perspectives 09.2009

DESCRIPTION

Perspectives 09.2009TRANSCRIPT

perspectives september 2009

macro analysisWhich country is best placed to emerge from the crisis?

asset allocation More than a rebound, a new trend

product FocusNatixis ActionsEuropeConviction

Macroeconomic Analysis

Asset Allocation

Market Data

Product Focus

News

2

4

5

6

11

Per

spec

tives

is a

Nat

ixis

Ass

et M

anag

emen

t's

pub

licat

ion

- N

atix

is A

sset

Man

agem

ent

- C

omm

unic

atio

ns D

epar

tmen

t -

Bus

ines

s D

evel

opm

ent

- co

mm

unic

atio

n-na

m@

am.n

atix

is.fr

Cover picture: © Roman Sigaev/Shutterstock.

NAtixis Asset MANAgeMeNtLimited Liability CompanyShare Capital 50 434 604,76 €RCS Number 329 450 738 ParisRegulated by AMF under n°GP 90-009Registered Office: 21 quai d’Austerlitz75 634 Paris, Cedex 13 - Tel. +33 1 78 40 80 00

www.am.natixis.com

NAtixis MultiMANAgerSubsidiary of Natixis Asset ManagementA French simplified joint-stock company Share Capital of 7 536 452 euros - RCS Number 438 284 192 ParisRegulated by AMF under n°GP 01-054Registered Office: 1-3, rue des Italiens 75009 Paris Tel. +33 1 78 40 32 00

www.multimanager.natixis.com

Publishing Director: F. LenoirEditorial Committee: T. Benoist, F. Delorme, S. de Quelen, K. Massicot, Ph. Le Mée, C. Michel, R. Monclar, F. Nicolas, C. Point, M-L. Rouy, B. Thiery, Ph. WaechterCoordination - Writing: N. ClémotHead of design: F. DupertuysContributors: L. Faure, M. Louvrier-Clerc, S. Potard

The funds mentioned in this material are not registered or authorized in all jurisdictions and may not be available to all investors in a jurisdiction. The provision of this material does not constitute an offer of services, nor an offer or recommendation to purchase or sell shares in any financial instrument. Investors should consider the investment objectives, risks and expenses of any investment carefully before investing. In the case of a fund, these can be found in the fund’s prospectus or offering memorandum, which should be read carefully before investing. If you would like further information about any of the funds, including charges, expenses and risk considerations, contact the sender of this document or your financial advisor for a free prospectus, simplified prospectus, copy of the Articles of Incorporation, the semi and annual reports, and/or other materials and translations that are relevant to your jurisdiction. Any reference to a ranking, a rating or an award provides no guarantee for future performance results and is not constant over time.

In certain cases, this material is provided by one of the Natixis Global Associates entities listed below to its clients who qualify as Professional Clients or Qualified Investors. Natixis Global Associates is the global distribution organization of Natixis Global Asset Management, the holding company of a diverse line-up of specialised investment management and distribution entities worldwide. Although Natixis Global Associates believes that the information provided in this material to be reliable, it does not guarantee the accuracy, adequacy, or completeness of such information.

• In the UK: This material is provided by Natixis Global Associates UK Limited which is authorised and regulated by the UK Financial Services Authority (register no. 190258). This material is intended to be communicated to and/or directed at persons (1) in the United Kingdom, and should not to be regarded as an offer to buy or sell, or the solicitation of any

offer to buy or sell securities in any other jurisdiction than the United Kingdom; and (2) who are authorised under the Financial Services and Markets Act 2000; or are high net worth businesses with called up share capital or net assets of at least £5 million or in the case of a trust assets of at least £10 million; or any other person to whom the material may otherwise lawfully be distributed in accordance with the Financial Services and Markets Act 2000 (Financial Promotion) Order 2005 or the (Promotion of Collective Investment Schemes) (Exemption) Order 2001 (the "Intended Recipients"). To the extent that this material is issued by Natixis Global Associates UK Limited, the fund, services or opinions referred to in this material are only available to the Intended Recipients and this material must not be relied nor acted upon by any other persons. Natixis Global Associates UK Limited, Cannon Bridge House, 25 Dowgate Hill, London, EC4R 2YA.

• In the E.U. (outside of Germany, Austria, Italy and the UK): This material is provided by Natixis Global Associates S.A. or its branch office in France, Natixis Global Associates International. Natixis Global Associates S.A. is a Luxembourg management company that is authorized by the Commission de Surveillance du Secteur Financier and is incorporated under Luxembourg laws and registered under n. B 115843. Registered office of Natixis Global Associates S.A.: 2-8 Avenue Charles de Gaulle, L-1653 Luxembourg, Grand Duchy of Luxembourg. Registered office of Natixis Global Associates International (n.509 471 173 RCS Paris): 21 quai d'Austerlitz, 75013 Paris.

• In Germany and Austria: This material is intended to be communicated to and/or directed at persons in Germany and Austria by Natixis Global Associates Germany GmbH, a tied agent of Natixis Global Associates UK Limited. In the case the fund(s) referenced within this material is/are not registered in Germany or Austria, this material is intended to be

communicated to and/or directed at persons who are (a) lawfully authorized to receive this material under the provisions of § 2 (11) paragraph of the German Investment Act or (b) Qualified Investors as defined in Article 1 (1) 5a of the Austrian Capital Market Act (“Intended Recipients”). To the extent that this material is issued by Natixis Global Associates Germany GmbH, the fund, services or opinions referred to in this material are only available to the Intended Recipients and this material must not be relied or acted upon by any other person. Registered office of Natixis Global Associates Germany GmbH (Frankfurt am Main HRB 45540): Im Trutz Frankfurt 55, Westend Carrée, 7. Floor, Frankfurt am Main 60322, Germany.

• In Italy: This material is provided by Natixis Global Associates Italia SGR, S.p.A., an investment management company (“Societa’ di Gestione del Risparmio”) registered and regulated by the Bank of Italy (registration no. 119, code no. 15143.1). Registered office: Via Larga, 4 - 20122, Milan, Italy.

• In Switzerland: This material is provided to Qualified Investors by Natixis Global Associates Switzerland Sàrl. Registered office: place de la Fusterie 12, 1204 Genève.

• In the DIFC: This material is provided in and from the DIFC financial district by Natixis Global Associates Middle East, a branch of Natixis Global Associates UK Limited, which is regulated by the DFSA. Related financial products or services are only available to persons who have sufficient financial experience and understanding to participate in financial markets within the DIFC, and qualify as Professional Clients as defined by the DFSA. Registered office: PO Box. 118257, 5th Floor, Building 8, Gate Village, DIFC, Dubai, United Arab Emirates.

this material has been prepared by Natixis Asset Management, a subsidiary of Natixis global Asset Management. Natixis Asset Management is a French asset manager authorized by the Autorité des Marchés Financiers (Code 1200009, Agreement No. gP90009) and licensed to provide investment management services in the eu.

Legal information

ContactsProspectus and sales documents required for subscription are available on demand:

n Natixis Global Associates (Operations): [email protected] or CACEIS Luxembourg (Prime Transfer Agent): [email protected] (352) 47 67 70 78n or Natixis Asset Management (Clients servicing): [email protected]

1September 2009www.am.natixis.com

philippe zaouatiHead of Business Development

In his Macroeconomic Analysis [page 2], Philippe Waechter, Chief Economist, takes a look at this autumn’s overall recovery trend in attempting to determine which of France, Germany, the United Kingdom and the United States is the best placed to emerge from the crisis. He highlights three macroeconomic indicators in order to identify more clearly the trends, reversals or inflexion points at work which are going to affect activity and outline the shape of an exit from recession.

For Franck Nicolas, Head of Global Asset Allocation & ALM, the advance indicators do not prejudge the current state of all the key economic factors (employment, external trade, real estate, etc.) but one thing is certain: the spring of 2009 marked a clear inflexion point in the crisis within a context of a calming of the banking crisis. A turning point which has not been refuted since [Asset Allocation page 4].

This issue includes also a summary of Natixis Asset Management’s international offer [page 6 to 8] with a particular focus on Natixis Actions Europe Convictions managed by Maurice Gravier [Product Focus page 9]. The I share of this fund, intended for institutional clients, has effectively been created three years ago.

On the occasion of the 25-year anniversary of Natixis Impact Nord-Sud Développement, a solidarity-based fund of Natixis Asset Management, we have chosen to focus on this pioneering Sicav in our News section. Over its 25 years of social commitment, the Sicav has sought to balance performance(1) with solidarity, notably in its ethical dimension through microcredit and microfinance [News section, page 11].

To conclude this editorial, Natixis Asset Management is the French market leader in terms of funds inflow according to EuroPerformance(2), with more than €10 billion of subscriptions during the first half, its market share increasing by 0.5 of a point over the same period to reach 14% at end June. Figures which testify to the confidence our clients afford us.

Enjoy reading it,

editorial

(1) Natixis Impact Nord-Sud Développement is an AMF-approved "International bonds and other debt securities" type open-end investment fund (SICAV). It does not guarantee capital or performance.

(2) Source: EuroPerformance as of 30/06/2009.

Per

spec

tives

is a

Nat

ixis

Ass

et M

anag

emen

t's

pub

licat

ion

- N

atix

is A

sset

Man

agem

ent

- C

omm

unic

atio

ns D

epar

tmen

t -

Bus

ines

s D

evel

opm

ent

- co

mm

unic

atio

n-na

m@

am.n

atix

is.fr

2 September 2009 www.am.natixis.com

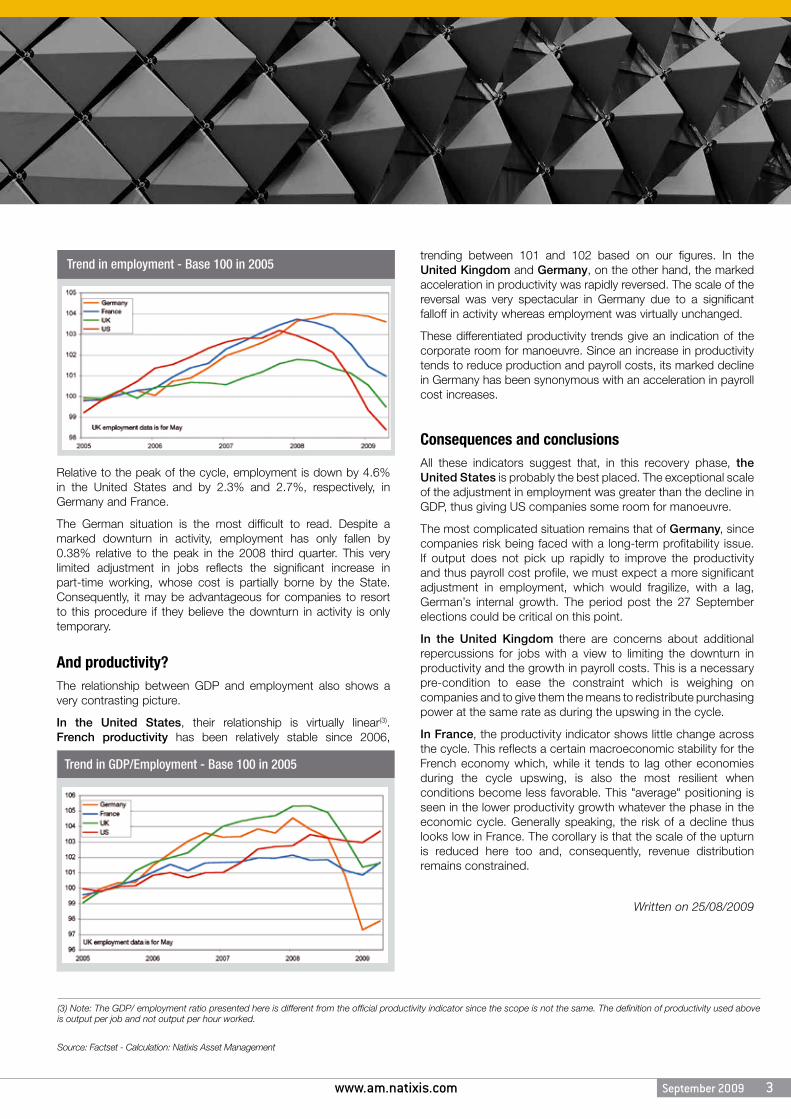

What is the GDP trend?At the end of the 2009 second quarter, French GDP was the best oriented. Relative to a base of 100 in 2005(1), it stood at 102.7 versus 102 in the United States, 101.4 in Germany and 101.1 in the United Kingdom.

France effectively performed in line with the United States in the cycle upswing(2). Over this period, the average annual growth rate was + 2.2 % in France and + 2.1 % in the United States.

Then followed a significantly decoupling: activity declined by 3.1 % in France and by 3.9 % in the United States between the peak of the cycle and the 2009 second quarter.

Germany and the United Kingdom had a rougher ride since they benefited from a spectacular performance before experiencing a significant reversal. Between 2005 and a peak during the 2008 first quarter, Germany’s average annual growth rate was 3 % and that of the UK 2.7 %. A sharp downturn then ensued: German GDP fell by 6.4 % (even taking into account the +0.3 % recovery in spring 2009) while UK GDP fell by 5.7 %.

Employment trendThe employment profiles are much more heterogeneous than those of activity.

The United States experienced a significant downturn in net employment as of the peak in the 2007 final quarter which was far more rapid than the fall in GDP.

While employment also underwent an adjustment in France and the United Kingdom, the move was of lesser magnitude than in the United States and more limited in view of the decline in activity.

Which country is best placed to emerge from the crisis?

(1) All the indicators are based at 100 in 2005, making it easier to observe present-day trends. A base of 100 on a more recent date would have tended to "compress" the data, thus limiting (visually speaking) the comparisons. The ranking on the latest points is not affected by this base.

(2) Cycle upswing: 2005 first quarter to the 2008 first quarter for France, whereas it lasted until the 2008 second quarter for the United States.

Macro Analysis

The indicators on economic activity were more encouraging in the 2009 second quarter. In Germany and France, after four quarters of decline, the growth rate again turned positive at 0.3%. In the United States, the downturn in activity slowed considerably and the trend in the employment market improved: job destruction is now well below the levels recorded in late 2008/early 2009.

Some perspective is, however, necessary in order to perceive the trends, reversals and inflexion points at work more clearly. This effectively means identifying the orientations which are going to affect activity in coming months and outline the shape of an exit from recession. This comparison is based on 4 countries: one in North America (the United States) and three in Europe (Germany, the United Kingdom and France). We have also looked at two indicators(1)

and their ratio: GDP, employment and the relationship between GDP and employment which gives an indication on the trend in productivity.

philippe WaechterChief Economist

The Context The relationship between the key macro indicators of Activity and Employment gives different signals. The productivity indicator continues to rise in the United States but is trending within a tight range in France, whereas it is slightly down in the United Kingdom and has collapsed in Germany in the absence of any jobs adjustment.

The Key PointThe activity profiles in the United States, Germany, the United Kingdom and France are broadly similar but the magnitude varies: moderate in France and the United States but very spectacular in Germany and the United Kingdom. The adjustment in employment has been more heterogoneous: drastic in the United States and limited in Germany while France and the United Kingdom have a median position.

The stakesThe productivity profile gives a powerful signal on the corporate room for manoeuvre. On this metric, the United States has the most scope whereas that of Germany is significantly constrained (an additional adjustment in employment in Germany is foreseeable if the economy does not recover rapidly). In France, the room for manoeuvre is limited since productivity tends to show little variation, whether on the upside or downside.

GDP trend - Base 100 in 2005

3September 2009www.am.natixis.com

Relative to the peak of the cycle, employment is down by 4.6% in the United States and by 2.3% and 2.7%, respectively, in Germany and France.

The German situation is the most difficult to read. Despite a marked downturn in activity, employment has only fallen by 0.38% relative to the peak in the 2008 third quarter. This very limited adjustment in jobs reflects the significant increase in part-time working, whose cost is partially borne by the State. Consequently, it may be advantageous for companies to resort to this procedure if they believe the downturn in activity is only temporary.

And productivity?The relationship between GDP and employment also shows a very contrasting picture.

In the United States, their relationship is virtually linear(3). French productivity has been relatively stable since 2006,

trending between 101 and 102 based on our figures. In the United Kingdom and Germany, on the other hand, the marked acceleration in productivity was rapidly reversed. The scale of the reversal was very spectacular in Germany due to a significant falloff in activity whereas employment was virtually unchanged.

These differentiated productivity trends give an indication of the corporate room for manoeuvre. Since an increase in productivity tends to reduce production and payroll costs, its marked decline in Germany has been synonymous with an acceleration in payroll cost increases.

Consequences and conclusionsAll these indicators suggest that, in this recovery phase, the United States is probably the best placed. The exceptional scale of the adjustment in employment was greater than the decline in GDP, thus giving US companies some room for manoeuvre.

The most complicated situation remains that of Germany, since companies risk being faced with a long-term profitability issue. If output does not pick up rapidly to improve the productivity and thus payroll cost profile, we must expect a more significant adjustment in employment, which would fragilize, with a lag, German’s internal growth. The period post the 27 September elections could be critical on this point.

In the United Kingdom there are concerns about additional repercussions for jobs with a view to limiting the downturn in productivity and the growth in payroll costs. This is a necessary pre-condition to ease the constraint which is weighing on companies and to give them the means to redistribute purchasing power at the same rate as during the upswing in the cycle.

In France, the productivity indicator shows little change across the cycle. This reflects a certain macroeconomic stability for the French economy which, while it tends to lag other economies during the cycle upswing, is also the most resilient when conditions become less favorable. This "average" positioning is seen in the lower productivity growth whatever the phase in the economic cycle. Generally speaking, the risk of a decline thus looks low in France. The corollary is that the scale of the upturn is reduced here too and, consequently, revenue distribution remains constrained.

Written on 25/08/2009

(3) Note: The GDP/ employment ratio presented here is different from the official productivity indicator since the scope is not the same. The definition of productivity used above is output per job and not output per hour worked.

Source: Factset - Calculation: Natixis Asset Management

Trend in GDP/Employment - Base 100 in 2005

Trend in employment - Base 100 in 2005

4 September 2009 www.am.natixis.com

allocation: more than a rebound, a new trend

Asset Allocation

The summer of 2009 was witness to an increasing number of encouraging signs of economic recovery, mainly in the US and Asia. For the time being, these are only leading indicators and many key economic factors such as the job market, exports or the real estate market remain grim. One thing however is certain: the springtime was marked by a clear about-face in the crisis following mitigation of the banking crisis.

Franck nicolasHead of Global Asset Allocation & ALM

Our recommendations by asset class

Fixed IncomeThe Strategic Investment Committee of Natixis Asset Management ruled in favor of credit bonds, significantly increasing their weight in all asset allocation portfolios. We are now seeing clearer signs of a recovery which will be beneficial to private bonds which were completely abandoned during the recession due to their illiquidity in connection with the large number of restructuring plans carried out over previous years and difficulties faced by banks (which are still important issuers).On the other hand, portfolios have remained underweighted in government bonds which seem to relinquish their status as safe investments as soon as the signs of recovery appear.Though it is still a bit too early to truly question the Fed’s policy to emerge from the recession, any such doubts should increase volatility on interest rate markets when raised.

EquitiesThe most dramatic rebound generally takes place between the market’s low point and the bottom of the economic cycle upon a turn-around following recession. If the market hit its bottom in March and the low point of the global cycle is observed in the fall, performance on the stock market should remain robust until then. This is why Natixis Asset Management has overweighted its share portfolios with a preference for emerging markets (strong vectors of the impending global recovery), developed Asia and Japanese markets (which profit fully from a dynamic economy in the zone). The US market was also considered,

though to a lesser degree due to its lead in the cycle. Europe was also underweighted: given the weak nature of government aid, it will probably be slower to pick up.On the heels of the market’s change of course, volatility has clearly slackened. This has sparked several categories of investors to renew their appetite for risk which is so beneficial to stock markets.

CurrenciesThough the more precocious US recovery would seem to be favorable to the Dollar, this is not necessarily the case. The Dollar served as a safe currency during the crisis, but this role is waning in the current market context which is more oriented towards recovery. Therefore, our allocation remains overweighted in Euros and exposure to commodity currencies (Australian Dollar, Canadian Dollar) has been accentuated.

CommoditiesOil, followed by agricultural raw materials and industrial metals, should profit from the impending recovery. Indeed, we have seen that these underliers progressed rapidly in unison with stock markets and credit markets, driven by one common theme: that of more intense economic growth in 2010.The performance of precious metals should however be somewhat “capped”. This, in comparison to their high value at the peak of deflationary risks. This is no longer the case now that deflationary risks are considered to be behind us.

Written on 13/09/2009

Scale from -- to ++

Risk categories Risk subcategories

Tactical allocation*

July 09(1) Aug. 09(2)

FixED incomE = =

EquiTiEs - +

FixED incomE united states - -

Euro = =uK - -Emerging countries

= =

Japan = =

Euro issuErs

corporate + +

EquiTiEs united states = +Euro - +

uK = +

Japan + =

currEnciEs Dollar = =

(against the euro)

Yen = =

Pound = =

commoDiTiEs oil = =

Gold = =

(1) Investment committee on 25/06/2009.(2) Investment committee on 30/07/2009.* weighting gap v.s. strategic allocation of an investor.

5September 2009www.am.natixis.com

Since 8 October 2008, we have seen a change in monetary policy functioning. The refinancing operations are now done at a fixed rate and the ECB grants all the liquidity requested at this rate. The aim is to be as accommodative as possible with the liquidity needs of the banks. This has also been reflected in a gradual lengthening of refinancing operations (now at 3, 6 and 12 months) with a reduction in the constraints on the nature of assets to provide for these operations.

EONIA, which had previously tracked the main refinancing rate, has changed trend since 8 October 2008, being situated slightly below the average of the refinancing rate and the marginal deposit facility rate. Since the 12-month operation on 25 June 2009, EONIA has completely decoupled with a median level situated at 0.36%. Jean-Claude Trichet does not wish to intervene more in the functioning of the money market which he sees as currently functioning 'normally' with EONIA ranging between the refinancing rate and the marginal deposit facility rate. This suggests three important points:

• As long as there are doubts about the health of the banking system and its ability to find liquidity, the ECB will intervene massively and over the long term. This is clearly what it is indicating in the latest report on financial stability. The yield curve thus enables highly profitable transformation operations for the banks;• Furthermore, the ECB will maintain a very low refinancing rate as long as the risks on economic activity remain significant; • Inflation is low and will remain below the 2% ceiling for a long time.

The ECB’s refinancing rate will probably remain at 1% until mid-2010. EONIA will remain under this level and we can thus expect a rate of 0.5% for some time to come.

The monthly Index

Source: Factset - Calculation: Natixis Asset Management From October, the 8th 2008 to August, the 13th 2009

Value 1 year 2009 CAC 40 3 426.27 -21.99% 6.47%CAC Mid 100 5 238.86 -18.51% 18.47%IT CAC 20 3 006.23 -22.70% 3.27%SBF 120 2 490.75 -21.43% 7.77%SBF 250 2 432.10 -21.45% 8.03%

Value 1 year 2009 MSCI Europe 78.37 -20.96% 12.88%Euro Stoxx 50 2 638.13 -21.67% 7.61%DAX 5 332.14 -17.71% 10.85%Footsie 4 608.36 -14.68% 3.93%

Value 1 year 2009 Dow Jones 9 171.61 -19.39% 4.50%S&P 500 987.48 -22.08% 9.33%Nasdaq 1 978.50 -14.92% 25.46%Brent Crude Future 71.70 -42.17% 57.27%

Value 1 year 2009 Nikkeï 10 356.83 -22.58% 16.90%Hong Kong 20 573.33 -9.49% 42.99%Singapore 2 659.20 -9.23% 50.96%Shanghaï 218.61 4.08% 97.09%

Value 1 year 2009 MSCI World 1 044.75 -23.56% 13.53%

Rate 1 year 2009 Eonia 0.358 % -4.023 % -1.994 %Euribor 3 months 0.893 % -4.075 % -1.999 %Euribor 6 months 1.142 % -4.014 % -1.829 %Euribor 1 year 1.355 % -4.011 % -1.694 %Fed Funds 0.180 % -1.910 % 0.090 %

Rate 1 year 2009 5 years French Treasury Bond 2.719 % -1.673 % -0.004 %5 years USTN 2.518 % -0.713 % 0.966 %10 years French Treasury Bond 3.665 % -0.866 % 0.225 %10 years USTN 3.478 % -0.462 % 1.264 %30 years French Treasury Bond 4.259 % -0.500 % 0.536 %30 years USTN 4.298 % -0.274 % 1.630 %

Value 1 year 2009 Euro/Dollar 1.418 -9.13 % 1.99 %Euro/Yen (100) 134.963 -19.97 % 7.11 %Euro/Sterling 0.855 8.58 % -11.55 %Dollar/Yen 95.195 -11.93 % 5.01 %

Money Market

Fixed Income

Currencies

France

Europe

United-States

Asia

World

ECB rates and EONIA

Market DataAs of 31/07/2009

6 September 2009 www.am.natixis.com

These 7 sub funds of the Natixis International Funds (lux) I SICAV reflect the key expertise of Natixis Asset Management

I, A EUR LU0161120547I, D EUR LU0391146155R, A EUR LU0161121271R, D EUR LU0390502184

H-I, A USD LU0390502267H-I, D USD LU0390502341I, A EUR LU0255251166I, D EUR LU0255251596R, A EUR LU0255251679R, D EUR LU0255251752

I, A EUR LU0155376477I, D EUR LU0391146072R, A EUR LU0155380156R, D EUR LU0390502770

• Investment universe: Mainly Euro denominated government or private issuers rated Investment / Diversifying fixed income assets

• Benchmark: Barclays Capital Euro Aggregate• Minimum recommended investment period: 3 years

• Investment universe: International inflation-linked bonds • Benchmark: Barclays World Government Inflation linked all

maturities Index hedged in euro• Minimum recommended investment period: 2 years• Risk Indicator: Target tracking-error ex ante of 2%(maximum)

• Investment universe: Mainly Euro-denominated investment grade debt securities issued by OECD as well as cash, money market instruments or other securities

• Benchmark: Barclays Euro Aggregate Corporate Index• Minimum recommended investment period: 3 years

Isabelle Delannée-Méric

Sophie Potard

Christine Barbier

Benefit from a broad range of fixed income investment opportunities

Get the most out of diversification in inflation-indexed bonds in a global universe

Benefiting from the SRI expertise of Natixis Asset Management through a socially responsible portfolio of

investment grade corporate bonds

Natixis Euro Aggregate Plus Fund

Natixis Global Inflation Fund

Natixis Impact Euro Corporate Bond Fund

See the full prospectus which is the only legally binding document.

Overwiew of our international Product rangesub funds of the niF (lux) i sicaV managed by natixis am

7September 2009www.am.natixis.com

I, A EUR LU0147917792I, A USD LU0095830922I, D USD LU0095831060R, A EUR LU0147918923R, A USD LU0084288595R, D USD LU0084288678

I, C EUR LU0095828512I, D EUR LU0095828785R, C EUR LU0066549592R, D EUR LU0066549832

I, A EUR LU0095827381I, D EUR LU0095828272R, A EUR LU0064070138R, D EUR LU0064070211

I, A EUR LU0389329003I, D EUR LU0389329185R, A EUR LU0389329342R, D EUR LU0389329425

• Investment universe: Emerging Europe Equities• Benchmark: None (MSCI Emerging Europe Index: indicative only)• Minimum recommended investment period: 5 years• Risk Indicator: Target tracking-error ex ante between

6 and 10

• Investment universe: European Small and Mid Equities• Benchmark: None (MSCI Europe Small Caps NDR: indicative only)• Minimum recommended investment period: 5 years• Risk Indicator: Target tracking-error ex ante between 4 and 7

(indicative)

• Investment universe: Eurozone Equities• Benchmark: None (MSCI EMU NDR: indicative only)• Minimum recommended investment period: 5 years

• Investment universe: European equities• Benchmark: None (MSCI Europe: indicative only)• Minimum recommended investment period: 3 years

Matthieu Belondrade François Théret

Thierry Cuypers

Olivier Lefèvre

Christine Lebreton

Get the most out of the growth in the emerging European zone as part of a conviction management strategy

Benefiting from the potential of European Small & Midcaps within the scope of a

conviction-based strategy

Tapping the potential of Eurozone value equities within the scope of a conviction-based strategy

Active and responsible investing to maximise SRI value added

Natixis Europe Smaller Companies Fund

Natixis Euro Value Fund

Natixis Impact Europe Equities Fund

See the full prospectus which is the only legally binding document.

Natixis Emerging Europe Fund

8 September 2009 www.am.natixis.com

Overwiew of our international Product rangeFunds of natixis asset management available through private placement

25 complementary funds covering all asset classes are available through Private Placement. This quarterly reviewed list of funds aims to provide Natixis Global Associates' teams* with the most innovative products of Natixis Asset Management and to offer a wider range of expertise.

Fixe

d in

com

e

Natixis Souverains Euro 1-3 I: FR0010208421

Natixis Souverains Euro 3-5 FR0010036400

Natixis Souverains Euro 5-7 FR0010201699

Natixis Souverains Euro 7-10 FR0000449092

Natixis Souverains Euro RC: FR0000003196

Natixis Inflation Euro I: FR0007475413 R: FR0010170944

Natixis Crédit Euro I: FR0010171108 R: FR0010690966

Natixis Convertibles Euro I: FR0010658963 R: FR0010660142

Natixis Convertibles Europe C: FR0010171678

Alte

rn.

Natixis Constellation European Event IC: LU0161071237 IC: LU0161073951

Alpha Hedge + RC: FR0010058453

Abso

lute

re

turn Natixis Absolute Quant Bond 18 M I: FR0010232348 R: FR0010249219

Natixis Absolute Swap Arbitrage IC: FR0010654921 RC: FR0010657924

Bala

n-ce

d Réactis Emerging I: FR0010634345 RC: FR0010626218

eq

uiti

es

Natixis Actions Europe Dividende IC: FR0010582478 RC: FR0010573782

Natixis Impact Life Quality C: FR0010410274 E: FR0010458539

Natixis Actions US Value I: FR0010256412 R: FR0010236893

Natixis Actions US Growth I: FR0010256404 R: FR0010236877

Natixis Actions Europe Convictions C: FR0010346429

Sonic Monde I: FR0010555797 RC: FR0000993446

Mo

ney

Mar

ket Natixis Cash Première C: FR0010157834

Natixis Cash A1P1 C: FR0010322438

Natixis Impact Cash C: FR0010008003

Natixis Cash Eonia I: FR0010298943 R: FR0007084926

Natixis Tréso Euribor 3 Mois FR0000293714

These funds are authorized for sale in France and possibly in other country(ies) where their sale is not contrary to local legislation. Please refer to legal information of this material.

* Natixis Global Associates is a global distribution platform which brings their investment expertise of the affilliated investment managers to clients outside France.

Asset class Fund name Share and ISIN code

9September 2009www.am.natixis.com

Product Focus

maurice GraVierPortfolio manager of Natixis Actions Europe Conviction

natixis actions europe conviction

What is the fund's strategy?

Natixis Actions Europe Conviction aims to outperform its benchmark index, MSCI Europe, over a recommended investment horizon of 5 years. The investment team concentrates the portfolio on the strongest convictions of Natixis Asset Management’s European equities team, i.e. 20 to 40 stocks. If the Equity team sees no new opportunities, the fund may hold up to 20% in cash. Natixis Actions Europe Conviction invests mainly in stocks with a market capitalisation of over €500 million. This strategy means that the portfolio’s tracking error can go up to 8% (by way of indication).

Focus on Natixis Actions Europe Convictions and its conviction-based management: the I Share of this fund intended for institutional clients is celebrating its three-year anniversary.

What are the key stages in the investment process?

The investment team of Natixis Actions Europe Conviction tests each investment idea suggested by the specialists. The fund managers then sort the ideas according to the stock’s upside potential in absolute terms, combined with a risk level and a degree of confidence. The final portfolio thus comprises 20 to 40 stocks. Positions, of which the weight on acquisition represents 2 % to 5 % of assets, are calibrated based on each stock’s specific criteria, their contribution to risk and the portfolio’s global composition.

Besides the selectivity of investment ideas, the investment team complies with a strict buy and sell discipline, when target prices are met, when expected catalysts materialise or when an unfavourable event occurs, in order to optimise entry points and profit-taking. The investment team uses options on equities marginally, in order to maximise a position’s risk/reward profile and offer the best of European equities at any given moment.

What are the source of performance?

The investment team of Natixis Actions Europe Conviction pools the best ideas of a team of experts. Based on the premise that a manager cannot single-handedly grasp the range and complexity of the universe of European equities, the fund manager relies on the recommendations of 30 Natixis Asset Management managers-analysts. These managers-analysts are spread into 4 macro-sectors, comprising 15 sector experts, and 4 peripheral sectors grouping specialists of emerging European mid-caps, quantitative management and special situations.

Defensives

sector ideas(large cap)

Idea generation sources in European universe

thematic ideas

tMt* small and mid cap

special situations(ie : M&A)

emerging europe

Cyclical Financial Quantitative

* Technology, Médias, Telecoms.

n A conviction-based management covering a broad universe of European equities

n The mastery of a team of 30 experts in European equities

n A flexible, reactive management approach, well-adapted to market configurations

KEY POINTS

OVERVIEW

investment universe European equities (mainly stocks with a market capitalisation of over €500 million)

Benchmark MSCI Europe NDR

Minimum recommended investment period 5 years

risk indicator Ex-ante tracking error of up to 8 (by way of indication)

10 September 2009 www.am.natixis.com

I Share R Share

Management company Natixis Asset Management

Legal form French mutual fund (FCP)

UCITS compliant Yes

Inception date 4 December 2001

Accounting currency EUR

ISIN / Allocation of income FR0010346429 / Accumulation FR0010756866 / Accumulation

Maximum operating and management fees including taxes 1%* 2%*

Maximum subscription fee

not paid to the fund None 3%**

paid to the fund None None

Maximum redemption fee

not paid to the fund None None

paid to the fund None None

Performance fee including taxes 20% of performance above MSCI Europe NDR***

Minimum share fraction One ten-thousandth One ten-thousandth

Minimum initial subscription / subsequent k 50 000 / One ten-thousandth

One ten-thousandth / One ten-thousandth

Initial Net Asset Value k 101 k 100

Net Asset Value calculation Daily

Cut-off time D 15:30 (CET)

FUND FEATURES

* Basis: net assets ** Excluding any exoneration *** For R Share, from January, 1st 2010

Conviction and Volatility?

A management of conviction, as part of a fundamental approach, implies a sufficiently long investment period to enable catalysts to materialise and inefficiencies to be corrected. Our approach is therefore a long-term one. A question arises, however, at times of high volatility: what is the impact on our conviction-based management? In terms of portfolio construction, when volatility is high, we reduce sector plays to limit the systematic risk and neutralise irrational rotations. Moreover, with regard to stock-picking, we focus on a limited number of positions with clear valuations, enabling us to react instantly: non-fundamental movements thus generate buy and sell opportunities.

The main risk presented by Natixis Actions Europe Conviction is the equity risk. Tracking-error can go up to 8 % (by way of indication) owing to the investment team’s leeway in relation to the MSCI Europe index. Control of the portfolio’s ex-ante risk is performed by the front office, quantitatively and qualitatively. The main active plays, the performance and consistency of the portfolio with the views of Natixis Asset Management are monitored continuously.

At Natixis Asset Management, the Equity management team comprises 35 fund managers, specialised by sector, market segment and management technique, with assets under management of €25,7 billion as of 31 March 2009. The European Equities team has 30 portfolio managers-analysts. The conviction-based approach applied to the Natixis Actions Europe Conviction fund makes the most of this cross-divisional organisation, combining the value added of expertise with the risk assessment founded on 20 years of core management.

Source: Natixis Asset Management

INVESTMENT TEAM

RISK MANAGEMENT

11September 2009www.am.natixis.com

Natixis Impact Nord-Sud Développement is celebrating its 25th anniversary. During those 25 years, this SICAV, based on an original concept, has looked to combine solidarity and performance*.

A pioneering SICAV

Launched in 1984, this SICAV was one of the first to be aimed at investors wanting to participate actively in the development of countries in the southern hemisphere through the investment of savings from northern hemisphere countries. This pioneering fund incorporated a commitment to promoting development within a classic investment process.

Natixis Impact Nord-Sud Développement thus provides an opportunity to invest in supranational institutions (World Bank, European Bank for Reconstruction and Development) financing major infrastructure projects, in emerging market bonds that have been screened on the basis of the World Bank's aggregate Worldwide Governance Indicators** and in microcredit institutions, which provide credit to the most underprivileged sections of society that do not have access to traditional funding sources.

Natixis Impact Nord-Sud Développement: 25 years of commitment

News

A highly topical "microcredit" componentAccording to the portfolio manager Sophie Potard, the exposure to microcredit institutions is one of the aspects of Natixis Impact Nord-Sud Développement that makes this solidarity fund so relevant today: “The subprime crisis has had unprecedented financial and economic repercussions, reviving interest in values that go beyond simply seeking performance. More than ever, solidarity is growing in importance, and with it the concept of solidarity.”

*Natixis Impact Nord-Sud Développement is an AMF-approved "International bonds and other debt securities" type open-end investment fund (SICAV). It does not guarantee capital or performance.

**The Worldwide Governance Indicators (WGI Index) : this composite index produced by the World Bank analyses 6 criteria for 212 countries, namely democracy, political stability, government effectiveness, regulatory quality, rule of law and control of corruption.

A COMMITTED fund and a dedicated communication campaign

The choice of the key word for the communication campaign dedicated to Natixis Impact Nord-Sud Développement was obvious:

“COMMITTED - Natixis Impact Nord-Sud Développement: 25 years of commitment to

combining solidarity with performance”

A special conference held on September 15: clients of Natixis Asset Management will meet Christophe Point, Head of Sales at Natixis Asset Management and Director of the SICAV; Sophie Potard, Porfolio Manager; Pierre Van Peteghem, Group Treasurer at AFDB (African Development Bank); and Alka Couet, Voluntary Consultant at SIDI (Société Internationale pour le Développement de l’Investissement), an international investment development institution, long-standing partner of the SICAV.

A press breakfast meeting on the SICAV is also scheduled on September 23.

Sophie Potard

COMMITTED.NATIxIS IMPACT NOrD-SuD DévELOPPEMENT

25 yEArS Of COMMITMENT TO COMBINING SOLIDArITy wITH PErfOrMANCE*

• Invest in a solidarity fund with 25 years of experience, particularly in the financing of microcredit programs

• Benefit from the potential performance of supranational bonds or emerging market securities selected through an active management process

• Provide real support to economic and social development projects

*Non-contractual document. Natixis Impact Nord-Sud Développement is an AMF-approved "International bonds and other debt securities" type open-end investment fund (SICAV). It does not guarantee capital or performance. The fund's simplified prospectus must be provided to the investor prior to purchase. This prospectus can be obtained from Natixis Asset Management or at www.am.natixis.com

Natixis Asset Management - AMF authorization no. GP 90-009 – Paris Trade and Companies Register (RCS) 329 450 738