performance review note q3 fy2014-15brands & retail segment excludes figures of arvind internet...

TRANSCRIPT

5th February 2015, Ahmedabad

Performance Review Note Q3 FY2014-15

2

Agenda

• Financial Performance: Consolidated

• Financial Performance: Standalone

• Business Analysis

3

Agenda

• Financial Performance: Consolidated

• Financial Performance: Standalone

• Business Analysis

4

2,074

1,772

500

1,000

1,500

2,000

2,500

17%

Q3 13-14 Q3 14-15

Rev, Rs Cr

288249

0

100

200

300

16%

Q3 14-15 Q3 13-14

EBITDA, Rs Cr

112103

0

50

100

150

PAT*, Rs Cr

9%

Q3 14-15 Q3 13-14

Financial Performance: Q3 2014-15 Consolidated Revenue growth of 17% and EBITDA growth of 16%

Strong growth in revenues... ...with steady weighted margins

*PAT before exception item

5

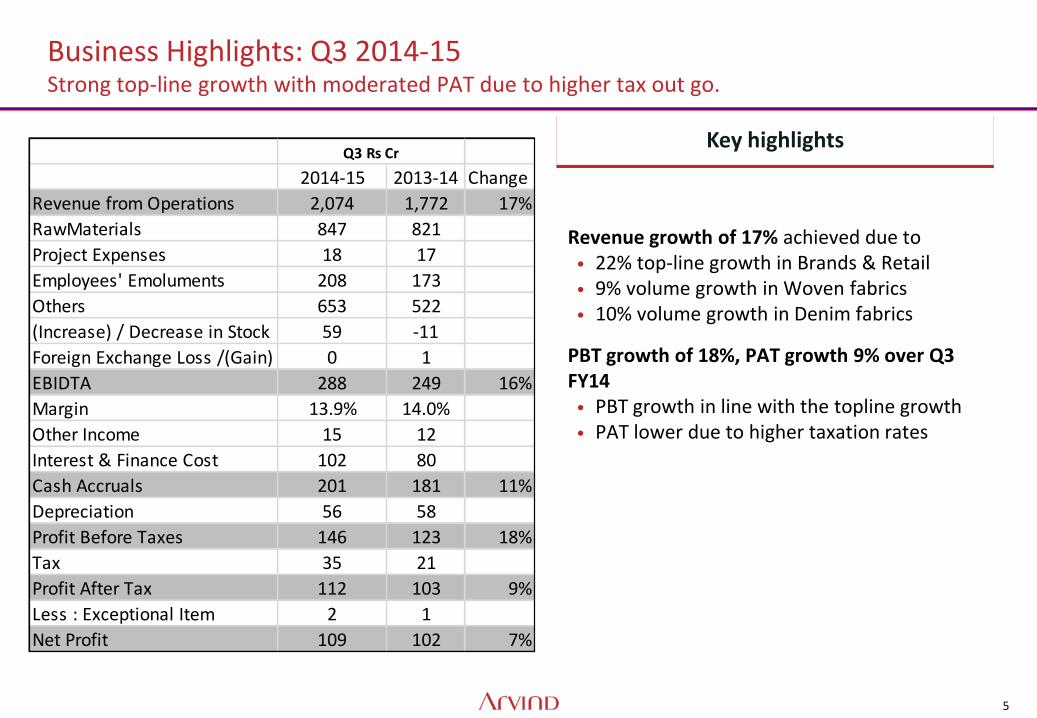

Business Highlights: Q3 2014-15 Strong top-line growth with moderated PAT due to higher tax out go.

Key highlights

Revenue growth of 17% achieved due to • 22% top-line growth in Brands & Retail • 9% volume growth in Woven fabrics • 10% volume growth in Denim fabrics

PBT growth of 18%, PAT growth 9% over Q3 FY14 • PBT growth in line with the topline growth • PAT lower due to higher taxation rates

2014-15 2013-14 Change

Revenue from Operations 2,074 1,772 17%

RawMaterials 847 821

Project Expenses 18 17

Employees' Emoluments 208 173

Others 653 522

(Increase) / Decrease in Stock 59 -11

Foreign Exchange Loss /(Gain) 0 1

EBIDTA 288 249 16%

Margin 13.9% 14.0%

Other Income 15 12

Interest & Finance Cost 102 80

Cash Accruals 201 181 11%

Depreciation 56 58

Profit Before Taxes 146 123 18%

Tax 35 21

Profit After Tax 112 103 9%

Less : Exceptional Item 2 1

Net Profit 109 102 7%

Q3 Rs Cr

6

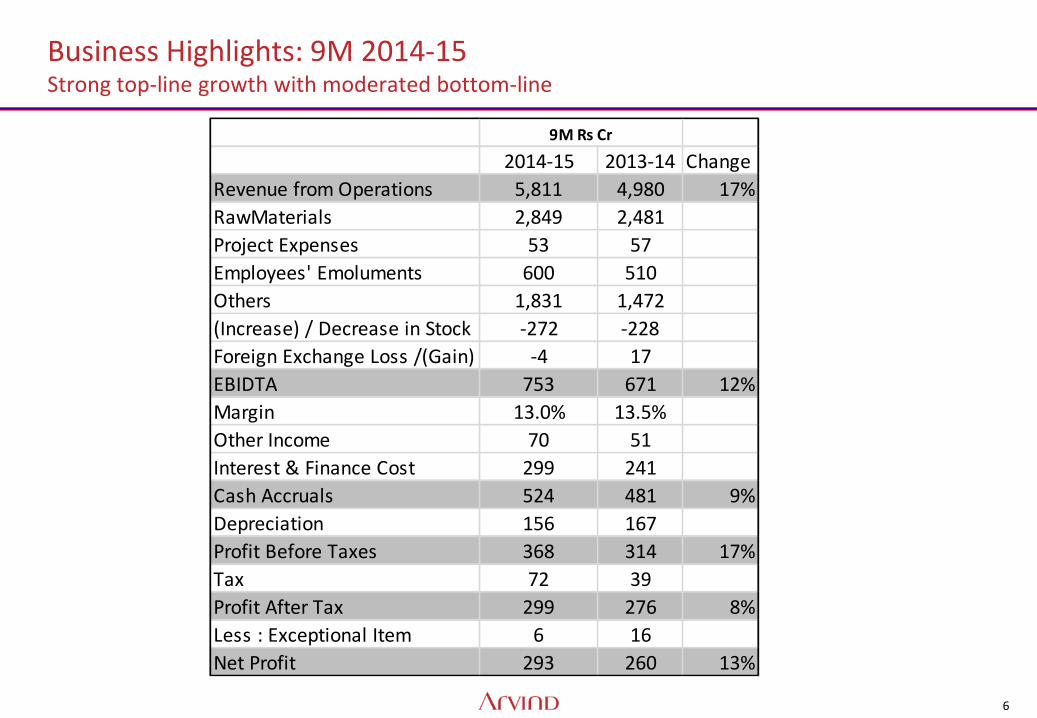

Business Highlights: 9M 2014-15 Strong top-line growth with moderated bottom-line

2014-15 2013-14 Change

Revenue from Operations 5,811 4,980 17%

RawMaterials 2,849 2,481

Project Expenses 53 57

Employees' Emoluments 600 510

Others 1,831 1,472

(Increase) / Decrease in Stock -272 -228

Foreign Exchange Loss /(Gain) -4 17

EBIDTA 753 671 12%

Margin 13.0% 13.5%

Other Income 70 51

Interest & Finance Cost 299 241

Cash Accruals 524 481 9%

Depreciation 156 167

Profit Before Taxes 368 314 17%

Tax 72 39

Profit After Tax 299 276 8%

Less : Exceptional Item 6 16

Net Profit 293 260 13%

9M Rs Cr

7

B & R Revenue growth moderate and Margin impacted due to weak festive season: Textile growth in line with expectation

Brands & Retail Textiles

EBITDA %, Q3 Vs LY

Revenue, Q3 Vs LY

0.02.5

5.07.5

10.0

Q3 13-14 Q3 14-15

7.0% 8.1%

EBITDA %

MM 3.4%, Other 8.5%

MM 7.4%, Other 9.0%

661544

0

500

1,000

Revenue, Rs Cr

22%

Q3 14-15 Q3 13-14

10

15

20

Q3 13-14

17.6%

EBITDA %

Q3 14-15

18.0%

1,2751,173

0

500

1,000

1,500

Revenue, Rs Cr 9%

Q3 14-15 Q3 13-14

9% volume growth in Woven

& 10% Volume growth in Denim

*Brands & Retail segment excludes figures of Arvind Internet Limited

8

Consolidated Balance Sheet, as at Dec 31st 2014

Rs Crs

31st

Dec'14

30th

Sept'14

Shareholders' Fund

Share Capital 258 258

Reserves and Surplus 2433 2328

Share application Money pending allotment0 0

Non Current Liabilities 1517 1462

Shortterm Borrowings 1828 1767

Current Liabilities 1827 1981

Minority Interest 34 33

Total 7897 7828

Assets

Fixed Assets 3243 3188

Non -Current Investment 57 57

Long Term Loans and Advances 607 624

Other Non Current Assets 7 8

Current Assets 3983 3951

Total 7897 7828

As at

9

Key Financial Ratios

2013-14 Q1 14-15 Q2 14-15 Q3 14-15 9M 14-15

EPS 14.4 3.5 3.7 4.3 11.4

Debt / Equity 1.16 1.28 1.34 1.34 1.34

Debt / EBIDTA 3.0 3.4 3.2 3.0 3.3

ROCE 13.5% 13.7% 14.5% 15.6% 14.0%

ROE 14.0% 14.3% 14.9% 16.6% 14.8%

Revenue Growth 30% 17% 14% 17% 17%

Current Ratio 2.3 2.1 2.3 2.6 2.6

Inventory Turn 4.2 3.9 4.0 4.4 4.1

Interest Cover 2.8 2.6 2.7 3.0 2.8

Asset Turn 1.2 1.2 1.0 1.1 1.0

10

Agenda

• Financial Performance: Consolidated

• Financial Performance: Standalone

• Business Analysis

11

Standalone Financial Performance Q3 14-15

2014-15 2013-14 Change

Revenue from Operations 1,330 1,205 10%

RawMaterials 563 553

Project Expenses 2 2

Employees' Emoluments 146 128

Others 432 343

(Increase) / Decrease in Stock -32 -19

Foreign Exchange Loss /(Gain) -2 -3

EBIDTA 222 201 11%

Margin 16.7% 16.7%

Other Income 22 17

Interest & Finance Cost 82 68

Cash Accruals 163 150 9%

Depreciation 31 40

Profit Before Taxes 132 110 20%

Tax 30 15

Profit After Tax 102 95 8%

Less : Exceptional Item 2 1

Net Profit 99 94 6%

Q3 Rs in Crs

12

Balance Sheet, as on 31st Dec 2014

31st

Dec'14

30th

Sept'14

Shareholders' Fund

Share Capital 258 258

Reserves and Surplus 2538 2441

Share application Money pending allotment0 0

Non Current Liabilities 1253 1257

Shortterm Borrowings 1435 1371

Current Liabilities 972 1001

Minority Interest

Total 6456 6329

Assets

Fixed Assets 2661 2615

Non -Current Investment 806 728

Long Term Loans and Advances 388 392

Other Non Current Assets 0 0

Current Assets 2601 2594

Total 6456 6329

As at

13

Agenda

• Financial Performance: Consolidated

• Financial Performance: Standalone

• Business Analysis

14

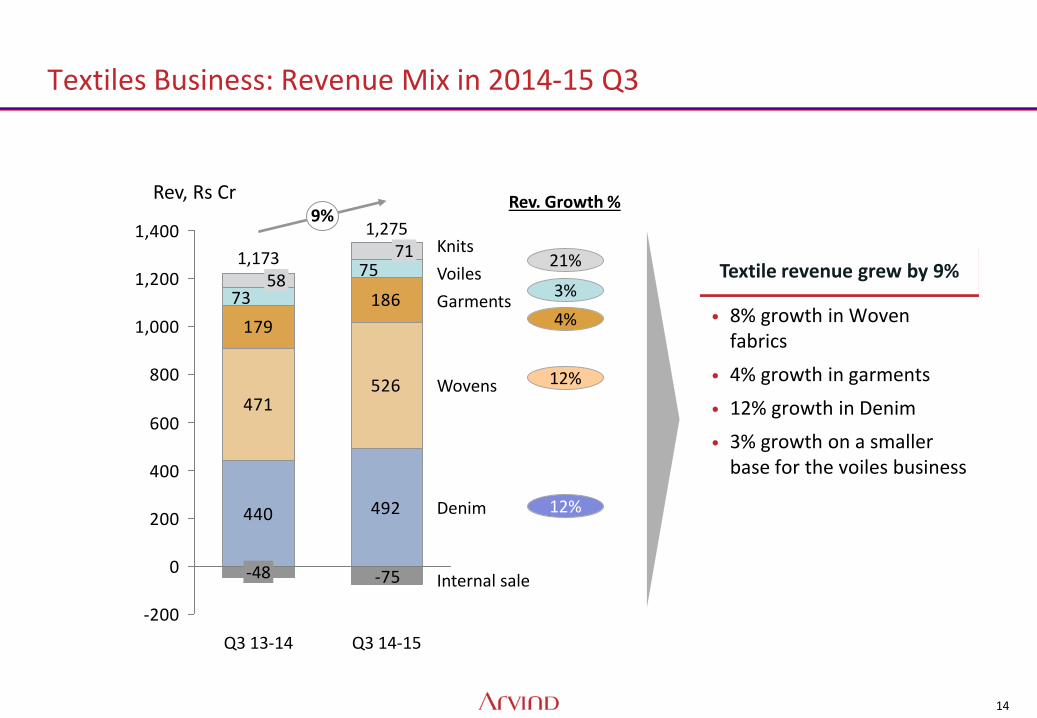

Textile revenue grew by 9%

Textiles Business: Revenue Mix in 2014-15 Q3

440 492

471526

179

186

-75

75

73

-200

0

200

400

600

800

1,000

1,200

1,4009%

Internal sale

Denim

Rev, Rs Cr

Garments

Knits

Wovens

Voiles

-48

1,173 58

71

Q3 13-14

1,275

Q3 14-15

• 8% growth in Woven fabrics

• 4% growth in garments

• 12% growth in Denim

• 3% growth on a smaller base for the voiles business

21%

3%

4%

12%

12%

Rev. Growth %

15

Volume growth: Denim volumes growth at 10%, while Wovens achieved 9% volume growth in Q3 14-15

29.827.3

0

10

20

30

9% Volume, Mn Mtrs

Q3 13-14 Q3 14-15

26.824.2

0

10

20

30

Q3 13-14 Q3 14-15

Volume, Mn Mtrs +10%

Denim Wovens (Shirting & Khaki)

Q3 comparison

Vs LY

83.577.0

0

50

100

9M 14-15

8% Volume, Mn Mtrs

9M 13-14

80.176.7

0

50

100

9M 14-15

+4%

9M 13-14

Volume, Mn Mtrs

9M comparison

Vs LY

16

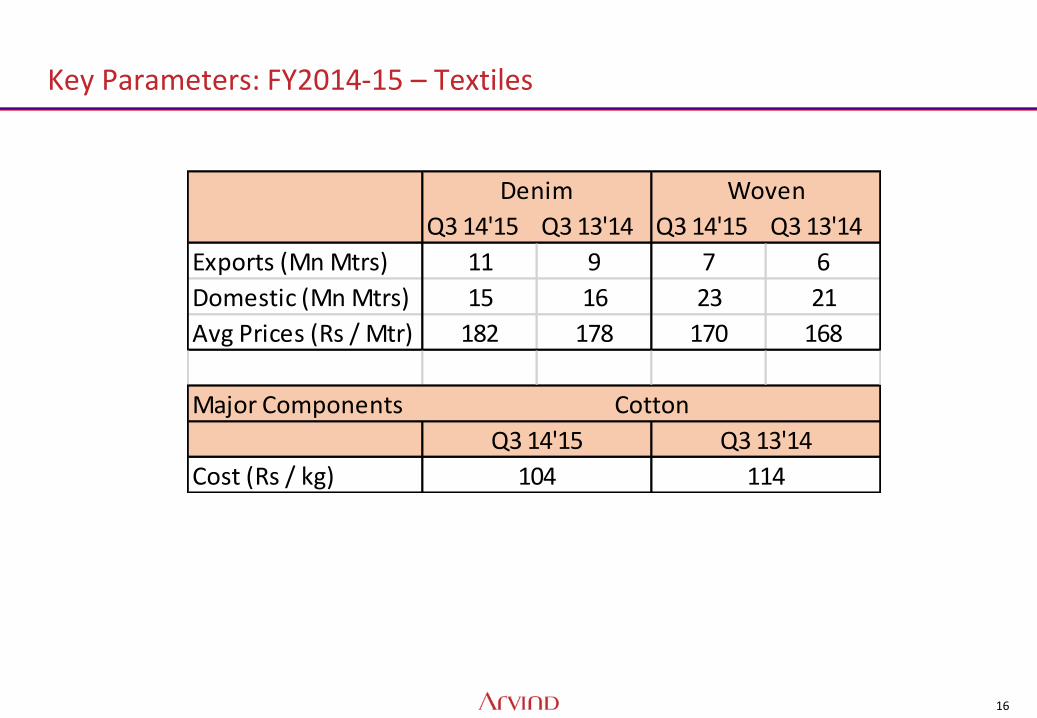

Key Parameters: FY2014-15 – Textiles

Q3 14'15 Q3 13'14 Q3 14'15 Q3 13'14

Exports (Mn Mtrs) 11 9 7 6

Domestic (Mn Mtrs) 15 16 23 21

Avg Prices (Rs / Mtr) 182 178 170 168

Major Components

Cost (Rs / kg)

Denim Woven

Cotton

Q3 14'15 Q3 13'14

104 114

17

Brands & Retail – Financial Performance: Q3 FY15 Revenue Growth of 22% despite subdued festive season

661544

0

200

400

600

800

Revenue, Rs Cr

22%

Q3 14-15 Q3 13-14

Strong revenue growth Key highlights

• Revenue growth of 22% achieved due to

31% revenue growth in Brands /other formats

3% revenue de-growth in Mega-Mart Retail

Like to Like growth

1.9% LTL growth in Brands

(-)2.3% LTL growth in Mega-Mart Retail

Margin lowered

Margin lowered from 8.1% in Q3 FY14 to 7% in Q3 FY 15

0

2

46

8

10

EBITDA %

Q3 14-15

7.0%

Q3 13-14

8.1% MM 3.4%, Other 8.5%

MM 7.4%, Other 9.0%

*Brands & Retail without Arvind InternetLimited

18

Performance of Power Brands

3748

0

30

60

0

5

10

15

Q3 FY14

12.8%

Q3 FY15

13.4%

EBITDA Rs Cr EBITDA %

360288

0

200

400

Q3 FY14 Q3 FY15

Revenues Rs Cr +25% Power brands

EBITDA Rs Cr EBITDA % Revenue Rs Cr

Q3 FY15 Vs Q3 FY14 YTD FY15 Vs YTD FY14

88 112

0306090

120

0

5

10

15

YTD FY14

EBITDA % EBITDA Rs Cr

11.4% 11.5%

YTD FY15

978776

0

500

1,000

YTD FY14

+26%

YTD FY15

Revenues Rs Cr

Note: 1. EOSS = ‘End of Season Sale’ period 2. Note: Tommy Hilfiger numbers reflect 50% Arvind share of the JV company

19

• Sales Increase in Key Account Counters: Growth of 27% in Q3 14-15

• ** 2014-15 figures include Calvin Klein

Brands & Retail Business – Distribution

Particulars Q4 2013-14 Q1 2014-15** Q2 2014-15** Q3 2014-15**

# Stores Sq ft # Stores Sq ft # Stores Sq ft # Stores Sq Ft

Brands 698 717,236 741 7,54,529 761 765,450 800 7,89,753

MM 166 744,785 158 7,96,467 146 806,143 145 8,42,078

Total 864 1462021 899 15,50,995 907 1,571,593 945 1,631,831

No of KA Exclusive Counters

692 810 819 923

20

Outlook for FY2014-15

• Revenue growth expected to be 14-15%

– Sales prices of textile products to fall in Q4 in line with fall in cotton/yarn prices

• International demand for textiles strong: Indian retail demand very sluggish due to failed festive season

• Cotton prices, which witnessed sharp correction are likely to remain stable at current levels

• Company expects that weighted margins for the current year to be slightly lower than last year

– Margin for textiles business and B & R business likely to be maintained/marginally better

Thank You