pg 22. interview: dr. ganesh natarajan, vc & ceo...

TRANSCRIPT

1ST - 30TH Apr 2015 . Vol 2 Issue 3 . For Private Circulation Only

pg 22. INTERVIEW: Dr. Ganesh Natarajan, VC & CEO, Zensar Tech.

pg 24. Indian Economy – Trend indicators

3GROUND VIEW GROUND VIEW 1 - 30 Apr 2015 1 - 30 Apr 2015 2

VOL 2 . ISSUE 3 . 1ST - 30TH APR 2015

Vineet Bhatnagar- Managing Director and CEO

EDITORIAL BOARD:Naveen Kulkarni, Manish Agarwalla, Kinshuk Bharti Tiwari

COVER & MAGAZINE DESIGN Chaitanya Modak, www.inhousedesign.co.in

FOR EDITORIAL QUERIES:PhillipCapital (India) Private LimitedNo. 1, 18th Floor, Urmi Estate, 95 Ganpatrao Kadam Marg, Lower Parel West, Mumbai 400 013

RESEARCH Automobiles Dhawal Doshi, Priya Ranjan

Banking, NBFCs Manish Agarwalla, Pradeep Agrawal, Paresh Jain

Consumer, Media, Telecom Naveen Kulkarni, Jubil Jain, Manoj Behera

Cement Vaibhav Agarwal

Economics Anjali Verma

Engineering, Capital Goods Ankur Sharma, Hrishikesh Bhagat

Infrastructure & IT Services Vibhor Singhal, Deepan Kapadia

Metals Dhawal Doshi, Ankit Gor

Mid-caps Vikram Suryavanshi

Oil & Gas, Agri Inputs Gauri Anand, Deepak Pareek

Pharmaceuticals Surya Patra, Mehul Sheth

Retail, Real Estate Abhishek Ranganathan, Rohit Shroff

Portfolio Strategy Anindya Bhowmik

Technicals Subodh Gupta

Production Manager Ganesh Deorukhkar

Database Manager Deepak Agrawal

Sr. Manager – Equities Support Rosie Ferns

SALES & DISTRIBUTION Ashvin Patil, Shubhangi Agrawal, Kishor Binwal, Sidharth Agrawal, Bhavin Shah, Varun Kumar, Narayan Mulchandani

CORPORATE COMMUNICATIONS Zarine Damania

GROUND VIEW - PREVIOUS ISSUES

1st Sep 2014 Issue 9

15th Nov 2014 Issue 11

1st Feb 2015 Issue 2 1st Jan 2015 Issue 1

1st Oct 2014 Issue 10

16th Dec 2014 Issue 12

3GROUND VIEW GROUND VIEW 1 - 30 Apr 2015 1 - 30 Apr 2015 2

4. COVER STORY: Not enough credit in the wallet

Ground View explores the opportunity ahead for payment banks and its impact on existing industry players like commercial bank and NBFCs

22. INTERVIEW: Dr. Ganesh Natarajan

Is ex-chairman of NASSCOM and currently the Vice Chairman & CEO of Zensar Technologies. We spoke to him about the growth prospects of the Indian IT Services companies, NASSCOM annual growth estimates and overall trends in the industry.

24. Indian Economy – Trend indicators

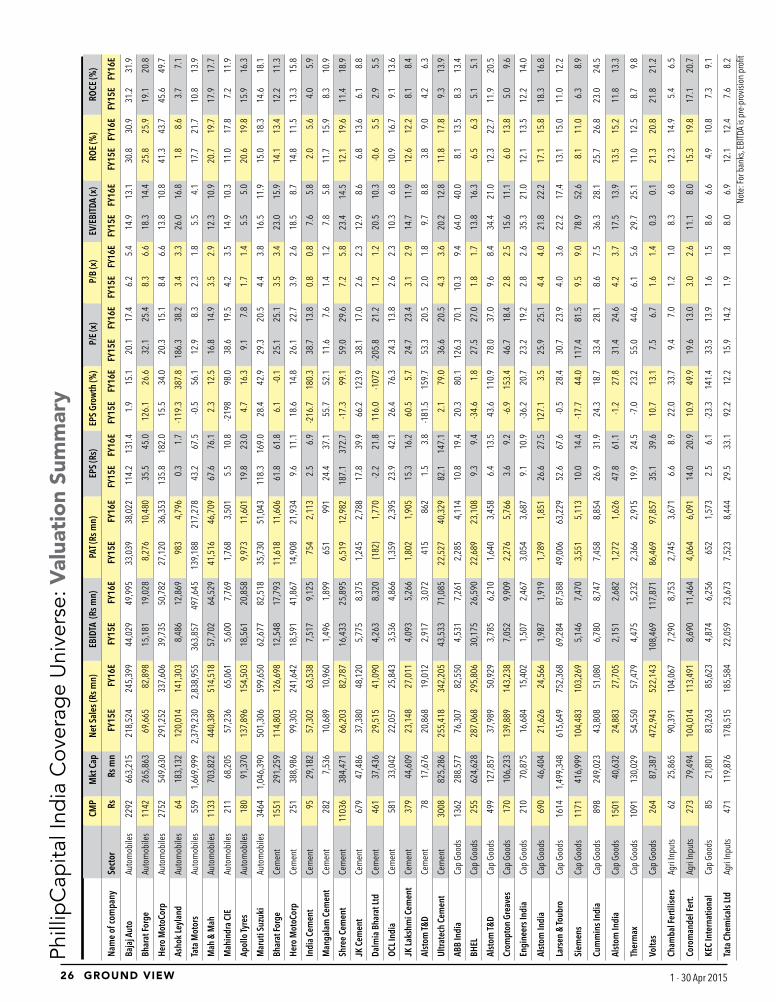

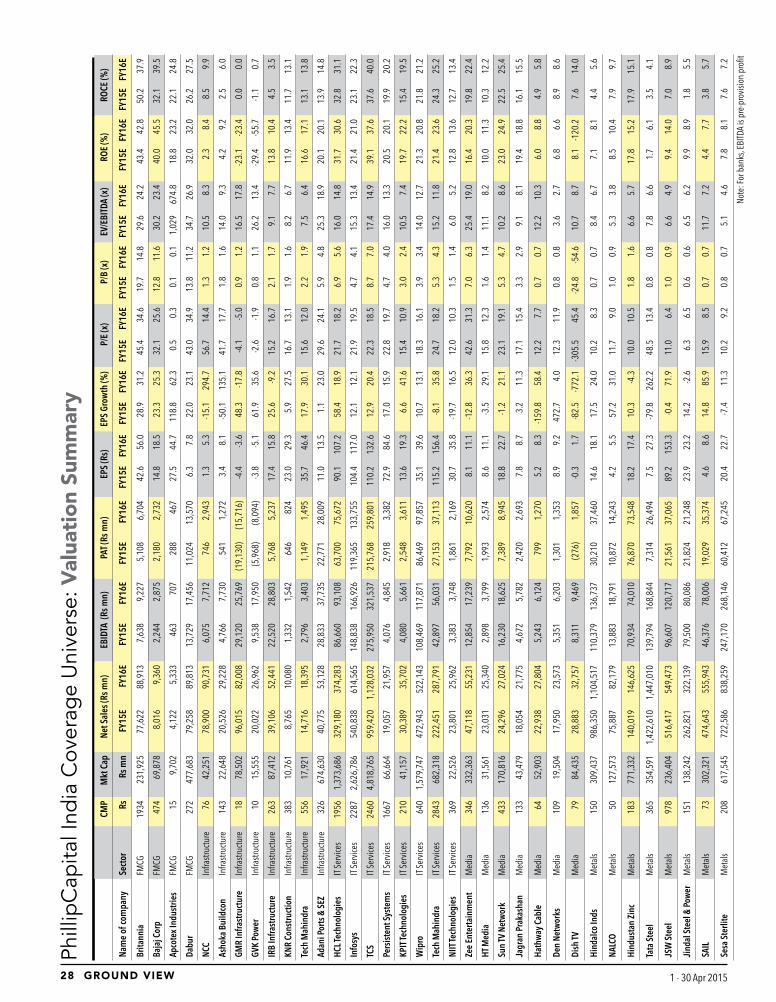

26. PhillipCapital Coverage Universe: Valuation Summary

LETTER FROM THE MANAGING DIRECTORIn an endeavour to provide ubiquitous access of

payment Services and deposit Products to small

businesses and low income households, the central

bank’s initiated to add new vertical in the banking

value chain called “payment bank”. This vertical will

include large section of population, especially the

low income household, migrant labour force and

economically weaker section under the net of basic

banking services and financial products. Along with

financial inclusion, the primary objective of pay-

ment banks will also be to facilitate high volume

and low value transactions in deposit, remittance

and payments, that will be driven through cost

efficient technology.

The payment bank’s business model would evolve

around payment solution as the restriction on

lending activity would put a cap on its intermedia-

tion business. The sheer size of market opportunity

available in payment services vertical and com-

pressed intermediation margin does not seem to

be a very exciting proposition. Despites this, the

level of participation for payment bank license is

immense. The advent of new vertical in financial

value chain would complement commercial bank’s

presence in the market. Our cover story on Pay-

ment Bank penned by analyst Manish Agarwalla

explores the opportunity ahead for payment banks

and its impact on existing industry players like com-

mercial bank and NBFCs.

Also read in this issue discussion with Dr. Ganesh

Natarajan, ex-chairman of NASSCOM and currently

the Vice Chairman & CEO of Zensar Technologies.

We spoke to him about the growth prospects of the

Indian IT Services companies, NASSCOM annual

growth estimates and overall trends in the industry.

Best Wishes

Vineet

CONTENTS

5GROUND VIEW GROUND VIEW 1 - 30 Apr 2015 1 - 30 Apr 2015 4

Villager depositing money at BC outlet

5GROUND VIEW GROUND VIEW 1 - 30 Apr 2015 1 - 30 Apr 2015 4

COVER STORY

Umesh Bhatka, a migrant worker in the textile mills in the industrial city of Surat sends

money to its native village in Ganjam district in Orissa. The money takes a time consuming

complicated route to reach his family. The money is dispatched through people from his

community who travel to his village. Many a times some amount goes missing. Ramadhir

kumar again a migrant worker at a construction site, keeps his wage with the contractor (for

safe keeping), which he draws when he visits his native place. The contractor charges undue

amount for just safe keeping. There are many such cases as migrant workers do not visit

bank branch due to limited financial literacy; lack of proper documentation;complexity; and

inaccessibility.

There is a need for commercial bank to shift the bulk of low-value transactions to a much

lower-cost and more ubiquitous retail channel, which makes for a significantly more

compelling business case to serve the poor. The key is to leverage corner shops/merchant

establishment that can be found in every village and in every neighbourhood. The payment

bank initiative by the central bank is an attempt to provide Ubiquitous Access to Payment

Services and Deposit Products at Reasonable Charges. “Not enough credit in the wallet”

is an indepth study of the potential opportunity for payment banks and its impact on other

participants in financial value chain like commercial banks and NBFCs

pg. 6 Financial Inclusion Foremost priority of policy maker___________________________________________________pg.8 Payment Bank Model An endeavour to provide Ubiquitous Access to basic banking services___________________________________________________pg.18 Potential market size Payment bank – enticing interest across industry segment – However motive defers___________________________________________________pg.19 Challenges and Key Success factors Little margin of error___________________________________________________

BY MANISH AGARWALLA, PRADEEP AGRAWAL & PARESH JAIN

7GROUND VIEW GROUND VIEW 1 - 30 Apr 2015 1 - 30 Apr 2015 6

Providing low-income households and

small businesses with access to financial

services is not a new goal for India. Policy

makers are well aware of its importance

and have been very willing to learn from the

successful experiences of other countries and

to experiment with new ideas. However, pro-

F I N A N C I A L I N C L U S I O N

Foremost priority of policy maker

gress on this front leaves much to be desired.

When financial inclusion goals are specified and

strategies articulated, there is little consideration

of credit risk and cost to serve. Consequently,

the Nachiket Mor Committee report aimed to

address issues of credit risks and costs to serve

for providing better access of financial services

The banking system design in any economy can be char-

acterised asa horizontally differentiated banking system

(HDBS) and a vertically differentiated banking system

(VDBS). A well-functioning financial system has insti-

tutions that collectively meet the needs of the country

while enhancing the stability of the system as a whole.

Fortunately, in India, many elements referred to and ex-

perience with multiple kinds of banking system designs

exist. For example, India has significant experience of

both the national bank and the regional bank design.

There is a robust set of NBFCs and several PPIs are

active. What is required is to evaluate these experiences

systematically and accelerate the growth of the designs

that seem to hold promise for financial inclusion and that

are consistent with the design principles. Additionally,

there is need to enable significant partnerships between

institution types that leverage each of their strengths

Banking system design

Categories Characteristics Example

National bank with Branches / agents Deposit, Credit, payment, etc (full service) PAN India SCBs like SBI, ICICI Bank, HDFC Bank, PNB, BOB etc

Regional Banks Deposit, Credit, payment, etc (full service) RRBs, Old private sector banks

National - Consumer Bank Deposit, Credit NBFCs like Bajaj finance, STFC etc & Housing finance companies

National - Wholesale Bank Deposit, Credit IDFC, PFC, REC etc

Horizontally differentiated banking system

Categories Characteristics Example

Payment network operators Payments VISA, MasterCard, FINO, NPCI, BCs, Whitelevel ATMs

Payment Banks Payments M-Pesa, Airtel Money, Oxigen (in India these are nested payment banks)

Full service Banks Deposit, Credit, payment, etc (full service) PAN India SCBs like SBI, ICICI Bank, HDFC Bank, PNB, BOB etc

National - Consumer Bank Deposit, Credit NBFCs like Bajaj finance, STFC etc & Housing finance companies

National - Wholesale Bank Deposit, Credit IDFC, PFC, REC etc

Vertically differentiated banking system

7GROUND VIEW GROUND VIEW 1 - 30 Apr 2015 1 - 30 Apr 2015 6

to small businesses and low-income households.

The committee recommends six vision statements

on financial inclusion.

1. Universal Electronic Bank Account (UEBA)

2. Ubiquitous Access to Payment Services and

Deposit Products at Reasonable Charges

3. Sufficient Access to Affordable Formal Credit

4. Universal Access to a Range of Deposit and

Investment Products at Reasonable Charges

5. Universal Access to a Range of Insurance and

Risk Management Products at Reasonable

Charges

6. Right to Suitability

The vision statement for Ubiquitous Access to

Payment Services and Deposit Products at

Vision Goal

A Universal Electronic Bank Account Each Indian resident, above the age of 18

Ubiquitous Access to Payment Services and Deposit Products at Reasonable Charges

Full services access point within a fifteen minute walking distance from every household in India

Reasonable Charges

At least one product with positive real returns

Sufficient Access to Affordable Formal Credit Credit to GDP Ratio in every District of India to cross 10%

Credit to GDP Ratio in every District of India to cross 50%

Credit to GDP Ratio for every \significant. sector of the economy to cross 10%

Credit to GDP Ratio for every \significant. sector of the economy to cross 50%

Convenient Access

Affordable Rates

Universal Access to a Range of Deposit and Investment Products at Reasonable Charges

Deposit & Investments to GDP Ratio in every District of India to cross 15%

Deposit & Investments to GDP Ratio in every District of India to cross 65%

Reasonable Charges

Universal Access to a Range of Insurance and Risk Man-agement Products at Reasonable Charges

Total Term Life Sum Assured to GDP Ratio in every District of India to cross 30%

Total Term Life Sum Assured to GDP Ratio in every District of India to cross 80%

Reasonable Charges

Right to Suitability

All financial institutions to have a Board approved Suitability Policy.

Presence of district level redressal offices for all customers availing any financial service

Vision statement on financial inclusion - Nachiket Mor Committee recommendation

Reasonable Charges for small businesses and

low-income households is as follows.

By January 1, 2016, the number and distribution

of electronic payment access points would be such

that every resident would be within a 15-minute

walking distance from such a point anywhere in

the country. Each such point would allow residents

to deposit and withdraw cash to and from their

bank accounts and transfer balances from one

bank account to another, in a secure environment,

for both very small and very large amounts, and

pay reasonable charges for all of these services.

At least one of the deposit products accessible to

every resident through the payment access points

would offer a positive real rate of return over the

consumer price index.

9GROUND VIEW GROUND VIEW 1 - 30 Apr 2015 1 - 30 Apr 2015 8

the payment bank. The goal of the central bank

is to provide basic banking services to 450,000

unbanked villages. The payment bank will des-

ignate merchant establishments / corner shop

as its access points on the pay- and-use model.

This access point will address the issue of costly

brick-and-mortar branches and offer low cost and

easy access to the customer. From the merchant

establishments’ point of view it is an additional

source of revenue and increase in footfalls in his

establishment.

1. Acceptance of demand deposits (current de-

posits, and savings bank deposits). Payments

banks will initially be restricted to holding a

maximum balance of Rs. 100,000 per customer.

After the performance of the Payments bank is

gauged by the RBI, the maximum balance can

be raised. KYC norms are also simplified for

small value transaction limited transaction.

2. Payments and remittance services through

various channels including branches, BCs

and mobile banking. The payments / remit-

tance services would include acceptance of

funds at one end through various channels

including branches and BCs and payments of

cash at the other end, through branches, BCs,

and Automated Teller Machines (ATMs) and

point of sale terminal.

3. Issuance of PPIs as per instructions issued

from time to time under the PSS Act.

Umesh Bhatka, a migrant worker in the

textile mills in the industrial city of

Surat sends money to its native village

in Ganjam district in Orissa. The mon-

ey takes a time consuming complicated route

to reach his family. The money is dispatched

through people from his community who travel

to his village. Many a times some amount goes

missing. Ramadhir kumar again a migrant worker

at a construction site, keeps his wage with the

contractor (for safe keeping), which he draws

when he visits his native place. The contractor

charges undue amount for just safe keeping.

There are many such cases as migrant workers do

not visit bank branch due to limited financial lit-

eracy; lack of proper documentation;complexity;

and inaccessibility (due to limited banking hour).

In an endeavour to provide ubiquitous access of

payment services and deposit products to small

businesses and low-income households, the

central bank initiated a vertical in the banking

value chain called “payment bank”. This vertical

aims to cover a large section of the population,

especially low-income households, migrant labour

and economically weaker sections under the net

of basic banking services and financial products.

Along with financial inclusion, the primary ob-

jective of payment banks will also be to facilitate

high volume and low value transactions in deposit,

remittance and payments, driven through cost-effi-

cient technology.

The concept of the payment bank in not new in

India and some of its basic functions are similar to

pre-paid payment instruments or the business-cor-

respondent model. Due to difficulties faced by

such entities and the risk associated with the

model, the central bank promoted the concept of

PA Y M E N T B A N K M O D E L

An endeavour to provide Ubiquitous Access to basic banking services

Scope of payment bank

9GROUND VIEW GROUND VIEW 1 - 30 Apr 2015 1 - 30 Apr 2015 8

4. Internet banking - The RBI is also open to

applicants transacting primarily using the Inter-

net.

5. Functioning as Business Correspondent

(BC) of other banks – A Payments bank may

choose to become a BC of another bank for

credit and other services which it cannot offer.

6. The Payments bank cannot undertake lend-

ing activities. Apart from amounts maintained

as Cash Reserve Ratio (CRR) with RBI, it will be

required to invest all its monies in Government

securities/Treasury Bills with maturity up to one

year that are recognized by RBI as eligible se-

curities for maintenance of Statutory Liquidity

Ratio (SLR).

Capital requirement. Since the payment banks

will not be allowed to assume any credit risk,

and if its investments are held to maturity, such

investments need not be marked to market and

there may not be need for capital for market risk.

However, the payment banks will be exposed to

operational risks. They will also be required to

invest heavily in technological infrastructure for

operations. The capital will be used to create such

fixed assets. Therefore, the minimum paid-up

voting equity capital of a payment bank shall be

Rs1 bn. The payment bank shall be required to

maintain a minimum capital adequacy ratio of 15%

of its risk weighted assets (RWAs) on a continuous

basis, subject to any higher percentage as may be

prescribed by the RBI from time to time. However,

as payment banks are not expected to deal with

sophisticated products, the capital adequacy ratio

will be computed under simplified Basel I stand-

ards.

As payment banks will have almost zero or negligi-

ble RWAs, its compliance with a minimum capital

adequacy ratio of 15% would not reflect the true

risk. Therefore, the bank should have a leverage

ratio of not less than 5%—its outside liabilities

should not exceed 20 times its networth/paid-up

capital and reserves.

Promoter’s contribution. The promoter’s min-

imum initial contribution to the paid-up voting

equity capital of a payment bank shall be at least

40%, which shall be locked in for five years from

the date of commencement of business of the

bank. Shareholding by promoters in the bank in

excess of 40% shall be brought down to 40% with-

in three years of the date of commencement of

business of the bank. Further, the promoter’s stake

should be reduced to 30% of the paid-up voting

equity capital of the bank within 10years, and to

26 % within 12 years from the date of commence-

ment of business of the bank. Proposals with a

diversified shareholding and time frame for listing

are preferred.

Foreign shareholding. The foreign shareholding

in the bank would be as per the extant FDI policy.

Voting rights and transfer/acquisition of shares.

As per Section 12 (2) of the Banking Regulation

Act, 1949, voting rights in private sector banks are

capped at 10%, which can be raised to 26% in a

phased manner by the RBI. Further, as per Section

12B of the Act, any acquisition of 5% or more of

voting equity shares in a private sector bank will

require prior approval of the RBI. This will also

apply to payment banks.

Prudential norms. As payment banks will not have

loans and advances in their portfolios, they will

not be exposed to credit risks and the prudential

norms and regulations of the RBI as applicable

to loans and advances, will therefore not apply

to them. However, the banks will be exposed to

operational risks and should establish a robust op-

erational risk-management system. They may face

liquidity risks and therefore are required to follow

the RBI’s guidelines on liquidity-risk management,

to the extent applicable.

Regulatory norms

11GROUND VIEW GROUND VIEW 1 - 30 Apr 2015 1 - 30 Apr 2015 10

There is need for transactions and savings ac-

counts for the under-served in the population.

Also, remittances have both macro-economic

benefits for the region receiving them as well as

micro-economic benefits for the recipients. Higher

transaction costs of making remittances diminish

these benefits. Therefore, the primary objective

of setting up of payment banks is to enhance

financial inclusion by providing (i) small savings ac-

counts and (ii) payments/remittance services to the

migrant labour workforce, low-income households,

small businesses, other unorganised-sector enti-

ties and other users, by enabling high volume and

low value transactions in deposits and payment/

remittance services in a secured technology-driven

environment.

Apart from web-based and mobile app-based

banking services, the payment bank would des-

ignate various merchant establishments / corner

stores as its access points on the pay-and-use

model. The merchant establishments / corner

stores, unlike costly brick-and-mortar branches,

will offer easy and low cost access to the customer.

From the merchant establishments’ point of view,

it is an additional source of revenue and increase

in footfalls in his establishment.

Banking beyond branches is about shifting the

bulk of low-value transactions to a much low-

er-cost and more ubiquitous retail channel, which

makes for a significantly more compelling business

case to serve the poor. The key is to leverage

corner shops/merchant establishment that can

be found in every village and in every neighbour-

hood. In much the same way as shops exchange

their pre-purchased inventory of rice or cooking

oil against cash, they can also exchange their own

bank balance against cash (and vice versa). This

can be done safely as long as the store takes in

and pays back customers’ cash against an equal

and simultaneous electronic transfer of value

between the bank accounts of the customer and

the store. The payment bank must put in place

a technology platform (which can be based on

cards, biometrics or mobile phones) through which

it can authorize and record each transaction in real

time, thereby ensuring that all client transactions

are fully funded before the customer leaves the

store.

A retail store’s business is to buy a stock of a good

that people want –let’s call it rice—and to resell it

in smaller amounts. Through this process, it stead-

ily reduces its stock of rice and increases its stock

of cash. When the cash inventory is depleted, the

store needs to take some of its cash and exchange

it for a fresh supply or rice.

Substituting “electronic money” or “bank bal-

ance” for rice, and the same mechanics apply for

its bank reselling business. The store starts with a

balance of electronic money in its bank account,

and when a customer walks into the store to make

a deposit, the store transfers electronic value to

the customer in exchange for cash. When it runs

out of bank balance, the store can no longer fund

more customer deposits and it must go to the

bank to re-stock on electronic money using the

cash it has received from customers. A customer

withdrawal is the same operation but in reverse.

Thus, the only difference with the rice merchant is

that the cash merchant can buy as well as sell elec-

tronic money for cash, i.e. it can conduct deposits

as well as withdrawals.

Normal stores can thus act as cash merchants,

aggregating the cash needs of customers so that

only the shopkeeper, and not the entire commu-

nity, has to travel to a branch in order to service

their account. Cash merchants handle the logistics

of local cash distribution, in effect bridging the

distance between the bank branch (acting as a

kind of wholesale cash aggregation point for cash

merchants) and the places where poor people live

and work. The store is paid a small commission

per transaction served, making this a variable-cost

transactional channel for the bank and at the

same time a profitable new line of business for the

shopkeeper / merchant establishment. The bank

retains full control over the customer proposition,

the marketing of the service, and in ensuring the

safety and soundness of the IT platform and risk

management policies.

Business model

11GROUND VIEW GROUND VIEW 1 - 30 Apr 2015 1 - 30 Apr 2015 10

Currently PPI issuers and business correspondents

use biometric scanners to allow their customers to

make remittances. A customer who wants to remit

funds to another individual (receiver), needs to

walk into the centre and authenticate his identity

by using the thumb impression in a biometric

scanner. After verification, the customer deposits

the money at the centre and in turn the centre

manager will credit the receiver’s wallet from his

own wallet and later deposit the money re-

ceived in his account. Another way of making the

remittance is that the customer directly transfers

the money from his own wallet to the intended

receiver’s wallet after the identity is authenticated.

In this process, there is no handling of cash by the

centre manager, only the customer’s wallet is deb-

ited and the intended receiver’s wallet is credited

immediately.

Due to restriction in lending activity, the spread

earned by payment banks is expected to be very

thin and hence the entire business model would

evolve around payment services. In order to

enable a low cost easy access to the customer, the

model would be similar to a banking correspond-

ent model, wherein the payment bank would

appoint merchant establishments / corner shops

as its access point enabled by strong IT support.

The advantage which payment banks would have

compared to business correspondents or PPIs is

that, under payment bank model cash out from

merchant establishments / corner shops would be

allowed, thus removing the major hindrance faced

by BCs & PPIs.

Thin Intermediation margin

A competitive deposit product is a pre-requisite

for customer acquisition, which is crucial to a

stable remittance business. But the restriction on

lending activity would put a cap on its ability to

provide higher interest on its deposit product.

However the deposit product offered by payment

banks is expected to provide interest rates higher

than the prevailing market rate in savings deposits.

Large commercial banks provide 4.5% interest on

saving deposits.

Theoretically, a payment banks margin should not

be more than margin of SCB adjusted for credit

risk, tenure premium and high operating cost.

Long term credit risk adjusted margin of top six

commercial banks is averaged at 230bps. The

seven year average tenure premium between 1

year and 5 year corporate bond is 40bps. Oper-

ating cost of SCBs would average at 2% of asset.

The transaction cost in alternate banking model is

30%-40% of cost incurred under branch banking

model. Hence opex under agency / franchisee

model can be around 80bps compared to 200bps

opex (operating cost to asset ratio) under branch

banking model. The upper limit of margin for

payment bank is expected to around 100bps (i.e.

230bps credit risk adjusted margin - 40bps tenure

premium - 100bps opex). However the actual

margin would depend on the individual company’s

business model and market dynamics (which again

will depend on number of new licensees).

Current shortcomings of existing Pre-paid Instrument Issuer (PPI) model and business correspondent model1. The most important concerns pertaining to PPI model is the opacity of the Nested business model. Currently, the PPI are

not required to maintain any capital requirement. In addition the PPIs runs the risk of the sponsor bank getting insolvent with which it holds the escrow account and on the other and the sponsor bank runs the risk of operating quality and the likelihood of a run on its PPIs banking system design.

2. PPIdoesn’tofferinteresttothecustomersonthebalancesmaintainedinthewallet/Account.Sothereforefromafinancialinclusion point of view, this doesn’t help the poor people and small businessmen save their money.

3. Business correspondent model also faces the similar risk. In the absence of a regulator for BCs and capital requirement, the trust of the sponsor bank has always been low. Also, the sponsor bank does not control the pricing of the product and services offered by the BC, thus exposing them to criticism by the regulator. Past experience puts a question mark on the scalability of both the models.

13GROUND VIEW GROUND VIEW 1 - 30 Apr 2015 1 - 30 Apr 2015 12

Strong reliance on payment solution

The payment bank model would revolve around

low cost payment solution for small ticket transac-

tion. Payment solution would include

a. Domestic remittance services

b. Cash ins and Cash outs services

c. Airtime top-up and related recharge services

d. Utility bill payments

Domestic household remittance market is pegged

at Rs2000bn per annum, growing at CAGR of

~12%. According to industry surveys, 40% of

the domestic remittance business is channelized

through formal sources like commercial banks;

banking correspond (BC) and post office etc.

The informal system which operates primarily

through friends and family, couriers, bus services,

hawala channels and in-person transfers, is still

Payment bank NIM Scenario

Leverage (times networth)

10x 15x 20x

Interest on deposit (%)

5 1.95 1.79 1.7

6 1.04 0.85 0.75

7 0.13 -0.09 -0.2Source: PhillipCapital India Research

A scenario analysis

Major route Estimated migrant workers

(mn)

Annual remittance by migrant

workers (Rsbn)

Average Montly

remittance per worker

(Rs)

Surat/Daman - Orissa 2.0 168 7000

Mumbai - Bihar / UP 10.0 720 6000

Delhi - Bihar / UP 8.0 576 6000

Kerala - West Bengal 0.2 18 6500

Tamil Nadu - Orissa / Bihar 0.3 20 6000Source: Oxygen

Major household remittance route in India

widely preferred over the formal financial system.

Migrants prefer informal channels for a variety

of reasons which among others include costs in-

curred in making transfers, and opportunity costs.

Even access to the formal financial system is not

sufficient to ensure its usage. Migrants may simply

refuse to use the channel due to low levels of fi-

nancial literacy, lack of penetration in the home re-

gion, and time consuming process. Intuitively, the

lower a person is placed in the income distribution

ladder the more likely is he/she to be excluded

from the financial system or be more dependent

on the informal system.

Transferring money through informal sources is

inconvenient and more time consuming and risky.

Rural Urban All India

Friend/family member 30.8 18.8 29.2

Money transfer (Western Union) 2.2 4.4 2.5

Bank 36 53.8 38.3

Post office 5.2 3.3 4.9

Courier 2.4 0.2 2.1

Bus service 0.2 0 0.2

In person 22.8 19.2 22.4

Others 0.4 0.3 0.4

All 100 100 100Source: NCAER

Mode of money transfer

Average Number of days taken for the money to reach the recipient

Source: NCAER

13GROUND VIEW GROUND VIEW 1 - 30 Apr 2015 1 - 30 Apr 2015 12

For example, money is transferred free of charge

through friends or relatives who are travelling back

to a migrant’s home town. Similarly, cash couriers

operating in specific migration corridors whose

livelihood are to travel and physically deliver cash

for migrants are another choice for making the

transfers. Migrants may also prefer to transfer the

amount themselves during trips to their own vil-

lages and towns for social occasions and between

Received Sent

Bihar 46 21

Uttar Pradesh 29 15

Uttarakhand 4 5

West Bengal 4 2

Rajasthan 3 5

Jharkhand 3 6

Orissa 2 5

Punjab 1 1

Maharashtra 1 8

Madhya Pradesh 1 7

Tamil Nadu 1 7

Rest 4 18Source: NCAER

Distribution of Remittent Households across Major States

STATES Sent Received

Punjab 1.7 0.5

Rajasthan 0.2 0.3

Uttar Pradesh 0.1 0.2

Bihar 1 1

West Bengal 0.4 0.3

Jharkhand 0.8 0.5

Orissa 1.2 0.6

Madhya Pradesh 0.1 0.2

Total 0.7 0.6Source: NCAER

Cost of Money transfer (percent to amount remitted)

Vvarious channels (remittance cost on Rs5000)

% to transaction value

Money Order, India Post 0.50%

Business correspondent of SBI 2%

Airtel Money 0.50%Source: RBI

Indicative cost of transaction on domestic remittance

The domestic household remittance market

offers a market opportunity of Rs20bn in terms of

revenue, factoring a commission rate of 1% (0.5%

on both side of the transaction sender & receiver).

The Rs12bn( 60%) unorganised market remains

the potential market for payment bank and other

organised player in the financial value chain like

PPIs, business correspondent, small banks etc.

Customer queue at SBI Tatkal

jobs. Although the formal financial

system does offer security, speed, and

cost effectiveness, attributes that are

cherished by the migrants, the system

has cumbersome documentation

procedures, is often inconvenient and

does not have deep enough penetra-

tion.

15GROUND VIEW GROUND VIEW 1 - 30 Apr 2015 1 - 30 Apr 2015 14

The only other comparable country of India’s size

with a large internal migrant population is China.

A few studies estimate that the Chinese domestic

remittances market is nearly three times the size of

the Indian market. However, the crucial point that

needs to be mentioned is that the formal sector

in China accounts for 75% of the total remittances

market transactions as opposed to less than 40%

Key Services offered Commission rates

BFSI

Deposit 0.30%

Withdrawal 0.30%

Fund transfer Rs8 Per transfer

B2C

Light Bill Rs3/ Bill

DTH Customers 0.30%

Mobile Recharge 0.30%

G2C

Gas Subsidy -

Indra Awas Yojna -

NAREGA Job Card -

Financial products

LIC -

Total Earning/ Rural centre Rs 5000-20000Source: Vakrangee

Various financial services and commission rate charged by a retail centre of a business correspondent in a village with population of 5000

PPI (Paytm) offers various payment solutions

15GROUND VIEW GROUND VIEW 1 - 30 Apr 2015 1 - 30 Apr 2015 14

M-Pesa, a mobile money transfer service, innovated

by the Vodafone group, was first launched in Kenya in

March 2007 through Safaricom, a leading mobile oper-

ator in Kenya. It was initially designed to facilitate dis-

bursement and repayment of microfinance loans through

the mobile phone to reduce the cost associated with

handling cash and increasing efficiency. After the com-

pletion of pilot testing M-Pesa services were launched to

facilitate money transfers.

How M-Pesa works

M-Pesa is an SMS-based system that enables users to

deposit, send and withdraw funds, using their mobile

phones. It does not pay interest on deposits maintained

in the account and does not offer loans. Customers are

not required to have a bank account and can open an

account, transact with agents appointed by M-Pesa to

deposit and withdraw money. Customers find it conven-

ient to transact though M-Pesa, given the network of

over 80,000 agents.

M-Pesa initially started basic services like domestic and

International remittances, bill payments and airtime top-

ups. Subsequently it evolved into a complete mobile

money service with facilities such as

• ATM withdrawals

• Opening of interest paying savings accounts

• Offering other financial products like insurance and

credit facilities

• Making on-premise retail payments for buying goods

and services

• Mobile ticketing and payment of services for con-

certs and events

• Offering accounts to companies with higher trans-

action limits, which can be used to make bulk B2C

payments and through which they can receive funds

and bill payments.

Reasons for the acceptance of M-Pesa

Lower access to financial services. The access to finan-

cial services in Kenya has been low. During the launch

of the service only 19% of the population had access to

formal financial services. The country’s 31 mn people

had about five million accounts.

Huge demand for remittance services. Due to lack of

availability of remittance services at a reasonable cost

and need for reduced dependence on cash for security

reasons, the acceptability of M-Pesa services was a suc-

cess. Also it is a common practice in Kenya for migrant

workers in urban places to send back money to their

families in villages.

Adoption of technology. Prior to the launch of M-Pesa

services mobile phone penetration was considerable,

with 83% of the population aged above 15 years having

access to mobile phone technology and most being

familiar with the basic operations of making voice calls

and texting.

First mover advantage. Safaricom, being a familiar and

trusted brand, was the first telecom operator to launch

a mobile technology-based banking service in Kenya,

making it easy for the telecom operator to capture a

large market share.

Conducive regulatory environment. The Central Bank

of Kenya understood the need for efficient and low cost

remittance services, so it allowed telecom operators to

offer banking services without partnering with banks.

Advantages of M-Pesamobile money services to

financial institutions

• M-Pesa services enabled financial institutions like

banks and micro-finance institutions (MFIs) to achieve

considerable reduction in transaction costs and

increase staff efficiency. Earlier an MFI disbursing

loans though branches/groups had to bear huge cost

on cash logistics and insurance. An MFI disbursing

loans through cheque is charged for each clearing.

Through the B2C service, MFIs need to deposit

the money in their M-Pesa accounts and can easily

disburse the loan amount at a lower cost. Similarly,

bank branches can accept deposits or receive loan

repayments through M-Pesa and reduce or avoid ex-

Case study: M-Pesa

17GROUND VIEW GROUND VIEW 1 - 30 Apr 2015 1 - 30 Apr 2015 16

penses for branch infrastructure, manpower,

equipment and security expenses.

• The M-Pesa platform allows FIs to de-con-

gest their banking offices, allowing the

staff more time to focus on product sales,

business development, customer acquisition

and related activities, without worrying much

about cash management, deposits, with-

drawals and disbursement services.

Advantages of M-Pesa to customers

• Customers availing of M-Pesa services can

avoid travelling long distances to transaction

their account or to fill in bank forms and

queue up to deal with tellers and cashiers.

They just need to deposit the money in their

M-Pesa account at the nearest M-Pesa agent

and transfer money to their bank accounts.

This helps users to save time and travel

expenses and avoid the risk of carrying cash.

Challenges faced by FIs of M-Pesa to FIs and

customers

• A few FIs claim that one of the biggest

challenges has been in reconciling M-Pesa

deposits in their customers’ accounts, fol-

lowed by a lag in Safaricom crediting funds,

resulting in customers being unable to with-

draw money. The reconciling problem occurs

mainly due to system errors and poor integration of software

between the Safaricom and the FIs.

• Sometimes, customers key-in the wrong account number and

their money is transferred to an unintended account. If customers

type out an invalid account number, the money is credited to a

suspended account. Either way, customers cannot access their

deposits.

in India. Roughly 45% of the remittances are chan-

nelled through China Post, while 25% are handled

by the commercial banks.

Cash ins and Cash outs services

Transaction fee from cash ins and cash outs can be

source of revenue for the payment bank. A rough

estimate suggests that India has 100mn migrant

workers. As per NCAER survey, average house-

hold food expenditure of remittent households is

Rs34057 per annum. This translates into annual

cash out of Rs3406bn for these households. The

cash ins and cash outs are chargeable due to infra-

structure and working capital cost. The transaction

charge varies between 2% to 3% depending on

the volume. Thus the domestic migrant worker

cash ins – cash outs market size can be pegged at

Rs3trn, offering a revenue potential of Rs85bn.

Airtime top ups, related recharge services and

utility bill payments

The overall mobile recharge market is about

Rs1,000 bn a year. Around 95% of the recharge

is done at retailer outlets on a cash basis. These

offer opportunities for payment banks by offering

recharge solutions at their access points (mobile,

Internet, or franchise outlet) by aggregating the

recharge facility for multiple telecom service

providers. Similarly, the DTH recharge market is

pegged at Rs74 bn annually. Utility bill payment

facility can also be sources of revenue.

17GROUND VIEW GROUND VIEW 1 - 30 Apr 2015 1 - 30 Apr 2015 16

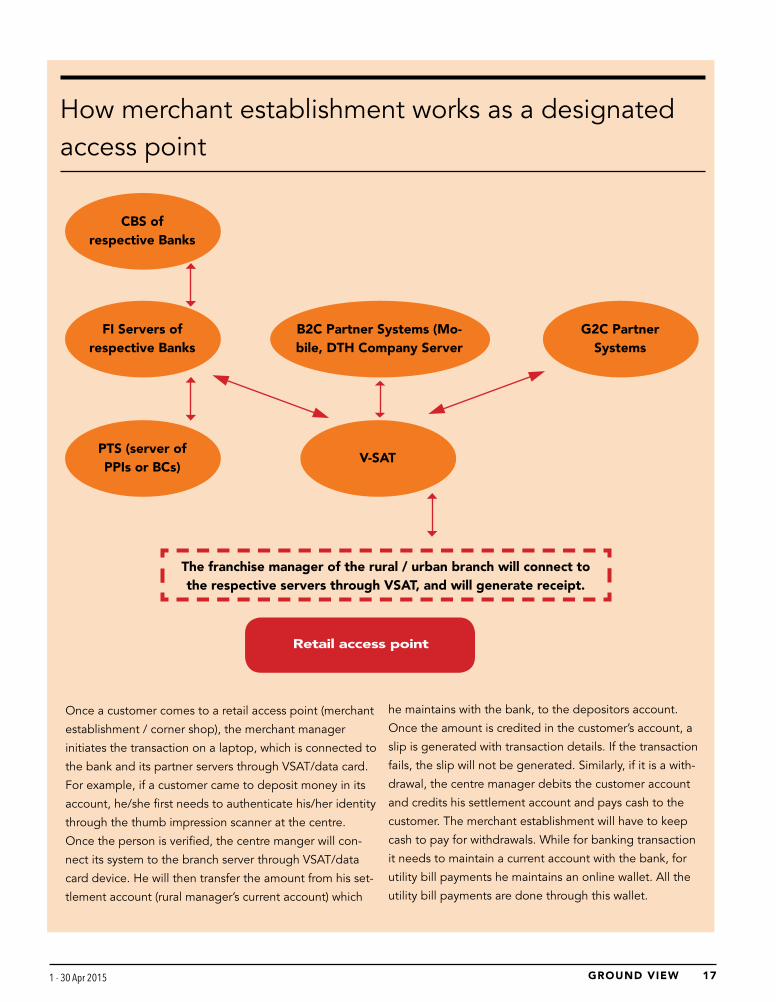

CBS of respective Banks

FI Servers of respective Banks

PTS (server of PPIs or BCs)

V-SAT

Retail access point

The franchise manager of the rural / urban branch will connect to the respective servers through VSAT, and will generate receipt.

G2C Partner Systems

B2C Partner Systems (Mo-bile, DTH Company Server

Once a customer comes to a retail access point (merchant

establishment / corner shop), the merchant manager

initiates the transaction on a laptop, which is connected to

the bank and its partner servers through VSAT/data card.

For example, if a customer came to deposit money in its

account, he/she first needs to authenticate his/her identity

through the thumb impression scanner at the centre.

Once the person is verified, the centre manger will con-

nect its system to the branch server through VSAT/data

card device. He will then transfer the amount from his set-

tlement account (rural manager’s current account) which

he maintains with the bank, to the depositors account.

Once the amount is credited in the customer’s account, a

slip is generated with transaction details. If the transaction

fails, the slip will not be generated. Similarly, if it is a with-

drawal, the centre manager debits the customer account

and credits his settlement account and pays cash to the

customer. The merchant establishment will have to keep

cash to pay for withdrawals. While for banking transaction

it needs to maintain a current account with the bank, for

utility bill payments he maintains an online wallet. All the

utility bill payments are done through this wallet.

How merchant establishment works as a designated access point

19GROUND VIEW GROUND VIEW 1 - 30 Apr 2015 1 - 30 Apr 2015 18

Applicant for Payment Bank Bank as JV partner

Reliance Industries ltd State Bank Of India

Airtel M commerce Kotak Mahindra Bank

Oxigen services Ratnakar Bank

Commercial banks partnering for payment bank

P O T E N T I A L M A R K E T S I Z E

Payment bank – enticing interest across industry segment – However motive defers

The concept of the payment bank is

unique and offers an opportunity in

a huge, untapped market for basic

banking services. But the initial journey

is expected to be painful due to intense competi-

tiveness and the limited scope of operations. The

space is expected to be crowded with different

players focusing on the space – not necessarily

with an aim of profitability.

Various banks have partnered with either telecom

service providers or pre-paid instrument issuers for

payment bank licences (banks can only become

an equity partner with maximum equity holding

of 30%). Interest is seen across industries like

telecom service providers (Airtel, Vodafone, Idea,

Reliance Jio); NBFCs (Cholamandalam, Muthoot);

business correspondents (Vakrangee) ; IT ser-

vices (Tech Mahindra), PPIs (Oxygen, Itzcash, GI

Technology), India Post etc. Banks like ICICI bank;

Axis bank and Yes bank are also in discussions with

various applicants for a possible tie up.

Business potential not exciting

The potential market opportunity for payment

bank in remittance and cash in – cash outs can be

pegged at Rs100bn (domestic remittance market

Rs20bn and cash ins – cash outs Rs85bn). The

intermediation business would earn a wafer thin

margin, which can be anything between 50bps

to 100bps based on industry dynamics. The total

opportunity for payment banks does not seem too

exciting. The moot question remains, than why so

many applicant – RBI received 41 application for

payment bank license.

Deep pocket players - profitability not the sole

motive

Despite a not-so-encouraging market potential

for payment banks, interest seems to be immense

from deep pocket players like Reliance, SBI,

Airtel, Vodafone, Idea and Tech Mahindra etc. The

potential opportunity is insignificant for these play-

ers in the overall scheme of things. The primary

motive for telecom operators can be customer

stickiness whereas for PPI issuers and BCs it is a

natural upgrading. PPIs and BCs have been facing

challenges due to restrictions on cash out at points

of sale. Also due to lack of control by sponsor

banks in pricing of services by BCs, the scalability

of the model has been in question. Banks’ motive

in payment bank is to ensure captive customers for

loan products and de-congest branch.

Barring PPIs and BCs, where the upgrading to a

payment bank is driven by commercial motives,

the motive of other participants is to ensure cus-

tomer stickiness or customer acquisition. In such

a scenario, the industry will be impacted by fierce

competition.

19GROUND VIEW GROUND VIEW 1 - 30 Apr 2015 1 - 30 Apr 2015 18

C H A L L E N G E S A N D K E Y S U C C E S S F A C T O R S

Little margin of error

The multiplicity of market players. Payment

banks will be competing with different participants

in the financial value chain (like banks, PPIs, BCs,

small banks, RRBs, Cooperative bank etc) for

same set of customer. The regulatory frame work,

corporate objective and goal would differ amongst

various participants. This could create chaos and

fierce competition leading significant pricing

pressure.

Robust risk management process. Dealing with

small ticket multiple transactions would require

robust IT infrastructure. The customer transaction

would largely be biometric enabled which would

require superior infrastructure to process this.

Since the access point would not be owned by the

bank, ensuring quality customer services would

remain a key challenge

Rising customer expectations. Customer expec-

tations are currently being shaped by experiences

outside of the banking industry, where content,

ease of use, interactions and features deliver a

more engaging and rewarding experience. This

means that new services and related technology

would need to work properly once launched, as

any technical issue potentially leading to fraudu-

lent activity or data leakage, could have a sig-

nificant impact on the reputation of the financial

institution.

Device fragmentation and tablet popularity.

Mobile banking platforms will need to continue to

be developed for multiple platforms, supported

by the current and future smart-phone market.

Apart from the established operating systems iOS,

Android, as well as Windows and Blackberry, new

operating systems such as Tizen are emerging.

Depending on their market success, these plat-

forms will also need to be serviced. In addition,

the growing success of tablets means that mobile

app developers will also need to adapt the bank-

ing solutions to the tablet experience of a wider

screen, similar to that of a PC.

Lack of lending activity. Restriction in lending

activity would keep the compress the margin.

Also from customer point of view, absence of loan

product may hinder customer acquisition. Though

payment banks can act as a business correspond-

ent for loan product but this would throw up other

challenges.

Market segmentation and understanding

customer needs. Banking needs of urban areas

would be different from those of rural areas. Ser-

vices such as tailor-made reporting and real-time

information, provided by a client-relationship

manager should help a bank to differentiate itself

from its competitors. Retail banks could primarily

consider the development of solutions to auto-

mate common banking activities such as transfer

payments, transaction histories and automated

notifications related to negative account balances

or security concerns.

Brand protection. Trust and good service are

fundamental brand values of any bank. Payment

banks appointing merchant establishment / corner

shop as cash merchants are not only delegating

the handling of customer transactions to third

parties, but also placing their brand logo in an

environment they don’t directly control. They must

find ways to ensure that trust is never undermined.

In return for the use of the logo and access to

its transactional platforms, banks must insist on

proper contractual terms with cash merchants.

The contract should define the roles and responsi-

Challenges

Key success factors

21GROUND VIEW GROUND VIEW 1 - 30 Apr 2015 1 - 30 Apr 2015 20

bilities of both bank and store. The establishment /

shops must be required to maintain confidentiality of

customers’ transactional data, and to post adequate

information so that customers are informed of ser-

vices available, fees, customer complaint procedures

and the like. The bank will need to supervise compli-

ance with contractual terms and monitor the levels

of customer service attained, both through frequent

scheduled visits and mystery shopping programs.

The bank must also put in place information systems

to track reported incidents at cash merchants, and

must be prepared to take prompt action (including

contract termination) when a pattern of misbehav-

iour or abuse emerges. Beyond ensuring the safety

of transactions, managing store branding and agent

processes is essential to maintain a consistent cus-

tomer experience and build trust in the new channel.

Incentivizing the channel of cash merchants. Pay-

ment banks need to incentivize the cash merchant

channel adequately in order to ensure that the stores

maintain a proper level of liquidity at all times, vis-

ually protect the bank’s brand presence within their

store, actively promote the service with the public,

and take the time to train customers unfamiliar with

electronic transactions. If the bank has a transac-

tion-based revenue model, customer transaction

fees can be used to compensate the cash merchant.

Increased foot-traffic and branding advantages from

this new line of business may help the store, but it

will still expect to be directly and sufficiently com-

pensated for the service.

Channel management hierarchy. Payment banks

will need an effective channel to select, sign up,

train, manage and monitor a rapidly expanding net-

work of stores. One approach is to manage the new

merchant channel in a decentralized fashion through

the existing branch management structure. In this

case regional and branch managers’ targets and

reward structures will need to incorporate adequate

performance measures for the new cash merchants.

If the payment bank does not have enough staff at

branch level to be able to take on this additional role

effectively, a second approach is to have the new

cash merchant channel managed by a centralized

team set up in parallel to the branch management

structure. In this case there will need to be an effec-

tive mechanism for capital allocation and business

planning to trade off the capabilities and aspirations

of the competing channels. Alternatively, the man-

agement of the cash merchant channel itself may be

outsourced to one or more third parties. In this case,

the payment bank will need to ensure contractually

sufficient control over the character and growth of

the channel.

Speed of roll-out. Payment banks will have sub-

stantial flexibility in terms of how to sequence the

roll-out of cash merchants, in terms of speed to scale

and geographic coverage strategy. They might start

with a presence in the vicinity of areas with migrant

workers. The experience gained can help them to

spread.

Account opening and product sales. Beyond the

provision of liquidity, cash merchants will likely play

a significant role in facilitating account opening for

prospective bank clients. The new channel will not

result in rapid market expansion if account opening

is onerous and limited. It is important to make ac-

count opening as easy and quick as possible. Going

a step further, thinking through the mechanism for

product cross-selling and up-selling is necessary

from the start, as new product placement is a key

revenue driver. Separating the sales and service

channels is one of the reasons the use of cash mer-

chants is appealing, and it is possible payment banks

may decide cash merchants play no role in product

sales initially, strictly processing deposits and with-

drawals. Nevertheless, payment banks should con-

sider to what extent cash merchants could support

the product sales process, if at all.

Strategic partnership. Strategic cooperation could

be considered for specific projects. For example

banks could join forces to identify a suitable IT

supplier to provide an established mobile banking

platform and share the development costs and

resources necessary for the development of new

solutions.

Ongoing assessment and continuous improve-

ment through customer feedback. Seeking direct

feedback from customers via a mobile banking app

or social media platforms is a crucial source of infor-

mation to assess if expectations are met. Individuals

use them to express their opinion, which should help

banking institutions to continuously improve their

services.

21GROUND VIEW GROUND VIEW 1 - 30 Apr 2015 1 - 30 Apr 2015 20

Conclusion

The idea of payment banks was mooted with the sole objective of including small businesses and low income households in formalised banking channels. The previous experience of SCBs, RRB, co-operative banks, and business correspondents has not been very encouraging owing to credit risks and the high cost of service. The objective of the payment bank is to provide basic deposit and payment solutions in a cost effective manner.

The payment bank’s business model would evolve around payment solution. The total market opportunity in remittance and cash ins-cash outs is pegged at Rs100bn. The margin from intermediation business will remain narrow ranging from 50bps to 100bps. Given the number of interested applicant, the sheer size of market opportunity does not seem to be very exciting. The object differs amongst various applicant of payment bank license. The telco and banks objective will be customer stickiness or customer acquisition and branch de-congestion whereas it will be a natural upgradation for pre-paid payment instrument (PPIs) and business correspond-ent (BCs). In such a scenario, the industry will be impacted by fierce competition.

Payment Bank a boon to commercial bank

Focus on developing business in new locations. Signing up merchant establishment is a low-investment, low-risk way to test the waters in new geographic markets. Payment bank can act as business correspondent of commercial banks for loan product but is not allowed to carry lending operation on its own. This would provide commercial bank access to potential customer segment for loan product.

De-congest Branches. Crowded banking halls and long queues are a common part of customers’ experience in India. Commercial banks can offer a better service to their existing customers by allowing them to conduct basic transactions at a range of merchant establishments / corner shops. In this fashion, commercial banks can offer more choice and con-venience to their customers; they can make their branches more appealing for higher-end customers with more sophis-ticated needs; and they can reduce the average per-trans-action cost by shifting low-value transactions (including over-the-counter bill-pay transactions of non-customers) to a cheaper, variable cost channel. Today commercial banks see transactions largely as a cost and operational burden, while most corner stores / merchant establishments would like more transactions to increase foot traffic. It’s a win-win for

corner stores / merchant establishment, commercial banks and their customers. Increased rural outreach by payment banks can provide a platform to commercial banks to shift its low value high volume transaction and focus on core activity. Cost per transaction through alternate channel is 30%-40% of cost per transaction through brick and mortar branch. The cost to asset ratio of payment banks is expected to be 0.6%-0.8% compared to ~2% for public sector bank like State bank of India. State bank of India has highest operating cost amongst public sector bank owing to its wide presence in un-banked area. De-congested branches will improve efficiency and aid the public sector giant to cut operating costs. If State Bank of India can shift even 30% of its transaction to alter-nate channel like payment bank, it can reduce its overall cost by huge margin. Rough estimates suggest that cost to asset ratio of public sector giant State Bank of India, can decline by 35bps to 40bps aiding to its return ratio.

Payment bank saving deposit offering will not impact ex-isting interest rate in saving deposit. A competitive depos-it product is a pre-requisite for customer acquisition, which is a key for a stable remittance business. The deposit product offered by payment banks is expected to provide interest rate higher than the prevailing market rate in saving deposit. Depending upon individual’s entities competitive intensity and objective, the interest rate which is likely to be offered by payment banks on its saving product can be anywhere between 5% to 6%. This will not distort the market pricing of saving deposit product as payment bank will not be able to command significant market share due to late entrant in the deposit acquisition space and operational challenges.

Pose risk to micro finance institute

The outreach to small businesses and low income household by payment bank will provide an access to commercial banks to market micro credit product. The low cost of transac-tion, proximity to customer will address the larger issue of reaching out these customer segments. Payment bank can act as collecting agents for commercial bank which will bring down the cost of operations. The loan origination can still be done by commercial bank in order to reduce credit risk. As commercial banks enjoys advantage in terms of funding cost, micro finance institutes cannot compete in terms of pricing.

The government’s thrust to include the small businesses and low income household to formal channel will create competi-tion for micro finance model. Major reason why MFIs are de-siring to enter the mainstream banking channel. Bandhan has secured universal licence and SKS Micro intends to apply for small banking license. Securing a small bank licence will be

crucial to SKS Microfinance’s long-term business prospects.

23GROUND VIEW GROUND VIEW 1 - 30 Apr 2015 1 - 30 Apr 2015 22

BY VIBHOR SINGHAL

Dr. Ganesh Natarajan a Vice Chairman and CEO, Zensar Technologies

Dr. Ganesh Natarajan is Vice Chairman & CEO of Zensar Technologies. He was the Chairman of NASSCOM in 2008-09. He is also a Founder and Board Member of Global Talent Track, a pioneer in Employability Skills Training in Asia. Ganesh’s industry responsibilities include leadership of the HBS Club of India, Chairman of the National Committee on Knowledge Management and Business Transformation and the Western Region Committee on Skills for the Confederation of In-dian Industry. He is a member of the Chairmen’s Council of NASSCOM. He is also a fellow of the Computer Society of India. Ganesh is a Director of Social Venture Partners India and Convener of SVP Pune. He has been appointed the Chairman of NASSCOM Foundation for 2014-16.

NASSCOM estimates are out. The industry expects

growth to accelerate compared to last year. What do you

think about them.

NASSCOM estimates 12-14% dollar revenue growth for the

sector. I’m confident about the acceleration in growth for the

industry due to improvement in demand scenario in US. Re-

tail sales for this quarter has improved and employment data

hints of lower unemployment which should translates into

higher confidence for companies to invest. We are witnessing

strong deal pipeline and shorter decision making cycles.

How does NASSCOM arrive at its estimates, and what

are the chances of it being close/far from the actual

numbers?

NASSCOM estimates are based on survey of industry partic-

ipants ranging from Indian IT company, MNCs and captives.

There is fair amount of data that is available for the publicly

listed companies. NASSCOM also polls companies regarding

their growth estimates for the next year. Left are GIC (Global

In-house Centres) which might not reveal that data but there

you also get some idea using their hiring numbers.

23GROUND VIEW GROUND VIEW 1 - 30 Apr 2015 1 - 30 Apr 2015 22

sourcing has three important stakeholders – CIO: decision

maker for Run the Business (RTB), Functional Head and

CTO: Change the business (CTB) especially SMAC strategies

and Chief Digital Officer (CDO) for digital transformation of

legacy systems. Vendors are actively trying to explore all the

three avenues to increase share of wallet.

SMAC is the new buzz word in the industry. How can it

cannibalise IMS?

Cannibalisation of IMS due to cloud isn’t big. It has impacted

data centre project marginally. However even large organisa-

tion are yet to completely configure their digital IT strategies.

Helping them to migrate to cloud can easily mitigate large

part of the cannibalisation impact.

Do MNC have competitive advantage in SMAC and what

is the competitive positioning among Indian IT company.

Well in consulting MNC do have a managerial advantage

however Indian It companies strategy have to dual in nature.

Agile for development of SMAC related projects and inte-

grate with the old legacy systems and as well as help them

move to cloud. The client’s comfort across incumbent is more

important as deliver capabilities across companies remain

same. Having said that, the MNCs do have better board

room access, and are able to influence decisions more – but

Indian companies are not far in terms of delivery capabilities.

Which other regions apart from US and Europe, do you

see outsourcing opportunity opening up, for Indian IT

companies?

Africa as a continent offers tremendous opportunity – Zensar

is doing really well in South Africa and Kenya. Verticals like

BFSI and retail, and mining (esp in South Africa) offer huge

growth potential. Apart from that, Australia too appears to

be attractive destination.

Talk us through what strategy Zensar is adopting, in or-

der to gain market-share in various verticals and geogra-

phies?

Zensar has partnered with BCG in the digital transformation

practice, where BCG will general management and functional

advisory part, and Zensar will be responsible for the tech-

nology part. Today Zensar operates in a 3x3x3 cube: Geog-

raphies of US, UK and Africa; Service lines of Application ,

Infrastructure and E-commerce; and verticals of Manufactur-

ing, Retail and Insurance. So almost 95% of Zensar’s reve-

nues come from within this cube and that is what we remain

focussed on.

How is the overall demand environment looking, esp in

US, and also Europe, which is now being touted as the

next big outsourcing destination?

Demand is good for companies with good business models.

Domains like SMAC are offering tremendous opportunities

and so companies with presence in those fields will benefit

from the demand environment – irrespective of the geo-

graphical presence.

Which pockets in US are witnessing strong growth and

why does Europe not form integral part of your confi-

dence.

US growth is stronger than Europe as economic revival in US

is faster. Also the markets are more open to outsourcing than

Europe. Insurance and Banking are showing signs of revival

with increase in discretionary spends towards digital and

stable budget for run the budget business. Manufacturing

firms are investing in improving data collection from external

sources as well as shop floors to increase efficiency and thus

the throughput. Retail is investing in upgrading the supply

chain of brick and mortar store as well as integrating it to

online through click and collect model. Retail companies are

also investing in creating e-commerce presence. Europe on

the other hand is suffering from slower growth and also have

varied cultural outlook across every country having different

perspective to outsourcing.

So what, according to you, are the challenges for the

Indian companies as they try to penetrate European

conglomerates?

The economic reality of European countries is quite different

and you can’t paint the whole region with same brush. So

unlike US, which one large homogeneous market, penetrat-

ing Europe is more difficult where the language and culture

changes in every 30 min flight. UK and Switzerland are fairly

mature markets, and have traditionally been awarding large

outsourcing contracts. Germany, Netherland and France have

large organisations that have already outsourced and few

other large organisations are ready to outsourcing in retail

and manufacturing industries. Spain, if you see, is trying to

portray itself as outsourcing destination rather than outsourc-

ing country. So pretty diverse region in terms of outsourcing

potential, and hence it will have to be tackled accordingly.

How has outsourcing changed over the last few years

and how do you see it transforming over the next few?

Outsourcing has undergone radical changes. Adaptive

outsourcing is replacing pure play advisors. Adaptive out-

25GROUND VIEW GROUND VIEW 1 - 30 Apr 2015 1 - 30 Apr 2015 24

Indian Economy – Trend Indicators

Monthly Economic Indicators

Quarterly Economic Indicators

Growth Rates (%) Jan-14 Feb-14 Mar-14 Apr-14 May-14 Jun-14 Jul-14 Aug-14 Sep-14 Oct-14 Nov-14 Dec-14 Jan-15 Feb-15

IIP 1.1 -2.0 -0.5 3.7 5.6 4.3 0.9 0.5 2.6 -2.7 3.9 3.2 2.6 4.7

PMI 51.4 52.5 51.3 51.3 51.4 51.5 53.0 52.4 51.0 51.6 53.3 54.5 52.9 51.2

Core sector 3.7 6.1 2.5 4.3 2.3 7.2 2.6 5.8 1.9 6.3 6.7 2.4 1.8 1.4

WPI 5.1 5.0 6.0 5.5 6.2 5.7 5.4 3.9 2.4 1.7 -0.2 -0.5 -0.4 -2.1

CPI 9.9 8.8 8.0 8.3 8.6 8.3 7.5 8.0 7.7 6.5 5.5 4.4 5.0 5.2

Money Supply 14.5 14.5 13.5 13.9 13.2 12.2 12.7 13.0 12.7 12.0 11.4 10.2 11.5 11.4

Deposit 15.7 15.9 14.6 15.1 13.8 12.2 12.7 13.2 13.0 12.4 12.2 10.6 11.9 11.8

Credit 14.7 14.4 14.3 14.1 12.8 13.1 13.1 10.6 9.4 10.8 10.7 10.6 10.4 10.1

Exports 4.3 -4.9 -3.2 5.3 12.4 10.2 7.3 2.4 2.7 -5.0 7.3 -3.8 -11.2 -15.0

Imports -18.8 -17.5 -2.1 -15.0 -11.4 8.3 4.3 2.1 26.0 3.6 26.8 -4.8 -11.4 -15.7

Trade deficit (USD Bn) -9.5 -8.3 -10.5 -10.1 -11.2 -11.8 -12.2 -10.8 -14.2 -13.4 -16.9 -9.4 -8.3 -6.8

Net FDI (USD Bn) -0.6 -0.1 2.1 2.0 4.8 2.4 3.6 2.5 2.9 2.8 1.8 4.0 5.5 0.0

FII (USD Bn) 2.6 1.5 5.4 -0.1 7.7 4.8 5.4 2.1 2.4 1.7 4.8 -0.4 6.6 0.0

ECB (USD Bn) 1.8 4.3 3.6 3.2 1.5 1.9 3.7 0.5 3.2 2.8 3.5 0.6 2.6 0.0

NRI Deposits (USD Bn) 62.1 62.2 61.0 60.4 59.3 60.2 60.1 60.9 61.8 61.4 62.0 63.0 61.9 61.8

Dollar-Rupee 292.2 294.4 303.7 309.9 312.4 315.8 320.6 318.6 314.2 315.9 316.3 319.7 327.9 338.1

FOREX Reserves (USD Bn) 295.8 291.9 293.4 296.4 287.9 284.6 280.2 275.5 276.3 283.0 291.3 295.7 292.2 294.4

Balance of Payment (USD Bn) Q2FY13 Q3FY13 Q4FY13 Q1FY14 Q2FY14 Q3FY14 Q4FY14 Q1FY15 Q2FY15Exports 72.6 74.2 84.8 73.9 81.2 79.8 83.7 81.7 85.3Imports 120.4 132.6 130.4 124.4 114.5 112.9 114.3 116.4 123.8Trade deficit (47.8) (58.4) (45.6) (50.5) (33.3) (33.2) (30.7) -34.6 -38.6Net Invisibles 26.7 26.6 27.5 28.7 28.1 29.1 29.3 26.8 28.5CAD (21.1) (31.8) (18.2) (21.8) (5.2) (4.1) (1.3) -7.9 -10.1CAD (% of GDP) 5.1 6.5 3.5 4.9 1.2 0.8 0.3 1.7 2.1Capital Account 20.7 31.5 20.5 20.6 (4.8) 23.8 9.2 19.8 18.7BoP (0.2) 0.8 2.7 (0.3) (10.4) 19.1 7.1 11.2 6.9

GDP and its Components (YoY, %) Q2FY13 Q3FY13 Q4FY13 Q1FY14 Q2FY14 Q3FY14 Q4FY14 Q1FY15 Q2FY15Agriculture & allied activities 1.8 0.8 1.6 4.0 5.0 3.7 6.3 3.8 3.2 Industry 0.1 2.0 2.0 (0.9) 1.8 (0.9) (0.5) 4.0 1.2 Mining & Quarrying (0.1) (2.0) (4.8) (3.9) - (1.2) (0.4) 2.1 1.9 Manufacturing (0.0) 2.5 3.0 (1.2) 1.3 (1.5) (1.4) 3.5 0.1 Electricity, Gas & Water Supply 1.3 2.6 0.9 3.8 7.8 5.0 7.2 10.2 8.7 Services 6.5 6.1 5.8 6.5 6.1 6.4 5.8 6.6 6.8 Construction (1.9) 1.0 2.4 1.1 4.4 0.6 0.7 4.8 4.6 Trade, Hotel, Transport and Communications 5.6 5.9 4.8 1.6 3.6 2.9 3.9 2.8 3.8 Finance, Insurance, Real Estate & Business Services 10.6 10.2 11.2 12.9 12.1 14.1 12.4 10.4 9.5 Community, Social & Personal Services 7.4 4.0 2.8 10.6 3.6 5.7 3.3 9.1 9.6 GDP at FC 4.6 4.4 4.4 4.7 5.2 4.6 4.6 5.7 5.3

25GROUND VIEW GROUND VIEW 1 - 30 Apr 2015 1 - 30 Apr 2015 24

Annual Economic Indicators and Forecasts Indicators Units FY6 FY7 FY8 FY9 FY10 FY11 FY12 FY13 FY14E FY15E

Real GDP growth % 9.5 9.6 9.3 6.7 8.6 8.9 6.7 4.5 4.7 5.5

Agriculture % 5.1 4.2 5.8 0.1 0.8 8.6 5 1.4 4.7 2.0

Industry % 8.5 12.9 9.2 4.1 10.2 8.3 6.7 0.9 (0.1) 3.0

Services % 11.1 10.1 10.3 9.4 10 9.2 7.1 6.2 6.0 6.9

Real GDP Rs Bn 32,531 35,644 38,966 41,587 45,161 49,185 52,475 54,821 57,418 60,576

Real GDP US$ Bn 733 787 967 908 953 1,079 1,096 1,008 950 993

Nominal GDP Rs Bn 36,925 42,937 49,864 56,301 64,778 77,841 90,097 101,133 113,551 125,424

Nominal GDP US$ Bn 832 948 1,237 1,229 1,367 1,707 1,881 1,859 1,878 2,056

Population Mn 1,106 1,122 1,138 1,154 1,170 1,186 1,202 1,219 1,236 1,254

Per Capita Income US$ 753 845 1,087 1,065 1,168 1,439 1,565 1,525 1,519 1,640

WPI (Average) % 4.5 6.6 4.7 8.1 3.8 9.6 8.7 7.4 6.0 3.0

CPI (Average) % 4.2 6.8 6.4 9 12.4 10.4 8.3 10.2 9.5 6.6

Money Supply % 15.5 20 22.1 20.5 19.2 16.2 15.8 13.6 13.5 12.0

CRR % 5 6 7.5 5 5.75 6 4.75 4.0 4.0 4.0

Repo rate % 6.5 7.5 7.75 5 5 6.75 8.5 7.5 8.0 8.0

Reverse repo rate % 5.5 6 6 3.5 3.5 5.75 7.5 6.5 7.0 7.0

Bank Deposit growth % 24 23.8 22.4 19.9 17.2 15.9 13.5 14.4 14.6 15.0

Bank Credit growth % 37 28.1 22.3 17.5 16.9 21.5 17.0 15.0 14.3 16.0

Centre Fiscal Deficit Rs Bn 1,464 1,426 1,437 3,370 4,140 3,736 5,160 5,209 5,245 5,136

Centre Fiscal Deficit % of GDP 4 3.3 2.9 6 6.4 4.8 5.7 5.2 4.8 4.1

Gross Central Govt Borrowings Rs Bn 1,310 1,460 1,681 2,730 4,510 4,370 5,098 5,580 5,639 5,970

Net Central Govt Borrowings Rs Bn 954 1,104 1,318 2,336 3,984 3,254 4,362 4,674 4,689 4,573

State Fiscal Deficit % of GDP 2.4 1.8 1.5 2.4 2.9 2.1 2.3 2.2 2.2 2.5

Consolidted Fiscal Deficit % of GDP 6.4 5.1 4.4 8.4 9.3 6.9 8.1 7.4 7.0 6.6

Exports US$ Bn 105.2 128.9 166.2 189.0 182.4 251.1 309.8 306.6 318.6 328.2

YoY Growth % 23.4 22.6 28.9 13.7 -3.5 37.6 23.4 -1.0 3.9 3.0

Imports US$ Bn 157.1 190.7 257.6 308.5 300.6 381.1 499.5 502.2 466.2 473.0

YoY Growth % 32.1 21.4 35.1 19.7 -2.5 26.7 31.1 0.5 -7.2 1.5

Trade Balance US$ Bn -51.9 -61.8 -91.5 -119.5 -118.2 -129.9 -189.8 -195.6 -147.6 -144.8

Net Invisibles US$ Bn 42.0 52.2 75.7 91.6 80.0 84.6 111.6 107.5 115.2 113.8

Current Account Deficit US$ Bn -9.9 -9.6 -15.7 -27.9 -38.2 -45.3 -78.2 -88.2 -32.4 -31.1

CAD (% of GDP) % -1.2 -1.0 -1.3 -2.3 -2.8 -2.6 -4.2 -4.7 -1.7 -1.5

Capital Account Balance US$ Bn 25.5 45.2 106.6 7.8 51.6 62.0 67.8 89.3 48.8 59.5

Dollar-Rupee (Average) 44.4 45.3 40.3 45.8 47.4 45.6 47.9 54.4 60.5 60.0

Source: RBI, CSO, CGA, Ministry of Agriculture, Ministry of commerce, Bloomberg, PhillipCapital India Research

27GROUND VIEW GROUND VIEW 1 - 30 Apr 2015 1 - 30 Apr 2015 26

Note

: For

ban

ks, E

BITD

A is

pre-

prov

ision

pro

fit

Phill

ipC

apita

l Ind

ia C

over

age

Uni

vers

e: V

alua

tio

n Su

mm

ary

CMP

Mkt

Cap

Ne

t Sal

es (R

s mn)

EB

IDTA

(Rs

mn)

PAT (

Rs m

n)EP

S (R

s)

EPS

Grow

th (%

) P

/E (x

) P

/B (x

) EV

/EBI

TDA

(x)

ROE

(%)

ROCE

(%)

Nam

e of

com

pany

Sect

orRs

Rs m

nFY

15E

FY16

EFY

15E

FY16

EFY

15E

FY16

EFY

15E

FY16

EFY

15E

FY16

EFY

15E

FY16

EFY

15E

FY16

EFY

15E

FY16

EFY

15E

FY16

EFY

15E

FY16

E

Baja

j Aut

oAu

tom

obile

s22

92 6

63,2

15

218

,524

2

45,3

99

44,

029

49,

995

33,

039

38,

022

114.

213

1.4

1.9

15.1

20.1

17.4

6.2

5.4

14.9

13.1

30.8

30.9

31.2

31.9

Bhar

at Fo

rge

Auto

mob

iles

1142

265

,863

6

9,66

5 8

2,89

8 1

5,18

1 1

9,02

8 8

,276

1

0,48

0 35

.545

.012

6.1

26.6

32.1

25.4

8.3

6.6

18.3

14.4

25.8

25.9

19.1

20.8

Hero

Mot

oCor

pAu

tom

obile

s27

52 5

49,6

30

291

,252

3

37,6

06

39,

735

50,

782

27,

120

36,

353

135.

818

2.0

15.5

34.0

20.3

15.1

8.4

6.6

13.8

10.8

41.3

43.7

45.6

49.7

Asho

k Le

ylan

dAu

tom

obile

s64

183

,132

1

20,0

14

141

,303

8

,486

1

2,86

9 9

83

4,7

96

0.3