planning for life & death wills, trusts and estates claralyn martin hill attorney at law

TRANSCRIPT

Planning for Life & DeathWills, Trusts and Estates

Claralyn Martin HillClaralyn Martin HillAttorney at LawAttorney at Law

Goals of Estate Planning

1. Live life fully1. Live life fully Provide for yourself (& spouse)Provide for yourself (& spouse) Provide for others according to your valuesProvide for others according to your values Provide for own possible incompetenceProvide for own possible incompetence

2. Pass property according to desires2. Pass property according to desires Provide for administration (who does the work)Provide for administration (who does the work) Provide for disposition (who gets what)Provide for disposition (who gets what)

Goals of Estate Planning, cont.

3. Provide for guardianship of minor children3. Provide for guardianship of minor children

4. Avoid probate if desired or use probate 4. Avoid probate if desired or use probate strategicallystrategically

5. Decrease or eliminate taxes5. Decrease or eliminate taxes Income tax (capital gains basis problems)Income tax (capital gains basis problems) Gift & estate taxGift & estate tax

Live Life FullyProvide for own incompetence

Advance DirectivesAdvance Directives Living WillLiving Will Special Power of Attorney for Health CareSpecial Power of Attorney for Health Care

Other Powers of Attorney: Durable, Other Powers of Attorney: Durable, Special, General--Exercise cautionSpecial, General--Exercise caution

Trust provisionsTrust provisions

Pass Property at Death According to Desires

How do we pass property during life?How do we pass property during life?

DEED

Grantor grants

Black Acre

to grantee.

Signed,

Grantor

Pass Property at Death According to Desires

Probate. What is it? Probate. What is it? It is the court procedure for It is the court procedure for transferring title and settling claims after death.transferring title and settling claims after death.

Probate is necessary for:Probate is necessary for: Transfer of land or titled property over $25,000 Transfer of land or titled property over $25,000

(amount varies by state)(amount varies by state) Other reasons (e.g. contested will)Other reasons (e.g. contested will) We can avoid these by funding a well drafted We can avoid these by funding a well drafted

trust.trust. Probate may be necessary or desirable for:Probate may be necessary or desirable for:

Establishing guardianship of minorsEstablishing guardianship of minors Cutting off creditors or avoiding later lawsuitsCutting off creditors or avoiding later lawsuits Clearing “clouded title” to landClearing “clouded title” to land

Pass Property at Death According to Desires

There are four ways designate where There are four ways designate where property should go after death:property should go after death: Will--does not transfer property, so must be Will--does not transfer property, so must be

probatedprobated Law--(the state writes your will)--does not Law--(the state writes your will)--does not

transfer property, so must be probatedtransfer property, so must be probated Contract (e.g. life insurance) bypasses probateContract (e.g. life insurance) bypasses probate Trust or other scheme that actually transfers Trust or other scheme that actually transfers

property during life, but doesn’t make a property during life, but doesn’t make a complete giftcomplete gift

Pass Property at Death According to Desires

Pass Property at Death According to Desires

By Will

““. . .And to my faithful servant Sidney, who I promised to . . .And to my faithful servant Sidney, who I promised to remember in my will, ‘Hi, there, Sidney!’”remember in my will, ‘Hi, there, Sidney!’”

Pass Property at Death According to Desires

By Will By will you canBy will you can

Appoint personal representativeAppoint personal representative Appoint guardians and conservators for minor Appoint guardians and conservators for minor

childrenchildren Provide for disposition of property at deathProvide for disposition of property at death Keep a separate updated list of tangible Keep a separate updated list of tangible

personal property dispositions in some statespersonal property dispositions in some states Revoke or change an earlier willRevoke or change an earlier will

Pass Property at Death According to Desires

By Will Some states allow holographic willsSome states allow holographic wills

All in your own handwritingAll in your own handwriting Date at top, signature at bottomDate at top, signature at bottom Name a guardian, alternates, disposition of assetsName a guardian, alternates, disposition of assets No notary or witnessesNo notary or witnesses Caution: Consult attorney about languageCaution: Consult attorney about language Caution: Use only if you don’t have significant assets Caution: Use only if you don’t have significant assets

or a complicated family situation.or a complicated family situation.

Holographic wills are valid in UtahHolographic wills are valid in Utah

Do Your Own Holographic Will:

In your own hand, write the date at the top of the In your own hand, write the date at the top of the page.page.

““I, (your full name), being over 18 years of age, of I, (your full name), being over 18 years of age, of sound mind and not acting under duress, declare this sound mind and not acting under duress, declare this my last will and testament, revoking all prior wills & my last will and testament, revoking all prior wills & codicils.codicils.

““I am married. My husband’s (wife’s) name is (full I am married. My husband’s (wife’s) name is (full name). We have the following children, who are issue name). We have the following children, who are issue of our marriage: (list names & birth dates.) (Or state of our marriage: (list names & birth dates.) (Or state that you are single, no children)that you are single, no children)

Do Your Own Holographic Will:

““I intend to dispose of all my property at the time of my I intend to dispose of all my property at the time of my death through this will.death through this will.

“ “ I give (list specific items & who you want them to go to).I give (list specific items & who you want them to go to). ““I give the residue of my estate to (if married, my I give the residue of my estate to (if married, my

husband/wife), (state full name). If (name) does not husband/wife), (state full name). If (name) does not survive me, I give the residue to my minor children, to be survive me, I give the residue to my minor children, to be distributed equally (per stirpes/capita).distributed equally (per stirpes/capita).

““I have intentionally omitted any existing heirs who are I have intentionally omitted any existing heirs who are not specifically mentioned here. Any who shall contest this not specifically mentioned here. Any who shall contest this

will shall receive only one dollarwill shall receive only one dollar..

Do Your Own Holographic Will:

““If any part of this will is invalid, such invalidity If any part of this will is invalid, such invalidity shall not affect any other provision.shall not affect any other provision.

““My estate shall be administered by one Personal My estate shall be administered by one Personal Representative. I nominate the following to serve Representative. I nominate the following to serve as Personal Representative to administer my as Personal Representative to administer my estate, to serve without bond in the order in which estate, to serve without bond in the order in which listed: (List about 3 people, in order of choice.)listed: (List about 3 people, in order of choice.)

““My Personal Representative is authorized to do My Personal Representative is authorized to do whatever is necessary to administer my estate.whatever is necessary to administer my estate.

Do Your Own Holographic Will:

““If my spouse does not survive me, I nominate the If my spouse does not survive me, I nominate the following, in the order listed, to act as guardians of & following, in the order listed, to act as guardians of & conservators for my minor children: (List about two conservators for my minor children: (List about two or three, in order of choice, the same as spouse’s list.)or three, in order of choice, the same as spouse’s list.)

““In witness whereof, I voluntarily sign my name this In witness whereof, I voluntarily sign my name this day.”day.”

Sign the document at the bottom and keep it in a Sign the document at the bottom and keep it in a place where it can be found.place where it can be found.

Spouse should do a similar document.Spouse should do a similar document.

Pass Property at Death According to Desires

By Contract Examples:Examples:

Third party contractsThird party contracts InsuranceInsurance Pay on Death accountsPay on Death accounts IRA’s, pension plans, etc. IRA’s, pension plans, etc.

DeedsDeeds Joint tenancy -- rights of survivorshipJoint tenancy -- rights of survivorship Tenancy in common -- no rights of survivorship Tenancy in common -- no rights of survivorship

Avoid probateAvoid probate Do not avoid tax consequencesDo not avoid tax consequences

Typical Ways to Hold Title:

Pass Property at Death According to Desires

Tenancy in Common

Typical Ways to Hold Title:

Pass Property at Death According to Desires

Joint Tenancy

Typical Ways to Hold Title:

Pass Property at Death According to Desires

Joint Tenancy

Typical Ways to Hold Title:

Pass Property at Death According to Desires

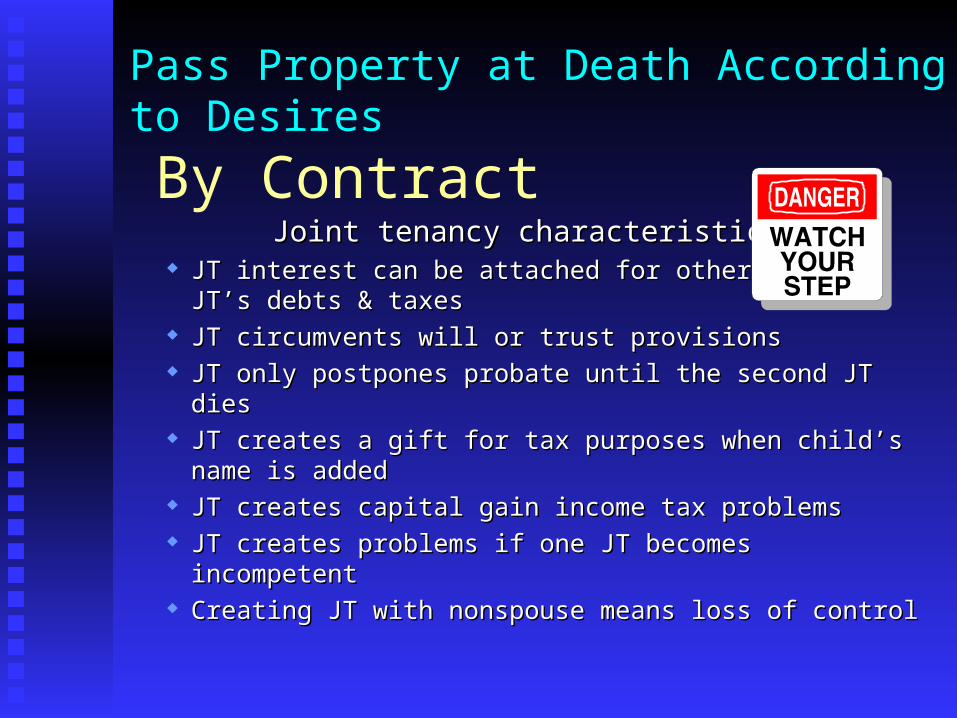

Joint Tenancy Characteristics

Your interest can be attached for the other person’s debts and taxes.

Typical Ways to Hold Title:

Pass Property at Death According to Desires

Joint Tenancy Characteristics

A joint tenancy circumvents will or trust provisions.

Typical Ways to Hold Title:

Pass Property at Death According to Desires

Joint Tenancy Characteristics

A joint tenancy only postpones probate until the second joint tenant dies.

Typical Ways to Hold Title:

Pass Property at Death According to Desires

Joint Tenancy Characteristics

A joint tenancy only postpones probate until the second joint tenant dies

Typical Ways to Hold Title:

Pass Property at Death According to Desires

Joint Tenancy Characteristics

It creates a gift for tax purposes when a child’s name is added.

Typical Ways to Hold Title:

Pass Property at Death According to Desires

Joint Tenancy Characteristics

It creates capital gains income tax problems.

Typical Ways to Hold Title:

Pass Property at Death According to Desires

Joint Tenancy Characteristics

It creates transfer problems if one person becomes incompetent.

Typical Ways to Hold Title:

Pass Property at Death According to Desires

Joint Tenancy Characteristics

Creating a joint tenancy with a nonspouse means LOSS OF CONTROL

Pass Property at Death According to Desires

By ContractJoint tenancy characteristicsJoint tenancy characteristics

JT interest can be attached for other JT interest can be attached for other JT’s debts & taxesJT’s debts & taxes

JT circumvents will or trust provisionsJT circumvents will or trust provisions JT only postpones probate until the second JT diesJT only postpones probate until the second JT dies JT creates a gift for tax purposes when child’s name is JT creates a gift for tax purposes when child’s name is

addedadded JT creates capital gain income tax problemsJT creates capital gain income tax problems JT creates problems if one JT becomes incompetentJT creates problems if one JT becomes incompetent Creating JT with nonspouse means loss of controlCreating JT with nonspouse means loss of control

2. Pass Property at Death According to Desires

By Trust

How a Trust is CreatedHow a Trust is Created

title

usetitle

use

2. Pass Property at Death According to Desires

By Trust

How a Trust is CreatedHow a Trust is Created

title

usetitle

use

2. Pass Property at Death According to Desires

By Trust

How a Trust is CreatedHow a Trust is Created

title

usetitle

use

A Trust is Just an Empty Box

Family Living Trust

Stock

Advantages of a Revocable Living Trust Advantages of a Revocable Living Trust It can avoid probate - multiple properties in several It can avoid probate - multiple properties in several

statesstates It can avoid probate if funded properlyIt can avoid probate if funded properly It can reduce or eliminate estate taxesIt can reduce or eliminate estate taxes It can allow for privacyIt can allow for privacy It can facilitate advanced planningIt can facilitate advanced planning It can handle complex family situationsIt can handle complex family situations It can provide for a smooth transition in case you It can provide for a smooth transition in case you

become incapacitated by avoiding court competency become incapacitated by avoiding court competency proceedingsproceedings

It can create other trusts & control a number of other It can create other trusts & control a number of other issuesissues

2. Pass Property at Death According to Desires

By Trust

Avoid Taxes

Avoid Taxes

““Internal Revenue Code Section 341 contains a single sentence that is longer Internal Revenue Code Section 341 contains a single sentence that is longer than the entire Gettysburg Address.” than the entire Gettysburg Address.” Peter L. FaberPeter L. Faber

““If Patrick Henry thought that taxation without representation was bad, he If Patrick Henry thought that taxation without representation was bad, he should see how bad it is with representation.” The Old Farmer’s Almanacshould see how bad it is with representation.” The Old Farmer’s Almanac

““When Congress talks about simplification, taxpayers may well be reminded When Congress talks about simplification, taxpayers may well be reminded of Emerson’s comments regarding an acquaintance, ‘the louder he talked of Emerson’s comments regarding an acquaintance, ‘the louder he talked of his honor, the faster we counted our spoons.’” Michael J. Graetzof his honor, the faster we counted our spoons.’” Michael J. Graetz

Avoid Taxes Income Tax Stepped-Up Basis

19951995 20002000 20052005

Dad buys real estateDad buys real estate Dad adds son as JTDad adds son as JT 1. Dad sells house for $150,0001. Dad sells house for $150,000

$50,000 basis$50,000 basis Son: $50,000 taxable incomeSon: $50,000 taxable income

Dad: $50,000 taxable incomeDad: $50,000 taxable income

2. Dad dies, house worth $150,0002. Dad dies, house worth $150,000

Son gets houseSon gets house

Dad’s interest “stepped up”Dad’s interest “stepped up”

Son owes $50,000 taxable incomeSon owes $50,000 taxable income

Avoid Taxes Income Tax Stepped-Up Basis

19951995 20002000 2005 2005

Dad buys real estateDad buys real estate 1. Dad sells house for $150,0001. Dad sells house for $150,000

$50,000 basis$50,000 basis No tax consequences for sonNo tax consequences for son

Trust names son as beneficiary on deathTrust names son as beneficiary on death 2. Dad dies, house worth $150,0002. Dad dies, house worth $150,000 Son gets houseSon gets house

Son’s entire interest “stepped up”Son’s entire interest “stepped up”

Son owes no taxable incomeSon owes no taxable income

Bottom line: There may be basis issues for any transfers or gifts prior to deathBottom line: There may be basis issues for any transfers or gifts prior to death

Avoid Taxes Unified Gift & Estate Tax

A small estate, for estate tax purposes, is anything under A small estate, for estate tax purposes, is anything under $1.5M (2005)$1.5M (2005)

Annual exclusion for gifts=$11,000 per donor per doneeAnnual exclusion for gifts=$11,000 per donor per donee Example:Example:

Grandfather ---> Grand child 1Grandfather ---> Grand child 1 $11,000$11,000 Grandmother ---> Grand child 1Grandmother ---> Grand child 1 $11,000$11,000 Grandfather ---> Grand child 2Grandfather ---> Grand child 2 $11,000$11,000 Grandmother ---> Grand child 2Grandmother ---> Grand child 2 $11,000, etc$11,000, etc

No gift tax consequencesNo gift tax consequences Anything over adds up for estate tax purposes, triggers form 709Anything over adds up for estate tax purposes, triggers form 709

Avoid Taxes Unified Gift & Estate Tax

20032003 $1M $1M

2004 2004 $1.5M$1.5M

20062006 $2M$2M

20092009 $3.5M$3.5M

20102010 Estate (not gift) tax repealed Estate (not gift) tax repealed

Stepped up basis disappears ($1.3M exemption)Stepped up basis disappears ($1.3M exemption)

20112011 $1M restored$1M restored

2012-->2012--> $1M$1M

Year Exclusion Amount

Total Lifetime Exclusion

Avoid Taxes Unified Gift & Estate Tax

20012001 $4.92M$4.92M

20092009 $2.93M$2.93M

2010 2010 $0 (except gift & capital gains $0 (except gift & capital gains taxes)taxes)

20112011 $4.8M$4.8M

2012-->2012--> $4.8M$4.8M

Year Tax

On a $10M Estate

Avoid Taxes Unified Gift & Estate Tax

Jane Bryant Quinn: “Ailing parents will keep Jane Bryant Quinn: “Ailing parents will keep their bedroom doors locked when their their bedroom doors locked when their children are in the house. It’s going to be a children are in the house. It’s going to be a great year to die.”great year to die.”

The Year 2010--“Push Dad Out of the Lear Jet Year”

Avoid Taxes Unified Gift & Estate Tax

Confused? You Confused? You are not alone.are not alone.

Avoid Taxes Unified Gift & Estate Tax

The Estate Tax probably won’t actually be repealed.The Estate Tax probably won’t actually be repealed.

It may settle somewhere around the 2009 $3.5M It may settle somewhere around the 2009 $3.5M exemption, but for now it will settle at $1M.exemption, but for now it will settle at $1M.

States may fill in the void by creating more state States may fill in the void by creating more state estate taxes.estate taxes.

Some Predictions by Experts:

Avoid Taxes Unified Gift & Estate Tax

Definitions:Definitions: Tax base = Taxable estate + prior taxable giftsTax base = Taxable estate + prior taxable gifts Taxable estate = Gross estate (including insurance proceeds, Taxable estate = Gross estate (including insurance proceeds,

stocks, personal property, everything Deceased had control over stocks, personal property, everything Deceased had control over when he died) minus deductions (e.g., marital deduction) when he died) minus deductions (e.g., marital deduction)

Estate tax payable:Estate tax payable: Tax on baseTax on base minus gift tax payable on prior gifts minus gift tax payable on prior gifts minus unified creditminus unified credit minus other creditsminus other credits

What about married couples?What about married couples?

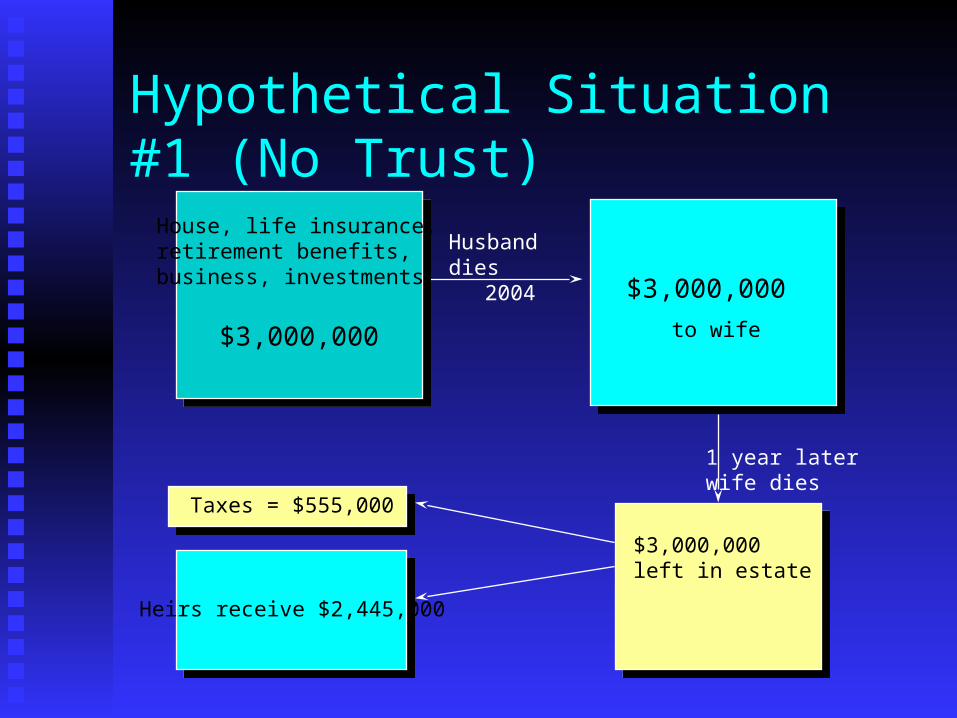

Hypothetical Situation #1 (No Trust)

$3,000,000

House, life insurance, retirement benefits,business, investments

$3,000,000

Husband dies2004

to wife

1 year laterwife dies

$3,000,000left in estate

Taxes = $555,000

Heirs receive $2,445,000

Hypothetical Situation #2 (Trust)

$1,500,000House, life insurance, retirement benefits,business, investments, etc.

$3,000,000

Husband dies2004

1 year laterwife diesTaxes = $0

Heirs receive $3,000,000

Trust A

Trust B

$1,500,000

Trust A

Trust B

$1,500,000

$1,500,000

Saves $555,000

Other Uses for Trusts Wealth replacement (ILIT’s)Wealth replacement (ILIT’s) Charitable giftingCharitable gifting Avoidance of GST Avoidance of GST Valuation discounts & “freezing” appreciated Valuation discounts & “freezing” appreciated

assetsassets Grantor retained annuity trustsGrantor retained annuity trusts Personal Residence TrustsPersonal Residence Trusts Medicaid & Special Needs TrustsMedicaid & Special Needs Trusts Etc.Etc.

Other estate planning tools

LLC’s & FLP’sLLC’s & FLP’s Retirement PlansRetirement Plans AnnuitiesAnnuities Etc.Etc.

Conclusions Probate and taxes are not the same thing. Plan Probate and taxes are not the same thing. Plan

for both.for both. Other considerations may trump either tax or Other considerations may trump either tax or

probate avoidanceprobate avoidance Plan ahead. Everyone goes sometimePlan ahead. Everyone goes sometime Under all circumstances, plan for the possibility Under all circumstances, plan for the possibility

of death while you still have minor children of death while you still have minor children Live life fully!Live life fully!