build / buy that new automation system or factory?• Our new venture? Should we pursue the opportunity to develop and market a new

product range?• Buy versus build? Should we invest in the capacity to produce key inventory ourselvesor outsource this?

• Our acquisition plans? Will the anticipated future profit streams and the savings fromsynergies justify the cost of acquisition?

8/14/2019 Planning to Succeed - The Definitive eGuide for Building Company Financial Forecasts Mark Ostryn DRAFT 180708

http://slidepdf.com/reader/full/planning-to-succeed-the-definitive-eguide-for-building-company-financial 6/94

June 1,2008

FORECASTING, FINANCING & FAST TRACKING YOUR BUSINESS GROWTH

6 | P a g e

© 2008. Knowledge 2020 Pty Ltd. Please do not reproduce without prior permission, which will usually begranted. Contact Mark Ostryn 02 8005 1240 http://www.knowledge2020.com The above text containsgeneric financial information that does not constitute financial advice

The forecasting process is often one of iteration, where you can try out different ‘what if’ levelsof investment in your budget model and see the different outcomes. If you increase the salesbudget, how many additional sales people will you need to generate that level of extra sales?

Developing your forecast on a spreadsheet or specialist software allows you more flexibility andcomplexity in trying out these different scenarios.

The different scenarios will also show the impact of relevant risk factors. How will interestrates affect the demand for housing? What is the relationship between the amount of rain nextsummer and my ice cream sales?

There are a couple more points, I’ll make before getting into the detail:

Firstly, there's no need to reinvent the wheel in regards to building your own forecastingspreadsheets. There are a wide range software packages and spreadsheets commerciallyavailable. They vary in quality, robustness, price and applicability to your demands of yourparticular industry. I have not specifically mentioned any in this booklet, but would bedelighted to understand more about your company and talk you through your options.

Secondly, I’ve tried to cover as many different types of industry, position on the supply chain,and way of doing business as I can within the limited space below. I haven’t managed to cramin every variable for every company, but would be delighted to receive your feedback aboutwhat needs to be addressed. The booklet remains a PDF soft copy only at present, meaning Ican update it whenever I get the urge to. Hence your insight would be most welcome.

Happy reading and most important of all, good luck with your business!

Mark [email protected] July 2008

8/14/2019 Planning to Succeed - The Definitive eGuide for Building Company Financial Forecasts Mark Ostryn DRAFT 180708

http://slidepdf.com/reader/full/planning-to-succeed-the-definitive-eguide-for-building-company-financial 7/94

June 1,2008

FORECASTING, FINANCING & FAST TRACKING YOUR BUSINESS GROWTH

7 | P a g e

© 2008. Knowledge 2020 Pty Ltd. Please do not reproduce without prior permission, which will usually begranted. Contact Mark Ostryn 02 8005 1240 http://www.knowledge2020.com The above text containsgeneric financial information that does not constitute financial advice

2 STRATEGIC VISION

It is often said that there are four types of company:

Those that make things happen.Those that watch things happen and respond.Those that watch things happen and don’t respond.Those that didn’t notice that anything had happened.

We’d all like to be in the first group, but no matter how visionary we are, much of our work is inresponding to other’s first moves. We’ve even got it wrong from time to time, and notresponded when we needed to!

This eBook is all about planning to make things happen – having a strategy. We’ll also try tohelp you with responding to market shifts – mainly by guessing that they may occur and doingsome scenario planning (what if….?), some sensitivity analysis (if interest rates increase by x%what will be the effects on sales?) and some risk management.

Crudely, you can liken any business to a poker machine that swallows up money put into it, andhopefully spits out more. However that chance is based on the operators skill rather than theluck of the pull.

A business entity is simply a collaboration of resources that is must make the greatest possiblereturn on a flow of financial inputs provided to it. These inputs are DEBT, primarily fromfinancial institutions and EQUITY from shareholders.

For the long term, your company is only sustainable if for a given level of risk:

• A holder of EQUITY in your company (i.e. a part ‐owner) can get a greater return on thatinvestment compared with other investment opportunities

• A holder of DEBT in your company earns a market competitive rate of interest forlending funds to your company.

Along the way there are a series of stakeholders in the company that also need to be satisfied

8/14/2019 Planning to Succeed - The Definitive eGuide for Building Company Financial Forecasts Mark Ostryn DRAFT 180708

http://slidepdf.com/reader/full/planning-to-succeed-the-definitive-eguide-for-building-company-financial 8/94

© 200grantegeneri

June 1,2008

8 | P a g

8. Knowledge 20d. Contact Mark

financial inform

While mmeasure

• •

•

2. 1

As forec

You muscompaninvestor

These ficompanconvinceinformat

FORE

e

0 Pty Ltd. Pleasestryn 02 8005 12tion that does no

ny of thesements gene

RequireRequirecity, provRequirenot be “fi

good cor

HY FORE

sts are inva

t have a setto achieve.and ventur

ures will bebased on a

d that yourion, they wi

ASTING, FI

do not reproduce40 http://www.kt constitute finan

stakeholderated by th

ent for envient to lookide employent to looknancial rati

orate citize

AST

riable inacc

of financialAdditional

e capitalists

used by thvaluation t

frameworkll have mor

ANCING &

without prior pernowledge2020.coial advice

rs may notcompany,

ronmentalat the com

ent to reidat “financianal” to sha

n e.g. chari

rate or eve

projections,ly, lenders nwill calcula

investor tochnique su

has been scconfidenc

FAST TRAC

mission, which wim The above tex

ave a direcheir indirec

easures, sunity impa

ents of thatl dispersmeeholders, b

y donations

n wrong, is

a numericaeed to seete what the

calculate tch as multiprupulously

to invest i

ING YOUR

ll usually becontains

t bearing ont impact m

stainabilityct of decisiocityts” made b

ut which m

etc.

there any n

l statementstrong likethink is th

e potentialles of earnirepared usiyour comp

USINESS G

the perfory be substa

etc.ns to locate

y the compy show the

ed to forec

of what yolihood of re

value of y

future valugs or profit

ng best avaiany.

OWTH

ancential e.g.

in a particu

ny which mcompany a

st?

want yourpayment; aur compan

of yours. If they arlable

lar

aya

gel.

8/14/2019 Planning to Succeed - The Definitive eGuide for Building Company Financial Forecasts Mark Ostryn DRAFT 180708

http://slidepdf.com/reader/full/planning-to-succeed-the-definitive-eguide-for-building-company-financial 9/94

June 1,2008

FORECASTING, FINANCING & FAST TRACKING YOUR BUSINESS GROWTH

9 | P a g e

© 2008. Knowledge 2020 Pty Ltd. Please do not reproduce without prior permission, which will usually begranted. Contact Mark Ostryn 02 8005 1240 http://www.knowledge2020.com The above text containsgeneric financial information that does not constitute financial advice

The process of generating these figures also adds reality to your expansion plans. For example,

if you want to open up offices or factories in China you will have to research and allocate thecosts for doing so. Having performed that financial anlysis, you will be in a better position toassess alternatives such as building a distribution channel instead.

A supplier of funds will also see where you are more financially vulnerable and where you aremost likely to require financial injections. You may find that you do not require all $5m investedupfront and by having it staged over time you have the opportunity to obtain a higher valuationfor your company as you move through from start up to expansionary phase.

In short, while no investor is expecting you to get your future projections "correct", the

discipline required in doing the projections in the first place alerts you to potentialopportunities or threats that you may not have otherwise considered.

2.2 PROFILE OF SUCCESS

The financial data that you forecast will tend to quantify some of the characteristics thatunderly a successful company. Successful growth companies will share many of the followingcharacteristics:

• Proprietary technology, owned by the company. This acts as a barrier to entry,

preventing other players from coming into the market. That way margins remain high,and there’s less need to discount price.

• Entrepreneurs with a great track record.• Large and growing potential market for the product or service. Typically with a forecast,

the demand curve will start off slowly as the product or serviceestablshes itself as“needed” by its target market. Early versions may be slower sellers, and the companyhas to adjust its operating cost base in order to fulfil growing demand. Here’ workingcapital pressures can be at their greatest.

• Good potential and sustainable margins. This can be through ownership of IP or

proprietary know ‐how or through the organisation always remaining innovative and onthe cutting edge of technology

• Proven market need for the product.• A sustainable competitive advantage with high barriers to entry for potential

competitors.

8/14/2019 Planning to Succeed - The Definitive eGuide for Building Company Financial Forecasts Mark Ostryn DRAFT 180708

http://slidepdf.com/reader/full/planning-to-succeed-the-definitive-eguide-for-building-company-financial 10/94

8/14/2019 Planning to Succeed - The Definitive eGuide for Building Company Financial Forecasts Mark Ostryn DRAFT 180708

http://slidepdf.com/reader/full/planning-to-succeed-the-definitive-eguide-for-building-company-financial 11/94

© 200grantegeneri

June 1,2008

11 | P a

8. Knowledge 20d. Contact Mark

financial inform

An interapply yo

2. 3

Followin

• D

• Hb

• H• D

p• D

n

FORE

e

0 Pty Ltd. Pleasestryn 02 8005 12tion that does no

rsting exerr industry

AKING FO

g in from thi

o you knowonths?

ave you esteyond to th

ave you set

o you haveriorities and

oes your mext financia

ASTING, FI

do not reproduce40 http://www.kt constitute finan

ise, prior too the Five F

RECASTIN

s, ask yours

how marke

ablished yoe next three

financial ta

a method f financial ta

nagementl year, and

ANCING &

without prior pernowledge2020.coial advice

crunchingorces frame

EFFECTI

elf the follo

tplace tren

r company’to five yea

gets for the

r measurinrgets?

eam knowhat they n

FAST TRAC

mission, which wim The above tex

he numberwork.

E

ing:

s will affect

s goals ands?

next financ

your comp

our compaed to do to

ING YOUR

ll usually becontains

for your ow

your comp

priorities fo

ial year?

any’s perfo

ny’s goals aachieve the

USINESS G

n company

ny over th

r the next fi

mance agai

d financialm?

OWTH

orecast is t

next 12 to

nancial year

nst your go

targets for

18

, and

ls,

he

8/14/2019 Planning to Succeed - The Definitive eGuide for Building Company Financial Forecasts Mark Ostryn DRAFT 180708

http://slidepdf.com/reader/full/planning-to-succeed-the-definitive-eguide-for-building-company-financial 12/94

June 1,2008

FORECASTING, FINANCING & FAST TRACKING YOUR BUSINESS GROWTH

12 | P a g e

© 2008. Knowledge 2020 Pty Ltd. Please do not reproduce without prior permission, which will usually begranted. Contact Mark Ostryn 02 8005 1240 http://www.knowledge2020.com The above text containsgeneric financial information that does not constitute financial advice

"Planning differs between budgeting and forecasting in intent. While the budget is used tocontrol, the forecast is used to predict, the plan sets out desired outcomes and expectationsusually over a longer ‐term period. In essence plans are used to affect change." PA ConsultingGroup

There are several major steps to ensure that the forecasting approach is effective and that theresults are credible:

Forecasts imply a plan so your team should be familiar at least with the aims of their ownfunctional or strategic area. Issues such as confidentiality which may preclude full opennessshould be ironed out prior to a session.

Parameters and assumptions such as the size of the market, major production or productchanges, expected sales growth, exchange rates and so on should be set early and disseminateduniformly to form the basis of the plan.

The sales budget should be the first part to be tackled, as it reflects the economic andcompetitive forecasts and shapes all of the other component parts of the budget. All otherbudgets should be developed consistently with the sales volumes. Manufacturing production

targets, stock levels and product support are all dependent.Once the forecast has shaped up, your cash flow forecast is needed to assess affordability. Thiswill ensure that the forecast when finalised is consistent with broad financial parameters anddoes not, for example, assume unrealistic borrowing requirements.

Effective forecasting requires good communications throughout your organisation. Thebudgeting component may move up and down the organisation and sanity checks betweensenior managers of the various divisions may be required before all changes are agreed.

Once agreed, the final figures need to be reviewed and confirmed that at a corporate level thereturn on assets / investment is sufficiently high. If not, consideration needs to be given tocutting costs, selling more or increasing efficiency.

2.4 UNDERSTANDIN G CUSTOMERS

8/14/2019 Planning to Succeed - The Definitive eGuide for Building Company Financial Forecasts Mark Ostryn DRAFT 180708

http://slidepdf.com/reader/full/planning-to-succeed-the-definitive-eguide-for-building-company-financial 13/94

June 1,2008

FORECASTING, FINANCING & FAST TRACKING YOUR BUSINESS GROWTH

13 | P a g e

© 2008. Knowledge 2020 Pty Ltd. Please do not reproduce without prior permission, which will usually begranted. Contact Mark Ostryn 02 8005 1240 http://www.knowledge2020.com The above text containsgeneric financial information that does not constitute financial advice

An important aspect of forecasting is in understanding the makeup of customers who purchase

your products. One key issue for planning is – are they profitable? Consider the types of products they purchases and they services that they may require with them. Consider also theimplications of negotiating a volume deal over time with a large company.

Will the discounted price, plus all of the free priority support and service offering they mayrequire, make Big Complany overall a viable customer.

And what if Big Company doesn’t renew or repurchase in the future. Might you have lost thefocus or even the contact of smaller customer companies?

2.4.1 MARKET SEGMENTATION

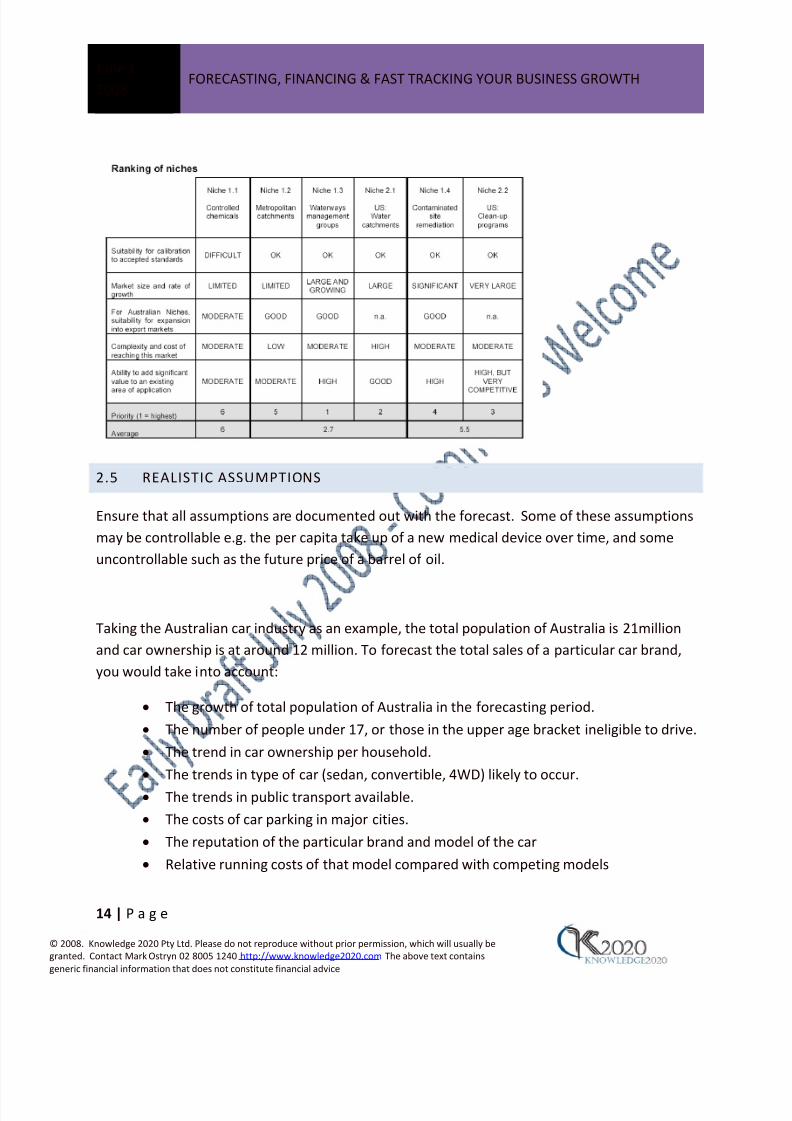

Importantly, you will also need to consider what customers you effectively wish to target.Some target markets can be addressed more profitably than others. As a general rule, you cansegment your market by dividing up your total market into a series of niches, and reviewingeach niche (below) in order to rank the priority levels that you will address those markets.Some niches may never be cost efffective, as it will cost you more to service them than therevenues you can expect from them.

Take the potential markets for a product such as a device to test water quality. Management

and advisors have determined that given limited personnel , promotional; budget and R&Dfunds, it would be best to concentrate on two specific niches (1.3 and 2.1) initally, beforeattempting to grab the woder market.

8/14/2019 Planning to Succeed - The Definitive eGuide for Building Company Financial Forecasts Mark Ostryn DRAFT 180708

http://slidepdf.com/reader/full/planning-to-succeed-the-definitive-eguide-for-building-company-financial 14/94

June 1,2008

FORECASTING, FINANCING & FAST TRACKING YOUR BUSINESS GROWTH

14 | P a g e

© 2008. Knowledge 2020 Pty Ltd. Please do not reproduce without prior permission, which will usually begranted. Contact Mark Ostryn 02 8005 1240 http://www.knowledge2020.com The above text containsgeneric financial information that does not constitute financial advice

2.5 REALISTIC ASSUMPTIONS

Ensure that all assumptions are documented out with the forecast. Some of these assumptionsmay be controllable e.g. the per capita take up of a new medical device over time, and someuncontrollable such as the future price of a barrel of oil.

Taking the Australian car industry as an example, the total population of Australia is 21millionand car ownership is at around 12 million. To forecast the total sales of a particular car brand,you would take into account:

• The growth of total population of Australia in the forecasting period.• The number of people under 17, or those in the upper age bracket ineligible to drive.• The trend in car ownership per household.• The trends in type of car (sedan, convertible, 4WD) likely to occur.• The trends in public transport available.• The costs of car parking in major cities.• The reputation of the particular brand and model of the car• Relative running costs of that model compared with competing models

8/14/2019 Planning to Succeed - The Definitive eGuide for Building Company Financial Forecasts Mark Ostryn DRAFT 180708

http://slidepdf.com/reader/full/planning-to-succeed-the-definitive-eguide-for-building-company-financial 15/94

June 1,2008

FORECASTING, FINANCING & FAST TRACKING YOUR BUSINESS GROWTH

15 | P a g e

© 2008. Knowledge 2020 Pty Ltd. Please do not reproduce without prior permission, which will usually begranted. Contact Mark Ostryn 02 8005 1240 http://www.knowledge2020.com The above text containsgeneric financial information that does not constitute financial advice

And a whole host of other factors.

Thus key determinants may be based on actual results from you or from companies of a similarsize in a similar industry.

2.6 GETTING STARTED WITH YOUR FORECAST

Before you calculate and type in your first numbers, you have to consider a series of issuespertaining to your forecast. These include:

CUSTOM SOFTWARE OR EXCEL SPREADSHEET?

The market for purpose built financial software is expanding, both as downloadable software orsoftware ‐as‐a‐service, where you log on to a provider via an internet connection. Amongstspreadsheets, typically Excel(R) based, you may choose to build your own from scratch (with itsinherent time consuming challenges) or purchase ready made forecasting spreadsheets. Themerits and pitfalls of each option call for another booklet worth of discussion!

TIME SPAN OF FORECAST

How long do you want to forecast forward for (in years)? This answer will depend on what youwant from your forecast. If you want to do a discounted cash flow for a valuation, or if you

want to track the longer term performance of return on your assets, you’ll probably want to doat least five years. Conversely, if your concern is running out of money and you want to trackyour end of month, or even end of week bank balance, you’ll need to focus on one year or less.

LENGTH OF PERIOD

When you’ve decided how many months or years out yourwish to forecast, consider then, anideal number of columns that are useful for your business and are not time consuming orunecessary for you to fill in. A 60 column spreadsheet (monthly forecast for five years) isuncessaryily large , unwieldy to view on your screen and the monthly figures will likely becomemeaningless as your move toward the distant future.

COMPANY STRCUTURE

8/14/2019 Planning to Succeed - The Definitive eGuide for Building Company Financial Forecasts Mark Ostryn DRAFT 180708

http://slidepdf.com/reader/full/planning-to-succeed-the-definitive-eguide-for-building-company-financial 16/94

June 1,2008

FORECASTING, FINANCING & FAST TRACKING YOUR BUSINESS GROWTH

16 | P a g e

© 2008. Knowledge 2020 Pty Ltd. Please do not reproduce without prior permission, which will usually begranted. Contact Mark Ostryn 02 8005 1240 http://www.knowledge2020.com The above text containsgeneric financial information that does not constitute financial advice

How will you sub ‐divide your forecast as to make it meaningful without overburdening yourself

with data? Assume you have 10 product groupos with a total of 700 SKU’s and sales offices in10 territories in Australia and another 20 worldwide. Will you try and incoroprate all of thisdata on a single spreadsheet? Will you ccreate sepatate spreadsheets and feed in the macrodata into a master spreadsheet? How will you make allowance for future products orterritories?

DEALING WITH COMPLEXITY.

To produce a thorough forecasting model may be much more complex that you will have giveallowance to. Consider some of the following challenges:

• The phasing in of receipt and payment of Sales Taxes such as GST abnd their impact oncash flow.

• Taking account of the time span between receiving an order, completion, delivery,invoicing and payment for the goods and services.

• The capacity to produce meaningful working capital estimates when so many variableshave to be factored in.

• Applying deprecaition and amortisation estimates to tanglibe and intangible assets.

HISTORICAL DATA

You’ll need to have an up to date set of financial statements with sufficicently detailedbackground information behind them to get started. The key detail may also relate to trends insales across product lines and seasonal fluctuations. Details of this data may help you detectand programme in growth trends. You’ll also need to know the detail behind your currentstatus of payables, receivables, loans and other balance sheet items, as they will form a part of your near term forecast.

Also you will need to factor out (or in) the following:

• Historical items of income or expense that were unusual, non recurring or unlikely tohave any influence within the forecasting period.

• Revenue that was derived from assets no longer operating within the company.

INTEGRATION WITH YOUR ACCOUNTING SOFTWARE

8/14/2019 Planning to Succeed - The Definitive eGuide for Building Company Financial Forecasts Mark Ostryn DRAFT 180708

http://slidepdf.com/reader/full/planning-to-succeed-the-definitive-eguide-for-building-company-financial 17/94

June 1,2008

FORECASTING, FINANCING & FAST TRACKING YOUR BUSINESS GROWTH

17 | P a g e

© 2008. Knowledge 2020 Pty Ltd. Please do not reproduce without prior permission, which will usually begranted. Contact Mark Ostryn 02 8005 1240 http://www.knowledge2020.com The above text containsgeneric financial information that does not constitute financial advice

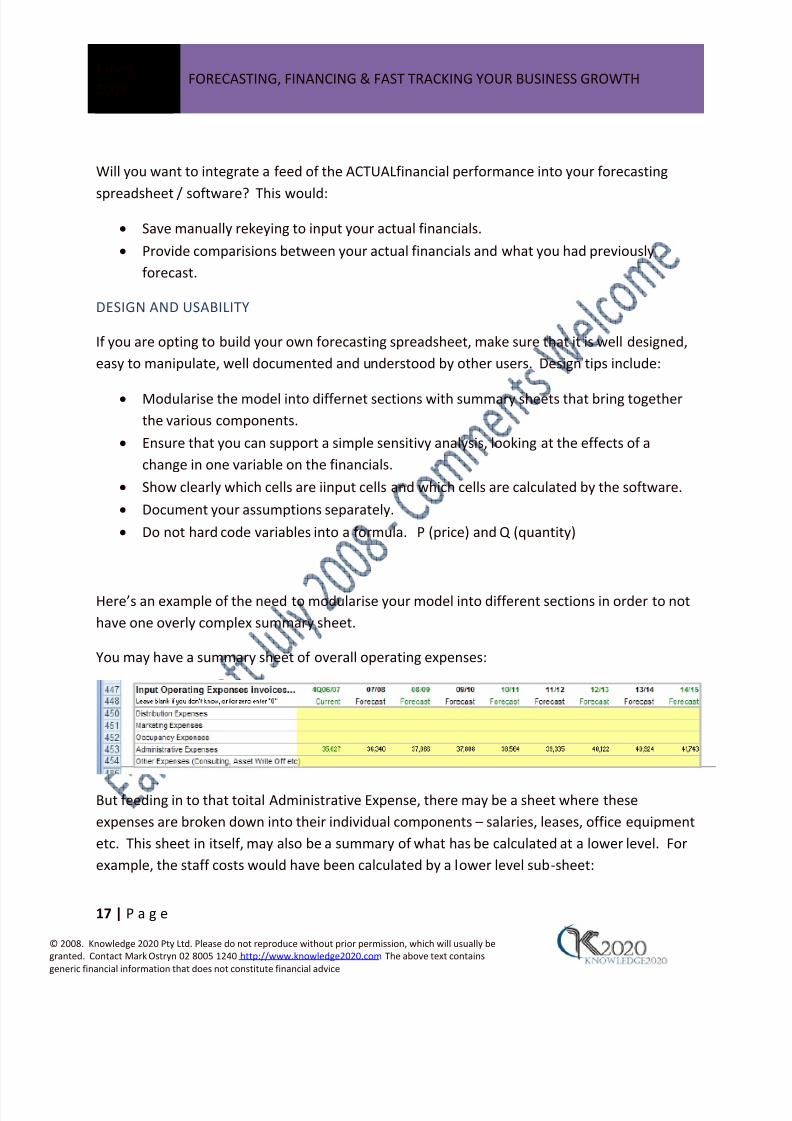

Will you want to integrate a feed of the ACTUALfinancial performance into your forecasting

spreadsheet / software? This would:• Save manually rekeying to input your actual financials.• Provide comparisions between your actual financials and what you had previously

forecast.

DESIGN AND USABILITY

If you are opting to build your own forecasting spreadsheet, make sure that it is well designed,easy to manipulate, well documented and understood by other users. Design tips include:

• Modularise the model into differnet sections with summary sheets that bring togetherthe various components.

• Ensure that you can support a simple sensitivy analysis, looking at the effects of achange in one variable on the financials.

• Show clearly which cells are iinput cells and which cells are calculated by the software.• Document your assumptions separately.• Do not hard code variables into a formula. P (price) and Q (quantity)

Here’s an example of the need to modularise your model into different sections in order to nothave one overly complex summary sheet.

You may have a summary sheet of overall operating expenses:

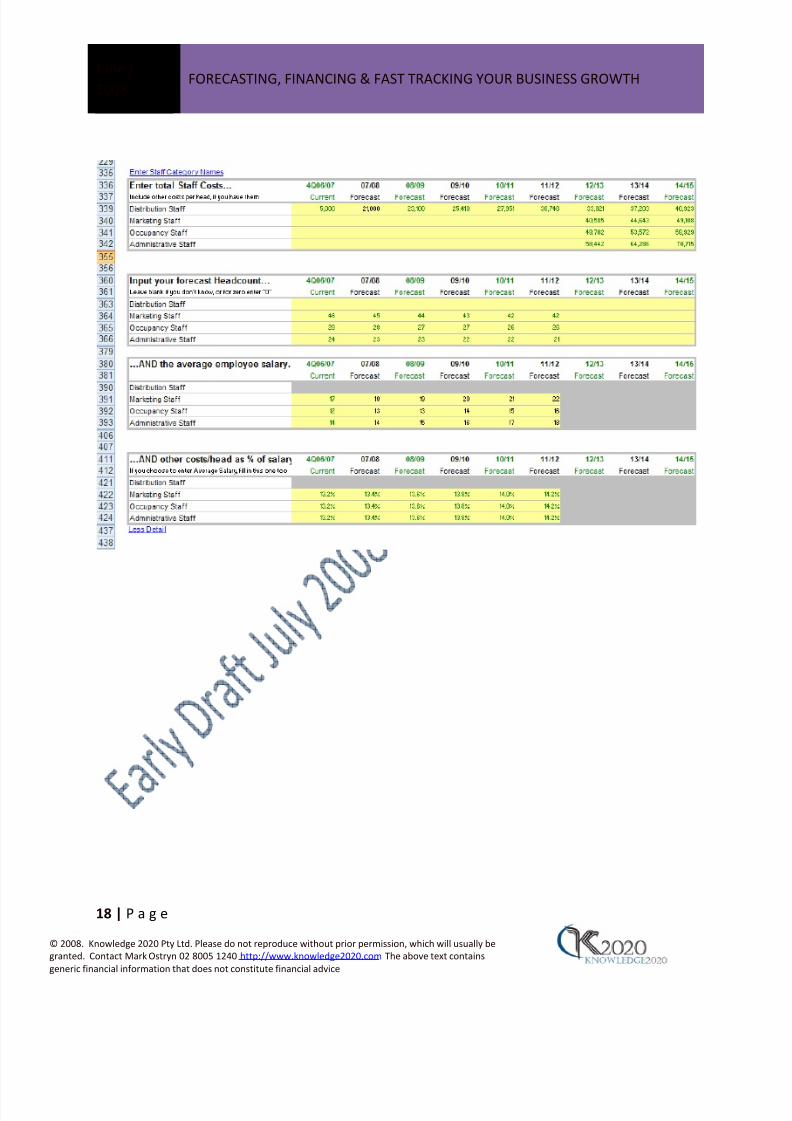

But feeding in to that toital Administrative Expense, there may be a sheet where theseexpenses are broken down into their individual components – salaries, leases, office equipmentetc. This sheet in itself, may also be a summary of what has be calculated at a lower level. Forexample, the staff costs would have been calculated by a lower level sub ‐sheet:

8/14/2019 Planning to Succeed - The Definitive eGuide for Building Company Financial Forecasts Mark Ostryn DRAFT 180708

http://slidepdf.com/reader/full/planning-to-succeed-the-definitive-eguide-for-building-company-financial 18/94

June 1,2008

FORECASTING, FINANCING & FAST TRACKING YOUR BUSINESS GROWTH

18 | P a g e

© 2008. Knowledge 2020 Pty Ltd. Please do not reproduce without prior permission, which will usually begranted. Contact Mark Ostryn 02 8005 1240 http://www.knowledge2020.com The above text containsgeneric financial information that does not constitute financial advice

8/14/2019 Planning to Succeed - The Definitive eGuide for Building Company Financial Forecasts Mark Ostryn DRAFT 180708

http://slidepdf.com/reader/full/planning-to-succeed-the-definitive-eguide-for-building-company-financial 19/94

June 1,2008

FORECASTING, FINANCING & FAST TRACKING YOUR BUSINESS GROWTH

19 | P a g e

© 2008. Knowledge 2020 Pty Ltd. Please do not reproduce without prior permission, which will usually begranted. Contact Mark Ostryn 02 8005 1240 http://www.knowledge2020.com The above text containsgeneric financial information that does not constitute financial advice

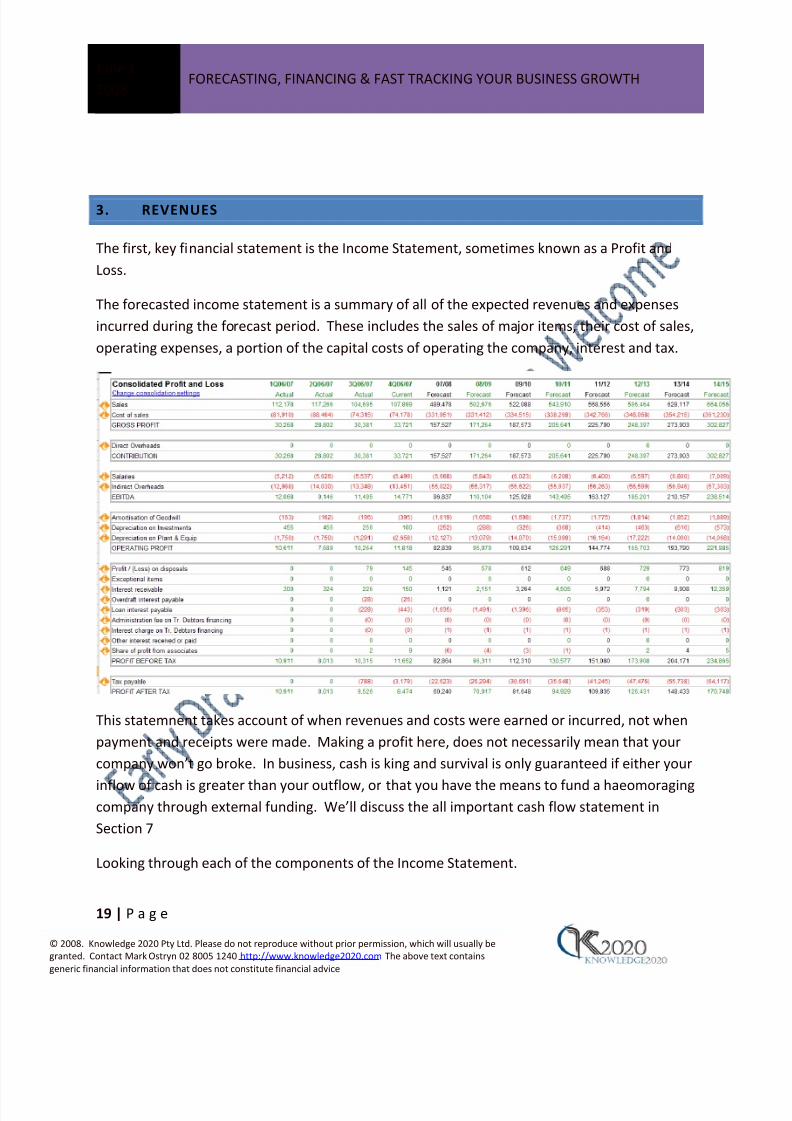

3. REVENUES

The first, key financial statement is the Income Statement, sometimes known as a Profit andLoss.

The forecasted income statement is a summary of all of the expected revenues and expensesincurred during the forecast period. These includes the sales of major items, their cost of sales,operating expenses, a portion of the capital costs of operating the company, interest and tax.

This statemnent takes account of when revenues and costs were earned or incurred, not whenpayment and receipts were made. Making a profit here, does not necessarily mean that yourcompany won’t go broke. In business, cash is king and survival is only guaranteed if either your

inflow of cash is greater than your outflow, or that you have the means to fund a haeomoragingcompany through external funding. We’ll discuss the all important cash flow statement inSection 7

Looking through each of the components of the Income Statement.

8/14/2019 Planning to Succeed - The Definitive eGuide for Building Company Financial Forecasts Mark Ostryn DRAFT 180708

http://slidepdf.com/reader/full/planning-to-succeed-the-definitive-eguide-for-building-company-financial 20/94

June 1,2008

FORECASTING, FINANCING & FAST TRACKING YOUR BUSINESS GROWTH

20 | P a g e

© 2008. Knowledge 2020 Pty Ltd. Please do not reproduce without prior permission, which will usually begranted. Contact Mark Ostryn 02 8005 1240 http://www.knowledge2020.com The above text containsgeneric financial information that does not constitute financial advice

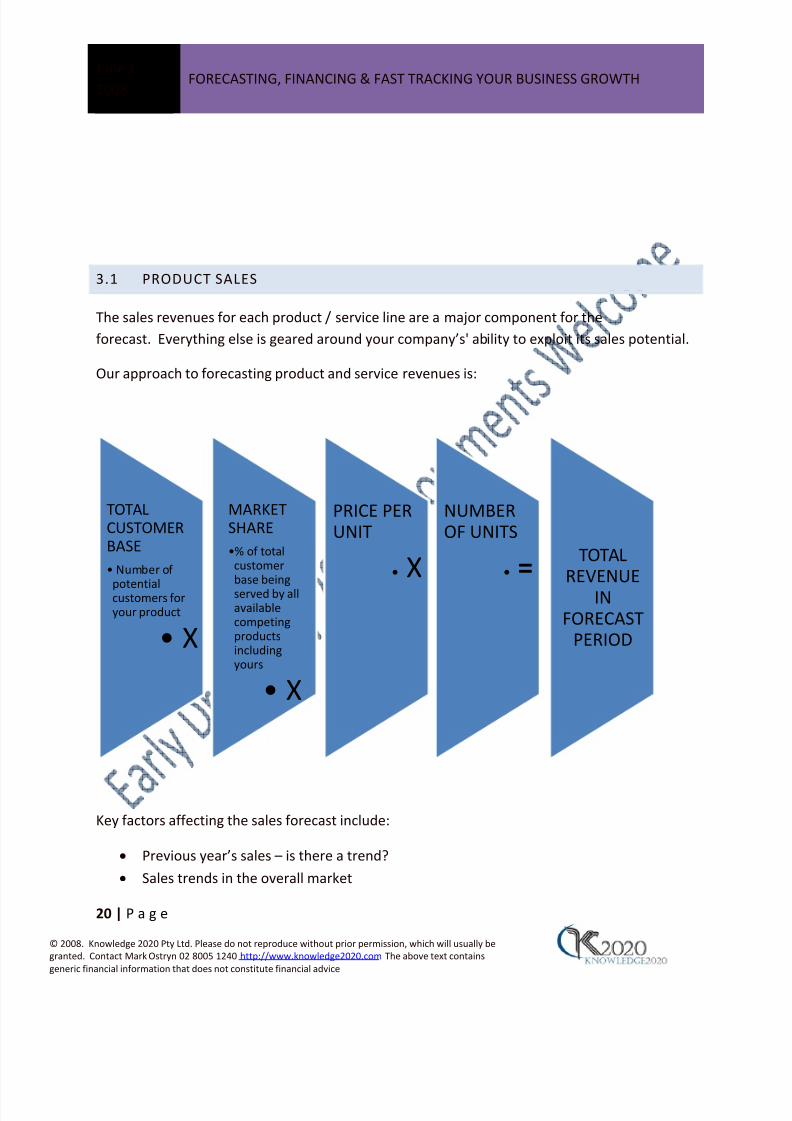

3.1 PRODUCT SALES

The sales revenues for each product / service line are a major component for theforecast. Everything else is geared around your company’s' ability to exploit its sales potential.

Our approach to forecasting product and service revenues is:

Key factors affecting the sales forecast include:

• Previous year’s sales – is there a trend?• Sales trends in the overall market

TOTALCUSTOMERBASE• Number of

potentialcustomers foryour product

• X

MARKETSHARE•% of totalcustomerbase beingserved by allavailablecompetingproductsincludingyours

• X

PRICE PERUNIT

• X TOTALREVENUE

INFORECAST

PERIOD

NUMBEROF UNITS

• =

8/14/2019 Planning to Succeed - The Definitive eGuide for Building Company Financial Forecasts Mark Ostryn DRAFT 180708

http://slidepdf.com/reader/full/planning-to-succeed-the-definitive-eguide-for-building-company-financial 21/94

June 1,2008

FORECASTING, FINANCING & FAST TRACKING YOUR BUSINESS GROWTH

21 | P a g e

© 2008. Knowledge 2020 Pty Ltd. Please do not reproduce without prior permission, which will usually begranted. Contact Mark Ostryn 02 8005 1240 http://www.knowledge2020.com The above text containsgeneric financial information that does not constitute financial advice

• New promotions, sales initiatives or other marketing drives

• New product launches• Overall changes in the economy• Changes in consumer tastes• Seasonal trends – ice cream sales in summer compared to winter• Changes in competitive strategy• Varying competitor scenarios

If you have multiple product lines, services, divisions or geographical locations, you’ll naturallybe forecasting each as a sepatrate line item.It is important to forecast each of the productlines. Consider also what the effects are on sales of one product line on another product line:

• One product may be complementary to another in which case there is a directrelationship between one and the other. As one increases, so does the other.

• Increases in sales for one product may negatively affect the sales of another product• The sales of two lines of product may both increase as a result of outside factors – sales

of gym memberships generally increase at the beginning of the year after people makeNew Year resolutions.

Next, factor in all of the potential revenue streams that could accrue to your company in the

coming years? These may be new revenue streams that you currently do not enjoy, including:

• Existing products into new market• Complementary products• Packaged bundles of product• Upgrade revenues• Support revenues• Training revenues• Service revenues•

Consulting revenues• Licencing revenues

When considering future revenues, it is important to keep a running total of the installed baseof total users of your product or service. They may require service, upgrades or support at any

8/14/2019 Planning to Succeed - The Definitive eGuide for Building Company Financial Forecasts Mark Ostryn DRAFT 180708

http://slidepdf.com/reader/full/planning-to-succeed-the-definitive-eguide-for-building-company-financial 22/94

June 1,2008

FORECASTING, FINANCING & FAST TRACKING YOUR BUSINESS GROWTH

22 | P a g e

© 2008. Knowledge 2020 Pty Ltd. Please do not reproduce without prior permission, which will usually begranted. Contact Mark Ostryn 02 8005 1240 http://www.knowledge2020.com The above text containsgeneric financial information that does not constitute financial advice

tiume in the future. They would also be a great propsect for future compoany offerings,

provided they are satisfied with their current products. So• How many people are out using your product (installed base)?• What is the propensity for customers (in % terms of installed base) to seek out

additional products, services or support?• Can you increase the frequency of purchases for each customer? Or, the value of each

purchase made.

Total Revenue is simply price per unit x number of units sold. This can be increased in one of three ways:

• Increasing the number of customers• Increasing the value of each sale• Increasing the value of each sale.

3.2 PRICING

Price is a key business driver and a proper pricing policy can assist growth more than eitherincreases in volume or cost reductions. Depoending on your industry and your company’sstrength within it, you may have the capability to set price. If not, you still may have thecapacity to create your own niche (perhaps through sustasinable product differentiation)inorder to obtain economic profit. The introduction of 3,4, and now 5 bladed shavers haveallowed producers such as Gilette to charge enormous price premiums oin what was once a lowmargin industry.

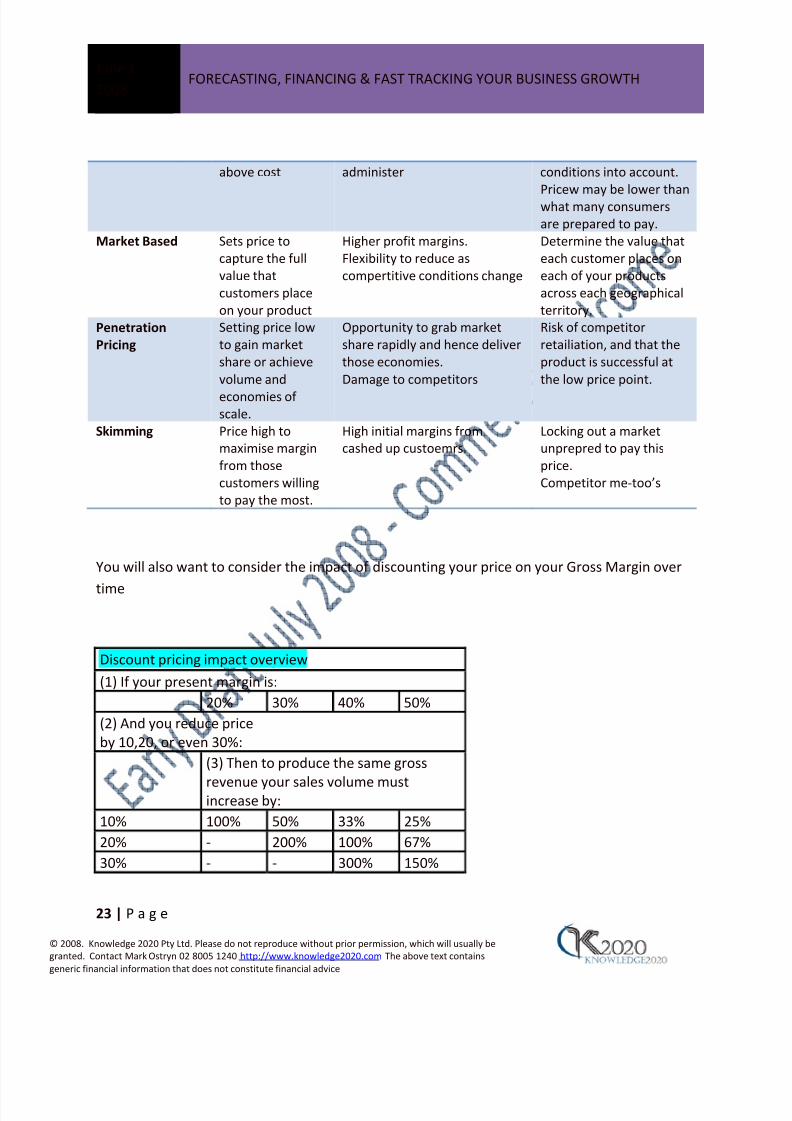

Here are some alternative pricing strategies. Consider which you would want to apply to what

products or services you sell or intend to sell, and how your pricing policy may change overtime:

PRICINGAPPROACH

DESCRIPTION ADVANTAGES DISADVANTAGES

Cost Plus Standard margin Easy to calculate and Doesn’t take market

8/14/2019 Planning to Succeed - The Definitive eGuide for Building Company Financial Forecasts Mark Ostryn DRAFT 180708

http://slidepdf.com/reader/full/planning-to-succeed-the-definitive-eguide-for-building-company-financial 23/94

June 1,2008

FORECASTING, FINANCING & FAST TRACKING YOUR BUSINESS GROWTH

23 | P a g e

© 2008. Knowledge 2020 Pty Ltd. Please do not reproduce without prior permission, which will usually begranted. Contact Mark Ostryn 02 8005 1240 http://www.knowledge2020.com The above text containsgeneric financial information that does not constitute financial advice

above cost administer conditions into account.Pricew may be lower thanwhat many consumersare prepared to pay.

Market Based Sets price tocapture the fullvalue thatcustomers placeon your product

Higher profit margins.Flexibility to reduce ascompertitive conditions change

Determine the value thateach customer places oneach of your productsacross each geographicalterritory.

PenetrationPricing

Setting price lowto gain marketshare or achievevolume andeconomies of scale.

Opportunity to grab marketshare rapidly and hence deliverthose economies.Damage to competitors

Risk of competitorretailiation, and that theproduct is successful atthe low price point.

Skimming Price high tomaximise marginfrom thosecustomers willingto pay the most.

High initial margins fromcashed up custoemrs.

Locking out a marketunprepred to pay thisprice.Competitor me ‐too’s

You will also want to consider the impact of discounting your price on your Gross Margin over

time

Discount pricing impact overview(1) If your present margin is:

20% 30% 40% 50%(2) And you reduce priceby 10,20, or even 30%:

(3) Then to produce the same gross

revenue your sales volume mustincrease by:10% 100% 50% 33% 25%20% ‐ 200% 100% 67%30% ‐ ‐ 300% 150%

8/14/2019 Planning to Succeed - The Definitive eGuide for Building Company Financial Forecasts Mark Ostryn DRAFT 180708

http://slidepdf.com/reader/full/planning-to-succeed-the-definitive-eguide-for-building-company-financial 24/94

June 1,2008

FORECASTING, FINANCING & FAST TRACKING YOUR BUSINESS GROWTH

24 | P a g e

© 2008. Knowledge 2020 Pty Ltd. Please do not reproduce without prior permission, which will usually begranted. Contact Mark Ostryn 02 8005 1240 http://www.knowledge2020.com The above text containsgeneric financial information that does not constitute financial advice

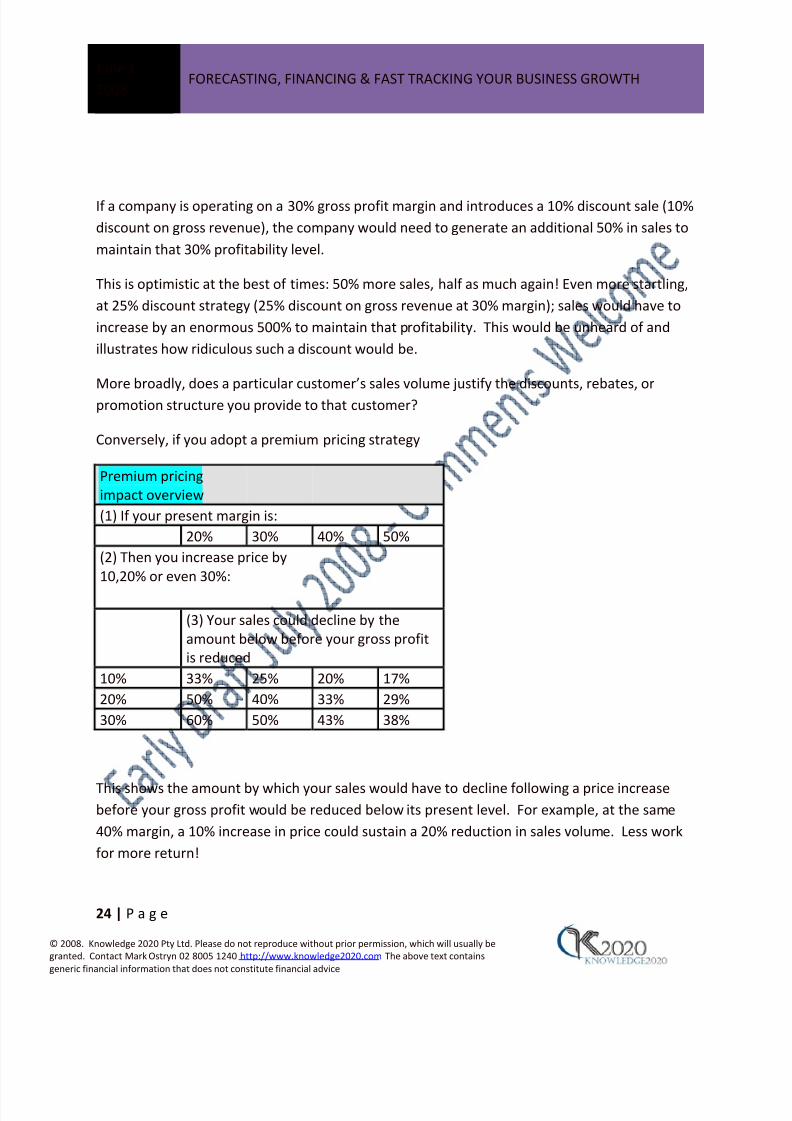

If a company is operating on a 30% gross profit margin and introduces a 10% discount sale (10%discount on gross revenue), the company would need to generate an additional 50% in sales tomaintain that 30% profitability level.

This is optimistic at the best of times: 50% more sales, half as much again! Even more startling,at 25% discount strategy (25% discount on gross revenue at 30% margin); sales would have toincrease by an enormous 500% to maintain that profitability. This would be unheard of andillustrates how ridiculous such a discount would be.

More broadly, does a particular customer’s sales volume justify the discounts, rebates, orpromotion structure you provide to that customer?

Conversely, if you adopt a premium pricing strategy

Premium pricingimpact overview(1) If your present margin is:

20% 30% 40% 50%(2) Then you increase price by10,20% or even 30%:

(3) Your sales could decline by theamount below before your gross profitis reduced

10% 33% 25% 20% 17%20% 50% 40% 33% 29%30% 60% 50% 43% 38%

This shows the amount by which your sales would have to decline following a price increasebefore your gross profit would be reduced below its present level. For example, at the same40% margin, a 10% increase in price could sustain a 20% reduction in sales volume. Less workfor more return!

8/14/2019 Planning to Succeed - The Definitive eGuide for Building Company Financial Forecasts Mark Ostryn DRAFT 180708

http://slidepdf.com/reader/full/planning-to-succeed-the-definitive-eguide-for-building-company-financial 25/94

June 1,2008

FORECASTING, FINANCING & FAST TRACKING YOUR BUSINESS GROWTH

25 | P a g e

© 2008. Knowledge 2020 Pty Ltd. Please do not reproduce without prior permission, which will usually begranted. Contact Mark Ostryn 02 8005 1240 http://www.knowledge2020.com The above text containsgeneric financial information that does not constitute financial advice

Finally, if competitive pressures are forcing you to evaluate your current pricing, consider some

of the following options for offering “a better deal” to certain customers:• Discounts on volume.• Time dependent promotional bonuses.• If selling through channels, marketing allowances and co ‐operative advertising• Alternate payment terms e.g. discount on early payments.• Bundling multiple products.• Money back guarantees

All of these initiatives would need to be included in a forecast.

3.3 GEOGRAPHICA L EXPANSION

New markets may be alluring whether you are considering increasing sales, improvements inoperational cost ‐ effectiveness or new international customers, but your forecasting processneed to rigourusly assess their cost benefit. This is particualrly so in the sales start up phaseswhere it may be expensive to establish a brand and a suitable distribution channel in a marketthat may have little awareness of your products and services.

In short, doesa my international expansion add value to the company or simply just grow mytop line revenue figures?

When cdonsidering expansion the forecast needs to evaluate the prioritisation of countrys (sizeand accessibility) and an entry plan for each including company expansion, acquisition orpartering with a local provider.

When forecasting product revenues, you need to consider and evaluate the following

• Determining the total customer base or market size• Segmenting the market to identify what portion should be targeted by your product or

service• Expected penetration of the product or service into the market segment• Competitive envrionment

8/14/2019 Planning to Succeed - The Definitive eGuide for Building Company Financial Forecasts Mark Ostryn DRAFT 180708

http://slidepdf.com/reader/full/planning-to-succeed-the-definitive-eguide-for-building-company-financial 26/94

8/14/2019 Planning to Succeed - The Definitive eGuide for Building Company Financial Forecasts Mark Ostryn DRAFT 180708

http://slidepdf.com/reader/full/planning-to-succeed-the-definitive-eguide-for-building-company-financial 27/94

June 1,2008

FORECASTING, FINANCING & FAST TRACKING YOUR BUSINESS GROWTH

27 | P a g e

© 2008. Knowledge 2020 Pty Ltd. Please do not reproduce without prior permission, which will usually begranted. Contact Mark Ostryn 02 8005 1240 http://www.knowledge2020.com The above text containsgeneric financial information that does not constitute financial advice

• Are there obsolescence costs that will created for the customers current way of doing

things?

Once the new product has launched:

• How quickly will sales ramp up?• What are the costs of bringing this product to market?• How much will it cost to achieve adequate exposure in the market?

The commercial viability for any new product needs to ber established early in the new productdevelopment programme. Aside from the bottom line financial impact, consider the following:

• Will it encourage customers to buy other products as well?• Can the development act as a catalyst for improvements in overall manufacturing

efficiency and quality?• Can new intellectual property be generated or new manufacturing techniques

exploited?

3.5 BUSINESS SEGMENTS

Your forecast should break down product and service revenue figures into appropriate businessand geographical segments:

Geographical Segment ‐ This will be segmented by geographical territory, either within acountry (Northern Division, Southern Division) or internally (Americas, Europe)

Business Segments ‐ Distinguishable component of an enterprise providing a product or servicethat faces different risks from other businesses within the enterprise.

3.6 ALLIANCES, PARTNERSHIPS, LICENSING AND DISTRIBUTION AGREEMENTS

There are a wide range of allainces that can be formed using your unique know how, location,technology, intellectual property. These allainces can help you increase your revenues andproftabilty without the risk that “going direct” would assume. Broadly speaking such allainces

8/14/2019 Planning to Succeed - The Definitive eGuide for Building Company Financial Forecasts Mark Ostryn DRAFT 180708

http://slidepdf.com/reader/full/planning-to-succeed-the-definitive-eguide-for-building-company-financial 28/94

June 1,2008

FORECASTING, FINANCING & FAST TRACKING YOUR BUSINESS GROWTH

28 | P a g e

© 2008. Knowledge 2020 Pty Ltd. Please do not reproduce without prior permission, which will usually begranted. Contact Mark Ostryn 02 8005 1240 http://www.knowledge2020.com The above text containsgeneric financial information that does not constitute financial advice

and partnerships incude: joint ventures, marketing alliances, licensing arrangements,

selling/distribution agreements, channel partnerships and software agreements.

These alliances and partnerships may give you a competitive advantage, create barriers toentryand help you reach customers more efficiently.

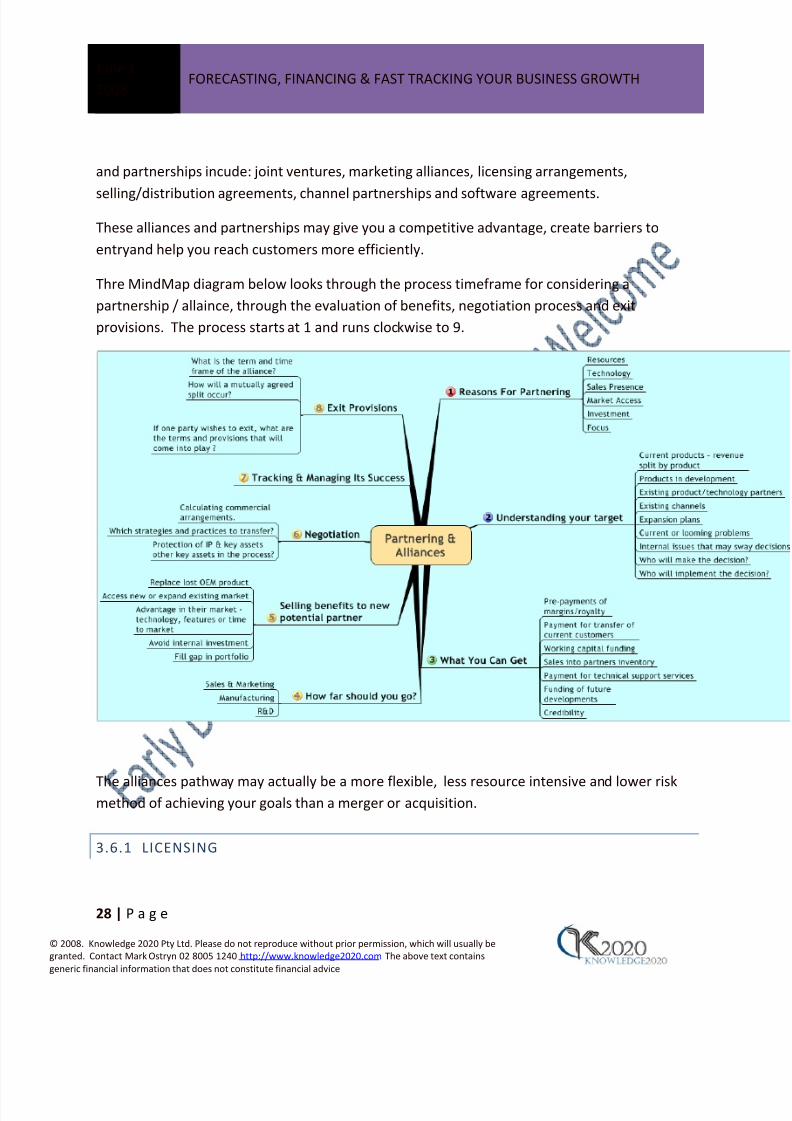

Thre MindMap diagram below looks through the process timeframe for considering apartnership / allaince, through the evaluation of benefits, negotiation process and exitprovisions. The process starts at 1 and runs clockwise to 9.

The alliances pathway may actually be a more flexible, less resource intensive and lower riskmethod of achieving your goals than a merger or acquisition.

3.6.1 LICENSING

8/14/2019 Planning to Succeed - The Definitive eGuide for Building Company Financial Forecasts Mark Ostryn DRAFT 180708

http://slidepdf.com/reader/full/planning-to-succeed-the-definitive-eguide-for-building-company-financial 29/94

June 1,2008

FORECASTING, FINANCING & FAST TRACKING YOUR BUSINESS GROWTH

29 | P a g e

© 2008. Knowledge 2020 Pty Ltd. Please do not reproduce without prior permission, which will usually begranted. Contact Mark Ostryn 02 8005 1240 http://www.knowledge2020.com The above text containsgeneric financial information that does not constitute financial advice

Licensing is the capacity to exploit another parties IP, perocess or technology in return for

agreed fees.

Licensing can generate a revenue stream by giving permission to others to sell your products orintegrate your technology or know how into their products orservices.

This revenue stream may potentially be lower risk as many of the costs of market entry may beremoved. In addition, the licencee may incorporate their own know ‐how into the final solutionthat may be well targeted at their customer base.

Licensing works by transferring technology to a licensee and fees can be generated throughroyalties, management assistance etc. These royalties can be either upfront payments, runningroyalties or a combination of both.

Can negotiate multiple non ‐ exclusive licenses, minimum guaranteed license revenues

From a business and forecasting perspective, the following needs to be considered:

• Is the license exclusive or nonexclusive?• How long should the license be granted for?• What is the size of the market and market penetration?• Without the license, what is the investment required for manufacture?• Does the market already exist or must it be created?• Without the license, how much will it cost to establish sales channels?• What is the prospective return on investment?• What are the nature and extent of competition to be expected?• What is the market life for the licensed technology?• What kind of lead time will the license afford?• What technical help, know ‐how, or show ‐how is provided?• Without the license, what would it cost to “reinvent the wheel”?• Will we create a new market or reduce production costs?• Are profit margins in the industry sufficiently high?• How do we wish to get paid?• Can the licencee sub ‐license?

Finally, there’s an often quoted 25%rule of thumb for licensing revenue. It’s 25% to licensor,75% to licensee of an expected profit margin. Probably best used as a starting point fornegotiations!

8/14/2019 Planning to Succeed - The Definitive eGuide for Building Company Financial Forecasts Mark Ostryn DRAFT 180708

http://slidepdf.com/reader/full/planning-to-succeed-the-definitive-eguide-for-building-company-financial 30/94

June 1,2008

FORECASTING, FINANCING & FAST TRACKING YOUR BUSINESS GROWTH

30 | P a g e

© 2008. Knowledge 2020 Pty Ltd. Please do not reproduce without prior permission, which will usually begranted. Contact Mark Ostryn 02 8005 1240 http://www.knowledge2020.com The above text containsgeneric financial information that does not constitute financial advice

3.6.2 STRATEGIC ALLIANCES

The world doesn’t come looking for a better mousetrap, and the economy is a machine thatinvolves companies acting together as well as competiting. It’s very difficult to build a whollyself sufficient company, so it makes sense to assemble a group of companies together that forma sustainable force.

Alliance opportuniies enable:

• INNOVATION: Generate new product ideas and acelerate commcialisation• EXTENSION: enable your company to enter new channels and reach new custom

segments• GEOGRAPHIC EXPANSION: Enable your company to entedr new markets or improve

existing international or interstate operations using the alliance partners local assets• PERFORMANCE IMPROVEMENT: Enable improvements in efficiency and lower

operating costs and capital requirments through outsourcing.

3.6.3 DISTRIBUTION CHANNELS

It’s easy to see why a food manufacturer would use wholesalers or supermnarkets to sell theirproducts, but a component of your forecast is to evaluate whether your financial interests arebest served by using a channel strategy. If you wre comparing product revenues and costs byusing direct sales versus via indirect, here are some of the key considerations:

• LOWER COST: Using resellers can save on the costs of a direct salesforce whileextending the range of customers you are effectively speaking to. Simuilar you maysavbe on warehouse management, inventory management and logistics by taking upspace in a distributors facilties rather than building your own.

• INTEGRATION WITH OTHER PRODUCTS: Your products may require intengration orbundling with other products in order to provide a complete solution to a custoemrsrequirements. In this instance you may require specialist resellers with integration skillsto sell complementary technology and effectively support and advise customers.

8/14/2019 Planning to Succeed - The Definitive eGuide for Building Company Financial Forecasts Mark Ostryn DRAFT 180708

http://slidepdf.com/reader/full/planning-to-succeed-the-definitive-eguide-for-building-company-financial 31/94

June 1,2008

FORECASTING, FINANCING & FAST TRACKING YOUR BUSINESS GROWTH

31 | P a g e

© 2008. Knowledge 2020 Pty Ltd. Please do not reproduce without prior permission, which will usually begranted. Contact Mark Ostryn 02 8005 1240 http://www.knowledge2020.com The above text containsgeneric financial information that does not constitute financial advice

• CUSTOMER REACH: As your business grows you may require resellers to reacha diverse

range of customers. If your product addresses many market segments and requiresgeographical coverage then customer convenience in accessing a reseller becomes akey criteria

If you are considering usinf non ‐direct sales, remember to evaluate a range of options, thatultimately will depend on your own industry structure:

Master distributors

Local distributors

Value added resellers

eSelling via the web (auction sites, catalogues etc)

Integrators

3.7 FRANCHISING

With brand name backing and reliable systems in place, it’s no surprise that franchising is oneof the fastest growing forms of business strcutre in Australia. In indsutries from fast food toaccountancy advice, franchising removes much of the need for promotiuonal expenditure tobrand build and gives clients the reassurance that they can trust the products and services of the franchisee.

Franchising works best for businesses that have a good past sales and profit history, can beeasily replicated in new territories, are easy and inexpensive to operate and have good brandname recognition.

3.7.1 BEING A FRANCHISOR

The "franchisor" authorizes the proven methods and trademarks of their business to the"franchisee" for a fee and a usually a percentage of gross monthly sales. In return for this,

8/14/2019 Planning to Succeed - The Definitive eGuide for Building Company Financial Forecasts Mark Ostryn DRAFT 180708

http://slidepdf.com/reader/full/planning-to-succeed-the-definitive-eguide-for-building-company-financial 32/94

June 1,2008

FORECASTING, FINANCING & FAST TRACKING YOUR BUSINESS GROWTH

32 | P a g e

© 2008. Knowledge 2020 Pty Ltd. Please do not reproduce without prior permission, which will usually begranted. Contact Mark Ostryn 02 8005 1240 http://www.knowledge2020.com The above text containsgeneric financial information that does not constitute financial advice

support systems, advertising, training and other benefits will be made available to the

franchisee.

The key financial benfits of franchising your operation are:

• Once you have a methodology and a strcutre in place,,its easier to open “cookie cutter”type operations through franchisees than doing it yourself.

• Costas are substantially lower as the franchisees upfront fees will defray much of therisk.

• The franchisee may have much greater exerpoeice dealing with their local market.• Greaer motivation on the franchisees behalf to make it successful than ifd you were to

do it through your own employees.

The key downsides of franchising your operations are:

• There may be some loss of control, as it may be more difficult to manage and get thingsdone through an individual franchisee than through a staff member.

• Getting the price right. Price it too highrelative to the franchisees income streams andit’s a permanent demotivator to the franchisee. Price it too low, and you’ve left valueon the table.

• Potential for conflicts: An incompetent franchisee can damage the customers goodwillfor the brand by providing inferior goods and services

The key issues and controls you need to put into place are:

Length of agreement – could be from five (sufficnet time to realise returns from the initialoutlay and the lean start up period) to twenty years.

What would trigger an early termination of a contract?

What is the extent of a territory?

Exclusive or non exclusive?

8/14/2019 Planning to Succeed - The Definitive eGuide for Building Company Financial Forecasts Mark Ostryn DRAFT 180708

http://slidepdf.com/reader/full/planning-to-succeed-the-definitive-eguide-for-building-company-financial 33/94

June 1,2008

FORECASTING, FINANCING & FAST TRACKING YOUR BUSINESS GROWTH

33 | P a g e

© 2008. Knowledge 2020 Pty Ltd. Please do not reproduce without prior permission, which will usually begranted. Contact Mark Ostryn 02 8005 1240 http://www.knowledge2020.com The above text containsgeneric financial information that does not constitute financial advice

3.7.2 BEING A FRANCHISEE

The key financial benfits of purchasing a franchise are:

• You have likely to have a recognised brand and an exclusive territory such that you cango to market and earn postitive cash flows comparatively quickly.

The key downsides of being a franchisee are:

• An incompetent franchisor can destroy their franchisees by not promoting the brand

adequately or being too aggressive for profits.

3.8 PROJECT MANAGEMENT

Much of the emphasis of this book so far is on the production and sale of tangible goods andservices. If your company’s busiuness is based on the successful completion of specific projectsincludinga whole series of differtent financial and forecasting considerations come into play.

Your scucess id managed a set of resources – people and expertise, materials, money in orderto achieve the objectives of a project. The goal is profit, the classic constraints are time, quality

and budget.

Your initial analysis determines the price you will charge for the project based on an estimate of the costs involved. From a financial viewpoint the key risk is that the project timescales or costsoverrun, and this can be partially mitigated by:

• Thorough pre ‐planning and consideration of each variable.• A clear understadning and alignment with the customers requirements.• Taking account of all potential risks and having a strategy in place to address them.• Having flexibility in the contract to be able to pass on unforseen challenges to the

customer.• Effective people, process and budgetary management throughout the project phases,

including sub ‐contractors.

To ensure that the project remains on cost and ontime, consider the following:

8/14/2019 Planning to Succeed - The Definitive eGuide for Building Company Financial Forecasts Mark Ostryn DRAFT 180708

http://slidepdf.com/reader/full/planning-to-succeed-the-definitive-eguide-for-building-company-financial 34/94

June 1,2008

FORECASTING, FINANCING & FAST TRACKING YOUR BUSINESS GROWTH

34 | P a g e

© 2008. Knowledge 2020 Pty Ltd. Please do not reproduce without prior permission, which will usually begranted. Contact Mark Ostryn 02 8005 1240 http://www.knowledge2020.com The above text containsgeneric financial information that does not constitute financial advice

• Ewha tis the critical path and what are the interrelationsips and interactions and

interdependencies between the resources?• What key events, milestones, progress evaluations and critical activities been identified?• Has time been allocated for quality, customer and stakeholder involvement?• How has time contingency been incorporated into the plan?• How thoroughly have target or actual project costs been clearly identified and

documented?• Does the project cost estimation involve cost related risks and how are these managed?• Is the project budget consistent with the project requirements, assumptions, risks and

contingencies? How are the project costs managed to ensure that the project is

completed within budget?• Is there a satisfactory process for accounting of project purchasing and other

expenditure? Has this purchasing process been documented?• Can you identify the root causes for budget variances, both favourable and

unfavourable? Is this revciewed?• How has cost contingency been incorporated into the plan?

3.9 CONSULTANCY

There’s a lot of cynicism about Consultants, but good ones, well briefed can do much to helpcompanies evaluate their market opportunities, strategies and tactics.

3.10 OTHER INCOME

There are a wide rang eof other items that can fall into the “Other Income” category of yourPfoit and loss. These can range from Grants from governments of private bodies, donations oreven the proceeds of your intellectual property. Some examples follow, but you’ll haVE your

own

3.10.1 GRANTS & FINANCIAL ASSISTANCE

Financial asssitance programmes at a federal (AusIndustry), state and export body (Austrade)level can assist with grants and loans and tax offsets.

8/14/2019 Planning to Succeed - The Definitive eGuide for Building Company Financial Forecasts Mark Ostryn DRAFT 180708

http://slidepdf.com/reader/full/planning-to-succeed-the-definitive-eguide-for-building-company-financial 35/94

June 1,2008

FORECASTING, FINANCING & FAST TRACKING YOUR BUSINESS GROWTH

35 | P a g e

© 2008. Knowledge 2020 Pty Ltd. Please do not reproduce without prior permission, which will usually begranted. Contact Mark Ostryn 02 8005 1240 http://www.knowledge2020.com The above text containsgeneric financial information that does not constitute financial advice

Examples include:

• AusIndustry’s COMET support program gives financial support to innovative early stagecompanies, their R&D Tax Concession prgorammes allows tax concession of up to 125%of expedniture incurred on R&D and they offers specific industry support in areas suchas Tourism, Automoativer, Biofuels, Climiate change and green based initiatives.

• EFIC (Export Finance & Insurance Corporation) is Australia’s export cr3edit agency offersexport guarantees and direct loans.

• State governments offer a variety of programmes for SME’s. In NSW, for example, theDeaprtment of State & Regional Development (DSRD) provides assistance withcommercialising R&D, regional relocation incentives, export incentives and payroll taxrebates.

• Austrade, Australia’s export authority provides an Export Market Development Grant(EMDG), as a rebate on the proprtion of total expenses incurred on eligible exportpromotion activities.

3.10.2 INTELLECTUAL PROPERTY INCOME

Obtaining a royalty stream from yourIntellectual Property can, once the IP has been developed,protected and marketed, be one of the significant income streams as it goes straight to the

bottom line. (IBM for example have over $1 billion dollars of income annually accruing fromtheir past IP).

Here’s a MindMap checklist of the considerations when embarking on a ruote to market thatinvolves the devlopment and licencing of IP.

8/14/2019 Planning to Succeed - The Definitive eGuide for Building Company Financial Forecasts Mark Ostryn DRAFT 180708

http://slidepdf.com/reader/full/planning-to-succeed-the-definitive-eguide-for-building-company-financial 36/94

8/14/2019 Planning to Succeed - The Definitive eGuide for Building Company Financial Forecasts Mark Ostryn DRAFT 180708

http://slidepdf.com/reader/full/planning-to-succeed-the-definitive-eguide-for-building-company-financial 37/94

June 1,2008

FORECASTING, FINANCING & FAST TRACKING YOUR BUSINESS GROWTH

37 | P a g e

© 2008. Knowledge 2020 Pty Ltd. Please do not reproduce without prior permission, which will usually begranted. Contact Mark Ostryn 02 8005 1240 http://www.knowledge2020.com The above text containsgeneric financial information that does not constitute financial advice

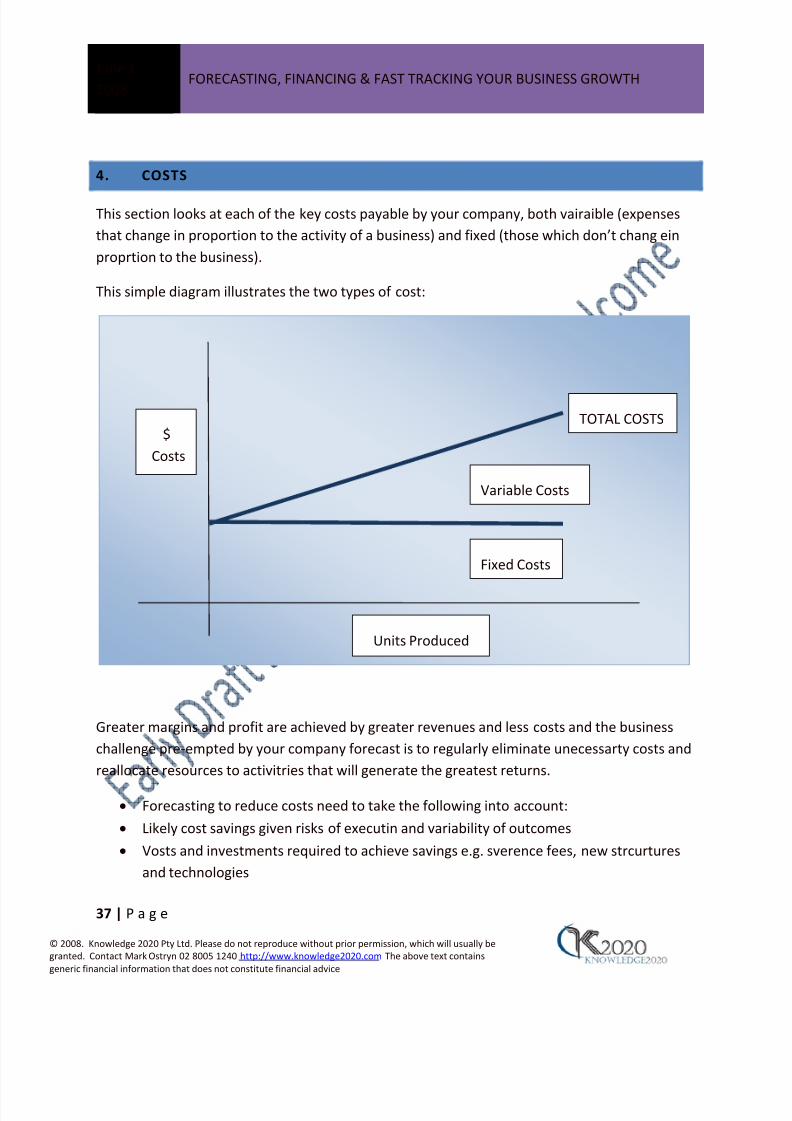

4. COSTS

This section looks at each of the key costs payable by your company, both vairaible (expensesthat change in proportion to the activity of a business) and fixed (those which don’t chang einproprtion to the business).

This simple diagram illustrates the two types of cost:

Greater margins and profit are achieved by greater revenues and less costs and the businesschallenge pre ‐empted by your company forecast is to regularly eliminate unecessarty costs andreallocate resources to activitries that will generate the greatest returns.

• Forecasting to reduce costs need to take the following into account:• Likely cost savings given risks of executin and variability of outcomes• Vosts and investments required to achieve savings e.g. sverence fees, new strcurtures

and technologies

Fixed Costs

Variable Costs

TOTAL COSTS

Units Produced

$Costs

8/14/2019 Planning to Succeed - The Definitive eGuide for Building Company Financial Forecasts Mark Ostryn DRAFT 180708

http://slidepdf.com/reader/full/planning-to-succeed-the-definitive-eguide-for-building-company-financial 38/94

June 1,2008

FORECASTING, FINANCING & FAST TRACKING YOUR BUSINESS GROWTH

38 | P a g e

© 2008. Knowledge 2020 Pty Ltd. Please do not reproduce without prior permission, which will usually begranted. Contact Mark Ostryn 02 8005 1240 http://www.knowledge2020.com The above text containsgeneric financial information that does not constitute financial advice

• Impact on revenue and earnings

• Timing required to implement initiatve and realize benefits• Execution risks.

4.1 COST OF SALE

Cost of sale refers to the direct costs attributed to the production of goods sold by yourcompany, including the material costs and labour costs incurred when producing the goods.

A simple way of calculating this is:

INVENTORY AT BEGINNING OF PERIOD + TOTAL AMOUNT OF PURCHASES MADE DURING THEPERIOD – INVENTORY AT END OF PERIOD = COST OF INVENTORY SOLD BY COMPANY IN PERIOD

In a retailing or wholesaling company a large proportion of your cost of sale will be finishedgoods inventory. A full discussion on reducing the risks from an extended working capital cyclemay be found in the section on xxx.

You may be reviewing your sourcing strategy as there may be substantial cost savings fromsourcing from outside Australia, particularly in the Asia Pacific region. However, these reducedcosts must be weighed up against

• the costs and risks of a buildup in inventory from having to purchase more,• the costs involved in having a lengthier supply chain with much of your stock “on the

water”• advanced contractual commitments to produce more in remote manufacturing plants.

Thus you have to weigh up reduced costs with the potential of carrying greater inventory andless flexibility.

Also, a lower cost of sale will also result from making adjustments to the costs involved inserving a customer. This could result from automated order taking processes to reducingdelivery costs to automated purchasing set up based on minimum reorder quantities beingreached by the customer.

4.1.1 REFUNDS, WARRANTIES AND GUARANTEES

8/14/2019 Planning to Succeed - The Definitive eGuide for Building Company Financial Forecasts Mark Ostryn DRAFT 180708