performance audit of production sharing contracts relating to hydro carbon exploration and...

TRANSCRIPT

PERFORMANCE AUDIT OF PRODUCTION SHARING CONTRACTS RELATING TO HYDRO CARBON EXPLORATION AND PRODUCTION.

Government of India (GOI) offered acreages for exploration in 1980, 1982 and 1986

GOI further liberalized the petroleum exploitation and exploration policy in 1991

New Exploration Licensing Policy

A more attractive policy was formulated by the Government in 1999 and designated as the New Exploration Licensing Policy (NELP)

Exploration blocks in onshore and offshore to offered to domestic private parties, NOCs and foreign parties on global bidding to accelerate exploration and exploitation of hydrocarbon and for induction of new technology

Production Sharing Contracts

The Government of India signed Production Sharing Contracts (PSCs) for 28 exploration blocks under Pre-NELP rounds since 1993

12 blocks have been relinquished / surrendered

At present, 12 exploration blocks are under operation and 4 block are awaited for approval of additional exploration

New Exploration Licensing Policies (NELP) - I to VI Ist round- GOI invited bids in Jan,

1999 for 48 blocks 2nd round- GOI invited bids in Dec

2000 for 25 blocks 3RD round- GOI invited bids in March

2002 for 27 blocks (9-Deepwater,7-shallow and 11-onland, out of which PSCs signed for 9,6 and 8 respectively )

NELP – I to VIcontd….

4th round- GOI invited bids in May, 2003 for 24 blocks (12 -deepwater , 1 -shallow and 11- onland, out of which, PSC’s signed for 20 exploration blocks comprising 10 deepwater and 10 onland)

5th round- twenty exploration blocks have been awarded to different consortiums/ individual company. A total of two discoveries have been made in KG deepwater block

6th round- GOI invited bids in Feb, 2006 (highest offering so far) for 52 blocks and 165 bids received by bid closing date. (PSC’s signed for 52 exploration blocks comprising 21 deepwater, 6 shallow water and 25 onland.

28

75

48

2725 25

23 23

27

23 23 2421 20 20 20 20

5552 52

0

10

20

30

40

50

60

No. of blocks offered No. of blocks bid for Blocks Awarded

AUDIT GOAL

To assess the effectiveness of production sharing contracts (PSCs) in achieving the objectives of petroleum exploration and production policies of Government of India.

Audit Objectives

Audit objectives – to verify whether Systems/ procedures of Ministry/

Directorate General of Hydrocarbons (DGH) to monitor and ensure compliance with PSC terms were adequate and effective;

Revenue interests of GoI were properly protected and adequate and effective mechanisms were in position

9

AUDIT OBJECTIVES

To examine that the objectives of increase in explorable base, reserve accretion and production have been achieved under Pre-NELP and NELP regime.

To examine whether the procedure for selection of exploration blocks under pre-NELP and NELP regime is adequate, well defined and consistently followed.

AUDIT OBJECTIVES CONTD.

To examine whether formulation of Bid Evaluation Criteria (BEC) and Bid Evaluation process under various exploration rounds are fair, transparent, competitive, consistent and in accordance with policy objectives.

To review whether contracts are as per terms of model PSC (MPSC), approved guidelines and best practices.

To review the performance of pre-NELP/NELP blocks and fields in adherence to provisions of signed PSC.

DETAILED SUB OBJECTIVES

28 sub objectives to the main objectives which can be categorised under selection of blocks, formulation of BEC, evaluation of bids, compliance with PSC terms and conditions, crude/gas pricing, remittance of royalty, Govt.’s share of profit petroleum, etc.

Justification for performance audit

Risk Assessment - High Media reports –

award of blocks monitoring of PSCs fixation of gas price gold plating of capital expenditure, etc.

Complaints received - Gas pricing Gold plating of expenditure

HQrs directions

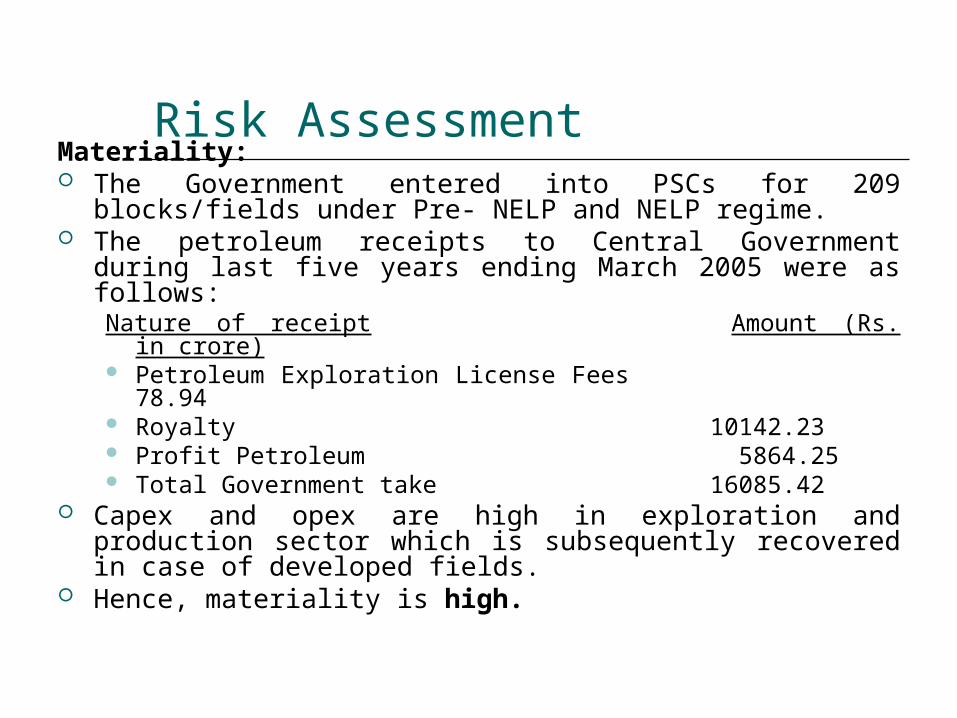

Risk AssessmentMateriality: The Government entered into PSCs for 209 blocks/fields

under Pre- NELP and NELP regime. The petroleum receipts to Central Government during last

five years ending March 2005 were as follows:Nature of receipt Amount (Rs. in crore) Petroleum Exploration License Fees 78.94 Royalty 10142.23 Profit Petroleum 5864.25 Total Government take 16085.42

Capex and opex are high in exploration and production sector which is subsequently recovered in case of developed fields.

Hence, materiality is high.

Criticality:

Energy security of the nation depends on the ability to explore, accrete and produce crude oil or natural gas on a sustainable basis

Expansion of the explorable base and maximisation of accretion of hydrocarbon

Production sharing contracts are critical instruments

In view of the above, the audit of this programme is considered to be an important one as the programme is mission critical to the core activity.

Control risk:

monitoring mechanism of the Government has to be analysed

The internal and external audit appear to be not so effective

Changes in regulatory and administrative frame work and in the BEC mechanism

Request of GoI for special audit by CAG

• Request of Ministry (November 2007) for special audit of Production Sharing Contracts (PSCs) for 8 blocks– In the context of large stakes of Govt in the

form of royalty & profit petroleum, and concerns about capital expenditure

• Audit agreed (March 2008) to Ministry’s request and decided to undertake a Performance Audit of Hydrocarbon PSCs covering a sample of discovered/ pre-NELP PSCs and NELP PSCs

17

Sample selection for detailed review

A sample of 20 blocks/fields out of more than 200 blocks fields selected for detailed review, cutting across pre-NELP, NELP, producing, exploration, relinquished blocks/fields

List of blocks selected for detailed scrutiny.

TEAM COMPOSITION

Two teams led by the Group Officer from the office of PDA-ESM and one team led by the Group Officer from the office of MAB-II, Mumbai.

Work Allocation

8 blocks were assigned to the audit team from O/o Pr. DCA/MAB-II, Mumbai.

Apart from audit of the short listed blocks, analysis of NELP rounds was also conducted

Audit Scope

Audit scope covered a twin approach Scrutiny of records at Ministry/ DGH for a

sample of 20 PSCs from 2003-04 TO 2007-08

Supplementary scrutiny of records of operators of 4 blocks/ fields (KG-DWN-98/3, Panna-Mukta, Tapti and RJ-ON-90/1) for 2006-07 and 2007-08

Access to records of operators of selected blocks was only supplementary to the scrutiny of records of MoPNG and DGH

22

Conduct of Audit

Entry conference was held with the Secretary (Petroleum) in November 2007.

The teams visited MOPNG and DGH office and collected preliminary data on the subject.

The team commenced the field audit with the JV blocks (Panna-Mukta and Tapti) located in Mumbai.

Plan documents (Risk Analysis, Audit Implementation Guidelines, Study Design Matrix along with Checklist) were formulated

Difficulties in accessing record of operators

Audit interrupted (July 2008 to September 2009) due to difficulties in accessing records of operators

Issue was resolved with active assistance of Ministry

24

Major Audit Findings

Findings relating to KG-DWN-98/3 block (Operator: RIL)

Findings related to RJ-ON-90/1 block (Operator: Cairn Energy)

Findings related to Panna-Mukta & Tapti fields (Joint Operators – BG, RIL and ONGC)

Compliance & Control Issues Conclusions & General Recommendations

25

Major Findings in respect of KG-DWN-98/3 block

Contractor: A consortium of Reliance Industries Limited (Operator) and Niko Resources Limited (90:10)

Non-relinquishment of area and declaration of entire contract area as discovery area (Para 4.2.1)

• PSC (signed on 12 April 2000) stipulated relinquishment of 25% each of total contract area at end of Exploration Phases I and II

– Contractor allowed to enter Phases II & III w/o relinquishment– Subsequently, in February 2009, GoI approved treating entire

contract area (7645 sq km) as ‘Discovery Area’• Discovery Area (as per PSC)

– “.. That part of the contract area about which, based on discovery and results obtained from a well or wells drilled in such part, the contractors is of the opinion that petroleum exists and is likely to be produced in commercial quantities”

– Discovery is defined as “ the finding, during petroleum operations, of a deposit of petroleum not previously known to have existed, which can be recovered at the surface in a flow measurable by conventional petroleum industry testing methods”

27

Non-relinquishment (Contd.)• Sequence of events b/w April 2004 and

February 2009– May 2004, DGH did not agree to operator’s

proposal– May 2005, DGH ‘waived’ its earlier objection, and

advised operator to complete 3D seismic data in entire block

– July 2006, DGH completed its about turn, and agreed to the operator’s proposal

– February 2009, Ministry approved and communicated the non-relinquishment & declaration of the entire contract area as ‘discovery area’.

28

Non-relinquishment (Contd.)

– Even interpretation of declaration of discovery area from July 2006 not followed through properly by Ministry/ DGH

• Cessation of exploration activities; completion of appraisal within 3 years (July 2009); prepare development plans on the basis of appraisal

• Recommendation – Ministry should review the determination of the

entire contract area as discovery area strictly in terms of the PSC provisions

– Further, it should delineate 25% relinquishment area at the time of conclusion of Exploration Phases I and II, and correctly delineate ‘discovery area’ based on PSC provision

29

Development activities

• D1-D3 gas discovery– PSC provisions (for gas discovery)

• After declaration of discovery as a ‘Commercial Discovery’, the operator would submit a development plan within 1 year for Management Committee’s approval

• After approval of development plan, gas discovery should be promptly developed by operator in accordance with the approval plan

• Revisions to the development plan, if any, should be proposed for good cause

30

Development activities (Contd.)

– Operator submitted Initial Development Plan (IDP) in May 2004, which envisaged

• Estimated capex of $2.4 billion• Gas production rate of 40 million standard cubic meter

per day (mmscmd)• First gas production by August 2006

– MC approved IDP in November 2004– After approval of IDP, operator was expected to

proceed in line with the approved plan. However, audit observed that

• Immediate action for procurement of major equipment/ materials/ services was not initiated, and

• Progress in field development work was not as per IDP

31

Development activities (Contd.)

– Operator submitted Addendum to IDP (AIDP) in October 2006

• Estimated capex increased to $ 8.8 billion• Gas production rate of 80 mmscmd• First gas production by mid-2008

– Audit found that • Most procurement activities were undertaken

late in line with schedules of IDP• By contrast, activities in respect of AIDP were

initiated even before submission/ approval of AIDP

– Clearly, development activities of operator were guided by AIDP, rather than IDP

32

Development activities (Contd.)

The scale of revision of IDP through the addendum in such a short time span cast doubts on the robustness of the data and assumptions underlying the development plans

Recent reports, as appearing in the media, indicate production coming down to even below 40 mmscmd (the level envisaged in the original plan). This raises doubts as to whether the upgradation to 80 mmscmd in AIDP with substantial increase in development cost was justified.

• Validating the cost incurred by operator can be done only after audit of actual cost– Part of expenditure in respect of items under AIDP

incurred during 2006-08 has been audited; remaining expenditure incurred from 2008-09 onwards would be covered in future audits

33

Profit Sharing Formula

34

Investment Multiple (IM) Government Share

Contractors’ Share

Less than 1.5 10 % 90%

1.5 to less than 2.0 16 % 84 %

2.0 to less than 2.5 28 % 72 %

2.5 and above 85 % 15 %

• IM = Cumulative Net Cash Income/ Cumulative Exploration & Development Costs• The more capital intensive the project, the lower the IM and GoI share of profit petroleum as low as 10%• Higher the IM, higher the GoI share (as high as 85%)

Profit Sharing Formula (Contd.)

• Private contractors have inadequate incentive to reduce capital expenditure, and substantial incentive to increase/ ‘front-end’ capital expenditure

• Such moves will help operator to retain the IM in lower slabs or to delay movement to higher slabs

35

Procurement activities

• PSC allows for cost recovery• Audit objective - Verifying whether

revenue interests of GoI properly protected; towards this larger objective, verifying whether:

• Capital and operating expenditure and individual items thereof were accurately and reliably reflected

• Individual items of capex/ opex were reasonable and also commensurate with budgets etc.

• Collateral evidence available to provide assurance

36

Procurement activities (Contd.)

• Audit could not derive assurance as to reasonableness of costs incurred on payments during 2006-07 and 2007-08, primarily due to lack of adequate competition

– Award on single financial bids;– Major revisions in scope/ quantities/

specifications post-price bid opening– Substantial variation orders

• Consequential adverse implications for cost recovery and GoI’s financial take

37

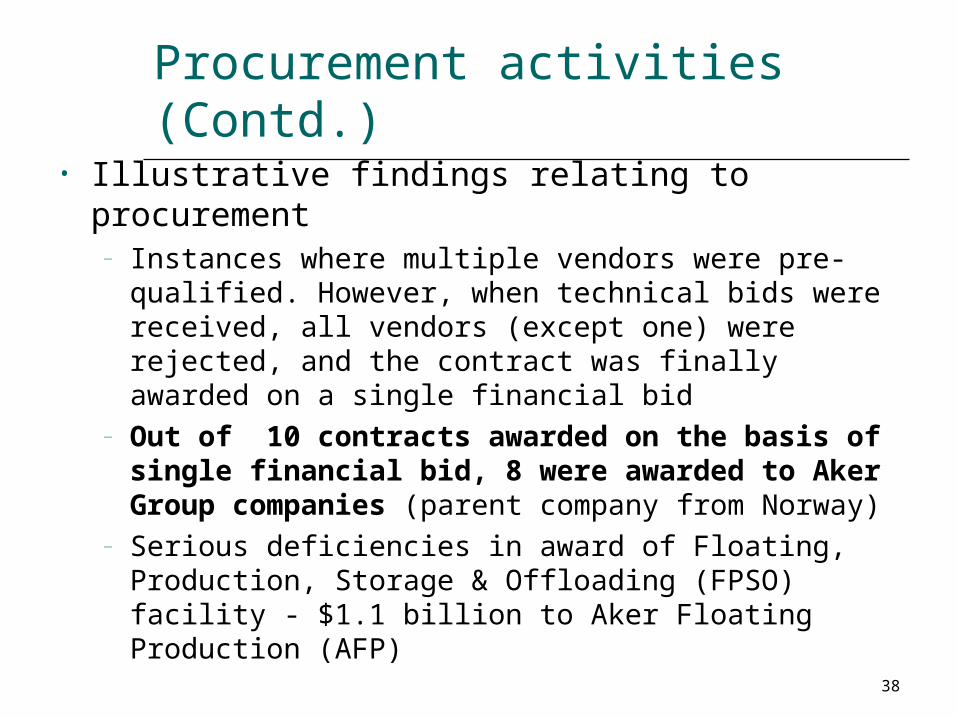

Procurement activities (Contd.)• Illustrative findings relating to procurement

– Instances where multiple vendors were pre-qualified. However, when technical bids were received, all vendors (except one) were rejected, and the contract was finally awarded on a single financial bid

– Out of 10 contracts awarded on the basis of single financial bid, 8 were awarded to Aker Group companies (parent company from Norway)

– Serious deficiencies in award of Floating, Production, Storage & Offloading (FPSO) facility - $1.1 billion to Aker Floating Production (AFP)

38

Procurement activities (Contd.)• Recommendations

– For High Value procurements (as per PSC definition), where pre-qualified bidders are disqualified and only one financial bid is being considered, operator should

• Either go back to the pre-qualification process and ensure more vendors are pre-qualified;

• Or refer the matter to GoI representatives on the Mgmt Committee for prior relaxation from PSC procedures

– In the case of KG-DWN-98/3, Ministry should carefully review in depth the award of 10 specific contracts (refer pg 94 of the report) on the basis of single financial bid (including 8 awarded to Aker Group companies)

• Not even remotely suggesting that the operator should follow Govt. procurement procedures

• Yet, any commercially prudent private acquisition would also attempt to generate competition, and thereby obtain the most competitive price

39

Major Findings – RJ-ON-90/1 BlockContractor: A consortium of Cairn Energy India Limited (Operator) and ONGC

• 13 fresh discoveries made during/ between appraisal and development phase in areas already delineated as development areas

• Instances of non-compliance with PSC provisions

40

Major Findings – Panna-Mukta & Tapti Fields Contractor: A JV of British Gas E&P India Limited, RIL and ONGC (joint operators)

– Scrutiny of records incomplete due to non-production of records

– GoI incurred substantial loss on account of royalty

– Ministry had accepted all findings– Ministry and its nominee (GAIL) failed to

comply with the terms of the PSC during 2005-08 w.r.t. gas pricing formula

– PMT JV had not completed key work commitments in respect of the Mukta field; committed work programme for Mid & South Tapti fields was also incomplete 41

Compliance & Control Issues

• Numerous deficiencies in compliance & control vis-à-vis PSC provisions by Ministry/ DGH, notably w.r.t.

– Irregular declaration of entire contract area of KG-OSN-2001/2 as discovery area

– Non-compliance to PSC provisions – Delay in submission/ review of appraisal

programme– Deficiencies in functioning of Mgmt

Committees– Deficiencies in timely submission of

periodical reports

42

Conclusions & General Recommendations

• The PSC is based on a scaled formula for profit sharing between GoI and the private contractors

– Investment Multiple – essentially an index of the capital-intensive nature of the project

• Private contractors have inadequate incentive to reduce capital expenditure, and substantial incentive to increase/ ‘front-end’ capital expenditure

– So as to retain the IM in lower slabs or to delay movement to higher slabs

43

Conclusions/ Recommendations (Contd.)

• Given similar conclusions reached by us (and the Ashok Chawla Committee), there does seem to be enough ground to revisit the formula

– PSC as drawn up in the late 1990’s was with the limited expertise available them

– In view of knowledge gained now (albeit by hindsight), there is need to conclusively address the issue in r/o future PSCs

• Management of existing PSCs – Recommendations– Approval of development plans should be on the stipulation

that changes in capex/ opex, production quantities which have the impact of reducing GoI share beyond a stipulated range (15/20/25%) must be submitted for prior approval by GoI representatives on MC

– Incurring of costs varying from Plans/ Budgets beyond the stipulated range w/o prior GoI approval should be ineligible for cost recovery

44

Problems faced

Problems of inadequate and slow flow of records in DGH/MOPNG and generic replies to audit observations.

Further, issue of limited access to the records of ‘operator’ to ensure correctness in calculation of cost petroleum, profit petroleum by the JV so as to protect the Government interest in form of Profit Petroleum and statutory levies is still unresolved.

Thanks